Measuring distribution risk in discrete models

Abstract

Model risk measures consequences of choosing a model in a class of possible alternatives. We find analytical and simulated bounds for payoff functions on classes of plausible alternatives of a given discrete model. We measure the impact of choosing a risk-neutral measure on convex derivative pricing in incomplete markets. We find analytical bounds for prices of European and American options in the class of all risk-neutral measures, and we also find simulated bounds for given classes of perturbations of the minimal martingale equivalent measure.

keywords: Model risk, discrete distribution, convex polytope, discrete pricing models, incomplete multinomial models, risk-neutral evaluation.

1 Introduction

Mathematical models are essential in order to develop quantitative methods in finance that are used, for example, in pricing, risk management and portfolio selection. As a consequence, model risk cannot be ignored and must be quantified. A statistical model in finance has two main ingredients: the distribution of a random source, and a payoff function describing how risk factors impact on the quantities of interest ([1]). In this paper we consider the payoff function as given and focus on what [1] refers to as distribution model risk, that is the risk associated with a wrong choice of a random source distribution.

Distribution model risk aims to quantify the impact on a payoff function of working with a wrong distribution in the class of plausible distributions for a random phenomenon. Given a random variable in a space of random variables , let be a law invariant functional, i.e. if and have the same distribution then ([2]). The functional can be a measure of risk as well as the payoff of a financial derivative. The cost of a wrong choice of the distribution of in a class of plausible distributions for can be measured as the range spanned by across . As a consequence, the identification of a class of plausible alternatives for the distribution of and the ability to find a range for a functional defined on it are the two key issues to address in distribution model risk.

This paper studies distribution model risk for all the cases where the source of risk is a random variable with discrete support included in . As the largest plausible class of discrete distributions for we consider the class of distributions with support included in and with given mean . We therefore do not consider the risk associated with the mean.

The mathematical foundation of this work is the geometrical representation of the class as a convex polytope and the analytical closed form of its extremal points. We provide this representation by generalizing the results in [3]. Furthermore, we find analytical bounds in of a class of functionals commonly used in pricing and risk measurement. The range spanned by a functional across is analytical and is a measure of the distribution model risk associated with the whole class . However, in some cases the class , the range spanned by or both of these are too wide. The geometrical characterization of allows us to overcome these issues by simulation. Indeed, the full characterization of the class allows us not only to simulate from the class, but also to simulate from subclasses properly defined. Given a subclass of plausible alternatives for we can find empirically the distribution across and the bounds in of a wide class of functionals. The problem of defining a proper subclass of alternative distributions to a given does not have a theoretical solution and depends on the specific context. A possible choice that we consider is the one proposed in [1] to take a ball of distributions, defined in terms of relative entropy, centered at .

In this paper we have two applications in mind: the first is pricing in incomplete models and the second is credit portfolio management. The latter application is an extension of the model risk analysis performed in [3], where we relax the assumption of an equally weighted portfolio. Removing the assumption of equal weights, the loss has a probability mass function in . The results discussed here can be used to measure the risk associated with a wrong choice of the joint default distribution. However, we leave the development of this application to future research and we focus on the application to pricing.

When closed form solutions for derivative prices are not available numerical methods have to be used. One method consists of approximating the underlying dynamics. In the classical Cox, Ross and Rubinstein Binomial model [4], the lognormal price dynamics is approximated with a binomial tree. Alternative approximations based on multinomial lattices are proposed, for example in [5], to account for asymmetry and kurtosis of logreturns, as discussed in [6]. Multinomial lattices are workable models used to price derivatives, including exotic derivatives, but they lead to incomplete markets. As discussed in [7] there is a risk associated with the choice of a risk-neutral martingale measure used to price, since a wrong choice results in wrong prices. Our knowledge of the class of discrete distributions allows us to measure the impact on prices of a wrong choice of the martingale equivalent pricing measure in a discrete pricing model. We consider a market with a risky asset and a riskless one and we model the risky asset dynamics with a multinational recombining tree to account for asymmetry and kurtosis in logreturns, as discussed in [6].

Our main result is to find analytical bounds for the prices of convex derivatives in incomplete markets, using the geometrical structure of the class of risk-neutral probabilities. Furthermore, by uniform simulation we can find empirical bounds in smaller classes of plausible choice of risk-neutral measures, for example a class of perturbations of the minimal martingale equivalent measure. We provide explicit analytical bounds for the case of European call and put options and for the more interesting case of American put options. We also provide a first application example on real data.

The paper is organized as follows. Section 2 provides the geometrical representation of the class of discrete distributions with given mean and provides analytical bounds for a wide class of functional . These results are applied to pricing models in Section 3 that provide analytical and empirical bounds for derivative prices in multinomial models. Although the construction of an approximating tree for a continuous model is beyond the scope of this work, Section 4 presents a simple application on real data, where the multinomial parameters are chosen to fit the sample moments of real logreturns. Section 5 concludes and briefly describes the future development of the application to credit risk portfolio management.

