Quantifying Dimensional Change

in Stochastic Portfolio Theory

Abstract

In this paper, we develop the theory of functional generation of portfolios in an equity market with changing dimension. By introducing dimensional jumps in the market, as well as jumps in stock capitalization between the dimensional jumps, we construct different types of self-financing stock portfolios (additive, multiplicative, and rank-based) in a very general setting. Our study explains how a dimensional change caused by a listing or delisting event of a stock, and unexpected shocks in the market, affect portfolio return. We also provide empirical analyses of some classical portfolios, quantifying the impact of dimensional change in portfolio performance relative to the market.

MSC 2020 subject classifications: Primary 60G48, 60H05, 91G10.

Keywords and phrases: functional generation, piecewise semimartingale, self-financing portfolio, stochastic dimension, stochastic portfolio theory.

1 Introduction

In this paper, we study an equity market model of stochastic dimension. This is a continuation of our previous work (Bayraktar \BOthers., \APACyear2022), where a complete version of the fundamental theorem of asset pricing is developed in a stock market with a changing number of companies, and access to a money market. On the other hand, this paper focuses solely on the stock market of fluctuating dimension, without access to the money market, and develops the theory of functional generation of portfolios which only invest in stocks.

The theory of functional generation of portfolios, introduced by R. Fernholz (\APACyear1999) over years ago, is the central part of the stochastic portfolio theory (E\BPBIR. Fernholz, \APACyear2002) (see also R. Fernholz \BBA Karatzas (\APACyear2009) for a brief overview). It explains how to construct a class of self-financing portfolios from a function depending on the companies’ relative capitalization. It also derives an explicit decomposition of their log relative return with respect to the entire stock market, as the sum of the log of generating function and a drift process. Such decomposition enables us to find conditions on the portfolio-generating function, such that the drift process is increasing in time and the generated portfolio outperforms the market over the long run. More recently, Karatzas \BBA Ruf (\APACyear2017) introduced a new construction of portfolios which they call ‘additive’ generation, whereas Fernholz’s original construction is called ‘multiplicative’. This new method provides a simpler formulation of conditions for portfolios to outperform the market over appropriate time horizons.

All of these previous works assume a fixed number of stocks in the market. Our primary purpose is to remove this assumption on the market dimension when constructing self-financing portfolios. Concretely, we shall use a piecewise semimartingale of stochastic dimension, introduced by Strong (\APACyear2014), to model the capitalization dynamics of stocks; the moments of dimensional changes are given by a sequence of stopping times, and the stock capitalization process is assumed to be a semimartingale of some fixed dimension, during each ‘epoch’ of the market between those dimensional jumps. Using this concept, our equity market model incorporates all types of listing/delisting events such as IPO, splits, mergers, bankruptcies, etc.

The main difficulty is then to make the (functionally-generated) portfolios self-financing whenever the market undergoes a dimensional change. In order to handle this, we shall normalize our portfolio-generating function at the starting moment of each epoch by an -measurable random variable, and construct portfolios in a recursive manner for each epoch of the market. Now that we have two different methods of generating portfolios, both additive and multiplicative normalizations will be applied accordingly. The introduction of such normalizations yields an extra correction term in the decomposition of the relative return of the generated portfolios with respect to the market, and this correction term quantifies precisely the impact of dimensional change in the performance of the portfolios relative to the market.

The correction term arises at each dimensional change, when a new stock enters or an old stock exits the market, due to two factors; a jump in total market capitalization and a jump in the portfolio-generating function. The former is an uncontrollable factor, whereas the latter can be controlled by choosing an appropriate generating function. For multiplicatively generated portfolios, these two factors are nicely separated so that we can quantify them individually in portfolio returns with respect to the market. However, in the case of additively generated portfolios, there is no such simple uncoupling between these two correction factors.

Moreover, the aforementioned portfolio returns measure the wealth of generated portfolios with respect to the total market capitalization (total market index fund); at the time of dimensional change, the latter quantity jumps, whereas the wealth of the portfolio remains the same, as it is designed to be self-financing. Thus, we introduce a new notion of a ‘self-financing’ market portfolio, which follows the total market index fund as a buy-and-hold strategy between dimensional jumps, but remains self-financed at times of dimensional change, as an alternative baseline for comparing the wealth of functionally-generated portfolios. Especially for multiplicatively generated portfolios, the relative wealth with respect to the new baseline only contains the second factor of the correction term. Since this second factor will be shown to offset exactly the jump in the portfolio-generating function at moments of dimensional change, we recover Fernholz’s original decomposition of log relative wealth, as the sum of the log of generating function and a drift term accumulated between two consecutive dimensional changes, with respect to the self-financing market portfolio.

The second contribution of this paper is that our model relaxes the continuity assumption on the capitalization process between dimensional jumps, as it is modeled by an RCLL semimartingale of some fixed dimension between dimensional jumps. Allowing such left-discontinuities can help explain not only how certain unexpected shocks from the market between dimensional jumps affect the portfolios, but also how a delisting event of a stock influences the portfolio returns (see Remark 2.2 for more details).

Therefore, this equity market model using piecewise RCLL semimartingales (see Definition 2.2 below) is the most general model considered so far in the realm of stochastic portfolio theory. The method of constructing functionally generated portfolios developed in this paper generalizes the previous theories in both continuous-time and discrete-time market models, and is also easily applicable to rank-based portfolio generation in the stock market of stochastic dimension.

Finally, we provide empirical analyses for classical examples of (multiplicatively generated) portfolios in stochastic portfolio theory. Using a stock dataset over years on two U.S. stock exchanges (NYSE and AMEX), we present the explicit decompositions (see Section 4.4) of the relative wealth processes of functionally-generated portfolios. When we use the original total market index as baseline, the first uncontrollable correction factor significantly influences the relative performance of the functionally-generated portfolios; when the self-financing market portfolio is used as baseline, the drift process (so-called excess growth) mainly contributes to the outperformance of generated portfolios over long-run, very much in accordance with Fernholz’s original theory.

Preview: This paper is organized as follows. Section 2 reviews the concept of piecewise semimartingale and describes our equity market model of stochastic dimension. Section 3 explores how to construct functionally-generated portfolios under the market model. In Section 4, we provide a discrete-time version of the results developed in previous sections and present empirical analyses of classical portfolios using real stock data. Section 5 contains some concluding remarks, and Appendix A illustrates how to construct rank-based portfolios.

2 Equity market of stochastic dimension

We provide in this section some preliminary concepts and definitions and describe an equity market model of stochastic dimension, which we shall use throughout the paper.

2.1 Piecewise semimartingales

We first recall the notion of piecewise semimartingales of stochastic dimension, which was originally introduced by Strong (\APACyear2014). The same definitions and notations were provided in Section 2 of our earlier paper (Bayraktar \BOthers., \APACyear2022), but we include them in this subsection for the completeness of the paper.

Let us denote a state space , equipped with the topology generated by the union of the standard topologies of . Besides the additive identity element , the -dimensional vector of zeros, in for each , we define an additive identity element , a topologically isolated point in satisfying and for each . We define the modified indicator

| (2.1) |

which will be used for dissecting -valued stochastic processes. We shall sometimes add the zero vector with an appropriate dimension to some expressions involving the modified indicator , to make sure that the resulting expression has the correct dimension in . We denote the usual indicator function for a set .

We use the notations , for every , and the transpose of a matrix .

All relationships among random variables are understood to hold almost surely. On a filtered probability space satisfying the usual conditions, let be a -valued progressive process having paths with left and right limits at all times, and denote the dimension process of . The following definition characterizes time instants of dimensional jumps for a given -valued process , as a sequence of stopping times.

Definition 2.1 (Reset sequence).

A sequence of stopping times is called a reset sequence for a progressive -valued process , if the following hold for -a.e. :

-

(1)

, for all , and ;

-

(2)

for every and ;

-

(3)

is right-continuous on for every .

When has a reset sequence , we shall always consider the minimal one in the sense of the fewest resets by a given time:

and assume that the initial dimension is deterministic, i.e., .

In what follows, we fix such -valued process with the reset sequence , and define the dissections of and

| (2.2) | ||||

| (2.3) |

Definition 2.2 (Piecewise semimartingale).

A piecewise semimartingale is a -valued progressive process having paths with left and right limits at all times, and possessing a reset sequence such that is an -valued semimartingale for every .

A piecewise semimartingale is called piecewise continuous (RCLL) semimartingale, if each dissection is an -dimensional continuous (RCLL, i.e., right continuous with left limits, respectively) semimartingale for every .

We note that the -dissection of , defined in (2.3), will be used when plays the role of an integrator. For integrands, a different version of dissection is necessary.

Definition 2.3 (Stochastic integral).

For a piecewise semimartingale and its reset sequence , let be a -valued predictable process satisfying . We dissect in the following manner

| (2.4) |

and define

| (2.5) | |||

For , the stochastic integral is defined as

| (2.6) |

Note that each dissection of (2.4) is predictable, since the process and the )-dissection set are predictable.

The stochastic integral in (2.6) is an -valued semimartingale, and it generalizes the usual -valued semimartingale stochastic integration since any sequence of stopping times is a reset sequence. We also note that is a vector space, i.e., holds for .

2.2 Capitalization and market weight processes

With the concept of piecewise semimartingale, we now describe a model of an equity market having a finite, but unbounded, stochastic number of investable assets.

We first define a -valued capitalization process allowing left-discontinuities between two consecutive dimensional jumps. In order to handle discontinuities, we shall denote and the jump and the left-continuous process of a RCLL semimartingale at time , respectively, for any .

Definition 2.4 (Capitalization process).

A -valued piecewise RCLL semimartingale with reset sequence is called a capitalization process, if every component of is nonnegative, but at least one component is strictly positive on each dissection set for every .

The dimension process of represents the number of companies present in the market, and the components of on the -dissection set, i.e., , represent the capitalizations of the extant companies, for every . For simplicity of the model, we assume without loss of generality that every stock has a single outstanding share, thus the capitalization of a stock is equal to its price. By definition, this model allows individual stock prices to hit zero, but the market’s total capitalization should always remain strictly positive.

Example 2.1.

This model, which adopts a piecewise RCLL semimartingale of variable dimension as a capitalization process, describes a more realistic equity market in the most flexible way. It includes several other models depicting a market with a changing number of assets. We present here a few such examples.

