Reliable Bayesian Inference in Misspecified Models

Abstract.

We provide a general solution to a fundamental open problem in Bayesian inference, namely poor uncertainty quantification, from a frequency standpoint, of Bayesian methods in misspecified models. While existing solutions are based on explicit Gaussian approximations of the posterior, or computationally onerous post-processing procedures, we demonstrate that correct uncertainty quantification can be achieved by replacing the usual posterior with an intuitive approximate posterior. Critically, our solution is applicable to likelihood-based, and generalized, posteriors as well as cases where the likelihood is intractable and must be estimated. We formally demonstrate the reliable uncertainty quantification of our proposed approach, and show that valid uncertainty quantification is not an asymptotic result but occurs even in small samples. We illustrate this approach through a range of examples, including linear, and generalized, mixed effects models.

Keywords: Bayesian inference, Generalized Bayesian inference, Model misspecification, Estimated likelihood, pseudo-marginal

1. Introduction

Bayesian methods are lauded for their ability to tackle complicated models, deftly handle latent variables, and for providing a holistic (if subjective) treatment of the uncertainty regarding all model unknowns. While subjective in nature, under well-known regularity conditions, the expressions of uncertainty obtained using Bayesian methods asymptotically agree with frequentist methods. However, when the model underlying the (Bayesian) posterior update is misspecified the agreement between the Bayesian and frequentist statistical paradigms is lost, and expressions of uncertainty obtained using Bayesian methods are no longer ‘valid’ from a frequentist standpoint.

To correct this issue, several posterior post-processing methods have been suggested (see, .e.g., Müller,, 2013, Syring and Martin,, 2019, and Matsubara et al.,, 2021). In general, all such procedures of which we are aware amount to the application of ex-post, frequentist, principles to the output of a Bayesian learning algorithm. Herein, we propose an intrinsically Bayesian solution to the fundamental problem of producing Bayesian inferences that are well-calibrated from a frequency standpoint.

Inspired by the literature on generalized Bayesian inference (Bissiri et al.,, 2016; Chernozhukov and Hong,, 2003), we devise a new type of posterior approximation that, when used in likelihood-based settings delivers equivalent behavior to ‘exact’ Bayesian methods when the model is correctly specified, but produces posteriors whose credible sets are ‘valid’ - from a frequentist standpoint - regardless of model specification. This approach is not based on any ad-hoc correction of posterior draws, or other extrinsic calibration techniques, and can be equally applied when the likelihood must be estimated. We demonstrate theoretically that under weak regularity conditions, and even when the likelihood is estimated, our proposed approach delivers valid frequentist uncertainty quantification regardless of model specification. Hence, we give for the first time a general framework for conducting Bayesian inference in possibly misspecified models that also delivers valid (frequentist) uncertainty quantification.

However, unlike frequentist methods, our Bayesian approach delivers valid uncertainty quantification without needing to calculate second-derivative information. Thus, in cases where second derivatives are difficult to obtain, as in models with many latent variables, this approach provides a useful alternative to frequentist methods that must explicitly calculate these derivatives to correctly quantify uncertainty.

When the model is misspecified, Bayesian methods may not deliver inferences that are ‘fit for purpose’. To circumvent this issue, several researchers have suggested using generalized Bayesian procedures that produce posteriors based on loss functions that are specific to the task at hand; see, e.g., Syring and Martin, (2020), Matsubara et al., (2021), Jewson and Rossell, (2021), and Loaiza-Maya et al., (2021) for examples. Unfortunately, as discussed by several authors, see, e.g., Miller, (2021) and Syring and Martin, (2019), generalized Bayesian posteriors are not well-calibrated: a credible set for a quantity of interest with posterior probability contains the true quantity with actual probability - calculated under the true data generating process - smaller or larger than . Several approaches have been suggested to solve this issue; see, e.g., Holmes and Walker, (2017), Syring and Martin, (2019), and see Wu and Martin, (2020) for a review of these methods. However, the proposed methods of which we are aware amount to the application of an extrinsic, and ad-hoc, correction to the output of the Bayesian learning algorithm.

We demonstrate that our approach can be directly adapted to the context of generalized Bayesian inference, where the likelihood function is replaced by a generic loss function, or a quasi-likelihood that is, at best, an approximation to the likelihood. The result is a class of posteriors for generalized Bayesian inference that produce loss-based credible sets that are well-calibrated. As such, we give, for the first time, a generalized Bayesian posterior whose credible sets are guaranteed to have the correct width, and which does not rely on the use of expensive post-processing techniques.

The remainder of the paper proceeds as follows. Section 2 discusses the general issue of model misspecification in likelihood-based Bayesian inference, and demonstrates how a particular generalized posterior approach overcomes the known issues with Bayesian inference in this setting. Section 3 extends this posterior approach to deal with situations where the likelihood depends on unobservable latent variables, and we show that even when the likelihood must be estimated our proposed approach delivers well-calibrated inferences. Section 4 demonstrates that the generalized posterior construction used in the likelihood-based Bayesian setting also applies in the context of posteriors built using general loss functions (as in Bissiri et al.,, 2016). Section 5 concludes the paper. Proofs of all stated results are given in the supplementary material.

2. Bayesian Inference in Misspecified Models

The observed data , where (), is generated from some true unknown distribution . Since is unknown, we approximate the distribution of using a class of models , which depends on unknown parameters . We assume there exists a measure that dominates both joint distributions and so that the joint densities and exist for all . Our prior beliefs on are expressed via the probability density function . The prior beliefs are updated upon the observation of via Bayes rule, to produce the exact posterior

| (1) |

When can be analytically evaluated there exist many ways to obtain samples from . However, in many interesting situations within Bayesian inference is analytically intractable. This often occurs in models that depend on unobservable, or latent, variables , where , and (). The observed-data likelihood is then obtained by integration over in the complete-data likelihood :

If the integration cannot be performed analytically it often remains feasible to obtain an estimator that depends on simulated random variables , where indexes the number of ‘simulated draws’ used to construct . The use of within an MCMC algorithm results in a pseudo-marginal algorithm (Andrieu and Roberts,, 2009) that targets a joint posterior over :

where denotes the conditional density for the simulated data . If , the marginal posterior agrees with the exact posterior (Andrieu and Roberts,, 2009).

Regardless of whether must be estimated, when posterior inference is not generally ‘well-calibrated’. To state precisely what we mean by well-calibrated inferences, first define as the value of that minimizes the (limiting) Kullback-Liebler divergence from to , and where denotes the expectation operator under . A credible set for based on and having posterior probability is said to be well-calibrated if the set asymptotically contains with -probability . Such a definition directly extends to any function of .

To illustrate why is not well-calibrated in general, we require a few additional definitions. For a twice differentiable function , let denote the gradient of , and its Hessian matrix. For as defined in (1), let and denote the gradient and (minus the) Hessian, respectively; while denotes the expected observed information, and denotes the Fisher information.

For the value of that solves , i.e., the maximum likelihood estimator, under classical regularity conditions, see White, (1982) or Kleijn and van der Vaart, (2012), it is known that , where , denotes the Gaussian cumulative distribution function (CDF) with mean and variance , and denotes weak convergence under . Furthermore, the posterior satisfies the Bernstein-von Mises result

where denotes the Gaussian probability density function (PDF) with mean and variance ; see, e.g., Theorem 2.1 in Kleijn and van der Vaart, (2012). The Bernstein-von Mises result demonstrates that the ‘width’ of credible sets based on are determined by , while the first result states that (asymptotically) valid frequentist confidence sets have ‘width’ determined by the sandwich covariance . Thus, credible sets for with posterior probability will not contain with -probability in general, unless . Consequently, posterior credible sets are not well-calibrated, and Bayesian uncertainty quantification may be too optimistic to be practically useful.

