Great year, bad Sharpe?

A note on the joint distribution of performance and risk-adjusted return

Abstract

Returns distributions are heavy-tailed across asset classes. In this note, I examine the implications of this stylized fact for the joint statistics of performance and risk-adjusted return. Using both synthetic and real data, I show that the Sharpe ratio does not increase monotonically with performance: in a sample of price trajectories with the same distribution of returns, the largest Sharpe ratios are associated with suboptimal mean returns; conversely, the best performance never corresponds to the largest Sharpe ratios. This counter-intuitive effect is unrelated to the risk-return tradeoff familiar from portfolio theory: it is a consequence of asymptotic correlations between the sample mean and sample standard deviation of heavy-tailed variables (which are absent in the Gaussian case). In addition to its very large sample noise, the non-monotonic association of the Sharpe ratio with performance puts into question its status as the gold standard of investment quality.

I Introduction

Of two investments with comparable returns, the one with lower volatility is more desirable. From this commonsense observation derives the notion of risk-adjusted returns as target for optimization. This logic is formalized in Markowitz’s “modern portfolio theory”, where a portfolio is considered efficient if it maximizes the Sharpe ratio (mean return)/(volatility). In practice, risk-adjusted performance measures, of which the Sharpe ratio is the most common, are routinely used to benchmark and select funds, compensate their managers, etc.

From a statistical perspective, the Sharpe ratio is simply the coefficient of variation of excess returns. Assuming returns with finite variance, its sampling distribution can be described with standard asymptotic theory [1]. However, precisely because investors are focused on maximizing their Sharpe ratio, it interesting to ask not just about the center of its sampling distribution, but also about its tails. What kind of events lead to large deviations of the Sharpe ratio?

The purpose of this note is to examine the tails of the joint sampling distribution of performance (mean return) and risk-adjusted return (Sharpe ratio) of funds. A natural expectation is that the Sharpe ratio takes the largest values along prices trajectories with exceptionally large returns. I show that this expectation is true in a Gaussian world, but false when returns are heavy-tailed, a well-known feature of empirical returns [2]. In particular, I show that, with heavy-tailed returns, the strategies with the largest Sharpe ratios never maximize long-term performance, and strategies with exceptional performance are associated with suboptimal Sharpe ratios. We might call this counter-intuitive phenomenon the “great returns, bad Sharpe” effect.

Two cautionary remarks. First, the present study is strictly about in-sample statistics: we do not consider issues of prediction or out-of-sample validity. Second, the relationship between performance and risk-adjusted returns discussed here is unrelated to the risk-return tradeoff familiar from portfolio theory: throught the paper, the distribution of returns (and in particular its mean and standard deviation ) is fixed.

II Results

II.1 Definitions

Let us begin with some definitions and assumptions. We consider an asset or strategy with price and log-returns at time resolution by . We suppose that a riskfree asset provides returns at rate , and denote the excess log-return. (Henceforth will be called return for short.) We assume are independent and drawn from a common distribution with mean and standard deviation .

The performance of the strategy over the time horizon of periods is measured by its mean return : after a time , dollar invested in this strategy has grown into times the riskfree return . Similarly, the volatility of the strategy over the same horizon is the standard deviation of returns, defined by . Given its performance and volatility , the Sharpe ratio of the strategy is then defined as

| (1) |

This ratio is approximately invariant with respect to , and can be interpreted as a signal-to-noise ratio (signal , noise ). When is large ( for daily returns), the sampling distribution of is asymptotically Gaussian, with standard error [1] (see Fig. 1).

Strictly related measures of risk-adjusted return include the information ratio (where the reference rate is the market rate), the Sortino ratio (where is replaced by the downside risk), and the Treynor ratio (where is replaced by ). These give similar results and we do not discuss them here.

II.2 Data

We consider daily returns data of two kinds. First, we generate synthetic returns from a Student distribution with mean , standard deviation , and tail index :

| (2) |

where follows a Student distribution with degrees of freedom. (The associated probability density function reads has tail behavior .) Empirically, the tail index of daily returns is found to be (see Ref. [2] and references therein); in the limit a Gaussian distribution is recovered.

