Bayesian Modeling with Spatial Curvature Processes

Aritra Haldera, Sudipto Banerjeeb and Dipak K. Deyc aDepartment of Biostatistics,

Drexel University, Philadelphia, PA, USA.

bDepartment of Biostatistics,

University of California,

Los Angeles, CA, USA.

cDepartment of Statistics,

University of Connecticut,

Storrs, CT, USA

Abstract

Spatial process models are widely used for modeling point-referenced variables arising from diverse scientific domains. Analyzing the resulting random surface provides deeper insights into the nature of latent dependence within the studied response. We develop Bayesian modeling and inference for rapid changes on the response surface to assess directional curvature along a given trajectory. Such trajectories or curves of rapid change, often referred to as wombling boundaries, occur in geographic space in the form of rivers in a flood plain, roads, mountains or plateaus or other topographic features leading to high gradients on the response surface. We demonstrate fully model based Bayesian inference on directional curvature processes to analyze differential behavior in responses along wombling boundaries. We illustrate our methodology with a number of simulated experiments followed by multiple applications featuring the Boston Housing data; Meuse river data; and temperature data from the Northeastern United States.

Spatial data science manifests in a variety of domains including environmental and geographical information systems (GIS) (Webster & Oliver, 2007; Burrough et al., 2015; Schabenberger & Gotway, 2017; Plant, 2018), digital cartography and terrain modeling (Law et al., 2000; Santner et al., 2003; Jones, 2014; Vaughan, 2018), imaging (Winkler, 2003; Chiu et al., 2013; Dryden & Mardia, 2016), spatial econometrics and land use (LeSage & Pace, 2009), public health and epidemiology (Elliot et al., 2000; Waller & Gotway, 2004; Lawson, 2013) and public policy (Haining, 1993; Wise & Craglia, 2007). Spatial data analysis seeks to estimate an underlying spatial surface representing the process generating the data. Specific inferential interest resides with local features of the surface including rates of change of the process at points and along “spatial boundaries” to understand the behavior of the underlying process and identify lurking explanatory variables or risk factors. This exercise is often referred to as “wombling”, named after a seminal paper by Womble (1951); (also see Gleyze et al., 2001). For regionally aggregated data, it identifies boundaries delineating neighboring regions and has been used to study health disparities (Lu & Carlin, 2005; Li et al., 2015; Gao et al., 2022) and ecological boundaries (Fitzpatrick et al., 2010). For point-referenced data, where variables are mapped at locations within an Euclidean coordinate frame with a sufficiently smooth spatial surface, it refers to estimating spatial gradients and identifying boundaries representing large gradients (Banerjee et al., 2003; Banerjee & Gelfand, 2006; Qu et al., 2021).

Our current contribution develops Bayesian inference for spatial curvature along curves on Euclidean domains. Modeling curvature will require smoothness considerations of the process (Adler, 1981; Kent, 1989; Stein, 1999; Banerjee & Gelfand, 2003). Observations over a finite set of locations from these processes cannot visually inform about smoothness. Therefore, smoothness of the process is specified from mechanistic considerations which can be introduced through prior specifications as needed.

While Bayesian inference for first order derivatives and directional gradients have received considerable attention (see, e.g., Morris et al., 1993; Banerjee et al., 2003; Majumdar et al., 2006; Liang et al., 2009; Heaton, 2014; Terres & Gelfand, 2015; Wang & Berger, 2016; Terres & Gelfand, 2016; Wang et al., 2018; Qu et al., 2021, for inferential developments involving spatial gradients from diverse modeling and application perspectives) such processes inform about directional change, but do not enable inference on curvature (departure from flatness) of the spatial surface.

Analyzing surface roughness from sampling considerations can be traced at least as far back as Greenwood (1984). We offer full inference with uncertainty quantification about spatial curvature at a point and average curvature along a curve from observed data after accounting for explanatory variables. Considering second-order finite differences we establish a valid spatial curvature process as a limit of such finite difference processes. When formulating directional curvature, we favor the normal direction corresponding to a chosen curve and devise a “wombling” measure to track curvature of the surface along the curve. We derive and exploit analytical expressions of higher order processes to avoid numerical finite differences. The Bayesian inferential framework delivers exact posterior inference for the above constructs on the response as well as latent (or residual) processes.

Section 2 develops the directional curvature processes through a differential operator. Section 3 develops the vector analytic framework for curvilinear wombling using curvature processes. Section 4 builds a hierarchical model to exploit the preceding distribution theory and conduct curvature analysis on the response and the latent process. Section 5 presents detailed simulation experiments for assessing directional gradients and curvatures. Section 6 considers applications to three different data sets: Boston housing data, Meuse river data, and Northeastern US Temperatures (the third data is presented in the Supplement).

2 Spatial Curvature Processes

Let be a univariate weakly stationary random field with zero mean, finite second moment and a positive definite covariance function for locations .

In particular, under isotropy we assume , where is the Euclidean distance between the locations (Matérn, 2013).

Building upon notions of mean square smoothness (see, e.g., Stein, 1999) at an arbitrary location in , we focus upon second order differentiability, , where as in the sense and and are the gradient and Hessian operators, respectively.

For the scalar and unit vectors , , we define

to be the second order finite difference processes in the directions , at scale . Being a linear function of stationary processes it is well-defined. Passing to limits, . Provided the limit exists, is defined as the directional curvature process. If is a mean square second order differentiable process in for every then is well-defined with

, where .

In practice, we need only work with computing these derivatives for an orthonormal basis of , say the Euclidean canonical unit vectors along each axis . If , and are arbitrary unit vectors, we can compute .

The directional curvature process is linear in the sense that

, . Since , where and is a unit direction, we henceforth only consider unit directions.

First order directional gradient processes, , are reviewed in Banerjee & Gelfand (2006) and in Section S1.1 of the Supplement. Choosing a direction is emphasized with respect to interpreting the directional curvature processes. Directional curvature is the change in the normal to the surface at when moving along a slice of the surface in the direction . The associated algebraic sign locally classifies the nature of curvature at —for instance, convex or concave ellipsoids (see Stevens, 1981). A detailed discussion, with illustration, is available in Section S2 of the Supplement.

Since is a symmetric matrix, to avoid singularities arising from duplication we modify as follows. If is the usual half-vectorization operator for symmetric matrices and is the duplication matrix (Magnus & Neudecker, 1980) of order then,

where and is the Kronecker product for matrices. If , then .

The process in consists of the pure and mixed second order derivatives in . The distributions needed for inference on directional curvature processes depend on rather than . We refer to as the differential process and , as the directional differential processes induced by along .

Inference for differential processes requires to be a valid multivariate process. Its existence is derived from the limit of corresponding finite difference approximations,

which yields the cross-covariance matrix depending on fourth (and lower) order derivatives of . We investigate the parent and differential processes

using

a

differential operator , ,

where

. The resulting process is also stationary with a zero mean and a cross-covariance matrix

(1)

where , is the gradient, is the Hessian, is the matrix of third derivatives and is the matrix of fourth order derivatives associated with . Under isotropy, , if then, , ,

where and its derivatives are analytically computed for our covariance functions of interest in Section S3 of the Supplement. Let , , be reordered tensors (matrices) of order conforming to the order of corresponding elements in . Let be the element-wise product of with in the same order, and . Then, is,

(2)

The resulting multivariate differential process, , is stationary but not isotropic. Evidently, for the differential operator to be well-defined under isotropy, must exist since (analogous to results in Banerjee et al., 2003, Section 3). The directional differential operator is defined analogously as such that . If , then analogous to (2) the covariance function of the directional curvature process, .

To characterize covariance functions that admit such processes, we turn to spectral theory. Recall that for a positive definite function defined in , Bochner’s theorem (see e.g., Williams & Rasmussen, 2006) establishes the existence of a finite positive spectral measure on . can be expressed as the inverse Fourier transform of , . In cases where admits a spectral density, . For to exist, a trivial extension of the result in Wang et al. (2018) requires that possess a finite fourth moment. Examples of covariance kernels that satisfy this condition are (a) the squared exponential covariance kernel with (), and then, ; and (b) the Matérn class with fractal parameter, ; is known to belong to the -family (see e.g., Stein, 1999) with then, , for all (since the fourth central moment for the -distribution exists if ). Here, we consider formulating the directional differential processes using these two classes of covariance functions (a) the squared exponential, , ; and (b) members of the Matérn class, , where is the modified Bessel function of order (see e.g., Abramowitz et al., 1988), and controls the smoothness of process realizations. We are particularly interested in .

The multivariate process, , is valid under the above assumptions without any further specific parametric assumptions over what has been outlined above. To facilitate inference for , a probability distribution is specified for the parent process. We assume that is a stationary process specified on . In what follows we also assume that admits four derivatives. There are some immediate implications of a Gaussian assumption on the parent process. If and are zero mean, independent stationary Gaussian processes on , then (i) the differential processes and are independent of each other; (ii) if are scalars, then is stationary and (iii) any sub-vector of , for example or , is a stationary Gaussian processes.

If is -times mean square differentiable (i.e. exists), the proposed differential operator can be extended to include higher order derivatives of (Mardia et al., 1996). Differential operators characterizing change in the response (and gradient) surface also follow valid stationary Gaussian processes. For instance, at an arbitrary location the divergence operator, , where is an vector with 0’s in all places except for first order derivatives where it takes a value of 1,

and the Laplacian, defined as the divergence operator for gradients, , where is a vector with 0’s in all places except for pure second order derivatives where it takes a value of 1. Furthermore, they

follow valid Gaussian processes with and .

Let be a Gaussian parent process with a twice-differentiable mean function , i.e. and exist, and let be a covariance function with variance and range . Let be the observed realization over with mean and be the associated covariance matrix with elements , and be an arbitrary location.

Let and

be and matrices, respectively, and , . The distribution , where , is the -dimensional Gaussian,

(3)

which is well-defined as long as the fourth order derivative of exists.

The posterior predictive distribution for the differential process at is

(4)

Posterior inference for curvature proceeds by sampling from . We sample from (4) by drawing one instance of for each sample of obtained from .

The conditional predictive distribution of the differential process is given by where , and

(5)

(6)

Analogous results follow for posterior predictive inference on the curvature process.

If is a constant, as in simple “kriging”, then . More generally, if , where is a vector of spatially indexed covariates and produces a twice differentiable trend surface then explicit calculation of and are possible. In case , where and is a white noise process, inference on gradients for the residual spatial process, , can be performed from the posterior predictive distribution, . We address this in Section 4 in the context of curvature wombling.

3 Wombling with Curvature Processes

Bayesian wombling deals with inference for line integrals

(7)

where is a geometric structure of interest, such as lines or planar curves, residing within the spatial domain of reference, is an appropriate measure, often taken to be the arc-length measure, is a linear function (or functional) of the differential operator . and are referred to as the total and average wombling measures respectively. The structure is defined to be a wombling boundary if it yields a large total (or average) wombling measure. Depending on the spatial domain, geometric structures of interest constructed within them may vary. For example, if we are dealing with surfaces in , choices of are curves and lines within the surface, with the local co-ordinate being . In higher dimensions they would be planes (curves) or hyperplanes (hypercurves). Specifically, Bayesian curvilinear wombling involves estimating integrals in (7) over curves, which tracks rapid change over the spatial domain by determining boundaries (curves) with large gradients normal to the curve (see for e.g., Banerjee & Gelfand, 2006). The integrand in (7) inherently involves a direction, in particular change measured is always in a direction normal to . Hence, can equivalently be expressed as a linear function (functional) of , where denotes the unit normal vector to at . The next few paragraphs provide more detail.

With wombling measures for directional gradients discussed the Supplement, Section S1.2, we construct wombling measures for curvature. Given , depending on the smoothness of the surface, the rate at which gradients change along the curve may present sufficient heterogeneity while traversing the curve. If forms a wombling boundary with respect to the gradient, then wombling boundaries for curvature are subsets of that feature segments with large positive (negative) directional curvature along a normal direction to the curve. Leveraging only gradients, we develop wombling measures for curvature that further characterize such boundaries located for gradients. The wombling measure for curvature in along ascertains whether also forms a wombling boundary with respect to curvature. We associate a directional curvature to each , (a linear function of ) along the direction of a unit normal to at . Using (7) we define wombling measures for total and average curvature as,

(8)

respectively, where denotes the arc-length of . Parameterized curves, , offer further insights.

As varies over its domain, outlines the curve . Implicitly assuming that is regular, i.e., , allows the tangent and normal to exist at all points on the curve. The unit tangent and normal at each point of the curve are and , respectively, while from Section 2.

The arc-length of is or . If , then and .

If is an open curve, then is the average directional curvature.

For example, is the arc of a parameterized circle of radius . It follows that , and . The average curvature in the tangential direction of is .

Hence, the average directional curvature remains path independent and is the difference of directional gradient at the end points of .

For a closed curve , .

If the surface admits up to three derivatives, i.e. exists, the average curvature of the region, , enclosed by , is free of . If , with and then, .

The last equality is obtained using Green’s theorem (see for e.g., Rudin, 1976). This can be interpreted as “flux” in the gradient within . Since, , the integrand in the last equality require the existence of , . Denoting, , vector of unique third derivatives, and then,

(9)

This extends the development in Section 3.2 of Banerjee & Gelfand (2006) to study the behavior of spatial curvature over closed curves on surfaces in . Sampling along is generally harder than sampling inside . Hence, the computational implications of (9) are more appealing. When studying the same behavior along a tangential direction to with , , again a consequence of path independence.

This validates the choice of a normal direction to when measuring change in the gradient. Using the rectilinear approximation to curvature wombling, as discussed later, provides a more computationally tractable and simpler approach, where double integrals manifest when computing variances of the wombling measures.

Curvature wombling requires predictive inference performed using gradient measures on the interval , to include (or ) in (8). Leveraging inference for differential processes in Section 2, we obtain joint inference on the wombling measures. Suppose is generated over . For any , let denote the curve restricted to and its arc-length. Line integrals for curvilinear gradient and curvature wombling measures are ,

and .

Since and are Gaussian processes on , and are valid dependent Gaussian processes on . Therefore, , where and whose elements are evaluated as

(10)

where and .

Simplifications arise in . For example, , while , for , are matrices of orders , and , respectively, of partial and mixed second, third and fourth derivatives of and . For any two points , the dependence is specified through ,

where , , . Generally, for points partitioning the above can be analogously extended. Clearly, is a mean squared continuous process. However, stationarity of does not imply stationarity of .