The lack of well-calibrated credible sets in misspecified models has led researchers to consider many different approaches to ‘correct’ this issue. However, each of the suggested approaches of which we are aware are either based on computationally onerous bootstrapping procedures, or amount to an explicit Gaussianity assumption on the posterior and the application of ex-post corrections of to correct the coverage. Section 5.1 discusses several such methods.

2.1. Reliable Bayesian Uncertainty Quantification

If we are willing to move away from conducting inference using the ‘exact’ posterior to a posterior based on a certain approximate likelihood that we will propose, then we can produce Bayesian credible sets that are asymptotically well-calibrated. To motivate this approach, consider the artificially simple case where the observed data are , with , and we wish to conduct inference on the unknown mean . We have meaningful prior beliefs about the unknown , and our goal is to conduct posterior inference given and .

While it is possible to conduct nonparametric Bayesian inference on , this seems overly-complicated machinery for such a simple task. A simpler approach is to notice that even though is unknown, the sample average can be used as a statistic to conduct Bayesian inference on . Following the synthetic likelihood (SL) approach proposed by Wood, (2010), see also Price et al., (2018) and Frazier et al., (2022), even though is unknown we can approximate the distribution of using a known distribution, with this approximation then used as our likelihood to produce posterior inference.

For general summary statistics , Wood, (2010) suggests approximating the distribution using where , and are the mean and (scaled) variance of under the assumed model .111In the case of the summaries , SL suggests conducting Bayesian inference on using the approximate likelihood where is an estimator of . While Bayesian SL (BSL) is most commonly applied to intractable likelihood problems, BSL can be applied in any situation where we wish to conduct posterior inference on summaries rather than the full dataset; for further discussion on this point see Drovandi et al., (2021). As highlighted by Lewis et al., (2021), in misspecified models it may be particularly beneficial to condition posterior inferences not on the entire sample, encapsulated via , but on summary statistics that are ‘robust’ to model misspecification. Indeed, when the model is misspecified the exact posterior is not ‘robust’ from the standpoint of uncertainty quantification, and it may instead be feasible to produce Bayesian inferences based on a vector of summaries that ensure our posterior inference for is ‘robust’ to this particular form of misspecification.

Noting that the average score is simply a summary statistic whose mean is zero under the assumed model (under weak regularity conditions),222For denoting the assumed model, for all , so long as , for all . We recall that the exchange of integration and differentiation is valid under the following conditions: 1) is an integrable function of with respect to ; 2) For almost all , exists for all ; 3) There is an integrable function such that for all and almost all . we can apply the SL logic to this setting by constructing a matrix that is a consistent estimator of . In particular, viewing as a centred summary statistic, we can follow Wood, (2010) and approximate the distribution of using a mean-zero Gaussian distribution with variance , which produces the following BSL posterior

| (2) |

where , and where the notation encodes the posteriors dependence on .333This distributional approximation takes as mean-zero Gaussian with variance . The term in (2) follows by re-arranging . Critically, unlike standard BSL methods, the posterior in (2) will not lead to a loss in information since, asymptotically, the information in is the same as in .

While BSL is often applied to intractable models, in our case the exact posterior is tractable, but we replace the information in the full sample with that in the statistic in the hopes that this statistic delivers posterior inferences that are robust to the model misspecification. The posterior amounts to replacing the usual likelihood , with the information in , which resembles a type of (random) quadratic form in the scores . Hence, to differentiate the usual BSL posterior from the posterior in (2), throughout the remainder we refer to as a Q-posterior.

While resembles a quadratic approximation of the log-likelihood, this does not imply that will resemble a Gaussian distribution. More generally, remains meaningful when the parameters are defined over a restricted space, and when the posterior places mass near the boundary of the support. In such cases, a Gaussian approximation to the posterior will not be particularly meaningful. In this way, the Q-posterior differs from existing approaches used to produce well-calibrated Bayesian inference, as it does not rely on post-processing of the accepted draws, or on additional replications of the sampling algorithm. As argued more explicitly in Section 5, post-processing steps are generally based on an implicit, or explicit, normality assumption and thus are not meaningful in cases where the parameter has restricted support. In addition, unlike frequentest methods that seek to correctly quantify uncertainty, the Q-posterior correctly quantifies uncertainty without needing to estimate the second derivative matrix .

The following remarks relate the Q-posterior with several existing approaches in the literature.

Remark 1.

The posterior resembles a form of the generalized posterior of Bissiri et al., (2016) under a (weighted) quadratic loss. In particular, if we have , , and , we have which resembles the generalized posterior based on a (weighted) quadratic loss function. However, our approach is motivated by attempting to produce posteriors with appropriate uncertainty quantification, and not the use of other loss functions within Bayesian inference (see Section 4 for discussion). Moreover, unlike existing generalized Bayes methods the Q-posterior does not require the difficult choice of tuning constant, which can greatly impact the posterior uncertainty quantification produced using generalized Bayesian methods.

Remark 2.

Chernozhukov and Hong, (2003) propose a type of generalized Bayesian inference based on either a set of over-identified estimation equations for , more equations than unknown parameters, by taking a quadratic form of a vector of sample moments (see, also, Chib et al.,, 2018), or by replacing the likelihood altogether with an -estimator criterion; the latter is also used in a decision theoretic framework by Bissiri et al., (2016) to produce their generalized posterior. However, neither approach covers the case where the loss function defining the posterior is based on the score equations from the likelihood. Philosophically, the approaches of Chernozhukov and Hong, (2003) and Bissiri et al., (2016) are based on conducting a form of Bayesian inference by bypassing the likelihood, and not on conducting Bayesian inference using the likelihood in misspecified models. Therefore, from a philosophical standpoint, the two are distinct. Structurally, the two are also distinct since the posterior in (2) and that proposed by the aforementioned authors are of different, but related, forms.

Example 1 (Linear Regression).

Consider the standard linear regression model

where the error distribution is assumed to be , and where and are -dimensional vectors. For simplicity, we consider diffuse priors for these parameters: and . While we believe the model specification for the regression components to be correct, we are uncertain about the error specification. The true data generating process produces observed data under the following specification for the error term: where , and denotes the first element of the vector . When the assumed model with homoskedastic errors is correctly specified, whereas if , the assumed model is misspecified and the exact posterior will likely produce credible sets that are too narrow.

We consider generating observations from the model under the designs of , and ; is generated as tri-variate independent standard Gaussian random vectors, and we set the true values as , and . When the model is misspecified it can be shown that the pseudo-true value of is unchanged and so we focus in this example only on inferences for . We replicate this design 1000 times, and for each dataset sample the exact posteriors using Gibbs sampling, and the Q-posterior is sampled using random walk Metropolis-Hastings (RWMH) with a Gaussian proposal kernel; both posteriors are approximated using 10000 samples with the first 5000 discarded for burn-in. We set the matrix in the Q-posterior to be . Across each dataset and method, we compare the posterior bias, variance and marginal coverage for the regression coefficients.

Table 1 summarizes the results, and demonstrates that the Q-posterior produces results that are similarly located to exact Bayes, but which have larger posterior variance under both regimes. This larger posterior variance produces coverage rates that are close to the nominal 95% level, and much more so than under the exact posterior. Even in the homoskedastic regime (), the exact posterior has converge rates around 85%, while in the heteroskedastic regime (), the lowest level of coverage is less than 70%.

| Q-posterior | Exact | |||||

|---|---|---|---|---|---|---|

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.0009 | 0.0395 | 0.9720 | -0.0110 | 0.0104 | 0.8380 | |

| 0.0188 | 0.0388 | 0.9680 | -0.0049 | 0.0103 | 0.8370 | |

| -0.0212 | 0.0408 | 0.9710 | -0.0103 | 0.0105 | 0.8540 | |

| Q-posterior | Exact | |||||

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.0072 | 0.0520 | 0.9590 | -0.0215 | 0.0104 | 0.6860 | |

| -0.0265 | 0.0343 | 0.9660 | -0.0196 | 0.0104 | 0.8380 | |

| -0.0027 | 0.0277 | 0.9680 | -0.0082 | 0.0104 | 0.8440 | |

2.2. Conjugacy for Exponential Family Models in Natural Form

Consider the case where where is a vector of sufficient statistics, a reference measure on , and the log-partition function. Then, the joint density takes the form

where .

