Multi-objective near-optimal necessary conditions

for multi-sectoral planning

Abstract

This paper extends the concepts of epsilon-optimal spaces and necessary conditions for near-optimality from single-objective to multi-objective optimisation. These notions are first presented for single-objective optimisation, and the mathematical formulation is adapted to address the multi-objective framework. Afterwards, we illustrate the newly developed methodology by conducting multi-sectoral planning of the Belgian energy system with an open-source model called EnergyScope TD. The cost and energy invested in the system are used as objectives. Optimal and efficient solutions for these two objectives are computed and analysed. These results are then used to obtain necessary conditions corresponding to the minimum amount of energy from different sets of resources, including endogenous and exogenous resources. This case study highlights the high dependence of Belgium on imported energy while demonstrating that no individual resource is essential on its own.

keywords:

Multi-objective optimisation; near-optimality; necessary conditions; energy system modelling; multi-sectoral planning1 Introduction

Energy system planning determines the appropriate mix of energy sources and technologies to satisfy a community’s or region’s future energy demand. The goal of this process is to inform decision-makers to allow them to plan an efficient and sustainable transformation of energy systems. Energy system optimisation models (ESOMs) are commonly used to perform energy system planning [1]. These models rely on optimisation techniques to predict how an energy system should evolve. However, ESOMS are often used in ways that limit the quality of their insights and, thus, their usefulness to decision-makers. Indeed, these insights are often derived from a unique cost-optimal solution. While cost is a crucial indicator of the affordability and viability of an energy system, focusing solely on this objective might negatively impact other important factors, such as environmental sustainability and social equity. Moreover, these insights might not satisfy stakeholders with diverging interests.

1.1 The cost as leading indicator: limits and solutions

ESOMs determine the energy system configurations that minimise or maximise a specified objective. Most studies choose the cost as the objective, and the best configuration is the most cost-effective [1]. This choice is historical, as explained by Pfenninger et al. [2]. Indeed, the first ESOMs (from the MARKAL/TIMES [3] and MESSAGE [4] models) were initially designed for cost minimisation. The study of Yue et al. [5] highlights that by default, ESOMs ignore non-economic factors entering into energy investment decisions and how politics, social norms, and culture shape public policies. This claim is also supported by Pfenninger et al. [2], who specifies that energy system models focus heavily on economic and technical aspects. This focus is inadequate for energy system planning as this problem involves multiple stakeholders with different policy objectives, for whom cost-optimal solutions might not be satisfying. Moreover, several studies have demonstrated that ignoring non-economic factors increases the uncertainty of the models [2, 5]. Fazlollahi et al. [6] also states that, due to uncertainty in some parameters, it is insufficient for energy system sizing to rivet on a unique mono-objective optimal solution. Finally, Trutnevyte [7] shows how cost-optimal scenarios do not adequately represent real-world problems. However, there exist methods for going beyond cost and considering non-economic factors.

1.1.1 Scenario analysis

The first approach to incorporate non-economic factors is scenario analysis. Scenario analysis involves optimising the same model over multiple scenarios with different values for some parameters. Differences between scenarios can result from uncertainties over technological or economic parameters - e.g. future cost of technology. However, they can also stem from political (e.g. nuclear decommissioning) or social considerations (e.g. limitation of onshore wind turbines or transmission lines development). Using scenarios that differ through those considerations allows for studying the effects of non-economic factors. For instance, the study by Fujino et al. [8] compares a fast-growth, technology-oriented scenario to a slow-growth, nature-oriented one. However, using scenarios to include non-economic factors is not perfect. Indeed, Hughes and Strachan [9] reviewed studies using scenarios for low greenhouse gases (GHG) emission targets, and they conclude that those modelling studies still have the weakness of simplifying social and political dynamics.

1.1.2 Multi-objective optimisation

The second approach to include non-economic factors is multi-objective optimisation. This approach allows for optimising several objectives simultaneously, highlighting the trade-offs that can be obtained.

More formally, while different methods exist to apply multi-objective optimisation (e.g. weighted-sum approach, integer cut constraints, -constraint method, evolutionary algorithm), they exhibit the common goal of obtaining solutions from a Pareto optimal set, also called the Pareto front. This Pareto front is composed of efficient solutions, i.e. solutions that are at least better than any other solutions in one objective. Thus, it is composed of the set of optimal trade-offs between the studied objectives, i.e. any solution that is not part of the Pareto front is worse in all objectives than at least one solution in the Pareto front.

Using multi-objective optimisation, the cost can still be optimised while considering other indicators. For instance, Becerra-López and Golding [10] conducted a study of a Texas power generation system analysing the trade-offs between economic and exergetic costs, i.e. the cumulative exergy - entropy-free energy - consumption. They demonstrated how these trade-offs provide insights to the decision-makers by not focusing exclusively on economic cost. Other objectives, such as water consumption, grid dependence on imports or energy system safety, are compared to cost by Fonseca et al. [11, 12]. They show how much the assessed criteria impact the design and operation of distributed energy systems. A final example of an alternative objective that is often combined with the cost is the amount of carbon emissions [13].

1.1.3 Near-optimal spaces analysis

The last methodology that allows taking social and political factors into account is the study of near-optimal spaces, also called sub-optimal or epsilon-optimal spaces. The idea is to analyse solutions close to the optimal solution to understand how the use of resources and technologies varies when allowing a slight deviation in the objective function. This paradigm goes further than multi-objective optimisation, as mentioned by DeCarolis [14]. It allows incorporating unmodelled objectives, typical of social factors, as they are unknown or difficult to model. Indeed, the near-optimal region might contain solutions that are worse in terms of the main objective - e.g. the cost of the system - but better in terms of unmodelled objectives such as risk or social acceptance. This concept was introduced in the 1980s by Brill et al. [15]. The authors proposed the first method for exploring those spaces: the Hop-Skip-Jump method. This algorithm was coined as part of a broader exploration methodology that the authors refer to as Modelling to Generate Alternatives (MGA). This methodology was brought back recently and applied to energy system modelling by DeCarolis [14] and DeCarolis et al. [16]. They led to a renewed interest in such methods. Authors such as Price and Keppo [17] developed new exploration algorithms while Li and Trutnevyte [18] combined MGA with Monte-Carlo exploration to minimise parametric uncertainty.

There are several ways of extracting insights from near-optimal spaces. Most researchers exploring near-optimal spaces focus on computing numerous near-optimal solutions from which they derive insights [17, 18, 19]. An alternative approach is to use methods to obtain such insights directly without needing to compute many alternative solutions [20]. The authors of Dubois and Ernst [21] took this approach by introducing the concept of necessary conditions for near-optimality, i.e. conditions that are true for every solution in the near-optimal space. For instance, this can provide insight into the required capacity in a given technology to retain a certain level of system cost-effectiveness. More specifically, Dubois and Ernst [21] showed how, for instance, at least 200 GW of new offshore wind need to be installed Europe-wise to not deviate by more than 10% from the cost optimum.

1.2 Research gaps, scientific contributions and organisation

The exploration of near-optimal spaces has been used in mono-objective optimisation problems but not, according to the best knowledge of the authors, in multi-objective optimisation problems. However, these methods could also be valuable in multi-objective optimisation setups. Indeed, while modelling and integrating more objectives, multi-objective optimisation still leaves aside some unmodeled objectives. Analysing solutions in the near-optimal space of multi-objective optimisation problems is a method to address this issue. This paper thus aims to fill this gap by:

-

1.

extending the concepts related to near-optimal spaces to multi-objective optimisation;

-

2.

computing necessary conditions in a multi-objective context to highlight the range of insights that can be derived from them.

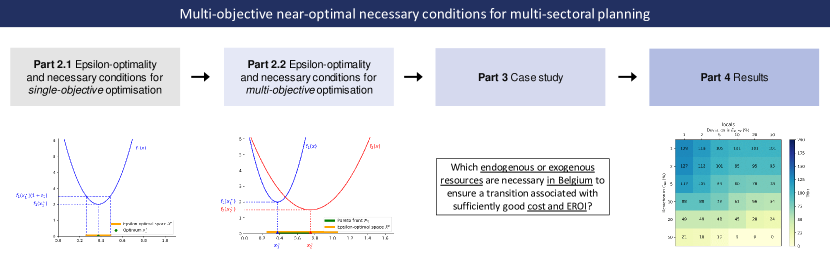

The first point is addressed in Section 2 by first introducing the mathematical concepts of near-optimality and necessary conditions in a single-objective framework (see Section 2.1) and then extending them to multi-objective optimisation (see Section 2.2). Section 3 then translates those concepts to a real case study: the multi-sectoral expansion of the Belgian energy system. The results of this case study, including necessary conditions representing the necessary amount of different energy resources, are presented in Section 4 before highlighting the contributions of this paper in Section 5. We can already highlight one of those contributions: the open-source release of the code [22] and the data [23] used to achieve this study. The graphical representation of the organisation of this paper is depicted in Figure 1.

2 Problem statement

The first part of this section introduces the concepts of epsilon-optimal space and necessary conditions for single-objective optimisation [21]. The second part extends these concepts to multi-objective optimisation by:

-

1.

generalising the optimisation problem to multiple objectives,

-

2.

presenting generic notions related to multi-objective optimisation, including the image of the feasible set, efficient solutions, and the Pareto front, and

-

3.

explaining the extension of the concepts of epsilon-optimality and necessary conditions to multi-objective optimisation.

2.1 Epsilon-optimality and necessary conditions for single-objective optimisation

Let be a feasible space and an objective function in the positive reals. The single-objective optimisation problem is

| (1) |

Let denote an optimal solution to this problem that is: .

