Robust Portfolio Selection

Under Recovery Average Value at Risk

Abstract

We study mean-risk optimal portfolio problems where risk is measured by Recovery Average Value at Risk, a prominent example in the class of recovery risk measures. We establish existence results in the situation where the joint distribution of portfolio assets is known as well as in the situation where it is uncertain and only assumed to belong to a set of mixtures of benchmark distributions (mixture uncertainty) or to a cloud around a benchmark distribution (box uncertainty). The comparison with the classical Average Value at Risk shows that portfolio selection under its recovery version enables financial institutions to exert better control on the recovery on liabilities while still allowing for tractable computations.

Keywords: Robust portfolio management; risk measures; recovery average at risk; efficient frontier; mean-risk optimal portfolios.

1 Introduction

Portfolio selection is one of the central topics in mathematical finance and has been extensively studied in the literature. Since the pioneering publications by \citeasnounMarkowitz52, \citeasnounsharpe1963simplified, \citeasnounbudgets1965valuation, much attention has been devoted to optimal portfolio problems in a mean-risk framework, where the objective is to study portfolios of financial assets that maximize expected returns subject to a given risk control. As in every optimization problem, the key questions from a theoretical perspective are those about existence, uniqueness, stability, and explicit identification of optimal portfolios. This, of course, highly depends on the chosen risk measure as well as on the assumptions on the (joint) distribution of the various assets. At the beginning, the literature has almost exclusively used the variance of the aggregated portfolio as the underlying measure of risk. In more recent years, especially after the publication of \citeasnounADEH99, there has been growing interest in revisiting mean-risk portfolio problems replacing the variance with risk measures that were deemed to capture risk in a more appropriate form, e.g., by focusing on the tail distribution of aggregated portfolios only. The bulk of the literature has focused on Value at Risk (V@R) and Average Value at Risk (AV@R) and on their comparison; see, e.g., \citeasnounRU00, \citeasnounbasak2001value, \citeasnouncampbell2001optimal, \citeasnounfrey2002var, \citeasnounRU02, \citeasnounyiu2004optimal, \citeasnounyamai2005value, \citeasnounleippold2006equilibrium, \citeasnounciliberti2007feasibility, \citeasnoundoi:10.1287/opre.1070.0433, \citeasnounpirvu09. \citeasnounGUNDEL20081126 study risk constraints in terms of utility-based shortfall risk. While most of the initial literature worked under the basic assumption that the joint distribution of portfolio assets is known, the subsequent literature has expanded the scope of research to include situations where there is uncertainty about the joint dependence across assets. The corresponding robust optimal portfolio problems under dependence uncertainty have been studied, e.g., in \citeasnounGUNDEL20071663, \citeasnounquaranta2008robust and \citeasnounZhuFu09.

The goal of this note is to investigate optimal portfolio problems in a mean-risk framework where risk is measured by Recovery Average Value at Risk (RecAV@R). This is a prominent example of a recovery risk measure, a concept that has been recently introduced in \citeasnounMWW23. As argued there, recovery risk measures are designed to complement standard risk measures used in solvency regulation by offering portfolio managers the ability to exert a tighter control on the recovery of liabilities. In this sense, recovery risk measures have natural applications to mean-risk portfolio problems in an asset-liability management setting, where the risk constraint plays, for example, the role of an external regulatory constraint that can be interpreted as a solvency capital requirement. In the case of AV@R, one can only ensure solvency on average in the worst, say, (as in the Swiss Solvency Test) or (as in Basel III) of scenarios, but this per se does not provide any information about the ability to cover any pre-specified fraction of liabilities. However, it clearly matters to liability holders, and regulators on their behalf, if, say, or only of liabilities is recovered in the case of insolvency. A recovery risk measure like RecAV@R can be employed to this effect. By definition, RecAV@R ensures that assets are sufficient to cover on average any pre-specified fraction of liabilities in the worst of scenarios. The function can be chosen to tailor the relevant size of the tail distribution depending on the size of liabilities to be recovered. In particular, it is reasonable to assume that is increasing and coincides with a regulatory threshold like (as in the Swiss Solvency Test) or (as in Basel III) to make sure a priori that RecAV@R is more stringent than the AV@R used in insurance or banking regulation.