Consider that our goal is inference on the natural parameters . Then, we can show that the Q-posterior has a closed-form expression so long as our prior for is conjugate. In particular, it is simple to see that the above model has average scores , where . Since is non-random, the variance of can be estimated using the sample variance which does not depend on .444More generally, any consistent estimator of could also be used. One could then consider inference on using , where

Define the mean form parameter by the function . In regular models the function exists and is invertible for all . The parameter is referred to as the mean parameterization of the model and satisfies . The form of the Q-posterior for then follows by finding the Q-posterior for , and using the change of variables formula.

Lemma 1.

Consider that . If our (transformed) prior beliefs for the mean parameter can be written as , then the Q-posterior for is , where

Lemma 1 demonstrates that for exponential families in normal form, the Q-posterior for the natural parameters is a transformed Gaussian density.555So long as the (transformed) prior under the mean parameterization, , can be written as a Gaussian kernel. Interestingly, calculation of can be entirely avoided by first sampling , and then (numerically) inverting the equation to obtain the draw . The latter can be carried out in any case where can be reliably calculated.

3. Estimated Likelihoods

The Q-posterior in (2) requires that , and are known up to . In many interesting cases, however, the observed data likelihood is only expressible as

where is called the complete-data likelihood, , and () are unobservable. In such cases, is often intractable, and we cannot obtain analytic, or computationally tractable, forms for and . Further, while it may be feasible to obtain an estimator of the likelihood, say , differentiating to obtain an estimator for may be undesirable; in many cases, may not be differentiable in , as is the case with particle filtering methods. Consequently, we must somehow approximate to extend the Q-posterior to cases where must be estimated.

Fisher’s identity (Cappé et al.,, 2005) is a relationship between the gradient of the observed log-likelihood, , and the complete data log-likelihood , which allows us to express as

where is the posterior for conditional on . Given draws (), we can estimate using the simple Monte Carlo estimator

where, again, denotes all simulated variables necessary to construct .666For notational simplicity, we disregard the estimators dependence on , as we will later take as a function of . All we require to obtain , and by extension an estimator of , is that we can generate samples from .777While more efficient estimators of can be obtained, such as those based on importance sampling, the simple Monte Carlo estimator is both effective and theoretically convenient to analyze. We conjecture that more efficient estimators can be used, but leave a formal study of such estimators for future research.

The ability to generate draws from is not particularly restrictive, as we do not require that be available in closed-form. As the following examples demonstrate, this is feasible in many cases, such as, e.g., state-space models, and generalized random effects models.

Example 2.

In state space models the complete-data likelihood can often be written as

where is the transition density of some unobservable (state) process , is the conditional density of , and is the invariant measure of the states, and where the process is conditionally independent given .

The Markovian nature of the states implies that filtering and smoothing methods can be used to produce draws from . In addition, there are many situations, such as linear-Gaussian models and some stochastic volatility models, where draws from can be obtained using Gibbs or MH sampling algorithms. Regardless of how draws from are obtained, can be estimated using

for . Further, given values of and , and can often be calculated in closed-form.

Example 3.

Random effects models are ubiquitous in the analysis of clustered and longitudinal data. In such models, the outcome variable, , and , is influenced by a vector of covariates and an unobservable random effect . In most cases, conditional on a scale parameter , the random effects are assumed to be iid, so that their joint distribution is , with a mean-zero distribution, known up to . Conditional on and , the distribution of the outcomes is , where is a member of the exponential family that depends on the linear index , and where is a vector of regression parameters, so that . The complete-data likelihood again has a product form, and given posterior draws from , the estimator can be constructed as before.

Fisher’s identity and simple Monte Carlo allow us to approximate by averaging draws from , where, for each , the -th draw depends on random variables . Concatenating all such random variables as , we denote the simulated estimator of the score equations, , as , and let denote an estimator of the variance of . These functions dependence on is similar to the pseudo-marginal literature, where the likelihood estimator is also viewed as dependent on simulated variables .

Given , and , posterior inferences for can proceed using, e.g., a RWMH-MCMC scheme that replaces the intractable with the estimated version

See Algorithm 1.

3.1. Posterior Target, and Behavior in Large Samples

The need to estimate , via , and the replacement of the intractable “likelihood term” within the MCMC algorithm by results in an algorithm that does not deliver draws from , the posterior we would like to target if were tractable. Following the results of Andrieu and Roberts, (2009), Algorithm 1 can be viewed as an exact MH algorithm on with stationary distribution

where . Therefore, the marginal posterior for from Algorithm 1 is

Unlike standard pseudo-marginal methods, is a biased estimator of the posterior kernel . Consequently, the use of within an MCMC algorithm results in a posterior that does not agree with in (2).

The posterior is only expressible as an intractable integral, so that deriving anything concrete about its behavior for fixed and seems infeasible. However, so long as we can ensure that is uniformly close to , as for any .

3.1.1. Main Result

To control the behavior of we must control the behavior of . We achieve this control under certain moment assumptions on and .

Assumption 1.

There exists a function such that the following are satisfied for all and for .

-

(1)

.

-

(2)

.

-

(3)

For an appropriate matrix norm, some , large enough, and all , , and .

Assumption 1 restricts the behavior of the estimators used for and . Assumption 1(1-2) require that the simulation-based estimators have second moments in that are bounded by some function . Assumption 1(3) gives a relationship between the infeasible , i.e., covariance of the scores, and the function that bounds their moments, . Such an assumption is similar to those required when carrying out perturbation analyses for the solution of linear systems (Chapter 5.8 in Horn and Johnson,, 2012). Together, these restrictions allow us to upper bound the mean and variance of . As we are unaware of a general result that bounds the mean and variance of a quadratic form with a random weighting matrix, we provide such a general result as Lemma 6 in Appendix A, which may itself be of independent interest.

Theorem 1.

For all assume that exists, and for some known function , assume that , and . If Assumption 1 is satisfied, then as

Theorem 1 demonstrates that, for , the difference between the intractable posterior and its ‘estimated version’ , converges to zero at rate . This result is not an ‘in probability’ result, and is true for any fixed , as . Furthermore, this equivalence holds for any function of such that : posterior moments calculated from are equivalent to those based on the intractable , at order . Thus, for large, Theorem 1 implies that , and its moments, , behave precisely as if and were known.

Intuitively, Theorem 1 implies that for large, inferences based on the feasible posterior , are uniformly close to those of the infeasible posterior that we would hope to target if the likelihood was analytically tractable. An immediate implication of Theorem 1 is that if has credible sets that are well-calibrated, then credible sets based on will also be well-calibrated, even though the likelihood must be estimated to feasibly conduct inference.

3.1.2. Uncertainty Quantification

If we are willing to make additional assumptions regarding the behavior of and , we can formally demonstrate that and have credible sets that are asymptotically well-calibrated, regardless of whether the model is, or is not, correctly specified. Importantly, unlike frequentist methods for models with latent variables, credible sets obtained from do not require the calculation of second-derivative information.

Before presenting our regularity conditions and results, we collect here notations that are used to simplify the statement of the result. For a positive sequence as , we say that if the sequence converges to zero in probability, while we use the notation to denote that is bounded in probability. For a set , let denote the interior of . The notation denotes weak convergence under .

Assumption 2.

There exists a function such that:

-

(1)

.

-

(2)

There exist a unique , such that, iff .

