Estimating the loss of economic predictability from aggregating

firm-level production networks

Abstract

To estimate the reaction of economies to political interventions or external disturbances, input-output (IO) tables — constructed by aggregating data into industrial sectors — are extensively used. However, economic growth, robustness, and resilience crucially depend on the detailed structure of non-aggregated firm-level production networks (FPNs). Due to non-availability of data little is known about how much aggregated sector-based and detailed firm-level-based model-predictions differ. Using a nearly complete nationwide FPN, containing 243,399 Hungarian firms with 1,104,141 supplier-buyer-relations we self-consistently compare production losses on the aggregated industry-level production network (IPN) and the granular FPN. For this we model the propagation of shocks of the same size on both, the IPN and FPN, where the latter captures relevant heterogeneities within industries. In a COVID-19 inspired scenario we model the shock based on detailed firm-level data during the early pandemic. We find that using IPNs instead of FPNs leads to errors up to 37% in the estimation of economic losses, demonstrating a natural limitation of industry-level IO-models in predicting economic outcomes. We ascribe the large discrepancy to the significant heterogeneity of firms within industries: we find that firms within one sector only sell 23.5% to and buy 19.3% from the same industries on average, emphasizing the strong limitations of industrial sectors for representing the firms they include. Similar error-levels are expected when estimating economic growth, CO2 emissions, and the impact of policy interventions with industry-level IO models. Granular data is key for reasonable predictions of dynamical economic systems.

keywords:

production networks , supply chain disruptions , shock propagation , resilience , firm heterogeneity , economic dynamics

Supplier-buyer relationships between economic agents such as firms and companies — the production network (PN) — constitutes the backbone of every economy. The PN is crucial for understanding and predicting central economic processes, including innovation, growth, development, adaptation, and transition. The network structure of the PN, and its ability to change, fundamentally determine how economies respond to severe crises, policy interventions, supply chain disruptions, or shocks in general. The decisions of firms largely determine the way the PN operates, restructures over time, or how it adapts to changes in global markets, their environment, and society. These decisions include what and how much to produce, the combination of material inputs and technology, prices, who to hire, how to finance production and innovation, and — importantly — how to react to crises and shocks like, for example, to natural disasters, loss of essential suppliers, wars, pandemics, trade wars, or economic sanctions. The decisions of firms cause the PN to constantly change and hence alter its systemic features such as its efficiency, robustness, or resilience.

So far the study of economic processes on and the systemic features of PNs has yielded fascinating insights. PNs determine and constrain the paths of future economic growth of regions and countries (Hidalgo et al., 2007; Neffke et al., 2011). The position of industries within the national and international PN is predictive of price trends, changes in productivity, and future economic growth (McNerney et al., 2022). The ways economic shocks affect the agents of an economy depend on the PN. Firms that fail might be essential suppliers for other firms, which have to stop their production as a consequence (Ivanov et al., 2014; Yan et al., 2015). Consequently, production disruptions can cascade, similarly to financial contagion (Battiston et al., 2012; Glasserman and Young, 2016; Diem et al., 2020; Thurner, 2022). In this context it is important to mention that PNs can amplify micro-level sector shocks, to cause fluctuations of macro-economic relevance (Acemoglu et al., 2012; Carvalho and Tahbaz-Salehi, 2019; Moran and Bouchaud, 2019). The COVID-19 pandemic showed that models utilizing PNs can produce high quality forecasts of the economic effects of lock-downs (Pichler et al., 2022). Tightly connected to shock propagation in PNs is the topic of the resilience of countries and industries with respect to economic shocks (Henriet et al., 2012; Contreras and Fagiolo, 2014; Klimek et al., 2019; Han and Goetz, 2019; Martin and Sunley, 2015). PNs are directly linked with the environment and the climate crisis (Willner et al., 2018); they determine the CO2 emission levels of industries and countries (Wiedmann, 2009; Davis and Caldeira, 2010; Wiedmann et al., 2015), and in the other direction, natural disasters may lead to direct and in-direct economic damages that need to be quantified (Hallegatte, 2008; Otto et al., 2017; Colon et al., 2021). Finally, PNs are an integral part of national accounting of almost every economy (Horowitz et al., 2006; Eurostat, 2008; Mahajan et al., 2018), and serve as essential inputs for growth forecasts, employment projections, and estimates for policy interventions.

However, the PNs behind these insights are generally accessible only on an aggregated level in the form of industry-level input-output tables (IOTs) that record how the entire output of one industry enters as a production input into other industries. For almost a century, IOTs have been used to represent countries’ PNs (Leontief, 1936; Miller and Blair, 2009). They are widely available and highly standardised (Eurostat, 2008; Mahajan et al., 2018), so that they can be globally connected (Dietzenbacher et al., 2013; Yamano and Ahmad, 2006), thus, enabling the study of global PNs (Timmer et al., 2015; Otto et al., 2017; Klimek et al., 2019). Typically, the dimensionality of IOTs ranges from 56 industries, e.g., in the world input output database 2016 release (Dietzenbacher et al., 2013; Timmer et al., 2015)), to 405 sectors, as in the US-American economy (Bureau of Economic Analysis, benchmark input-output statistics) (Horowitz et al., 2006). Industry-level IOTs are a cornerstone of economic research and modelling. However, industry-level production networks (IPNs), such as IOTs, are highly aggregated representations of the economy and can not capture the details of the supply-chain relations between firms. The aim of this paper is to demonstrate that these details (manifesting themselves in significant inhomogeneities) are often essential, and their omission can be a source of considerable errors in economic predictions.

Studying firm-level production networks (FPNs) has been almost impossible until recently, when large-scale FPNs that include (almost) all firms and (almost) all their supply links have become available for countries such as Japan (Fujiwara and Aoyama, 2010) (1.1 million firms, 5.5 million links), Belgium (Dhyne et al., 2015) (0.8 million firms, 17.3 million links), or Hungary (Borsos and Stancsics, 2020) (0.25 million firms, 1.2 million links); for a review see (Bacilieri et al., 2022). Subsequently, new methods have been developed to reconstruct FPNs (Brintrup et al., 2020; Wichmann et al., 2020; Reisch et al., 2022; Ialongo et al., 2022; Kosasih and Brintrup, 2022; Mungo et al., 2023; Mungo and Moran, 2023). Based on this firm-firm supply network data, novel insights are gained on the effects of shock propagation after natural disasters (Inoue and Todo, 2019; Carvalho et al., 2020), on interactions of the financial system with the FPN (Demir et al., 2022; Huremovic et al., 2020; Borsos and Mero, 2020), and quantifying systemic risk contributions of individual firms in an economy have become possible (Diem et al., 2022). Further, the importance of indirect exposures of firms to imports and exports through the FPN was shown in (Dhyne et al., 2021), the origins of firm-size heterogeneity identified (Bernard et al., 2022), and the question of how price changes (inflation) propagate through the FPN was understood (Duprez and Magerman, 2018).

Aggregating FPNs containing millions of firms to IPNs consisting of a few dozens of industries leads to a massive loss of information on production processes and to possibly substantial biases, as this was the case even when aggregating (the already aggregated) IOTs (Kymn, 1990; Su et al., 2010; Lenzen, 2011). Before we illustrate two severe problems that emerge when aggregating firms and their supply relations into IPNs, we specify the necessary notation.

The IPN consisting of industries is represented by the weighted directed adjacency matrix, , where, a link, , denotes the sales of goods or services (price times quantity) from industry to industry for a given time period. Figure 1a shows an example, , with industry sectors, where, e.g., industry 3 buys inputs needed for its production process from industry 2 and sells its output to sectors 1 and 5. Colors represent the different industries and link weights indicate sales volume. Figure 1b shows the corresponding FPN, , with firms. A link, , denotes the sales of firm to firm for the same time period. Every firm, , belongs to one of the industries, specified by the element of the industry classification vector, , where, . In the example, firm within industry () is denoted by , and e.g., firms , and of sector 2 sell to firms and of sector 3. Due to data constraints we assume that each firm only produces one product, corresponding to its industry classification, , as in (Henriet et al., 2012; Inoue and Todo, 2019; Diem et al., 2022). We construct the IPN, , by aggregating all product flows between firms from the respective industries, e.g., and more generally .111Official IOTs are constructed differently and are based on surveys and other data sources (Eurostat, 2008; Miller and Blair, 2009). The total number of sales of firm to all other firms in the FPN, are measured by its out-strength, . It is a proxy for firm ’s output (amount produced). The in-strength, , represents all purchases of from other firms.

Problem 1: Aggregated industries are not representative

Figure 1b demonstrates how aggregation causes the first problem. and of sector have no overlap in their customers’ industries; sells only to firms in sector 1, and sells only to firms in sector 5. Aggregation to the industry-level erases this information and industry 3 sells equally to industry 1 and industry 5; see Fig. 1a. This means that the output vector of industry 3 is not representative of the output-vectors of the firms it contains. Similarly, the IPN, , is not representative of the FPN, .

Problem 2: Aggregation mis-estimates economic dynamics

The second problem is that aggregation leads to a mis-estimation of firm-level economic dynamics. Figure 1 illustrates how the mis-estimation of production losses arises by comparing the same production shock propagating on the industry-level network, , an the firm-level, . We compare three scenarios. Figure 1a shows scenario 1, a 25% initial disruption of industry 2 (blue X), at time . The production of sector 2 drops by 25% (indicated by the bar to the right filled 25% blue), and the production level, , is . This initial shock is specified by the vector of remaining production levels, . Then, the shock spreads downstream (blue edge) to sector 3 at (25% production loss, ), and at to sectors 1 (12.5% production loss, ), and 5 (16.7% production loss, ).222The index , denotes the “internal” time steps of the shock propagation model, not calendar time. The shock propagates, as industries 3, 1, and 5 lack inputs for their production processes. Note that the 25% disruption of industry 2 could originate from various combinations of individual shocks to firms, and , in industry 2. Figure 1b shows scenario 2, the 100% disruption of firm 3, , (red X, red bar). The production of firm 3 drops to 0%, i.e., a total operational failure (). The firm-level shock is specified by the remaining production level vector , where and , for all . The disruption propagates downstream (red edge) to (50% production loss, ), and further to firms and (25% production loss, ). Aggregating the production losses of firms yields a loss of 25% for industries 1, 2 and 3 and a 0% loss for industries 4 and 5. Figure 1c shows scenario 3, the propagation of a 100% disruption of firm 5, , (red X, red bar). Aggregating the resulting production losses yields a loss of 25% for industries 2 and 3, a 0% loss for industries 1 and 4, and a 33% loss for industry 5. Figure 1d compares for each industry, , (x-axis) the industry-specific production loss, , (y-axis), across the three scenarios, 25% shock to sector 2 (blue ‘+’), 100% shock to firm 3 (red squares) and firm 5 (red circles). When aggregated both firm-level shocks yield the industry-level shock of 25% disruption of industry 2 and for industry 3 and 4 the production losses form shock propagation are also the same (0.25, and 0, respectively) — the symbols ‘+’, circle, and square overlap. However, the output losses of sectors 1 and 2 are vastly different across the three shocks — ‘+’, circle, square do not overlap. The FPN-based losses vary from 0 to 0.25 for sector 1 and from 0 to 0.33 for sector 5, whereas the aggregation-based IPN losses are the same for both firm-level shocks, 0.125 for sector 1 and 0.167 for sector 5. The IPN-based loss mis-estimates the FPN-based losses by 100%. Other network dynamics such as growth, innovation, or productivity spill overs, — happening to a large extent at the firm- and not the industry-level — are potentially affected in similarly drastic ways.

In this paper we quantify the relevance of these two problems by utilizing a unique data set that allows us to observe almost every firm-level supply chain relation of the entire production network of Hungary, containing 243,399 firms and 1,104,141 links in 2019, see Data and Methods. First, we assess how representative industry-level production networks are of real-world firm-level production networks. We do that by quantifying the intra-sector overlaps of firms’ input- and output vectors. Second, we quantify the estimation-errors of economy-wide and industry-specific production losses that arise when using industry-level production networks to approximate firm-level shock propagation dynamics. Firm-level labor data with monthly time resolution enables us to realistically estimate the size of the COVID-19 shock for individual firms in the beginning of 2020. Then, we compare the production losses from propagating a realistic COVID-19 shock and 1,000 synthetic shock realizations, either on the firm- or the industry-level production network. We sample the synthetic shocks such that they are of the same size when aggregated to the industry-level, but affect firms within industries differently. This feature allows us to clearly show the effects of intra-sector heterogeneity in firms’ input-output vectors for estimating production losses, while controlling for size and industry effects.