This note is organized as follows. In Section 2 we briefly review the definition and the main properties of RecAV@R. In Section 3 we focus on optimal portfolio problems under RecAV@R both without and with dependence uncertainty. The main contribution is to show, by means of suitable minimax theorems, that optimal portfolios can be determined by solving appropriate linear programming problems that are both conceptually and computationally akin to the problems studied by \citeasnounRU00, \citeasnounRU02, and \citeasnounZhuFu09 in the setting of mean- portfolio selection. In Section 4 we apply our results to study optimal portfolios in two concrete case studies. The first case study shows that there can be a marked difference between optimal portfolios under and . More specifically, in the presence of a risk-free and a risky asset, there are realistic situations where it is optimal under to fully invest in the risky asset whereas the optimal holding in the risky asset is capped if is used to measure risk. In the second case study we focus on the more computational aspects and show that, in the presence of two risky assets whose returns follow standard distributions encountered in applications, the determination of robust efficient frontiers under is feasible and computationally similar to the one under .

2 Recovery Average Value at Risk

In this section we recall the definition and the basic properties of the risk measure Recovery Average Value at Risk () introduced in \citeasnounMWW23, to which we refer for the relevant proofs and for additional details. In the next sections we will take up the study of mean-risk portfolio problems where risk is quantified by .

Let be a probability space and denote by the vector space of Borel measurable functions (modulo -almost sure equality). Throughout the paper we assume that positive values of represent a profit or a positive balance whereas negative values of represent a loss or a negative balance. The Value at Risk () of at level is defined by

The Average Value at Risk () of at level is defined by

Definition 1.

Let be an increasing function. The Recovery Average Value at Risk () of with level function is defined by

Clearly, is an extension of . Indeed, by taking a constant function , say for some , one easily verifies that for every and for every positive

The definition of is motivated by the following application. Consider a financial firm with stylized balance sheet at a generic time given by

| Assets | Liabilities |

|---|---|

The quantity represents the net asset value of the firm and can be either positive or negative depending on whether the asset value is larger than the liability value or not. In the typical setting of a one-year horizon there are two reference dates, (today) and (end of the year). In a risk-sensitive solvency framework, the firm is adequately capitalized if its available capital is larger than a suitable solvency capital requirement that depends on the size of and therefore captures the inherent risk in the evolution of the balance sheet. In practice, solvency capital requirements are determined by applying a suitable risk measure like or to the variation444In practice, instead of the expectation of , typically discounted, is frequently used, see \citeasnounHKW20 for a discussion. in the net asset value . The corresponding solvency test therefore takes the form

The risk measure can be used to define a solvency test of this type. Indeed, if the random variables and in Definition 1 are interpreted, respectively, as the net asset value and liabilities in the firm’s balance sheet, then we can design the solvency test

| (1) |

The financial interpretation is clear once we observe that (1) is equivalent to requiring that

In words, the firm is adequately capitalized with respect to if, for every fraction , a firm with assets and liabilities is solvent on average in the worst scenarios (under ). In particular, the firm must be solvent on average in the worst scenarios (under ), showing that (1) is more stringent than a standard test at level . It therefore comes as no surprise that, in the special case where the level function is constant, say for some , the test (1) boils down to a standard test

| (2) |

In this case the firm is adequately capitalized if it is solvent on average in the worst scenarios (under ). The flexibility added by (1) to the standard test (2) is that one can control recovery on liabilities, which is not permitted by standard solvency capital requirements based on . This control is made possible by prescribing, in principle for each recovery level , a different tail threshold . In this sense, it is natural to assume, as in Definition 1, that is an increasing function: When we target a higher recovery on liabilities, we require solvency over a larger portion of the tail of . It should be noted that (1) also allows to control the probability of recovering the pre-specified fractions of liabilities. This is because, for any given level, is larger than and therefore

Translated in terms of recovery probabilities, we obtain as claimed

The next proposition records an equivalent formulation of when the level function is piecewise constant. In this case, is especially tractable and it is precisely this type of level functions that will be later used in our numerical studies.

