Interpretable System Identification and Long-term Prediction on Time-Series Data

Abstract

Time-series prediction has drawn considerable attention during the past decades fueled by the emerging advances of deep learning methods. However, most neural network based methods lack interpretability and fail in extracting the hidden mechanism of the targeted physical system. To overcome these shortcomings, an interpretable sparse system identification method without any prior knowledge is proposed in this study. This method adopts the Fourier transform to reduces the irrelevant items in the dictionary matrix, instead of indiscriminate usage of polynomial functions in most system identification methods. It shows an interpretable system representation and greatly reduces computing cost. With the adoption of norm in regularizing the parameter matrix, a sparse description of the system model can be achieved. Moreover, Three data sets including the water conservancy data, global temperature data and financial data are used to test the performance of the proposed method. Although no prior knowledge was known about the physical background, experimental results show that our method can achieve long-term prediction regardless of the noise and incompleteness in the original data more accurately than the widely-used baseline data-driven methods. This study may provide some insight into time-series prediction investigations, and suggests that an white-box system identification method may extract the easily overlooked yet inherent periodical features and may beat neural-network based black-box methods on long-term prediction tasks.

Index Terms:

Time-series prediction, Long-term prediction, Sparse identification, Model-based method, Machine learning1 Introduction

Accurate time-series prediction is of crucial importance in the era of big data, which is widely used in many fields of modern industry, such as prediction on energy consumption, weather change, disease spreading, traffic flow and economic evolution [1, 2, 3, 4, 5]. It has attracted widespread attention of scientists ranging from mathematics, computer science, and other related specific engineering fields. Therein, a large number of achievements have been obtained and show appreciable performance. However, long (e.g., more than one thousand steps) and stable prediction has still been a tricky but significant problem to untangle due to the lack of deep understanding of the hidden mechanism in the targeted physical system [6]. Moreover, most existing methods are proposed in a deep learning framework, which cannot meets the requirement of interpretable and reliable mechanism to be used in large-scale industrial systems. This motivates us to further investigate the mechanism of the system evolution with a white-box format and get rid of the usage of a black-box neural network module.

Towards time-series prediction, two mainstream ways have emerged in order to solve this problem over recent years. One arises from data-driven methods, e.g., neural networks (NN) and statistical learning. These kinds of approaches can form end-to-end prediction without explicit mechanistic model. The early data-driven methods include Back-Propagation Net (BP Net) [7] and Auto-regressive Integrated Moving Average model (ARIMA) [8], which work well in prediction for small-scale system with simple rules. However, in most systems with complex nonlinearity and stochasticity, neither of these models can guarantee prediction accuracy in long-term prediction. In order to increase the capability of long-term prediction, a variety of recurrent neural networks (RNNs) have been proposed. Two widely-used RNNs are Long Short-Term Memory (LSTM) [9] and Gate Recurrent Unit (GRU) [10], which show priority in handling and predicting important events with long interactions in time series [11, 12]. But RNNs and their variant models have far more parameters than typical NNs, which require longer time to train the model and have more risk of over-fitting. To overcome this, Temporal Convolution Network (TCN) [3] was subsequently proposed. TCN uses causal convolution to model temporal causality, allowing parallel computation of output which can improve network performance compared to RNNs. Unfortunately, using TCN for long-term prediction requires multiple iterations of multi-step (or single-step) forecasting, which will induce error accumulation and thus lose effect in capturing long-term mechanisms [13]. Recently, with the invention of Transformer [14] which only based on self-attention mechanism, many variants of Transformer models [15, 4, 1] have been successively used for long-term prediction without multiple iteration. Among them, Autoformer [1] yielded state-of-the-art results with both accuracy and computational speed. Nevertheless, Autoformer requires sufficient amount of data for training, and the prediction length can only reach up to hundreds of time points with guaranteed accuracy. Although these data-driven methods achieved great performance in specific prediction tasks and have been widely used in practical systems, they still suffer from interpretability and stability in extracting physical mechanism. Because they uniquely adopt the black-box NN framework and lack the capability of inferring system dynamics.

The other prevailing way is based on system identification. Considering that most engineering systems evolve with underlying physical mechanisms in real scenes [16, 17, 18, 19], original problem can be transformed into a sparse identification of time-series. Orthogonal Matching Pursuit algorithm (OMP) [20] is one of the earliest algorithms to solve this problem. By using greedy idea, this method can quickly obtain the sparse model, but it cannot reach the optimal solution in most cases. To improve it, LASSO [21] and Sparse Bayes Method [22] were proposed, respectively, which can obtain the optimal solution under prior knowledge and assumptions. However, such prior assumptions may be difficult to satisfy in reality and the prior knowledge is limited or even unable to obtain in most target systems. Recently, Sparse Identification of Nonlinear Dynamics (SINDy) [23] and Identification of Hybrid Dynamic System (IHYDE) [24] based on discovering governing potential equation in noisy complex systems showed well performance in real scenes, such as autonomous vehicles, fluid convection, medical applications, etc. Many related models [25, 26, 27, 28] emerged quickly in this field. However, an inevitable bottleneck in current sparse identification methods is the dilemma between balancing the number of basis functions and the complexity of computation. Paying too much attention to the former will lead to unbearable computational time [29], which will even spend more time than training large-scale neural networks. On the contrary, taking excessive interest in the latter will lead to inaccurate identification results [23]. Such a dilemma hinders the long-term prediction of sparse identification in time-series.

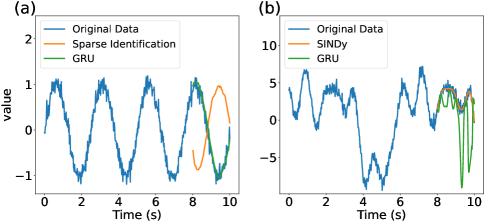

To further illustrate the current bottlenecks of existing model-based and data-driven methods, a controlled experiment has done. Two classes of time series as follows are constructed. Both model-based and data-driven methods are used for prediction of the constructed time series, respectively. The sparse identification method fails in extracting the mechanism in Fig 1.(a), because the generated rule is not assumed in the basis functions, while GRU predicts well due to the simple generated rule of time series [30]. In contrast, when fitting an erratic curve in Fig. 1.(b), NN can only make short-term accurate predictions. But owing to the assumed basis functions including part of the generated rule, SINDy yields better prediction results [23].

