Data Augmentation for Imbalanced Regression

Samuel Stocksieker Denys Pommeret Arthur Charpentier

Univ. Lyon, UCBL, ISFA LSAF Aix-Marseille Univ., CNRS, I2M UQAM - Montréal

Abstract

In this work, we consider the problem of imbalanced data in a regression framework when the imbalanced phenomenon concerns continuous or discrete covariates. Such a situation can lead to biases in the estimates. In this case, we propose a data augmentation algorithm that combines a weighted resampling (WR) and a data augmentation (DA) procedure. In a first step, the DA procedure permits exploring a wider support than the initial one. In a second step, the WR method drives the exogenous distribution to a target one. We discuss the choice of the DA procedure through a numerical study that illustrates the advantages of this approach. Finally, an actuarial application is studied.

1 INTRODUCTION

Many real world forecasting problems are based on predictive models in a supervised learning framework. Most of these algorithms fail when the variable of interest is imbalanced. This situation also occurs when the population observed is significantly different from the true population. This is the case when certain parts of the support are observed less than in theory or are even not observed. We may face unrepresentative training data due to sampling noise or due to the sampling method, even for large samples. Such selection bias or sampling bias, could affect the models and impact the results, by biasing the estimates. We naturally find this problem in clinical trial data (Morgan and Rubin, (2012), Friede, (2006), Kahan et al., (2015), Ciolino et al., (2011), Ciolino et al., (2013)) and in survey sampling theory (Yang et al., 2021b ,Gupta et al., (2022), Tillé, (2022)). We also have such an issue in Regression Discontinuity (Caughey and Sekhon, (2011), Peng and Ning, (2019), Frölich and Huber, (2019), Cattaneo et al., (2021)). This problem also appears in actuarial science as illustrated in our application.

This kind of situation can strongly impact standard learning algorithms, particularly if the rarely observed (or unobserved) values are the most relevant for the modeling. The learning from imbalanced data concerns many problems with numerous applications in different fields, with still some open issues and challenges (Krawczyk, (2016)). This research topic, very active, has mostly focused on solving classification tasks where many solutions have been discussed (Branco et al., 2016a , Fernández et al., 2018a , Fernández et al., 2018b ).

However, very few works exist in a regression framework. One of the best solutions currently proposed is to use the concept of utility-based regression defining the notion of relevance for a continuous target variable (Torgo et al., (2015), Branco et al., 2016b , Branco, (2018), Ribeiro and Moniz, (2020)). Yang et al., 2021a propose to use distribution smoothing to handle this issue. All these different techniques offer specific treatments to deal with the imbalanced distribution of variables of interest. Several sampling techniques for regression models (Pair Bootstrap, Stratified Bootstrap, Residuals Resampling - Wild Bootstrap, etc.) have already been proposed in order to improve learning or get/reduce confidence intervals, without directly dealing with the imbalanced phenomenon Horowitz, (2019), Flachaire, (2001). There also exists some sample adjustment techniques that can be used to create a synthetic dataset with statistical similarities to the true population of interest Templ et al., (2017) but the covariates considered are categorical or discrete.

Finally, there does not seem to be any work handling specifically the case of imbalanced continuous covariates and no method proposes to adjust the sample according to a continuous target covariate distribution.

In this work, we consider the problem of imbalanced continuous covariates in a regression context and we propose two solutions: first, a weighted resampling (WR), driving the distribution of the covariates to the target one; second, a two-step data augmentation algorithm that combines a data augmentation (DA) procedure, exploring a wider support than the initial one, with the WR procedure. Interestingly, that method is valid for continuous, or discrete, as well as categorical covariates. A numerical study illustrates the advantages of combining this method with six different DA approaches through measures of predictive performance indicators in regression. As a particular case, we also study the WR method which corresponds to a one-step version of the algorithm.

The main contributions of this paper are: i) analyzing the potential impact of an imbalance of a covariate in a regression context; ii) introducing a WR method to deal with this phenomenon; and iii) presenting a combination of this method with several data generators to avoid an overfitting phenomenon and try to improve the regression. The paper is organized as follows: In Section 2 we describe the WR procedure and we introduce the DA-WR algorithm. Section 3 contains simulation results and Section 4 presents an analysis of a dataset from the literature. The perspectives of this work are presented in Section 5. Code, data and results are available at: https://github.com/sstocksieker/DAIR.

2 WR AND DA-WR ALGORITHMS

2.1 Notation

Consider a sequence of iid random variables , which are realizations of , where the variable of interest is univariate and the covariates is a -dimensional vector. and are supposed to be continuous or discrete and we consider the regression framework where the objective is to explain and predict according to the following structure:

for some function , parametric or not. Here we consider a random design where has an unknown joint cumulative distribution function (cdf) with probability . We assume a target distribution , which can be the distribution function of in the true population, which can be known, or a distribution of interest.

When the observations of are far from the target distribution we call this situation an imbalanced covariates regression, or simply an imbalanced regression here. This issue is slightly different from the imbalanced situation in a regression framework, in literature, because it handles one or more covariates () and not the target variable (). This case allows us to easily get a target distribution to drive the data generation (for example, from the population in survey analyses). More precisely, we should say that the imbalanced phenomenon occurs when . To measure the degree of imbalance we can denote by and the empirical estimators and we propose the following definition: we face a -imbalanced regression problem if there is a set with such that . In other words, an imbalanced regression means having a sample significantly different from the target population for at least a significant part of the support of . Clearly, the larger the values of , the greater the degree of imbalance. This problem also depends of the sample size. If and have the same support, then the phenomenon will diminish with . On the other hand, if a part of the support of is never observed then the problem may persist even for large .

To handle this situation, we want to draw a -sample, from the initial -sample , such that the cdf of converges to the target with associated probability .

We consider here the case where the random vector is composed of discrete or continuous variables and in both cases, we denote by its joint probability density function (pdf) or probability mass function. For simplicity of notation, we consider the case and from now on we then write instead of . The method can be extended to the multivariate case by using joint density estimators. Moreover, the case where X is qualitative could be treated in exactly the same way.

2.2 WR algorithm

We consider a classical kernel estimator of

with an appropriate bandwidth . To avoid unstable numerical results we add a trimming sequence , such that , as . Write

and we now consider instead of . We write the target probability density function associated to .

Define

- the drawing weight of observation , and

- the normalized drawing weight of observation such that

The weighted resampling is inspired by Smith and Gelfand, (1992) and consists in sampling the observations according to their drawing probabilities . This variant of the classical Bootstrap Efron, (1982) is close to the Monte Carlo method Sampling Importance Resampling Rubin, (1988). We draw a random variable from using the probabilities ; that is . By construction the cdf of given is

Clearly, and depend on the sample size but we omit the index in the notation.

We introduce a classical assumption

-

(C) : holds and ( times derivable) for some .

Proposition 1.

Assume that (C) holds and that the support of contains the support of . Then for all , the cdf of converges in probabilities to as .

Proof.

We recall a result of Collomb (1984):

Lemme 1 (Collomb, G. 1984).

Assume that , then we have

We have :

where

Write

We want to prove that

We can write

Noting that , and that we obtain

We have

since converges by the Law of Large Numbers and . We now consider

which converges to zero in probabilities since converges by law of large numbers, and by Lemma 1 combined with Assumption (C). Finally, we deduce that . Similar considerations apply to and we conclude that

The study of is done in Smith and Gelfand, (1992) where the authors proved that it converges to , which achieves the proof. ∎

The use of the WR procedure in regression yields a new sample with which tends to the target distribution. This oversampling can be applied with the following algorithm.

With this method, the cdf of converges to the target one from Proposition 1. The conditional distribution of given remains unchanged since the drawing is done on the whole observation. It is important to note that if there are auxiliary variables, they are drawn as .

The particularity of the WR algorithm is that it generates on the same support as the observations, which is imbalanced. Indeed, with a finite sample size, bootstrap procedures naturally return the same values as the sample. There is thus an important risk of over-fitting for the segments poor in observations with a high draw weight.

2.3 DA-WR algorithm

We propose to combine the previous WR algorithm with a method of DA generating synthetic data. This artificial data simulation allows to extend the support of the distribution and possibly reduces the risk of over-fitting associated with oversampling.

In order to enlarge the support of the covariates, we apply the DA first. We obtain the following algorithm, adding a DA step to the previous WR algorithm.

As we can see, this approach does not require complex parameterization: only a target distribution for the covariate of interest and a density estimator for the empirical density (e.g kernel density estimate). In practice, a preliminary step of WR can be used to increase the performance of the DA-WR algorithm that becomes a WR-DA-WR algorithm. The last step of the algorithm must be a WR step to bring closer the synthetic distribution to the target one. It is important to note that if there are auxiliary variables then they are generated and drawn as . Note that the result of Proposition 1 now depends on the DA procedure and additional conditions are needed to get the convergence to the target distribution. We give here an illustration (the proof is relegated in the Supplement) by considering the new data obtained from the DA procedure, for , respectively, and by assuming that for all ,

-

(C’) :

-

(C”) : ,

where and denote the weights associated with the initial and the augmented dataset, respectively.

Proposition 2.

Assume that (C)-(C”) hold and that the support of contains the support of . Then for all , the cdf resulting from the DA-WR algorithm converges in probabilities to as .

For the DA step, we consider the following six approaches:

- •

-

•

Interpolation approaches: k Nearest Neighbors inspired by Chawla et al., (2002): SMOTE

-

•

Latent structure model approaches:

- Gaussian Mixture Models: GMM

- Factor Analysis: FA -

•

Copula approach: Gaussian Copula Model Patki et al., (2016): Copula

-

•

Deep Learning approach: Conditional Generative Adversarial Networks Xu et al., (2019): GAN

-

•

Machine Learning approach: Ramdom forest Nowok et al., (2016): RF

More details on these generators are given in A in the Supplement. All these methods have been used as synthetic data generators, that is, to construct samples with only artificial data. This choice has the advantage of defining the original observations as a test sample and it also avoids the loss of information by separating learning and testing. In our study, this allows us to compare the different techniques. The existing algorithms in imbalanced regression cannot be applied in this context because they do not focus on the covariate distribution. More precisely, they do not propose to manage the selection bias although our WR algorithm tries to correct the lack of representativeness of the sample compared to the population (convergence to the target distribution).

All these generators were tested before and after a clustering (via a Gaussian Mixture Model) in order to eventually improve the accuracy of the data generation. Typically, this means performing a cluster-conditioned learning. Indeed, the structure (variance, dependence, etc.) of the data can be different according to certain subparts of the data space. It can be relevant to apply a resampling by cluster rather than on the whole sample.

3 NUMERICAL ILLUSTRATION

We illustrate our approach numerically by first showing the different generated data obtained with the WR and the DA-WR algorithms. Then, we analyze the impact of bias selection in regression when an imbalanced sample is used for training the learning model. At last, we measure the benefit obtained with both WR and DA-WR algorithms and compare the results obtained by the different generators. In this illustration, the algorithms are intentionally evaluated on a complicated case with two inflection points on the border of the observed support to get a strong impact on the regression in order to assess the method.

3.1 Dataset design

We consider a bi-dimensional initial population , of size such that and , where denotes the Beta distribution and denotes the Gaussian distribution.

From this population, we uniformly draw a test sample . From the remaining population, \, we uniformly draw a balanced sample , supposed to be representative of the population. Finally, we draw an imbalanced sample from this remaining population. The draw weights to construct this imbalanced sample are defined by the distribution . The test, balanced, and imbalanced samples are all of size .

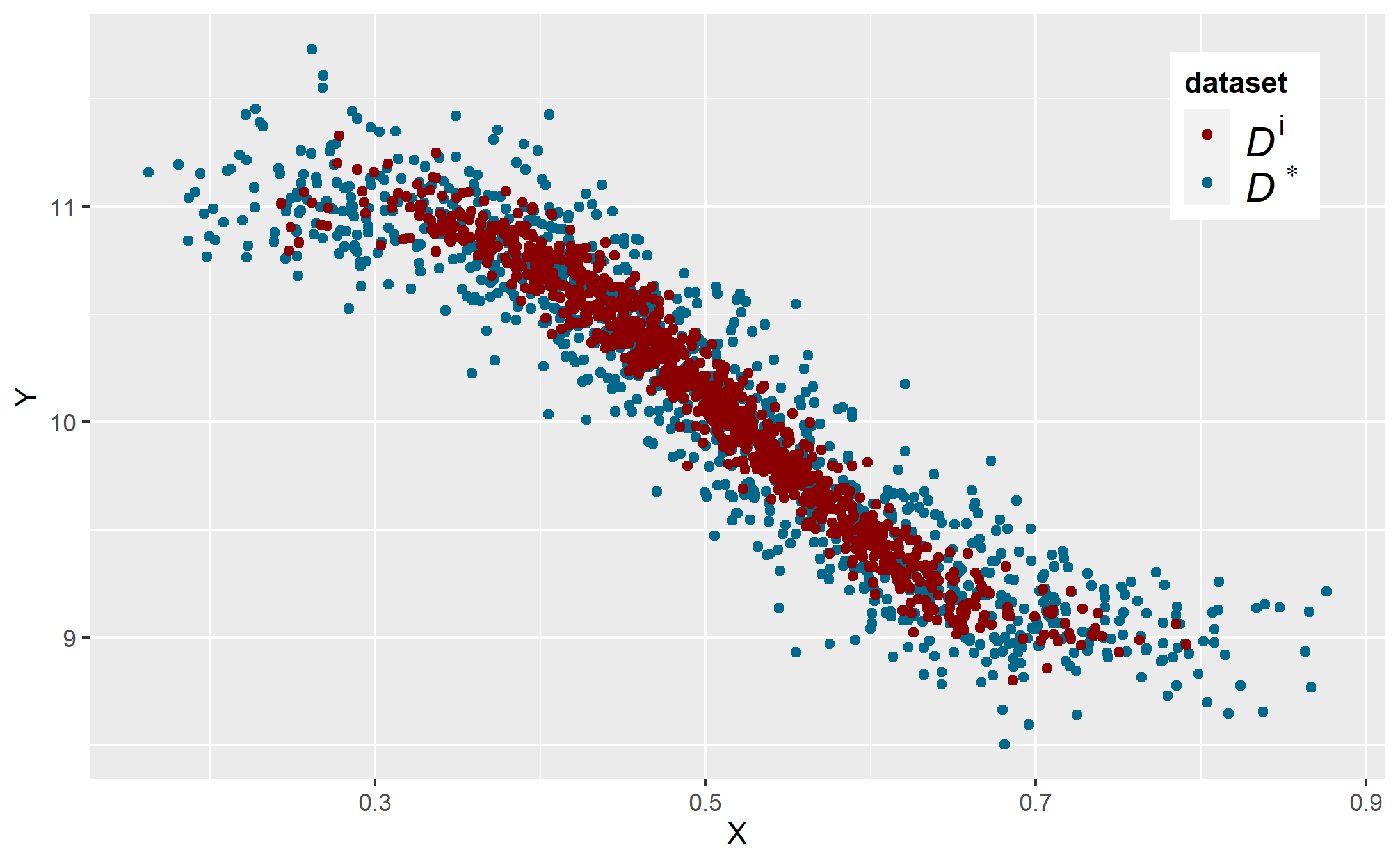

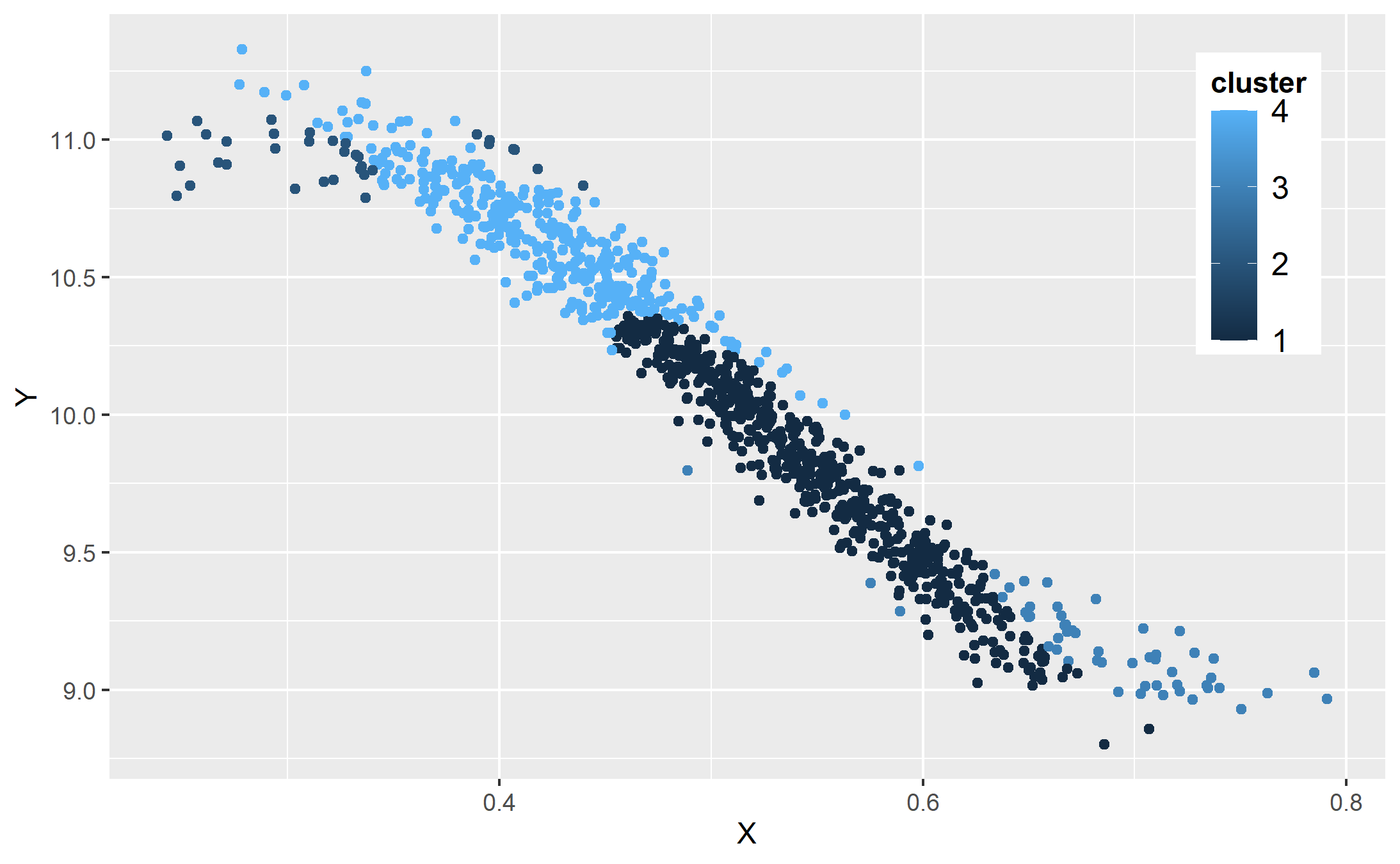

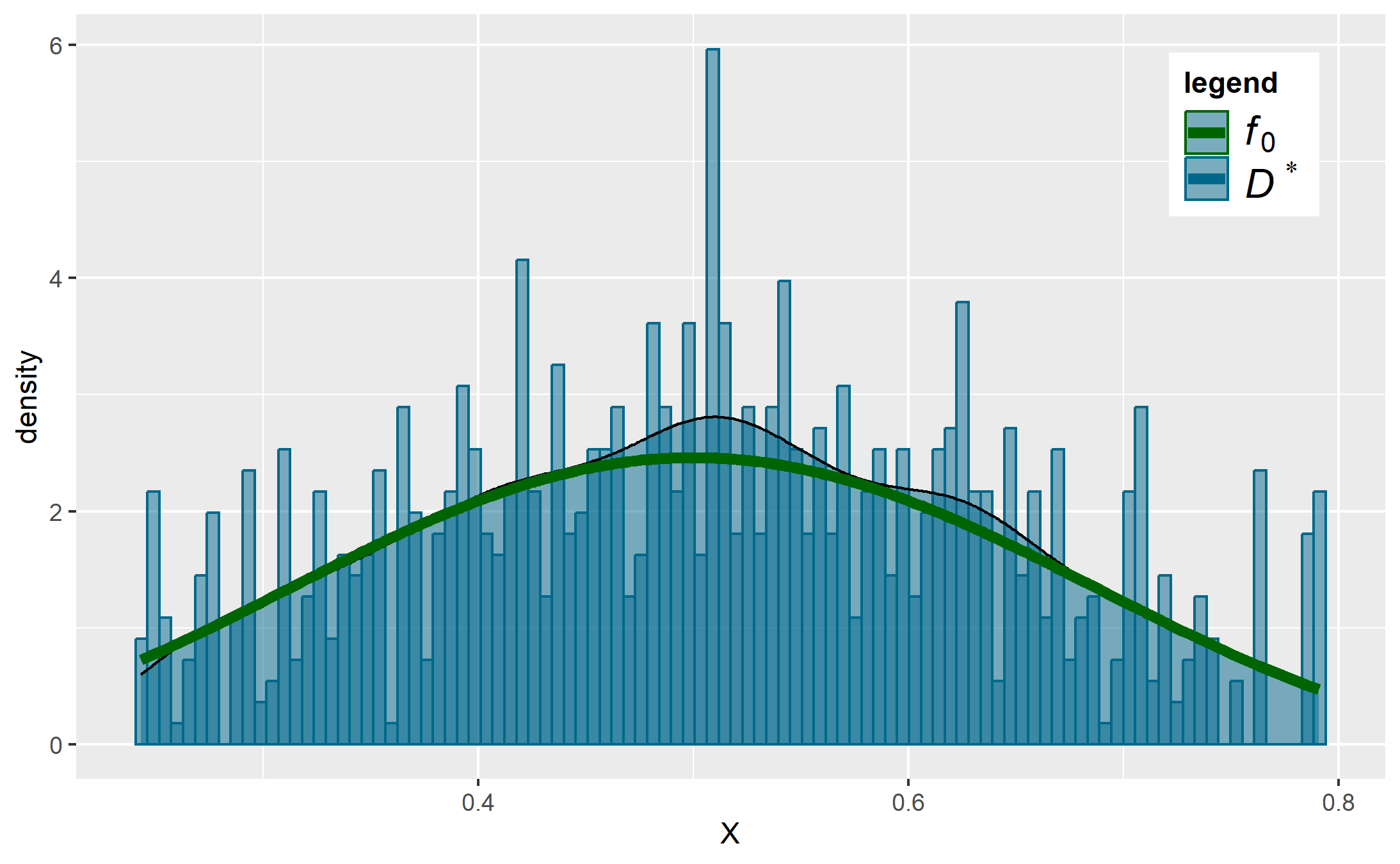

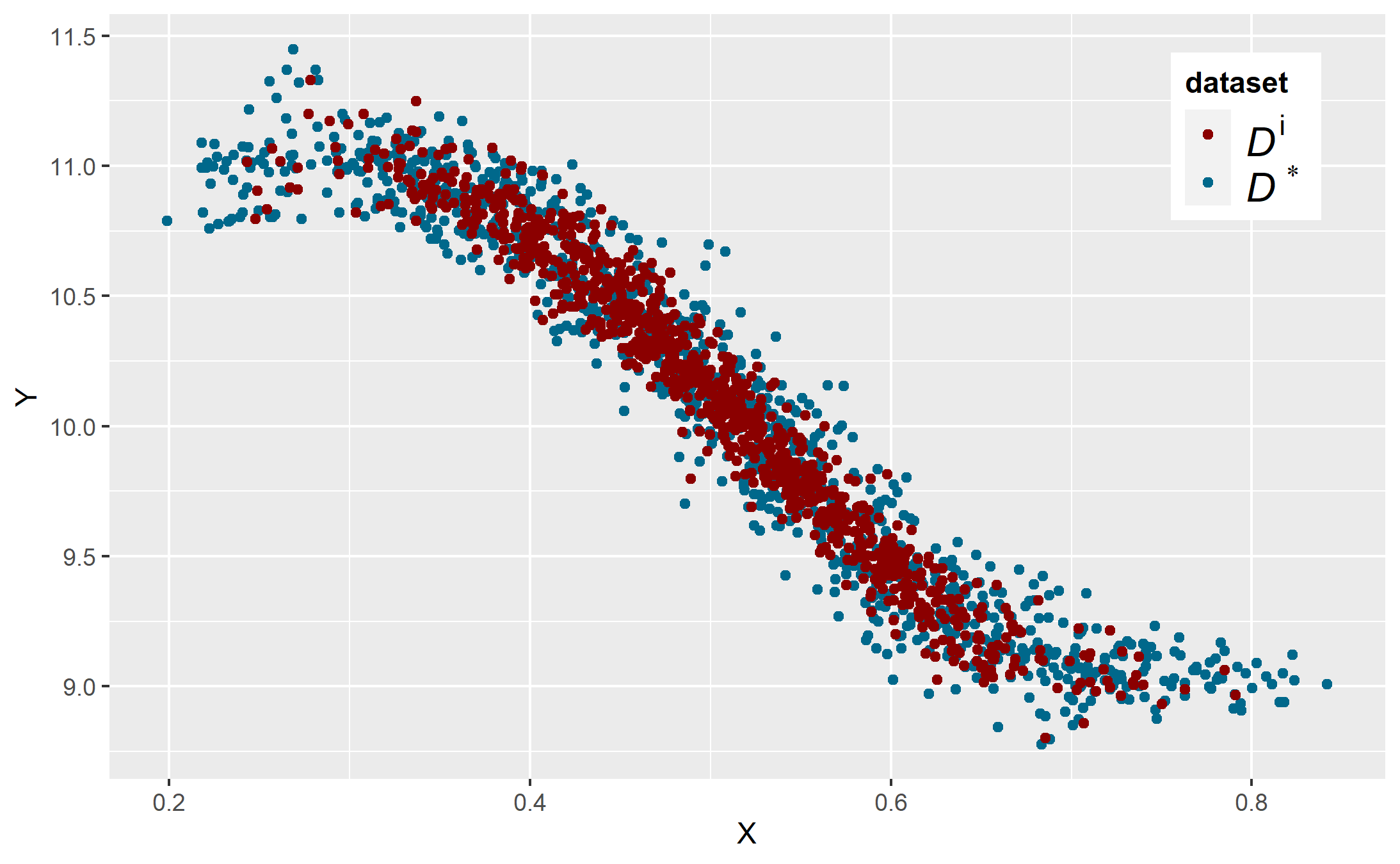

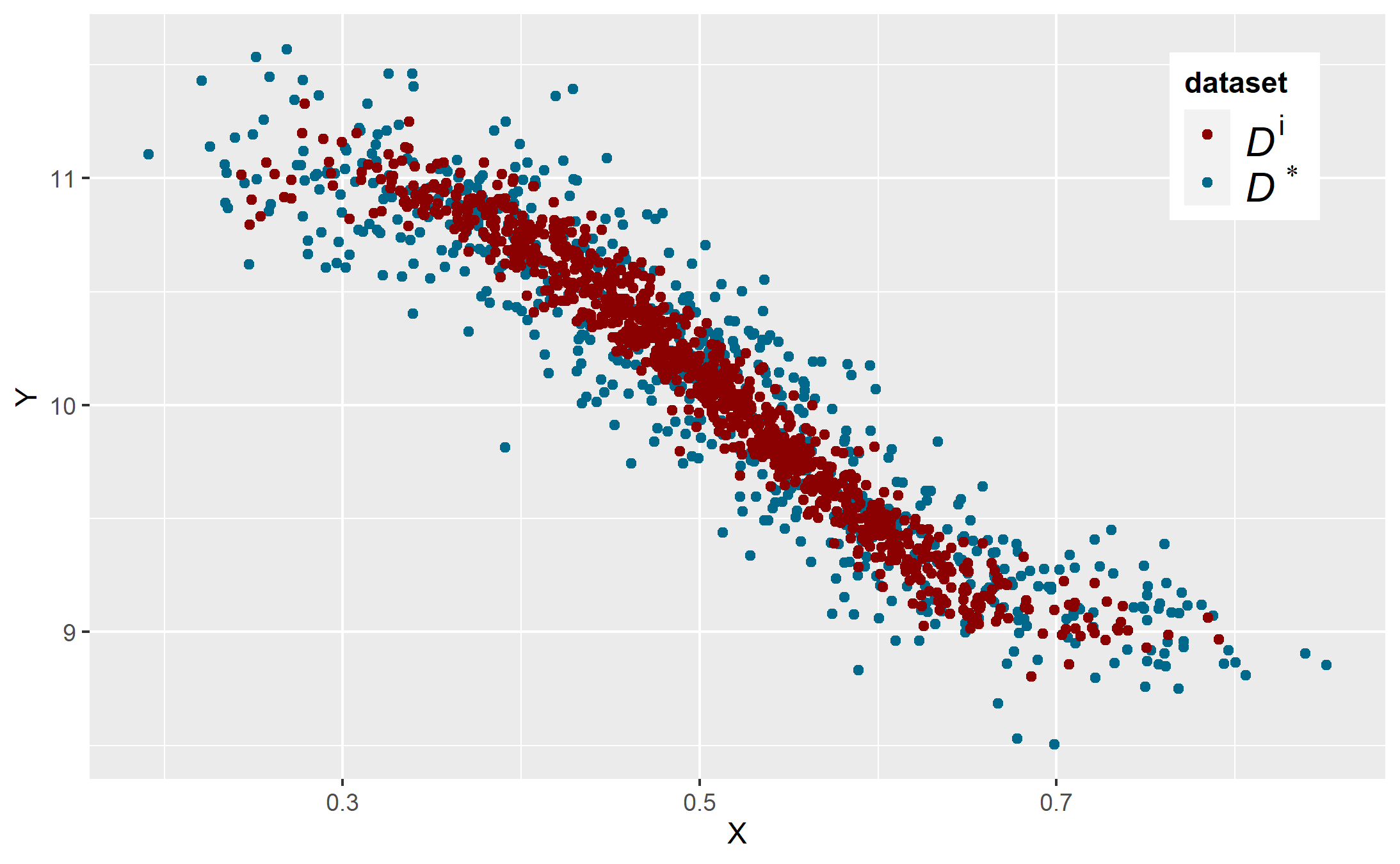

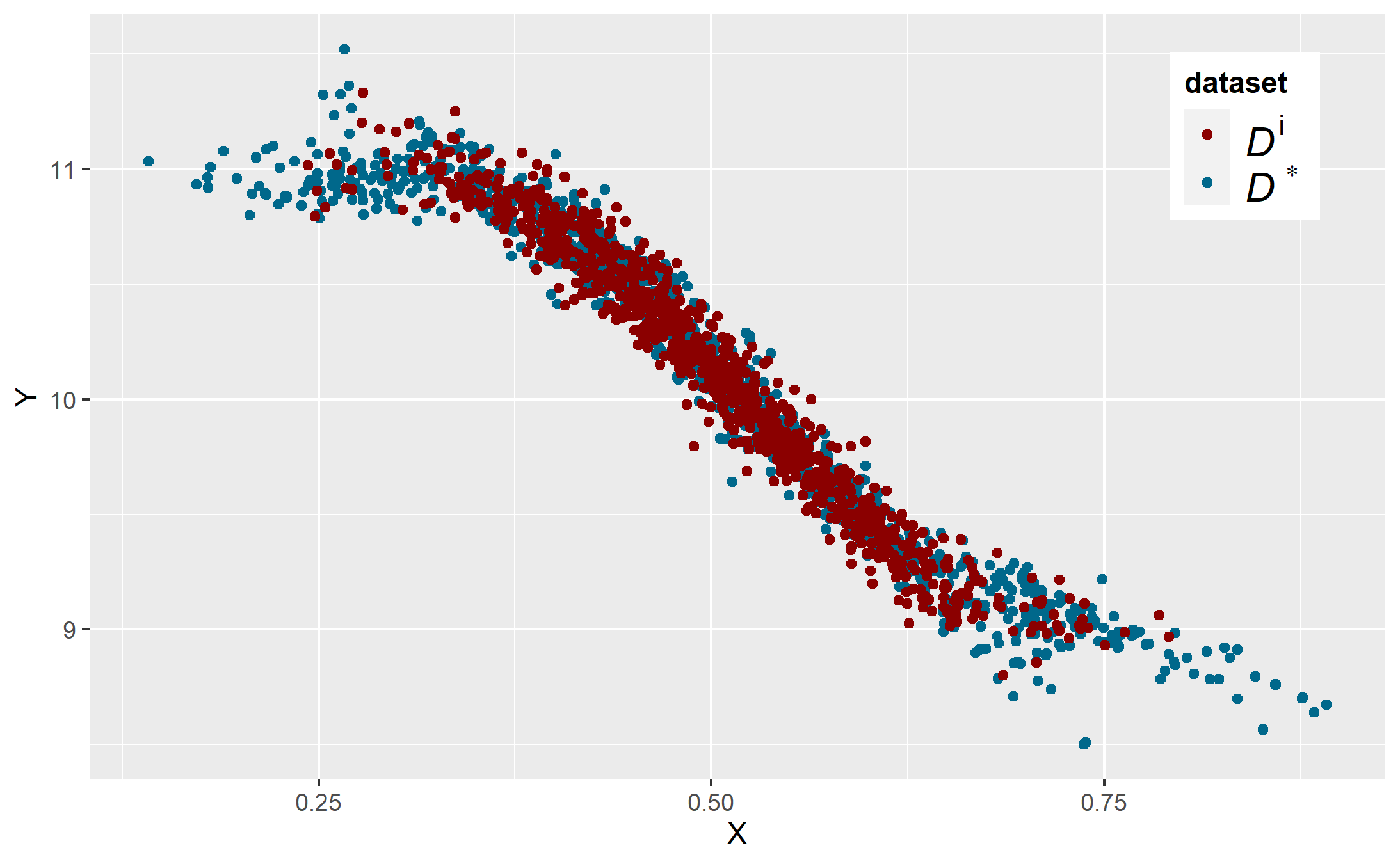

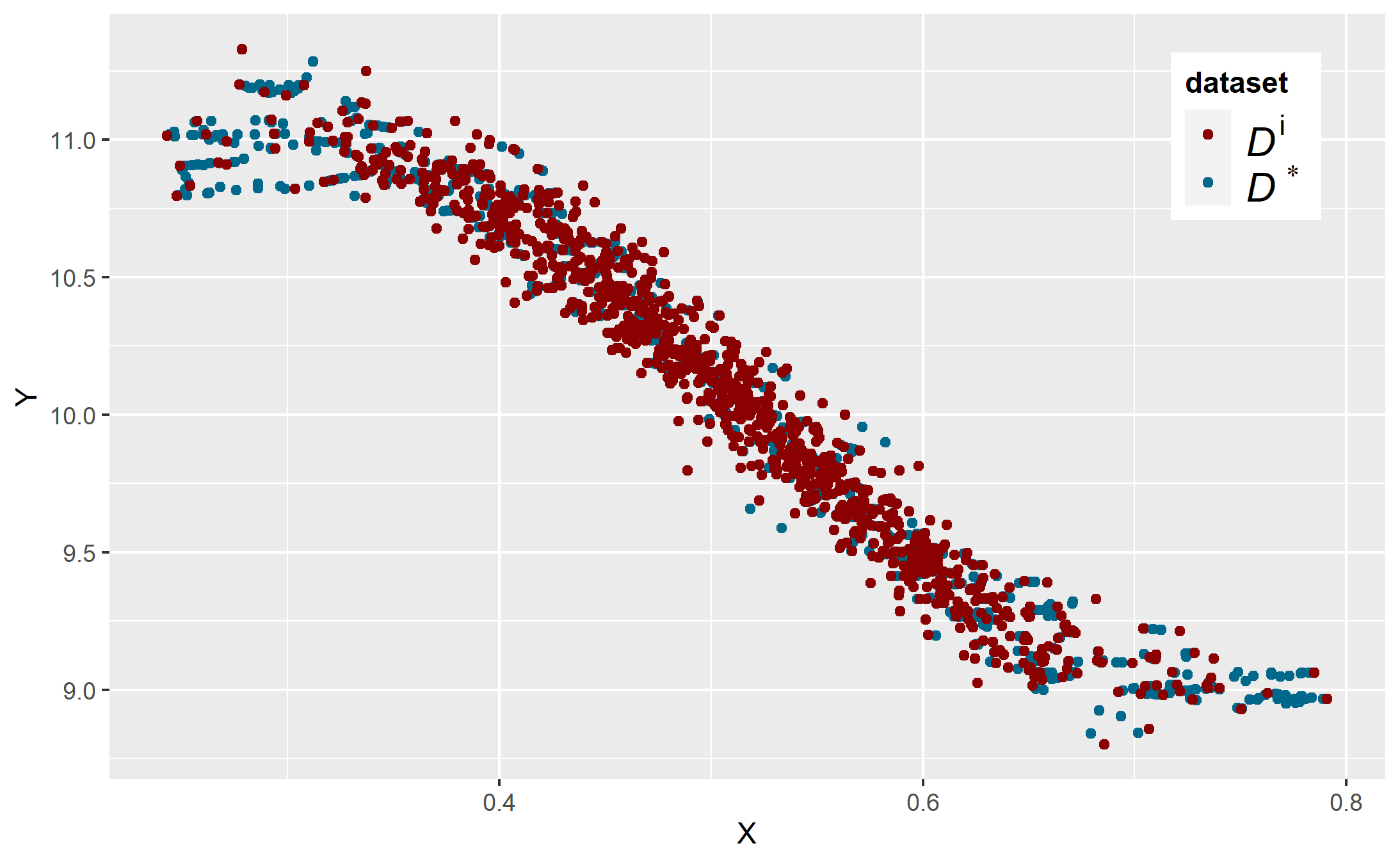

Figure 1(a) shows the empirical densities of in the population and in the imbalanced sample . Figure 1(b) shows the scatter plot from . As we can see, the imbalanced sample is more centered than the population and poorly covers the whole support of : there is less data on the sides and is different on these parts of the space. We face an imbalanced regression: a -imbalanced problem with, for example, when or and (). Here we are in the situation where and have the same support and the imbalanced problem will be less with large.

3.2 Data generation and resampling analysis

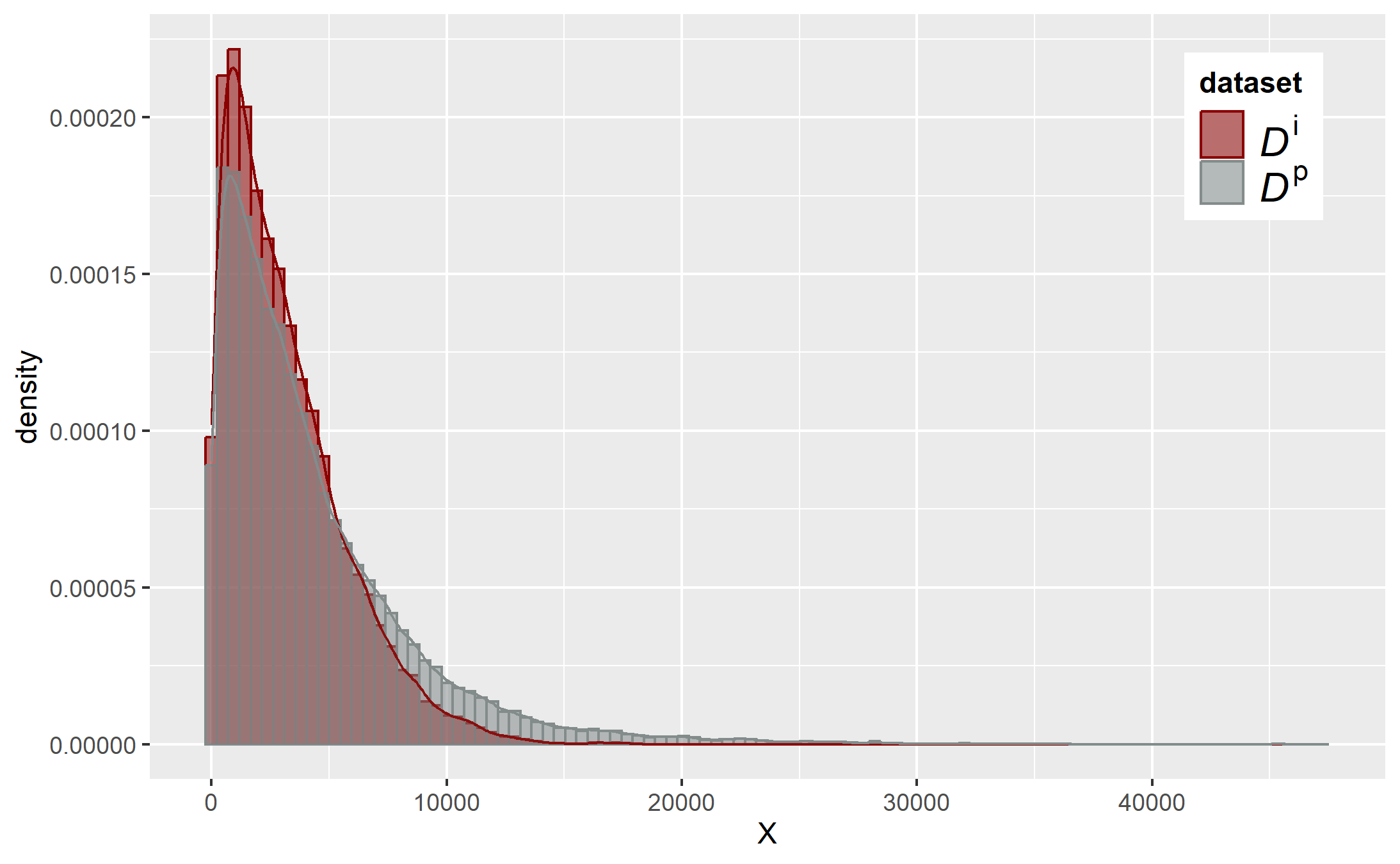

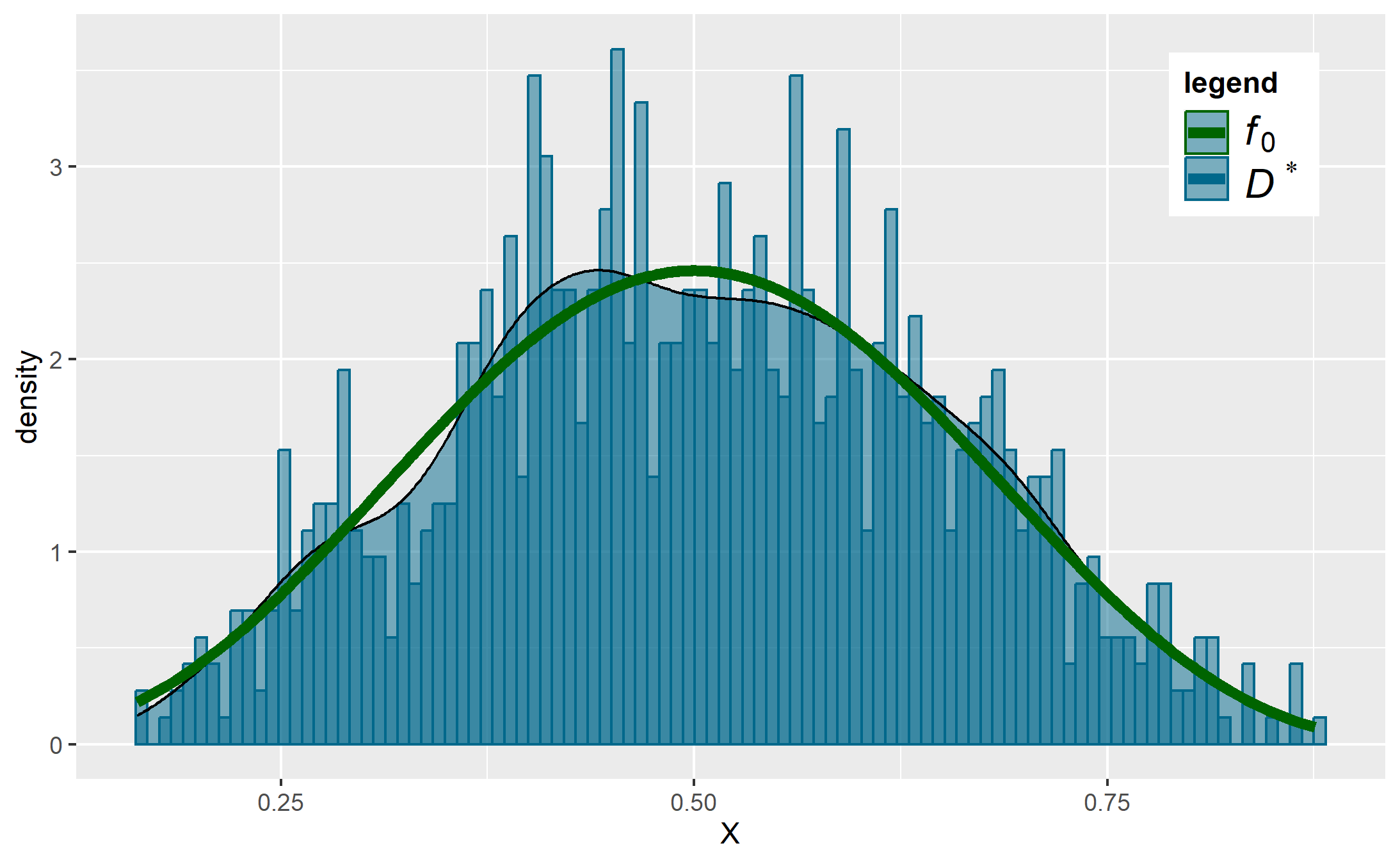

The aim is to build a new sample having a cdf close to the target one , as observed in Figure 5(a) in the Supplement. We define . We therefore want to obtain a wider distribution with more observations on the sides.

