latexText page

f-Betas and Portfolio Optimization with f-Divergence induced Risk Measures

Abstract

In this paper, we build on using the class of f-divergence induced coherent risk measures for portfolio optimization and derive its necessary optimality conditions formulated in CAPM format. We derive a new f-Beta similar to the Standard Betas and also extended it to previous works in Drawdown Betas. The f-Beta evaluates portfolio performance under an optimally perturbed market probability measure, and this family of Beta metrics gives various degrees of flexibility and interpretability. We conduct numerical experiments using selected stocks against a chosen S&P 500 market index as the optimal portfolio to demonstrate the new perspectives provided by Hellinger-Beta as compared with Standard Beta and Drawdown Betas. In our experiments, the squared Hellinger distance is chosen to be the particular choice of the f-divergence function in the f-divergence induced risk measures and f-Betas. We calculate Hellinger-Beta metrics based on deviation measures and further extend this approach to calculate Hellinger-Betas based on drawdown measures, resulting in another new metric which is termed Hellinger-Drawdown Beta. We compare the resulting Hellinger-Beta values under various choices of the risk aversion parameter to study their sensitivity to increasing stress levels.

1 Introduction

The Capital Asset Pricing Model (CAPM) (Sharpe [29], Sharpe [30]) is a fundamental model in portfolio theory and risk management. It is based on a Markowitz mean-variance portfolio optimization problem (Markowitz [18]). Tremendous literature is available on CAPM, see for instance, critical review papers by Galagedera [13], and Rossi [27]. The Standard Beta relates the expected return of a security and the expected excess return of a market. Since its introduction, Beta has been used as a key indicator of asset performance in portfolio management. The variance risk measure used in the standard CAPM formulation has a conceptual drawback: it does not distinguish losses and gains of a portfolio. For this reason, Markowitz [17] considered Semi-Variance based only on negative returns, and the associated Beta was called Downside Beta. Although the idea sounds conceptually attractive, Downside Beta and Standard Beta have close values therefore, it provides little information in addition to Standard Beta. In the vast literature on CAPM models, various non-symmetric risk measures have been proposed as an alternative to variance. In particular, Conditional Value-at-Risk (CVaR) is a popular choice of risk measure. It was introduced by Rockafellar and Uryasev [21] for continuous distributions as the conditional expected loss exceeding Value-at-Risk (VaR) and generalized to discrete distributions in Rockafellar and Uryasev [22]. CAPM has been extended to non-symmetric risk measures such as Generalized Deviations by Rockafellar et al. [24], which demonstrated that CAPM equations are necessary optimality conditions for portfolio optimization problems. In particular, Beta was computed for CVaR and Lower Semi-Deviation (the square root of Semi-Variance). See the review paper by Krokhmal et al. [15] for detailed discussions on these and other non-symmetric risk measures, which provide formulas for Betas.

In this paper, we discuss a new Beta metric based on a recently studied family of return-based risk measures called f-divergence induced risk measures. This is a coherent risk measure for every choice f-divergence function and the statistical confidence radius. Dommel and Pichler [10] contains a detailed study of the properties and characterizations of this risk measure. Based on their theoretical results, as reviewed in Section 2, we discuss portfolio optimization problems with f-divergence induced risk measures in Section 3 and propose in Section 4 a family of Beta metrics called f-Beta that relates the losses of a stock to that of the market under given optimal perturbations as characterized through a dual maximization problem for the f-divergence induced risk measure. The f-divergence induced risk measures have more desirable properties as compared with CVaR risk or VaR. Compared with CVaR, which shares very similar definitions, the f-divergence induced risk measures are smoother, and the corresponding risk identifier functions are more continuous with respect to the changing risk aversion parameter. This means that attention (weights) on the stressful scenarios being considered are transitioning more gradually. Moreover, the choice of the generating divergence function provides flexibility in characterizing the shape of the risk measure and hence characterizes different types of risk aversion behaviors. In particular, we can interpret f-divergence induced risk measures as views on the worst-case expected loss under assumptions of various degrees of market distribution shift, where the distance between distributions is measured using well-defined statistical divergences/distances. Both facts make it more natural to be considered as a risk measure. Similar to CVaR under smaller tail risk levels (with the tail risk level of 1 being the risk-neutral expectation), f-divergence induced risk measures transition from risk-neutral expectation to worst-case loss as the risk aversion parameter(which is also a statistical confidence region radius) increases from zero to larger values, hence providing a complete and continuous middle-ground between risk-neutral and worst-case loss averse. See more related discussion in Section 5. We expect the desirable properties of f-divergence induced risk measures to translate to corresponding Beta metrics based on such risk measures in the CAPM framework. Numerical results of Hellinger-Beta, based on choosing squared Hellinger distance as the f-divergence function, is demonstrated in Section 6 using DOW 30 data.

We further build on f-Betas and extend them to previous work on Drawdown Betas. A considerable drawback of Variance, CVaR, Semi-Deviation, and many other risk measures is that they are static characteristics, which do not account for persistent consecutive portfolio losses (may be resulting in a large cumulative loss). The dynamic drawdown risk measure is actively used in portfolio management as an alternative to static measures. Portfolio managers try to build portfolios with low drawdowns. The most popular drawdown characteristic is the Maximum Drawdown. However, the Maximum Drawdown is not the best risk measure from a practical perspective: it accounts for only one specific event on a price sample path. For instance, Goldberg and Mahmoud [14] suggested the so-called Conditional Expected Drawdown (CED), which is the tail mean of the maximum drawdown distribution. Chekhlov et al. [5] proposed Conditional Drawdown-at-Risk (CDaR), which averages a specified percentage of the largest portfolio drawdowns over an investment horizon. CDaR is defined as CVaR of the drawdown observations of the portfolio cumulative returns. CDaR possesses the theoretical properties of a deviation measure, see Chekhlov et al. [6]. Zabarankin et al. [33] developed CAPM relationships based on CDaR. The paper derived necessary optimality conditions for CDaR portfolio optimization, which resulted in a CDaR Beta relating cumulative returns of a market (optimal portfolio) and individual securities. Ding and Uryasev [9] extended this previous result to consider Expected Regret of Drawdowns (ERoD) based on a reformulation of the CDaR risk through expected regret where a clear interpretation of the chosen drawdown threshold can be provided instead of using a predefined tail risk level as in CDaR Beta. Their proposed metric is called ERoD Beta, which also relates consecutive returns of a security to those of the market. A negative ERoD Beta identifies a security that has positive returns when the market has drawdowns exceeding the threshold. See also Drawdown Beta Website [11]. In Section 7, we propose to use an f-divergence induced risk measure for drawdown observations to obtain a new f-Drawdown Beta and demonstrate their new perspectives via numerical results.

2 Preliminaries on f-Divergence induced Risk Measures: Formulations and Properties

We provide in this section a brief review of the f-divergence induced coherent risk measures and their properties, as introduced in Dommel and Pichler [10] in greater detail. The family of f-divergence induced risk measures is defined for each divergence generating function on domain() = which is convex, lower semicontinuous, and satisfies . For two probability measures on the sample space , the corresponding f-divergence generated by is defined as:

| (1) |

if and otherwise. The convex conjugate of is defined as . These two functions satisfy the Fenchel–Young inequality among other important properties:

For each pair of conjugate functions satisfying previous assumptions, the f-divergence induced risk measure is defined through the following minimization problem, where is a risk aversion parameter:

| (2) |

The divergence function characterizes the shape of risk aversion for increasing risk, while the risk aversion coefficient describes the tendency of an investor to avoid risk. This risk measure is well defined for all , satisfying the inequality . It is law invariant but can be unbounded. As a remark, we know that and are both generating functions for the same divergence function due to conservation of probabilities. Their conjugate functions satisfy , which leads to the same risk measure from the primal problem (2) for the same loss random variable .

