A Queueing Model of Dynamic Pricing and Dispatch Control for Ride-Hailing Systems Incorporating Travel Times

Abstract

A system manager makes dynamic pricing and dispatch control decisions in a queueing network model motivated by ride hailing applications. A novel feature of the model is that it incorporates travel times. Unfortunately, this renders the exact analysis of the problem intractable. Therefore, we study this problem in the heavy traffic regime. Under the assumptions of complete resource pooling and common travel distribution, we solve the problem in closed form by analyzing the corresponding Bellman equation. Using this solution, we propose a policy for the queueing system and illustrate its effectiveness in a simulation study.

Keywords—ride-hailing, dynamic pricing, matching, diffusion approximations, heavy traffic analysis, stochastic control

Introduction

This paper studies a dynamic control problem for a queueing model motivated by taxi and ride hailing systems. In those systems, customers and drivers can be matched centrally by a platform using web or mobile applications. In addition, the platform can adjust the prices dynamically over time. We consider a city partitioned into a set of geographical regions. Each such region should be thought of as a pick-up or drop-off location. Simultaneously, cars reside in these regions waiting to pick up customers. We use a queueing model to study this problem, following a growing number of papers in the operations research literature. However, much of the relevant literature assumes away the travel times between the pick-up and drop-off locations, see for example Ata et al. (2020) and the references therein. A key novelty of our model is that it incorporates travel times, but this leads to a significantly more challenging analysis.

We assume that the platform, also referred to as the system manager hereafter, has two levers: pricing and dispatch controls. She seeks an effective policy that makes both dynamic pricing and dynamic dispatch control decisions in order to maximize the long-run average profit. We allow the prices to depend on time and the customer location. Dynamically adjusting prices elicits two competing effects. On the one hand, increasing prices increase the per-ride revenue for the platform. On the other hand, customers are price sensitive, so higher prices result in lower customer demand. Dispatching refers to the process of matching a car with a customer requesting a ride and constitutes an important operational decision for the platform.

We model a ride-hailing or taxi system as a closed queueing network with a fixed number of jobs, denoted by . There are buffers, single-server nodes, and an infinite-server node in the SPN. The terms “server” and “resource” will be used interchangeably to refer to a single-server node. Similarly, the terms “buffer” and “class” will be used interchangeably. As such, jobs in buffer will be referred to as class jobs, for . In addition to choosing prices dynamically, the system manager can engage in possible (dispatch) activities, where each activity corresponds to a server serving jobs in a buffer. Following service at a single-server node, jobs are routed to the infinite-server node. Jobs then continue their service at the infinite-server node, after which they are probabilistically routed back to the buffers. The infinite-server node models the travel times. This process continues indefinitely.

In the context of our motivating application, jobs correspond to cars that circulate in the system perpetually. The buffers correspond to city regions where cars wait to get matched with a customer. In addition, the service rates at a single-server node can be thought of as the customer arrival rate to the corresponding region, which depends on the price. As a result, customer demand dynamically changes over time as the platform varies the prices of rides. An activity corresponds to dispatching a car from one region to serving an arriving customer possibly in another region. Thus, a service completion at a single-server node corresponds to a car getting matched with a customer. After getting matched with a customer, the car must travel to pick up the customer and bring him to his destination. We assume that all customer requests that are not met immediately are lost. In the queueing model, this corresponds to jobs getting routed to and served at the infinite-server node. That is, the infinite-server node models the travel time of a car from its initial dispatch time to the drop off time of the customer. Upon completing service at the infinite server node, the job is routed to the buffer that is associated with the customer’s destination. This is modeled through a probabilistic routing structure as is usually done in the queueing literature. Although the SPN we study is motivated by the ride-hailing and taxi systems, in what follows we use the queueing terminology that is standard in the literature. However, we will occasionally make reference to our motivating applications when intuition or interpretation are needed.

As mentioned above, incorporating travel times makes the problem significantly more challenging. To ease the analysis, we assume there is a single travel node. This assumption has two implications: First, the travel times between any two regions have the same distribution. Second, upon completing service at the infinite-server node all job classes share the same probabilistic routing structure. Admittedly, this is a restrictive assumption, but it simplifies the analysis and allows us to incorporate the travel times into the model. We view our model as an important first step in the analysis of ride-sharing network models that incorporate travel times.

However, even under the single travel node assumption, the problem is not amenable to exact analysis. As such, we consider a diffusion approximation to it in the heavy traffic asymptotic regime. In that regime, under the so called complete resource pooling condition, see Harrison and López (1999), we solve the problem analytically and derive a closed-form solution for the optimal dynamic prices.

Notwithstanding these restrictive assumptions, the paper makes two contributions. First, it incorporates the travel times in the model and solves the resulting dynamic pricing and dispatch control problem analytically in the heavy traffic regime. Second, it makes a methodological contribution by solving a drift-rate control problem on an unbounded domain, which could be of interest in its own right.

The rest of the paper is structured as follows. Section 2 reviews the literature. Section 3 presents the control problem for the ride-hailing platform, and the associated Brownian control problem is derived formally in Section 4. The equivalent workload formulation is formulated in Section 5 and it is solved in Sections 6 and 7 by studying a related Bellman equation. Section 8 interprets the solution of the equivalent workload formulation in the context of the original control problem and proposes a pricing and dispatch policy. Section 9 conducts a simulation study to illustrate the effectiveness of the proposed policy. Section 10 concludes the paper. There are two appendices: Appendix A provides a formal derivation of the Brownian control problem, and additional proofs are given in Appendix B.

Literature Review

Our paper is related to two streams of literature: the modeling and analysis of ride-hailing and taxi systems and the dynamic control of queueing networks.

In recent years several authors have modeled ride-hailing and taxi systems using queueing networks. A majority of this literature has focused on how pricing, dispatch (matching), and relocation decisions can improve system performance. From a modeling perspective, Ata et al. (2020) and Braverman et al. (2019) are most closely related to ours. Ata et al. (2020) model a ride-hailing system closed stochastic processing network with dispatch and relocation control. Under heavy traffic conditions, they approximate the original control problem by a Brownian control problem (BCP). After reducing the BCP to an equivalent workload formulation, they propose an algorithm to solve it numerically. However, their model does not include travel times, whereas ours does. Incorporating travel times leads to a significantly more challenging problem in the heavy traffic limit under the diffusion scaling. On the other hand, Braverman et al. (2019) model a ride-hailing system as a closed queueing networks with travel times and relocation control. By solving a suitable linear program, they propose a static routing policy and prove that it is asymptotically optimal in a large market asymptotic regime under fluid scaling. Hosseini et al. (2021) extends the analysis of Braverman et al. (2019) by designing a dynamic relocation that outperforms the asymptotically optimal static policy in realistic problem instances. In a related study, Zhang and Pavone (2016) uses a combination of single-server and infinite-server queueing model to study the control of autonomous vehicles. The authors derive an open loop policy by solving a linear program. Building on this solution, they also propose an effective dynamic rebalancing policy.

Several other papers are at the intersection of ride-hailing and queueing, but differ more in their modeling choices and analysis. Banerjee et al. (2015) study pricing on a single-region model with a single travel time node and show that an optimal static pricing policy performs well. Banerjee et al. (2021) develop an approximation framework to study vehicle sharing systems under pricing, matching, and repositioning policies for several objective functions and under various system constraints. In particular, they develop algorithms and show that the approximation ratio of the resulting policy improves as the number of cars in each region grows. Banerjee et al. (2019) study matching for a general closed queueing network that can be used to model ride-hailing systems. They propose a family of state-dependent matching policies that do not use any demand arrival rate information. Under a complete resource pooling assumption, they show that the proportion of dropped demand under any such policy decays exponentially as the number of supply units in the network grows. Afèche et al. (2018) develop a game-theoretic fluid model to study admission control and repositioning in a ride-hailing system with strategic drivers. Their analysis provides insights into spatial demand imbalances and how demand admission control can impact the strategic behavior of drivers in the network. Afèche et al. (2018) studies the optimal dynamic pricing and dispatch control under demand shocks. Özkan and Ward (2020) model a ride-hailing system as an open queueing network model with impatient customers. They propose a matching policy and prove asymptotically optimality in the fluid scale in a large market regime. Özkan (2020) studies a fluid model with strategic drivers that incorporates both pricing and matching decisions, highlighting the importance of looking at multiple controls simultaneously. Besbes et al. (2021b) study the effect of pick up and travel times on capacity planning for a ride-hailing system by modeling it as a spatial multi-server queue. Chen et al. (2020) proposes static and dynamic policies that are asymptotically optimal. Varma et al. (2022) studies an open network model and proposes an asymptotically optimal policy. Examples of other papers that use spatial models for pricing include Yang et at. (2018), Jacob, J. and Roet-Green, R (2021), and Hu et al. (2022).

Several other researchers focused on different aspects of the ride-hailing and taxi systems without using queueing theoretic models. These include Wang et al. (2017), Ata et al. (2019), Bertsimas et al. (2019), Besbes et al. (2021a), Bimpikis et al. (2019), Cachon et al. (2017), Castillo et al. (2021), Chen and Sheldon (2016), Garg and Nazerzadeh (2019), Gokpinar and Selcuk (2019), Guda and Subramanian (2019), He et al. (2020), Hu et al. (2022), Hu and Zhou (2021), Korolko et al. (2020), and Lu et al. (2018).