-

(i)

The entrance of a new company and the exit of an existing company are modeled by a birth-death process; for each , whenever the dimension of the market is , a new company enters the market according to the exponential arrival rate of , and one of the companies exits the market with the exponential departure rate of . The dimension process is then the birth-death process with birth and death rates and , respectively. The reset sequence describes the time of either birth or death of a company, and the size of each dimension change is always one, i.e., for each .

-

(ii)

The diverse market model introduced in Karatzas \BBA Sarantsev (\APACyear2016) studies a fluctuating number of companies by describing a certain form of splits and mergers. When the market weight (relative capitalization with respect to total market capitalization) of the largest company exceeds a fixed threshold value between and , the company is split into two companies of random size, modeling a regulatory breakup. On the other hand, any two of the existent companies excluding the largest one, can merge at random times, whenever the exponential clock rings. The reset sequence then depicts the time of either split of the largest company or merger between two small companies, and the size of each dimension change is again equal to one at each stopping time .

-

(iii)

We can even consider a combination of (i) and (ii) above, i.e., a stock market allowing all kinds of events including the entrance, exit, splits, and mergers of companies, whenever each stopping time describes such dimensional change.

For a given capitalization process in Definition 2.4, we define another -valued process whose components represent the relative capitalizations of individual stocks.

Definition 2.5 (Market weight).

We call a -valued process the market weight process, if it is defined via dissection

where the components of and for are given by

| (2.7) |

Note that the -dissection of the market weight process , in the sense of (2.3), is different from of (2.7) for each . Due to its construction, the quantity is equal to zero when , and has an important property

| (2.8) |

on the dissection set ; whereas the dissection of is not necessarily equal to zero when , and does not have such property. However, since each is a RCLL semimartingale, is a -valued piecewise RCLL semimartingale (Definition 2.2), thus the dissection shall play the role of integrators. When does not appear as integrators, we shall use instead of , in order to exploit the property (2.8). We finally note that on each -dissection set, their increments coincide, i.e.,

| (2.9) |

and thus also from (2.8)

| (2.10) |

Remark 2.1.

Though we shall use two different dissections (for integrands) and (for integrators) of the market weight process , every integral in this paper having as an integrator (see, e.g. (2.11) and (3.4)) will only be considered on the -dissection set, therefore the integrator can be replaced by , thanks to (2.9). However, we shall keep using as the integrator in the following to maintain the same notation as in our earlier paper (Bayraktar \BOthers., \APACyear2022).

Example 2.2.

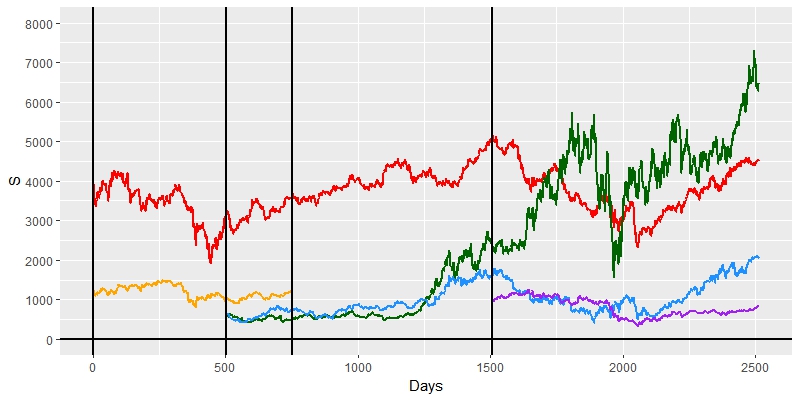

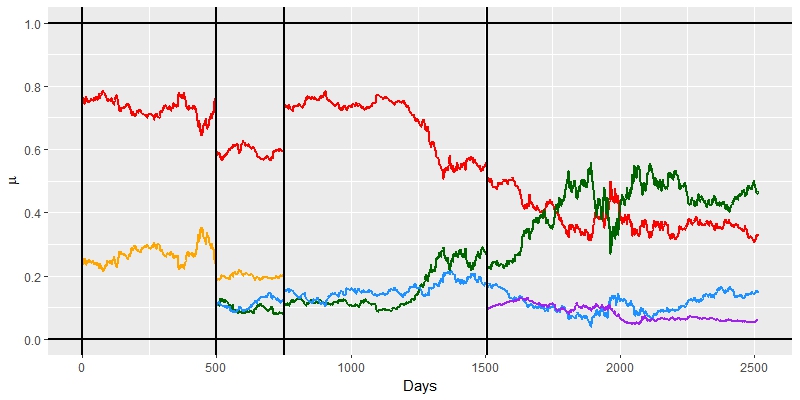

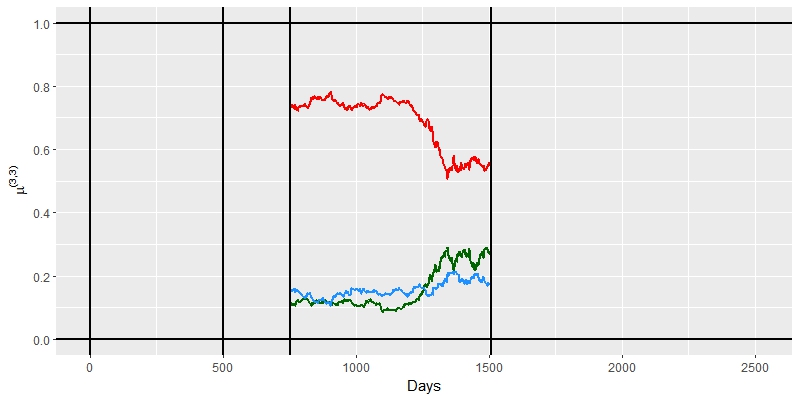

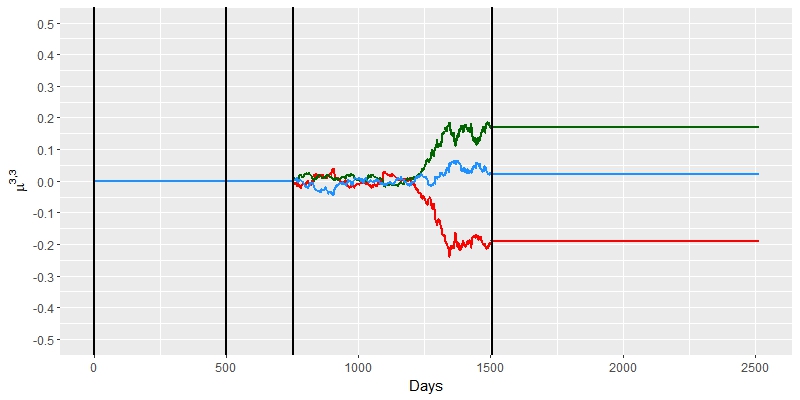

Figure 1 shows an example of a trajectory of -valued (daily) capitalization process and corresponding market weight process during 10 years (2515 trading days). For this trajectory, the reset sequence is and ‘active’ dissections of are , and . Figure 1(c) shows a trajectory of the dissection defined in (2.7), whereas Figure 1(d) illustrates a trajectory of the other dissection .

Though the trajectories shown in Figure 1 are continuous between the dimensional changes, we emphasize here that the capitalization process and the market weight process , defined in Definitions 2.4 and 2.5, have RCLL paths between two consecutive dimensional jumps. Any left-discontinuity between the dimensional jumps models an unexpected change in the price of an individual stock (e.g. a company announces/distributes dividends, etc), and such left-discontinuity of does affect the stochastic integration , which represents the capital gains of holding shares in the stocks.

On the other hand, the dimensional jumps at the stopping times of are mandated to occur only as right-discontinuities such that the dimensional jumps do not affect the integral for any integrand . The stochastic integration just stops at each jump and resumes a new piece just afterward. Since each piece has RCLL paths, the integral remains right-continuous at all times.

This shows how different types of jumps (between and at the stopping times ) of the capitalization process are interpreted in the setting of piecewise RCLL semimartingale. We refer to Section 1.1.2 and Remark 3.1 of Strong (\APACyear2014) for more details on the aforementioned discontinuity properties of the piecewise RCLL process and the integration with their financial interpretation. The market weight process and the stochastic integration for some also have the same discontinuity properties as and .

We conclude this subsection with a remark providing a more detailed description of a delisting event of stock from the market (e.g. due to bankruptcy).

Remark 2.2 (Delisting event).

If the -th stock leaves the -dissected market at the stopping time , there are two possible scenarios: (i) the component is left-continuous at the moment of delisting, i.e., ; (ii) has a left-discontinuity at , i.e., . In case (i), since the dissection remains continuous (both left- and right-continuous) at , the exit of the -th company does not affect at , which means the investor doesn’t lose any money from the exit of the -th company. In other words, we have a chance to liquidate the shares holding in the -th stock at the final moment of its death. However, in case (ii), the left jump at does affect the integral such that we may lose some of (all) the money holding in the -th stock from its delisting, if the final capitalization is close (equal, respectively) to zero.

2.3 Trading strategies and portfolios

Recalling the market weight process of Definition 2.5 and the class of the integrands for in (2.5), we present the following notion of trading strategy. Here and in what follows, we shall use the notation for stochastic integral which starts from of any -integrable -dimensional process :

| (2.11) |

for every and .

Definition 2.6 (Trading strategy).

A -valued process is called trading strategy, if , and satisfies the following two self-financing conditions on each dissection set for every :

| (2.12) |

and

| (2.13) |

where .

Here, the quantity represents the number of shares held in the -th stock at time in the -dissected market. The self-financing property means that there should be neither withdrawals nor injections of capital at all times; gains are reinvested, and losses are absorbed. It is straightforward to notice such property from the second identity (2.13); the absolute wealth (not relative wealth with respect to the market) of is maintained, at the moment of dimensional change , on every -dissection set.

On the other hand, for the first self-financing condition (2.12), we shall need a more detailed explanation. We first denote the left-hand side of (2.12)

| (2.14) |

where the last identity follows from the definition (2.7). Thus, represents the ratio of the wealth of the trading strategy to the total capitalization of the -dissected market. This shows the self-financing property of with respect to the relative capitalization on the interval , but it also implies the self-financing property of with respect to the capitalization vector on the same interval, since the self-financing property is numéraire independent (see Lemma 2.9 of Herdegen (\APACyear2017)).

Using the definition (2.7), we can combine the two self-financing conditions (2.12) and (2.13) by

| (2.15) |

on the -dissection set. Thanks to the usual condition on the filtration, we note that the first term on the right-hand side is -measurable, thus also -measurable, since on the -dissection set (see Problem 2.22 of Karatzas \BBA Shreve (\APACyear1991)).

