Differentially Private Diffusion Auction: The Single-unit Case

Abstract

Diffusion auction refers to an emerging paradigm of online marketplace where an auctioneer utilises a social network to attract potential buyers. Diffusion auction poses significant privacy risks. From the auction outcome, it is possible to infer hidden, and potentially sensitive, preferences of buyers. To mitigate such risks, we initiate the study of differential privacy (DP) in diffusion auction mechanisms. DP is a well-established notion of privacy that protects a system against inference attacks. Achieving DP in diffusion auctions is non-trivial as the well-designed auction rules are required to incentivise the buyers to truthfully report their neighbourhood. We study the single-unit case and design two differentially private diffusion mechanisms (DPDMs): recursive DPDM and layered DPDM. We prove that these mechanisms guarantee differential privacy, incentive compatibility and individual rationality for both valuations and neighbourhood. We then empirically compare their performance on real and synthetic datasets.

1 Introduction

New technological shift in AI and data science has given rise to an imminent need to address data privacy issues in online platforms. Indeed, a Gartner survey shows that of the surveyed organisations have experienced a privacy breach or security incident111https://blogs.gartner.com/avivah-litan/2022/08/05/ai-models-under-attack-conventional-controls-are-not-enough/. Data privacy issues have been especially serious and impactful around the use of social commerce platforms such as Instagram and Facebook. As users of such a platform find, browse and buy products through the social network, they are also exposed to a significant risk of privacy leakage. A recent PCI Pal survey shows that fewer than of users are confident about their data security on social commerce sites222https://www.pcipal.com/knowledge-centre/resource/fewer-than-10-of-people-are-confident-about-their-data-security-on-social-media-according-to-survey-from-pci-pal/. Thus designing new tools to facilitate safe and private use of social commerce platforms is of crucial importance.

Auction is important in facilitating online commerce. Auctions have been applied in many contexts, e.g., radio spectrum, sponsored search ads, virtual resource allocation. In an auction, buyers submit their (private) valuations in bids to the auctioneer. The bids often imply buyers’ preferences and confidential business strategies, and competitors may exploit them to gain an advantage. Hence, there is a need to protect the privacy of bid information. The privacy issues in auctions have recently been studied in [McSherry and Talwar, 2007, Jian et al., 2018, Zhu et al., 2014, Ni et al., 2021]. To mitigate privacy risks, these studies employ the well-established notion of differential privacy (DP) [Dwork et al., 2006]. Here, DP is used to protect individual’s bid information when the auction outcome is published. To achieve DP on bids, the work of McSherry and Talwar [2007] proposed exponential mechanism. The mechanism randomises auction results so that a change in a buyer’s bid does not significantly affect the auction outcome. In this way, the mechanism prevents the bid from being inferred from the auction outcome. This mechanism has so far been a predominant method to protect privacy in auctions.

Diffusion auction is an emerging form of auction. In this setting, a seller is able to harness the power of social network to diffuse auction information, inviting friends, friends-of-friends, etc., to join the auction, thereby attracting a large number of potential buyers. This differs from a standard auction (without social network) where the participants are fixed beforehand. Thus, diffusion auction are especially suitable for facilitating online social commerce platforms where the social network plays a prominent role. A challenge in diffusion auctions lies in resolving the conflict between the seller who wants to attract more participants for better revenue and the buyers who are reluctant to invite their friends to avoid competition. Thus there is a need to extend incentive compatibility (IC) for hidden valuations in classical auctions, to diffusion IC for hidden valuation as well as social ties. Numerous studies, e.g., [Li et al., 2017, 2019, Zhang et al., 2020b, a], have proposed mechanisms for diffusion auction that achieve diffusion IC.

Diffusion auctions are prone to all aforementioned privacy risks for auctions in general. However, no study has focused on the privacy issues for diffusion auctions. Here we close this gap by investigating the following question:

How do we design a differentially private diffusion mechanism (DPDM) that guarantees desirable properties and preserves valuation privacy?

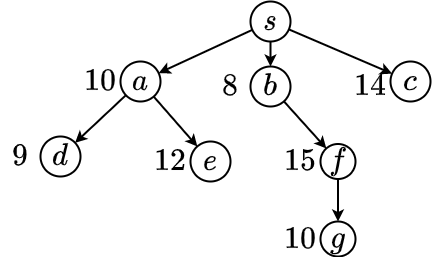

Answering this question is not a trivial task. As mentioned above, the exponential mechanism is the main approach to ensure DP for auctions. An exponential mechanism firstly creates a probability distribution over all possible auction results such that more preferable result is associated with a higher probability, and then outputs an auction result according to the distribution. However, this mechanism can not be directly extended to diffusion auctions as it fails to ensure diffusion IC property. For instance, run the exponential mechanism to the scenario in Figure 1 (See Example 4.1 for a detailed implementation). Assume that all buyers except buyer reveal their neighbours truthfully. From ’s perspective, revealing her neighbour means getting a lower probability of winning the auction, as the exponential mechanism would distribute the winning probabilities over buyers instead of . Therefore, the buyers are not incentivised to diffuse auction information to their friends.

Contribution. In this paper, we design a DPDM for the single-unit auction case where a single seller sells one indivisible item to multiple potential buyers. The seller and the buyers are assumed to be nodes in a social network with their connections represented as edges. The seller initially only has access to her direct neighbours, and must incentivise the buyers to truthfully report both their valuations of the item, and their neighbourhood. At the same time, the DPDM should ensure the DP property for buyers’ bids. We design two DPDMs: recursive DPDM and layered DPDM. The idea for these two mechanisms is market division that partitions the buyers into sub-markets. The mechanism then associates a probability with each sub-market. To ensure diffusion IC, the probability should be monotonic on the size of the sub-markets:

-

•

The recursive DPDM maps the network into a tree that captures information flow among buyers. Then it recursively divides the market such that each sub-tree is a sub-market and its probability is non-decreasing on the size of the sub-tree.