This paper also contributes to the broader literature on dynamic control of queueing systems. Two prominent approaches in that literature are: (i) Markov decision process (MDP) formulations, and (ii) heavy traffic approximations. Intuitively, the workload problem studied in Sections 5–7 relates to the service rate and admission control problems studied using MDP formulations, see for example Stidham and Weber (1989) and references therein. The most closely related papers are George and Harrison (2001) and Ata (2005). These papers study the service rate control problems for an queue and provide closed-form solutions; also see Ata and Shneorson (2006), Ata and Zachariadis (2007), Adusumilli and Hasenbein (2010), and Kumar et al. (2013).

The second approach is pioneered by Harrison (1988), also see Harrison (2000, 2003). In particular, a number of papers studied drift rate control problems for one-dimensional diffusions arising under heavy traffic approximations, see Ata et al. (2005), Ata (2006), Ghosh and Weerasinghe (2007, 2010), Rubino and Ata (2009), Kim and Ward (2013), and Ata and Tongarlak (2013). More recently, Ata and Barjesteh (2020) and Ata et al. (2021) studied drift-rate control problems arising in different contexts such as volunteer capacity management and make-to-stock manufacturing. The analysis of the drift-rate control problem solved in this paper differs significantly from the analysis in those papers because it involves a quadratic cost of drift rate, unbounded set of feasible drift rates, and an unbounded state space. The combination of these features lead to a more challenging analysis. Our paper also makes a modeling contribution by formulating the dynamic dispatch and pricing control problem that incorporates travel times. Furthermore, it proposes an analytically tractable approximation in the heavy traffic limit and solves that in closed form.

Model

Motivated by the taxi and ride-hailing application described in the introduction, we consider a closed queueing network with jobs, buffers, single-server nodes, and one infinite-server node. Figure 1 displays an illustrative network with and , also see Section 9 for the motivation behind this example.

As mentioned earlier, in addition to dynamic pricing decisions, the system manager also makes dispatch decisions dynamically. There are dispatch activities she can choose from. Each dispatch activity involves a unique buffer and a unique server–we use the terms single-server node and server interchangeably. Let and denote the server and the buffer, respectively, associated with activity for . In other words, activity is undertaken by server and it servers jobs in buffer . We describe the association between activities and resources by the capacity consumption matrix and the association between activities and buffers by the constituency matrix . That is, is the matrix given by

| (3) |

and is the matrix given by

| (6) |

Let denote the set of activities server undertakes. Similarly, let denote the set of activities that serve buffer . We have that

| (7) | ||||

| (8) |

For each activity , we associate a unit rate Poisson process . We also associate a unit rate Poisson process with the infinite-server node. The processes are mutually independent. The service rate at the infinite-server node is denoted by . We denote the service rate for activity at time by for and . The system manager chooses prices dynamically over time, where denotes the price charged to customers who seek rides from region at time . As the reader will see below, these prices ultimately determine activity service rates for and . We assume for , where . The price sensitivity of demand is captured by a nonnegative demand function , where . Namely, the demand rate vector at time , denoted by , is given by111The customer demand rate in region , , depends only on the price .

| (9) |

We make the following monotonicity assumption to simplify the analysis:

Assumption 1.

The demand rate function is strictly decreasing in price, i.e., is strictly decreasing in for .

From this monotonicity assumption, it follows that has an inverse function, denoted by . Moreover, the pricing decisions can be replaced with choosing the demand rate vector dynamically over time. This is convenient for our analysis. In order to proceed with that approach, we first define the set of admissible demand rate vectors as follows:

| (10) |

where for . Denoting for , it is easy to see that is the inverse function of . Viewing the demand rates as the platform’s pricing control, we define the revenue rate function as follows:

| (11) |

We also make the following regularity assumptions for the revenue rate function:

Assumption 2.

The revenue rate function is: (a) three-times continuously differentiable and strictly concave on , and (b) has a maximizer in the interior of .

Upon completing service at a single-server node, each job goes next to the infinite-server node. Once its service there is complete, the job next joins buffer with probability for where . The routing probability vector does not depend on the single-server node the job departed from prior to joining the infinite-server node. In other words, customers’ destination distribution is identical across different origins. This is a restrictive assumption, but it simplifies the analysis significantly and enables us to incorporate travel times into the model. As discussed in the Introduction, we view this as an important first step in the analysis of ride-sharing network models that incorporate travel times. In order to model this probabilistic routing structure mathematically, we let denote a sequence of -dimensional i.i.d. random vectors with for , where is an -dimensional vector with one in the th component and zeros elsewhere. Then letting

| (12) |

we note that the th component of , denoted by , represents the total number of jobs routed to buffer among the first jobs that have finished service at the infinite-server node.

As discussed earlier, there are two types of control decisions that the system manager must make. First, she must choose an -dimensional demand rate process . This is equivalent to making dynamic pricing decisions. Recall that the customer arrival process at single-server node corresponds to its service process. Because these customers can be transported by cars in regions corresponding to activities , we let

| (13) |

This defines the -dimensional service rate process , where . Second, she must decide on how servers allocate their time to various (dispatch) activities. This decision takes the form of cumulative allocation processes for . In particular, represents the cumulative amount of time server devotes to activity (serving class jobs) during .

Next, we introduce the system dynamics equations that govern the movement of jobs in the network. To that end, we let and denote the number of jobs in the infinite-server node and in buffer at time , respectively, for . We also let and be the total number of jobs that have arrived to the infinite-server node and to buffer by time , respectively, for . Then we have that

| (14) | |||||

| (15) |

Moreover, letting and denote the total number of jobs that have left the infinite-server node and buffer by time , respectively, for , we have that

| (16) | |||||

| (17) |

We refer to the -dimensional process as the queue length process, whose dynamics is given next:

| (18) |

where is the vector of initial queue lengths such that . Letting denote the cumulative amount of time that server is idle during the interval for , we have that

| (19) |

or in matrix notation, for . Note that Equations (14)–(18) imply that

expressing the fact that the total number of jobs in the system remains fixed in a closed network.

In order to state the platform’s objective and its control problem formally, we introduce two vectors of cost parameters and . In the context of the ride-hailing system, the platform incurs a fuel cost at a rate of per traveling car. Moreover, for , there is a holding cost at a rate of for each car waiting for a ride in region , reflecting the fact that no driver likes sitting idle. We assume that for all . Finally, for , there is an idleness cost at the rate of per unit of time server is idle. This represents the lost revenue from picking up customers arriving to region and goodwill loss.222One can assume naturally, where is defined in Equation (27) below. A control policy is denoted by and must satisfy the following conditions:

| , are nonanticipating with respect to , | (20) | ||

| , are nondecreasing and continuous with , | (21) | ||

| for all , | (22) | ||

| for all , . | (23) |

Equation (20) expresses the fact that the policy can only depend on observable quantities, Equation (21) is natural given the interpretations of the processes and . Equation (22) requires that come from the set of achievable demand rates. Equation (23) expresses the fact that queue lengths are nonnegative. The arriving customer demand is allocated to cars waiting in various buffers through the dispatch activities , see for example Equations (14) and (17). Given a control policy , we define the cumulative profit collected up to time as

| (24) |

The platform’s control problem is to choose a policy so as to

| maximize | (25) | |||

| subject to | (26) |

Because control problem (25)–(26) in its original form is not amenable to exact analysis, the next section considers a related control problem in an asymptotic regime where the number of cars gets large and derives the approximating Brownian control problem. The Brownian control problem is an approximation to the original problem, yet it is far more tractable.

Brownian Control Problem

Following an approach that is similar to the one taken in Harrison (1988), this section develops a Brownian approximation to the control problem presented in Section 3. Many authors have proved heavy traffic limit theorems to rigorously justify such Brownian approximations—see for example Harrison (1998), Williams (1998), Kumar (2000), Bramson and Dai (2001), Stolyar (2004), Bell and Williams (2001, 2005), Ata and Kumar (2005), Ata and Olsen (2009, 2013) and references therein. We do not attempt to prove a rigorous convergence theorem in this paper, but refer the reader to Harrison (1988, 2000, 2003) for elaborate and intuitive justifications of the approximation procedure we follow.

The approximation procedure starts by solving the following static pricing problem (existence of the optimal solution is guaranteed by Assumption 2), which helps us articulate the heavy traffic assumption that underlies the mathematical development to follow. We set

| (27) |

Recall from Assumption 2 that we assume is in the interior of , i.e., . The vector represents the average demand rates that would result in the largest revenue rate ignoring variability in the system. Note that the corresponding nominal service rates for the various activities are given by333In particular, for all , . This is true because there exists only one such that for each . That is, an activity only uses one server. In matrix notation, , where is the transpose of .

| (28) |

Using these nominal service rates, we define an input-output matrix as follows:

| (29) |

Following Harrison (1988, 2000), we interpret as the long-run average rate of class material consumed per unit of activity under the nominal service rates for . We also define the -dimensional input vector as

| (30) |

We interpret as the long-run average rate of input into buffer from the infinite-server node. As a preliminary to stating the heavy traffic assumption, we introduce the notion of local activities. In the context of the motivating application, it corresponds to a customer in a region being picked up by a car in the same region. Using the terminology that is standard in queueing theory, it corresponds to a server processing its own buffer. Without loss of generality, we assume that the first activities are local. That is,

This is equivalent to assuming that the first columns of matrices and constitute the dimensional identity matrix. The following is the heavy traffic assumption:

Assumption 3.