Collecting the relative wealth on each dissection set, we shall denote

| (2.16) |

the relative wealth process of with respect to the (undissected) market.

We conclude this subsection by defining a portfolio corresponding to a trading strategy via dissection

where for each

| (2.17) |

The component is interpreted as the proportion of wealth invested in the -th stock among stocks at time , on the -dissection set. Every trading strategy we construct in the later sections will have left-continuous components , i.e., for , on every -dissection set. Thus, all components of the corresponding portfolio are also left-continuous on every dissection set.

3 Functional generation of portfolios

Under the stock market model of stochastic dimension described in Section 2, we develop the theory of functional generation of portfolios in this section. After defining the measurable family of generating functions, we describe how to construct additively and multiplicatively generated portfolios from this family. We then decompose their (log-) relative wealth process with respect to the market into 3 terms; the generating function, the excess growth, and the correction term arising due to dimensional jumps.

3.1 Measurable family of generating functions

Our goal is to construct trading strategies (and corresponding portfolios) from a function of the market weight process . Since the process has changing dimensions on each epoch, we shall need a family of generating functions with different dimensions of domains. When is a -valued semimartingale with a reset sequence , we introduce the following notion of piecewise function for . For notational simplicity, we shall use the two notations interchangeably.

Definition 3.1 (Piecewise function).

We call a piecewise function of , if there exists a family of functions such that , , and the function values are defined by

| (3.1) | ||||

A piecewise function of is said to be -times continuously differentiable, if every element of the family is -times continuously differentiable, i.e., , for every . We denote the collection of -times continuously differentiable piecewise functions.

Given a family of functions and , we can construct a piecewise function of :

| (3.2) |

Moreover, for any , we consider the vectors of partial derivatives of the family having different dimensions

| (3.3) |

and call the -valued process , defined by

the gradient of . It is straightforward to check from (2.4) that dissection of the process is given by the standard -dimensional gradient of in (3.3), i.e., for all , and .

From each piece of a piecewise function of , we shall generate the corresponding piece, or the dissection , of trading strategy in a self-financing way. Then, the initial value on the interval should depend on the right-hand side of (2.13), which is -measurable. This implies that the generating function should also depend on an -measurable random variable, in other words, should be determined at the moment of each dimensional change to satisfy the second self-financing identity (2.13). To this end, we introduce the following definition.

Definition 3.2 (Measurable modifications).

For every and any function , we call an additive -measurable modification of , if can be represented as for some -measurable random variable . Similarly, we call a multiplicative -measurable modification of , if can be represented as for some -measurable random variable .

Moreover, given a family of functions corresponding to a piecewise function of , piecewise random function () of is called a additive (multiplicative) measurable modification of , if the corresponding collection of ( of ) satisfies that () and each () is an additive (multiplicative, respectively) -measurable modification of for every .

With this notion, we shall handle the second self-financing condition (2.13) by constructing trading strategies in a recursive manner. Given a family of generating functions and a dissection of trading strategy on the previous ‘epoch’ of the market, a -measurable modification (either additive or multiplicative) of satisfying (2.13), is determined at the moment , and shall be used to generate the next piece of on each -dissection set, for .

3.2 Functionally generated portfolios

In this subsection, we shall construct two types of functionally generated portfolios from a piecewise generating function with its family , using the market weight process of Definition 2.5 as its input. Here and in what follows, we assume without loss of generality that holds, after some normalization (we can consider -measurable modification satisfying and rename to ).

3.2.1 Additive generation

Since we have , standard -dimensional Itô’s formula with jumps yields

| (3.4) | ||||

on the -dissection set, where is the continuous part of , and denotes the Bregman divergence associated with for points

| (3.5) |

Let us define

| (3.6) |

the Gamma process of on each -dissection set. From (3.4), each -Gamma process admits a different formulation

| (3.7) |

on the -dissection set, and it is of finite variation. In particular, if is a concave function, then the Bregman divergence is nonpositive, i.e., for every (by Jensen’s inequality), thus the -Gamma process is nondecreasing on the -dissection set.

We could now take the integrand of the stochastic integral in (3.4) as a candidate for a trading strategy, but we need to make it self-financing. In this effort, we start from defining a dissection of a trading strategy at time

| (3.8) | ||||

| (3.9) |

where is called a defect of balance at time (see Definition 3.3 below). In order to construct the next dissections satisfying the first self-financing condition (2.12) on the interval , recursively in , we shall subtract the so-called defect of self-financibility from the ‘basis’ (see the definition (3.15) below), following the work of Karatzas \BBA Ruf (\APACyear2017). Here, the basis is defined as

| (3.10) |

and the defect of self-financibility is given by

| (3.11) | ||||

Note that we have by definition. We also consider an additive measurable modification of :

| (3.12) |

where is a -measurable random variable

| (3.13) |

We next define a -measurable random variable , and an -dimensional vector process by

| (3.14) |

| (3.15) |

We emphasize again that is defined in a recursive manner for ; from the initial configuration (3.8) and (3.9), of (3.13) depends on the last value of the previous epoch, thus, defined in (3.15), also depends on the quantity .

Finally, we construct a -valued process collecting the dissections

| (3.16) |

We show that this process is indeed a trading strategy, and it is called an additively generated trading strategy from the piecewise generating function .

Proposition 3.1 (Additive generation).

The process in (3.16) is a trading strategy and its relative wealth process is given by

| (3.17) |

Proof.

Since is -integrable and the -dissection set is predictable, is also predictable for every . Moreover, is also predictable and -integrable (Lemma 4.13 of Shiryaev \BBA Cherny (\APACyear2002)) for every . We also have the predictability of -measurable random variable on the dissection set. This shows that .

Next, we check that satisfies the combined self-financing identity (2.15) for an arbitrary pair . We recall the properties (2.8) - (2.10), along with the identity

| (3.18) |

from Theorem II.13 of Protter (\APACyear2003), to derive the series of identities on the -dissection set:

| (3.19) | ||||

Thus, the self-financing condition (2.15) for holds, and is indeed a trading strategy.

Proposition 3.1 generalizes the earlier construction introduced in Karatzas \BBA Ruf (\APACyear2017) for each piece of the dissected market of a fixed dimension and patches these pieces seamlessly in the sense that the second self-financing identity (2.13) is satisfied by introducing a modified version of generating function at the beginning of each piece.

When computing the relative wealth of in Proposition 3.1, we need to use the identity (3.17) in a recursive manner, since depends on the quantity , which in turn depends on the last relative wealth of the previous epoch. This is due to the recursive construction of the trading strategy , however, the following result provides an alternative representation of the relative wealth process for any given .

In order to simplify some of the notations in the following, we denote

| (3.21) |

the ratio of total capitalization at to total capitalization right afterward for the -dissection set, and write their products from the -th epoch to the -th epoch for any by

| (3.22) |

Theorem 3.1 (Additive generation).

For an arbitrary pair with , belonging to a -dissection set for , the relative wealth of the additively generated trading strategy in Proposition 3.1 can be decomposed as the sum of the generating function, the excess growth (EG), and the correction term (C) which arises from dimensional jumps up to time :

| (3.23) |

| (3.24) | ||||

| (3.25) |

with the notation .

3.2.2 Multiplicative generation

In what follows, we also fix a piecewise generating function in , but with an extra condition that the reciprocal is locally bounded on every -dissection set. Recalling the notations in Section 3.2.1, we shall recursively define two -valued process and as follows. At time , let us set

| (3.26) |

as in (3.9). For each consider a -measurable random variable

| (3.27) |

and a multiplicative measurable modification of

| (3.28) |

Let us recall from (3.6) the Gamma process on the -dissection set and define

| (3.29) |

where denotes the stochastic exponential of a finite variation process with defined on the -dissection set:

| (3.30) |

such that holds. Thanks to the assumption on that the reciprocal is locally bounded, the process is of finite variation on the -dissection set. We continue to define for , and any

| (3.31) |

Furthermore, a -measurable random variable and the defect of self-financibility for are defined as before in (3.11), (3.14), and an -dimensional vector process is given by

| (3.32) |

Finally, we construct a -valued process collecting the dissections

| (3.33) |

The next result shows that is indeed a trading strategy and we call it multiplicatively generated from the generating function .

Proposition 3.2 (Multiplicative generation).

For a piecewise function of such that the reciprocal is locally bounded for every , the process in (3.33) is a trading strategy and its relative wealth process is given by

| (3.34) |

Proof.

As in the proof of Proposition 3.1, it is straightforward to check the predictability and -integrability of and , thanks to the local boundedness assumption on for each . This shows . Moreover, we can prove in the same manner that satisfies the self-financing condition (2.15) and conclude that is a trading strategy.

We fix an arbitrary pair and note that the process is of finite variation and the identity holds. By applying the product rule (Theorem I.4.49 of Jacod \BBA Shiryaev (\APACyear2003)) and recalling the definition (3.6), we derive on each -dissection set, i.e., :

| (3.35) | ||||

Here, the second-last equality is from the property (2.10), and the last identity follows from the self-financing condition (2.12) for . Furthermore, we derive from and that

| (3.36) |

From these derivations, we conclude that

| (3.37) |

on the -dissection set. When , it is trivial to check , and the result (3.34) follows. ∎

As in Theorem 3.1, we now derive the decomposition of the log-relative wealth for any given .

Theorem 3.2 (Multiplicative generation).

For an arbitrary pair with , belonging to a -dissection set for , the log relative wealth of the multiplicatively generated trading strategy in Proposition 3.2 can be decomposed as the sum of the generating function, the excess growth (EG), and the correction term (C) which arises from dimensional jumps up to time :

| (3.38) |

| (3.39) | ||||

| (3.40) |

with convention . Here, denotes the continuous part of the Gamma process , the first term on the right-hand side of (3.7).

Proof.

Since dissection sets are disjoint, we have the identity from (2.16) for the given pair (omitting ). We repeatedly apply (3.37) and (3.42) to derive

We rearrange some of the terms on the right-hand side by using the identity and the definitions (3.41), (3.21) to obtain the correction term :

For the remaining terms, we use (3.29), (3.30), and Theorem II.13 of Protter (\APACyear2003), to derive

| (3.43) |

and similar expressions for for . Thus, the result (3.38) follows. ∎

3.2.3 Balance condition

We first note that the component of additively generated trading strategy in (3.15) has an alternative representation on the -dissection set :

| (3.44) |

from the identities (3.18) and (3.20). Moreover, the last term can be replaced with the right-hand side of (3.23), so the strategy is expressed in terms of the original generating family and its gradient, the excess growth and the correction term, up to time .