Results

Quantifying input and output vector overlaps of firms

Large overlaps (firms within sectors are similar) would suggest that aggregation to the industry-level does not lead to large distortions of network dynamics. Small overlaps (firms within sectors are heterogeneous) would lead to potentially large aggregation effects. First, we aggregate for every firm its firm-level in- and output vector to the industry-level (NACE2), see SI Section 1. Second, for each pair of firms, , and, , within a given NACE2 industry we calculate the input overlap coefficient (IOC) and the output overlap coefficient (OOC) as,

| (1) |

| (2) |

where is the number of NACE2 industries (here 86), and and are the normalized input- and output vectors of firm, , respectively, see SI Section 1. specifies the fraction of total inputs, and buy from the same industries. It quantifies the common exposure of and to supply shocks originating from the same upstream industries and indicates the fraction of a demand shock that is forwarded by and to the same upstream industries. , specifies the fraction total sales, and sell to the same industries. It quantifies the common exposure of and to demand shocks originating from the same downstream industries and indicates the fraction of a shock that is forwarded by and to the same downstream industries. For more information, see SI Section 2. In Fig. 1b, the relative input vector is for firm 10 and for firm 11, hence, . The propagation of upstream shocks by 10 and 11 will only overlap by 50% (sector 3), while 50% spread to distinct sectors.