There exists a unique such that

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) |

The vector is referred to as the nominal processing plan and the component can be interpreted as the long-run average rate at which activity is undertaken. Equation (34) says that all nominal activity levels must be non-negative. Equation (33) means that under the nominal processing plan, servers are fully utilized. Equation (32) is a flow balance condition which says that the rate of jobs leaving the buffers equals the rate of jobs entering the buffers under the nominal processing plan. Note that by Equations (29)–(32) we have for each , which then implies that by summing over . We interpret as the rate of jobs entering the infinite-server node under the nominal processing plan, and Assumption 3 ensures that this equals the service rate at the infinite-server node.444Based on intuition from the classical queue, this condition implies that the steady-state fraction of jobs in the infinite-server node under the nominal processing plan is equal to one as the number of jobs in the system grows, i.e. as . Equation (31) ensures that local activities are used at maximal rates. In the context of the motivating application, this means customer demand is met by cars in the same region as much as possible.

Following Harrison (2000), we call activity basic if , whereas it is called nonbasic if . We let denote the number basic activities. After possibly relabeling, we assume without loss of generality that activities are basic and that activities are nonbasic. Recall that the first of them are the local activities. As done in Harrison (2000), we partition the matrices and as follows:

| (35) |

where and . The submatrices and correspond to the basic activities of and , respectively, while the submatrices and correspond to the nonbasic activities.

In order to derive the approximating Brownian control problem, we consider a sequence of closely related systems indexed by the total number of jobs . The formal limit of this sequence as is the approximating Brownian control problem. We attach a superscript of to quantities associated with the th system in the sequence. To be specific, we define the scaled demand rate function by

| (36) |

Then we define the set of admissible scaled demand rate vectors as the following:

| (37) |

We note from Equations (9)–(10) and (36)–(37) that , and that has the inverse function for . We define the scaled revenue rate function as follows:

| (38) |

Observing that if and only if , it can equivalently be shown that555The first equality in (39) is proved by applying (38) and noting that for . The second equality in (39) then follows by (11).

| (39) |

Therefore, in the th system, the revenue rate process is simply scaled by . We also scale the holding cost rates and the idleness cost rates as follows:

| (40) | |||||

| (41) |

Lastly, we allow the mean travel time to vary with as follows:

| (42) |

where . As observed in Kogan and Lipster (1993) and Ata et al. (2021), under our heavy traffic assumption we expect that the queue lengths at the buffers to be of order and that the number of jobs in the infinite-server node be of order . Therefore, we define the centered and scaled queue length processes as follows:

| (43) |

Observe that since for all , it follows that for all .

As argued in Harrison (1988) (see also Harrison (2000, 2003)), any policy worthy of consideration satisfies , for all and large . That is, the nominal allocation rate given in Assumption 3 should give a first-order approximation to the allocation rates of the various activities under policy . However, the system manager can choose the second-order, i.e., order , deviations from that. In order to capture such deviations from the nominal rates, we define the centered and scaled processes as follows:

| (44) |

Similarly, in the heavy traffic regime, we expect the servers to be always busy to a first-order approximation, but they may incur idleness on the second order, i.e., order . As such, we define the scaled idleness processes as follows:

| (45) |

Then, it follows from Equations (19) and (33) that

| (46) |

In addition, we define the centered and scaled demand and service rate processes, respectively, as follows:

| (47) | ||||||

| (48) |

Note that by Equation (13) we have for each . Finally, we define the centered cumulative profit function. To do so, we first introduce the auxiliary function that will serve as the centering function. To be specific, we define

| (49) |

where the second equality follows from the definition of , see Equation (40). Note that does not depend on the system manager’s control. Therefore, instead of maximizing the average profit, she can focus on minimizing the average cost, where the cumulative cost up to time , denoted by , is defined as follows:

| (50) |

We then proceed with replacing the processes , , , , , and with their formal limits , , , , , and , respectively, as . In particular, the cost process in the Brownian approximation is given by

| (51) |

where for . The steps outlining the formal derivation of the Brownian Control Problem and of Equation (51) are given in Appendix A.

The Brownian control problem (BCP) is given as follows: Choose processes and that are nonanticipating with respect to so as to

| (52) | |||

| subject to | |||

| (53) | |||

| (54) | |||

| (55) | |||

| (56) | |||

| (57) | |||

| is nondecreasing with , | (58) |

where is an -dimensional Brownian motion with starting state that has drift rate vector where and covariance matrix given by

| (59) |

Although the BCP (53)–(56) is simpler than the original control problem that it approximates, it is not easy to solve because it is a multidimensional stochastic control problem. Thus, we further simplify it in Section 5 and derive an equivalent workload fomulation that is one-dimensional under the complete resource pooling condition which we solve analytically in Section 6.

Equivalent Workload Formulation

As a preliminary to the derivation of the workload problem, letting and using Equation (29), we first rewrite Equation (53) in vector form as follows:

| (60) |

where is an -dimensional vector of ones and is the diagonal matrix whose th element is .

Motivated by the development in Harrison and Van Mieghem (1997) and Harrison (2000), we define the space of reversible displacements as follows:

| (61) |

where is the vector consisting of the components of indexed by the basic activities . We let be the orthogonal complement of the space and call the workload dimension. Any matrix whose rows form a basis for is called a workload matrix. Lemma 1 provides a canonical choice of the workload matrix based on the notion of communicating buffers, which is defined next, see Ata et al. (2020). Also see Harrison and López (1999) for a related definition of communicating servers.

Definition 1.

Buffers and are said to communicate directly if there exist basic activities and such that , , and . That is, buffers and are served by a common server using basic activities. Buffers and are said to communicate if there exist buffers such that , , and buffer communicates directly with buffer for .

Buffer communication is an equivalence relation. Thus, the set of buffers can be partitioned into disjoint subsets where all buffers in the same subset communicate with each other. We call each subset a buffer pool and denote the th buffer pool by , . Associated with each buffer pool is a server pool. The th server pool is defined as follows:

| (62) |

In words, server pool consists of all servers that can serve a buffer in buffer pool using a basic activity. Note that since the buffer pools partition the buffers, it follows from Equation (62) that the server pools partition the servers. Thus, the buffer pools and the server pools are in a one-to-one correspondence. As a result, there is an equivalent notion of server communication, but we stick with the definition of buffer communication for mathematical convenience. The following lemma characterizes the workload dimension and the workload matrix, see Appendix B for its proof.

Lemma 1.

The workload dimension equals the number of buffer pools, i.e., . Furthermore, the matrix given by

| (65) |

for and constitutes a canonical workload matrix.

To facilitate the derivation of the workload state dynamics, we define the matrix as follows:

| (66) |

That is, the th row of , contains the nominal service rates for those servers in server pool and zeros for the rest of the servers. The next lemma provides a useful result that helps us derive the workload problem. It is proved in Appendix B.

Lemma 2.

We have that .

We define the -dimensional workload process as

| (67) |

whose th component represents the total number of jobs for the th server pool at time for . By Equation (67) and Lemma 2, we arrive at the following equation which describes the evolution of the workload process:

| (68) |

where , so that is a -dimensional Brownian motion with drift vector , covariance matrix , and starting state .

Next, we introduce a closely related control problem referred to as the reduced Brownian control problem (RBCP). Its state descriptor is the workload process . To be more specific, the RBCP involves choosing a policy that is nonanticipating with respect to so as to

| (69) | |||

| subject to | |||

| (70) | |||

| (71) | |||

| (72) | |||

| (73) | |||

| (74) |

The BCP (52)–(56) and the RBCP (69)–(74) are equivalent as shown by the next proposition, see Appendix B for its proof.

Proposition 1.

Every admissible policy for the BCP (52)–(56) yields an admissible policy for the RBCP (69)–(74) and these two policies have the same cost. On the other hand, for every admissible policy of the RBCP, there exists an admissible policy for the BCP whose cost is equal to that of the policy for the RBCP.

Hereafter, we make the complete resource pooling assumption that corresponds to having a single resource pool in our context, see Assumption 4 below. Harrison and López (1999) observes that the complete resource pooling assumption leads to a one-dimensional workload formulation, also see Ata and Kumar (2005). Similarly, Assumption 4 allows us to formulate a one-dimensional workload formulation that is equivalent to the RBCP formulated in Equations (69)–(74).

Assumption 4.

All buffers communicate under the nominal processing plan, i.e., .

This assumption says that servers have sufficiently overlapping capabilities under the nominal processing plan; see Harrison and López (1999) for further details. The following lemma allows us to simplify the RBCP under Assumption 4, see Appendix B for its proof.

Lemma 3.

Under Assumption 4, we have and . Moreover, we have that

| (75) |

Using Lemma 3, the RBCP can be equivalently written as follows: Choose a policy that is nonanticipating with respect to so as to

| (76) | |||

| subject to | |||

| (77) | |||

| (78) | |||

| (79) | |||

| (80) |

where is a one-dimensional Brownian motion with drift rate parameter and variance parameter and starting state .

To further simplify the RBCP, we define the cost function by

| (81) |

and the optimal (state-dependent) drift rate function by

| (82) |

Defining , the following lemma characterizes these functions—similar results are found in Çelik and Maglaras (2008) and Ata and Barjesteh (2020).

Lemma 4.