Similarly, the component of multiplicatively generated strategy in (3.32) also admits an alternative representation from the identities (3.35) and (3.36):

| (3.45) |

and we can apply the decomposition (3.38) to the last term of (3.45). Furthermore, for , there is a condition to impose on each generating function to further simplify the representation of the corresponding portfolio .

Definition 3.3 (Balance condition).

For each , an -dimensional differentiable function is called balanced, if satisfies

This balance condition is known not only to simplify the representations of functionally generated trading strategies and corresponding portfolios (Karatzas \BBA Ruf, \APACyear2017; Karatzas \BBA Kim, \APACyear2020), but also to handle discontinuities of an additional process other than market weights when generating trading strategies (Kim, \APACyear2023). The balance condition shall also be used in Section A.2, since it enables rank-based portfolios to invest only in the fixed number of large capitalization stocks in open markets, adopting the idea of Karatzas \BBA Kim (\APACyear2021).

When satisfies the balance condition, it is straightforward to check the identity

for every . The last equality, together with (3.45) and (3.34), yields

| (3.46) |

Recalling the definition (2.17) of portfolio weights and the fact that (and its portfolio weight ) is left-continuous, we have the following result.

Corollary 3.1.

If every generating function satisfies the balance condition, then the portfolio weight of multiplicatively generated trading strategy is expressed as

| (3.47) |

Note that the right-hand side depends only on the market weight process and on the original generating function (not its measurable modification ), even though the components of the trading strategy in (3.46) depend on , or a normalizing random variable .

3.2.4 Self-financing market portfolio

The relative wealth of the functionally generated trading strategy , which appears in Theorems 3.1 and 3.2, measures the wealth of relative to the total market capitalization at time , as defined in (2.14). By its construction, the trading strategy is designed to be self-financing at all times, whereas the total market capitalization (the denominator in (2.14)) can undergo a jump at each moment of dimensional change.

Moreover, the correction term in (3.40) of a multiplicatively generated strategy can be further decomposed as

| (3.48) |

Note that the first term on the right-hand side is independent of the generating function . It accumulates the (log values of) jumps in the total market capitalization, whereas the second term captures the (log values of) jumps in the generating function, at all previous dimensional changes up to time .

These observations give rise to the following notion of self-financing market portfolio. Consider a family of functions, given by and . It is easy to check the two trading strategies, additively and multiplicatively generated from , coincide; let us denote it by . Its corresponding portfolio is computed as

| (3.49) |

for every from Corollary 3.1.

Definition 3.4 (Self-financing market portfolio).

The trading strategy and its portfolio of (3.49) are called the self-financing market trading strategy and self-financing market portfolio, respectively. We denote them by and .

From Theorem 3.2 and (3.48), the log relative wealth of only contains the correction term , in other words, , and

| (3.50) |

for any on the -dissection set, recalling the notation (3.22). We emphasize again that the above term appears in the decomposition (3.38) of every functionally generated trading strategy, independent of the generating function. Moreover, from the identity (3.46), we can easily deduce that all components of are equal to . Therefore, is just a buy-and-hold trading strategy investing equal shares in all the extant stocks between dimensional jumps; at each dimensional jump, the number of shares holding for every stock is adjusted according to the jumps in total market capitalization, redistributing its wealth to the next constituents of the market in a self-financing way. This also explains how the portfolio in (3.49) distributes its wealth according to relative capitalizations of extant stocks at all times.

If an investor believes that the self-financing market portfolio should be the baseline to compare the relative performance of the functionally generated trading strategy , one can easily compute the ratio of to . We note here that takes positive values for every , due to the positivity assumption on the capitalization process in Definition 2.4. Let us denote

| (3.51) |

the relative wealth of trading strategy with respect to the self-financing market portfolio. As in the manner of (2.16), the process can be expressed as a collection of on each -dissection set. In particular, for a multiplicatively generated trading strategy in Theorem 3.2, we have the decomposition of the log relative wealth of with respect to

| (3.52) |

with the same excess growth term of (3.39), but with the correction term replaced by of (3.48).

3.2.5 Long-term growth of relative wealth processes

In this part, we shall compare the behavior of the excess growth term in (3.24) with that of (3.39), and point out some disadvantages of the additively generated trading strategies over the multiplicatively generated ones.

The excess growth terms of (3.24) and (3.39) contribute to the long-term growth of the relative wealth processes and . We recall from the representation (3.7) that each Gamma process is nondecreasing if each is a concave function. Therefore, both of the expressions (3.24) and (3.39) are nonnegative, if every generating function in the family is concave. However, even with concave generating functions, the former excess growth term (3.24) is generally not nondecreasing in time. For an additively generated strategy , the expression (3.24) may decrease at the next dimensional change , if the next ratio of total market capitalization (where is a next market dimension) is significantly less than . This is because all the accumulations of Gamma processes for in the ‘past’ epochs, are affected by the ratios of the total market capitalization at ‘future’ dimensional changes , as the quantity will be multiplied to the whole expression of (3.24) at the moment of the next dimensional jump, and so on. In this sense, we can say that the excess growth of (3.24) is only ‘piecewise nondecreasing’ in time with a potential of occasional plummet at the moments of dimensional changes.

In contrast, the excess growth (3.39) of the multiplicatively generated strategy is independent of the ratios . Therefore, every term of (3.39) is nonnegative and nondecreasing in time, if all the generating functions are positive and concave. This shows that the long-term growth of a multiplicatively generated strategy is not affected by the shocks that arise from dimensional jumps in the market.

Moreover, the correction term of has a nice decomposition (3.48), which separates the universal term with the other term , whereas that of in (3.25) does not admit such decomposition. Thus, there is no simple representation of the relative wealth of the additively generated strategy with respect to the self-financing market portfolio; should depend on the ratios of (3.21). However, in (3.52) is free of such ratios, so the excess growth contributes to the long-term outperformance of with respect to the self-financing market portfolio if we expect long-term stability of the remaining part , which only depends on the generating function .

Because of the aforementioned drawbacks of the additively generated strategies, we shall provide in the next section examples of multiplicatively generated portfolios with empirical evolution of each term that appears in the decompositions (3.38) and (3.52).

4 Empirical analyses

Our main purpose of this section is to examine how dimensional changes in the equity market affect portfolio performances. More specifically, using real stock market data, we would like to identify the correction terms , , and in the equations (3.38), (3.50), and (3.52) of the log relative wealth processes and for some classical portfolios, all of which are multiplicatively generated.

For the reason that we shall use daily stock price data, we first develop the previous theory of functional generation of portfolios in a discrete-time market model as a special case of the general theory we studied in Section 3, for a more precise comparison of the correction terms. When computing the excess growth term of (3.39), we are subject to approximation errors for measuring the integral terms involving the Gamma processes from a given discrete-time dataset. Since we shall consider a long period of time (40 years) for analyzing portfolios, the approximation errors tend to be accumulated over a long time which hinders the exact analysis of the correction terms.

4.1 Discrete-time model

Since we allow jumps in the capitalization (and market weight) process, all of the results in the previous sections can be easily reformulated in a discrete-time equity market model. For the purpose of introducing a discrete-time model, we shall fix in this subsection an index set satisfying . Moreover, for a given -valued discrete-time stochastic process on a probability space , let us consider a sequence of stopping times at which the dimension of changes, i.e.,

Then, we can construct a -valued piecewise-constant process by the recipe and for

| (4.1) | ||||

such that is right-continuous between the dimensional jumps and left-continuous at the dimensional jumps. For the filtration, we consider a right-continuous extension for of the natural filtration of . From this construction, it is straightforward to verify that is a -progressive process and the sequence is the (minimal) reset sequence of satisfying the conditions of Definition 2.1, thus is recognized as a piecewise RCLL semimartingale in the sense of Definition 2.2.

Therefore, when observing capitalizations of an equity market (of stochastic dimension) only at the discrete times , such that the capitalization process is given as a -valued discrete stochastic process, we shall consider its piecewise-constant continuous-time version with the corresponding market weight process of , having the dimension process , to apply the previous theory for generating trading strategies from . In other words, for any , we shall identify the trajectory of the discrete process with its continuous-time version .

Now that is piecewise-constant, the continuous part of every integral with the integrator involving (dissections of) vanishes, and we can rewrite all the expressions in the earlier sections in terms of the original discrete-time process from the construction (4.1). In particular, for , the first self-financing condition (2.12) can be rewritten as

and each -Gamma process of (3.7) is represented as

The equation (3.43) is now simplified to

Therefore, Theorem 3.2 holds with the decomposition (3.38) (and (3.48)), rewritten as

| (4.2) | ||||

| (4.3) | ||||

| (4.4) |

with the convention and the notation

for a given pair in each -dissection set for with . Here and in what follows, represents the last time index before , whereas is the next index after , i.e., and if , with the convention . The expression represents the discrete excess growth from to , when the market is in the -th epoch with dimension , thus is the cumulative discrete excess growth until time .

Since there is a dimensional jump between and , the last three terms of the equation (4.2) remains unchanged, i.e., , , and , due to its construction (4.1). However, during the next time window between and , the increment of the last term on the right-hand side of (4.2), is offset by the previous increment of the first term :

| (4.5) |

In other words, every summand of in (4.4), which occurs due to dimensional jump between and , is canceled out by the increment of during the same period. Therefore, the decomposition (4.2) - (4.4) can be rewritten as

i.e., the evolution of the log generating function and the excess growth accumulated between the past dimensional jumps and the universal correction term accumulated at those dimensional jumps affect the relative wealth .

For the log relative wealth in (3.52), we have the same representation in this discrete-time setting, except for the last correction term:

The above derivations generalize the results of Wong (\APACyear2017), where the functional generation of portfolios is developed in a discrete-time market model of a fixed dimension. Here, we also refer to Campbell \BBA Wong (\APACyear2022), Pal \BBA Wong (\APACyear2016), and Wong (\APACyear2015), for different aspects of the discrete-time setup of portfolio generation in a market of fixed dimension.

4.2 Examples

We provide in this subsection some of the classical examples in the Stochastic portfolio theory under the discrete-time model. Empirical analyses of these examples will be given in the following subsections.

