Forecasting and stabilizing chaotic regimes in two macroeconomic models via artificial intelligence technologies and control methods

Abstract

One of the key tasks in the economy is forecasting the economic agents’ expectations of the future values of economic variables using mathematical models. The behavior of mathematical models can be irregular, including chaotic, which reduces their predictive power. In this paper, we study the regimes of behavior of two economic models and identify irregular dynamics in them. Using these models as an example, we demonstrate the effectiveness of evolutionary algorithms and the continuous deep Q-learning method in combination with Pyragas control method for deriving a control action that stabilizes unstable periodic trajectories and suppresses chaotic dynamics. We compare qualitative and quantitative characteristics of the model’s dynamics before and after applying control and verify the obtained results by numerical simulation. Proposed approach can improve the reliability of forecasting and tuning of the economic mechanism to achieve maximum decision-making efficiency.

keywords:

chaos, self-organized migration algorithm; Pyragas control method; continuous deep Q-learning method, economic models, Hénon map1 Introduction

The processes taking place in the modern economy are characterized by increasing complexity and unpredictability, due to transformation of its structure, development and implementation of new technologies, as well as climate change and the epidemiological environment. Such challenges motivated posing a set of important problems in economic research as well as in actual economics activities: studying the complex behavior of models, for example, associated with non-linearity, large-scaling and a large number of variables or parameters (see, e.g. [1, 2]); forecasting irregular dynamics of economic processes, including critical transitions and crises (see, e.g. [3]); solving complex dynamic nonlinear models with a large number of heterogeneous agents in the presence of numerous stochastic shocks, for example Dynamic Stochastic General Equilibrium (DSGE) models (see, e.g. [4, 5]) which are used by central banks to analyze and produce real or near-real time forecasting of important macro variables such as inflation and economic activity; monitoring of the degree of financial system’s interconnectedness and stability, etc. [6]; detecting patterns of behavior by different economic agents that are causing concerns (fraud, money laundering, collusion in procurement auctions, intentional default, etc.).

In economic research the tasks are focused on mathematical modeling of economic processes, forecasting the qualitative properties of their dynamics and controlling various regimes that arise in the economic mechanism, including under conditions leading to crisis states. In nonlinear mathematical models, signals of crisis conditions can manifest themselves in the form of irregular dynamics, including quasiperiodic and even chaotic ones. Additional complexity of the dynamics can be also associated with various unstable periodic trajectories embedded into the chaotic attractor of the dynamical system. Irregular behavior reduces the reliability of forecasts and thus undermines the predictive power of the model. In this case, decision-makers do not have the ability to predict and regulate the expectations of agents as well as evaluate the implications of economic policies.

Successfully overcoming these difficulties crucially depends on the choice of methods and effective ways of their application to the analysis and control of model dynamics. Artificial Intelligence (AI) technologies such as evolutionary algorithms (EAs) [7, 8] and the reinforcement learning (RL) (the continuous deep Q-learning method and the actor-critic method) [9, 10, 11, 12] have significant advantages as optimization and adata-based control policy algorithms. However, we found that to correctly solve the problem of controlling irregular dynamics, including chaotic, and to reliably forecast the behavior of models, the usage of these technologies as sole method is not always sufficient. In some cases, the application of time-delay feedback control method (TDFC) proposed by K. Pyragas [13] as comlement to EAs or Q-learning is more effective approach. Such combination of the methods allows targeted utilization of the control procedure to stabilize unstable periodic orbits (UPOs) of the model taking into account a problem statement in a subject field (in this case, in economics), the structure of the mathematical model and the limitations of the TDFC computational method.