In Tables 1 and 2 (tables adapted from Nowozin et al. [20]), we list some examples of f-divergences, including the well-known KL-divergence, total variation distance, and squared Hellinger distance. For each f-divergence listed, the generator function and its conjugate function are shown in the tables in accordance with notations of Dommel and Pichler [10].

| Name | Generator | |

|---|---|---|

| Total Variation | ||

| Kullback-Leibler | ||

| Reverse Kullback-Leibler | ||

| Pearson | ||

| Neyman | ||

| Squared Hellinger | ||

| Jensen-Shannon | ||

| -Divergence () |

| Name | Conjugate | |

|---|---|---|

| Total Variation | ||

| Kullback-Leibler | ||

| Reverse Kullback-Leibler | ||

| Pearson | ||

| Neyman | ||

| Squared Hellinger | ||

| Jensen-Shannon | ||

| -Divergence () | ||

| -Divergence () |

The f-divergence induced risk measure satisfies the following four axioms:

1. Monotonicity: provided that almost surely.

2. Translation equivariance: for any and .

3. Subadditivity: for all .

4. Positive homogeneity: for all and .

Hence it is a coherent risk measure by definition. It also satisfies ,

Conversely, for any non-negative random variable , it holds that,

The most important property of the f-divergence induced risk measures is that they can be equivalently stated through a dual representation involving a maximization problem. For a given divergence generating function and its convex conjugate , define the Orlicz space as for some . Dommel and Pichler [10] showed that for every , the f-divergence induced risk measure has the dual representation:

| (3) |

where . The above dual representation in (3) can be alternatively expressed as:

| (4) |

The proposed risk can therefore be interpreted as the largest expected value over all probability measures within an f-divergence ball around . The divergence function characterizes the shape of the ball, while determines the radius. Under suitable conditions where and holds true, then the infimum in the defining equation (2) of the risk measure is attained. Again, one can make the remark that for generating functions which generate the same divergence, the resulting risk measure is the same since the feasible region in (4) is the same. As an additional remark, Entropic Value-at-Risk (EVaR), see [1] and [2], is a frequently used coherent risk measure in finance and engineering, defined as:

| (5) |

EVaR is an example of the family of f-divergence induced risk measures by choosing the Kullback-Leibler divergence (KLD) to be the f-divergence and the confidence radius to be for some confidence level . When is a univariate Gaussian distributed loss random variable, EVaR takes the analytical form . Similarly, an analytic formula can be computed for a uniform random variable.

The f-divergence induced risk measure also has the representation in terms of spectral risk measures [10], which is equivalent to the Kusuoka representation:

| (6) |

where the supremum is taken over all non-decreasing with and . Notice that every function of the form where with is a coherent risk measure itself, hence the spectral representation is useful for deriving bounds between the f-divergence induced risk measure and its spectral components. An important special example is the CVaR risk functional, which has the following spectral form:

where the function is in the spectral set of the f-divergence induced risk measure (over which the supremum is taken) if the following holds: . Hence under this condition, we can relate the corresponding CVaR risk to the f-divergence induced risk by the inequality:

Dommel and Pichler [10] elaborate on the optimality inside of the minimization representation (2) and the dual maximization representation (3) based on facts concerning the ‘derivatives’ of the convex function and its conjugate . Let and suppose solve the characterizing equations:

| (7) | |||

Then they are the optimal values in the primal minimization problem. Furthermore, the random variable is optimal in the dual maximization problem, i.e., and,

Lastly, the primal formulation of the f-divergence induced risk measure can be efficiently used in portfolio optimization problem objectives where we can solve a single augmented minimization problem with only two additional variables instead of two nested optimization problems when using the dual maximization problem representation or its alternative forms. With the primal formulation, we solve for:

Here the portfolio loss random variable is where is a random vector of returns for the assets in consideration with expected values . The feasible region can be chosen using standard constraints on the (long-only) portfolio weights in combination with a target return constraint with threshold such as:

Similar to the discussion before, controls the shape of the risk function and hence the sensitivity of the solution to the return distribution and the desired risk level . Larger implies higher risk aversion and more conservative portfolio choices.

In the following sections, we can study CAPM-type necessary optimality conditions of optimization problems based on risk objectives and derive corresponding Beta values for assets in a market under CAPM assumptions, which generalizes the Standard Beta and provides an alternative to CVaR Betas and CVaR-based Drawdown Betas as discussed in Ding and Uryasev [9], [33].

3 f-Divergence induced Risk Measure and Portfolio Optimization

Let us denote by the vector of historic returns of a portfolio with weights vector . Also, we denote by the associated loss observations.

We denote

-

•

vector of weights for assets in the portfolio;

-

•

vector of returns of portfolio assets at time moment on scenario ;

-

•

corresponding vector of losses of portfolio assets;

-

•

probability of the scenario (sample path of returns of securities);

-

•

portfolio return at time moment on scenario ;

-

•

vector of portfolio returns with components , ;

-

•

portfolio loss at time moment on scenario ;

Following Zabarankin et al. [33], we state the risk (multiple paths) minimization problem over periods subject to a constraint that the portfolio’s expected return exceeds a given target :

| (8) |

This problem is similar to a Markowitz mean-variance optimization with variance replaced by the f-divergence induced risk .

4 CAPM: Necessary Optimality Conditions for Portfolio Optimization with f-Divergence induced Risk Measures

Similar to Zabarankin et al. [33] and Ding and Uryasev [9], we provide necessary optimality conditions for optimization problems (8) and (9) in the form of CAPM equations. In particular, the formula for f-Beta can be derived similarly to the Standard Beta, which relates returns of the market and individual assets. Let be the loss associated with the optimal(market) portfolio, the necessary optimality conditions for the solution of both problems (8) and (9) are stated in the form of CAPM:

| (10) |

| (11) |

The f-Beta CAPM equation (10) relates the expected returns of the market and instruments under a constrained perturbation measure. On the efficient frontier with the risk measure against the target return, the optimal solution is the point where the capital asset line makes a tangent cut with the efficient frontier.

Theorem 1.

Let be the return vector for an optimal portfolio of the problem (8). The necessary optimality conditions for (8) can be stated in the form of CAPM:

| (12) |

where

-

•

f-Beta relating the expected returns, , of the optimal portfolio (market) and expected return, , of security ;

-

•

are the loss observations associated with the optimal(market) portfolio for all ;

-

•

is the f-divergence induced risk for the optimal(market) portfolio, where is the set of feasible perturbation measures under f-divergence function and confidence radius , where is the empirical probability vector for observations in a single historic path;

-

•

optimal perturbed measure from which maximizes the perturbed market expected loss as in the dual representation of ;

Consequently, for a single path:

| (13) |

where

-

•

f-Beta relating the expected returns, , of the optimal portfolio (market) and expected return, , of security in a single path;

-

•

is the f-divergence induced risk for the optimal(market) portfolio, where is the set of feasible perturbation measures under f-divergence function and confidence radius , where is the empirical probability vector for observations in a single historic path;

-

•

= optimal perturbed measure from which maximizes the perturbed market expected loss as in the dual representation of for a single path;

Proof.

Let us denote by the objective function and by an optimal portfolio vector of problem (8). The expected loss function linearly depends upon vector . The objective function is convex in . The necessary optimality condition for the convex optimization problem (8) is formulated as follows (see, for reference, Theorem 3.34 in Ruszczynski [28]):

| (14) |

where

-

•

gradient of the constraint function at ;

-

•

Lagrange multiplier such that and ;

-

•

subdifferential of convex in function at .

The gradient of the constraint function, which is linear in , equals:

| (15) |

According to the standard results in convex analysis,

| (16) |

With (15) and (16) we obtain the following system of equations

| (17) |

Multiplying the left and right hand sides of the previous equation by the optimal and summing up terms for , we have:

Consequently,

| (18) |

Substituting (18) to (17) gives necessary conditions (10), (12) in CAPM format, where we denote the optimal portfolio as the market portfolio , and the optimal risk is . ∎

5 Discussion of f-Divergence induced Risk and f-Betas

Compared with other coherent risk measures such as CVaR, f-divergence induced risk measures have the advantage that it is the result of a well-defined distributionally robust optimization problem under probability model uncertainty as specified through information-theoretic distances or divergences. The risk measured in this formulation has a direct meaning related to the choice of f-divergence functions.

The flexibility in the choices of allows for a spectrum of solutions that are comparable and interpretable. In particular, the relations between and CVaR gives a direct comparison between Betas calculated based on these two risk measures, respectively.