-

•

The layered DPDM also relies on the tree above, except the market is not partitioned by sub-trees, but rather by buyers’ distances from the seller. In this way, each layer is a sub-market and its probability is fixed.

These two mechanisms are proven to meet all the desirable properties. The layered DPDM has a lower bound on expected social welfare. The recursive DPDM achieves a better social welfare empirically. We demonstrate this using a series of experiments that simulate diffusion auctions over three real-world social network datasets. Our experiments reveal that in most cases, the recursive DPDM reaches comparable social welfare as the theoretical upper bound. We now highlight our contributions:

2 Related work

Differentially private mechanism.

Differential privacy (DP) is proposed to protect individual data from inference attacks on an aggregate query over a database [Dwork et al., 2006]. The notion has since been extended to various domain such as statistical data inference [Dwork, 2008], decision trees [Fletcher and Islam, 2019], and unstructured data [Zhao and Chen, 2022]. McSherry and Talwar [2007] extend DP to auctions and propose exponential mechanism. This mechanism ensures a weaker version of IC, namely approximate IC, which ensures that any user can only gain a bounded extra utility from misreporting. This solution concept is adopted in subsequent studies [Zhu et al., 2014] and [Diana et al., 2020] on multi-item auctions and one-shot double auctions. As approximate IC allows bidders to have non-zero incentives to lie, these methods would not meet the requirements in our problem.

Many works design DP auctions that ensure traditional version of IC [Huang and Kannan, 2012, Xiao, 2013, Zhu and Shin, 2015, Jian et al., 2018]. Specifically, Huang and Kannan [2012], Xiao [2013] propose general methods to transform a classical IC mechanism to a privacy preserving counterpart that is still IC. The method of [Xiao, 2013] works only when the valuation space is small and can not be applied to general problems, including ours. In contrast, the transformation method in [Huang and Kannan, 2012] can be applied to more general problems. The transformed mechanism can be seen as a generalisation of Vickrey-Clarke-Groves (VCG) mechanism [Groves, 1973], which is paired with a carefully designed payment rule. However, when the mechanism is applied to multi-item auctions, it is approximately IC rather than IC. Later, Zhu and Shin [2015] and Xu et al. [2017], Jian et al. [2018] propose mechanisms that combine the exponential mechanism with the payment rule in [Archer and Tardos, 2001], applying to combinatorial auctions and reverse auctions, respectively.

No mechanism above can be applied to our problem of designing DPDM because they fail to ensure diffusion IC. We next introduce existing diffusion auction mechanisms.

Diffusion auction.

Diffusion auction is an emerging topic in mechanism design. Li et al. [2017] are the first to investigate diffusion auction and propose information diffusion mechanism (IDM), a mechanism for single-unit auction in a social network. The basic idea is to give monetary reward to buyers who are critical to diffusion, and it ensures diffusion IC. Following this idea, Li et al. [2019], Zhang et al. [2020b, a] further study single-unit diffusion auction from different aspects. Later, Zhao et al. [2018], Kawasaki et al. [2020] extend single-unit diffusion auctions to multiple-unit cases and propose generalised IDM (GIDM) and DNA-MU, resp. However, all of these mechanisms are deterministic and suffer from privacy leakage risks.

3 Problem formulation

3.1 Preliminaries

Consider the following setup: There is a seller, denoted by , and buyers, denoted by . Seller has a single indivisible item to sell. Each buyer is willing to buy the item and attaches a valuation to the item. Valuation is the maximum amount of money that is willing to pay. This value is private to the seller.

The seller and the buyers form a social network, represented by a graph , where is the vertex set and is the edge set. Each node has a neighbour set, denoted by . We assume that only the seller’s neighbours know the auction information initially. The seller would like to attract more buyers to participate in the auction and spread the auction information. Each buyer is able to deliver the auction information to her neighbours. The set is also a private information of buyer .

Each buyer , once informed with the auction, can participate in the auction. Also, for each buyer a pair consisting of her valuation and neighbour set is called the profile of the buyer. We use to denote this profile. The profile is known to the buyer and it is hidden to anyone else. Let denote the set of all possible profiles. Also, we let be the global profile of all buyers and be the global profile of all buyers except for . In the auction, each buyer is asked to report her profile , which is not necessarily the true one. We define as the reported global profile of all buyers. Given , we construct a directed graph : add a directed edge if is reported by as a neighbour. We call such graph profile digraph.

Diffusion auction has two forms of information asymmetry: (1) Valuation asymmetry. The buyers’ true valuations are private information and hidden from the seller. Thus buyers have an advantage over the seller as they can misreport their valuations. The auction should prevent misreporting of valuation through appropriate allocation and pricing strategies. (2) Neighbourhood asymmetry. By Bulow-Klemperer theorem, the revenue of an auction increases as the number of buyers grows [Bulow and Klemperer, 1996]. However, as buyers’ neighbours on the social network are hidden, the seller would hope the buyers to diffuse the auction information to their neighbours to allow more participants to join. However, being rational, the buyers are not necessarily willing to disseminate the auction information as this may hinder their own chance of winning. Here, we follow the standard convention and assume that the reported neighbour set is a subset of .

Diffusion auction mechanisms are designed to address these two challenges. Now we give the definition of a mechanism. A mechanism, denoted by , takes the reported global profile of all buyers as input, and determines who is allocated the item and how much to pay.