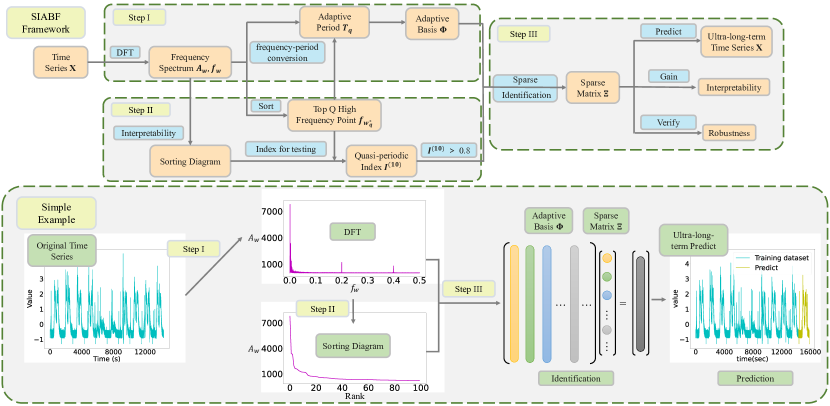

Thus, in order to improve accuracy and computation speed for time-series prediction, especially in long-term tasks, this study proposes a novel sparse system identification method with adaptive basis functions (SIABF), including three implementing steps. In the first step, the prior basis function library is given and the selection criterion is evaluated. Considering that the vast majority of time-series potentially contain periodicity [31], Discrete Fourier Transform (DFT) [32] is used at first to transfer time domain to frequency domain. By sorting the frequency rank in descending order according to the amplitude of the DFT spectrum, the resorting diagram which implies the strength of intrinsic potential periodicity were obtained. The prior period obtained in the top ranks of the resorting diagram by time-frequency conversion formula [33] will be used in the prior Fourier basis functions. In the second step, an evaluation index for the quality of prior basis is provided before making the prediction. We define the quasi-periodic index as the ratio of the top ten fastest decline slope to the maximum amplitude in the sorting diagram, which indicates the period complexity of the whole time series. The value of can provide an effective reference for the applicability of prior basis selection. The third step is long-term prediction by using sparse identification. The format of the prior basis functions are assumed to mainly include a series of sine and cosine functions with that evaluated top frequency ranks in the first step. With adopting the norm in regularizing the parameter matrix [21, 22], a sparse identification of time-series is achieved. One may use the identification result to make long-term prediction for time series.

Compared with existing model-based and data-driven methods, SIABF has the following advantages. The prior periods obtained by DFT not only provide the most likely candidates in the basis function library, but also endow the entire model with interpretability in the frequency domain which NN based methods cannot provide [34]. SIABF greatly reduces the dimension of basis functions matrix compared to other model-based methods [23, 24, 28]. Moreover, it can achieves long-term prediction by leveraging the underlying dominant frequency hidden in any physical systems, compared to most widely-used celebrated data-driven methods [1, 10, 11].

The main contributions of this paper are as follows:

-

1.

A novel interpretable sparse system identification method is proposed, which captures the essential periodic factors with transformation into the frequency domain. The underlying frequency features obtained and used in the basis functions clearly describe the evolution mechanism of the physical system.

-

2.

The proposed SIABF model achieves highly accurate and stable prediction results with less computation and training time in the long-term prediction task on time series.

-

3.

The state-of-the-art results are obtained via comprehensive comparisons with other well-accepted latest model-based and data-driven baseline methods under the test on temperature, water conservancy and finance datasets. Obvious priority has been observed in the comparison experiments.

The rest of this paper is organized as follows. Section 2 describe the problem and preliminaries of sparse identification for time-series prediction. Section 3 presents the details of the proposed SIABF model. Section 4 shows the comparison with other baseline methods via numerical experiments. Section 5 concludes this paper.

2 Problem and Preliminaries

In this section, the description of sparse identification problem is presented along with some preliminaries in order to describe more clearly the methodology later.

2.1 Problem Description

The traditional sparse identification problem of time-series prediction can be described as follows [23]:

| (1) |

where, , is the state of the -th of output of the system with predicted steps. is a -dimensional vector-valued function, which represents the basis function library in sparse identification. is the prediction time, represents the 1, 2, …, -step data of all systems before the prediction data in the -order dynamic equation. Especially, for the 0-order dynamic equation (i.e., algebraic equation), it has . is the tolerable error term of the model, and . is the sparse coefficient matrix which is the core of sparse identification. The target is to obtain the sparse matrix in the model, i.e.,

| (2) |

Here, . The basic idea of time-series prediction with sparse identification is to train with in the sample data, so that conforms to Eq. (2), and are subject to Eq. (1).

2.2 Preliminaries for System Identification

Without loss of generality, for sparse identification of time series, two basic problems need to be solved. One is the selection of basis function library , the other is the applicability of the sparse solution under equation Eq. (1) in sample data.

The selection of basis function is a thorny problem in sparse identification. Most of the existing methods put all the basic elementary functions into the library matrix [23, 28], including polynomial basis, trigonometric basis, logarithmic basis, exponential basis, constant basis, etc. In brief, can be written as

| (3) |

where, are real numbers and represents . In the basis function library, because the functions of different exponents or logarithms are linearly correlated, only one exponential or logarithmic basis is required. In this case, the main part of lies in the polynomial and trigonometric basis. Considering that in Eq. (3) can be any real number, one solution is to select one basis according to the data and traverse or to get as many natural numbers as possible. The theoretical basis for this is Weierstrass’ two approximation theorems[35]. This seems to be a good way if one knows the possible composition of the right term of the dynamical equations. Many studies have obtained significant performances [25, 26, 24] with knowledge of its possible underlying governing equations. However, it is not possible to obtain the form of the right-hand term in advance. Because without a prior knowledge, even fitting the simplest curve with a large number of basis functions, one may get bad prediction results (see Fig. 1.(a)). Meanwhile, excessive selection of basis functions may not only bring the risk of over fitting, but also need to bear large computational pressure, which is called dimensional disaster [36]. In this circumstance, a novel method to find the basis function library is urgent to be proposed.