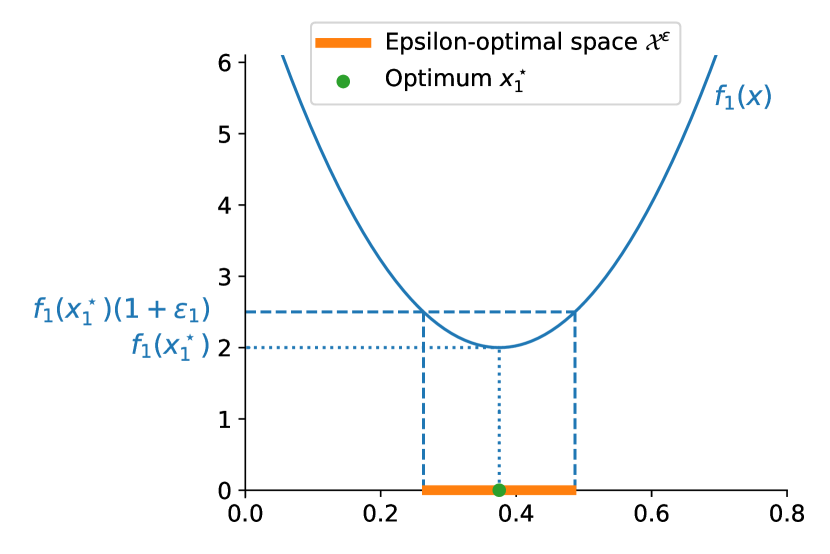

Definition 1.

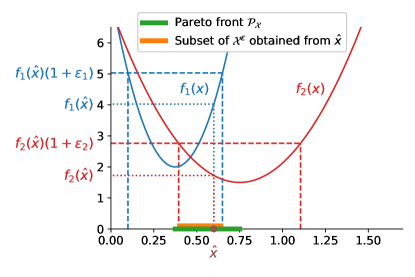

An -optimal space, with , is defined as follows

| (2) |

It is the set of the feasible solutions with objective value no greater than . The deviation from the optimal objective value is measured via , called the suboptimality coefficient. Figure 2 illustrates those concepts.

A note must be made on the specific case . In this case, resumes to , making the analysis of near-optimal spaces trivial.

2.1.1 Necessary conditions

The concepts of condition, necessary condition and non-implied necessary condition introduced in this section allow determining features which are common to all solutions in a given -optimal space.

Definition 2.

A condition is a function . A set of conditions is denoted .

We illustrate this definition and the following using an example. Let , can be the set of conditions of the form with (thus and .

Definition 3.

A necessary condition for -optimality is a condition which is true for any solutions in .

For a given feasible space , set of conditions and suboptimality coefficient , is a necessary condition if

The set of all necessary conditions for -optimality in is denoted .

In our example, let , then is respected by all , making a necessary condition. Moreover, the set of all necessary conditions is . Indeed, it is straightforward to show that is true over for any .

As shown in Dubois and Ernst [21], necessary conditions can provide insights into features common to many near-optimal solutions. However, depending on how conditions are defined, their study also claims the number of necessary conditions can be infinite, which is counterproductive in providing insights. This is, for instance, the case in our previous example. Indeed, the set contains an infinite number of necessary conditions. Nevertheless, the only condition of interest is . Indeed, knowing that is true over implies that is true when . Thus, knowing that is a necessary condition implies that any with is a necessary condition. On the opposite, it is not possible to imply that is a necessary condition from the knowledge of other necessary conditions in the set . This defines as a non-implied necessary condition. Knowing this, we can provide the first definition of non-implied necessary conditions.

Definition 4.

A condition is a non-implied necessary condition if it cannot be implied to be a necessary condition from the sole knowledge of other necessary conditions. The set of non-implied necessary conditions is denoted .

This definition can be made more formal. In the following, we formalise it mathematically, starting with the notion of implication.

Definition 5.

An implication function is a function that indicates whether condition implies condition . When , then . When , then .

Using this function, a non-implied necessary condition can be defined in the following way.

Definition 6.

A non-implied necessary condition is a necessary condition that is not implied by any other necessary condition. It is a necessary condition such that .

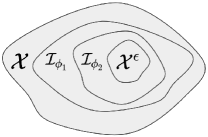

We can refine the definitions of necessary and non-implied necessary conditions by defining the space over which a condition is true.

Definition 7.

The space is the subset of where a condition is true, that is:

| (3) |

Necessary conditions can then be defined in the following way.

Definition 8.

A condition is a necessary condition for -optimality if .

Indeed, this implies that , which corresponds to definition 3. Using this same notion, we can give an implementation of the implication function.

Definition 9.

Let and be conditions with and the spaces over which they are respectively true, then the implication function is defined as:

| (4) |

This formulation fits our definition of an implication function because if , then it means , which in turns implies that for any for which . Similarly, if , it means that , which means such that when . This definition of implication leads to a new definition of non-implied necessary conditions.

Definition 10.

A non-implied necessary condition is a necessary condition that is true over a space which does not include any of the spaces over which other necessary conditions are true. It is a necessary condition such that .

Figure 3 illustrates these concepts, where implies as . They are both necessary conditions because they are true over . Finally, if there are no other conditions in the set of conditions , then is a non-implied necessary condition as no other necessary condition implies it.

2.1.2 Computation of a non-implied necessary condition

This section presents an example to provide a practical sense of these concepts. It demonstrates how to compute a non-implied necessary condition from a set of conditions taking the form of constrained sums of variables. In the case studies described in Section 3, this type of condition is used to study the minimum amount of energy that can be driven from different sources.

Let be a feasible space, an objective function to minimise over this space, and a set of conditions defined as follows:

| (5) |

where , and . The conditions are constrained sums of variables . In this particular case, Dubois and Ernst [21] have proven that with is the only non-implied necessary condition that can be derived from . The value represents the minimum value that can take over the set , that is when allowing a deviation of from the optimal value . Algorithm 1 illustrates the computation of this value in three steps.

-

1.

Solve to obtain .

-

2.

Build by adding to the original problem the constraint .

-

3.

Solve .

2.2 Epsilon-optimality and necessary conditions for multi-objective optimisation

This section extends the concepts presented previously to multi-objective optimisation while introducing notions specific to this type of optimisation problem.

Let be a vector of objective functions such that . We seek to minimise these functions over the feasible set , which, using the notation of Ehrgott [24], we note:

| (6) |

Let be the image of the feasible set in the objective space:

| (7) |

This space is the image of under the objective functions , and . Therefore, and each of its components are defined by for some .

2.2.1 Efficient solutions and Pareto front

One way to highlight compromises between the objectives () is to compute efficient or Pareto optimal solutions. Following the definition of Ehrgott [24]:

Definition 11.

A feasible solution is called efficient when there is no other such that and for some , that is, no other has a smaller or equal value in all objectives than .

According to Ehrgott [24], multiple denominations exist for the set of efficient points. This paper uses the term Pareto front to indiscriminately name the set of efficient points or their image in the objective space.

Definition 12.

A Pareto front is the set

| (8) | ||||

In the objective space, a Pareto front is defined as:

| (9) | ||||

2.2.2 Approximation of Pareto fronts

A Pareto front can be composed of an infinity of points. Thus, it is typical to compute a subset of the efficient solutions which compose it. This set is named approximated Pareto front and is denoted by (or equivalently ) where is the number of points in the approximation.

Definition 13.

An approximate Pareto front , with , is a subset of efficient solutions in the Pareto front .

Several techniques exist to obtain those efficient solutions, the two most famous being the ‘weighted-sum approach’ and the ‘-constraint method’ [24]. The weighted-sum approach consists of solving:

| (10) |

with . The -constraint method resolves in solving:

| (11) |

where .

2.2.3 Multi-criteria epsilon-optimal spaces

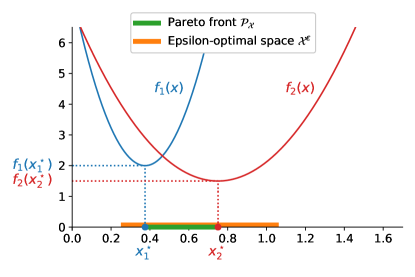

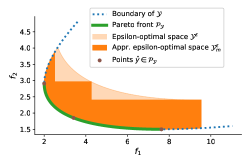

Starting from a Pareto front , it is possible to define an -optimal space, given a suboptimality coefficients vector of deviations in each objective: . This space is denoted by in the decision space and in the objective space.

In the mono-objective setup, the -optimal space is defined as the set of points whose objective value do not deviate by more than an fraction from the optimal objective value, i.e. . In a multi-objective case, there is no optimum but a set of efficient points composing the Pareto front. This leads us to define the -optimal space as follows:

Definition 14.

In a multi-objective optimisation problem, the -optimal space , with , is the set of points whose objective values for each do not deviate by more than an fraction from the objective value of at least one solution of the Pareto front .

It is the space

| (12) |

Alternatively, this space can be defined as:

| (13) |

Figure 4 depicts a graphical representation of an -optimal space in a multi-objective framework and how it is built from efficient solutions.

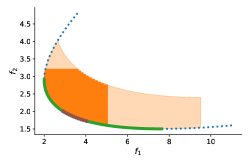

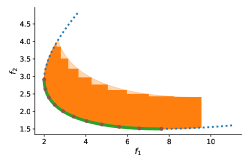

Definition (12) relies on the entire Pareto front. However, practically, only a subset of efficient points of the Pareto front is computed and used to obtain an approximation of the -optimal space, denoted .

Definition 15.

An approximation , with , of an -optimal space is the space

| (14) |

Alternatively, this space can be defined as:

| (15) |

The alternative formulation defines as a union of spaces, where each space is the set of points whose objective value in each does not deviate by more than an fraction from the objective values of one solution in the approximated Pareto front .