Definition 3.1.

A mechanism consists of two functions , where is an allocation function and is a payment function.

The allocation function determines whether the buyers get the item while the payment function determines the amount of money that the buyers need to pay. Given a reported global profile of all buyers, we write the allocation result as and the payment result as , where and is buyer ’s allocation and payment. The utility of buyer with profile is when reported global profile is . The social welfare of mechanism on , denoted by , is defined as the sum of the seller and the buyers’ utility, i.e., . We aim to maximise the social welfare.

3.2 Privacy-aware diffusion auction

In addition to Challenges (1) and (2) above, we consider a third challenge in diffusion auction when the buyers are privacy-aware. (3) Valuation privacy. Once the auction result is annouced, an attacker with certain background information may infer the bid information from the published auction result. This is known as the inference attack [Li et al., 2017]. This disadvantages the buyer(s) whose private valuation is diclosed. Therefore, the buyers require the guarantees that their private valuations are protected.

To achieve privacy preservation, we apply a randomised mechanism to implement an auction on the reported global profile.

Definition 3.2.

A randomised mechanism is one that, given a global profile , outputs a pair such that is a randomised allocation function and is a randomised payment function.

Given a global profile , the randomised mechanism outputs and such that is a random variable with possible values and is a random variable with possible values . We use the concept of differential privacy to define the privacy protection of a mechanism. Basically, differential privacy requires that the distributions over the outcomes are nearly identical when the global profiles are nearly identical. The privacy protection level is measured by a privacy parameter .

Definition 3.3.

A randomised mechanism is -differential privacy (-DP) if for any two global profiles that differ on a single buyer’s valuation, and for any possible outcome ,

| (1) |

Eqn. (1) shows if any buyer changes her reported profile from to , the auction outcome does not change too much. Therefore, no one could infer the valuation of any buyer from the randomised outcome.

Exponential mechanism [McSherry and Talwar, 2007] is an existing mechanism that ensures -DP for valuation privacy. Given a global profile, an exponential mechanism creates a distribution over all possible auction outcomes, and outputs an outcome according to the distribution. Intuitively, the higher a reported valuation is, the more likely the corresponding buyer is selected as a winner. Specially, given a global profile , define a score function that assigns a real valued score to each pair from . The more preferable an outcome is, the higher the score of the outcome is. An exponential mechanism outputs a result with probability

In our problem, a result corresponds to that a certain buyer wins, and we use to denote this result.

In randomised mechanisms, we assume that the buyers are risk-neutral and care about their utilities in expectation. We use to denote ’s expected utility in and redefine the standard IC and IR properties by expected utility.

Definition 3.4.

Let be a randomised mechanism,

-

•

The mechanism is IC if for all , all and for all , we have the following,

-

•

The mechanism is IR if for all and all , we have

The IR and IC properties ensure that buyers are willing to participate in the auction and to reveal their true valuations and neighbours, as they are rational and doing so leads to the best expected utilities. Hence, information asymmetry issues can be addressed.

The social welfare of is also in expectation, i.e.,

We aim to design a randomised mechanism that is IC, IR, -DP (for reasonable ) while maximising social welfare.

4 Recursive DPDM

Preserving valuation privacy in diffusion auctions is not a trivial task. On one hand, existing diffusion auctions, including IDM [Li et al., 2017], CMD [Li et al., 2019], and FDM [Zhang et al., 2020b], are deterministic, and thus fail to preserve privacy. On the other hand, existing differential private mechanisms, including exponential mechanism, fail to incentivise truthful report of neighbours, which is illustrated in Example 4.1.

Example 4.1.

We apply exponential mechanism paired with score function to the scenario in Figure 1. That is, the score of the result that wins is ’s reported valuation . We assume that the buyers truthfully report their valuations. Then buyer wins with probability . Now if buyer reports her neighbour , wins with probability , whereas she wins with probability had she chose not to report . In the latter case, the winning probability is even higher, and thus has incentive to hide her neighbours.

To incentivise buyers to diffuse auction information, we need to ensure each buyer’s utility of reporting her neighbours should be no less than that of non-reporting. We now propose recursive DPDM to achieve this condition. The basic idea is “market division”, i.e., treat the social network as a market, partition the market into multiple sub-markets and assign each sub-market a probability with which buyers in this sub-market win, as shown in Eqn. (2). In this case, each buyer would report as many neighbours as possible in order to maximise the probability of the sub-market she belongs to. Then the buyers in a sub-market share the probability of the sub-market in such a way that the winning probability of any buyer is independent from her children, as shown in Eqn. (3). Therefore, the buyers have no competition with their children and have no incentive to misreport them.

We now describe in detail: Fix a score function that is non-decreasing in reported valuation . Given a reported global profile , a privacy parameter and the score function as input, works as follows:

(1) Construction of diffusion critical tree. Given a profile digraph , first constructs a diffusion critical tree, denoted by . When the context is clear, we write the tree as . The idea of diffusion critical tree is originally introduced by [Zhao et al., 2018]. For any buyers , we say that is -critical to , denoted by , if all paths from to in go through . A diffusion critical tree is a rooted tree, where the root is seller and the nodes are the buyers who are connected to , and for each , her parent is the node who has the closest distance to . When there are more than one parents, only one node is randomly selected as the parent. The depth of buyer , denoted by , is the distance from to .

(2) Assignment of winning probabilities. This step determines the probabilities that buyers win the item. This is a recursive process. This process starts with the constructed rooted by . Given a (sub-)tree rooted by , assigns a probability to each sub-tree rooted by , and a winning probability to each . This operation is repeated for ’s children, children of ’s children and so on until there is no more children.