Proposition 2.

For let and . Define a function by

For all and

We conclude this section by stating some basic properties of , which follow at once from well-known properties of .

Proposition 3.

Let be increasing. The following properties hold:

-

(i)

Cash-invariance in the first component: For all and

-

(ii)

Monotonicity: For all such that and

-

(iii)

Subadditivity: For all

-

(iv)

Positive homogeneity: For all and

3 Optimal portfolio selection under

Risk measures are an important instrument to limit downside risk in portfolio optimization problems. This idea is related to the classical portfolio problem studied in \citeasnounMarkowitz52, where the objective was to select portfolios of reference financial assets with the goal of maximizing the expected return of the portfolio without exceeding a pre-specified level of standard deviation. In this sense, optimal portfolios represent the best tradeoff between risk and return. A similar problem can be reformulated in the language of asset-liability management for a financial institution, in which case the risk constraint is interpreted as a regulatory constraint. Standard deviation is, however, not a good risk measure in this type of applications because it fails to disentangle upside and downside risk. For this reason, the subsequent literature has investigated the mean-risk problem under different choices of tail risk measures, including and ; see, e.g., \citeasnounRU00, \citeasnounbasak2001value, \citeasnouncampbell2001optimal, \citeasnounRU02, \citeasnounZhuFu09. Special attention has been devoted to because the resulting problem becomes convex and allows to exploit the rich methodology of convex optimization to characterize optimal portfolios.

In this section, we study the mean-risk problem for a financial institution that is subject to solvency capital requirements expressed in terms of the convex recovery risk measure . Our goal is to characterize the corresponding optimal portfolios. This task is, at first sight, more challenging than under because its recovery counterpart is defined as a supremum of standard ’s, making the mean-risk problem mathematically more involved. With the help of a suitable minimax theorem, which we establish for this purpose, we can nevertheless reduce the problem and show that standard techniques from linear programming can be exploited to identify optimal portfolios.

We consider a financial institution with total budget at time . The company can invest in financial assets whose prices at dates are described by and whose relative returns are denoted by so that . We assume that . For every the company invests a fraction of its total budget into asset so that . For later convenience we define

We also set and . The total asset value at time is thus equal to

In addition, we suppose that the company’s liabilities at time amount to a random fraction of the initial budget, i.e., the liabilities are equal to . We assume that . The net asset value of the company equals

The expected net asset value is therefore given by

The mean-risk problem can equivalently be stated either as the maximization of expected returns under a risk constraint or as the minimization of risk for a target expected return. We focus on the latter formulation. For a given level function and for given , we are thus interested in the following problem:

| (3) | ||||

It is convenient to formulate the constraint for the expected return instead of the expected asset value. Using the properties of recorded in Proposition 3 and filtering out all constant terms, we can equivalently focus on the following problem for given :

where the set of admissible portfolios is defined by

We focus on the special case of piecewise-constant level functions introduced in Proposition 2. In this case, is a maximum of finitely many ’s and the optimal portfolio problem can be equivalently written for given as:

As a last step, we exploit the representation of established in \citeasnounRU00 and \citeasnounRU02 to conveniently reformulate the problem above. To this effect, for and we can write

where the auxiliary function is defined by

As a consequence, our original optimal portfolio problem can be equivalently reformulated into the following minimax problem for given :

| (4) |

At first sight, this optimization problem seems difficult to cope with because of the entanglement between minimization and maximization. The following theorem shows that, by appropriately increasing the dimensionality of the internal minimization problem, we can interchange the order of minimum and maximum, thereby reducing the problem of finding optimal portfolios to a tractable linear programming problem.

Theorem 1.

For every the following minimax equality holds:

In particular, problem (4) can be equivalently written as

Proof.