For any with and we have,

(11)

A valid joint distribution can be specified over by,

(12)

where is the cross-covariance matrix.

In practical applications curvilinear wombling is performed by approximating the curve using linear segments. These measures at the segment level are then aggregated to produce a wombling measure for the curve. The curve is segmented using a partition. Consequently, the accuracy of estimated wombling measures for the curve depend on the choice of partition. Figures S2 and S3 in the online Supplement illustrate this concept. Explicitly, let be a regular rectifiable curve and be a compact interval. Let be a uniformly continuous function. For any partition, of , , with its norm defined as . A polygonal (piecewise-linear) approximation to the curve is, , where , and . Note that for and, hence, . Wombling measure for is, . As we have, . This provides us with an estimate, for curvilinear wombling measures associated with any general curve . Further details are provided in the Supplement, at the end of Section S5.

The choices of for our wombling measures result in, and , which are linear and therefore uniformly continuous over any compact interval. Since predictive inference is performed iteratively on individual line segments, it is sufficient to show the inferential procedure for an arbitrary curve segment . The normal to is free of and denoted as, , which is the normal to . The associated wombling measures with are .

For a point define , . Their joint distribution is specified by (12), where is obtained from (11) by replacing with and is obtained from (10) replacing in the integrand. The analytic tractability of the line integrals in is not a concern. Given choices of and , they are all one or two dimensional integrals which are efficiently computed using simple quadrature. For example, let be the isotropic Gaussian process with mean and , where . , is obtained from (2) and related results.

where, , , and denotes the standard Gaussian cumulative distribution function. These are simple computations with quadrature required only for computing .

4 Bayesian Hierarchical Model

We operate under a Bayesian hierarchical model, which is specified as

(13)

where is a Gaussian process, and is a white noise process, termed as the nugget (see Banerjee et al., 2014, and references therein). The process parameters are . More generally, we can consider a latent specification for response arising from exponential families, , and , where is a monotonic link function, is a member of the exponential family and is the natural parameter. Predictive inference on differential processes and curvature wombling proceeds on the latent surface through . The joint posterior for differential processes is obtained through, , while wombling measures for a curve within the estimated posterior surface for , are sampled from the posterior, . Customary prior specifications for yield

(14)

where denotes the inverse-gamma distribution with a shape-rate parameterization, is a uniform distribution and is the correlation matrix corresponding to . The resulting full conditionals are , , , , where is the matrix with as rows, , , , and . is updated using Metropolis steps with a normal proposal and an adaptive variance.

Under this setup posterior samples for the differential processes and wombling measures result from (5) and (6). For each posterior sample of , we draw ,

where , , and are computed from (10) and (11). Algorithms 1 and 2 in the Supplement, Section S4, present further details for posterior sampling.

Next, we turn to numerical experiments and data analyses. Codes required for reproducing and emulating the analyses presented in the manuscript are produced for the R statistical programming environment and available for download in the public domain

at https://github.com/arh926/spWombling .

5 Simulation Experiments

5.1 Data generation

The proposed differential processes are not observed in reality, but are induced by an observed spatially indexed parent process. To evaluate statistical learning of the curvature process

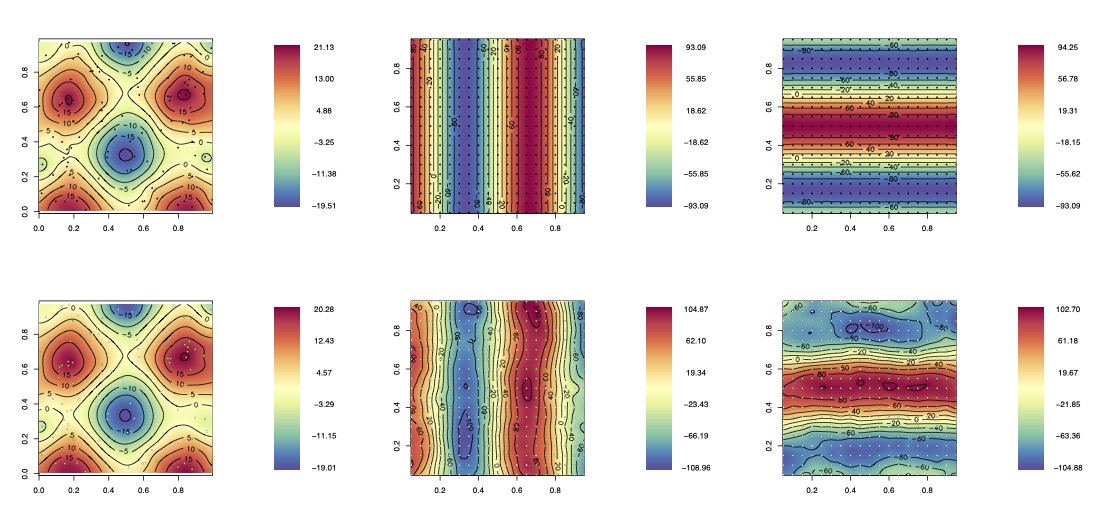

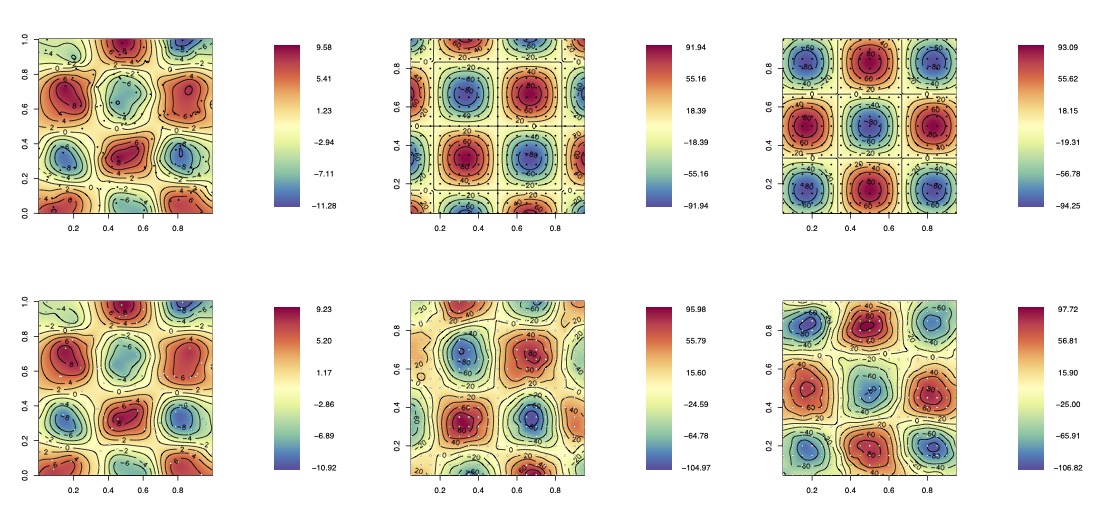

we perform simulation experiments within a setup where true values of the differential process and wombling measures are available. We consider locations over the unit square

. We generate synthetic data from two distributions: (a) Pattern 1: ; (b) Pattern 2: ,

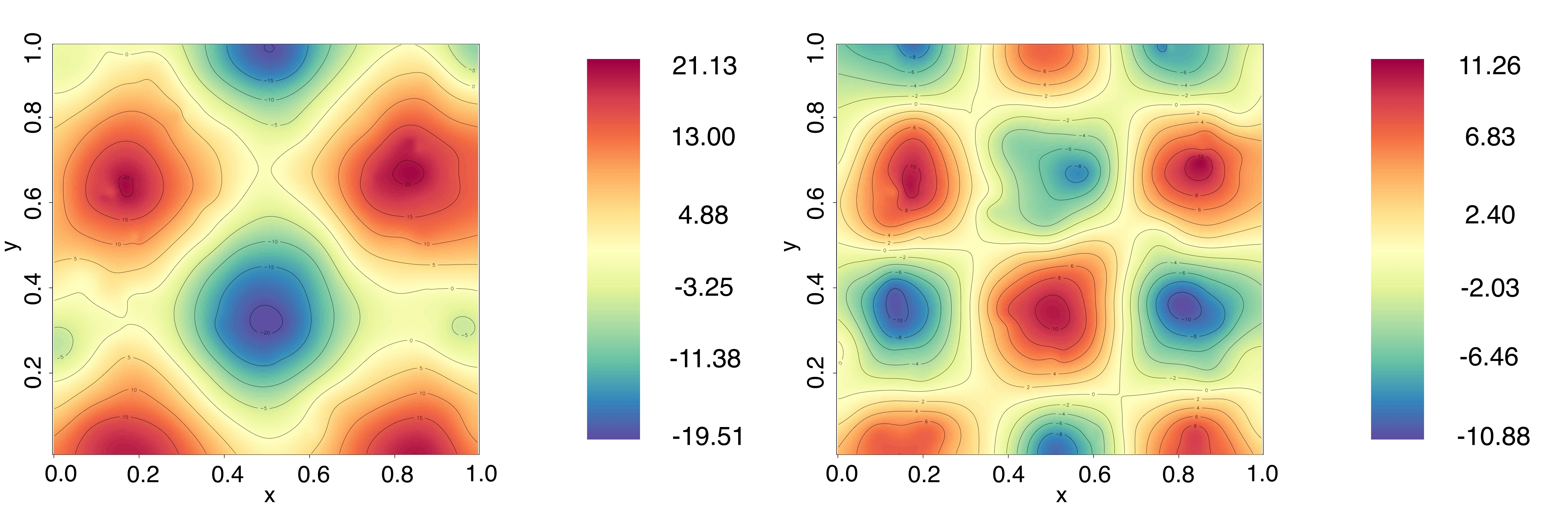

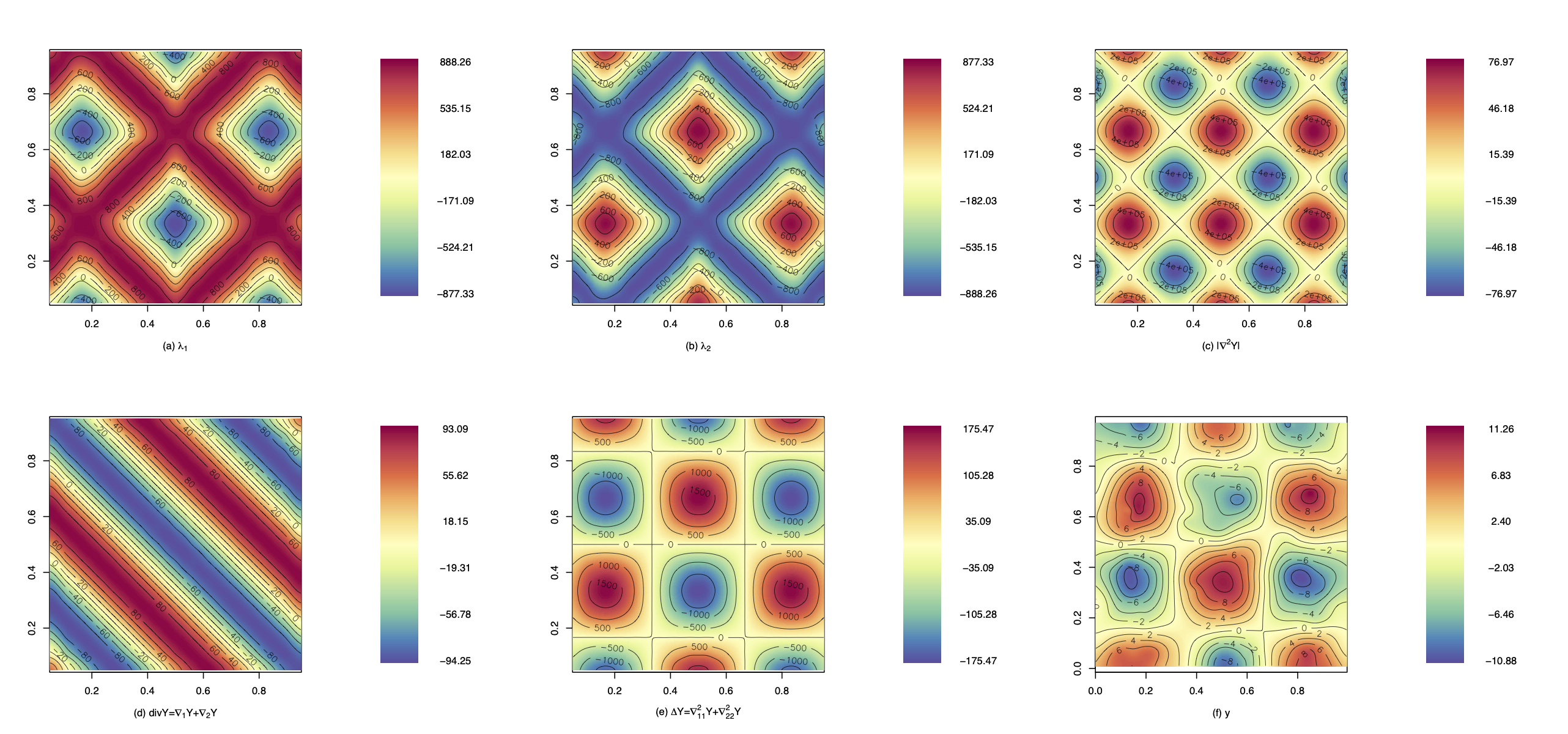

Figure 1: Spatial plots for synthetic patterns, from Pattern 1 (left) and Pattern 2 (right). Scales are shown in the legend alongside.

where the value of . Figure 1 presents spatial plots of the generated synthetic response from these patterns. The rationale behind selecting these distributions is: (i) synthetic data is more practical and not from the model in (13), and (ii) true gradient and curvature can be computed at every location .

The synthetic patterns chosen feature two different scenarios that may arise. In the first pattern expressions for differentials along the principal directions and are functions of either or , , .

The curvature along does not influence curvature along , for all . While , , where is a matrix with, , and with differentials being functions of both and and for some .

While setting up the experiments we vary with 10 replicated instances under each setting.

5.2 Bayesian model fitting

We fit the model in (14) with only an intercept allowing the spatial process to learn the functional patterns in the synthetic response. We use the following hyper-parameter values in (14): , , , , , and . These choices comprise reasonable weakly informative priors. While a prior on can be specified (and was implemented as part of this experiment) to ensure the existence of the curvature process, here our choice of scales in the data generating patterns ensured that provided the best model fit when compared with values of . Hence, we present the results with .