-

(3)

For some , is continuously differentiable over , and is invertible.

-

(4)

There exists a positive semi-definite matrix , such that .

-

(5)

For any , there is a such that

We require that the weighting matrix satisfy the following assumption.

Assumption 3.

The following conditions are satisfied for some : (i) for large enough, the matrix is positive semi-definite and symmetric uniformly over , and positive-definite for all ; (ii) there exists some matrix , positive semi-definite, and symmetric, uniformly over , and such that , and, for all , is continuous and positive-definite; (iv) ; (v) for any , .

Remark 3.

Assumptions 2 and 3 jointly enforce smoothness and identification conditions for the infeasible criterion These conditions permit the existences of a quadratic expansion of that is smooth in near , and with a remainder term that can be suitably controlled. In particular, our assumptions do not require that the loss function is differentiable everywhere, but only that it is equicontinuous. The latter is an important distinction as many loss functions are only differentiable almost surely; e.g., loss functions based on absolute value functions.

The following assumption requires the existence of certain prior moments.

Assumption 4.

For as defined in Assumption 2, and is continuous on . For some , , and for all large enough .

The following result demonstrates that delivers valid (frequentist) uncertainty quantification. Before stating this result, recall that , and define

and .

The following result is a consequence of Lemma 2.

Lemmas 2-3 demonstrate that even when the likelihood must be estimated, so long as it is feasible to simulate draws from , we can accurately quantify uncertainty using (for ). However, if we wish for our posterior means to not be asymptotically biased, due to the need to simulate data, we require that . The latter condition is the same condition on the number of simulated draws required for asymptotically Gaussian point estimation in the context of simulated maximum likelihood estimation (see Shephard and Pitt,, 1997 for early work). Therefore, so long as the number of draws grows appropriately, in any situation to which filtering methods can be applied, the Q-posterior can be used to produce Bayesian inferences that are well-calibrated.

3.1.3. Variance Estimation

In order for Q-posteriors to be well-calibrated, a consistent estimator of is required. In cases where takes the form , for some known functions depending only on the -th sample unit, the matrix can be taken as

| (3) |

If one is worried that in (3) may not be consistent for , we suggest the user employ bootstrapping techniques to estimate the covariance matrix; this can often be achieved using some variation of the estimating equations bootstrap (Hu and Kalbfleisch,, 2000 and Chatterjee and Bose,, 2005). Such an approach can either be directly embedded within the MCMC algorithm, or a preliminary estimator , based on some in the high-probability density region of the posterior, can be used throughout the MCMC algorithm.888The latter follows since Assumption 3 is actually a stronger condition than is required for the validity of Lemma 2. The result can be shown to be satisfied if the matrix is replaced by , where is any preliminary consistent estimator of .

For the Q-posterior , choosing as the sample variance in (3) may not deliver a Q-posterior that is well-calibrated in general. This issue is readily seen even where , so that takes the form

which we note has variability in both and . To see that both pieces of variability matter, write , , , and consider

Since , , and this expectation can be estimated by . However, applying the usual sample covariance estimator to yields

Intuitively, is only an estimator of as the influence of the simulated has already been ‘integrated out’ via the averaging in . Consequently, unless for all , the usual sample covariance estimator for under-estimates the variance, and delivers credible sets that are too narrow.

However, given that is an estimator of , all that remains is to obtain an estimator of . Since , an obvious choice is

where we note that the term in brackets is an estimator of . Critically, since (), is consistent by the usual law of large numbers. This latter feature remains true even if the series displays dependence.

However, we do note that if is dependent, an alternative estimator for is required. Such an estimator can be achieved by replacing with some heteroskedastic and auto-correlation (HAC) consistent covariance estimator (Newey and West,, 1987), or by using bootstrapping methods for the series . For instance, in the case of dependent data, a version of the wild bootstrap (Shao,, 2010) or the stationary bootstrap of Politis and Romano, (1994), applied to the ‘data’ , can be used to obtain consistent estimators of the variance.999Alternatively, the matrix can be estimated using the waste-free SMC sampler Dau and Chopin, (2022) which allows us to obtain, from a single run of the algorithm, a consistent estimator of the asymptotic variance of our particle estimate .

3.2. Example: Random Effects Models

3.2.1. Linear Random Effects Models

To demonstrate the benefits of our generalized approach to Bayesian inference with latent variables we revisit the simple linear regression model in Example 1, and demonstrate that the performance of our approach is similar in cases with latent variables. To this end, we consider the standard linear regression model with random effects

where we assume that the error distribution , and where and are -dimensional vectors, and is an unobservable random effect parameter with assumed distribution . Similarly to the linear regression example given earlier, our main inferential goal is inference on the fixed effect parameters .

Priors for and are the same given before, and now we augment this with the additional prior for , where . Under this prior choice, and conditional on , and , the conditional posterior for the random effects is known in closed-form: letting denote the -dimensional matrix with columns , and an -dimensional identity matrix,

More generally, the conditional posteriors for and are also known in closed-form.

Similarly to the linear regression example, suppose we again wish to ensure that our inferences for are robust to possible deviations from the modelling assumptions regarding the error term ; and in particular the possible form and presence of heteroskedasticity. Given that the conditional posterior is known in closed-form in this example, this can be achieved by estimating and using independent sets of draws from the conditional posterior .

Consequently, inference for can proceed using a (pseudo-marginal) Metropolis-within-Gibbs scheme, whereby for each Metropolis step for we evaluate the loss by first sampling from , then forming and then deciding whether to accept or reject according to the usual criterion. We now implement such a sampling approach using simulations from the conditional posterior to estimate the gradient and its variance, at each step of the algorithm.

Similarly to Example 1, we generate observed data from the linear regression model under the following specification for the disturbance term: where , and denotes the first element of the vector . Clearly, when the DGP is homoskedastic, whereas if , the exact posterior will likely produce credible sets that are too narrow to yield reliable coverage. Alternatively, from Lemmas 2-3 suggest that the generalized posterior we propose correctly quantifies uncertainty regardless of the value of .

To this end, we generate observations from the assumed DGP under the designs of , and , where the are generated as tri-variate independent standard Gaussian random vectors, and we set the true values as , and . We replicate this design 1000 times, and for each dataset sample the exact posterior using Gibbs sampling, and the generalized posterior using the RW sample in Algorithm 1, both posteriors are approximated using 10000 samples with the first 5000 discarded for burn-in. Across each data set and method, we then compare the posterior bias, variance and coverage for the regression coefficients. Table 2 summarises the repeated sampling results.

| Q-posterior | Exact | |||||

|---|---|---|---|---|---|---|

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.0519 | 0.0310 | 0.9350 | -0.0804 | 0.0555 | 0.9820 | |

| -0.0017 | 0.0220 | 0.9320 | -0.0015 | 0.0154 | 0.8830 | |

| -0.0132 | 0.0299 | 0.9450 | -0.0136 | 0.0208 | 0.8880 | |

| 0.0079 | 0.0295 | 0.9200 | 0.0076 | 0.0191 | 0.8490 | |

| Q-posterior | Exact | |||||

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.0572 | 0.0308 | 0.9300 | -0.0844 | 0.0536 | 0.9800 | |

| -0.0047 | 0.0474 | 0.9150 | -0.0060 | 0.0206 | 0.7620 | |

| -0.0034 | 0.0312 | 0.9290 | -0.0034 | 0.0194 | 0.8740 | |

| 0.0000 | 0.0296 | 0.9290 | 0.0001 | 0.0191 | 0.8480 | |

Similarly to the simple linear regression example, the results in Table 2 demonstrate that our generalized Bayes approach based on estimated likelihood gradients produces results that are similar to exact Bayes when the model is correctly specified. However, while the coverage rates for exact Bayes are relatively far from the nominal levels under both correct specification and misspecification , our approach produces coverage rates that are very close to the nominal 95% level in both settings.

