Asymptotics of generalized Pólya urns with non-linear feedback

Abstract

Generalized Pólya urns with non-linear feedback are an established probabilistic model to describe the dynamics of growth processes with reinforcement, a generic example being competition of agents in evolving markets. It is well known which conditions on the feedback mechanism lead to monopoly where a single agent achieves full market share, and various further results for particular feedback mechanisms have been derived from different perspectives. In this paper we provide a comprehensive account of the possible asymptotic behaviour for a large general class of feedback, and describe in detail how monopolies emerge in a transition from sub-linear to super-linear feedback via hierarchical states close to linearity. We further distinguish super- and sub-exponential feedback, which show conceptually interesting differences to understand the monopoly case, and study robustness of the asymptotics with respect to initial conditions, heterogeneities and small changes of the feedback mechanisms. Finally, we derive a scaling limit for the full time evolution of market shares in the limit of diverging initial market size, including the description of typical fluctuations and extending previous results in the context of stochastic approximation.

1 Introduction

In the near future, customers who intend to buy a new car will have the choice between several different technologies like modern cars powered by fossile or synthetic fuels, hydrogen or batteries. Although electric cars seem to be in the pole position in the race for the future car market, it is still open which technology will win or whether there will be a mixture of different technologies. The economist Brian R. Arthur suggests in [4] to model the competition between technologies as a generalized Pólya urn, which was basically introduced by Hill, Lane and Sudderth in [24]. In this model the decision which technology to choose depends on three factors. First, it supposes that each technology has an intrinsic deterministic attractiveness or fitness. Second, the decision depends on the choice of earlier customers. For example, if many bought an electric car before, there will be a dense charging infrastructure and thus electric cars get more attractive for future customers. A second argument for this reinforcement is that high revenues in the past provide financial means for a faster technological development as well as cheaper prices because of lower production costs per unit. The resulting overall attractiveness of technology is now modeled as a hypothetical feedback-function depending on the number of customers, who chose technology before. High values of indicate high attractiveness of technology i. A typical example is , where models the intrinsic attractiveness and the reinforcement effects in the market. The third determinant of customers decision is their personal preference, which is difficult to include in a deterministic model and probabilistic approaches are more appropriate. We assume that customers enter the market sequentially and have full information. Given the current state of the market, a customer will opt for technology with probability

where is the number of different technologies. The market size increases by one in each step. If , then this corresponds to the original Pólya urn, which was introduced by Pólya and Eggenberger in [19]. Depending on the feedback function, monopoly may occur where one technology achieves full market share, as well as random or deterministic non-zero asymptotic market shares for several technologies. The monopolist is in general random and depends on the behaviour of the young market. Analyzing which feedback function leads to which regime provides an understanding of the determinants of the long-time behavior of markets.

Mathematically, this setup corresponds to a discrete-time Markov process, which is called a (generalized) non-linear Pólya urn in the following and introduced in detail in the next Section. Apart from the competition of technologies, many other interpretations and applications of generalized Pólya urns are possible. An obvious one is the competition of companies in the same market for new customers or the competition between regions for new companies to settle. The dynamics of household wealth is another growth process with reinforcement (see e.g. [20] and references therein) that can be modelled with urns. [39] summarizes further applications in psychology or evolutionary biology, and more recently, [44, 41] use Pólya urns in the context of cryptocurrencies. In the following we will adapt the more general terminology of agents instead of technologies.

Mathematical properties of non-linear Pólya urns have been examined before, often focused on polynomial feedback functions [29, 17, 30, 37, 24, 28, 12, 33] or homogeneous models with [38, 36, 34]. In applications, the feedback functions are usually a hypothetical construction that can barely be measured in real systems similar to utility functions in economic situations, thus a general mathematical understanding without restrictive conditions on is important. This paper investigates the long-time behavior of non-linear Pólya urns for a very general class of feedback functions. could even be decreasing or exponentially increasing, which reveals some surprising differences to the usually studied polynomial case. An important restriction is, however, that depends only on , which excludes stationary limit cycles as studied e.g. in [13].

In Section 2 we introduce the model, give a detailed summary of previous related results and highlight the main novelties of the paper. In the monopoly case, we present in Section 3 an asymptotic result for large initial market sizes on the distribution of the winner, extending previous results for particular feedback functions. In the non-monopoly case we present in Section 4 a novel approach to compute the deterministic long-time market shares, which do not depend on the initial condition or early dynamics. In Section 5, we study in detail the transition between both cases for almost linear feedback functions, which are particularly relevant in various applications including wealth dynamics [20]. Moreover, we derive in Section 6 a law of large numbers for the dynamics of the process for large initial market size, which is asymptotically described by an ordinary differential equation and has previously been studied for particular feedback functions in the context of stochastic approximation [11, 39, 42]. Extending these results, we also establish a functional central limit theorem to describe typical dynamic fluctuations by a system of SDEs in Section 7. The question of a Gaussian approximation of the dynamics of Pólya urns has also been addressed in recent research, see [10] and [16]. Predictable behaviour can only be expected for large initial market size, the behavior of very young markets is intrinsically random. While bounds on the probabilities of certain events can be obtained, we focus here mostly on asymptotic results and provide a rather complete account of the possible dynamic and long-time behaviour of generalized non-linear Pólya urns. To our knowledge this paper provides the first complete account for the generalized non-linear Pólya urn, which is a classical model for reinforcement dynamics.

More generalisations of Pólya’s urn (e.g. for infinitely many agents and more complex replacement mechanisms) have been addressed in further recent research [32, 13, 5, 27, 7, 31, 42, 48, 49], and in [1, 2, 3] the authors include a rescaling mechanism to inhibit long-range dynamic dependencies. The study of generalized Pólya urns is also closely related to reinforced random walks, see e.g. [15, 45, 14]

2 The generalized Pólya urn model

2.1 Basic definitions and background

We now formally introduce the model. All random variables are defined on some large enough probability space . Let be the number of agents and the feedback function of agent . We define a homogeneous, discrete-time Markov process on the state space with initial condition such that for all , and transition probabilities

| (1) |

where is the -th unit vector. We denote by the initial market size. Whenever needed, we set , and whenever useful, we take continuously differentiable extensions to the positive real line, which is supposed to be monotone on intervals of the form .

We interpret as the number of customers of agent at time and define the corresponding time-inhomogeneous Markov process of market shares

with , where is the interior of the unit simplex . Moreover, we establish the notation

for the long time market share whenever it exists. We will see throughout the paper that is well defined in all generic situations, but it is possible to construct counterexamples (see Example 4.7). For later use we introduce the notation

| (2) |

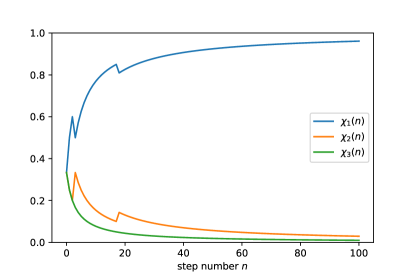

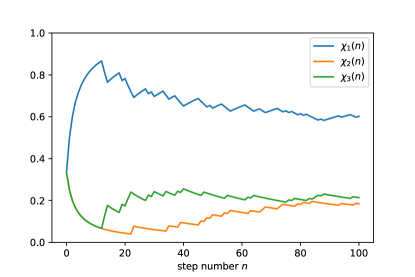

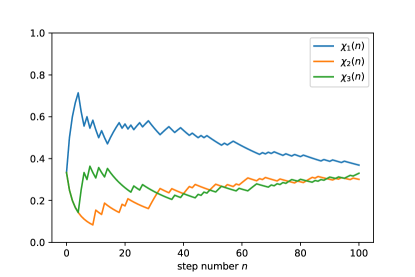

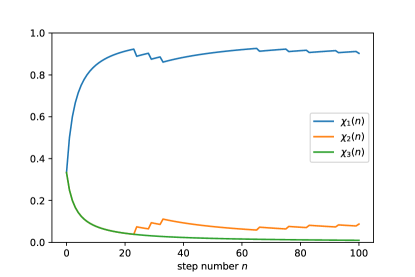

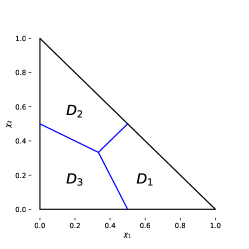

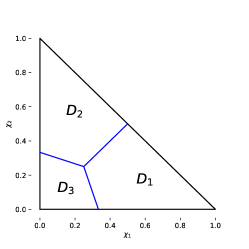

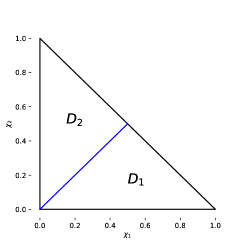

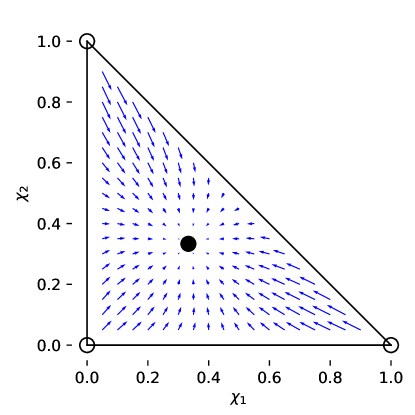

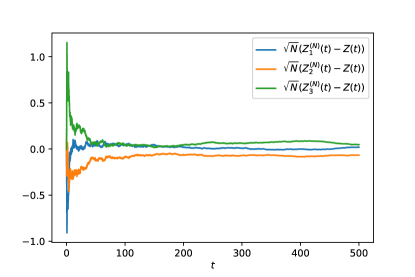

for the transition probabilities, where and . Figure 1 shows three simulations of this process for different feedback functions.