We demonstrate the efficiency of this approach for two discrete-time macroeconomic models as examples, presenting two possible options for combining one of the AI technologies and the Pyragas method. In the first case, we apply a combination of EAs with the Pyragas method to one of overlapping generations (OLG) models [14, 15] that an ‘‘internal’’ control variable is included as economic feature [16]. Using the computational abilities of a supercomputer, we show how the combination of differential evolution (DE) [17] and self-organized migration (SOMA) algorithms [18] with the Pyragas method can overcome the problems associated with fractional-power nonlinearities in economic variables, significantly increase the performance of chaotic dynamics control and allow us to obtain much faster and more accurate fine-tuning of control parameters to achieve the desired state of the model and improve its forecasting behavior. Our second model describes spatio-temporal (ST) model of pricing patterns in the global network market of goods [19] that can demonstrate a rich spectrum of nontrivial dynamics, including multistability and chaotic regimes, which stimulate the use of increasingly sophisticated analytical and numerical techniques and tools based on artificial intelligence technologies. Using this model as an example, we show how to model ‘‘external’’ control and stabilize the chaotic regime by the Q-learning procedure and the Pyragas method.

2 Problem statement

Irregular behavior is an undesirable phenomenon in the economy, since the model of economic phenomenon has some interpretative power for making decisions and affecting the agents’ expectations only if model possesses determinate (unique) economic equilibria. Therefore, revealing regular regime of the model behavior and regularization of the dynamics in the case of an irregular regime using control is one of the important tasks of modeling [20, 21, 22]. In this paper, we consider two economies represented by an OLG model and a spatio-temporal (ST) model of pricing patterns in the global network market of goods; both models can demonstrate irregular, including chaotic, dynamics for some parameter values. To control chaos we may find and stabilize an UPO embedded within a chaotic attractor. To solve this problem we refer to the time-delay feedback control (TDFC) approach, suggested by K. Pyragas. The main idea behind the Pyragas approach is to stabilize UPO by constructing a control force proportional to the difference between the current state of the system and an earlier state of the system (delayed by some time interval). In this paper, we represent mentioned above models in the following extended mathematical form:

| (1) |

where , is a vector-function, is control input. In the spirit of the ideas by Pyragas, we can consider as the Pyragas-like control:

| (2) |

such that along UPO with the period- (i.e. for , ) the following relation holds:

| (3) |

For the original Pyragas method, we have:

| (4) |

where the feedback gain can be represented either a scalar or a constant matrix.

For the OLG model, control variable is naturally embedded in the model in the form of a proportional tax, thus, it is inherently ‘‘internal’’ economic characteristic. Therefore, we can stabilize the chaotic dynamics in the OLG model using a sufficiently small control by adjusting the proportional tax a little. The pricing model in the global network market does not contain a control variable explicitly, so we introduce an additive ‘‘external’’ control variable into this model. Next, using mathematical modeling we synthesize control variables in the Pyragas form in such a way that the current unstable trajectory could be attracted to a periodic orbit, upon reaching which the control variable is set to 0. To effectively optimize and fine-tune the control parameters we apply evolutionary algorithms (EAs) in the OLG model and the continuous deep Q-learning and the actor-critic method in the pricing model.

3 Pyragas method and evolutionary algorithms: implementation in OLG model

We consider a two period OLG model with production and endogenous labor choice. Similar OLG models allow to exploring important intergenerational mechanisms such as demographic trends, the dynamics of education and retirement, capital accumulation, public policies, inflation, fiscal policies, etc. Two types of agents, consumers and firms, solve their dynamical optimization problems.

Consumer problem

| (5) |

| s.t. | (6) | ||||

where is consumption of young in period ,

is consumption of young in period when they

will be old;

is the utility of consuming while

young, the (future) utility of consuming

when old, and disutility of labor. In the first

period, the budget constraint (6) says that consumption plus capital

equals the income of the young, given by their labor income

net of proportional taxes with rate .

Here are working hours (labor) when young, is the real wage rate, is the gross real interest rate at the relevant time.

In the second period of their life (physical time ), the agents born at consume their savings with interest. Non-negativity constraints form part of the model.

Firms’ problem

| (7) |

where is the profit, is the parameter of the Leontieff production function.

