ODEWS: The Overdraft Early Warning System

Abstract.

When a customer overdraws their account and their balance is negative they are assessed an overdraft fee. Americans pay approximately $15 billion dollars in unnecessary overdraft fees a year, often in $35 increments; users of the Mint personal finance app pay approximately $250 million dollars in fees a year in particular. These overdraft fees are an excessive financial burden and lead to cascading overdraft fees trapping customers in financial hardship. To address this problem, we have created an ML-driven overdraft early warning system (ODEWS) that assesses a customer’s risk of overdrafting within the next week using their banking and transaction data in the Mint app. At-risk customers are sent an alert so they can take steps to avoid the fee, ultimately changing their behavior and financial habits. The system deployed resulted in a $3 million savings in overdraft fees for Mint customers compared to a control group. Moreover, the methodology outlined here can be generalized to provide ML-driven personalized financial advice for many different personal finance goals–increase credit score, build emergency savings fund, pay down debt, allocate capital for investments.

1. Introduction

Overdraft fees largely fall on the most vulnerable customers often living paycheck-to-paycheck and are considered excessive and exploitative(Valenti, 2022). Americans typically pay $15 billion a year in avoidable overdraft fees. The same 9% of customers pay 80% of overdraft fees, often paying more than 10 overdraft fees in a year. Moreover, overdraft fees can discourage the most vulnerable customers from even participating in the banking system due to the high cost of banking by incurring these fees(CFPB, 2013).

An overdraft fee is charged by the bank for accepting a transaction when there are insufficient funds; a non-sufficient fund fee is charged for denying a transaction when there are insufficient funds. When an overdraft or non-sufficient fund fee is charged depends on a bank’s terms of service. For this work we use the term overdraft fee for both types of fees as we are interested in preventing both. An account can be overdrawn in one of five ways due to insufficient funds: a check is denied (bounce a check), electronic debit, debit card transaction, ATM withdrawal, or in person withdrawal. Originally, overdraft fees were a rare occurrence. The bank would charge a fee to customers who had not properly balanced their checkbook. With the popularization of debit transactions and electronic bill payments, overdraft fees have ballooned into a billion dollar revenue stream for banks. This is how a $5 coffee transaction can become a $40 transaction or a $15 electronic bill payment can become a $50 bill payment. Ultimately, this can lead to cascading overdraft fees, creating a financial burden, and trapping customers in a cycle of fees and low balances.

There has been a patchwork of temporary and uneven measures to combat overdraft fees. During the Covid-19 pandemic many banks granted waivers to customers who knew to request them while some banks waived overdraft fees for all customers temporarily. There has also been legislation proposed in the United States, 2021 Stop Overdraft Profiteering Act(Booker, 2022), but not passed. Existing AI work in the financial space revolves around explainable AI for trading(Kumar et al., 2022), trading strategies(Jevtic et al., 2022), risk management(Zhao et al., 2022), and fraud detection(Varmedja et al., 2019); these works focus on financial markets(Tadapaneni, 2019) rather than personal finance. There have also been retrospective economic studies on the impact of overdrafts and predatory lending(Melzer and Morgan, 2015; Alan et al., 2018) and the positive benefits of providing SMS notifications for overdrafts and loan repayments(Caflisch et al., 2018). In the behavioral sciences, there has been work on finding effective nudge messaging to reduce overdrafts(Ben-David et al., 2019).

In light of temporary and uneven measures from banks, stalled legislative efforts, and other challenges in preventing overdraft fees, the authors have created an ML-driven Overdraft Early Warning System (ODEWS) on the Mint app. Currently, there is to the best of our knowledge no ML-driven solution to prevent overdrafts. The problem has been cast as a binary classification problem where the system predicts a customer’s likelihood of overdrawing their checking account in the next week by leveraging platform and transaction data. At-risk customers are then provided an early warning through email notification to prevent overdrafts and ultimately save our customer’s money. This work builds on prior work (Ben-David et al., 2019) by focusing on the ML-aspects of assessing the risk of overdrafting and providing an effective intervention. ODEWS was deployed in November 2019. An example of the output of the model is shown in Table 1, where customers are ranked by their risk of overdrafting.

There are several challenges in preventing overdrafts fees that make it suitable for an ML-driven solution. Firstly, different banks have different policies regarding the cost of the overdraft fee, the number of overdraft fees that can be charged to a customer in a day, the grace period an account can be made current, different thresholds until an overdraft fee is assessed, and different fees for different types of overdrawing an account(Chang, 2020). A ML-based model can learn these policies per bank and adapt to changes over time. Secondly, banks order transactions in order of largest amount transaction to lowest amount transaction during nightly processing (known as Transaction Processing Order) which can make it difficult to predict an overdraft. Although the Mint app receives balance and transaction data, the app does not receive the data in real time, oftentimes there can be a delay of hours to days depending on the financial institution. The transaction processing order and lag in receiving data rule out the possibility of simply waiting for a pending transaction to appear, calculating whether the transaction will place a customer in a negative balance, and then alerting the customer before the transaction is posted. Instead, an ML-model can leverage financial data and predict if a customer is going to overdraft. Finally, we are seeking to quantify the risk of a customer overdrawing their account. There are a constellation of factors that lead to an overdraft besides a point-in-time balance and debits that can be leveraged in a systematic and structured way using an ML-model to provide an individualized measure of risk, ranking of customers based on risk, and even inform the type of intervention.

| ID |

Total

Overdrafts |

Overdrafted

this week |

Days Since

Overdraft |

Balance | Risk Score |

| 01 | 95 | True | 2 | -$700.00 | 99 |

| 02 | 5 | False | 9 | $11.30 | 81 |

| 03 | 1 | False | 104 | $700.00 | 74 |

Since the time of this work and current time of this writing many banks have reduced overdraft fees, adopted less punitive policies, and a few smaller banks have outright eliminated the fees(Arnold, 2022). Despite this positive change, many of the largest banks are still charging overdraft fees and overdraft fees still remain an unnecessary drag on a customer’s cash flow.