A useful alternative construction of the process is provided by the so-called exponential embedding (see e.g. [38] and references therein). We take independent random variables , where is exponentially distributed with rate parameter . For each we define the corresponding continuous-time counting process with

| (3) |

These are independent birth processes with , where the time between the -th and -th event of is given by . If is the sequence of jump-times of the process , i.e.

then Rubin’s theorem (proven in e.g. [38]) states, that the jump chain has the same distribution as the process . Thus we can define:

| (4) |

In fact, the birth processes can explode as the sum might be finite. We therefore define the random explosion times

In the following we are especially interested in the occurrence of monopoly, which requires some definitions.

Definition 2.1.

For we define the events

-

1.

weak monopoly

i.e. the market share of agent converges to one;

-

2.

strong monopoly

i.e. agent wins in all but finitely many steps;

-

3.

total monopoly

i.e. agent wins in all steps.

Obviously, a total monopoly is also a strong monopoly and a strong monopoly always implies a weak monopoly. Via exponential embedding one can express the event by the explosion times through

| (5) |

as equality of finite explosion times has probability zero (see below). With the observation

one can easily derive the following generally known criterion for the occurrence of strong monopoly (see e.g. [15, 38]).

Theorem 2.2.

Strong monopoly occurs with probability one, i.e.

if and only if

| (M) |

otherwise the probability is zero.

If (M) holds, the density of the explosion time (computed in [47]) as a sum of exponential variables has support on the whole positive real line for all choices of . So the probability of is positive if and only if agent fulfills (M) and the monopolist is random among all agents that satisfy (M). For the polynomial case , Theorem 2.2 implies that strong monopoly occurs if and only if .

On the other hand, when no agent fulfills (M), almost surely for all , and we have the following consistency property.

Proposition 2.3.

Assume that none of the satisfies (M). Define a ’partial’ Pólya urn process for a subset of agents with the same feedback functions and initial condition . Then the process can be identified as a (random) subsequence of .

Proof.

The independence property of the exponential embedding provides a canonical coupling of the processes and . For that, define recursively and

Note that is well defined for all , since none of the fulfill (M). Then set , which directly implies the claim since is a subsequence of . ∎

In particular, if one of the limits

exists, then so does the other and both have the same distribution. This implies further neutrality of the limit in the sense of [26], so that it has a (possibly degenerate) Dirichlet distribution on , whenever it exists. In the degenerate case, the Dirichlet distribution is either deterministic or concentrated on the vertices of with . This will be discussed in several examples in Sections 4 and 5. Note that in the case of weak monopoly this corresponds to hierarchical states, where the asymptotic distribution among losing agents again exhibits a weak monopolist.

2.2 Review of previous results

As already described in the introduction, generalisations of Pólya urns have been studied in numerous papers. In this section, we shortly present a selection of results related to our work. To our knowledge, the most comprehensive result concerning the long time limit of the process of market shares is the following.

Theorem 2.4.

Note that a Lyapunov function does always exist in the case and when is differentiable with equal feedback functions for all agents. Moreover, [11] shows under mild technical assumptions that each stable fixed point of the vector field is attained in the limit with positive probability, whereas unstable fixed points are never attained.

Theorem 2.4 allows to compute the long time market shares in generic situations, like . Nevertheless, condition (6) is not fulfilled e.g. for or .

In the monopoly case described in Theorem 2.2, the monopolist is in general random. Consequently, one is interested in the probability that a specific agent is the monopolist, at least in the limit . [34] derives such a result in a situation with only two symmetric agents.

Theorem 2.5.

[34, Theorem 2] Let and . Assume that fulfills (M) and that

Moreover, suppose that there is a constant such that for all and all large enough

holds. Let for and . Then the probability of agent being the monopolist converges to for , where denotes the cumulative distribution function of the normal distribution.

For these assumptions are fulfilled and . Under similar assumptions as in Theorem 2.5, [38] shows that the number of steps, in which the looser wins, has a heavy tailed distribution. Moreover, if for an agent , then is exponentially decreasing in , i.e. the first steps of the process decide who wins. [18] provides similar results for the asymmetric case . More recently in [33], a result for polynomial feedback with different exponents was shown.

Theorem 2.6.

[33, Theorem 2.2] Let and with . Define the critical values

Morover, set for .

-

1.

If either or and , then .

-

2.

If either or and , then .

In addition, [33] provides a result for the critical case .

For with , we know from Theorem 2.4 that almost surely for all irrespective of the initial configuration . The rate of convergence is specified in [30].

Theorem 2.7.

[30, Propsition 3] Let for all and .

-

1.

If , then

for a random, nonzero vector .

-

2.

If and , then

where denotes a Gaussian distribution.

-

3.

If and , then

The convergence in part 2 and 3 can be extended to the vector . Part 1 implies that the leading agent does only change finitely often. According to [36, Theorem 1], this happens in general if and only if

where fulfills .

2.3 Main contributions of this paper

One important purpose of this paper is to provide a comprehensive approach and a complete picture for the asymptotics of the generalized Pólya urn model, which applies for a large class of feedback functions. This allows us to fully characterize the emergence of monopoly in a transition from sub-linear to super-linear feedback, where the system exhibits interesting behaviour including hierarchical states and weak monopoly. We outline our main results for symmetric feedback , although most of the results in this paper do also hold in asymmetric situations:

These regimes react differently to unequal fitness of agents. For with distinct, we will show the following properties:

- 1.

- 2./3.

- 4.

Furthermore, we derive a scaling limit for the process of market shares in Theorem 6.1 and characterize the fluctuations in the Functional Central Limit Theorem 7.1. This part uses standard techniques from stochastic approximation, but we include it to provide a complete picture of the asymptotics of the generalized Pólya urn.

3 Asymptotics for the strong monopoly case

We assume that at least one agent fulfills (M), so that a random strong monopoly occurs with probability one. To characterize the asymptotics, we have to distinguish two different types of feedback functions with slightly different behavior.

Definition 3.1.

Let agent (or ) fulfill (M). We call (or ) of type P (for polynomial) if

| (7) |

and of type E (for exponential) if

| (8) |

For the rest of this section we assume that all agents with feedback functions that fulfill (M) are either of type P or type E. Of course it is possible to construct counter-examples (see Example 3.3), but these two types still cover a very large range, including most previous results.

Proposition 3.2.

If

| (9) |

then is of type P, and if

| (10) |

then is of type E.

Proof.

First we assume (9) and observe that

| (11) |

Consequently, for any given there exists such that . Then we get for :

The result for type E follows similarly. ∎

This means that functions that grow exponentially or faster are of type E whereas functions that grow slower than exponential (like polynomials) are of type P. Note that Oliveira’s ”valid feedback functions” in [38] or [36] are of type P, which includes furthermore all regular varying functions.

Example 3.3.

- 1.

-

2.

A possible construction of a feedback function that is neither of type P nor type E, but satisfies (M), is the following. Take a function such that

holds, e.g. . Then define a new feedback function by replacing each by elements that all equal , i.e.

One can easily check that has the desired properties.

3.1 Asymptotic attraction domains

If at least one agents fulfills the monopoly condition (M), we know by Theorem 2.2 that there is a strong monopoly, where all agents satisfying (M) have a positive probability of being the monopolist. Thus, the monopolist is in general random. Nevertheless, in most situations it is possible to predict the winner with high probability for large initial market size.

Definition 3.4.

The asymptotic attraction domain of an agent is defined as

Obviously, the asymptotic attraction domains are disjoint, since for . The main result of this section states that the asymptotic attraction domains cover the whole simplex up to boundaries under mild regularity conditions.

Theorem 3.5.

Let at least one agent satisfy (M) and all agents satisfying (M) are either of type P or type E. Moreover, assume that one of the following conditions holds:

-

1.

At least one agent is of type E and for all

-

2.

No agent is of type E and all agents of type P (there is at least one) fulfill

(12) In addition, suppose that exists for all .

Then the asymptotic attraction domains are polytopes that dissect the simplex up to boundaries, i.e.

where is the topological closure. If agent does not satisfy (M) then .