The solution of this OLG model with respect to variables is described by the following two-dimensional map

| (8) |

which generates the following discrete-time dynamical model

| (9) |

where is the government spending in period ; is the parameter of the Leontieff production function, and are model parameters (elastisities of functions).

Model (9) describes complex behavior of the agents in conditions of economic equilibrium – a situation when supply and demand in all markets are balanced. Dynamics of agent’s consumption and labor in the model can be irregular, involving chaotic regime, that decreases predictable power of the model and agents’ expectations. In this case, one of the effective ways to suppress chaotic behavior in (9) through stabilizing UPOs embedded in a chaotic attractor using a minimal control. The latter task requires to determine any period- UPO and introduce a control in the model. To solve this problem and provide the minimum control through the variable in (9) we choose in the Pyragas form (4) ( thus equals 0 on the target trajectory, i.e. UPO). Within framework of the economic problem, can be generated as a time series and implemented as follows:

| (10) |

where is the rate of the proportional tax on the young. In the absence of a control variable (i.e. ), we get the following

| (11) |

For system (11), let us find a period- UPO such that , . Here, the original Pyragas approach (2)–(4) does not allow us to identify and stabilize the UPO using only one control parameter. To overcome this difficulty we solve an auxiliary mathematical problem by adding third equation and artificial variable to system (9), and consider the following extended system:

| (12) |

where specifies the delay, control parameters use only for stabilization UPO and pick up by TDFC method. That allows obtaining the control variable through economic parameters according to (10) and adjusting the behaviour of the economy using a fairly small disturbance inside model. Along the desired period- UPO in (8) or (9) the following condition holds . Plugging this equality into second and third equations of (12), we receive and, consequently, . Therefore, to numerically analyze the dynamics of (12) we choose the initial conditions so that if they get captured in the UPO, i.e. , then . System (12) is the notation of general mathematical model (2) in terms of OLG model with:

| (13) |

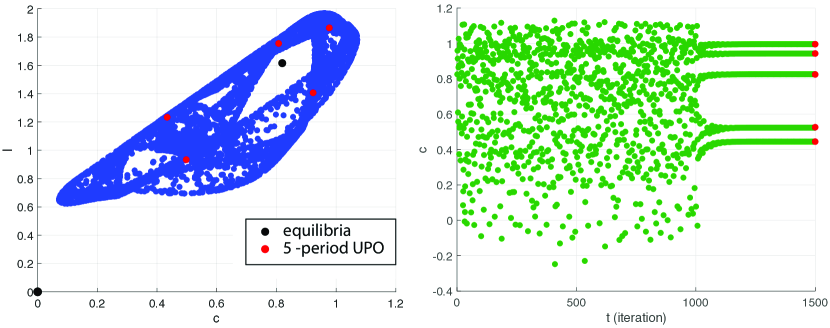

In this work, to determine parameters of time-delay feedback control within Pyragas procedure, we used three most powerful and commonly used evolutionary algorithms: differential evolution algorithm (DE/rand/1/bin) [7]; self-organized migration algorithm (SOMA) [18]; SOMA with Team To Team Adaptive strategy (SOMA T3A) [23, 24]. Using these EAs and solving numerically the corresponding equation , , we obtain that for system (11) with parameters , , , it is possible to reveal a candidate for a period- UPO, where , to be further stabilized, i.e.

| (14) |

To fine-tune , , we again use the EAs, finding the minimum value of the cost function defined as a spectral radius of the fundamental matrix for the corresponding map , computed along the points of the UPO in (14) and reflecting its orbital stability after stabilization. As a result, we obtain the following values: , .

Remark that the obtained values deliver stabilization only locally, i.e. for some initial points in a vicinity of the UPO. So, the next task in our experiments was to solve an optimal control problem of finding optimal values of control parameters , to maximize the basin of attraction of the stabilized UPO. To this end, we consider two regions: for control parameters , and for system’s parameters together with the specific partition step . We define a specific grid of points

which consists of points, from which trajectories go to infinity (set ); from which trajectories after iterations tend to the stabilized UPO (set ); from which trajectories after iterations tend to some other attractors (set ). To use the computational abilities of EAs, we write this optimal control problem in the following form with the corresponding cost function: .