In the following section, we use a particular f-divergence function to illustrate the behavior of the proposed Beta metrics. Consider the following symmetric f-divergence called the squared Hellinger distance (Yang and Le Cam [32]) for two univariate probability distributions with densities :

| (19) |

Squared Hellinger distance is related to the total variation distance, an important symmetric f-divergence, via the following inequalities, , where is defined as,

| (20) |

Squared Hellinger distance is also closely related to Kullback-Leibler divergence (Kullback and Leibler [16]) and can be bounded by , where is defined as,

| (21) |

The squared Hellinger distance (19) belongs to a one-parameter family of f-divergences called the -divergences (Cichocki and Amari [7]), which smoothly connects well-known divergences such as the KL divergence, reverse KL divergence, and Pearson divergence by varying the parameter [4]:

| (22) |

Among its other properties, the squared Hellinger distance (up to a constant scaling factor) has been shown to be the minimum distance within a symmetrized -divergence family [19].

For a given historic path of length , the nominal probability vector is with length . Hence the squared Hellinger distance for any perturbation measure is bounded between . The Hellinger-Beta is proposed as follows (for a single path):

| (23) |

-

•

is the squared Hellinger distance induced risk for the optimal(market) portfolio, where is the set of feasible perturbation measures, where is the empirical probability vector for observations in a single historic path;

-

•

= optimal perturbed measure from which maximizes the perturbed market expected loss as in the dual representation of for a single path;

The optimal perturbation measure of the inner maximization problem of perturbed loss can be efficiently solved using convex optimization procedures, from which the Hellinger-Beta calculation follows easily. The squared Hellinger distance possesses desirable properties such as symmetry, boundedness between 0 and 1, and provides lower and upper bounds for total variation distance while varying smoothly as the probability vectors change. The boundedness of squared Hellinger distance gives a clear range of choice for risk aversion parameter when designing Beta metrics based on its induced risk measure.

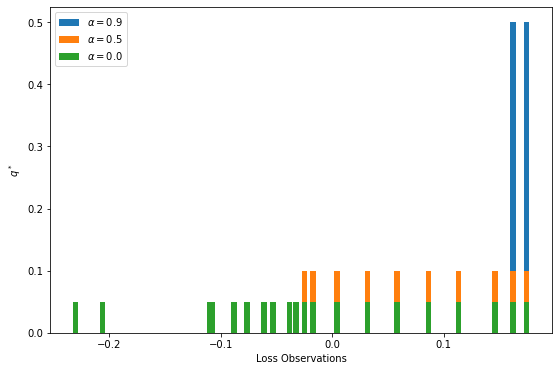

As a comparison of the different behavior of f-divergence (and in particular squared Hellinger distance) induced risk measures and CVaR risks, Figure 1 shows the risk identifiers of for 20 loss observations sampled from a Gaussian distribution, where is varying, compared against risk identifiers which are scaled indicator functions (step functions) on the tail for various . This shows the different risk behaviors offered by the family of f-divergence induced risk measures, which generally have smoother transitions of the risk identifiers than the tail indicator functions for CVaR. In particular, large corresponds to worst-case loss, which is similar to large , while and both reduce to the risk-neutral expectation. The behavior for intermediate values of is not directly comparable with intermediate values of . Notice that for an empirical distribution of loss observations and for any fixed , the optimal risk identifiers for are always larger for larger (more severe) loss observations. This result can be formalized as follows, where is the probability vector associated with the empirical loss distribution based on loss observations.

Lemma 2.

Consider the dual maximization problem for the f-divergence induced risk measures of an empirical loss distribution with a given divergence generating function and risk aversion radius :

| (24) |

where and . Let be an optimal solution to (24). Then for any , such that the loss observations , we must have in the optimal solution.

Proof.

Suppose is an optimal solution for (24), where there exists , such that and . Consider the alternative solution such that such that and , , and . is a feasible solution to (24) because by assumption. However, this solution strictly increases the objective because,

where by our assumptions and , hence . This raises a contradiction since is assumed to be an optimal solution. This completes the proof. ∎

Lemma 2 formalizes the behavior of the risk identifiers for f-divergence induced risk measures, as demonstrated in Figure 1 for the case of squared Hellinger distance in particular. Hence we expect such risk measures to put a heavier focus on more extreme losses, which is natural for a risk measure. For empirical loss observations (which are bounded), the optimal objective value of (24) is always greater than the empirical mean but no larger than the most extreme loss: .

As a last remark, the proposed f-Betas are also related to a more general theory about deviation-based Betas, see Rockafellar et al. [24]. The particular Beta in the deviation-based framework would be (for a single path):

| (25) |

where the deviation measures are defined as and and the risk identifiers are defined similarly as before.

6 Numerical Experiments

In the following numerical experiments, we computed Beta values using the S&P 500 index as the chosen optimal (market) portfolio. For demonstration, only the resulting values for the DOW 30 stocks are presented. To evaluate the stability over time of the different Betas, we first considered two non-overlapping 7.5-year historic periods:

-

•

Period 1 (containing Financial Crisis 2008): from 2006/01/01 to 2013/06/28;

-

•

Period 2 (containing COVID-19 Crisis): from 2013/07/01 to 2021/01/01.

| Standard | Standard | |||||||||

| Period 1 | Period 2 | Period 1 | Period 2 | Period 1 | Period 2 | Period 1 | Period 2 | Period 1 | Period 2 | |