2 Distribution risk

This section introduces a measure of distribution model risk for discrete models. According to [1] we are interested to measure the risk associated with uncertainty knowledge of a random variable distribution that belong to a class of plausible alternatives. We focus on discrete models, thus we consider the class of discrete probability mass functions (pmfs) with support in and mean , without loss of generality we assume . If we write , and . Given a pmf in a class of plausible alternatives is defined to be a subclass of , we therefore do not measure uncertainty related to the mean value, that is given. Define to be the set of random variables with support included in . The pmfs are the possible distributions of . Given a random variable , let be a law invariant functional, i.e. if and have the same law -- then ([2]). We consider two different cases: in the pricing application, is a payoff function and, in the portfolio application, it is a measure of risk. We study how the choice of a wrong distribution for in a plausible class of distributions impact on and we build on the geometrical characterization of the class .

We recall that a polytope (or more specifically a -polytope) is the convex hull of a finite set of points in called the extremal points of the polytope. We say that a set of points is affinely independent if no one point can be expressed as a linear convex combination of the others. For example, three points are affinely independent if they are not on the same line, four points are affinely independent if they are not on the same plane, and so on. The convex hull of affinely independent points is called a simplex or -simplex. For example, the line segment joining two points is a 1-simplex, the triangle defined by three points is a 2-simplex, and the tetrahedron defined by four points is a 3-simplex. A complete reference on computational geometry is [8].

In [3] the authors proved that the class is a convex polytope. The following Theorem 2.1 is a generalization of this result and provides the generators of in closed form.

Theorem 2.1.

The class is a convex polytope with extremal points:

| (2.1) |

where , and

| (2.2) |

i.e., any measure has the representation

| (2.3) |

where are the generators of and is their number.

If or there is also

| (2.4) |

Proof.

Let be a discrete probability measure. We have iff

| (2.5) |

with the conditions and . From the standard theory of linear equations we know that all the positive solutions of (2.5) that sums up to one are elements of the convex polytope

where is the identity matrix. The matrix is the row vector of the coefficients. Since then an extremal point of the polytope has at most two non-zero components, say . Therefore the extremal points can be found as the positive solutions of the reduced linear system

| (2.6) |

where we make the non restrictive assumption , therefore . The above system has a unique solution:

We call the extremal points of extremal pmfs or probability measures.

Let , we measure the effect on of the uncertainty about as in [7], by:

| (2.8) |

where and . We denote and .

If for any measurable function the following proposition proves that and are reached on the extremal generators. The proof is similar to the special case in [9].

Proposition 2.1.

If for a measurable function the bounds in (2.8) are attained at two extremal points of .

Proof.

Let .

| (2.9) |

where are the extremal measures and . Therefore is a point in a convex polytope generated by the expectations , thus the maximum and the minimum values of are reached on the extremal points.

∎

If is also convex we can explicitly find the corresponding extremal pmfs. This is important for our main application, where we measure the effect of model risk on convex derivatives (e.g. options) prices. The convex order is necessary to prove one of our main results.

Definition 2.1.

Given two random variables and with finite means, is said to be smaller than in the convex order (denoted ) if

for all real-valued convex functions for which the expectations exist.

The convex order is a variability order, in fact it is easy to verify that implies , and . It can also be proved, see e.g. [10], that

iff and for all ,

where . See [11] for a complete overview on the convex order.

Proposition 2.2.

Let , then

where , , with being the largest smaller than and the smallest bigger than , and .

Proof.

Let . From Proposition 2.1 for any measurable the maximum and the minimum values of are reached on the extremal points. It is therefore sufficient to prove that for any convex and

where and are the extremal measures.

Since by construction, it is sufficient to prove that

We prove that . Let , with support on and let . We consider three cases:

Case 1: . We have and for any and the assert is proved.

Case 2: . Since , we have

where the last inequality follows from direct computations. Then we observe that , thus is decreasing in and

the assert is proved.

Case 3: . If then

for any and the assert is proved. If

| (2.10) |

for any and the assert is proved.

We now prove that . We have

Case 1: . We have and the assert is proved.

Case 2: . As in Case 2 above, we have

Case 3: . If then

∎

We thus have proved that if , where is a convex function and , than

| (2.11) |

The risk associated with the whole class is analytical, because and are analytical, nevertheless using the methodology developed in [9] we can find empirical bounds also on subclasses , as we do in our application to derivative pricing.