Figure 5 shows three examples of approximate -optimal spaces in the objective space (therefore noted ) using three approximated Pareto fronts , with different numbers and spread of efficient solutions.

2.2.4 Necessary conditions

In the multi-objective optimisation framework, necessary conditions for -optimality can be defined in the same manner as in the one-dimensional setting, i.e. conditions which are true for any solutions in .

Definition 16.

A necessary condition for -optimality is a condition which is true for any solutions in . Let be a feasible space, a set of conditions, and a suboptimality coefficients vector, a necessary condition is a condition such that

The set of all necessary conditions for -optimality in is denoted .

Similarly, a non-implied necessary conditions -optimality can be defined in the following way.

Definition 17.

A non-implied necessary condition is a necessary condition that is not implied by any other necessary condition. It is a necessary condition such that .

2.2.5 Computation of a non-implied necessary condition

The computation of a non-implied necessary condition from conditions of type presented in Section 2.1.2 is generalised to the multi-criteria case. In the mono-objective case, it was sufficient to minimise the sum over to obtain the value corresponding to the non-implied necessary condition . However, in a multi-objective setup, we do not have access to but to its approximation , which is the union of several subsets, each corresponding to one point in (i.e. a subset of the Pareto front). The minimum over this space can thus be obtained by taking the minimum of the minima of over each of these subsets. Even with this approach, being a subset of , minimising over it will only provide an upper bound of the value , i.e. . Algorithm 2 shows how this value can be obtained.

-

1.

Draw points of the Pareto front using an appropriate method.

-

2.

For all , compute over the space .

-

3.

Take the minimum of these values to find the appropriate condition .

There is no guarantee that the condition is a (non-implied) necessary condition. Indeed, it could be the case that for a solution that . To make the upper bound as close as possible to the real minimal value , one must reduce the size of the difference . This can be done by improving the number and spread of efficient solutions in the approximated Pareto front. As defined by Alarcon-Rodriguez et al. [25], solutions with a good spread can be seen as having good coverage of the actual Pareto front. The three graphs of Figure 5 show visually how, by increasing the number and the spread of efficient solutions drawn from the Pareto front, the approximated -optimal space covers a more significant subset of the points of the entire -optimal space.

3 Case study

In this section, a case study will illustrate the concepts and methodology presented in the previous section. First, the context of the case study and the question to which it tries to provide an answer are presented. The modelling tool used to implement the methodology is then introduced, and its main features are detailed. Finally, each element introduced in Section 2 is specified to the problem at hand.

3.1 Context

In the European Green Deal [26], the European Commission raided the European Union’s ambition to reduce GHG emissions to at least 55% below 1990 levels by 2030.

Then by 2050, Europe aims to become the world’s first carbon-neutral continent.

Europe still relies massively on fossil fuels to satisfy its energy consumption ( 75% coming from coal, natural gas and oil according to the International Energy Agency [27]) as well as non-energy usages (e.g. chemical feed-stocks, lubricants and asphalt for road construction [28]).

The use of these fuels is the primary source of GHG emissions.

Carbon-neutral sources of energy must thus be developed to curb emissions.

The possibilities are numerous, and one of the coming decade’s main challenges will be deciding which resources to invest in.

Several criteria will motivate these choices.

The most common criterion for discriminating between options is cost. Indeed, as highlighted by Pfenninger et al. [2] and DeCarolis [14], most studies use the cost indicator to plan the energy transition. This choice makes sense as the cost of investment, maintenance and operation of the energy system impacts the final consumers’ energy bill. Thus, minimising the system cost is a social imperative to allow every citizen access to affordable energy.

A lesser-known indicator, encompassing technical and social challenges, is the system’s energy return on investment (EROI). When defined system-wise, the EROI is a ratio that measures the usable energy delivered by the system () over the amount of energy required to obtain this energy () [29]. When the amount of energy required to deliver a given energy service increases, the EROI of the system decreases. In some sense, EROI measures the ease with which energy is extracted to transform it into a form that benefits society. There are various manners of defining and , and incidentally, the EROI of a system. These definitions depend mainly on what parts of the energy cascade - as presented in Brockway et al. [30] or Dumas et al. [31] - are considered. This paper considers that invested energy encompasses the energy used to build the system infrastructure, ‘from the cradle to the grave’, and to operate this system. Following the methodology of Dumas et al. [31], will correspond to the final energy consumption (FEC) of the system, as defined in the European Commission [32] standard. FEC is the total energy, measured in TWh, consumed by end-users. It encompasses the energy directly used by the consumer and excludes the energy used by the energy sector, e.g. deliveries and transformation.

While cost and EROI can be linked (e.g. the transport of energy resources will increase both the system cost and invested energy), they are not fully correlated and favouring one or the other can lead to different system configurations, as illustrated later in Section 4. Both criteria can be included in the decision process by modelling them as objectives in optimisation problems. These objectives can be optimised individually or co-optimised using multi-criteria optimisation techniques. In this case study, we will show how, using these objectives in the methodology presented in Section 2, the following question can be addressed:

Which resources are necessary to ensure a transition associated with sufficiently good cost and EROI?

Indeed, the answer to this question can be obtained by computing necessary conditions corresponding to the minimum amount of energy that needs to come from these resources.

This question is, however, relatively broad, and for the sake of conciseness, it needs to be specified. On top of decision criteria, considerations such as energy independence (i.e. which has been enhanced with the Russian invasion of Ukraine) and social acceptance (i.e. the ‘not-in-my-backyard’ phenomena) are paramount in planning the energy transition. These considerations will impact the type of resources that will be exploited. Indeed, the first consideration incentives a push for domestically produced energy, while the latter favours the opposite. The first tends to minimise the amount of exogenous resources in the system, while the latter minimises the amount of energy coming from endogenous resources. To take these elements into consideration, the previous question can be refined to:

Which endogenous or exogenous resources are necessary to ensure a transition associated with sufficiently good cost and EROI?

This study focuses on one of the European countries: Belgium. Belgium made the same commitments for 2030 and 2050 as the European Union [33]. Thus, it faces the challenge of replacing its fossil-based economy with carbon-free solutions while striking the right balance between endogenous and exogenous resources. Belgium’s population density exacerbates this challenge. In 2019, Belgium had the second-highest population density in Europe (excluding Malta) with 377 people per km2, behind the Netherlands (507 people per km2) [34]. The available land for onshore energy development is thus limited, while offshore production is limited to around 8 GW of wind potential [35]. Other domestic resources such as solar, biomass, waste or hydro also have limited potential. This situation entails a small local energy potential compared to its demand. The study Limpens et al. [36] evaluates that available local Belgian resources can only cover 42% of the country’s primary energy consumption. This situation strongly impacts the type of resources Belgium must rely on. Therefore, the question that will be addressed in this case study is:

Which endogenous or exogenous resources are necessary in Belgium to ensure a transition associated with sufficiently good cost and EROI?

3.2 EnergyScope TD

To answer this question, an appropriate ESOM is needed. The commitments set for 2035 and 2050 cover all sectors of the economy, not just electricity production. To achieve net zero ambitions, carbon-neutral solutions must be implemented for electricity, heat, mobility, and non-energy. These different sectors can be modelled using an open-source whole-energy system model called EnergyScope TD (ESTD) [37]. ESTD can be categorised as an ESOM. Using optimisation techniques, it determines the optimal mix of technologies (e.g. wind turbines, gas power plants, boilers, etc.) and resources (e.g. wind, gas, diesel, etc.) which are needed to satisfy different types of end-use demand (EUD) listed in B. This optimal mix depends on the user-defined objective function. Mathematically, ESTD models the energy system as a linear programming problem. It takes a series of parameters as input and outputs the values of investment and operational variables determined by minimising an objective while respecting a series of constraints. The objective is a linear function; constraints are linear equalities or inequalities. Parameters and variables can be indexed temporally. The default temporal horizon is one year with an hourly resolution. To reduce the computational burden of the optimisation, the horizon is clustered by selecting a number of typical days, 12 by default. Thus, time-dependent parameters and variables are indexed by a typical day and an hour . The equivalence between the original hourly-resolution temporal horizon and the typical days is done via a time-indexed set associating each hour of the year with a corresponding couple . This set is essential to understand some of the equations in the rest of this section.

ESTD has been extensively used and validated in the Belgian case [31, 36, 38, 39, 40, 41]. More specifically, in Limpens et al. [36], the authors studied the 2035 Belgian energy system using ESTD and built the corresponding data set. This year is a trade-off between a long-term horizon where policies can still be implemented and a horizon short enough to define the future of society with a group of known technologies. To build on these resources, we will model the Belgian energy system for 2035.

To finish this section, it is important to note that while the results presented in this paper are valid for Belgium, they could easily be extended to other countries. Indeed, ESTD has already been used to model the energy systems of other countries such as Switzerland [42, 43] and Italy [44]. Moreover, adapting those models to implement the methodology presented in this paper only requires minor modifications, as presented in the following sections.

3.3 Feasible space

In the initial optimisation problem

| (16) |

the first element to define is the feasible space over which the optimisation is performed. This study modelled the feasible space using ESTD as a linear programming problem. Therefore, the problem to solve has the following form:

| (17) | ||||

where is the vector of variables of the problem, while and are a matrix and vector of parameters, respectively. More information on the specific variables, parameters and constraints used in ESTD can be found in Limpens et al. [37] and in the model’s documentation [45].