As a direct consequence of the exponential embedding, for all agents that do not fulfill (M). Hence, their attraction domains are empty. The rest of Theorem 3.5 basically follows from the results presented in the following subsections, where e.g. explicit conditions for

as well as bounds of are derived. The final proof of Theorem 3.5 will be presented in subsection 3.4. It will turn out that the explosion times from Section 2 concentrate on their expectations, i.e.

only for agents of type P, but not for type E, so we need to study these two types of feedback functions separately. The technical conditions in each case are mild and will be discussed in the following subsections. Another characteristic of type E is, that a strong monopoly is typically even a total monopoly, at least when is large.

Theorem 3.6.

Let Assumption 1 in Theorem 3.5 be satisfied. If agent is of type E and is in the interior of , then

| (13) |

Theorem 3.6 is a direct consequence of Theorem 3.7 given below. As explained in Corollary 3.11, total monopoly does in general not occur, if is on the boundary of the attraction domain. In adddition, it turns out that in generic situations the probability of total monopoly is bounded away from one, if all agents are of type P.

3.2 Agents of type E and total monopoly

This subsection examines the process, when at least one agent is of type E. The following results basically imply the first part of Theorem 3.5 as well as Theorem 3.6 as described in Section 3.4. The main result of this subsection provides a useful lower and upper bound for the probability of total monopoly.

Theorem 3.7.

Proof.

Direct calculation yields

using the inequality for . For the upper bound, we estimate

using in . ∎

An immediate consequence of Theorem 3.7 is, that for any agent fulfilling (M) the probability of a total monopoly is positive but less than one. In addition, the theorem reveals a significant behavioural difference between agents of type E and type P: whereas total monopoly is very likely for type E agents when the initial market size is large, it is rather untypical for type P, which is explained in the following corollary and example.

Corollary 3.8.

Proof.

1. If is of type E, then (14) implies

using (8), and (15) follows from the lower bound of Theorem 3.7. The necessity of (14) follows from

2. (16) implies that the lower bound of Theorem 3.7 converges to one so that (15) holds. Now we assume that (16) does not hold. If does not converge to infinity for some , then with 1., (15) cannot hold. Thus we can assume (14) for all , which implies for the upper bound in Theorem 3.7 due to asymptotic monotonicity of as . The upper bound then implies that does not converge to one. ∎

Example 3.9.

Remarkably for type E agents, if for all and a function fulfilling (8), then for large the almost surely deterministic monopolist does not depend on the attractiveness-parameters , but is only determined by the initial condition due to the strong feedback effect of type E functions.

Moreover, Theorem 3.7 provides information about the rate of convergence in (15) and (22). If agent is of type E, then Theorem 3.7 states together with and

where

because of (8). Thus the convergence can be considered as quite fast. For example for , and the bounds in Theorem 3.7 are:

Indeed, condition (14) is fulfilled for an in most generic cases, when at least one agent is of type E. To be more precise: If the expression in (14) neither tends to infinity nor to zero, then an arbitrarily small change in the initial market shares provides (14).

Proposition 3.10.

Let agent be of type E.

-

1.

If is of type P for all , then (14) holds.

-

2.

If is of type E and

(17) then for any :

Proof.

1. By (8) we have for agent of type E that

| (18) |

for some and large enough, thus the sequence converges to zero faster than . For an agent of type P we have by (7) for any

for large enough, thus the sequence converges to zero slower than . Together this yields

exponentially fast as d is arbitrarily small. Finally (14) follows from

| (19) |

as slower than exponentially.

Corollary 3.8 implies that for any agent of type E

Due to Proposition 3.10, these sets are even equal up to boundaries under Assumption 1 of Theorem 3.5. Moreover, the first part of Proposition 3.10 states that the attraction domains of all agents of type P are empty, if there is at least one agent of type E. Recall that for finite the probability of monopoly is positive for all agents satisfying (M).

Finally, one can ask what happens for large and critical market shares, i.e. for lying exactly on the edge between the asymptotic attraction domains. It stands to reason that in this situation the monopolist remains random even for large . Nevertheless, the exact limiting behaviour depends on whether the feedback functions grow exponentially or even super-exponentially.

Corollary 3.11.

Let all agents be of type E and consider , such that

| (20) |

for all . Then the following holds:

-

1.

For all agents we have .

-

2.

If for all agents we have super-exponentially growing feedback, i.e.

then .

-

3.

If for all agents we have at most exponentially growing feedback, i.e.

then .

Proof.

3. Similarly to the second part, this follows from

∎

Example 3.12.

We summarize the main conclusions for total mononpoly in the limit of large initial market size : If for all agents the feedback functions grow super-exponentially, the winner of the first step will win all steps. This does not hold for any if all feedback functions grow at most exponentially. In general, total monopoly of an agent can occur with probability one according to Corollary 3.8: if is of type and (14) holds, or if (16) holds.

3.3 Agents of type P

Let us now turn to the more widely studied case when all agents are of type P. We already saw in Example 3.9 that in this case a total monopoly is rather untypical. Since the definition of type P includes the monopoly condition (M), strong monopoly still occurs with probability one. Again, it is possible to predict the monopolist in the limit .

Theorem 3.13.

Let all agents be of type P or not fulfill (M). If there is an agent of type P such that

| (21) |

then

| (22) |

Note that condition (21) can be replaced by the easier, but stricter condition

due to de l’Hospital’s Theorem. This implies that for regular varying , where and is a slowly varying function, the attraction domains are equal to the polynomial case, where . Moreover, the attraction domains do not change if is replaced by another function satisfying .

Proof.

Lemma 3.14.

If agent is of type P, then:

Proof.

We can find an appropriate regular extension of , such that for all

By the theorem of de L’Hospital and (7) this implies

∎

Example 3.15.

Lemma 3.14 uncovers another behavioral difference between type P and type E agents: For type P agents the explosion time concentrates on its expectation, whereas the variance of remains bounded from below for type E agents by an analogous argument, using (8). For many type P agents, including , it is possible to prove that the convergence of is even almost sure (see the proof of Proposition 3.19 together with the Lemma of Borel-Cantelli).

It is now natural to look for an analogy to Proposition 3.10 for type P agents in order to make sure that (21) is fulfilled for almost all initial market shares . Unfortunately, this attempt is meant to fail as the example for shows. In this case

where for sequences and we write if for . Therefore (21) is not fulfilled for all choices of , since

Nevertheless, with a further condition we can find a similar result as Proposition 3.10.

Proposition 3.16.

Proof.

Example 3.17.

If for all and a feedback function fulfilling (24), e.g. for , then if for all .

If all agents are of type P, Theorem 3.13 implies that for any agent

Assuming 2. in Theorem 3.5, we get from Proposition 3.16 that the sets are equal up to boundaries.

In the situation of the second part of Proposition 3.16, the explosion times concentrate asymptotically on the same value, i.e. in distribution. Thus, it is not possible to predict the monopolist for large by the means of this section. If and for all , then holds for all for symmetry reasons, i.e. does not belong to any attraction domain as the monopolist remains random even in the limit . The following example underlines that this property does not hold in general, because in some cases the boundary between the attraction domains belongs to one of them.

Example 3.18.

Consider the process for and for and . Then we have

and

for . Moreover, set , such that (23) holds, and define . Chebyshev’s inequality yields

since and

In addition, we have for large enough that

because implies

Thus for large

using the independence of and . Hence, .

We finish this subsection with a result on the rate of convergence in (22). [18] presents a bound for in the case , but a straight-forward generalization of this procedure is possible.

Proposition 3.19.

This means that the rate of convergence in (7) gives a lower bound for the rate of convergence of .

Proof.

Once again, the proof uses the exponential embedding from Section 2. Let and . Then the Markov-inequality and monotone convergence yield for all and :

where . Setting

(which is positive for small enough since for all ) yields

The second estimate uses by monotonicity. Analogously, one can show

which will be used only for . Both estimates then imply for large enough together with (5):

In the last inequality we use for . For large enough we have

for because of (7) and due to (9). Finally, this leads to

∎

For we have , thus the convergence of can be considered as fast. Hence, is close to one even for moderate , when is in the asymptotic attraction domain.

In the type E case we saw that a total monopoly is very likely whereas in the type P case the losers might also win in some steps. It is now a question of interest how many steps the losers win, i.e. the value of if agent is not the monopolist. Results on this question can be found in [38] and [47]. It is remarkable that for polynomially growing feedback functions the distribution of has heavy tails. [14, 47] also present results on the time when the monopoly occurs. Further asymptotic results on strong monopoly, mainly in the type P case, can be found e.g. in [30, 34, 37, 18, 17, 33, 28].

3.4 Proof of Theorem 3.5 and Theorem 3.6

Finally, we shortly explain how Theorem 3.5 and Theorem 3.6 follow from the results of the previous sections.