3

Distribution risk in discrete pricing models

We consider the effect of model risk on derivative pricing in incomplete discrete markets. As in [7] we consider uncertainty in the choice of the pricing model, specifically we study the risk arising from the choice of an equivalent martingale measure. We consider a market with a risky asset and a risk-free bond with states of the world. We denote the price of the stock at discrete times with by and the risk-free bond price by , where is the single period risk-free rate. The reference historical probability is represented as a vector , , .

After introducing the stock market price dynamics, using the results in Section 2, we find the generators of all the risk-neutral measures defined on the possible states of the world. We have an arbitrage free price for each measure equivalent to in the polytope. Usually, the risk-neutral measure selected to price is the minimal equivalent martingale measure (MEMM), that is unique given . We measure the risk associated with this choice of the risk-neutral measure at three levels:

-

1.

we find the analytical bounds for prices in the whole polytope, that define the maximal admissible prices interval;

-

2.

we find by simulations bounds for prices in the class of plausible risk-neutral measures, i.e. the risk-neutral measures equivalent to ;

-

3.

we measure the effect on prices of small perturbations of the MEMM.

We also provide an illustrative example on real data considering an European style call option. For the simple case of European options we observe that increasing the number of steps the price interval is close to the no arbitrage interval with convex, that is entirely spanned in most of the continuous incomplete models as proved in [12].

3.1 The model

Assume that the stock price process evolves randomly on an state lattice model (i.e., given the price of the stock at time . there are possible future prices that it can take at time ). Suppose that and satisfy then a multinomial recombining lattice can be constructed by taking the possible future states for from as

| (3.1) |

with probabilities , satisfying . In this case, the stock may achieve possible prices at time given by

| (3.2) |

Let now so that we have

| (3.3) |

3.1.1 risk-neutral probabilities generators

A strictly positive probability measure is said to be a risk-neutral probability measure for iff the discounted price process is a -martingale, i.e. for any

| (3.4) |

The no arbitrage condition, i.e. the existence of a risk-neutral probability measure, is , where and . We assume that the market is arbitrage free and therefore an equivalent martingale measure exists. If there are more the two states of the world the market is not complete and the martingale measure is not unique. Theorem 3.1 provides a geometrical representation of the class of all the risk-neutral probabilities as a convex polytope and analytically provides the set of extremal generators.

Theorem 3.1.

Proof.

Let us introduce the random variable with support on and distribution , i.e. and let it be independent of , we can write

| (3.8) |

Equation 3.4 is equivalent to

and

that is equivalent to

| (3.9) |

We call a martingale measure extremal generator (MMEG).

Remark 1.

Theorem 3.1 implies that for the market is complete, i.e. the martingale measure is unique, and we find the Binomial model. For any , the generators of have support on two points. It follows from (2.7) that they are the unique martingale measure of the complete Binomial model with and . The conditions (3.6) are the no arbitrage conditions for each Binomial model. We call the Binomial tree with the risk-neutral measure .

The MMEGs do not depend on the historical probability measure and in general they are not equivalent to the historical measure . In fact, since and are discrete measures, is equivalent to () iff they have the same support. We introduce the family of plausible risk-neutral measures, as the measures in equivalent to :

| (3.10) |

Remark 2.

Notice that is a polytope in , since if and it satisfies two conditions -sum to one and mean. The pmfs without full support are included in lower dimension spaces. In fact if it exists , then , thus the polytope is included in because of the two constraints - sum to one and mean that still remain. As a consequence uniform simulation from or from gives the same results, in fact we have null probability to pick a pmf without full support. We also show that analytical bounds of prices and bounds found by simulation on are very close, for the same reason discussed above.

The simplest example of incomplete lattice model is the trinomial model. We have three states of the world and therefore three states for the model: . Without loss of generality assume . The risk-neutral probabilities are convex combinations of the risk-neutral probabilities associated with Binomial trees. The no arbitrage condition is , thus we have two cases:

Example 1.

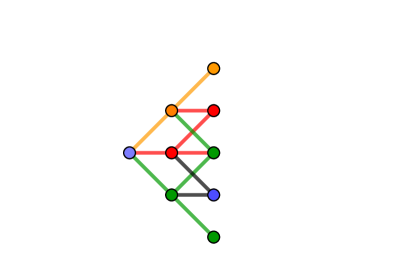

We propose a trivial but explicative example. Let us consider a one step trinomial model, i.e. , with . The support of is and the no arbitrage condition in satisfied. The generators of the risk-neutral probabilities are and . A trinomial recombining tree with the two Binomial generators is shown in Figure 1.

3.1.2 Minimal entropy martingale measure

Derivatives evaluation in incomplete markets requires a criterion to choose a suitable risk-neutral pricing measure. A standard criterion is based on the relative entropy with respect to the historical reference measure .

Definition 3.1.

Let Q and P be probability measures on a finite probability space . The relative entropy of Q with respect to a probability measure P is a number defined as

| (3.11) |

with the assumption that . If and do not have the same support we define .