The parameter estimates for are computed using posterior medians and their highest posterior density (HPD) intervals (Chen & Shao, 1999; Plummer et al., 2015). For each replicate, we assess our ability to estimate the local geometry of the resulting posterior surface. For this we overlay a grid spanning the unit square. We perform posterior predictive inference for the differential processes at each grid location following Section 2. Posterior predictive medians (accompanied by % HPD intervals) summarize inference for the differential processes over the grid locations (Section 5.4 offers supplementary analysis).

5.3 Bayesian wombling with curvature processes

For wombling with curvature processes, or curvature wombling, we focus on locating curves that track rapid change within the simulated random surfaces. For example, consider the surface produced by the first pattern. If a curve is provided to us, we can evaluate the posterior distribution of the average or total curvature wombling measures to assess their statistical significance. On the other hand, without a given curve, we consider three different approaches for constructing them from a boundary analysis or wombling perspective: (a) level curves: : Bayesian wombling literature finds that curves parallel to contours often form wombling boundaries (see, e.g., Banerjee & Gelfand, 2006) and level curves on a surface are parallel to local contours by definition; (b) smooth curves: produces a smooth curve using Bézier splines (see, e.g., Gallier & Gallier, 2000) from a set of annotated points that are of interest within the surface; and (c) rectilinear curves: produces a rectilinear curve joining adjacent annotated points of interest within the surface using straight lines, performs curvature wombling using a Riemann sum approximation (see (S1) in the Supplement).

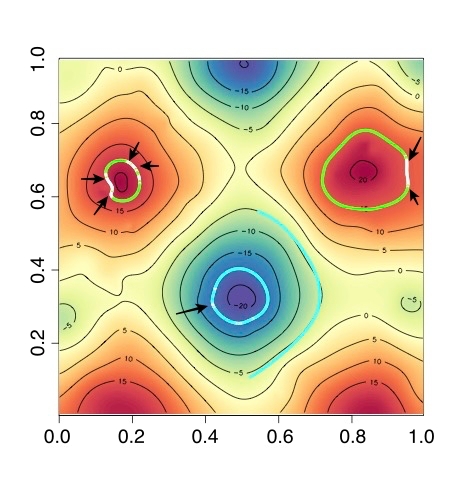

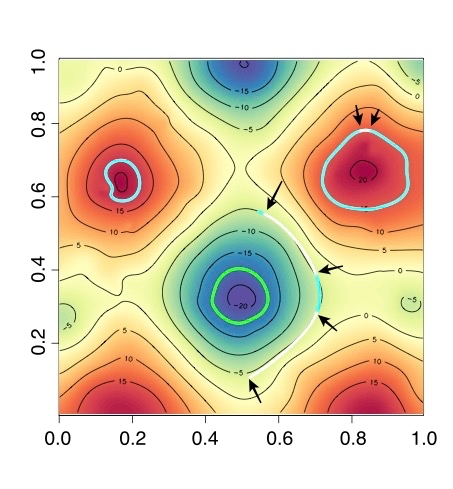

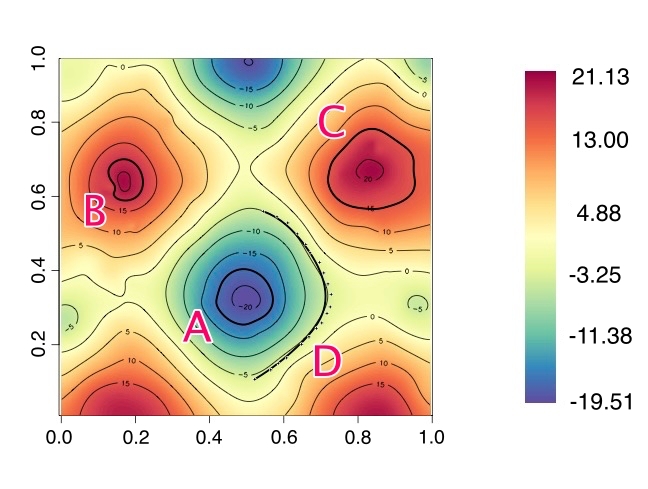

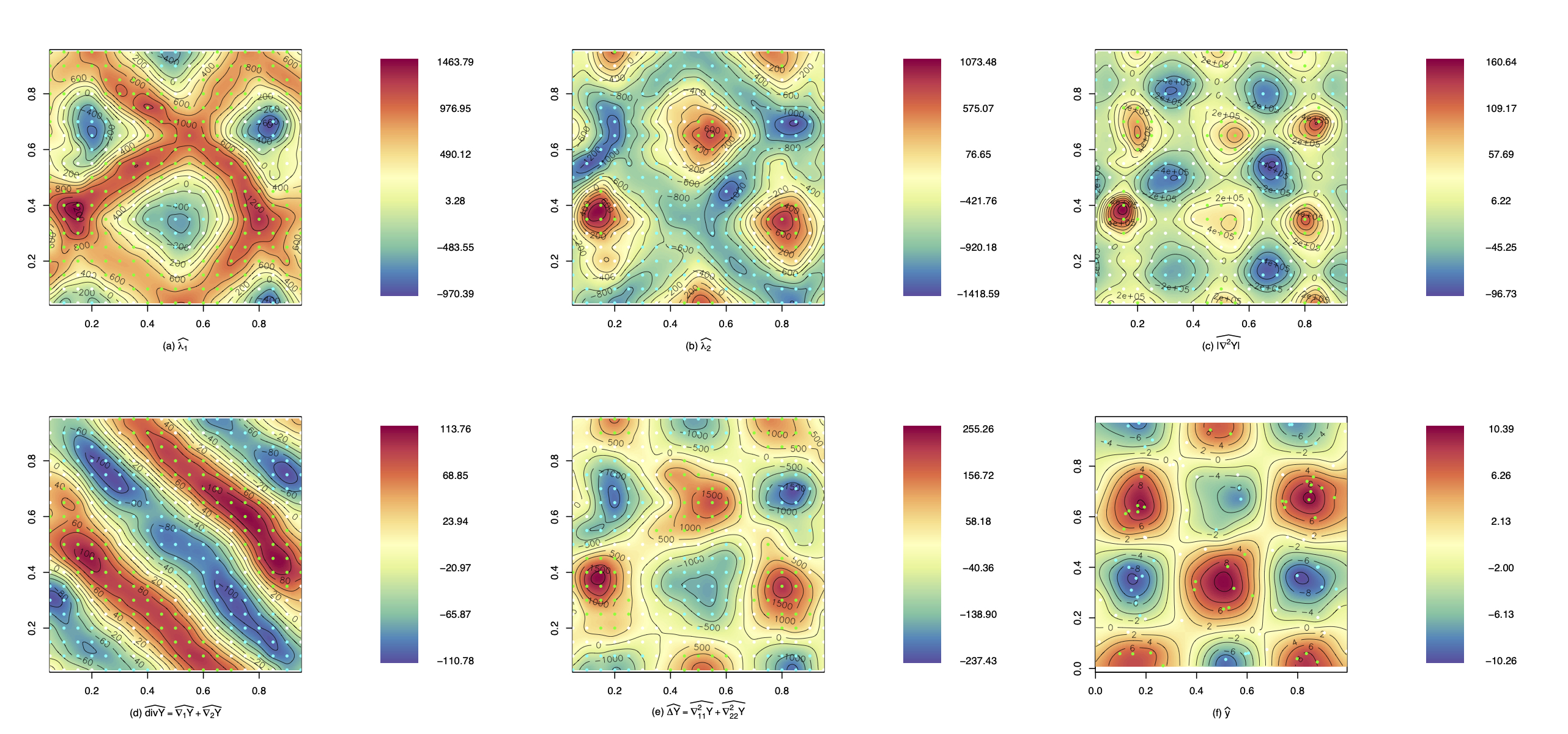

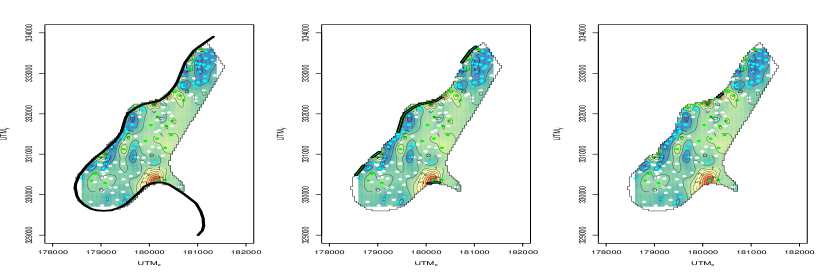

Curves of types (b) and (c) allow the investigator to specify a region of interest that house possible wombling boundaries. For the surface realization produced by Pattern 1, we consider four different types of curves on the response surface, (A) a closed curve enclosing a trough corresponding to a level curve, , (B) a closed curve enclosing a peak corresponding to a level curve, , (C) a closed curve that outlines a contour corresponding to a level curve, and (D) an open curve along a contour constructed using a Bézier spline. These curves are marked in Figure 2c.

Figure 2: (left) shows color coded directional gradients for segments, (center) shows color coded directional curvature for segments in the direction normal to the curve, (right) shows curves selected for performing curvature wombling. green indicates a positive significance, cyan indicates negative significance and white indicates no significance.

Curvature wombling is performed using methods outlined in Section 3.

Referring to the discussion on rectilinear approximation, for each curve, given a partition, we compute and . Combining the segments produces a vector and a matrix of directions, that represents the curve. Algorithm 2 in the Supplement, Section S4 devises efficient computation using and .

The total (and average) wombling measures are sampled from their posteriors using (12). For curves A, B, C and D, we use partitions with sufficiently small norms () to achieve accuracy (, , and respectively).

One and two dimensional line integrals (refer to (10) and (11)) are computed via quadrature using grids of size 10 on , and size 100 on respectively, for . The median of sampled is our estimated wombling measure for the curve. Significance at the curve-segment level is assessed based on the inclusion of 0 within the HPD intervals. Our design allows us to compute true values of average wombling measures for each rectilinear segment in the curve. They are computed using, . We compute HPD intervals for the wombling measures at the segment level. Coverage probabilities (CPs) are then constructed by aggregating coverage of true values by HPD intervals over segments.

Table 1: Results from curvature wombling performed on curves A, B, C and D as shown in Figure 2. The estimated average directional gradient and curvature are accompanied by their respective HPD intervals in brackets. HPD intervals containing 0 are marked in bold.

Curves

Average Gradient ()

Average Curvature ()

True

Estimated

True

Estimated

Curve A

-61.54

-64.97

731.94

768.03

(-92.37, -38.57)

(599.30, 913.70)

Curve B

40.85

49.19

-808.04

-850.84

(20.45, 73.12)

(-1066.98, -630.09)

Curve C

84.03

85.65

-558.58

-504.98

(59.81, 109.97)

(-767.55, -241.61)

Curve D

-110.84

-113.27

11.32

-94.64

(-153.23, -77.01)

(-386.94, 233.78)

Curve A encloses a trough and a local minima for the surface, while B and C enclose peaks and local maximums (referring to corresponding locations in Figures S8c and S9c). Along all segments of A we expect negative gradients owing to the decreasing nature of the response in that region, while for B and C we expect positive gradients. Each of them would be expected to yield significant wombling measures for gradients. Referring to the Laplacian surface (see Supplement, Figures S8e and S9e) A, B, and C are located in regions manifesting rapid change in the gradient surface, implying they should yield large positive (curve A) or negative (curves B and C) curvature, forming curvature wombling boundaries. These are all aligned with our findings presented in Table 1, which presents measures of quality assessment for wombling. The magnitude and sign of wombling measures also allow us to differentiate between the type of curvature for the different wombling boundaries. For instance, B is located in a region of higher convexity compared to C, while the nature of convexity for regions enclosed by them are different compared to A. Plots in Figure 2 (left and center) show line segment level inference for average wombling measures. Arrows indicate segments which were not significant with respect to gradient or curvature, while regions of significance are color coded. D is located in a “relatively flat” region of the surface (see Figures S8e and S9e) and is expected to have gradients but no curvature, which aligns with results shown in Table 1. We conclude by noting that the true values, of the wombling measures for the curves considered, are all covered by the estimated HPD intervals for respective curves. Additionally, at the line segment level we achieved a CP of 1.0 across all curves.