First, assume that Assumption 1 of Theorem 3.5 is satisfied, i.e. at least one agent is of type E. Then Corollary 3.8 implies that for any agent of type E

Obviously:

Due to Proposition 3.10, there is a ratio such that

for each pair of agents. Note that

Hence,

is an intersection of half-spaces and the simplex, i.e. a polytope. Moreover, cover the whole simplex up to boundaries, since the ”winning”-relation is transitive. Thus, cover the simplex up to boundaries as well and equals up to boundaries. According to Corollary 3.8, we even have for , if . Hence, Theorem 3.6 is proven, too.

If Assumption 2 of Theorem 3.5 is satisfied, the proof is analogous using Theorem 3.13 and Proposition 3.16. Note that

due to the Theorem of de l’Hospital.

In summary, for finite the monopolist is random and even disadvantageous agents can win. If the initial market size is large, it is possible to predict the winner with high probability depending on the initial market shares.

4 The non-monopoly case

Now we consider the case when no agent fulfills (M), such that no strong monopoly occurs. It is known that in the case of a standard Pólya urn, i.e. for all agents, the limit exists almost surely and has a Dirichlet-distribution with parameter (see e.g. [21]). Thus, in the long run all agents have a stable, non-zero, random market share.

It is basically known (e.g. from [11]) that if the feedback functions grow significantly slower than linear, then is deterministic. We present an alternative approach to the sub-linear case, which allows some additional insights. For example, the case is not included in the results of [11]. In addition, our approach allows to construct feedback functions such that does not even converge for . In order to get deterministic limits in our approach, we will need a condition, which ensures that the feedback functions grow slow enough. We will mainly use:

| (26) |

Note that this already implies that does not fulfill (M). We add some examples to gain an understanding of this restriction.

Example 4.1.

In fact, condition (26) contains a monotonicity in the following sense.

Proof.

In general, our approach even allows feedback functions that converge to zero as long as this convergence is not to fast, which is ensured by the condition

| (27) |

Note that (27) is fulfilled for any feedback function with as well as for , but not for . In analogy to Proposition 4.2 we get a monotonicity here in the sense that if fulfills (27) and

then fulfills (27), too. We are now prepared for the main result of this section regarding the counting processes (3) of the exponential embedding from Section 2.

Note that exists as is strictly monotone. The asymptotics of birth processes have been studied in the literature before, e.g. in [6]. One main result of [6] will be used for a special case in Section 5 to abandon condition (26). The following lemma provides the first step of the proof of Theorem 4.3, using standard ideas from renewal theory.

Lemma 4.4.

If fulfills (27) for , then

Proof.

Now Theorem 4.3 is easy to prove.

Proof.

Theorem 4.3 implies that the market shares in the exponential embedding are asymptotically given by

Via (4) we can now conclude for the discrete-time urn model.

Corollary 4.5.

Note that the do not depend on and , thus the long time behavior of market shares in the generalized Pólya urn does not depend on initial conditions if (26) and (27) are satisfied. If the limit in (29) exists, a market modeled by a Pólya urn under the assumptions of the corollary reveals stable and deterministic market shares in the long run and these market shares do not depend on the current market situation and can also take values in . If the limit exists it is in , since is compact and therefore the laws of form a tight sequence. The corollary provides a way to explicitly calculate these long-time market shares.

Example 4.6.

-

1.

If with , then

and hence:

Consequently, the impact of the fitness parameters in the long-time limit increases with , where

The limiting case will be discussed later in Proposition 4.9.

-

2.

If with , then

and thus:

Note that this is the same asymptotic market share as if the customers’ decisions were independent (with constant feedback functions as for above), so that the strong law of large numbers applies.

It is also possible to find examples where the limit (29) does not exist. In the following situation the market share of the agents oscillates with constant amplitude but increasing period.

Example 4.7.

Take and set

This corresponds to and , which is well defined due to . Then Theorem 4.3 implies

and hence oscillates between and .

We now add a criterion that ensures the existence of the limit in (29).

Corollary 4.8.

Proof.

Recall that is strictly increasing. For a fixed we show that converges to . First, we assume , such that agents and fulfill (26) and (27). (31) implies via the theorem of de l’Hospital for and consequently for a function with . In combination with Theorem 4.3 it remains to show that converges to for . For this we consider

as (30) implies via time-shift

Thus:

For agents with the asymptotic market share is for sure bigger than in a situation where is replaced by , i.e. is for larger than any . Hence, it converges to infinity. Similarly for agents with . ∎

Note that in the case (including e.g. feedback functions such as , or functions converging in ) the limit is equal to the case , i.e. draws from the urn are independent and the usual strong law of large numbers applies. So this weak reinforcement does not play any role in the long run.

So far, we did not consider cases near the classical Pólya urn with , where random limits are possible. Nevertheless, as Lemma 4.4 does not require (26), our approach provides some insight into such asymmetric cases as well. The symmetric case with feedback functions close to the classical Pólya urn is treated in Section 5.

Proposition 4.9.

Proof.

First note that via exponential embedding, the event is equivalent to for all . Obviously, agent fulfills (27). First, we assume that agent does, too. Define

and thus . Assumption (33) implies that for any there is a constant with for large enough and consequently . Lemma 4.4 states that and almost surely. Thus it remains to show that

which is equivalent to . It is sufficient that

which follows since and Assumption (32) is equivalent to .

If agent does not fulfill (27), then is bounded from above and hence is stochastically dominated by a homogeneous Poisson process (with constant rate). Consequently, grows asymptotically not faster than linear and hence almost surely. ∎

Condition (32) includes feedback functions of the form for all , including the linear case for . If in addition (33) holds, i.e. for an agent and all , then we have an almost sure weak monopoly for agent . This is consistent with the strong monopoly for as described in Example 3.17. Note that the weak monopoly in Proposition 4.9 is almost sure even for finite , in contrast to the results on strong monopoly derived in Section 3, where the strong monopolist is random and can only be predicted in the limit .

On the other hand, condition (26) includes sublinear feedback functions of the form with , which have positive long-time market shares for all agents as discussed in Example 4.6.

Exponentially decreasing feedback functions were not taken into account so far as they do not fulfill (27). Since such cases do not seem to be of great importance for the mentioned interpretations of the model, we are content with an example, which we discuss in Appendix A.2 using the method of stochastic approximation.

We conclude the presentation with a short overview of further related results. [35, 37, 29] discuss another change of behaviour that is not apparent from our approach. Consider the case

If , e.g. for , then the leading agent changes only finitely often with probability one, whereas in the case this probability is zero.

For , it is shown in [30] that converges to at rate for (almost surely), at rate for and at rate for (in a weak sense). For , a central limit theorem holds.

In the case and [28] derives the tail distributions of the number and last times of ties .

5 Feedback functions close to the classical Pólya urn

We know from Theorem 2.2 that a generalized Pólya urn reveals strong monopoly if and only if at least one feedback function grows significantly faster than linear, i.e. fulfills (M). As described in Section 4, linear feedback functions imply random long-time market shares, whereas a deterministic limit occurs for feedback functions growing significantly slower than linear, i.e. those fulfilling (26). Nevertheless, some feedback functions that are close to linear (like ) are not covered by our results so far. To our knowledge, the literature does not provide results on the long time behaviour of a generalized Pólya urn with almost linear feedback. For instance, if for a slowly varying function , then Theorem 2.4 does not determine the long-time limit, since for all . We approach this question exploiting general results on birth processes, which require that does not fulfill (M) but inverted squares are summable, i.e.

| (34) |

Recall the exponential embedding from Section 2 and notations introduced therein. For this section, it is convenient to adapt previous definitions using

| (35) |

and to extend on by a right-continuous step function. The key to the desired results is provided by the following result in [6].

Theorem 5.1.

We can now apply this general result in our situation.

Corollary 5.2.

Assume that fulfills (34). Then:

-

1.

If , then

-

2.

If , then

-

3.

If , then

for a (deterministic) function with .

Proof.

Like in Section 4, we can now conclude from the exponential embedding to the evolution of market shares in the Pólya urn via

provided that the limit exists.

We are now particularly interested in cases with equal feedback functions for all agents, since agents with different attractiveness are already covered by Proposition 4.9.

Corollary 5.3.

Assume that all agents have the same feedback function and that fulfills (34). Then for all :

-

1.

If , then

-

2.

If , then the limit exists almost surely and has a non-degenerate Dirichlet distribution on .

-

3.