We have that and for and .

In the workload formulation, it is optimal to keep all workload in the buffer with the lowest holding cost, i.e., buffer where

| (83) |

with holding cost . Moreover, the system manager will only idle the server that is cheapest to idle, i.e., server where

| (84) |

with idling cost .

The workload formulation can now be stated as follows: Choose a policy that is nonanticipating with respect to so as to

| (85) | |||

| subject to | |||

| (86) | |||

| (87) | |||

| (88) |

The RBCP (69)–(74) and the EWF (85)–(88) are equivalent as proved by the following proposition, see Appendix B for its proof.

Proposition 2.

Every admissible policy for the EWF (85)–(88) yields an admissible policy for the RBCP (76)–(80) and these two policies have the same cost. On the other hand, for every admissible policy of the RBCP, there exists an admissible policy for the EWF whose cost is less than or equal to that of the policy for the RBCP.

In what follows, we add two additional constraints to the equivalent workload formulation. First, we require that

| (89) |

which requires that the process can increase only when . That is, the control policy must be work conserving. We include this restriction because its optimality is intuitive from the cost structure, i.e., there are both holding and idleness costs, and that the workload process is one dimensional. Second, we impose the following regularity condition:

To repeat, we further require a policy to satisfy these conditions to be admissible.

Solving the Equivalent Workload Formulation

This section solves the EWF (85)–(88). In order to minimize technical complexity, we restrict attention to stationary Markov policies. That is, the drift chosen at time will be a function of the current workload only, and so we write it as . To facilitate the analysis, we next consider the Bellman equation for the workload formulation which is the following second-order nonlinear differential equation: Find a function and a constant satisfying

| (90) |

subject to the boundary conditions

| (91) |

The optimization problem on the right hand side of Equation (90) is convex. Therefore, its solution is easily seen to be

| (92) |

The Bellman equation can then be simplified as follows: Find a function and a constant satisfying

| (93) |

subject to the boundary conditions

| (94) |

Setting , the Bellman equation can be written as follows: find a function and a constant satisfying

| (95) |

subject to the boundary conditions

| (96) |

This expresses the Bellman equation as a first-order differential equation. The following theorem provides its solution. Its proof is given at the end of Section 7.

With and given by Theorem 1, we define

The next result is immediate from Theorem 1 and provides a solution to the original Bellman equation:

Define the following candidate policy by

| (97) |

The following proposition facilitates the proof of our main result, Theorem 2; see Appendix B for its proof.

Proposition 3.

The candidate policy is admissible for the equivalent workload formulation. That is, letting denote the workload process under the candidate policy , we have

The following result establishes that the candidate policy is optimal:

Theorem 2.

Next, we state an auxiliary lemma used in the proof of Theorem 2.

Lemma 5.

Proof.

By Proposition 4.7 in Harrison (2013), to prove part (i) it suffices to show that

Because for all by Equation (91) and because for all by Equation (87), it follows that

proving part (i).

In order to prove part (ii), note that it suffices to show that

We also note that

Thus, by definition of an admissible policy, it follows that

proving part (ii). ∎

We conclude this section with a proof of Theorem 2.

Proof of Theorem 2.

By Equation (86), note that for an admissible policy ,

| (98) |

Furthermore, since is nondecreasing in , the processes is a VF function almost surely; see Section B.2 in Harrison (2013). Therefore,

| (99) | ||||

Note that the last two terms on the right hand side of Equation (99) are zero; see Chapter 4 in Harrison (2013). Then, for , Itô’s Lemma gives

| (100) |

Define the differential operator by

| (101) |

Then, combining Equations (98)–(101) gives

| (102) |

Integrating both sides of Equation (102) over gives

| (103) |

Recall that by Equation (89) the process increases only when . Thus, for satisfying we have

| (104) |

By Lemma 5 and Equations (103)–(104), it follows that

| (105) |

In particular, for the solution of the Bellman equation (90)–(91) it follows that

| (106) |

with equality holding when . Therefore, by Equations (101) and (105)–(106) we have

| (107) |

with equality holding when . Rearranging terms in Equation (107), taking expectations, and dividing by gives

| (108) |

with equality holding when . Finally, taking limits on both sides of Equation (108) and applying Lemma 5 gives

with equality holding when . Therefore, the policy is optimal for the equivalent workload formulation and its long-run average cost is . ∎

Solution to the Bellman Equation

In this section we prove Theorem 1 by considering an initial value problem that is closely related to the Bellman equation. Namely, for each fixed consider the following initial value problem, denoted by IVP(): Find a function such that

| (109) | |||

| (110) |

The following result is standard and its proof is provided in Appendix B.

For the remainder of this section, we analyze the (unique) solution to Equations (109)–(110), focusing on how the behavior of the solution varies with the parameter . Using this approach, we ultimately find a , with corresponding solution , such that the pair solves the original Bellman equation. Namely, we look for such that satisfies the second condition in Equation (94) that is increasing with .

For much of our analysis, we consider parameters that satisfy one of the two cases, given in Assumption 5. To state the assumption, let

Assumption 5.

One of the following holds:

-

(a)

Case 1: and ;

-

(b)

Case 2: and .

Remark.

Note that under Assumption 5(b), we have that .

Lemma 7.

If is a local maximizer of , then .

Proof.

Because is a local maximizer, we have that , and . Differentiating both sides of Equation (109) and using , we write

from which it follows that . ∎

Lemma 8.

Under Assumption 5, increases to its supremum.

Proof.

First, note that in either case of Assumption 5. Aiming for a contradiction, suppose does not increase to its maximum. Then we must have such that

In particular, we have the following equations:

| (111) | |||

| (112) | |||

| (113) |

On the one hand, subtracting (112) from (111) yields

| (114) |

Because , we conclude from (114) that

| (115) |

On the other hand, subtracting (112) from (113) gives

| (116) |

But, we deduce from Equation (115) and from that the left hand side of Equation (116) is negative, which is a contradiction. This completes the proof. ∎

Lemma 9.

Let . Under Assumption 5, the following condition is necessary for to be constant on :

| (117) |

Moreover, if is constant on , then for , and letting , it follows that is nondecreasing on and stays constant at value thereafter.

On the other hand, if Equation (117) does not hold, then there is no interval on which is constant, i.e., the set has Lebesgue measure zero.

Proof.

Suppose the condition in Equation (117) is violated, which implies

| (118) |

Aiming for a contraction, suppose there exist an interval such that on it. This implies on . Differentiating both sides of Equation (109) and using on gives

Thus, on . Substituting this into Equation (109) yields

which follows from (118) and contradicts that on . Therefore, if (117) does not hold, then there is no interval on which is constant.

Now, we turn to the first part of the lemma. If is constant on , then on . As argued above, these imply on . In addition, it follows from (109) and on that

proving the necessary condition (118). Building on these, because at any local maximum by Lemma 7 and is the first time reaches to its maximum by Lemma 8, we conclude that is nondecreasing on . To conclude the proof, consider an auxiliary IVP involving (109) on with the initial condition . Then setting solves it. Moreover, combining that with on constitutes a solution to the IVP (109)-(110). By Lemma 6, this is the unique solution. ∎

To facilitate the analysis below, we define the following four sets. First, consider Case 1 identified in Assumption 5 (i.e., Assumption 5(a)) and let

Similarly, in Case 2 of Assumption 5 (Assumption 5(b)), we define

Lemma 10.

Proof.

First, note from Lemma 9 that it is necessary that increases to and stay constant thereafter for it to be constant on any interval. In that case, we would have ( under Assumption 5(a) and under Assumption 5(b)). Thus, for the remainder of the proof, we assume there is no interval on which is constant.

We prove Cases (i) and (ii) simultaneously because their proofs are identical. For , let . Aiming for a contradiction, assume there does not exist such that . Then, for all , i.e., is nondecreasing on . Thus, , a contradiction. Therefore, there exists such that .

For the other direction, suppose there exists such that . Because increases to its maximum (Lemma 8), it is not constant on any interval (by the argument given in the opening paragraph of this proof) and , it achieves its maximum at some . Thus, by Lemma 7, we have that

| (119) |

Aiming for a contradiction, suppose that . Then cannot be decreasing over . Thus, there exist and such that

In particular, the following holds:

| (120) | |||

| (121) |

Subtracting (120) from (121) gives

where the last inequality follows because and by Equation (119), leading to a contradiction. Thus, . ∎

Corollary 2.

Proof.

Consider Case (i). For , if for some , then by Lemma 10. Otherwise, for all , in which case by definition. Proof of (ii) follows similarly. ∎

Corollary 3.

Proof.

For , by definition of , such that is nondecreasing on and it is decreasing on . First, note that if , then is decreasing everywhere and and the result follows. Thus, we assume . Note that achieves its maximum at . Also, we conclude from Lemma 7 that . Aiming for a contradiction, suppose . Note that because is the maximizer. From these, by differentiating both sides of Equation (109), we conclude that . Then we can argue as in the proof of Lemma 9 that for , implying , a contradiction. Thus, , completing the proof. ∎

Lemma 11.

Under Case of Assumption 5 (), we have that if , then .

Proof.

It follows from Corollary 3 that has a maximizer such that

| (122) |

Also define

| (123) |

To prove , we argue by contradiction. To that end, suppose there exists a such that for . Then we have that

| (124) |

Recalling IVP(), we bound using (122)–(124) as follows:

| (125) |

Integrating both sides of (125) over and using the initial condition gives

| (126) |

Since , the right hand side of (126) tends to as , implying that as , a contradiction. ∎

Lemma 12.