3.3.1 Constraint on GHG emissions

A constraint that is of particular interest given the context of this case study is the limit on GHG emissions, i.e.

| (18) |

In this section, we briefly describe how this constraint is defined. The total yearly GHG emissions of the system are computed using a life-cycle analysis (LCA) approach. Thus, they include the GHG emissions along the whole life cycle, i.e. ‘from the cradle to the grave’ of the technologies and resources considered in ESTD. In ESTD, the global warming potential (GWP) expressed in Mt-eq./year is used as an indicator to aggregate emissions of different GHG. Then, the yearly emissions of the system, which are denoted , are defined as follows:

| (19) |

where and are the sets of technologies and resources modelled in ESTD. represents the GWP for the construction of a technology, while gives the GWP linked to the operation of a resource. More specifically, is the GWP of technology over its entire lifetime allocated to one year based on the technology lifetime . is the GWP related to the use of resource over one year.

The 35 Mt-eq/y limit chosen in this case study comes from the following reasoning. According to the International Energy Agency (IEA), Belgium’s 1990 territorial GHG emissions were approximately 105 Mt-eq [27]. Thus, the targets of the European Green Deal imply reaching 47 Mt-eq/y in 2030 and 0 Mt-eq/y in 2050111Practically, the 2050 target is to be climate neutral, meaning the GHG emission can be greater than 0 but must be compensated by carbon capture.. By conducting a linear interpolation between these dates, the 2035 Belgian GHG emissions should reach approximately 35 Mt-eq/y. This target is used as a hard constraint for in the model: [Mt-eq/y].

3.4 Objectives

The second step in formalising the problem consists in choosing appropriate objectives. As mentioned at the start of this section, our interest lies in solutions with a sufficiently good cost and EROI. This choice implies optimising the system by minimising cost and maximising EROI. To better match the methodology presented in Section 2 where functions are minimised, (i.e. the energy invested in the system) will be used as objective instead of EROI. The following sections define precisely the two objectives used in the case study.

3.4.1 System cost

The first objective is the total annual cost of the system, , defined as:

| (20) |

The yearly system cost is the sum of , the annualised investment cost of each technology with the total investment cost and the annualisation factor, , the operating and maintenance cost of each technology and , the operating cost of the resources. This last variable is equal to

| (21) |

where is the cost of resource in [€/MWh] and corresponds to the use in [MWh] of resource at time . The values of for each resource used in the study case are given in Tables 1 and 2. The study of Limpens et al. [37] or the online documentation [45] provides more detail on this indicator.222In the mathematical formulation of the model, an additional factor is added to equation (21), (23), and (27). This parameter is set to 1 in the implementation of the model used in this case study. It is thus removed from equations for clarity.

3.4.2 Energy invested in the system

The second objective is , the energy invested in the system over one year:

| (22) |

with , the energy invested to built technology , annualised by dividing it by its lifetime, and the energy to operate, i.e. produce, and transport resource over one year. Similarly to the cost indicator, this last variable is equal to

| (23) |

where is the energy invested (in [MWh/MWh]) to obtain 1 MWh of the resource . The values of for each resource used in the study case are given in Tables 1 and 2. More detail is provided by Dumas et al. [31] (in which is referred to as ).

Minimising would be equivalent to maximising EROI, i.e. , if , which in our case is the FEC, was constant. It is not the case in ESTD. In this model, only the values for the EUD, presented in Table 5, are fixed. While EUD measures an energy service, FEC measures the quantity of energy used to deliver this service. FEC is thus always measured in [TWh], while the unit for EUD will depend on the demand. For instance, the EUD for heat will be measured in [TWh] while [Mt-km] will be used for mobility. Using technology-dependent conversion factors, FEC can be converted into EUD and vice-versa. For instance, in ESTD, a FEC of 1 kWh of electricity supplies an EUD of 5.8 passenger-km with a battery-electric car. As the conversion factors depend on the installed technologies, which depend on the optimisation results, FEC is an output of the ESTD model and is not constant. Nonetheless, the constant EUD cannot be employed directly as to compute the EROI, as it is an energy service, not an amount of energy. Therefore, the FEC is used to compute and, incidentally, the EROI of the system.

3.5 Pareto front

Once all the elements of the initial optimisation problem (6) are set up, one can compute efficient solutions from the Pareto front using one of the methods described in Section 2.2.2. This case study uses a modified version of the -constraint method. It is applied by minimising over the feasible space with the additional constraint where and is the cost-optimal value, i.e. solving

| (24) |

This method is a slight modification of the method described in equation (11) where is a relative rather than absolute value. It has the benefit of defining the constraint proportionally to the optimal value in the associated objective and thus be directly interpretable. For instance, if the optimal cost is 75 B€, one would use values of 1, 5, and 10% instead of absolute values of 75.75, 78.75 and 82.5 B€. To obtain several points over the Pareto front, the method was repeated for different values of in where is the value of at the optimum and is the cost optimum.

3.6 Near-optimal spaces

The efficient solutions are used to define approximate near-optimal spaces , with following equation (15) of definition 15. They are unions of spaces defined around unique, efficient solutions, . Each space can be easily defined by adding to the original ESTD model the two linear constraints, which are:

| (25) | |||

| (26) |

| [€/MWh] | [MWh/MWh] | |

| Endogenous resources | ||

| Hydro | 0 | 0 |

| Solar | 0 | 0 |

| Waste | 23.1 | 0.0577 |

| Wet biomass | 5.76 | 0.0559 |

| Wind | 0 | 0 |

| Wood | 32.8 | 0.0491 |

| Exogenous resources | ||

| Ammonia | 76.0 | |

| Ammonia (Re.) | 81.8 | |

| Diesel | 79.7 | 0.210 |

| Bio-diesel | 120 | |

| Elec. import | 84.3 | 0.123 |

| Gas | 44.3 | 0.0608 |

| Gas (Re.) | 118 | |

| Gasoline | 82.4 | 0.281 |

| Bio-ethanol | 111 | |

| H2 | 87.5 | 0.083 |

| H2 (Re.) | 119 | |

| LFO | 60.2 | 0.204 |

| Methanol | 82.0 | 0.0798 |

| Methanol (Re.) | 111 | |

| [€/MWh] | [MWh/MWh] | |

|---|---|---|

| Hydro | 53.7 | 0.0489 |

| Solar | 50.0 | 0.147 |

| Wind | 47.0 | 0.0350 |

3.7 Necessary conditions

The last concept to define is the type of necessary conditions computed in the case study. We are interested in the necessary resources for a transition with a sufficiently good cost and EROI. We will thus compute the necessary conditions corresponding to the minimum amount of energy that needs to come from a specific individual or group of resources. Mathematically, the set of such conditions would be:

| (27) |

where is a set of resources, the use of resource at time and . can contain any resource. However, in the context presented in Section 3.1, we have highlighted a particular interest in two groups of resources: endogenous and exogenous. We will focus primarily on those two sets and give a more detailed description of their resources. In ESTD, endogenous resources (noted ) include wood, wet biomass, waste, wind, solar, hydro, and geothermal energy. Exogenous resources (noted ) are the other resources in the model: ammonia, renewable ammonia, imported electricity, methanol, renewable methanol, hydrogen, renewable hydrogen, coal, gas, renewable gas, liquid fuel oil, gasoline, diesel, bio-diesel, and bioethanol. Renewable fuels such as renewable ammonia, methanol, and gas are assumed to be produced from renewable electricity. Tables 1 and 2 list the model’s resources and the associated input parameters required to compute the cost and invested energy when employing them.

4 Results

In this section, we provide the answer to the question that was asked at the beginning of Section 3:

Which endogenous or exogenous resources are necessary in Belgium to ensure a transition associated with sufficiently good cost and EROI?

This answer is obtained by computing necessary conditions corresponding to the minimum amount of energy coming from specific resources required to ensure a -optimality in and . However, before diving into the necessary conditions, we first analyse how the system is configured at the two optimums and show the differences between those configurations. Then, by analysing efficient solutions, we determine how this system evolves when trade-offs are made between and . Finally, knowing the Pareto front, we compute -optimal spaces and examine necessary conditions corresponding to the minimum amount of energy coming from different resources in Belgium.

4.1 Analysis of the system configuration at the two optimums

The Belgian energy system is analysed when optimising and individually, with a maximum carbon budget of 35 Mt-eq/y. To set a baseline to which we can compare the necessary conditions computed in the following sections, we analyse the amount of endogenous and exogenous resources used at each optimum. Table 3 shows the value of the two objective functions at the two optimums, and Table 4 details which energy sources are used in the system.

| optimum | optimum | |

|---|---|---|

| [B€ /y] | 52.8 | 56.8 |

| [TWh/y] | 74.0 | 61.0 |

| Energy | Max. | ||

|---|---|---|---|

| optimum | optimum | potential | |

| Endogenous | 185 | 164 | 185 |

| Hydro | 0.469 | 0.486 | |

| Solar | 61.5 | 54.2 | |

| Waste | 17.8 | 4.12 | 17.8 |

| Wet Biomass | 38.9 | 38.9 | 38.9 |

| Wind | 42.6 | 43.0 | |

| Wood | 23.4 | 23.4 | 23.4 |

| Exogenous | 202 | 211 | / |

| Ammonia (Re.) | 65.6 | 0 | / |

| Bio-diesel | 0 | 3.14 | / |

| Elec. import | 27.6 | 27.6 | 27.6 |

| Gas | 28.2 | 34.5 | / |

| Gas (Re.) | 4.98 | 48.5 | / |

| H2 (Re.) | 19.4 | 44.8 | / |

| Methanol (Re.) | 56.4 | 52.8 | / |

| Total | 387 | 375 | / |

4.1.1 Results at the optimum

The optimal cost is equal to 52.8 B€ /y. At this optimum, the total amount of primary energy used in the system is 387 TWh/y, 48% of which comes from endogenous resources and the rest from exogenous resources.