3.2.2. Generalized Linear Random Effects Models

We observe binary outcomes on individual from group , , and let denote a vector of strictly exogenous regressors. In particular, we believe that the outcomes are generated according to a binary random effects probit model of the form

| (4) |

for individual , with observations per individual, where denotes the unobservable random effect for individual , and denotes the standard Gaussian CDF. Similarly to the linear random effects case, we again take the prior on to be diffuse, . The standard assumption on the random effects parameter is that . However, the very nature of the random effect term makes its precise parametric representation unclear.

This section demonstrates how to apply the Q-posterior in this model, and compares our approach against the exact posterior in the case where the random effects are correctly and incorrectly specified. For simplicity, we take , and denote quantities using only the sub-script, however, the case proceeds similarly.

Conditional on , the complete-data likelihood is

note that the only occurrence of comes from the contribution in the density components . Using Fisher’s identity, the log gradient with respect to is

where

while the gradient with respect to is

Unlike the linear case, is analytically intractable in this generalized linear model. However, following the approaches of Zeger and Karim, (1991) and McCulloch, (1997), it is possible to reliably generate samples from using a Metropolis-Hastings algorithm based on the proposal .

It is then feasible to use a Metropolis-within-Gibbs approach to evaluate the Q-posterior, whereby at the -th step we sample paths , , and then use these draws to estimate the gradients. Once the gradients have been estimated, their variance can be estimated using the methods discussed in Section 3.1.3.

We now compare the behavior of the Q-posterior and the exact posterior in the random effects probit model. We generate sample observations from the random effects probit model under two different distributions for the random effects distribution: the first DGP correctly assumes that the random effect distribution is ; while in the second DGP the actual distribution of the random effects is student-t with four degrees of freedom, so that the assumed model is misspecified under the second design. The regressor is again generated as tri-variate independent standard Gaussian random vectors, and we set the true values as . In both cases the scale of the random effects parameter is set to unity.

We replicate these two design 1000 times, and for each dataset sample the exact posteriors using a Gibbs-within-Metropolis sampling scheme, similar to Zeger and Karim, (1991). The Q-posterior is also sampled using a Gibbs-within-Metropolis discussed above, and where we use draws from the conditional posterior in all experiments.101010Since this is a Gibbs-within-Metropolis scheme, we run the sampler to obtain draws of , and then discard the first for burn-in. Both posteriors are approximated using 10000 samples with the first 5000 discarded for burn-in. Across each data set and method, we then compare the posterior bias, variance and coverage for the regression coefficients. Table 3 summarises the repeated sampling results.

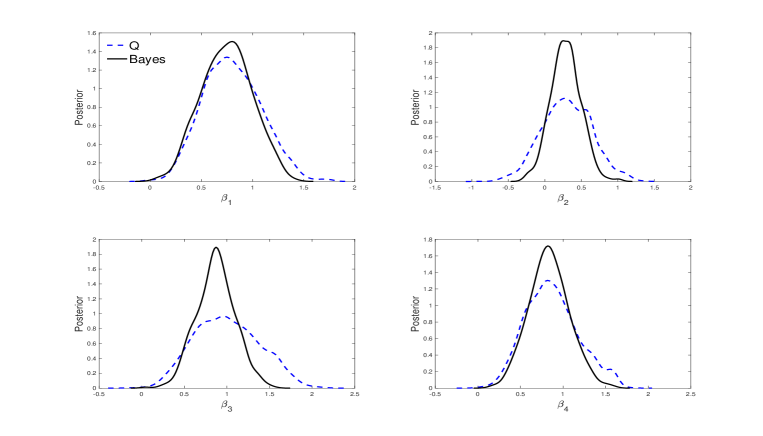

Similarly to the other examples, the Q posterior delivers posterior locations that are similar to those of exact Bayes, but again its uncertainty quantification remains close to the nominal level regardless of correct or incorrect model specification. In contrast, since the variances of exact Bayes are (on average) smaller than those given by the Q-posterior, the coverage of the exact Bayes posteriors is generally further away from the nominal level than for the Q-posterior. This difference is particularly stark for the corresponding posteriors themselves, which we plot in Figure 1 for one particular replication under the misspecified DGP. In this case, it is clear that while the posteriors have similar locations, their scales are quite different. It is this increase in uncertainty that produces reliable uncertainty quantification even though the model is misspecified.

| Q-posterior | Exact | |||||

|---|---|---|---|---|---|---|

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.0438 | 0.0358 | 0.9760 | -0.1016 | 0.0266 | 0.9060 | |

| -0.0414 | 0.0375 | 0.9740 | -0.0841 | 0.0306 | 0.9420 | |

| -0.0360 | 0.0339 | 0.9680 | -0.0955 | 0.0344 | 0.9160 | |

| -0.0352 | 0.0396 | 0.9780 | -0.0863 | 0.0298 | 0.9280 | |

| Q-posterior | Exact | |||||

| Bias | Var | Cov | Bias | Var | Cov | |

| -0.1255 | 0.0365 | 0.9440 | -0.1638 | 0.0249 | 0.8350 | |

| -0.1053 | 0.0401 | 0.9480 | -0.1509 | 0.0273 | 0.8450 | |

| -0.1208 | 0.0391 | 0.9440 | -0.1607 | 0.0277 | 0.8450 | |

| -0.1171 | 0.0405 | 0.9490 | -0.1595 | 0.0282 | 0.8520 | |

4. General Loss Function Posteriors

When the model is misspecified there is no reason to assume that the KL minimizer delivers inferences that are fit for purpose. A solution to this issue is to instead conduct inference using generalized posteriors, which produce Bayesian inferences using a loss function that is specific to the problem at hand. To ensure Bayesian inferences remain fit for purpose in misspecified models, Bissiri et al., (2016) suggest replacing the likelihood posterior update with that based on a loss function that is important to the specific inferential task at hand. If one then considers as a cumulative loss function over the observed sample, a posterior update can be based on the generalized posterior

for some learning rate .

While useful, generalized posteriors are not well-calibrated, and do not correctly quantify uncertainty in general; see Section 4 of Miller, (2021) for a discussion, and the references therein, for a discussion of existing methods to circumvent this issue. In this section, we demonstrate that the Q-posterior can be equally applied to generalized Bayesian posteriors to deliver valid uncertainty quantification. Given , we can represent the information in this loss by the set of -dimensional estimating equations , where we assume that these derivatives exists for all , and each .111111In general, all we will require is that this derivative exists with probability one, which permits the case where the derivatives are not defined at a countable collection of points; e.g., such as the case where our loss function is median loss. Letting be an estimator of , we can update our prior beliefs to posterior beliefs using the following Q-posterior

| (5) |

Given the results in Section 3.1, the Q-posterior should deliver a generalized Bayesian posterior that correctly quantifies uncertainty without the need to choose any tuning constants; see Theorem 2 for details. Before presenting this result, we first demonstrate the applicability of the Q-posterior by showing in a simple example that correctly quantifies uncertainty in the context of Bayesian inference for an unknown parameter based on a general loss function.

4.1. Robust Quantile Inference

Consider observing an iid sequence from the model

where the unknown parameter has prior density and is independent of . Following Doksum and Lo, (1990), for reasons of robustness, we do not wish to estimate the posterior of from but from the sample median ; for a related approach see Lewis et al., (2021). When has density , this then gives rise to the exact posterior distribution

when is odd.