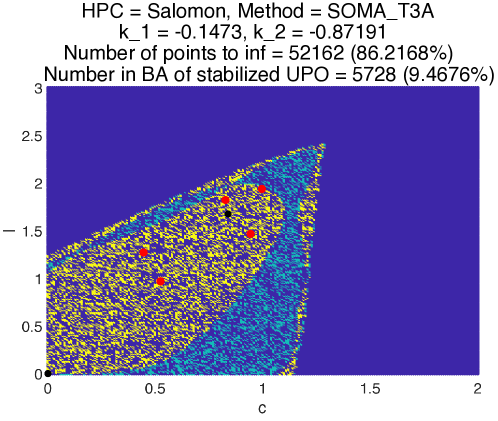

Solving such a computational problem implies calculation and examination of the behavior for the number of trajectories of system (12) equal to at each iteration of the evolutionary algorithm. As decreasing and increasing, it turns into an extremely time and resource consuming computational procedure. In order to make this procedure more efficient, we implement it in MathWorks Matlab using Parallel Computing Toolbox and launch it on two powerful HPCs at IT4Innovations National Supercomputing Center of the Czech Republic, i.e. Barbora Cluster and Salomon Cluster. It took 324 Matlab workers (Matlab computational engines) in total with 48 hours of calculation time at each worker.

For stabilized UPO (14) and procedure parameters , using three evolutionary algorithms 3, 3, 3 we obtain that the best value of cost function (i.e. the maximum number of points in ) equals and is reached at the point . This value is obtained by SOMA T3A algorithm launched on Salomon Cluster. The simulation consumed about core hours for the computation, which is equivalent to around continuously working years of the single CPU with GHz.

4 Deep reinforcement learning: implementation in ST-model of pricing and Hénon map

One of the natural economic mechanisms in which irregular dynamics is formed is the pricing in the markets for goods that could only be stored for short-term, for example, in the markets for trade in fish and agricultural products. Such effects can be described by any type of cobweb model with non-linear supply and/or demand functions and various types of expectations of economic agents (naive, rational, adaptive). In addition, in the economic context, of interest may be the spatiotemporal behavior of the model associated with the interaction of local cobweb-type markets. Prices in such a model may demonstrate irregular dynamics, including chaotic ones.

In our work, we represent an economy in which the global market consists of a network of local markets represented by two types of alternating nodes: ‘‘even’’ (or ‘‘recipients’’) and ‘‘odd’’ (or ‘‘donors’’), i.e. markets with a higher and a lower preference in the consumption of a good. This leads to a model of global trade in which the stationary net inflow of goods into different types of markets has opposite directions.

We explain the global market dynamics by Lattice Dynamical System (LDS) [25, 19]. At each node of a dimensional lattice we consider a finite dimensional local dynamical systems as map , () is a local phase space at the node (or an infinite chain), . Price dynamics could be formulated as follows:

| (15) |

where is good’s price at node and at time , is the evolution operator, , is a differentiable map of class , indexes the degree of nonlinearity in the local market dynamics , is the logistic map with the parameter , is the diffusion coefficient measuring the intensity of interaction between the neighboring local markets. A solution is stationary if , . Then, the stationary solution of the global market dynamics could represent as the following

| (16) |

where . Taking we can transform (16) to the 2D dynamical system

| (17) |

generated by the Hénon map with , , , and . It has the unstable equilibria :