| AAPL | 0.861 | 0.868 | 0.835 | 0.828 | -0.986 | 1.126 | -0.796 | 1.207 | 0.894 | 1.064 |

| AMGN | 0.650 | 0.663 | 0.647 | 0.648 | -0.218 | 0.468 | -0.163 | 0.523 | 0.817 | 0.954 |

| AXP | 1.648 | 1.260 | 1.641 | 1.266 | 0.540 | 1.606 | 0.659 | 1.547 | 1.601 | 1.056 |

| BA | 0.702 | 2.613 | 0.693 | 2.637 | 1.332 | 1.277 | 1.376 | 1.342 | 0.866 | 1.365 |

| CAT | 1.148 | 1.329 | 1.141 | 1.328 | 0.558 | 1.892 | 0.626 | 1.868 | 1.252 | 1.406 |

| CRM | 1.224 | 0.964 | 1.198 | 0.935 | -1.438 | 0.154 | -1.268 | 0.207 | 1.533 | 1.170 |

| CSCO | 1.091 | 1.234 | 1.086 | 1.236 | 1.119 | 0.664 | 1.015 | 0.641 | 1.116 | 1.245 |

| CVX | 1.225 | 1.442 | 1.214 | 1.467 | -0.129 | 1.323 | -0.038 | 1.303 | 1.042 | 1.259 |

| DIS | 1.038 | 1.270 | 1.025 | 1.267 | 0.081 | 0.859 | 0.197 | 0.893 | 0.951 | 1.025 |

| GS | 1.304 | 1.518 | 1.298 | 1.529 | 0.640 | 1.956 | 0.564 | 1.896 | 1.445 | 1.325 |

| HD | 0.755 | 1.026 | 0.743 | 1.012 | -0.037 | 0.253 | 0.040 | 0.373 | 1.003 | 0.901 |

| HON | 0.957 | 1.173 | 0.944 | 1.168 | 0.768 | 0.967 | 0.830 | 1.015 | 1.026 | 1.105 |

| IBM | 0.617 | 1.424 | 0.604 | 1.453 | -0.410 | 1.986 | -0.337 | 1.901 | 0.721 | 1.002 |

| INTC | 0.860 | 1.095 | 0.857 | 1.090 | 0.317 | 0.405 | 0.323 | 0.386 | 0.776 | 1.205 |

| JNJ | 0.572 | 0.777 | 0.566 | 0.773 | -0.110 | 0.519 | -0.071 | 0.565 | 0.491 | 0.728 |

| JPM | 1.273 | 1.401 | 1.261 | 1.400 | -0.910 | 1.190 | -0.893 | 1.257 | 1.436 | 1.243 |

| KO | 0.237 | 1.016 | 0.224 | 1.023 | -0.227 | 0.356 | -0.108 | 0.400 | 0.411 | 0.657 |

| MCD | 0.686 | 0.745 | 0.669 | 0.736 | -0.903 | -0.478 | -0.787 | -0.366 | 0.674 | 0.795 |

| MMM | 0.778 | 1.098 | 0.772 | 1.103 | 0.585 | 1.145 | 0.588 | 1.154 | 0.881 | 1.016 |

| MRK | 0.850 | 0.877 | 0.842 | 0.874 | 0.727 | 0.359 | 0.854 | 0.394 | 0.705 | 0.725 |

| MSFT | 0.801 | 0.954 | 0.796 | 0.923 | -0.047 | -0.197 | -0.014 | -0.090 | 0.877 | 1.177 |

| NKE | 1.060 | 1.110 | 1.044 | 1.092 | -0.788 | -0.378 | -0.660 | -0.269 | 1.023 | 0.941 |

| PG | 0.642 | 0.467 | 0.637 | 0.456 | 0.152 | 0.107 | 0.201 | 0.159 | 0.576 | 0.634 |

| TRV | 1.363 | 1.397 | 1.355 | 1.407 | -0.511 | 0.551 | -0.415 | 0.593 | 0.947 | 0.926 |

| UNH | 0.880 | 1.203 | 0.877 | 1.182 | 0.685 | 0.180 | 0.842 | 0.245 | 0.683 | 0.925 |

| VZ | 0.757 | 0.467 | 0.745 | 0.464 | 0.414 | 0.285 | 0.542 | 0.289 | 0.741 | 0.625 |

| WBA | 0.666 | 1.208 | 0.664 | 1.225 | 0.223 | 0.856 | 0.320 | 0.848 | 0.644 | 0.820 |

| WMT | 0.688 | 0.198 | 0.681 | 0.180 | -0.916 | 1.007 | -0.884 | 0.976 | 0.739 | 0.550 |

The results are shown in Table 3 for -Beta along with three other Beta metrics: Beta, Beta, and the Standard Beta. We observe that the new Hellinger-Beta with confidence radius gives relatively similar results to Standard Beta since they are both derived based on returns, while the behavior is quite different from the two Drawdown Betas in both periods. The Hellinger-Beta differs from Standard Beta in values due to the different perspectives of risk they focus on. Specifically, the values reported for Hellinger-Betas in Table 3 can be indicate more or less correlations with the market for different stocks and different periods. We also included the f-Betas calculated using deviations as a comparison. In addition, we report the Pearson correlation and Spearman correlation between the two columns of for Period 1 and Period 2 below:

Pearson Correlation: 0.318

Spearman Correlation: 0.545

The relatively strong correlations suggest that the Hellinger-Beta metrics are stable across different time periods.

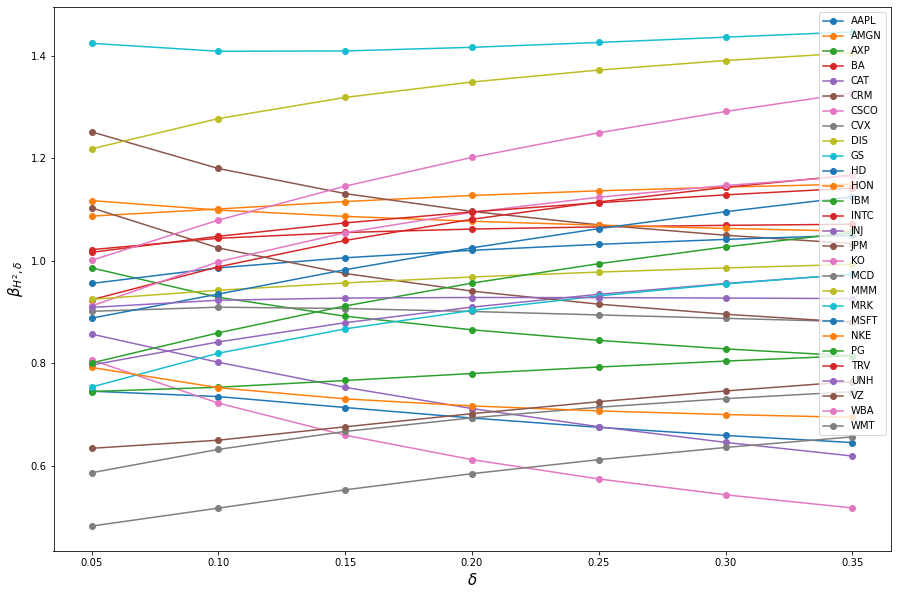

The second set of tests we performed is to understand the sensitivity of the calculated Beta metric as the risk aversion parameter changes from small to relatively medium value, where the deviation-based Beta is used. Here we take the data in a single year as a test range and calculated for different values of . Table 4 summarizes the results of this experiment for the period . Notice that for this period, most of the Hellinger-Beta values have a monotonic relationship as the risk aversion parameter is increased from 0.05 to 0.35. The monotonicity relationship can be positive or negative depending on the specific direction of movement of the particular asset with the market. The direction of change of the Beta values, as risk aversion parameter increases, can be seen as a measure of correlation between the asset and the market under increasingly more stressful scenarios. Assets with negative drift in the Beta values as stress level increases can be seen as good tools for hedging against large market downside risks, examples include CRM, GS, MCD, and MRK.