Given the above form of the posterior, Miller, (2021) suggests instead generalized Bayesian inference for using the simpler loss function . While Miller, (2021) demonstrates that such a posterior is well-behaved in large samples, the resulting posterior does not have correct coverage even when the model is correctly specified. In contrast, we suggest conducting Bayesian inference using the Q-posterior, which would be based on the gradient of the above loss, with respect to ,

The variance of the , for any , can be consistently estimated using the iid bootstrap. Letting denote such an estimate; we can then conduct inference on using the Q-posterior

In this example, we use the estimating equations bootstrap (see, Hu and Kalbfleisch,, 2000 and Chatterjee and Bose,, 2005 for discussion) to compute the matrix at every value of .

We now compare the uncertainty quantification produced using the generalized and Q-posteriors in correctly and misspecified models. In both cases, we assume is a standard Gaussian distribution. In the first experiment, referred to as DGP1, observed data is generated from a Gaussian distribution with mean , and with variance 4. In the misspecified regime, referred to as DGP2, we generate observed data from a mixed Gaussian distribution with parameterization

In the first case the true median is unity, while in the second case the true median of the data is actually approximately .121212This value must be found numerically by inverting the cdf of the mixture distribution. We simulate 1000 observed datasets from both DGPs and compare the results of generalized Bayes and that based on the Q-posterior. Table 4 compares the posterior means, variances and coverage of the two procedures. The results demonstrate that the generalized posterior suggested by Miller, (2021) does not produce reliable coverage for the true median, while the coverage of the Q-posterior is again close to the nominal level.

| Q-posterior | Exact | |||||

|---|---|---|---|---|---|---|

| DGP1 | Bias | Var | Cov | Bias | Var | Cov |

| -0.0031 | 0.0654 | 0.9420 | -0.0031 | 0.0152 | 0.6700 | |

| DGP2 | Bias | Var | Cov | Bias | Var | Cov |

| -0.0115 | 0.0607 | 0.9360 | -0.0118 | 0.0157 | 0.7160 | |

4.2. Uncertainty Quantification

If the regularity conditions maintained for and in the likelihood-based Bayesian context are satisfied for and in the generalized Bayesian context, then the posterior correctly quantifies uncertainty.

Theorem 2.

The generalized Bayesian posterior of Bissiri et al., (2016) has credible sets whose width is determined by , whereas, those of the Q-posterior are determined by , which ensures that correctly quantifies uncertainty. Existing approaches to coverage correction in generalized Bayesian inference rely on ex-post processing of the posterior and calculating second-derivative information, e.g., Holmes and Walker, (2017), Syring and Martin, (2019), Giummolè et al., (2019), or the application of expensive bootstrapping procedures, e.g., Matsubara et al., (2021). In contrast, our approach requires no post-processing and delivers an intrinsically (generalized) Bayesian solution to the problem of well-calibrated generalized posterior inferences.

Remark 4.

A common class of generalized posteriors occurs when is itself obtained from a pseudo-likelihood of some sort, including partial likelihoods (Cox,, 1975) and composite likelihoods (Lindsay,, 1988, and Varin et al.,, 2011). For example, Sections 5 and 7 of Miller, (2021) give several useful examples of such approaches and their link with generalized posteriors. However, as acknowledged by Miller, (2021), generalized posteriors built from these loss functions “do not exhibit correct coverage, even asymptotically.” However, in each of the cases covered in Miller, (2021), the loss function is sufficiently smooth to permit its representation in terms of the Q-posterior in (5). Hence, for instance, so long as the composite likelihood is sufficiently smooth in , we can apply the Q-posterior to produce generalized Bayesian inferences based on this loss function that have correct coverage.

5. Discussion and Conclusions

5.1. Alternative Approaches

In a likelihood context, when the model is correctly specified we have that , and the Q-posterior and exact posterior asymptotically agree. However, if the model is misspecified, the Q-posterior still yields credible sets that are well-calibrated; such a result will only hold if is a consistent estimator of . Otherwise, the Q-posterior will not correctly quantify uncertainty. As discussed in Section 3.1.3, however, in most cases reliable estimators of are available using existing formulas, or bootstrapping methods.

The Q-posterior approach represents a significant departure from existing approaches to Bayesian inference in possibly misspecified models. Two approaches that have so far received meaningful attention are the ‘sandwich’ correction suggested in Müller, (2013), and the BayesBag approach, see Huggins and Miller, (2019).

Müller,’s approach amounts to correcting the draws from the standard posterior using the explicit Gaussian approximation , where is the posterior mean. Such a correction can be implemented either by drawing directly from a multivariate normal, or by taking each posterior draw and modifying it according to the linear equation

see, also, Giummolè et al., (2019) for a related approach in the case of generalized posteriors built using scoring rules. We argue that this ex-post correction is sub-optimal for several reasons: firstly, philosophically, it amounts to the application of frequentist principles to the output of a Bayesian learning algorithm, and thus is not intrinsically Bayesian; second, it requires the explicit calculation of second-derivatives, which can be difficult and may be ill-behaved; thirdly, this Gaussian approximation is poor when posteriors are not roughly Gaussian, such as when the parameters have restricted support, or when we have small sample sizes; finally, this correction can easily produce a value of lying outside the support of , for instance, when is a bounded subset of .131313While it may be feasible to transform the draws so that they are restricted to the appropriate space, such transformations may not be invariant, and the choice of which transformation to utilize generally has no theoretical basis.

An alternative approach is the use of posterior bagging, as suggested in the BayesBag approach; see Huggins and Miller, (2019) for an in-depth discussion of BayesBag. This procedure attempts to correct posterior coverage through bagging. Letting denote bootstrap indices, and the -th bootstrap sample, where is sampled with replacement from the original dataset. The BayesBag posterior is given by

BayesBag is easy to use, and requires no additional algorithmic tools. However, it does require re-running the MCMC sampling algorithm to obtain posterior draws of for each . The latter can be computationally intensive if the model is high-dimensional or contains latent variables. Even then, Huggins and Miller, (2019) demonstrate that the BayesBag posterior has credible sets that are not well-calibrated. Asymptotically, the BayesBag posterior variance is given by where . Hence, depending on the choice of , the BayesBag posterior displays over-or under-coverage. Only when the parameter is scalar valued, is it possible to choose such that the posterior has valid frequentist coverage; i.e., such that Lastly, the applicability of BayesBag approach itself to models with weakly dependent data, or when the likelihood is intractable, does not seem straightforward.

In contrast with the ex-post correction approach and BayesBag, the Q-posterior does not require any ex-post sampling correction, or bootstrapping approaches to obtain well-calibrated posteriors. Moreover, it is feasible to use the Q-posterior in cases where pseudo-marginal methods are required to conduct Bayesian inference.

5.2. Conclusion

We have proposed a new approach to Bayesian inference, referred to generally as Q-posteriors, that deliver reliable uncertainty quantification. In likelihood-based settings the Q-posterior can be thought of as a type of Bayesian synthetic likelihood (Wood,, 2010) posterior where we replace the likelihood for the observed sample with an approximation for the likelihood of the score equations. The critical feature of the Q-posterior is that it is guaranteed to deliver credible sets that are asymptotically well-calibrated regardless of model specification, while if the model is correctly specified the Q-posterior agrees with the exact posterior (in large samples). Critically, even when the likelihood must be estimated due to the presence of latent variables, the Q-posterior still delivers well-calibrated inferences under fairly weak regularity conditions.

When applied to generalized Bayesian posteriors (Bissiri et al.,, 2016), we have shown that the Q-posterior remains well-calibrated. All existing approaches of which we are aware attempt to correct the coverage of generalized posteriors use either ex-post correction of the posterior draws, which are ultimately based on some (implicit) normality assumption on the resulting posterior draws, or may require complicated bootstrapping approaches. In contrast, the Q-posterior delivers correct uncertainty quantification without the need of any additional tuning or ex-post correction of the draws.