The applicability of the sparse solution is also a tough problem. Since the original problem is an NP-hard [37] one, most of the existing solutions are approximate or optimal solutions under some additional conditions. At present, there are three main ways to solve sparsely. The first idea is to solve through greedy thought. OMP [20], Relaxed-Greedy Algorithm (RGA) [38] and SINDy [23] are all representatives of such an idea. They select the local optimal solution in each iteration, so that the original NP-hard problem can be solved in polynomial time. Taking SINDy [23] as an example, when solving in the -th iteration, the iterative process is as follows,

| (4) |

where, is the -th column of , and the and are defined as

where the threshold is the super parameter that can be adjusted. This method can quickly find a sparse solution by using the least squares method in Eq. (4), but it is obviously not the sparsest case in the model.

The second idea is to replace the norm in Eq. (2) with norm, which transforms the original problem into a convex optimization problem. In that case, it can be solved in polynomial time. The original problem is equivalent to the following optimization, which can be described as

| (5) |

where is the super parameter that can be adjusted. The original problem refers to LASSO with , and Ridge Regression with . Coordinate descent method[21] and least angle regression[39] are both mature solutions of the method. Among norm, the best sparse effect can be obtained with norm. However, although the obtained result is sparse, it is not the solution of the original problem. obtained by this method is a good alternative to the original problem in cases where the sparsity of is not strictly required.

The third idea is to give a prior probability to the coefficient of original problem, and use Bayesian statistical learning method to solve the problem. One may assume that each is independent of each other, and they all obey the Gaussian distribution , i.e.,

with (Normal-Jeffreys prior). According to Bayesian formula, the posterior probability of is obtained after simplification, i.e.,

where is the kernel function of , while . The final optimization form can be obtained by using the log maximum likelihood estimation for a posterior probability , i.e.,

| (6) | ||||

where the superscript (or ) represents the value of the -th (or -th) moment in time series. Eq. (6) is a solvable convex optimization problem. Here, the prior probability does not have to be Gaussian prior, and other types of prior probability are also emerging quickly [40, 41, 42]. These three ideas Eq. (4)-(6) greatly enrich the solution of sparse identification.

However, following the research line, the naturally inspired question is whether it is possible to choose a model-based rather than a data-driven method to solve the practical prediction problem? To put it another way, can we know the effectiveness of sparse identification methods before solving ? The existing methods do not give an index to evaluate the effectiveness of the model, so we can only constantly try various methods including model-based and data-driven, which is quite laborious and time-consuming.

In the following section, we will give a unique and general prior knowledge for the basis functions and propose the evaluation index for SIABF. This will alleviate these two problems to a certain extent.

3 Sparse Identification with Adaptive Basis Functions (SIABF)

In this section, the core methodology will be introduced. SIABF is divided into three steps. The first step is used to find adaptive basis in time series. The second step is to discriminate the effectiveness of basis. The third step is to compute sparse matrix and verify the robustness of the model. The implementing process of SIABF is shown in Fig. 2. With SIABF, the problems of current model-based method mentioned in section 2 can be effectively solved.

3.1 Methodology

In this part, a method for selecting adaptive basis functions will be proposed, which differs from traditional model-based methods under artificial experience. On this circumstance, a validation method on the effectiveness of adaptive basis is given as well.

3.1.1 Step I: Adaptive Period

First, it is necessary to determine what basis function to select for identification in Eq. (3). Note that most practical data embed periodicity, tendency and stochasticity[31]. Targeted prior basis functions should be designed. Considering that there often exist mutation points in the practical sample data and the tail of high-order polynomial identification will produce a large Runge phenomenon[43], polynomial fitting is inadequate. Moreover, owing to the polynomial function has infinite values at infinity, the long prediction points may produce large errors. Thus, the identification basis function library will mainly adopt the triangular base in Eq. (3).

For the time series of a certain physical system with length , in order to obtain the potential period information hidden in the data, DFT() with module of amplitude and frequency is adopted,

| (7) |

| (8) |

where represents sample frequency, refers to the value of the -th component in and is the imaginary unit. Due to the conjugate symmetry of DFT, only positive frequency needs to be take into consideration, which means that only needs to traverse half length of the data. According to the property of DFT, the greater value of , the more influence of the corresponding frequency in the time series data. Therefore, we sort from large to small, selecting top , and find the corresponding argument , i.e.,

where, represents the -th largest number in . In this way, one can find the high frequency of the time series. By using the frequency-period conversion formula , the most likely period existing in the time series can be obtained. These periods are recorded as and named as the adaptive period. These are brought into the basis function library of the identification process, in which, each in Eq. (3) can be written as

| (9) |

It is worth noting that the change of time series can be basically expressed by these periods. Therefore, one can describe the main period of transformation in this time series by selecting the maximum corresponding amplitude in the periods. This improves interpretability of the model to a higher level compared with artificially selecting adaptive basis functions or only using polynomials inspired by Taylor expansion. In addition, the number of prior cycles (i.e., the size of ) for selection may not be very large. Compared with the traditional traversal scheme for natural numbers[23, 24], our model will greatly reduce the computational complexity. This makes the model more suitable for solving large-scale and long-term prediction.

In this way, the basis function in sparse identification is adaptively selected from (7) and (8). It is worth noting that the main parts of adaptive basis functions are chosen only through sample time series, which is adaptive and includes the key periodicity features that are easily ignored. The first problem of sparse identification mentioned above, i.e., selecting adaptive basis functions is solved accordingly.