3.2.1 WR algorithm

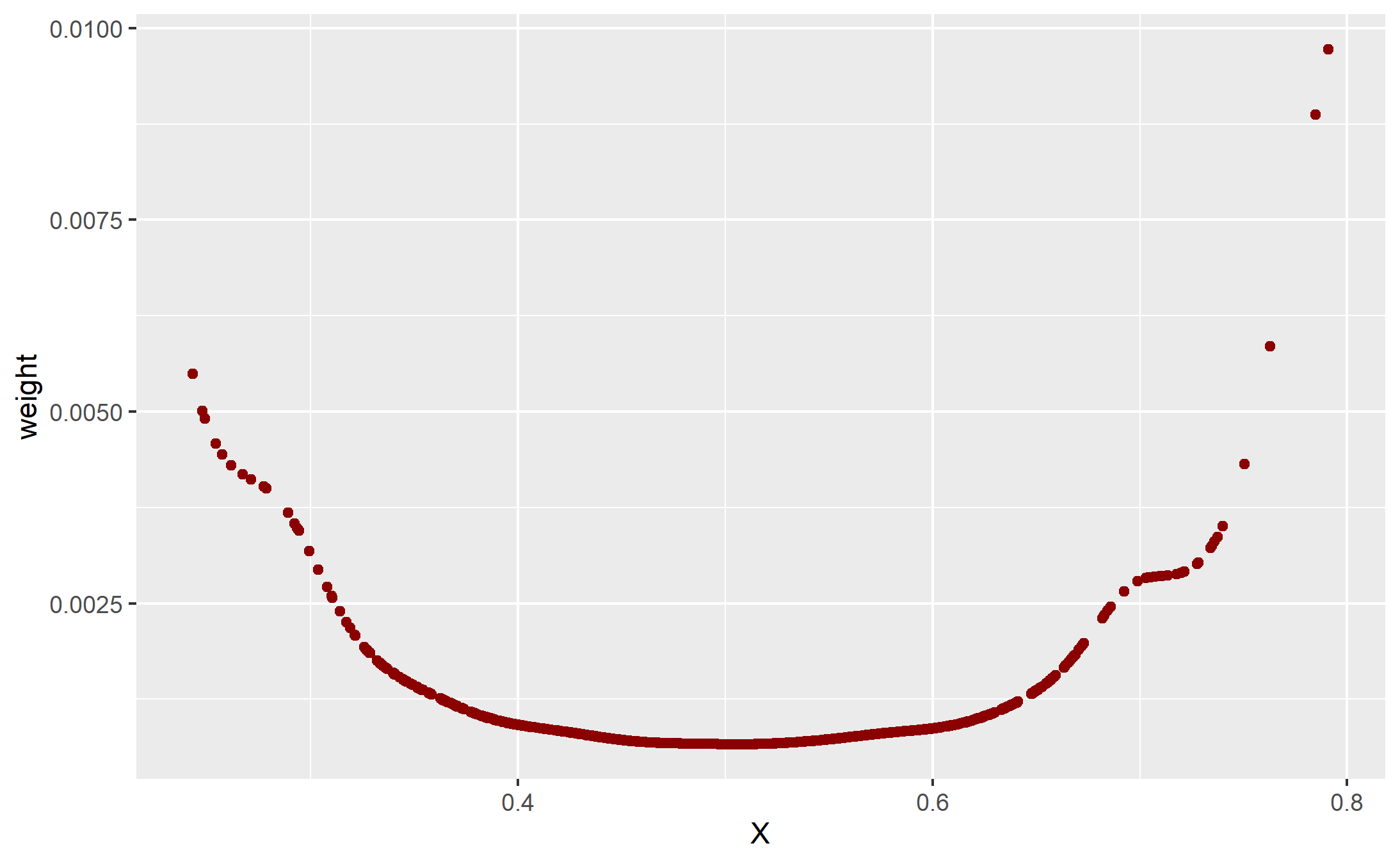

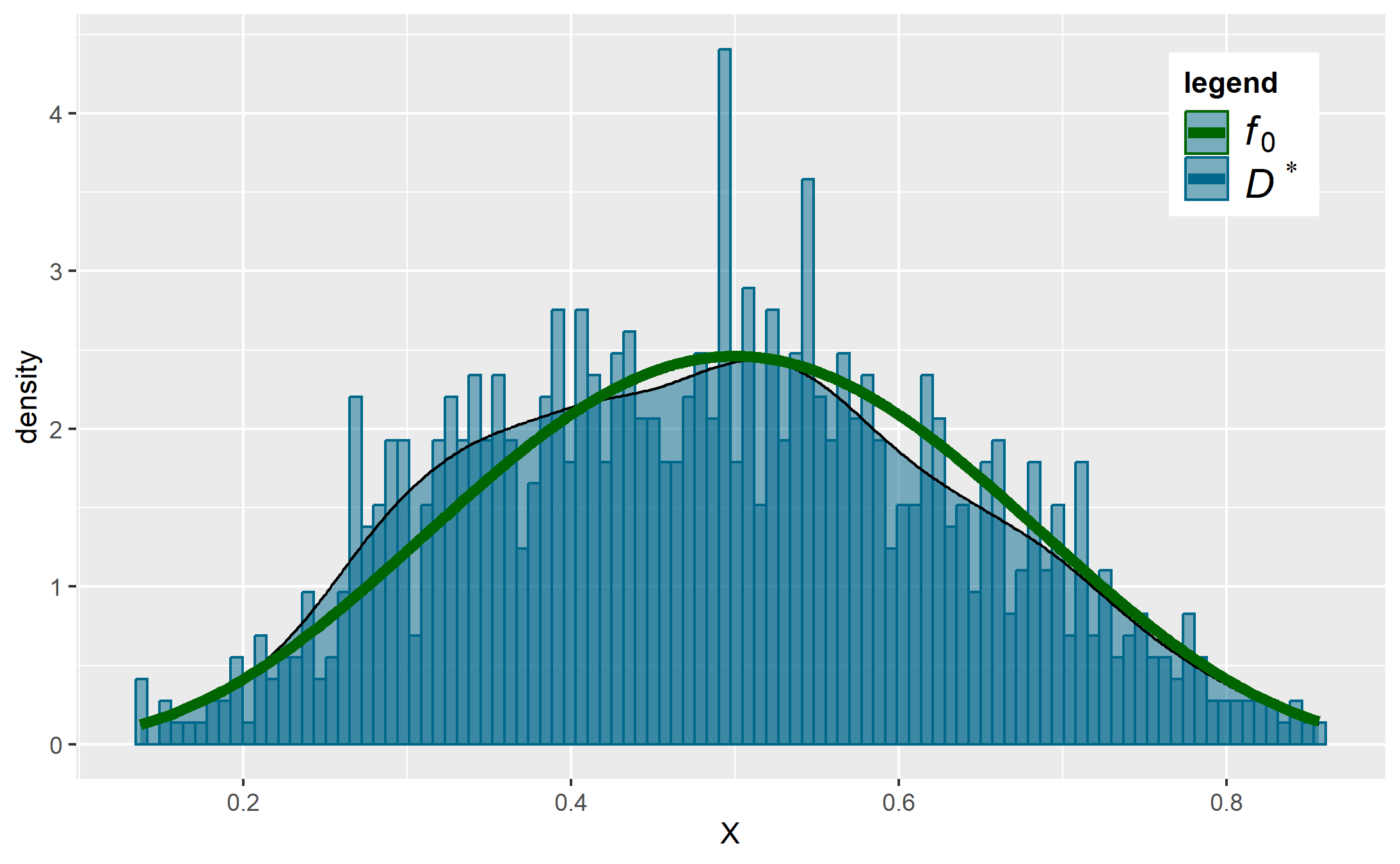

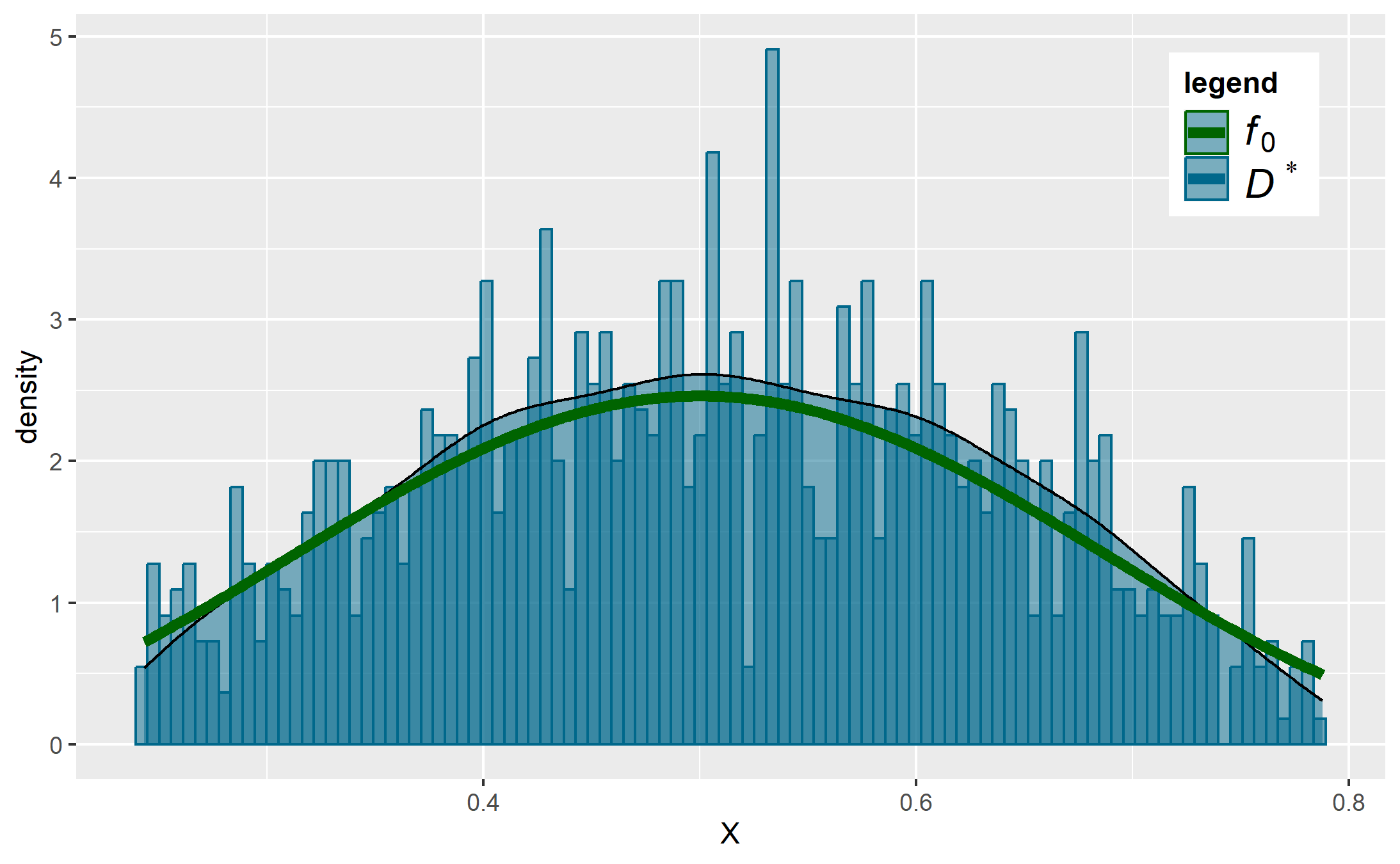

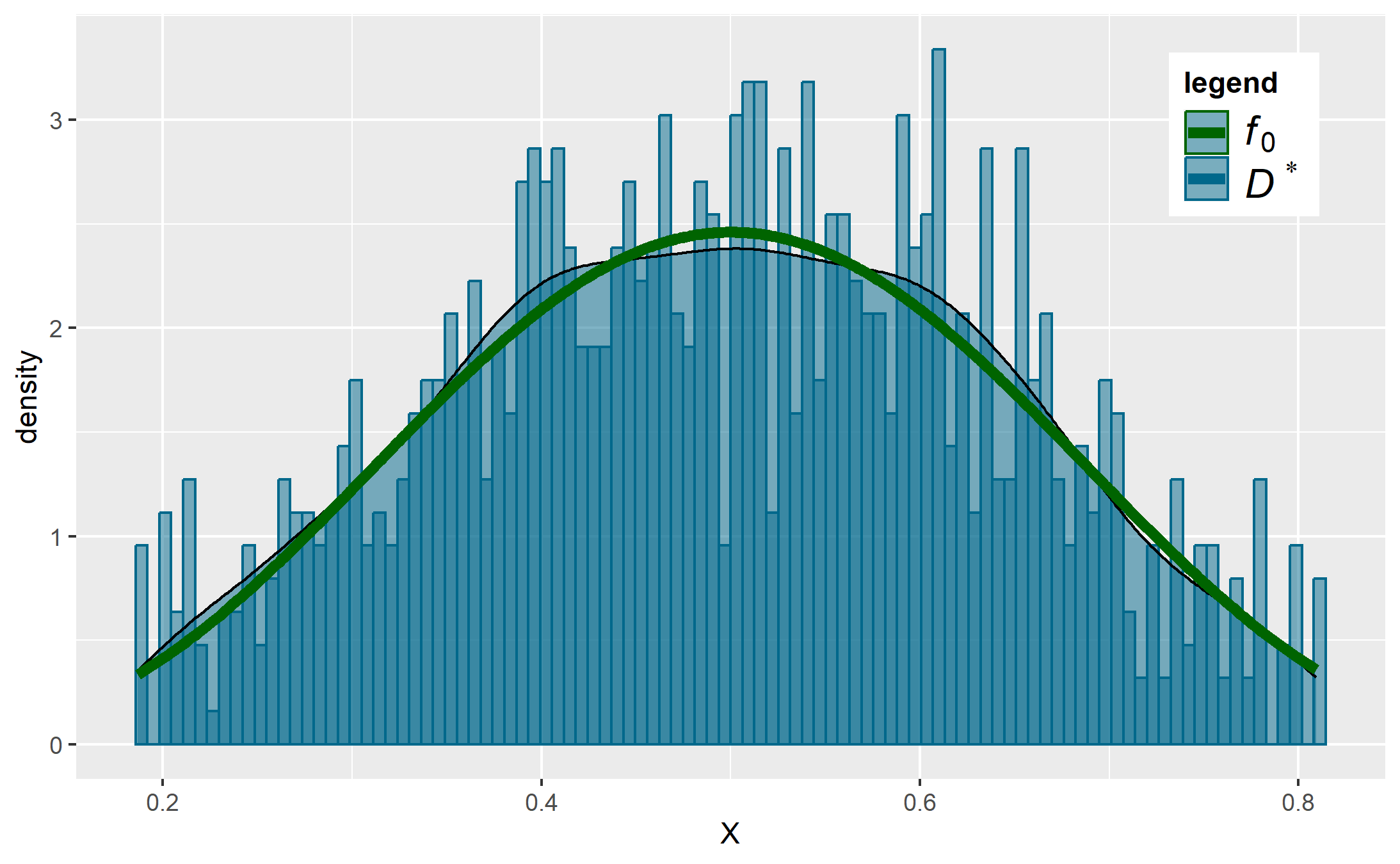

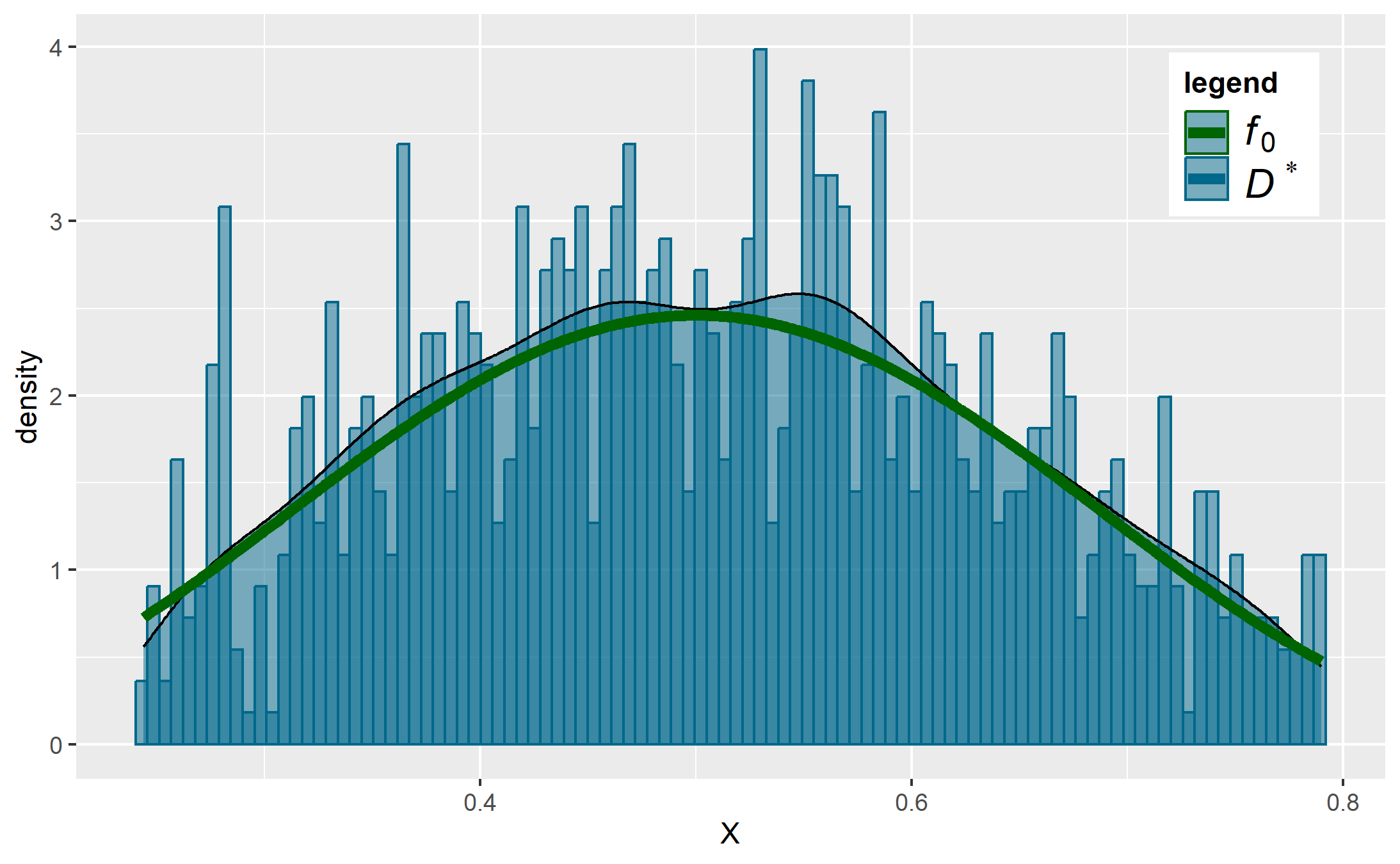

We first use the one-step WR algorithm. The draw weights calculated by the WR are represented in Figure 5(b) in the Supplement. Figure 2 shows the distribution of in the WR sample which is closer to the target distribution than the initial one. The values on the sides, quite rare, are naturally often drawn. We see there are still some parts of the support without observation, especially on the right side. This situation could lead to an overfitting phenomenon because the same observations are replicated several times and could lead to an over-fitting effect.

3.2.2 DA-WR algorithm

The different data generators are applied directly on the imbalanced sample or by a clustering obtained with a Gaussian Mixture Model (GMM) in order to generate synthetic observations within each cluster. The results of this clustering on the initial sample are presented in Figure 6 in the Supplement.