Our goal of chaos control is to stabilize (17) at one of its UPOs. To achieve that, we can rewrite general system (1) in terms of Hénon map (17) with111* is the transpose of a matrix:

| (18) |

and following the main ideas from [11, 12], apply approach based on a RL algorithm called continuous deep Q-learning method to synthesize a small control and use it to stabilize UPO with period in (17). In the framework of RL is considered as a controller action, subject to a certain control policy, in the process of interacting with a controlled environment, i.e. system (18), in order to transition the system from the current state to the next one in the best way. Thus, we can say the control problem is to find a control policy (function) which associates with each state in (18) a control action such that the given goal is achieved in an optimal way indicating the quality of the control policy. As the criterion for the quality of control action taken in state a Q-function is used. It can be expressed by the sum of expected rewards for the transition of the system from the current state to the next one at time after taking an control action. We consider reward at time in the form of the following function:

| (19) |

where are some positive definite matrices. Accordingly, we solve the following problem: calculate such a stabilizing control in which the Q-function takes the maximum value if control was started from a randomly chosen initial state. Extending the system, by analogy with the above case, we can look for a control in the Pyragas-like form (2) .

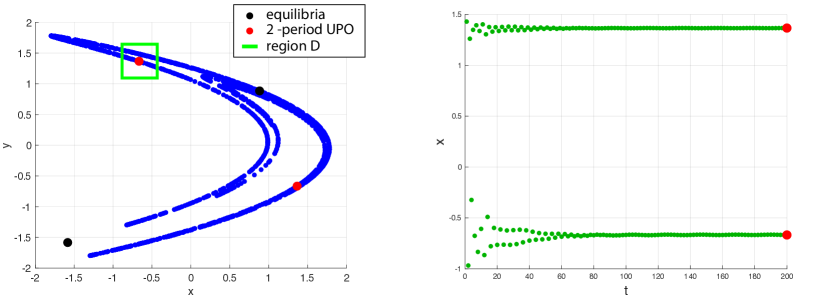

The proposed approach based on the continuous deep Q-learning algorithm allows us to tune the optimal control more efficiently and stabilize the system faster compared to the direct application of control in the Pyragas form (4), i.e. , where the selection of the control action depends significantly on the skills of the researcher. For instance, for a Hénon map (17) with ‘‘classical’’ parameter values , , we picked up the following matrix and considered the following initial conditions , from which we were able to stabilize (see Fig. 3) the following period-2 UPO:

in the region .

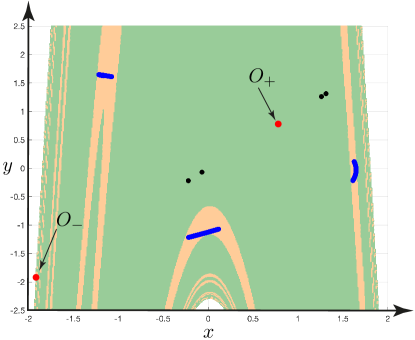

Difficulties in obtaining a guaranteed result of UPO stabilization may be connected with complex dynamics effects such as multistability and possible existence of hidden attractor [26, 27, 28, 29, 30, 31]. For example, if we consider (17) with parameter values , given in [32], then from some initial point on the unstable manifold of the saddle a self-excited attractor with respect to can be visualized and a self-excited periodic attractor can be visualized from vicinity of (see Fig. 4). In this case, other modifications of RL are required to stabilize the chaotic dynamics in the system, e.g., the actor-critic method [9] may be effective. This method is inherently an extension of policy gradient approaches, in which the model tries to learn (optimize) the policy while simultaneously using it to explore the environment. It nonetheless borrows from another class of methods (Q-learning methods) a value function for the estimation of selected actions instead of rewards given directly by the environment. We show that such an expansion of the range of AI tools makes it possible to achieve maximum progress in revealing and analyzing of the complex irregular behavior of the Hénon model for various admissible values of the model parameters. This, in turn, will enrich not only the mathematical results in this field, but also improve the connection with applications.