5.4 Supplementary analysis

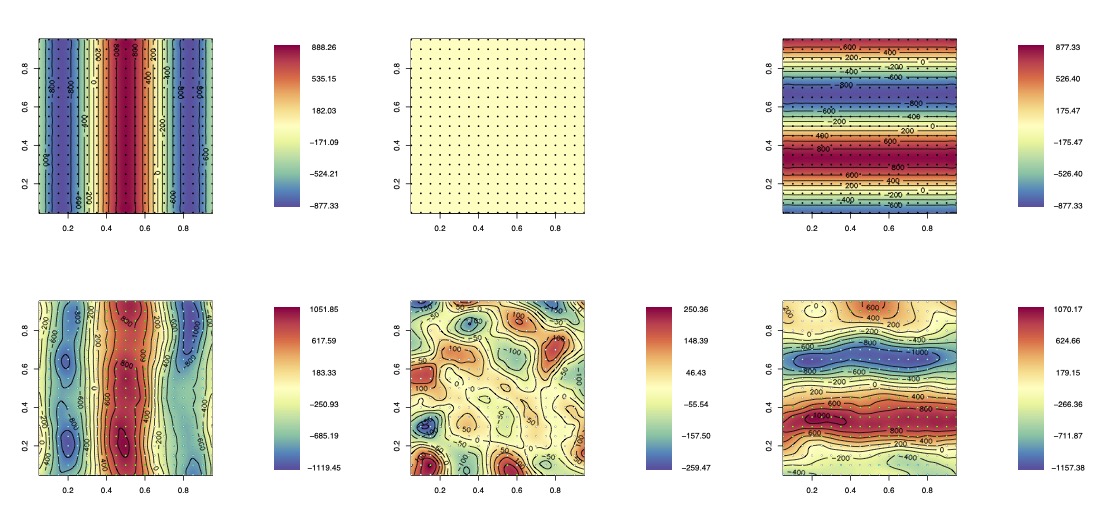

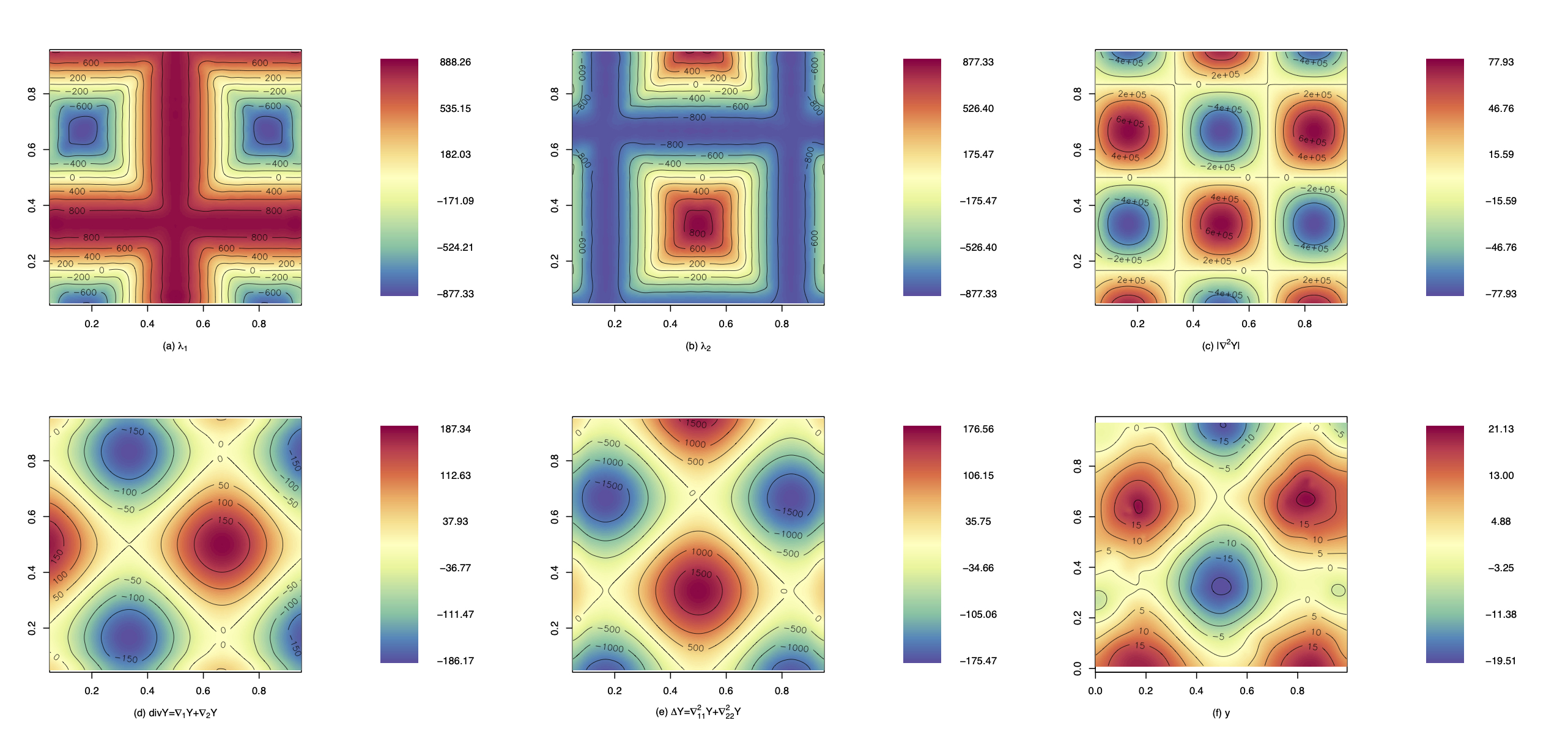

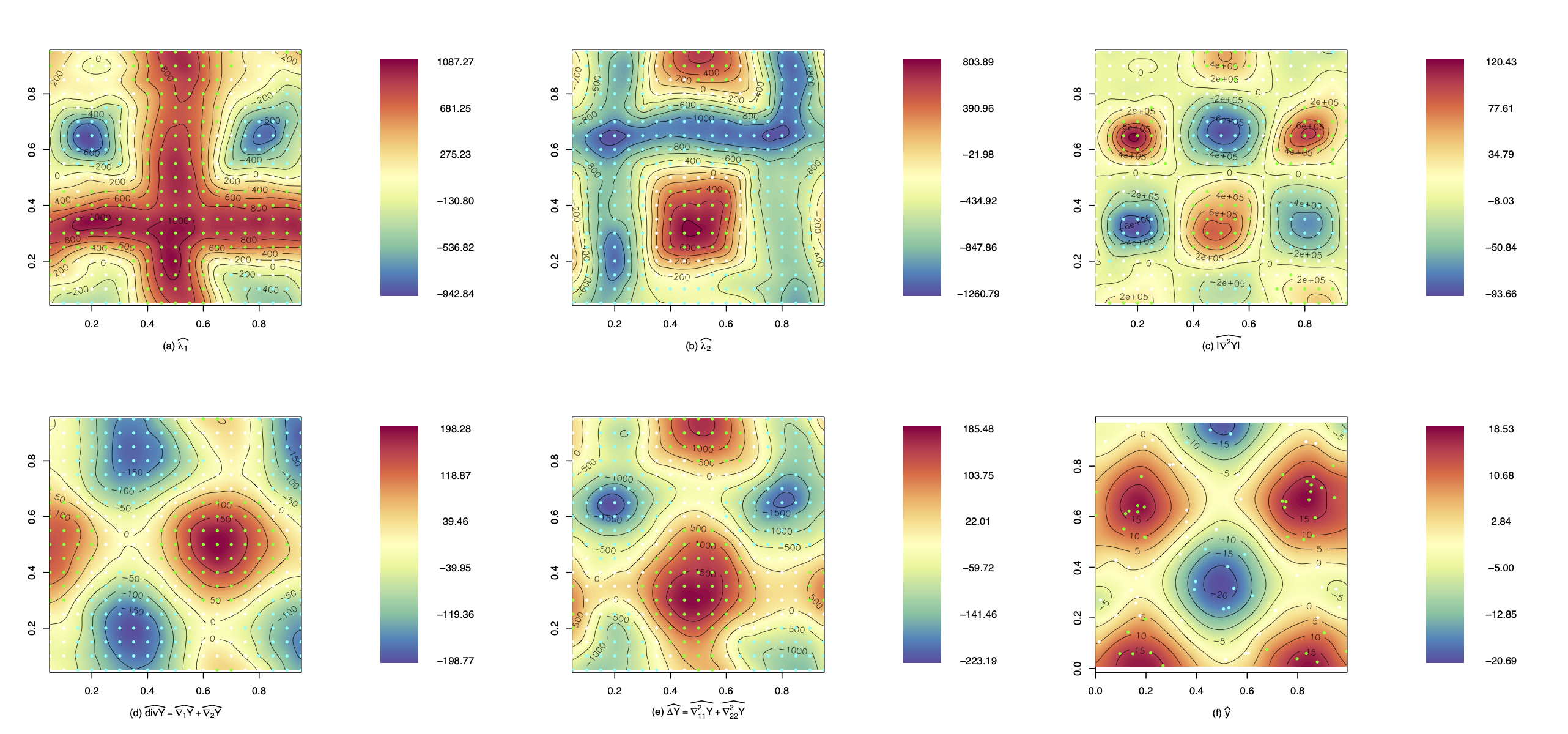

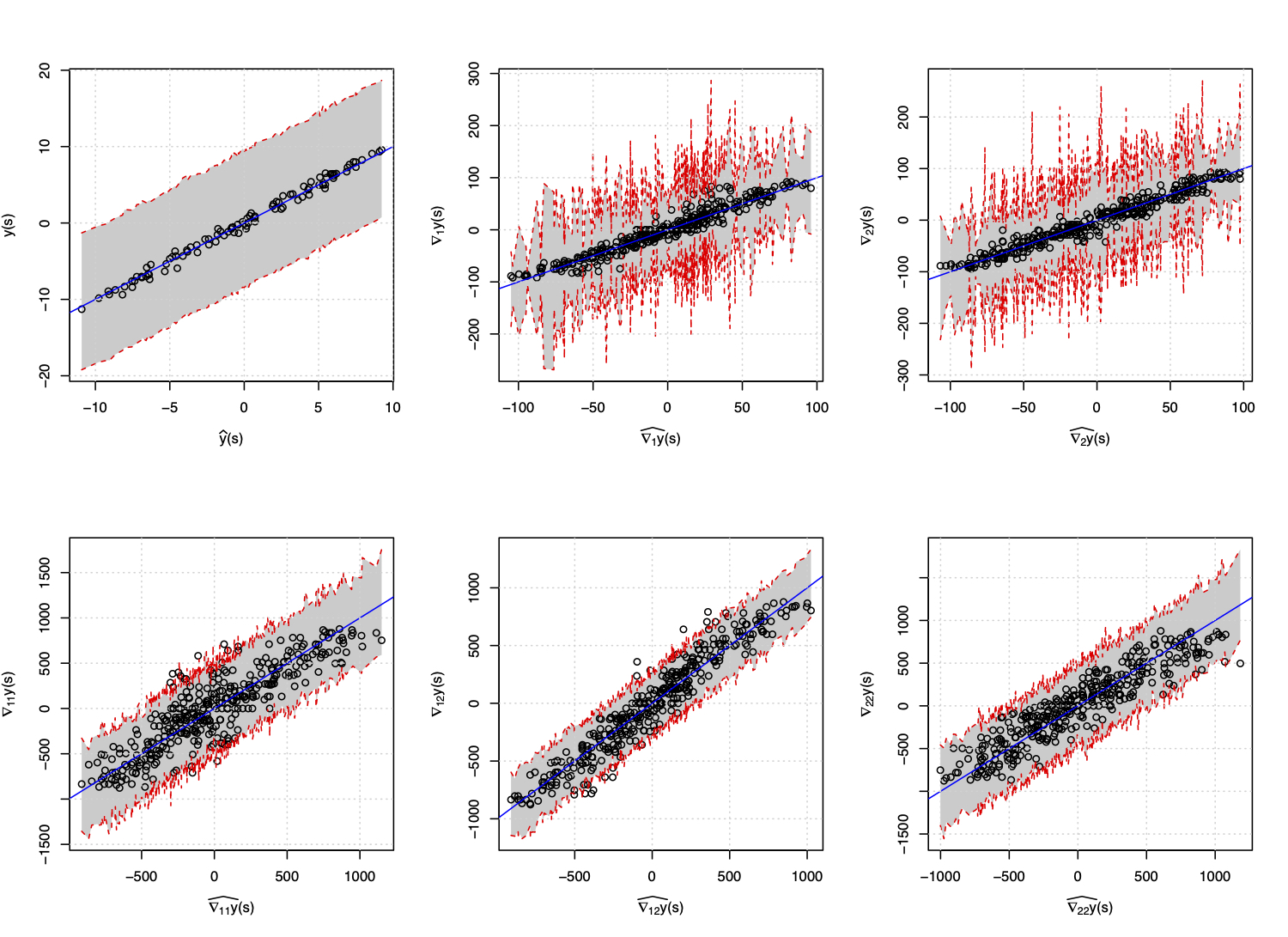

We present additional results in the online supplement. Tables S1 and S2 present parameter estimates, measures of goodness of fit for the fitted process, and assessment of derivative process characteristics for each pattern considered. We compute root mean square errors (RMSE) across observed locations averaged over 10 replicates for each sample size setting for the fitted process , and , . We report standard deviations across replicates. With increasing number of observed locations we are able to effectively learn the underlying process and induced differential processes. Figures S4, S5, S6 and S7 present spatial plots of posterior medians of gradient and curvature processes, for locations. These plots demonstrate the effectiveness of our methods in learning about the differential processes from the underlying patterns. Similarly plots shown in Figures S8, S9, S10 and S11 demonstrate the same for derived quantities and operators of —principal curvature (eigenvalues), Gaussian curvature (determinant) (see, e.g., Spivak, 1999; Do Carmo, 2016), divergence and Laplacian, which pertain to geometric analysis of curvature for the random surface resulting from the underlying patterns. Statistical significance is assessed at every grid point by checking the inclusion of 0 in their HPD intervals. Significantly positive (negative) points are color coded. We compute average CPs at every grid location to measure the accuracy of our assessment. These CPs are then averaged over replicates. We observed high CPs across the grid for parent and differential processes. Figures S12 and S13 compare observed against estimated differential processes coupled with their HPD regions.

6 Applications

Frameworks developed for differential assessment and boundary analysis in spatially indexed response are applied to multiple data sets with the aim of locating curvature wombling boundaries that track rapid change in response. The chosen data arise from varied areas of scientific interest, we briefly describe the origin and significance of each with respect to our methods before performing our analysis. Response is modeled using the hierarchical model in (13). Prior specifications used in (14) are, , , (mean 1, infinite variance), , being the number of covariates and for the Matérn kernel ensuring existence of the differential processes.