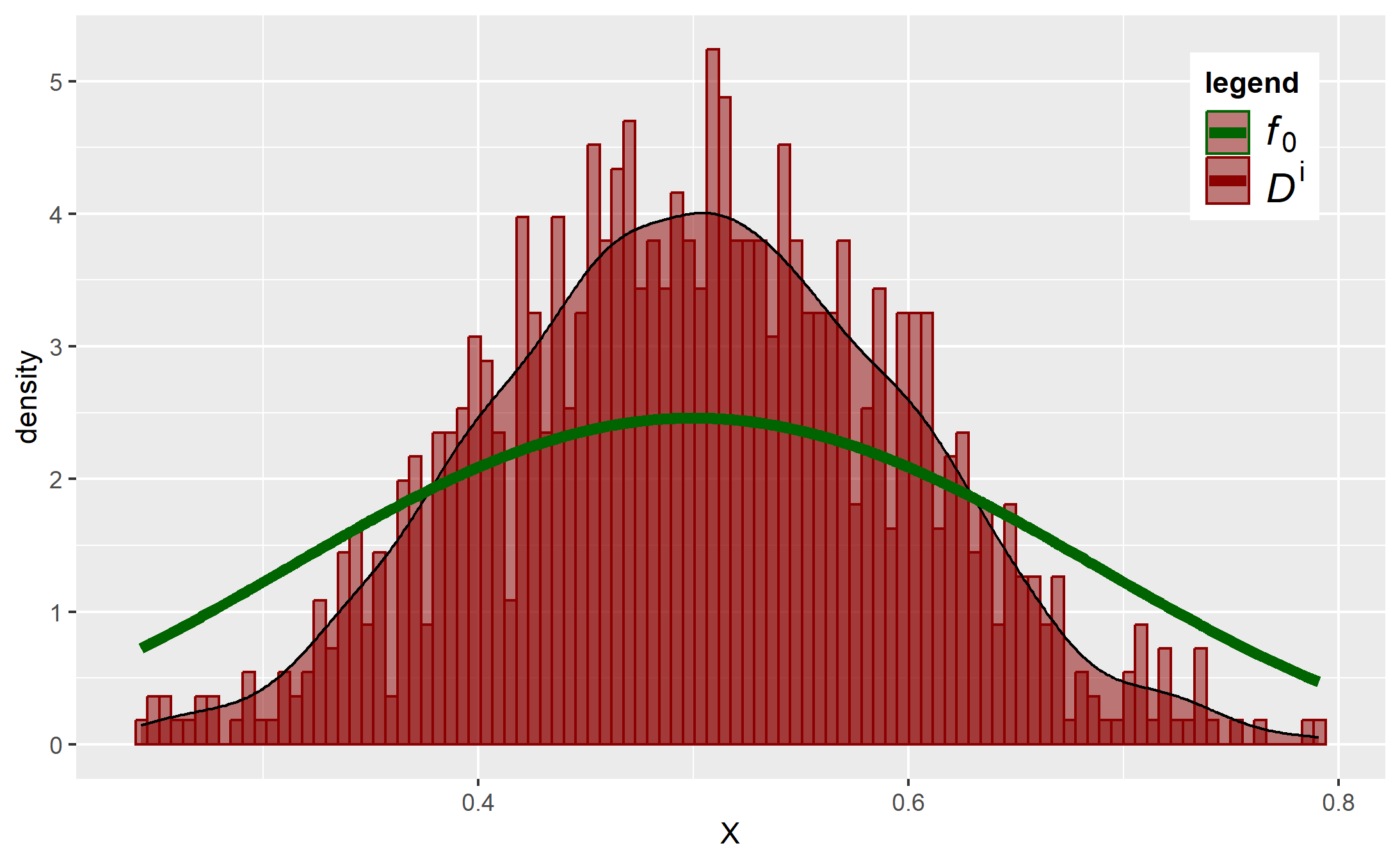

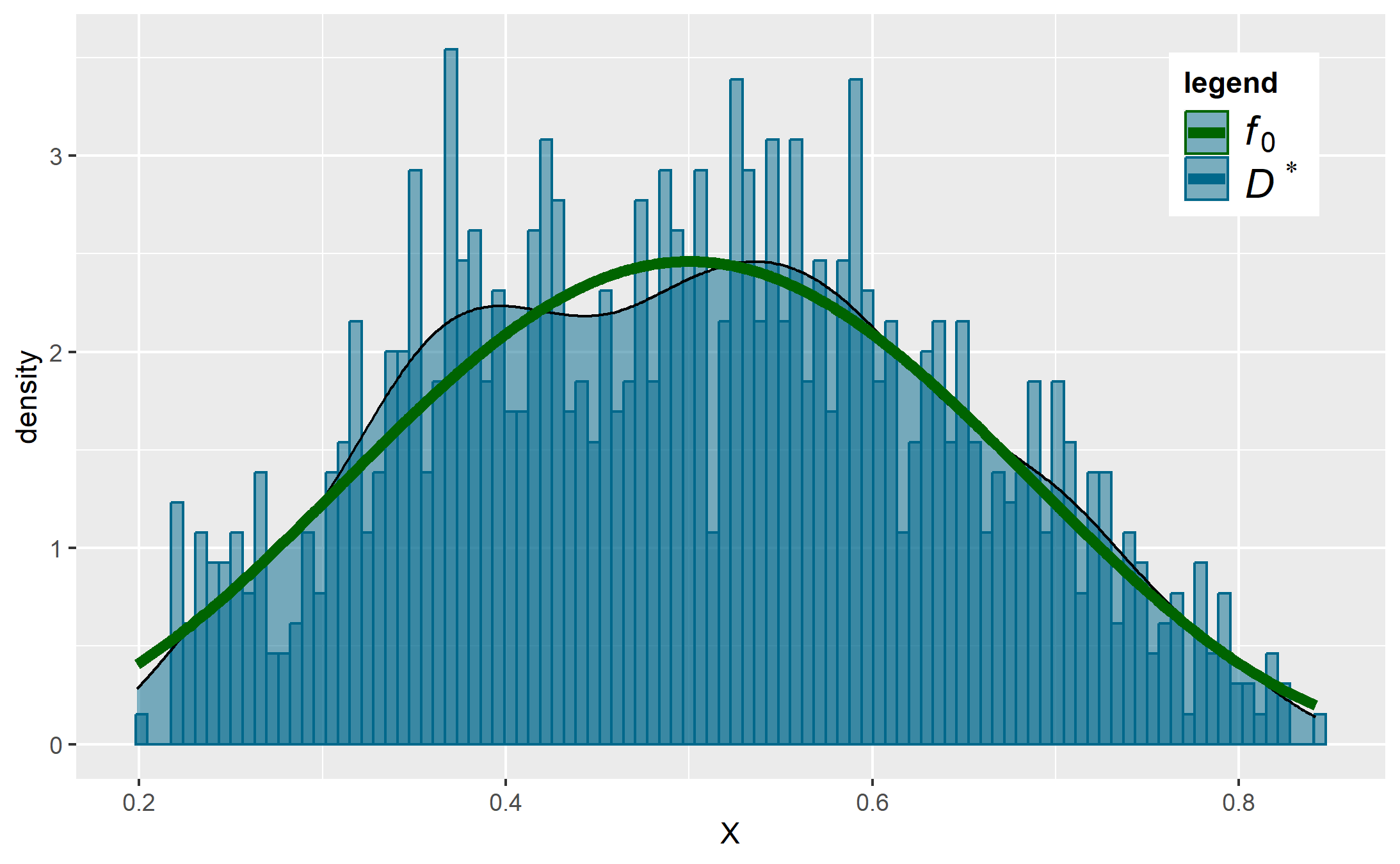

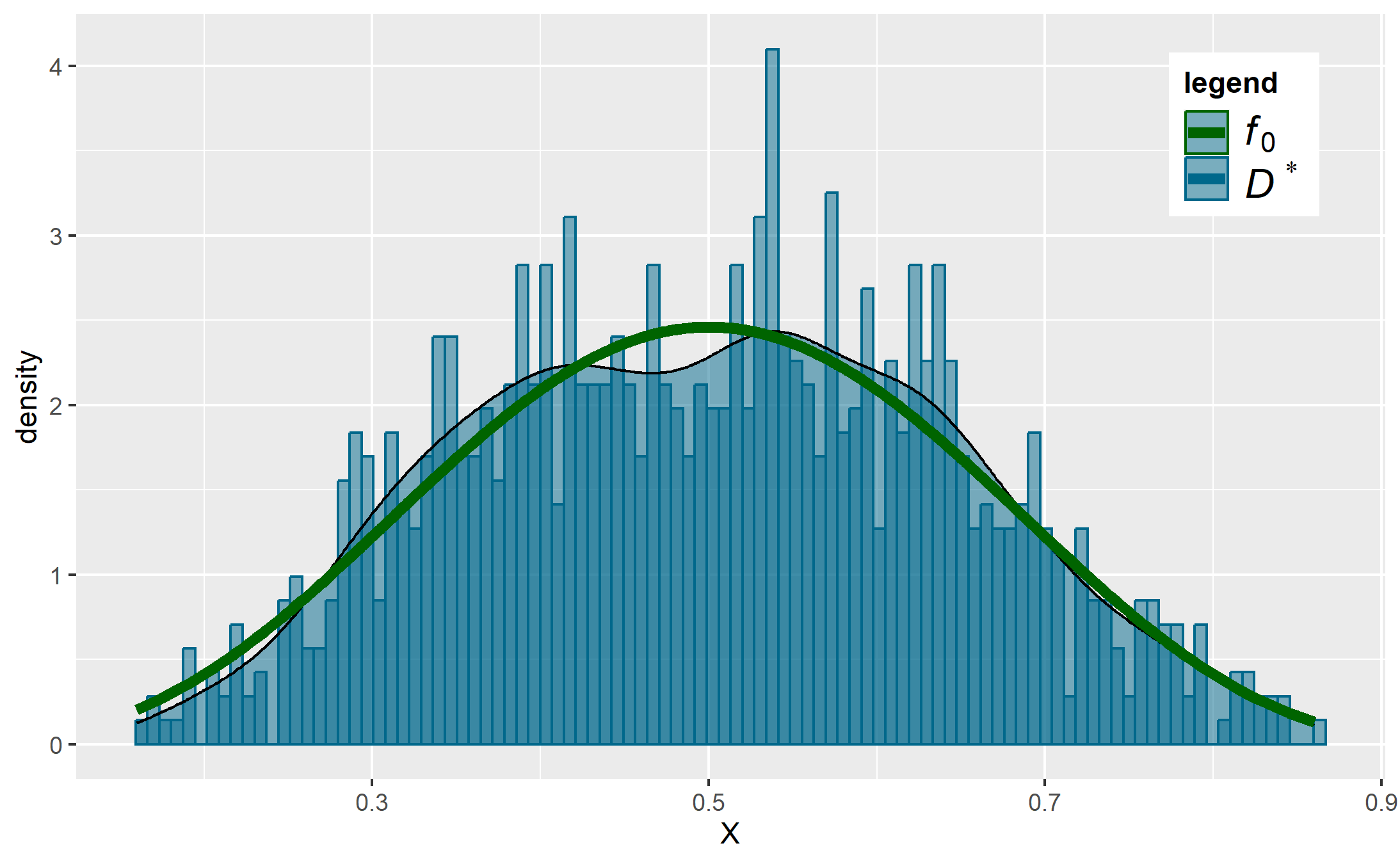

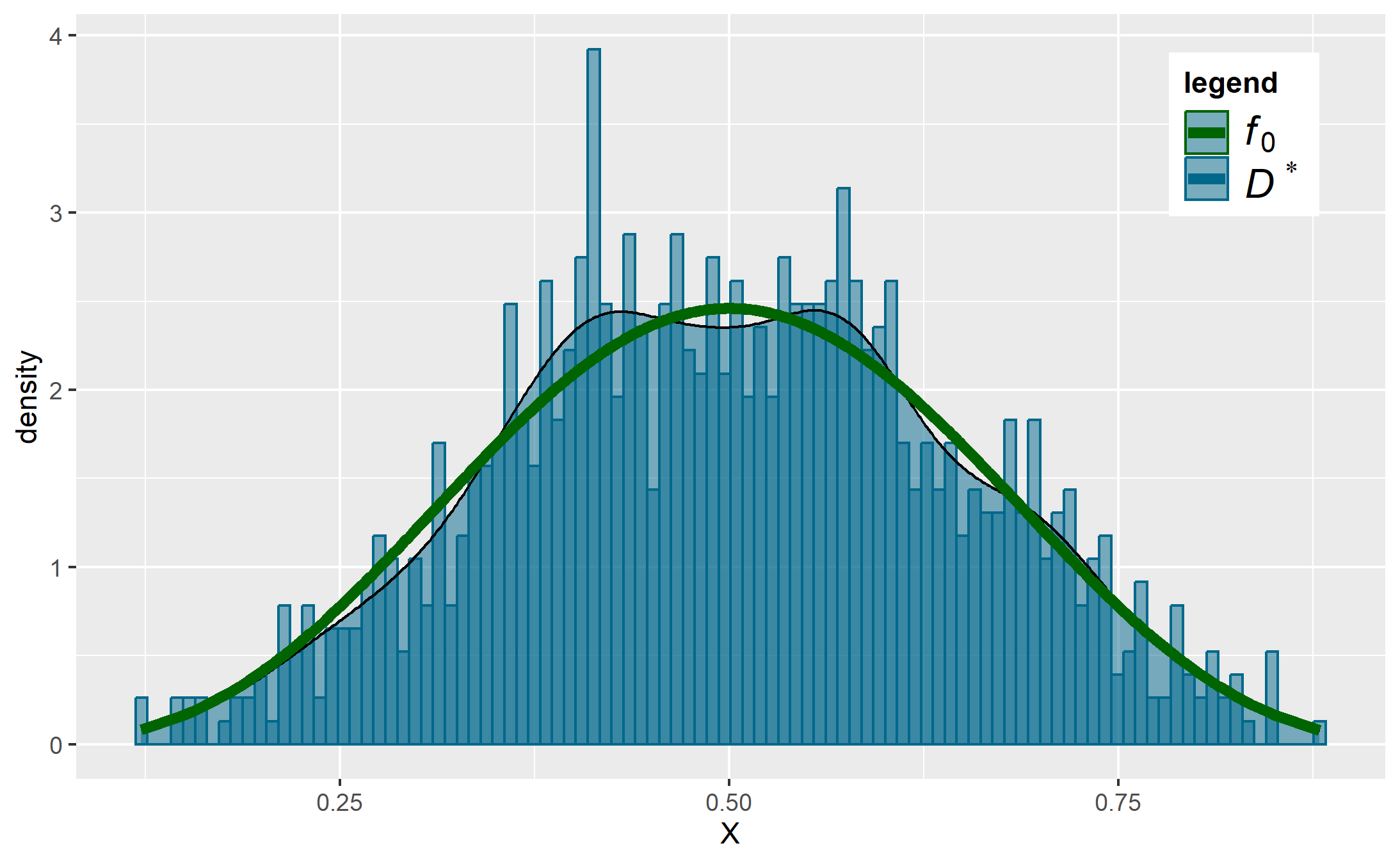

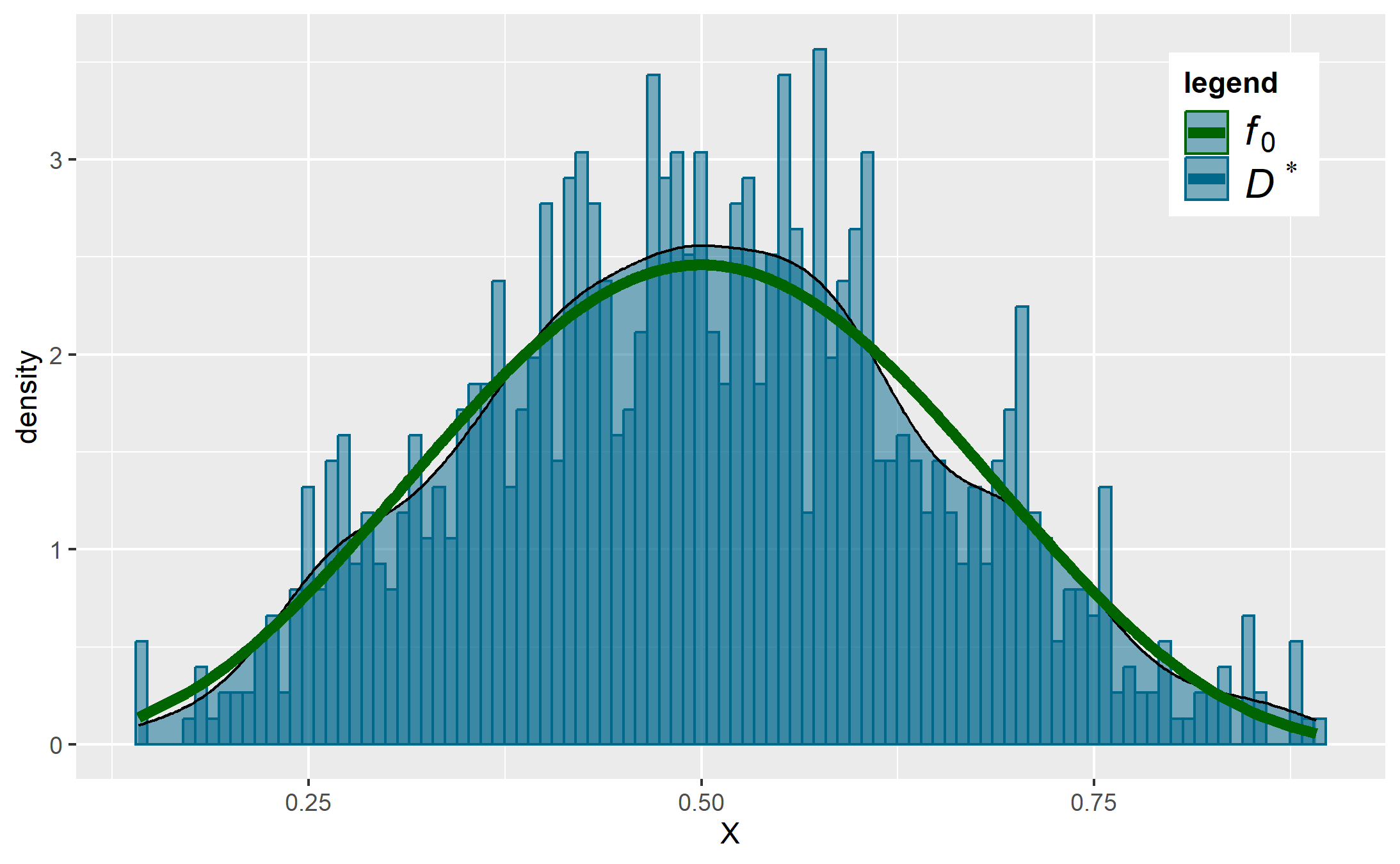

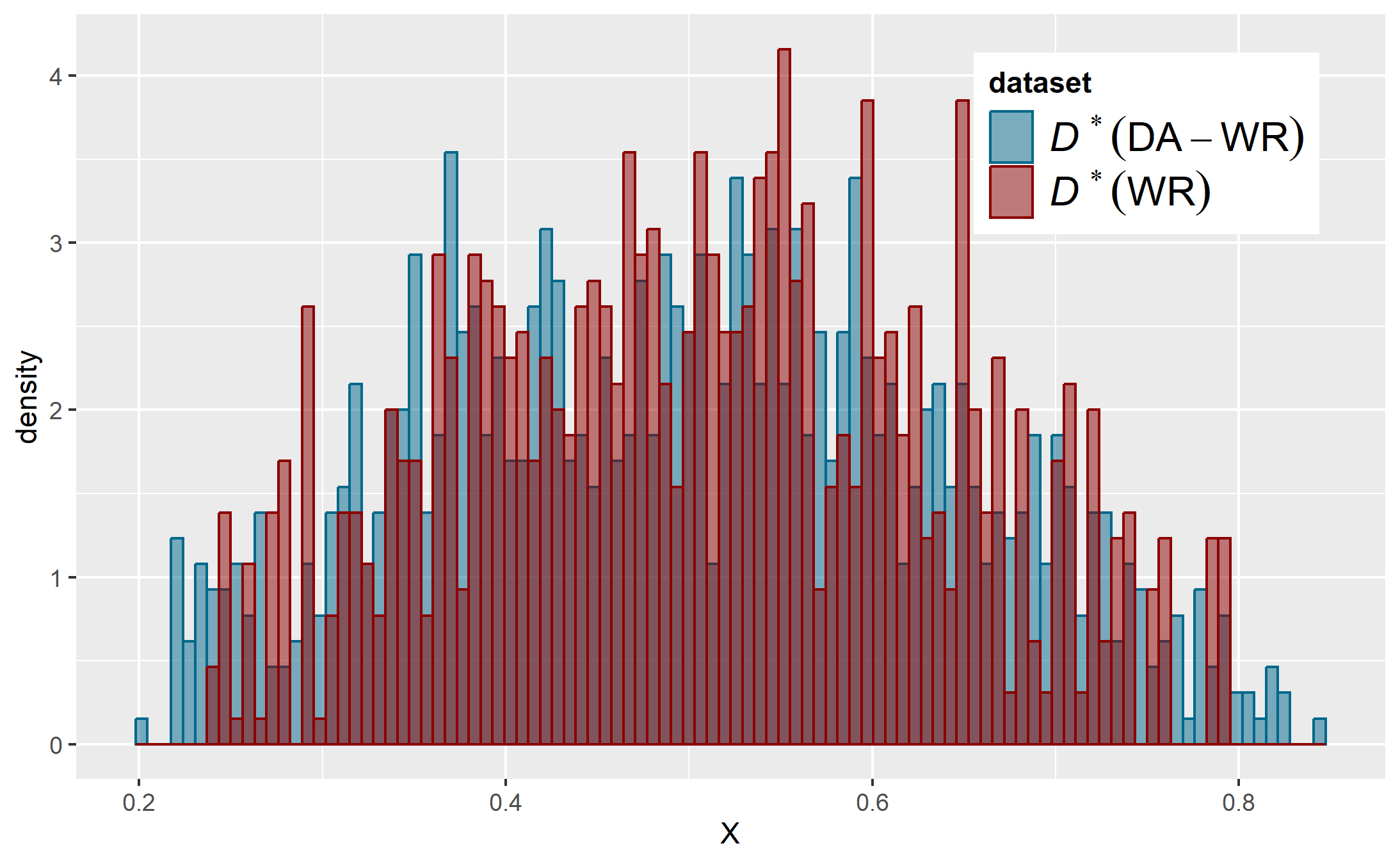

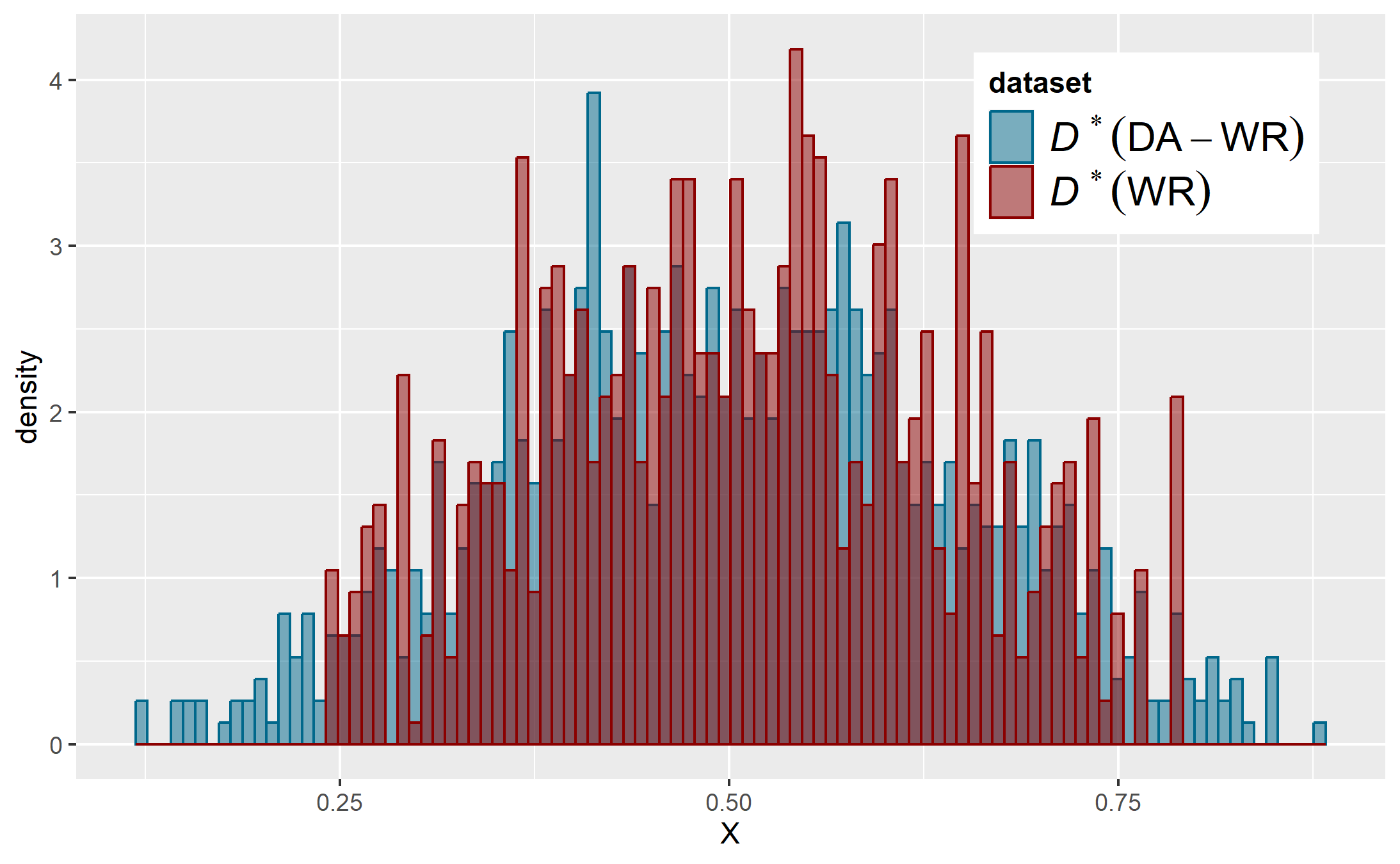

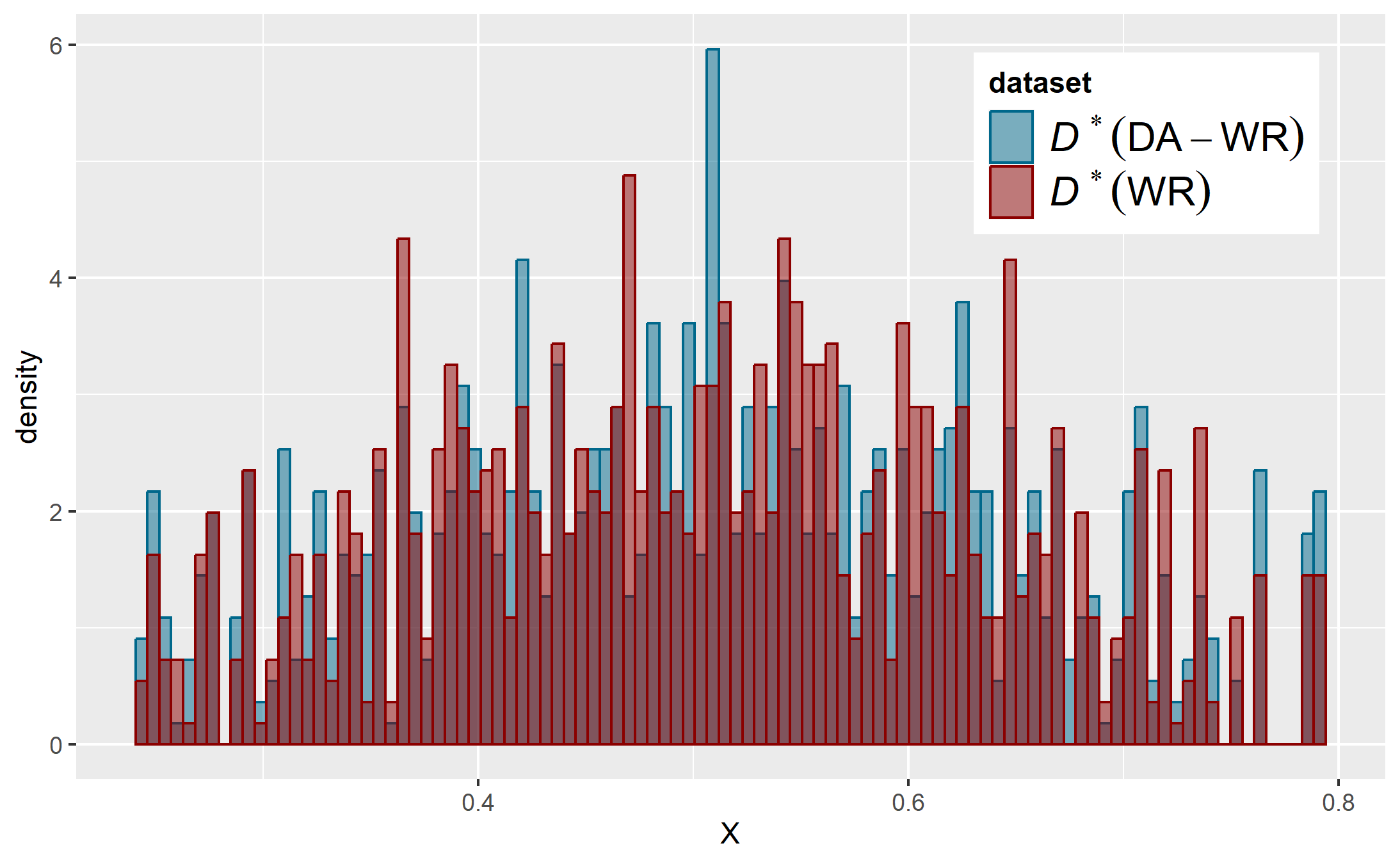

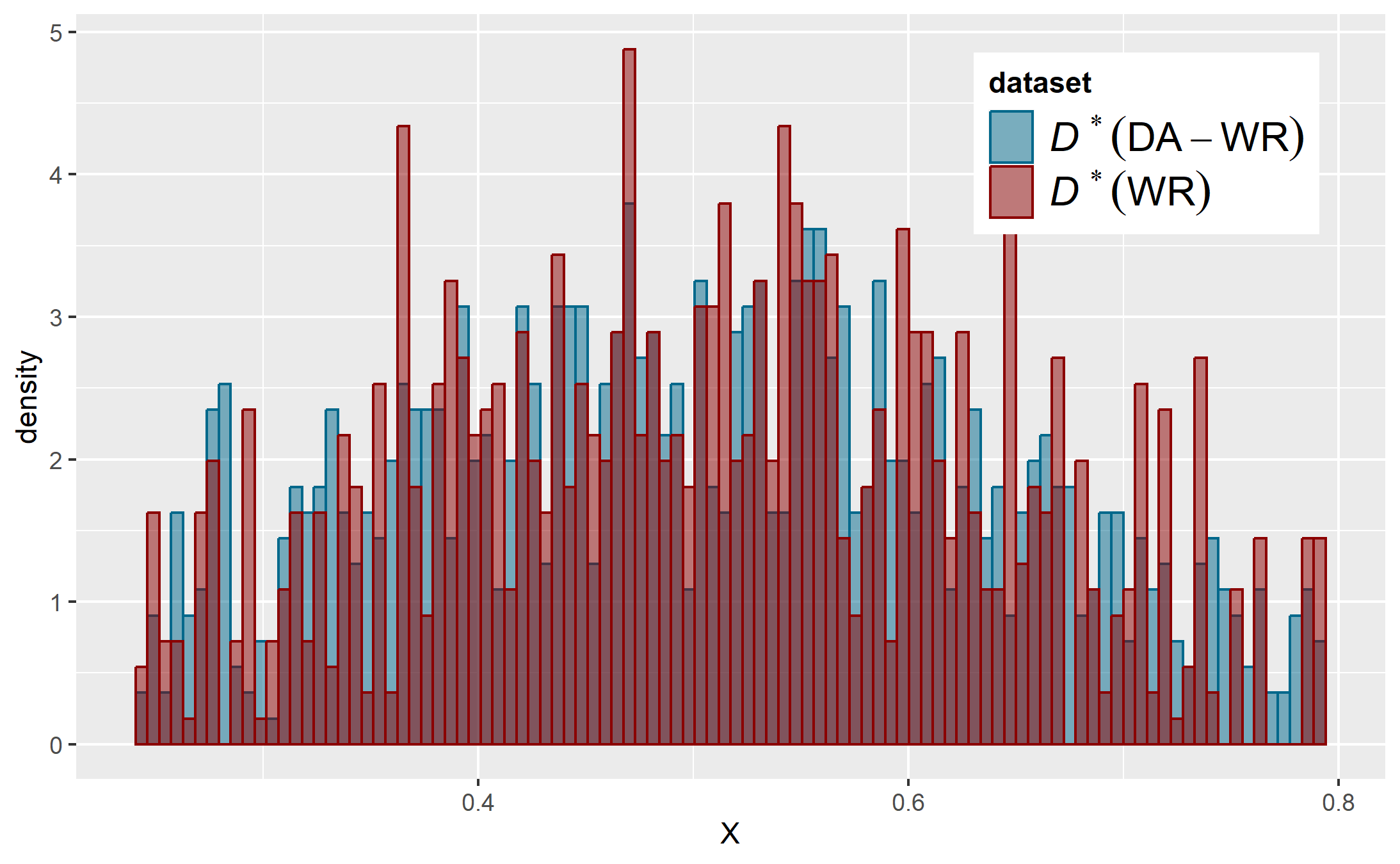

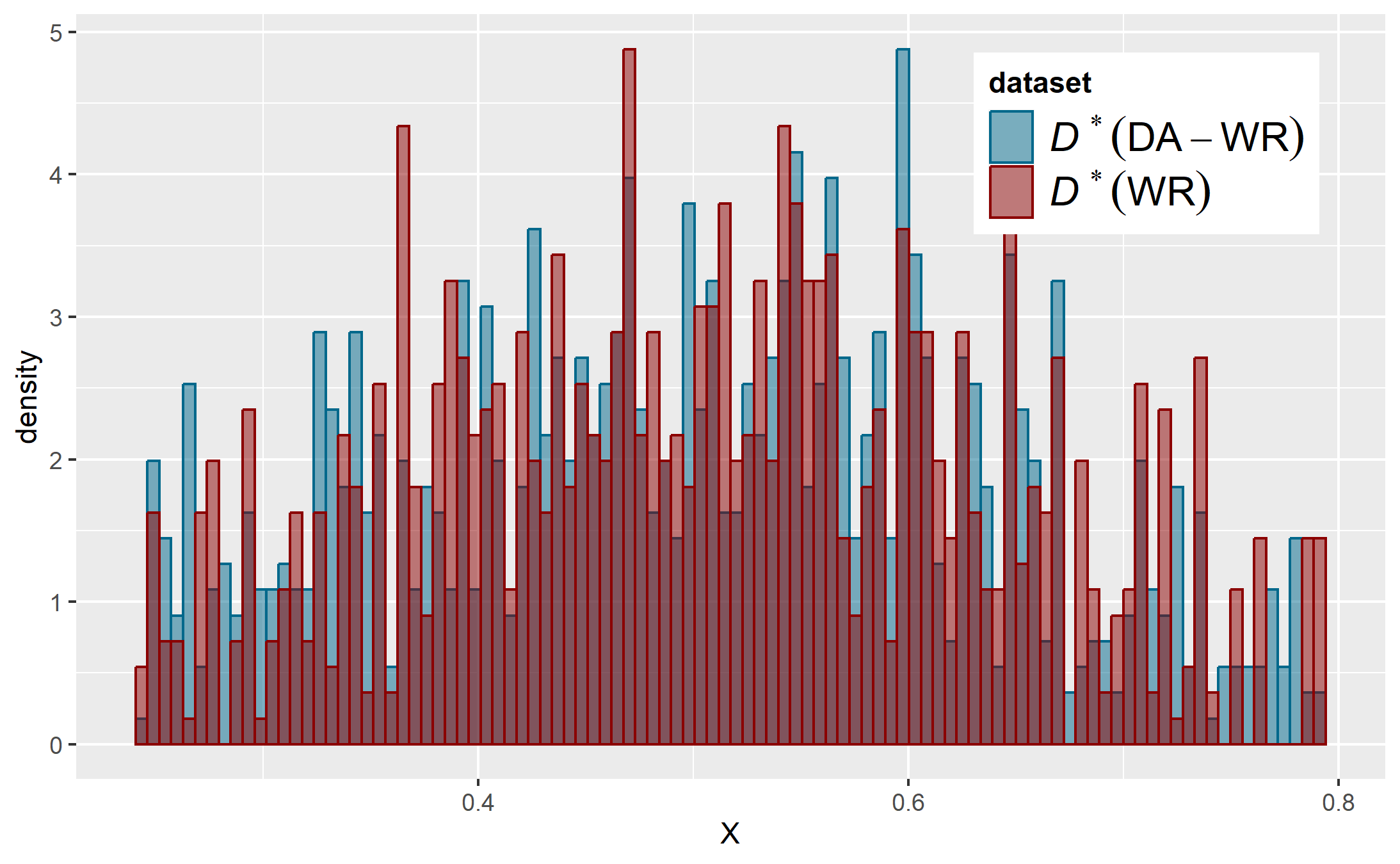

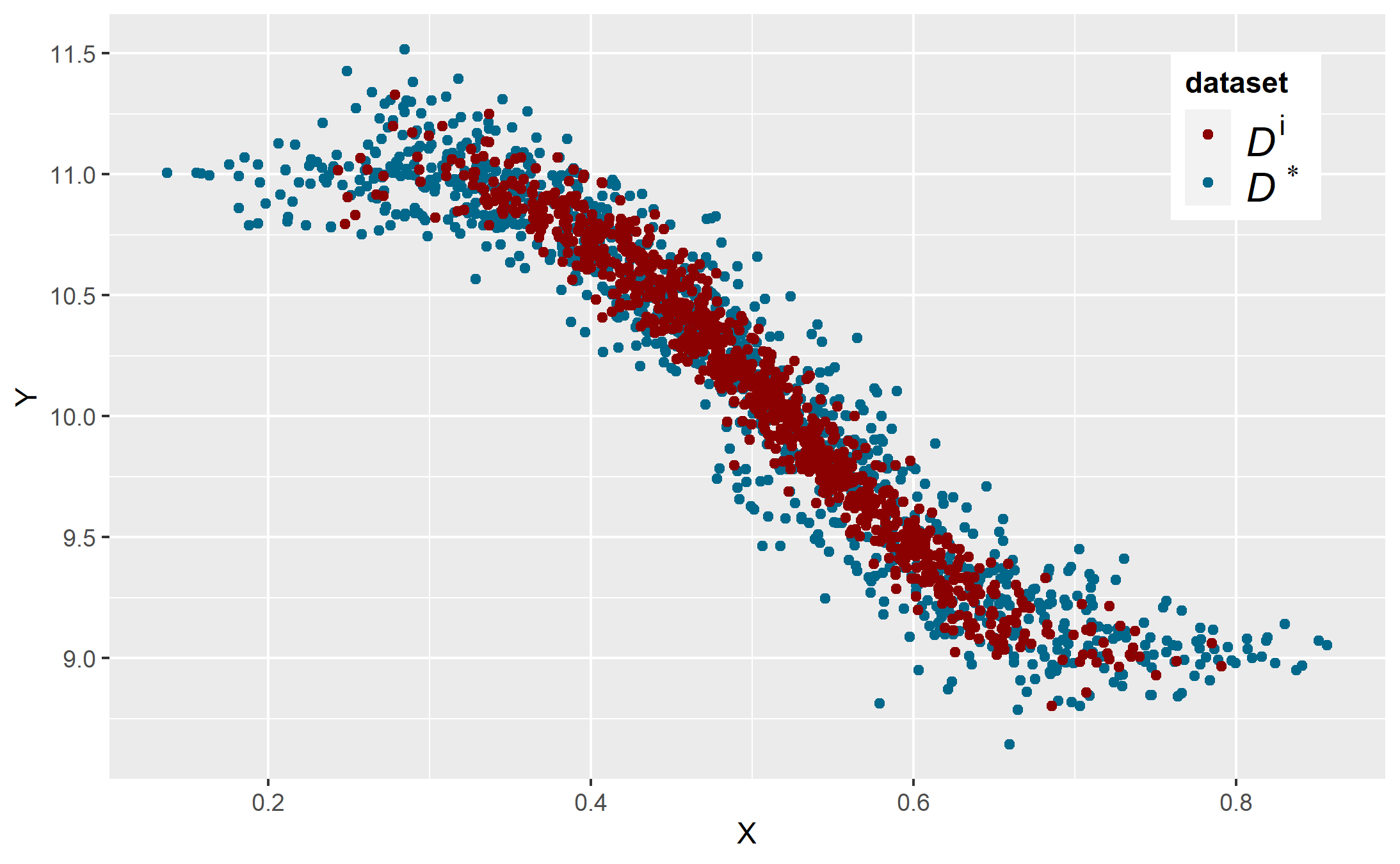

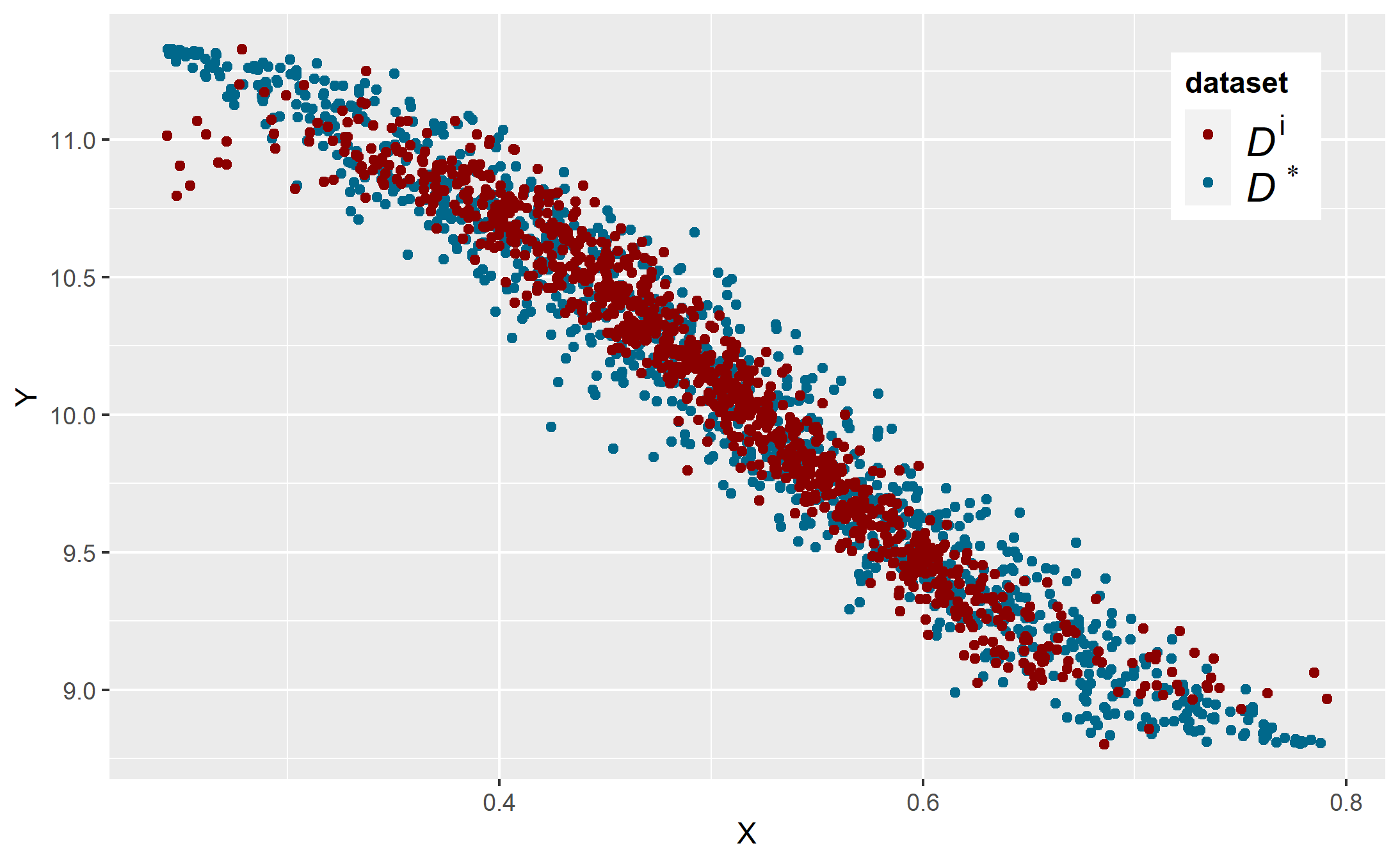

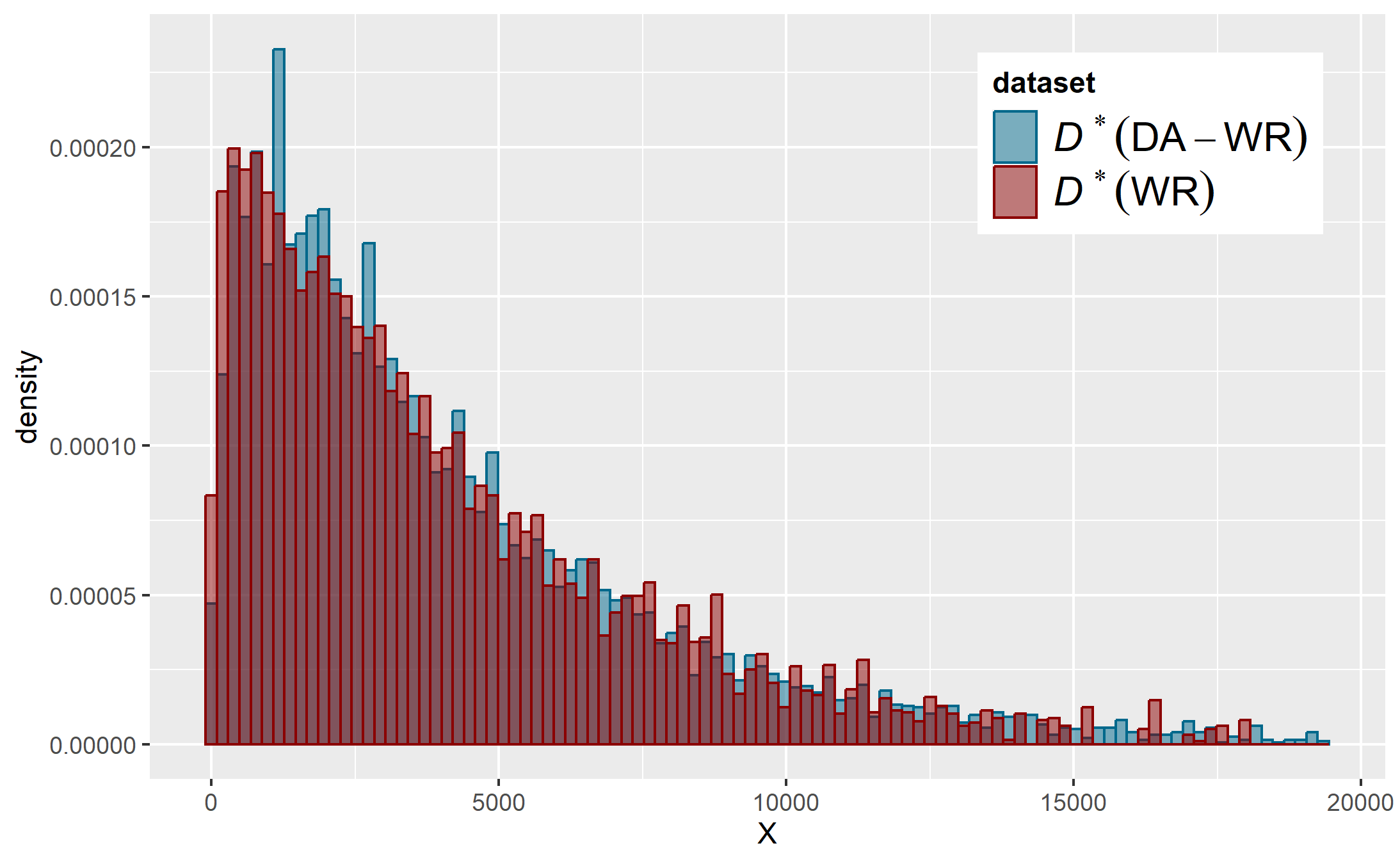

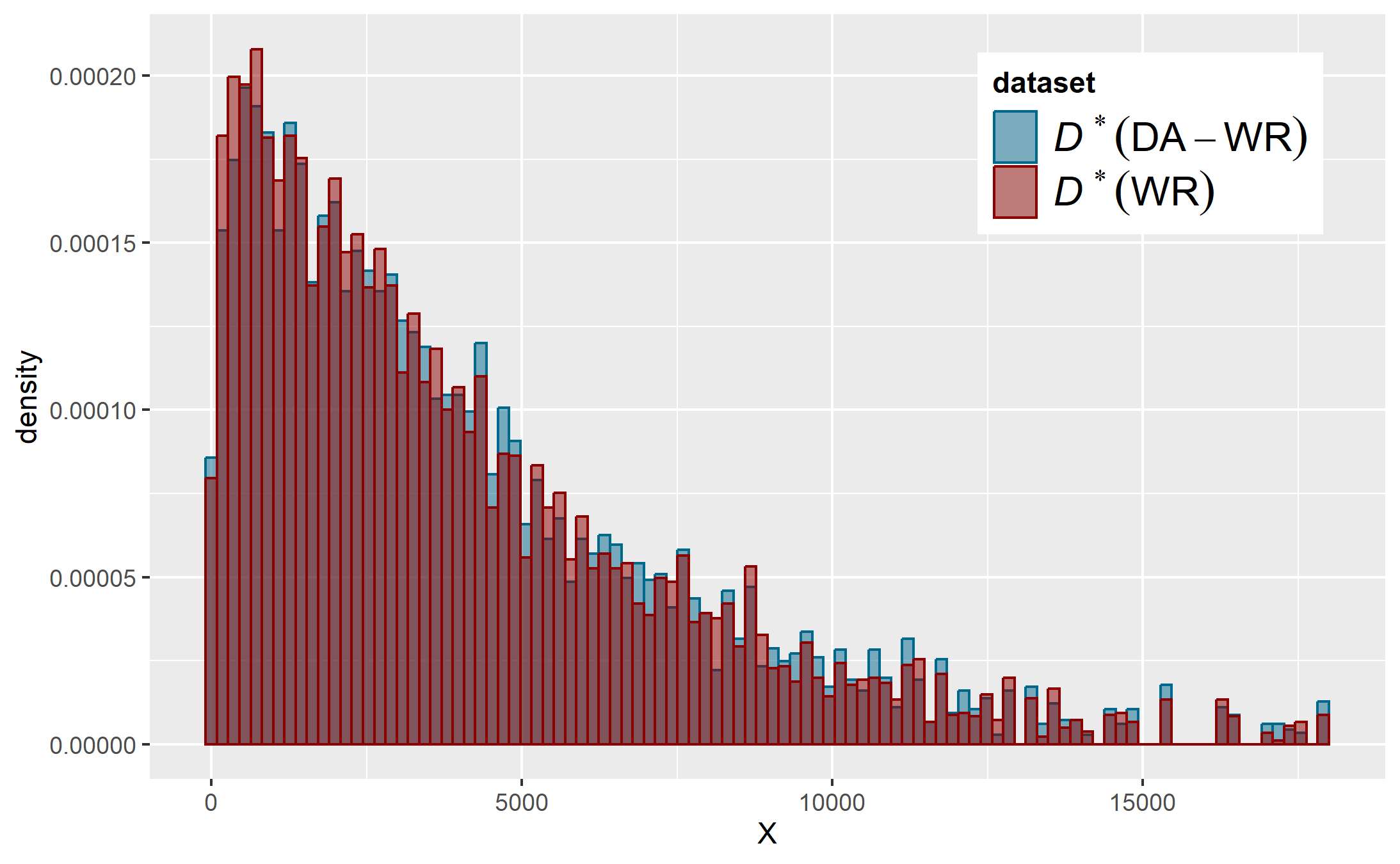

Figure 3(a) shows the histograms of obtained both with WR and DA-WR algorithms (with a Gaussian Noise method). As expected, the observations are more extended on the sides and cover more the support with Da-WR: some initial parts without observations are filled in. We also observe that the DA-WR distribution is closer to the target one than the WR sample. Figure 3(b) presents the scatterplot obtained with a generator versus the initial (or with the weighted resampling that draws the same samples).

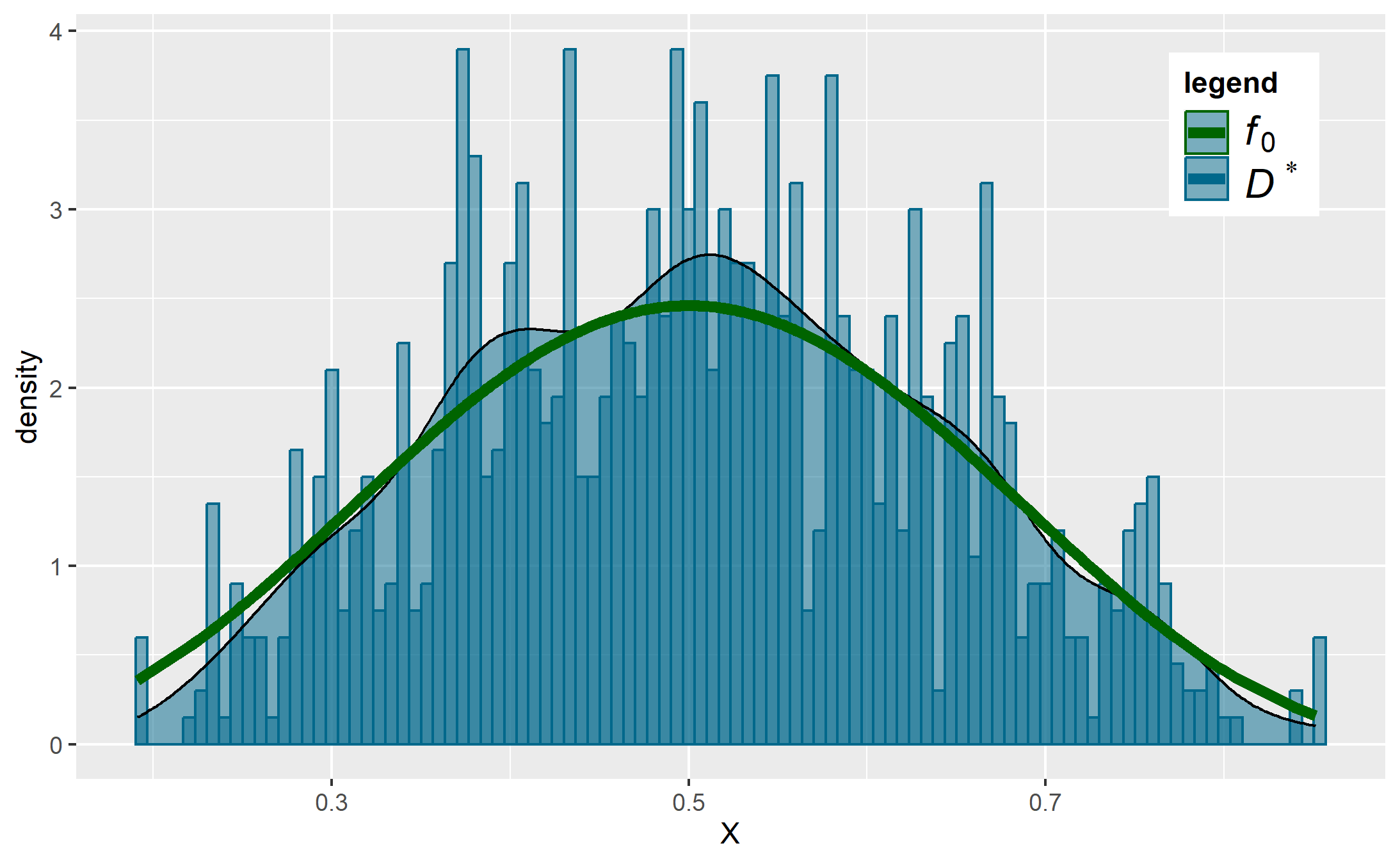

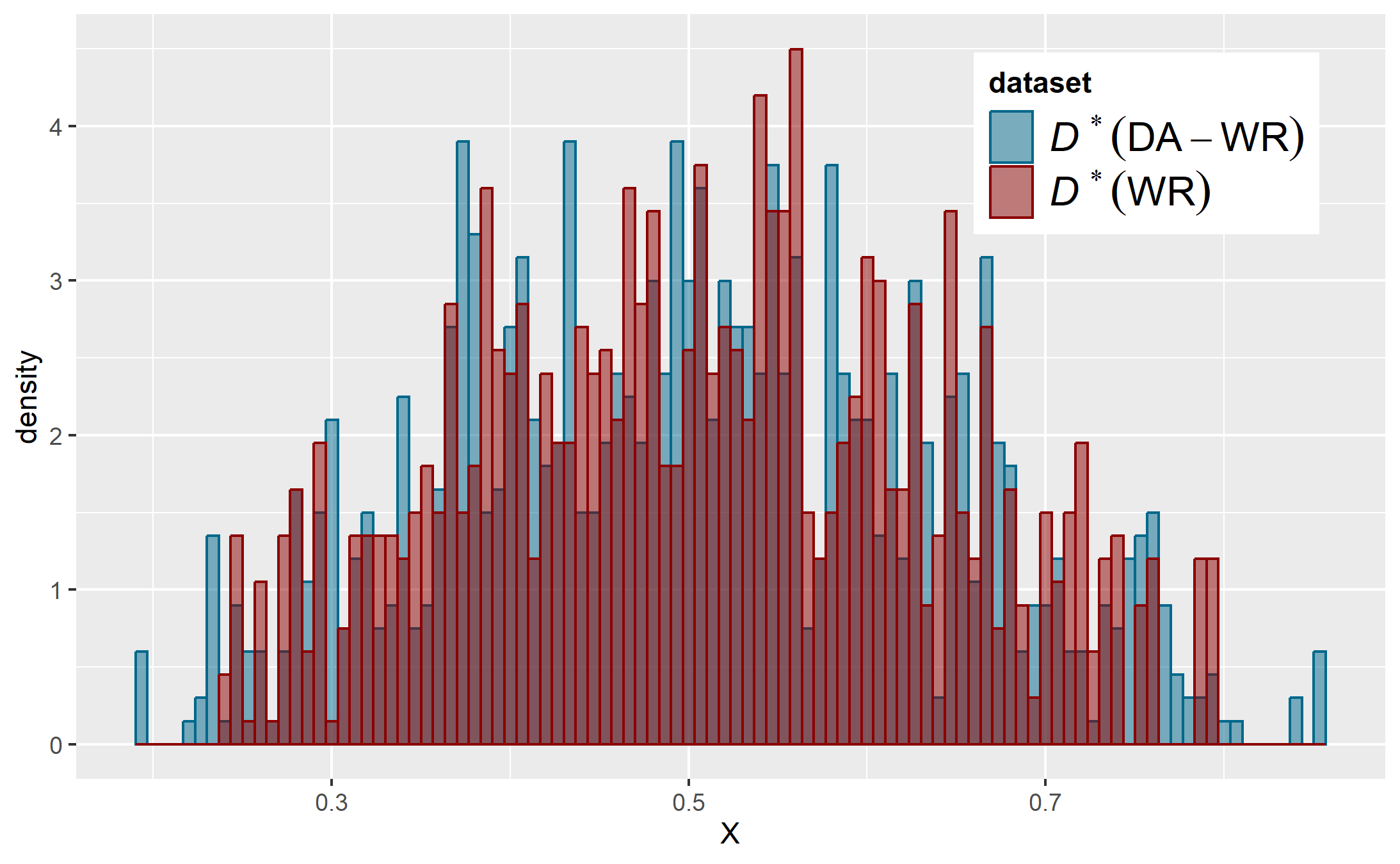

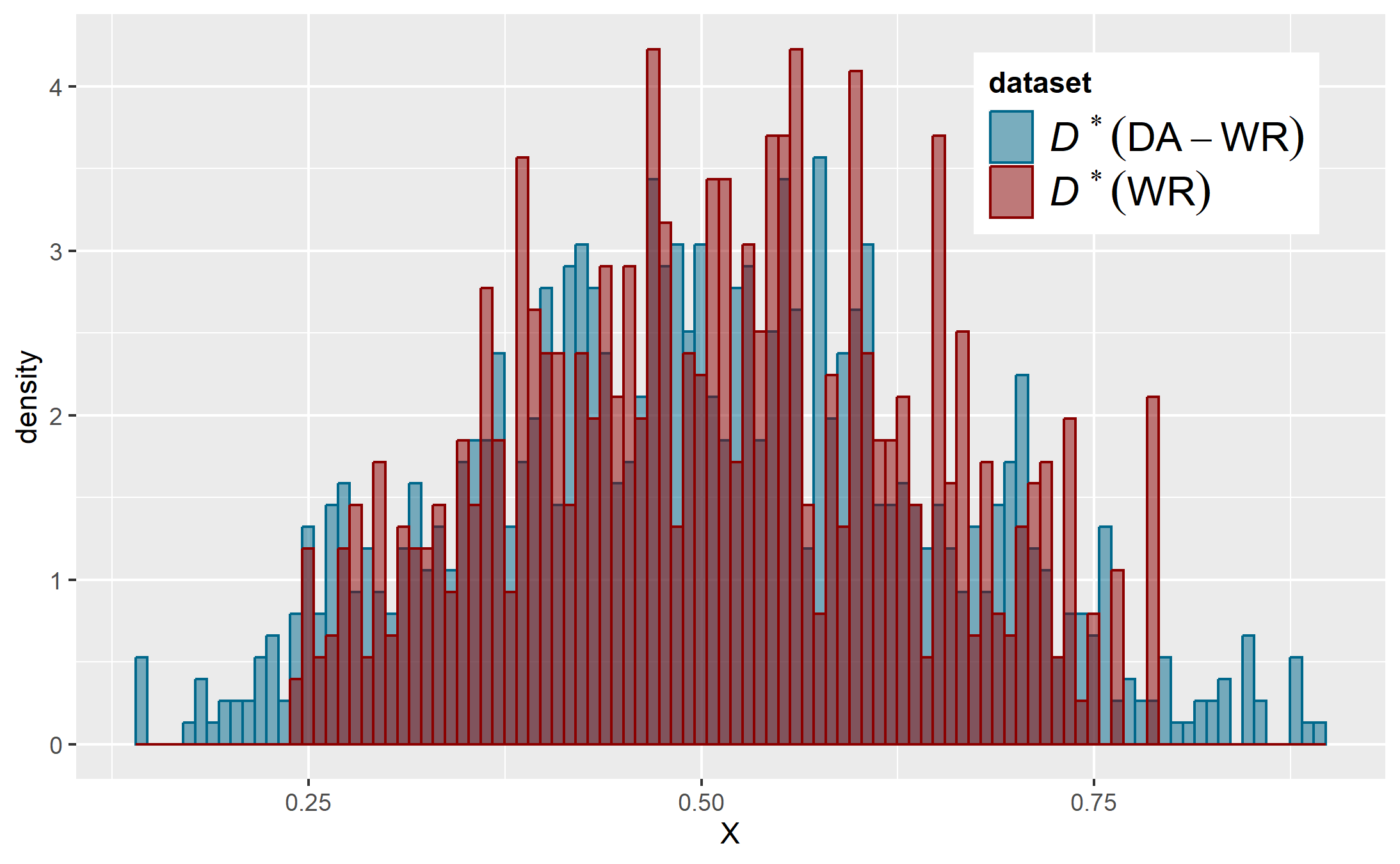

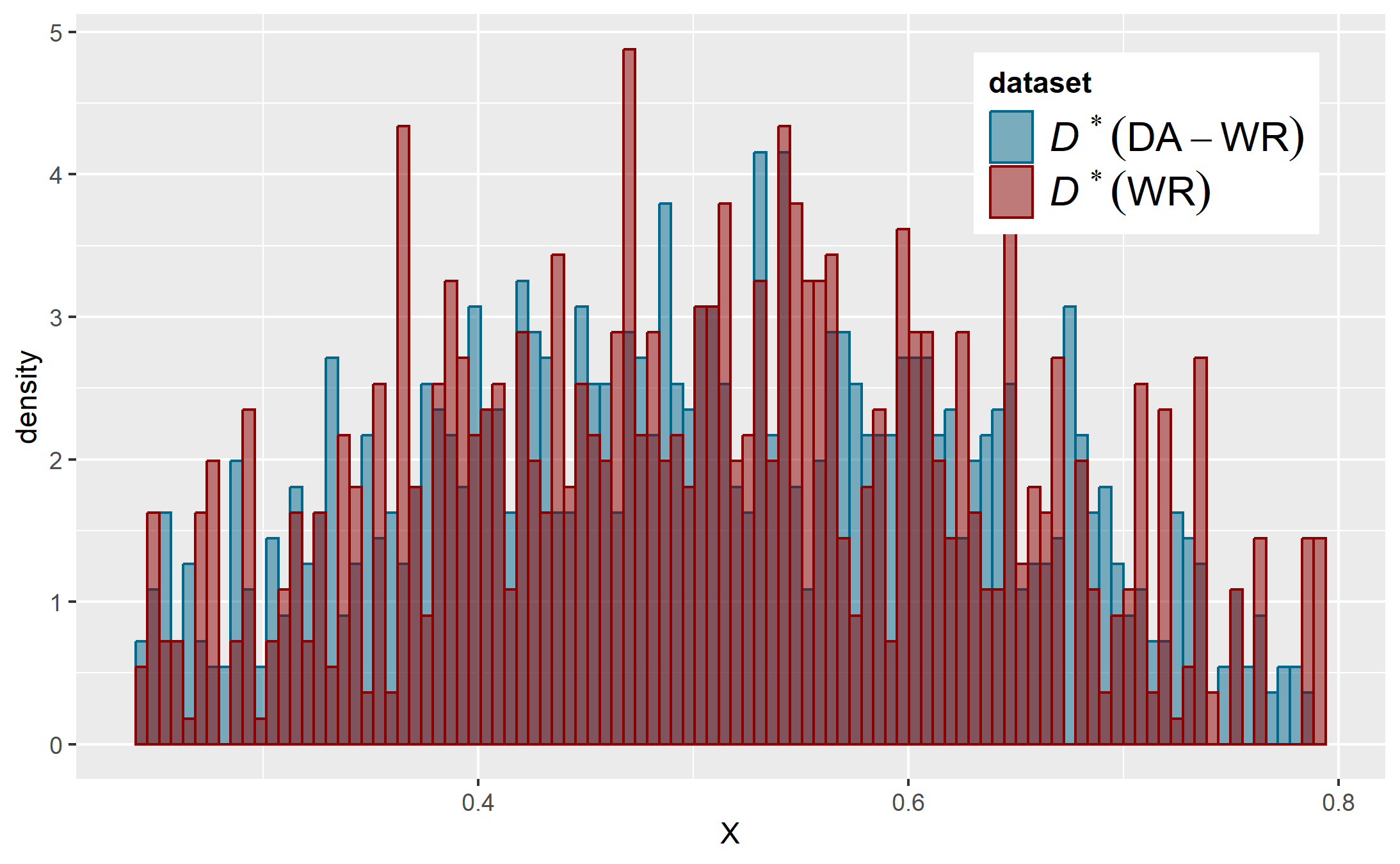

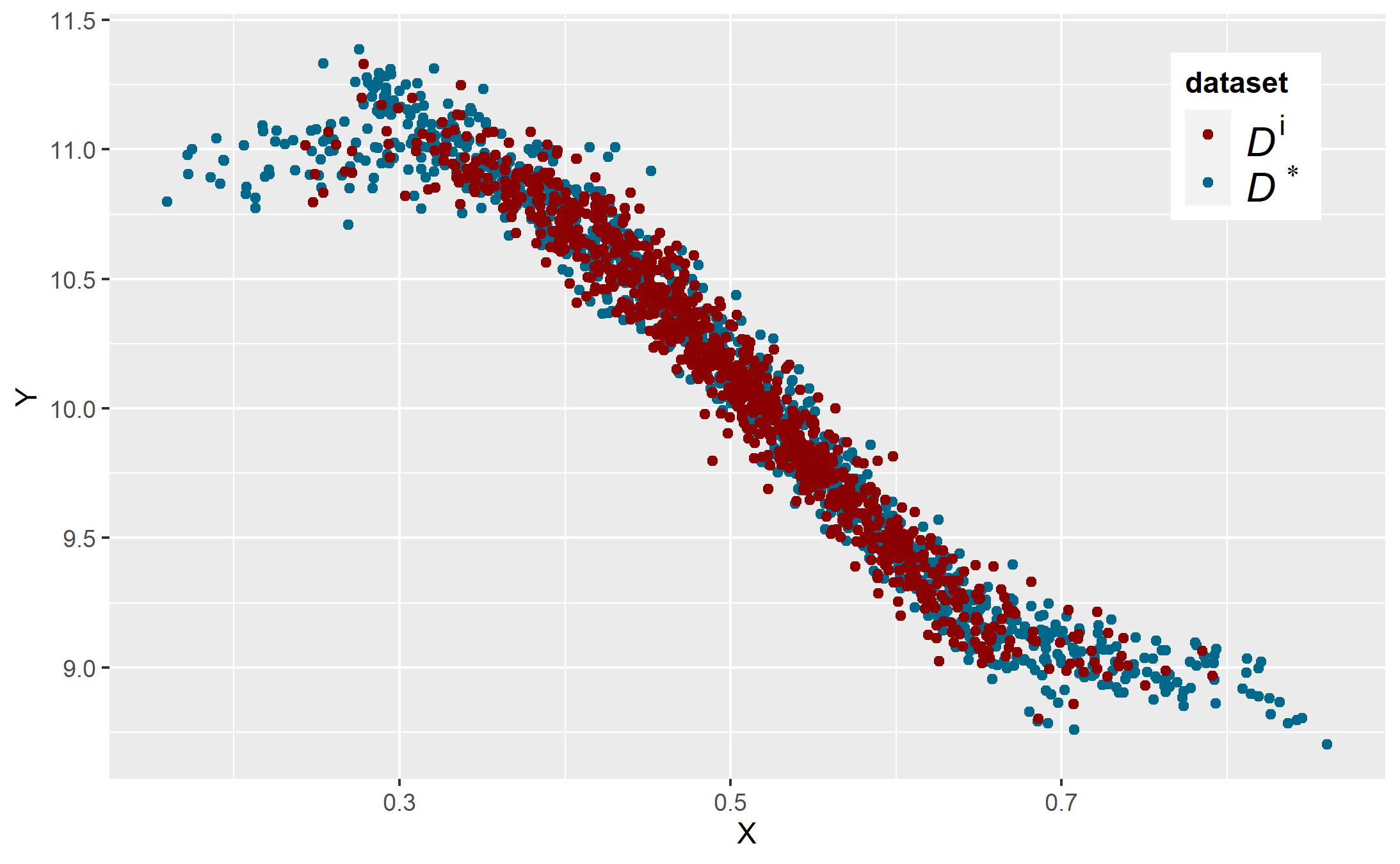

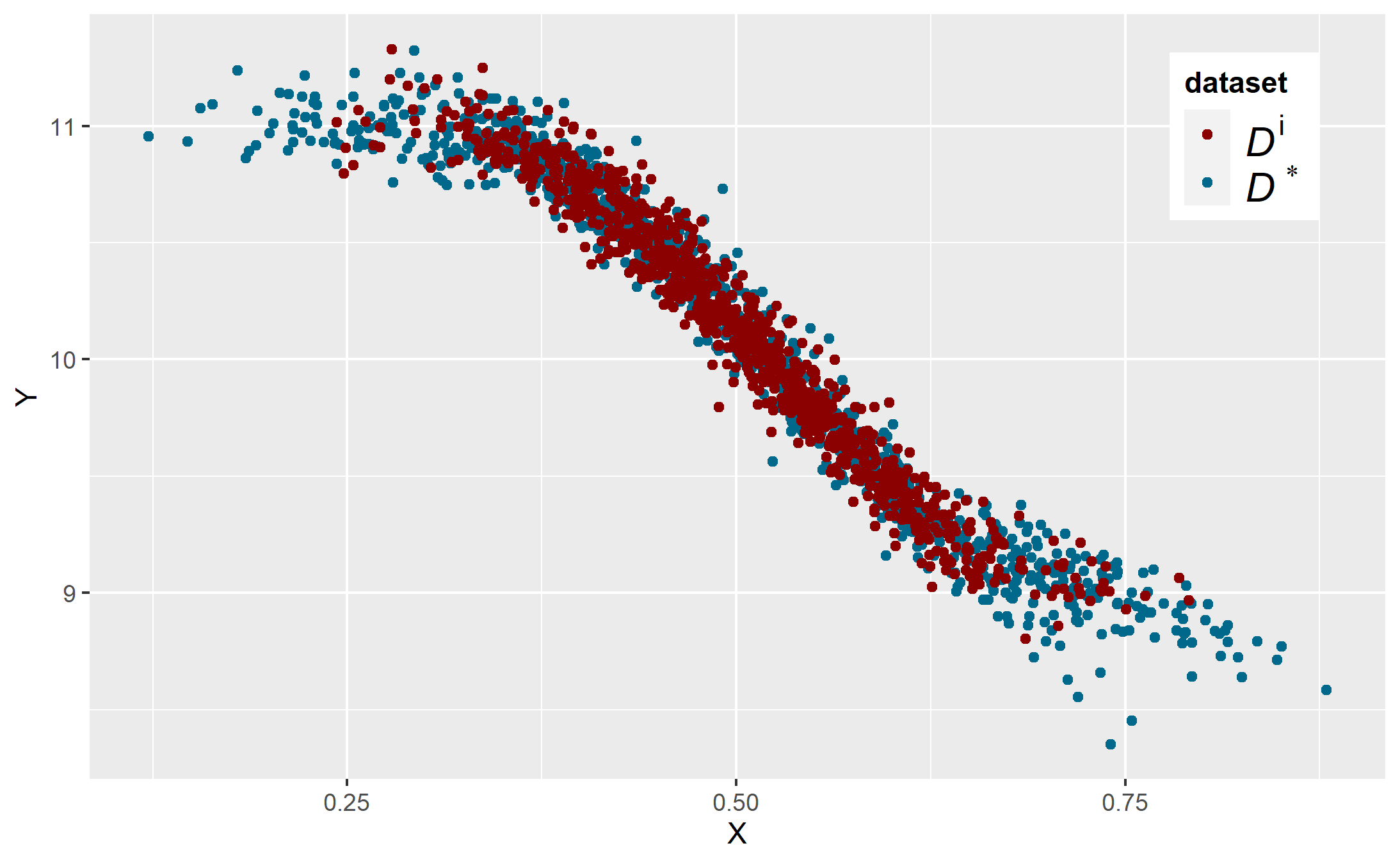

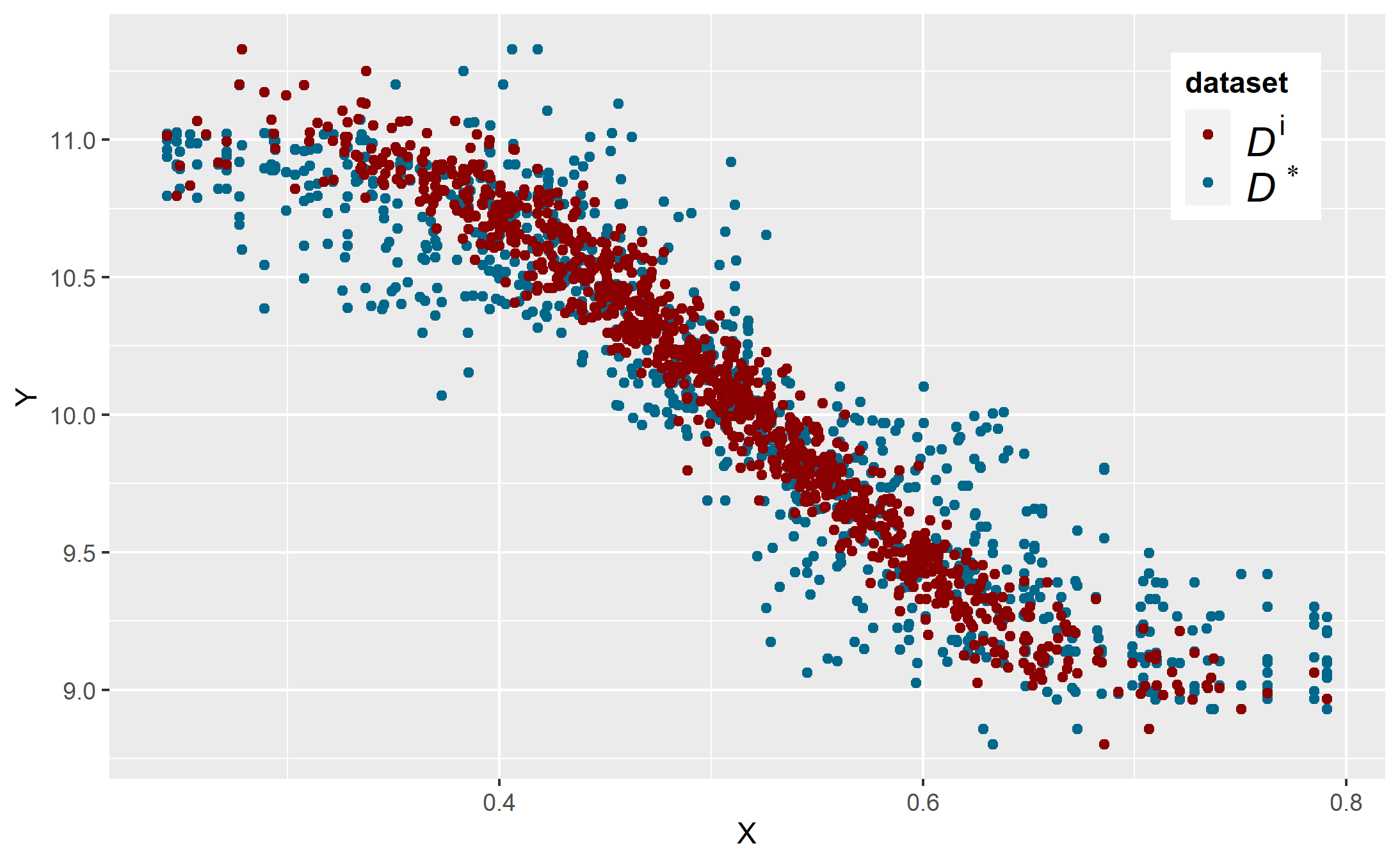

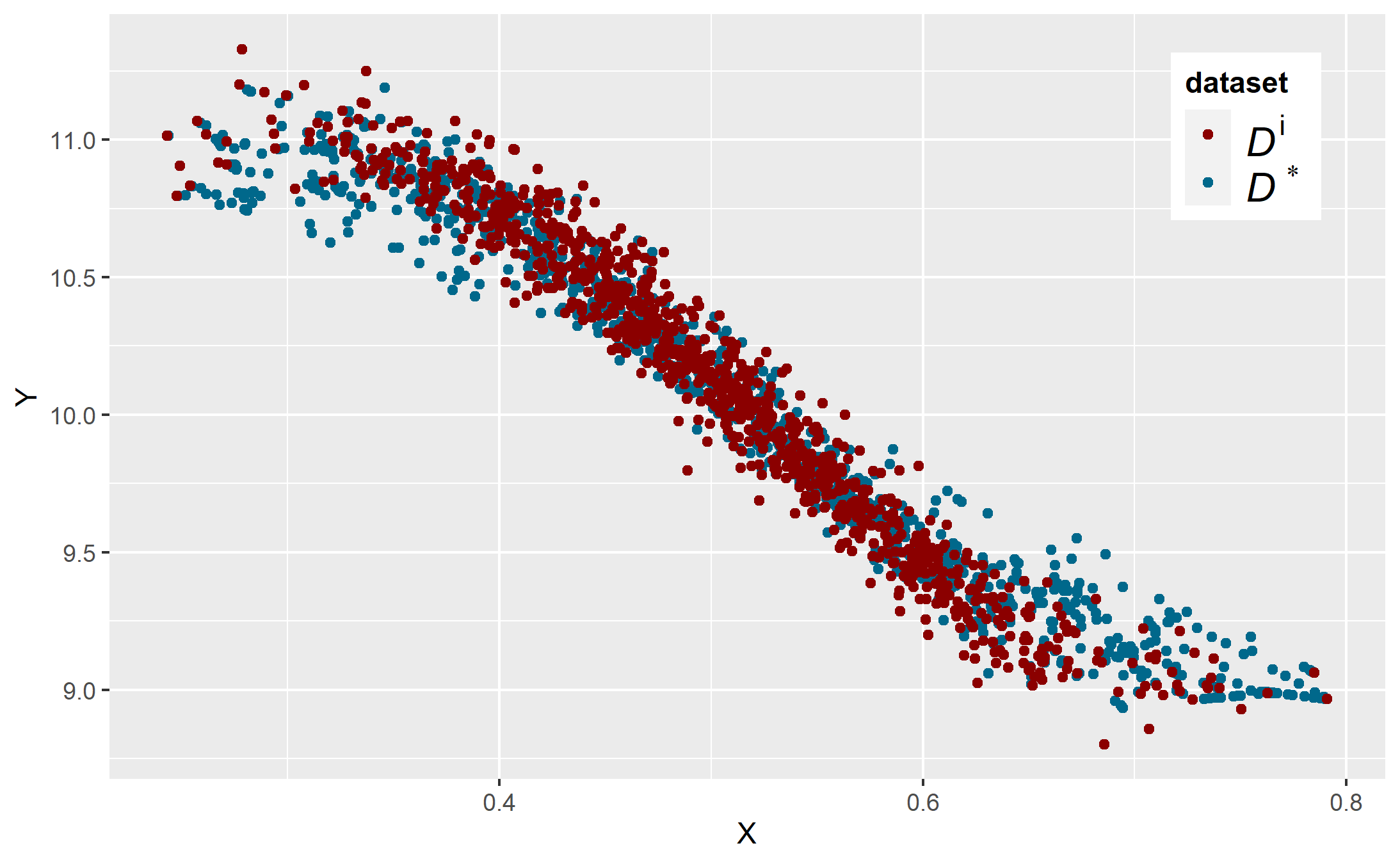

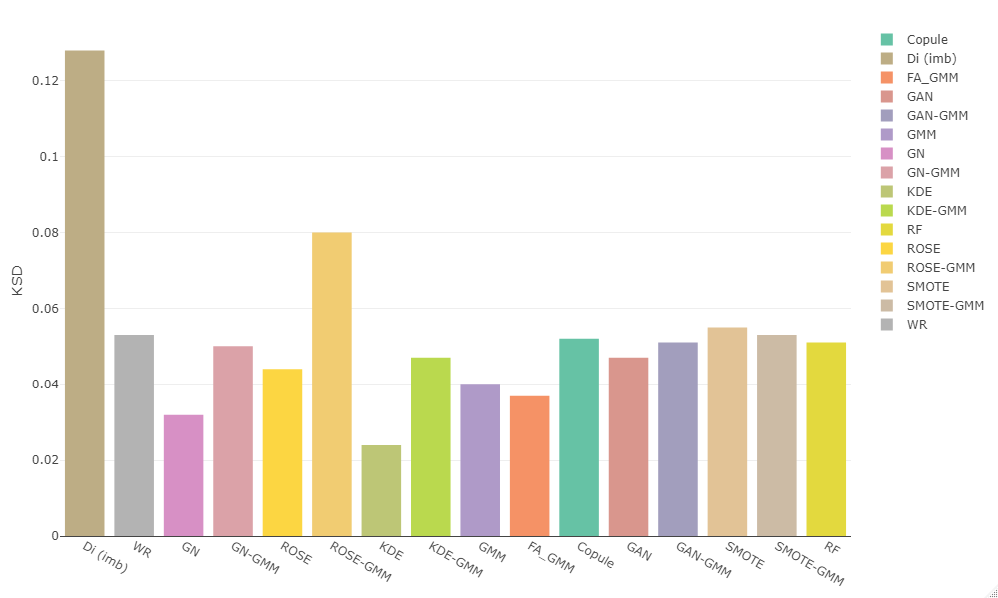

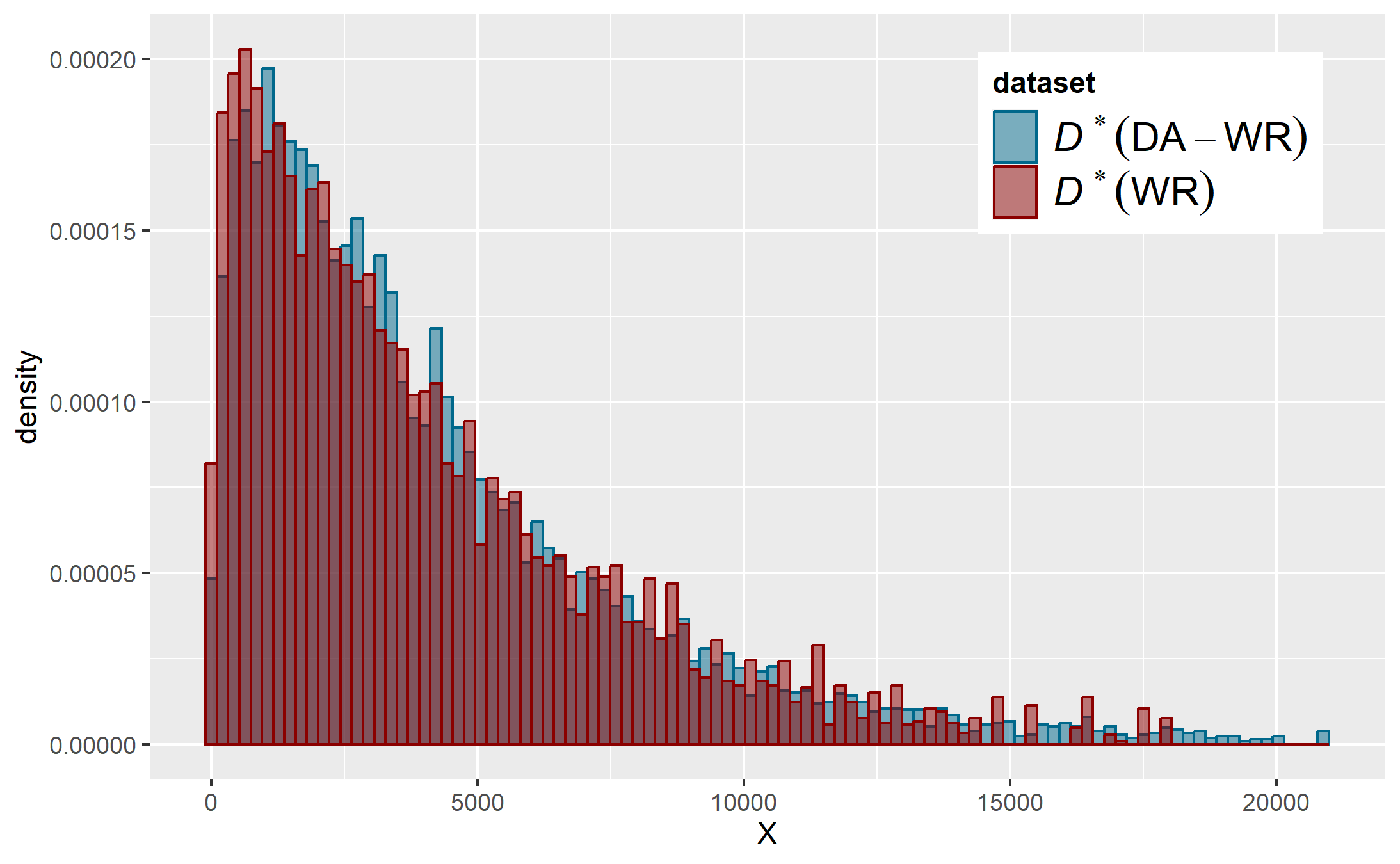

To compare the effect of the different generators, we analyze the histogram of from , called ”new” in the figures. The comparison is made according to the target distribution (7 in the Supplement) and also according to the histogram of obtained with the weighted resampling (8 in the Supplement). Figure 13 in the Supplement represents the Kolmogorov-Smirnov distance between the distributions of for the balanced sample and the different samples. It confirms that the augmented samples are closer to the balanced sample. At last, we analyze the scatter plot from the sample that we compare to the imbalanced one from (9 in the Supplement). We can see in Figure 7 in the Supplement that all obtained distributions are quite close to the target one. In Figure 8 in the Supplement, we see that the DA-WR algorithm does not necessarily improve the WR one: with the random forest it provides the same values of ; with copulas, Smote, or Smote-GMM, it generates values within the observed range. This is a drawback in our illustration since we need to get more values on the sides.