If , then exists almost surely and the process exhibits a weak monopoly, i.e

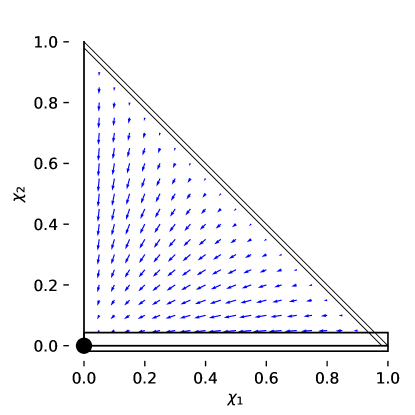

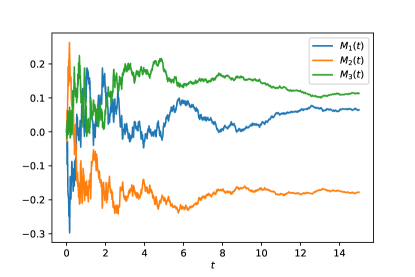

In other words: If the feedback function grows any slower than the identity, then the market shares converge to a deterministic limit as time tends to infinity, and the limit does not depend on the initial condition. If the feedback functions grow any faster than the identity, the process exhibits weak monopoly, which is not strong as (M) is necessary in Theorem 2.2. The weak monopoly can been seen in the Simulation shown in Figure 1 (d). In contrast to the non-symmetric situation of Proposition 4.9, the monopolist is random with probability depending on the initial condition .

Proof.

Note that the from Theorem 5.1 are independent with distribution depending on and . In addition, their distribution is continuous as emerges from a sum of independent, centered exponentially distributed random variables. By definition (35) we get with constants depending on the initial conditions and , and after inversion we have for all . With (36) this implies

| (37) |

and note that in all cases.

Lemma 5.4.

For all choices of , we have

Proof.

The implication is trivial. Thus, assume that the process starts in and that . Moreover, take any . Then the claim follows directly from the Markov property,

since . ∎

The following example presents a class of feedback functions, for which four different regimes are possible.

Example 5.5.

Let for all and . Depending on , four different regimes occur for :

-

1.

For , for each agent converges almost surely to independently of .

-

2.

For , the market shares converge almost surely to a random limit , which is not a corner point and its distribution depends on the initial condition .

-

3.

For , the process exhibits a weak monopoly which is not strong, i.e. all agents win in infinitely many steps, but the market share of one agent converges to one. The monopolist is random, and the distribution of on the corner points of depends on .

-

4.

For , there is a strong monopoly. The monopolist is random and the distribution of on the corner points of depends on the initial condition as well.

According to Theorem 5.1, we have by definition of the exponential embedding with jump times . If , this convergence can be specified by replacing by a deterministic function and by computing the distribution of .

Theorem 5.6.

Assume that does not fulfill (M) and that holds. Then there exist independent random variables such that

almost surely. Moreover, the cumulant generating function (CGF) of each is given by

| (38) |

and the radius of convergence is .

In particular, there is exactly one agent, namely the weak monopolist, such that the limit of is zero. For the proof, we characterize the distribution of by computing its CGF. For that, we exploit that is also the limit of for according to Theorem 5.1.

Lemma 5.7.

Proof.

The CGF of the limit is the pointwise limit of the CGFs:

We now use the series representation of and change the order of summation due to absolut convergence:

Note that for . Now, define and let . The radius of convergence of the power series representation of the CGF is given by

since and if . ∎

In particular, since the first term in the series is , and the -th cumulant of is for . For the proof of Theorem 5.6, it remains to show that converges as desired.

Lemma 5.8.

Proof.

By definition of and and by Theorem 5.1, we have

as . Furthermore,

This holds because

for a mean value using . ∎

According to Theorem 5.6, is asymptotically well described by

where for all . Now, consider two distinct agents and assume for simplicity of notation that , such that . Then Theorem 5.6 states that

Moreover, the CGF of is the sum of the CGFs of and due to independence. Hence, is finite if and only if . Thus, the distribution of has exponential tails, and these findings can be used as follows.

Example 5.9.

Let and for two agents , so that . Then the continuous mapping theorem yields

where has a power-law distribution due to the explanations above. Remarkably, the log-ratios and are asymptotically also independent for distinct pairs of agents .

An important application of Theorem 5.6 is its implication for the rate of convergence. In fact, the convergence of the process of market shares to an edge of the simplex can be considered as logarithmically slow.

Corollary 5.10.

Assume that and is increasing, but (M) does not hold. Then there is a random constant such that

Proof.

Since the limit in Theorem 5.6 is finite, there is a constant such that

Since , we have

for an updated constant , which proves the claim. ∎

In particular, converges to zero slower than any polynomial when. The following example discusses that bound in a generic situation.

Example 5.11.

Let for . For , the lower bound is constant since does converge to a non-zero limit. For , the bound converges to zero slower than any polynomial, whereas it is of order for . Note that is random and unbounded. Finally for , the process reveals strong monopoly such that converges to an edge of the simplex at rate . In that specific case for , we can also derive an upper bound for , provided that agent is not the monopolist. Since the limit in Theorem 5.6 is non-zero and , there is a positive constant such that

and consequently

Defining yields:

Note that converges to zero at rate , so that we finally get the following estimate:

Thus, the bound in Corollary 5.10 can be considered as sharp.

If the second part of (34) is not fulfilled, i.e. , then fulfills the Lindeberg condition. Hence, Theorem 5.1 and its implications are wrong if we drop the condition . As already described at the end of Section 4, [30] derives a central limit theorem for polynomial feedback functions with . Moreover, [35, 37, 29] present another transition between functions satisfying this condition and those who do not.

Another remarkable property is the following: The proof of part 3 of Corollary 5.3 reveals that or for for all . This corresponds to a hierarchical structure of asymptotic market shares consistent with weak monopoly and the consistency property in Proposition 2.3, such that within each subset of agents a weak monopolist has full relative market share. Such hierarchical structures are often observed at phase transition points, in our case the transition between strong monopoly and deterministic limit shares.

6 A Law of Large Numbers for the dynamics

So far our investigations focused on the analysis of the long-time behavior of a generalized Pólya urn. This section examines the dynamics of the process in the limit for large initial market size , based on the concept of stochastic approximation (see e.g. [11, 39, 42, 9]), which traces back to [40]. Note that and depend on , thus we establish the notation and for this section and assume that is equal for all (up to roundings).

Theorem 6.1.

Define for

| (39) |

where we assume that converges for uniformly to a Lipschitz-continuous function on an open neighborhood of the image of the solution of the differential equation

| (40) |

Moreover, we define the following sequence of stochastic processes in :

Then: converges to weakly on the Skorochod space .

Similar ODE approximations of the generalized Pólya urn model have also been derived in [43, 8], but they rather focus on the embedded process from the exponential embedding and on the limit instead of .

Proof.

By construction, we have for all , where denotes the supremum norm. This implies by [25, Proposition VI.3.26] that the sequence is tight in , with the additional property that all weak limits of converging subsequences are concentrated on the subspace of continuous functions. We now take any converging subsequence and show that the limit solves (40). As the solution of (40) is unique due to the assumed Lipschitz-continuity of , this implies the claim. For simplicity of notation assume that the subsequence is itself. Then we can write the increments as

with . Note that is -measurable, where is the filtration generated by the process . Furthermore,

since with (39) . The are also uncorrelated, as for

| (41) |

Summing up the increments yields the standard Doob-Meyer decomposition

with predictable and martingale part, respectively

| (42) |

With uncorrelated and centered increments is a centered martingale with respect to the filtration , thus Doob’s inequality yields for any :

| (43) | ||||

| (44) |

since almost surely by definition. Hence, the sequence of stochastic processes converges to zero weakly on .

Now we turn to the predictable part . By the Skorochod representation theorem we can find a probability space such that the convergence of is almost sure. Then for fixed converges with respect to the Skorochod norm to a process on . As is continuous, the convergence is uniform on bounded time intervals. Denote the stopping time, when first leaves . Then for any and large enough we have and consequently

as the sequence of functions converges uniformly to on bounded time intervals. Thus, we have for that converges weakly on to which fulfills (40) and by uniqueness of solutions we have and . ∎

This means, that is asymptotically deterministic and driven by the vector-field modulo a time change. Let be the solution of the time-homogeneous differential equation

| (45) |

so that . Then for large the process is approximately given by . We can use this result e.g. to estimate the number of steps until the process reaches a given neighborhood of its long-time limit for large .

Corollary 6.2.

In the situation above let be an open neighborhood of and define the following last entrance times:

Then we have

This follows directly from the Theorem 6.1 via the continuous mapping theorem.

Another interesting consequence of Theorem 6.1 is the following. In the monopoly case described in Section 3, we may start our process in an unstable fixed point of the vector field . Although we know that the process exhibits strong monopoly, we have for all times in Theorem 6.1. This implies that a linear scaling of time is not sufficient to capture the escape from an unstable equilibrium.

Corollary 6.3.

Proof.

Simulations for indicate that the escape from an unstable equilibrium is faster the larger is. Recall that for superexponential feedback functions (see Corollary 3.11) the winner of the first step wins in all further steps with high probability if is large. Hence, it only takes time to escape from an unstable equilibrium in this case. Nevertheless, this does not pose a contradiction to Corollary 6.3 since the convergence of to is not uniform in an unstable equilibrium. Thus, Theorem 6.1 is not applicable and the assumption of uniform convergence can not be removed.