(a) Assignment of probabilities to sub-trees. Let denote the sub-tree rooted by . consists of node and all of ’s descendants. Let denote with removed, i.e., . Given a sub-tree , divides the market in to sub-markets, one for and each of the other for a sub-tree , where . Then assigns a probability to with and to each , where . When the context is clear, we write and for and , respectively. We define later in Step (2).b. For notational convenience, given a set of nodes , we let be the sum

Now we define for each as

| (2) |

(b) Assignment of winning probabilities to buyers within a sub-market. In a sub-tree , assigns the winning probability to each as

| (3) |

At the very beginning, starts with the tree rooted by . We label as node and set and . ends with the leaves. For a sub-tree where each are leaves, assigns the winning probability to each as .

(3) Allocation and payment. Randomly select a buyer as a winner according to the constructed distribution in Step (2). Set ’s allocation , and payment as

| (4) |

Example 4.2.

We apply paired with score function to the scenario in Fig. 1. Firstly, and . Next we calculate the probabilities of ’s children. The probability for is . Buyer wins with probability . Similarly, we can get the probabilities for and . Consider buyer . wins with probability . Similarly, we can also get the probabilities for .

Next we show that recursive DPDM satisfies IC, IR and DP. The next classical result is important for IC.

Theorem 4.3 ([Archer and Tardos, 2001]).

Let be the probability that wins when she reports . A mechanism is incentive compatible in terms of valuations if and only if, for any ,

-

1.

is monotonically non-decreasing in ;

-

2.

Lemma 4.4.

Recursive DPDM is incentive compatible in terms of both valuations and neighbours.

Proof.

We first show is IC in terms of valuations. By Equation (2), the probability for any sub-tree is proportional to the score, which is non-decreasing in . Hence, in non-decreasing in . Similarly, by Equation (3), given a sub-tree , the winning probability is non-decreasing in , which meets the condition (1) in Thm. 4.3. Also, by Equation (4), the expected payment

which meets the condition (2) in Theorem 4.3 when is fixed. Therefore, is IC in terms of valuations.

Next we show is IC in terms of neighbours. By the definitions of expected utility and payment function (4), we know that ’s expected utility is only determined by the winning probability . Let be an ancestor of with distance . When reports truthfully as and the reported global profile is , then ’s winning probability is

| (5) | ||||

If hides some of her neighbours and reports any where , instead, and the others report . Then in Equation (5), , and does not change. Also, for each , remains intact, but decreases. So we can know that decreases when misreports her neighbourhood. Therefore, we have ∎

Lemma 4.5.

Recursive DPDM is individually rational in terms of both valuations and neighbours.

Proof.

Given a global profile , for each buyer with , Therefore, the lemma holds. ∎

In following lemma, we use the following terminologies:

-

•

denotes the maximum depth of the diffusion critical tree,

-

•

denotes the largest possible difference in the score function when applied to two global profiles that differ only on a single user’s valuation, for all possible outcome .

Lemma 4.6.

Given a reported global profile , recursive DPDM is -differential privacy, where is the privacy parameter of .

Proof.

Given two reported global profiles and that differ in an arbitrary buyer ’s reported valuation such that reports in and in , we consider the probabilities that and return a winner . In a critical diffusion tree , let denote the depth of , be an ancestor of with distance . Also, let and denote the value derived from and , respectively. Then by Equation (3), we have

We repeatedly replace , , , by expressions of until we get an expression of . For each distance , we denote as , as . For , we have similar notations as and . Then the above ratio can be written as

Next we proof the lemma through that for each , is bounded by . Here we skip the proof for this due to space limitation. See details in App. B. Then we have

∎

Theorem 4.7.

Recursive DPDM is IC, IR and -DP.

5 Layered DPDM

Following the same idea of market division, we propose layered DPDM in this section. Different from , divides the market by the buyers’ distances to the seller. Specifically, given a constructed critical diffusion tree, allocates a certain probability to each layer of the tree, which will be shared by the buyers on this layer. For any buyer, once she is invited by her parent(s), her layer is fixed. Also, the buyer(s) whom she invites will be on the next layer, and thus has no competition with her.

executes the same operations as in , where the only difference is in Step (2) “Assignment of winning probabilities”. Below we describe Step (2) of in detail:

(2) Assignment of winning probabilities. In this step, given a critical diffusion tree , assigns a probability to each layer of the tree and then assigns a winning probability to buyers on each layer.

(a) Assignment of probability to layers. Now we give the definition of layer. Given a tree, the buyers with the same distance form a layer of a tree. The distance . We use to denote the set of buyers with distance , i.e., . For each layer , assigns a probability, denoted by . We write it as when there is no ambiguity. Given an infinite decreasing sequence , where , we define the probability for layer as

| (6) |

(b) Assignment of winning probability to the buyers on a layer. On the th layer, assigns buyer with on layer with probability

| (7) |

Once the probability distribution over all possible outcomes is determined, computes the payment and randomly selects a winner , following Step (3) of .

The complete process of layered DPDM is shown in Alg. 3. Example 5.1 provides a running example of Step (2).

Example 5.1.

Apply paired with score function and sequence to the scenario in Figure 1. Then in this graph, three layers, , correspond to probabilities , resp. In , buyer wins with probability . Similarly, we get the probabilities for and . Then in , wins with probability . The probabilities for can be obtained in a similar way. Lastly, in , buyer wins with probability .

Next we show that layered DPDM has the desirable properties, including IC, IR and DP.