For endogenous resources, the values for wet biomass, waste and wood are equal to their maximum potentials - set as input model parameters. This observation makes sense as the of these resources in Table 1 indicate they are among the cheapest resources. The hydro, solar and wind energy quantities are also very close to their maximum potential. For these resources, the maximum is not set directly on the quantity of energy but on the capacities of the technologies using these resources. For instance, the model can install a maximum of 6 GW of offshore wind turbines and 10 GW of onshore wind turbines, which are the two technologies using wind as a resource. These maximum capacities can then be multiplied by the capacity factors of the corresponding technologies to obtain a maximum energy potential. Moreover, these resources are considered free in terms of cost and invested energy, as shown in Table 1. The cost of using them arises from the technologies to extract them from the environment. Table 2 shows approximated values for and . They are computed by dividing the cost or energy invested for building and maintaining the technologies using them by the total energy used from these resources - shown in Table 4. These approximated values show that hydro, solar and wind are among the cheapest resources, which explains their extensive use.

The model has no maximum potential for exogenous resources except for imported electricity. This potential is reached as, even though is relatively high for imported electricity, it does not require any conversion technology to produce the final electricity demand. Some 65.6 TWh/y of renewable ammonia is used in the system, 55.4 TWh/y of which is used for electricity production and low-temperature heat generation, while the remaining 10.2 TWh/y is used to satisfy non-energy demand. Most renewable methanol is used to produce high-value chemicals, even though 3.6 TWh/y of this resource is used for fuelling boat freight. Finally, gas (renewable or not) is used to produce heat and electricity and fuel buses for public mobility.

4.1.2 Results at the optimum

The optimal energy invested amounts to 61 TWh/y. Among the 375 TWh/y of primary energy in the system, 164 TWh/y (44%) come from endogenous resources and 211 TWh/y (56%) from exogenous resources. A series of resources, including wet biomass, wood, wind, hydro and imported electricity, are used at or near their maximum potential. This is not the case for waste and solar. In particular, for solar, is about three times higher than any other endogenous resource. This result can be explained by the higher energy needed to build 1 GW of PV combined with a low average capacity factor compared to hydro river plants or wind turbines. Some electricity is produced using natural and renewable gas, while ammonia for non-energy demand is produced from H2 using the Haber-Bosch process. The remaining amount of gas is used to produce heat. Finally, high-value chemicals are produced using renewable methanol, while 3.14 TWh/y of bio-diesel is used for boat freight.

4.1.3 Comparison

Table 3 shows how the two objective functions vary from one optimum to the other. The increase in cost when optimising is limited to 7.67%. Invested energy at the optimum is around 74 TWh/y, representing an increase of more than 20% from the optimal value.

As shown in Table 4, the total amount of energy needed in the system differs only by 3%, but there are some differences between the two energy mixes. At the optimum, the energy coming from endogenous resources is 21 TWh/y higher, while energy from exogenous resources is 9 TWh/y smaller. At each optimum, the share of endogenous resources in the energy mix (48% and 44%, respectively) is close to the maximum of 42% primary energy coming from endogenous resources computed by Limpens et al. [36]. These values confirm the substantial dependence of Belgium on imported resources to supply its energy consumption.

Looking at individual resources, solar and renewable ammonia, used to produce electricity when optimising , are replaced by fossil and renewable gas at the optimum. At this optimum, a percentage of the total 80 TWh/y of gas is used to produce high-temperature heat instead of waste. The additional 35.4 TWh/y of renewable hydrogen is used for three things: ammonia production (which was directly imported when optimising cost), combined heat and electricity production, and public mobility. Finally, while boat freight is fuelled using renewable methanol at the optimum, bio-diesel is the preferred option at the optimum.

4.2 Pareto Front

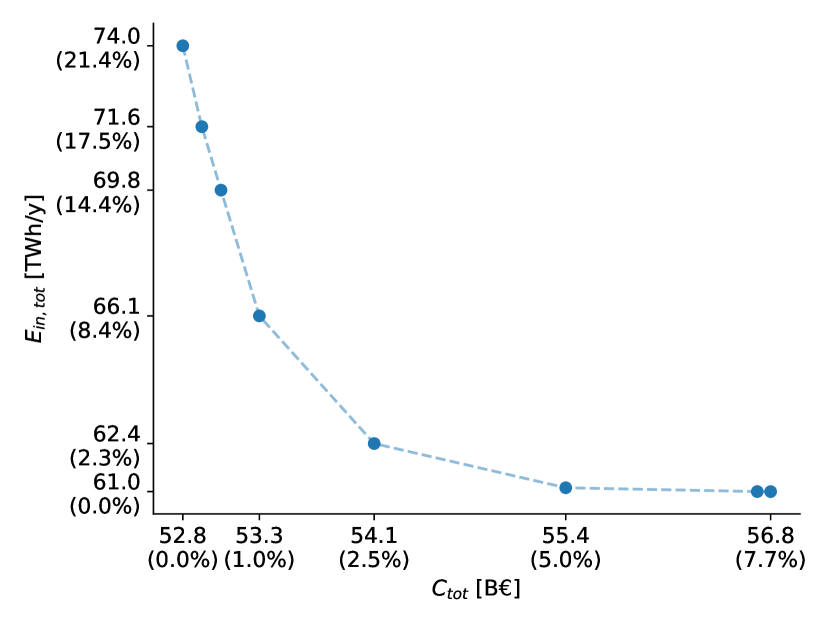

Figure 6 shows the values of and at the efficient solutions obtained using the method described in Section 3.5 for values of equal to 0.25, 0.5, 1.0, 2.5, 5.0 and 7.5%. The two additional points at the curve extremes correspond to each objective’s optimum. The axes are labelled both in terms of the absolute values of the objective functions but also - in parenthesis - in terms of the deviations of these values from the optimal objective value, i.e. and .

This graph shows that decreases quite rapidly, saving 10 TWh/y out of 74 TWh/y ( -14%) when increasing by a relatively small amount of 2.5%. This behaviour can also be interpreted as: choosing the optimal cost implies a considerable addition in invested energy. Inversely, as already mentioned, is still relatively low at the optimum, i.e. it only increases by 7.5%.

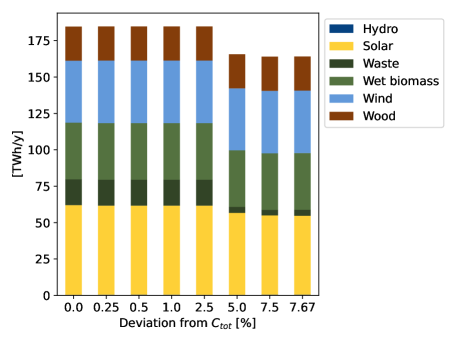

Figure 7 shows the amount of endogenous and exogenous resources used at each efficient solution, starting on the left with the cost optimum and moving towards the invested energy optimum on the right. As stated when comparing optimums, there is only a minor change for endogenous resources when going from one optimum to the other. This change, the reduction of solar and waste energy, appears when allowing a 5% deviation in cost.

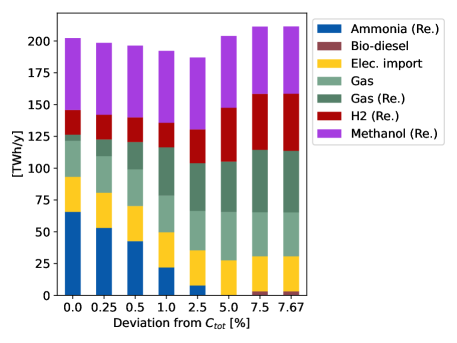

More change is happening for exogenous resources (Figure 7(b)). As we increase cost and decrease the invested energy, ammonia is gradually replaced by gas (both natural and renewable). At a 2.5% cost increase, the amount of renewable H2 starts increasing. Ammonia is wholly removed from the system at 5%, while natural gas use reaches its maximum and starts to decline. The same happens for renewable ammonia when reaching a 7.5% cost increase, and some bio-diesel appears. Overall, the change in the total amount of exogenous resources used is non-monotonic. Starting to decrease, it then increases when reaching the 5% threshold, corresponding to the drop in endogenous resources use.

4.3 Necessary conditions

Analysing efficient solutions gives a first appreciation of the variety of system configurations, offering a trade-off between different objectives. However, using the necessary conditions, we can go one step further by providing features respected by all those solutions and some slightly less efficient solutions. We use Algorithm 2 to compute non-implied necessary conditions stemming from different sets of conditions of the type defined by (27) in Section 3.7. The main parameter defining these conditions is , the set of resources over which the constrained sum is computed. The output of this algorithm is a value , which defines a non-implied necessary condition for this set of resources. Practically, this value represents the minimum amount of energy that needs to come from this set of resources to ensure that and do not deviate by more than an fraction from at least one solution in the Pareto front. We will first compute this value for conditions defined using the set of endogenous and the set of exogenous resources. We will then look at sets containing one individual resource.

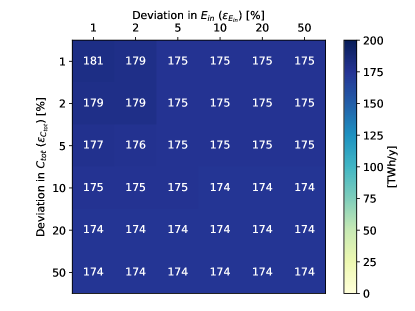

4.3.1 Endogenous vs exogenous resources

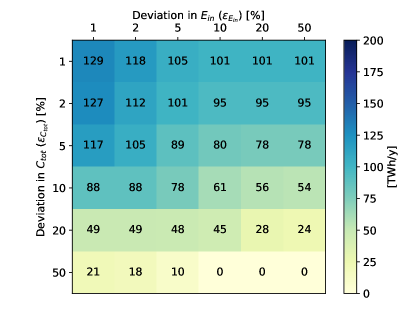

In this first section, we compare the values of non-implied necessary conditions computed from the sets and . These conditions are computed for different values of deviations . In this case, the tuples corresponds to all the possible combinations of 1%, 2%, 5%, 10%, 20%, and 50%.