When introducing a portfolio-generating function as a piecewise function of the market weight process in the following examples, we shall only specify an -dimensional ‘representative piece’ , for a fixed pair . All the other pieces can be easily inferred from this representative form; in fact, for any . Moreover, we assume in the following that a general time index is in the -th epoch with market dimension equal to , i.e., the pair belongs to the -dissection set .

Example 4.1 (Diversity-weighted portfolio).

For a fixed real number , the function

is balanced (Definition 3.3) and multiplicatively generates the portfolio from (3.47)

| (4.6) |

The parameter determines a measure of diversity; a portfolio with a smaller value of invests more wealth in smaller stocks. We also note that the case corresponds to the self-financing market portfolio in Section 3.2.4. After some computation, we obtain from (4.2) the following decomposition of the log-relative wealth of the corresponding trading strategy

| (4.7) |

the excess growth is given as (4.3) with

and the correction term

Example 4.2 (Equal-weighted portfolio).

The following balanced function

multiplicatively generates the portfolio from (3.47)

which invests the same proportions of current wealth in all the existing stocks. We note that this portfolio is the limit of the diversity-weighted portfolio (4.6) when . The decomposition (4.2) of the log-relative wealth is then computed as

| (4.8) |

the excess growth is given as (4.3) with

and the correction term equal to

4.3 Data description

Our data contain daily closing prices of the stocks listed on the New York Stock Exchange (NYSE) and American Stock Exchange (AMEX) during 40 years (10086 trading days) between 1982 January 4th and 2021 December 31st. These data were obtained from the Center for Research in Security Prices (CRSP, \APACyear2023) database, accessed via the Wharton research data services. We refer to Ruf (\APACyear2023) for a more extensive description of the CRSP database.

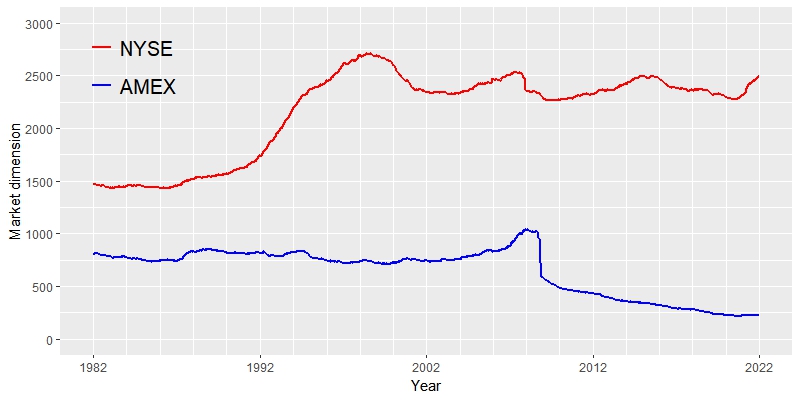

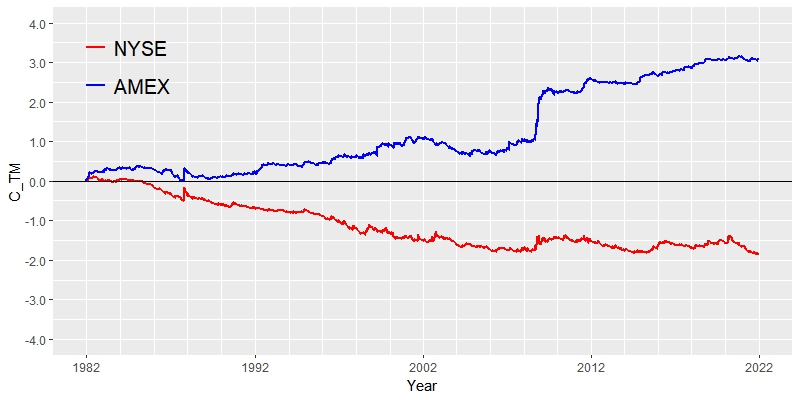

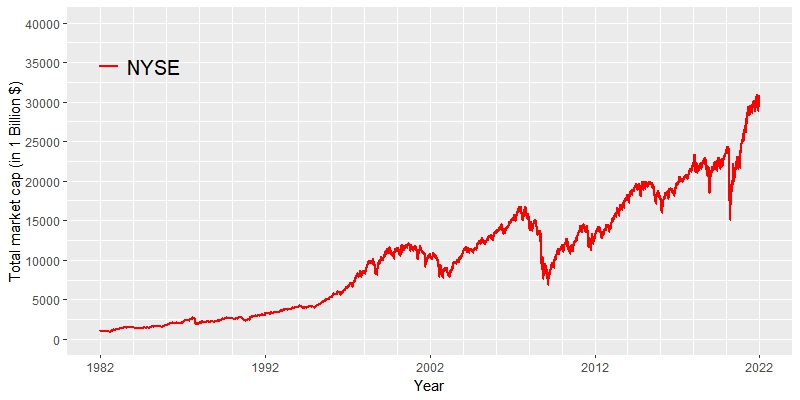

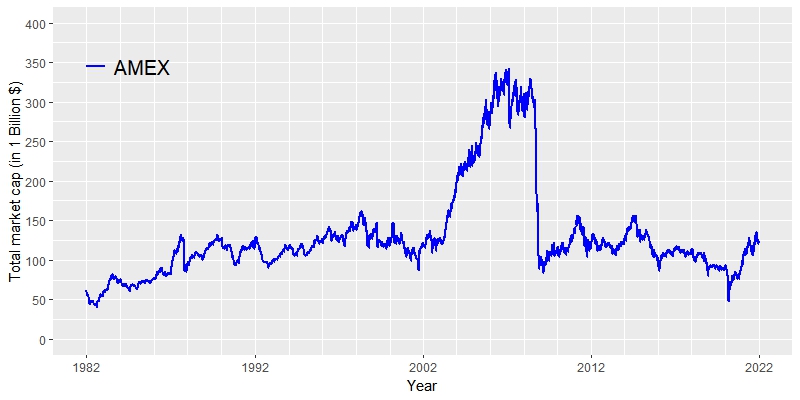

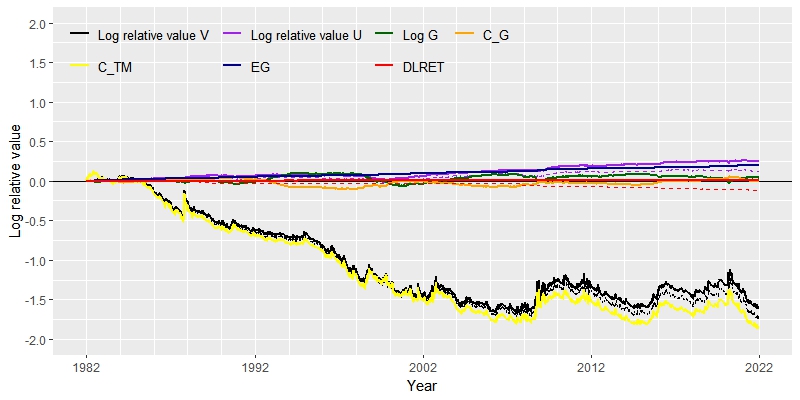

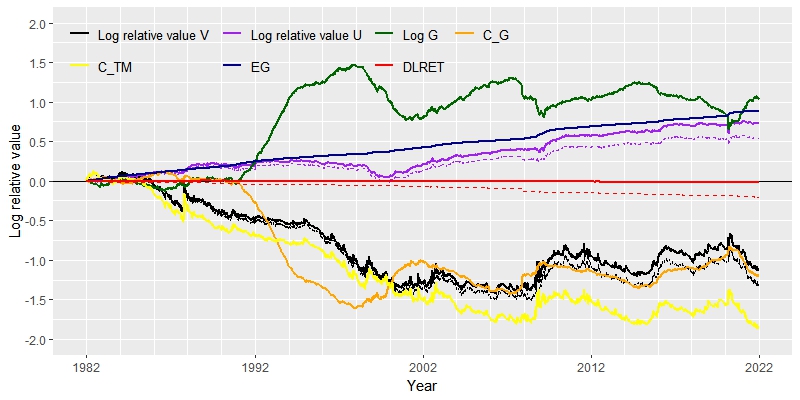

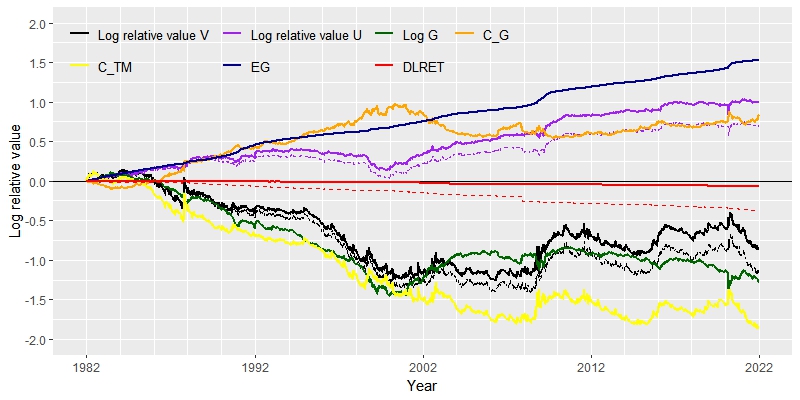

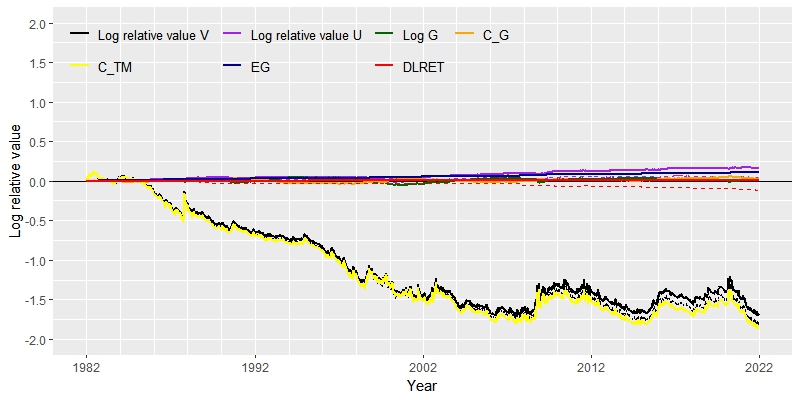

In the discrete-time model introduced in Section 4.1, each element of the time index set represents the -th trading day. Figure 2 describes the evolutions of dimensional changes, the universal correction term in (3.50), and the total market capitalizations of the two stock exchanges over years. In Figure 2 (a), there were and jumps in dimension during days for NYSE and AMEX respectively; in other words, on average, dimensional changes occurred every and trading days, respectively.