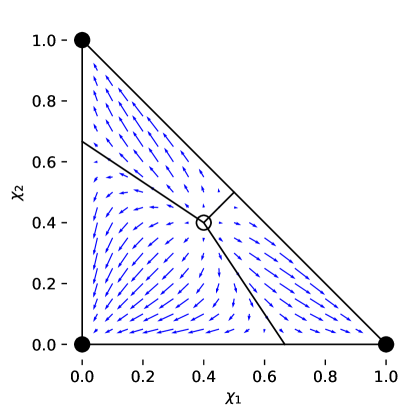

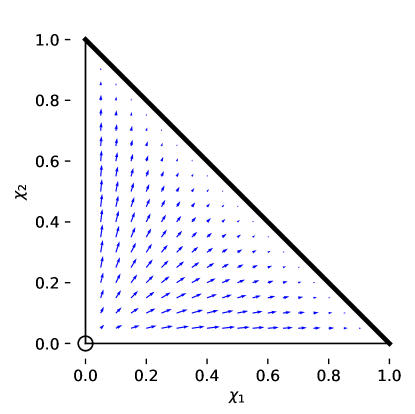

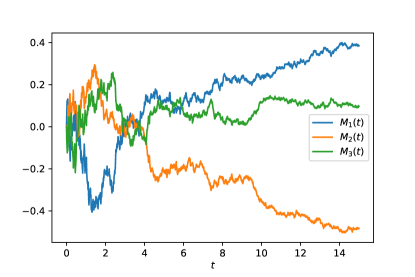

Figure 3 shows the dynamics of the process in various generic situations. The fixed points of the dynamics, i.e. the zeros of the vector-field , are the long-time market-shares of our generalized Pólya-urn, but only the stable fixed points are attained with positive probability. Figure (a), (b) and (c) comply with the properties found in the sections before, i.e. monopoly in the superlinear case and stable, non-zero market-shares in the sublinear case. Figure (d) underlines that the set of stable fixed points is not necessarily discrete. Note that when for all agents and a slowly varying function , then the field is constantly zero, such that all points are fixed points. In particular, this holds for the original Pólya urn, where is a constant function. If diverges, then the process exhibits weak monopoly resp. deterministic limits for finite (see Section 5), which is again not captured by Theorem 6.1 as it takes more than steps to reach the long-time limit.

Moreover, the assumptions of Theorem 6.1 are not fulfilled for exponential feedback, since is not continuous. Nevertheless, the dynamics in the limit are already described by Corollary 3.8, which states that all steps are won by the same agents as long as is not on the boundary between the attraction domains. Note that this is consistent with Theorem 6.1, i.e. (40) still holds.

Since only depends on and not , there are no limit cycles and the dynamics tends to a fixed point, as opposed to models discussed in [13].

7 A Functional Central Limit Theorem for the dynamics

In Section 6 we derived a functional law of large numbers for the process of market shares for large initial values, which states that the time-scaled process can be well approximated by a deterministic process for large . In order to gain an understanding of the fluctuations around this limit, we prove a corresponding functional central limit theorem in this section. Let us first state our main result. We use the notations introduced in Section 6 and establish furthermore the notation

| (46) |

for all . Note that the existence of is equivalent to the existence of . Denote by

| (47) |

the tangent space of .

Theorem 7.1.

Suppose that

| (48) |

Moreover, let be continuously differentiable on . Then we have

where is the solution of the system of stochastic differential equations

| (49) |

Here, denotes the differential operator of and is a standard Brownian motion, which is independent of if and for .

The differential operator for is the product with the gradient , when is defined on an open neighbourhood of in . [9] presents a central limit theorem in a general stochastic approximation setting. Further functional central limit theorems in the context of Pólya urns have recently been studied in [10] and [16].

For the proof, we use again the method of stochastic approximation. In the Doob decomposition (42), we prove separately a limit theorem for the martingale part in Subsection 7.1 and for the predictable part in Subsection 7.2, which directly imply Theorem 7.1 by summing up both. Note that Theorem 7.4 for the martingale does not use the rather restrictive condition (48). Within these Subsections, we discuss in detail the properties and interpretation of the diffusion part and the drift part of (49).

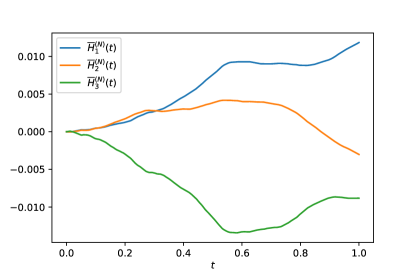

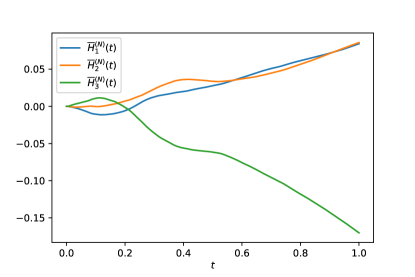

Figure 4 shows the process for large . We can observe that is close to zero for large . Indeed, this complies with formula (53).

Proposition 7.2.

In the situation of Theorem 7.1, assume that exists and that is a negative definite operator. Then

Proof.

As explained in Subsection 7.1, the generator of is given by

for . Thus, for we have

for a bounded function . Since is continuous and is negative definite, is also negative definite for , when is large enough. Thus, there is such that

for all and . In summary, we get

for . Now, applying Dynkin’s formula yields

for . Finally, the claim follows from Grönwall’s inequality:

For the almost sure convergence we fix a realisation , such that exists. Then we get from (53) and the Cauchy-Schwarz inequality that

for . Hence

which implies as . ∎

In generic examples one can show that is indeed negative definite, but it is also possible to find a counterexample.

Example 7.3.

Let for , such that

Since there is an obvious extension of to , the operator is negative definite if and only if the well-defined differential matrix is negative definite.

-

1.

Consider the monopoly case . Moreover, let be in the attraction domain of agent , i.e. . A simple computation shows for all , where denotes the Kronecker delta. Hence, is negative definite.

-

2.

In the monopoly case assume that is the unique unstable fixpoint of the vector field . Then and is positive definite. Thus, follows by similar argumentation.

-

3.

For , we have since . In this case does not converge to zero for . This is due to the fact that for and large (but finite) the time-limit is close to , but still random. For , the long-time limit can be predicted precisely for large (at least with high probability).

-

4.

Now, let . For simplicity, assume for all , but a similar argument is possible in a non-symmetric situation. Then . It can be shown that for some , i.e. is negative definite.

Note that the time-change factor in (49) does not change the long-time limit of the dynamics, but slows down the rate of convergence. The Grönwall estimate in the proof of Proposition 7.2 implies that converges to zero at least at rate . For the classical Pòlya urn we have , such that there is no convergence to zero.

As we can see, the first steps of our process are of particular interest. In order to put focus on this, Appendix A.1 examines the limiting behaviour of for and non-linear time scale .

7.1 Convergence of the martingale part

This subsection examines the martingale as defined in (42). We have already seen in Section 6 that vanishes for . Under appropriate scaling, we can yield the following central limit theorem, which accounts for the diffusion part of (49). For simplicity we will at first only consider one fixed agent (without loss of generality agent 1) while keeping general.

Theorem 7.4.

We assume that the convergence (46) is uniform on an open neighborhood of the image of and that is a Lipschitz continuous function on this neighbourhood. Moreover, denote by a time-inhomogeneous Markov process with generator

and . Then

Alternatively, the inhomogeneous Markov-process is characterized as the solution of the stochastic differential equation

where denotes a standard Brownian motion. Thus, is a time-changed Brownian motion. To be more precise, , where

is the quadratic variation process of . Note that is deterministic and monotone increasing in , and thus converges almost surely for and the limit has a centered Gaussian distribution with variance .

For the proof of Theorem 7.4, we first show tightness of the sequence on and then prove that the limit of any converging subsequence is a Markov-process with generator . For later use in Appendix A.1, we keep the tightness result a bit more general than necessary.

Lemma 7.5.

The sequence of martingales is tight for all .

Proof.

According to a version of the Aldous criterion in [46, Lemma 3.11], the following two properties are sufficient for the tightness.

2. Similarly, we get for and :

uniformly in . ∎

By the definition of tightness and Theorem 6.1, we also get tightness of the joint sequence . Before we turn to the proof of Theorem 7.4, we add another helpful lemma.

Lemma 7.6.

Proof.

Taylor-expansion of with Lagrange’s remainder yields:

Here, denotes a (random) intermediate value between and . Note that at rate . ∎

Now we are well prepared for the proof of Theorem 7.4.

Proof.

We show that for any limit of a convergent subsequence of, is a Markov process with generator . For simplicity of notation, assume that the sequence is convergent itself.