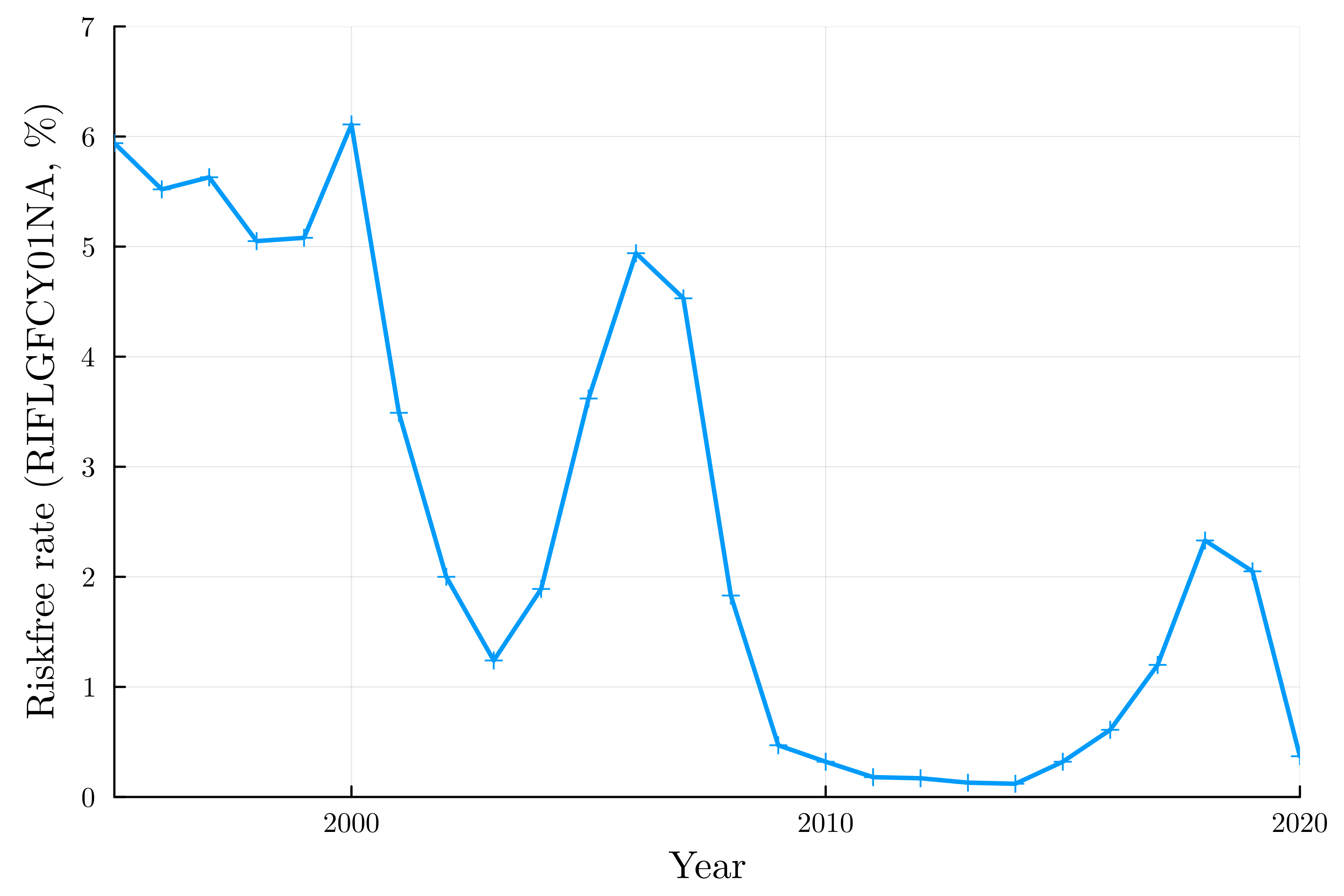

We also consider a public dataset of the adjusted close price of exchange traded funds (ETFs) spanning the period 1995-2019 and multiple categories (equities, commodities, short-term bonds, etc.) [3]. To compute excess returns we use as riskfree rate the market yield on 1-year T-bills (the RIFLGFCY01NA ticker from FRED), plotted in Fig. 2.