Remark 3.

The historical measure measure is assumed to have full support, thus the extremal pmfs are not equivalent to and have relative entropy .

Among all the risk-neutral measures we select a measure that minimizes the relative entropy with respect to . Formally, a probability measure is called the Minimal entropy martingale measure (MEMM) if it satisfies

| (3.12) |

To find a minimal entropy measure we have to solve the problem

| (3.13) |

In the multinomial model, under the no arbitrage condition, the MEMM does exist and is unique ([13]). We can determine the MEMM using the method of Lagrangian multipliers [6] and we find:

| (3.14) |

where is the solution of

| (3.15) |

The minimal relative entropy is equivalent to the real world and therefore cannot be reached on the extremal points of the polytope, thus the MEMM is not a MMEG. Nevertheless, using the procedure in [9] we can simulate the distribution of the relative entropy across the class . We measure the risk of selecting the MEMM measure by considering the effect on prices consequent to a perturbation of . We then consider the following class of distributions in :

| (3.16) |

and then we study the price distribution and their range across this class.

Example 1 (continued).

Let the historical probability measure be , the corresponding MEMM is . It holds with . Table 1 provides the minimal relative entropy and the relative entropies of and .

| Measure | Relative entropy |

|---|---|

| 0.0073 | |

Figure 2 shows the simulated entropy distribution across the class of risk-neutral martingale measures equivalent to .

The next Section provides the analytical bounds, and therefore an analytical interval, for prices of convex derivatives in the whole class .

3.2 Analytical price bounds on

Let be a positive function. Suppose there is a contingent claim which pays off an amount at time . Let be the derivative value at time . A no arbitrage price of is given by

| (3.17) |

We can derive bounds for as follows:

| (3.18) |

where is the risk-neutral distribution of corresponding to . Without loss of generality we assume , and (3.4) becomes

| (3.19) |

We define and . Following [7] we define model uncertainty . The following is a corollary to Proposition 2.1.

Corollary 3.1.

In the one-period model the bounds in (3.18) and are attained at two extremal points of .

Let and , they are the maximum and minimum possible prices and therefore any other price, corresponding to a martingale measure can then be expressed by:

| (3.20) |

The two extremal measures are not equivalent to and they generates two Binomial trees. Since we are able to analytically find all the generators, we can also find the maximum and minimum price for each contingent claim as defined above.

Theorem 3.2 is our main results and it provides analytical bounds for prices of convex derivatives in a multi-period lattice model.

Theorem 3.2.

Let and let be a convex function. We have:

where:

with , is the maximum index such that and is the minimum index such that , and

with .

Proof.

Let be the discrete random variables with support and pmf representing the number of jumps down of in a unit time, i.e. , and let be independent for . We have:

We have to prove that

we prove only

because proof of the other inequality is similar. We first prove the result for . For any convex function ,

where is a convex function since it is the composition of two convex functions. We have (since ), and by Proposition 2.2

where , , with being the largest smaller than and the smallest larger than , and . Let ; , we have and by construction and:

where the inequality holds observing that if is convex is convex. Since are i.i.d. by the closure properties of the convex order (see [10]) we have

| (3.21) |

where and are independent, and are independent. We finally have:

where the first and the last equality are by construction and the inequality follows from (3.21). ∎

Corollary 3.2 comes observing that [] is a convex function.

Corollary 3.2.

Let [] be an European put [call] option. Then, for any choice of the strike price the risk-neutral probability that gives the lower price is , where is the maximum index such that and is the minimum index such that , and the risk-neutral probability that gives the higher price is .

Increasing the number of steps the bounds found in Corollary 3.2 goes to the analytical no arbitrage bounds and . This is not surprising, since [12] proved that most of the incomplete models span the whole range of admissible prices by changing the risk-neutral measure and multinomial models are approximating models. For this reason, in our example we will study empirical bounds on a subclasses of , to show how the knowledge of the class allow us to measure the distribution risk associated with perturbation of the risk-neutral measure chosen.

The analytical bounds are more interesting for American options, that are also convex derivatives. American options have the same payoff of European options at maturity , but they can be exercised at any time before maturity, i.e. any , , with payoff . To price an American option one must account for the possible exercise policies. In the simple case without dividends, the value of the American call is equal to that of the European call and holding to expiration is optimal. On the contrary, the optimal exercise policy for American put options is not to hold until expiration no matter what. Therefore, the price of a put option is higher than the price of the corresponding European put. Proposition 3.1 also follows from convexity of the payoff, see [14], and gives analytical bounds for the price of an American put option.

Proposition 3.1.

Let us consider an American put option with maturity and final payoff . Then, for any choice of the strike price , the risk-neutral probability that gives the lower no arbitrage price is , where is the maximum index such that and is the minimum index such that , and the risk-neutral probability that gives the higher price is .