Comparing Figures 8(a) and 8(b) shows how the behaviours of the minima in endogenous and exogenous resources are very different. For endogenous resources, the minimum for deviations of 1% in both objectives is already down to 130 TWh/y, representing a 42% and 26% decrease from the and optima, respectively. This amount is divided by more than two when the deviation reaches 10% in both objectives, leaving only 60 TWh/y left from endogenous resources. The value then reaches 0 TWh/y when allowing for an increase of 50% in . These results show that energy from endogenous resources can be reduced by a significant amount for reasonably low increases in cost and invested energy.

For exogenous resources, there is little to no decrease in the total energy needed. Starting from 202 and 211 TWh/y at the optimums in cost and energy invested, the minimum amount of this type of energy is still around 174 TWh/y (i.e. -20% and -15% respectively) for deviations of 10%. Most of the decrease is already present for deviations of 1% with an amount of energy of 180 TWh/y, which is only 6 TWh/y less than the energy used at one of the efficient solutions. The value of non-implied necessary conditions then plateaus at 174 TWh/y. This result shows how, contrarily to endogenous resources, exogenous resources are essential, whatever the cost and energy invested. Indeed, to respect a constraint of 35 Mt-eq/y, at least 174 TWh/y of energy needs to be imported.

4.3.2 Individual exogenous resources

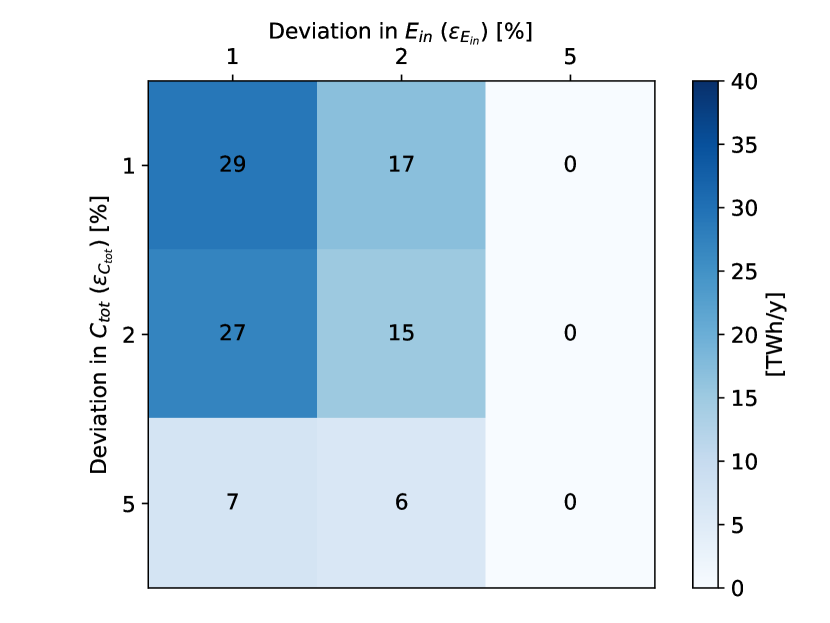

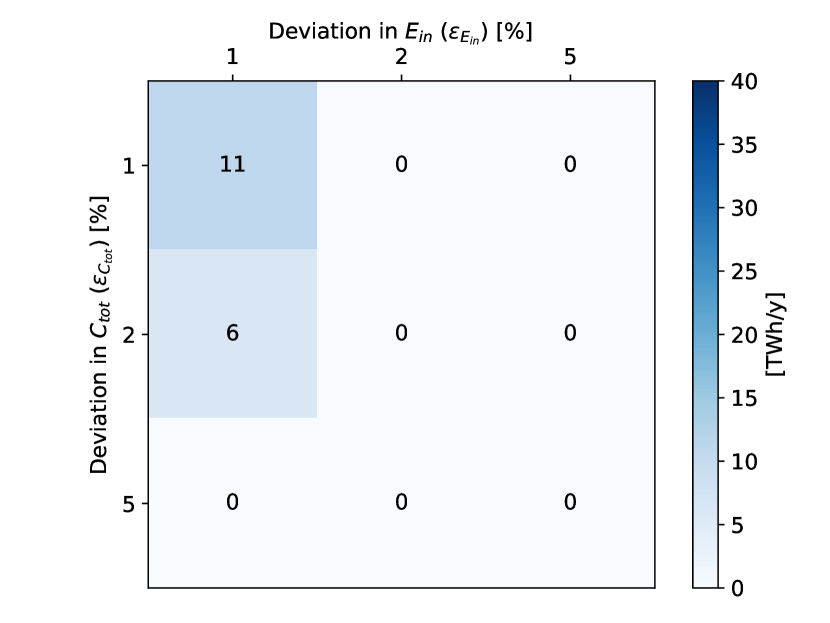

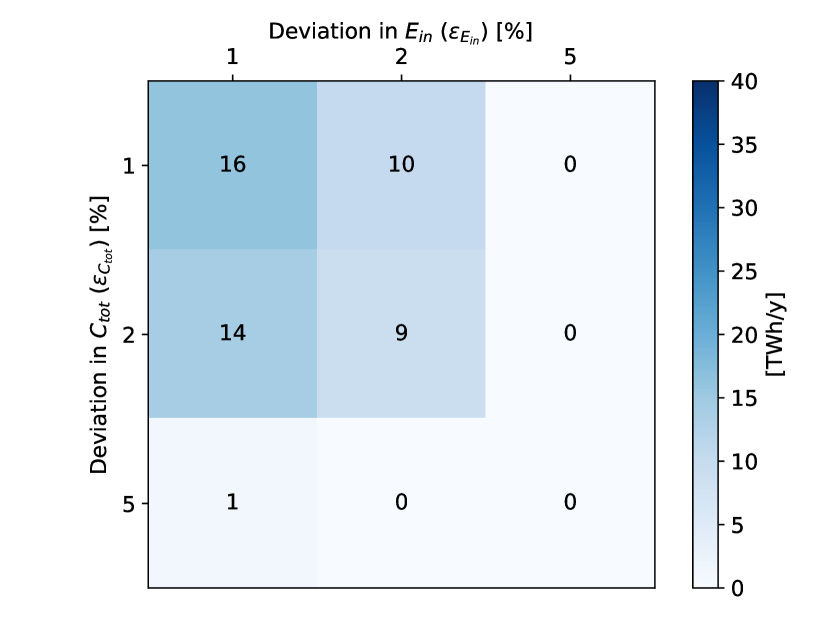

We have shown that a certain amount of exogenous resources is necessary due to limited endogenous resources. However, the previous results do not show which specific exogenous resource is essential. This analysis can be done by computing necessary conditions for groups of conditions where corresponds to an individual resource. We could perform this analysis for all individual resources, but in Figure 7(b), the amounts of renewable methanol, gas, and imported electricity are quasi-constant across the Pareto front. Therefore, it is interesting to focus on these resources to see if they are essential or if we can eliminate them by increasing the cost or the invested energy. In this section, we compute non-implied necessary conditions corresponding to the minimum energy from these three resources.

The values of non-implied necessary conditions for deviations and of 1%, 2% and 5% are shown in Figures 8(c), 8(d), and 8(e). We limit the analysis to deviations of 5% as we can see that we are already equal (or near to) 0 TWh/y for all three resources at this percentage. The amount of energy coming from the resources at the and optimums are respectively 56.4 and 52.8 TWh/y for renewable methanol, 28.2 and 34.5 for gas, and 27.6 (at both optima) for imported electricity. The minimum energy from each resource is around 50% lower than at the efficient solutions when allowing deviations of 1% in each objective. For renewable methanol and gas, the amount of necessary energy is more sensitive to deviations in invested energy than to deviations in cost. However, the conclusion is similar for the three resources: for a relatively small increase in cost and invested energy, they can be replaced by other resources.

5 Conclusion

This paper presents an extension of the concepts of necessary conditions for epsilon-optimality introduced by Dubois and Ernst [21] for mono-objective optimisation to multi-objective optimisation. This methodology provides a new way of overcoming the limitation that energy system models face when focusing on cost.

We first highlight the limits of cost-based optimisation problems and a series of existing solutions: scenario analysis, multi-objective optimisation and near-optimal spaces analysis. To outline how this last methodology can be combined with multi-objective optimisation, the concepts of epsilon-optimality and necessary conditions are presented in a single-objective setup and extended to multi-objective problems. Then, these concepts are illustrated in a case study addressing the Belgian energy transition and answering the question: “Which endogenous or exogenous resources are necessary in Belgium to ensure a transition associated with sufficiently good cost and EROI?”. The answer is obtained by computing non-implied necessary conditions corresponding to the minimum amount of energy coming from different sets of resources to ensure a constrained deviation in cost and energy invested. The results show Belgium’s dependence on imported resources but that no individual resource is essential.

This paper introduces a methodology and applies it for the first time to a concrete problem. There are, therefore, limitations to overcome and work tracks to explore. Regarding methodology, the main limitation is that, as explained in Section 2.2, in a multi-objective optimisation problem, the epsilon-optimal space can only be approximated. This approximation, in turn, removes the guarantees of finding non-implied necessary conditions. Increasing the number of efficient solutions used is a straightforward way to improve the quality of the results, but it comes at the expense of computational time. More research could be done to evaluate how the number and spread of efficient solutions affect the results. Taking a more general viewpoint, the techniques presented in this paper provide insights using fixed feasible spaces and objective functions. To reach their full potential, they ought to be combined with methods for fighting parametric uncertainty, such as sensibility analysis. We explored how the concept of necessary conditions could be extended to a multi-objective set-up. However, other methodologies were developed to explore near-optimal spaces in a mono-objective setup as presented, for instance, in [17, 18, 19, 49]. An interesting research track would thus be to extend these methodologies in a multi-objective setup.