It is known from \citeasnounRU00 that, for each , the convex function attains its minimum on the (nonempty) compact interval , where and are the lower, respectively upper, -quantiles of . The desired minimax equality therefore follows at once from Theorem 4 in the appendix. ∎

In view of Theorem 1, the problem of determining the portfolios with miminal risk for a fixed expected target return can be equivalently expressed as

The evaluation of the functions ’s involves the calculation of an expected value. In typical real-world applications, this is performed through Monte Carlo simulation. If are independent simulations of the pair , we obtain the associated problem

The original problem can eventually be formulated as a tractable linear program of the form

4 Robust optimal portfolio selection under

In this section we study the optimal portfolio problem under uncertainty about the underlying probabilistic model. We will show that, in spite of the added complexity, the problem can still be reduced to a tractable linear programming problem.

Throughout the section we fix a measurable space and denote by the vector space of Borel measurable functions . The set of all probability measures on is denoted by . Throughout we use a superscript to make explicit the dependence of our risk measures on the chosen probability measure in .

Definition 4.

Let be an increasing function and . The Worst-Case Recovery Average Value at Risk of with level function and uncertainty set is defined by

For a given level function and a given uncertainty set , and for given , we are interested in the following robust version of problem (3):

| (5) | ||||

In the sequel we specify our analysis to two ways to define the uncertainty set , which have been applied in \citeasnounZhuFu09 to the study of robust mean-risk portfolio problems where the reference risk measure is .

4.1 Mixture uncertainty

In a first step, we assume the existence of a finite number of benchmark probability measures, denoted by , and consider all possible convex combinations mixing them. This corresponds to the uncertainty set

Consider a piecewise constant level function as in Proposition 2. For and and for define the auxiliary function by

Repeating the reasoning in Section 3 we can recast the robust portfolio problem (5) with uncertainty set in the following equivalent form for given :

| (6) |

where the set of admissible portfolios is defined by

The next theorem shows that the maxima and minima appearing in problem (6) can be reordered and coupled, thereby reducing the problem to a tractable linear programming problem.

Theorem 2.

For every the following minimax equality holds:

In particular, problem (6) can be equivalently written as

Proof.

By \citeasnounRU00, for all and the convex function attains its minimum on the (nonempty) compact interval , where and are the lower, respectively upper, -quantiles under of the random variable . For every and for every choice of the function must therefore attain its minimum in the same compact interval, namely

For every the sets and are compact and convex and the function is linear in and convex in . As a consequence, the minimax theorem in \citeasnounfan1953minimax delivers for every

Since we can always interchange two consecutive maxima, we infer that

As for every the convex function attains its minimum on , a direct application of Theorem 4 in the appendix yields the desired minimax equality. ∎

In the spirit of Section 3, one can use Theorem 2 to conveniently reformulate the portfolio problem under mixture uncertainty as

By approximating the expected value in the functions ’s using Monte Carlo simulation as before, the problem can again be written as a tractable linear programming problem.

4.2 Box uncertainty

In a second step, we fix a benchmark probability measure under which the random vector is discrete and takes the values . To simplify the notation, we set for every

We consider all possible probability measures under which remains discrete and that are obtained by a slight perturbation of the reference probability measure . The set of perturbation parameters is defined for given such that and by

For every we consider a probability measure such that for

The corresponding uncertainty set is given by

Consider a piecewise constant level function as in Proposition 2. For and and for define the auxiliary function by

Repeating the reasoning in Section 3 we can recast the robust portfolio problem (5) with uncertainty set in the following equivalent form for given :

| (7) |

where the set of admissible portfolios is defined by

Once again, the maxima and minima appearing in problem (7) can be reordered to yield a tractable linear programming problem. This is recorded in the next result.

Theorem 3.

For every the following minimax equality holds:

In particular, problem (7) can be equivalently written as

Proof.

We mimic the argument in the proof of Theorem 2. By \citeasnounRU00, for all and the convex function attains its minimum on the (nonempty) compact interval , where and are the lower, respectively upper, -quantiles under of the discrete random variable . For every we can thus define

Clearly, for every the sets and are compact and convex and the function is linear in and convex in . As a consequence, the minimax theorem in \citeasnounfan1953minimax delivers for every

Since we can always interchange two consecutive maxima, we infer that

As for every the convex function attains its minimum on , a direct application of Theorem 4 in the appendix yields the desired minimax equality. ∎

Similarly to the case of mixture uncertainty, Theorem 3 can be used to conveniently reformulate the original portfolio problem as

Once again, by approximating the expected value in the functions ’s using Monte Carlo simulation, the problem can be written as a tractable linear programming problem. The procedure is described in detail for the case where in the case study in Section 5.2.