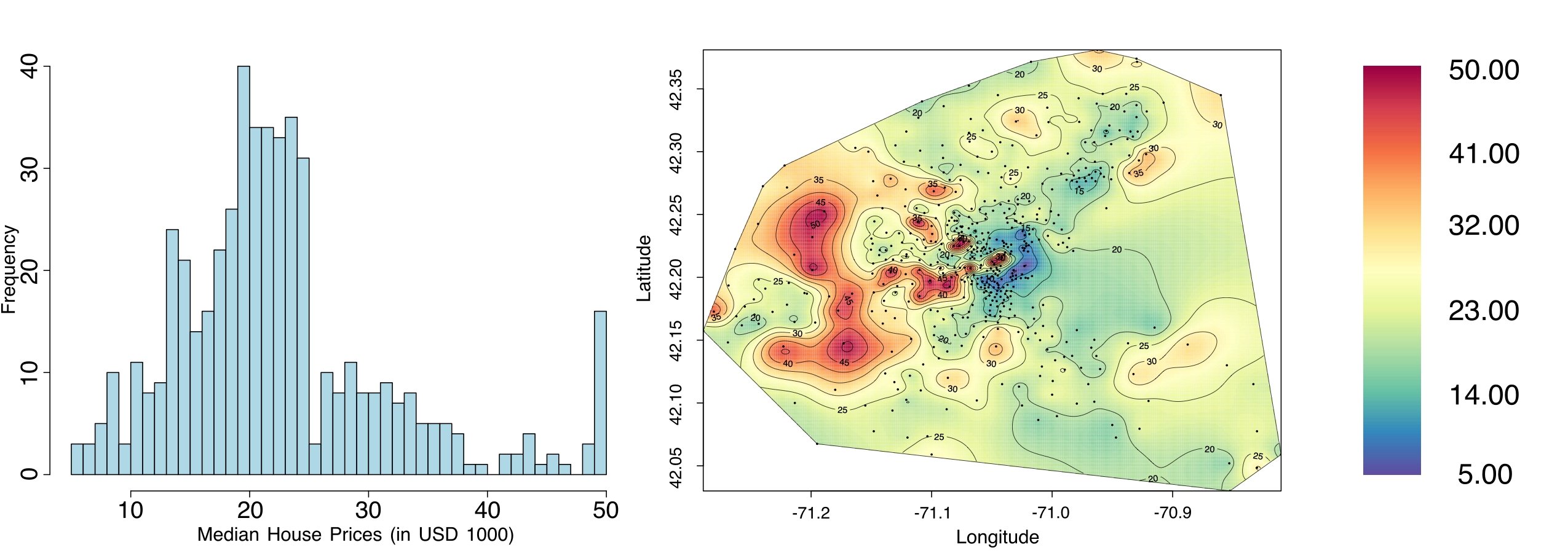

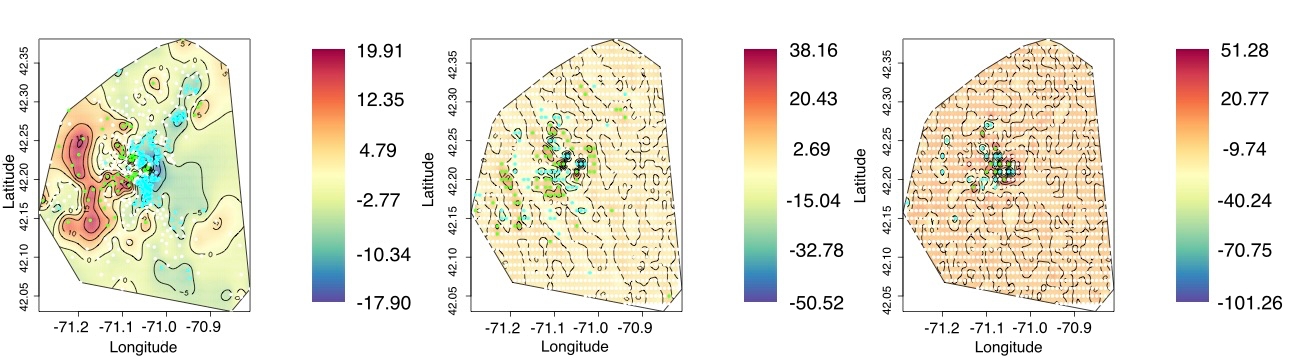

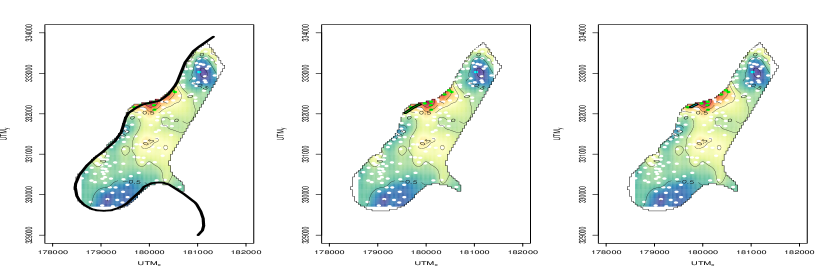

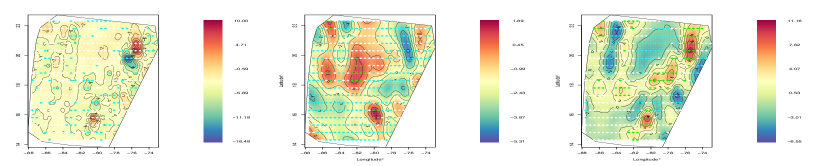

Boston Housing: The Boston housing data (see, e.g., Harrison Jr & Rubinfeld, 1978) was collected by the United States Census Service featuring median house prices for tracts and towns in Boston, Massachusetts area. The purpose was to study heterogeneity in the market caused by the need for residents to have clean air. To study such heterogeneity, modern equitable housing policies are incorporating statistical modeling to quantify such behavior. Often they are a result of unobserved effects of rapidly shifting socioeconomic conditions (see, e.g., Hu et al., 2019). Within a spatial map this manifests as neighboring regions of disparity. Figure 3 shows two such regions: high priced including Downtown Boston, Cambridge, Newton, Wellesley, Brookline etc. and low priced including South and East End. For effective policy implementation, identifying such regions becomes crucial. Spatial variation in the median house prices is evidenced in Figure 4. Curvature wombling effected on the house price surface would locate regions that feature such change.

Figure 3: Plots showing (left) probability density of median house prices (in USD 1000) (right) spatial plot of median owner occupied house prices in Boston.

The data contains median house price values for 506 census-tracts along with demographic data. Latitude-longitude centers of the census-tracts are used for spatial referencing. To allow to capture all the spatial variation, we include only an intercept in the model. Table 2 shows posterior estimates and HPD intervals for process parameters. We observe that —larger portion of total variance being explained by varying location.

Table 2: Posterior Estimates from the hierarchical linear model in (13) to Boston housing

Parameters ()

Posterior Estimates ()

HPD

0.96

(0.83, 1.11)

55.18

(43.91, 68.06)

14.89

(11.77, 18.71)

25.58

(24.29, 27.34)

Figure 4: Plots (left to right) showing fitted process, divergence and Laplacian for the median house price surface.

Modeled spatial variation in the response is shown in Figure 3 (left). Significance for the estimate, , is assessed using the inclusion of 0 in its posterior HPD. Using posterior samples we estimate the derivative processes for . A grid, (, containing 1229 equally spaced locations) is overlaid over the region with the same purpose. To effect posterior surface analysis on the estimated surface we use posterior predictive distributions of and revealing zones that manifest rapid change in response and gradients respectively. They are shown in Figures 4 (center and right).

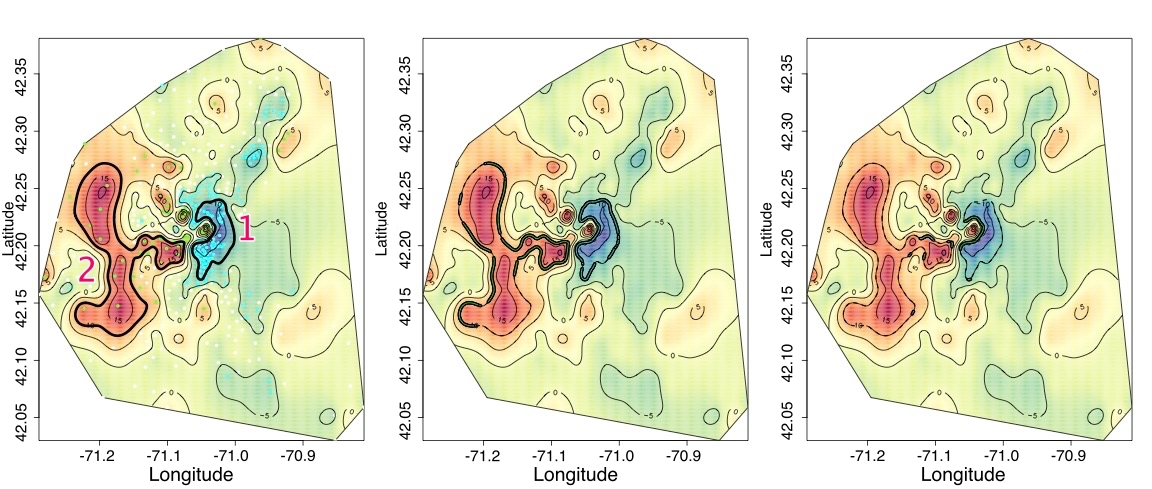

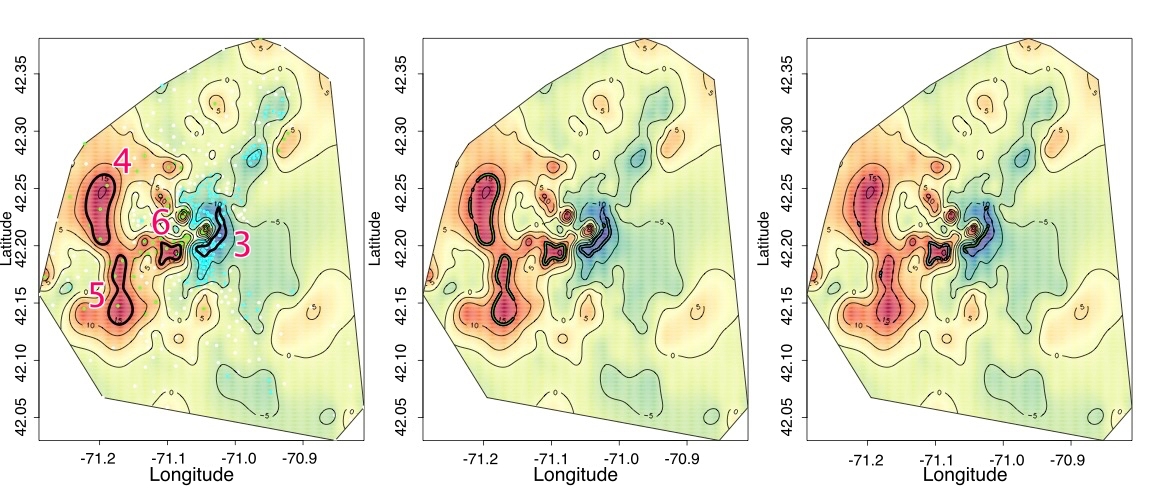

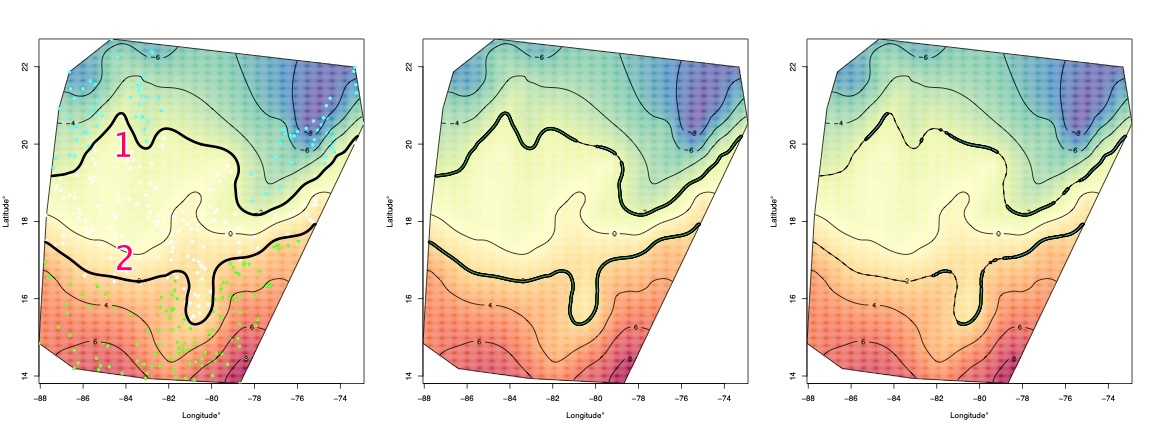

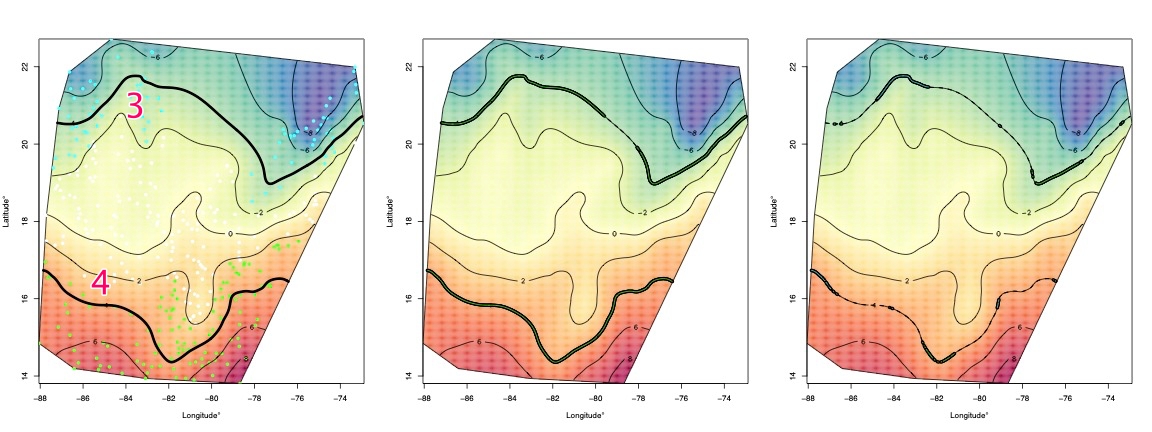

Figure 5: Curvature wombling on the Boston Housing Data.

Next, we focus on performing curvature wombling on the estimated surface. Strategic posterior surface analysis is used to locate level-sets of interest within the surface that could possibly contain wombling boundaries. We start with contours shown in Figure 5 (left column). Boundary 1 (2) bounds a region where the fitted process has positive (negative) significant estimates. Evidently, the chosen curves should house significant gradients along most segments, but significant curvature should only be detected for segments located at the center (lat-long: ) of the surface in Figures 4 (center and right). Estimated average wombling measures for these curves are shown in Table 3. Figures 5 (center and right) correspond to segment level posterior inference for the curves, line segments with significant directional differentials are indicated in bold. Summarizing, we observe that the gradient, curvature and posterior surface analysis allow us to highlight towns (with census-tracts) within Boston that exhibit heterogeneity in prices. Curvature wombling performed on the surface allows us to delineate zones that house such heterogeneity. For instance, towns located within boundaries 3 (South and East End) and 6 (Newton and Brookline) show significant change in price gradients, compared to towns within boundaries 4 (Lincoln and Weston) and 5 (Wellesley and Dover). These findings can be verified referring back to price dynamics for real estate in Boston during 1978 (see e.g., Schnare & Struyk, 1976). The same regions are scrutinized for studying segmentation—towns within curves 1 and 3 are accessible to lower income groups willing to sacrifice air quality.