Since the number of listed stocks on NYSE has increased over years, the correction term of (3.50) for NYSE in Figure 2 (b) exhibits overall decreasing movement. For the AMEX graph, we can observe the opposite tendency. A small hike near the year 1987 in the two graphs of Figure 2 (b) is on account of the stock market crash in October 1987, known as Black Monday.

In the graphs of AMEX in Figure 2, there was a significant delisting event in , which led to noticeable decreases in market dimension and total capitalization. The main reason is that NYSE Euronext, the multinational financial corporation which operates NYSE, acquired AMEX in , and AMEX is now known as the NYSE American. During this process of acquisition, many stocks are liquidated or dropped from the exchange, due to various reasons, e.g. failure to meet the new exchange’s financial guidelines for continued listing, or just company’s request. The stock market crash in is also responsible for the huge drop in total market capitalization of the two exchanges.

We finally mention here that tradings of the portfolios in the next subsection are made every trading day (daily rebalance) without any transaction costs, in order to precisely measure how much the correction terms impact the long-run relative performance of the portfolios in the decomposition identities. Since finding an outperforming portfolio (or a relative arbitrage in Section 3.2.5) is not our goal, no transaction costs are considered in our empirical analysis. In the presence of transaction costs, trading frequency should be wisely determined by actual portfolio managers to maximize their profit, and we refer to Ruf \BBA Xie (\APACyear2020) in this direction of study.

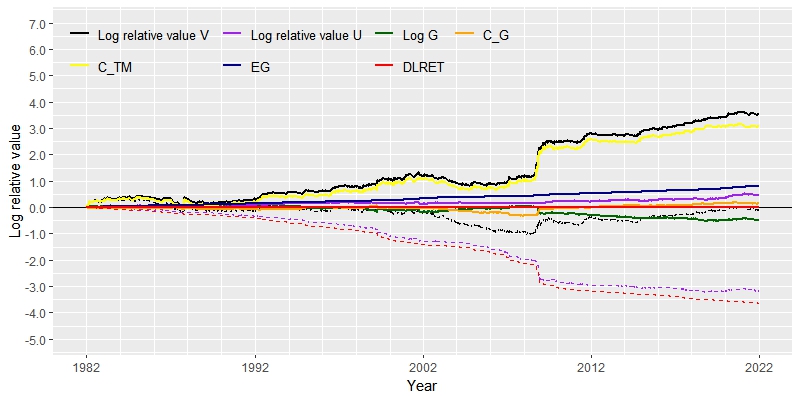

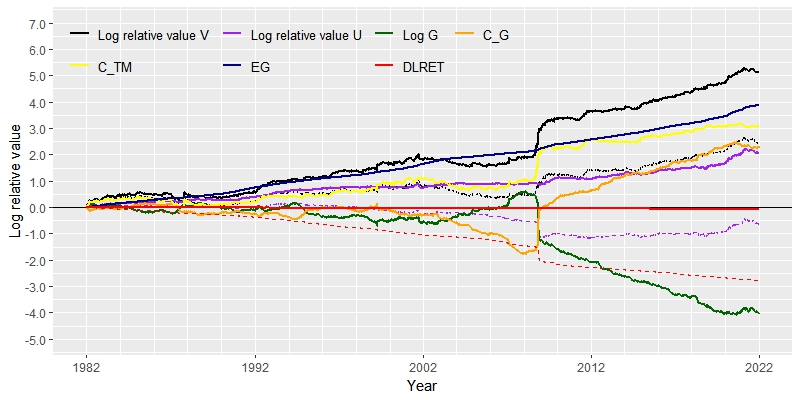

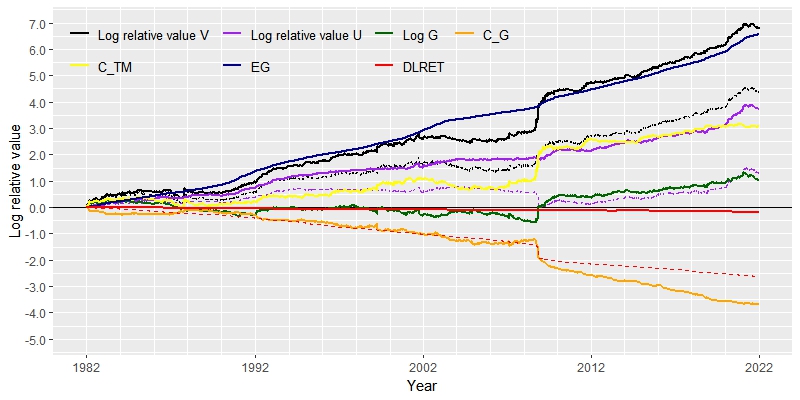

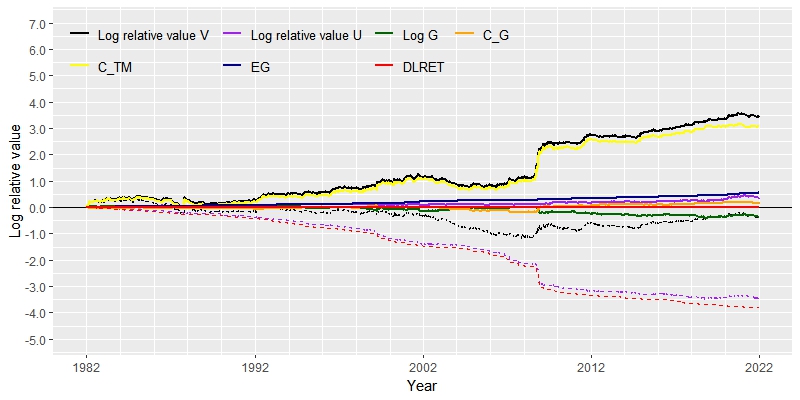

4.4 Empirical results

We now provide the empirical results of individual terms in the decompositions (4.7), (4.8), and (4.9), of the log relative wealth processes of the classical portfolios introduced in Section 4.2, using the dataset described in Section 4.3. The evolutions of the term (the first term on the right-hand side) and the excess growth () will be illustrated in green and blue, respectively. The universal correction term , which is also depicted in Figure 2 (b), will be in yellow, and the other correction term will be drawn in orange.

Under the discrete-time market model, we note that the identities (4.7), (4.8), and (4.9) are exact, except at the moment when a stock is delisted from each of the two exchanges. In a delisting event, we use its delisting return which is available through our dataset from the CRSP database. However, our dataset contains a lot of missing delisting return variables. For those missing values, we shall consider two cases: (i) the most conservative case by setting all missing delisting returns equal to (which means we lose all money which was allocated to the delisting stock), (ii) the most desirable case by setting the values equal to (which means we can liquidate the whole value of a stock before delisting from the exchange). In our dataset, there are some positive delisting returns, due to some reasons, but these are rare cases. When the -th stock is delisted from the exchange with delisting return at day , we will accumulate the quantity , which represents the change in the log return of due to the delisting, and we call this new term DLRET. For case (i), the DLRET graph will be drawn as a red solid line; for case (ii), it will be represented as a red dotted line. We recall here Remark 2.2 how our general continuous-time model in Section 3 handles such delisting event.

Finally, the two log relative wealth of the portfolios, with respect to the total market capitalization (), and to the self-financing market portfolio () will be illustrated in black and purple, respectively. Therefore, from the identities (3.38) and (3.52), we have the relationships in the following figures ‘black = green + blue + yellow + orange + red’, and ‘purple = green + blue + orange + red’. Since there are solid and dotted red graphs, black and purple graphs also have two corresponding line types. We normalized the trading strategies at time such that every term in the decomposition takes an initial value of zero.

Figures 3 and 4 show the aforementioned decompositions of the three portfolios, invested in the NYSE and AMEX, respectively.

We now illustrate several important observations from Figures 3 and 4.

-

(i)

The universal correction term , an inevitable term due to the jump in the total market capitalization, is quite huge; it is in fact a major factor of the relative wealth of the portfolios with respect to the total market capitalization, especially for the diversity-weighted portfolio with and the entropy-weighted portfolio. Moreover, as mentioned in Section 4.3, it influences the portfolio return on the two exchanges in the opposite way; for the portfolios on NYSE, it drags down the relative wealth , whereas it contributes to the growth of for those on AMEX. This gives a reason for investors to use the self-financing market portfolio as the baseline when comparing the relative outperformance of their portfolios.

-

(ii)

For the diversity-weighted portfolios, smaller values (or more concentration on the smaller stocks) result in higher excess growth ( term), which is well-known in the Stochastic portfolio theory (see, e.g. Example 3.4.4 of E\BPBIR. Fernholz (\APACyear2002)). Especially, in graphs (b) and (c), the excess growth significantly contributes to the growth in the log relative wealth . However, such portfolios which overweight the smaller stocks, are subject to high turnover, thus should be carefully implemented in the presence of transaction costs.

-

(iii)

Furthermore, in those portfolios of (b) and (c), both the green graph ( term) and the orange graph ( term) fluctuate tremendously, but the directions of change are almost the opposite, like reflected mirror images of each other. This is expected from the fact that the dimensional change is quite frequent (see Figure 2 (a)), and from the relationship (4.5) of their increments at those moments of dimensional changes. Therefore, only the fluctuation of the generating function and the excess growth term between two consecutive dimensional changes affect the evolution of relative wealth with respect to the self-financing market portfolio.

-

(iv)

As expected, the red graph (DLRET) negatively affects the portfolio performance, and its impact is larger for those on AMEX than on NYSE. Since there are more stocks on NYSE, a loss from a delisting of stock on NYSE (in the worst case of delisting return equal to ) should have a smaller influence, on average, on the portfolio performance than that on AMEX. The actual evolution of the DLRET term should be somewhere in the middle of the red graphs, so these graphs provide at least bounds of the log relative wealth processes (black and purple graphs).

5 Conclusion

By incorporating dimensional changes of an equity market in the functional generation of portfolios, this paper removes the assumption on the immutable size of the investable universe. We conclude by summarizing some directions for further extending the functional generation theory of portfolios from Karatzas \BBA Kim (\APACyear2020).