1.1. Overdraft Problem for Mint Customers

The Mint app is a personal finance app with 20 million users in the United States and Canada that tracks customer’s transactions by linking their bank accounts, credit cards, and investment accounts; the app also provides budgeting tools, forecasting, and personal finance insights. A decrease in unnecessary overdraft fees paid by Mint customers is a significant savings that protects our customer’s cash flow–especially for those who are living paycheck-to-paycheck. Mint users pay on average $250 million dollars in unnecessary overdraft fees every year. The average customer overdrafts 1.8 times before they are aware they overdrafted their account. Before this project, Mint customers would incur overdraft fees without warning. Figure 1 shows the breakdown of overdraft fees of Mint customers across nine banks over the period 9/2019-9/2020. Typically, the amount of fees collected scales with the number of customers with the largest three American banks, Chase, Bank of America, and Wells Fargo, collecting the largest share.

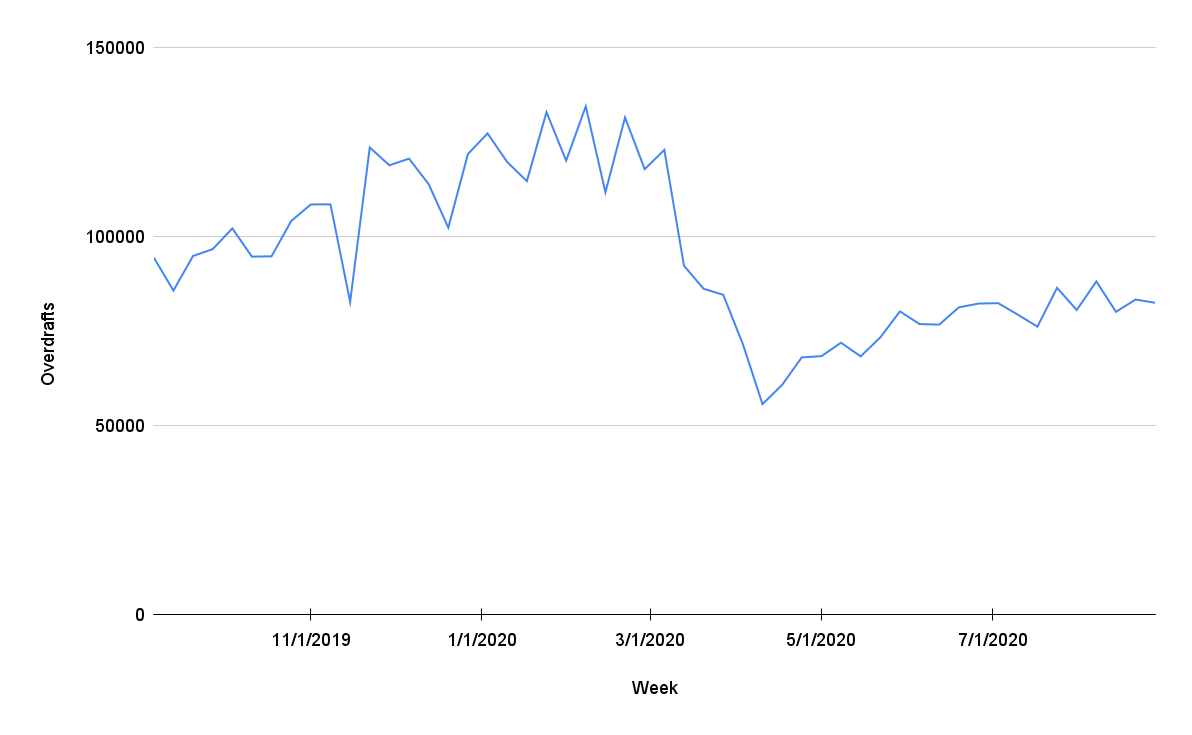

ODEWS was deployed during the Covid-19 pandemic which saw a sudden and extreme shock on the American economy. Suddenly, many Americans were unemployed and businesses were shuttered, leading to a precipitous decline in economic activity. As Figure 2 shows, there was a sudden decrease in overdrafts at the beginning of the pandemic, approximately 03-2020, due to a sudden decrease in transaction volume as a result of shutdowns caused by the pandemic. Secondly, banks modified their overdraft policies to temporarily suspend overdrafts or adopt more lenient overdraft policies. In this case both the behavior of the customer as well as overdraft policies were changing lending itself to an ML-solution that is adaptable to a rapidly changing environment.