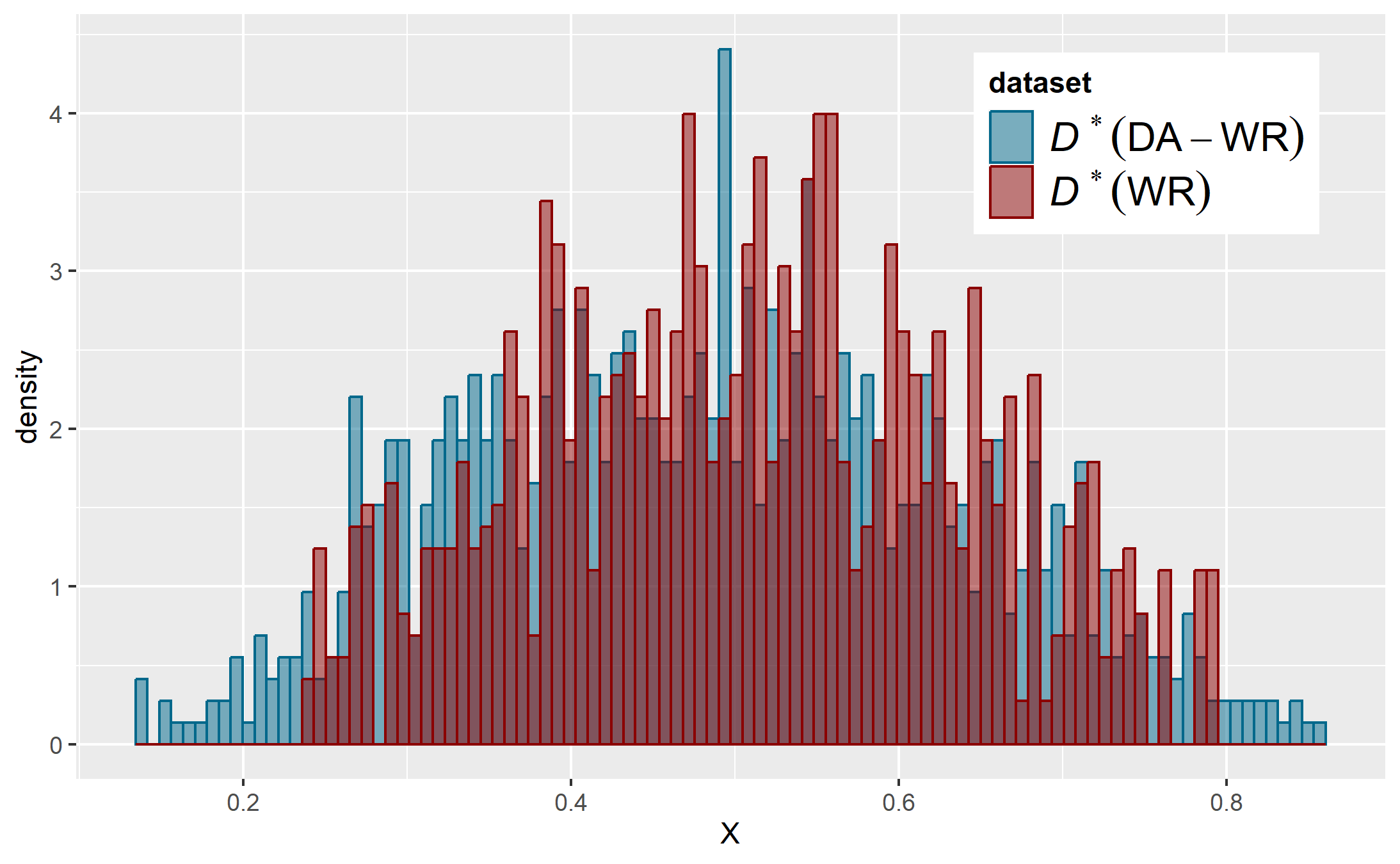

About generation, we observe in Figure 9 in the Supplement that the generations obtained with the clustering are closer to the initial values. As previously, the copula, Smote, Smote-GMM approaches generate within the observed range. Random forests generate the same values for while the GAN and ROSE generation are disappointing: the values are too extended and scattered.