| AAPL | 1.5613 | 1.5547 | 1.5679 | 1.5916 | 1.6214 | 1.6547 | 1.6902 |

| AMGN | 0.9676 | 1.1055 | 1.2079 | 1.2888 | 1.3562 | 1.4144 | 1.4661 |

| AXP | 1.0704 | 1.0936 | 1.113 | 1.1295 | 1.1438 | 1.1564 | 1.1677 |

| BA | 1.2913 | 1.3134 | 1.3231 | 1.3276 | 1.3298 | 1.331 | 1.3319 |

| CAT | 1.6078 | 1.6591 | 1.6947 | 1.7177 | 1.731 | 1.7364 | 1.735 |

| CRM | 1.6941 | 1.5299 | 1.4384 | 1.3889 | 1.3663 | 1.3624 | 1.3723 |

| CSCO | 1.3424 | 1.3565 | 1.3716 | 1.3874 | 1.4036 | 1.4196 | 1.4352 |

| CVX | 0.906 | 0.9221 | 0.9186 | 0.9039 | 0.8822 | 0.8558 | 0.8259 |

| DIS | 0.8469 | 0.8231 | 0.8067 | 0.7987 | 0.7983 | 0.8043 | 0.8163 |

| GS | 1.635 | 1.5502 | 1.4762 | 1.4127 | 1.3572 | 1.3076 | 1.2625 |

| HD | 0.9981 | 1.0113 | 1.0364 | 1.0641 | 1.0924 | 1.121 | 1.1498 |

| HON | 1.2996 | 1.3738 | 1.4405 | 1.4999 | 1.5533 | 1.6022 | 1.6475 |

| IBM | 0.8231 | 0.8104 | 0.8116 | 0.8207 | 0.8347 | 0.8524 | 0.873 |

| INTC | 1.3659 | 1.3066 | 1.2769 | 1.263 | 1.2588 | 1.2615 | 1.2694 |

| JNJ | 0.5138 | 0.5874 | 0.6506 | 0.706 | 0.7561 | 0.8025 | 0.8461 |

| JPM | 1.272 | 1.2805 | 1.289 | 1.2971 | 1.3051 | 1.3133 | 1.3217 |

| KO | 0.7207 | 0.7607 | 0.793 | 0.8217 | 0.8484 | 0.8741 | 0.8993 |

| MCD | 0.6063 | 0.4171 | 0.2655 | 0.1385 | 0.0272 | -0.0736 | -0.1674 |

| MMM | 0.9147 | 0.9656 | 1.0053 | 1.0366 | 1.0616 | 1.0818 | 1.0983 |

| MRK | 0.8299 | 0.8114 | 0.7754 | 0.7317 | 0.6849 | 0.6373 | 0.5896 |

| MSFT | 0.8842 | 0.9199 | 0.9448 | 0.9653 | 0.9842 | 1.0028 | 1.0216 |

| NKE | 0.5297 | 0.5469 | 0.5557 | 0.5583 | 0.5562 | 0.5504 | 0.5414 |

| PG | 0.6709 | 0.6892 | 0.6968 | 0.6993 | 0.699 | 0.6969 | 0.6935 |

| TRV | 0.9607 | 0.983 | 1.0117 | 1.0386 | 1.0623 | 1.0823 | 1.0989 |

| UNH | 0.739 | 0.8158 | 0.8942 | 0.97 | 1.0424 | 1.1116 | 1.178 |

| VZ | 0.9604 | 0.9674 | 0.9648 | 0.9573 | 0.9477 | 0.9374 | 0.9272 |

| WBA | 0.9219 | 0.9876 | 1.0417 | 1.0892 | 1.1326 | 1.1732 | 1.2118 |

| WMT | 0.9784 | 0.9909 | 0.988 | 0.9799 | 0.9704 | 0.9611 | 0.9527 |

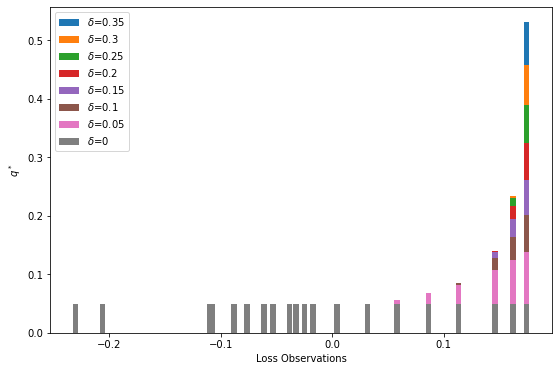

We also observe that for this one-year period, the risk aversion parameter is actually large enough in the sense that the optimal perturbation measure allocates more than 50% of the probabilities onto the top two deviation loss scenarios, which is smaller than 1% of the total number of dates. The perturbation allocation for different risk aversion parameters in the deviation-based Hellinger Beta calculation can be visualized in Figure 2 based on the loss observations (x-axis) in the S&P 500 market index from the year 2006. The y-axis plots the optimal risk identifiers in bars for each loss observation and for different risk aversion parameters , shown in different colors. We can see that increasing levels of will perturb the probability distribution of towards more extreme deviation (loss) scenarios. Hence we conclude that, in general, a risk aversion level of is large enough for enough stress to be put on extreme worst cases of the deviation (loss) scenarios. Keep increasing the risk aversion parameter won’t mean much as we just keep adding probabilities onto the top few extreme scenarios. Instead, a wider range of behavior is observable by considering smaller values of the risk aversion parameter as the perturbed probabilities shift gradually from the uniform distribution towards a more concentrated one.

| AAPL | 0.7453 | 0.7348 | 0.7134 | 0.6929 | 0.6747 | 0.6588 | 0.645 |

| AMGN | 1.0872 | 1.1012 | 1.1158 | 1.1276 | 1.1367 | 1.144 | 1.1498 |

| AXP | 0.9862 | 0.9287 | 0.8918 | 0.8652 | 0.8445 | 0.8279 | 0.8141 |

| BA | 1.0219 | 1.044 | 1.0553 | 1.062 | 1.0663 | 1.0693 | 1.0714 |

| CAT | 0.8569 | 0.8017 | 0.7529 | 0.7114 | 0.6759 | 0.6453 | 0.6187 |

| CRM | 1.2519 | 1.1803 | 1.1313 | 1.0964 | 1.0702 | 1.0499 | 1.0336 |

| CSCO | 0.8064 | 0.722 | 0.6593 | 0.6116 | 0.5737 | 0.5429 | 0.5172 |

| CVX | 0.9013 | 0.9094 | 0.9068 | 0.901 | 0.8943 | 0.8876 | 0.8811 |

| DIS | 1.2187 | 1.2778 | 1.3191 | 1.3493 | 1.3726 | 1.3912 | 1.4063 |

| GS | 1.4248 | 1.4093 | 1.4099 | 1.417 | 1.4265 | 1.4368 | 1.4471 |

| HD | 0.9557 | 0.9862 | 1.0059 | 1.0205 | 1.0322 | 1.0418 | 1.05 |

| HON | 1.1175 | 1.0991 | 1.0868 | 1.0774 | 1.0698 | 1.0633 | 1.0578 |

| IBM | 0.7449 | 0.7532 | 0.7664 | 0.7799 | 0.7926 | 0.8042 | 0.8147 |

| INTC | 0.9239 | 0.9882 | 1.0397 | 1.0811 | 1.115 | 1.1435 | 1.1678 |

| JNJ | 0.7964 | 0.8415 | 0.8791 | 0.9095 | 0.9346 | 0.9557 | 0.9737 |

| JPM | 1.1035 | 1.0251 | 0.9752 | 0.9407 | 0.9153 | 0.8956 | 0.88 |

| KO | 0.9118 | 0.9982 | 1.0549 | 1.0946 | 1.1242 | 1.147 | 1.1653 |

| MCD | 0.586 | 0.6317 | 0.6667 | 0.6932 | 0.714 | 0.7307 | 0.7444 |

| MMM | 0.9247 | 0.9425 | 0.9568 | 0.9684 | 0.978 | 0.9861 | 0.9931 |

| MRK | 0.7537 | 0.8198 | 0.8673 | 0.9033 | 0.9318 | 0.955 | 0.9744 |

| MSFT | 0.888 | 0.935 | 0.9826 | 1.0253 | 1.0629 | 1.0959 | 1.125 |

| NKE | 0.7917 | 0.7521 | 0.7303 | 0.7165 | 0.7068 | 0.6997 | 0.6942 |

| PG | 0.8004 | 0.8593 | 0.9118 | 0.9564 | 0.9945 | 1.0272 | 1.0556 |

| TRV | 1.0165 | 1.0479 | 1.074 | 1.0955 | 1.1135 | 1.1288 | 1.142 |

| UNH | 0.9071 | 0.922 | 0.9268 | 0.9281 | 0.9281 | 0.9274 | 0.9264 |

| VZ | 0.6337 | 0.6496 | 0.6757 | 0.7015 | 0.7248 | 0.7457 | 0.7642 |

| WBA | 1.0009 | 1.0795 | 1.1458 | 1.202 | 1.2501 | 1.2917 | 1.3281 |

| WMT | 0.4818 | 0.5169 | 0.5526 | 0.5842 | 0.6116 | 0.6354 | 0.6561 |

The same experiment as in Table 4 is carried out for the period . We arrive at very similar observations as the movement of Hellinger-Beta values (based on deviations) are mostly monotonic as the risk aversion parameter is increased. The results are summarized in Table 5.

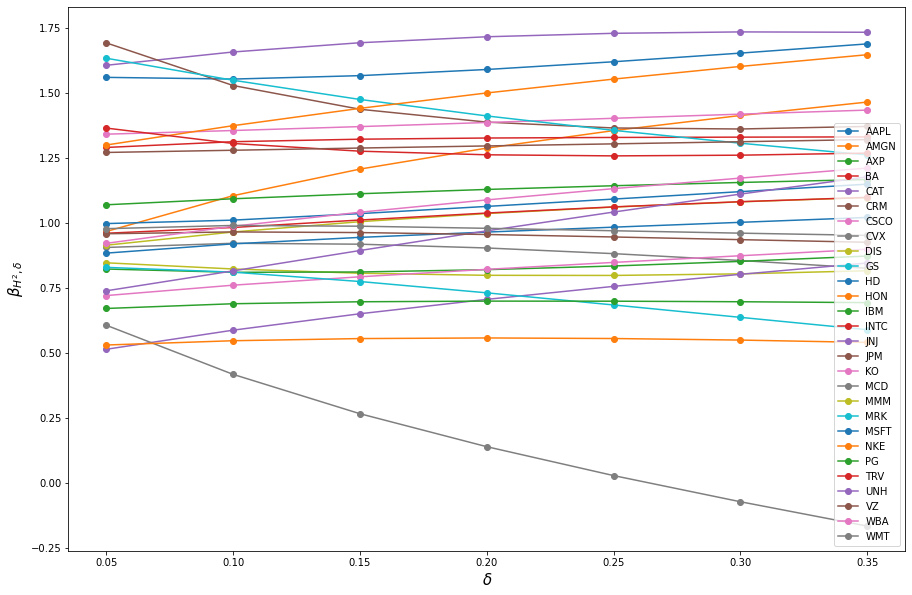

We also make the observation that while most reported Hellinger-Beta values are monotonic with respect to changing risk aversion parameters, the direction of movement can be different in 2013 from what is reported in 2006. Hence this indicates that meaningful hedging can be obtained by looking at the direction of Hellinger-Beta drifts, which adapts to stress scenarios under different market conditions in different time periods. Figure 3(a) (and 3(b)) demonstrates the general monotonic drift behavior of (deviation-based) Hellinger-Beta values for changing , reported respectively in Table 4 (and Table 5) for each stock in the year 2006 (and the year 2013). The risk aversion parameter is plotted on the x-axis in each panel, and the Hellinger-Beta values for each DOW 30 stock are plotted on the y-axis.