Conclusion

Revealing an irregular regime, including a chaotic one, and stabilizing such complex dynamics with the help of control in economic models significantly improves the forecasting of economic processes and, thereby, optimizes the complicated management decision-making system. We considered two economic concepts represented by the continuous time OLG model and the discrete time ST model reduced to the Hénon map. On the example of these models, we demonstrated the effectiveness and limitations of using the combination of DE and SOMA algorithms and the Pyragas-like method (the first model) and the continuous deep Q-learning algorithm (the second model) to solve the problem of forecasting and controlling models with irregular dynamics. We found two period-5 UPOs in OLG model via DE and SOMA algorithms, performed fine-tuning of parameters for delayed control in the Pyragas method to stabilize UPOs, conducted the optimal tuning of control parameters to maximize the basin of attraction. In a Hénon-like model of pricing patterns, we stabilized period-2 UPO via the continuous deep Q-learning method, by considering specific form of the reward (19), compaired the result with direct application of the Pyragas method, and revealed practical issues of this approach in the case of multistability. Proposed approach allows us not only to identify critical states and stabilize chaotic dynamics in the models, but also to make substantial progress in testing powerful artificial intelligence tools to form recommendations for adoption policy decisions.

Acknowledgments

The work is carried out with the financial support of the Russian Science Foundation: project 22-11-00172 (sections 1), St.Petersburg State University grant Pure ID 75207094 (sections 2), the Leading Scientific Schools program: project NSh-4196.1.1 (sections 4), and the Grant of SGS No. SP2023/050, VŠB-Technical University of Ostrava, Czech Republic (section 3).

References

- [1] L. Maliar, S. Maliar, P. Winant, Deep learning for solving dynamic economic models, Journal of Monetary Economics 122 (2021) 76–101.

- [2] J. Fernández-Villaverde, G. Nuño, G. Sorg-Langhans, M. Vogler, Solving high-dimensional dynamic programming problems using deep learning, National Bureau of Economic Research.

- [3] R. Z. Aliber, C. P. Kindleberge, Manias, Panics, and Crashes: A History of Financial Crises, Palgrave Macmillan UK, 2015.

- [4] J. Lindé, F. Smets, R. Wouters, Chapter 28 - Challenges for Central Banks’ macro models, Vol. 2 of Handbook of Macroeconomics, Elsevier, 2016, pp. 2185–2262.

- [5] S. Slobodyan, R. Wouters, Learning in a medium-scale DSGE model with expectations based on small forecasting models, American Economic Journal: Macroeconomics 4 (2) (2012) 65–101.

- [6] S. Consoli, D. R. Recupero, M. Saisana (Eds.), Data Science for Economics and Finance: Methodologies and Applications, Springer, 2021.

- [7] R. Storn, K. Price, Differential evolution – a simple and efficient heuristic for global optimization over continuous spaces, Journal of global optimization 11 (4) (1997) 341–359.

- [8] D. Davendra, I. Zelinka (Eds.), Self-Organizing Migrating Algorithm. Methodology and Implementation, Springer, 2016.

- [9] C. Watkins, P. Dayan, Q-learning, Machine Learning 8 (3–4) (1992) 279–292.

- [10] R. Sutton, A. Barto, Introduction to Reinforcement Learning, Cambridge: MIT press, 1998.

-

[11]

J. Ikemoto, T. Ushio, Model-free

control of chaos with continuous deep Q-learning, arXiv (2019).

URL https://arxiv.org/abs/1907.07775 - [12] J. Ikemoto, T. Ushio, Continuous deep Q-learning with a simulator for stabilization of uncertain discrete-time systems, Nonlinear Theory and Its Applications, IEICE 12 (4) (2021) 738–757.

- [13] K. Pyragas, Continuous control of chaos by self-controlling feedback, Physics letters A 170 (6) (1992) 421–428.

- [14] P. Diamond, National debt in a neoclassical growth model, American Economic Review 55 (5) (1965) 1126–1150.

- [15] P. A. Samuelson, An exact consumption-loan model of interest with or without the social contrivance of money, Journal of Political Economy 66 (6) (1958) 467–482.