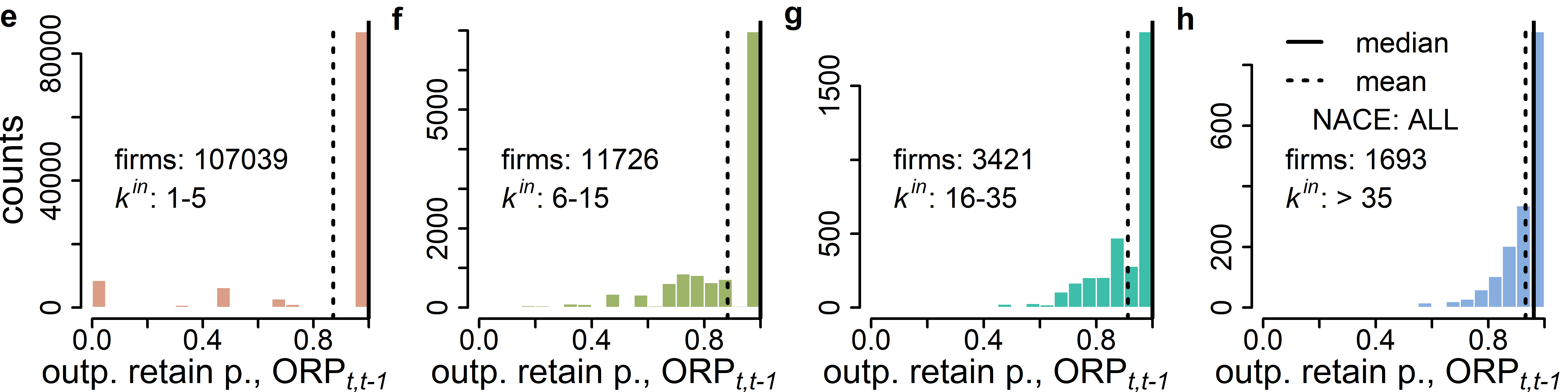

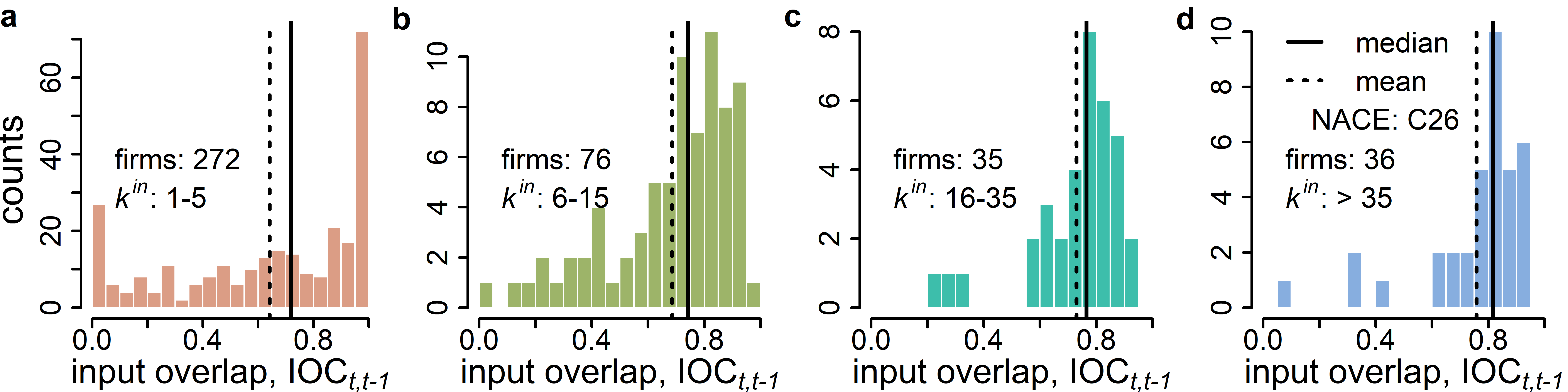

Firms within industries are highly different

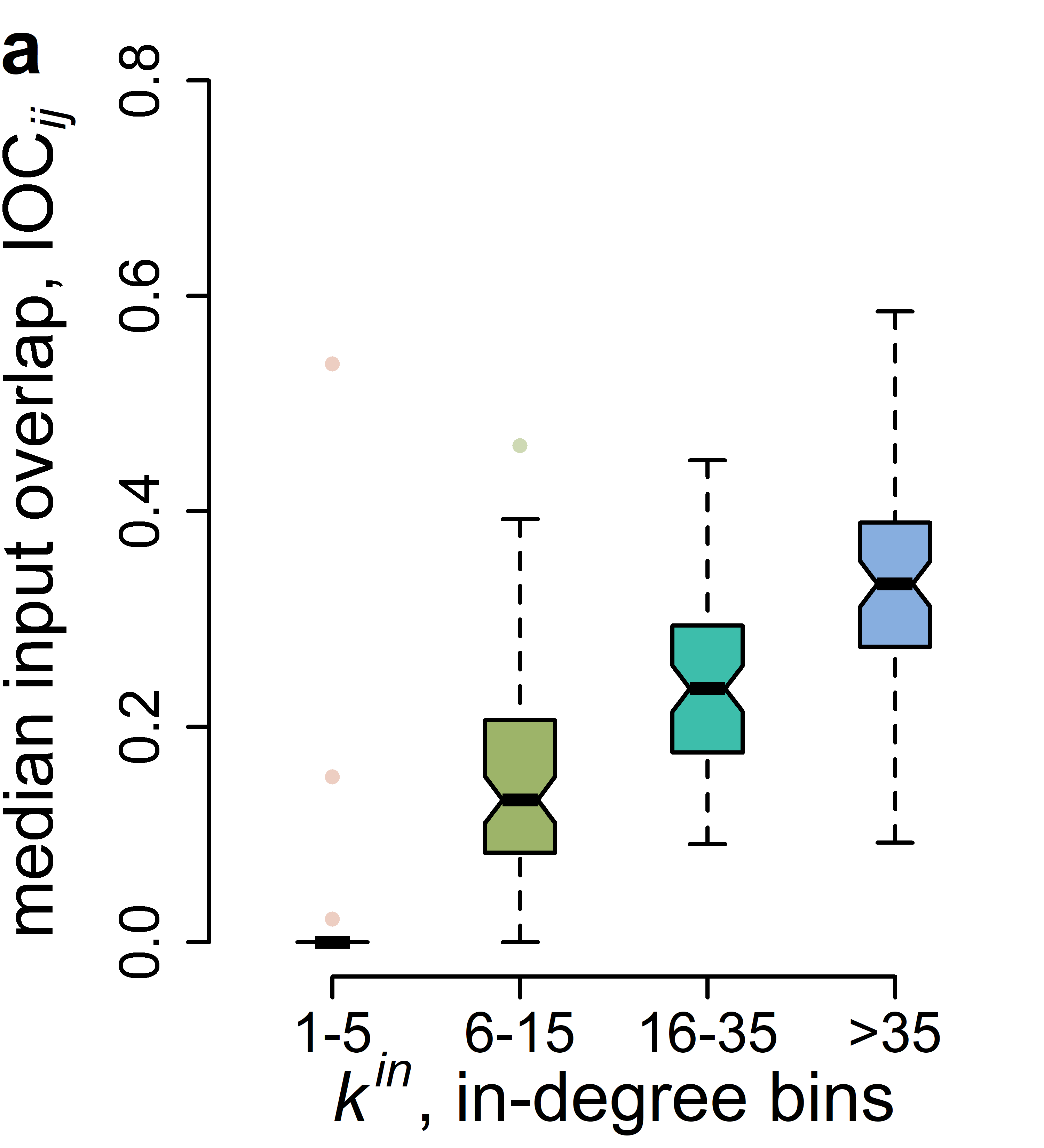

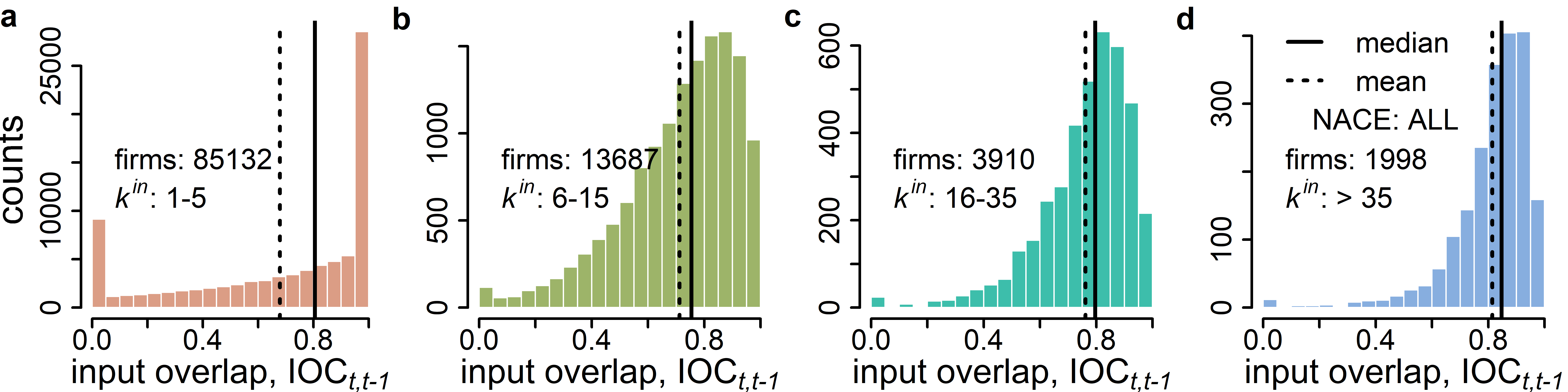

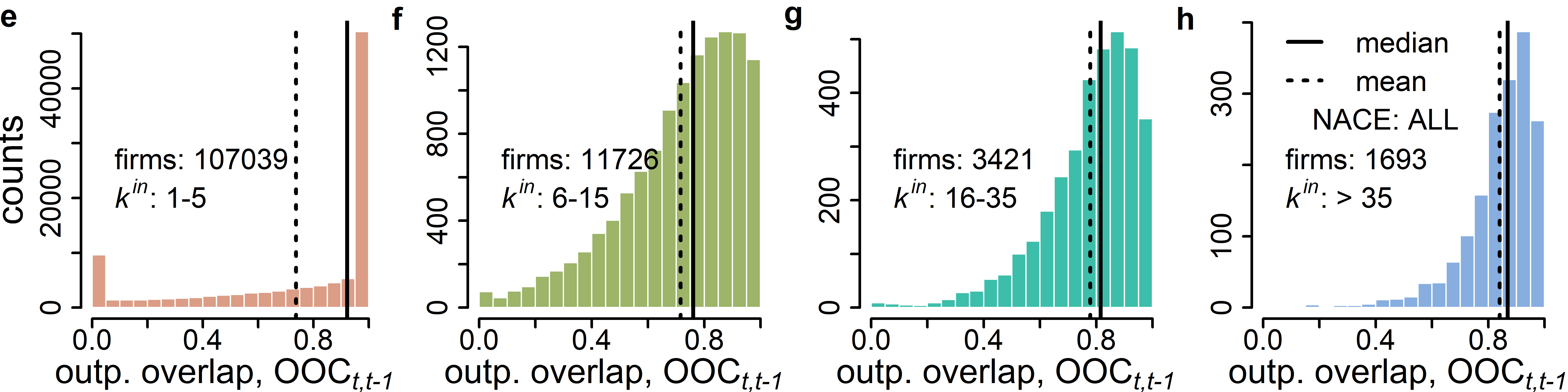

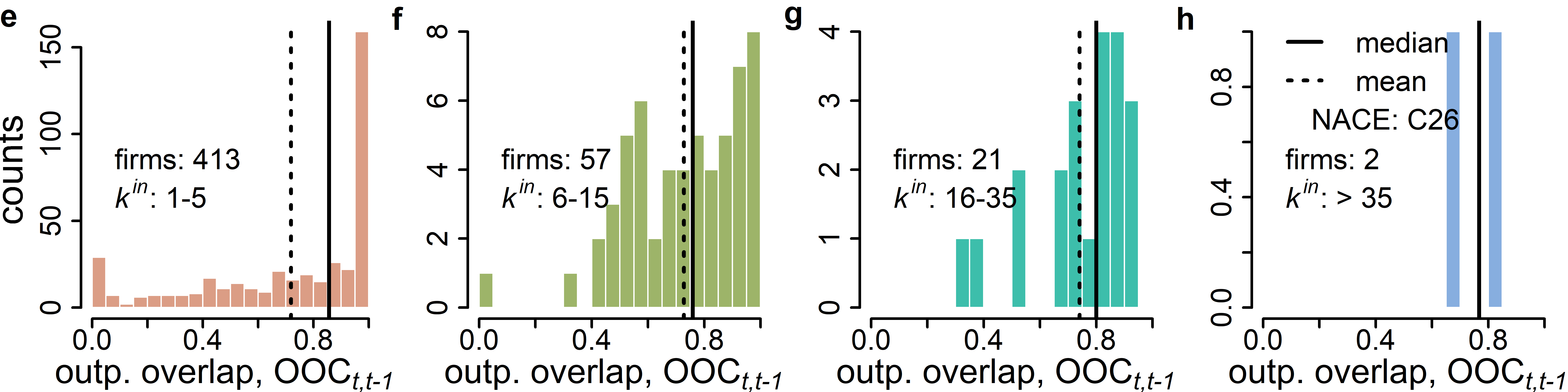

We show the distribution of the pairwise similarities and for all firms in NACE2 industry C26, ‘Manufacture of computer, electronic and optical products’ in Fig. 2. Figure 2a-d show the distributions stratified by their number of suppliers (in-degree, ). Figure 2a contains all firms that have 1 to 5 suppliers, Fig. 2b 6 to 15, Fig. 2c 16-35, and Fig. 2d more than 36. The average similarity of firms’ input vectors is small across all four groups for which the median (vertical solid line) and mean (dashed line) overlaps are 0, 0.121, 0.199 343, and 0.141, 0.196, 0.239, 0.343, respectively. Clearly, the average similarity of input vectors is increasing for firms with more suppliers. The distribution for firms with one to five suppliers (Fig. 2a) is bi-modal, most pairs of firms have either almost no overlap or almost perfect overlap. For firms with a few suppliers (2b-c) the distributions become unimodal and right skewed, implying that very high similarities appear in the right tail, but are not very frequent. Finally, the distribution of input overlaps for firms with more than 35 suppliers are centered around 0.34 (2d). Figure 2e-h show the distribution of the pairwise output overlap coefficients, OOCij, grouped according to their number of buyers (out-degree, ). The bin sizes are the same as before. The average similarity of output vectors is visibly smaller than those of input vectors. The median and mean overlaps for the respective out-degree bins are 0, 0.025, 0.119, 0.119 and 0.054, 0.087, 0.169, 0.143, respectively. The distributions are more concentrated towards low overlaps and remain right skewed for all out-degree bins.

Similarity of firms is low and varies across industries

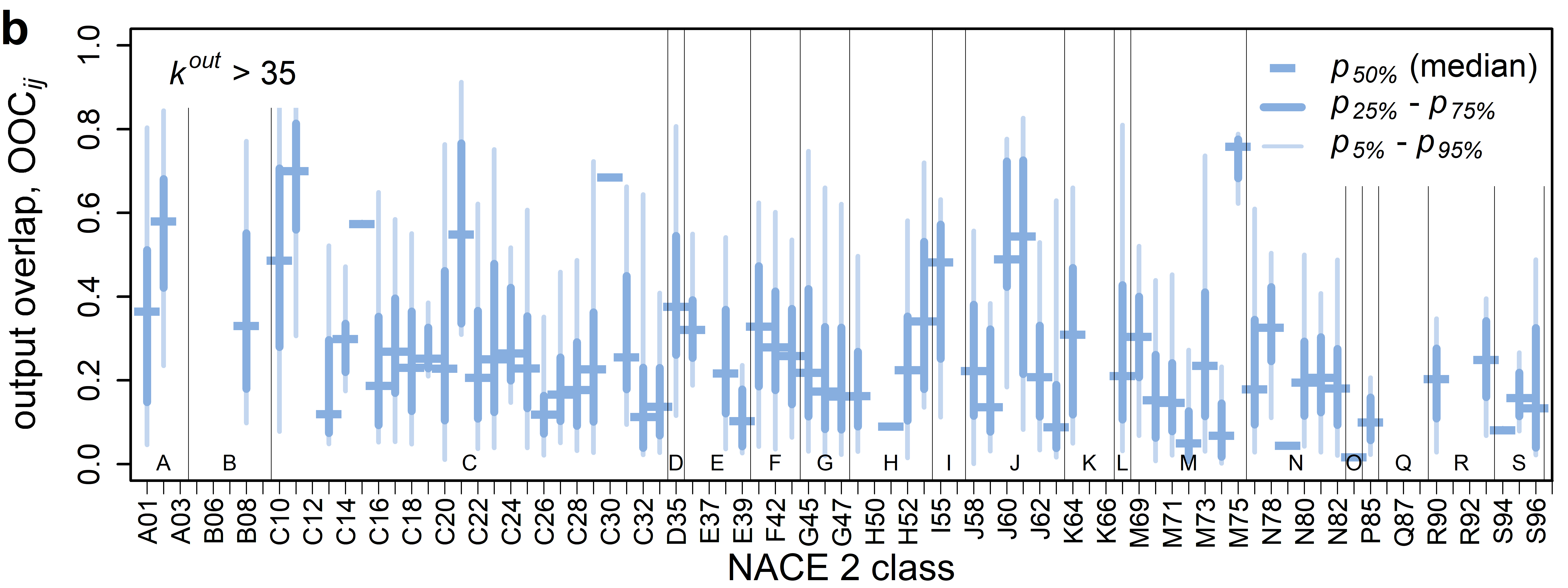

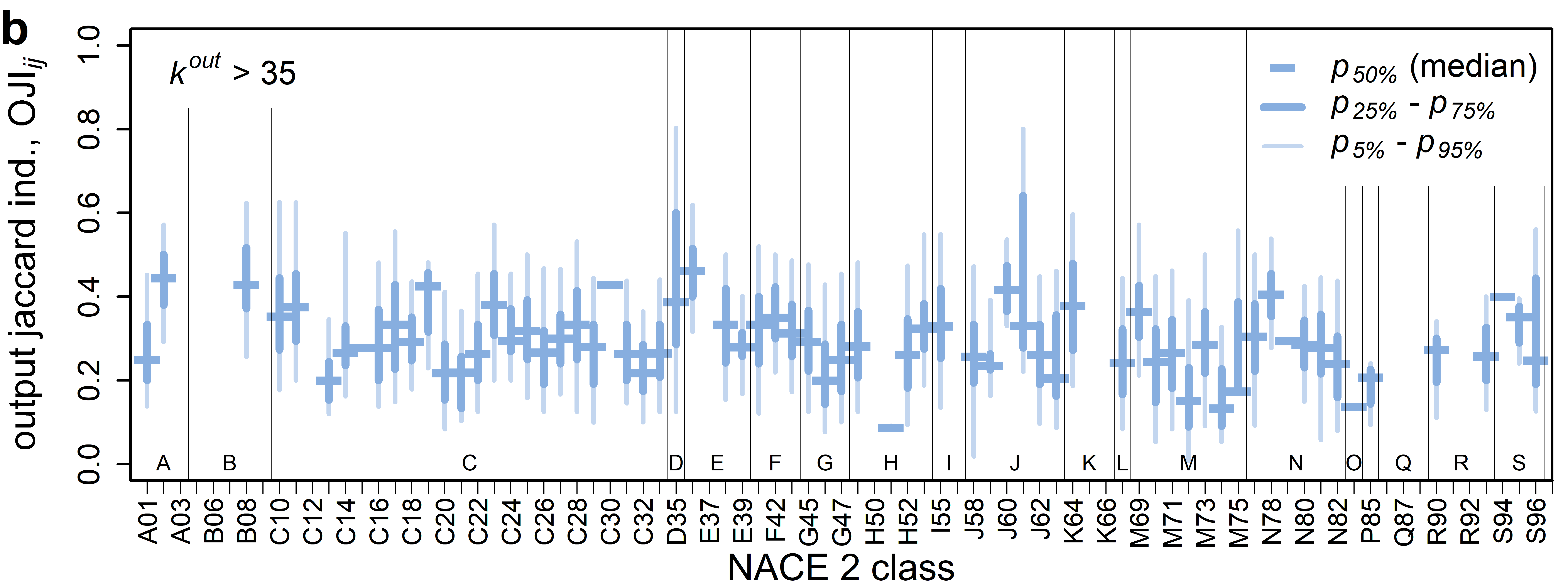

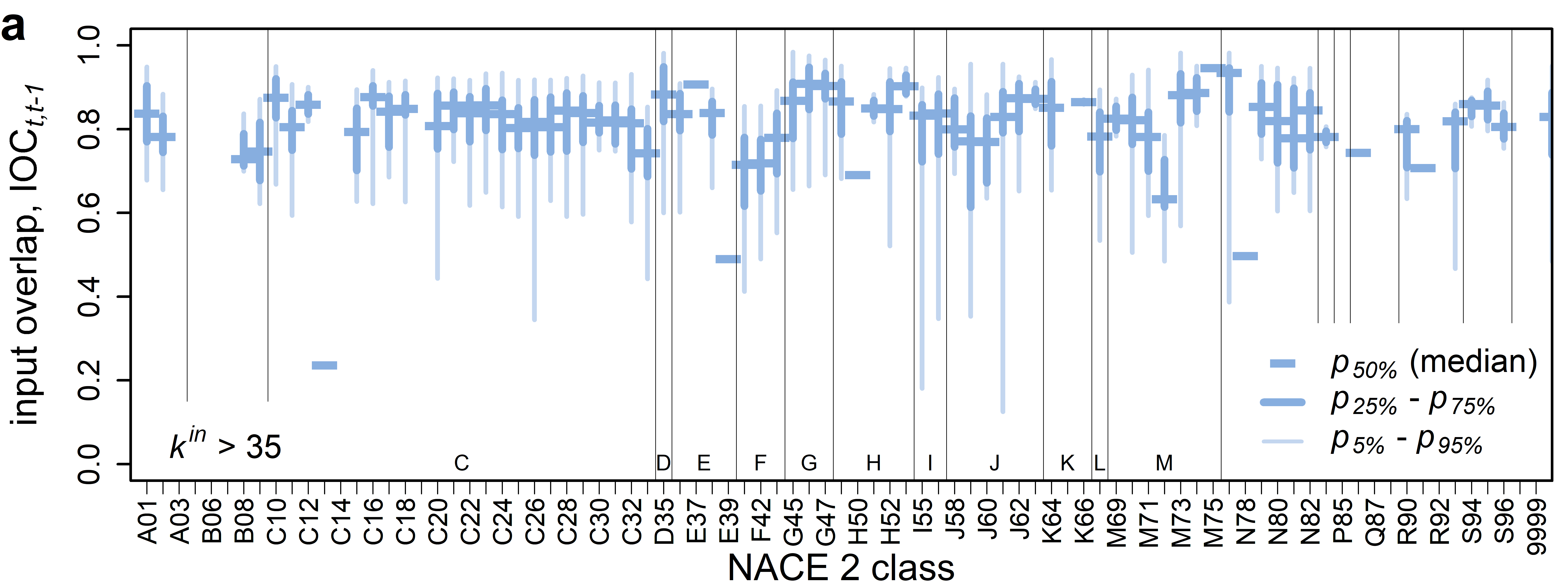

We now show the summary statistics of the pairwise IOCij and OOCij distributions for all NACE2 industries in Fig. 3, in particular, the mean, 5%, 25%, 50% (median) 75%, and 95% percentiles. Only firms with more than 35 suppliers and buyers are included. The x-axis shows the 86 NACE2 codes present; the y-axis represents the overlap coefficients, each boxplot corresponds to one NACE2 class. Dark blue horizontal bars indicate the median, (), thick dark blue vertical lines indicate the inter-quartile range ( – ), thin light blue vertical lines indicate error bars ( – ), and thin vertical black lines separate NACE1 class affiliations. Empty columns indicate that less than 2 firms exist in the respective sector and degree bin. Figure 3a shows that the low input overlaps of industry C26 are not just an outlier. The mean of the mean (median) input overlaps, IOCij, across NACE2 industries is 0.35 (0.33) and the standard deviation of mean (median) input overlaps is 0.084 (0.102). This indicates that relatively low input overlaps are the norm with few outliers. The highest median IOCij are found in the ‘agricultural industry’ (A1-A2), ‘water collection, treatment and supply’ (E36) and in the ‘transport’ sectors (H53), whereas the lowest median IOCij are found in service sectors, such as ‘other professional’, ‘scientific and technical activities’ (M74), ‘travel agency, and related activities’ (N79), ‘sports activities and amusement and recreation activities’ (R93) and ‘activities of membership organisations’ (S94). The average standard deviation is 0.156. The standard deviation of standard deviations is small 0.048, and the length of error bars appears to be relatively homogeneous across sectors, suggesting that the variation of pairwise input overlaps, IOCij, is relatively constant across sectors. Figure 3b shows that output overlaps, OOCij, are on average lower than the input overlaps, but have a higher variation across industries. The mean of the mean (median) output overlaps, OOCij, across all NACE2 industries is 0.282 (0.257) and the standard deviation of mean (median) output overlaps is 0.147 (0.161), indicating that relatively low output overlaps are the norm with several outliers. For more details, see SI Section 3.