Proof.

Let . Consider the multinomial tree starting in node , for any . Since

| (3.22) |

is equivalent to

| (3.23) |

by Corollary 3.2 the continuation value of the put option satisfies

Thus

for any and the assert is proved.

∎

Example 1 (continued).

Let us consider a call option on . The price of a call option with strike and maturity is bounded by the prices obtained with the Binomial trees , that is , and , that is . All the no arbitrage prices are convex combinations of and that are the upper and lower bounds.The MEMM price is . Figure 3, left side, shows the distribution of prices across .

Consider now ten steps, . The ten periods trinomial model has the above risk-neutral one step probabilities, i.d. the risk-neutral probabilities in the polytope generated by and . According to proposition 3.2 the risk-neutral prices are convex combinations of the two Binomial prices and , that are the lower and upper bounds for a risk-neutral price. The MEMM price is . Figure 3 (right side) shows the price distribution across the class.

We conclude this section with an example with states of the world. This is the simplest case with more than two generators, for this reason we keep Example 2 also to illustrate the distribution risk across and the effect on prices of small perturbation of the MEMM .

Example 2.

Let us keep as in Example 1. Let us consider a one step multinomial model with . The no arbitrage condition in satisfied. The support of is . The generating Binomial trees, their risk-neutral probabilities and the corresponding option prices are in Table 2.

| Binomial tree | Price | ||

|---|---|---|---|

| 0.2062 | 0.7938 | 11.8284 | |

| 0.5822 | 0.4178 | 29.8168 | |

| 0.3437 | 0.6563 | 9.7794 | |

| 0.7375 | 0.2625 | 18.7353 |

The MMEGs and , the MEMM for a reference historical measure with support and the corresponding relative entropies are in Table 3.

| Measure | probabilities | Relative entropy | Price |

|---|---|---|---|

| 9.7794 | |||

| 20.8168 | |||

| ( | 0.0207 | 12.7391 |

The maximum and minimum prices are in correspondence of the Binomial trees and , respectively.

In Theorem 3.2 and Proposition 3.1 analytical bounds are found using two risk-neutral measures that are not equivalent to , since they are extremal and have support on two points and they generate two Binomial trees. Section 3.3 finds the bounds in and empirically shows that the bounds found are close to the analytical.

3.3 Price distribution and bounds on

In this section we look for the bounds in and for the price distribution across , the class of measures in equivalent to . We proceed by simulations, building on the simulation algorithm developed in [9]. We simulate uniformly from and throw out the measures not equivalent to . According to Remark 2 all the randomly extracted from have full support, i.e. they belong to .

Example 2 (continued).

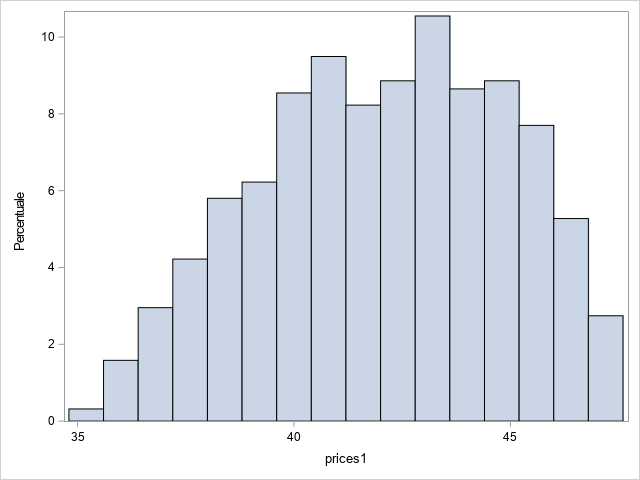

We now consider the class , we recall that: . We first consider one step, i.e. . Figure 4 (left side) shows the distribution of the relative entropy across the class and figure 4 (right side) shows the distribution of prices across the class .

Figure 5 shows the price distribution across the class in a ten step multinomial model, i.e. .

Table 4 gives the MEMM price and the analytical bounds with and, as one can see the simulated bounds across the class of equivalent measures are close to the analytical bounds found on the MMEGs.

| Martingale measure | Price |

|---|---|

| 70.0699 | |

| 31.9443 | |

| 41.3017 |

In this case the analytical bounds given by the no arbitrage condition (check) are and .

3.4 MEMM perturbation: effect on prices

This section develops an example where we measure the risk associated with small perturbation of the MEMM. Also in this case we do not have analytical bounds and we proceed by simulations. In the following continuation of Example 2, we simulate the distribution of prices across the set in (3.16), following the algorithm in [9], reported in Appendix B and find the simulated bounds for prices.

Example 2 (continued).