2. Data Sources

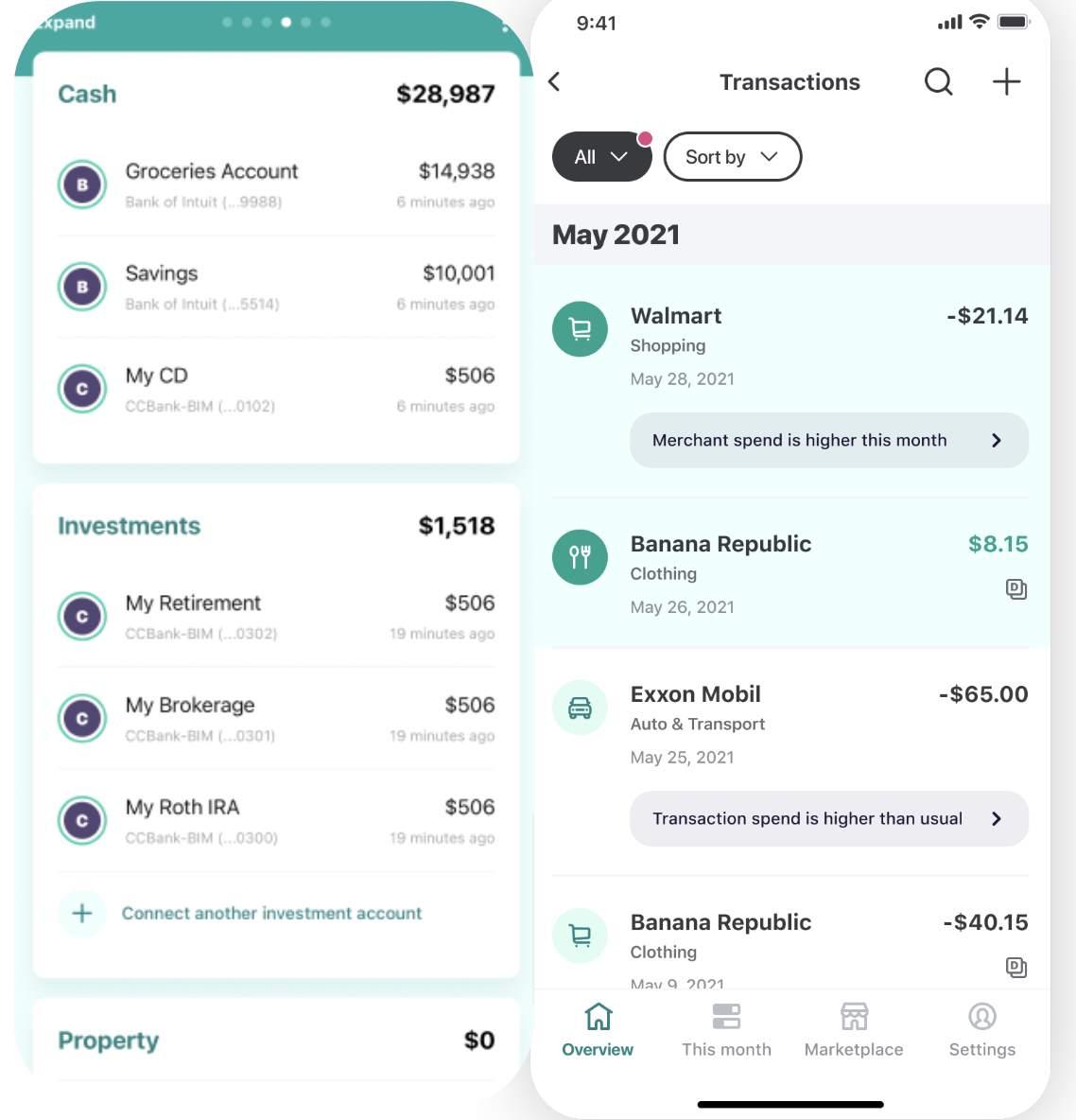

The data used for this work is derived from a customer’s banking, platform, and transaction data collected by the Mint app (Figure 3).

2.0.1. Banking

The Mint app allows customers to link their financial accounts. This includes checking and savings accounts, CDs, money market accounts, credit card accounts, and investment accounts as well as their respective balances.

2.0.2. Platform

Platform data includes the number of logins a user has in the Mint app as well as clickstream regarding what pages they access in the app.

2.0.3. Transaction History

As part of linking financial accounts to the app, Mint will fetch the transaction history of customers. This includes the transaction timestamp, amount, transaction description, and transaction category.

2.0.4. Data Limitations

The main limitation of the data is due to the velocity the Mint app receives the latest banking and transaction data. The time from when a transaction is made and transits to the Mint app can be anywhere from hours to days. Several banks require customers to log-in to Mint, provide a two-factor authentication, and then the app can fetch the latest transactions. Moreover, several banks do not provide data over the weekend while transaction processing is occurring, which can lead to scenarios where a customer can spend over the weekend and not realize they have overdrafted until transaction processing is complete on Monday morning. Secondly, Mint bank balance data also has a lag that is often slower than the velocity that the app receives the latest transaction data. This can lead to scenarios where the app believes a customer has a positive balance but in actuality they have a negative balance and are actively overdrafting their account.

3. Methodology

This section describes the overall methodology from extracting features to training, selecting and evaluating machine learning models.

The unit of prediction is a customer and checking account on a given day. The majority of customers have a single checking account. There are a set of features derived from the customer as well as a set of features derived from the transaction history of the checking account.

The label of whether a customer has overdrafted is derived by searching through transaction history. Each bank has their own unique transaction descriptions to indicate whether a fee has been assessed. Searching through transaction history through manual curation and keyword search, we were able to identify the transaction descriptions that indicate an account was overdrawn and match the description to a bank based on the origin of the account. On the (simulated) day of prediction, we look-forward one week to search through customer transaction history and find any overdraft fee transactions. If any overdraft fees are found then this is a positive label (overdrafted within the next week) otherwise the customer/account is given a negative label (did not overdraft in the next week).

The features of the model can be divided into two categories: user-level features and account-level features. The user level features are the number of checking accounts, credit card accounts, savings accounts, CD accounts, and investment accounts on the day predictions are made. Other features include the number of logins and total number of overdrafts across all accounts looking back one-month from the day of prediction. The account level features are the last known balance in the account before the day of prediction as well as transaction activity before the day of prediction. Due to fetching both transactions and balances at different times, customer balances can often be out of sync of the true balance. To address this problem a new balance is calculated by fetching the last known balance, transactions that were made after the last known balance timestamp, and calculating a new balance. The transaction history of an account is featurized by first dividing transactions into credit and debits and creating the following features: The total number of credit and debit transactions, min, max, and average amounts over a four-week and one-week look back window from the day of prediction; the number of debit transactions under $50 as well the number of credits over $200 over the last two months from the day of prediction; the total number of times an account has been overdrafted in the last six months from the day of prediction; the average number of weekly overdrafts over the last six months, whether a customer has overdrafted this week (last seven days) from the day of prediction, as well as the number of days since the last overdraft in the last six months. Different look-back windows were tested for different features. The look-back windows for features reported here provided the best model performance.