5 Numerical illustrations

This final section is devoted to an illustration of mean-risk portfolio selection under in the context of two cases studies. In the first case study we compare optimal portfolios under and and document that already the choice of a simple level function may lead to a drastic difference in the composition of optimal portfolios. More specifically, in the presence of a risk-free and a risky asset, there are realistic situations where it is optimal to fully invest in the risky asset under whereas the optimal holding in the risky asset is capped if is used to measure risk. In the second case study we focus on the more computational aspects and show that, in the presence of two risky assets whose returns follow standard distributions encountered in applications, the determination of robust efficient frontiers under is feasible and computationally similar to the one under . To achieve this, we exploit the minimax theorems established in the previous section and combine them with standard Monte Carlo simulation.

5.1 Case study 1: Optimal portfolio without dependence uncertainty

We consider a financial institution with total budget at the initial date. The management can invest in two assets with one-period relative returns given by

At the terminal date the institution is exposed to deterministic liabilities amounting to for given . We denote by the fraction of total budget that is invested in the risky asset. The corresponding end-of-period net asset value is therefore equal to

Set and for define the set of admissible holdings in the risky asset by

Since , we readily see that . In a first step we focus on the problem

| (8) |

Using the properties of we can equivalently write

This shows that the composition of the optimal portfolio will be driven by the sign of . A direct computation shows that

As a result, problem (8) admits a unique optimal solution given by . In words, the optimal portfolio under corresponds to investing the entire available budget into the risky asset. We turn to investigating how the optimal portfolio changes if is replaced by . To this effect, take and and consider a simple level function of the form

We modify problem (8) by replacing with , thereby obtaining the new problem

| (9) |

In view of Proposition 2, we can equivalently write

Using the properties of we obtain the more explicit problem

The optimal portfolio is thus determined by the sign of and . By design, we always have . Moreover, recall that . A direct computation shows that

In particular, we have

As a consequence, we obtain the following picture about optimal portfolios under as a function of the parameters and that determine the level function . On the one hand, if , then problem (9) admits a unique optimal solution given by . In this case, there is no difference between and and the optimal portfolio in both cases corresponds to investing the whole budget in the risky asset. On the other hand, if , then problem (9) admits the unique optimal solution

In particular, we observe that if and only if

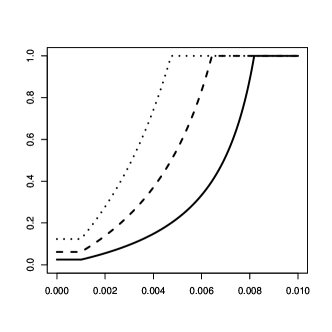

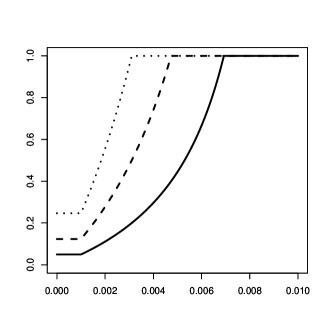

As a result, the optimal proportion of the budget invested in the risky asset depends on the relative size of the recovery parameters and as well as of the liability parameter . Everything else remaining equal, the optimal portfolio weight for the risky asset is increasing in and while it is decreasing in , as one would expect. In Figure 1 (top) we display the optimal percentage of the initial budget invested in the risky asset as a function of for different choices of and . More precisely, we consider the situation where management targets a recovery of , , or of liabilities and where the size of liabilities amounts to or of the entire budget. In each of these situations there are realistic choices of under which, differently from the case, it is not optimal to fully invest in the risky asset. In fact, there are situations where a considerable size of the budget is optimally invested in the risk-free asset.