3.3 Predictive performance analysis

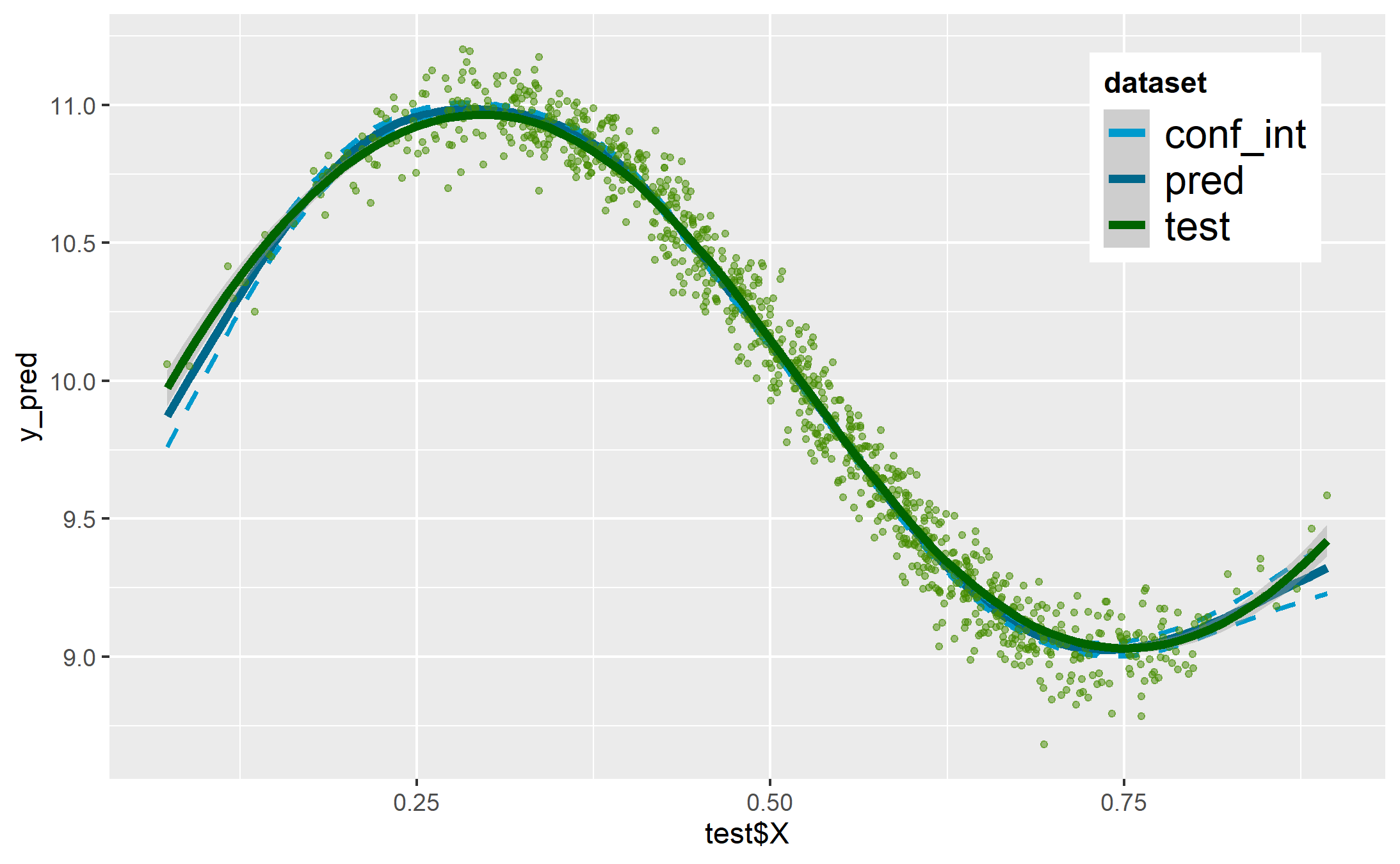

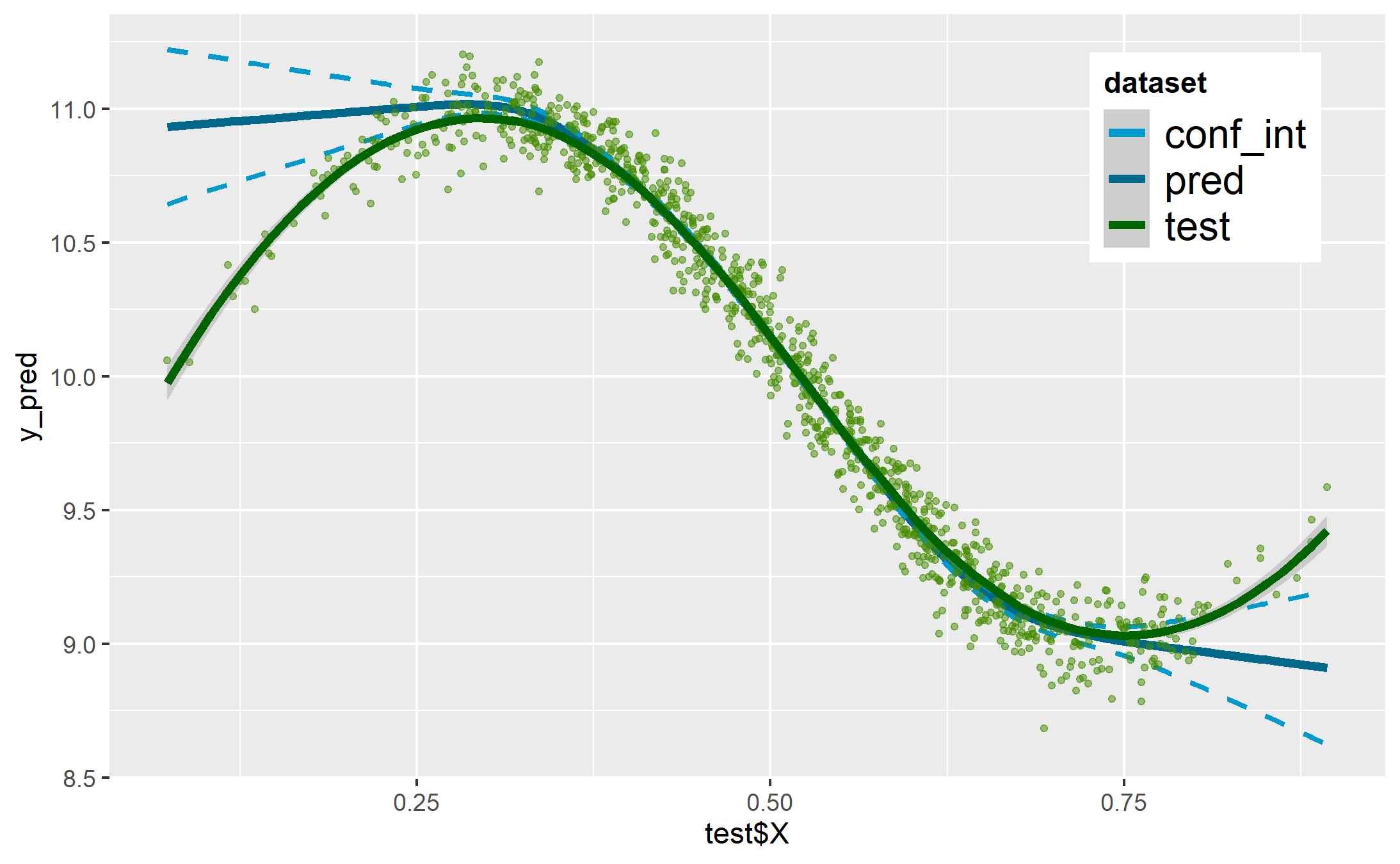

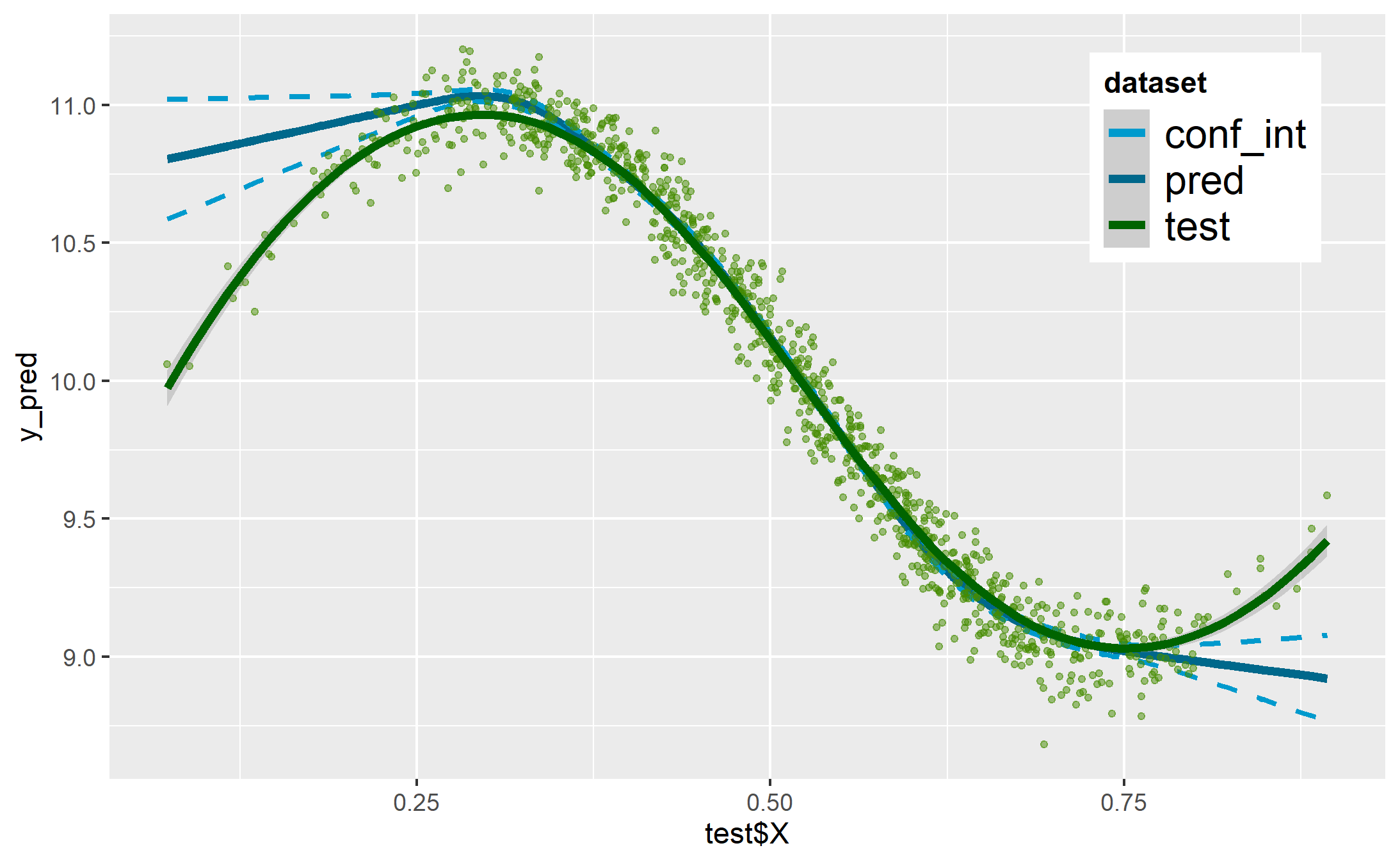

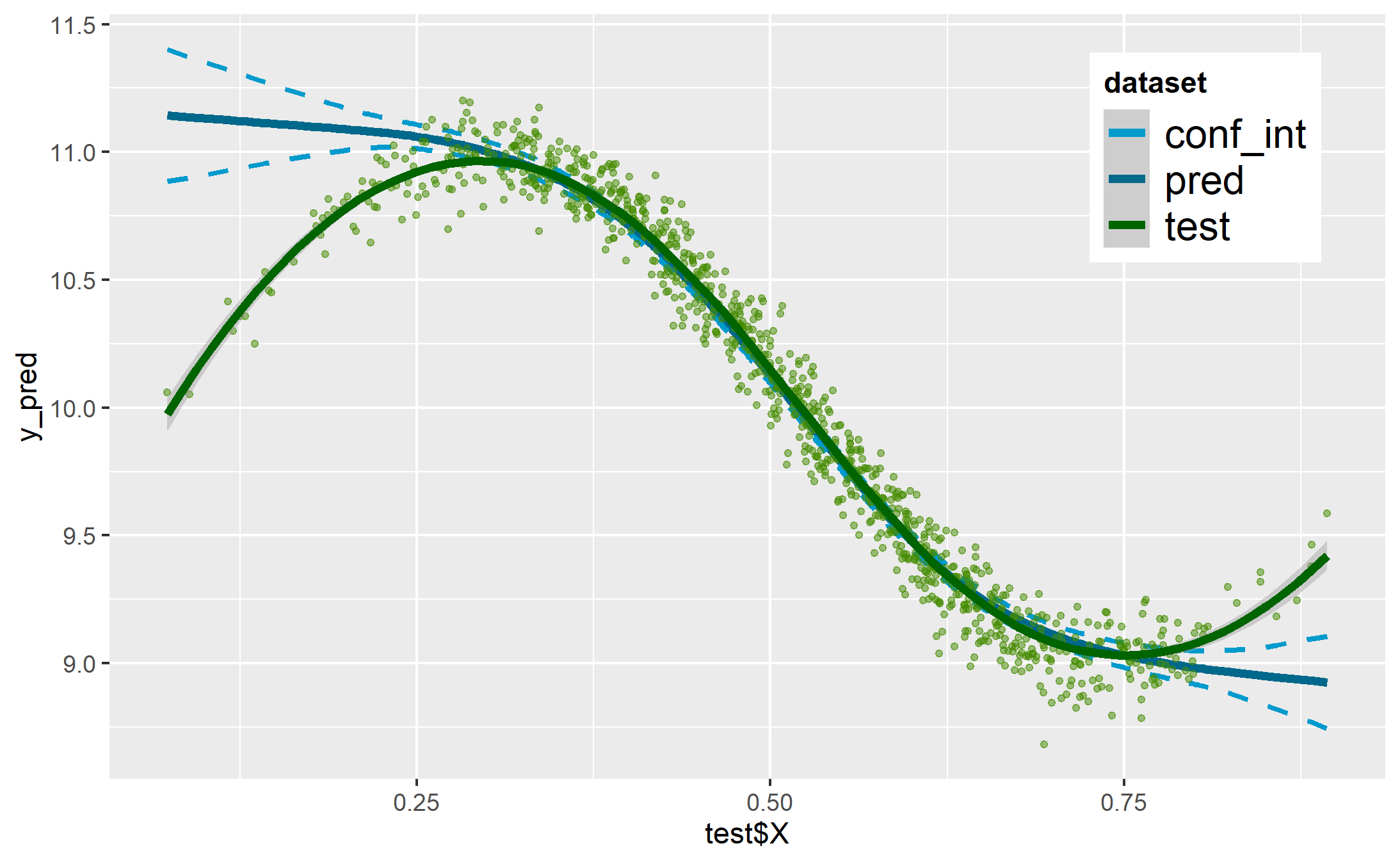

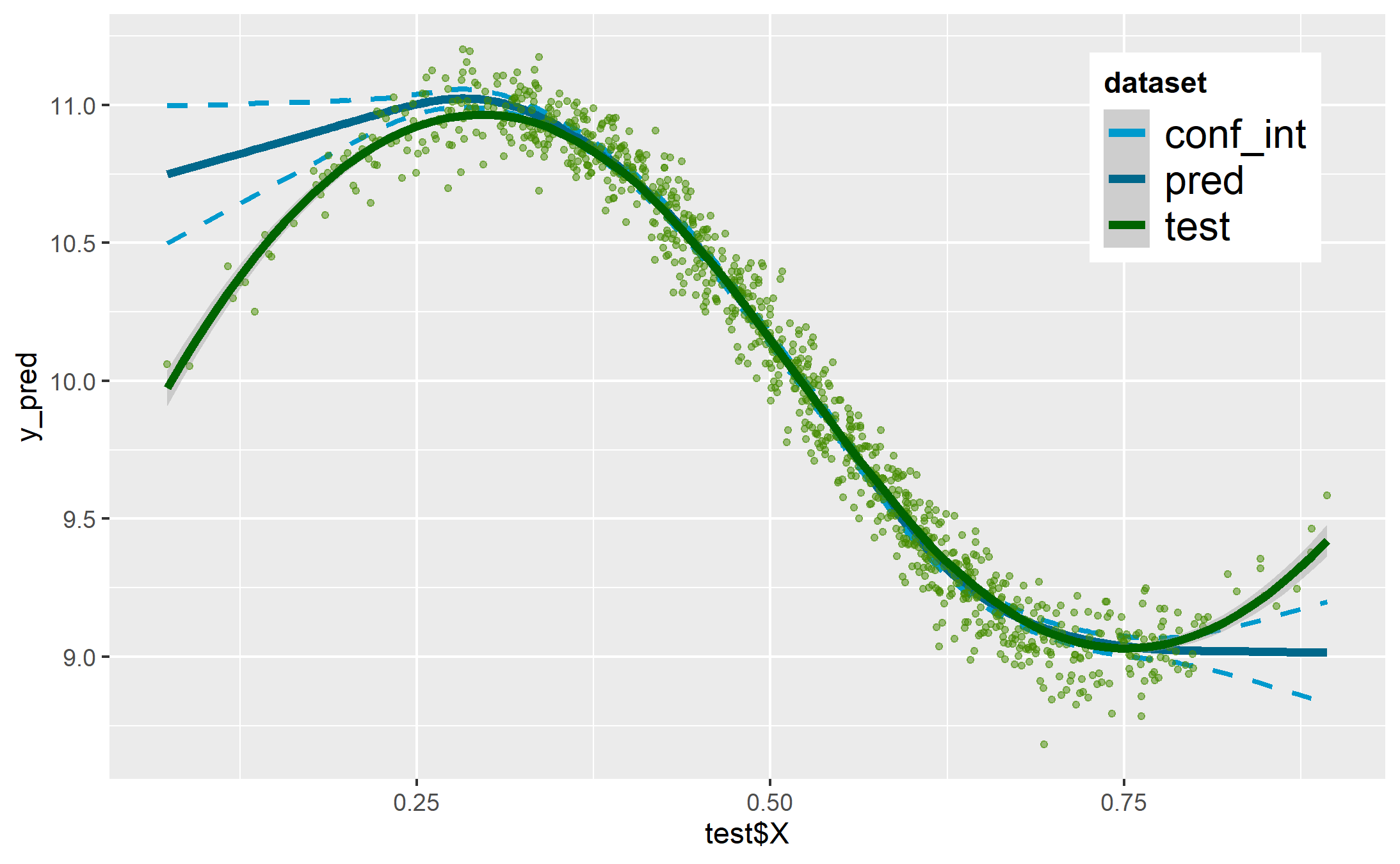

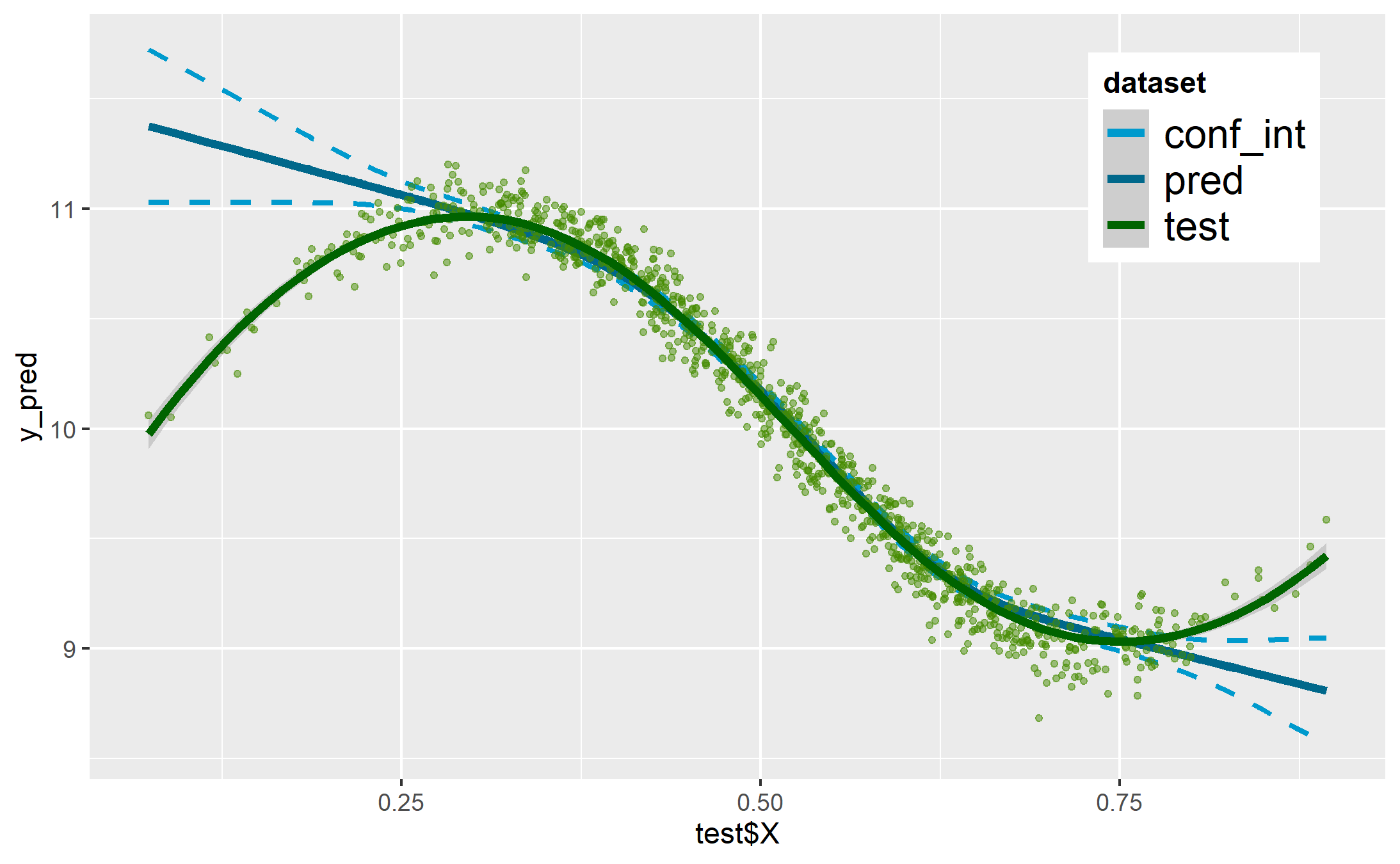

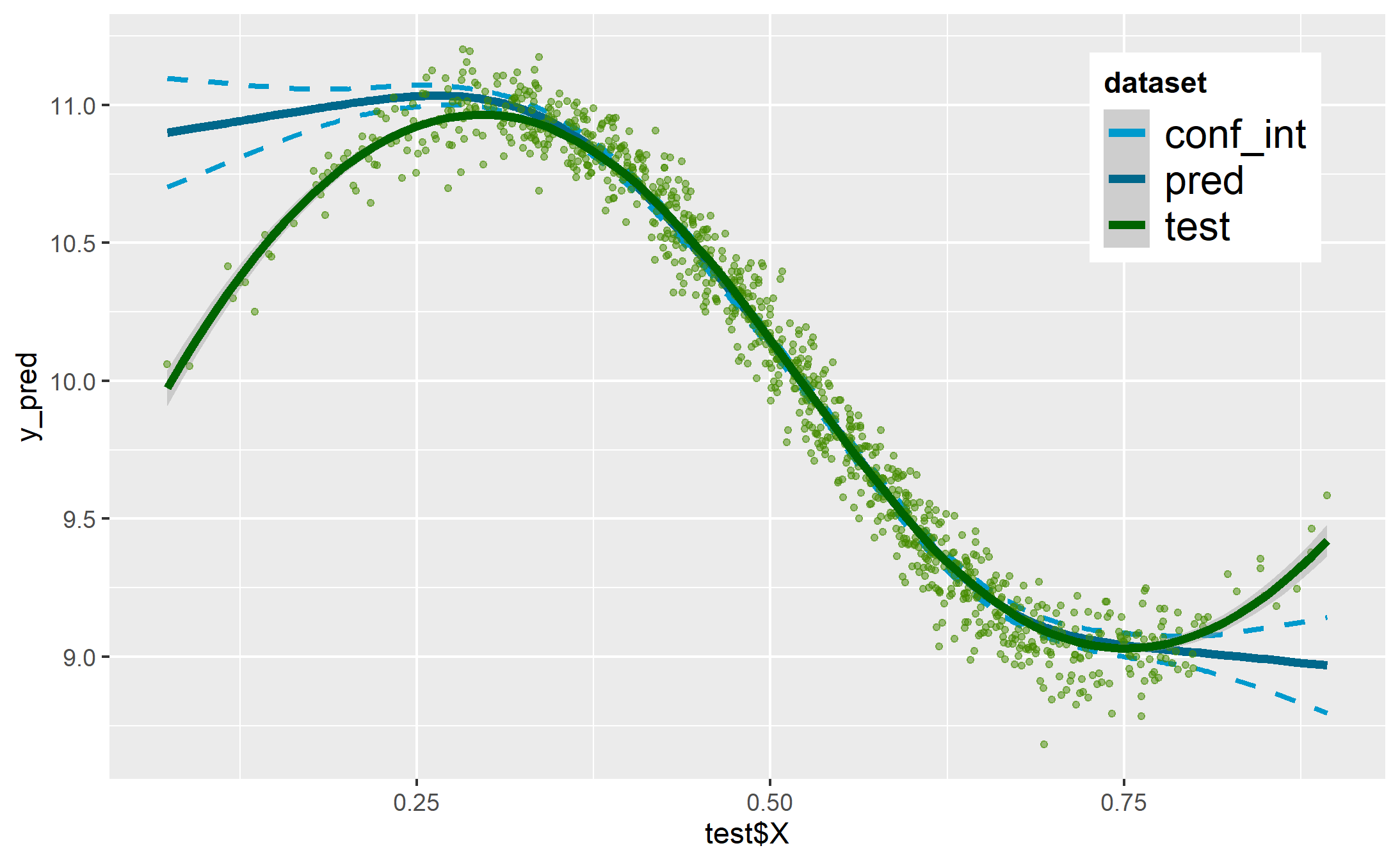

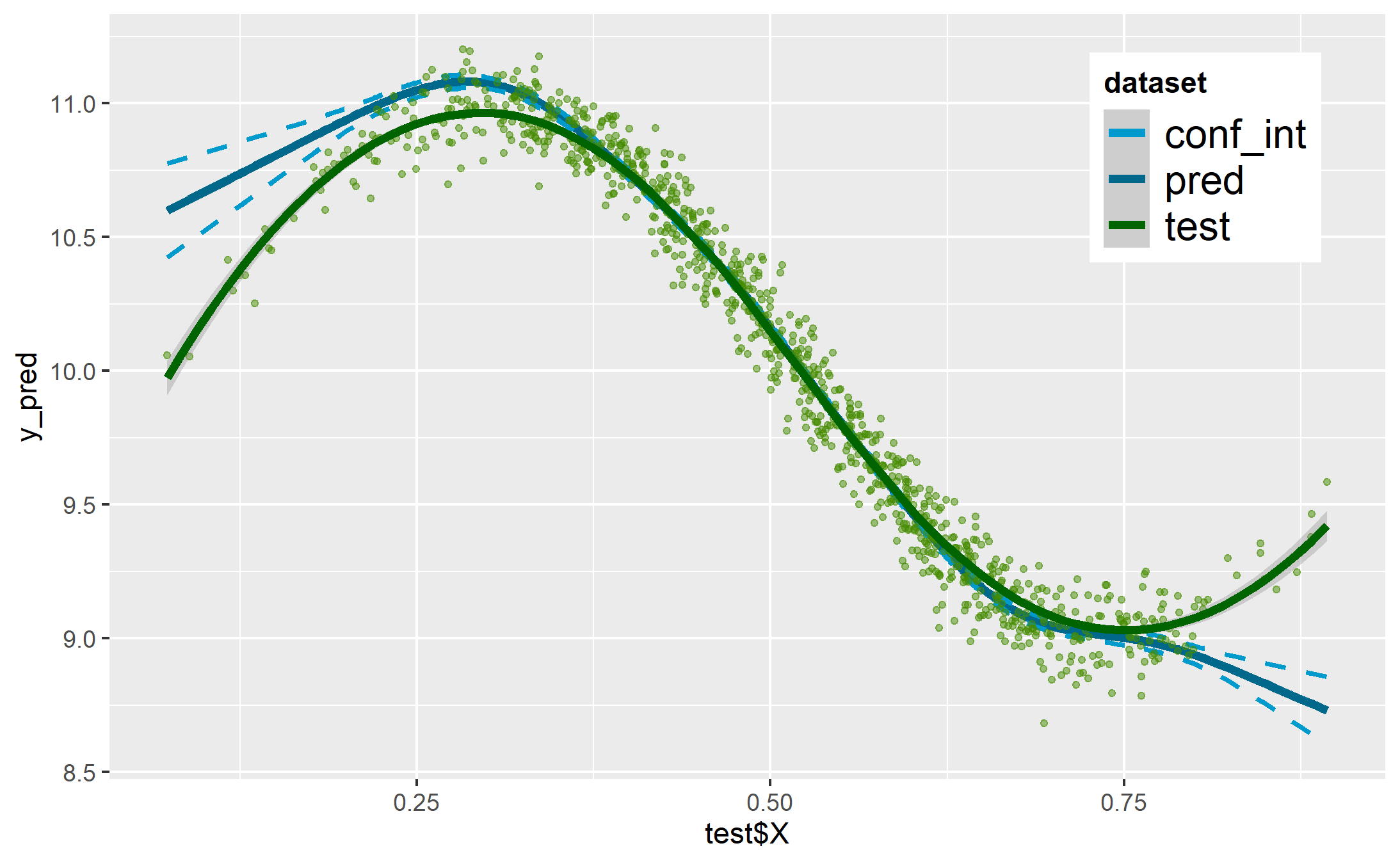

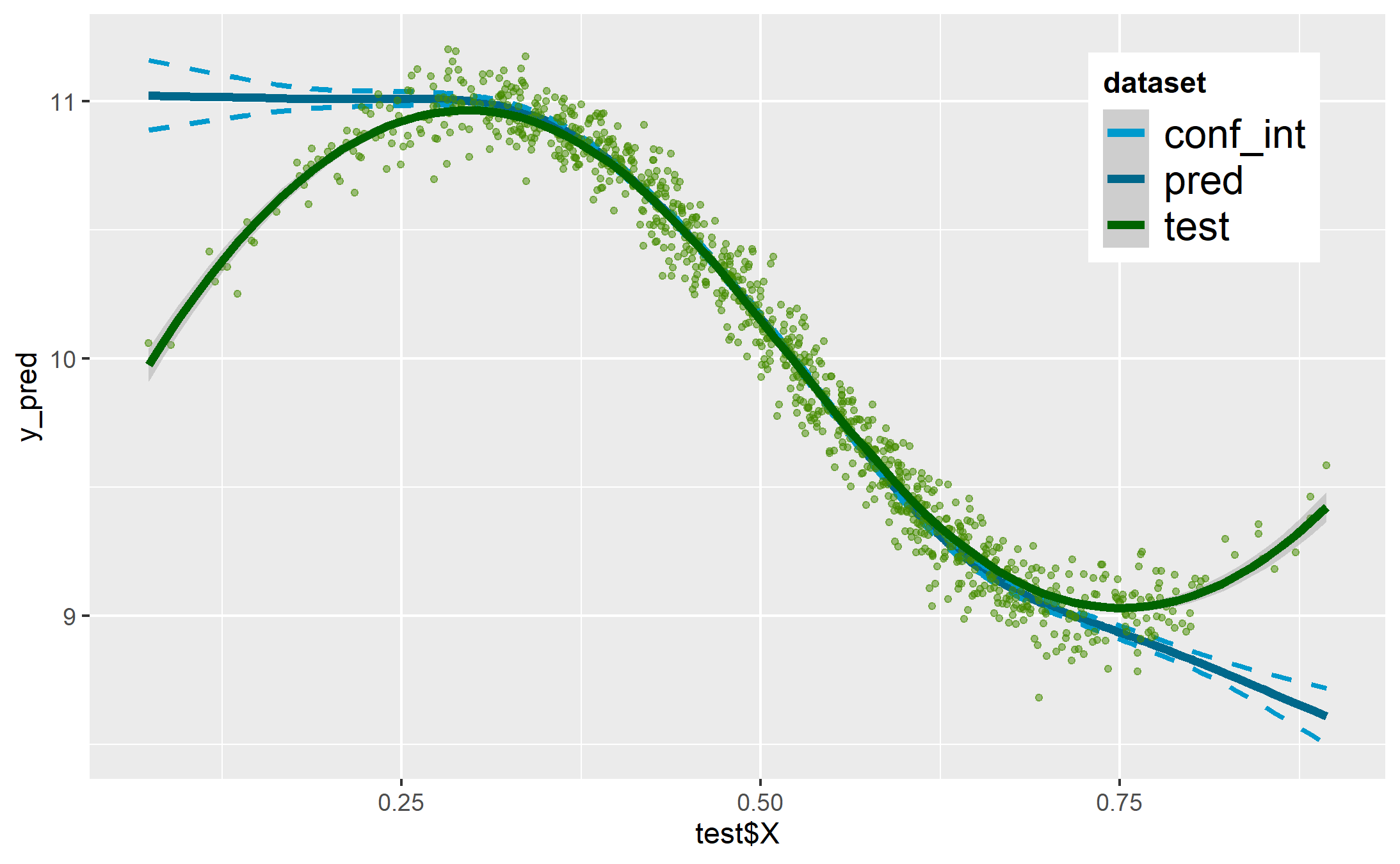

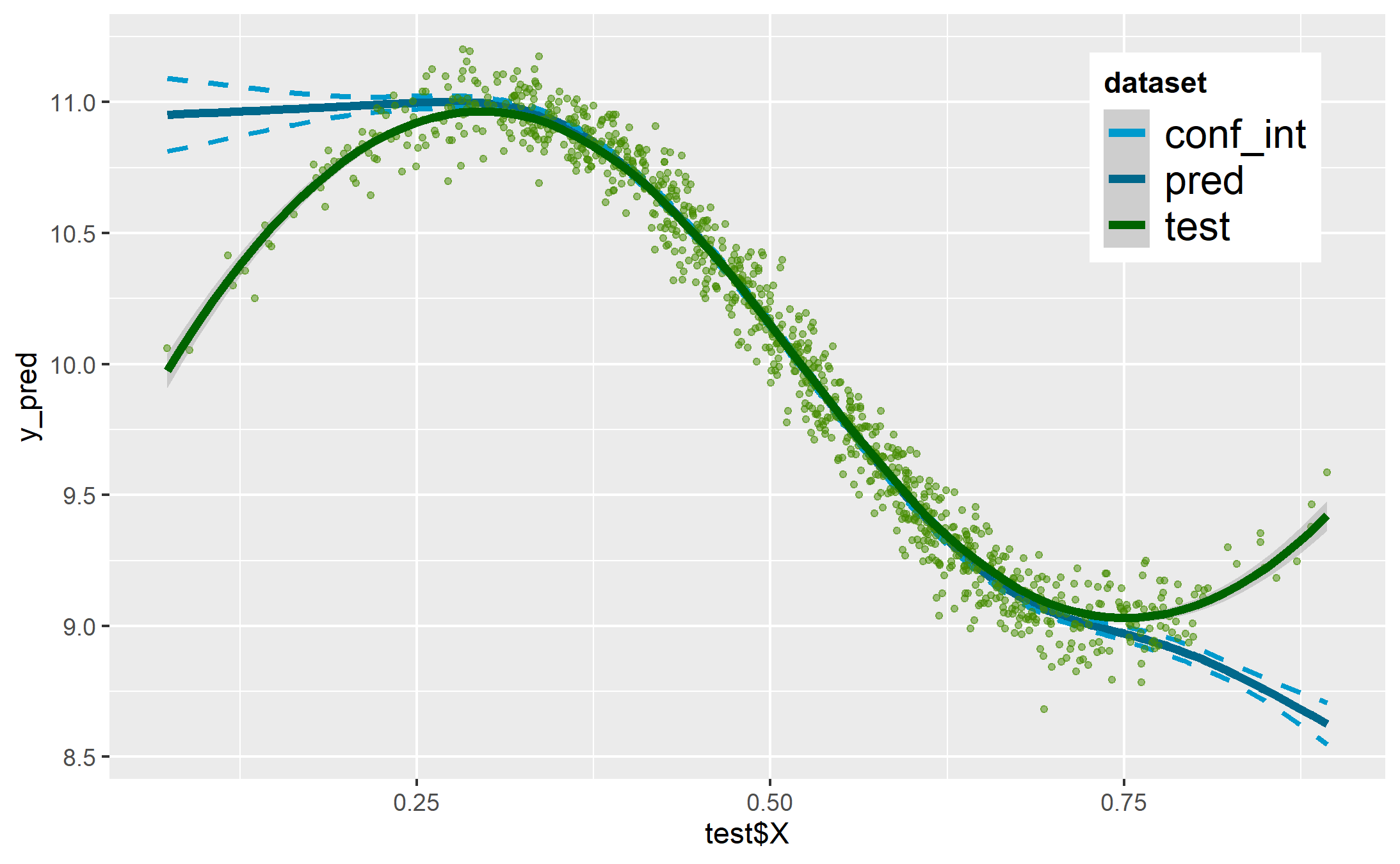

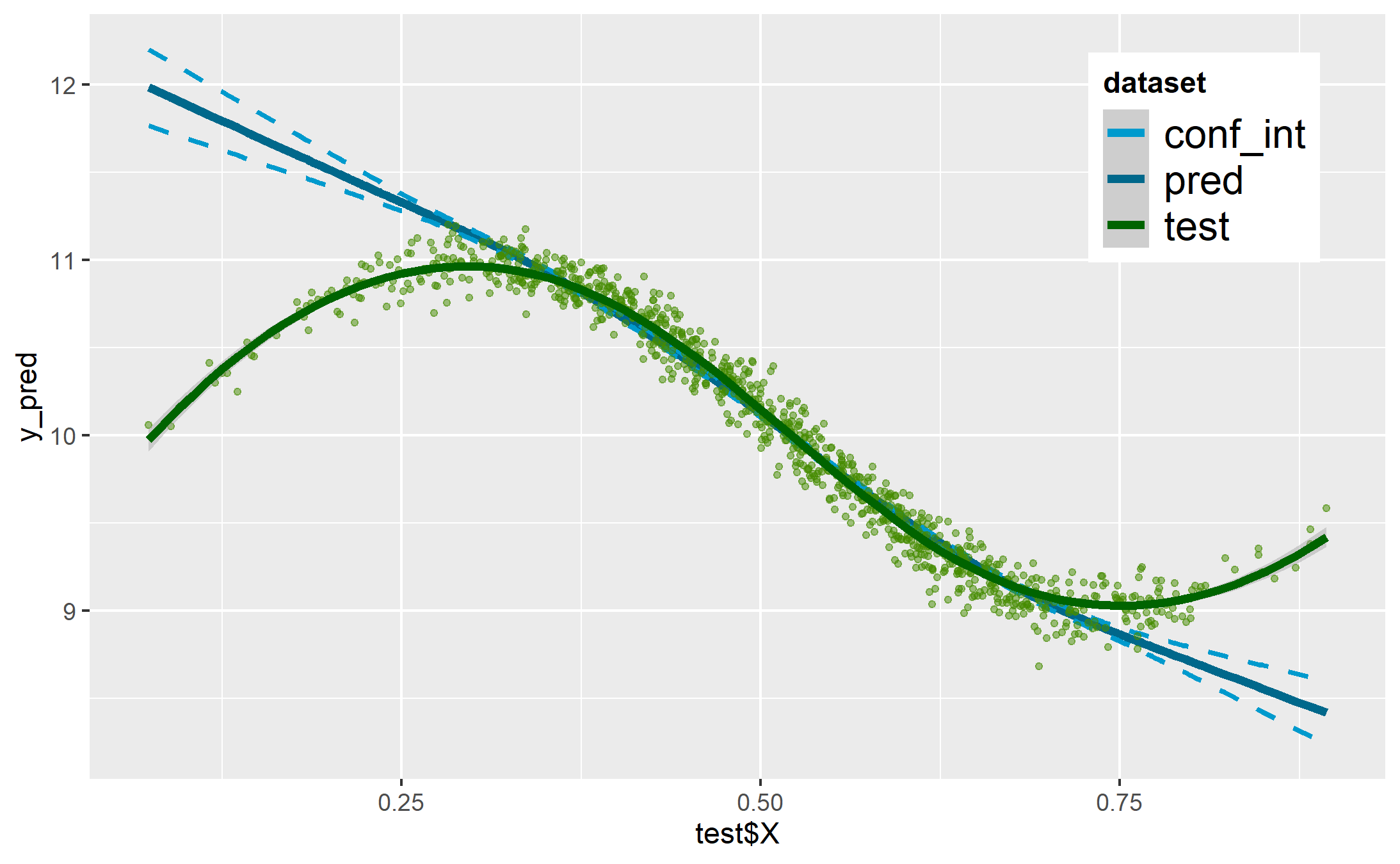

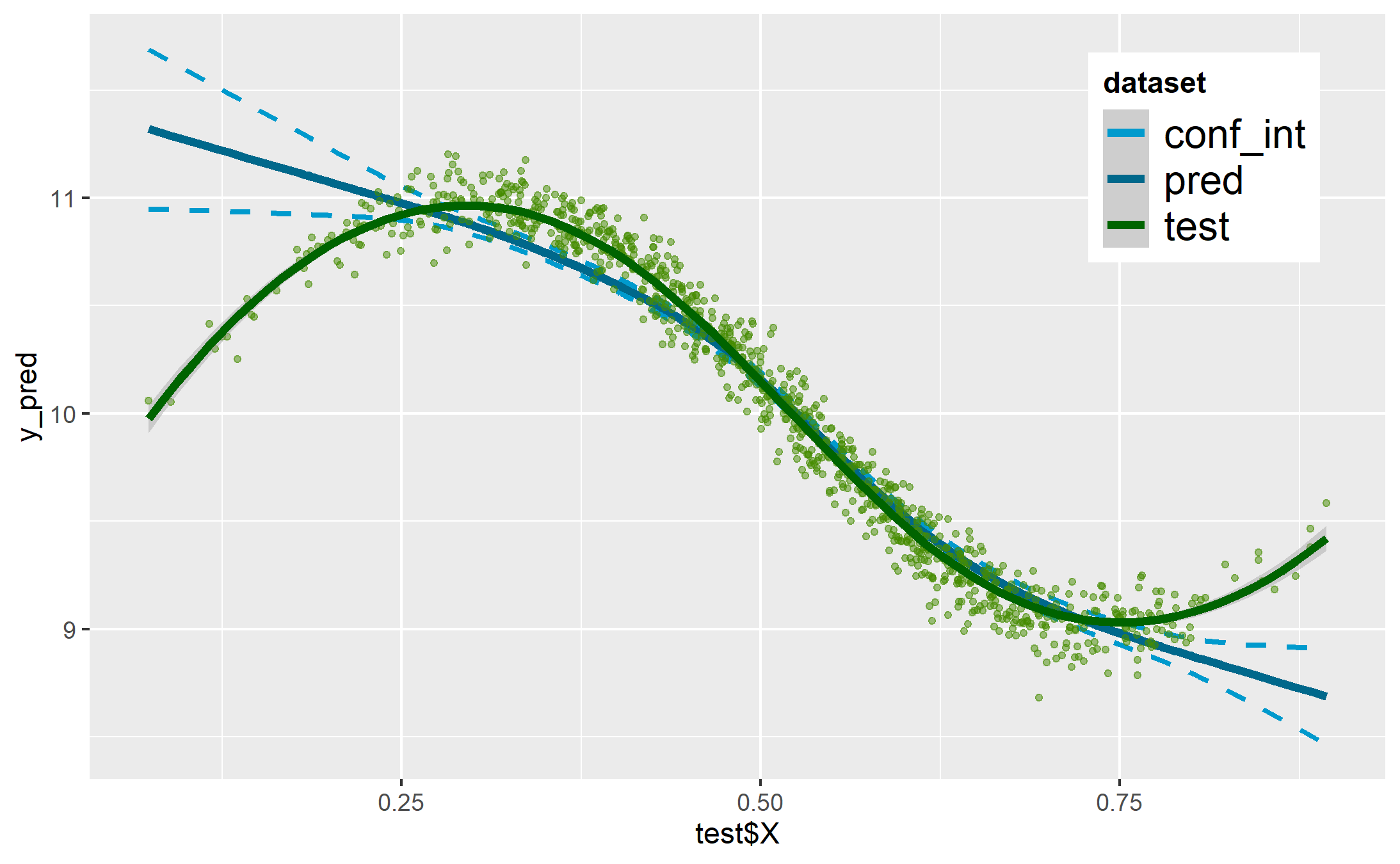

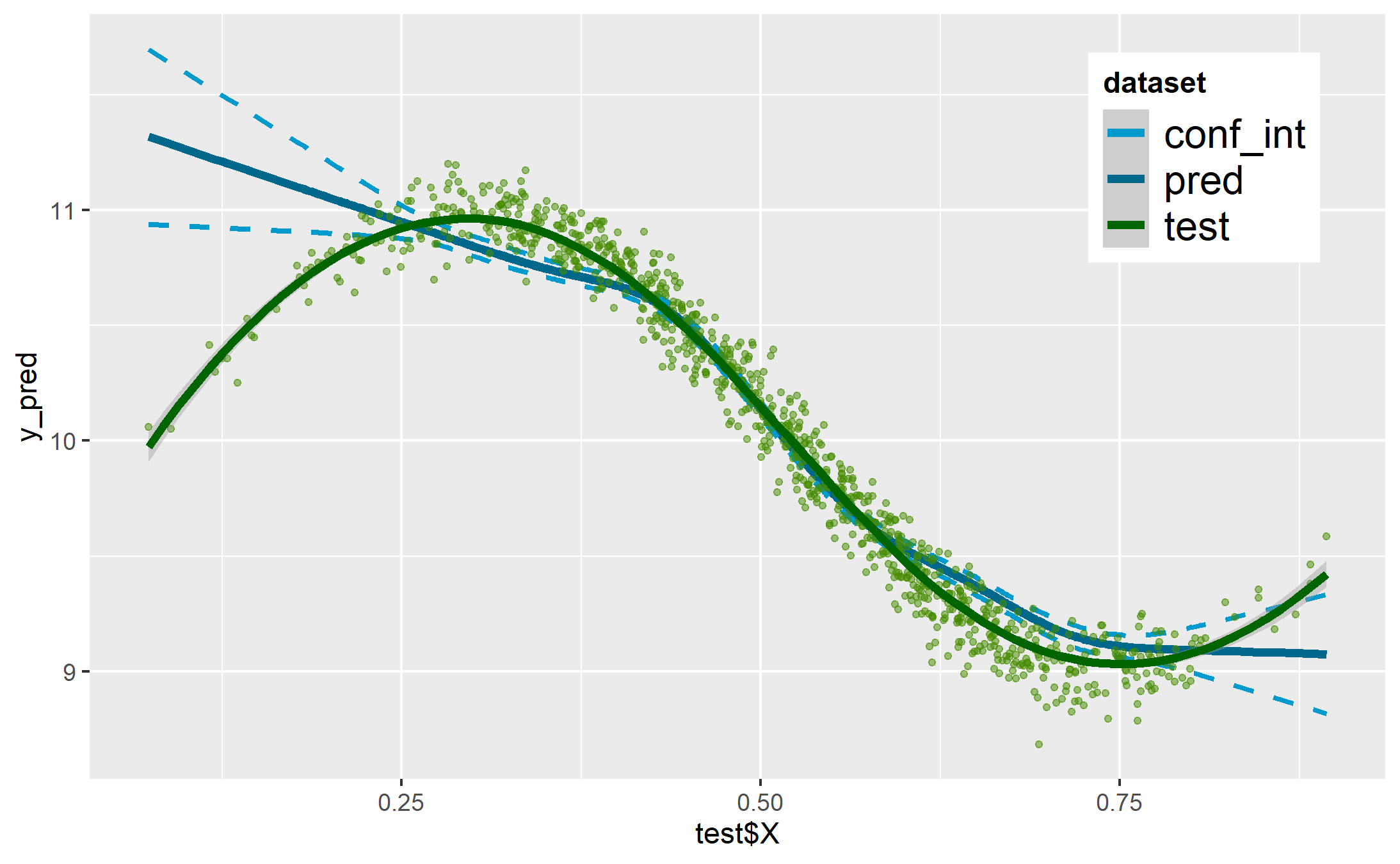

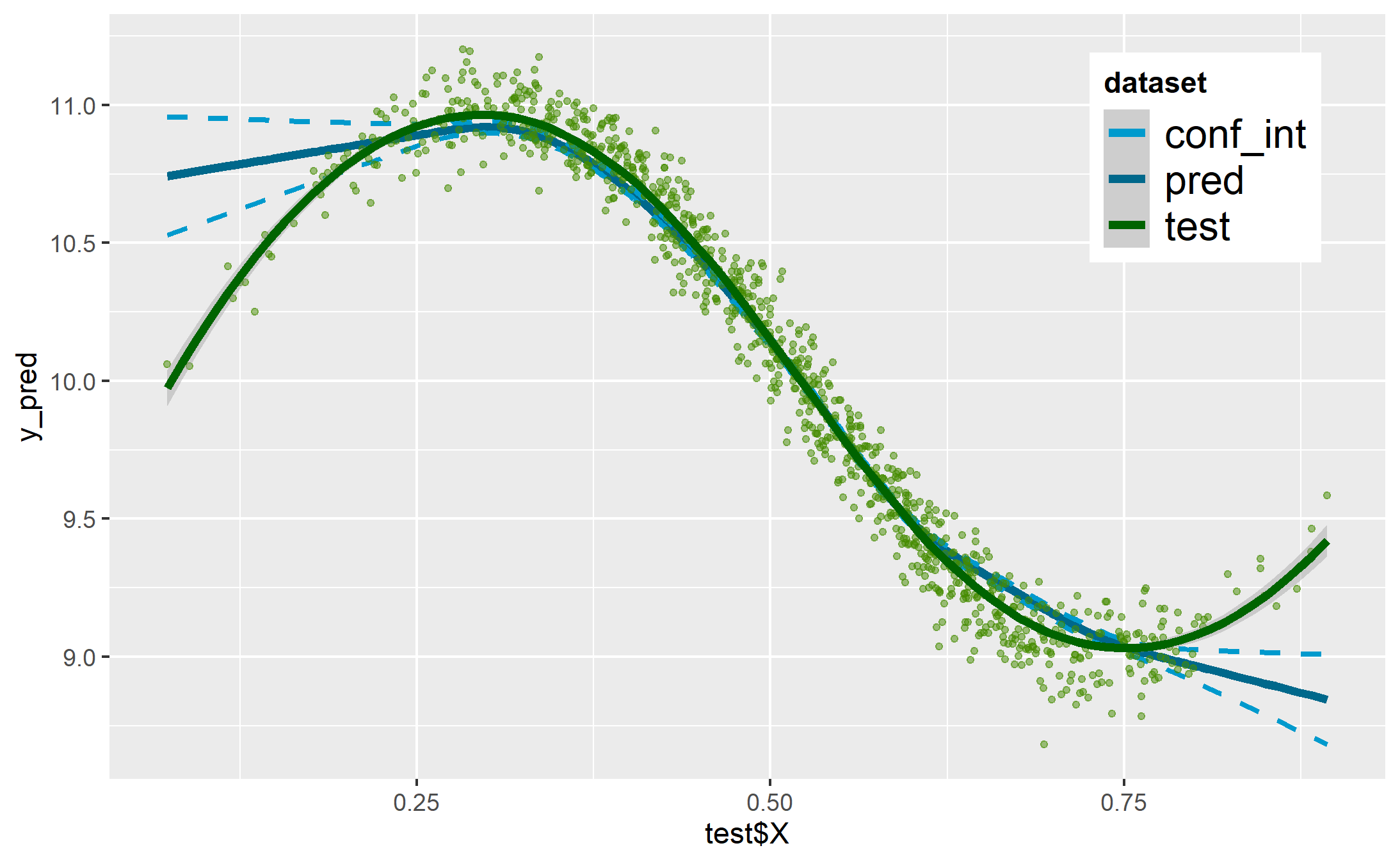

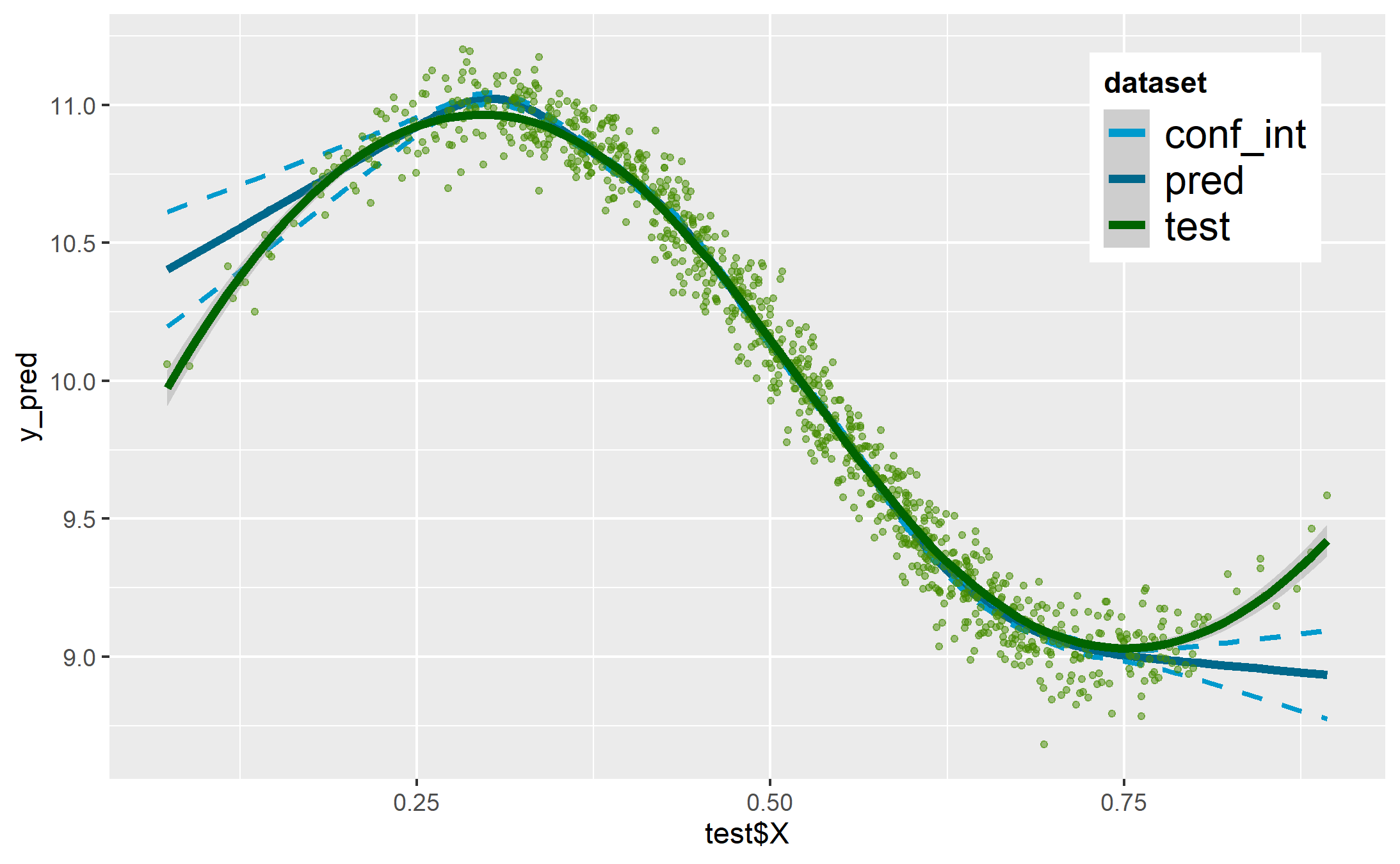

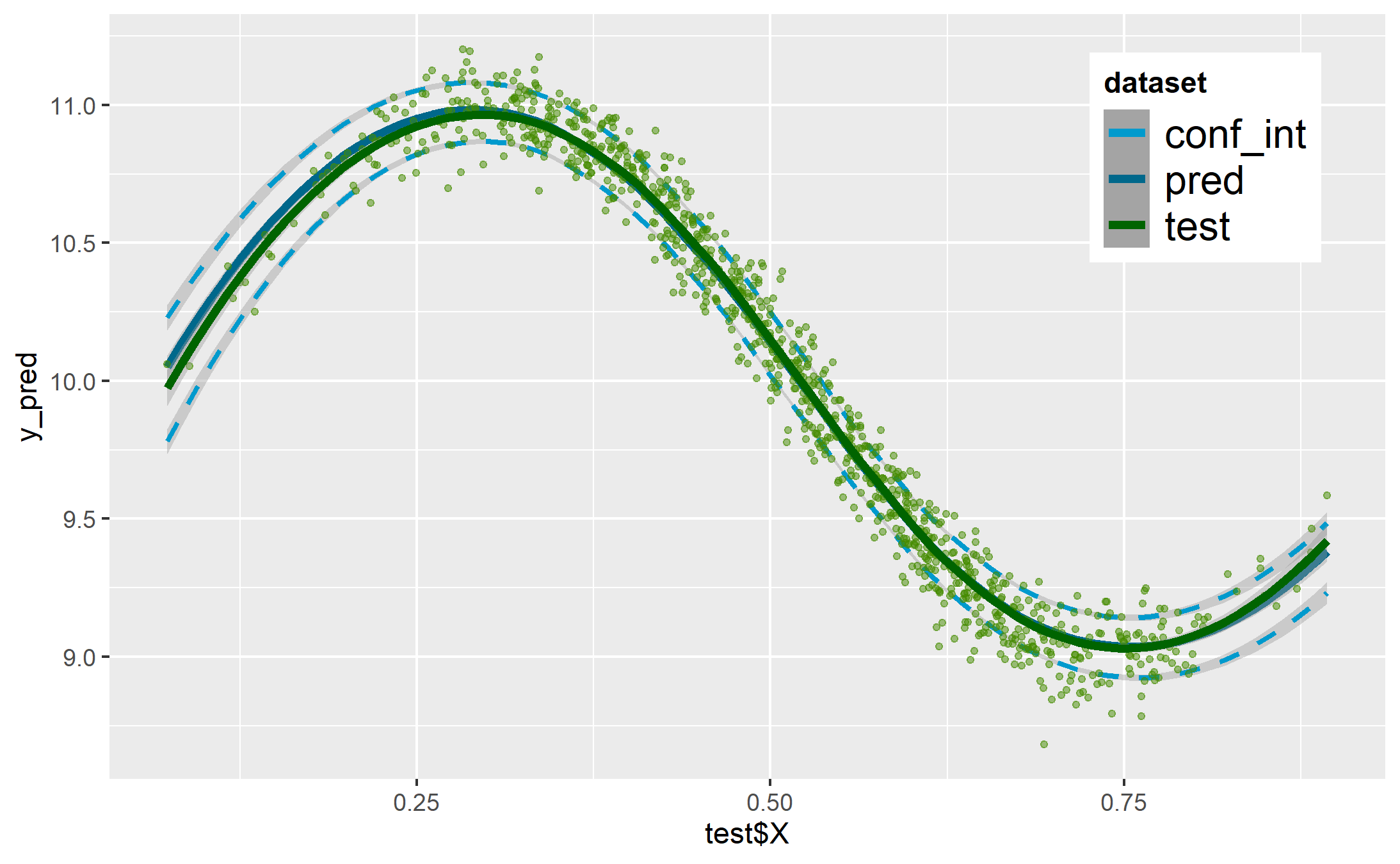

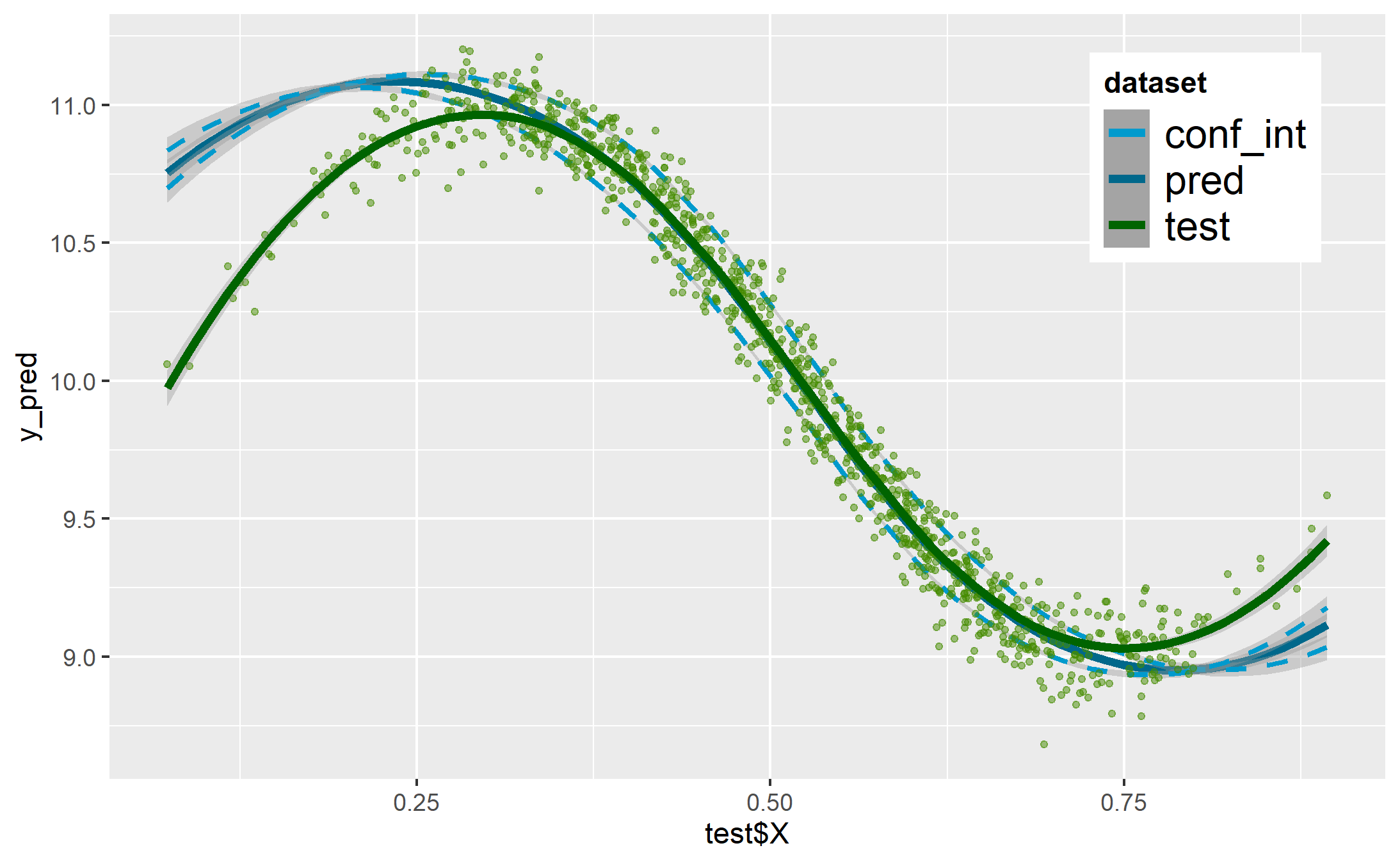

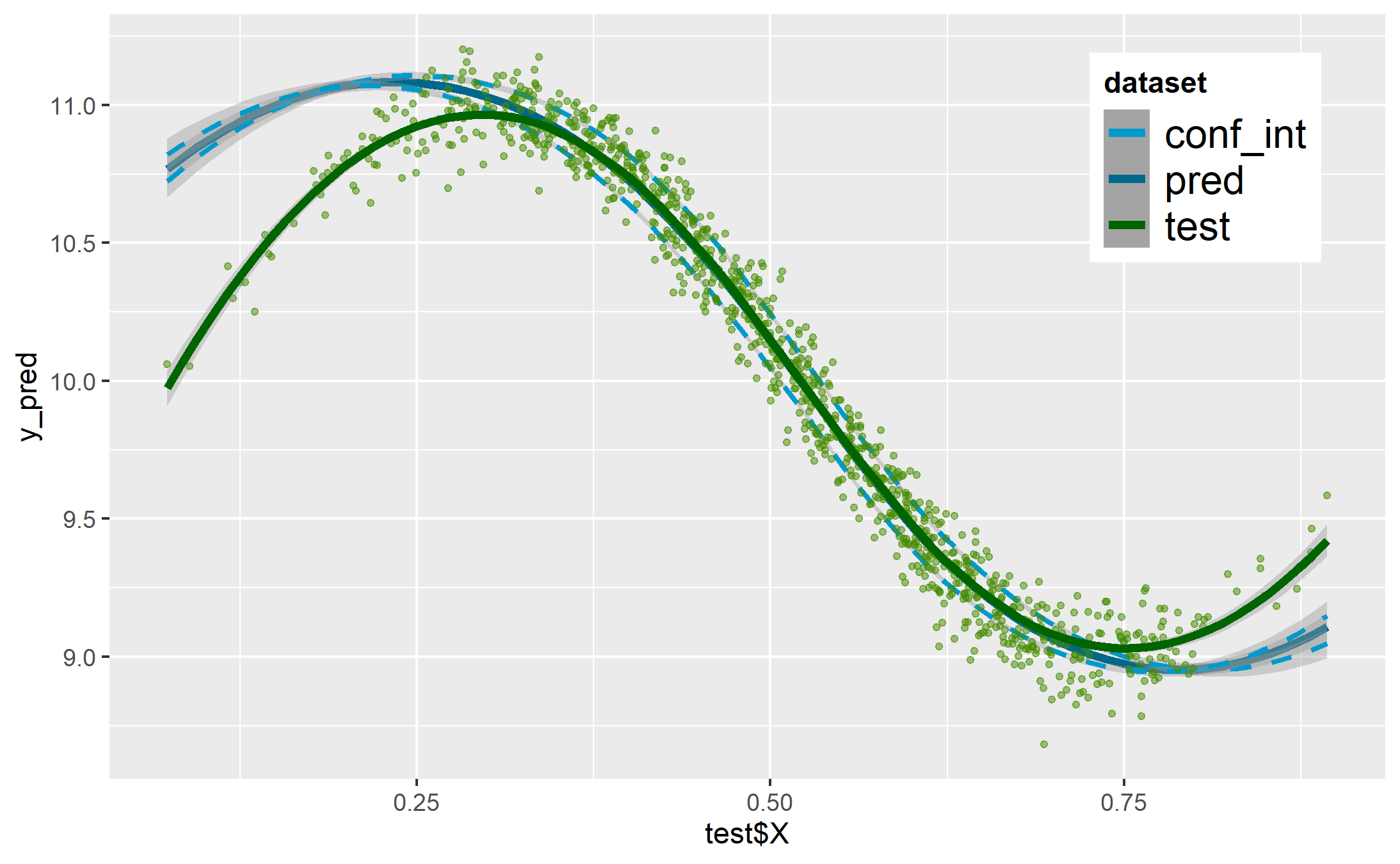

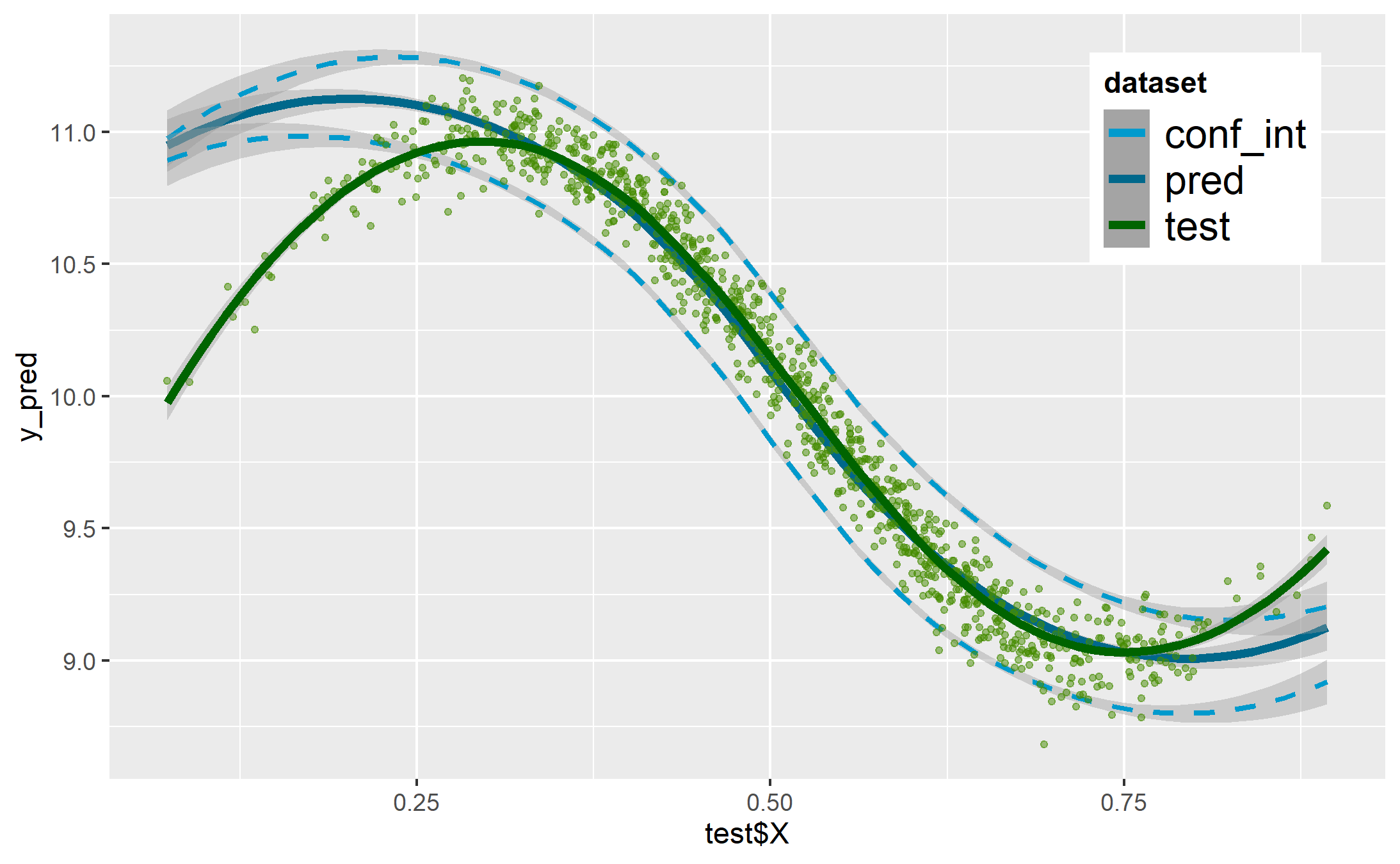

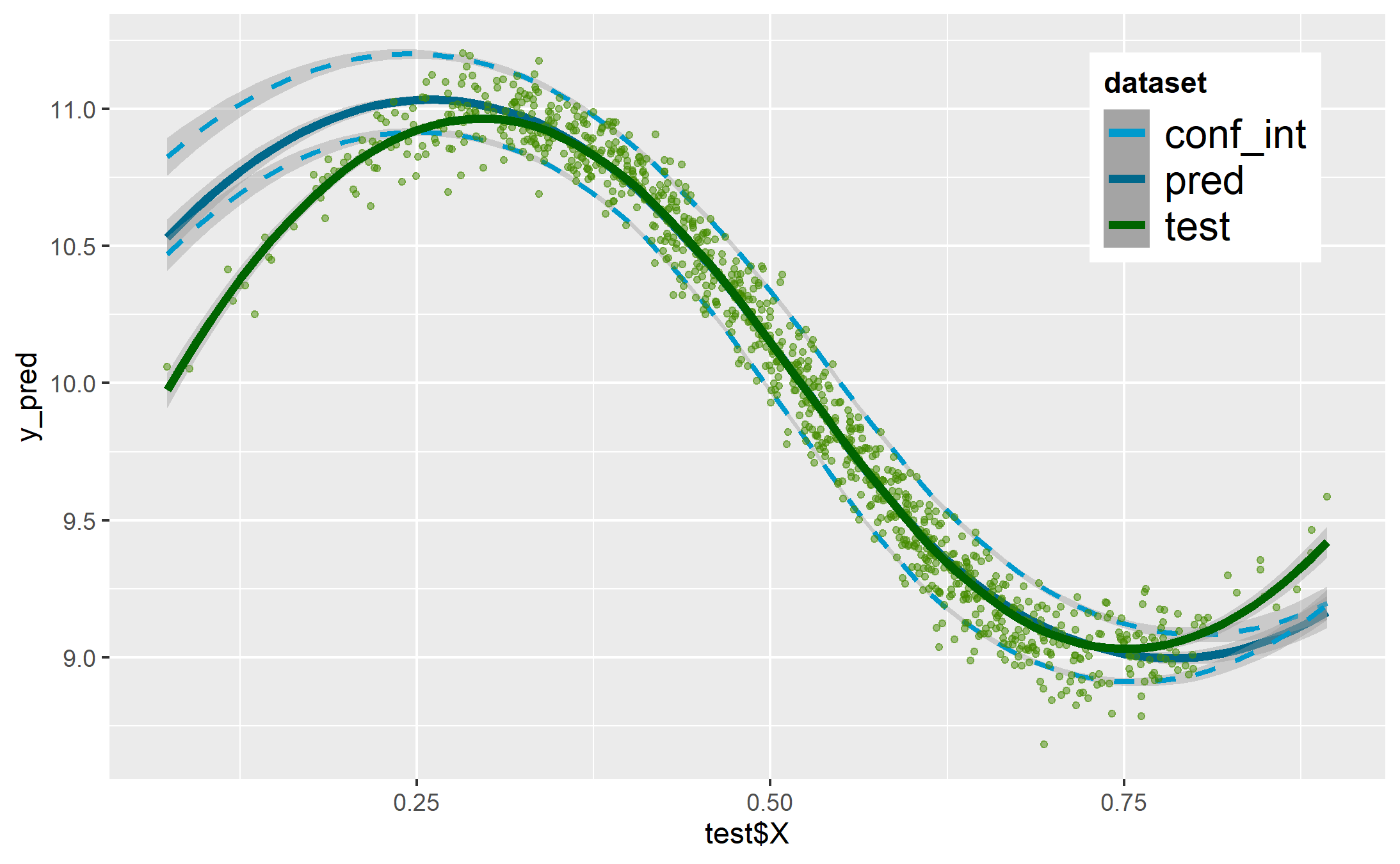

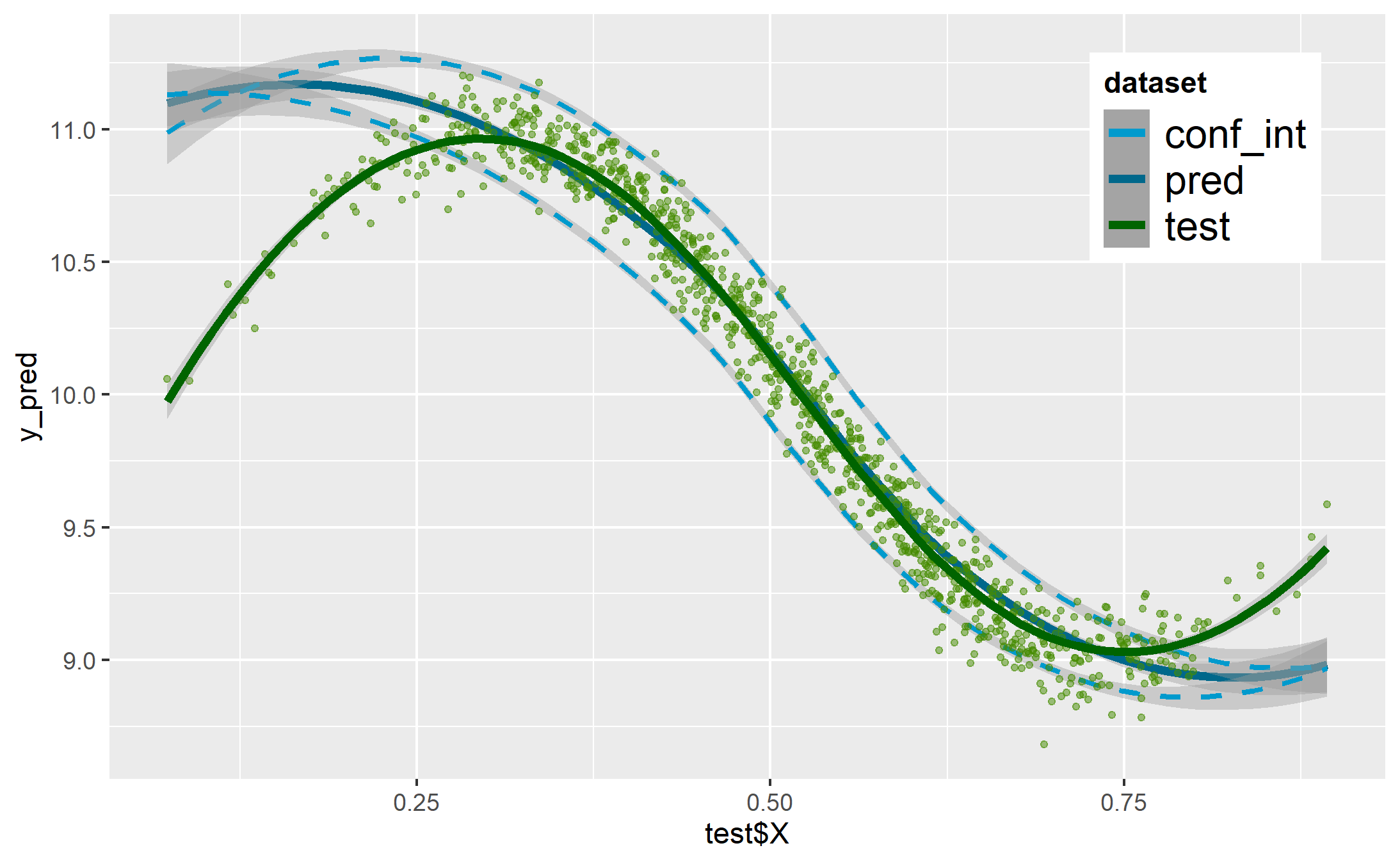

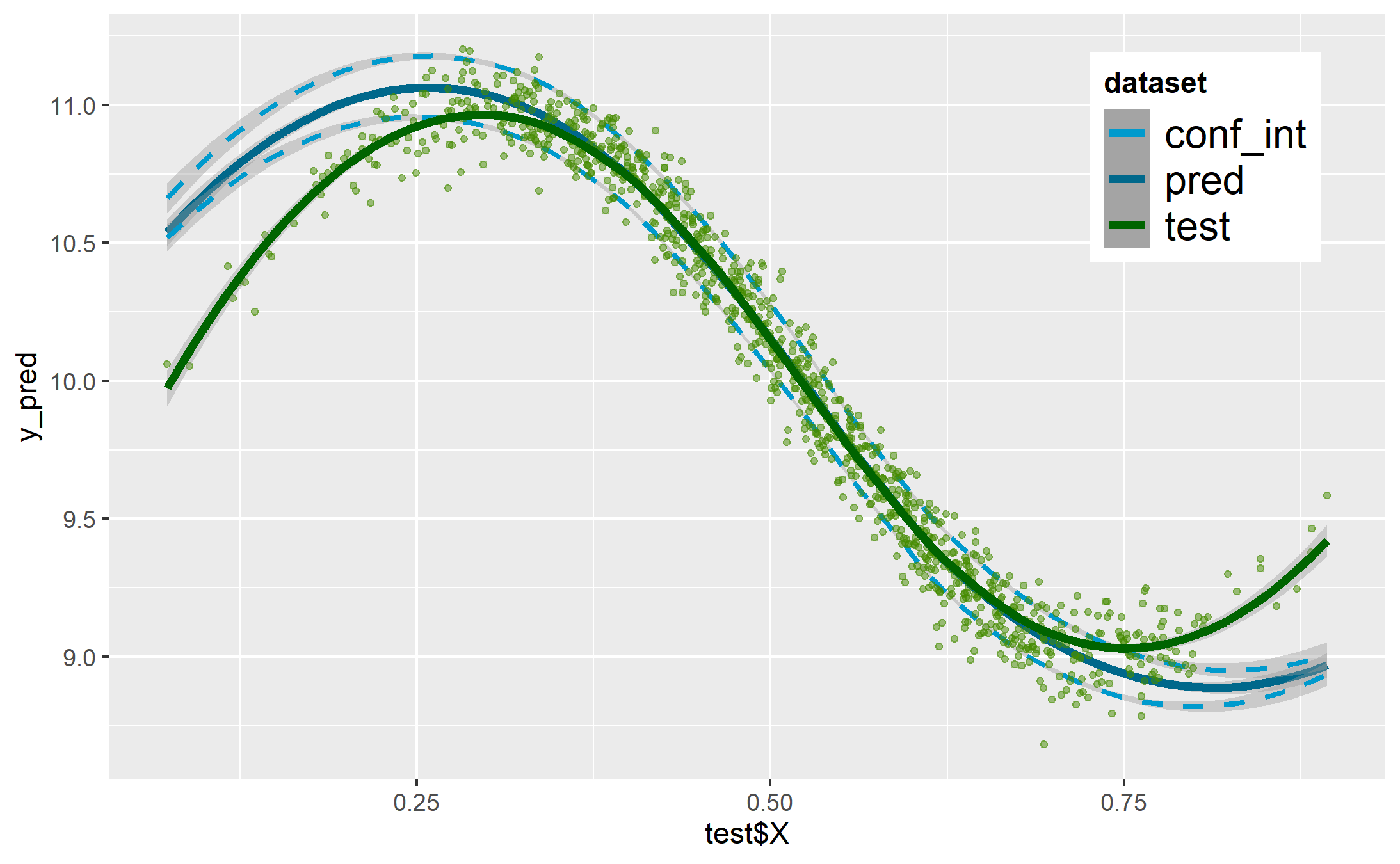

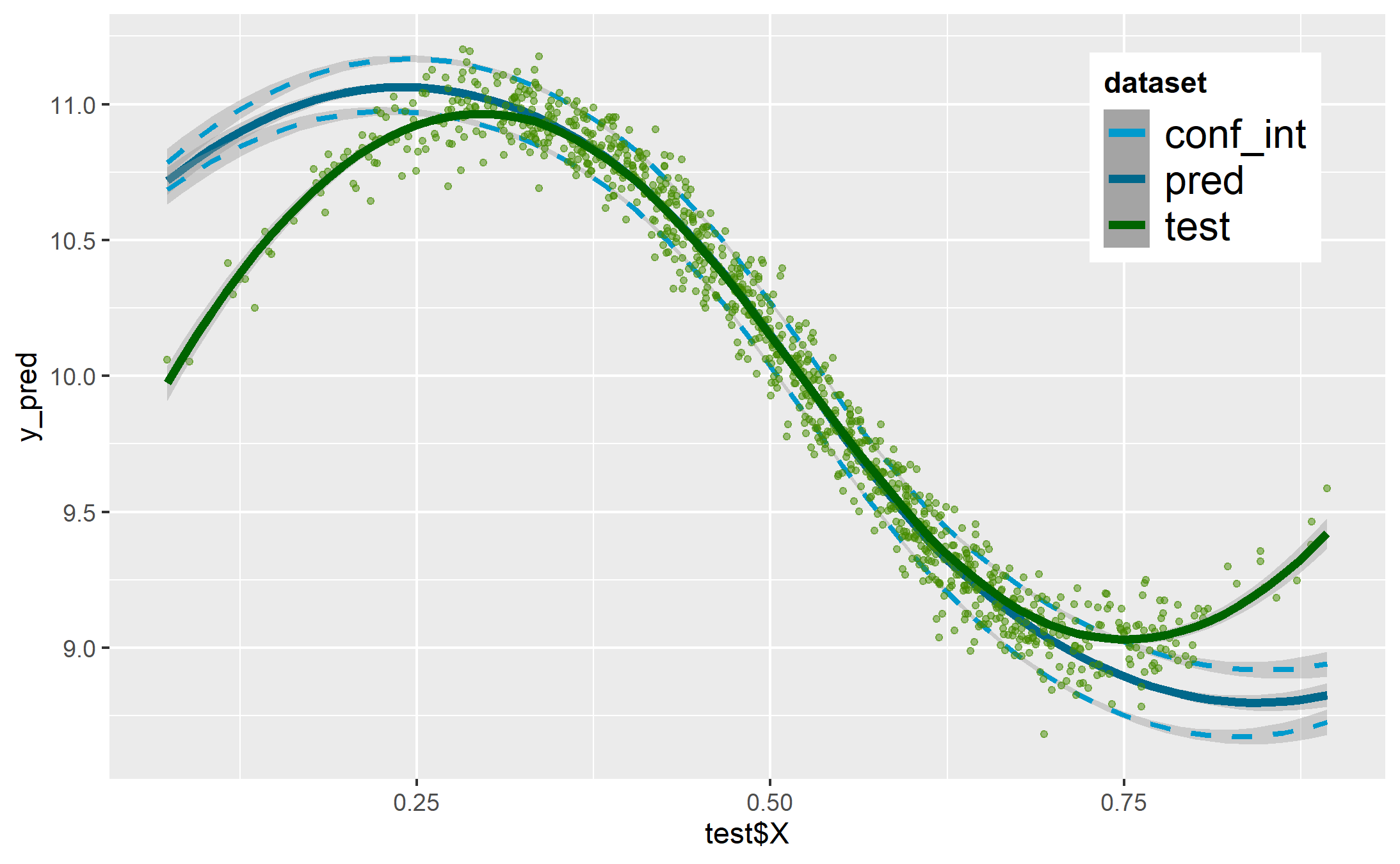

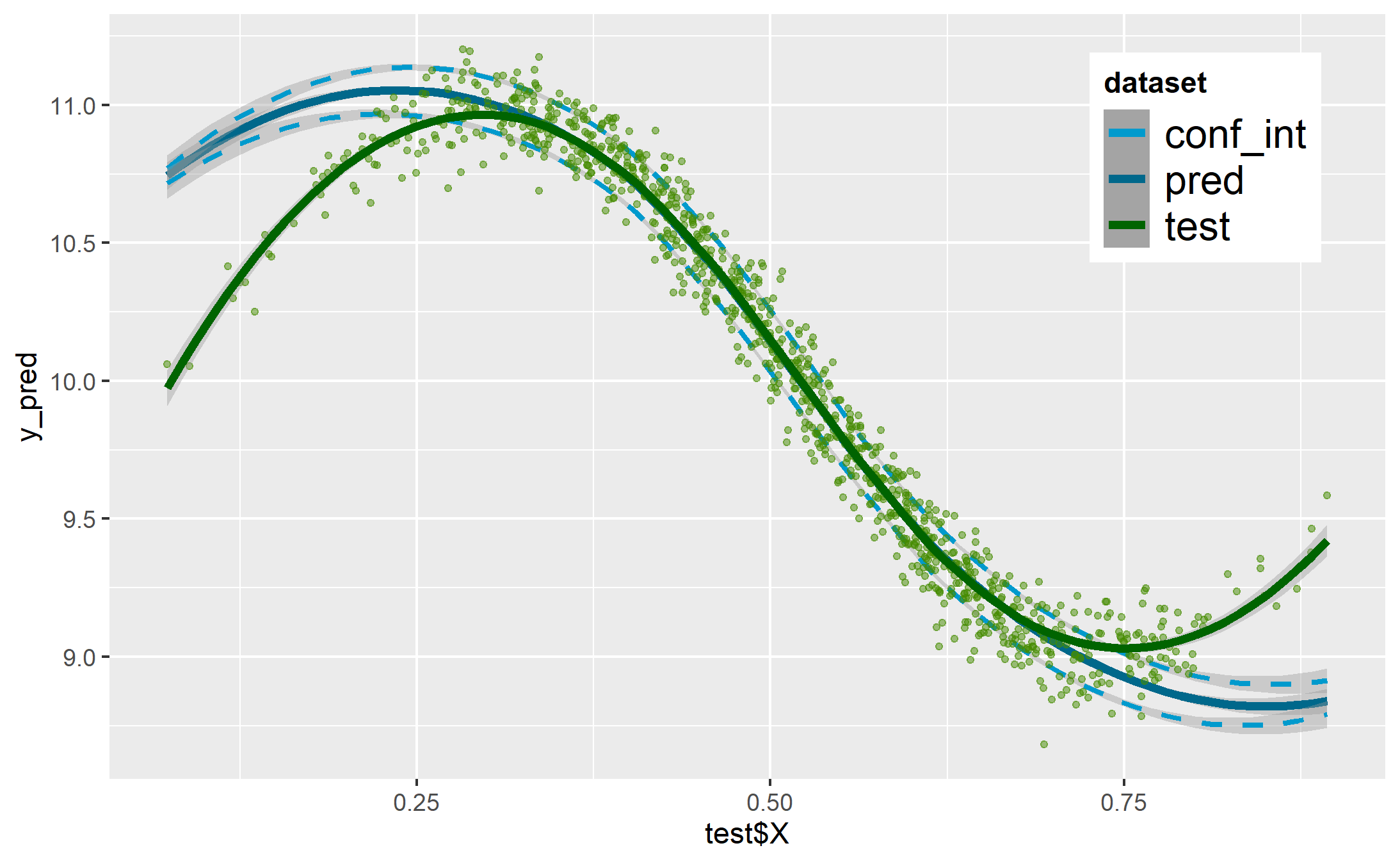

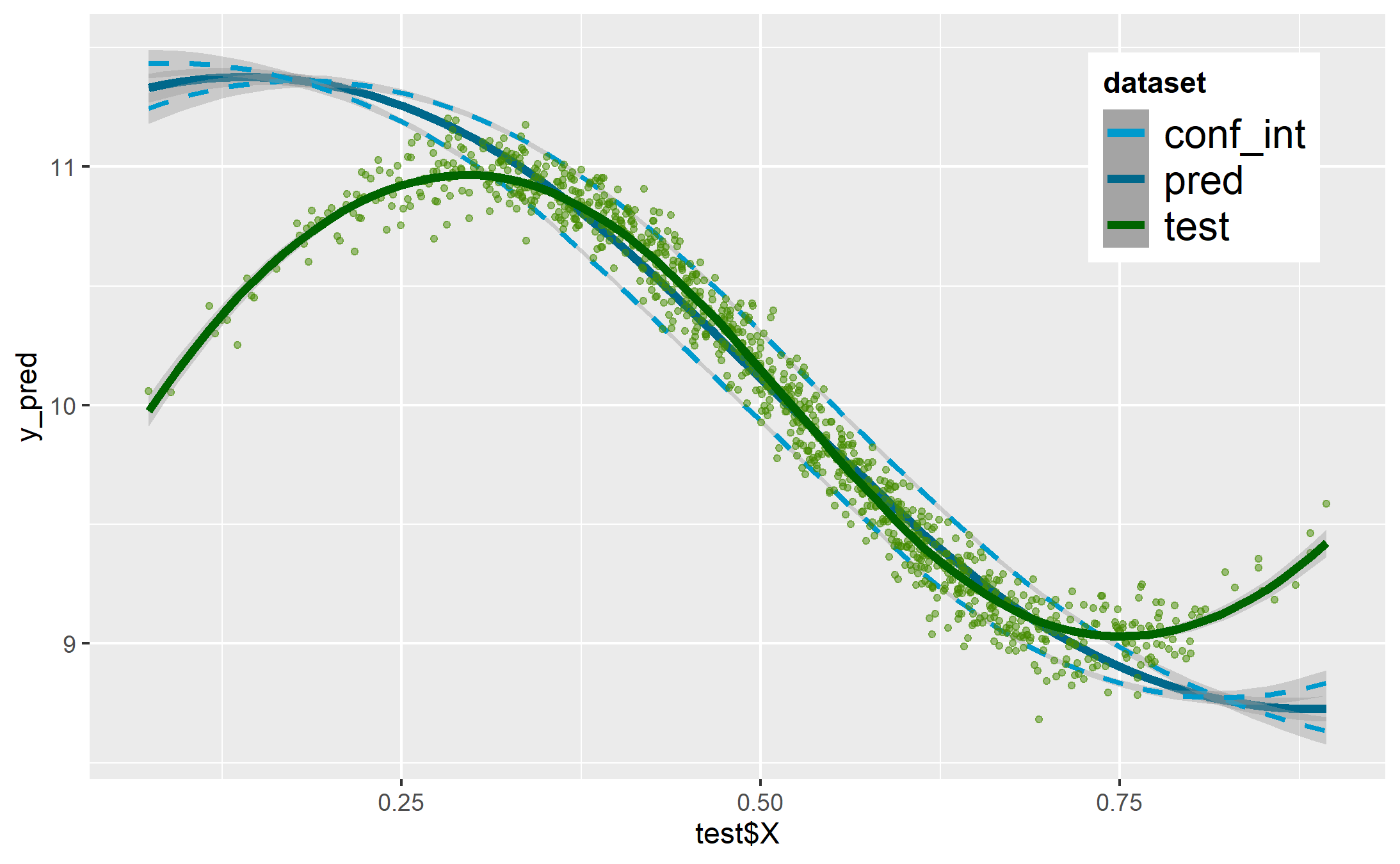

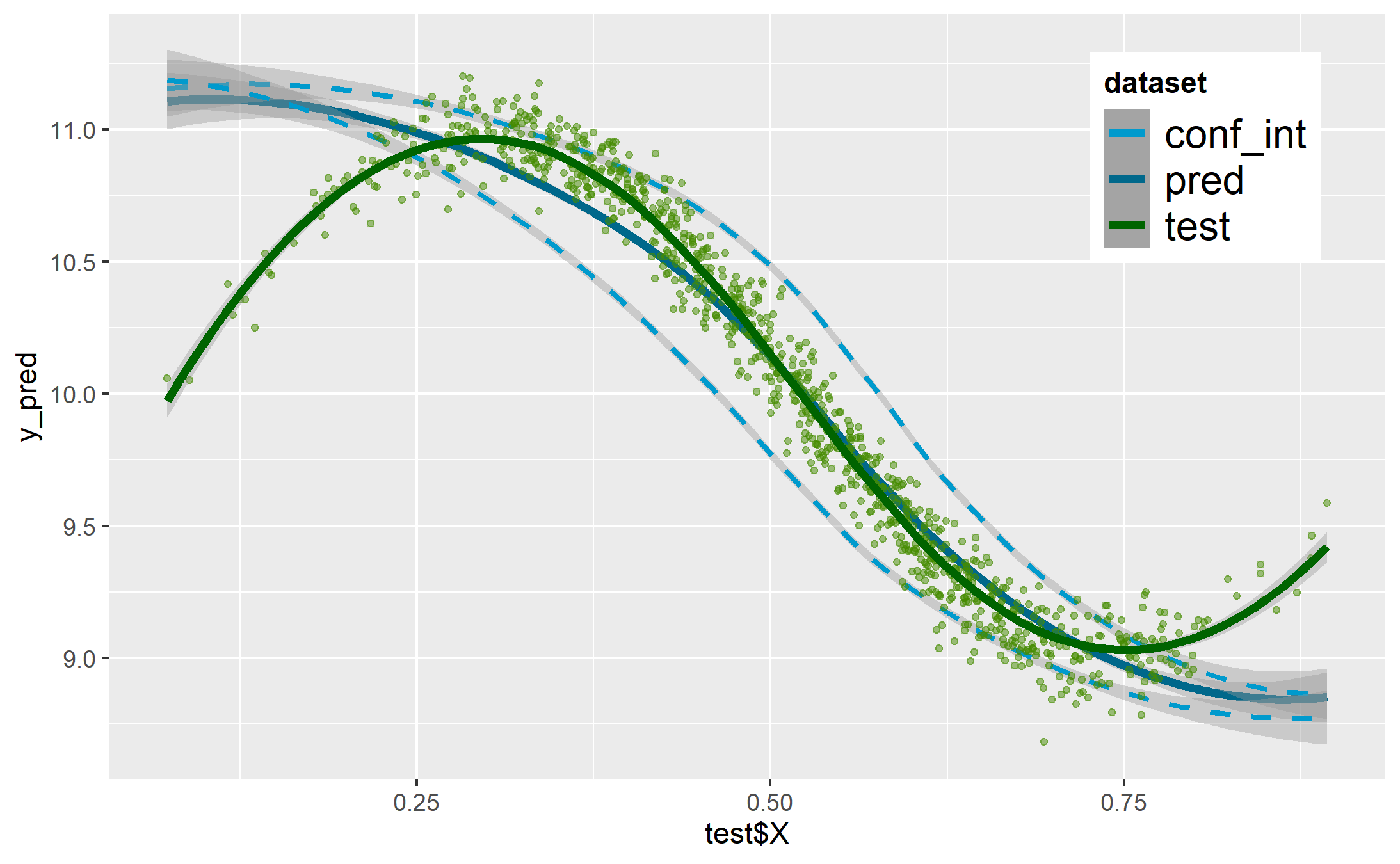

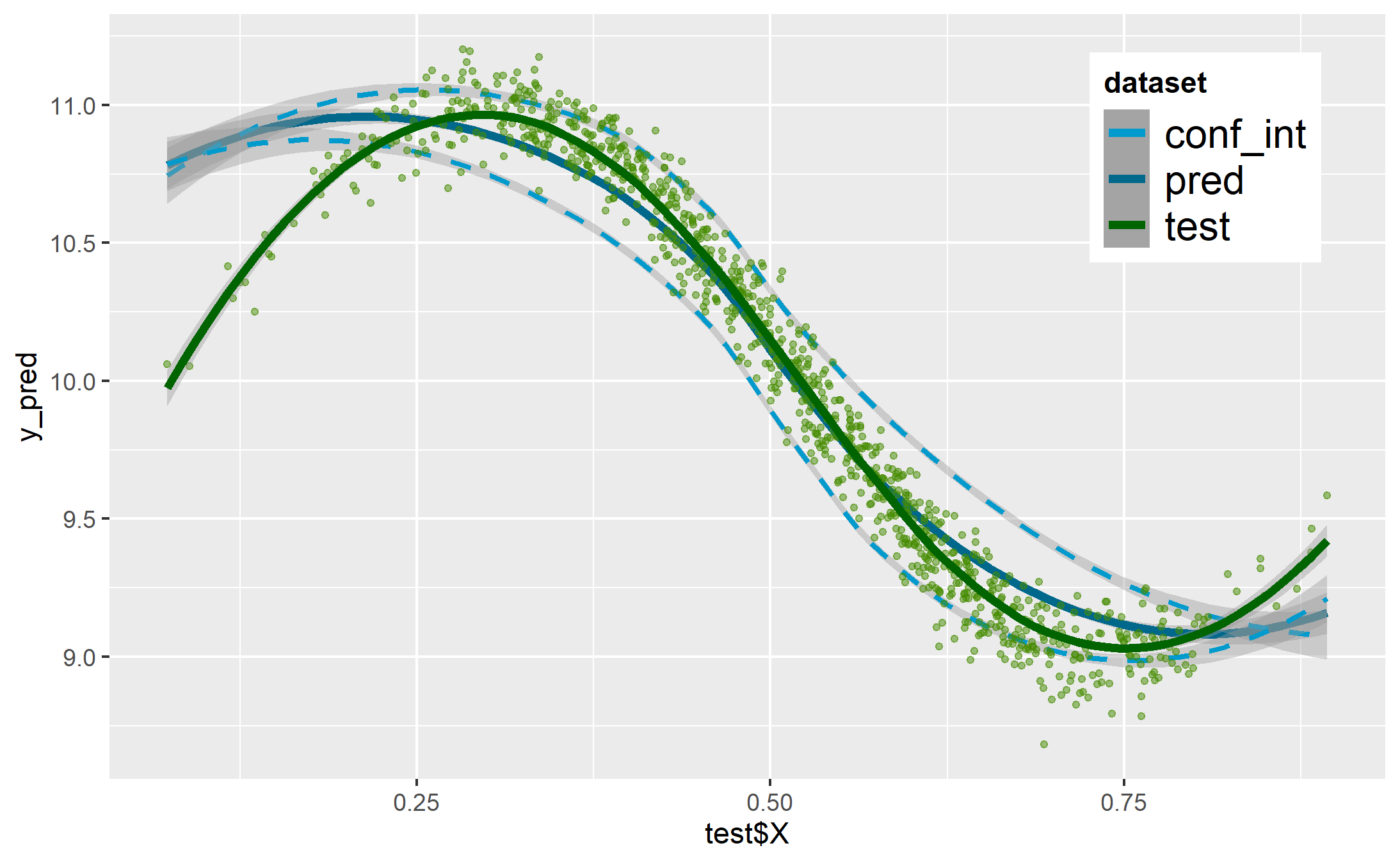

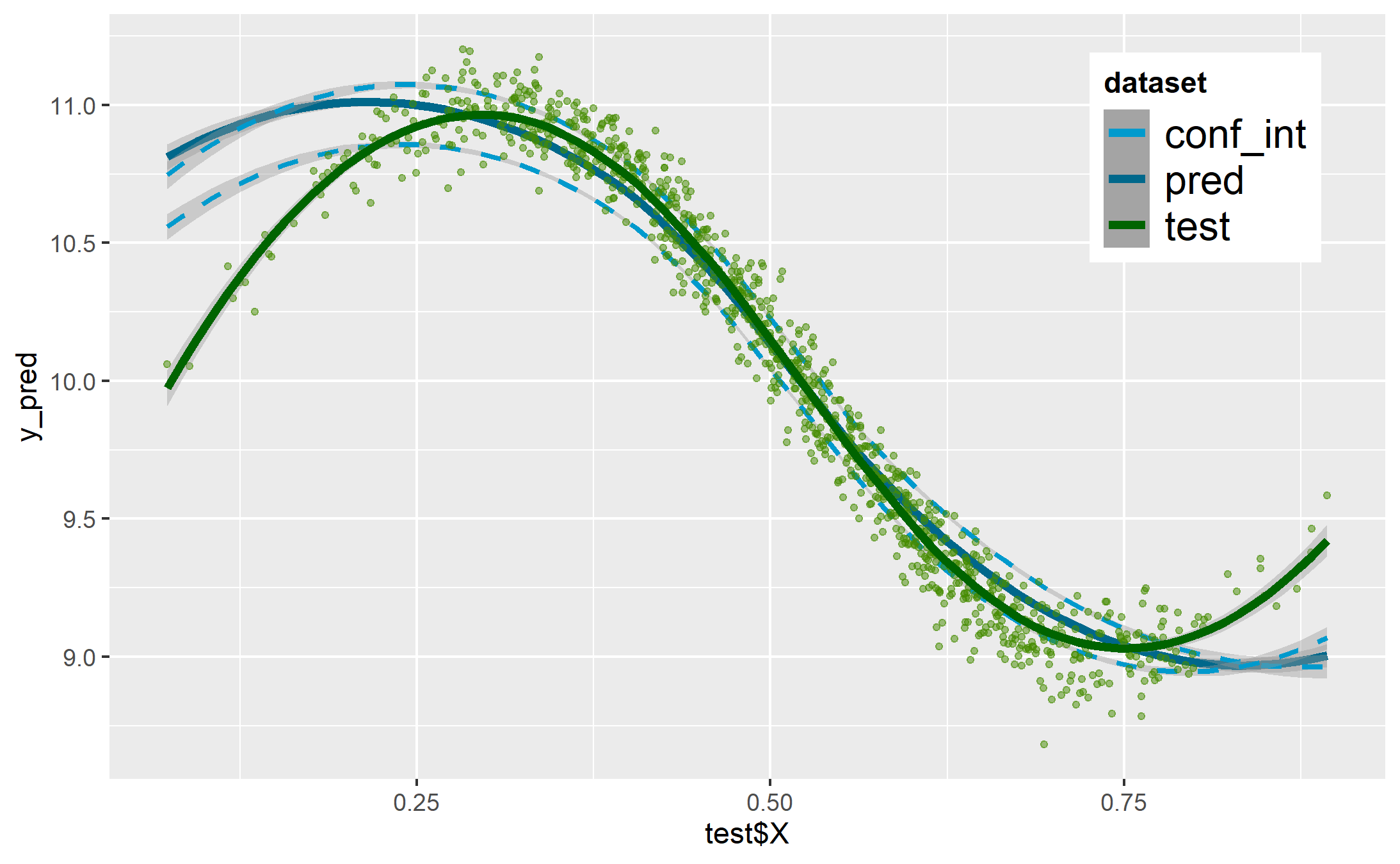

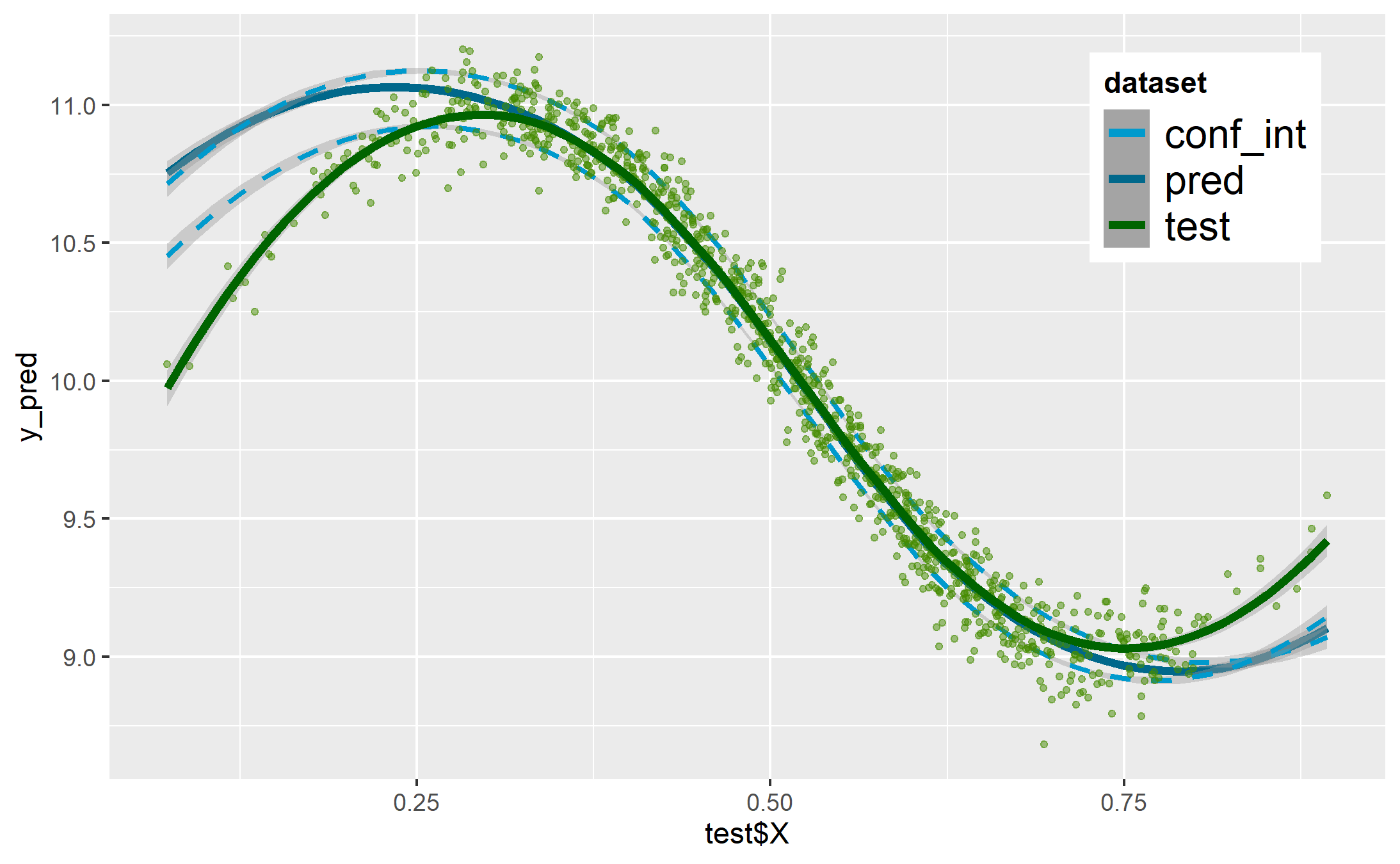

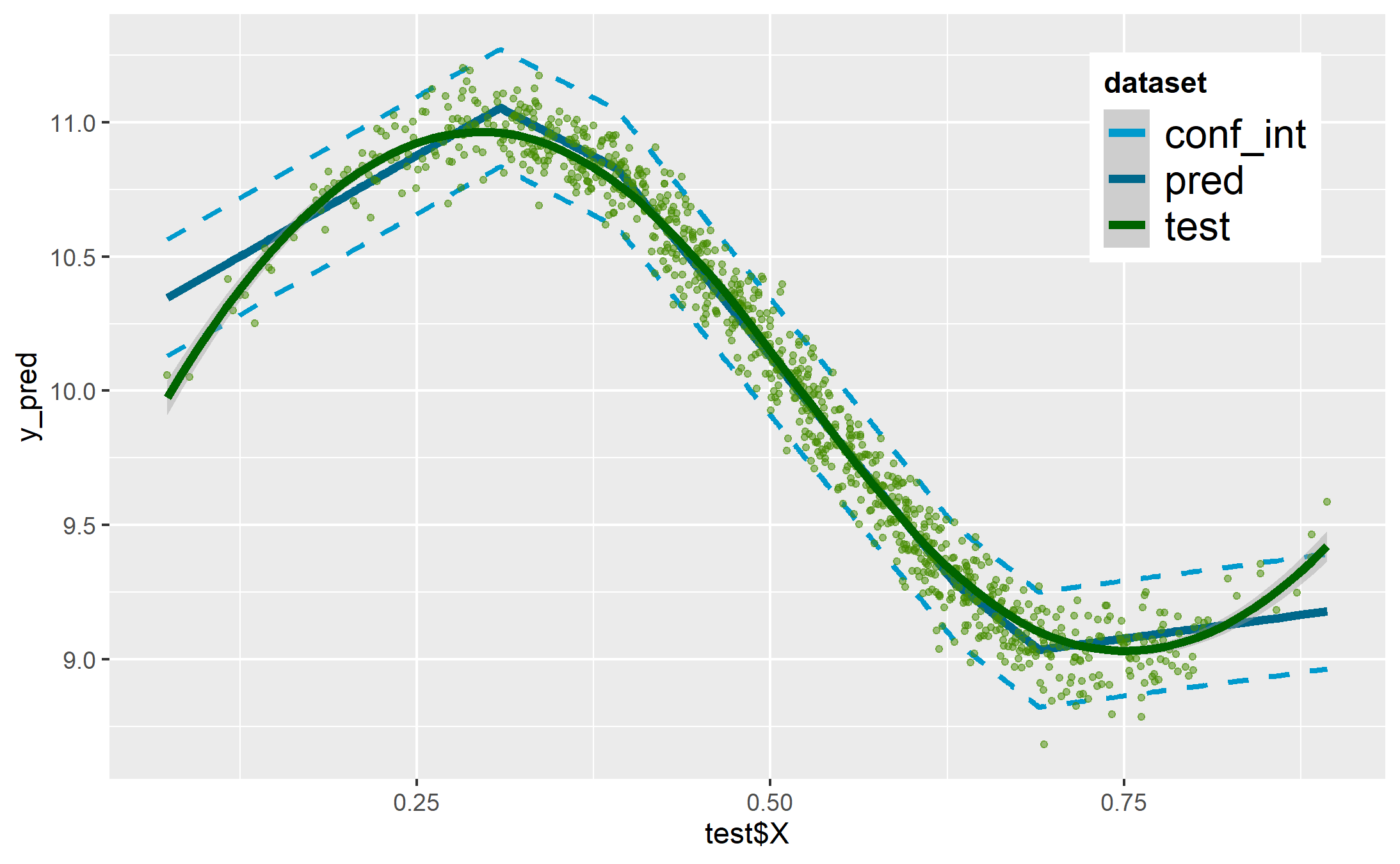

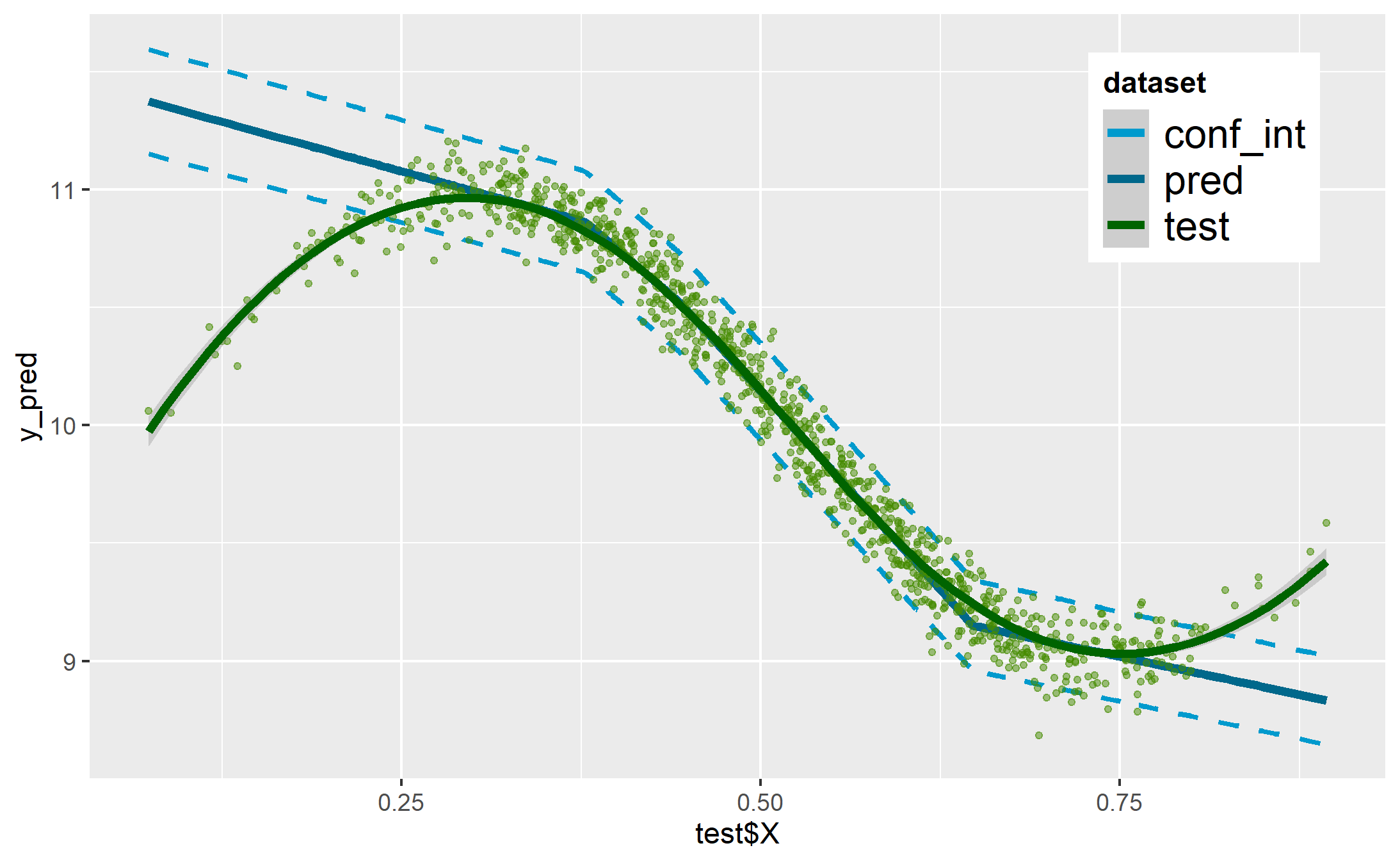

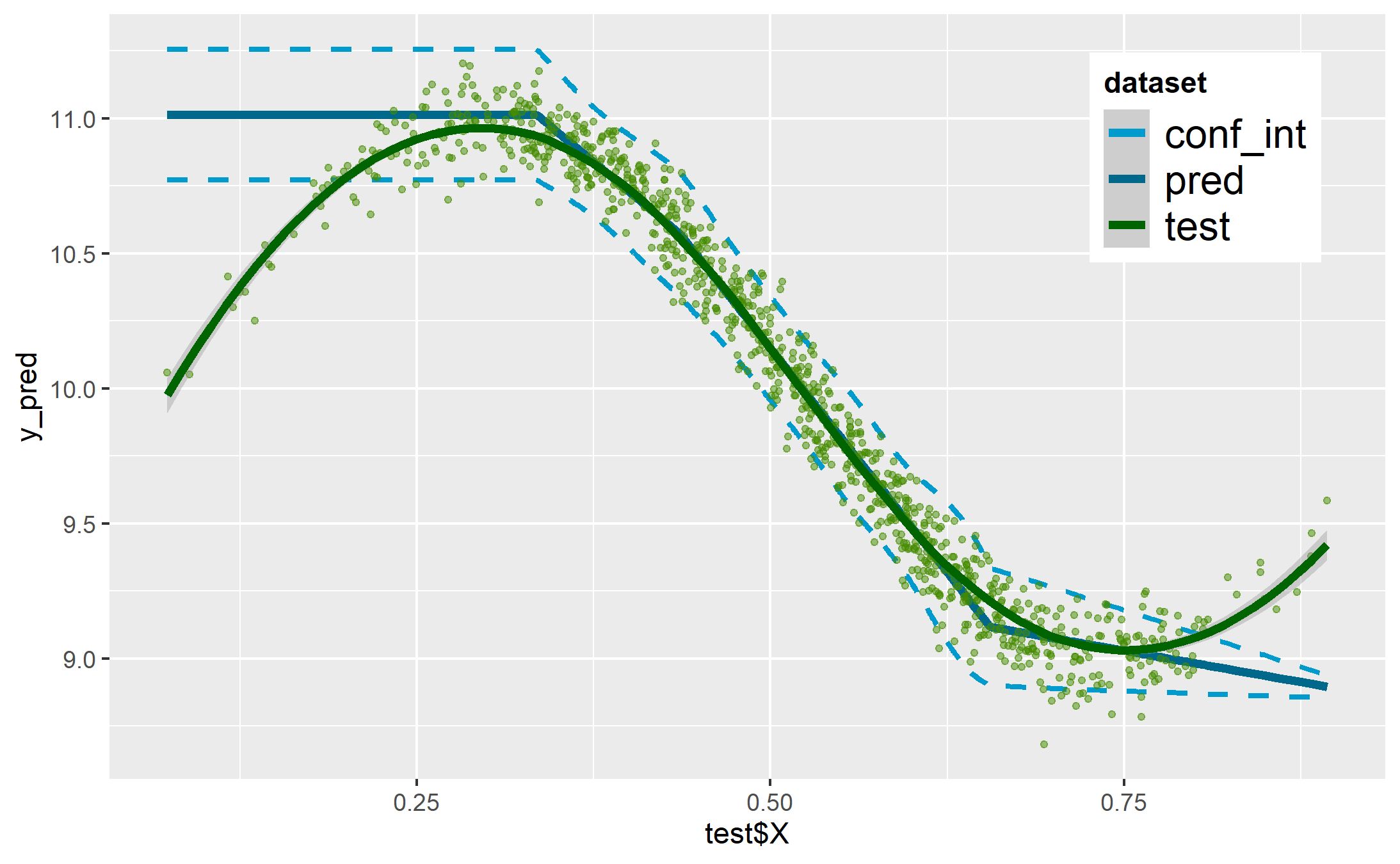

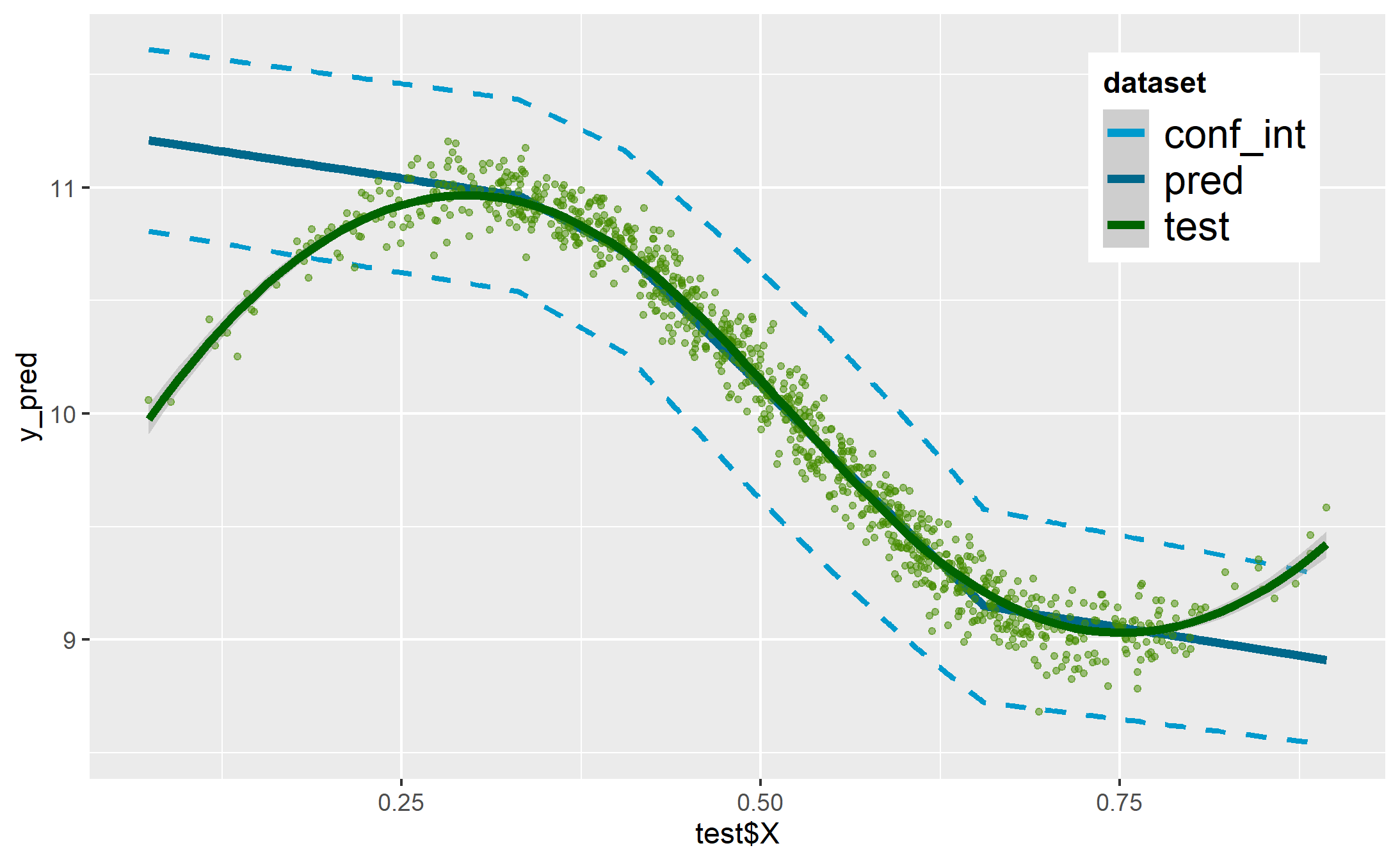

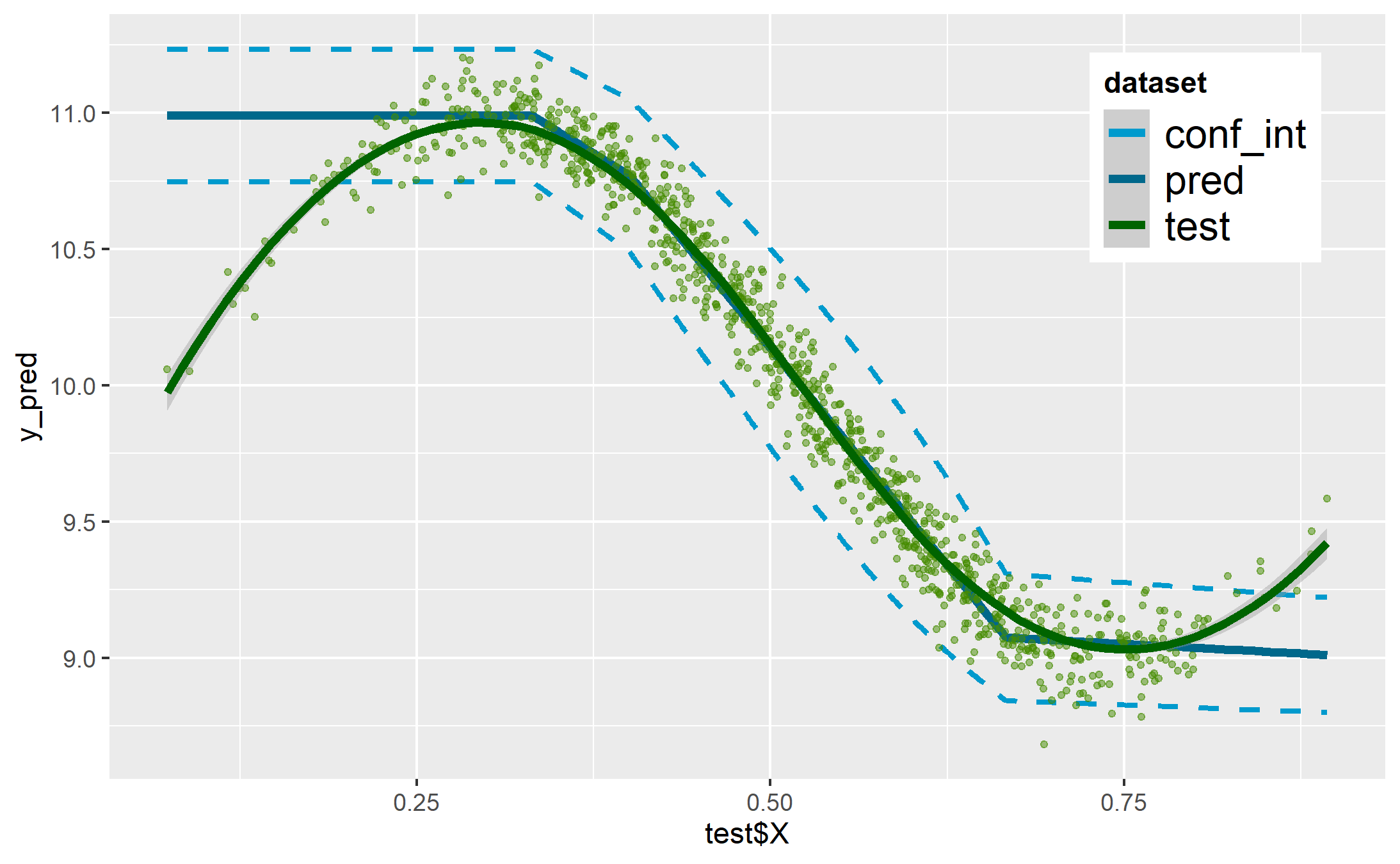

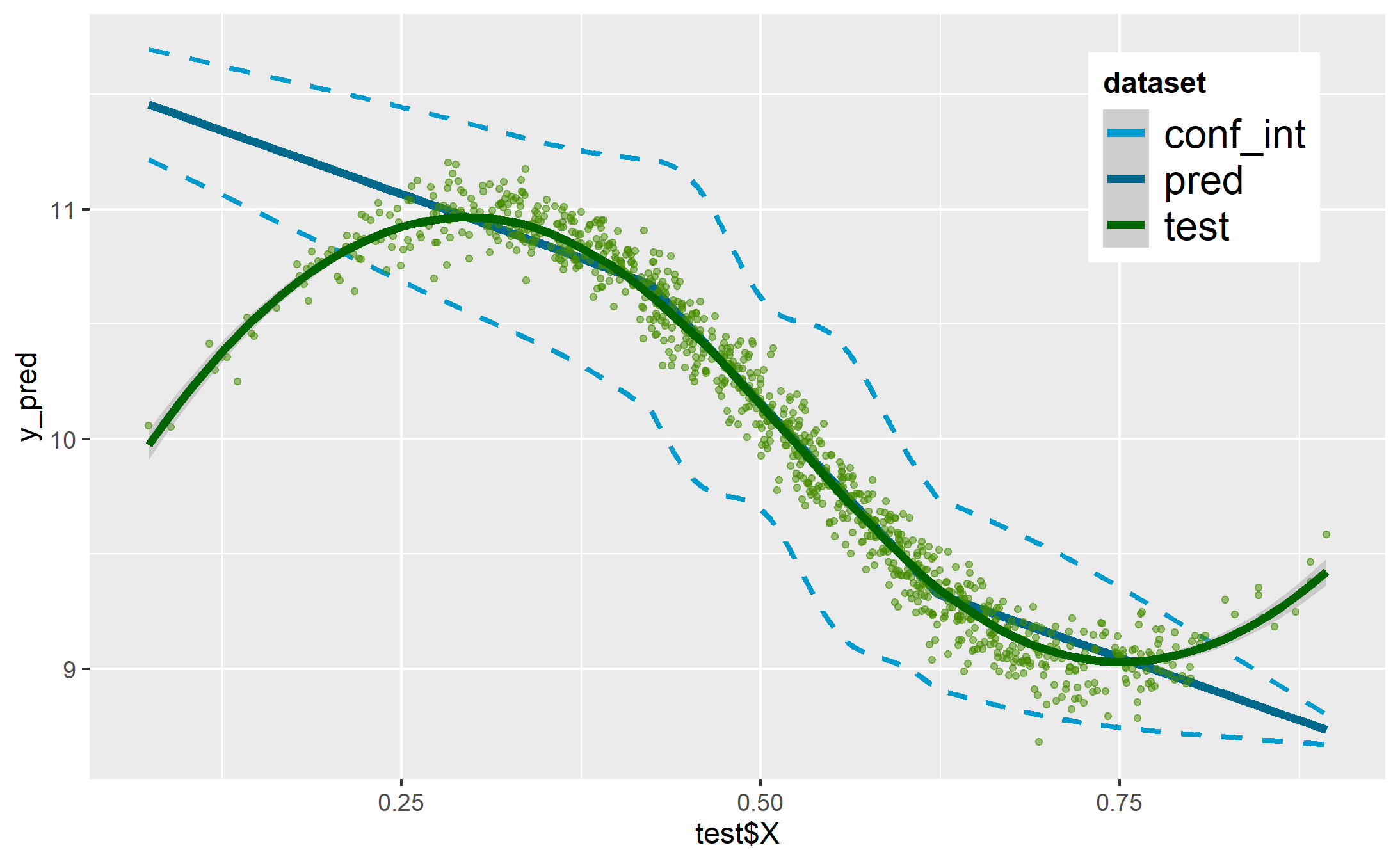

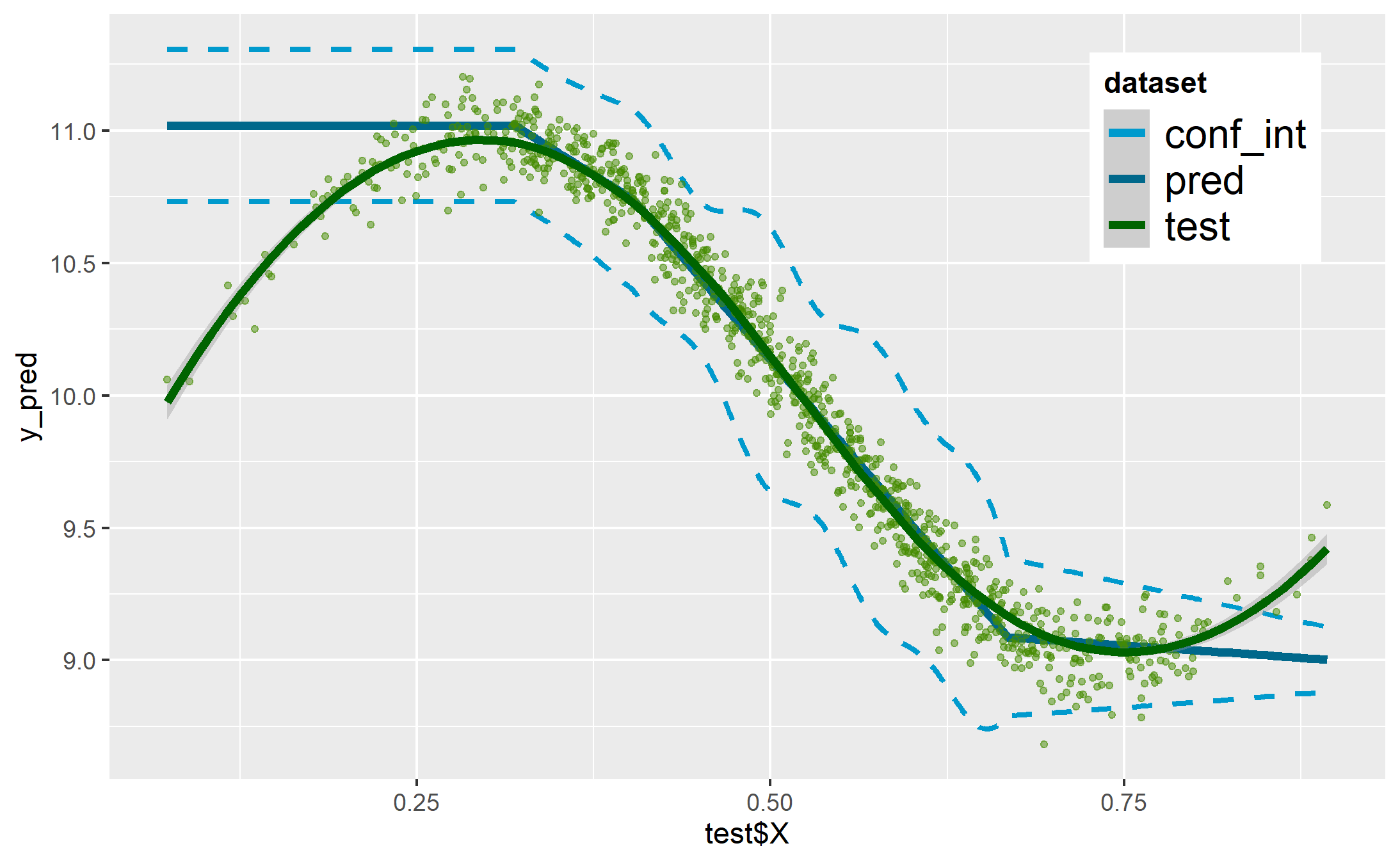

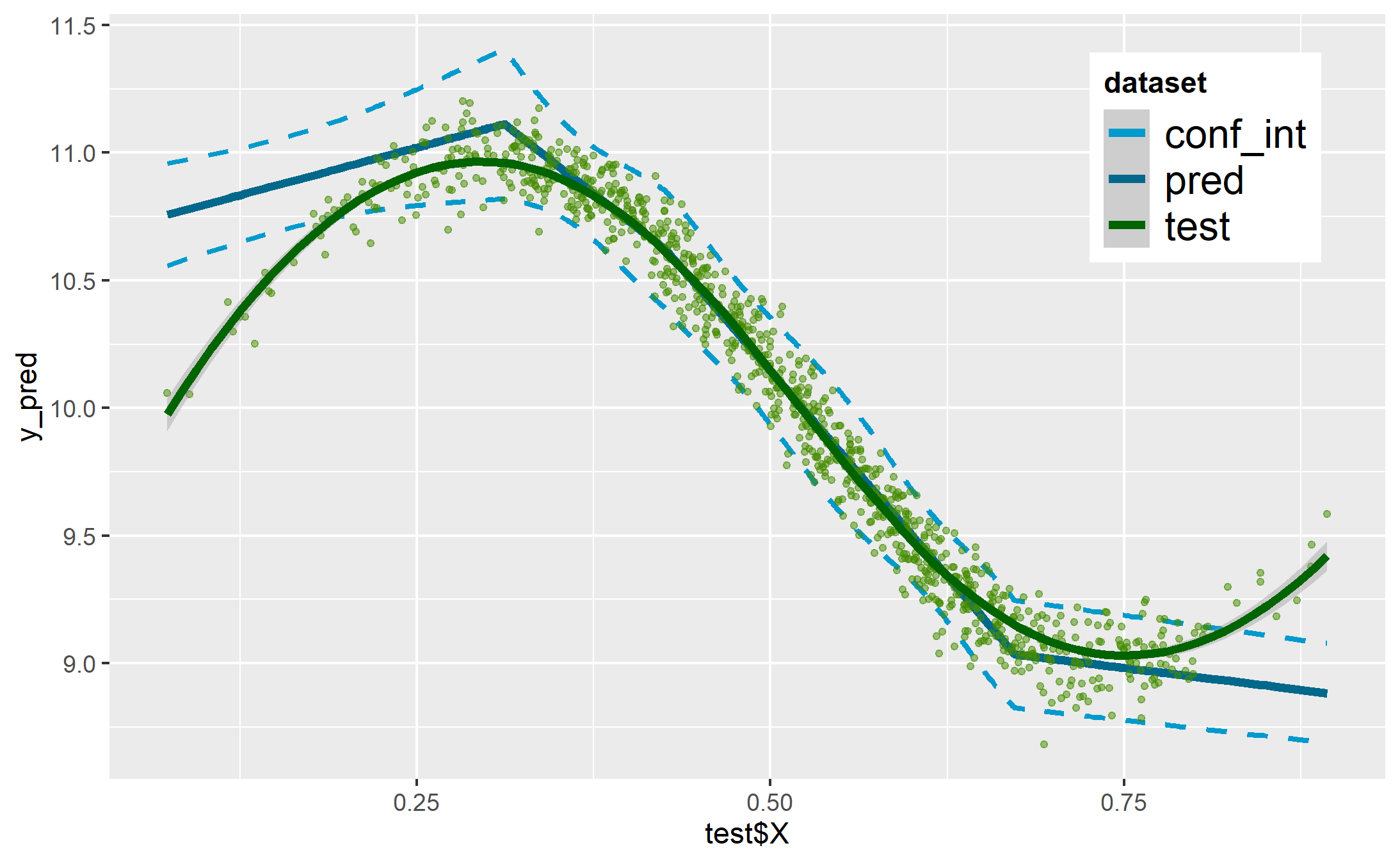

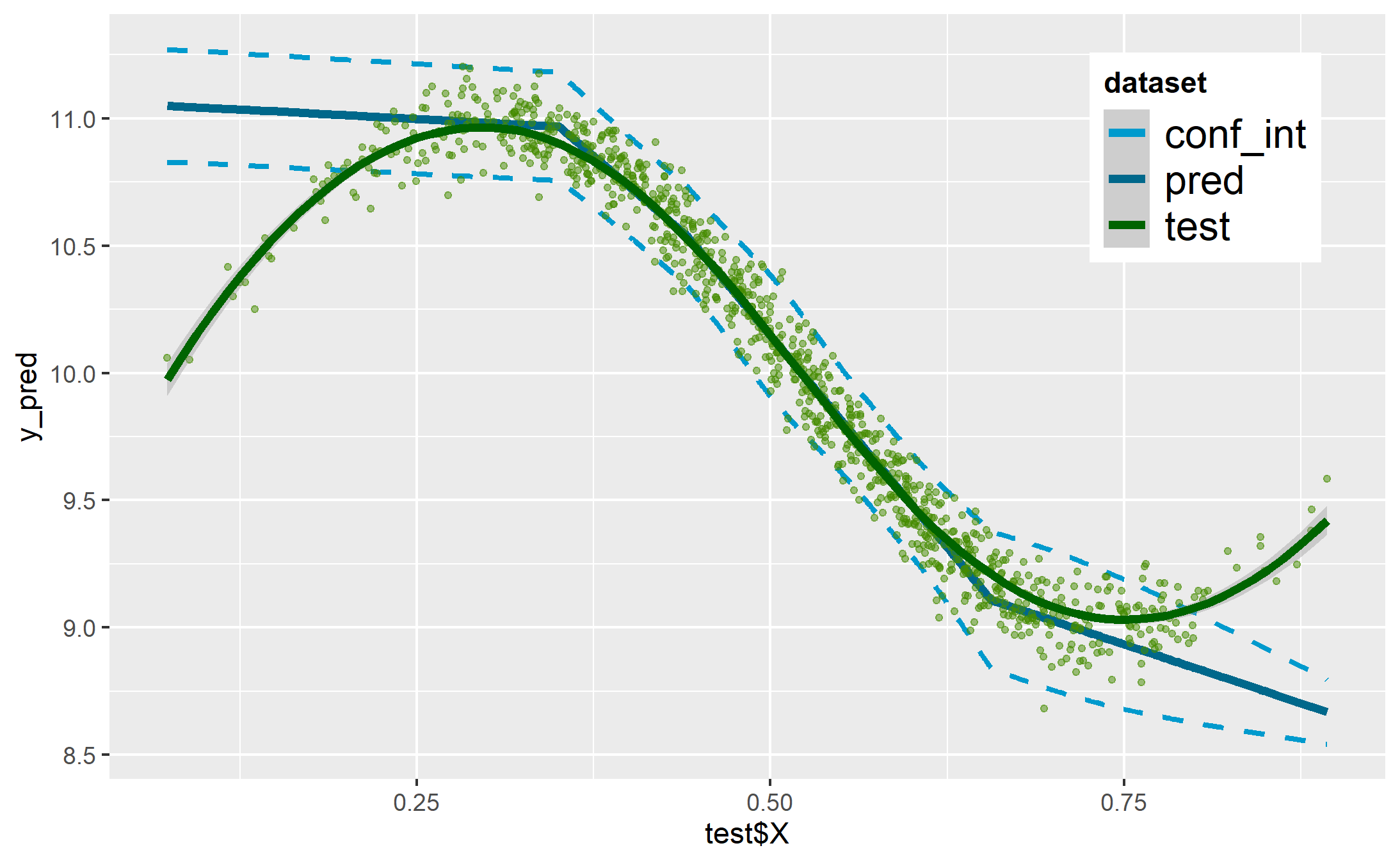

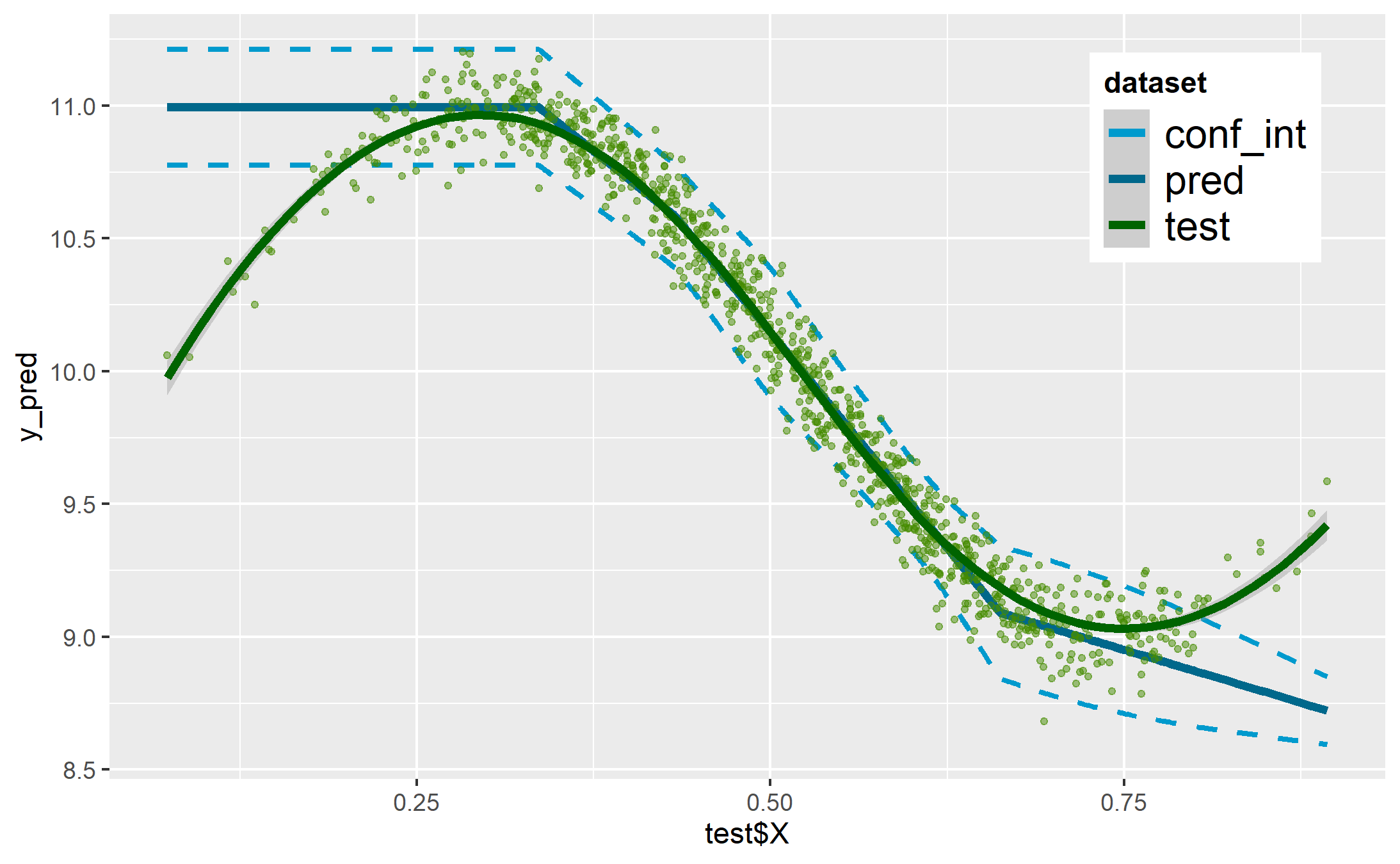

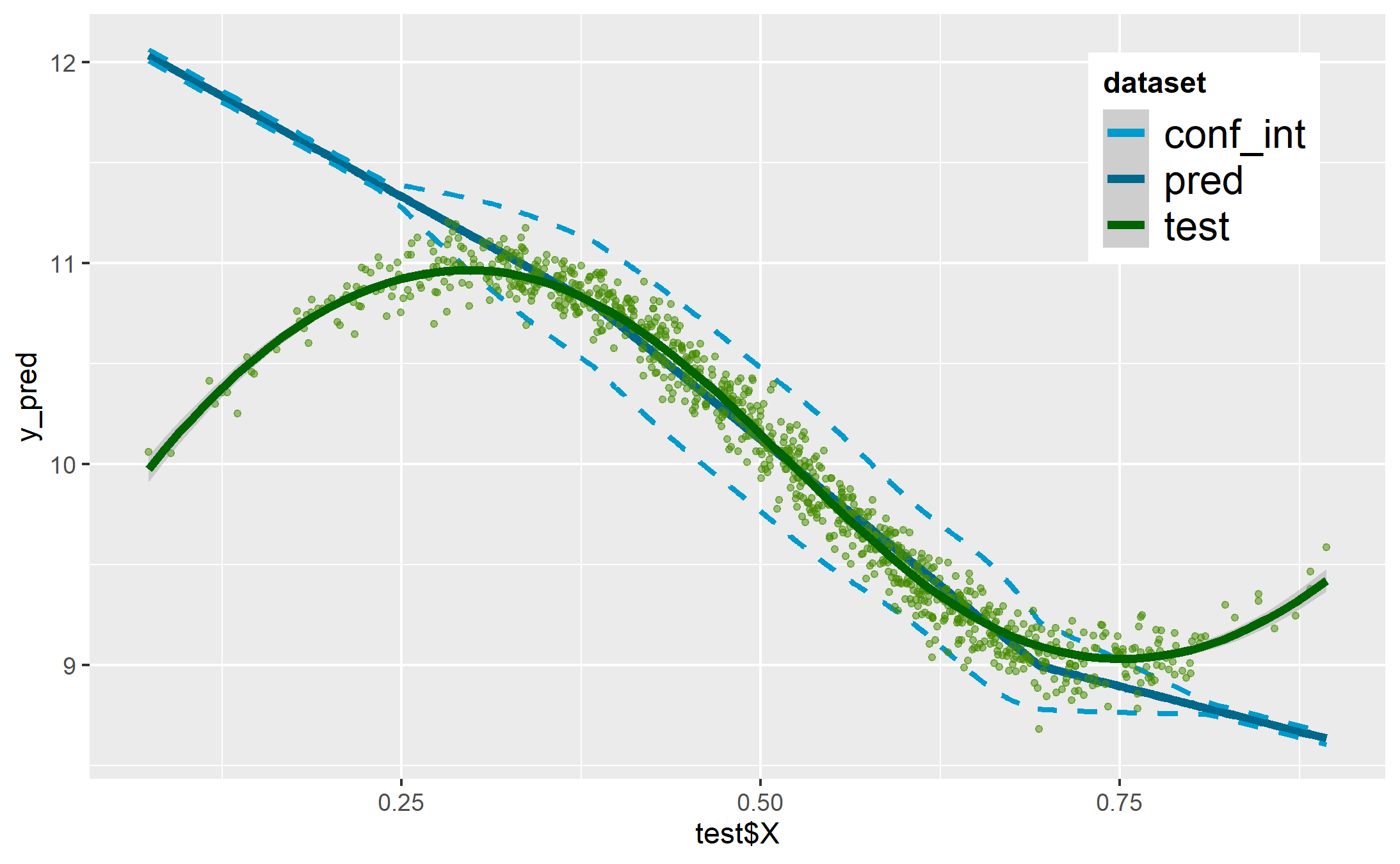

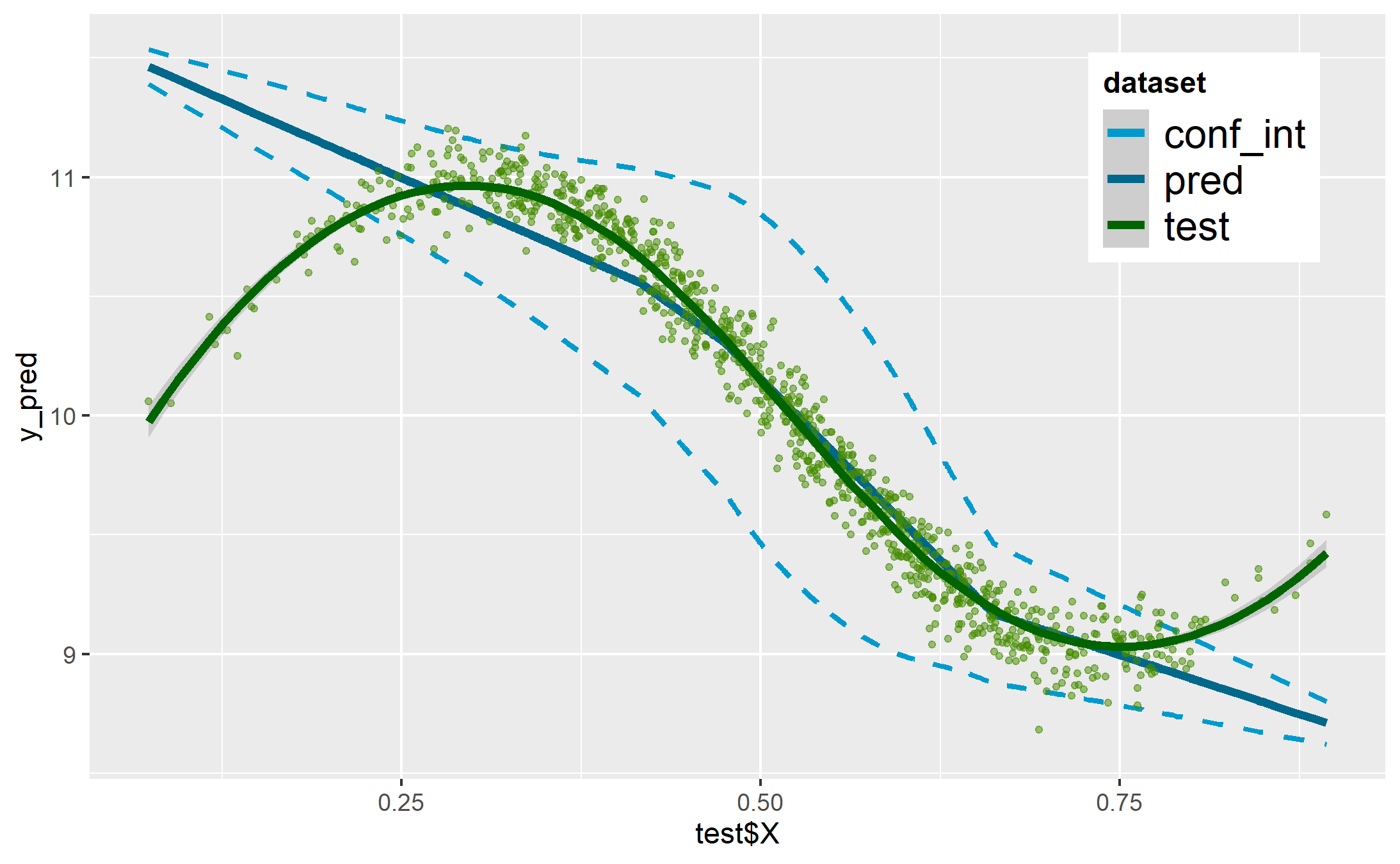

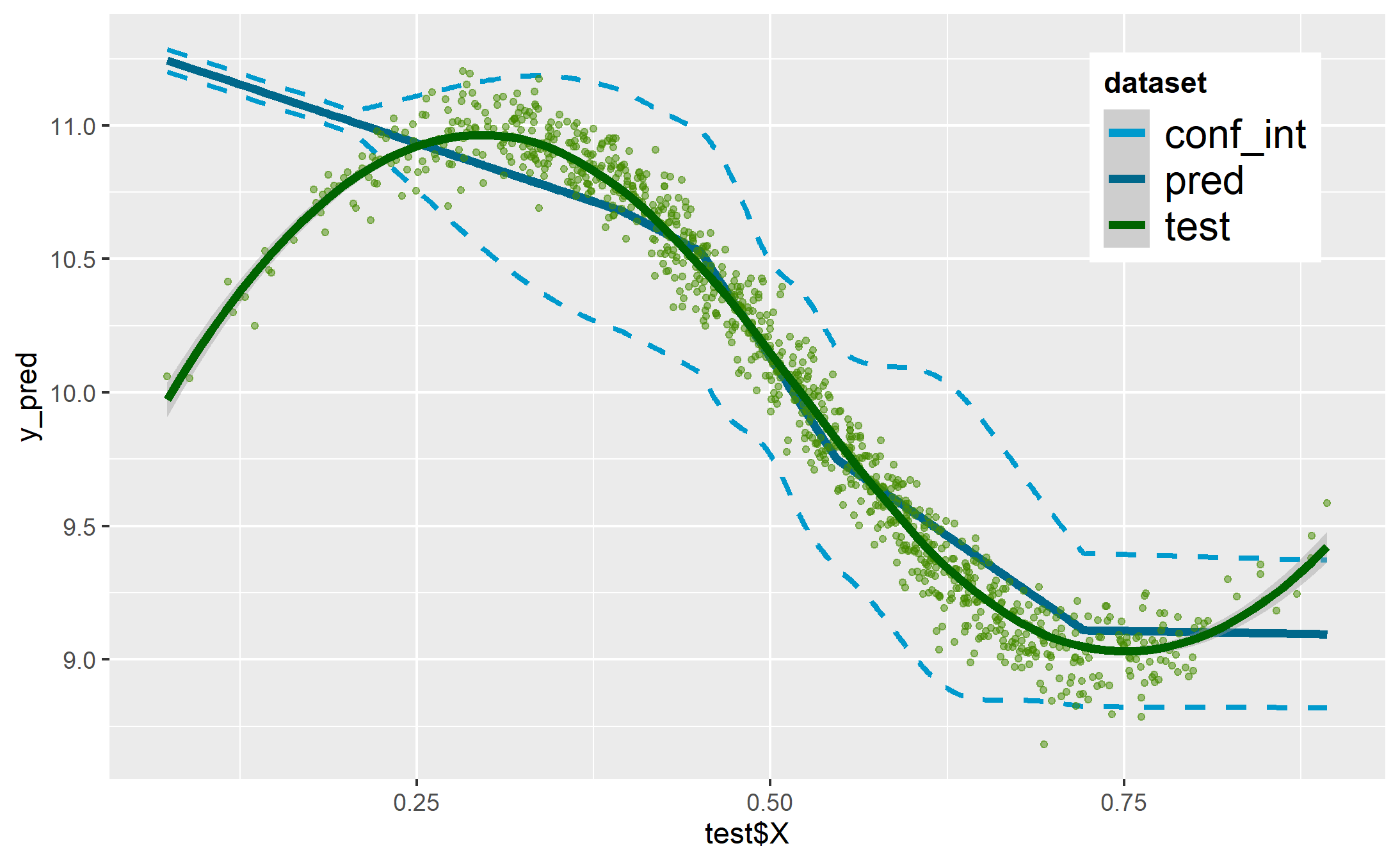

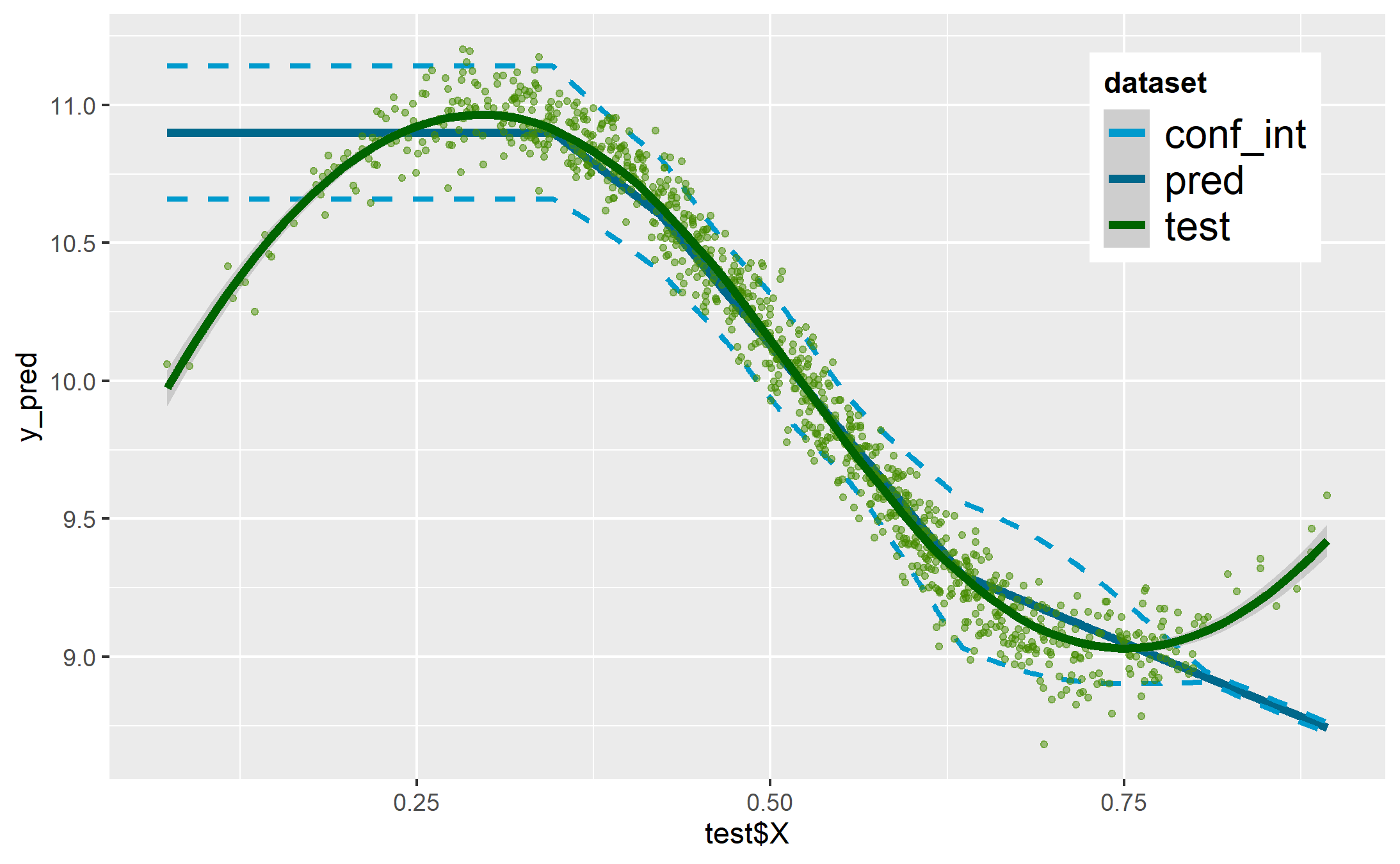

We evaluate the impacts of the WR and DA-WR algorithms on three learning models: Generalized Additive Models (GAM), Random Forest (RF) and Multivariate Adaptative Regression Splines (MARS). More details on these algorithms are given in the supplement. We evaluate the prediction results of these three models on the test sample through Root Mean Square Error (RMSE). The different smoothed predictions on the test dataset () are shown in Figures 10- 12 in the Supplement, for each learning model. The stability of the results for the different generators is analyzed by applying the method on several training samples (Figures 14- 16 in the Supplement).

3.3.1 Impact of an imbalanced dataset

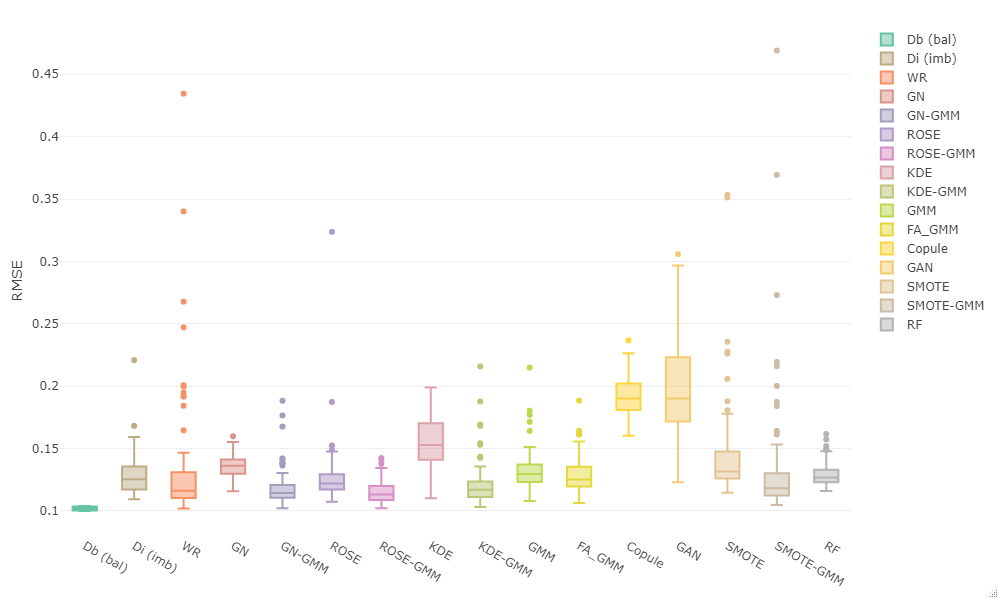

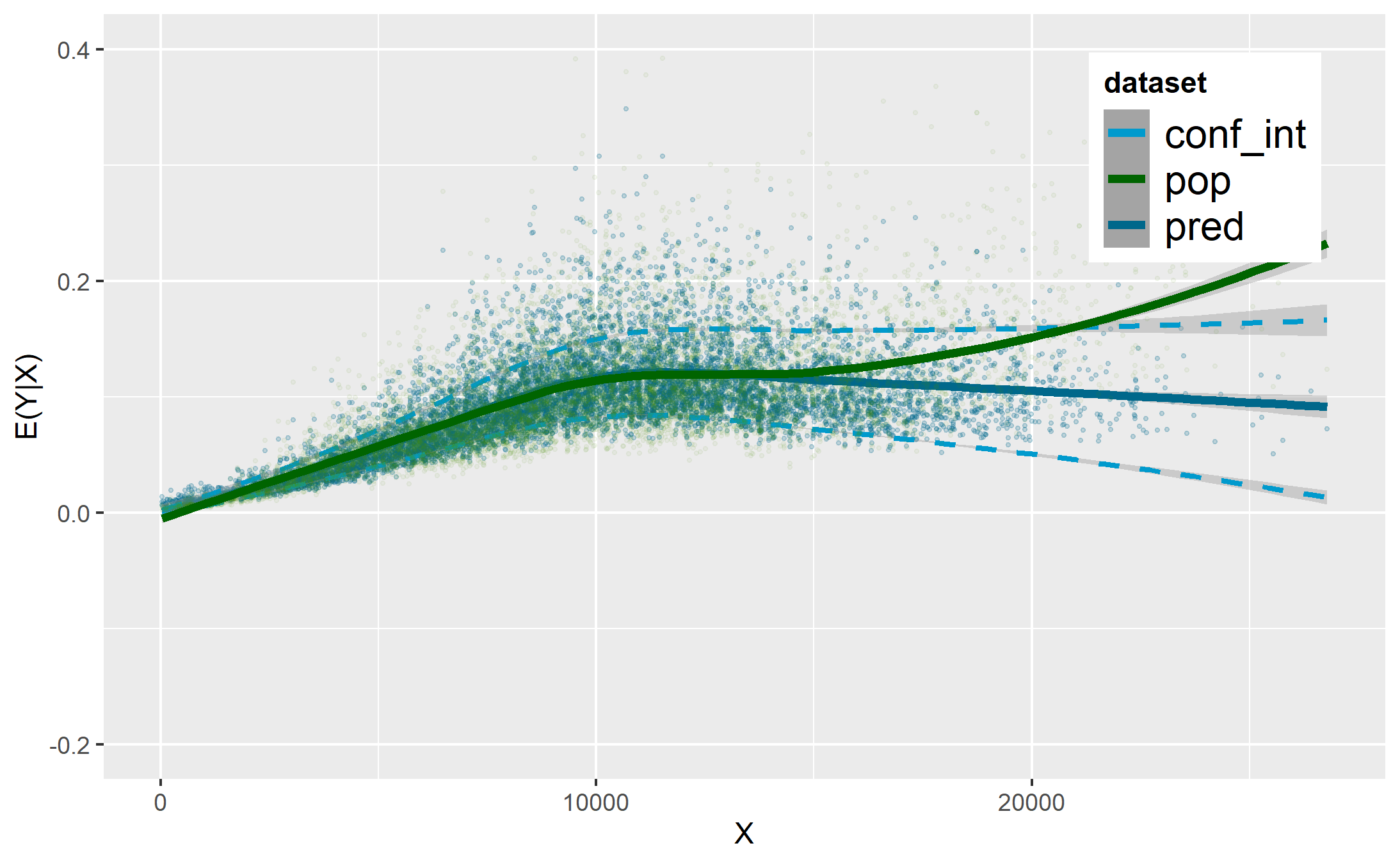

Compared to the balanced training dataset (), we observe, on the different figures, that the predictions with the imbalanced sample () are quite far from the real values on the sides, whatever the model. In addition, we can see the increase of RMSE in Table 1.

3.3.2 Effect of the DA-WR algorithm