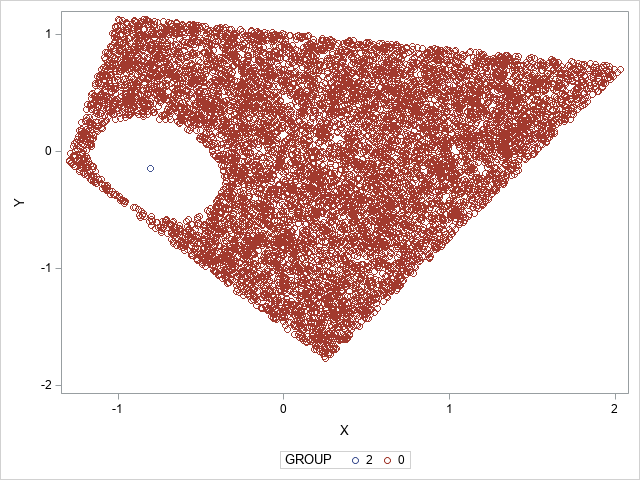

Figure 6 shows the polytope , dots represent uniformly simulated outside the set , that is the white set inside the polytope. The point inside the white ball is .

Table LABEL:tabPriceball exibits (simulated) price bounds on obtained with a one-step and step binomial tree.

| Price N=1 | Price N=10 | |

| max | 15.2084 | 47.3172 |

| min | 10.6699 | 35.2663 |

| 12.7391 | 41.3017 |

Finally, Figure 7 shows the distribution of prices across the class for and steps.

As one can see comparing Table LABEL:tabPriceball and 4, the range of prices spanned on a perturbation of the measure is significantly smaller than the whole range of prices.

4 Example on real data

As a first illustrative application we study the distribution of risk-neutral European call prices and their bounds for a lattice with realistic parameters, i.e. parameters are chosen to match the moments of real asset returns. Empirical study of financial log returns data shows the presence of significant degree of skewness and excess kurtosis. To incorporate such information, higher order lattices are used. We follow [15] to calibrate the pentanomial lattice parameters on the empirical moments of observed log-returns. Let us consider i.i.d. daily log returns

| (4.1) |

To incorporate mean, variance skewness and kurtosis in the price distribution we calibrate the probabilities by solving the five linear equations (2.11) in [15]. Their expression and the corresponding jump amplitudes are in equation (16) in [6]. We report them in Appendix A. Notice that jump amplitudes depend on the kurtosis and not on the skewness of log-returns, while depends on both. This is because the jump amplitudes are assumed to be symmetric by construction. Applying Theorem 3.1 we can find the generators of the polytope of the risk-neutral probabilities corresponding to the pentanomial lattice and consequently we can find the minimum and maximum option prices, the MEMM measure and the corresponding price. We proceed as follows:

-

1.

We find the empirical mean, variance, skewness and kurtosis of daily returns: , , and ;

- 2.

-

3.

we find the MMEGs and the MEMM;

-

4.

we consider European options and we find the minimal entropy price, bounds for the risk-neutral prices of call and put options in the whole class of martingale measures and in a class of perturbation of the MEMM and - for years- the call price distribution across the class;

We consider daily logreturns of Moncler S.p.A. (MONC.MI) on FTSE MIP Market Index from November 10, 2017 to November 10, 2022, with a total of 1270 daily observations. The empirical daily mean, variance, skewness and excess kurtosis are reported in Table 6.

| 0.0006 | 0.0005 | 0.1019 | 4.4305 |

We have . We choose the annual rate , we consider four maturities years and K=22. Since the only purpose of this application is to show how the methodology applies with realistic numbers, we construct a simple toy example. Each step is one year, so we have steps. For we have the one-period model and we use annualized parameters to find the jump amplitudes and the historical probability. Then we show the results we can obtain in a -period model simply considering years. We provide as a benchmarks in Table 7 the Black and Scholes put and call prices.

| Call Price | Put Price | |

|---|---|---|

| 3.3025 | 2.7031 | |

| 4.9826 | 3.3509 | |

| 6.3034 | 3.7009 | |

| 7.4272 | 3.9011 |

The jump amplitudes obtained from the annualized empirical mean, variance, skewness and excess kurtosis are in Table 8.

| 2.3817 | 1.6667 | 1.1664 | 0.8162 | 0.5712 |

The no arbitrage condition is satisfied with . The historical probability is in Table 9.

| 0.0829 | 0.1656 | 0.5029 | 0.1658 | 0.0828 |

The MMEGs and the corresponding risk-neutral European call and put prices for (one-period tree) are in Table 10. The call price bounds on the whole polytope are and , the analytical no arbitrage bounds are and .