To illustrate the methodology, a specific case study with a limited scope was used. A natural extension is thus to replicate this case study for other countries or territories where limited resources and energy dependence represent a challenge. Alternative questions regarding other resources or technologies could also be addressed using this framework. Finally, going one step further, a follow-up to this work would involve studying near-optimal spaces for other optimisation problems inside or outside the energy systems field.

Acknowledgements

Antoine Dubois is a Research Fellow of the F.R.S.-FNRS, of which he acknowledges the financial support.

Data Availability

Datasets related to this article can be found at https://zenodo.org/record/7665440#.Y_YyltLMIUE, hosted at Zenodo ([22]).

References

- DeCarolis et al. [2017] J. DeCarolis, H. Daly, P. Dodds, I. Keppo, F. Li, W. McDowall, S. Pye, N. Strachan, E. Trutnevyte, W. Usher, M. Winning, S. Yeh, M. Zeyringer, Formalizing best practice for energy system optimization modelling, Applied Energy 194 (2017) 184–198. URL: https://www.sciencedirect.com/science/article/pii/S0306261917302192. doi:https://doi.org/10.1016/j.apenergy.2017.03.001.

- Pfenninger et al. [2014] S. Pfenninger, A. Hawkes, J. Keirstead, Energy systems modeling for twenty-first century energy challenges, Renewable and Sustainable Energy Reviews 33 (2014) 74–86. URL: https://www.sciencedirect.com/science/article/pii/S1364032114000872. doi:https://doi.org/10.1016/j.rser.2014.02.003.

- Fishbone and Abilock [1981] L. G. Fishbone, H. Abilock, Markal, a linear-programming model for energy systems analysis: Technical description of the bnl version, International journal of Energy research 5 (1981) 353–375. doi:https://doi.org/10.1002/er.4440050406.

- Schrattenholzer [1981] L. Schrattenholzer, The energy supply model message (1981). URL: http://pure.iiasa.ac.at/1542.

- Yue et al. [2018] X. Yue, S. Pye, J. DeCarolis, F. G. Li, F. Rogan, B. Ó. Gallachóir, A review of approaches to uncertainty assessment in energy system optimization models, Energy Strategy Reviews 21 (2018) 204–217. URL: https://www.sciencedirect.com/science/article/pii/S2211467X18300543. doi:https://doi.org/10.1016/j.esr.2018.06.003.

- Fazlollahi et al. [2012] S. Fazlollahi, P. Mandel, G. Becker, F. Maréchal, Methods for multi-objective investment and operating optimization of complex energy systems, Energy 45 (2012) 12–22. URL: https://www.sciencedirect.com/science/article/pii/S0360544212001600. doi:https://doi.org/10.1016/j.energy.2012.02.046, the 24th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy, ECOS 2011.

- Trutnevyte [2016] E. Trutnevyte, Does cost optimization approximate the real-world energy transition?, Energy 106 (2016) 182–193.

- Fujino et al. [2008] J. Fujino, G. Hibino, T. Ehara, Y. Matsuoka, T. Masui, M. Kainuma, Back-casting analysis for 70% emission reduction in japan by 2050, Climate Policy 8 (2008) S108–S124. URL: https://doi.org/10.3763/cpol.2007.0491. doi:10.3763/cpol.2007.0491.

- Hughes and Strachan [2010] N. Hughes, N. Strachan, Methodological review of uk and international low carbon scenarios, Energy Policy 38 (2010) 6056–6065. URL: https://www.sciencedirect.com/science/article/pii/S0301421510004325. doi:https://doi.org/10.1016/j.enpol.2010.05.061, the socio-economic transition towards a hydrogen economy - findings from European research, with regular papers.

- Becerra-López and Golding [2008] H. R. Becerra-López, P. Golding, Multi-objective optimization for capacity expansion of regional power-generation systems: Case study of far west texas, Energy Conversion and Management 49 (2008) 1433–1445. URL: https://www.sciencedirect.com/science/article/pii/S0196890408000058. doi:https://doi.org/10.1016/j.enconman.2007.12.021.

- Fonseca et al. [2021a] J. D. Fonseca, J.-M. Commenge, M. Camargo, L. Falk, I. D. Gil, Multi-criteria optimization for the design and operation of distributed energy systems considering sustainability dimensions, Energy 214 (2021a) 118989. URL: https://www.sciencedirect.com/science/article/pii/S036054422032096X. doi:https://doi.org/10.1016/j.energy.2020.118989.

- Fonseca et al. [2021b] J. D. Fonseca, J.-M. Commenge, M. Camargo, L. Falk, I. D. Gil, Sustainability analysis for the design of distributed energy systems: A multi-objective optimization approach, Applied Energy 290 (2021b) 116746. URL: https://www.sciencedirect.com/science/article/pii/S0306261921002580. doi:https://doi.org/10.1016/j.apenergy.2021.116746.

- Jing et al. [2018] R. Jing, X. Zhu, Z. Zhu, W. Wang, C. Meng, N. Shah, N. Li, Y. Zhao, A multi-objective optimization and multi-criteria evaluation integrated framework for distributed energy system optimal planning, Energy Conversion and Management 166 (2018) 445–462. URL: https://www.sciencedirect.com/science/article/pii/S0196890418304023. doi:https://doi.org/10.1016/j.enconman.2018.04.054.

- DeCarolis [2011] J. F. DeCarolis, Using modeling to generate alternatives (mga) to expand our thinking on energy futures, Energy Economics 33 (2011) 145–152. URL: https://www.sciencedirect.com/science/article/pii/S0140988310000721. doi:https://doi.org/10.1016/j.eneco.2010.05.002.

- Brill et al. [1982] E. D. Brill, S.-Y. Chang, L. D. Hopkins, Modeling to generate alternatives: The hsj approach and an illustration using a problem in land use planning, Management Science 28 (1982) 221–235. URL: http://www.jstor.org/stable/2630877.

- DeCarolis et al. [2016] J. DeCarolis, S. Babaee, B. Li, S. Kanungo, Modelling to generate alternatives with an energy system optimization model, Environmental Modelling & Software 79 (2016) 300–310. URL: https://www.sciencedirect.com/science/article/pii/S1364815215301080. doi:https://doi.org/10.1016/j.envsoft.2015.11.019.

- Price and Keppo [2017] J. Price, I. Keppo, Modelling to generate alternatives: A technique to explore uncertainty in energy-environment-economy models, Applied Energy 195 (2017) 356–369. doi:https://doi.org/10.1016/j.apenergy.2017.03.065.

- Li and Trutnevyte [2017] F. G. Li, E. Trutnevyte, Investment appraisal of cost-optimal and near-optimal pathways for the uk electricity sector transition to 2050, Applied Energy 189 (2017) 89–109. URL: https://www.sciencedirect.com/science/article/pii/S0306261916318104. doi:https://doi.org/10.1016/j.apenergy.2016.12.047.

- Pedersen et al. [2021] T. T. Pedersen, M. Victoria, M. G. Rasmussen, G. B. Andresen, Modeling all alternative solutions for highly renewable energy systems, Energy (2021) 121294.

- Neumann and Brown [2021] F. Neumann, T. Brown, The near-optimal feasible space of a renewable power system model, Electric Power Systems Research 190 (2021) 106690. doi:https://doi.org/10.1016/j.epsr.2020.106690.

- Dubois and Ernst [2022] A. Dubois, D. Ernst, Computing necessary conditions for near-optimality in capacity expansion planning problems, Electric Power Systems Research 211 (2022) 108343. URL: https://www.sciencedirect.com/science/article/pii/S0378779622005077. doi:https://doi.org/10.1016/j.epsr.2022.108343.

- Dubois et al. [2023a] A. Dubois, J. Dumas, G. Limpens, P. Thiran, Multi-objective near-optimal necessary conditions for multi-sectoral planning - code (2023a). doi:10.5281/zenodo.7665440.

- Dubois et al. [2023b] A. Dubois, J. Dumas, G. Limpens, P. Thiran, Multi-objective near-optimal necessary conditions for multi-sectoral planning - dataset, 2023b. doi:10.5281/zenodo.7665340.

- Ehrgott [2005] M. Ehrgott, Multicriteria optimization, volume 491, Springer Science & Business Media, 2005.

- Alarcon-Rodriguez et al. [2010] A. Alarcon-Rodriguez, G. Ault, S. Galloway, Multi-objective planning of distributed energy resources: A review of the state-of-the-art, Renewable and Sustainable Energy Reviews 14 (2010) 1353–1366. URL: https://www.sciencedirect.com/science/article/pii/S1364032110000146. doi:https://doi.org/10.1016/j.rser.2010.01.006.

- EU- [2021] European Green Deal, 2021. URL: https://ec.europa.eu/clima/eu-action/european-green-deal_en, [accessed 08-June-2022].

- International Energy Agency [2022] International Energy Agency, IEA - Energy Statistics Data Browser, 2022. URL: https://www.iea.org/data-and-statistics/data-tools/energy-statistics-data-browser, [accessed 17-June-2022].