We complement the previous analysis by assessing the ability of and to cover a pre-specified portion of liabilities when budget is invested optimally and capital is adjusted to respect regulatory requirements. To this effect, we denote the underlying probability by and compute for difference choices of the recovery probability

where is the optimal percentage of the budget invested in the risky asset and

We know that under . In this case, one can easily show that for every

If we work under , we obtain for every

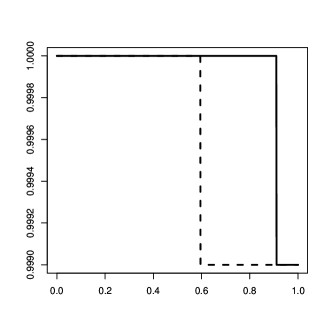

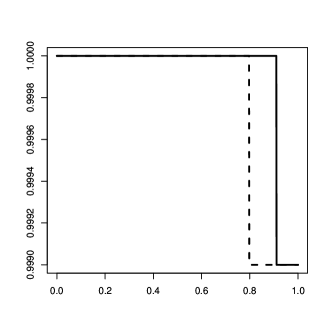

In Figure 1 (bottom) we plot recovery probabilities under and for recovery parameters and . By definition of , the recovery probability is at least in both cases. If , then the optimal portfolio weight for the risky asset is . In this case, guarantees full recovery up to of liabilities whereas performs much better by ensuring full recovery up to of liabilities. The gap is narrower but still clear when , in which case the optimal portfolio weight for the risky asset is . In this case, guarantees full recovery up to of liabilities while continues to ensure full recovery up to of liabilities.

5.2 Case study 2: Optimal portfolio with dependence uncertainty

We consider a financial institution with total budget at the initial date. The management can invest in two assets with one-period relative returns and with the following characteristics:

-

•

has a normal distribution with mean and standard deviation .

-

•

has a Student distribution with mean , scale , and degrees of freedom.

-

•

and have a Student copula with linear correlation and degrees of freedom.

The second asset is clearly riskier as it has infinite variance. At the terminal date the institution is exposed to deterministic liabilities amounting to for given . We denote by the fraction of total budget that is invested in the second asset. The corresponding end-of-period net asset value is therefore equal to

We study robust portfolio optimization under box uncertainty using the notation introduced in Section 4.2. As a first step, we apply Monte Carlo simulation to generate a sample of realizations of the random vector , which are denoted by for , and fix a benchmark probability measure under which is discrete and satisfies

For a given we set and and consider the corresponding perturbation set . In particular, observe that for every we have

The degree of box uncertainty therefore increases with the parameter . In particular, the case corresponds to no box uncertainty. As in the previous case study, set and for and consider the level function given by

For given define the set of admissible holdings in the second asset by

We focus on the robust optimization problem

| (10) |

Filtering out the constant and using the explicit shape of we equivalently obtain

To determine the efficient frontier we rely on the minimax identity established in Theorem 3 and adapt the approach of \citeasnounZhuFu09, which was applied to mean-risk problems under . First, it follows immediately from Theorem 3 that problem (10) is equivalent to

We now follow \citeasnounZhuFu09, to which we refer for the necessary details, and use the explicit form of (remember that and for some ) to rewrite the inner optimizations over as convenient linear programs. With respect to the maximization over , it suffices to observe that, by duality, for any given we have

Similarly, with respect to the minimization over , for fixed we obtain by duality that