Under Case of Assumption 5 (), the following are equivalent:

-

(i)

,

-

(ii)

such that ,

-

(iii)

such that ,

-

(iv)

.

Proof.

Lemma 13.

Under Assumption 5, we have that if and only if there exists an such that .

Proof.

First, if , then clearly, there exists an such that . To prove the other direction, suppose there exists such that , and define

Because , by the intermediate value theorem, . Next, we argue that for all . If not, then there exists an such that . Then let

Note that by continuity of . Furthermore, note that since and

| (127) |

where the last inequality holds because

-

(i)

by definition of ,

-

(ii)

and increases to its maximum,

-

(iii)

we cannot have by Lemma 9 because .

Thus, (127) follows. Consequently, we have that

| (128) |

By continuity, achieves a local maximum at some and , but this contradicts Lemma 7. Therefore, we conclude that

| (129) |

In particular, . Rather, and is nondecreasing by Corollary (2). So, we have that

| (130) |

To conclude the proof, we consider two cases: Case (i) , Case (ii) . When , we note from (109) that

| (131) |

Integrating both sides of (131) over gives

| (132) |

where the right hand side tends to , completing the proof when .

Lemma 14.

For , we have that for all . That is, is an increasing function of for each .

Proof.

Let . We argue by contradiction. Suppose for some , and let

Then there exists a sequence that decreases to , i.e., as , such that for all . Recall that and . Hence, in a neighborhood around zero. This and continuity of and imply that

| (135) |

Consequently, we can write

Passing to the limit as , we conclude that

| (136) |

Note, however, from IVP() that for we have

| (137) | ||||

| (138) |

Subtracting (137) from (138) and using (135) yield

which contradicts (136). Thus, we conclude that for . ∎

Lemma 15.

For , we have that is continuous in on . That is, for , given and , there exists a such that for all .

Proof.

Let and . Integrating IVP over for , we arrive at the following two equations:

| (139) | ||||

| (140) |

Subtracting (139) from (140) gives the following:

| (141) |

In order to facilitate the bound, let and note from Lemma 14 that

Hence for we have that

from which we conclude that

Thus, letting

we arrive at the following for :

Combining this with (141) and letting

yield the following inequality:

Then by Gronwall’s inequality (e.g., see page 498 of Ethier and Kurtz (2005)) we conclude that

Thus, given , we can let

so that implies that . This concludes the proof. ∎

Lemma 16.

Proof.

Lemma 17.

Proof.

Consider part (i). We first show . Aiming for a contradiction, suppose so that by Corollary 2. We consider the following two cases:

-

Case A: for all .

-

Case B: for some .

Consider Case A. Because , for all . Then, we have that for all . Substituting this into IVP() for , we consider the following two subcases of Case A: and , 0).

For , we conclude that

where the right-hand side tends to . Thus, there exists such that , contradicting .

For , we conclude that

where the right-hand side tends to . Once again, there exists such that , contradicting .

Consider Case B. In this case, we let . By continuity of and , we have that and . Substituting this into IVP() for at gives

Thus, by Lemma 12, a contradiction. Combining Cases A and B, we conclude that . Then it follow from Lemma 12 that as . Thus, there exists a such that . Then, by continuity of in (see Lemma 15), there exists a such that . By Lemma 12, we conclude . Then we conclude by Lemma 16 that .

Consider part (ii). Recall that in Case 2 of Assumption 5, and . Consider and note that . It follows from (109) that . Moreover, differentiating both sides of (109) and using , we conclude that

Thus, is decreasing and below in a neighborhood of zero. Next, we argue that for all .

Suppose not, and let . By continuity of , we have . We also have by its definition that and . Then by combining these with (109), we write

a contradiction. Thus, for all .

Next, we argue that . Suppose not (Note that we can rule out oscillatory behavior following the same technique in the proof of Lemma 8). Then, there exists such that

But using (109), we conclude that

Integrating both sides from to yields

where the right-hand side tends to as . Thus, as and there exists such that . Then, by Lemma 14, there exists such that . In particular, by Lemma 12. Then, by Lemma 16, we conclude that . ∎

Lemma 18.

Under Assumption 5, we have for . In particular,

Proof.

We establish the result by showing that as for sufficiently large . The result then follows from Corollary 2 and Lemmas 12 and 14. To that end, we rewrite IVP() as follows:

Multiplying both sides with the integrating factor yields the following bound:

Integrating both sides of the above inequality over and using gives:

| (142) |

where

First, we consider and write

Applying the change of variable yields

| (143) |

where is the CDF for the standard normal distribution. Next, we turn to and facilitate its derivative by first deriving

Note that . Using the change of variable , we write

Then, using , we arrive at

| (144) |

Substituting (143)–(144) into (142) then gives

| (145) |

Note that there exists large enough so that

| (146) |

Then for and , combining (145) and (146), we write,

Thus, we have the following lower bound on :

| (147) |

In particular, we note that for , the right-hand side of (147) tends to as . Thus, for whenever it is above , completing the proof. ∎

To facilitate the analysis, under Case of Assumption 5, we define for . The remaining results will prove that this along with its corresponding , solve the Bellman equation in Case for .

Lemma 19.

Under Case of Assumption 5, we have that for .

Proof.

Recall from Lemma 17 that there exists a such that for . Clearly, we must have for and . Thus, we conclude that for . ∎

Lemma 20.

Under Case of Assumption 5, We have that and is bounded for .

Proof.

Consider Case of Assumption 5 for . We argue by contradiction. Suppose . Then, by Corollary 2, . In particular, by Lemma 12, there exists a such that . Because is continuous in (see Lemma 15), there exists a such that

| (148) |

However, by definition of , there exists a such that . Applying Lemma 12 again, it follows that for all , contradicting (148). Thus, .

We now prove that is bounded. Aiming for a contradiction, suppose it is not bounded. Then there exists a such that . Then, because is continuous in (by Lemma 15) and (by Lemma 19), there exists an such that . It follows that is unbounded by Lemma 13, which in turn implies that by Corollary 2 and Lemma 11. That , however, contradicts the definition of . ∎

Lemma 21.

Under Assumption 5, the following hold:

-

(i)

and ,

-

(ii)

and .

Proof.

Lemma 22.

Under Case of Assumption 5, we have that is nondecreasing with for .

Proof.

Consider Case of Assumption 5 for . Because by Lemma 20, is nondecreasing. Also, by Lemma 20 we have that is bounded. Consequently, by Lemma 13, we have that

Moreover, because is nondecreasing, its limit is well-defined and satisfies

Now let and suppose that . Consider IVP():

Passing to the limit on both sides and noting that gives the following:

Thus, there exists a such that . We conclude by Lemma 12 that , a contradiction. Therefore,

∎

We conclude this section with a proof of Theorem 1:

Proof of Theorem 1.

First, consider the case that is covered by Case 1 of Assumption 5 (Assumption 5(a)). In this case, solves Equations (109)–(110) and this solution in unique by Lemma 6. Moreover, by Lemma 22, we have that . Finally, by Lemma 19, we have that . Therefore, solves the Bellman equations (95)–(96) in this case. When , Case 2 of Assumption 5 applies, and the proof follows from the same steps as in the first case. ∎

Proposed Policy

In this section we propose a dynamic pricing and dispatch policy for the problem introduced in Section 3 by interpreting the solution of the equivalent workload formulation (85)–(89) in the context of the original control problem. To describe the policy, recall that we considered a sequence of systems indexed by the number of jobs , whose formal limit was the Brownian control problem (52)–(56) under diffusion scaling. To articulate the proposed policy, we fix the system parameter and use it to unscale processes of interest. We define the (unscaled) workload process as follows:

Proposed Pricing Policy: Given the workload process , we choose the demand rates

where is the solution to the Bellman equation (95)–(96). This follows from Equations (47) and (97), Lemma 4, and Theorem 2. The corresponding proposed pricing policy is given by

| (149) |

where is the inverse of the demand rate function for region . Equation (149) is derived in Appendix A.

Proposed Dispatch Policy: We propose two dispatch policies and refer to them as Dispatch Policy 1 (DP1) and Dispatch Policy 2 (DP2). Dispatch Policy 1 (DP1) is motivated by the following observation. In the Brownian control problem under the complete resource pooling assumption, we set all but one of the inventory levels to zero. (The buffer with nonzero inventory corresponds to the one with lowest holding cost.) However, as articulated in Harrison (1996), zero inventory in the Brownian control problem corresponds to small positive inventory levels in the original system. Thus, we put small safety stocks in the various buffers and only serve them when inventory levels are at or above the threshold. To that end, denote by the safety stock for buffer .

To be more specific, letting denote the set of basic activities undertaken by server and letting denote the set of basic activities that serve buffer , our proposed dispatch policy is as follows: If server becomes idle at time , it serves a job from the buffer in with largest holding cost . In words, when server becomes idle, it looks at all buffers it servers by means of basic activities and serves the buffer with largest holding cost that is above its safety stock. To complete the policy description, suppose that at time the inventory in buffer increases from to , i.e., reaches the safety stock. The system manager serves buffer by an idle server in with largest effective idling cost , see Equation (84). In words, when buffer reaches the safety stock, i.e., that buffer becomes eligible for service, the system manager selects an idle server with largest effective idling cost than can serve the buffer by means of a basic activity.