- Commission et al. [2016] E. Commission, D.-G. for Climate Action, D.-G. for Energy, D.-G. for Mobility, Transport, M. Zampara, M. Obersteiner, S. Evangelopoulou, A. De Vita, W. Winiwarter, H. Witzke, S. Tsani, M. Kesting, L. Paroussos, L. Höglund-Isaksson, D. Papadopoulos, P. Capros, M. Kannavou, P. Siskos, N. Tasios, N. Kouvaritakis, P. Karkatsoulis, P. Fragkos, A. Gomez-Sanabria, A. Petropoulos, P. Havlík, S. Frank, P. Purohit, K. Fragiadakis, N. Forsell, M. Gusti, C. Nakos, EU reference scenario 2016 : energy, transport and GHG emissions : trends to 2050, Publications Office, 2016. doi:doi/10.2833/001137.

- Dupont et al. [2021] E. Dupont, M. Germain, H. Jeanmart, Estimate of the societal energy return on investment (eroi), Biophysical Economics and Sustainability 6 (2021) 1–14. doi:https://doi.org/10.1007/s41247-021-00084-9.

- Brockway et al. [2019] P. E. Brockway, A. Owen, L. I. Brand-Correa, L. Hardt, Estimation of global final-stage energy-return-on-investment for fossil fuels with comparison to renewable energy sources, Nature Energy 4 (2019) 612–621.

- Dumas et al. [2022] J. Dumas, A. Dubois, P. Thiran, P. Jacques, F. Contino, B. Cornélusse, G. Limpens, The energy return on investment of whole-energy systems: Application to belgium, Biophysical Economics and Sustainability 7 (2022) 12.

- European Commission - Eurostat [2022] European Commission - Eurostat, Glossary: Final Energy Consumption, 2022. URL: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Glossary:Final_energy_consumption, [accessed 17-June-2022].

- Khattabi [2021] Z. Khattabi, Press release - 8 Octobre 2021, 2021. URL: https://khattabi.belgium.be/, [accessed 26-Jul-2022].

- eur [2022] Eurostat - Population density, 2022. URL: https://ec.europa.eu/eurostat/databrowser/view/tps00003/default/table, [accessed 17-June-2022].

- be- [2022] Belgian Offshore Platform, 2022. URL: https://www.belgianoffshoreplatform.be/en/, [accessed 26-Jul-2022].

- Limpens et al. [2020] G. Limpens, H. Jeanmart, F. Maréchal, Belgian energy transition: What are the options?, Energies 13 (2020). URL: https://www.mdpi.com/1996-1073/13/1/261. doi:10.3390/en13010261.

- Limpens et al. [2019] G. Limpens, S. Moret, H. Jeanmart, F. Maréchal, Energyscope td: A novel open-source model for regional energy systems, Applied Energy 255 (2019) 113729. URL: https://www.sciencedirect.com/science/article/pii/S0306261919314163. doi:https://doi.org/10.1016/j.apenergy.2019.113729.

- Limpens et al. [2020] G. Limpens, D. Coppitters, X. Rixhon, F. Contino, H. Jeanmart, The impact of uncertainties on the belgian energy system: Application of the polynomial chaos expansion to the energyscope model, ECOS 2020 - Proceedings of the 33rd International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems (2020) 724–733. URL: http://hdl.handle.net/2078.1/231513.

- Rixhon et al. [2021] X. Rixhon, G. Limpens, D. Coppitters, H. Jeanmart, F. Contino, The role of electrofuels under uncertainties for the belgian energy transition, Energies 14 (2021). URL: https://www.mdpi.com/1996-1073/14/13/4027. doi:10.3390/en14134027.

- Colla et al. [2022] M. Colla, J. Blondeau, H. Jeanmart, Optimal use of lignocellulosic biomass for the energy transition, including the non-energy demand: The case of the belgian energy system, Frontiers in Energy Research 10 (2022). URL: https://www.frontiersin.org/article/10.3389/fenrg.2022.802327. doi:10.3389/fenrg.2022.802327.

- Limpens and Jeanmart [2021] G. Limpens, H. Jeanmart, System lcoe: Applying a whole-energy system model to estimate the integration costs of photovoltaic, in: Proceedings of the ECOS2021—The 34th International Conference, Taormina, Italy, June, 2021, pp. 28–2. URL: http://hdl.handle.net/2078.1/252944.

- Li et al. [2020] X. Li, T. Damartzis, Z. Stadler, S. Moret, B. Meier, M. Friedl, F. Maréchal, Decarbonization in complex energy systems: A study on the feasibility of carbon neutrality for switzerland in 2050, Frontiers in Energy Research 8 (2020). URL: https://www.frontiersin.org/article/10.3389/fenrg.2020.549615. doi:10.3389/fenrg.2020.549615.

- Guevara et al. [2020] E. Guevara, F. Babonneau, T. H. de Mello, S. Moret, A machine learning and distributionally robust optimization framework for strategic energy planning under uncertainty, Applied Energy 271 (2020) 115005. URL: https://www.sciencedirect.com/science/article/pii/S0306261920305171. doi:https://doi.org/10.1016/j.apenergy.2020.115005.

- Borasio and Moret [2022] M. Borasio, S. Moret, Deep decarbonisation of regional energy systems: A novel modelling approach and its application to the italian energy transition, Renewable and Sustainable Energy Reviews 153 (2022) 111730. URL: https://www.sciencedirect.com/science/article/pii/S1364032121010030. doi:https://doi.org/10.1016/j.rser.2021.111730.

- rea [2022] EnergyScope TD Documentation, 2022. URL: https://energyscope-td.readthedocs.io/en/master/, [accessed 17-June-2022].

- Muyldermans and Nève [2021] B. Muyldermans, G. Nève, Multi-criteria optimisation of an energy system and application to the Belgian case, Master’s thesis, UCL - Ecole polytechnique de Louvain, 2021. URL: http://hdl.handle.net/2078.1/thesis:33139.

- Wernet et al. [2016] G. Wernet, C. Bauer, B. Steubing, J. Reinhard, E. Moreno-Ruiz, B. Weidema, The ecoinvent database version 3 (part i): overview and methodology, The International Journal of Life Cycle Assessment 21 (2016) 1218–1230. doi:https://doi.org/10.1007/s11367-016-1087-8.

- Orban [2022] A. Orban, Energy Return on Investment of Electrofuels, Master’s thesis, ULiège, 2022.

- Nacken et al. [2019] L. Nacken, F. Krebs, T. Fischer, C. Hoffmann, Integrated renewable energy systems for Germany–A model-based exploration of the decision space, in: 2019 16th International Conference on the European Energy Market (EEM), IEEE, 2019, pp. 1–8.

- Limpens [2021] G. Limpens, Generating energy transition pathways: application to Belgium, Ph.D. thesis, UCL-Université Catholique de Louvain, 2021. URL: http://hdl.handle.net/2078.1/249196.

Appendix A Example

The functions depicted in Figures 2, 4, and 5 are

The coordinates of their minimums are and , respectively.

One-dimensional epsilon-optimal space

In Figure 2, the -optimal space of a one-dimensional optimisation problem was obtained by first computing

where . Then, the limits of can be obtained by computing the inverse image of this value, i.e. the set , which leads to .

Two-dimensional epsilon-optimal space

In Figure 4(a) and 4(b), the Pareto front is represented in green. This set of points respects definition 12 of a Pareto front. Indeed, each point in the interval is such that where and .

In Figure 4(b), a subset of the -optimal space of a two-dimensional optimisation problem is computed for a suboptimality coefficients vector . This subset is computed from the point , which is part of . To obtain the subset of , the images of , and , are computed. Multiplying these values by the corresponding suboptimality coefficients gives

The inverse image of these values are for and for . The set of points respecting are then contained in .

To obtain the full -optimal space depicted in Fig. 4(a), one should repeat this process with all points in . However, in this simple example, one can easily compute the limits of the complete space by using the two optimums, which are the extreme points of the Pareto front. These limits are obtained by taking the inverse images of

which gives and . The lower and upper bound of are then respectively given by the lower and upper bound of those two sets, i.e. .

Approximate Pareto fronts and epsilon-optimal spaces

Figures 5(a), 5(b), and 5(c) show approximate -optimal spaces for three different set of efficient points. These sets are

-

1.

Fig. 5(a): [(2.0, 2.91), (3.41, 1.85), (7.62, 1.5)];

-

2.

Fig. 5(b): [(2.9, 2.01), (2.99, 1.97), (3.09, 1.94), (3.19, 1.91), (3.3, 1.88), (3.41, 1.85), (3.52, 1.82), (3.64, 1.8), (3.77, 1.77), (3.9, 1.75), (4.03, 1.72)];

-

3.

Fig. 5(c): [(2.0, 2.91), (2.06, 2.64), (2.23, 2.40), (2.51, 2.19), (2.9, 2.01), (3.41, 1.85), (4.03, 1.72), (4.76, 1.63), (5.61, 1.56), (6.57, 1.51), (7.62, 1.5)].

Appendix B Types of end-use demand in EnergyScope-TD

Four main types of EUD are considered in the model: electricity, heat, transport, and non-energy demand. Electricity is further divided between lighting and other electricity uses. Heat is subdivided into high-temperature heat for industry, low temperature for space heating, and low temperature for hot water. Mobility is composed of public and private passenger mobility and freight demands. Finally, the non-energy demand includes demand for ammonia, methanol, and high-value chemicals (HVCs). Table 5 lists the values for each EUD type in 2035 based on Limpens [50].

| EUD type | Unit | EUD |

|---|---|---|

| Electricity (other) | TWhe | 62.1 |

| Lighting | TWhe | 30.0 |

| Heat high T. | TWh | 50.4 |

| Heat low T. (SH) | TWh | 118 |

| Heat low T. (HW) | TWh | 29.2 |

| Passenger mobility | Mpass.-km | 194 |

| Freight | Mt-km | 98.0 |

| Non-energy | TWh | 53.1 |