When the likelihood is intractable and must be estimated, a version of the Q-posterior can be constructed using Fisher’s identity and simple Monte Carlo estimators. In principle, it would be feasible to apply other Monte Carlo approaches, such as importance sampling, to construct the Q-posterior. This paper restricts itself to simple Monte Carlo estimators as they are the easiest to apply, and theoretically analyze. In ongoing work by the authors, we explore the use of sequential importance sampling estimators, and the resulting performance of the Q-posterior is similar. However, in such cases, analysing the behavior of the posterior becomes more difficult due to the sequential nature of the Monte Carlo estimators, and obtaining theoretical results similar to those in the Theorem 1 becomes more onerous. We leave this important question for future research.

References

- Andrieu and Roberts, (2009) Andrieu, C. and Roberts, G. O. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. The Annals of Statistics, 37(2):697–725.

- Bissiri et al., (2016) Bissiri, P. G., Holmes, C. C., and Walker, S. G. (2016). A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(5):1103–1130.

- Cappé et al., (2005) Cappé, O., Moulines, E., and Rydén, T. (2005). Springer series in statistics.

- Chatterjee and Bose, (2005) Chatterjee, S. and Bose, A. (2005). Generalized bootstrap for estimating equations. The Annals of Statistics, 33(1):414–436.

- Chernozhukov and Hong, (2003) Chernozhukov, V. and Hong, H. (2003). An MCMC approach to classical estimation. Journal of Econometrics, 115(2):293–346.

- Chib et al., (2018) Chib, S., Shin, M., and Simoni, A. (2018). Bayesian estimation and comparison of moment condition models. Journal of the American Statistical Association, 113(524):1656–1668.

- Cox, (1975) Cox, D. R. (1975). Partial likelihood. Biometrika, 62(2):269–276.

- Dau and Chopin, (2022) Dau, H.-D. and Chopin, N. (2022). Waste-free sequential Monte Carlo. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 84(1).

- Doksum and Lo, (1990) Doksum, K. A. and Lo, A. Y. (1990). Consistent and robust Bayes procedures for location based on partial information. The Annals of Statistics, 18(1):443–453.

- Drovandi et al., (2021) Drovandi, C., Nott, D. J., and Frazier, D. T. (2021). Contributed discussion on Bayesian restricted likelihood methods: Conditioning on insufficient statistics in Bayesian regression. Bayesian Analysis, 16(4):1393–1462.

- Frazier et al., (2022) Frazier, D. T., Nott, D. J., Drovandi, C., and Kohn, R. (2022). Bayesian inference using synthetic likelihood: asymptotics and adjustments. Journal of the American Statistical Association, (just-accepted):1–28.

- Giummolè et al., (2019) Giummolè, F., Mameli, V., Ruli, E., and Ventura, L. (2019). Objective Bayesian inference with proper scoring rules. Test, 28(3):728–755.

- Holmes and Walker, (2017) Holmes, C. C. and Walker, S. G. (2017). Assigning a value to a power likelihood in a general Bayesian model. Biometrika, 104(2):497–503.

- Horn and Johnson, (2012) Horn, R. A. and Johnson, C. R. (2012). Matrix analysis. Cambridge university press.

- Hu and Kalbfleisch, (2000) Hu, F. and Kalbfleisch, J. D. (2000). The estimating function bootstrap. Canadian Journal of Statistics, 28(3):449–481.

- Huggins and Miller, (2019) Huggins, J. H. and Miller, J. W. (2019). Robust inference and model criticism using bagged posteriors. arXiv preprint arXiv:1912.07104.

- Jewson and Rossell, (2021) Jewson, J. and Rossell, D. (2021). General Bayesian loss function selection and the use of improper models. arXiv preprint arXiv:2106.01214.

- Kleijn and van der Vaart, (2012) Kleijn, B. J. and van der Vaart, A. W. (2012). The Bernstein-von-Mises theorem under misspecification. Electronic Journal of Statistics, 6:354–381.

- Lehmann and Casella, (2006) Lehmann, E. L. and Casella, G. (2006). Theory of point estimation. Springer Science & Business Media.

- Lewis et al., (2021) Lewis, J. R., MacEachern, S. N., and Lee, Y. (2021). Bayesian restricted likelihood methods: Conditioning on insufficient statistics in Bayesian regression (with discussion). Bayesian Analysis, 16(4):1393–1462.

- Lindsay, (1988) Lindsay, B. G. (1988). Composite likelihood methods. Contemporary mathematics, 80(1):221–239.

- Loaiza-Maya et al., (2021) Loaiza-Maya, R., Martin, G. M., and Frazier, D. T. (2021). Focused Bayesian prediction. Journal of Applied Econometrics, 36(5):517–543.

- Matsubara et al., (2021) Matsubara, T., Knoblauch, J., Briol, F.-X., Oates, C., et al. (2021). Robust generalised Bayesian inference for intractable likelihoods. arXiv preprint arXiv:2104.07359.

- McCulloch, (1997) McCulloch, C. E. (1997). Maximum likelihood algorithms for generalized linear mixed models. Journal of the American Statistical Association, 92(437):162–170.

- Miller, (2021) Miller, J. W. (2021). Asymptotic normality, concentration, and coverage of generalized posteriors. Journal of Machine Learning Research, 22:168–1.

- Müller, (2013) Müller, U. K. (2013). Risk of Bayesian inference in misspecified models, and the sandwich covariance matrix. Econometrica, 81(5):1805–1849.

- Newey and West, (1987) Newey, W. K. and West, K. D. (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3):703–708.

- Politis and Romano, (1994) Politis, D. N. and Romano, J. P. (1994). The stationary bootstrap. Journal of the American Statistical Association, 89(428):1303–1313.

- Price et al., (2018) Price, L. F., Drovandi, C. C., Lee, A., and Nott, D. J. (2018). Bayesian synthetic likelihood. Journal of Computational and Graphical Statistics, 27(1):1–11.

- Shao, (2010) Shao, X. (2010). The dependent wild bootstrap. Journal of the American Statistical Association, 105(489):218–235.

- Shephard and Pitt, (1997) Shephard, N. and Pitt, M. K. (1997). Likelihood analysis of non-Gaussian measurement time series. Biometrika, 84(3):653–667.

- Syring and Martin, (2019) Syring, N. and Martin, R. (2019). Calibrating general posterior credible regions. Biometrika, 106(2):479–486.

- Syring and Martin, (2020) Syring, N. and Martin, R. (2020). Robust and rate-optimal Gibbs posterior inference on the boundary of a noisy image. The Annals of Statistics, 48(3):1498–1513.

- Varin et al., (2011) Varin, C., Reid, N., and Firth, D. (2011). An overview of composite likelihood methods. Statistica Sinica, 21(1):5–42.

- White, (1982) White, H. (1982). Maximum likelihood estimation of misspecified models. Econometrica, 50(1):1–25.

- Wood, (2010) Wood, S. N. (2010). Statistical inference for noisy nonlinear ecological dynamic systems. Nature, 466(7310):1102–1104.

- Wu and Martin, (2020) Wu, P.-S. and Martin, R. (2020). A comparison of learning rate selection methods in generalized Bayesian inference. arXiv preprint arXiv:2012.11349, 6.

- Zeger and Karim, (1991) Zeger, S. L. and Karim, M. R. (1991). Generalized linear models with random effects; a Gibbs sampling approach. Journal of the American Statistical Association, 86(413):79–86.

Appendix A Main Lemmas

This section contains lemmas that are used to prove the results in the main text, and are of independent interest. We first establish the following additional notation used throughout the remainder of this appendix. For two (possibly random) sequences we say that if for some large enough, and all , there exists a such that (almost surely); while we write if and (almost surely). For a known function , we will denote the expectation of wrt a probability measure as . Throughout, we abuse notation and let denote the Euclidean norm in the case of vectors or a convenient matrix norm. The latter abuse of notation is immaterial since we will only treat vectors and matrices of fixed length.

Lemma 4.