Dispatch Policy 2 (DP2) is motivated by the maximum pressure policy, see for example Stolyar (2004), Dai and Lin (2005), Dai and Lin (2008), and Ata and Lin (2008). Under this policy, each server prioritizes his own (local) buffer. If his own buffer is empty, then he checks the other buffers that he can serve using basic activities. If there are multiple such buffers, the server works on the buffer with the largest queue length. If the server’s own (local) buffer is empty and he cannot serve any other buffers using basic activities, then he considers all remaining buffers he can serve (using nonbasic activities) and works next on the buffer with the largest queue length.

Simulation Study

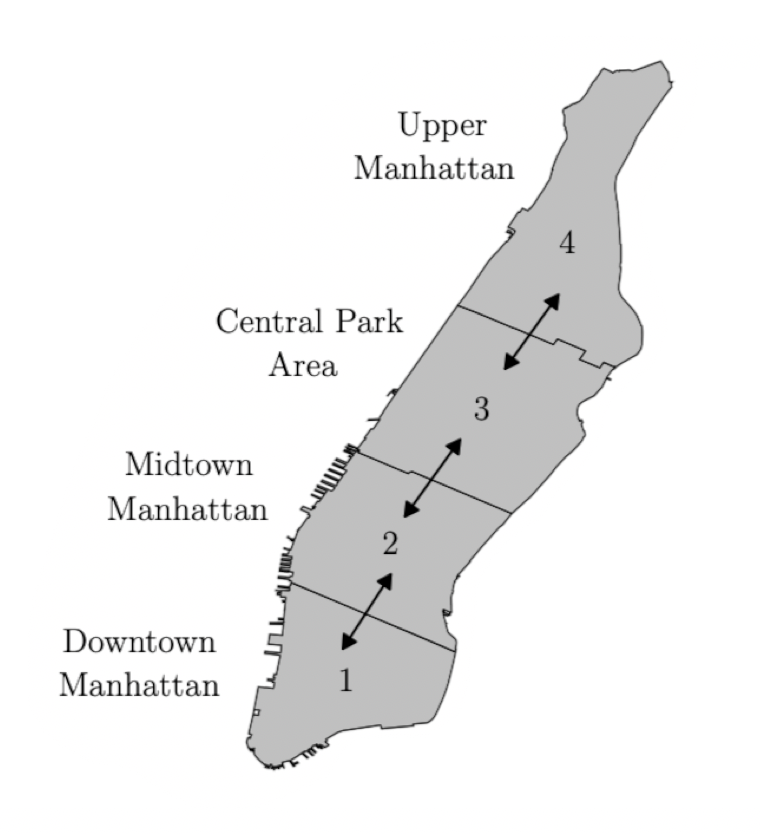

This section presents a simulation study to illustrate the effectiveness of the proposed policy. The simulation setting and its parameters are motivated, albeit loosely, by the taxi market in Manhattan, see Ata et al. (2019) and the references therein. We set the number of cars, i.e., the system parameter, as . As done in Ata et al. (2019), we divide Manhattan into regions, see Figure 2.

We assume cars can pick up customers in their own regions as well as from the neighboring regions. This gives rise to the following capacity consumption matrix:

Using the same dataset in Ata et al. (2019), we set666For simplicity, we use the preliminary results from Ata et al. (2019) to estimate and (based on a four-year dataset from January 2010 to December 2013). In doing so, we focus on the day shift of the non-holiday weekdays. the demand rate (per hour) vector as follows:

The corresponding limiting rate vector is then computed as , which yields

| (150) |

Using this and Equation (29), we derive the input-output matrix as follows:

Ata et al. (2019) reports the mean travel time as 13.2 minutes. To account for the pick up time and for other inefficiences that are not incorporated in our model, we inflate this by a factor of two, and set the mean trip time to 26.4 minutes. Thus per hour. Moreover, because we study the system under the heavy traffic assumption (Assumption 3), we set . Therefore, we have that .

We estimate the routing probability vector from the data as

which yields the limiting arrival rate vector to various buffers as follows:

Thus using the data , and , one can compute the unique nominal processing plan , referred to in Assumption 3. It is displayed in Figure 3.

Having characterized , we next compute the drift parameter and the variance parameter of the Brownian motion , see Equation (78). To this end, first note that the drift vector and the covariance matrix of the Brownian motion (see Equations (53), (59), and (60)) are given as follows:

Thus, we have that and .

Next, we describe the economic primitives of our example: the demand function, and its associated profit function, the holding cost rates and the cost of idleness. We assume that the demand function is linear. That is,

where are constants. Also, its inverse is given by

The profit function then follows from Equation (11) as follows:

We set the optimal static price as for all region , which is about the average price of a ride in the data, see Ata et al. (2019). Also, recall that the limiting demand rate vector is given by (150). We crucially assume that these are the optimal demand rate and the prices. This is equivalent to assuming and for . Namely, we set

Given these we compute the parameter as for . Thus, we obtain and .

Ata et al. (2019) suggest that the holding cost when taxis are traveling is dollars per hour (which can be derived from their fuel cost estimates). To estimate the holding cost rates for other buffers, we consider the driver’s opportunity cost. A driver can complete about two trips per hour, resulting in approximately dollars per hour. Thus, we set for . Thus, we have . Upon scaling, we derive the limiting holding cost rate for the equivalent workload formulation as . The idleness costs parameters are set to equal the lost revenue. That is, for . Upon rescaling, the limiting idleness cost is . Thus, the cheapest server to idle as with the idling cost .

Having computed the parameters , and , we solve the Bellman equation numerically for the example. Using this solution, we next describe our proposed policy.

Pricing Policy. It follows from Equation (149) that

This corresponds to the following demand rates:

Dispatch Policy. As discussed in Section 8, we propose two dispatch policies. Under the first proposed policy (Dispatch Policy 1), servers 2 and 4 work only on their own buffer throughout. Servers 1 and 3 prioritize their own buffers, but server 1 serves buffer 2 if buffer 1 is empty and buffer 2 exceeds threshold . Similarly, server 3 serves buffers 2 or 4 only if buffer 3 is empty and buffer 2 or 4 exceeds threshold . If both queues exceeds , then server 3 serves the longest one. We determine the threshold by a brute-force search. In particular, we set .

Under Dispatch Policy 2, each server prioritizes his own (local) buffer. If his own buffer is empty, then he checks the other buffers that he can serve using basic activities. If there are multiple such buffers, the server works on the buffer with the largest queue length. If the server’s own (local) buffer is empty and he cannot serve any other buffers using basic activities, then he considers all remaining buffers he can serve (using nonbasic activities) and works next on the buffer with the largest queue length.

In order to compare the performance of our policy, we calculate the total revenue by adding up the prices charged to each served customer. This also incorporates the cost of idleness. Also, we keep track of the holding costs incurred. Lastly, we use

(see Equation (49)) to compute the normalized cost , see Equation (50).

We compare our policy against the following benchmark policies that combine alternative pricing and dispatch policies. For pricing, in addition to our dynamic pricing policy, we also consider the static pricing policy which sets for all and . For dispatch, in addition to our two proposed policies, we consider (i) a static dispatch policy, and (ii) the closest driver policy as described next.

Static Dispatch Policy. Servers 2 and 4 always serve their own buffers. If both buffers 1 and 2 are nonempty, then server 1 works on buffer 1 with probability and it works on buffer 2 with probability . If only one of the buffers 1 and 2 is nonempty, then server 1 works on that buffer. Server 3 splits its effort among buffers 2, 3, and 4 similarly, i.e., proportional to , and , respectively.

Closest Driver Policy. We let be the distance matrix, i.e., corresponds to the distance (in miles) between regions and when and . Using the data from Ata et al. (2019), we have

Server engages in activity at time . In other words, under the closest driver policy each server prioritizes the buffer that is closest to him.