7 Extension to f-Drawdown Betas and Numerical Results

Similar to Ding and Uryasev [9], we can extend the f-Betas for a single path to a setting where the drawdown random variables are considered and the f-Beta would translate to f-Drawdown Beta defined as follows:

| (26) |

where the drawdown variables for the market index are defined as,

| (27) |

for each time step , with uncompounded cumulative returns of the market at time defined as,

Let denote the historic peak location in the previous definition for drawdowns, that is to say, . Then the change in cumulative returns in the market drawdown period defined at any given time for an individual asset is defined as,

| (28) |

The rest of the terms in (26) are defined similarly to those from previous f-Betas such as in (13). The proof for optimality conditions of drawdown type Betas is provided in Ding and Uryasev [9], Zabarankin et al. [33], and the optimality condition of f-divergence induced risk measures on drawdown observations can be obtained by considering the prior results in conjunction with general theories about deviation based Betas, see Rockafellar et al. [24]. While previous works on CDaR-Beta (Zabarankin et al. [33]) and ERoD-Beta (Ding and Uryasev [9]) are based on risk measures (applied to drawdown deviations) such as CVaR, our new approach uses the f-divergence induced risk measure which provides nicer properties and an intuitive interpretation from the point of view of distributional robustness.

Similar to Section 6, we performed several numerical experiments on f-Drawdown Betas, using the S&P 500 index as the optimal market portfolio. Only the results for DOW 30 stocks are presented for demonstration. In particular, the generating f-divergence is chosen to be the squared Hellinger distance, which gives the Hellinger-Drawdown Beta:

| (29) |

In the first experiment, consider the same two non-overlapping periods, Period 1 and Period 2, from Section 6. We reproduced the part of Table 3 corresponding to Drawdown Betas below in Table 6, but now introducing the column labeled that stands for Hellinger-Drawdown Beta calculated with . The results are shown in Table 6 for -Beta along with two other Drawdown Beta metrics: Beta and Beta. It can be seen that for some assets, the Hellinger risk measure offers different behaviors than CVaR-type risk measures on drawdown variables, but they also share some similarities on various assets. In addition, we report the Pearson correlation and Spearman correlation between the two columns of for Period 1 and Period 2 below:

Pearson Correlation: 0.469

Spearman Correlation: 0.284

| Period 1 | Period 2 | Period 1 | Period 2 | Period 1 | Period 2 | |

| AAPL | 0.316 | 0.834 | -0.986 | 1.126 | -0.796 | 1.207 |

| AMGN | -0.022 | 0.364 | -0.218 | 0.468 | -0.163 | 0.523 |

| AXP | 1.574 | 1.444 | 0.540 | 1.606 | 0.659 | 1.547 |

| BA | 1.429 | 2.797 | 1.332 | 1.277 | 1.376 | 1.342 |

| CAT | 1.243 | 0.975 | 0.558 | 1.892 | 0.626 | 1.868 |

| CRM | 0.132 | 0.714 | -1.438 | 0.154 | -1.268 | 0.207 |

| CSCO | 0.984 | 0.596 | 1.119 | 0.664 | 1.015 | 0.641 |

| CVX | 0.210 | 1.417 | -0.129 | 1.323 | -0.038 | 1.303 |

| DIS | 0.673 | 1.142 | 0.081 | 0.859 | 0.197 | 0.893 |

| GS | 0.867 | 1.315 | 0.640 | 1.956 | 0.564 | 1.896 |

| HD | 0.384 | 0.957 | -0.037 | 0.253 | 0.040 | 0.373 |

| HON | 0.993 | 1.100 | 0.768 | 0.967 | 0.830 | 1.015 |

| IBM | 0.146 | 1.212 | -0.410 | 1.986 | -0.337 | 1.901 |

| INTC | 0.639 | 0.763 | 0.317 | 0.405 | 0.323 | 0.386 |

| JNJ | 0.189 | 0.481 | -0.110 | 0.519 | -0.071 | 0.565 |

| JPM | 0.125 | 1.164 | -0.910 | 1.190 | -0.893 | 1.257 |

| KO | 0.265 | 0.962 | -0.227 | 0.356 | -0.108 | 0.400 |

| MCD | -0.240 | 0.706 | -0.903 | -0.478 | -0.787 | -0.366 |

| MMM | 0.829 | 0.616 | 0.585 | 1.145 | 0.588 | 1.154 |

| MRK | 0.877 | 0.302 | 0.727 | 0.359 | 0.854 | 0.394 |

| MSFT | 0.487 | 0.585 | -0.047 | -0.197 | -0.014 | -0.090 |

| NKE | 0.096 | 0.858 | -0.788 | -0.378 | -0.660 | -0.269 |

| PG | 0.378 | 0.384 | 0.152 | 0.107 | 0.201 | 0.159 |

| TRV | 0.016 | 0.858 | -0.511 | 0.551 | -0.415 | 0.593 |

| UNH | 0.956 | 0.723 | 0.685 | 0.180 | 0.842 | 0.245 |

| VZ | 0.451 | 0.260 | 0.414 | 0.285 | 0.542 | 0.289 |

| WBA | 0.526 | 0.284 | 0.223 | 0.856 | 0.320 | 0.848 |

| WMT | -0.409 | 0.106 | -0.916 | 1.007 | -0.884 | 0.976 |

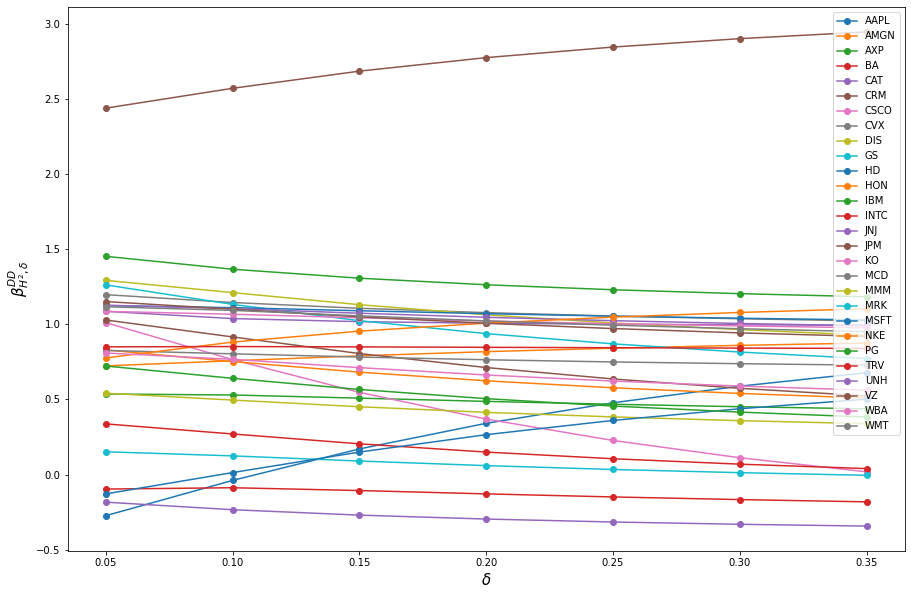

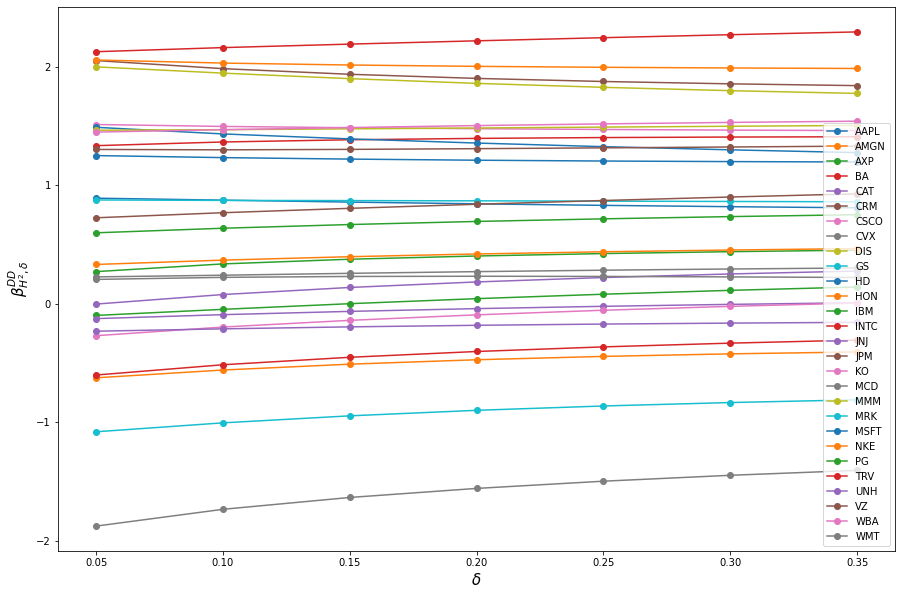

Similar to Table 5, we performed the risk level sensitivity test for Hellinger-Drawdown Beta in the year 2013 and the year 2022, which have quite different market drawdown behaviors in the S&P 500 index. Specifically, the year 2022 suffers from serious global financial instability as global markets were also impacted by fears of economic recession, resulting in large drawdowns in the S&P 500 index throughout the year. Similar to the observations we made with (deviation-based) Hellinger-Betas in Section 6, the Hellinger-Drawdown Betas for increasing risk aversion level tend to produce a monotonic shift relationship, which is indicative of the direction of correlation of the asset and the market in more and more extreme drawdown periods. Figure 4 demonstrates the general monotonic drift behavior of Hellinger-Drawdown Betas calculated with changing values for each of the DOW 30 stocks in the year 2013, as reported in Table 7, and the year 2022, as reported in Table 8. The risk aversion parameter is plotted on the x-axis in each panel, and the Hellinger-Beta values for each DOW 30 stock are plotted on the y-axis. The behavior of the values and drifts of Hellinger-Drawdown Betas is different in these two years, and this should be expected given the different market conditions in these two years. For instance, for the risk aversion parameters considered, the changes in Hellinger-Drawdown Betas in 2022 are less significant due to the market being in serious drawdown periods throughout the year.