Compared to the imbalanced training dataset (), we observe that the predictions with a rebalanced training sample are closer to the real values on the sides except when the random forest is used. Indeed, the random forest algorithm with only one covariate is actually a bagging algorithm. This algorithm generally offers good predictive performance but the predictions on the test sample are constant on the sides and they are not better than the initial.

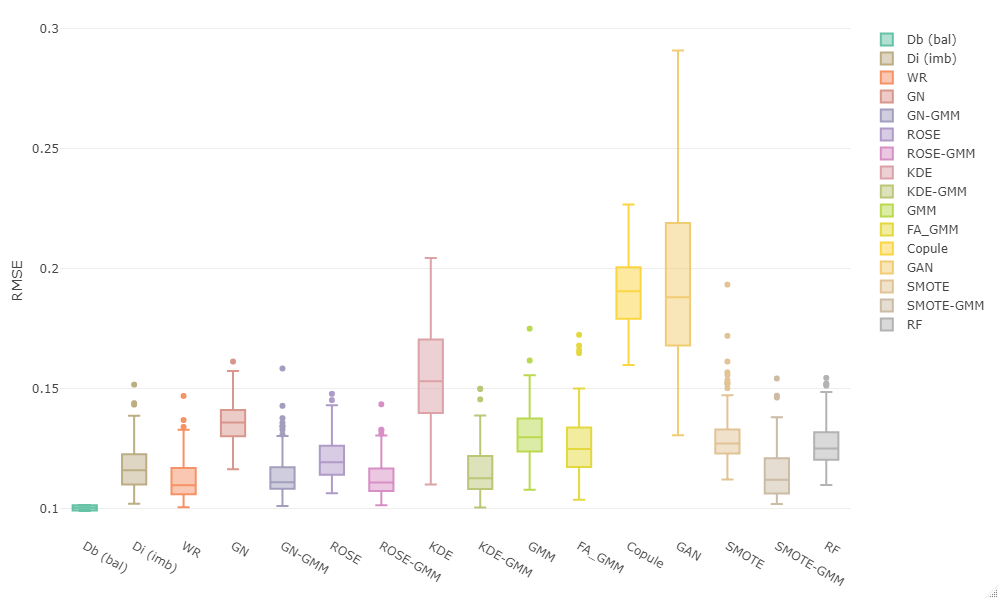

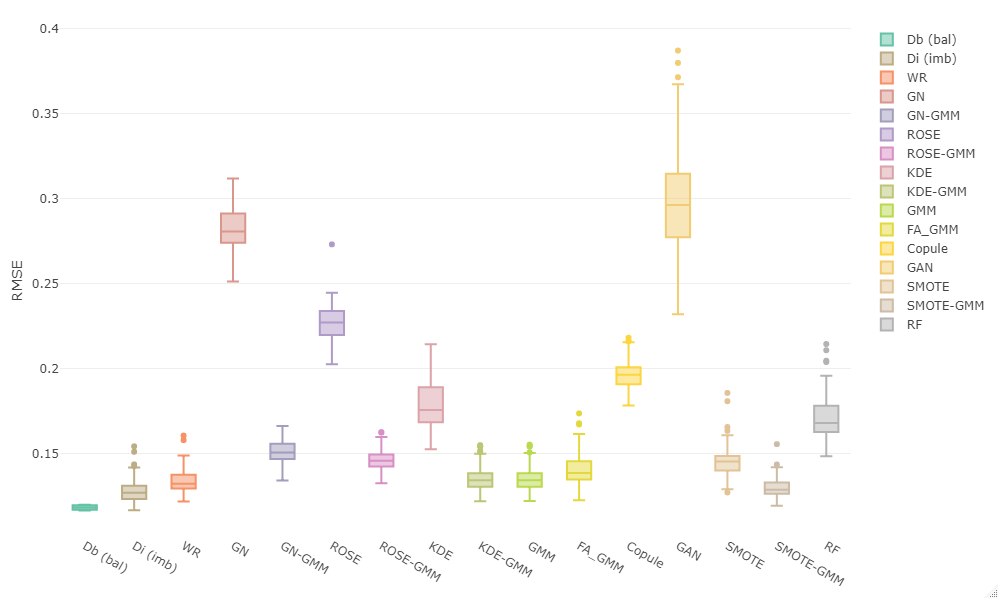

Based on the RMSE given in Table 1, it can be observed that, with GAM and MARS models, some approaches provide better results, especially WR, GN-GMM, ROSE, ROSE-GMM, KDE-GMM and Smote-GMM. However, some other approaches give worse results than the imbalanced sample: Copula at first, KDE (without GMM), GAN, RF and ROSE whatever the model. Others are slightly worse than the imbalanced sample for one of the two models: GN, GMM, Smote and FA-GMM. The clustering seems to improve the results. Even if the interpolation approaches give good results, their data generation technique could be a drawback because of their limit. Finally, the perturbations approach, with a kernel, seems to be effective.

![[Uncaptioned image]](/html/2302.09288/assets/imgs/Illu/recap_RMSE.png)

Figures 10- 12 in the Supplement confirm the previous comments: with some generators, we manage to adjust the sample to provide better predictions, closer to the real values. However, with others, our methodology does not give the expected results.

To avoid a sampling effect and give more robustness to the results, we test our method on 100 imbalanced samples. Figures 14- 16 in the Supplement shows the RMSE boxplot for these multiple simulations. The purpose is to provide a better RMSE (median and range) than the imbalanced sample. We can see that with the GAM model, the WR, GN-GMM, ROSE-GMM, KDE-GMM and Smote-GMM are really well and confirm the previous analysis. The GAN generator is the worst. KDE and copula are also pretty bad. The others are not significantly better than the imbalanced sample. We obtain the same behavior with MARS model but Smote, RF and ROSE are also better than the imbalanced. The results with the RF model confirm these previously obtained with a single simulation: the combined weighted resampling methods do not provide better results on prediction.

4 APPLICATION

4.1 Dataset design

We test our approach on a portfolio of automobile insurance described in a dataset of driver telematics from (So et al., (2021)). This dataset contains 100,000 observations considered as the whole population. The covariates are the driver’s characteristics and some telematic information. Traditional non-life pricing is based on estimating the claims frequencies which represent here our dependent variable .

The imbalanced dataset replicates a real case of sampling bias observed in insurance data, especially by the impact of the imbalanced covariate on the target variable . Typically, the distribution of the covariate in this application is quite asymmetric and we make the tail of the distribution poorer, just by removing some rare observations. We have thus intentionally applied a sampling bias on the datasets in order to obtain a significant impact of the imbalance on the regression.