| Measure | Probabilities | Call Prices | Put Prices |

|---|---|---|---|

| (0.1493,0,0,0.8507 ,0) | 4.1666 | 3.5809 | |

| (0.2645,0,0,0,0.7355) | 7.3789 | 6.7932 | |

| (0,0.2749,0, 0.7251,0) | 3.6382 | 3.0524 | |

| ( 0,0.4371,0,0,0.5629) | 5.7849 | 5.1991 | |

| ( 0,0,0.677,0.3323,0) | 1.9847 | 1.3990 | |

| ( 0,0,0.8045,0,0.1955) | 2.3915 | 1.8057 |

Table 11 provides the MEMM probability . The binomial trees () corresponding to the minimum and maximum price are shown in Figure 8.

| 0.0816 | 0.0877 | 0.4860 | 0.2440 | 0.1637 |

Now, for we find the MEMM prices and compare them with the analytical bounds of the entire in Table 12.

| T | -call | Min-call | Max-call | -put | Min-put | Max-put |

|---|---|---|---|---|---|---|

| 3.1245 | 1.9847 | 7.3789 | 2.5387 | 1.3990 | 6.7932 | |

| 4.6914 | 2.9518 | 8.3910 | 3.1079 | 1.3684 | 7.3474 | |

| 5.9427 | 3.8658 | 10.6681 | 3.4090 | 1.3321 | 8.1344 | |

| 7.0503 | 4.8386 | 12.4926 | 3.6117 | 1.3999 | 9.0539 |

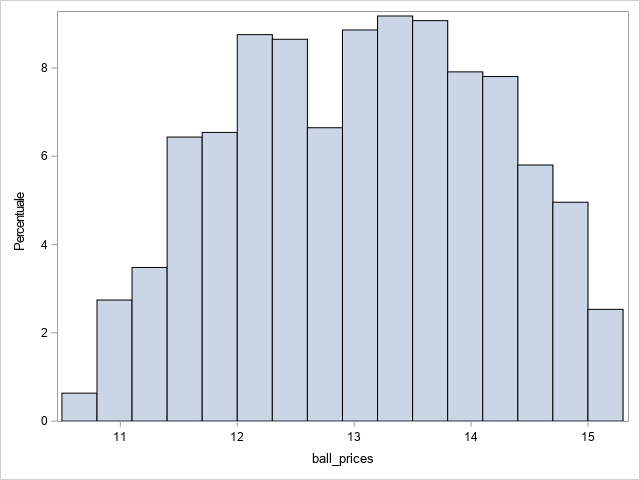

It is evident that the range of admissible prices is quite large and therefore in practice it could be more useful consider the range of prices in a class of perturbations of . We define a class of measures in with relative entropy with respect to smaller than . To choose we look at the distribution of the relative entropy across , that is shown in Figure 9. The maximal simulated relative entropy is , the minimal is . We choose that corresponds to the of the range spanned by the entropy across .

Table 13 provides the maximum and minimum call prices on the set of MEMM perturbations , i.e the class of equivalent martingale measures whose relative entropy with respect to is smaller that .

| T | Max call price | Min call price |

|---|---|---|

| 1 | 4.2224 | 2.5973 |

| 2 | 6.0540 | 3.8092 |

| 3 | 7.4961 | 4.9400 |

| 4 | 8.7721 | 5.9766 |

Table 13 shows that even small perturbation of the risk-neutral measures have an impact on prices. However, comparing Table 13 and Table 12 the range spanned by prices across is significantly smaller than the range spanned across the whole class. Properly define the class of plausible alternatives could be informative in real world application.

5 Conclusion and future research

The geometrical representation of discrete distributions with a given mean presented here improves our knowledge of discrete models. In this paper, we show its usefulness for measuring model risk in discrete models and we develop a first application to pricing of derivatives: we consider the model risk that arises from a wrong choice of the risk-neutral measure used to price derivatives in incomplete markets, among a class of plausible alternatives.

Part of our ongoing research is devoted to another application of the geometrical structure of discrete models. We are generalizing the model risk analysis performed in [3] to the case of unbalanced portfolios. Consider a credit portfolio with obligors. The components of random variable are the default indicators for the portfolio and we assume that they have the same Bernoulli marginal distribution with mean : no assumptions are made on their dependence.

To model the loss of a credit risk portfolio of obligors we consider the sum of the percentage individual losses

where and . If we assume that the weights are given we can measure the risk associated with the distribution of joint defaults. In fact, we can move the distribution of leaving its mean and its support fixed. Let the class of discrete distributions of the losses for a given .

Definition 5.1.

Let be a random variable representing a loss with finite mean. Then the at level is defined by

The case of equal weights has been discussed in [3], where analytical bounds for the VaR are reached on the extremal points. In this special case the relevant quantity is the number of defaults, a discrete distribution with support on . The results discussed in Section 2 allow us to consider unbalanced portfolios and, given the weights that define the support of the loss, we can measure how by changing the joint distribution of defaults in a given class we affect VaR of the loss, according to (2.8), that in this case becomes:

| (5.1) |

Since methodology developed in [9] works in high dimension, an empirical investigation on real data is planned. After estimating a distribution for the loss on real data, using for example a Bernoulli mixture model, as in [16], we can consider an unbalanced credit portfolio (e.g. credit cards) and then we can measure the risk associated with the estimated joint default distribution, as discussed above.