-

(i)

When constructing portfolios, some observable, but non-tradable quantities other than the market weights can be also used. Here, is a -valued stochastic process of finite dimension with its own dimension process (which may coincide with or not). The representative generating function then takes two -valued processes and as inputs.

Examples of such additional process include moving average, running maximum or minimum of the individual market weight from its ‘birth’ at time , realized quadratic covariation , and stock fundamentals such as the book value (which we assume to have finite variation). We refer the reader to Kim (\APACyear2023); Mijatovic (\APACyear2021); Ruf \BBA Xie (\APACyear2019); Schied \BOthers. (\APACyear2018) in this direction of studies.

-

(ii)

Throughout the paper, we assume the portfolio-generating piecewise function to be in (Definition 3.1), for the purpose of applying Itô’s formula. However, we can extend the class of portfolio-generating functions to less smooth functions when a generalized version of Itô’s formula (or Tanaka’s formula) is used.

-

(iii)

Even though the theory was developed in a probability space, we can remove any probabilistic assumptions and construct portfolios in a pathwise, probability-free setting. The capitalization process and the market weight vector can be modeled as -valued piecewise functions instead of semimartingales, in which case the reset sequence is just a sequence taking values in , and we apply the pathwise Itô-Tanaka theory when generating portfolios in a similar manner described in this paper. We refer to Allan \BOthers. (\APACyear2023) for a more recent study in this direction using the rough path theory.

Along with the above lists of applicable extensions of the theory from Karatzas \BBA Kim (\APACyear2020), we list a few more directions for future study in the context of our paper.

-

(i)

In the examples of Section 4, we have used the ‘same’ generating function for every epoch of the market even when its dimension changes. For example, in Section 4.4, the same parameter is used at all times for each diversity-weighted portfolio. However, we can choose different generating functions (or different parameters within a family of generating functions) for each epoch. Especially, if an investor can predict a certain trend in market diversity or expect a huge economic event (such as stock market crash) for an upcoming epoch of the market, she can choose the generating function accordingly for the next epoch in order to maximize her profit. How the adoption of different generating functions for each epoch influences the portfolio return would be a practically interesting topic.

-

(ii)

We may extend some theoretical results in SPT under the market model of changing dimension. For example, Cuchiero \BOthers. (\APACyear2019) connects SPT with Cover’s universal portfolio theory (Cover, \APACyear1991). It would be interesting to find out whether a similar result holds when the dimension of the market fluctuates over time.

Acknowledgments

The authors greatly appreciate Ioannis Karatzas for detailed reading and feedback which improved this paper.

Funding

E. Bayraktar is supported in part by the National Science Foundation under grant DMS-2106556 and by the Susan M. Smith Professorship.

Data availability statement

The data that support the findings of this study are available from CRSP. Restrictions apply to the availability of these data, which were used under license for this study. Data are available from https://www.crsp.org/ with the permission of CRSP.

References

- Allan \BOthers. (\APACyear2023) \APACinsertmetastarModel-free:Roughpath{APACrefauthors}Allan, A\BPBIL., Cuchiero, C., Liu, C.\BCBL \BBA Prömel, D\BPBIJ. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleModel-free portfolio theory: A rough path approach Model-free portfolio theory: A rough path approach.\BBCQ \APACjournalVolNumPagesMathematical FinanceTo appear. \PrintBackRefs\CurrentBib

- Bayraktar \BOthers. (\APACyear2022) \APACinsertmetastarBKT:arbitrage{APACrefauthors}Bayraktar, E., Kim, D.\BCBL \BBA Tilva, A. \APACrefYearMonthDay2022. \APACrefbtitleArbitrage theory in a market of stochastic dimension. Arbitrage theory in a market of stochastic dimension. \APACrefnotePreprint, arXiv:2212.04623 \PrintBackRefs\CurrentBib

- Campbell \BBA Wong (\APACyear2022) \APACinsertmetastarCampbell:Wong{APACrefauthors}Campbell, S.\BCBT \BBA Wong, T\BHBIK\BPBIL. \APACrefYearMonthDay2022. \BBOQ\APACrefatitleFunctional Portfolio Optimization in Stochastic Portfolio Theory Functional portfolio optimization in stochastic portfolio theory.\BBCQ \APACjournalVolNumPagesSIAM Journal on Financial Mathematics132576-618. \PrintBackRefs\CurrentBib

- Cover (\APACyear1991) \APACinsertmetastarCover_1991{APACrefauthors}Cover, T. \APACrefYearMonthDay1991. \BBOQ\APACrefatitleUniversal portfolios Universal portfolios.\BBCQ \APACjournalVolNumPagesMathematical Finance111-29. \PrintBackRefs\CurrentBib

- CRSP (\APACyear2023) \APACinsertmetastarCRSP{APACrefauthors}CRSP. \APACrefYearMonthDay2023. \APACrefbtitleCRSP US stock database. CRSP US stock database. \APACrefnotehttps://www.crsp.org, accessed via Wharton research data services \PrintBackRefs\CurrentBib

- Cuchiero \BOthers. (\APACyear2019) \APACinsertmetastarCuchiero_Scha_Wong{APACrefauthors}Cuchiero, C., Schachermayer, W.\BCBL \BBA Wong, T\BHBIK\BPBIL. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleCover’s universal portfolio, stochastic portfolio theory, and the numéraire portfolio Cover’s universal portfolio, stochastic portfolio theory, and the numéraire portfolio.\BBCQ \APACjournalVolNumPagesMathematical Finance293773-803. \PrintBackRefs\CurrentBib

- E\BPBIR. Fernholz (\APACyear2002) \APACinsertmetastarFe{APACrefauthors}Fernholz, E\BPBIR. \APACrefYear2002. \APACrefbtitleStochastic Portfolio Theory Stochastic portfolio theory (\BVOL 48). \APACaddressPublisherSpringer-Verlag, New York. \APACrefnoteStochastic Modelling and Applied Probability \PrintBackRefs\CurrentBib

- R. Fernholz (\APACyear1999) \APACinsertmetastarF_generating{APACrefauthors}Fernholz, R. \APACrefYearMonthDay1999. \BBOQ\APACrefatitlePortfolio generating functions Portfolio generating functions.\BBCQ \BIn M. Avellaneda (\BED), \APACrefbtitleQuantitative Analysis in Financial Markets. Quantitative analysis in financial markets. \APACaddressPublisherWorld Scientific. \PrintBackRefs\CurrentBib

- R. Fernholz (\APACyear2018) \APACinsertmetastarFernholz:2018{APACrefauthors}Fernholz, R. \APACrefYearMonthDay2018. \APACrefbtitleNumeraire markets. Numeraire markets. \APACrefnotePreprint, arXiv:1801.07309 \PrintBackRefs\CurrentBib

- R. Fernholz \BBA Karatzas (\APACyear2009) \APACinsertmetastarFK_survey{APACrefauthors}Fernholz, R.\BCBT \BBA Karatzas, I. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleStochastic Portfolio Theory: an overview Stochastic Portfolio Theory: an overview.\BBCQ \BIn \APACrefbtitleHandbook of Numerical Analysis Handbook of numerical analysis (\BVOL Mathematical Modeling and Numerical Methods in Finance). \APACaddressPublisherElsevier. \PrintBackRefs\CurrentBib

- Ghomrasni \BBA Pamen (\APACyear2010) \APACinsertmetastarGhomrasni:Pamen{APACrefauthors}Ghomrasni, R.\BCBT \BBA Pamen, O\BPBIM. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleDecomposition of Order Statistics of Semimartingales Using Local Times Decomposition of order statistics of semimartingales using local times.\BBCQ \APACjournalVolNumPagesStochastic Analysis and Applications283467-479. \PrintBackRefs\CurrentBib

- Herdegen (\APACyear2017) \APACinsertmetastarHerdegen:2015{APACrefauthors}Herdegen, M. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleNo-arbitrage in a numéraire-independent modelling framework No-arbitrage in a numéraire-independent modelling framework.\BBCQ \APACjournalVolNumPagesMathematical Finance272568-603. \PrintBackRefs\CurrentBib

- Itkin \BBA Larsson (\APACyear2021) \APACinsertmetastarItkin:Larsson:Open{APACrefauthors}Itkin, D.\BCBT \BBA Larsson, M. \APACrefYearMonthDay2021. \APACrefbtitleOpen Markets and Hybrid Jacobi Processes. Open markets and hybrid Jacobi processes. \APACrefnotePreprint, arXiv:2110.14046 \PrintBackRefs\CurrentBib

- Jacod \BBA Shiryaev (\APACyear2003) \APACinsertmetastarJacodS{APACrefauthors}Jacod, J.\BCBT \BBA Shiryaev, A\BPBIN. \APACrefYear2003. \APACrefbtitleLimit Theorems for Stochastic Processes Limit theorems for stochastic processes (\PrintOrdinal2nd \BEd). \APACaddressPublisherBerlinSpringer. \PrintBackRefs\CurrentBib

- Karatzas \BBA Kim (\APACyear2020) \APACinsertmetastarKaratzas:Kim{APACrefauthors}Karatzas, I.\BCBT \BBA Kim, D. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleTrading strategies generated pathwise by functions of market weights Trading strategies generated pathwise by functions of market weights.\BBCQ \APACjournalVolNumPagesFinance and Stochastics242423-463. \PrintBackRefs\CurrentBib

- Karatzas \BBA Kim (\APACyear2021) \APACinsertmetastarKaratzas:Kim2{APACrefauthors}Karatzas, I.\BCBT \BBA Kim, D. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleOpen markets Open markets.\BBCQ \APACjournalVolNumPagesMathematical Finance3141111-1161. \PrintBackRefs\CurrentBib

- Karatzas \BBA Ruf (\APACyear2017) \APACinsertmetastarKaratzas:Ruf:2017{APACrefauthors}Karatzas, I.\BCBT \BBA Ruf, J. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleTrading strategies generated by Lyapunov functions Trading strategies generated by Lyapunov functions.\BBCQ \APACjournalVolNumPagesFinance and Stochastics213753-787. \PrintBackRefs\CurrentBib

- Karatzas \BBA Sarantsev (\APACyear2016) \APACinsertmetastarKaratzas:Sarantsev{APACrefauthors}Karatzas, I.\BCBT \BBA Sarantsev, A. \APACrefYearMonthDay201606. \BBOQ\APACrefatitleDiverse market models of competing Brownian particles with splits and mergers Diverse market models of competing brownian particles with splits and mergers.\BBCQ \APACjournalVolNumPagesAnn. Appl. Probab.2631329–1361. \PrintBackRefs\CurrentBib