In SI Section 4 we show that for the degree bins 1-5, 6-15, and 16-35 the mean over mean (median) input overlaps, are 0.132, (0.009) 0.202 (0.148), 0.269 (0.241), respectively; the respective values for output overlaps are slightly lower. As for industry C26, generally input and output vectors of firms within industries become more homogeneous with the number of suppliers and buyers. In SI Section 5 we show the same analysis for NACE4 industries based on NACE4-level input-output vectors and find that the intra-sector variation of input-output vectors is higher than at the NACE2 level. In SI Section 6, we show that our results are robust with respect to the choice of the similarity measure. In SI Section 7 we show that the similarity of input and output vectors of firms over time is substantially higher than intra-industry similarities. Individual firms show significant similarity from one year to the next, as expected, while the observed low level of intra-industry similarities capture fundamental heterogeneities.

Overall, we clearly see that input and output overlaps of firms within industries are surprisingly low, across industries and across degree bins. The high level of heterogeneity of input-output vectors of firms within industries shows that for most industries sector-level aggregates are practically not representative for the actual firm-level supply chain inter-linkages and very likely will mis-represent dynamic processes occurring on the firm-level network.

Production loss mis-estimations from aggregating networks

We now compare the economy-wide production losses for Hungary caused by a COVID-19 shock propagating once on the firm-level production network (FPN), and once on the industry-level production network (IPN). Based on firms’ actual employment reductions, the shock realistically captures how individual firms were affected by COVID-19 in the beginning of 2020. The shock is represented by the vector, , where, , is the relative reduction of firm ’s labor input from January to May 2020, , and is the number of ’s employees in the respective month. The remaining production capacities of firms (after the shock) are given by the vector , where, , is the remaining fraction of firm ’s production, e.g., if reduced its employees by 20%, its remaining capacity is . Aggregating the capacities, , of all firms in sector gives sector ’s remaining production capacity, . For details on shock construction and aggregation, see Data and Methods.

Following the COVID-19 shock, we simulate how the adaptation of firms’ supply- and demand-levels propagate downstream and upstream along the PN, once on the firm-level and once on the industry-level. We employ the simulation model of (Diem et al., 2022), where each firm (industry) is equipped with a generalized Leontief production function, see Data and Methods for details. The simulation stops when the production levels of firms have reached a new stationary state at (model-internal) time, . Every firm (or sector ) has a final production level, (), that depends explicitly on the details of the shock (). It represents the fraction of the original production, , firm (sector ) maintains after the shock has propagated. We define the FPN-based economy-wide production-loss as

| (3) |

It is the fraction of the overall revenue in the network (measured in out-strength, , see Data and Methods) that is lost due to the shock and the in-direct effects of its propagation. The IPN-based economy-wide production-loss, , is defined accordingly, see Eq. [9] in Data and Methods.

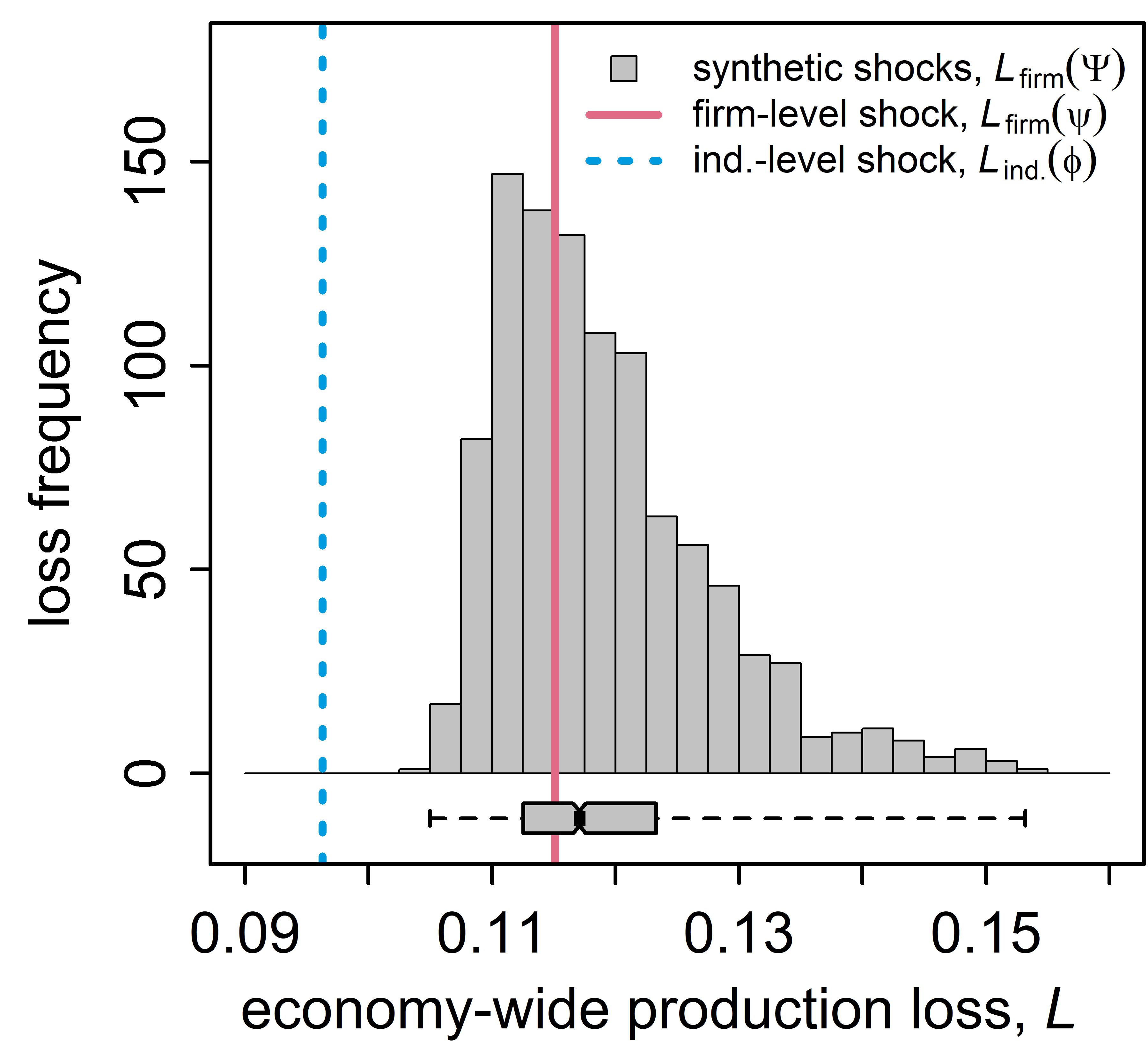

Figure 4 compares the production losses for the two simulations, FPN and IPN. The propagation on the FPN leads to a production loss, , of 11.5% (red solid line), while propagation on the IPN yields a loss, , of 9.6% (blue dashed line). Aggregated industry-level shock propagation substantially underestimates the production losses caused by firm-level shock propagation dynamics, for the COVID-19 shock, , by 16.5%. We quantify the size of mis-estimations if the firm-level shock was slightly different. We sample 1,000 distinct, synthetic realizations of the COVID-19 shock that are of the same size when aggregated to the industry-level, but affect firms within industries differently. For every sector, , we take the empirical distribution, , of firms belonging to that sector. Then, we sample for every company, , of sector a new value, , from this distribution, replace the old , and calculate the corresponding remaining production capacity vector, . In this way we generate the set of 1,000 synthetic capacity vectors, ; for the full algorithm, see SI Section 8. The resulting distribution of FPN-based economy-wide production-losses is shown as histogram and boxplot in Fig. 4. The losses vary strongly from 10.5% to 15.3% of economy-wide production, i.e. losses can vary by a factor of up to 1.46 for different initial shocks of the same size. The actual Hungarian GDP declined by 14.2% in Q2 2020 (OECD, 2023), showing that the losses obtained by our computations are within perfectly realistic bounds; a gross output estimate is not available for comparison.

Note that the 1,000 synthetic shocks propagating on the IPN always lead to the same economy-wide production-loss (9.6%, blue dashed line) because all firm-level shocks, , impact the industry-level production capacities by exactly the same amount, . On average the IPN based production losses underestimate FPN-based losses by 2.3% of the economy-wide production. In relative terms losses are on average underestimated by 18.7%. For 10% of the shocks the underestimation is even larger than 26.3% and the maximum underestimation is 37.1%. This tail of large losses is clearly visible in the histogram and is caused by shocks affecting systemically relevant firms stronger (Diem et al., 2022). The median and mean of the 1000 losses, , are 11.7% and 11.9%, respectively, and lie close to the FPN-based production loss, , based on the original COVID-19 shock, (red line).

Mis-estimating industry-specific production losses

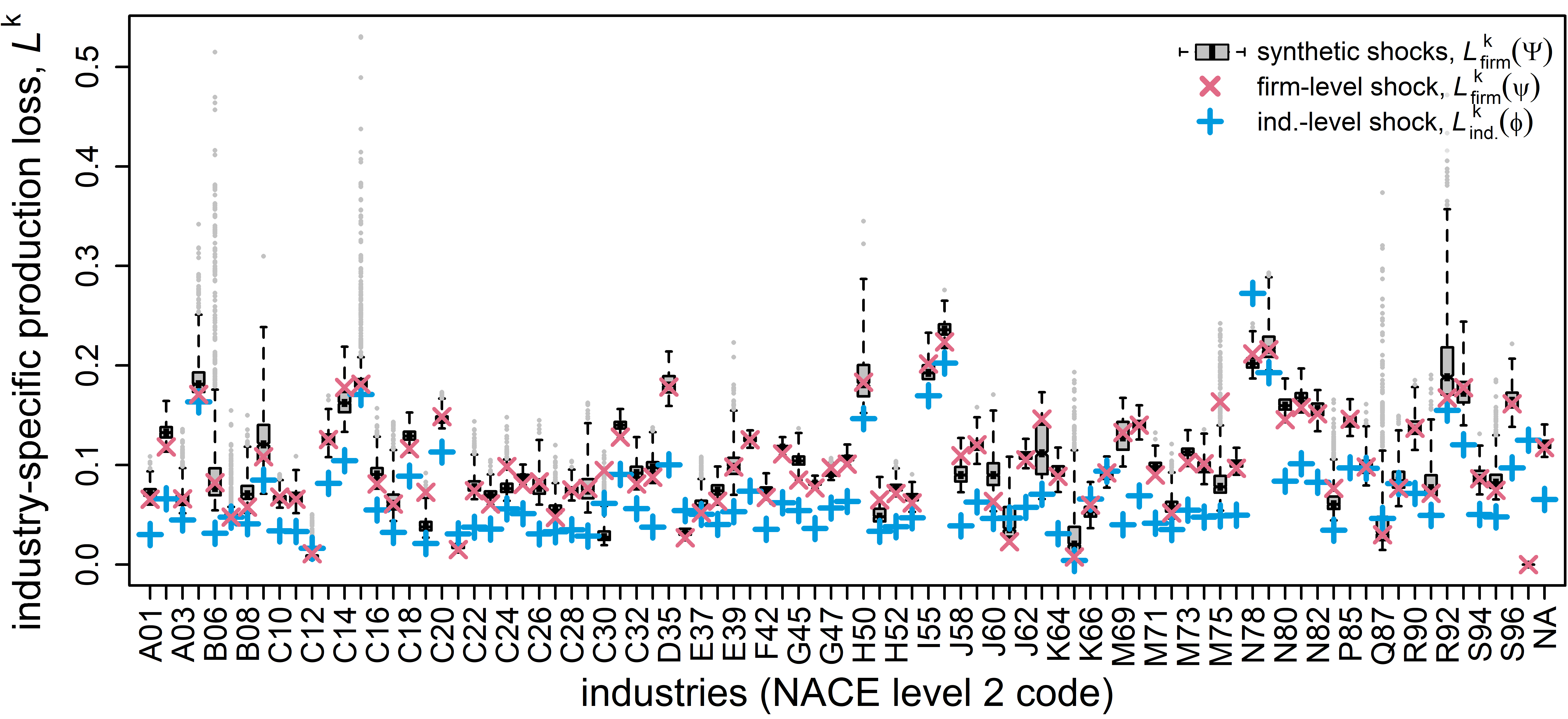

We now compare the IPN- and FPN-based production losses for every NACE2 industry separately. We define the FPN-based industry-specific production loss of industry, , in response to the COVID-19 shock, , as

| (4) |

It is the fraction of revenue (measured in out-strength) that firms in sector lost due to the direct and in-direct effects of the shock. The IPN-based industry-specific production loss, , is defined accordingly.