As in the illustration, we construct different samples as follows. From the initial population, we construct a test sample, denoted by , with a uniform draw. In order to have a training sample independent of the test one, the imbalanced sample, is drawn from the remaining population. The methodology of this drawing is given in the Supplement. We also draw, uniformly, a balanced sample, denoted by , from the remaining population to measure the impact of the imbalanced sample on the predictions.

We aim to obtain a new sample , from the imbalanced one, providing best predictions on . The covariate of interest, that we wish to rebalance, is the total miles driven per year, denoted by . The others covariates are the age of the car, the credit score and the years without a claim. We consider the duration as an offset in our model.

At first, the remaining population is used to estimate the claim frequencies on the test sample. These estimates can be considered as reference values. Next, the claim frequencies are estimated on from the different training samples, the aim being to get as close as possible to the reference values. We evaluate the prediction results on the test sample with the Root Mean Square Error (RMSE) relative to the reference values.

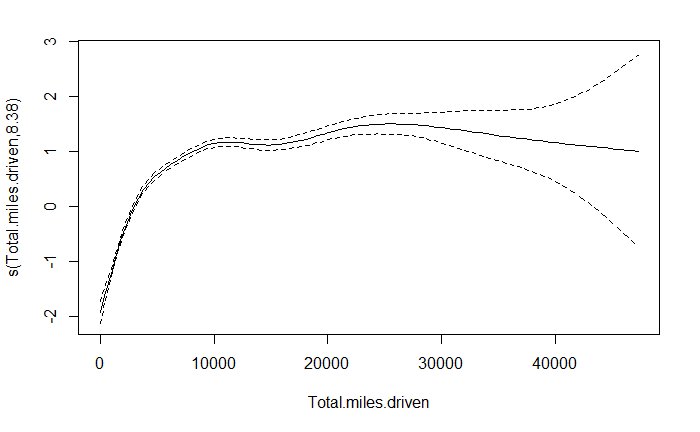

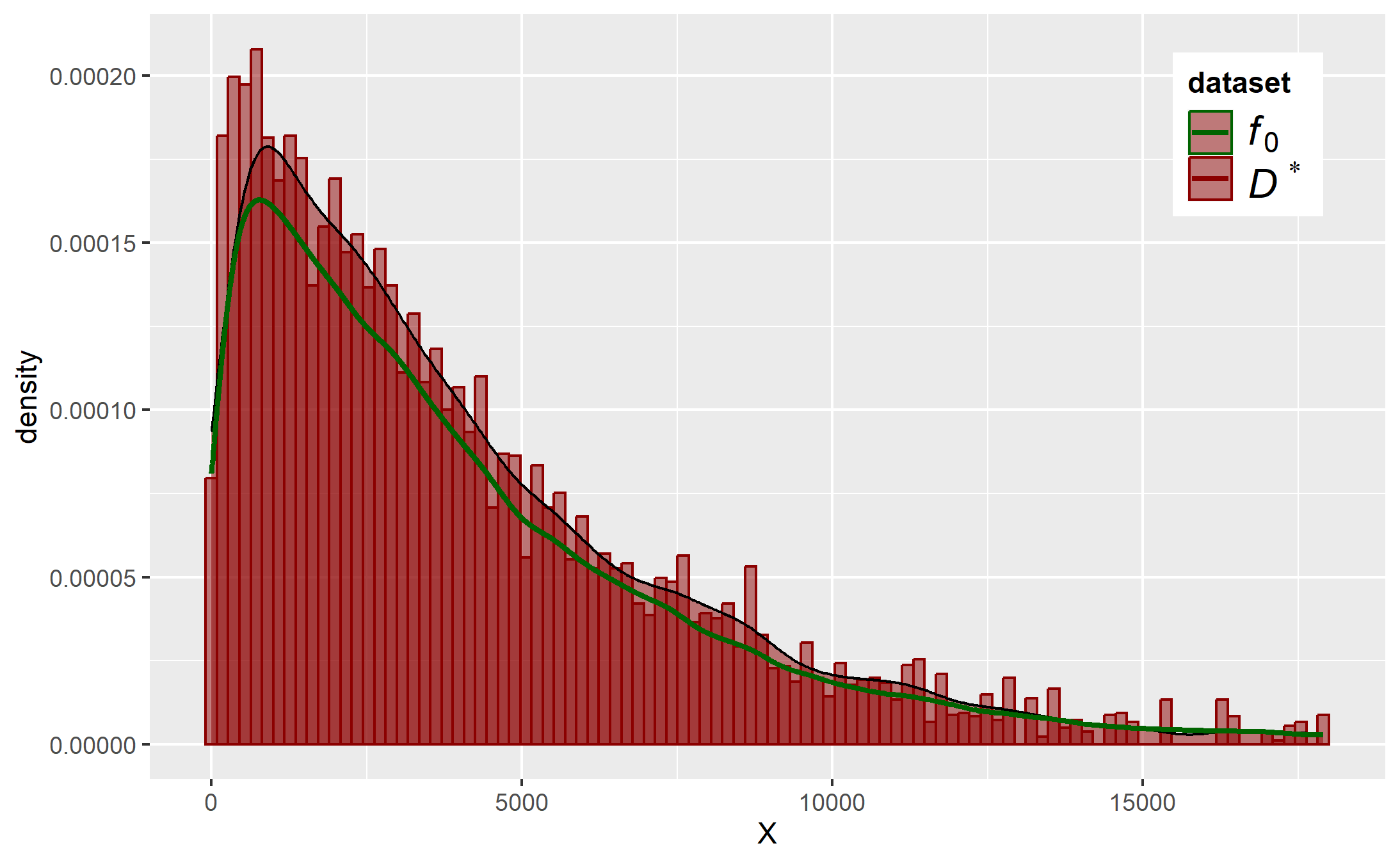

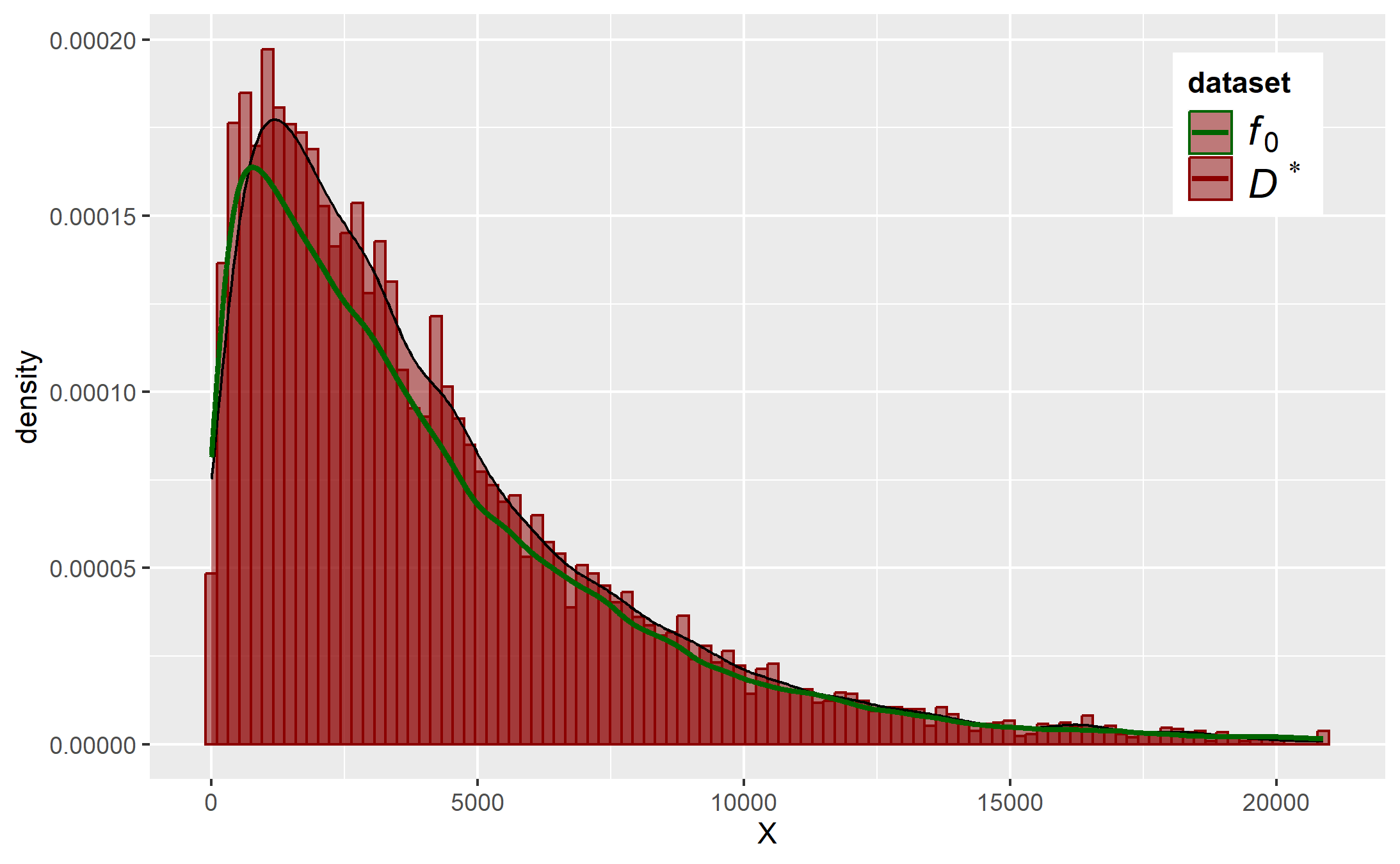

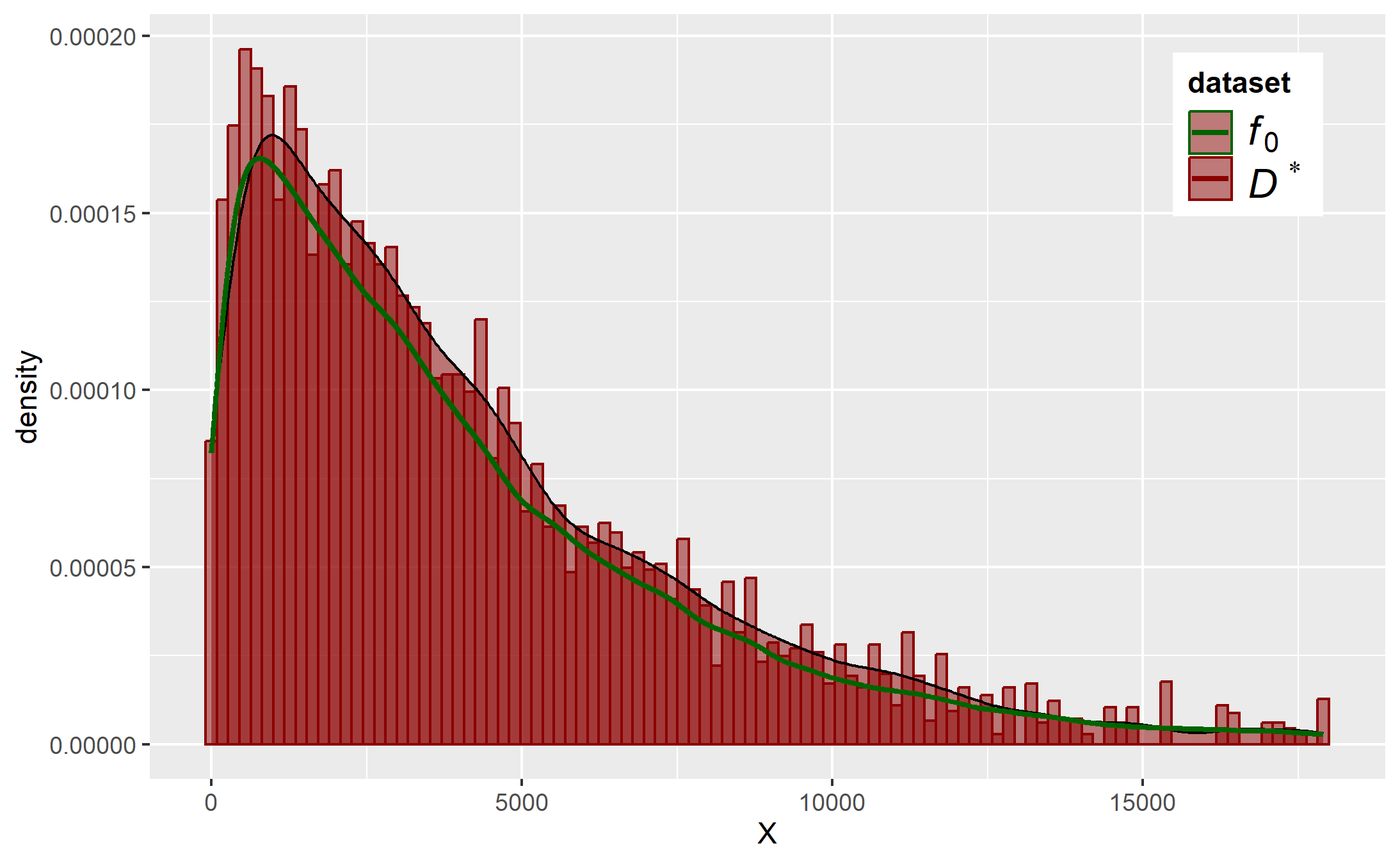

Figure 17 in the Supplement shows the estimated effect of on by the model (based on the whole population). We can observe that this effect increases until around 10,000 miles then becomes slightly constant. We used this information to construct our imbalanced sample.

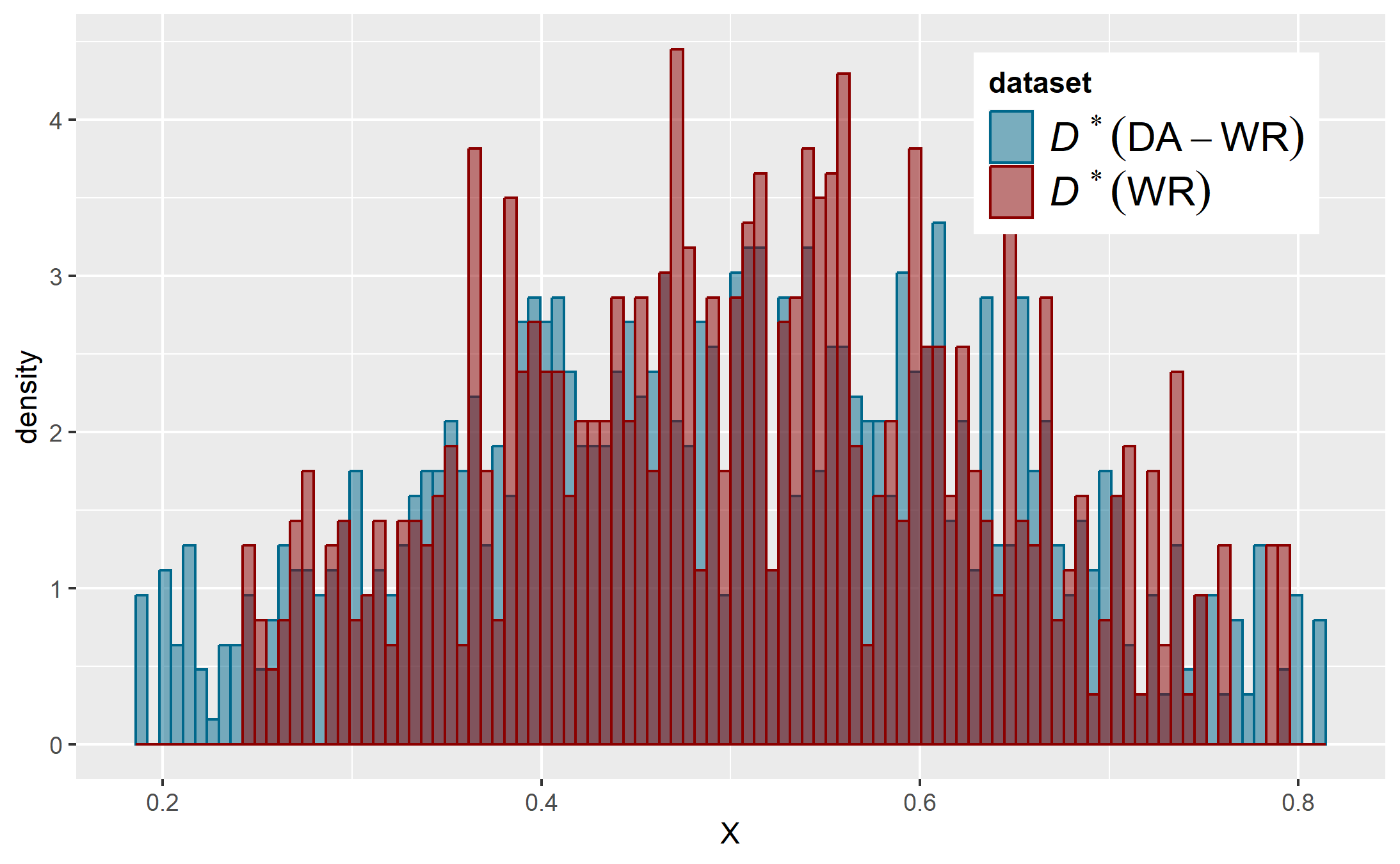

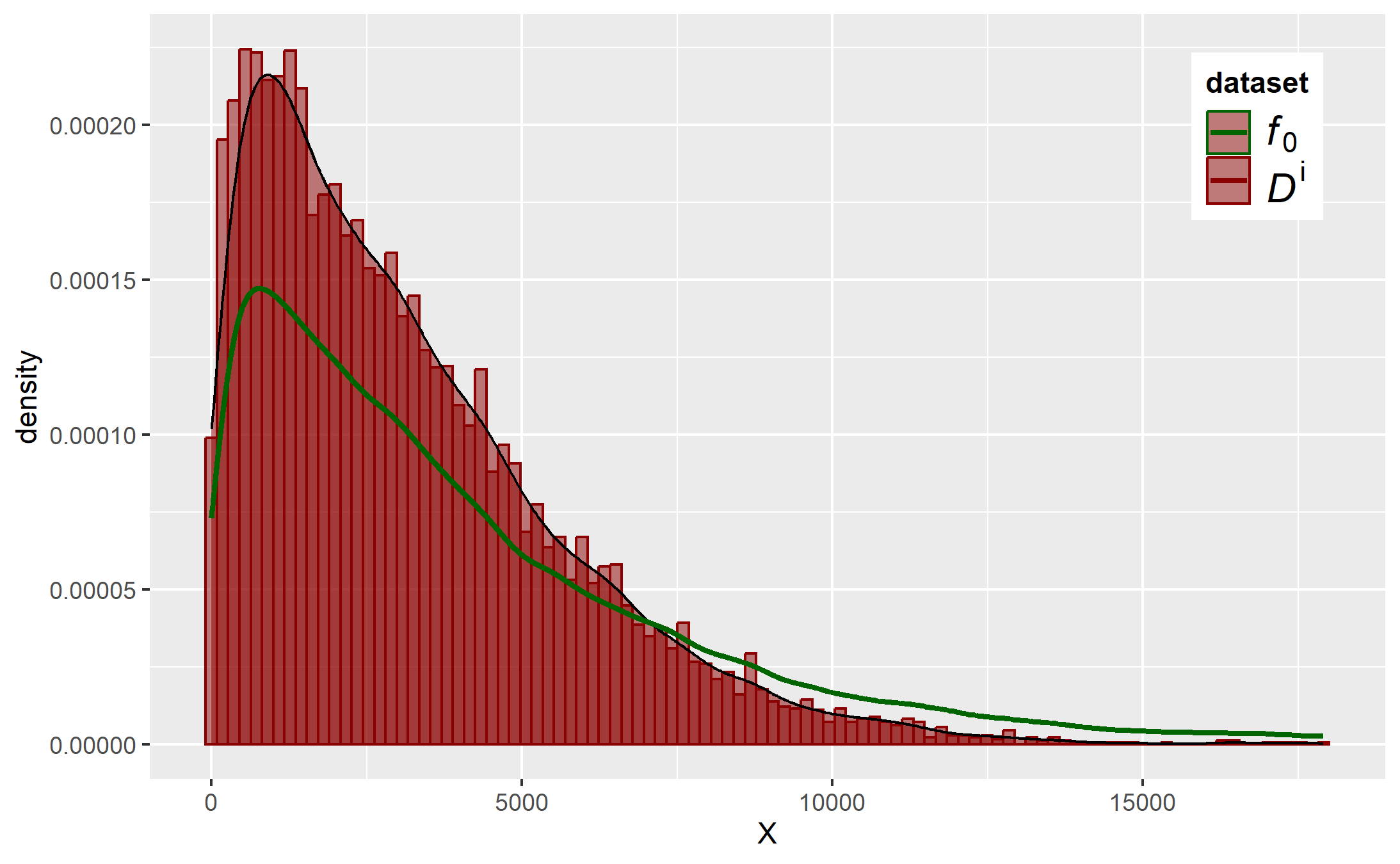

We can observe in Figure 4 the distribution of in the imbalanced sample is not as wide as the population. We can see there are fewer observations over 10,000 miles in the imbalanced sample than population.

4.2 Data generation analysis

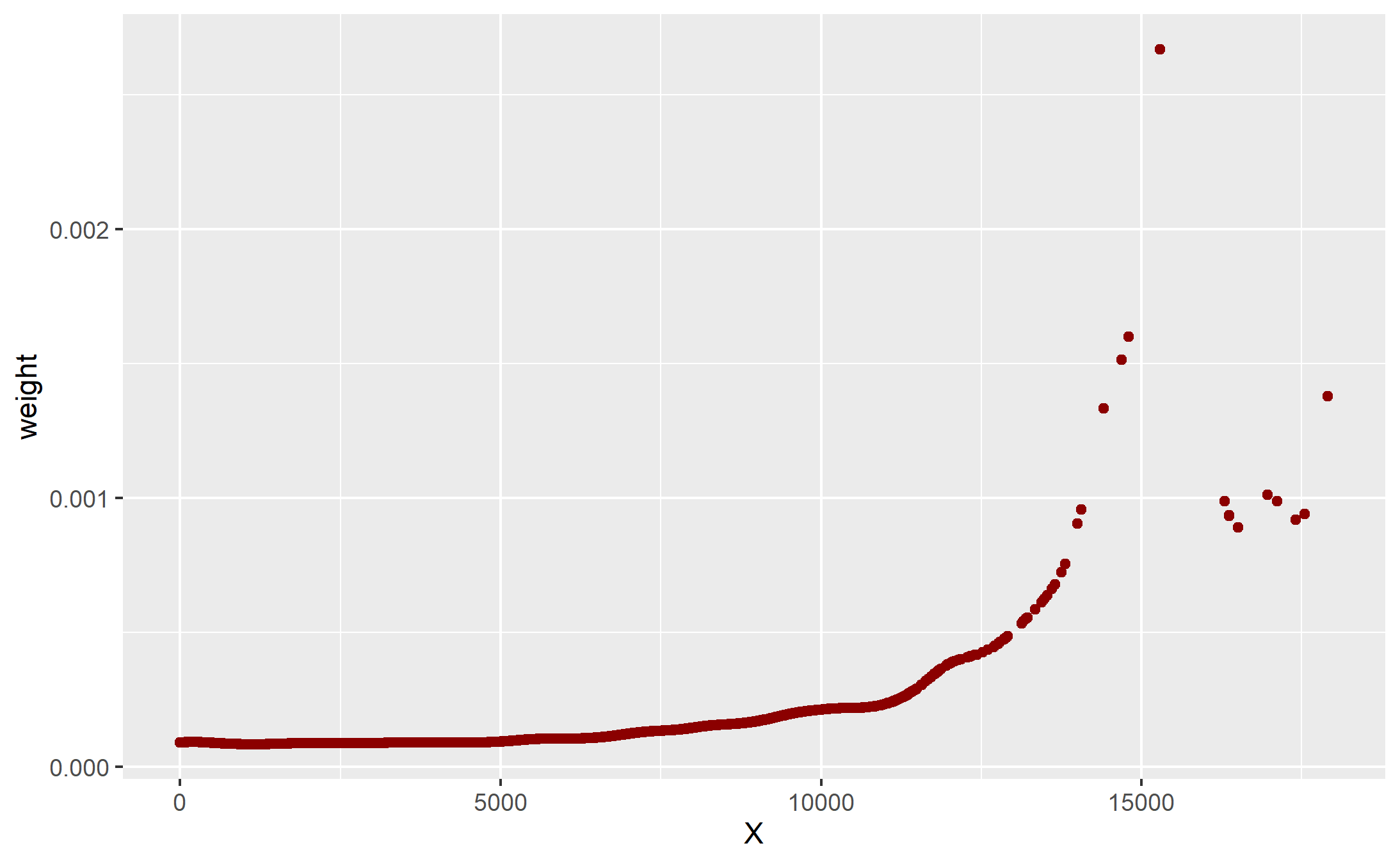

We defined the target distribution from the population with a kernel density estimator. Figure 18(a) in the Supplement, compares the distribution of in with the target distribution. The drawing weights obtained by the WR algorithm are given in Figure 18(b) in the Supplement. We can see that the weights increase with .

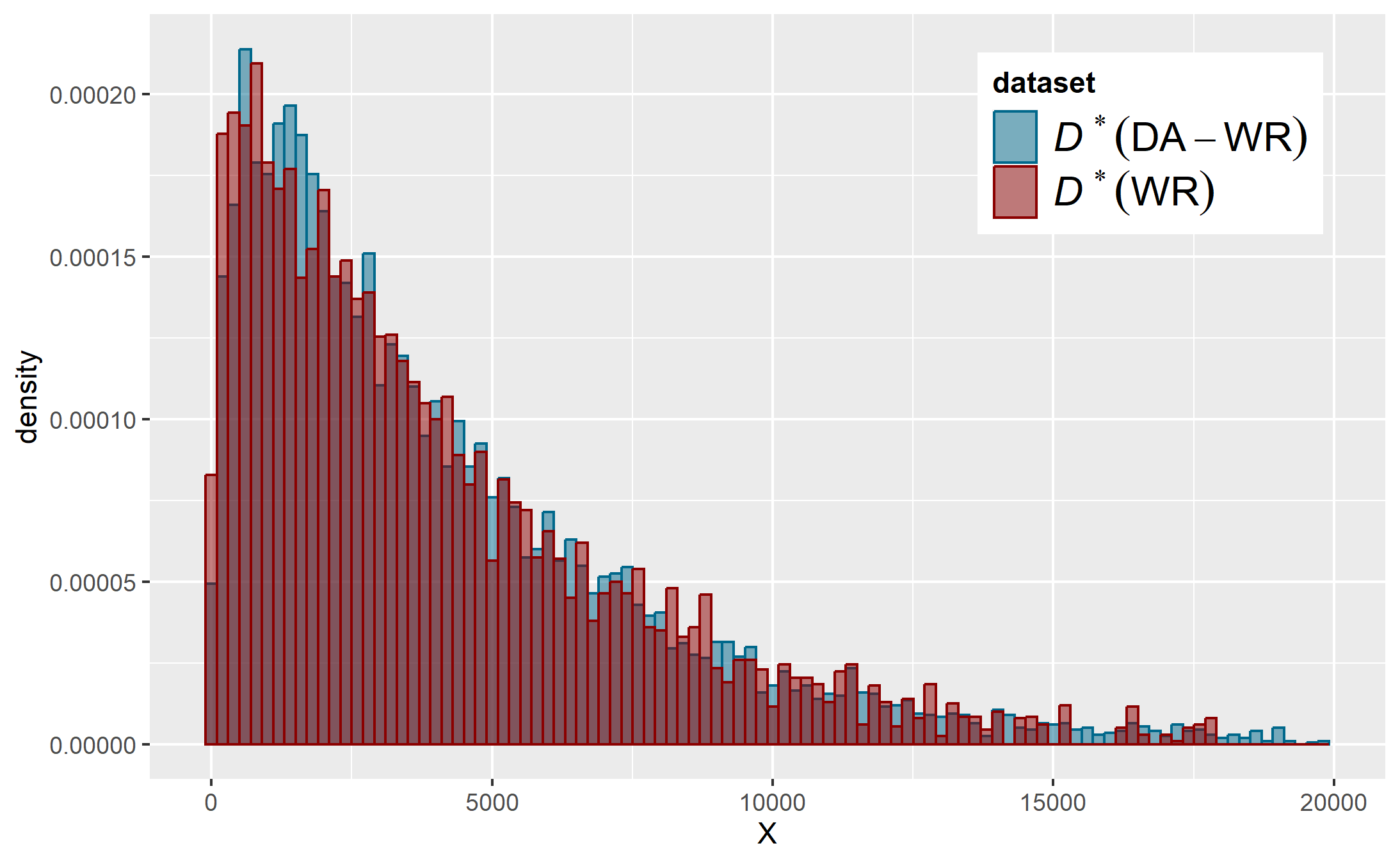

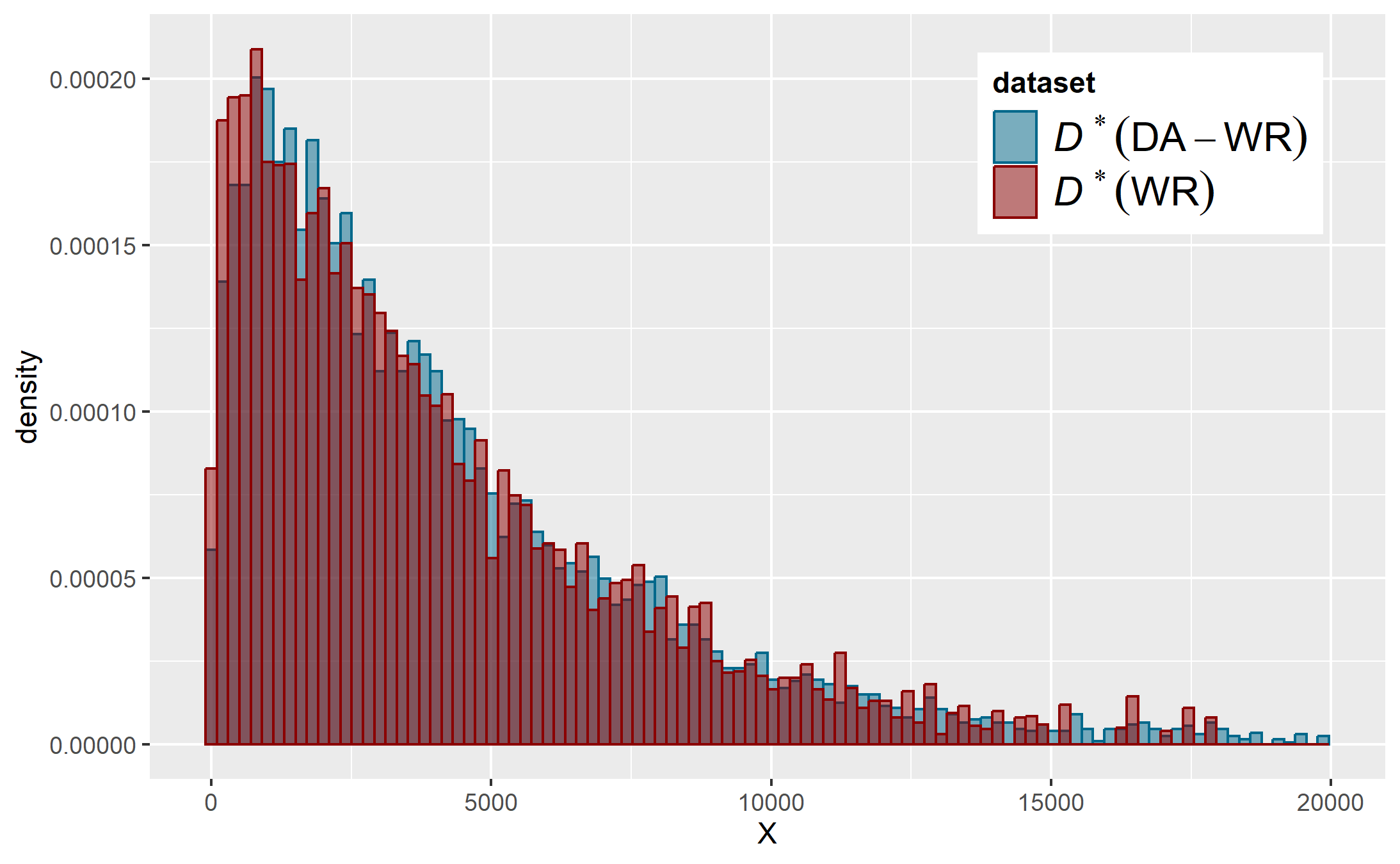

We can compare the WR method with the DA-WR method. Only the generators with the best results are considered. This comparison is done by the different histograms of in versus the target distribution (19 in the Supplement). We also compare these histograms versus the histogram of obtained from the WR algorithm (20 in the Supplement). We note that the data augmentation extends the distribution of (except for the random forest generator) which is closer to the target one. For the distributions of , it can be observed on Figure 22 that is much closer to than .