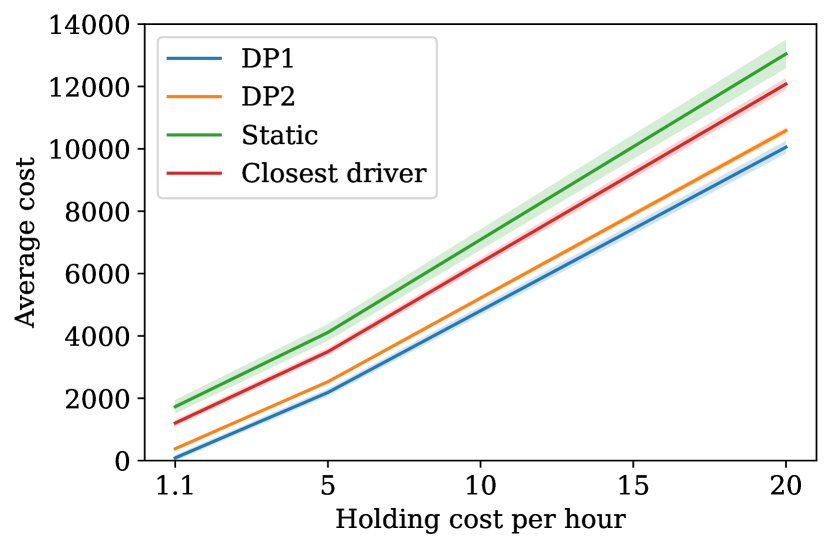

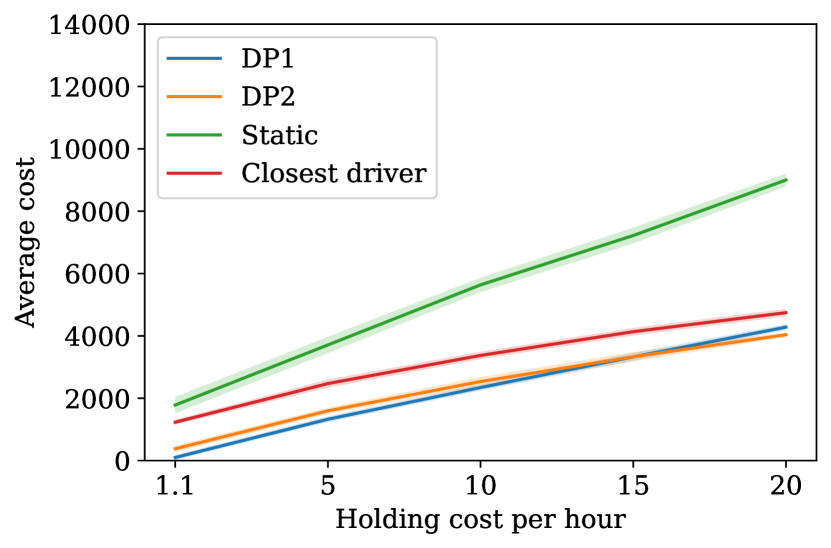

The result of the numerical study are given in Table 1. The simulated results are obtained based on a run-length of 1000 hours and the estimated average cost is computed by excluding the statistics from the first 200 hours warm-up period. The corresponding confidence intervals are calculated based on 10 macro-replications. We observe that the proposed dispatch policies (DP1, DP2) offer significant improvement (9.74%-55.01%) over the benchmark policies. More importantly, we observe that dynamic pricing can lead to significant improvement (30.96%-61.73%) for every dispatch policy considered. Among the policies considered, the dynamic pricing with Dispatch Policy 2 (DP2) has the best performance.

| Dispatch policy | Static pricing policy | Dynamic pricing policy |

|---|---|---|

| DP1 | 10075.23 201.59 | 4302.59 94.09 |

| DP2 | 10607.19 103.18 | 4059.35 73.73 |

| Static policy | 13066.83 457.31 | 9021.89 204.19 |

| Closest driver policy | 12100.53 193.57 | 4766.96 122.19 |

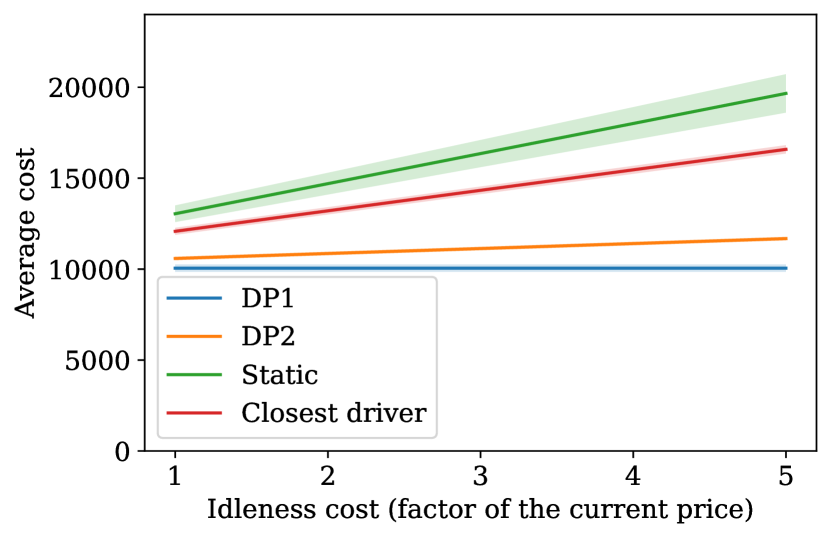

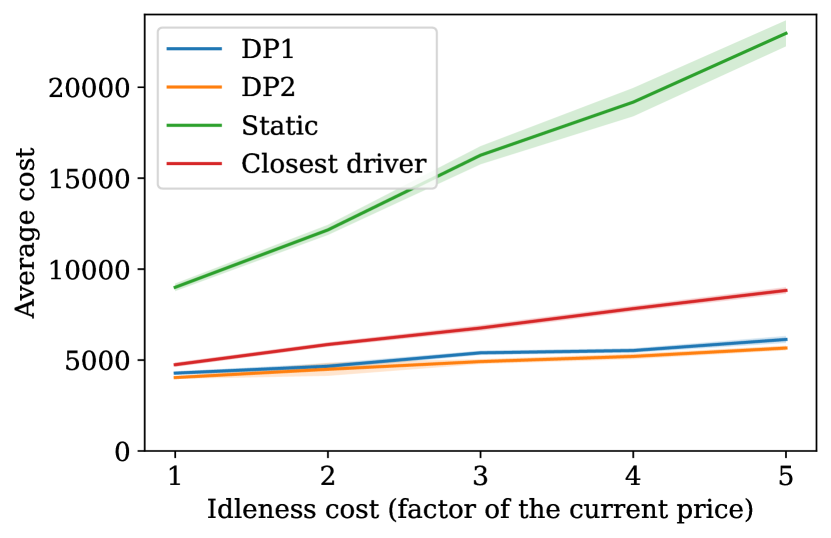

Unfortunately, we do not have any data to directly estimate the holding costs and the cost of idleness. For the former, the actual holding cost may be lower because the opportunity cost we estimate is likely an upper bound. On the other hand, the latter does not account for the loss of goodwill currently. Therefore, we conduct a sensitivity analysis that considers lower holding cost rates (Figure 4) and another one that considers higher cost of idleness that incorporate the loss of goodwill777The estimated performance and the corresponding confidence interval for the sensitivity analysis is also based on 10 macro-replications where each replication has a run-length of 1000 hours (and the statistics of the first 200 hour are discarded as a warm-up period). (Figure 5). These collectively show that the insights from Table 1 are robust to changes in holding and idleness cost parameters.

Concluding Remarks

We study a dynamic pricing and dispatch control problem motivated by ride-hailing systems. The novelty of our formulation is that it incorporates travel times. We solve this problem analytically in the heavy traffic regime under the complete resource pooling condition. Using this solution, we propose a closed form dynamic pricing policy as well as a dispatch policy. We compare the proposed policy against benchmarks in a simulation study and show that it is effective.

Our formulation has some limitations too. Namely, we assume there is only one travel node and that the complete resource pooling condition holds. Interesting future research directions include relaxing these assumptions.

References

- Abramowitz and Stegun (2003) Abramowitz, M. and Stegun, I.A. (2003), “Handbook Mathematical Functions with Formulas, Graphs, and Mathematical Tables,” Dover Publications, New York.

- Adusumilli and Hasenbein (2010) Adusumilli, K.M. and Hasenbein, J.J. (2010), “Dynamic Admission and Service Rate Control of a Queue,” Queueing Systems, 66 (2) 131–154.

- Afèche et al. (2018) Afèche, P., Liu, Z., and Maglaras, C. (2018), “Ride-Hailing Networks with Strategic Drivers: The Impact of Platform Control Capabilities on Performance,” Working Paper.

- Afèche et al. (2020) Afèche, P., Liu, Z., and Maglaras, C. (2020), “Surge Pricing an Dynamic Matching for Hotspot Demand Shock in Ride-hailing Networks,” Working Paper.

- Ata (2005) Ata, B. (2005) “Dynamic Power Control in a Wireless Static Channel Subject to a Quality-of-Service Constraint,” Operations Research, 53 (5) 842–851.

- Ata (2006) Ata, B. (2006) “Dynamic Control of a Multiclass Queue with Thin Arrival Streams,” Operations Research, 54 (5) 876–892.

- Ata and Barjesteh (2020) Ata, B. and Barjesteh, N. (2020), “Dynamic Pricing of a Multiclass Make-to-Stock Queue,” Working Paper.

- Ata et al. (2019) Ata, B., Barjesteh, N., and Kumar, S. (2019), “Spatial Pricing: An Empirical Analysis of Taxi Rides in New York City,” Working Paper.

- Ata et al. (2020) Ata, B., Barjesteh, N., and Kumar, S. (2020), “Dynamic Matching and Centralized Relocation in Ridesharing Platforms,” Working Paper.

- Ata and Kumar (2005) Ata, B. and Kumar, S. (2005), “Heavy Traffic Analysis of Open Processing Systems with Complete Resource Pooling: Asymptotic Optimality of Discrete Review Policies,” The Annals of Applied Probability, 15 (1A) 331–391.

- Ata et al. (2005) Ata, B., Harrison, J.M., and Shepp, L.A. (2005), “Drift Rate Control of a Brownian Processing System,” The Annals of Applied Probability, 15 (2) 1145–1160.

- Ata et al. (2021) Ata, B., Field, J., Lee, D., and Tongarlak, M.H. (2021), “A Dynamic Model for Managing Volunteer Engagement,” Working Paper.

- Ata et al. (2019) Ata, B., Lee, D., and Sönmez, E. (2019), “Dynamic Volunteer Staffing in Multicrop Gleaning Operations,” Operations Research, 67 (2) 295–314.