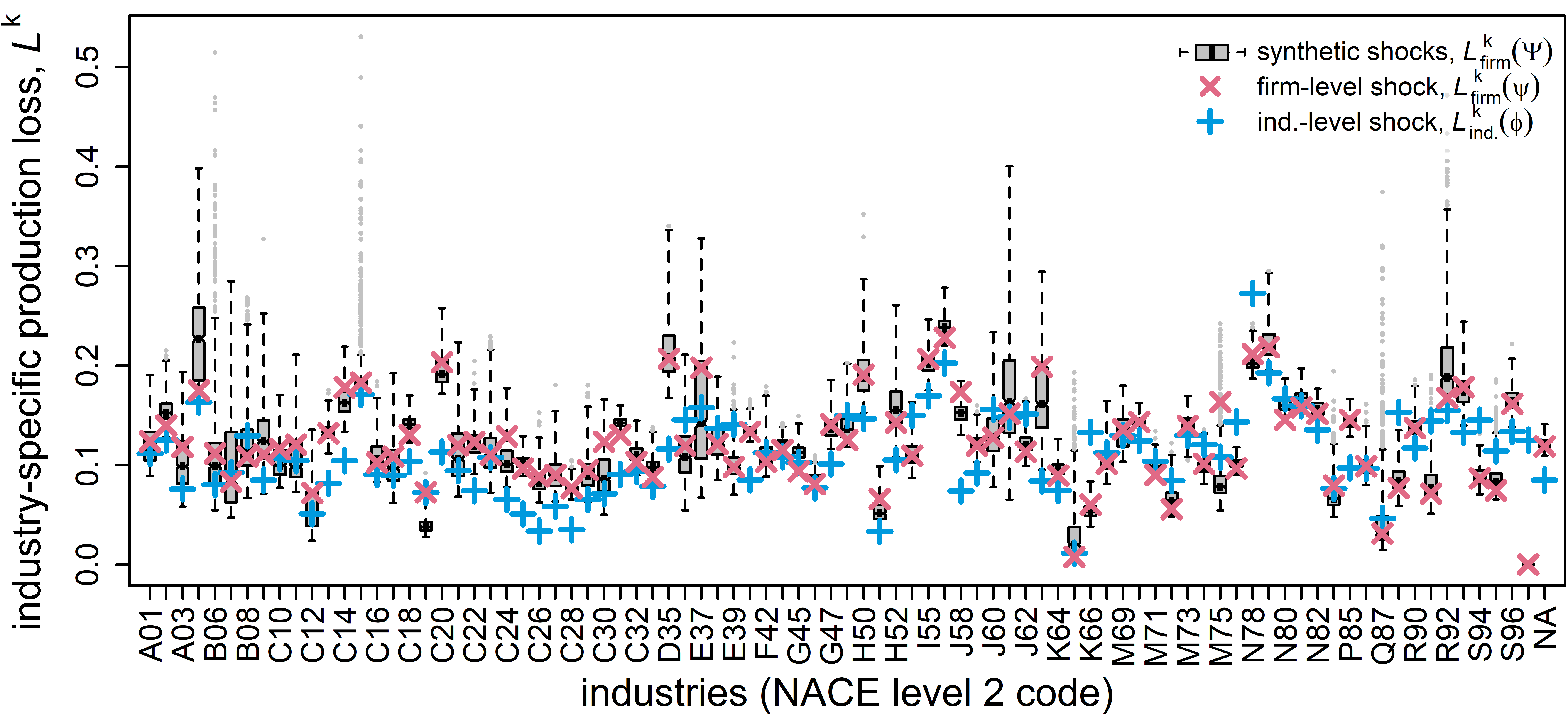

In Fig. 5 we show for each NACE2 industry the distribution of FPN-based production-losses, , caused by the 1,000 synthetic shocks as boxplot. The IPN-based production-losses, are indicated by the blue ‘+’es, the FPN-based production-losses for the original COVID-19 shock, , are given by red ‘x’es. It is clearly visible that for many industries losses vary strongly across the identically sized shocks, but also the variation between industries is noteworthy. For all but two industries (M73, N82), the production loss distributions are right skewed, few industries (B06, C15, K65, M75, Q87, and R92) have substantial outliers (grey dots) above 3 times the inter-quartile range. This means that for some particular shock realizations these sectors can suffer extremely large losses. The minimum and maximum values of production losses for different initial shocks can differ by factors of up to 9.5 (B06), 6.0 (B07), 5.7 (C12), 6.2 (J61), 41 (K65), or 25.9 (Q87). The median (mean) ratios of maximum to minimum loss is 2 (3.2). This variation in production losses across different shocks is inaccessible when using aggregated IPN data; it can not be inferred from the blue ‘+’es. The large variations emerge as different shocks affect firms at different positions in the supply networks that have different systemic relevance (Diem et al., 2022). IPN-based losses (‘+’es), lie frequently below the lowest FPN-based loss, while FPN-based COVID-19 losses (‘x’es) lie within boxplots. The industries where IPN-based shock propagation under-estimates output losses most are C26 (-59.5%), C28 (-53.5%), J58 (-51.3%), C25 (-50.3%), J63 (-47.8%), and C20 (-42.1%). Over-estimation of production losses from using IPN-based losses are highest for sectors, K66 (150%), C19 (87.4%), R91 (83.3%), Q88 (80%), S94 (65.4%) and E39 (42%). For other sectors, see SI Section 9. We calculate for each industry the mean absolute deviation and take the average across industries, which yields 30.2%.

Last, we consider the hypothetical case that shocks propagate on the same PN, but assuming that all firms have linear production functions, see SI Section 10. We find that the distribution of economy-wide production losses, , ranges from 9.5% to 10.8%. This is substantially less variation than when realistic non-linear production functions are used. As expected, the linear production function assumption makes the economy-wide production losses less dependent on which exact firms within industries are impacted by shocks. However, the variations of industry-specific production-losses, , are still very large for several sectors. This emphasizes immediately that in order to correctly estimate sector-level production losses it is crucial which firms are affected by shocks, even in the best-of-all worlds, where shocks would propagate linearly.

Discussion

Production networks are fundamental for explaining and predicting dynamical economic phenomena. For almost a century, these were only accessible as aggregated industry-level production networks (IPNs), usually represented as input-output tables (IOTs). Only recently, large scale firm-level production networks (FPNs), covering entire economies have become available. Based on a unique firm-level production network data set, containing almost all buyer-supplier links of the Hungarian economy, we demonstrated on the one hand that the aggregation of production networks to the industry-level can not be expected to yield anything close to correct predictions of dynamical processes, such as the propagation of short term shocks through production networks. On the other hand we showed that using firm-level supply networks instead, a much more realistic picture can emerge.

We first showcased that industries are not sufficiently representative of the firms they include, because firms within industries are highly heterogeneous wrt. the industries they buy from and sell to. Specifically, two firms within the same industry spend on average only 23.5% on inputs from the same industry, and sell on average only 19.3% of their revenues to the same industry. Even when two firms belong to the same industry their industry-level input and output vectors will differ substantially. Therefore, using industry-level production network data will likely cause substantial mis-estimations of dynamic processes actually occurring on the firm-level.

We next demonstrated that the aggregation of FPNs causes indeed large mis-estimations for economic shock propagation dynamics and the resulting production losses. The demonstration is based on a COVID-19 shock that is realistically calibrated with firm-level employment data and 1,000 synthetic COVID-19 shocks of the same size. While economy wide production losses, in response to the 1,000 shock scenarios, simulated on the FPN range from 10.5% to 15.3% (mean 11.9%), the corresponding IPN-based production losses are 9.6%. In the worst case scenario the underestimation amounts to 37.1%. For single industries the largest average mis-estimation of production losses range from -59.5% to 150%.

Implications for economic modelling and policy making

The presented results imply a range of immediate consequences for economic modelling, in particular for short-term economic dynamics such as shock propagation, but also more generally for the reliability of industry-level IO-models in the context of testing policy implications.

First, our findings make it crystal clear that the size of losses from shock propagation depends crucially on which exact firms are affected by the initial shock. Crises such as COVID-19, the war in Ukraine, or large natural disasters can affect firms within the same industry sectors and regions very differently and, hence, the exact materialization of the shock can lead to significantly different in-direct economic losses. Aggregated industry-level models, such as IO-models, can by design not account for this, potentially underestimating tail losses that appear when a group of systemically important firms receive shocks at the same time. Modelling impact propagation on firm-level production networks might significantly improve economic assessments of crises of this kind.

Second, our method for creating an ensemble of synthetic shock scenarios that are identical on the industry-level, but affect firms differently can be used to estimate realistic confidence intervals for economic impacts of crises. Experts can define a shock on the industry-level (as done routinely for IO-models) and obtain distributions of the quantity of interest for each firm, specific sectors or the whole production network. This approach could reveal which combination of shocks to individual firms causes particularly dangerous scenarios that would go unnoticed with industry-level models. This is useful for designing scenarios in economic stability stress tests.

Third, the presented framework extends well beyond shock propagation. Other forms of network dynamics that are certainly distorted by industry-level aggregation include economic growth, the estimation of CO2 emissions of economic activity, or the spread of price increases. Detailed future research on these topics, considering the details of firm-level production networks is necessary. These topics happen on larger time-scales and will be overlaid with other dynamics that were not covered here. These dynamics are most likely more complicated than the ones of short-term shock propagation and therefore it is reasonable to assume that the effects of aggregation are even stronger in these situations.

Fourth, specifically, for estimating CO2 emissions of industry sectors and countries, aggregating input-output tables causes substantial errors in emission estimates (Su et al., 2010; Su and Ang, 2010; Lenzen, 2011). Our results indicate, firms in the same NACE industries use very different inputs and sell to very different industries and therefore their resulting scope-3 emissions (indirect CO2 emissions along supply chains) can differ substantially. Firm-level data will be crucial for reliable and targeted CO2 emission estimates and for designing green transition enhancing economic policies that can target problematic firms (Stangl et al., 2023).

Fifth, in the past economic models, e.g. for assessing economic effects of natural disasters such, as (Henriet et al., 2012), have worked with the simplifying assumption that firms within an industry are the same wrt. their input and output vectors. Our results suggest that for estimating and predicting effects of natural disasters in the future more reliably, production network models should carefully feature firm-level heterogeneity within industries.

Limitations and future research

There is a list of limitations of the presented material. For self-consistency, the industry-level production network used here is simply the aggregation of a firm-level production network. IO tables are constructed with extensive survey methodologies and the available tables can differ (Borsos and Stancsics, 2020). However, also IO tables are aggregations of underlying firm- and establishment-level networks and are likely to be affected by the same problems and to a comparable extent.

Secondary NACE categories of firms are not contained in our dataset. Larger firms producing several different types of products (in potentially several establishments) are fully aggregated to their primary NACE category. This could lead to an over-estimation of heterogeneity of input and output vectors within industries. Future research should quantify the heterogeneity of input and output vectors of establishments used for creating IO-tables.

A potentially strong limitation is that we do not have information of firms’ international import and export links. Consider two firms in one sector, one imports a specific input and the other sources it domestically we would over-estimate the heterogeneity of their input vectors. However, for the Belgium production network it has been shown that only a small fraction of firms have direct import and export linkages (Dhyne et al., 2021).

In practice high quality economic data to calibrate industry-level economic models is widely available and some have achieved good forecasting performance (Pichler et al., 2022). To calibrate firm-level models, substantially larger amounts of data are needed. For example, quantifying how a shock (e.g. a natural disaster) affects hundreds of thousands of firms is substantially harder than for a few dozens of sectors. Firms within sectors do react differently, modelling their behavior realistically, involves many assumptions, but up to now data for calibration is scarce.