Table 3: Curvature wombling measures for boundaries in Boston housing accompanied by corresponding HPD intervals in brackets below. Estimates corresponding to HPD intervals containing 0 are marked in bold.

Curve ()

Average Gradient ()

Average Curvature ()

Boundary 1

-8.91

10.14

(-11.31, -6.65)

(2.84, 18.34)

Boundary 2

6.18

-0.09

(4.75, 7.49)

(-3.45, 3.35)

Boundary 3

-6.47

12.69

(-9.74, -3.27)

(2.65, 22.48)

Boundary 4

6.92

1.26

(4.63, 9.19)

(-5.04, 7.14)

Boundary 5

5.47

1.36

(2.95, 7.86)

(-4.33, 7.42)

Boundary 6

11.82

-16.27

(7.28, 16.14)

(-26.68,-6.57)

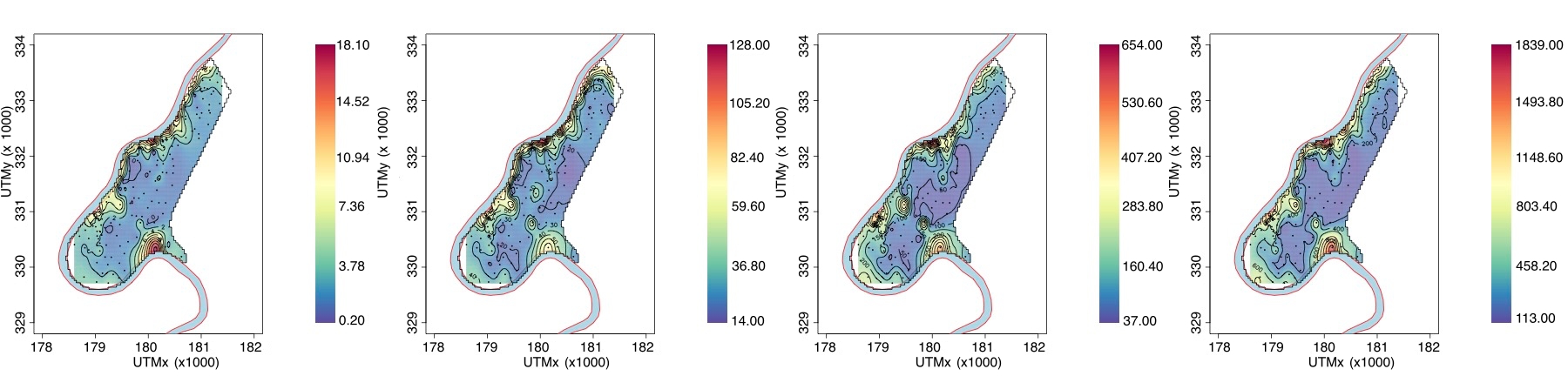

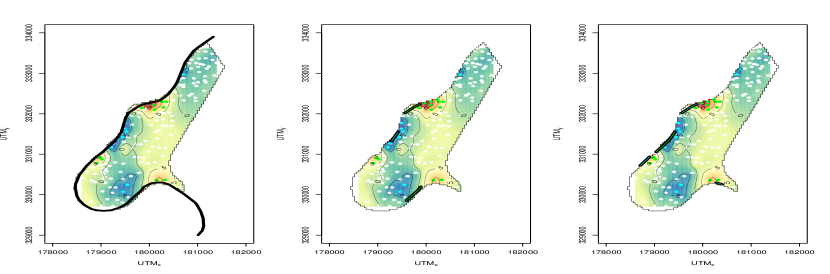

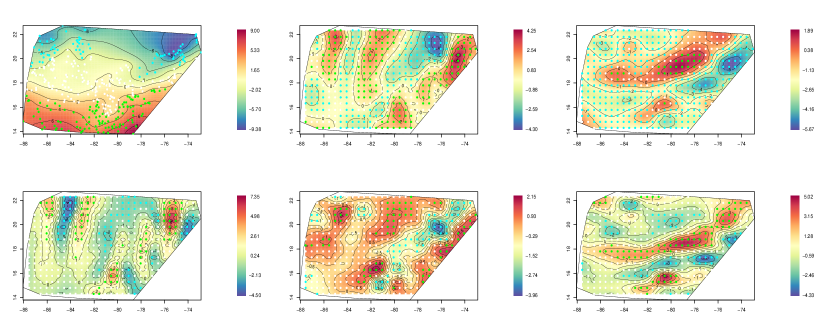

Meuse River Data: The Meuse river data features in Pebesma et al. (2012). It provides locations of topsoil heavy metal concentrations, along with soil and landscape variables at the observed locations, collected in a flood plain of the river Meuse, near the village of Stein, Netherlands. The heavy metal concentrations recorded include Cadmium (Cd), Copper (Cu), Lead (Pb) and Zinc (Zn). A distinguishing feature is the naturally occurring boundary—the Meuse. From a boundary analysis standpoint we are interested in examining differentials in heavy metal concentrations along the flood plain of the river to understand the heterogeneous effect of the river on the topsoil.

Figure 6: Plots showing heavy metal concentrations in the topsoil of a flood plain at 155 locations for (from left to right) Cadmium (Cd), Copper (Cu), Lead (Pb) and Zinc (Zn) (in mg/kg of soil).

The soils of the floodplain are commonly used for agriculture. Crops grown on the floodplain of the river banks of the Meuse may be consumed by man and/or livestock.

Table 4: Posterior estimates of process parameters and covariates for the Meuse river data accompanied by their corresponding HPD intervals in brackets below. Effects with HPDs containing 0 are marked in bold.

Parameters ()

Cadmium (Cd)

Copper (Cu)

Lead (Pb)

Zinc (Zn)

0.0379

0.1138

0.0399

0.0472

(0.0207, 0.0618)

(0.0871, 0.1471)

(0.0131, 0.1900)

(0.0230, 0.0744)

2.9566

3.2044

0.9303

38.3538

(1.2803, 5.2227)

(2.3955, 4.0892)

(0.2763, 1.7641)

(16.7815, 65.1450)

1.7771

0.0067

0.8555

23.2226

(0.9107, 2.6328)

(0.0012, 0.0244)

(0.0010, 1.2280)

(9.3743, 35.6867)

Intercept

9.4973

4.8503

6.1120

37.1315

(5.9750, 13.3704)

(3.1392, 6.8308)

(3.4615, 8.1910)

(25.0903, 53.0870)

elev

-0.7672

-0.4065

-0.5413

-2.8781

(-1.2531, -0.3574)

(-0.7418, -0.1656)

(-0.7853, -0.1442)

(-4.7805, -1.2834)

om

0.4011

0.4293

0.3434

0.8606

(0.2616, 0.5233)

(0.3276, 0.4728)

(0.2490, 0.4253)

(0.3681, 1.3166)

dist

-0.0033

-0.0025

-0.0011

-0.0081

(-0.0061, 0.0000)

(-0.0043, -0.0014)

(-0.0029, 0.0006)

(-0.0197, 0.0038)

ffreq (=2)

-1.4176

-2.4727

-0.8483

-4.3182

(-2.3202, -0.3432)

(-3.1794, -1.6716)

(-1.6109, -0.2598)

(-7.9184, -0.6220)

ffreq (=3)

-0.7322

-1.4298

-0.1865

-3.3159

(-2.0520, 0.6248)

(-2.4443, -0.5157)

(-1.2972, 0.6861)

(-7.9307, 1.9128)

soil (=2)

-0.3337

0.2236

0.5988

-2.2213

(-1.4661, 0.7491)

(-0.7248, 0.9799)

(-0.0345, 1.2956)

(-6.1446, 2.0831)

soil (=3)

-0.3884

0.6344

0.3707

-2.9922

(-2.0891, 1.2628)

(-0.2309, 1.8474)

(-0.7108, 1.4029)

(-9.0918, 3.6289)

lime (=1)

0.5752

1.3223

0.7759

-0.4759

(-0.3509, 1.4341)

(0.7152, 1.9427)

(0.1173, 1.4645)

(-3.9057, 2.6510)

The spatial variation in heavy metal concentration can be seen in Figure 6. The path of the Meuse river is shown in each of the spatial plots. Evidently, the heavy metal concentrations decreases with increasing distance from the river. We model the concentrations as independent Gaussian processes. Covariates used are relative elevation above local river bed (elev, measured in meters), organic matter (om measured in kg/(100kg) of soil), distance to Meuse (dist), frequency of flooding, soil type (soil), and lime content in soil (). Table 4 shows the posterior estimates of process parameters and model coefficients, for each of the heavy metals in question. We observe that 62.45%, 99.79%, 52.09%, 62.29% for Cd, Cu, Pb and Zn respectively, indicating larger portions of total variation being explained by spatial heterogeneity, except for Pb. Variation in Cd and Zn concentration is significantly affected by elevation, organic matter and flooding frequency, while variations in Cu and Pb concentration is significantly affected by elevation, organic matter and flooding frequency and lime content.

The estimated residual surface is shown in Figure 7 (left) for Cd concentrations. We observe significant positive gradients with varying curvature depending on segments of the river bed for all heavy metals.

We perform curvature wombling on the Meuse using the residual surface, . The results of curvature wombling for cadmium are shown in Figure 7. Results and plots for other metals can be found in the Supplement, Section S7, Figure S14. The accompanying wombling measures are shown in Table 5. We observe sufficient heterogeneity in the signs of the wombling measures, yielding contiguous positive (negative) segments. For example, in Cd concentration, boundaries located for average gradients in the northern and southern region are positive, as opposed to boundaries located in the north western region. Therefore, while displaying the wombling measures, in Table 5, we separate them by their sign.

Figure 7: Plots showing results for curvature wombling on the Meuse river for Cadmium (Cd) concentration. Plots showing (left) the resulting fitted process (center) the contiguous segments that display significant gradients (right) the contiguous segments with significant curvature.

We conclude that effects of river Meuse on regions of the flood plain exhibit significant heterogeneity when considered across heavy metals. Compared to other metals, Pb concentrations are limited to northern regions of the flood plain. Concentrations of Cd and Zn concentrations along the river are similar. Compared to the northern region, in the northwestern region Zn concentrations decrease significantly as we move inland. Studies corroborating such evidence can be found in Leenaers et al. (1988) and Albering et al. (1999).

7 Discussion and Future Work

We developed a fully model-based Bayesian inferential framework for differential process assessment and curvature-based boundary analysis for spatial processes. Introducing the directional curvature process and its associated inferential framework supplements the directional gradients with inference for their rates of change, while its induction

into the folds of Bayesian curvilinear wombling allows for further characterization of difference boundaries. Adopting a Bayesian hierarchical model allows for Gaussian calibration when characterizing points, regions and boundaries within a surface. This framework is widely applicable; our applications arise from selected disciplines indicating the utilities of mapping curvature process boundaries to understand spatial data generating patterns. Substantive case studies will be reported separately.

Table 5: Curvature wombling measures for the Meuse, separated by zones of positive and negative signs, they are accompanied by their corresponding HPD intervals in brackets below.

Wombling Measures

Cd

Cu

Pb

Zn

0.0510

0.1273

0.0375

0.1984

(0.0298, 0.07401)

(0.0913, 0.1729)

(0.0019, 0.1561)

(0.0876, 0.3162)

-0.0400

-0.2561

–

-0.1890

(-0.0635, -0.0170)

(-0.3187, -0.1997 )

–

(-0.2967, -0.0669)

0.0074

–

–

0.0422

(0.0019, 0.0158)

–

–

(0.0111, 0.0879)

-0.0078

-0.1247

-0.0039

-0.0473

(-0.0223, -0.0024)

(-0.1979, -0.0860)

(-0.1076, -0.0006)

(-0.1114, -0.0095)

Several avenues hold scope for future developments. A more generalized theoretical framework can be developed for studying joint behavior of the principal curvature (direction of maximum (or minimum) curvature) and the aspect (direction of maximum gradient) (see, e.g., Wang et al., 2018) leveraging dependent circular uniform distributions (see, e.g., Kent et al., 2008). We offer some brief remarks. To obtain the direction of maximum curvature for a spatial surface, we solve , such that , at an arbitrary point . Using Lagrange multipliers and denoting , define hence, , . With , eliminating we get .

Defining given and solving .

If then, is diagonal and corresponds to the direction of . We propose that follows a dependent circular uniform distribution over . Further developments with circular regression methods can proceed to examine the effect of covariates on . Multivariate extensions would involve formulating these differential processes on arbitrary manifolds. This requires simulating a Gaussian process on manifolds and inspecting the covariant derivative. Bayesian curvilinear wombling could then be implemented on curves of interest to the investigator. This would not only involve an inferential framework for normal curvature, but also geodesic curvature for such curves. Spatiotemporal curvature processes can build upon Quick et al. (2015) to study evolutionary behavior of the curvature processes with respect to variations in the response across time. Finally, we remark that while there have been substantial recent developments in scalable spatial processes for massive data sets—a comprehensive review is beyond the scope of the current article (see, e.g., Heaton et al., 2019)—not all scalable processes admit the correct degree of smoothness for curvature processes to exist. Constructing scalable processes for curvilinear wombling, and subsequent inference, remains a problem of interest in the wombling community.

Supplementary Materials

The following supplement includes additional theoretical derivations, computing details, additional simulation experiments and wombling for Northeastern US temperatures.

Supplementary Materials for

“Bayesian Modeling with Spatial Curvature Processes”

8 Review of Directional Gradients and Wombling

8.1 Directional Gradients

For the scalar and unit vector we define to be the first order finite difference processes at location in the directions of . Being a linear function of stationary processes this is well-defined. Passing to limits, we define . Provided the limit exist, is defined as the directional gradient process. If is a mean square differentiable process in for every then . Then, if , we can compute . The directional gradient process is linear in , hence and for any vector , . The directional gradient at in the direction is the slope at of the curve traced out by slicing in the direction (see e.g., Banerjee & Gelfand, 2006, Section 2, for more details).