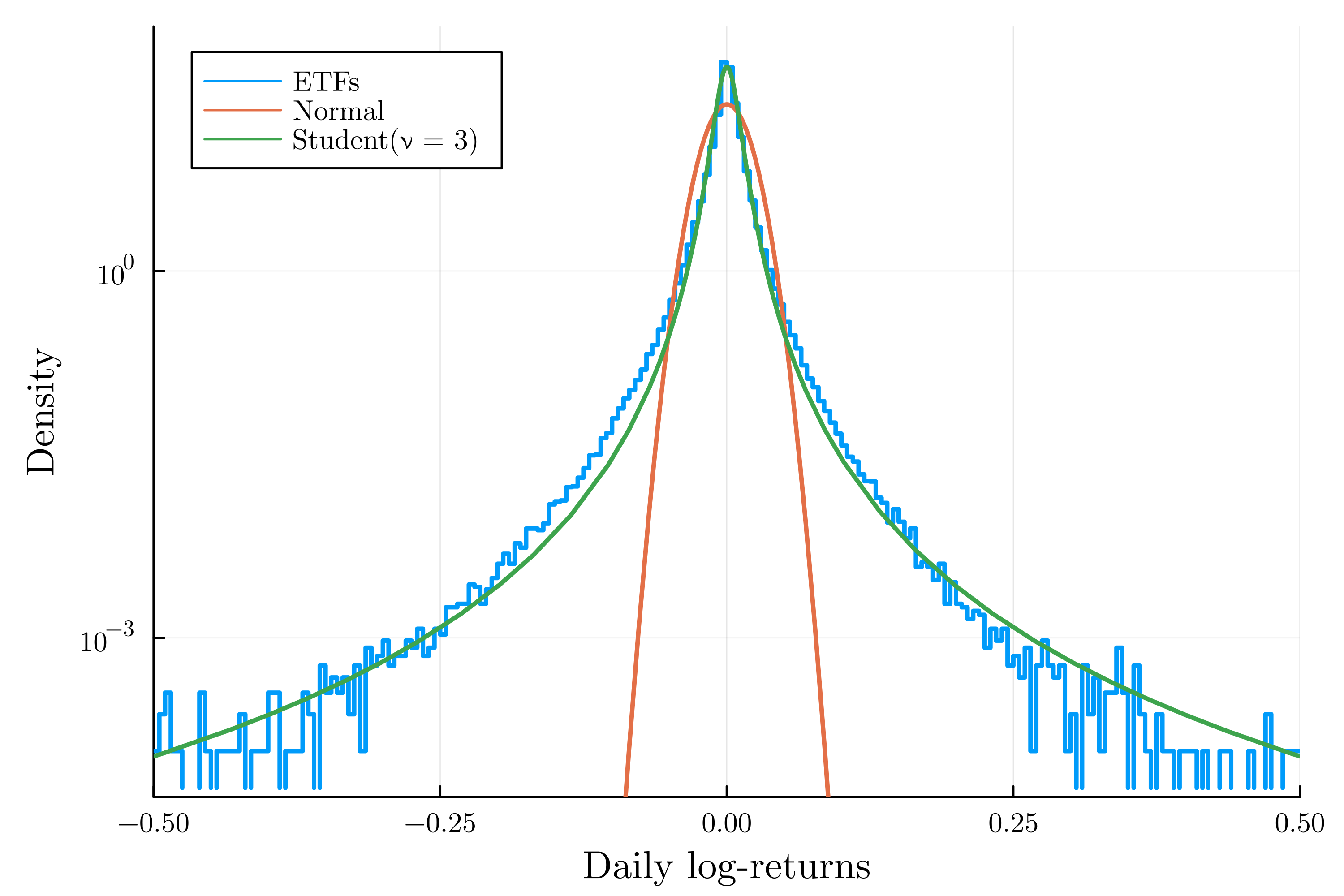

The agregate distribution of daily returns of these ETFs is shown in Fig. 3, together with the density of a Student distribution with and a Gaussian distribution with the same mean and standard deviation . As expected, the Student distribution fits ETF returns well, while the Gaussian clearly does not.