3.1.2 Step II: Quasi-periodic Index

Generally, complex systems encrypts specific physical mechanism that cannot be entirely uncovered and described. In other words, it is indeed that not all the prior knowledge including periods obtained by DFT can be taken into the identification model for prediction. In this paper, the index to evaluate the quality of basis function selection will be introduced before identification and prediction. The significance of this index is to avoid wasting time training unnecessary models. Moreover, this index also provides some insight into distinguishing the boundaries of model-based and data-driven models.

The original time series need to be represented by as few adaptive basis functions as possible. One advantage is that for a small number of basis function identification, the probability of forming over-fitting is very low. On the contrary, if the time series need a large number of adaptive periods to form the basis function, even if the original data is restored, it will not be used for prediction due to the high probability of over-fitting.

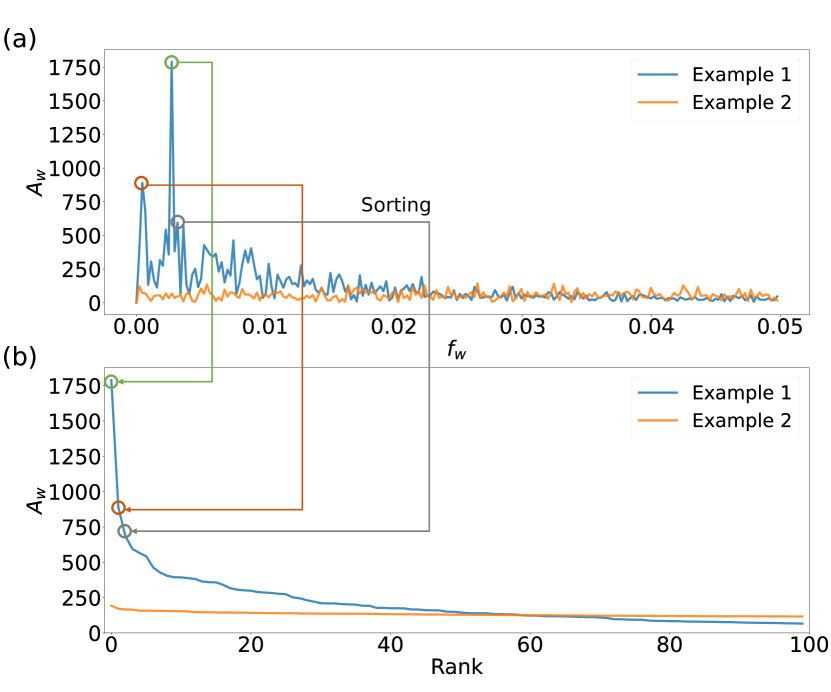

In order to quantify the effectiveness of the proposed method on adaptive period selection, the amplitude in DFT will be sorted to obtain the sorting diagram (Fig. 3). According to the property of DFT, the ordinate in sorting diagram represents the amplitude at the corresponding frequency. If the amplitude at the top ranks decreases fast enough in the diagram, that is, the modulus of most DFT results approaches zero, it can be concluded that the period feature affecting the time series is only limited to the top few ranks of frequency with larger amplitudes. Thus, it is sufficient to only use a few prior periods to describe the time series.

Accordingly, the quasi-periodic index is proposed, which is defined as the ratio of the sum of the top ten slopes in any sorting diagram formed by prior basis functions with the maximum amplitude in the DFT, i.e.,

Quasi-periodic index, , represents the contribution of the ten most important frequencies to the overall time series. We can empirically judge whether the obtained adaptive period can be further used for sparse identification according to the value of . From the current experimental situation, typically, if (Fig. 3 Example 1), the effect in long-term prediction will be much better than NN based methods, but if (Fig. 3 Example 2), such a system identification method may not work. When is between the middle value (), it has its own pros and cons compared with the data-driven method. Note that, the larger value of , the greater possibility that this method is better than data driven-methods in long-term prediction. This indicator may provide an effective criterion for distinguishing model-based or data-driven methods.

In this way, one can judge the applicability of this method before sparse identification. The second problem of sparse identification mentioned above is solved.

3.1.3 Step III: SPARSE IDENTIFICATION AND ROBUSTNESS TEST

In this step, can be identified sparsely by any traditional identification method with the obtained prior basis in step I-II.

Similar to Eq. (4)-(6), norm is used to identify the sparse matrix with the prior basis function, i.e.,

| (10) |

where is the identification duration and is a hyperparameter, which regulates the sparsity of . The value of can be obtained by the cross validation method[21, 28]. The solution process of Eq. (10) is to solve a convex optimization problem, and the sparse solution can be quickly obtained through Coordinate descent method [21] or least angle regression [39].

The resultant of captures the truly effective adaptive basis function in time series. These identified basis functions, including their coefficients, will be used together for long-term prediction. Each step can be expressed as,

| (11) |

Moreover, in algebraic equation, Eq. (11) does not need iteration. In this case, it will have an extreme long prediction ability without error accumulation.

Furthermore, it is necessary to test the robustness of SIABF. The following experiment is conducted: in the control group, the complete training data are used to predict through SIABF. For the experimental group, 5% of the training data are deleted. For the deleted data, the missing values are interpolated, so as to keep the dimension of the training data consistent with the control group. Secondly, a random disturbance is given to the training data, which does not necessarily follow the normal distribution, but is completely random. In this case, the training data will be different from the control group. The experiments are carried out on the experimental group and the control group, and the prediction indicators are compared, respectively. If the prediction effect of the experimental group is not significantly weaker than that of the control group, this shows that SIABF does have robustness.

3.2 Implementation and Algorithm

Adding the adaptive period and quasi-periodic index to the identification methods, by using norm as a penalty term and considering noise to the time series, a complete SIABF model process is obtained. SIABF can find the basis function library adaptively, as well as achieve self-evaluation.

As shown in Fig. 2, the entire identification process can be divided into two phrases with three steps. The first and second step can obtain the adaptive basis with verification. The third step solves sparse identification problem and completes the prediction. Recalling the entire model, the proposed method is summarized in Algorithm 1.

4 Experiments

4.1 Experimental Settings

4.1.1 Datasets

To test the performance and stability of the proposed model SIABF, three time series datasets are used, including water conservancy, global temperature and finance dataset[44, 45, 46].