4. Modeling Approach and Results

The cohort of interest that receives a prediction are Mint customers who have overdrafted at least once in the last six months and have a checking account from the following banks: Chase Bank, Bank of America, Wells Fargo, US Bank, TD Bank, Citibank, PNC Bank, Navy Federal Credit Union, and Ally Bank. (Note: At the time of this deployment Citibank and Ally Bank were charging customers overdraft Fees. They have since eliminated overdraft fees at the time of this writing. Now, each bank will simply deny transactions at their discretion based on their respective overdraft policies(noa, 2022, 2021)). Many Mint customers likely have overdraft protection coverage where if an overdraft occurs, rather than being charged a fee, the bank will draw funds from the customer’s savings account or charge a credit card. We do not have insight into which customers have overdraft protection and which do not. To prevent sending overdrafts warnings to customers with overdraft protection we restrict our cohort to customers who have overdrafted in the last six months and assume they have no overdraft protection since they have received an overdraft fee. There is a trade off to this approach where any customer who overdrafts for the first time in the last six months will not be in the prediction cohort. Although we are missing a small portion of overdraft fees through this conservative approach, we are avoiding false positive notifications ensuring customers have faith in the system when they do receive a notification. If a customer were to enable overdraft protection while being in the cohort, they would decrease in risk as time went on and fall out of the high-risk list of customers.

The goal of the model is to predict if a customer will overdraft within the next week; to that end, the model calculates predictions every Friday afternoon. We currently do not make a point-of-time prediction after a transaction is made due to technical limitations. Also due to limitations with fetcing data from banks, the Mint app receives transaction at different cadences from banks leading to performance differences for each bank compared to historical offline testing. At this time, this is a limitation of the system. After the model generates predictions, a list of at-risk customers is created and they are sent an email notifying them we believe they are about to overdraft. This then provides the customers the opportunity to adjust their spending, transfer money, or contact the bank for a waiver. Due to diverging overdraft policies of different banks, particularly during the height of the Covid-19 pandemic, a separate model was created for each individual bank. Empirically, this provided better performance.

4.0.1. Temporal Cross-Validation:

The model training scheme is designed to mimic the deployment process in order to have the most accurate performance results. The model is trained using temporal cross-validation to take into account temporal effects and serial correlations that affect customer behavior (features) and overdraft policies (labels)(Foster, 2021). As can be seen from Figure 2 and previously stated, during the height of the Covid-19 pandemic there were extreme exogenous shocks in customer behavior and overdraft policies. The model is retrained every week to take into account any temporal effects such as shutdowns, re-openings, government stimulus payments(Flitter, 2020), and changes in overdraft policies that would affect overdraft behavior. An example of temporal cross-validation is the following: if simulating making a prediction on 2020-06-14 the label is calculated between the dates 2020-06-07–2020-06-14 and features are calculated looking back six months from the date 2020-06-07. The test-set of the model is then calculated using a label from 2020-06-14–2020-06-21 and features looking back six months from 2020-06-14. In this way, train-test pairs are created every week over six months and used to train models.

4.0.2. Model Selection:

Different classification methods (Decision Trees, Gradient Boosted Decision Trees, and Neural Nets), hyperparameters, training data time ranges, and feature sets where compared to each other using precision@k%, recall@k%(Stąpor, 2018), as well as model stability over time. Precision@k% and recall@k% are metrics commonly found in information retrieval and search engine literature(Foster, 2021) where it is important that the items flagged at the top of a list are accurate. Rather than optimizing the model for an aggregate metric such as AUC, the local precision-recall space is optimized to maximize the number of customers that will overdraft in the top k% and provide an accurate measure of the performance of the deployed model.

The model informs which customers will receive an email intervention. An email is a low-cost intervention with no resource constraints allowing considerable flexibility regarding who receives an email as well as how many emails can be sent every week. To guide how many notifications are sent we have to consider the costs of false positive and false negative cases. A false positive case is where a customer receives a notification but will not overdraft. These messages can inure the customer to future messages and make them lose trust in the system when they receive future notifications. A false negative case is when a customer does not receive a notification and overdraws their account.

Models were selected with the goal to maximize precision@k% and recall@k% at the highest k%. To that end, models were selected where and to balance precision and recall. False positives and false negatives were implicitly balanced in this approach and assumed to be equally harmful. For the banks Wells Fargo, Chase Bank, US Bank, Navy Federal Credit Union, TD Bank and Citibank models that balanced precision@k% and recall@k% were found. In cases where precision@k% and recall@k% could not be easily balanced–Bank of America, PNC Bank, Ally Financial–precision@k% was favored and set to to minimize false positives. The k%, percentage of customers each week that receive a notification, precision@k%, recall@k% and model type can be found in Table 2. Figure 4, shows a specific example for Chase Bank. In this case the threshold of k% is set at 10% and precision@k% is 0.42 and recall@k% is 0.45, roughly balancing the precision@k% and recall@k%. For 8 of the 9 banks, a GBDT (Gradient Boosted Decision Trees)(Friedman, 2002) model was the most performant model and the best performing model for Ally Financial was a Feed Forward Neural Net. Model hyperparameters and architecture can be found in Table 3. As is common in problems assessing risk, boosting largely performed better than deep learning methods(Rudin and Carlson, 2019).

To understand if the system was worth deploying, each bank’s model was compared to the bank’s prior and a rules-based baseline. Overall, each model had a 4-15x lift compared to the prior. Since there is no current process for preventing overdrafts, a 2-deep decision tree was created for each bank to simulate the best business rules that can be found. Comparing each model to a 2-deep decision tree model, each model has a 1.17-2x lift compared to the 2-deep decision tree, showing the model was worth deploying. Full details can be found in Table 2.