- Karatzas \BBA Shreve (\APACyear1991) \APACinsertmetastarKS1{APACrefauthors}Karatzas, I.\BCBT \BBA Shreve, S\BPBIE. \APACrefYear1991. \APACrefbtitleBrownian Motion and Stochastic Calculus Brownian motion and stochastic calculus (\PrintOrdinalSecond \BEd, \BVOL 113). \APACaddressPublisherSpringer-Verlag, New York. \PrintBackRefs\CurrentBib

- Kim (\APACyear2023) \APACinsertmetastarKim:market-to-book{APACrefauthors}Kim, D. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleMarket-to-book ratio in stochastic portfolio theory Market-to-book ratio in stochastic portfolio theory.\BBCQ \APACjournalVolNumPagesFinance and Stochastics272401-434. \PrintBackRefs\CurrentBib

- Mijatovic (\APACyear2021) \APACinsertmetastarMijatovic{APACrefauthors}Mijatovic, P. \APACrefYearMonthDay2021. \APACrefbtitleBeating the Market with Generalized Generating Portfolios. Beating the market with generalized generating portfolios. \APACrefnotePreprint, arXiv:2101.07084 \PrintBackRefs\CurrentBib

- Pal \BBA Wong (\APACyear2016) \APACinsertmetastarPal:Wong:Geometry{APACrefauthors}Pal, S.\BCBT \BBA Wong, T\BHBIK\BPBIL. \APACrefYearMonthDay2016. \BBOQ\APACrefatitleThe geometry of relative arbitrage The geometry of relative arbitrage.\BBCQ \APACjournalVolNumPagesMathematics and Financial Economics10263-293. \PrintBackRefs\CurrentBib

- Protter (\APACyear2003) \APACinsertmetastarProtter{APACrefauthors}Protter, P\BPBIE. \APACrefYear2003. \APACrefbtitleStochastic Integration and Differential Equations Stochastic integration and differential equations (\PrintOrdinal2nd \BEd). \APACaddressPublisherNew YorkSpringer. \PrintBackRefs\CurrentBib

- Ruf (\APACyear2023) \APACinsertmetastarRuf:Github{APACrefauthors}Ruf, J. \APACrefYearMonthDay2023. \APACrefbtitleEmpirical Finance with Equity Data (Ph.D. Course), LSE. Empirical finance with equity data (Ph.D. course), LSE. \APACrefnoteGithub https://github.com/johruf/CRSP_on_WRDS_introduction \PrintBackRefs\CurrentBib

- Ruf \BBA Xie (\APACyear2019) \APACinsertmetastarRuf:Xie{APACrefauthors}Ruf, J.\BCBT \BBA Xie, K. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleGeneralised Lyapunov Functions and Functionally Generated Trading Strategies Generalised Lyapunov functions and functionally generated trading strategies.\BBCQ \APACjournalVolNumPagesApplied Mathematical Finance264293-327. \PrintBackRefs\CurrentBib

- Ruf \BBA Xie (\APACyear2020) \APACinsertmetastarRuf:Xie:transaction{APACrefauthors}Ruf, J.\BCBT \BBA Xie, K. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleThe Impact of Proportional Transaction Costs on Systematically Generated Portfolios The impact of proportional transaction costs on systematically generated portfolios.\BBCQ \APACjournalVolNumPagesSIAM Journal on Financial Mathematics113881-896. \PrintBackRefs\CurrentBib

- Schied \BOthers. (\APACyear2018) \APACinsertmetastarSchied:2016{APACrefauthors}Schied, A., Speiser, L.\BCBL \BBA Voloshchenko, I. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleModel-Free Portfolio Theory and Its Functional Master Formula Model-free portfolio theory and its functional master formula.\BBCQ \APACjournalVolNumPagesSIAM Journal on Financial Mathematics91074-1101. \PrintBackRefs\CurrentBib

- Shiryaev \BBA Cherny (\APACyear2002) \APACinsertmetastarShiryaev_vector{APACrefauthors}Shiryaev, A\BPBIN.\BCBT \BBA Cherny, A\BPBIS. \APACrefYearMonthDay2002. \BBOQ\APACrefatitleVector stochastic integrals and the Fundamental Theorems of Asset Pricing Vector stochastic integrals and the Fundamental Theorems of Asset Pricing.\BBCQ \APACjournalVolNumPagesProceedings of the Steklov Institute of Mathematics2376–49. \PrintBackRefs\CurrentBib

- Strong (\APACyear2014) \APACinsertmetastarStrong2{APACrefauthors}Strong, W. \APACrefYearMonthDay2014. \BBOQ\APACrefatitleFundamental theorems of asset pricing for piecewise semimartingales of stochastic dimension Fundamental theorems of asset pricing for piecewise semimartingales of stochastic dimension.\BBCQ \APACjournalVolNumPagesFinance and Stochastics183487-514. \PrintBackRefs\CurrentBib

- Wong (\APACyear2015) \APACinsertmetastarWong:Optimization{APACrefauthors}Wong, T\BHBIK\BPBIL. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleOptimization of relative arbitrage Optimization of relative arbitrage.\BBCQ \APACjournalVolNumPagesAnnals of Finance11345-382. \PrintBackRefs\CurrentBib

- Wong (\APACyear2017) \APACinsertmetastarWong:optimaltransport{APACrefauthors}Wong, T\BHBIK\BPBIL. \APACrefYearMonthDay2017. \APACrefbtitleOn portfolios generated by optimal transport. On portfolios generated by optimal transport. \APACrefnotePreprint, arXiv:1709.03169 \PrintBackRefs\CurrentBib

Appendix A Rank based generation of portfolios

Applying the similar method we developed in Section 3, we present in this Appendix generation of trading strategies depending on the ranks of companies, in terms of capitalization. We also study an open market embedded in the entire equity universe of stochastic dimension.

A.1 Rank based generation in the market of stochastic dimension

Let us define the -th ranked components of an -dimensional vector for every :

satisfying

We shall use boldface symbols to denote the vector arranged in a descending order.

Moreover, for any given -valued process , we denote

the -dimensional vector arranged in descending ranks of the dissection and construct the arranged -valued process via dissection

In particular, if is a -valued piecewise semimartingale, then is also a -valued piecewise semimartingale.

We now consider the arranged process of the market weight process of Definition 2.5. Recalling Remark 2.1, we have two dissections and for with the same increments, due to (2.9). However, the former dissection does not reflect the -th ranked component of on -dissection set, as it is reset to zero at by definition (see Figure 1 (d)). Thus, throughout this Appendix, we shall use the latter dissection as an integrator, as every such integral will be considered solely on the -dissection set.

The generating function now takes as an input instead of . On each -dissection set, Itô’s formula gives

In the stochastic integral

we can replace the ranked integrators with the original components using Theorem 2.3 of Ghomrasni \BBA Pamen (\APACyear2010):

| (A.1) |

Here, is the number of components of that are at rank at time :

and we denote , where is the local time accumulated at the origin by a semimartingale up to time :

| (A.2) |

with the notation .

On the right-hand side of (A.1), the expression

| (A.3) |

plays the role of integrand corresponding to the integrator . We use this integrand to define the new -Gamma process

| (A.4) |

and apply (A.1) to derive the alternative representation

| (A.5) |

In what follows, we shall recursively generate trading strategies as in Section 3, by making the vector self-financing. By analogy with (3.8) and (3.9), we set two -dimensional processes , :

| (A.6) | |||||

| (A.7) |

where . For , we define an -dimensional process with components

| (A.8) |

as in (3.15) for each . Here, , , and are defined as in (3.11) - (3.14), with replaced by . Then, the -valued process , constructed from these dissections as in (3.16), is a trading strategy satisfying the self-financing conditions.

Corollary A.1 (Additive generation).

The process is a trading strategy and its relative wealth process is given by

| (A.9) |

for , where the -Gamma process is given in (A.5). Moreover, when the pair belongs to the -dissection set for some , the relative wealth process of (A.9) has an alternative representation as in (3.23) - (3.25), but is replaced by and the Gamma processes take the form of (A.5).

Proof.

We can prove that is a trading strategy in the same manner as in the proof of Proposition 3.1. We now derive as in (3.19) that

holds for each . Plugging (A.1) into the last identity, along with (2.16), yields the result (A.9). The last claim follows from the same argument in the proof of Theorem 3.1. ∎

For the multiplicative generation, we also impose the condition on that the reciprocal is locally bounded on every -dissection set. Let us recall first in (A.7) and set

| (A.10) |

as before. We also consider the multiplicative measurable modification of as in (3.28) with replaced by in the expression of .

Furthermore, we define as in (3.29) based on the new -Gamma process in (A.4), where in the definition is replaced by . We next define two processes and in a recursive manner with

| (A.11) |

similar to (3.31), and

| (A.12) |

as in (3.32) for each . Then, the -valued process constructed as in (3.33) is a rank based multiplicatively generated trading strategy.

Corollary A.2 (Multiplicative generation).

The process is a trading strategy and its relative wealth process is given by

| (A.13) |

for as in (3.34), but with the new Gamma processes of (A.5) in the expression of . Furthermore, the log-relative wealth processes and can be represented as in (3.38) - (3.40), and (3.52), respectively, when belongs to the -dissection set, with instead of and the Gamma processes given in (A.5).

Proof.

Showing that is a trading strategy is again straightforward from the above construction. For the relative wealth process , we derive just like the series of the identities of (3.35), but replacing with and (3.6) with (A.4), to prove on the -dissection set. The last claim also follows from the proof of Theorem 3.2. ∎

Remark A.2.

Similar to (3.45), the component in Corollary A.2 also admits an alternative representation on the -dissection set:

where the new Gamma process (A.5) is used in defining . In particular, if every satisfies the balance condition, then we have a simpler representation

| (A.14) |

as in Corollary 3.1, since we have

from (A.3).

A.2 Open market

The concept of an open market, consisting of a fixed number , but fluctuating constituents of the largest capitalization stocks, has recently been studied in some literature (Campbell \BBA Wong, \APACyear2022; R. Fernholz, \APACyear2018; Itkin \BBA Larsson, \APACyear2021; Karatzas \BBA Kim, \APACyear2021) to construct portfolios in a more realistic market model. In what follows, under some additional assumptions, we shall generate trading strategies in an open market embedded in an entire stock market with a stochastic dimension.