Lemma 5.2.

Layered DPDM is incentive compatible in terms of both valuations and neighbours.

Proof.

The IC property in terms of valuations can be proved in a similar way for Lemma 4.4. What we need to show is is non-decreasing in her reported valuation . By Eqn. (7), is proportional to , which is non-decreasing in .

Then we show IC in terms of neighbours. For an arbitrary buyer , her expected utility is when the global profile is . We plug in Eqn. (4) (7) into . Then we can see is determined by and is determined by her ancestors. Therefore, her utility will not be effected if she misreports her neighbours, i.e., . ∎

Lemma 5.3.

Layered DPDM is individually rational in terms of both valuations and neighbours.

Lemma 5.4.

Given a reported global profile , layered DPDM is -differential private, where is the privacy parameter of .

Lem. 5.4 is proved by showing in Eqn. (7), the change on a single buyer’s valuation is bounded by . Due to space limit, the proof of Lem. 5.4 is deferred to App. D. The next thm. then easily follows from Lem. 5.2, 5.3 and 5.4.

Theorem 5.5.

Layered DPDM is IC, IR and -DP.

Next we analyse the expected social welfare of . We consider a hypothetical scenario where the exponential mechanism is applied to the whole social network where the seller knows all buyers. In this scenario, the auction information is diffused to all buyers without any incentive. We call such a mechanism as exponential mechanism with diffusion (EMD). EMD has the optimal expected social welfare than all DPDMs and thus is used as the benchmark.

Theorem 5.6.

Given a global profile , the expected social welfare of layered DPDM is at least .

Proof.

Given a global profile , the expected social welfare of is

See full derivation in Appendix E. ∎

The next result is an easy corollary.

Corollary 5.7.

For , where , layered DPDM achieves an expected social welfare . ∎

6 Experiment

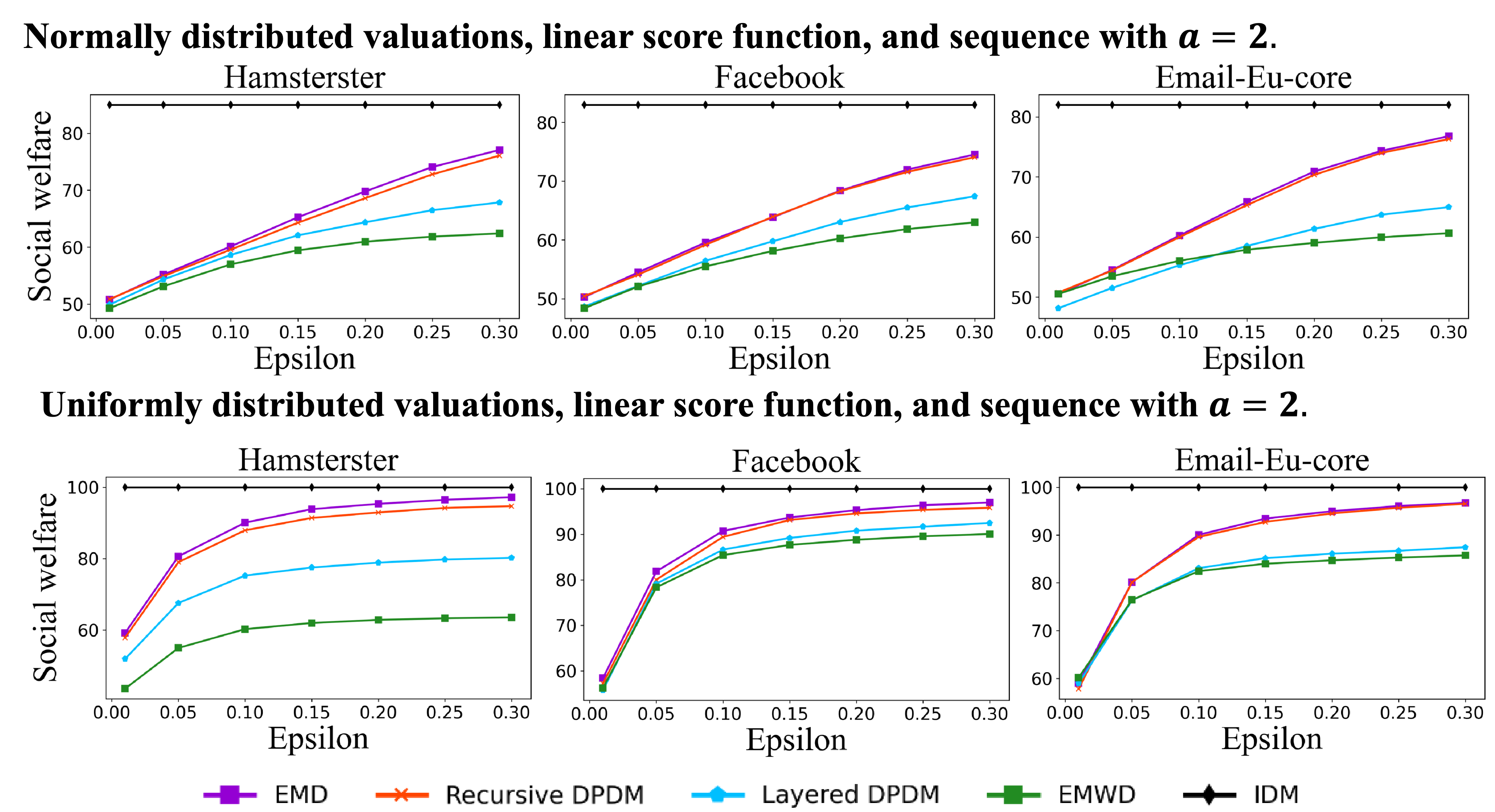

We evaluate the performances of and , in terms of social welfare under different privacy levels and valuations on three real world social network datasets. We also analyse the effect of sequence on the performance of . For each setup, we run times and get average social welfare.