Another aspect of the model that was important to optimize is balancing performance and stability over time. Different models had different levels of variance and performance over time which can lead to large variances in performance week over week. Through temporal-cross validation we are able to measure the model performance over time after choosing how many customers, k%, the model will flag. The final model selected is chosen for having the best performance over the last four weeks compared to the best possible performance of all models trained and being within 5% of the precision of the best possible model within the last four weeks. This method ensures both stability and performance.

| Bank | Model Type | k% | precision@k% | recall@k% | Prior (Baseline) | Lift over Prior | Lift over Business Rules |

| Wells Fargo | GBDT | 10 | 0.43 | 0.45 | 0.1 | 4.3 | 1.23 |

| Chase | GBDT | 10 | 0.42 | 0.49 | 0.09 | 4.67 | 1.17 |

| Bank of America | GBDT | 6 | 0.46 | 0.33 | 0.09 | 5.11 | 1.44 |

| Navy Federal Credit Union | GBDT | 7 | 0.45 | 0.5 | 0.05 | 9 | 2.05 |

| US Bank | GBDT | 5 | 0.5 | 0.49 | 0.05 | 10 | 1.56 |

| TD Bank | GBDT | 6 | 0.52 | 0.4 | 0.09 | 5.78 | 1.44 |

| PNC Bank | GBDT | 2 | 0.45 | 0.26 | 0.03 | 15 | 1.88 |

| Ally Financial | FFNL | 2 | 0.48 | 0.17 | 0.06 | 8 | 1.66 |

| Citibank Banking | GBDT | 6 | 0.46 | 0.4 | 0.07 | 6.57 | 1.44 |

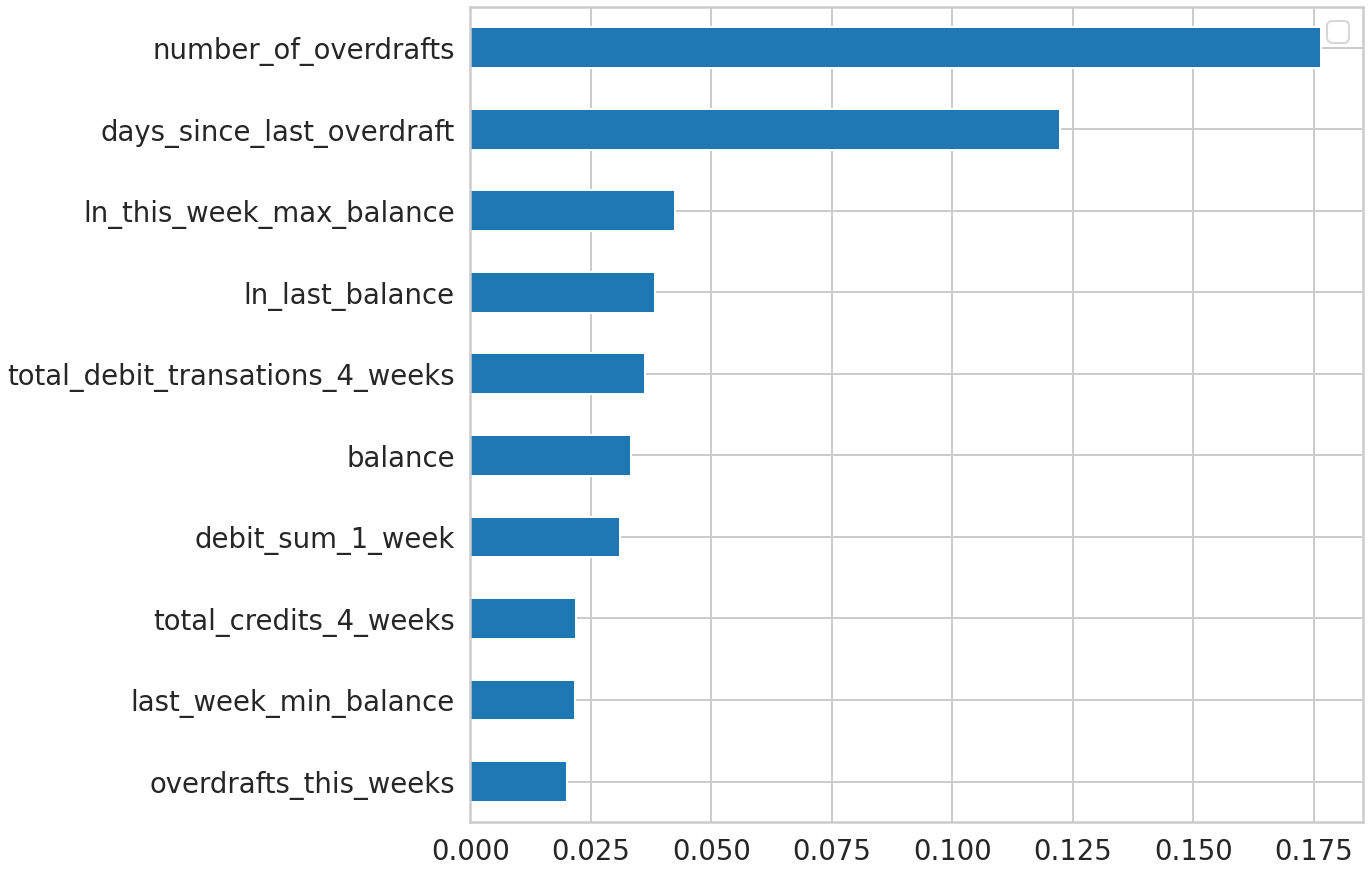

4.0.3. Feature Importances:

Feature importances were calculated using Gini Importance(Louppe et al., 2013). The top feature is the number of overdraft fees a customer has had in the past. This largely makes intuitive sense. Customers that are living paycheck-to-paycheck and have become accustomed to overdrafting are likely to continue overdrafting. Though, having a history of overdrafts is not solely predictive of overdrating an account in the next week. Secondly, the days since the last overdraft fee and if there has been an overdraft in the last week are also important. The average Mint customer overdrafts 1.8x before they realize they have overdrafted. The model can often catch customers that have had the first overdraft and alerts them before they have more. A large amount of debits indicates a highly active account where an overdraft is more likely. A low or already negative balance is also a high-risk indictator of an impending overdraft but not perfectly predictive. Certain banks will allow customers to hold a small negative balance, typically below $50 dollars before an overdraft fee is assessed. On the low risk end, if a customer has low transaction activity in their account or a large number of days since their last overdraft they are at a much lower risk of overdrafting their account.