We demonstrated that for how shocks propagate details do matter. In our simulation model important non-linearities appear in the generalized Leontief production functions (GLPF) of companies. The calibration of firms’ GLPFs is currently a rough approximation combining firms’ NACE4 industry affiliation with an expert based survey for 56 industry sectors conducted in Pichler et al. (2022). The calibration of the GLPF needs refinement in the future, e.g., with large scale firm-level surveys.

Our results point out relevant open questions. Duprez and Magerman (2018) find large idiosyncrasies in price changes of producers within the same product categories. It would be interesting to see, whether these could be explained by the heterogeneity of firms’ input and output vectors. In the direction of IO tables, differences of Leontief multipliers for different aggregation levels of IO-tables with potential implications for predicting economic growth were reported (McNerney et al., 2022). It would be of interest to see how this extends across all scales to the firm-level. Heinrich et al. (2022) show that correlation structures found on the sector level do not hold on the firm-level. Also for this phenomenon the intra-sector heterogeneity of firms could be part of the explanation. The effects of of heterogeneities should also be checked for establishment level supply networks (Schueller et al., 2022).

General equilibrium models (Acemoglu et al., 2012; Carvalho and Tahbaz-Salehi, 2019; Magerman et al., 2016) were shown to depend on network measures such as Leontief multipliers or the ‘influence vector’. These are likely to be distorted from aggregating production networks to the industry-level. The sensitivity of results to aggregation could be investigated under a similar framework as the present one.

It has been shown that both industry (Acemoglu et al., 2012) and firm-level (Borsos and Stancsics, 2020) production network exhibit power-law scaling patterns. It would be fascinating to find out under what conditions they preserved under aggregation and — if not — would that explain the differences in shock propagation and other network dynamics? Another open question is, which network modules are particularly affected by aggregation? And, finally, since our data shows that input and output vectors of firms remain relatively stable from one year to another. This raises the question of how fast can production networks adapt to technological change? And would an aggregate perspective of production networks under- or over-estimate the speed of adaption in the network?

Further remaining questions include input combinations. The reported large heterogeneity of inputs and outputs of firms within the same sectors implies that the same output can be produced from different input combinations. If one input is no-longer available this might affect a certain company, while others continue production. In the longer term, if one input is becoming structurally more expensive firms could change the production to mimic competitors that use a different input mix to produce the same good. This raises the question if this large amount of heterogeneity in input and output vectors is actually a source of resilience in the production network, or just an inefficiency in knowledge transfer?

To conclude, in this work we showed the importance of modelling production networks on the firm-level. However, currently data on firm-level production networks exist only in very few countries, and is rarely available to research. This work shows how necessary it is to make these data usable for researchers and policy institutions. Complementing traditional industry-level models with new models that are specifically designed for firm-level data is a great opportunity forward for both reliable policy making and progress of scientific research on resilience and transformability of the current economy.

Data and Methods

Data

The Hungarian FPN, , is based on the 2019 VAT micro-data of the Hungarian Central Bank (Borsos and Stancsics, 2020; Diem et al., 2022). Supply links between two firms are present if the tax content of the transactions was above 1 million Forint for 2018Q1-Q2 and 100,000 Forint for 2018Q3-2019Q4 (approx. 250 euros). The link weight, , represents the monetary value of all transactions between the two firms in the given year. We filter the data for stable supply links and keep a link if at least two supply transactions occurred in two different quarters, i.e. we exclude one-off transactions. The filtering reduces the number of links from approx. 2 millions to 1.1 millions, but the transaction volume drops only by approx. 10%. The number of firms drops from 315,259 to 243,339 in 2019 and for 2018 from 296,992 to 185,322. Imports and exports are not contained in the data set. The industry affiliation of firms, , correspond to the NACE classifications contained in the Hungarian corporate tax registry. On the NACE2 level 86 different classes are present, on the NACE 4 level 587. In 2019 the NACE affiliation is missing for 62,782 firms; in 2018 for 42,385 firms. We treat them as a residual NACE class.

Constructing firm- and industry-level COVID-19 shocks

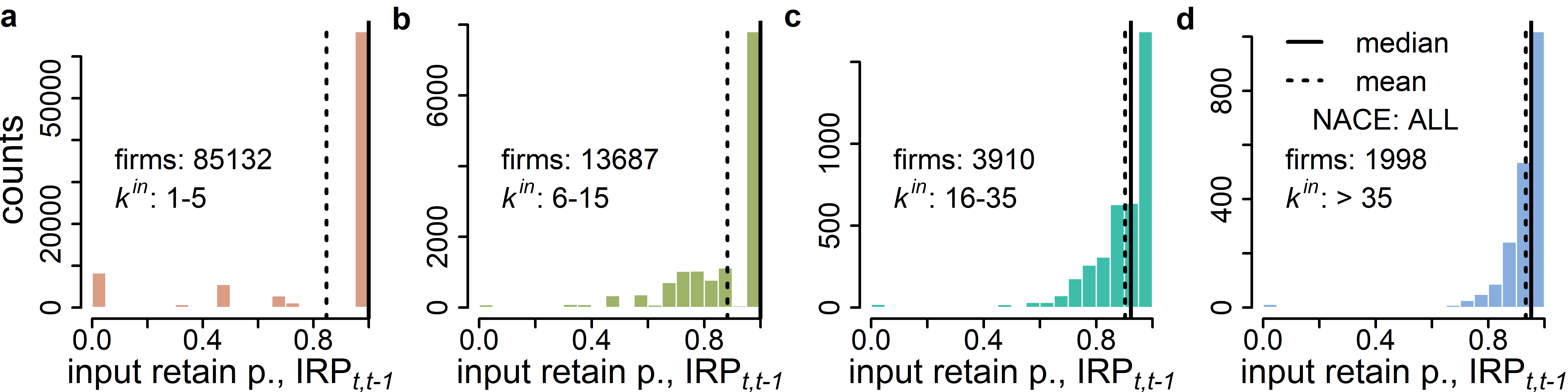

The employment data (collected by the Hungarian tax authority available at the central bank) contains the number of employees, , firm employed in the respective month . We assume that labor is an essential (Leontief-style) input to a firm’s production (Eq. [6]), and that after a shock firms only keep the amount of employees needed to operate at the new reduced production level. Therefore, we treat the empirical reduction of employees as a signal for how strong the firm was affected by the consequences of the pandemic in beginning of 2020. No furlough schemes were in place in Hungary. Note that January is sufficiently distant from COVID-19 affecting Europe and May is the time when the initial shock should be fully incorporated in the employment data; there is a two months leave notice period in Hungary. The Hungarian labor data is available for approx. 160,000 firms. For the firms with no data we impute the value by drawing the fraction of employment from firms in the respective NACE4 category where the data is available. We conduct the imputation 1,000 times and receive 1,000 completed vectors. For each of them, we calculate the value of economy-wide lost production, , (see Eq. [3]). We choose the completed shock vector that yields the median loss of production as . The corresponding industry-level COVID-19 shock is calculated by aggregating the vector , to the NACE2 industry-level. As firms within a sector mostly have different ratios of in- and out-strength — i.e., —, we aggregate the firm-level production capacities to a vector of downstream-constrained, , and a upstream-constrained remaining production capacity, . For industry , are calculated as

| (5) |

We use the notation . We show the aggregated shock, , for each NACE2 class in see SI Section 9. Creating synthetic shocks, , — that when aggregated to the industry-level are identical to and — can be achieved by fulfilling Eq. [5]. This implies that the aggregated firm-level shocks all fulfil and . For details, see SI Section 8.

Shock propagation model

The production process of each firm is represented by a generalized Leontief production function, defined as

| (6) |

is the amount of input firm uses for production, is the set of essential inputs, is the set of non-essential inputs of firm ; and are ’s labor and capital inputs. The essential and non-essential input types of firms are assigned according to their industry affiliation (NACE4) and an expert based survey for 56 industry sectors conducted by (Pichler et al., 2022). The parameters are technologically determined coefficients, is the maximum production level possible without non-essential inputs and is chosen to interpolate between the full production level (with all inputs) and . All parameters are determined by , and . The COVID-19 shock, , propagates through the Hungarian production network in the following way. Initially, at time the network, , is stable and the production amount of each firm corresponds to its out-strength, , where corresponds to firm ’ original revenue from its activity in the FPN, . We denote firm ’s remaining fraction of production, at time as , hence at time before any shocks occur . At time the initial shock materializes and production levels of each firm drop to the remaining production capacity, . Then, we simulate how firms propagate the received shock upstream by reducing their demand to suppliers and downstream by reducing their supply to customers. Missing non-essential inputs cause production reductions in a linear fashion, while a lack of essential inputs affects output in the non-linear Leontief way, i.e. downstream shocks can have strong negative impacts on production, depending on the supplier-buyer industry pair. The loss of a customer leads to a production reduction proportional to the customers’ revenue-share, i.e. upstream shocks have only linear impacts. For each firm, , we update the production output, , at , given the downstream constrained production levels of its suppliers, , at time as

The production output, , of firm at , given the upstream constrained production level of its customers, , at time is computed as

| (8) |

The algorithm converges at time , yielding final production levels, , for each firm . The dependence of the final production level on the initial shock is made explicit by writing as a function of . Note that the quantity, , is the amount of lost revenue of firm due to the initial shock and its propagation. For a complete description of the algorithm, see (Diem et al., 2022). For simulating shocks on the industry-level network, , in Eqs. [Shock propagation model]-[8] we replace with , in Eq. [Shock propagation model], with , and in Eq. [8] with . This results in the final production levels, , for each sector, , and we set . The overall production loss, , is calculated analogously as in Eq. [3], based on the out strengths, , of sectors, , as

| (9) |

Acknowledgements

This work was supported in part by the OeNB Anniversary fund project P18696, the Austrian Science Promotion Agency FFG project 886360, and the Austrian Federal Ministry for Climate Action, Environment, Energy, Mobility, Innovation and Technology project GZ 2021-0.664.668 and H2020 SoBigData-PlusPlus grant agreement ID 871042.

Author contributions

CD and ST conceived the work. AB cleaned and prepared the data. CD wrote the code. CD, AB performed the analysis. All analyzed and interpreted the results. CD and ST wrote the paper. All contributed towards the final manuscript.

References

- Acemoglu et al. (2012) Acemoglu D, Carvalho VM, Ozdaglar A, Tahbaz-Salehi A. The Network Origins of Aggregate Fluctuations. Econometrica 2012;80(5):1977–2016.

- Bacilieri et al. (2022) Bacilieri A, Borsos A, Reisch , Astudillo-Estevez P, Lafond F. Firm-level production networks: what do we (really) know? Technical Report; work in progress; 2022.

- Battiston et al. (2012) Battiston S, Puliga M, Kaushik R, Tasca P, Caldarelli G. DebtRank: Too Central to Fail? Financial Networks, the FED and Systemic Risk. Scientific Reports 2012;2(541).

- Bernard et al. (2022) Bernard AB, Dhyne E, Magerman G, Manova K, Moxnes A. The origins of firm heterogeneity: A production network approach. Journal of Political Economy 2022;130(7):000–.

- Borsos and Mero (2020) Borsos A, Mero B. Shock propagation in the banking system with real economy feedback. MNB Working Papers 2020;2022(6):1–56.

- Borsos and Stancsics (2020) Borsos A, Stancsics M. Unfolding the hidden structure of the Hungarian multi-layer firm network. Technical Report; Magyar Nemzeti Bank (Central Bank of Hungary); 2020.

- Brintrup et al. (2020) Brintrup A, Pak J, Ratiney D, Pearce T, Wichmann P, Woodall P, McFarlane D. Supply chain data analytics for predicting supplier disruptions: a case study in complex asset manufacturing. International Journal of Production Research 2020;58(11):3330–41.

- Carvalho et al. (2020) Carvalho VM, Nirei M, Saito YU, Tahbaz-Salehi A. Supply Chain Disruptions: Evidence from the Great East Japan Earthquake. The Quarterly Journal of Economics 2020;136(2):1255–321.

- Carvalho and Tahbaz-Salehi (2019) Carvalho VM, Tahbaz-Salehi A. Production Networks: A Primer. Annual Review of Economics 2019;11(1):635–63.

- Colon et al. (2021) Colon C, Hallegatte S, Rozenberg J. Criticality analysis of a country’s transport network via an agent-based supply chain model. Nature Sustainability 2021;4(3):209–15.

- Contreras and Fagiolo (2014) Contreras MGA, Fagiolo G. Propagation of economic shocks in input-output networks: A cross-country analysis. Physical Review E 2014;90(6):062812.