Take a smooth test-function with compact support. Then for each

| (50) |

is a martingale in continuous time as is a discrete-time Markov process. The continuous mapping theorem implies that converges to in . Due to Lemma 7.6, the sum converges as follows:

Convergence for holds almost surely on an appropriate probability space by Skorochod’s representation theorem, which implies weak convergence. Summing up, we have that (50) converges to

| (51) |

for . As and are bounded, the sequence in (50) is obviously uniformly integrable in . Thus, [46, Theorem 5.3] implies that (51) is a martingale as well. Moreover, the solution of the martingale problem (51) is unique as a time-changed Brownian motion is always the unique solution if its corresponding martingale problem. Hence, is a time-inhomogeneous Markov-process with generator . ∎

Example 7.7.

-

1.

Let and suppose that for an and all . Then almost surely for all , since for , in particular on the path of . This complies with the idea of a total monopoly described in Section 3.

-

2.

If , then for all and for all . Hence, for all . Note that in this case the martingale part encompasses the whole dynamic as for all .

-

3.

Let for all and . Since we start in a stable or unstable equilibrium point, we have and hence for all . In particular, does not depend on .

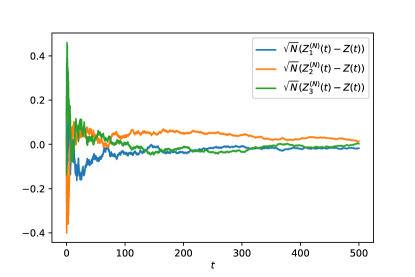

For non-linear, polynomial feedback functions and general initial market shares, the expressions for are lengthy or even not explicit. Figure 5 shows some realisations of the process . It can be seen that the convergence of for is faster the faster the feedback functions grow. In the monopoly case, the variation of is small if is already close to zero or one.

So far in this section, we only considered one fixed agent. Nevertheless, one can obtain an extension of Theorem 7.4 for all agents by a completely analogous, but lengthy argument, which we leave to the reader.

Theorem 7.8.

Suppose that the assumptions of Theorem 7.4 are fulfilled. Moreover, denote by an -dimensional time-inhomogeneous Markov process with generator

with and . Then

The specific form of the generator is due to the conditioned covariance matrix of the increments , which is for :

Alternatively, the -dimensional generator can be rewritten as

where is the second derivative along the diagonal . From this form of the generator it is easy to see (e.g. by a coordinate transformation) that solves the system of stochastic differential equations

| (52) |

where is a standard Brownian motion, which is independent of if and for . It follows immediately that for all . Hence, the sum is a conserved quantity. Consequently, the state space of is the tagent space . This allows the following interpretation of the limit process : Each pair of agents exchanges mass according to a time-changed Brownian motion and the exchange of several distinct pairs of agents is independent. Figure 5 finally shows two simulations of the process with polynomial feedback.

7.2 Convergence of the predictable part

In order to complete the proof of Theorem 7.1, let us now turn to the predictable part in the Doob decomposition (42), which accounts for the drift part of (49). It is important to recall that is deterministic when is given for . Because of that, it is possible to express the limit process of for in terms of the limit of . In Section 6, we derived that converges to the deterministic process for and the following result describes the deviation under appropriate scaling.

Theorem 7.9.

Suppose that the assumptions of Theorem 7.1 are fulfilled. Then

where is the solution of the system of random ordinary differential equations (RODE)

| (53) |

Here, denotes the differential operator of at the point , i.e. is the derivative of at in direction . Note that as well as (as described in the previous section) are in the tangent space (47), and therefore also . If is well defined on an open neighbourhood of in (like in Example 7.3), then can be interpreted as the common differential matrix and as the matrix-vector product.

The solution of a RODE is defined pathwise, in the sense that for any fixed realisation is a deterministic function, such that is the solution of the ordinary differential equation (53). Further details on the theory of RODEs can be found e.g. in [22].

Consequently for fixed , (53) is a linear, time inhomogeneous ordinary differential equation, whose solution can be expressed as the matrix exponential

An important part of the proof of Theorem 7.9 will be the tightness of the sequence of processes . For that, we bound its increments by the supremum of the martingale .

Lemma 7.10.

In the situation of Theorem 7.9 we have with probability one for all

where is a constant only depending on and .

Proof.

We are now ready for the proof of Theorem 7.9.

Proof.

Via [25, Proposition VI.3.26], we get tightness of from Lemma 7.10 and the stochastic boundedness of the sequence (see proof of Lemma 7.5). Now we show that the limit of any convergent subsequence is as desired. For simplicity of notation, assume that the sequence is convergent itself. Since Theorem 7.4 applies we can take an appropriate probability space , such that the convergence holds locally uniformly almost surely. Note that this already implies locally uniformly. Now, fix . Using (42) and the mean value theorem, we get

where is an intermediate value between and . In line 3, we used assumption (48) once again. The claim follows since (53) has a unique solution due to the Theorem of Picard-Lindelöf, and since for all . ∎

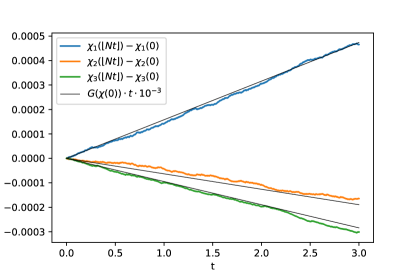

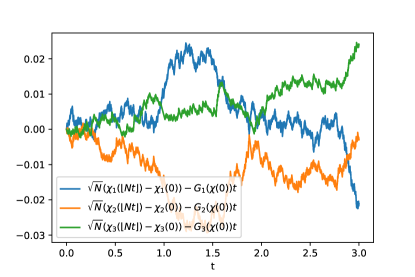

Figure 6 shows a simulation of the process for large and small . Note that the limit process (53) has continuously differentiable paths, their regularity is equivalent to that of integrated Brownian motion. As a consequence of Proposition 7.2, is convergent for with random limit in generic examples. Combining Theorem 7.8 and Theorem 7.9 yields the desired central limit theorem for the difference .

References

- [1] Giacomo Aletti and Irene Crimaldi, The Rescaled Pólya Urn and the Wright—Fisher Process with Mutation, Mathematics 9 (2021), no. 22, 2909.

- [2] Giacomo Aletti and Irene Crimaldi, Generalized Rescaled Pólya urn and its statistical application, Electronic Journal of Statistics 16 (2022), no. 1, 1635–1680.

- [3] Giacomo Aletti and Irene Crimaldi, The rescaled Pólya urn: local reinforcement and chi-squared goodness-of-fit test, Advances in Applied Probability 54 (2022), no. 3, 849–879.

- [4] W Brian Arthur et al., Increasing returns and path dependence in the economy, University of michigan Press, 1994.

- [5] Antar Bandyopadhyay and Debleena Thacker, A new approach to Pólya urn schemes and its infinite color generalization, The Annals of Applied Probability 32 (2022), no. 1, 46–79.

- [6] Andrew D Barbour, The asymptotic behaviour of birth and death and some related processes, Advances in Applied Probability 7 (1975), no. 1, 28–43.

- [7] Michel Benaïm, Itai Benjamini, Jun Chen, and Yuri Lima, A generalized Pólya’s urn with graph based interactions, Random Structures & Algorithms 46 (2015), no. 4, 614–634.

- [8] Michel Benaim, Sebastian J Schreiber, and Pierre Tarres, Generalized urn models of evolutionary processes, Annals of Applied Probability 14 (2004), no. 3, 1455–1478.

- [9] Vivek S Borkar, Stochastic approximation: a dynamical systems viewpoint, 48 (2009).

- [10] Konstantin Borovkov, Gaussian process approximations for multicolor Pólya urn models, Journal of Applied Probability 58 (2021), no. 1, 274–286.

- [11] W Brian Arthur, Yu M Ermoliev, and Yu M Kaniovski, Strong laws for a class of path-dependent stochastic processes with applications, Stochastic optimization, Springer, 1986, pp. 287–300.

- [12] Fan Chung, Shirin Handjani, and Doug Jungreis, Generalizations of Polya’s urn problem, Annals of combinatorics 7 (2003), no. 2, 141–153.

- [13] Marcelo Costa and Jonathan Jordan, Phase transitions in non-linear urns with interacting types, Bernoulli 28 (2022), no. 4, 2546–2562.

- [14] Codina Cotar and Vlada Limic, Attraction time for strongly reinforced walks, Annals of Applied Probability 19 (2007), no. 5, 1972–2007.

- [15] Burgess Davis, Reinforced random walk, Probability Theory and Related Fields 84 (1990), no. 2, 203–229.

- [16] Christopher BC Dean, Functional limit theorems for Pólya urns with growing initial compositions, arXiv preprint arXiv:2206.05138 (2022).

- [17] Eleni Drinea, Alan Frieze, and Michael Mitzenmacher, Balls and bins models with feedback, SODA, vol. 2, Citeseer, 2002, pp. 308–315.

- [18] Joe Dunlop, Monopoly in Balls-in-Bins Processes with Reinforcement and Fitness, Master’s thesis, University of Warwick, 2020.