Water conservancy dataset (Dataset 1), from NOAA National Water Model Retrospective dataset, records the mean, maximum and standard deviation of water conservancy data of a river with an sampling interval of 1 hour. The recording time is as long as several decades, and the number of the recording points is more than ten thousands.

Global temperature dataset (Dataset 2), from NCEP-NCAR Reanalysis, records the global temperature for nearly 70 years since 1950. The recording spatial resolution is . The number of spatio-temporal data points exceeds 500 thousands.

Finance dataset (Dataset 3) records the financial data of 22 major cities in China. This dataset includes nine days records with sampling interval of 1 hour. The total data volume exceeds 100 thousands.

4.1.2 Baselines

In order to demonstrate the effectiveness of SIABF, several commonly and newly used time series prediction models are selected. The baselines are classified into two categories based on model-based and data-driven methods.

The compared model-based methods include:

-

•

ARIMA [8] Auto-regressive Integrated Moving Average model. It is generally recorded as ARIMA, where is the number of auto-regressive terms, is the number of moving average terms, and is the number of differences (orders) to make it a stationary sequence.

-

•

SBL [22] Sparse Bayesian Learning method. A common and mature sparse identification method with the assumption that prior distribution of coefficients follows the normal distribution of zero mean.

-

•

SINDy [23] A method for discovering governing equations by the threshold least square. This method can quickly find the sparse solution of the coefficient matrix by using the greedy idea.

The compared data-driven methods include:

-

•

LSTM[9] A commonly used RNN for time series prediction is specially designed to solve the long-term dependence of the general RNN.

-

•

GRU[10] An improved RNN for LSTM. The network can achieve a prediction result close to that of LSTM with fewer training parameters.

-

•

ResNet[47] 2016 ImageNet champion network. After that, the network has been applied in various scenarios including time series.

-

•

Autoformer[1] The state-of-art network for long-term prediction at present. It has achieved the best results in the prediction of multiple open datasets.

4.1.3 Evaluation Methodology

For fair comparison, all the experiments were performed on the same machine and all the data are normalized. The prediction results are judged from the perspectives of time, accuracy and interpretability. In terms of accuracy, four popular indicators are adopted including RMSE (Root Mean Squared Error), MAE(Mean Absolute Error), R2(R square) and MAPE(Median Absolute Percentage Error) to judge their performances. In order to prevent the influence of the near zero point on MAPE, different from the traditional MAPE definition, the following format is adopted

where is the prediction value and is a small positive number in case the denominator is zero. Each method runs ten times to obtain the average results.

4.1.4 Parameter settings

Optimal parameters suitable for validation data as the initial input of all baselines have been searched and tested. After the repeated tests, the hyperparameters of model-based methods are set as: = 5e-4 in LASSO, = 1e-8, = 5e-5 in SBL, = 1e-2 in SINDy. are automatically selected in ARIMA. Parts of hyperparameters in data-driven methods are set as: batch size = 50, learning rate = 1e-3, all the epochs in training of network 200.

4.2 Performance Comparison

| Predict Type | Complete training dataset | Incomplete and noisy training dataset | Elapsed Time (s) | |||||||

| Metric | RMSE | MAE | R2 | MAPE (%) | RMSE | MAE | R2 | MAPE (%) | ||

| Data -set 1 | ARIMA | 1.052 | 0.859 | -1.37E5 | 35.011 | 1.052 | 0.861 | -7.89E5 | 34.517 | 30.874 |

| SBL | 0.791 | 0.548 | -0.833 | 23.153 | 0.789 | 0.547 | -0.831 | 23.148 | 0.042 | |

| SINDy | 0.864 | 0.643 | 0.046 | 38.186 | 0.864 | 0.643 | 0.050 | 38.323 | 0.022 | |

| LSTM | 1.058 | 0.876 | -9.22E3 | 33.054 | 1.586 | 1.271 | -2.009 | 72.813 | 718.962 | |

| GRU | 1.330 | 1.113 | -4.459 | 32.536 | 1.427 | 1.078 | -1.736 | 34.386 | 650.110 | |

| ResNet | 1.087 | 0.800 | -3.243 | 44.520 | 1.097 | 0.806 | -2.183 | 48.667 | 71.883 | |

| Autoformer | 0.814 | 0.613 | -1.382 | 25.668 | 0.903 | 0.661 | -1.817 | 26.782 | 92.802 | |

| SIABF | 0.491 | 0.393 | 0.777 | 19.222 | 0.494 | 0.392 | 0.772 | 19.749 | 0.247 | |

| Data -set 2 | ARIMA | 1.067 | 0.928 | -600.733 | 0.401 | 1.063 | 0.925 | -513.806 | 0.401 | 56.346 |

| SBL | 0.575 | 0.476 | 0.590 | 0.206 | 0.572 | 0.473 | 0.593 | 0.205 | 0.003 | |

| SINDy | 0.599 | 0.491 | 0.562 | 0.213 | 0.595 | 0.489 | 0.565 | 0.212 | 0.008 | |

| LSTM | 0.602 | 0.474 | 0.604 | 0.205 | 0.709 | 0.567 | 0.444 | 0.245 | 482.761 | |

| GRU | 0.683 | 0.553 | 0.509 | 0.239 | 0.666 | 0.537 | 0.508 | 0.232 | 337.221 | |

| ResNet | 0.585 | 0.471 | 0.532 | 0.204 | 0.529 | 0.420 | 0.646 | 0.182 | 38.537 | |

| Autoformer | 0.766 | 0.629 | 0.005 | 0.271 | 0.727 | 0.589 | -0.148 | 0.254 | 183.429 | |

| SIABF | 0.430 | 0.334 | 0.790 | 0.144 | 0.421 | 0.328 | 0.794 | 0.142 | 0.033 | |

| Data -set 3 | ARIMA | 0.999 | 0.747 | -16.372 | 123.700 | 1.134 | 0.822 | -39.582 | 257.555 | 176.488 |