8.2 Wombling Measures

Wombling measures constructed from (7) for total and average gradient are associated with curves to characterize the magnitude of change. To each point , a directional gradient is associated, (also a linear function of ), along the direction of a unit normal to the curve. For a curve tracking rapid change in the surface, choice of the normal direction to a curve is motivated by sharp directional gradients orthogonal to the curve; is chosen to be the arc-length measure. The rationale behind this choice is to measure change in response with respect to distance traversed on the curve. With reference to (7) the total and average gradients are, and respectively (see e.g., Banerjee & Gelfand, 2006, Section 3, for more details).

9 Interpretation of Spatial Curvature

Pursuits in geospatial analysis generally encounter surfaces which have canonical coordinate systems (e.g. latitude-longitude, easting-northing etc.). This facilitates a parameterization for the surface that leverages the coordinate system, commonly known as the Monge parameterization (also called a Monge patch, named after Gaspard Monge, see e.g., O’Neill, 2006; Pressley, 2010)—a surface, , embedded in , is parameterized by giving its height over some plane as a function of the orthonormal co-ordinates and in the plane, . A point is then, . The two tangent vectors at are, and , where . Let denote the gradient vector, consider a unit direction vector, , then corresponds to the directional derivative of along the direction , where is the local tangent plane at , that is generated by . The outward pointing normal to the surface , denoted by , where denotes the usual cross-product of vectors. Evidently, is orthogonal to the local tangent plane at that point, . Quantifying the local geometry of a surface, we are interested in how changes (“tips”) as we move in the direction from the point on the surface—derivatives for at the point , which lie in . This is quantified by the normal curvature of along a direction . Before defining normal curvature for a surface, we digress briefly to investigate effects of surface curvature on curves—for a curve parameterized by , , passing through , if the curvature of is, , the tangent to at , , and the principal unit normal, i.e. the normal to on , , then we have, , , which implies . We observe that,

Figure 8: A Monge patch, , showing a point , a curve passing through , normal to the surface, , normal to the curve , is the angle between them, and the local tangent plane to the surface, . The thin perpendicular pink arrows are tangent vectors, and . The thin outward pointing black arrows around demonstrate change in as we move along the direction (dotted line) on the surface.

since , , , where the expression in the parenthesis is a property of the surface, independent of curve , and is defined as the second fundamental form,

where and are the partial differentiation of and with respect to respectively, is the usual dot product for vectors and . The second to last equality is obtained under the Monge parameterization. The second fundamental form is invariant with respect to transformations of the local co-ordinate which preserves the sense of , i.e. the transformation does not change an outward (inward) pointing normal to an inward (outward) pointing normal for . Such surfaces are termed as orientable surfaces. The Möbius transformation is an example of non-orientable surfaces. The individual terms of , quantify the local geometry of a surface (or curvature) along orthonormal coordinates.

Curvature of the can be attributed to (a) the curvature of the curve itself, and (b) the curvature of the surface on which lies. is the curvature of , termed as geodesic curvature. The curvature of the surface is termed as normal curvature, computed along a direction is denoted by . The normal curvature, which is an intrinsic property of the surface independent of , is of primary interest to us, , under . is also the directional curvature of the along . For our exploits, , the normal direction to . The sign of , or equivalently eigen-values of inform about the nature of curvature at —for example, if and denote eigenvalues of , with , if , it implies that the surface is bending away from ; depending on whether (or ), can be locally classified as a concave (convex) ellipsoid (for more details see Stevens, 1981).

For a purely differential geometric treatment of this discussion see—Gauss (1902); Spivak (1999); Do Carmo (2016); Kreyszig (2019). Figure 8 illustrates this discussion.

10 Examples for selected Covariance Functions

The detailed calculations for closed form expression of selected covariance functions are presented. We start with the power exponential family of isotropic covariance functions, , . It is clear that and exists only for , we have the following form, . For this choice we have,

where . The squared exponential or the Gaussian covariance kernel is the only member of its class that admits such derivatives, although they have been critiqued to produce realizations that are too smooth to be of practical use in modeling (see Stein (1999)).

Turning to the Matérn class we see that with, , where is a parameter controlling the smoothness of realizations, that is mean square differentiability and is the modified Bessel function of order . At and , takes the forms,

where is the overall process variance. Matérn with is once mean square differentiable, where as Matérn with is twice mean square differentiable at 0. As , Matérn covariances tend to the Gaussian covariance. Unlike the Gaussian covariance, they do not yield overly smoothed process realizations. For we have,

where . Since the process is just once mean square differentiable higher order derivatives do not exist. However, for we have,

where .

The above expressions for entries of the cross-covariance matrices correspond to the joint process, with respect to our kernel choices. The following cross-covariance matrices are evaluated at .

1.

Squared Exponential: In , we have,

2.

Mateŕn : For this kernel the existence of only the gradient process is guaranteed, therefore the covariance is for the process, . In we have, .

3.

Mateŕn : In we have,

11 Algorithms

In what follows, we provide the required algorithms for sampling gradients and wombling measures. Although listed separately to highlight the requirement of only posterior samples, the required steps could be included within the MCMC subroutine devised for spatial learning (or fitting the model) of .

Sampling Gradients and Curvature:

The choice for varies between Gaussian, Matérn with and . There is scope for parallel computation across grid locations. Additionally if the inverse of estimated covariance matrices are stored for the MCMC runs from the model fit, sufficient gains in compilation can be achieved while sampling gradients. If is chosen the terms are not computed.

Input:, A Grid spanning , posterior MCMC samples , ,

Result:Posterior samples for gradients and curvature for

fordo

fordo

Compute distances of grid locations to observed process

fordo

fordo

*[r]

Posterior sample of Gradients and Curvature

return

Algorithm 1Algorithm for Sampling Gradients and Curvature

Input:, A curve , posterior MCMC samples , ,

Result:Posterior samples for wombling measures .

fordo

Compute and

fordo

fordo

Compute distances of points in curve to observed process and norms:

fordo

fordo

,

Posterior sample of Wombling Measures

return

Algorithm 2Algorithm for Sampling Wombling Measures

Sampling Wombling Measures

The choices for are again between Gaussian, Matérn with and . Choices for curves to be evaluated for wombling boundaries range from those outlined in Section 5.2. In case wombling measures for curvature are not computed. Choices for approximations include computing Riemann sums replacing quadrature for line integrals. There is scope for parallel computation with the curve being broken into segments evaluated in parallel for wombling boundaries.

The functions and denote one and two-dimensional quadrature respectively. In case a Riemann sum (see (15), Section 12) approximation is chosen, the points partitioning are treated as grid points and the algorithm for sampling gradients and curvature is used for predictive inference on the differential process. The Riemann sums are computed using and and returned.

12 Proofs and Discussion

For the curvature process formulated in Section 2, we aim to show that the covariance matrix associated with the process is valid (pg. 5 last paragraph). We obtain the expression for the covariance matrix by leveraging the directional finite difference process . For points , we denote and , are unit vectors specifying direction and as a map from , after suppressing dependence on and , , let denote a map from we compute the covariance ,

On repeated application of the chain rule and noting that , with all other higher order derivatives being 0 we have,

Similarly , and

. Next,

Similarly, , , and .

Evaluated at , i.e. , provides us with the required expression, and which exists if exists for all , including .

Note:

In the above proof we make some abuse of notation for brevity of mathematical expressions involved. To clarify, , and so on, , etc., etc.

To derive (2) and the covariance for the directional curvature process, we assume that is isotropic, i.e. therefore,

where,

suppressing dependence on , and , we define and let . Hence,

Since, , from the previous proof we can see that, . After some algebra, , , and . Substituting and grouping terms corresponding to , and we get,

which is the required expression. We discuss validity of the curvature process for surfaces in . It can be easily extended to surfaces in . Define,

as finite difference corresponding to the differential operator using the expressions of and , . For every this defines a linear transformation, since the determinant of is . We denote the differenced differential process on the right of , suppressing dependence on by . The associated covariance matrix is given by, , where elements of are obtained from . Hence, as , and , where the limits operate element-wise on the matrix and, the expression for each element is obtained from previous computations, by setting and .

For the directional operator, this can be established by observing that the directional differential operator is obtained as follows,

where denotes the direct sum for matrices, then as , . The covariance matrix is obtained following similar arguments presented in the proof for the previous result.

In case the covariance is isotropic we have , on repeated differentiation and noting that we have,

Differentiating w.r.t. we obtain,

On grouping terms for and we obtain the required expression,

To obtain we differentiate w.r.t. , we use notations , , for matricized tensors of order , where the order of matricization conforms to the listing order of the half-vectorization operator and denotes the element-wise product of with in the same order as the matricized tensor.

On differentiating the factor corresponding to the coefficient we obtain,

Differentiating ,

Differentiating the factor corresponding to the coefficient we obtain,

finally, differentiating . Grouping coefficients for , and we obtain the required expression, thereby completing the proof.

For proving the result focusing on spectral theory, note that since is symmetric about 0 by hypothesis,

Differentiating w.r.t. on both sides we have,

Since and under hypothesis, differentiation under the integral sign is valid. We repeat the process to obtain,

,

,

Next we make the following observations for limits of these derivatives,

We evaluate the results obtained above under these observations. Making note of,

,

stay bounded as implying as . For , we observe that the factors corresponding to , and remain bounded as , additionally as . For each diagonal element of which completes the proof.

For results in page 8, we prove this for , the proof can be extended to analogously. Under the hypothesis,

independently. Without loss of generality, consider the finite difference differential process,

noting that for every , follows a -dimensional normal distribution and , making the above linear transformation non-singular. We know from properties of multivariate normal distributions that , where , the cross-covariance matrix for the process is , where , with . As , and , where indicates convergence in distribution. As , implying that . The same arguments can be followed for showing .

1.

for (a) consider the associated finite differential operators, and . We note that for every , , which is the zero matrix (of order ). Now consider the process,

as , which implies , and since they jointly follow a multivariate Gaussian this implies that they are independent. Observing that the cross covariance for all , , we can establish that they are independent Gaussian processes.

2.

(b) and (c) follow from standard properties of the Gaussian processes.

For the discussion on page 14 preceding (14) we suppress dependence on and , we denote . By definition of the integral, given , there exists a such that if , then

(15)

where is a Riemann sum approximation of the integral. On the other hand, since is uniformly continuous over , given , there exists such that if with ,

Set , then , using the mean value theorem we obtain,

where the first inequality follows from the assumption of being regular. Together with the inequality in (15) we have,

Finally, almost sure convergence yields for every ,

Considering a sequence of , and using the preceding arguments for each we can find such that which concludes the proof.

13 Tables

Table 6: Table showing results for goodness of fit from the first synthetic experiment where the true response is generated from .

Sample Size

Parameter

Estimate

RMSE

2.91

(2.13, 3.81)

218.35

(69.69, 588.86)

0.05

9.74

9.86

150.82

91.49

180.38

(Truth = 1.00)

0.96

(0.00)

(0.23)

(0.31)

(4.94)

(1.94)

(2.10)

(0.63, 1.39)

0.00

(-0.06, 0.06)

2.30

(1.88, 2.73)

367.17

(166.27, 784.53)

0.04

6.66

6.84

127.99

68.11

126.71

(Truth = 1.00)

0.99

(0.00)

(0.10)

(0.12)

(3.40)

(2.56)

(2.69)

(0.86, 1.13)

0.00

(-0.06, 0.06)

2.00

(1.60, 2.36)

553.79

(231.95, 1385.62)

0.03

5.64

6.45

97.16

61.54

114.97

(Truth = 1.00)

1.04

(0.00)

(0.18)

(0.19)

(2.05)

(2.27)

(2.22)

(0.95, 1.14)

0.00

(-0.06, 0.06)

Table 7: Table showing results for goodness of fit from the second synthetic experiment where the true response is generated from .

Sample Size

Parameter

Estimate

RMSE

5.06

(3.69, 6.72)

38.96

(15.52, 85.33)

0.06

16.12

11.49

258.91

159.54

183.54

(Truth = 1.00)

0.83

(0.00)

(0.13)

(0.22)

(3.16)

(1.19)

(3.70)

(0.53, 1.23)

-3.12

(-0.34, 5.04)

3.63

(3.05, 4.38)

114.36

(44.59, 211.47)

0.04

7.04

7.39

179.23

98.39

169.19

(Truth = 1.00)

0.93

(0.00)

(0.17)

(0.17)

(6.94)

(3.76)

(5.16)

(0.80, 1.07)

-0.15

(-2.14, 2.49)

2.89

(2.55, 3.26)

173.19

(94.06, 297.76)

0.03

6.19

6.21

167.27

93.21

163.44

(Truth = 1.00)

1.01

(0.00)

(0.26)

(0.17)

(10.40)

(6.75)

(8.84)

(0.91, 1.10)

-0.22

(-2.03, 2.15)

14 Plots

Figure 9: Illustration showing geometric interpretation of curvilinear wombling. Local tangent planes are shaded around points , . Normals to the surface are marked as and , locally projected principal unit normals to the projected curve are marked as and respectively. The tangent vectors spanning the local tangent planes are shown with arrows.

Figure 10: Illustration of rectilinear wombling, showing a curve , an initial starting point on the curve, with following points, corresponding a partition , of the parameterized curve. Each linear segment consists of a norm-direction pair , where specifies the length of the segment and the direction of movement. The normal direction for each segment is indicated as .