| Bank | Model | Hyperparameters |

|---|---|---|

| Wells Fargo | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| Chase | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| Bank of America | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| Navy Federal Credit Union | GBDT | learning rate: 0.1, max depth: 5, estimators: 100, subsample: 0.5 |

| US Bank | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| TD Bank | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| PNC Bank | GBDT | learning rate: 0.01, max depth: 10, estimators: 100, subsample: 0.5 |

| Ally Financial | ANN | layers: 3, nodes: 128, dropout rate: 0.25, activation function: sigmoid, epochs 30, learning rate: 0.0001 |

| Citibank Banking | GBDT | learning rate: 0.01, max depth: 5, estimators: 100, subsample: 0.5 |

5. Email Variants

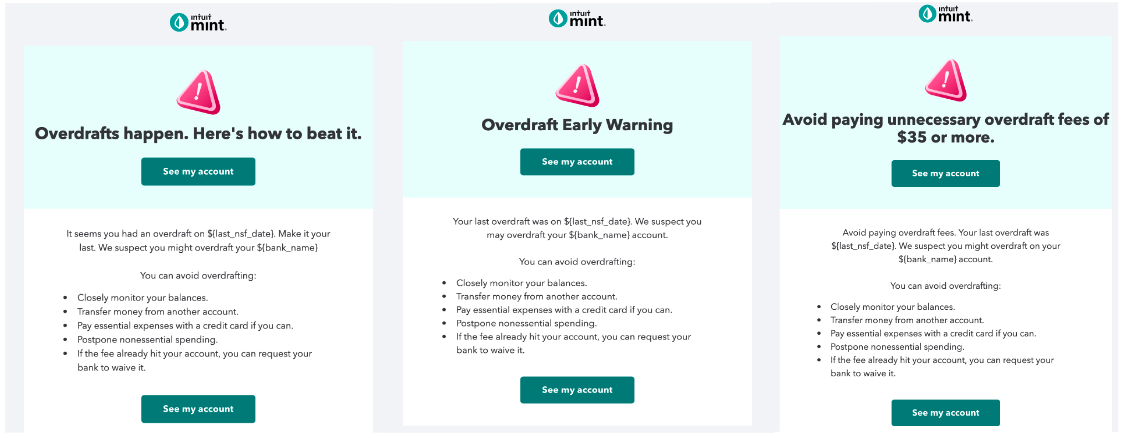

Different variants of an email message were composed using nudge theory(Thaler and Sunstein, 2021; Cai, 2020) and tested in order to find the most effective messaging, as measured by email open rates. Three variations of overdraft warnings were composed: “Overdrafts Happen. Here’s how to beat it” (Empowering Message), “Avoid paying overdraft fees of $35 or more” (Loss Aversion Message), and “Overdraft Early Warning” (Baseline Message). As Figure 6 shows, the subject line contains the nudge message. The body of the email contains the bank name of the account we believe the customer is at risk of overdrawing and the last time a customer received an overdraft fee. The bank name is provided so the customer knows what account we believe they will overdraw; for legal reasons that is the extent we can identify an account via email. Receiving a notification with the last overdraft fee date helps customers understand, intuitively, why they are receiving the message. There is also a list of actions we suggest to customers to avoid an overdraft.

6. Model Test Design and Results

The Overdraft Early Warning System was deployed and tested in an RCT (randomized control trial) to test the system’s ability to reduce overdraft fees. The test was run for 12 weeks from November 2020–January 2021. The model was retrained every Friday and subsequently used to generate a list of at-risk customers who were sent email notifications. For the test, customers were divided into four groups: control (at-risk but receive no notification) and a group for each of the three email variants, Baseline Message group, Loss Aversion Message group, and Empowering group. A customer is randomly assigned to one of the groups the first time they receive a notification and stay in that group for the duration of the test when receiving future notifications. Overall 200k notifications were sent and there were 60k participants in the test (48K in an email variant and 12k in control). As previously mentioned there is a lag in the velocity the Mint app receives the latest transaction data. In offline historical testing we measured a precision of 40%-45% for each bank’s model (Table 2) where there is no data lag. We would therefore expect on average 45% of customers to overdraft each week during model deployment. In the control group, the percentage of customers that overdrafted each week was approximately 27%. We attribute this performance difference to the lag in transaction data we receive at the time of prediction. Notably, users in the treatment group who had never opened an email had similar overdraft rates as the control group. In these cases, emails from the Mint app may be summarily ignored or not reach the recipient (e.g., sent to the spam filter). The overall email open rate across all three variants was 24%. Of the users who opened an email, there was a 3.71% (trending) reduction in customers overdrafting compared to the control group indicating the customer took some action or was mindful of overdrawing their account over the next week. Each email also contained a link to a user’s checking account on the Mint app. Of those users who clicked the link to see their balance, there is a 12.86% reduction in customers overdrafting compared to the control group (statistically significant), indicating these users monitored their balances and likely took action to prevent overdrafts over the next week.