In the following, we fix , , corresponding to the empirical mean and standard deviation of daily ETF returns.

II.3 Distribution of Sharpe ratios

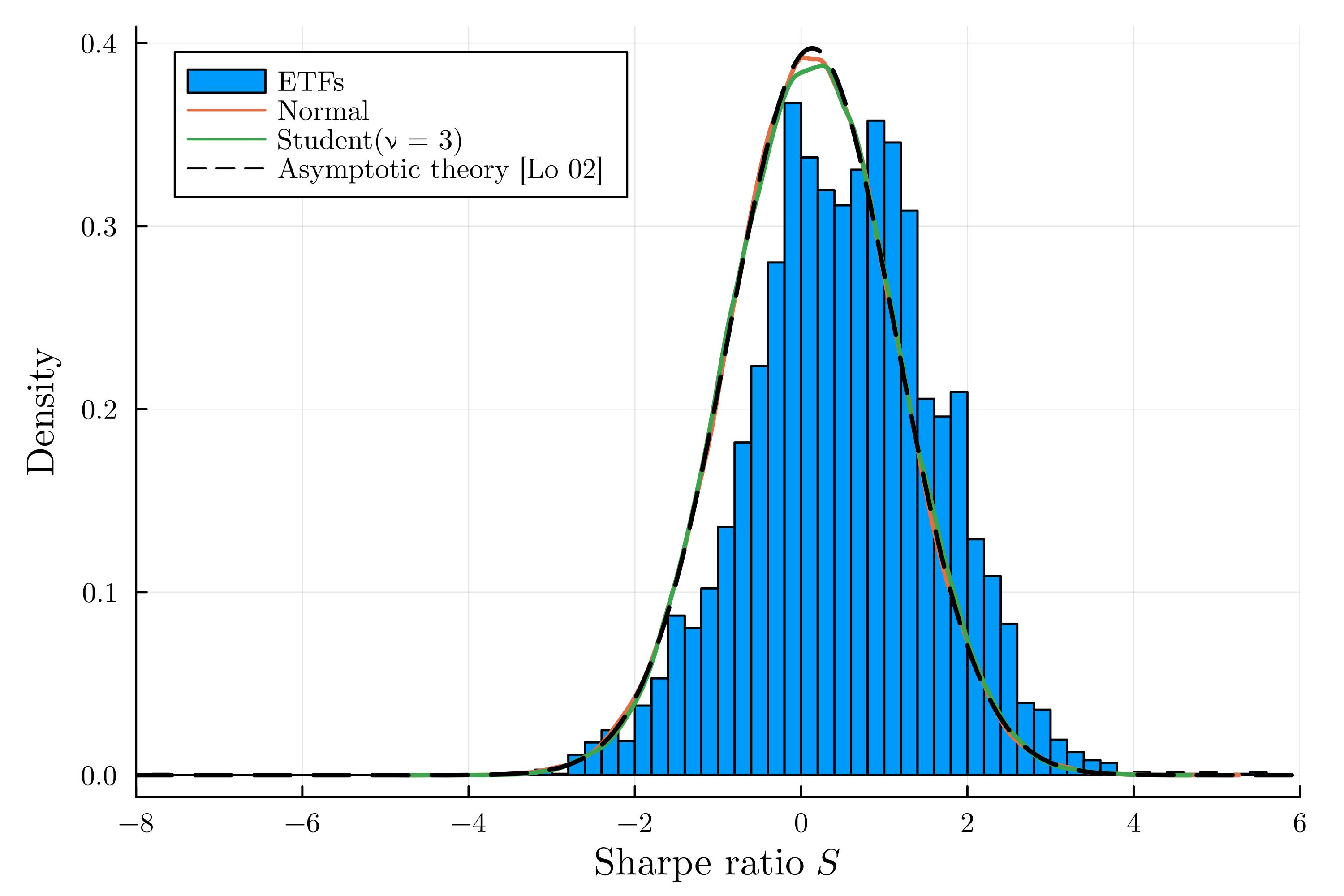

For each of our synthetic distributions (normal and Student with ), we generate samples of returns and compute their Sharpe ratios . The corresponding sampling distribution is plotted in Fig. 3, together with the 1-year Sharpe ratios of the ETFs in our sample. We also plot for comparison a normal density with mean and deviation , representing the asymptotic density derived by Lo [1].