Figure 11: Plots showing the true surfaces for the (a) process, (b) gradients along -axis, (c) gradients along -axis, and estimated surfaces for the (d) process, gradients (e), (f) w.r.t. synthetic response generated, Figure 12: Plots showing the true surfaces for the (a) curvature along -axis, (b) curvature along --axis, (c) curvature along -axis, and estimated surfaces for (d) curvature along -axis, (e) mixed curvature along --axis, (f) curvature along -axis, for synthetic response generated from, .Figure 13: Plots showing the true surfaces for the (a) process, (b) gradients along -axis, (c) gradients along -axis, and estimated surfaces for the (d) process, gradients (e), (f) for synthetic response generated from, .Figure 14: Plots showing the true surfaces for the (a) curvature along -axis, (b) curvature along --axis, (c) curvature along -axis, and estimated surfaces for (d) curvature along -axis, (e) mixed curvature along --axis, (f) curvature along -axis, for synthetic response generated from, .Figure 15: Plots showing the true surfaces for (a) eigen value, (b) eigen value , (c) Gaussian curvature (scales in ) (d) divergence (e) Laplacian (scales in ) over grid points, and (f) fitted process. This is shown for synthetic response generated from, .Figure 16: Plots showing the estimated surfaces for (a) eigen value, (b) eigen value , (c) Gaussian curvature (scales in ) (d) divergence (e) Laplacian (scales in ) (f) fitted process over grid points. Each point is color coded; green denoting the HPD intervals not containing 0, with positive end points, while cyan denotes HPD intervals not containing 0, with negative end points.Figure 17: Plots showing the true surfaces for (a) eigen value, (b) eigen value , (c) Gaussian curvature (scales in ) (d) divergence (e) Laplacian (scales in ) (f) fitted process over grid points. This is shown for synthetic response generated from, Figure 18: Plots showing the estimated surfaces for (a) eigen value, (b) eigen value , (c) Gaussian curvature (scales in ) (d) divergence (e) Laplacian (scales in ) (f) fitted process over grid points. Each point is color coded; green denoting the HPD intervals not containing 0, with positive end points, while cyan denotes HPD intervals not containing 0, with negative end points.Figure 19: Plots showing observed versus fitted values for (a) the response variable ; (b) gradients with respect to -axis; (c) gradients with respect to -axis; (d) curvature with respect to -axis; (e) mixed curvature over -; (f) curvature for with respect to -axis. The gray shades represent the 95% HPD regions for each estimate.Figure 20: Plots showing observed versus fitted values for (a) the response variable ; (b) gradients with respect to x-axis; (c) gradients with respect to -axis; (d) curvature with respect to -axis; (e) mixed curvature over -; (f) curvature for with respect to -axis. The gray shades represent the 95% HPD regions for each estimate.

Figure 21: Plots showing results for curvature wombling on the Meuse river (first row) Copper (Cu) (second row) Lead (Pb) (third row) Zinc (Zn).

15 Further Application

15.1 Temperatures in Northeastern US

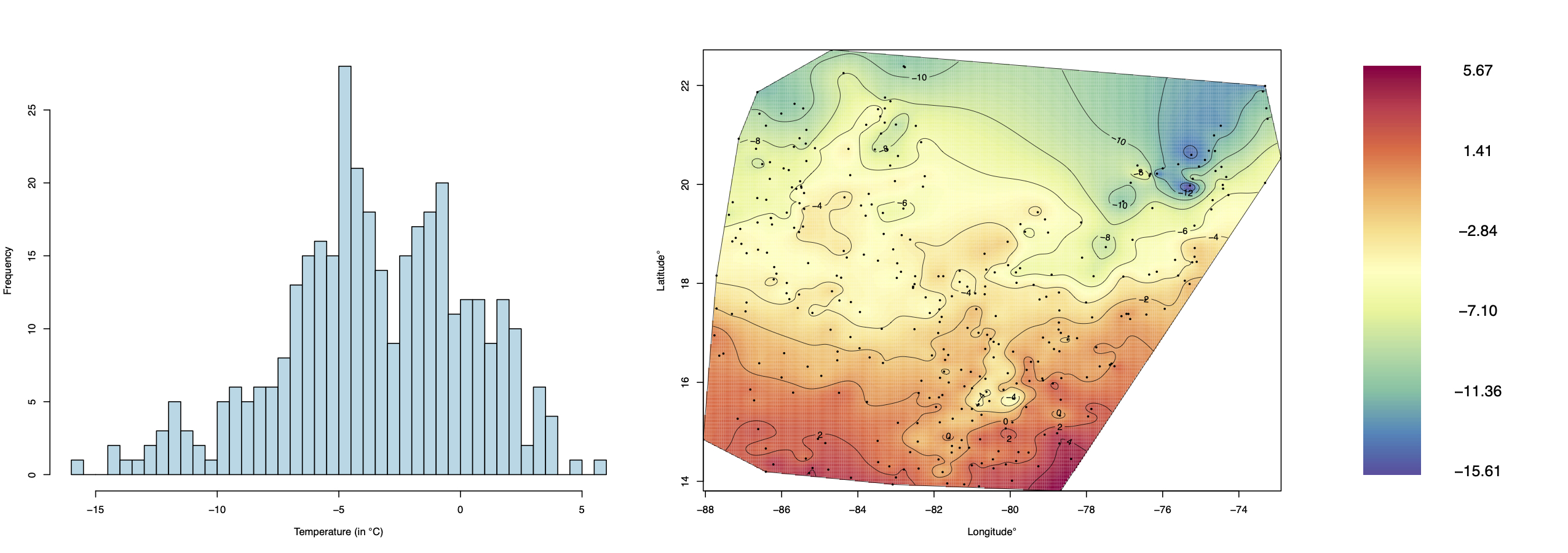

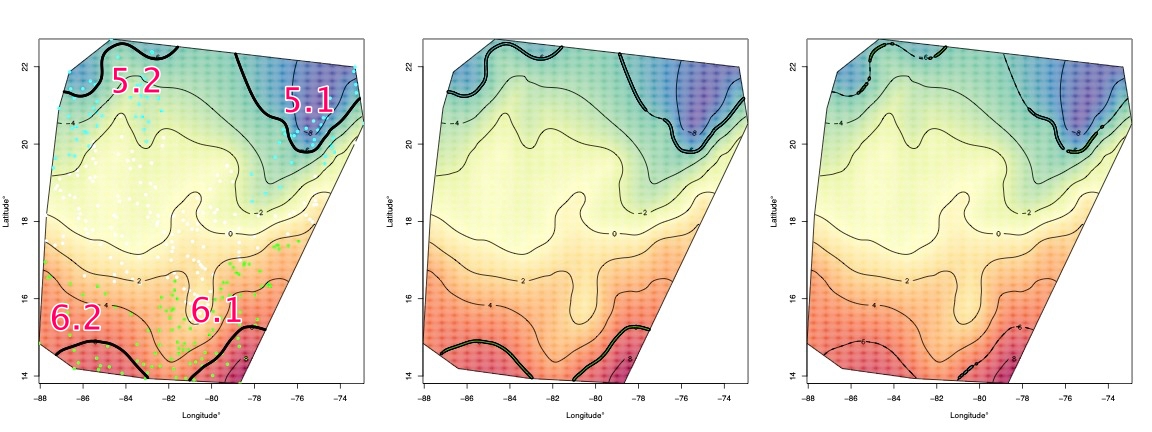

Temperatures are historically known to exhibit spatial variation. We focus on a data set that records monthly temperatures across weather monitoring stations in the Northeastern United States during January, 2000 from the R-package spBayes (Finley et al., 2007). Temperature gradients and curvature are of interest from an environmental science perspective to track and perform boundary analysis on zones that exhibit significant changes in the surface during a month. Curvature wombling performed on temperature reveals climate zones featuring rapid atmospheric changes. Quantifying such variations in atmospheric conditions is central to statistical modeling in environmental applications. The data consists of temperatures (in degree Celsius) from 356 weather monitoring stations. The probability distribution for temperatures and interpolated spatial plot is shown in Figure 22. We model the data using the hierarchical model outlined in (13) in the manuscript. We used the following hyper parameters for the model, , (mean 1 variance infinite), (mean 1 variance infinite), , and for the Matérn kernel. We consider iterations for MCMC chains, with burn-in diagnosed at . The posterior estimates from the model fit are shown in Table 8.

Figure 22: Plots showing (left) probability density of temperatures (in °C) (right) spatial plot of temperatures in Northeastern US during January 2000.

We fit the model with only an intercept, that allows the spatial process to capture most of the variation in the data. We observe from Table 8 that . Significance in process parameter estimates is assessed by checking containment of 0 within the HPD intervals. The fitted spatial process, along with significance is shown in Figure 23 (top row, left). For temperature observations falling in the middle no significant spatial effect is observed, with stations located in the northern and southern regions showing positive and negative spatial effects. This indicates a clear variation in the north-south direction for temperatures in January. The variance of the nugget process is small compared to . The average estimated temperature is C .

Table 8: Posterior Estimates for Temperatures in Northeastern US. The highest posterior density intervals are shown alongside for respective estimates.

Parameters ()

Posterior Estimates ()

Highest Posterior Density intervals (HPD)

0.38

(0.27, 0.51)

21.44

(10.11, 41.03)

0.92

(0.76, 1.10)

-3.78

(-5.92, -1.69)

Using the posterior estimates for and the spatial process we perform a gradient and curvature assessment over the estimated posterior surface. We use Algorithm 1 outlined in section 11 for sampling gradients and curvature. This is done over a grid encompassing the spatial domain of reference, . A grid consisting of 461 points is laid out over the convex-hull of . The estimated gradients along and -axis are shown in the first row for Figure 23. Elements of the directional curvature process along and -axis are shown in the second row. Significance is again indicated by checking containment of 0 within HPD intervals for posterior gradients and curvature. Significant directional curvature is indicative of significant rate of change in temperature gradients along the chosen axis. quantifies interaction between rates of change in gradients along and axis respectively. A significant at the grid location indicates that the rate of change with respect to axis was significantly influenced by change along -axis. Regions of local maxima (elliptic points) generally manifest themselves with alternating zones of increasing and decreasing gradients (or curvature) separated by a zone of saddle points (around the location of said maxima). This can be witnessed in the north-eastern region and south-eastern regions where these maxima (minima) occur.

Figure 23: Plots showing (top row) (left) the fitted spatial process (center) the estimated gradient, process along -axis (right) the estimated gradient, process along -axis (bottom row) (left) estimated curvature along -axis (center) estimated curvature, (right) estimated curvature, along -axis.

Posterior surface is effected on the same grid using the posterior estimates for , and . We leverage these to produce estimated surfaces for the Gaussian curvature (determinant) (shown in left of Figure 24), the divergence operator (shown in center of Figure 24) and Laplacian (shown in right of Figure 24). Posterior surfaces for the Gaussian curvature are indicative of locations/presence of maximas and saddle points, divergence surfaces show regions of rapid change in temperatures while the Laplacian shows regions of maximum change in gradients. Gaussian calibration for these estimate attaches significance allowing us to distinguish between contiguous zones housing significant change.

Figure 24: Plots showing surfaces for (left) Gaussian curvature (center) divergence and (right) Laplacian of temperatures in Northeastern US during January 2000.

We perform curvature wombling using inference obtained from the posterior analysis of the surface. Figure 25 and Table 9 show the results for curvilinear wombling on the resulting posterior estimates of the surface. The curves chosen are shown in plots on the left for Figure 25. We begin with curves (level sets) “1” and “2” that delineate zones of significant (positive in the south and negative in the north) spatial effects, iteratively proceeding to higher (lower) level sets while inspecting them for curvilinear gradients and curvature. Referring to Table 9, we observe that all curves located with respect to curvilinear gradients, observed from significant average gradients. With respect to directional curvature, we refer to significant segments located in the Figure 25 which show enormous heterogeneity, i.e. changes in directional concavity when traversing the curve, with separated contiguous segments indicating significant changes in concavity. For instance traversing curve “2” in the west-east direction, we observe this clearly. This naturally renders the average directional curvature (shown in Table 9) insignificant when considered along the entirety of curve “2”, which is also the case for other level sets. To be able to detect significance we could only summarize across significant segments (as was done for the Meuse river data).

Table 9: Curvilinear Wombling measures for boundaries in Northeastern US Temperatures, each measure is accompanied by its corresponding HPD interval in brackets below.

Curve ()

Average Gradient ()

Average Curvature ()

Boundary 1

2.44

-0.38

(1.90, 2.97)

(-1.48, 0.74)

Boundary 2

2.70

-0.40

(2.24, 3.18)

(-1.67, 0.79)

Boundary 3

2.69

-0.34

(2.10, 3.28)

(-1.71, 0.84)

Boundary 4

2.23

-0.31

(1.74, 2.72)

(-1.67, 1.11)

Boundary 5.1

-2.96

1.13

(-4.22, -1.73)

(-0.88, 3.16)

Boundary 5.2

-3.24

-0.23

(-4.22, -2.25)

(-2.19, 1.69)

Boundary 6.1

1.63

-0.23

(0.70, 2.58)

(-2.96, 2.62)

Boundary 6.2

2.90

-0.38

(1.93, 3.92)

(-3.00, 2.31)

Figure 25: Plots showing curvature wombling on temperatures data. The curves are marked in each row on the figure to the left are to be referenced with Table 9 showing average wombling measures for gradient and curvature for respective curves.

References

(1)

Abramowitz et al. (1988)

Abramowitz, M., Stegun, I. A. & Romer, R. H. (1988), ‘Handbook Of Mathematical Functions With

Formulas, Graphs, and Mathematical Tables’.

Adler (1981)

Adler, R. J. (1981), The Geometry Of

Random Fields, SIAM.

Albering et al. (1999)

Albering, H. J., Van Leusen, S. M., Moonen, E., Hoogewerff, J. A. & Kleinjans, J. (1999), ‘Human Health

Risk Assessment: A Case Study Involving Heavy Metal Soil

Contamination After The Flooding Of The River Meuse During

The Winter Of 1993-1994.’, Environmental Health Perspectives107(1), 37–43.

Banerjee et al. (2014)

Banerjee, S., Carlin, B. P. & Gelfand, A. E. (2014), Hierarchical Modeling And Analysis For

Spatial Data, CRC press.

Banerjee & Gelfand (2003)

Banerjee, S. & Gelfand, A. (2003),

‘On Smoothness Properties Of Spatial Processes’, Journal of

Multivariate Analysis84(1), 85–100.

Banerjee & Gelfand (2006)

Banerjee, S. & Gelfand, A. E. (2006), ‘Bayesian Wombling: Curvilinear Gradient

Assessment Under Spatial Process Models’, Journal of the

American Statistical Association101(476), 1487–1501.

Banerjee et al. (2003)

Banerjee, S., Gelfand, A. E. & Sirmans, C. (2003), ‘Directional Rates Of Change Under Spatial

Process Models’, Journal of the American Statistical Association98(464), 946–954.

Burrough et al. (2015)

Burrough, P. A., McDonnell, R. A. & Lloyd, C. D. (2015), Principles Of Geographical Information

Systems, Oxford University Press.

Chen & Shao (1999)

Chen, M.-H. & Shao, Q.-M. (1999),

‘Monte Carlo Estimation Of Bayesian Credible And HPD

Intervals’, Journal of Computational and Graphical Statistics8(1), 69–92.

Chiu et al. (2013)

Chiu, S. N., Stoyan, D., Kendall, W. S. & Mecke, J.

(2013), Stochastic Geometry And