- Ata and Lin (2008) Ata, B. and Lin, W. (2008), “Heavy traffic analysis of maximum pressure policies for stochastic processing networks with multiple bottlenecks,” Queueing System, 59 191-–235.

- Ata and Olsen (2009) Ata, B. and Olsen, T.L. (2009), “Near-Optimal Dynamic Lead-Time Quotation and Scheduling Under Convex-Concave Customer Delays,” Operations Research, 57 (3) 753–768.

- Ata and Olsen (2013) Ata, B. and Olsen, T.L. (2013), “Congestion-Based Leadtime Quotation and Pricing for Revenue Maximization with Heterogeneous Customers,” Queueing Systems, 73 (1) 35–78.

- Ata and Shneorson (2006) Ata, B. and Shneorson, S. (2006), “Dynamic Control of an Service System with Adjustable Arrival and Service Rates,” Management Science, 52 (11) 1778–1791.

- Ata and Tongarlak (2013) Ata, B. and Tongarlak, M.H. (2013), “On Scheduling a Multiclass Queue with Abandonments under General Delay Costs,” Queueing Systems, 74 (1) 65–104.

- Ata and Zachariadis (2007) Ata, B. and Zachariadis, K.E. (2007), “Dynamic Power Control in a Fading Downlink Channel Subject to an Energy Constraint,” Queueing Systems, 55 (1) 41–69.

- Banerjee et al. (2021) Banerjee, S., Freund, D., and Lykouris, T. (2021), “Pricing and Optimization in Shared Vehicle Systems: An Approximation Framework,” Operations Research, forthcoming.

- Banerjee et al. (2019) Banerjee, S., Kanoria, Y., and Qian, P. (2020), “Dynamic Assignment Control of a Closed Queueing Network under Complete Resource Pooling,” Working Paper.

- Banerjee et al. (2015) Banerjee, S., Riquelme, C., and Johari, R. (2015), “Pricing in Ride-Sharing Platforms: A Queueing-Theoretic Approach,” Proceedings of the Sixteenth ACM Conference on Economics and Computation, 639–639.

- Bateman and Erdélyi (1953) Bateman, H. and Erdélyi, A. (1953), “Higher Transcendental Functions, Volume I,” McGraw-Hill, New York.

- Bell and Williams (2001) Bell, S.L. and Williams, R.J. (2001), “Dynamic Scheduling of a System with Two Parallel Servers in Heavy Traffic with Resource Pooling: Asymptotic Optimality of a Threshold Policy,” The Annals of Applied Probability, 11 (3) 608–649.

- Bell and Williams (2005) Bell, S.L. and Williams, R.J. (2005), “Dynamic Scheduling of a Parallel Server System in Heavy Traffic with Complete Resource Pooling: Asymptotic Optimality of a Threshold Policy,” Electronic Journal of Probability, 10 1044–1115.

- Bertsimas et al. (2019) Bertsimas, D., Jaillet, P., and Martin, S. (2019), “Online Vehicle Routing: The Edge of Optimization in Large-Scale Applications,” Operations Research, 67 (1) 143–162.

- Besbes et al. (2021a) Besbes, O., Castro, F., and Lobel, I. (2021), “Surge Pricing and Its Spatial Supply Response,” Management Science, 67 (3) 1350–1367.

- Besbes et al. (2021b) Besbes, O., Castro, F., and Lobel, I. (2021), “Spatial Capacity Planning,” Operations Research, 70 (2) 1271–1291.

- Billingsley (1999) Billingsley, P. (1999), “Convergence of Probability Measures (Second Edition),” John Wiley & Sons, Inc., New York, NY.

- Bimpikis et al. (2019) Bimpikis, K., Candogan, O., and Saban, D. (2019) “Spatial Pricing in Ride-Sharing Networks,” Operations Research, 67 (3) 744–769.

- Bramson and Dai (2001) Bramson, M. and Dai, J.G. (2001), “Heavy Traffic Limits for some Queueing Networks,” The Annals of Applied Probability, 11 (1) 49–90.

- Braverman et al. (2019) Braverman, A., Dai, J.G., Liu, X., and Ying, L. (2019), “Empty-Car Routing in Ridesharing Systems,” Operations Research, 67 (5) 1437–1452.

- Browne and Whitt (1995) Browne, S. and Whitt, W. (1995), “Piecewise-Linear Diffusion Processes,” in Advances in Queueing: Theory, Methods, and Open Problems, J.H. Dshalalow (Eds.), 463–480, CRC Press, Boca Raton, FL.

- Budhiraja and Ghosh (2005) Budhiraja, A. and Ghosh, A.P. (2005), “A Large Deviations Approach to Asymptotically Optimal Control of Crisscross Network in Heavy Traffic,” The Annals of Applied Probability, 15 (3) 1887–1935.

- Budhiraja et al. (2016) Budhiraja, A., Liu, X., and Saha, S. (2018), “Construction of Asymptotically Control for Crisscross Network from a Free Boundary Problem,” Stochastic Systems, 6 (2) 459–518.

- Cachon et al. (2017) Cachon, G., Daniels, K., and Lobel, R. (2017), “The Role of Surge Pricing on a Service Platform with Self-Scheduling Capacity,” Manufacturing & Service Operations Management, 19 (3) 337–507.

- Castillo et al. (2021) Castillo, J.C., Knoepfle, D., and Weyl, G. (2021), “Matching in Ride Hailing: Wild Goose Chases and How to Solve Them,” Working Paper.

- Çelik and Maglaras (2008) Çelik, S. and Maglaras, C. (2008), “Dynamic Pricing and Lead-Time Quotation for a Multiclass Make-to-Order Queue,” Management Science, 54 (6) 1132–1146.

- Chen et al. (2020) Chen, Q., Lei, Y., and Jasin, S. (2020), “Real-time spatial-intertemporal dynamic pricing for balancing supply and demand in a network,” Working Paper.

- Chen et al. (1994) Chen, H., Yang, P., and Yao, D.D. (1994), “Control and Scheduling in a Two-Station Queueing Network: Optimal Policies and Heuristics,” Queueing Systems, 18 (3–4) 301–331.

- Chen and Sheldon (2016) Chen, M.K. and Sheldon, M. (2016), “Dynamic Pricing in a Labor Market: Surge Pricing and Flexible Work on the Uber Platform,” Proceedings of the 2016 ACM Conference on Economics and Computation.

- Dai and Lin (2005) Dai, J. G. and Lin, W. (2005), “Maximum Pressure Policies in Stochastic Processing Networks,” Operations Research, 53 (2) 197-218

- Dai and Lin (2008) Dai, J. G. and Lin, W. (2008), “Asymptotic optimality of maximum pressure policies in stochastic processing networks,” The Annals of Applied Probability, 18 (6) 2239–2299.

- Ethier and Kurtz (2005) Ethier, S. and Kurtz, T. (2005), “Markov Processes: Characterization and Convergences,” John Wiley & Sons, Inc., New York, NY.

- Garg and Nazerzadeh (2019) Garg, N. and Nazerzadeh, H. (2021), “Driver Surge Pricing,” Management Science, 68 (5) 3219–3235.

- George and Harrison (2001) George, J.M. and Harrison, J.M. (2001), “Dynamic Control of a Queue with Adjustable Service Rate,” Operations Research, 49 (5) 720–731.

- Gokpinar and Selcuk (2019) Gokpinar, B. and Selcuk, C. (2019), “The Selection of Prices and Commissions in a Spatial Model of Ride-hailing,” Working Paper.

- Ghosh and Weerasinghe (2007) Ghosh, A.P. and Weerasinghe, A.P. (2007), “Optimal Buffer Size for a Stochastic Processing Network in Heavy Traffic,” Queueing Systems, 55 (3) 147–159.

- Ghosh and Weerasinghe (2010) Ghosh, A.P. and Weerasinghe, A.P. (2010), “Optimal Buffer Size and Dynamic Rate Control for a Queueing System with Impatient Customers in Heavy Traffic,” Stochastic Processes and Their Applications, 120 (11) 2103–2141.

- Guda and Subramanian (2019) Guda, H. and Subramanian, U. (2019), “Your Uber is Arriving: Managing On-Demand Workers Through Surge Pricing, Forecast Communication, and Worker Incentives,” Management Science, 65 (5) 1995–2014.

- Harrison (1988) Harrison, J.M. (1988), “Brownian Models of Queueing Networks with Heterogeneous Customer Populations,” in Stochastic Differential Systems, Stochastic Control Theory and Applications, W. Fleming and P.-L. Lions (Eds.), IMA Volumes in Mathematics and its Applications, 10 147–186, Springer-Verlag, New York, NY.

- Harrison (1996) Harrison, J.M. (1996), “The BIGSTEP Approach to Flow Management in Stochastic Processing Networks,” in Stochastic Networks: Theory and Applications, F. P. Kelly, I. Ziedins and S. Zachary (Eds.), 57–90, Oxford University Press.

- Harrison (1998) Harrison, J.M. (1998), “Heavy Traffic Analysis of a System with Parallel Servers: Asymptotic Optimality of Discrete-Review Policies,” The Annals of Applied Probability, 8 (3) 822–848.

- Harrison (2000) Harrison, J.M. (2000), “Brownian Models of Open Processing Networks: Canonical Representation of Workload,” The Annals of Applied Probability, 10 (1) 75–103.