Fig. 1 shows that asymptotic theory provides a good approximation of the distribution of Sharpe ratios. More importantly, it shows that sampling noise of the Sharpe ratio is very large, as suggested by its standard error .

In applications, it is common to grade funds by Sharpe ratios; according to Forbes Advisor, a Sharpe ratio between 1 and 2 is considered good, a ratio between 2 and 3 is very good, and any result higher than 3 is excellent. Here we see that the sampling noise of Sharpe ratios covers this range. While the theoretical Sharpe ratio of our synthetic fund is (a mediocre value), about of the samples have (“good”), and a non-negligible fraction has (“very good”). Clearly, luck plays a big role in deciding whether a Sharpe ratio is “good” or not.

II.4 Joint sampling distributions

Next we consider the joint sampling distribution of performance (sample mean return ), volatility (sample standard deviation ), and Sharpe .

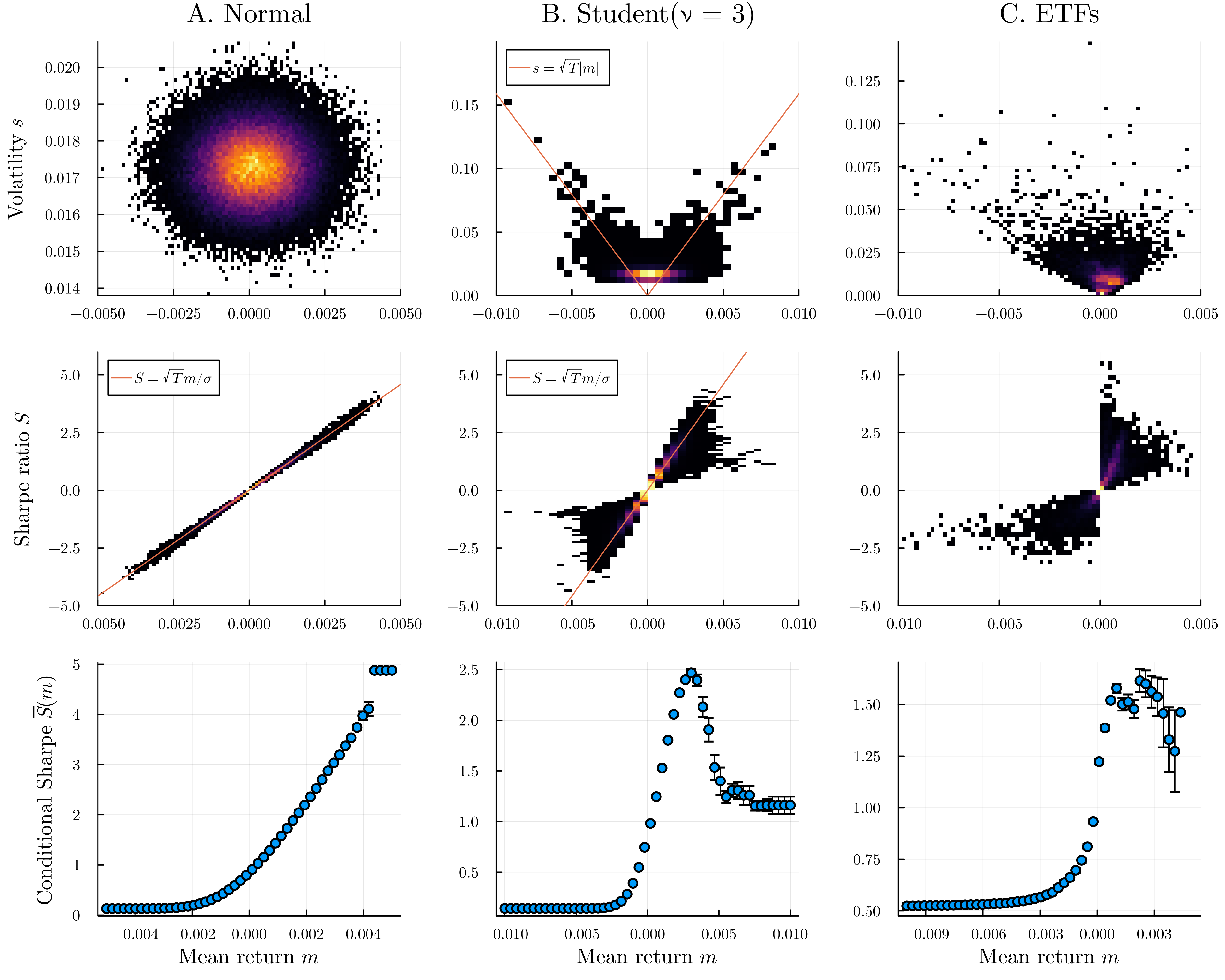

The relevant mathematical fact here is that the sample mean and sample standard deviation of iid samples are independent if and only if these samples are Gaussian [4]; in general their joint distribution is non-trivial, with a density given by a multi-dimensional integral [5]. The first line of Fig. 4 confirms this fact: while Gaussian funds (A) display no correlation between and , Student funds (B) and real ETFs (C) exhibit an asymptotic association between and . In the Student case, this association is captured by the asymptotic relation . Performance and volatility also exhibit statistical dependence in ETF case (C), albeit not one that can be easily interpreted.

Correlations between mean return and volatility translate into a non-trivial relationship between mean return and Sharpe , as illustrated in the second row of Fig. 4. While Gaussian Sharpe ratios are well described by the naive linear relationship (i.e. by fixing the volatility to its expected value), we see in column B and C that this pattern is broken by heavy-tailed returns. Instead of being maximized by the funds with the largest in-sample performance, the Sharpe ratio grows and then decreases with . This is especially clear if we consider the conditional Sharpe ratio , defined as the mean Sharpe ratio of funds with mean return , see third row of Fig. 4. Conversely, we find that the funds with largest Sharpe ratio are never the ones with the best performance.