| SBL | 0.901 | 0.822 | 0.070 | 64.558 | 0.898 | 0.819 | 0.036 | 64.522 | 0.003 | |

| SINDy | 1.207 | 1.124 | -10.855 | 84.089 | 1.202 | 1.120 | -10.858 | 83.714 | 0.008 | |

| LSTM | 0.638 | 0.447 | 0.541 | 46.816 | 0.610 | 0.426 | 0.416 | 80.708 | 1495.221 | |

| GRU | 0.540 | 0.388 | 0.328 | 50.072 | 0.595 | 0.435 | 0.240 | 60.308 | 1025.846 | |

| ResNet | 0.561 | 0.410 | 0.151 | 63.778 | 0.647 | 0.484 | 0.118 | 101.053 | 124.194 | |

| Autoformer | 1.065 | 0.909 | -3.273 | 174.858 | 1.147 | 0.979 | -3.112 | 144.069 | 141.836 | |

| SIABF | 0.336 | 0.240 | 0.863 | 41.269 | 0.345 | 0.250 | 0.855 | 49.225 | 0.032 | |

The performance comparison results is shown in Table. I. For each dataset, two types of prediction are considered: Complete and uncompleted training data for long-term prediction. For each type, total eight methods including the proposed SIABF are tested, and five indicators on accuracy and elapsed time for evaluation are used. From the results in Table. I, the following observations are found.

Firstly, SIABF achieves the consistent state-of-the-art results in both complete and incomplete training data. Compared to data-driven methods, SIABF gives 40 % RMSE improvement (0.4910.814) in water conservancy data, 26% improvement in temperature (0.4300.585), 38% improvement in fiance (0.3360.540). Overall, SIABF yields a 33 % average RMSE improvement among baseline data-driven methods.

Secondly, in all prediction methods, only R2 of SIABF is constantly greater than 0.5. In most methods, R2 is less than zero in long-term prediction. It clearly shows that most current methods can not accurately predict the trend of future data, that is, they cannot accurately predict the peak and valley values of the data. However, SIABF can accurately grasp long-term trend of the data, which can be attributed to two reasons: 1) SIABF can accurately calculate the potential periods underlying the data, although no prior knowledge of the data was known. 2) SIABF can sparsely select the potential prior periods to ensure that there is no over-fitting phenomenon in the training set.

Thirdly, SIABF saves a lot of training time compared with the data-driven methods. In this paper, although all data-driven methods are trained in the highly configured GPU, training time of each experiment is as long as several minutes. In contrast, SIABF can make long-term prediction within one second maintaining the prediction accuracy which is hundreds or thousands of times faster than the NN based methods.

Finally, SIABF is robust to incomplete and noisy data. In the second type of experiments, 5% of the training data are randomly deleted, and irregular noise is added to all the training data. However, it is obvious that SIABF is not affected by incomplete training data or noise. Almost all the indicators in Table. I change less than the baseline methods.

To sum up, SIABF is better than current methods in terms of precision, speed and robustness in the long-term prediction experiments of time series.

4.3 Interpretability

Another advantage of model based-methods is that they have a good interpretability compared with the NN based data-driven methods. Water conservancy dataset is adopted as an example to show the interpretability of SIABF.

4.3.1 Period implies prior information

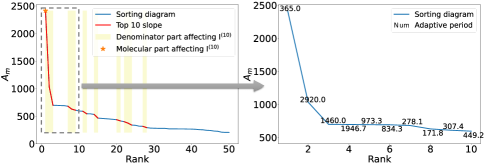

Unlike most model-based methods, e.g., [23, 24, 28], the possible adaptive basis functions are unknown for the datasets in our experiments. However, some interpretable information can be provided through the periodic prior method. The sorting diagram for the top ten ranks of period in water conservancy dataset is shown in Fig. 4 (right).

The periods most likely to exist in the data can be found through SIABF. Carefully checking these obtained prior periods, it is surprising to find that they are highly interpretable compared to neural networks. In the sorting diagram, the prior period corresponding to the top three ranks are 365, 2920, 1460, respectively, corresponding to the duration of one, eight and four years, respectively. This implies that water conservancy has periodic changes in one, four and eight years. Relevant professional research also confirms this observation [48]. Similarly, other cycle lengths can be divided by 16 years. The impact of these prior periods on water conservancy data can be analyzed as well by the observed amplitudes.

Through this example, it is clear that SIABF also provides some prior knowledge even if the potential functions underlying the data are unknown. It shows that SIABF can efficiently select the basis functions, and indicates that the parameters in SIABF are more interpretable than those in neural networks.

4.3.2 Quasi-periodic index work

Furthermore, the quasi-periodic index is calculated in the water conservancy dataset as an example. With , and the calculation process of quasi-periodic index is shown in Fig. 4 (left).

According to Eq. (3), in this dataset is . This shows that the time series formed by water conservancy data can be expressed with fewer prior periods, although it is not obvious intuitively (Fig. 5). In this case, the model-based method is basically better than most data-driven methods. This can also be verified in Table. I. In this circumstance, SIABF provides a considerable criterion to distinguish between model-based and data-driven methods.

5 Conclusion

In this paper, a novel model-based method, SIABF, for long-term prediction on time series with no prior knowledge is proposed. The adaptive period obtained by simply implementing DFT shows a highly-convincing format of underlying basis functions. The proposed quasi-periodic index, , also provides a high confidence in quantifying the prediction effects before adopting model-based white-box or data-driven black-box methods. When the quasi-periodic index is relatively large (typically ), SIABF has a great probability to obtain excellent prediction performance.

Moreover, SIABF provides an interpretable, efficient and effective identification and prediction framework with a simple implementing process. It is worth noting that this study indicates that underlying periodicity cannot be overlooked in any data, since it plays a crucial role in quantifying the physical mechanism of complex systems. In the future, more intrinsic features beyond periodicity will be taken into consideration in the framework, and SIABF will be extended to identifying and predicting networked systems.