4.3 Predictive performance analysis

The performance of both WR and DA-WR algorithms are compared on three learning models: a Generalized Additive Model with a Zero-Inflated Poisson distribution for (noted GAM-ZIP), a Generalized Additive Model with a Poisson distribution for (noted GAM-P) and a Random Forest (RF). For the first two models, we apply a regression spline on the insured driver’s age and .

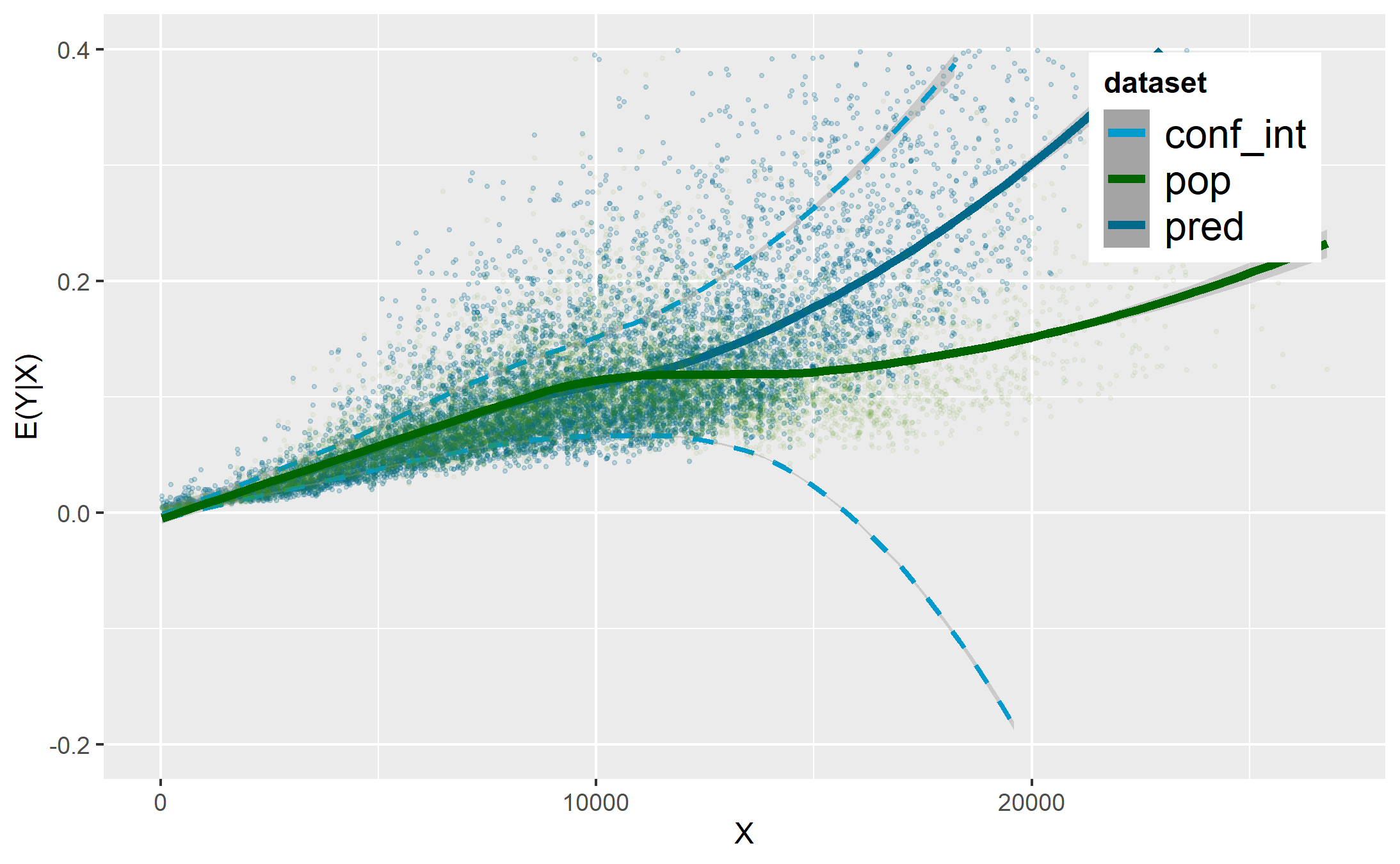

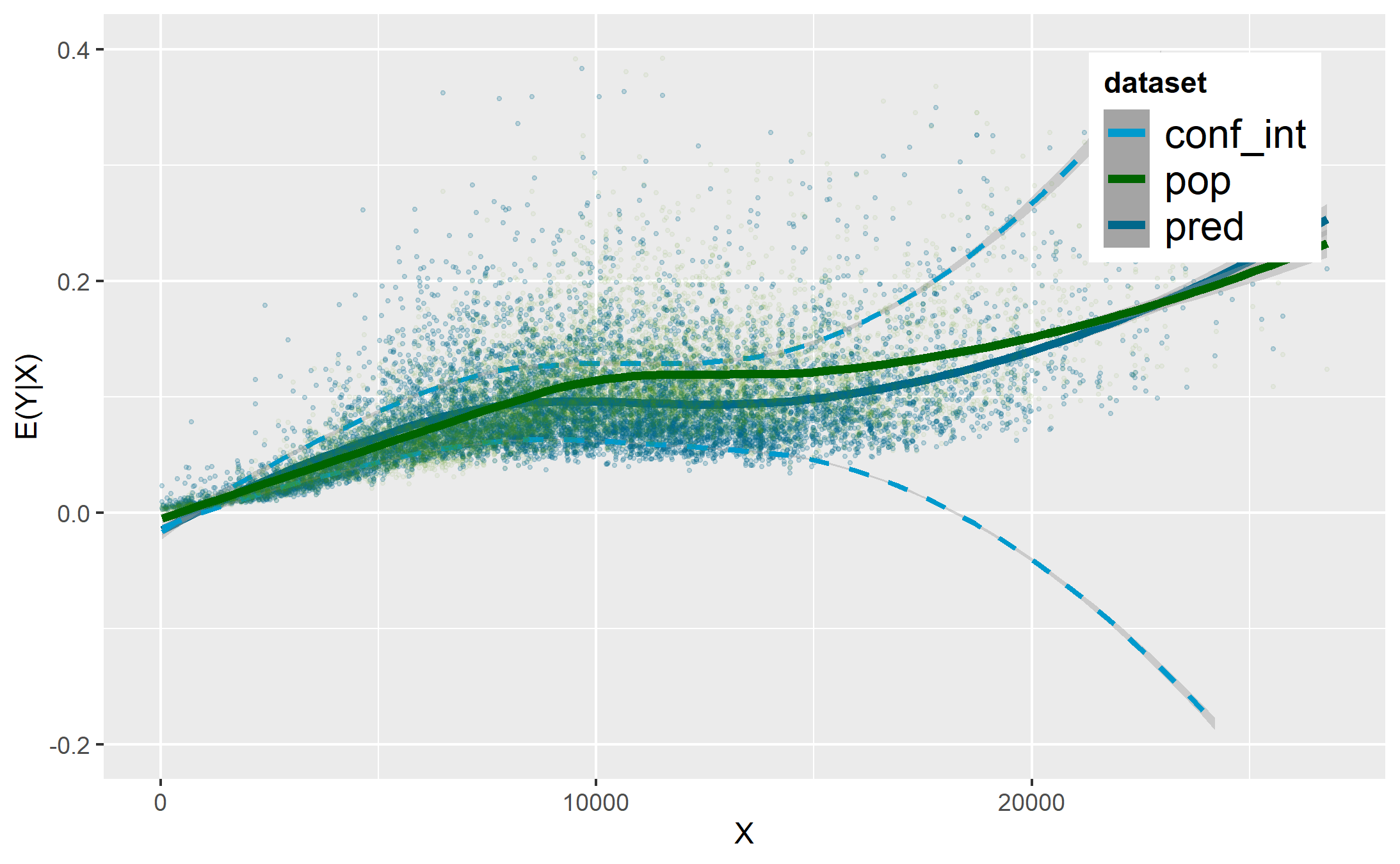

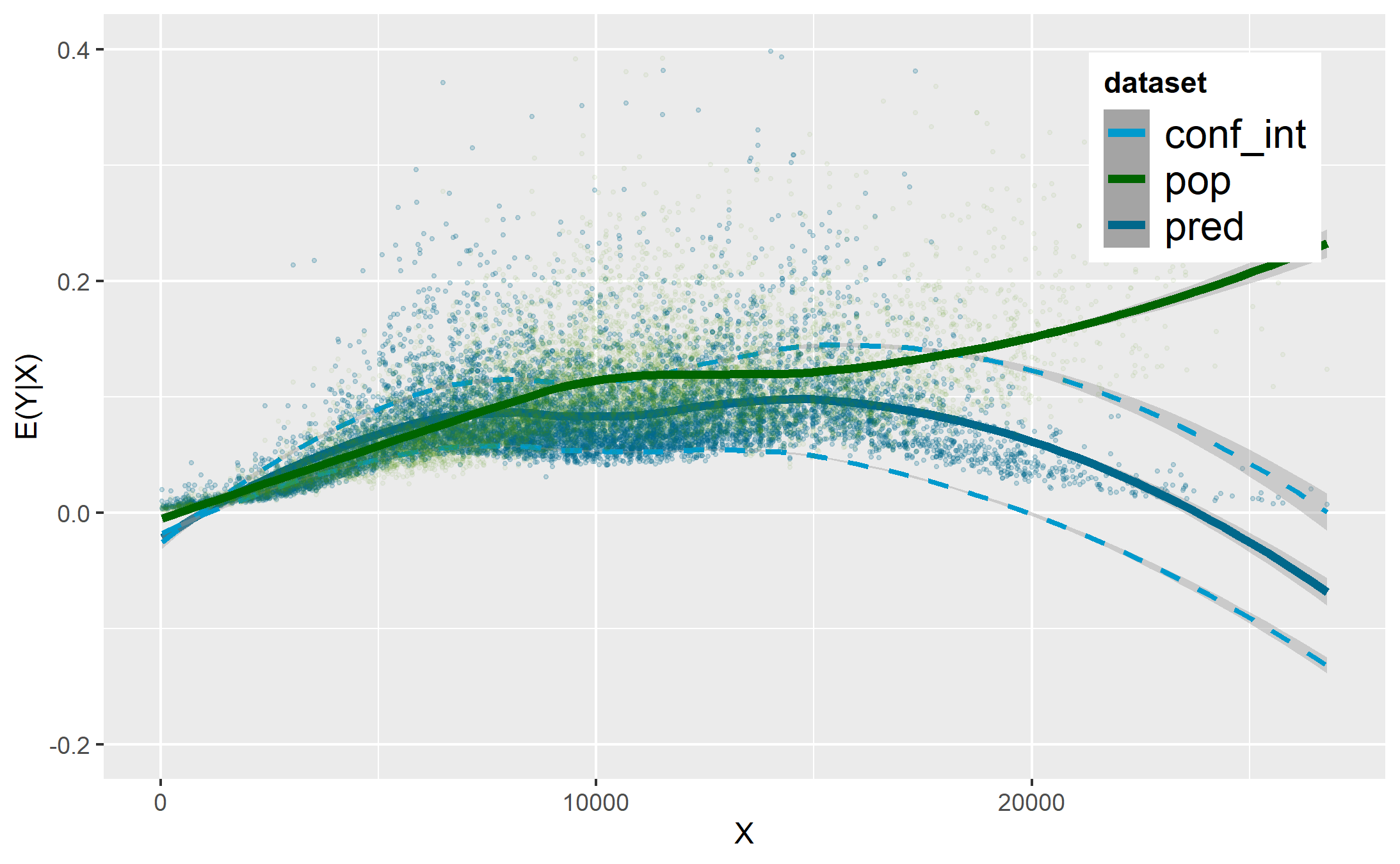

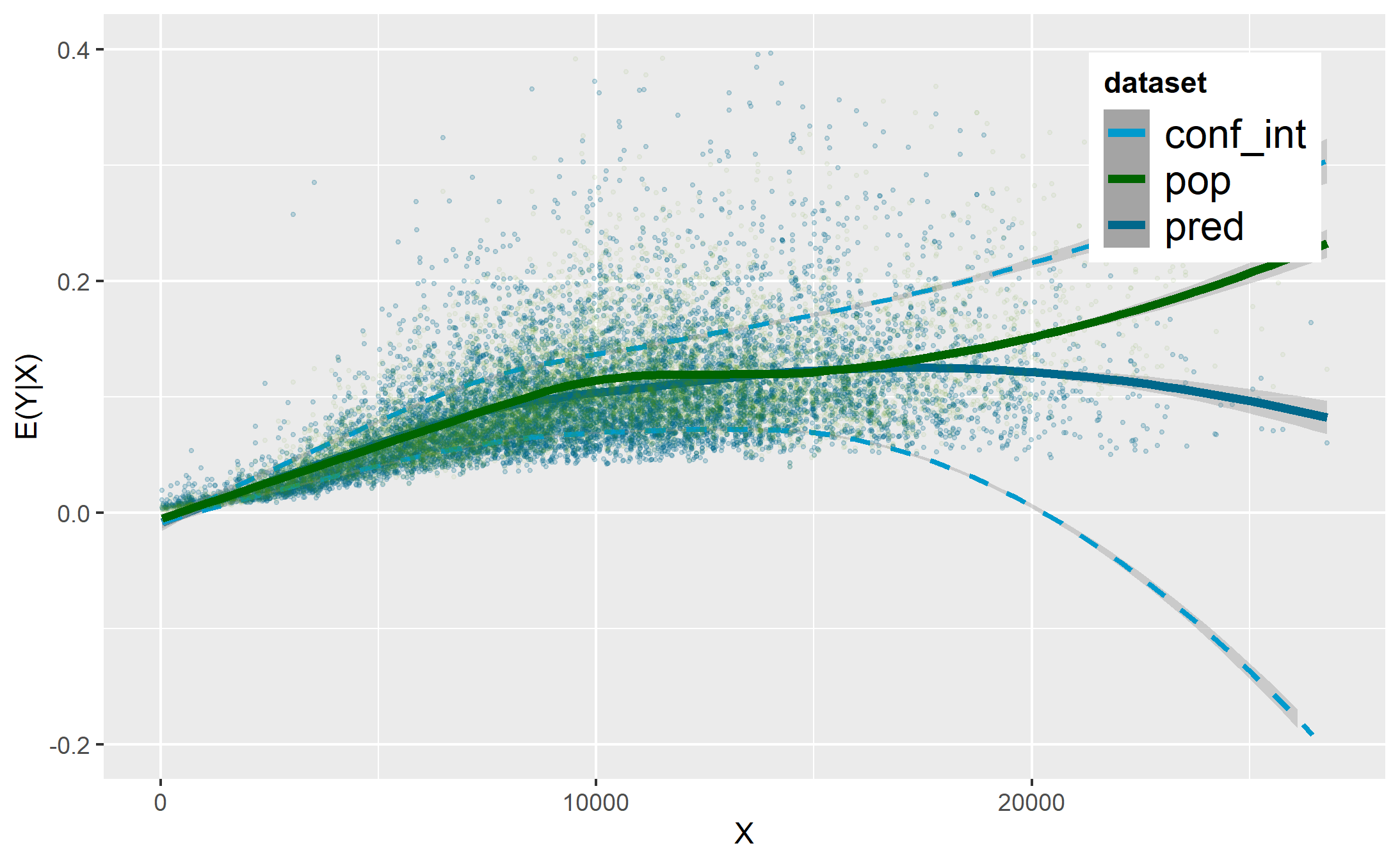

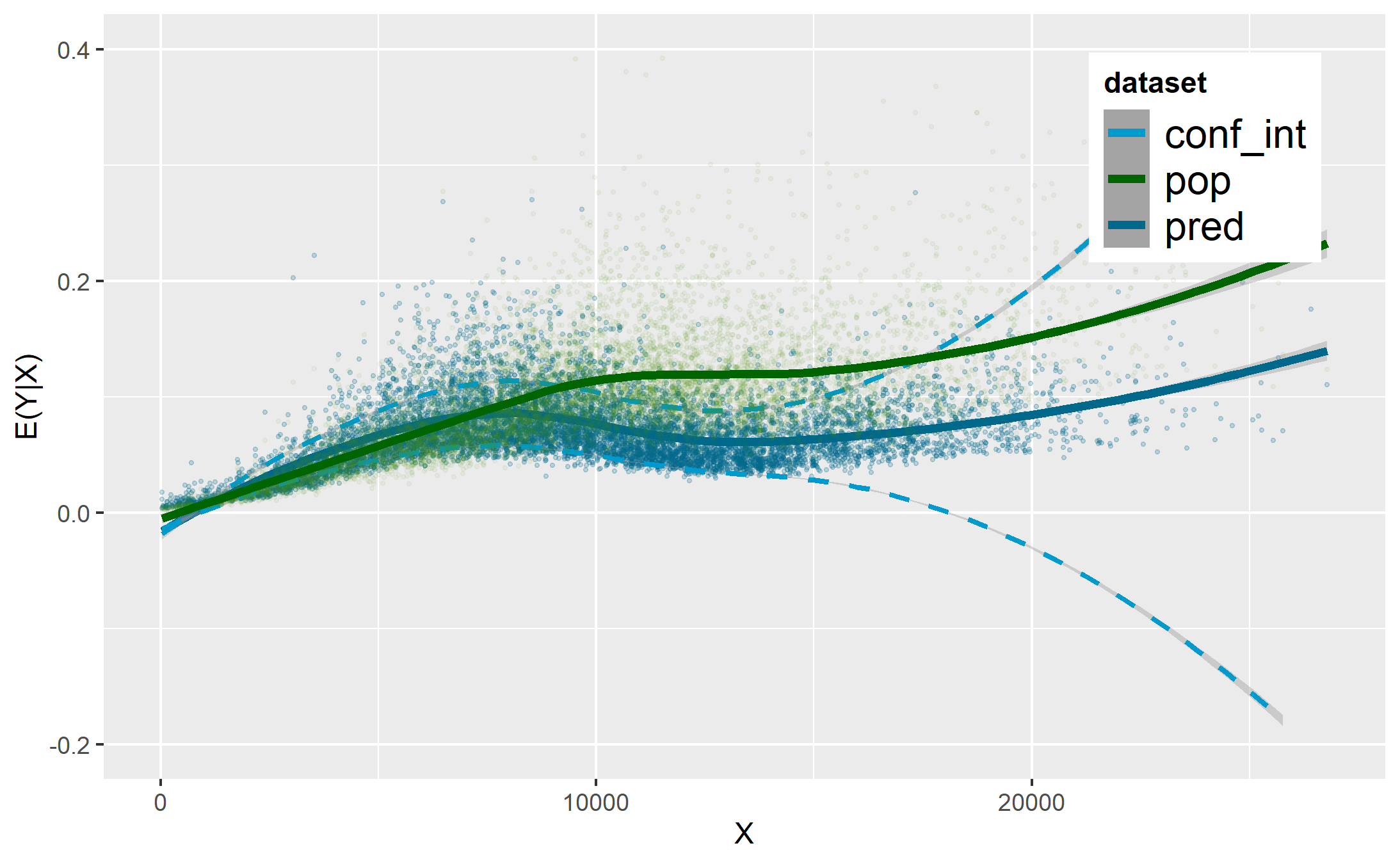

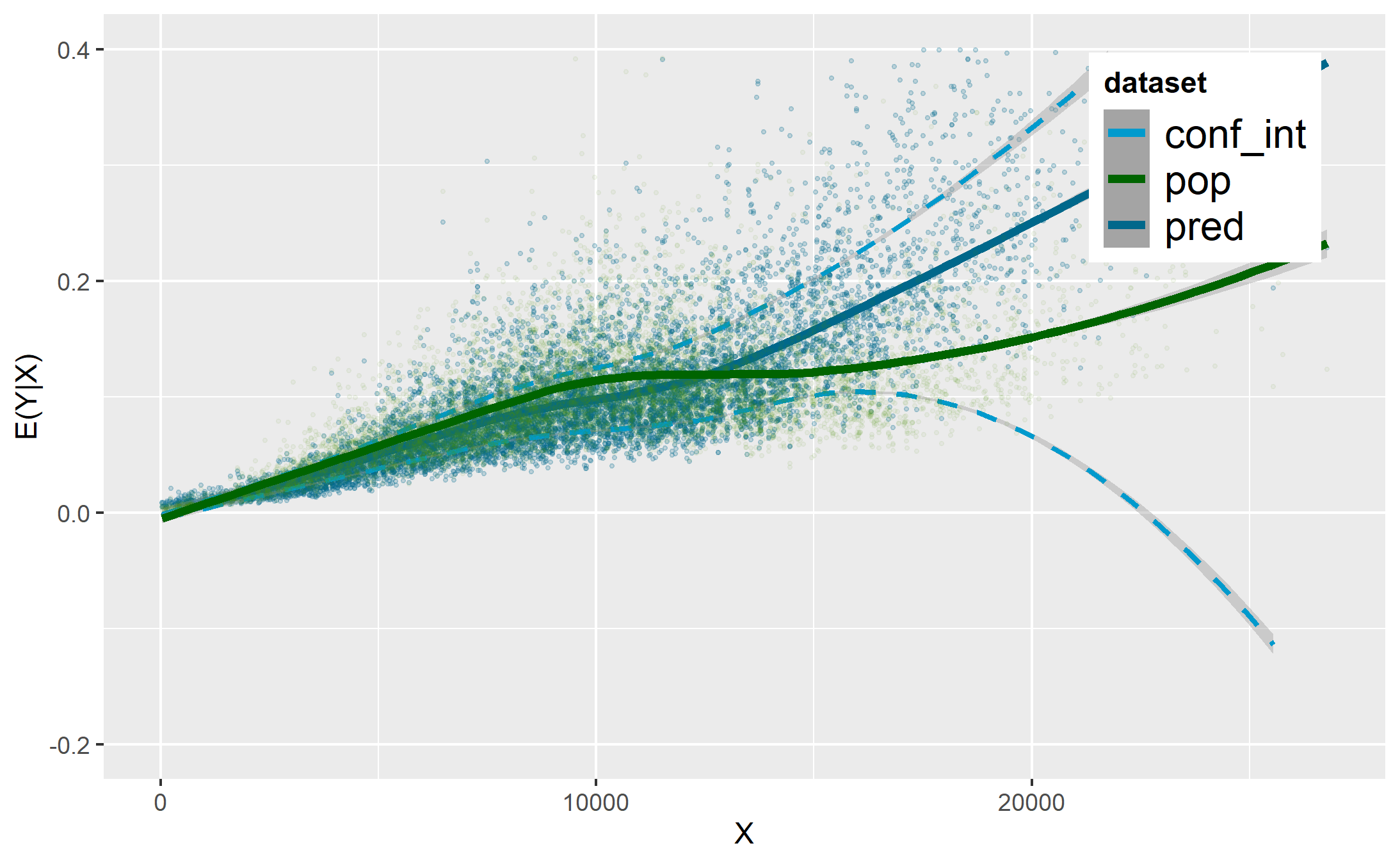

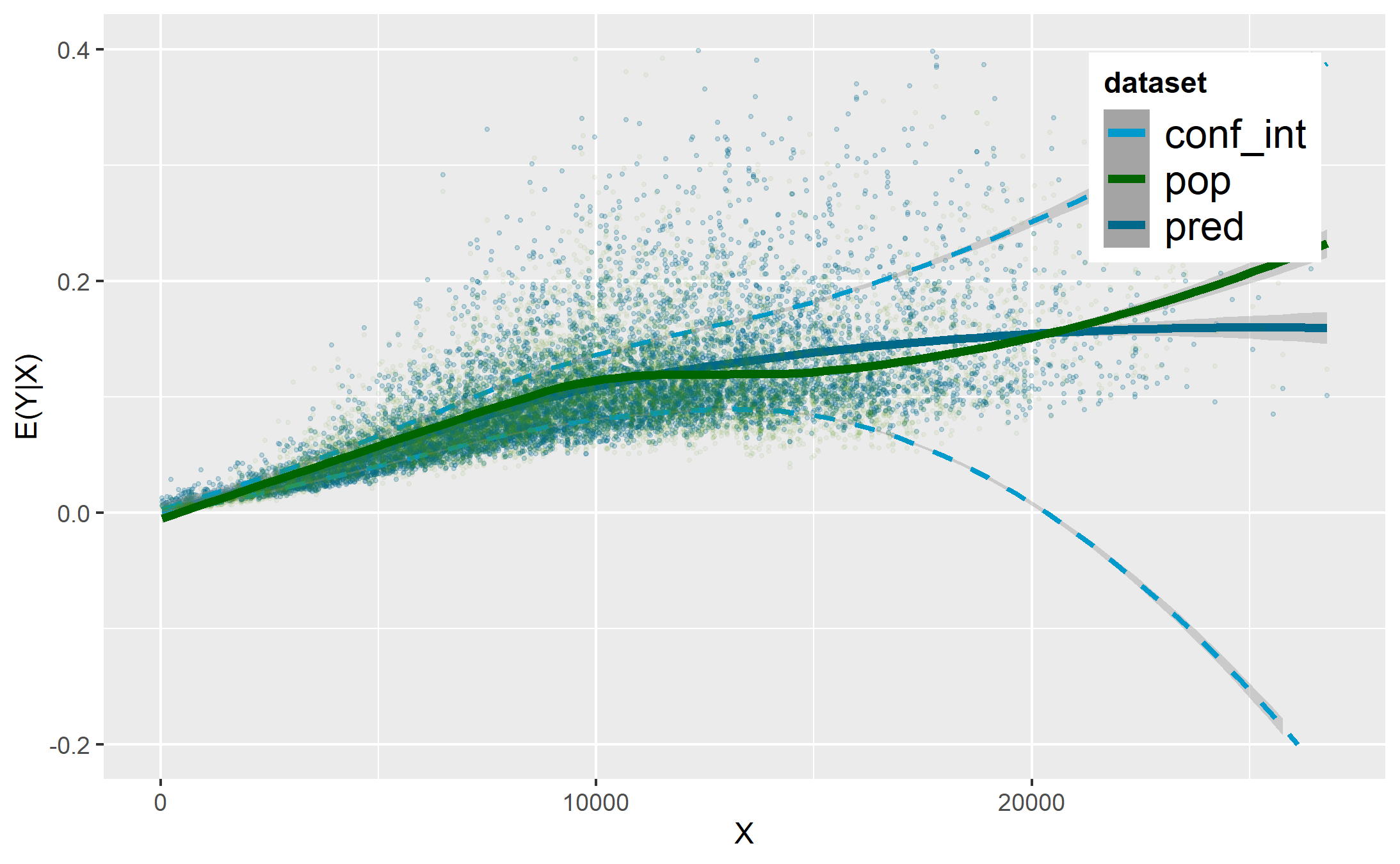

The different predictions obtained with the GAM-ZIP are shown in Figure 21 in the Supplement. Table 4 in the Supplement shows the RMSE for the balanced, imbalanced, WR and best DA-WR samples. These results are summarized in Table 2.

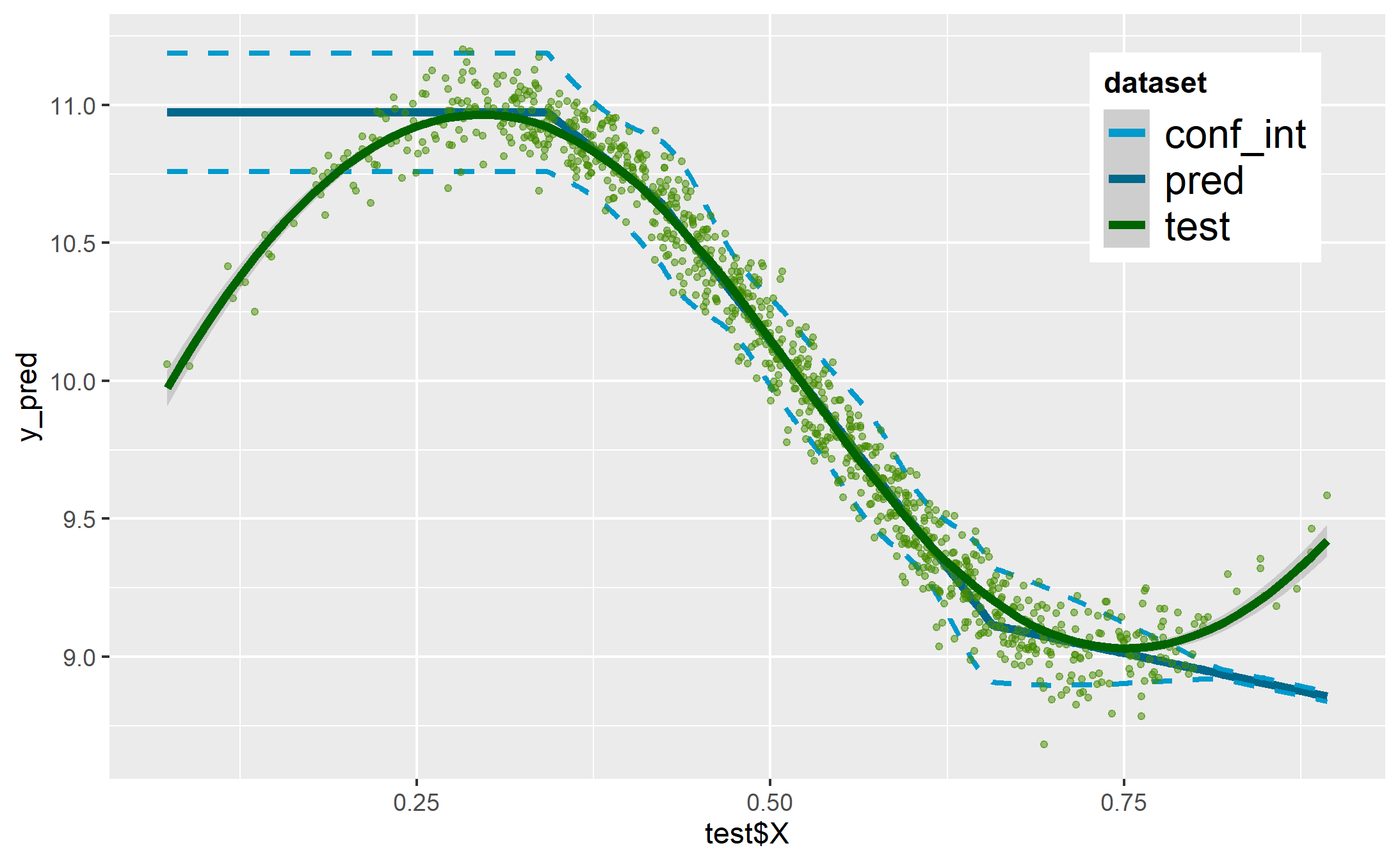

![[Uncaptioned image]](/html/2302.09288/assets/x1.png)

4.3.1 Impact of an imbalanced dataset

The predictions on obtained from are shown in Figure 21 in the Supplement. We can see that the predictions obtained from the imbalanced sample are further from the observed values and that the confidence interval is larger in the distribution tail, whatever model. This result is quantified in Table 4 where it can be observed that the RMSE with is strongly affected compared to .

4.3.2 Effect of the DA-WR algorithm

The WR and DA-WR samples yield much better predictions than . We can also see that the confidence intervals are reduced and that RMSE is reduced for the three models.

5 DISCUSSION AND PERSPECTIVES

The DA-WR algorithm is a new approach to balancing a training sample in an imbalanced regression context. This approach could be used: i) with other types of continuous distributions (e.g multimodal); ii) with multivariate distributions; iii) with other covariates, which would then be treated as the variable of interest , as in the application. The WR can easily be used with categorical covariates but the DA-WR approach depends on the capacity of the DA generator to handle such variables.

Through the illustration and the application, we have seen the potential impacts of an imbalanced sample for prediction with various learning algorithms. The WR algorithm can improve the learning and so the prediction by adjusting the sample to a target distribution. However, the results of the DA-WR approach are naturally dependent of the choice of the data generator. Some of the proposed generators do not provide the expected results. This may be due to the fact that both variables and are generated simultaneously under the imbalanced phenomenon. A local approach based on generators restricted on local parts of the support could certainly improve the DA step, considering more local relation between and and annihilating the imbalanced effect locally.

Moreover, the analyses of the results from multiple simulations show that some generators seem quite sensitive. Then the approach could also be improved by adding a treatment for large values, that is for the extremities of the support of , to avoid an extrapolation of atypical observations.

Eventually, the DA-WR algorithm can be extended to balance simultaneously several covariates, by specifying a multivariate target distribution. It can also be extended to a conditional approach, that is applying this technique within different subpopulations. It could also be extended to mixed data (with possibly a restatement of categorical covariates to get a multivariate target distribution for the covariates of interest) using a DA method dedicated to mixed data.

Acknowledgements

The authors thank the reviewers for their helpful comments which helped to improve the manuscript. This work benefited from the support of the Research Chair DIALog under the aegis of the Risk Foundation, a joint initiative by CNP Assurance

References

- Bowman and Azzalini, (1999) Bowman, A. W. and Azzalini, A. (1999). Applied smoothing techniques for data analysis : the kernel approach with s-plus illustrations. Journal of the American Statistical Association, 94:982.

- (2) Branco, Torgo, and Ribeiro (2016a). A survey of predictive modeling on imbalanced domains. ACM Computing Surveys, 49(2).

- Branco, (2018) Branco, P. (2018). Utility-based Predictive Analytics. PhD thesis, Universidades do Minho, Aveiro e Porto.

- (4) Branco, P., Ribeiro, R. P., and Torgo, L. (2016b). Ubl: an r package for utility-based learning. arXiv preprint arXiv:1604.08079.

- Cattaneo et al., (2021) Cattaneo, M. D., Keele, L., and Titiunik, R. (2021). Covariate adjustment in regression discontinuity designs.

- Caughey and Sekhon, (2011) Caughey, D. and Sekhon, J. S. (2011). Elections and the regression discontinuity design: Lessons from close us house races, 1942–2008. Political Analysis, 19(4):385–408.

- Chawla et al., (2002) Chawla, Bowyer, Hall, and Kegelmeyer (2002). Smote: Synthetic minority over-sampling technique. Journal of Artificial Intelligence Research, 16:321–357.

- Ciolino et al., (2011) Ciolino, J., Martin, R., Zhao, W., Hill, M., Jauch, E., and Palesch, Y. (2011). Measuring continuous baseline covariate imbalances in clinical trial data. Statistical methods in medical research, 24.

- Ciolino et al., (2013) Ciolino, J., Martin, R., Zhao, W., Jauch, E., Hill, M., and Palesch, Y. (2013). Covariate imbalance and adjustment for logistic regression analysis of clinical trial data. Journal of biopharmaceutical statistics, 23:1383–402.

- Efron, (1982) Efron, B. (1982). The jackknife, the bootstrap and other resampling plans. SIAM.

- (11) Fernández, A., García, S., Galar, M., Prati, R. C., Krawczyk, B., and Herrera, F. (2018a). Learning from imbalanced data sets, volume 10. Springer.

- (12) Fernández, A., Garcia, S., Herrera, F., and Chawla, N. V. (2018b). Smote for learning from imbalanced data: progress and challenges, marking the 15-year anniversary. Journal of artificial intelligence research, 61:863–905.

- Flachaire, (2001) Flachaire, E. (2001). Les méthodes du bootstrap dans les modèles de régression. Economie et Prévision, 142:183–194.

- Friede, (2006) Friede, T. (2006). A review of: “selection bias and covariate imbalances in randomized clinical trials, by v. w. berger”. Journal of Biopharmaceutical Statistics, 16(5):757–759.

- Frölich and Huber, (2019) Frölich, M. and Huber, M. (2019). Including covariates in the regression discontinuity design. Journal of Business & Economic Statistics, 37(4):736–748.

- Gupta et al., (2022) Gupta, R., Abdalla, S., Meausoone, V., Vicas, N., Mejía-Guevara, I., Weber, A. M., Cislaghi, B., and Darmstadt, G. L. (2022). Effect of imbalanced sampling and missing data on associations between gender norms and risk of adolescent hiv. eClinicalMedicine, 50:101513.

- Horowitz, (2019) Horowitz, J. L. (2019). Bootstrap methods in econometrics. Annual Review of Economics, 11(1):193–224.

- Kahan et al., (2015) Kahan, B., Rehal, S., and Cro, S. (2015). Risk of selection bias in randomised trials. Trials, 16:405.

- Krawczyk, (2016) Krawczyk, B. (2016). Learning from imbalanced data: open challenges and future directions. Progress in Artificial Intelligence, 5:221–232.

- Lee and Sauchi, (2000) Lee and Sauchi (2000). Noisy replication in skewed binary classification. Computational Statistics and Data Analysis, 34(2):165–191.

- Menardi and Torelli, (2014) Menardi and Torelli (2014). Training and assessing classification rules with imbalanced data. Data Mining and Knowledge Discovery, 28(1):92–122.

- Morgan and Rubin, (2012) Morgan, K. L. and Rubin, D. B. (2012). Rerandomization to improve covariate balance in experiments. The Annals of Statistics, 40(2):1263 – 1282.

- Nowok et al., (2016) Nowok, B., Raab, G. M., and Dibben, C. (2016). synthpop: Bespoke creation of synthetic data in r. Journal of Statistical Software, 74:1–26.

- Patki et al., (2016) Patki, N., Wedge, R., and Veeramachaneni, K. (2016). The synthetic data vault. In DSAA, pages 399–410. IEEE.

- Peng and Ning, (2019) Peng, S. and Ning, Y. (2019). Regression discontinuity design under self-selection.

- Ribeiro and Moniz, (2020) Ribeiro, R. and Moniz, N. (2020). Imbalanced regression and extreme value prediction. Machine Learning, 109:1–33.

- Rubin, (1988) Rubin, D. B. (1988). Using the sir algorithm to simulate posterior distributions. Bayesian statistics, 3:395–402.

- Silverman, (1986) Silverman, B. W. (1986). Density Estimation for Statistics and Data Analysis. Chapman & Hall, London.

- Smith and Gelfand, (1992) Smith, A. F. and Gelfand, A. E. (1992). Bayesian statistics without tears: a sampling–resampling perspective. The American Statistician, 46(2):84–88.

- So et al., (2021) So, B., Boucher, J.-P., and Valdez, E. A. (2021). Synthetic dataset generation of driver telematics.

- Templ et al., (2017) Templ, M., Meindl, B., Kowarik, A., and Dupriez, O. (2017). Simulation of synthetic complex data: The r package simpop. Journal of Statistical Software, 79:1–38.

- Tillé, (2022) Tillé, Y. (2022). Some solutions inspired by survey sampling theory to build effective clinical trials. International Statistical Review.

- Torgo et al., (2015) Torgo, L., Branco, P., Ribeiro, R. P., and Pfahringer, B. (2015). Resampling strategies for regression. Expert Systems, 32(3):465–476.

- Xu et al., (2019) Xu, L., Skoularidou, M., Cuesta-Infante, A., and Veeramachaneni, K. (2019). Modeling tabular data using conditional GAN. CoRR, abs/1907.00503.

- (35) Yang, Y., Zha, K., Chen, Y., Wang, H., and Katabi, D. (2021a). Delving into deep imbalanced regression. In International Conference on Machine Learning, pages 11842–11851. PMLR.

- (36) Yang, Z., Qu, T., and Li, X. (2021b). Rejective sampling, rerandomization, and regression adjustment in survey experiments. Journal of the American Statistical Association, 0(0):1–15.

Data Augmentation for Imbalanced Regression:

Supplementary Materials

Appendix A Synthetic Data Generators

We use the following notations for generators (in the same dorder as on the figures):

-

•

WR: Weighted Resampling

-

•

GN: Gaussian Noise

-

•

GN - GMM: GN applied on GMM clusters

-

•

ROSE: Smoothed Bootstrap, using the proposal of the algorithm ROSE for the bandwidth matrix (Bowman and Azzalini, (1999))

-

•

ROSE - GMM: ROSE applied on GMM clusters

-

•

KDE: Smoothed Bootstrap, using the R-package KernelBoot, The bandwidth matrix being defined according to Silverman’s proposal (Silverman, (1986))

-

•

KDE - GMM: KDE applied on GMM clusters

-

•

GMM: Gaussian Mixture Model, using the R-package MCLUST

-

•

FA - GMM: Factor Analysis, using the python-package Scikit-learn, applied on GMM clusters

-

•

Copula: Gaussian Copula Model, using the python-package Synthetic Data Vault

-

•

GAN: Conditional Generative Adversarial Networks, using the python-package Synthetic Data Vault

-

•

RF: Random Forest, using the R-package SynthPop

-

•

RF - GMM: RF applied on GMM clusters

-

•

SMOTE: interpolation by k nearest neighboors, using the proposal of the algorithm SMOTE

-

•

SMOTE - GMM: SMOTE applied on GMM clusters

Other generators used but not selected because not relevant: SMOTER, SMOGN, some techniques adapted for regression tasks from the R-package Branco et al., 2016b , by defining the weights resampling as relevance function and some previous methods applied on GMM clusters or values of in the application. More details on these approaches are given on F.

Appendix B Illustration results

B.1 On a single simulation

For the illustration, we chose a trimming sequence

B.1.1 Imbalanced sample

B.1.2 Data Generation

Histogram of obtained in new samples vs target

Histogram of obtained in new samples vs WR

Scatterplot obtained in new samples vs imbalanced sample

B.1.3 Predictions

Generalized Additive Model predictions

Random Forest predictions

Multivariate Adaptative Regression Splines predictions

B.2 Analysis of distribution of X

B.3 On multiple simulations

Note: the results for the GAN is slightly worse than for the single simulation because of the lower epoch parameter.

Appendix C Application

For the application, we chose a trimming sequence

C.1 Dataset details

Table 3 provides a brief description of the variables in the dataset, extracted from So et al., (2021).

| Type | Variable | Description |

|---|---|---|

| Traditional | Duration | Duration of the insurance coverage of a given policy, in days |

| Insured.age | Age of insured driver, in years | |

| Insured.sex | Sex of insured driver (Male/Female) | |

| Car.age | Age of vehicle, in years | |

| Marital | Marital status (Single/Married) | |

| Car.use | Use of vehicle: Private, Commute, Farmer, Commercial | |

| Credit.score | Credit score of insured driver | |

| Region | Type of region where driver lives: rural, urban | |

| Annual.miles.drive | Annual miles expected to be driven declared by driver | |

| Years.noclaims | Number of years without any claims | |

| Territory | Territorial location of vehicle | |

| Telematics | Annual.pct.driven | Annualized percentage of time on the road |

| Total.miles.driven | Total distance driven in miles | |

| Pct.drive.xxx | Percent of driving day xxx of the week: mon/tue/. . . /sun | |

| Pct.drive.xhrs | Percent vehicle driven within x hrs: 2hrs/3hrs/4hrs | |

| Pct.drive.xxx | Percent vehicle driven during xxx: wkday/wkend | |

| Pct.drive.rushxx | Percent of driving during xx rush hours: am/pm | |

| Avgdays.week | Mean number of days used per week | |

| Accel.xxmiles | Number of sudden acceleration 6/8/9/. . . /14 mph/s per 1000miles | |

| Brake.xxmiles | Number of sudden brakes 6/8/9/. . . /14 mph/s per 1000miles | |

| Left.turn.intensityxx | Number of left turn per 1000miles with intensity 08/09/10/11/12 | |

| Right.turn.intensityxx | Number of right turn per 1000miles with intensity 08/09/10/11/12 | |

| Response | NB Claim | Number of claims during observation |

| AMT Claim | Aggregated amount of claims during observation |

Figure 17 shows the effect of , total miles driven, on the claim frequency estimated by a GAM model. We can see that, with this model, the claim frequency increases with to about 10,000 miles then becomes quite constant.

As with the illustration, we defined three samples from population of size : balanced, imbalanced and test, all of a size . The test sample is uniformly drawn such as all observations in population have the same drawing weight (). The balanced sample is then drawn uniformly (with a probability equal to ) from the remaining population ( \). The imbalanced sample is defined according to , total miles driven, such as: the larger is the smaller the drawing weight is. We want to get a more asymmetric distribution than the population with fewer observations after 10,000 miles. More precisely, the proposed drawing weight to construct the imbalanced sample is defined by a Gaussian distribution . As we can see on Figure 4, the distribution obtained has very few values above 10,000 miles.

C.2 Imbalanced sample

C.3 Data Generation

Histogram of obtained in new samples vs target

Histogram of obtained in new samples vs WR

C.4 Predictions

Generalized Additive Model predictions

RMSE results

![[Uncaptioned image]](/html/2302.09288/assets/x2.png)

C.5 Analysis of distribution of X

Appendix D Proof of Proposition 2

Proof.

Writing and the cdf associated to the WR and DA-WR procedures, respectively. We have:

which tends to zero and the result follows from Proposition 1. ∎

Appendix E Learning algorithms and evaluation metrics

We evaluate the impacts of the DA-WR algorithm by analysing the predictions of the test sample with three learning algorithms (only the first two for the application): one parametric and two non-parametric:

-

•

GAM: Generalized Additive Models

GAM represent the model class that generalizes the Generalized Linear Models approaches by extending the relationship between the covariates and variable of interest via functions such as . The links between and are thus adjusted. We used the function gam of the R-package MGCV (the function zeroinfl of the R-package PSCL was also tested). -

•

RF: Random Forest

RF is a natural generalization of Classification And Regression Trees (CART). We used the function randomForest of the R-package randomForest. -

•

MARS: Multivariate Adaptative Regression Splines

MARS define a relationship between and using hinge functions in order to capture the non-linear links and variable interactions. Indeed, hinge functions can break the range of X into bins. Then, for each bins, an effect is estimated (by coefficient). We can write that model as: . is the knot number. is a hinge function of and take the following form: or , being a knot (constant). But it can be a product of two or more hinge functions, for example for two degrees of interaction. MARS automatically define variables and knot values of the hinge functions. We used the function earth of the R-package earth.

We evaluate the prediction results of the test sample through the performance indicator Root Mean Square Error (RMSE): . For the illustration, is observed on the test sample and is the prediction obtained with the training sample. For the application, is actually an estimate of prediction. So, we preferred used the estimate of obtained with using the remaining population as and the estimate of obtained with using the training sample as .

Appendix F Data generation methods

Below, we briefly describe the different generators used in the illustration and the application.

-

•

Perturbation approaches: Gaussian Noise and Smoothed Boostrap

The idea of these methods is to simulate synthetic data by adding a noise on the initial observations. At first, an initial observation , called seed, is selected from the WR sample (or from the imbalanced sample by weighting the observations according to the WR method). Then, a synthetic data is generated as follows: . The both methods are slightly different in the generation of the . The Gaussian Noise method assumes , being set by the user and a diagonal matrix , being the estimated variance of in the initial sample. We have . The Smoothed Boostrap method suggests to define according to a multivariate kernel density estimate centered on the seed. The bandwidth matrix is defined according to the proposal of Bowman and Azzalini, (1999), or the proposal of Silverman, (1986), , being the empirical covariance matrix from the initial sample. -

•

The interpolation approaches: k Nearest Neighbors inspired by Chawla et al., (2002)

The purpose of this kind of methods is to create synthetic data by interpolation between two nearest neighbors. At first, an initial observation is selected from the WR sample. One of the nearest neighbors of this seed is then drawn uniformly from the sample: . A synthetic data is generated as follows: . -

•

The latent structure approaches: Gaussian Mixture Models, Factor Analysis

As the kernel density estimate, the Gaussian Mixture Models method suggests to estimate the density and it can be used as a generative data model. The model assumes that the distribution of observations can be specified by a multivariate density defined as a mixture model of: where ; . The mixture model parameters are such as and ; the parameter of the Gaussian distribution . As the method GMM, the Factor Analysis technique allows to obtain a generative data model. This extension of the probabilistic model of principal component analysis proposes to decompose the observations such as where the vector is a latent vector supposed to be Gaussian: ; the paramter of the position (mean) ; the noise term distributed according to a centered Gaussian with a covariance matrix i.e. ; the ” factor loading matrix” allowing to link the latent factor and the data. This model gives the following density form: : . -

•

A copula approach: Gaussian Copula Model Patki et al., (2016)

The Gaussian copula is a distribution function defined on the unit hypercube and built from the multivariate Gaussian distribution. A copula allows to describe the joint distribution function of several random variables based on the dependence of the marginal distributions such as . This model allows also to generate some data from the copula: where is the inverse distribution function of the univariate standard Gaussian distribution ; the joint distribution function of a centered Gaussian and covariance matrix equal to the correlation matrix . -

•

A Conditional Generative Adversarial Networks approach Xu et al., (2019)

A GAN is a technique based on the competition between two networks: the generator, trying to replicate the observations as close as possible, and its adversary, the discriminator, trying to detect if the observations are real or simulated. The competition process allows them to improve their respective behaviors. The allows to apply the method conditionally to a variable. -

•

A Ramdom forest approach Nowok et al., (2016)

The method Ramdom forest consists to train several decision trees on various sets of observations and variables. This technique can be used to generate synthetic observations.