Let with , and let (resp., ), , denote the coordinates of (resp., ). Let be a positive semi-definite matrix with for some matrix . Assume that, for some , and each , , and for , , then

Proof.

Write

Then,

From Cauchy-Schwartz,

so that

Now, we bound using the moment hypothesis in the statement of the result. In particular,

and

For positive semi-definite matrices of conformable dimension, we have the following inequality

Using properties of , and the above inequality, we can obtain

Applying the two displayed equations then yields

∎

The following lemma is used to extend the result in Lemma 4 to the case where the matrix in the quadratic form is random.

Lemma 5.

Let be positive-definite, and with , then

Proof.

Since , and , is non-singular. Write

so that

| (6) |

It remains to bound . By the Woodbury identify,

where the second to last inequality follows since .

By the triangle inequality,

implying that

Placing the above into equation (6) then yields the result. ∎

Lemma 6.

Let with , and variance , and let be iid observations with the same distribution as . Also, let (resp., ), , denote the coordinates of (resp., ), and denote by their sample mean. Let be a random covariance matrix such that for some (random) square-root matrix . For some , and each , the following moment assumptions are satisfied: for each , and , , , , and

If as , then

and

Remark 5.

The moment assumptions in Lemma 6 for are precisely the same as those required in Lemma 4. The condition , as is required in order to apply the perturbation result in Lemma 5. Such a condition is useful as it allows us to bound the moments of using moment of , rather than moments of , which is less interpretable. Along with the other conditions, the moment assumptions on is enough to control the first two moments of , which depend on the variance , as well as the variance of .

Proof.

We first prove the mean result. From the law of iterated expectations, and properties of quadratic forms

For real, square matrices of similar dimension, and the Frobenius norm of , recall the inequality

Over matrices of fixed dimension, all matrix norms are equivalent, and we have that

for some finite and our chosen matrix norm . Using the triangle inequality and the above inequality then yields

By Lemma 5, for large enough such that ,

| (7) |

Applying equation (7) then yields

Taking expectations,

where we have used the fact that , and .

To upper bound the variance, we use the law of iterated variance:

| (8) |

and control each term separately. For the first term in (8), we can directly apply Lemma 4, conditional on and (7), to obtain the bound

and applying the moment bound on we have

Since , the first term in (8) is upper bounded by for all large enough.

To bound the second term in (8), use the proof of the first expectation, conditional on , to deduce

Take the variance of the above and use Cauchy-Schwartz to obtain

| (9) |

Consider the first term in equation (9); from the trace inequality

Applying equation (7), we have

Hence, using the moment bound assumption,

| (10) |

For the second term in (9), again by the trace inequality, and (7)

since . Thus, similar to the first term in (9)

| (11) |

∎

Lemma 7.

Let be a positive, scalar-valued random variable with mean that satisfies for some . Then, for any ,

Proof.

For any , a Taylor expansion of around yields

where is the truncation of the series

and is the Lagrange remainder term,

with a constant between and .

Boundedness of over , implies that for any and

Consequently,

By hypothesis, for some . Take expectations of both sides to obtain

∎

The following result demonstrates that if the regularity conditions in Assumptions 2-4 are satisfied for and , then the (possibly infeasible) Q-posterior is asymptotically Gaussian. Of course, if the regularity conditions are satisfied with and , then the result also applies to the Q-posterior based on the loss function with (see Section 4 for details).

Proof of Lemma 8.

The approach used to prove this result is similar to that given in Lehmann and Casella, (2006), Theorem 8.2, Ch 6, as well as Theorem 1 in Chernozhukov and Hong, (2003). Our proof differs, however, since the matrix is allowed to be singular away from , and since is not assumed compact. This makes the proof most similar to Lemma 1 in Frazier et al., (2022).

Throughout the remainder of this proof, let us abuse notation and define

For an appropriately defined remainder term , we have the identity

| (12) |

where , and . Define ,

and apply (12) to see that

Recalling , and for ,

where

The stated result follows if

where

However,

where

for .

Note that if , then

Therefore, if ,

since for any .

Consequently, the result follows if we can prove that . To demonstrate this, we split into three regions and analyze over each region. For some and , with , the regions are defined as follows. Region 1: ; Region 2: ; Region 3: .

Region 1: Over this region the result follows if

Note that, from Assumptions 3 and 4,

and

since by Assumption 2. Similarly, by Assumption 2,

so that by Lemma 9

Hence, from these equivalences and the dominated convergence theorem.

Region 2: If , then by Assumption 2 and the continuous mapping theorem. Then, for large enough and , where

The first term for any fixed , so that for , by the dominated convergence theorem. For , we have that for any there exists some large enough such that for all , and

Hence, can be made arbitrarily small by taking large enough and small enough.

The result follows if . To this end, we show that, for some , and all , with probability converging to one (wpc1),

| (13) |

If equation (13) is satisfied, then is bounded above by

which can be made arbitrarily small for some large and small. To demonstrate equation (13), first note that by continuity of , Assumption 4, is bounded over so that it may be dropped from the analysis.

Now, since , for any , for all and large enough. Therefore, by Lemma 9 there exists some and large enough so that (wpc1)

where denotes the minimum eigenvalue of . Since , we have . Thus, on the set

and for some

The result follows.

Region 3: For large,

can be made arbitrarily small and is therefore dropped from the analysis. Using the definition of , and the identity , consider

Now,

since by Assumption 2.

Define and note that by Assumption 2 and is positive-definite by Assumption 3. Thus, for any ,

From Assumptions 2 and 3, the first term converges to zero in probability. From Assumption 3, for any there exists an such that

Hence,

| (14) |

Use , the definition , and equation (14) to obtain

where the second inequality follows from the moment hypothesis in Assumption 4. ∎

The following result is used in the proof of Lemma 2 and is a consequence of Proposition 1 in Chernozhukov and Hong, (2003).

Lemma 9.

Proof.

The result is a specific case of Proposition 1 in Chernozhukov and Hong, (2003). Therefore, it is only necessary to verify that their sufficient conditions are satisfied in our context.

Appendix B Proofs of Main Results

Proof of Lemma 1.

Consider the Q-posterior under the mean parameterization , with prior beliefs , where and are known prior hyper-parameters. Writing , we see that

Hence, writing , the Q-posterior for is given by

Algebraic manipulations produce

for

and where the second equality follows from the Woodbury identity, and where

Thus, we see that . For a regular exponential family, the change-of-parameter from exists if the model is identifiable (in ). A change of variables then implies

where the second equality follows since . ∎

Proof of Theorem 1.

We prove the theorem by proving the more general result

Taking delivers the first result, while the second result follows since

Recall the definitions

and

Let denote expectation wrt the simulated data at a fixed and , where the dependence of on and is suppressed for notational simplicity. We first demonstrate that, uniformly over ,

| (15) |

We first bound using the law of iterated expectations and Lemma 6. In particular, taking , , , and , by Lemma 6

Since, under Assumption 1, , for all , it follows that , and we conclude that

| (16) |

We now bound the variance . Using the same definitions as above, Lemma 6 implies that, for large enough, and some ,

Again, by Assumption 1, for all , , so that

| (17) |

Using equations (16) and (17), we can upper bound , for some , using Lemma 7: take , with by definition, and such that ; then

Since the above holds for all , we take without loss of generality for large enough, which yields equation (15).

Under the hypothesis of the result, for all , so that

| (19) |

where the first term on the RHS of the first equation comes from dividing and multiplying the first term by , which is finite for all by hypothesis; and where the equality comes about since by hypothesis. Furthermore, by hypothesis, for , , and

| (20) |

It then follows from equation (20) that

| (21) |

and so

Write as

and apply the triangle inequality to obtain

Multiplying by , integrating both sides and applying equations (20) and (21),

For , , and the first term in the second inequality is ; the second term is also because . The stated result follows.

∎