Dataset. We use three real world network datasets, including Hamsterster friendships with nodes and edges [Kunegis, 2013], Facebook with nodes and edges [McAuley and Leskovec, 2012] and Email-Eu-core network nodes and edges [Yin et al., 2017]. For each dataset, the seller is randomly selected.

Valuation. The network datasets contain no information about buyers’ valuations. We generate random numbers as the valuations. We consider two commonly used distributions, normal distribution and uniform distribution . We set the parameters such that the average value are same. Nevertheless, our aim is to reveal the general pattern under different distributions and these patterns are independent from these parameters.

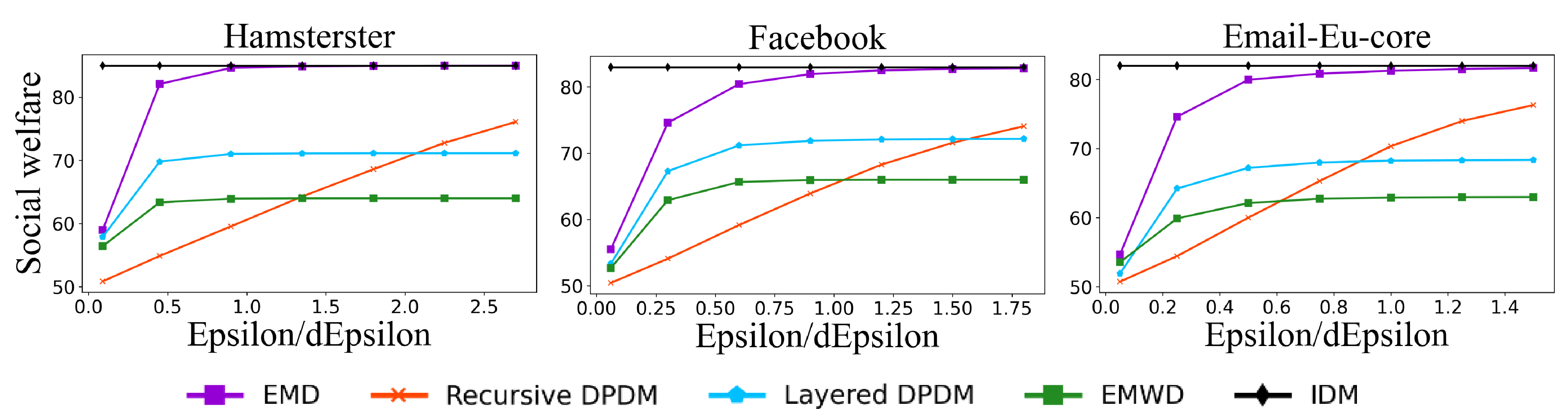

Privacy parameter. To verify the performance of our mechanisms, we also vary privacy parameter . Lem. 5.4 and 4.6 show that, under the same input , and ensure different privacy levels. To see the performance under the same guaranteed privacy, we set the input as for and for the others.

Score function. We use linear function, , as the score function. The linear score function is widely used in previous DP auctions, e.g., [McSherry and Talwar, 2007, Xu et al., 2017].

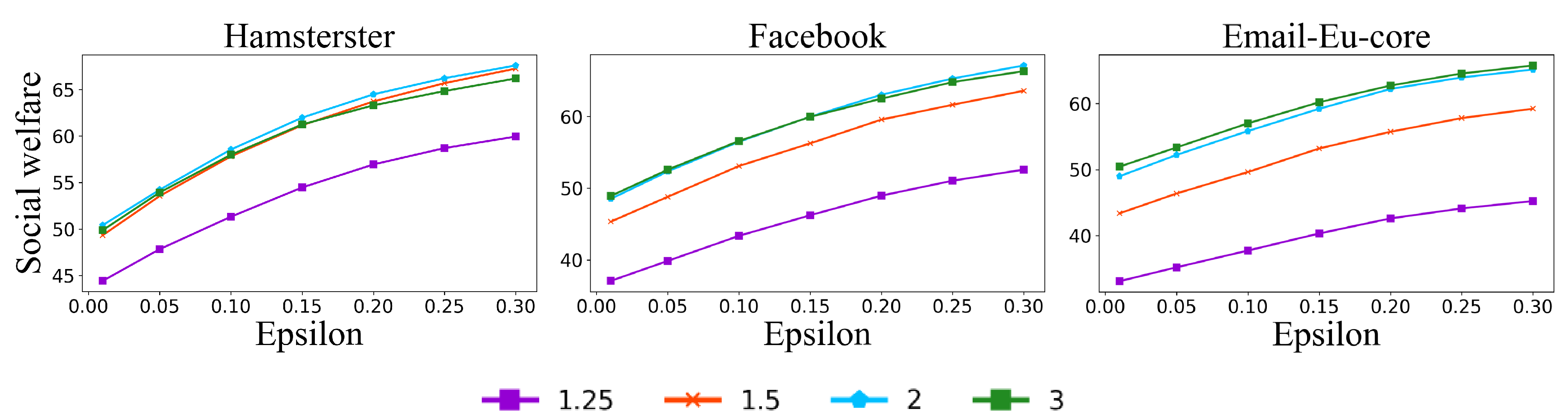

Decreasing sequence. For , we consider different value of in , and evaluate the impact of on expected social welfare.