Appendix A Pentanomial lattice

Let , , and be the empirical annualized mean, variance, skewness and excess kurtosis of returns. The relevant quantities to construct a pentanomial lattice are the estimated jump amplitudes and historical probability , that are provided in [15]. In [15] also and are derived, here we recall the jump amplitudes that are given by:

| (A.1) |

and the corresponding historical probabilities are given by:

| (A.2) |

For the construction of the lattice, the up and down rates and the derivation of the above quantities see [15].

Appendix B Uniform sampling

To simulate a functional on a class we use uniform sampling following [9]. We partition into simplices (e.g. using a Delaunay triangulation) where is a proper set of indices, and for . Let , where , . Let us denote by the distribution of , where . We get

| (B.1) |

If we assign a uniform measure on the space the probability of sampling a probability mass function in the simplex is simply the ratio between the volume of and the total volume of , i.e.

| (B.2) |

The volume of each and consequently that of can be easily computed because the volume of an -simplex in -dimensional space with vertices is

where each column of the determinant is the difference between the vectors representing two vertices [17].

The probability is the ratio between the volume of the region

| (B.3) |

and the volume of , i.e.

| (B.4) |

The computation of the volume of will depend on the definition of in the expectation measure . We uniformly sample at random over and determining the relative frequency of the points that fall in the region , as defined in (B.3)

where is the size of the sample. In these cases an estimate of the distribution will be obtained.

References

- [1] T. Breuer and I. Csiszár, “Measuring distribution model risk,” Mathematical Finance, vol. 26, no. 2, pp. 395–411, 2016.

- [2] F. Bellini, P. Koch-Medina, C. Munari, and G. Svindland, “Law-invariant functionals on general spaces of random variables,” SIAM Journal on Financial Mathematics, vol. 12, no. 1, pp. 318–341, 2021.

- [3] R. Fontana, E. Luciano, and P. Semeraro, “Model risk in credit risk,” Mathematical Finance, vol. 31, no. 1, pp. 176–202, 2021.

- [4] J. C. Cox, S. A. Ross, and M. Rubinstein, “Option pricing: A simplified approach,” Journal of financial Economics, vol. 7, no. 3, pp. 229–263, 1979.

- [5] B. Kamrad and P. Ritchken, “Multinomial approximating models for options with k state variables,” Management science, vol. 37, no. 12, pp. 1640–1652, 1991.

- [6] C. S. Ssebugenyi, I. J. Mwaniki, and V. S. Konlack, “On the minimal entropy martingale measure and multinomial lattices with cumulants,” Applied Mathematical Finance, vol. 20, no. 4, pp. 359–379, 2013.

- [7] R. Cont, “Model uncertainty and its impact on the pricing of derivative instruments,” Mathematical Finance, vol. 16, no. 3, pp. 519–547, 2006.

- [8] M. De Berg, M. Van Kreveld, M. Overmars, and O. Schwarzkopf, Computational geometry. Springer, 1997.

- [9] R. Fontana and P. Semeraro, “Exchangeable bernoulli distributions: High dimensional simulation, estimation, and testing,” Journal of Statistical Planning and Inference, vol. 225, pp. 52–70, 2023.

- [10] M. Shaked and J. G. Shanthikumar, Stochastic orders. Springer, 2007.

- [11] M. Denuit and C. Vermandele, “Optimal reinsurance and stop-loss order,” Insurance: Mathematics and Economics, vol. 22, no. 3, pp. 229–233, 1998.

- [12] E. Eberlein and J. Jacod, “On the range of options prices,” Finance and Stochastics, vol. 1, no. 2, pp. 131–140, 1997.

- [13] M. Frittelli, “Minimal entropy criterion for pricing in one period incomplete markets,” Dept. Metodi Quantitativi Tech. Report, no. 99, 1995.

- [14] E. Ekström, “Properties of American option prices,” Stochastic Processes and their Applications, vol. 114, no. 2, pp. 265–278, 2004.

- [15] Y. Yamada and J. A. Primbs, “Properties of multinomial lattices with cumulants for option pricing and hedging,” Asia-Pacific Financial Markets, vol. 11, no. 3, pp. 335–365, 2004.

- [16] M. Doria, E. Luciano, and P. Semeraro, “Machine learning techniques in joint default assessment,” arXiv preprint arXiv:2205.01524, 2022.

- [17] P. Stein, “A note on the volume of a simplex,” The American Mathematical Monthly, vol. 73, no. 3, pp. 299–301, 1966.