An important goal of the system is to promote behavior change among customers that led to reducing overdrafts. Users were tracked for three months from when they received their first email. Many certified financial planners suggest that it takes approximately three months for a new financial habit to develop. Overall, there was an estimated savings of $3 million dollars for customers in overdraft fees in the treatment group compared to control (statistically significant result). There was also a $5 difference in the average overdrafts fees per customer in the treatment group compared to the control group.

The purpose of creating and testing email variants is to find the most effective messaging. The results of the test support that customers who open the email are likely to have a reduction in overdrafts. A message that resonates and prompts the customer to action is therefore an important part of the system. The clear winner with a 30% open rate is the Baseline Message, ”Overdraft Early Warning”, compared to Empowering (21%), ”Overdrafts Happen Here’s how to beat it”, and Loss Aversion (22%), ”Avoid paying overdraft fees of $35 or more.” The authors speculate that the simple message, “Overdraft Early Warning”, has a higher open rate because the message communicates that an overdraft is imminent and requires immediate action as opposed to the other variants that sound more like they are providing generic financial advice.

Another goal of the test was understanding the customer’s ability to respond to an overdraft notification. The model predicted a customer’s risk but cannot predict if a customer has the means to prevent an overdraft when they are notified. Typically, customers in the low-mid range of risk opened notifications more often compared to customers at high risk. As part of the test analysis customers were divided into three groups: high ability to respond, positive balances in accounts and few overdrafts; medium ability to respond, positive balances and many overdrafts; low ability to respond, negative balances in accounts and many overdraft. The high and medium ability to respond groups generally always had a smaller percentage of customers that overdrafted than the low ability to respond group as well as higher email open rates. We find that the low ability to respond group is not unaware they are overdrafting, rather they do not have the means to prevent overdrawing their accounts making this intervention ineffective for them. In the future, we may be able to provide a stronger intervention (e.g., a low-interest short-term personal loan to maintain cash flow). This raises the question of whether chronic overdrafters should receive email notifications even if we believe they cannot prevent the overdraft or will not interact with the notification. Given that the model exists in a social and ethical context, we believe that all customers should be warned of an overdraft regardless of their ability to prevent overdrafts. If certain customers receive email interventions and others do not, we risk creating or exacerbating a disparity(Foster, 2021; Saleiro et al., 2018) by not providing everyone at-risk the chance to prevent the overdraft.

Customer interviews during the test provided valuable insight into how customers react to the warning. One major concern was that false positives messages would lead to customers losing faith in the system and ignore future messages as a result. In those interviews, we were able to learn that customers were not inured by false positives messages, email notifications that incorrectly identified customers that are about to overdraft, as long as they could intuitively understand why they received the notification based on their transaction and balance data. Customers that received messages and could not avoid an overdraft were also still engaged and believed the notifications could be helpful when they had the ability to respond in the future. Secondly, we found that no customer actually handled an overdraft the moment they received a notice and sometimes forgot until an overdraft fee was charged. We plan on adding an immediate push notification and later email reminder to be more effective in the future. A common request across interviews was for the Mint app to handle an impending overdraft automatically. In the future this could be done by automated or assisted movement of funds or requesting a waiver on the customer’s behalf.

7. Conclusions

In this paper we have presented a machine learning approach to develop a risk model for predicting which Mint customers will overdraft their checking account within the next week and provide an early warning email notification. Each bank’s model provides lift over the prior and outperforms a business rule model while also balancing stability and performance. Several message variations were tested using nudge theory to find the most effective messaging. Overall, the system has saved customers $3 million in overdraft fees during a test of the model. The model is deployed and protecting customers from overdrafting their accounts.

At a higher level, the methodology and approach can be used to provide different types of financial advice. We have shown in this paper we can help customers avoid unnecessary overdraft fees. Although most ML-based work has focused on investing and financial markets, we strongly believe that ML-based tools can benefit personal finances. Specifically, we believe that we can provide ML-driven advice to help customers with other important aspects of personal finance such as increasing credit scores, building emergency savings, paying down debt, and allocating capital for investments. In the future, we hope to report on more ML-guided tools in personal finance.

Acknowledgements.

This work took a village to accomplish. I (AK) should like to acknowledge the following individuals, specifically: Ido Mintz, Itay Granik and Daniel Ben David for the original work around overdraft messaging; Victor Escoto for creating graphics for this paper; Joanne Locascio for her work developing nudge messages; Kaitlin Inghilterra for coaching me on how to conduct a customer interview; Ken Yocum, and Kit Rodolfa for careful review of this manuscript.References

- (1)

- noa (2021) 2021. Ally Bank Overdraft Policy. https://www.ally.com/overdraft/

- noa (2022) 2022. Citibank Overdraft Policy. https://online.citi.com/US/JRS/portal/template.do?ID=Citi-Overdraft-Fees-Change

- Alan et al. (2018) Sule Alan, Mehmet Cemalcilar, Dean Karlan, and Jonathan Zinman. 2018. Unshrouding: Evidence from Bank Overdrafts in Turkey: Unshrouding: Evidence from Bank Overdrafts in Turkey. The Journal of Finance 73, 2 (April 2018), 481–522. https://doi.org/10.1111/jofi.12593

- Arnold (2022) Chris Arnold. 2022. People hate overdraft fees. Banks are ditching or reducing them. NPR (Jan. 2022). https://www.npr.org/2022/01/11/1071860136/people-hate-overdraft-fees-capital-one-is-ditching-them-and-other-banks-may-foll#:~:text=All%20U.S.%20banks%20together%20make,of%2010%20overdrafts%20a%20year.