Benchmark. Since there is no existing DPDM that can be applied in our problem, we design two hypothetical benchmarks. Exponential mechanism without diffusion (EMWD): We apply the exponential mechanism only to the seller’s neighbours. The expected social welfare of EMWD can be seen as the lower bound among all DPDMs. Exponential mechanism diffusion (EMD): See the description of EMD in Section 5. We also compare with IDM [Li et al., 2017] (See App. A), which is not DP, to see how much social welfare is sacrificed to achieve DP.

Results. Overall, when comparing to IDM, the difference in social welfare of the DPDMs decreases with increases. Then, among DPDMs, EMD performs best in most cases, followed by and . Particularly, performs very well. The lines of even coincide with those of EMD in some cases, e.g., on Facebook & Email-Eu-core in Fig. 2. The deviation of from EMD is at most . performs better than the layered counterpart. EMWD returns the worst expected social welfare. The reason why has better expected social welfare than is that in , a probability of is not distributed to any buyer, which means that the seller does not sell the item and the social welfare is with this probability.

Next we show the effect of different parameters. (1) Dataset. As shown in each column of Fig. 2, the same pattern can be found for different datasets. (2) Privacy parameter. The expected increases with . The less privacy is required, the less noisy is added, and thus the higher probability of returning a result with good social welfare. (3) Valuation. The st and the nd row of Fig. 2 show the results with normal and uniform distributions, resp.. Under both distributions, performs better than . (4) Sequence. Fig. 3 shows the average social welfare is best when for Hamsterster and when for Facebook and Email-Eu-core. When a buyer with the highest valuation is on a deeper layer, a smaller leads to a larger probability for the layer where is and also a larger probability for . The results verify this argument. In Hamsterster (Facebook, Email-Eu-core), the buyers with the highest valuation are on the th (rd, nd) layer. (5) same DP. Fig. 4 shows when the realised privacy is large, the avg. social welfare of is greater than that of , while when the realised privacy is small, is better.

7 Conclusion and future work

We consider the problem of designing diffusion auction mechanisms that sells a single item on social networks while preserving valuation privacy. We propose two DPDMs, recursive DPDM and layered DPDM. Also, we theoretically show their incentive and privacy properties and empirically show their good performances in social welfare. We could extend this study by considering the following questions: (1) How to design a DPDM for multi-item auctions? (2) How to design a DPDM that preserves both valuation and neighbourhood privacy? and (3) How to design a DPDM that is group IC where no group of buyers can benefit from joint misreporting?

References

- Archer and Tardos [2001] Aaron Archer and Éva Tardos. Truthful mechanisms for one-parameter agents. Proceedings 2001 IEEE International Conference on Cluster Computing, pages 482–491, 2001.

- Bulow and Klemperer [1996] Jeremy Bulow and Paul Klemperer. Auctions versus negotiations. The American Economic Review, 86(1):180–194, 1996.

- Diana et al. [2020] Emily Diana, Hadi Elzayn, Michael Kearns, Aaron Roth, Saeed Sharifi-Malvajerdi, and Juba Ziani. Differentially private call auctions and market impact. In Proceedings of the 21st ACM Conference on Economics and Computation, page 541–583, 2020.

- Dwork [2008] Cynthia Dwork. Differential privacy: A survey of results. In International conference on theory and applications of models of computation, pages 1–19. Springer, 2008.

- Dwork et al. [2006] Cynthia Dwork, Frank McSherry, Kobbi Nissim, and Adam Smith. Calibrating noise to sensitivity in private data analysis. In Theory of cryptography conference, pages 265–284. Springer, 2006.

- Fletcher and Islam [2019] Sam Fletcher and Md Zahidul Islam. Decision tree classification with differential privacy: A survey. ACM Computing Surveys (CSUR), 52(4):1–33, 2019.

- Groves [1973] Theodore Groves. Incentives in teams. Econometrica: Journal of the Econometric Society, pages 617–631, 1973.

- Huang and Kannan [2012] Zhiyi Huang and Sampath Kannan. The exponential mechanism for social welfare: Private, truthful, and nearly optimal. 2012 IEEE 53rd Annual Symposium on Foundations of Computer Science, pages 140–149, 2012.

- Jian et al. [2018] Lin Jian, Yang Dejun, Li Ming, Xu Jia, and Xue Guoliang. Frameworks for privacy-preserving mobile crowdsensing incentive mechanisms. In IEEE Trans. Mob. Comput, page 1851–1864, 2018.

- Kawasaki et al. [2020] Takehiro Kawasaki, Nathanaël Barrot, Seiji Takanashi, Taiki Todo, and Makoto Yokoo. Strategy-proof and non-wasteful multi-unit auction via social network. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 2062–2069, 2020.

- Kunegis [2013] Jérôme Kunegis. Konect: The koblenz network collection. In Proceedings of the 22nd International Conference on World Wide Web, WWW ’13 Companion, page 1343–1350. Association for Computing Machinery, 2013. 10.1145/2487788.2488173. URL https://doi.org/10.1145/2487788.2488173.

- Li et al. [2017] Bin Li, Dong Hao, Dengji Zhao, and Tao Zhou. Mechanism design in social networks. In Thirty-First AAAI Conference on Artificial Intelligence, 2017.

- Li et al. [2019] Bin Li, Dong Hao, Dengji Zhao, and Makoto Yokoo. Diffusion and auction on graphs. In Proceedings of the 28th International Joint Conference on Artificial Intelligence, pages 435–441, 2019.

- McAuley and Leskovec [2012] Julian McAuley and Jure Leskovec. Learning to discover social circles in ego networks. NIPS’12, page 539–547. Curran Associates Inc., 2012.