where the dual domain is defined by

In addition, we have where

As a consequence, problem (10) is equivalent to the tractable linear program

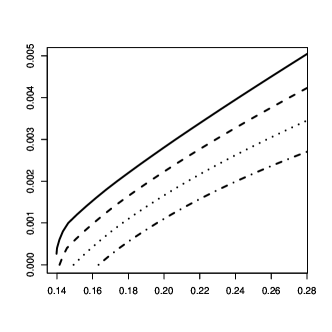

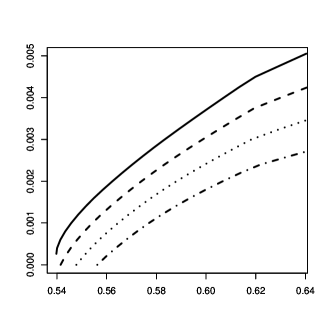

A standard dual simplex method can be employed to find the optimal value of this linear program as a function of a target expected relative return . In Figure 2 we plot the corresponding efficient frontier, i.e., the set of points , for a given range of expected relative returns. We focus on the two situations where liabilities amount to , respectively , of the initial budget. As is intuitive, in the latter case the same level of expected relative returns is achieved at the cost of higher risk. A direct inspection of the plots reveal that, for the chosen range of target returns, risk is to times higher when liabilities have a larger size. However, the qualitative impact of dependence uncertainty, in the form of box uncertainty, is the same in both situations. If the degree of uncertainty increases, the same level of expected relative returns is achieved at the cost of higher risk. Interestingly enough, the impact of dependence uncertainty on risk is more pronounced when the size of liabilities is smaller.

Appendix A A minimax theorem

In this appendix we record a special minimax theorem that we apply repeatedly in the paper. For we denote by the -dimensional simplex, i.e., the set of vectors in with nonnegative components summing up to .

Theorem 4.

Let be convex functions attaining their minimum on (nonempty) compact intervals . Then,

| (11) |

Proof.

Set . For every we can write

As and are compact and convex and the function is linear in and convex in , we can apply the classical minimax theorem in \citeasnounfan1953minimax to infer that

This delivers the desired minimax equality. ∎

Remark 5.

The outer minimum in the minimax equality (11) cannot be taken over in general. To see this, consider the convex functions defined by

Note that and attain their minimum on and , respectively. However,

References

- [1] \harvarditem[Artzner et al.]Artzner, Delbaen, Eber \harvardand Heath1999ADEH99 Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber \harvardand David Heath \harvardyearleft1999\harvardyearright, ‘Coherent measures of risk’, Mathematical Finance 9(3), 203–228.

- [2] \harvarditemBasak \harvardand Shapiro2001basak2001value Basak, Suleyman \harvardand Alexander Shapiro \harvardyearleft2001\harvardyearright, ‘Value-at-risk-based risk management: optimal policies and asset prices’, The review of financial studies 14(2), 371–405.

- [3] \harvarditem[Campbell et al.]Campbell, Huisman \harvardand Koedijk2001campbell2001optimal Campbell, Rachel, Ronald Huisman \harvardand Kees Koedijk \harvardyearleft2001\harvardyearright, ‘Optimal portfolio selection in a value-at-risk framework’, Journal of Banking & Finance 25(9), 1789–1804.

- [4] \harvarditem[Ciliberti et al.]Ciliberti, Kondor \harvardand Mézard2007ciliberti2007feasibility Ciliberti, Stefano, Imre Kondor \harvardand Marc Mézard \harvardyearleft2007\harvardyearright, ‘On the feasibility of portfolio optimization under expected shortfall’, Quantitative Finance 7(4), 389–396.

- [5] \harvarditem[Cuoco et al.]Cuoco, He \harvardand Isaenko2008doi:10.1287/opre.1070.0433 Cuoco, Domenico, Hua He \harvardand Sergei Isaenko \harvardyearleft2008\harvardyearright, ‘Optimal dynamic trading strategies with risk limits’, Operations Research 56(2), 358–368.

- [6] \harvarditemFan1953fan1953minimax Fan, Ky \harvardyearleft1953\harvardyearright, ‘Minimax theorems’, Proceedings of the National Academy of Sciences of the United States of America 39(1), 42.

- [7] \harvarditemFrey \harvardand McNeil2002frey2002var Frey, Rüdiger \harvardand Alexander J McNeil \harvardyearleft2002\harvardyearright, ‘Var and expected shortfall in portfolios of dependent credit risks: conceptual and practical insights’, Journal of banking & finance 26(7), 1317–1334.

- [8] \harvarditemGundel \harvardand Weber2007GUNDEL20071663 Gundel, Anne \harvardand Stefan Weber \harvardyearleft2007\harvardyearright, ‘Robust utility maximization with limited downside risk in incomplete markets’, Stochastic Processes and their Applications 117(11), 1663–1688.