- [19] Florian Eggenberger and George Pólya, Über die Statistik verketteter Vorgänge, ZAMM-Journal of Applied Mathematics and Mechanics/Zeitschrift für Angewandte Mathematik und Mechanik 3 (1923), no. 4, 279–289.

- [20] Samuel Forbes and Stefan Grosskinsky, A study of UK household wealth through empirical analysis and a non-linear Kesten process, Plos one 17 (2022), no. 8, e0272864.

- [21] David A. Freedman, Bernard Friedman’s Urn, The Annals of Mathematical Statistics 36 (1965), no. 3, 956 – 970.

- [22] Xiaoying Han and Peter E Kloeden, Random ordinary differential equations and their numerical solution, Springer, 2017.

- [23] Norbert Henze, Stochastik: eine Einführung mit Grundzügen der Maßtheorie: inkl. zahlreicher Erklärvideos, Springer-Verlag, 2019.

- [24] Bruce M Hill, David Lane, and William Sudderth, A strong law for some generalized urn processes, The Annals of Probability (1980), 214–226.

- [25] Jean Jacod and Albert Shiryaev, Limit theorems for stochastic processes, vol. 288, Springer Science & Business Media, 2013.

- [26] Ian R. James and James E. Mosimann, A New Characterization of the Dirichlet Distribution Through Neutrality, The Annals of Statistics 8 (1980), no. 1, 183 – 189.

- [27] Svante Janson, Cécile Mailler, and Denis Villemonais, Fluctuations of balanced urns with infinitely many colours, arXiv preprint arXiv:2111.13571 (2021).

- [28] Bo Jiang, Daniel R Figueiredo, Bruno Ribeiro, and Don Towsley, On the duration and intensity of competitions in nonlinear Pólya urn processes with fitness, ACM SIGMETRICS Performance Evaluation Review 44 (2016), no. 1, 299–310.

- [29] Michael J Kearney and Richard J Martin, First passage properties of a generalized Pólya urn, Journal of Statistical Mechanics: Theory and Experiment 2016 (2016), no. 12, 123407.

- [30] Kostya Khanin and Raya Khanin, A probabilistic model for the establishment of neuron polarity, Journal of Mathematical Biology 42 (2001), no. 1, 26–40.

- [31] Konrad Kolesko and Ecaterina Sava-Huss, Gaussian fluctuations for the two urn model, arXiv preprint :2301.08602 (2023).

- [32] Krishanu Maulik and Manit Paul, Feedback interacting urn models, arXiv preprint arXiv:2211.07573 (2022).

- [33] Mikhail Menshikov and Vadim Shcherbakov, Balls-in-bins models with asymmetric feedback and reflection, arXiv preprint arXiv:2204.05724 (2022).

- [34] Michael Mitzenmacher, Roberto Oliveira, and Joel Spencer, A scaling result for explosive processes, the electronic journal of combinatorics 11 (2004), no. 1, R31.

- [35] Roberto Oliveira, Preferential attachment, New York University, 2004.

- [36] Roberto Oliveira, Balls-in-bins processes with feedback and brownian motion, Combinatorics, Probability and Computing 17 (2008), no. 1, 87–110.

- [37] Roberto Oliveira and Joel Spencer, Avoiding defeat in a balls-in-bins process with feedback, arXiv preprint math/0510663 (2005).

- [38] Roberto Imbuzeiro Oliveira, The onset of dominance in balls-in-bins processes with feedback, Random Structures & Algorithms 34 (2009), no. 4, 454–477.

- [39] Robin Pemantle, A survey of random processes with reinforcement, Probability surveys 4 (2007), 1–79.

- [40] Herbert Robbins and Sutton Monro, A stochastic approximation method, The annals of mathematical statistics (1951), 400–407.

- [41] Ioanid Roşu and Fahad Saleh, Evolution of shares in a proof-of-stake cryptocurrency, Management Science 67 (2021), no. 2, 661–672.

- [42] Wioletta M Ruszel and Debleena Thacker, Positive reinforced generalized time-dependent Pólya urns via stochastic approximation, arXiv preprint arXiv:2201.12603 (2022).

- [43] Sebastian J Schreiber, Urn models, replicator processes, and random genetic drift, SIAM Journal on Applied Mathematics 61 (2001), no. 6, 2148–2167.

- [44] Wenpin Tang, Stability of shares in the proof of stake protocol–concentration and phase transitions, arXiv preprint arXiv:2206.02227 (2022).

- [45] Bálint Tóth, Limit theorems for weakly reinforced random walks on , Studia Scientiarum Mathematicarum Hungarica 33 (1997), no. 1, 321–338.

- [46] Ward Whitt, Proofs of the martingale fclt, Probability Surveys 4 (2007), 268–302.

- [47] Tong Zhu, Nonlinear Pólya urn models and self-organizing processes, Unpublished dissertation, University of Pennsylvania, Philadelphia (2009).

- [48] Somya Singh, Fady Alajaji and Bahman Gharesifard, Generating Preferential Attachment Graphs via a Pólya Urn with Expanding Colors, arXiv preprint arXiv:2308.10197 (2023).

- [49] Qin Shuo, Interacting urn models with strong reinforcement, arXiv preprint arXiv:2311.13480 (2023).

Appendix A Appendix

A.1 Functional Limit Theorems with non-linear time scale

From a stochastical point of view, the first steps of a generalized Pólya urn are of special interest because the randomness plays a significant role. In the later stages of the process, the market shares and thus the probability of winning in a certain step remain almost invariant, such that the sequence of winners is almost independent and identically distributed for large . Even in the Central Limit Theorem 7.4 the limiting process becomes virtually constant for large . In order to particularly focus on the early stages of the process, we analyse the process for large initial market size and . Recall the Doob decomposition (42) and the notations from Section 6.

Theorem A.1.

Suppose that the assumptions of Theorem 7.4 are fulfilled and denote by a standard Brownian motion. Then for any we have weak convergence to a Brownian motion on :

Proof.

We will only sketch the proof as it is quite analogous to the proof of Theorem 7.4. We use the tightness given by Lemma 7.5 and assume that the sequence converges to a process . Then we take a smooth test-function with compact support and consider the martingales

Then we know that converges to and via Lemma 7.6 we get:

where we have used and in the last step. This implies that is a Markov process with generator . Hence, is the desired Brownian motion. ∎

Note that Theorem A.1 is consistent with Theorem 7.4 for small . This limiting Brownian motion can be understood as a consequence of Donsker’s invariance principle, since the shares do barely change at the beginning of the process for large initial values. Again, a straight forward extension to higher dimensions is possible.

Theorem A.2.

Suppose that the assumptions of Theorem 7.4 are fulfilled and let . Then the sequence of processes converges for to a time-homogeneous Markov process with generator

weakly on .

As in Subsection 7.1, the limit process can be interpreted as independent exchanges of mass between pairs of agents according to a Brownian motion.

We already know from Theorem 6.1 that converges to for , when . Moreover, Theorem A.1 states, that the process converges to zero at rate . In addition, it follows from

that converges to at rate , which immediately implies the following law of large numbers.

Corollary A.3.

Under the assumptions of Theorem A.1 we have

Combining these results for an analysis of the deviations of requires further distinction of as specified in the following functional CLT.

Corollary A.4.

Let and as specified below. Suppose that

Moreover, let be continuously differentiable. Then

where the limiting process is defined as follows:

-

1.

For set . Then:

- 2.

-

3.

For set . Then .

Proof.

The assumptions of Theorem A.4 are satisfied e.g. for . To sum up, in the limit the process stays at for all time . After scaling, Corollary A.3 reveals a linear drift into direction . The fluctuations around this linear drift can itself be described by a random SDE for and by a deterministic ODE for , since second order terms dominate the randomness for too large . These findings are illustrated by Figure 7.

A.2 Exponentially decreasing feedback

Based on an example, this supplemental section discusses the long-time limits of a Pólya urn with exponentially decreasing feedback, since this case is not covered by our previous results.

Example A.5.

Let and . As explained in detail in Section 6, we can write

where is an almost sure convergent martingale and

is predictable with given by centered transition probabilities (2). In the case of exponentially decreasing feedback, we have the following convergence:

| (54) |

The convergence is locally uniform in apart from the point . Take . For large enough , is sufficiently close to outside an -neighborhood of . If for a large , , then the process enters the -neighborhood of in finite time because of the convergence of the martingale. As the same holds for instead of , we get that the process leaves this -neighborhood only finitely often. This yields

Thus, the limit is not only independent of the initial market shares, but also of the fitness-parameters (in contrast to polynomially decreasing feedback). Note that these findings are consistent with Corollary 4.5, i.e. (29) still holds. Because of the independence property in the exponential embedding in Section 2, this can easily be extended to general A. For different (at least) exponentially decreasing feedback, we basically only need a convergence as in (54) for an analogous result.

Remarkably, Example A.5 reveals the following behavioural difference between exponentially decreasing and polynomial feedback. Suppose that there are agents such that