III Conclusion

The Sharpe ratio has some well-known limitations as a measure of investment quality. For instance, the Sharpe does not distinguish between upside and downside risk; large tail risks can easily be concealed behind the veil of low volatility, e.g. by writing far out-of-the-money options; most importantly, as we saw, Sharpe ratios consist are largely noise, with standard errors an order of magnitude larger than their values.

None of these caveats relate to the quality of the Sharpe ratio as a descriptor of past returns. In this note I have shown that, in constrast with the Gaussian case, a very large Sharpe ratio is not synonymous with great in-sample performance. On the contrary, funds with maximal Sharpe ratios tend to have suboptimal performance.

A few years ago, a Financial Times columnist asked “If something has a Sharpe Ratio of 8.38, does that mean I should sell my grandmother down the river and buy it?” [6]. Before jumping to hazardous conclusions, it is reasonable to ask: did that thing actually make money?

The Julia code used to generate the present results is freely available at https://github.com/msmerlak/sharpe.

References

- Lo [2002] A. W. Lo, The Statistics of Sharpe Ratios, Financial Analysts Journal 58, 36 (2002).

- Bouchaud and Potters [2003] J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management, 2nd ed. (Cambridge University Press, Cambridge, 2003).

- [3] S. Leone, US Funds dataset from Yahoo Finance, https://www.kaggle.com/datasets/stefanoleone992/mutual-funds-and-etfs.

- Geary [1936] R. C. Geary, The Distribution of ”Student’s” Ratio for Non-Normal Samples, Supplement to the Journal of the Royal Statistical Society 3, 178 (1936).

- Springer [1953] M. D. Springer, Joint Sampling Distribution of the Mean and Standard Deviation for Probability Density Functions of Doubly Infinite Range, The Annals of Mathematical Statistics 24, 118 (1953).

- Shubber [2016] K. Shubber, If something has a Sharpe Ratio of 8.38, does that mean I should sell my grandmother down the river and buy it?, https://www.ft.com/content/08a2c6b6-0965-32b3-b016-cdaa736e8d09 (2016).