- Ben-David et al. (2019) Daniel Ben-David, Orly Sade, and Ido Mintz. 2019. Using AI and Behavioral Finance to Cope with Limited Attention and Reduce Overdraft Fees. SSRN Electronic Journal (2019). https://doi.org/10.2139/ssrn.3422198

- Booker (2022) Cory Booker. 2022. Stop Overdraft Profiteering Act of 2021. https://www.congress.gov/117/bills/s2677/BILLS-117s2677is.pdf

- Caflisch et al. (2018) Andrea Caflisch, Michael D. Grubb, Darragh Kelly, Jeroen Nieboer, and Matthew Osborne. 2018. Sending Out an SMS: The Impact of Automatically Enrolling Consumers Into Overdraft Alerts. SSRN Electronic Journal (2018). https://doi.org/10.2139/ssrn.3538527

- Cai (2020) Cynthia Weiyi Cai. 2020. Nudging the financial market? A review of the nudge theory. Accounting & Finance 60, 4 (Dec. 2020), 3341–3365. https://doi.org/10.1111/acfi.12471

- CFPB (2013) CFPB. 2013. CFPB Study of Overdraft Programs. https://files.consumerfinance.gov/f/201306_cfpb_whitepaper_overdraft-practices.pdf

- Chang (2020) Ellenn Chang. 2020. These Banks Are Waiving Overdraft Fees Because of the Coronavirus. U.S. News (March 2020). https://money.usnews.com/banking/articles/these-banks-are-waiving-overdraft-fees-because-of-the-coronavirus

- Flitter (2020) . Emily Flitter. 2020. Their Finances Ravaged, Customers Fear Banks Will Without Stimulus Checks. The New York Times (Dec. 2020). https://www.nytimes.com/2020/12/31/business/stimulus-checks-overdraft.html

- Foster (2021) Ian Foster (Ed.). 2021. Big data and social science: data science methods and tools for research and practice (second edition ed.). CRC Press, Boca Raton, FL.

- Friedman (2002) Jerome H. Friedman. 2002. Stochastic gradient boosting. Computational Statistics & Data Analysis 38, 4 (Feb. 2002), 367–378. https://doi.org/10.1016/S0167-9473(01)00065-2

- Jevtic et al. (2022) Danijel Jevtic, Romain Deleze, and Joerg Osterrieder. 2022. AI for trading strategies. http://arxiv.org/abs/2208.07168 arXiv:2208.07168 [q-fin].

- Kumar et al. (2022) Satyam Kumar, Mendhikar Vishal, and Vadlamani Ravi. 2022. Explainable Reinforcement Learning on Financial Stock Trading using SHAP. http://arxiv.org/abs/2208.08790 arXiv:2208.08790 [cs].

- Louppe et al. (2013) Gilles Louppe, Louis Wehenkel, Antonio Sutera, and Pierre Geurts. 2013. Understanding Variable Importances in Forests of Randomized Trees. In Proceedings of the 26th International Conference on Neural Information Processing Systems (Lake Tahoe, Nevada) (NIPS’13). Curran Associates Inc., USA, 431–439. http://dl.acm.org/citation.cfm?id=2999611.2999660

- Melzer and Morgan (2015) Brian T. Melzer and Donald P. Morgan. 2015. Competition in a consumer loan market: Payday loans and overdraft credit. Journal of Financial Intermediation 24, 1 (Jan. 2015), 25–44. https://doi.org/10.1016/j.jfi.2014.07.001

- Rudin and Carlson (2019) Cynthia Rudin and David Carlson. 2019. The Secrets of Machine Learning: Ten Things You Wish You Had Known Earlier to be More Effective at Data Analysis. (2019). https://doi.org/10.48550/ARXIV.1906.01998 Publisher: arXiv Version Number: 1.

- Saleiro et al. (2018) Pedro Saleiro, Benedict Kuester, Loren Hinkson, Jesse London, Abby Stevens, Ari Anisfeld, Kit T. Rodolfa, and Rayid Ghani. 2018. Aequitas: A Bias and Fairness Audit Toolkit. (2018). https://doi.org/10.48550/ARXIV.1811.05577 Publisher: arXiv Version Number: 2.

- Stąpor (2018) Katarzyna Stąpor. 2018. Evaluating and Comparing Classifiers: Review, Some Recommendations and Limitations. In Proceedings of the 10th International Conference on Computer Recognition Systems CORES 2017, Marek Kurzynski, Michal Wozniak, and Robert Burduk (Eds.). Vol. 578. Springer International Publishing, Cham, 12–21. https://doi.org/10.1007/978-3-319-59162-9_2 Series Title: Advances in Intelligent Systems and Computing.

- Tadapaneni (2019) Narendra Rao Tadapaneni. 2019. Artificial Intelligence in Finance and Investments. International Journal of Innovative Research in Science, Engineering and Technology 9, 5 (2019).

- Thaler and Sunstein (2021) Richard H. Thaler and Cass R. Sunstein. 2021. Nudge: the final edition (updated edition ed.). Penguin Books, an imprint of Penguin Random House LLC, New York.

- Valenti (2022) Joe Valenti. 2022. Overdraft fees can price people out of banking. Consumer Financial Protection Bureau (March 2022). https://www.consumerfinance.gov/about-us/blog/overdraft-fees-can-price-people-out-of-banking/

- Varmedja et al. (2019) Dejan Varmedja, Mirjana Karanovic, Srdjan Sladojevic, Marko Arsenovic, and Andras Anderla. 2019. Credit Card Fraud Detection - Machine Learning methods. In 2019 18th International Symposium INFOTEH-JAHORINA (INFOTEH). IEEE, East Sarajevo, Bosnia and Herzegovina, 1–5. https://doi.org/10.1109/INFOTEH.2019.8717766

- Zhao et al. (2022) Yu Zhao, Shaopeng Wei, Yu Guo, Qing Yang, Xingyan Chen, Qing Li, Fuzhen Zhuang, Ji Liu, and Gang Kou. 2022. Combining Intra-Risk and Contagion Risk for Enterprise Bankruptcy Prediction Using Graph Neural Networks. http://arxiv.org/abs/2202.03874 arXiv:2202.03874 [cs, q-fin].