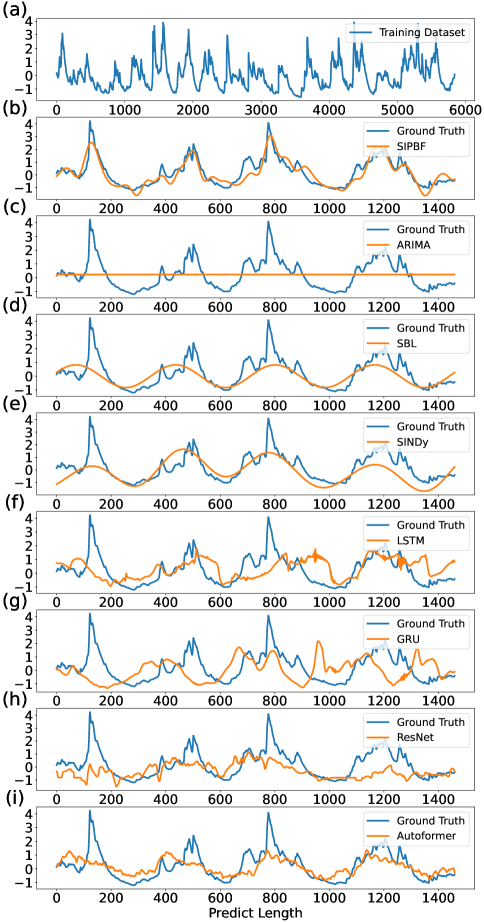

Appendix A Visualization and Code

Taking water conservancy data as an example, the visualization of long-term prediction of different models are shown in Fig. 5. Herein, the training data length is 16 years (data points = 365*16), while the prediction length is 4 years (data points = 365*4).

Moreover, our code is available at [46].

References

- [1] H. Wu, J. Xu, J. Wang, and M. Long, “Autoformer: Decomposition transformers with auto-correlation for long-term series forecasting,” Advances in Neural Information Processing Systems, vol. 34, pp. 22 419–22 430, 2021.

- [2] Z. Zhou, Y. Wang, X. Xie, L. Chen, and C. Zhu, “Foresee urban sparse traffic accidents: A spatiotemporal multi-granularity perspective,” IEEE Transactions on Knowledge and Data Engineering, 2020.

- [3] A. Borovykh, S. Bohte, and C. W. Oosterlee, “Conditional time series forecasting with convolutional neural networks,” arXiv preprint arXiv:1703.04691, 2017.

- [4] H. Zhou, S. Zhang, J. Peng, S. Zhang, J. Li, H. Xiong, and W. Zhang, “Informer: Beyond efficient transformer for long sequence time-series forecasting,” in Proceedings of the AAAI Conference on Artificial Intelligence, vol. 35, no. 12, 2021, pp. 11 106–11 115.

- [5] J. Deng, X. Chen, R. Jiang, X. Song, and I. W. Tsang, “A multi-view multi-task learning framework for multi-variate time series forecasting,” IEEE Transactions on Knowledge and Data Engineering, 2022.

- [6] X. Xu, L. Zhang, Q. Kong, C. Gui, and X. Zhang, “Enhanced-historical average for long-term prediction,” in 2022 2nd International Conference on Computer, Control and Robotics (ICCCR). IEEE, 2022, pp. 115–119.

- [7] D. E. Rumelhart, G. E. Hinton, and R. J. Williams, “Learning representations by back-propagating errors,” Nature, vol. 323, no. 6088, pp. 533–536, 1986.

- [8] R. H. Shumway and D. S. Stoffer, “Arima models,” in Time Series Analysis and Its Applications. Springer, 2017, pp. 75–163.

- [9] S. Hochreiter and J. Schmidhuber, “Long short-term memory,” Neural Computation, vol. 9, no. 8, pp. 1735–1780, 1997.

- [10] J. Chung, C. Gulcehre, K. Cho, and Y. Bengio, “Empirical evaluation of gated recurrent neural networks on sequence modeling,” arXiv preprint arXiv:1412.3555, 2014.

- [11] G. Lai, W.-C. Chang, Y. Yang, and H. Liu, “Modeling long and short-term temporal patterns with deep neural networks,” in The 41st international ACM SIGIR conference on research & development in information retrieval, 2018, pp. 95–104.

- [12] D. Salinas, V. Flunkert, J. Gasthaus, and T. Januschowski, “Deepar: probabilistic forecasting with autoregressive recurrent networks,” International Journal of Forecasting, vol. 36, no. 3, pp. 1181–1191, 2020.

- [13] B. Alhnaity, S. Kollias, G. Leontidis, S. Jiang, B. Schamp, and S. Pearson, “An autoencoder wavelet based deep neural network with attention mechanism for multi-step prediction of plant growth,” Information Sciences, vol. 560, pp. 35–50, 2021.

- [14] A. Vaswani, N. Shazeer, N. Parmar, J. Uszkoreit, L. Jones, A. N. Gomez, Ł. Kaiser, and I. Polosukhin, “Attention is all you need,” Advances in neural information processing systems, vol. 30, 2017.

- [15] N. Kitaev, Ł. Kaiser, and A. Levskaya, “Reformer: The efficient transformer,” arXiv preprint arXiv:2001.04451, 2020.

- [16] Y. Gu, J. Jin, and S. Mei, “ norm constraint lms algorithm for sparse system identification,” IEEE Signal Processing Letters, vol. 16, no. 9, pp. 774–777, 2009.

- [17] R. Wang, C. Zhang, J. Bian, Z. Wang, F. Nie, and X. Li, “Sparse and flexible projections for unsupervised feature selection,” IEEE Transactions on Knowledge and Data Engineering, 2022.

- [18] X. Ma, Y. Wang, X. Chu, L. Ma, W. Tang, J. Zhao, Y. Yuan, and G. Wang, “Patient health representation learning via correlational sparse prior of medical features,” IEEE Transactions on Knowledge and Data Engineering, 2022.

- [19] Y. Ye and S. Ji, “Sparse graph attention networks,” IEEE Transactions on Knowledge and Data Engineering, 2021.

- [20] Y. C. Pati, R. Rezaiifar, and P. S. Krishnaprasad, “Orthogonal matching pursuit: Recursive function approximation with applications to wavelet decomposition,” in Proceedings of 27th Asilomar conference on signals, systems and computers. IEEE, 1993, pp. 40–44.