- McSherry and Talwar [2007] Frank McSherry and Kunal Talwar. Mechanism design via differential privacy. In 48th Annual IEEE Symposium on Foundations of Computer Science (FOCS’07), pages 94–103. IEEE, 2007.

- Ni et al. [2021] Tianjiao Ni, Zhili Chen, Lin Chen, Shun Zhang, Yan Xu, and Hong Zhong. Differentially private combinatorial cloud auction. IEEE Transactions on Cloud Computing, 2021.

- Xiao [2013] David Xiao. Is privacy compatible with truthfulness? IACR Cryptol. ePrint Arch., 2011:5, 2013.

- Xu et al. [2017] Jinlai Xu, Balaji Palanisamy, Yuzhe Tang, and S.D. Madhu Kumar. Pads: Privacy-preserving auction design for allocating dynamically priced cloud resources. In 2017 IEEE 3rd International Conference on Collaboration and Internet Computing (CIC), pages 87–96, 2017. 10.1109/CIC.2017.00023.

- Yin et al. [2017] Hao Yin, Austin R. Benson, Jure Leskovec, and David F. Gleich. Local higher-order graph clustering. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’17, page 555–564. Association for Computing Machinery, 2017. 10.1145/3097983.3098069. URL https://doi.org/10.1145/3097983.3098069.

- Zhang et al. [2020a] Wen Zhang, Dengji Zhao, and Hanyu Chen. Redistribution mechanism on networks. In Proceedings of the 19th International Conference on Autonomous Agents and MultiAgent Systems, pages 1620–1628, 2020a.

- Zhang et al. [2020b] Wen Zhang, Dengji Zhao, and Yao Zhang. Incentivize diffusion with fair rewards. In ECAI 2020, pages 251–258. IOS Press, 2020b.

- Zhao et al. [2018] Dengji Zhao, Bin Li, Junping Xu, Dong Hao, and Nicholas R Jennings. Selling multiple items via social networks. In Proceedings of the 17th International Conference on Autonomous Agents and MultiAgent Systems, pages 68–76, 2018.

- Zhao and Chen [2022] Ying Zhao and Jinjun Chen. A survey on differential privacy for unstructured data content. ACM Computing Surveys (CSUR), 54(10s):1–28, 2022.

- Zhu and Shin [2015] Ruihao Zhu and Kang G Shin. Differentially private and strategy-proof spectrum auction with approximate revenue maximization. In 2015 IEEE conference on computer communications (INFOCOM), pages 918–926. IEEE, 2015.

- Zhu et al. [2014] Ruihao Zhu, Zhijing Li, Fan Wu, Kang Shin, and Guihai Chen. Differentially private spectrum auction with approximate revenue maximization. In Proceedings of the 15th ACM international symposium on mobile ad hoc networking and computing, pages 185–194, 2014.

Appendix

Appendix A IDM

Here, we introduce the first diffusion auction for selling single item, IDM [13]. A key concept of IDM is diffusion critical sequence. Given a profile digraph , for any buyers , is -critical to , denoted by , if all paths from to in go through . A diffusion critical sequence of , denoted by , is a sequence of all diffusion critical nodes of and itself ordered by -critical relation. That is, , where . Based on this concept, IDM works as follows. IDM first locates the buyer with the highest valuation among all buyers. Then it allocates the item to the buyer , who has the highest valuation when the buyers after are not considered. The winner pays the highest bid without her participation, and each diffusion critical node is rewarded by the increased payment due to her participation.

Appendix B Proof of Lemma 4.6

Lemma 4.6. Given a reported global profile , recursive DPDM is -differential privacy, where is the privacy parameter to .

Proof.

Given two reported global profiles and that differ in an arbitrary buyer ’s reported valuation such that reports in and in , we consider the probabilities that and return a winner . In a critical diffusion tree , let denote the depth of , be an ancestor of with distance . Also, let and denote the value derived from and , respectively. Then by Equation (3), we have

We repeatedly replace , , , by expressions of until we get an expression of . For each distance , we denote as , as . For , we have similar notations as and . Then the above ratio can be written as

Next we show for each , is bounded by . To prove it, we first show for for each , by cases.

(1) When , we have or

(2) When , then or

(3) When , then .

Without loss of generality, we assume that . Plug in these two equations, and we get

Then we consider two cases:

(1) When , we have

(2) When , we have

After that, we show that both and are bounded by as follows.

By definition of , we have

.

(1) When valuation , the second ratio is at most . Then we have

(2) When valuation , the first ratio is at most . We have

In a similar way, we can show that .

Therefore we have

∎

Appendix C Proof of Lemma 5.3

Lemma 5.3. Layered DPDM is individually rational in terms of both valuations and neighbours.

Proof.

Given a global profile , for each buyer with , we have

Therefore, the lemma holds. ∎

Appendix D Proof of Lemma 5.4

Lemma 5.4. Given a reported global profile , layered DPDM is -differential private, where is the privacy parameter of .

Proof.

Given two reported global profiles and that differ in an arbitrary buyer ’s reported valuation such that reports in and in , we consider the probabilities that and return a winner .

Without loss of generality, we assume that is in , then we have

When is not on layer , . Otherwise, when is on layer , we consider two cases.

(1) . As is non-decreasing in , the first ratio is at most . Then we have

(2) . In this case, the second ratio is at most . Then we have

∎

Appendix E Proof of Theorem 5.6

Theorem 5.6 Given a global profile , the expected social welfare of layered DPDM is at least .

Proof.

Given a global profile , the expected social welfare of is

∎