-

[16]

T. Alexeeva, Q. B. Diep, N. Kuznetsov, T. Mokaev, I. Zelinka,

Forecasting and control in

overlapping generations model: chaos stabilization via artificial

intelligence (2022).

doi:10.48550/ARXIV.2208.06345.

URL https://arxiv.org/abs/2208.06345 - [17] K. V. Price, Differential evolution, in: Handbook of optimization, Springer, 2013, pp. 187–214.

- [18] I. Zelinka, SOMA—self-organizing migrating algorithm, Self-Organizing Migrating Algorithm: Methodology and Implementation (2016) 3–49.

- [19] Y.-I. Kim, Stationary global dynamics of local markets with quadratic supplies, Journal of the Korean Society of Mathematical Education Series B-Pure and Applied Mathematics 16 (4) (2009) 427–441.

- [20] K. Pyragas, Delayed feedback control of chaos, Phil. Trans. Royal Soc. A. 369 (2006) 2039–2334.

- [21] E. Ott, C. Grebogi, J. Yorke, Controlling chaos, Physical review letters 64 (11) (1990) 1196.

- [22] S. Boccaletti, C. Grebogi, Y. C. Lai, H. Mancini, D. Maza, The control of chaos: Theory and applications, Physics Reports 329 (3) (2000) 103–197.

- [23] Q. B. Diep, Self-organizing migrating algorithm team to team adaptive–SOMA T3A, in: 2019 IEEE Congress on Evolutionary Computation (CEC), IEEE, 2019, pp. 1182–1187.

- [24] Q. B. Diep, I. Zelinka, S. Das, R. Senkerik, SOMA T3A for solving the 100-digit challenge, in: Swarm, Evolutionary, and Memetic Computing and Fuzzy and Neural Computing, Springer, 2019, pp. 155–165.

- [25] S.-N. Chow, Lattice Dynamical Systems, Vol. 1822, Springer Berlin Heidelberg, 2003, pp. 1–102.

- [26] D. Dudkowski, S. Jafari, T. Kapitaniak, N. Kuznetsov, G. Leonov, A. Prasad, Hidden attractors in dynamical systems, Physics Reports 637 (2016) 1–50. doi:10.1016/j.physrep.2016.05.002.

- [27] A. Prasad, Existence of perpetual points in nonlinear dynamical systems and its applications, International Journal of Bifurcation and Chaos 25 (2) (2015) 153005.

- [28] G. Leonov, N. Kuznetsov, Hidden attractors in dynamical systems. From hidden oscillations in Hilbert-Kolmogorov, Aizerman, and Kalman problems to hidden chaotic attractors in Chua circuits, International Journal of Bifurcation and Chaos in Applied Sciences and Engineering 23 (1), art. no. 1330002. doi:10.1142/S0218127413300024.

- [29] N. Kuznetsov, G. Leonov, T. Mokaev, A. Prasad, M. Shrimali, Finite-time Lyapunov dimension and hidden attractor of the Rabinovich system, Nonlinear Dynamics 92 (2) (2018) 267–285. doi:10.1007/s11071-018-4054-z.

- [30] N. Kuznetsov, T. Mokaev, O. Kuznetsova, E. Kudryashova, The Lorenz system: hidden boundary of practical stability and the Lyapunov dimension, Nonlinear Dynamics 102 (2020) 713–732. doi:10.1007/s11071-020-05856-4.

- [31] N. Kuznetsov, T. Mokaev, V. Ponomarenko, E. Seleznev, N. Stankevich, L. Chua, Hidden attractors in Chua circuit: mathematical theory meets physical experiments, Nonlinear Dynamics 2022/12/21 (2022) 1–29. doi:10.1007/s11071-022-08078-y.

- [32] D. Dudkowski, A. Prasad, T. Kapitaniak, Perpetual points and periodic perpetual loci in maps, Chaos 26 (2016) 103103.