- [21] R. Tibshirani, “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society. Series B, Statistical Methodology, vol. 73, no. 3, 2011.

- [22] M. E. Tipping, “Sparse bayesian learning and the relevance vector machine,” Journal of machine learning research, vol. 1, no. Jun, pp. 211–244, 2001.

- [23] S. L. Brunton, J. L. Proctor, and J. N. Kutz, “Discovering governing equations from data by sparse identification of nonlinear dynamical systems,” Proceedings of the national academy of sciences, vol. 113, no. 15, pp. 3932–3937, 2016.

- [24] Y. Yuan, X. Tang, W. Zhou, W. Pan, X. Li, H.-T. Zhang, H. Ding, and J. Goncalves, “Data driven discovery of cyber physical systems,” Nature communications, vol. 10, no. 1, pp. 1–9, 2019.

- [25] S. L. Brunton, J. L. Proctor, and J. N. Kutz, “Sparse identification of nonlinear dynamics with control (sindyc),” IFAC-PapersOnLine, vol. 49, no. 18, pp. 710–715, 2016.

- [26] N. M. Mangan, S. L. Brunton, J. L. Proctor, and J. N. Kutz, “Inferring biological networks by sparse identification of nonlinear dynamics,” IEEE Transactions on Molecular, Biological and Multi-Scale Communications, vol. 2, no. 1, pp. 52–63, 2016.

- [27] M. Quade, M. Abel, J. Nathan Kutz, and S. L. Brunton, “Sparse identification of nonlinear dynamics for rapid model recovery,” Chaos: An Interdisciplinary Journal of Nonlinear Science, vol. 28, no. 6, p. 063116, 2018.

- [28] T.-T. Gao and G. Yan, “Autonomous inference of complex network dynamics from incomplete and noisy data,” Nature Computational Science, vol. 2, no. 3, pp. 160–168, 2022.

- [29] D. Feller, “The role of databases in support of computational chemistry calculations,” Journal of computational chemistry, vol. 17, no. 13, pp. 1571–1586, 1996.

- [30] A. A. Bataineh and D. Kaur, “A comparative study of different curve fitting algorithms in artificial neural network using housing dataset,” in NAECON 2018 - IEEE National Aerospace and Electronics Conference, 2018, pp. 174–178.

- [31] M. G. Elfeky, W. G. Aref, and A. K. Elmagarmid, “Periodicity detection in time series databases,” IEEE Transactions on Knowledge and Data Engineering, vol. 17, no. 7, pp. 875–887, 2005.

- [32] T. Lu, Y.-F. Chen, B. Hechtman, T. Wang, and J. Anderson, “Large-scale discrete fourier transform on tpus,” IEEE Access, vol. 9, pp. 93 422–93 432, 2021.

- [33] Y. Wang, Time-frequency analysis of seismic signals. John Wiley & Sons, 2022.

- [34] R. Agarwal, L. Melnick, N. Frosst, X. Zhang, B. Lengerich, R. Caruana, and G. E. Hinton, “Neural additive models: Interpretable machine learning with neural nets,” Advances in Neural Information Processing Systems, vol. 34, pp. 4699–4711, 2021.

- [35] D. Pérez and Y. Quintana, “A survey on the weierstrass approximation theorem,” arXiv preprint math/0611038, 2006.

- [36] Y. Mao and F. Ding, “A novel parameter separation based identification algorithm for hammerstein systems,” Applied Mathematics Letters, vol. 60, pp. 21–27, 2016.

- [37] A. Hernandez, F. Ruiz, A. Desideri, C. Ionescu, S. Quoilin, V. Lemort, and R. De Keyser, “Nonlinear identification and control of organic rankine cycle systems using sparse polynomial models,” in 2016 IEEE Conference on Control Applications (CCA). IEEE, 2016, pp. 1012–1017.

- [38] C. Novara, “Sparse identification of nonlinear functions and parametric set membership optimality analysis,” IEEE Transactions on automatic control, vol. 57, no. 12, pp. 3236–3241, 2012.

- [39] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani, “Least angle regression,” The Annals of statistics, vol. 32, no. 2, pp. 407–499, 2004.

- [40] J. Jin, Y. Yuan, W. Pan, C. Tomlin, A. A. Webb, and J. Gonçalves, “Identification of nonlinear sparse networks using sparse bayesian learning,” in 2017 IEEE 56th Annual Conference on Decision and Control (CDC). IEEE, 2017, pp. 6481–6486.

- [41] W. R. Jacobs, T. Baldacchino, T. Dodd, and S. R. Anderson, “Sparse bayesian nonlinear system identification using variational inference,” IEEE Transactions on Automatic Control, vol. 63, no. 12, pp. 4172–4187, 2018.

- [42] A. Shahmansoori, “Sparse bayesian multi-task learning of time-varying massive mimo channels with dynamic filtering,” IEEE Wireless Communications Letters, vol. 9, no. 6, pp. 871–874, 2020.

- [43] Y. Wu and M. Zhu, “Attitude reconstruction from inertial measurement: mitigating runge effect for dynamic applications,” IEEE Transactions on Aerospace and Electronic Systems, 2021.

- [44] “Noaa national water model conus retrospective dataset,” https://registry.opendata.aws/nwm-archive/.

-

[45]

“Ncep-ncar reanalysis,” https://psl.noaa.gov/data/gridded/data

.ncep.reanalysis.html. - [46] https://github.com/cccs-data/SIABF-and-Finance-data.git.

- [47] K. He, X. Zhang, S. Ren, and J. Sun, “Deep residual learning for image recognition,” in Proceedings of the IEEE conference on computer vision and pattern recognition, 2016, pp. 770–778.

- [48] P. Hellard, M. Avalos, F. Guimaraes, J.-F. Toussaint, and D. B. Pyne, “Training-related risk of common illnesses in elite swimmers over a 4-yr period.” Medicine and science in sports and exercise, vol. 47, no. 4, pp. 698–707, 2015.