- [9] \harvarditemGundel \harvardand Weber2008GUNDEL20081126 Gundel, Anne \harvardand Stefan Weber \harvardyearleft2008\harvardyearright, ‘Utility maximization under a shortfall risk constraint’, Journal of Mathematical Economics 44(11), 1126–1151.

- [10] \harvarditem[Hamm et al.]Hamm, Knispel \harvardand Weber2020HKW20 Hamm, Anna-Maria, Thomas Knispel \harvardand Stefan Weber \harvardyearleft2020\harvardyearright, ‘Optimal risk sharing in insurance networks’, European Actuarial Journal 10(1), 203–234.

- [11] \harvarditem[Leippold et al.]Leippold, Trojani \harvardand Vanini2006leippold2006equilibrium Leippold, Markus, Fabio Trojani \harvardand Paolo Vanini \harvardyearleft2006\harvardyearright, ‘Equilibrium impact of value-at-risk regulation’, Journal of Economic Dynamics and Control 30(8), 1277–1313.

- [12] \harvarditemLintner1965budgets1965valuation Lintner, John \harvardyearleft1965\harvardyearright, ‘The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets’, The Review of Economics and Statistics 47(1), 13–37.

- [13] \harvarditemMarkowitz1952Markowitz52 Markowitz, Harry Max \harvardyearleft1952\harvardyearright, ‘Portfolio selection’, The Journal of Finance 7(1), 77–91.

- [14] \harvarditem[Munari et al.]Munari, Weber \harvardand Wilhelmy2023MWW23 Munari, Cosimo, Stefan Weber \harvardand Lutz Wilhelmy \harvardyearleft2023\harvardyearright, ‘Capital requirements and claims recovery: A new perspective on solvency regulation’, Journal of Risk and Insurance (to appear) .

- [15] \harvarditemPirvu \harvardand Zitkovic2009pirvu09 Pirvu, Traian A. \harvardand Gordan Zitkovic \harvardyearleft2009\harvardyearright, ‘Maximizing the growth rate under risk constraints’, Mathematical Finance 19(3), 423–455.

- [16] \harvarditemQuaranta \harvardand Zaffaroni2008quaranta2008robust Quaranta, Anna Grazia \harvardand Alberto Zaffaroni \harvardyearleft2008\harvardyearright, ‘Robust optimization of conditional value at risk and portfolio selection’, Journal of Banking & Finance 32(10), 2046–2056.

- [17] \harvarditemRockafellar \harvardand Uryasev2000RU00 Rockafellar, R. Tyrrell \harvardand Stanislav Uryasev \harvardyearleft2000\harvardyearright, ‘Optimization of conditional value-at-risk’, Journal of Risk 2(3), 21–41.

- [18] \harvarditemRockafellar \harvardand Uryasev2002RU02 Rockafellar, R. Tyrrell \harvardand Stanislav Uryasev \harvardyearleft2002\harvardyearright, ‘Conditional value-at-risk for general loss distributions’, Journal of Banking Finance 26, 1443–1471.

- [19] \harvarditemSharpe1963sharpe1963simplified Sharpe, William F \harvardyearleft1963\harvardyearright, ‘A simplified model for portfolio analysis’, Management science 9(2), 277–293.

- [20] \harvarditemYamai \harvardand Yoshiba2005yamai2005value Yamai, Yasuhiro \harvardand Toshinao Yoshiba \harvardyearleft2005\harvardyearright, ‘Value-at-risk versus expected shortfall: A practical perspective’, Journal of Banking & Finance 29(4), 997–1015.

- [21] \harvarditemYiu2004yiu2004optimal Yiu, Ka-Fai Cedric \harvardyearleft2004\harvardyearright, ‘Optimal portfolios under a value-at-risk constraint’, Journal of Economic Dynamics and Control 28(7), 1317–1334.

- [22] \harvarditemZhu \harvardand Fukushima2009ZhuFu09 Zhu, Shushang \harvardand Masao Fukushima \harvardyearleft2009\harvardyearright, ‘Worst-case conditional value-at-risk with application to robust portfolio management’, Operations Research 57(5), 1155–1168.

- [23]