- Davis and Caldeira (2010) Davis SJ, Caldeira K. Consumption-based accounting of co2 emissions. Proceedings of the national academy of sciences 2010;107(12):5687–92.

- Demir et al. (2022) Demir B, Javorcik B, Michalski TK, Ors E. Financial constraints and propagation of shocks in production networks. Review of Economics and Statistics 2022;:1–46.

- Dhyne et al. (2021) Dhyne E, Kikkawa AK, Mogstad M, Tintelnot F. Trade and domestic production networks. The Review of Economic Studies 2021;88(2):643–68.

- Dhyne et al. (2015) Dhyne E, Magerman G, Rubínová S. The Belgian production network 2002-2012. Technical Report; NBB Working Paper; 2015.

- Diem et al. (2022) Diem C, Borsos A, Reisch T, Kertész J, Thurner S. Quantifying firm-level economic systemic risk from nation-wide supply networks. Scientific reports 2022;12(1):1–13.

- Diem et al. (2020) Diem C, Pichler A, Thurner S. What is the minimal systemic risk in financial exposure networks? Journal of Economic Dynamics and Control 2020;116:103900.

- Dietzenbacher et al. (2013) Dietzenbacher E, Los B, Stehrer R, Timmer M, De Vries G. The construction of world input–output tables in the wiod project. Economic systems research 2013;25(1):71–98.

- Duprez and Magerman (2018) Duprez C, Magerman G. Price updating in production networks. Technical Report; NBB Working Paper; 2018.

- Eurostat (2008) Eurostat . Eurostat manual of supply, use and input–output tables. Technical Report; Eurostat methodologies and working papers; 2008.

- Fujiwara and Aoyama (2010) Fujiwara Y, Aoyama H. Large-scale structure of a nation-wide production network. The European Physical Journal B 2010;77(4):565–80.

- Glasserman and Young (2016) Glasserman P, Young HP. Contagion in Financial Networks. Journal of Economic Literature 2016;54(3):779–831.

- Hallegatte (2008) Hallegatte S. An Adaptive Regional Input‐Output Model and its Application to the Assessment of the Economic Cost of Katrina. Risk Analysis: An International Journal 2008;28(3):779–99.

- Han and Goetz (2019) Han Y, Goetz SJ. Predicting us county economic resilience from industry input-output accounts. Applied Economics 2019;51(19):2019–28.

- Heinrich et al. (2022) Heinrich T, Yang J, Dai S. Levels of structural change: An analysis of china’s development push 1998-2014. Journal of Evolutionary Economics 2022;32(1):35–86.

- Henriet et al. (2012) Henriet F, Hallegatte S, Tabourier L. Firm-network characteristics and economic robustness tonatural disasters. Journal of Economic Dynamics and Control 2012;36(1):150–67.

- Hidalgo et al. (2007) Hidalgo CA, Klinger B, Barabási AL, Hausmann R. The product space conditions the development of nations. Science 2007;317(5837):482–7.

- Horowitz et al. (2006) Horowitz KJ, Planting MA, et al. Concepts and Methods of the us input-Output Accounts. Technical Report; Bureau of Economic Analysis; 2006.

- Huremovic et al. (2020) Huremovic K, Jiménez G, Moral-Benito E, Vega-Redondo F, Peydró JL, et al. Production and financial networks in interplay: Crisis evidence from supplier-customer and credit registers. Technical Report; Barcelona GSE Working Paper Series; 2020.

- Ialongo et al. (2022) Ialongo LN, de Valk C, Marchese E, Jansen F, Zmarrou H, Squartini T, Garlaschelli D. Reconstructing firm-level interactions in the dutch input–output network from production constraints. Scientific reports 2022;12(1):1–12.

- Inoue and Todo (2019) Inoue H, Todo Y. Firm-level propagation of shocks through supply-chain networks. Nature Sustainability 2019;2(9):841–7.

- Ivanov et al. (2014) Ivanov D, Sokolov B, Dolgui A. The ripple effect in supply chains: trade-off ‘efficiency-flexibility-resilience’ in disruption management. International Journal of Production Research 2014;52(7):2154–72.

- Jones and Furnas (1987) Jones WP, Furnas GW. Pictures of relevance: A geometric analysis of similarity measures. Journal of the American society for information science 1987;38(6):420–42.

- Klimek et al. (2019) Klimek P, Poledna S, Thurner S. Quantifying economic resilience from input–output susceptibility to improve predictions of economic growth and recovery. Nature communications 2019;10(1):1–9.

- Kosasih and Brintrup (2022) Kosasih EE, Brintrup A. A machine learning approach for predicting hidden links in supply chain with graph neural networks. International Journal of Production Research 2022;60(17):5380–93.

- Kymn (1990) Kymn KO. Aggregation in input–output models: a comprehensive review, 1946–71. Economic Systems Research 1990;2(1):65–93.

- Lenzen (2011) Lenzen M. Aggregation versus disaggregation in input–output analysis of the environment. Economic Systems Research 2011;23(1):73–89.

- Leontief (1936) Leontief WW. Quantitative input and output relations in the economic systems of the united states. The review of economic statistics 1936;:105–25.

- Magerman et al. (2016) Magerman G, De Bruyne K, Dhyne E, Van Hove J. Heterogeneous firms and the micro origins of aggregate fluctuations. Technical Report; NBB Working Paper; 2016.

- Mahajan et al. (2018) Mahajan S, Beutel J, Guerrero S, Inomata S, Larsen S, Moyer B, Remond-Tiedrez I, Rueda-Cantuche JM, Simpson LH, Thage B, R CV. Handbook on Supply, Use and Input-Output Tables with Extensions and Applications. Technical Report; Department of Economic and Social Affairs Statistics Division, United Nations; 2018.

- Martin and Sunley (2015) Martin R, Sunley P. On the notion of regional economic resilience: conceptualization and explanation. Journal of economic geography 2015;15(1):1–42.

- McNerney et al. (2022) McNerney J, Savoie C, Caravelli F, Carvalho VM, Farmer JD. How production networks amplify economic growth. Proceedings of the National Academy of Sciences 2022;119(1):e2106031118.

- Miller and Blair (2009) Miller RE, Blair PD. Input-Output Analysis: Foundations and Extensions. Cambridge University Press, 2009.

- Moran and Bouchaud (2019) Moran J, Bouchaud JP. May’s instability in large economies. Phys Rev E 2019;100:032307.

- Mungo et al. (2023) Mungo L, Lafond F, Astudillo-Estévez P, Doyne Farmer J. Reconstructing production networks using machine learning. Journal of Economic Dynamics and Control 2023;:104607.

- Mungo and Moran (2023) Mungo L, Moran J. Revealing production networks from firm growth dynamics. Technical Report; arXiv:2302.09906; 2023.

- Neffke et al. (2011) Neffke F, Henning M, Boschma R. How do regions diversify over time? industry relatedness and the development of new growth paths in regions. Economic Geography 2011;87(3):237–65.

- OECD (2023) OECD . Quarterly GDP indicator. Technical Report; Organisation for Economic Cooperation and Development; 2023.

- Otto et al. (2017) Otto C, Willner SN, Wenz L, Frieler K, Levermann A. Modeling loss-propagation in the global supply network: The dynamic agent-based model acclimate. Journal of Economic Dynamics and Control 2017;83:232–69.

- Pichler et al. (2022) Pichler A, Pangallo M, del Rio-Chanona RM, Lafond F, Farmer JD. Forecasting the propagation of pandemic shocks with a dynamic input-output model. Journal of Economic Dynamics and Control 2022;144:104527.

- Reisch et al. (2022) Reisch T, Heiler G, Diem C, Klimek P, Thurner S. Monitoring supply networks from mobile phone data for estimating the systemic risk of an economy. Scientific reports 2022;12(1):1–10.

- Schueller et al. (2022) Schueller W, Diem C, Hinterplattner M, Stangl J, Conrady B, Gerschberger M, Thurner S. Propagation of disruptions in supply networks of essential goods: A population-centered perspective of systemic risk. arXiv preprint arXiv:220113325 2022;.

- Stangl et al. (2023) Stangl J, Borsos A, Diem C, Reisch T, Thurner S. Using firm-level production networks to identify decarbonization strategies that minimize social stress. arXiv preprint arXiv:230208987 2023;.

- Su and Ang (2010) Su B, Ang B. Input–output analysis of co2 emissions embodied in trade: The effects of spatial aggregation. Ecological Economics 2010;70(1):10–8.

- Su et al. (2010) Su B, Huang HC, Ang BW, Zhou P. Input–output analysis of co2 emissions embodied in trade: the effects of sector aggregation. Energy Economics 2010;32(1):166–75.

- Thurner (2022) Thurner S. A complex systems perspective on macroprudential regulation. In: Handbook of Financial Stress Testing. Cambridge, UK: Cambridge University Press; 2022. p. 593–634.

- Timmer et al. (2015) Timmer MP, Dietzenbacher E, Los B, Stehrer R, De Vries GJ. An illustrated user guide to the world input–output database: the case of global automotive production. Review of International Economics 2015;23(3):575–605.

- Vijaymeena and Kavitha (2016) Vijaymeena M, Kavitha K. A survey on similarity measures in text mining. Machine Learning and Applications: An International Journal 2016;3(2):19–28.

- Wichmann et al. (2020) Wichmann P, Brintrup A, Baker S, Woodall P, McFarlane D. Extracting supply chain maps from news articles using deep neural networks. International Journal of Production Research 2020;58(17):5320–36.

- Wiedmann (2009) Wiedmann T. A review of recent multi-region input–output models used for consumption-based emission and resource accounting. Ecological Economics 2009;69(2):211–22.

- Wiedmann et al. (2015) Wiedmann TO, Schandl H, Lenzen M, Moran D, Suh S, West J, Kanemoto K. The material footprint of nations. Proceedings of the national academy of sciences 2015;112(20):6271–6.

- Willner et al. (2018) Willner SN, Otto C, Levermann A. Global economic response to river floods. Nature Climate Change 2018;8(7):594–8.

- Yamano and Ahmad (2006) Yamano N, Ahmad N. The oecd input-output database: 2006 edition. OECD Science, Technology and Industry Working Papers 2006;No. 2006/08.

- Yan et al. (2015) Yan T, Choi TY, Kim Y, Yang Y. A theory of the nexus supplier: A critical supplier from a network perspective. Journal of Supply Chain Management 2015;51(1):52–66.

Supplementary Information

Appendix SI Section 1 Calculating input and output vectors

In this section we show how to calculate the intra-sector heterogeneity (or similarity) of the firms’ input-output vectors. We start aggregating every firms’ firm-level in- and output vector to the NACE2 industry-level. The th column of the FPN’s adjacency matrix, , represents the firm-level input vector, , of firm , while the th row gives the firm-level output vector, . We compute the corresponding industry-level input vector, , and output vector, , of firm , by aggregating all in links (purchases) of ’s suppliers from the same industry and all out links (sales) to ’s customers in the same industry, as

| (S.1) |

The element , specifies the amount of input firm is buying from suppliers, , of industry, , i.e., all with . The element specifies the amount firm is selling to firms, in industry, , i.e., all with . The expression is the Kronecker delta and is equal to one if firm produces product and zero otherwise, i.e.,

We focus on the relative importance of firms’ input types (industries) and customer industries, independent of firm size. To do so, we compute the normalized input-, , and output vectors, , of every firm, . The k entry of the normalized input vector, , represents the fraction of inputs firm buys from firms in industry . Similarly, the k entry of ’s normalized output vector, , represents the fraction of firm ’s revenue it receives by selling to firms in industry . and are the scaled technical and allocation coefficients in classical IO analysis. For firm the vectors and are computed as

| (S.2) |

where if firm belongs to industry and otherwise. We quantify the similarity between input and output vectors of two firms with the overlap coefficient (OC) due to its clear economic interpretability. To show that our results do not depend on the specific choice of the similarity measure we also look at the jaccard index (JI).

Appendix SI Section 2 Details for calculation and interpretation of the input and output overlap coefficient

In general the overlap coefficient of two vectors of dimension is defined as

| (S.3) |

We calculate the overlap coefficient of the 1-norm normalized input, and output vectors, i.e. and . Therefore, in each calculation both vectors sum to one, then the denominator is always equal to one and can be dropped. The overlap coefficient is closely related to the weighted Jaccard Index, which has the same numerator, and as the denominator. It is also called the Szymkiewicz-Simpson distance (Jones and Furnas, 1987; Vijaymeena and Kavitha, 2016).

As introduced in the main text, for our application we calculate the input overlap coefficient (IOC) and output overlap coefficient (OOC) of two firms and as,

| (S.4) | |||||

| (S.5) |

The denominator from Eq. S.3 can be omitted since and for all . We calculate the distribution of the two measures for each industry , by computing all pairwise and for all firms where, , and , in the respective industry, . The input overlap coefficient, , of two firms and gives the fraction of their overall inputs they source from the same industries, i.e. the overlap of their industry input shares. The output overlap coefficient, , of two firms and specifies the fraction of their overall sales they sell to the same industries, i.e. the overlap of their industry sales shares. Note that also quantifies ’s and ’s overlap of exposures to other economic dynamics, like price increases or innovations of supplying industries. Similarly, measures the common exposure to, e.g., innovation in the buyer industry that makes the input of firms obsolete.

In the example of Fig. 1, the relative input vector of firm 10 is and for firm 11 , hence . If a demand shock affects firm , 50% of the shock spreads upstream to sectors 3 and 4, respectively, while if the shock affects firm , 100% of the shock spreads upstream to sector 3. This means that the shock spreading dynamics overlap by only 50% (), while the other 50% spread to distinct sectors. For firms and the output vectors are and , hence, . This means that if either, or , receives a shock, 0% of the shock would affect the same industry and 100% would spread to different sectors, in one case towards sector and in the other to sector . Also their exposure to demand shocks has no overlap. Firm is only exposed to industry while firm is only exposed to sector .

Since we use industry-level input and output vectors, which neglect firm-level differences within industries, the real level of heterogeneity could be even larger. In our dataset cross border import and export links of firms are not available. This could lead to a potential underestimation of overlaps, but a study for Belgium (Dhyne et al., 2021) shows that firms’ import and export links are few in relation to national import and export links.

Appendix SI Section 3 Further results on input and output overlaps

Further results for NACE C26

Even though, in all four in-degree (out-degree) groups there are firms with very similar input (output) vectors, the results clearly show that in general firms have surprisingly small overlaps with respect to to their suppliers’ industries (inputs) and customers’ (output) industries. This implies that if two random firms in in-degree (out-degree) bin 35 receive the same absolute size shock, on average only 34% (14%) of the shock’s volume is propagated to firms of the same industry while 66% (86%) of the shock is propagated to firms in other industries. At the same time it means that two firms in this industry have on average 66% (86%) of their upstream (downstream) exposures to different supplier (buyer) industries. The low level of similarity of input and output vectors clearly shows that aggregating these firms into a single industry is not representative of the single firms’ input-output vectors and will lead to large biases and mis-estimations of economic dynamics.

Further results on output overlaps across industries

The highest median OOCij are found in Veterinary activities (M75), Manufacture of beverages (C11), Manufacture of other transport equipment (C30), Forestry and logging (A2), Manufacture of leather and related products (C15), Manufacture of basic pharmaceutical products (C21), Telecommunications (J61), whereas the lowest median OOCij are found in service sectors such as Public administration and defence; compulsory social security (O84), Travel agency and related activities (N79), or Scientific research and development (M72), but also non-service sectors such as Remediation activities and other waste management services (E39), Other manufacturing (C32), or Manufacture of textiles (C13) are among the lowest output overlap sectors. The average standard deviation is 0.17, the standard deviation of standard deviations is 0.047, and the error bar length appears to be relatively homogeneous across sectors. This indicates that the variation of pairwise output overlaps, OOCij, within sectors is relatively similar across sectors. For the other degree bins see SI Fig. S6.

The same results are shown for the other three out-degree bins 1-5, 6-15, and 16-35 in SI Section 4 Fig. S3. As for industry C26, the output overlaps are smaller for lower degree bins; the averages over the mean (median) output overlaps, are 0.110, (0.021) 0.157 (0.135), 0.223 (0.215), for the bins 1-5, 6-15, and 16-35, respectively. The averages over the standard deviations of output overlaps, are 0.266, 0.129, 0.109, respectively and therefore the variation of output overlaps within is on average decreasing with the number of out-links. Figure S1b illustrates this relationship more clearly by showing for each in-degree size bin (1-5, 6-15, 16-35, 35) the boxplot of the industries’ median OOC values. It is clearly visible that output vectors of firms within industries become more homogeneous with the number of suppliers. SI Section 5 shows that OOCij are even lower when computed for at NACE 4 level. SI Fig. S4b shows the average of the mean (median) output overlaps, across NACE4 industries is 0.231 (0.207). The standard deviation of mean (median) output overlaps is 0.179 (0.19), i.e. higher than for the NACE2 level. This indicates that the variation of average output vector overlaps is higher at the NACE 4 level. The average standard deviation is 0.126 and the standard deviation of standard deviations is 0.056. Note that the average IOC and OOC levels seem to be more similar on the NACE 4 level than at the NACE 2 level where the average IOC is higher than OOC. For the other degree bins see SI Fig. S7. SI Fig. S9 in SI Section 6 shows qualitatively similar results for the Jaccard Index for the degree bin 35. The pairwise input Jaccard Index (IJI) distributions are slightly shifted towards higher similarity values with a average mean (median), 0.398 (0.394) and slightly less variation with a standard deviation of means of 0.07 (0.067). The pairwise output Jaccard Index (OJI) distributions are also shifted towards slightly higher similarity values with a average over means (medians), of 0.301 (0.291) and slightly less variation with a standard deviation of means of 0.076 (0.077).

Appendix SI Section 4 Overlap coefficients across industries for other degree bins

This section shows the results of the pairwise input overlap coefficient, IOC, and output overlap coefficient, OOC, distributions across all NACE2 industries for the three degree bins 1-5, 6-15, and 16-35 that are not shown in Fig. 3. As for Fig. 3 we calculate the summary statistics — mean, 5%, 25%, 50% (median) 75% and 95% percentiles — for the pairwise IOC (SI Fig. S2) and OOC (SI Fig. S3) distributions for all NACE2 industries. Again these statistics are visualized as boxplots. The x-axis shows the 86 NACE2 codes present in the data set; the y-axis denotes the overlap coefficients, each boxplot corresponds to a NACE2 class. The dark thick horizontal bars correspond to the median, (), the interquartile range ( – ) is shown as thick dark vertical lines, and the error bars ( – ) are indicated by thin light vertical lines. The thin vertical black lines separate NACE2 classes by their NACE1 affiliation.

The results for the IOC distributions are shown in SI Fig. S2. SI Fig. S2a shows the pairwise IOCij for firms with in-degree between one and five, . The mean over the industries’ mean (median) IOC is 0.132 (0.009), the standard deviation of mean (median) IOCs is 0.081 (0.062). The mean standard deviation is 0.262. SI Fig. S2b shows the pairwise IOCij for firms with in-degree between one and five, . The mean over the industries’ mean (median) IOC is 0.202 (0.148), the standard deviation of mean (median) IOCs is 0.081 (0.088). The mean standard deviation is 0.192. SI Fig. S2c shows the pairwise IOCij for firms with in-degree between one and five, . The mean over the industries’ mean (median) IOC is 0.269 (0.241), the standard deviation of mean (median) IOCs is 0.083 (0.091). The mean standard deviation is 0.168. As for NACE C26 in the main text we see that on average input vector overlaps increase with the number of suppliers.

The results for the OOC distributions are shown in SI Fig. S3. SI Fig. S3a shows the pairwise OOCij for firms with out-degree between one and five, . The mean over the industries’ mean (median) OOC is 0.110 (0.021), the standard deviation of mean (median) OOCs is 0.094 (0.118). The mean standard deviation is 0.226. SI Fig. S3b shows the pairwise OOCij for firms with out-degree between one and five, . The mean over the industries’ mean (median) OOC is 0.157 (0.135), the standard deviation of mean (median) OOCs is 0.078 (0.074). The mean standard deviation is 0.129. SI Fig. S3c shows the pairwise OOCij for firms with out-degree between one and five, . The mean over the industries’ mean (median) OOC is 0.223 (0.215), the standard deviation of mean (median) OOCs is 0.078 (0.078). The mean standard deviation is 0.109. Again average overlaps seem to increase with degree (number of customers). Further, output overlaps are on average slightly lower than input overlaps.

Next we illustrate how average similarity increases with the degree bins. Fig. S1 illustrates this relationship more clearly by showing for each degree size bin (1-5, 6-15, 16-35, 35) the boxplot of the industries’ median IOC and OOC values. Fig. S1a shows boxplots of the median input overlap coefficients, IOC, for all NACE2 industries for each in-degree bin, respectively. We see that for the bin with 1 to 5 suppliers almost all medians are zero. Then the distribution of medians is substantially shifted upwards for the bin of 6-15 suppliers and it continues to increase for the other two in-degree bins with 16-35 and more than 35 suppliers, respectively. Fig. S1b shows boxplots of the median output overlap coefficients, OOC, for all NACE2 industries for each out-degree bin, respectively. We see that for the bin with 1 to 5 buyers almost all medians are zero. Then the distribution of medians is slightly shifted upwards for the bin of 6-15 buyers, but there are several outlier industries with higher output overlaps. The median OOC continue to increase for the other two out-degree bins with 16-35 and more than 35 buyers, respectively. It is visible that the upper tails of the median OOC distributions are longer than for the median IOC distributions. Overall median OOCs are lower than median IOCs.

Appendix SI Section 5 Overlap coefficients for NACE 4 level input output vectors

In this section we show that the pairwise input overlaps, IOCij, and output overlaps, OOCij, are lower for all pairs of firms within NACE 4 industries for the NACE 4 level input and output vectors. Remember, in the previous analysis we have computed the overlaps for all pairs of firms within a NACE2 industry and on the NACE2 level input and output vectors.

In the following figures we show the pairwise overlap coefficient distributions of input- and output-vectors of firms within each NACE4 industry for the respective degree-bins 1-5, 6-15, 6-35, and 35. The y-axis denotes the overlap coefficients, the x-axis shows the NACE4 code for the respective boxplots. The dark horizontal bars correspond to the median, (), dark vertical lines to the interquartile range ( – ), and thin light vertical lines to error bars ( – ). Thin black vertical lines separate NACE1 classes. Empty columns indicate sectors with less than two firms in this degree bin.

First, we show the distributions of the input overlap coefficients, IOCij. SI Fig. S6a shows the distributions of pairwise intra-industry input overlap coefficients, IOCij, for firms with more than 35 suppliers, . The average of the mean (median) input overlaps, across NACE2 industries is 0.237 (0.216) and the standard deviation of mean (median) input overlaps is 0.11 (0.12). The average standard deviation is 0.126. This indicates that relatively low input overlaps are the norm, but there are several outliers with higher similarities. SI Fig. S6a shows the distributions of pairwise input overlap coefficients, IOCij, for firms with in-degree between one and five, . The mean over the industries’ mean (median) IOCij is 0.063 (0.005), the standard deviation of mean (median) IOCs is 0.074 (0.057). The mean standard deviation is 0.168. SI Fig. S6b shows the distributions of pairwise input overlap coefficients, IOCij, for firms with in-degree between 6 and 15, . The mean over the industries’ mean (median) IOCij is 0.112 (0.063), the standard deviation of mean (median) IOCs is 0.084 (0.083). The mean standard deviation is 0.139. SI Fig. S6c shows the distributions of pairwise input overlap coefficients, IOCij, for firms with in-degree between 16 and 35, . The mean over the industries’ mean (median) IOCij is 0.165 (0.140), the standard deviation of mean (median) IOCs is 0.107 (0.112). The mean standard deviation is 0.130.

Second, we show the distributions of the output overlap coefficients, OOCij. SI Fig. S6b shows the distributions of pairwise intra-industry output overlap coefficients, OOCij, for more than 35 buyers, . The average of the mean (median) output overlaps, across NACE2 industries is 0.231 (0.207) and the standard deviation of mean (median) output overlaps is 0.179 (0.19), indicating that relatively low output overlaps are the norm, but there are relatively many outliers with higher similarities. The average standard deviation is 0.135. Output overlaps are on average only slightly lower than the input overlaps, but there is more variation across industries. SI Fig. S7a shows the distributions of pairwise output overlap coefficients, OOCij, for firms with out-degree between one and five, . The mean over the industries’ mean (median) OOCij is 0.056 (0.005), the standard deviation of mean (median) OOCs is 0.075 (0.054). The mean standard deviation is 0.148. SI Fig. S7b shows the distributions of pairwise output overlap coefficients, OOCij, for firms with out-degree between 6 and 15, . The mean over the industries’ mean (median) OOCij is 0.081 (0.057), the standard deviation of mean (median) OOCs is 0.063 (0.068). The mean standard deviation is 0.087. SI Fig. S7c shows the distributions of pairwise output overlap coefficients, OOCij, for firms with out-degree between 16 and 35, . The mean over the industries’ mean (median) OOCij is 0.127 (0.116), the standard deviation of mean (median) OOCs is 0.080 (0.082). The mean standard deviation is 0.078. Note that if industry-level aggregation was fully representative for the IO-vectors of firms in all figures all distributions would correspond to a single bar at the value 1.