| AAPL | -0.2736 | -0.0389 | 0.1706 | 0.3412 | 0.4779 | 0.5882 | 0.6781 |

| AMGN | 0.7235 | 0.7576 | 0.7901 | 0.818 | 0.8411 | 0.86 | 0.8756 |

| AXP | 0.5362 | 0.5296 | 0.5086 | 0.487 | 0.4679 | 0.4515 | 0.4378 |

| BA | -0.0965 | -0.0877 | -0.1064 | -0.1286 | -0.149 | -0.1666 | -0.1816 |

| CAT | 1.0864 | 1.0382 | 1.0177 | 1.0071 | 1.0008 | 0.9967 | 0.9939 |

| CRM | 2.4388 | 2.571 | 2.6852 | 2.7751 | 2.8455 | 2.9014 | 2.9463 |

| CSCO | 1.0111 | 0.7651 | 0.547 | 0.3693 | 0.2269 | 0.1119 | 0.0182 |

| CVX | 1.1974 | 1.1451 | 1.1067 | 1.0776 | 1.055 | 1.0371 | 1.0227 |

| DIS | 1.2926 | 1.2109 | 1.1307 | 1.0635 | 1.0088 | 0.9644 | 0.928 |

| GS | 1.2623 | 1.1326 | 1.0242 | 0.9381 | 0.87 | 0.8154 | 0.7713 |

| HD | 1.1244 | 1.1111 | 1.0903 | 1.0709 | 1.0543 | 1.0405 | 1.029 |

| HON | 0.8268 | 0.75 | 0.6801 | 0.6227 | 0.5765 | 0.5391 | 0.5086 |

| IBM | 1.4503 | 1.3647 | 1.3055 | 1.262 | 1.229 | 1.2033 | 1.1828 |

| INTC | 0.3372 | 0.2702 | 0.2046 | 0.1497 | 0.1052 | 0.0692 | 0.0397 |

| JNJ | 1.1276 | 1.1041 | 1.0739 | 1.0468 | 1.0242 | 1.0056 | 0.9902 |

| JPM | 1.0288 | 0.916 | 0.8055 | 0.7123 | 0.6362 | 0.5742 | 0.5234 |

| KO | 1.0862 | 1.067 | 1.0433 | 1.0221 | 1.0042 | 0.9894 | 0.9771 |

| MCD | 0.8262 | 0.8037 | 0.7821 | 0.7641 | 0.7497 | 0.7379 | 0.7283 |

| MMM | 0.5414 | 0.4959 | 0.4514 | 0.4141 | 0.3837 | 0.3589 | 0.3386 |

| MRK | 0.147 | 0.1191 | 0.0845 | 0.0534 | 0.0274 | 0.0059 | -0.0119 |

| MSFT | -0.1284 | 0.0132 | 0.1497 | 0.2655 | 0.3604 | 0.4381 | 0.502 |

| NKE | 0.7762 | 0.8818 | 0.9546 | 1.0077 | 1.0478 | 1.079 | 1.1038 |

| PG | 0.7226 | 0.6405 | 0.5664 | 0.5052 | 0.4558 | 0.4157 | 0.3829 |

| TRV | 0.8501 | 0.852 | 0.8498 | 0.847 | 0.8442 | 0.8419 | 0.8398 |

| UNH | -0.2243 | -0.281 | -0.3226 | -0.3534 | -0.3767 | -0.3948 | -0.4092 |

| VZ | 1.1515 | 1.1007 | 1.0499 | 1.0069 | 0.9717 | 0.943 | 0.9195 |

| WBA | 0.809 | 0.7669 | 0.7117 | 0.6628 | 0.6223 | 0.5891 | 0.5618 |

| WMT | 1.117 | 1.0928 | 1.0564 | 1.0228 | 0.9943 | 0.9706 | 0.951 |

| AAPL | 0.8916 | 0.8749 | 0.8586 | 0.8439 | 0.8309 | 0.8198 | 0.8104 |

| AMGN | -0.6252 | -0.5594 | -0.5101 | -0.4727 | -0.4444 | -0.4229 | -0.4068 |

| AXP | 0.2715 | 0.3366 | 0.3761 | 0.4034 | 0.4239 | 0.4399 | 0.4529 |

| BA | 1.3351 | 1.3661 | 1.3848 | 1.3964 | 1.4035 | 1.4078 | 1.4101 |

| CAT | -0.0025 | 0.0779 | 0.1377 | 0.1843 | 0.2215 | 0.2517 | 0.2765 |

| CRM | 2.0536 | 1.9853 | 1.9378 | 1.903 | 1.8769 | 1.8571 | 1.842 |

| CSCO | 1.5137 | 1.4975 | 1.4866 | 1.4783 | 1.4717 | 1.4665 | 1.4624 |

| CVX | -1.8773 | -1.7355 | -1.6356 | -1.5591 | -1.4982 | -1.4484 | -1.407 |

| DIS | 2.0005 | 1.9475 | 1.9009 | 1.8611 | 1.8276 | 1.7995 | 1.7762 |

| GS | 0.8766 | 0.8727 | 0.8712 | 0.8692 | 0.8666 | 0.8638 | 0.8612 |

| HD | 1.4899 | 1.4341 | 1.3922 | 1.3571 | 1.3266 | 1.2999 | 1.2764 |

| HON | 0.332 | 0.3685 | 0.3975 | 0.4205 | 0.4389 | 0.4538 | 0.4659 |

| IBM | -0.0984 | -0.047 | 0.0007 | 0.0432 | 0.0806 | 0.1133 | 0.1418 |

| INTC | 2.1284 | 2.1631 | 2.1925 | 2.2203 | 2.2468 | 2.272 | 2.2956 |

| JNJ | -0.1253 | -0.092 | -0.0643 | -0.041 | -0.0215 | -0.0051 | 0.0087 |

| JPM | 1.3031 | 1.2999 | 1.3036 | 1.3096 | 1.3166 | 1.3238 | 1.3313 |

| KO | -0.2696 | -0.1966 | -0.1399 | -0.0935 | -0.0547 | -0.0218 | 0.0062 |

| MCD | 0.227 | 0.2411 | 0.257 | 0.2713 | 0.2835 | 0.2937 | 0.3023 |

| MMM | 1.4654 | 1.4701 | 1.4769 | 1.4843 | 1.4918 | 1.4989 | 1.5056 |

| MRK | -1.0809 | -1.0056 | -0.9463 | -0.8997 | -0.8631 | -0.8341 | -0.8111 |

| MSFT | 1.2513 | 1.2341 | 1.2216 | 1.2122 | 1.2053 | 1.2005 | 1.1973 |

| NKE | 2.0585 | 2.0324 | 2.016 | 2.0047 | 1.9968 | 1.991 | 1.9868 |

| PG | 0.5992 | 0.6378 | 0.669 | 0.6951 | 0.7172 | 0.736 | 0.7521 |

| TRV | -0.6016 | -0.5149 | -0.4519 | -0.403 | -0.3641 | -0.3325 | -0.3067 |

| UNH | -0.2317 | -0.2117 | -0.195 | -0.1818 | -0.1714 | -0.1633 | -0.1568 |

| VZ | 0.7261 | 0.7689 | 0.8059 | 0.8402 | 0.872 | 0.9014 | 0.9283 |

| WBA | 1.4498 | 1.4697 | 1.4881 | 1.5046 | 1.5189 | 1.5313 | 1.5418 |

| WMT | 0.2057 | 0.223 | 0.2306 | 0.2324 | 0.2308 | 0.227 | 0.2219 |

8 Conclusions

This paper builds on using the class of f-divergence induced coherent risk measures [10] for portfolio optimization and derives its necessary optimality conditions formulated in the CAPM format. We derived a new f-Beta similar to the Standard Beta, CVaR Beta, and previous works in CDaR Beta [33] and ERoD Beta [9]. The f-Beta evaluates portfolio performance under an optimally perturbed market probability measure, and this family of Beta metrics gives various degrees of flexibility and interpretability. In particular, the choice of divergence-generating function controls the shape of the risk function, which dictates the sensitivity of the proposed Beta metric to changes in the risk aversion degree parameter . We conducted a numerical experiment using DOW 30 stocks returns against a chosen optimal market portfolio to demonstrate the new perspectives provided by Hellinger-Beta as compared with Standard Beta and Drawdown Betas, based on choosing the squared Hellinger distance to be the particular choice of f-divergence function in the general f-divergence induced risk measures and f-Betas. Our results show that the Hellinger-Betas (calculated based on deviations) provide different perspectives on the market from previous metrics such as CDaR Beta, ERoD Beta, and Standard Beta. For various choices of risk aversion parameter , the Beta values generally have a monotonic shift behavior which may indicate the positive or negative relation it has with the market when the market moves into more stressful scenarios. Such a relation can be useful for hedging purposes. Similar to risk measures on drawdown observations and related Beta metrics (Chekhlov et al. [6], Zabarankin et al. [33], Ding and Uryasev [9]), we can develop f-divergence induced drawdown risk measures and Drawdown Betas based on a chosen risk measure from a generating f-divergence function. This can be seen as a similar approach to CDaR Beta [33] and ERoD Beta [9] as proposed in earlier works, but now with the family of f-divergence induced risk measures providing more flexibility and richer risk aversion behaviors than the CVaR risk measures. Similarly, we provided numerical results for Hellinger-Drawdown Beta by choosing the squared Hellinger distance to be the generating f-divergence.

Future works include studying the impact of the choice of f-divergences on the resulting Beta metric. Based on their statistical properties, the squared Hellinger distance is chosen in this study to demonstrate the behavior of the family of f-divergences since they provide bounds for meaningful statistical estimation and have various desirable properties, such as being symmetric and bounded. However, a comparison with other choices of f-divergence functions (and their induced risk measures for the CAPM setting) will reveal further insights into how the shape of the risk function impacts the sensitivity of the resulting f-Beta metrics. In particular, we can study if there is an overarching optimization framework under which the choice of in the family of -divergences can be jointly optimized under some criteria. The relation between f-divergence induced risk measures and CVaR risks from the spectral risk measure point of view also suggests that we can compare and understand f-Betas and CVaR Betas in a more systematic way. In recent work, Frohlich and Williamson [12] proposed a general framework to construct specific divergence-induced risk measures that exhibit a desired tail sensitivity. Consequently, this result can be potentially used in our framework to obtain f-Betas that have a more explainable and controlled risk aversion behavior. Another interesting future work would be to quantify the incremental changes in the f-Beta values as the risk aversion parameter increases and use the generated marginal increment/decrement as a measure of directional movement between the asset and the market. This can be a more useful metric for hedging purposes under higher-stress situations. Finally, we propose to study further the behaviors of f-Drawdown Betas as compared with other drawdown-based Betas and quantify their incremental changes with respect to risk aversion parameter changes as well.

Data Availability Statement

Data for the case study were downloaded from Yahoo Finance https://finance.yahoo.com/.

Acknowledgements

The author thanks Dr. Andrew Mullhaupt (Stony Brook University), Dr. Stan Uryasev (Stony Brook University), Dr. Michael Albert (University of Virginia), and anonymous reviewers for valuable discussions and comments.

References

- Ahmadi-Javid [2012] A. Ahmadi-Javid, 2012. Entropic Value-at-Risk: A New Coherent Risk Measure, J. Optim. Theory Appl., 155(3), pp. 1105–1123.

- Ahmadi-Javid and Fallah-Tafti [2019] A. Ahmadi-Javid and M. Fallah-Tafti, 2019. Portfolio Optimization with Entropic Value-at-Risk, Eur. J. Oper. Res., 279(1), pp. 225-241,

- Baghdadabad et al. [2013] M. R. T. Baghdadabad, F. M. Nor, and I. Ibrahim, 2013. Mean-Drawdown Risk Behavior: Drawdown Risk and Capital Asset Pricing, J. Bus. Econ. Manag., 14, pp. S447-S469.

- Belousov and Peters [2018] B. Belousov and J. Peters, 2018. f-Divergence Constrained Policy Improvement, arXiv:1801.00056.

- Chekhlov et al. [2003] A. Chekhlov, S. Uryasev, and M. Zabarankin, 2003. Portfolio Optimization with Drawdown Constraints, B. Scherer (Ed.) Asset and Liability Management Tools, Risk Books, London.

- Chekhlov et al. [2005] A. Chekhlov, S. Uryasev, and M. Zabarankin, 2005. Drawdown Measure in Portfolio Optimization, Int. J. Theor. Appl. Finance, 8, pp. 13-58.

- Cichocki and Amari [2010] A. Cichocki and S. Amari, 2010. Families of Alpha- Beta- and Gamma- Divergences: Flexible and Robust Measures of Similarities, Entropy, 12, pp. 1532-1568.

- Ding and Uryasev [2020] R. Ding and S. Uryasev, 2020. CoCDaR and mCoCDaR: New Approach for Measurement of Systemic Risk Contributions, J. Risk. Financial. Manag., 13, pp. 270-287.

- Ding and Uryasev [2022] R. Ding and S. Uryasev, 2022. Drawdown Beta and Portfolio Optimization, Quantitative Finance, 22(7), pp. 1265-1276.

- Dommel and Pichler [2020] P. Dommel and A. Pichler, 2020. Convex Risk Measures based on Divergence, arXiv:2003.07648.

- Drawdown Beta Website [2021] Drawdown Beta Website, 2021. http://qfdb.ams.stonybrook.edu/index_SP.html, Quantitative Finance Program at Stony Brook University.

- Frohlich and Williamson [2022] C. Fröhlich and R. C. Williamson, 2022. Tailoring to the Tails: Risk Measures for Fine-Grained Tail Sensitivity, arXiv:2208.03066.

- Galagedera [2004] D. Galagedera, 2007. A Review of Capital Asset Pricing Model, Managerial Finance, 33, pp. 821-832.

- Goldberg and Mahmoud [2017] L. R. Goldberg and O. Mahmoud, 2017. Drawdown: from Practice to Theory and Back Again, Math. Finan. Econ., 11, pp. 275–297.

- Krokhmal et al. [2011] P. Krokhmal, M. Zabarankin, and S. Uryasev, 2011. Modeling and Optimization of Risk, Surv. Oper. Res. Manag. Sci., 16, pp. 49-66.

- Kullback and Leibler [1951] S. Kulllback and R. A. Leibler, 1951. On Information and Sufficiency, Ann. Math. Statistics, 22(1), pp. 79-86, 3.

- Markowitz [1959] H. M. Markowitz, 1959. Portfolio Selection: Efficient Diversification of Investments, Yale University Press.

- Markowitz [1991] H. M. Markowitz, 1991. Foundations of Portfolio Theory, J. Finance, 46, pp. 469-477.

- Mullhaupt [2022] A. Mullhaupt, 2022. Personal communications.

- Nowozin et al. [2016] S. Nowozin, B. Cseke, and R. Tomioka, f-GAN: Training Generative Neural Samplers using Variational Divergence Minimization, arXiv:1606.00709, 2016.

- Rockafellar and Uryasev [2000] R. T. Rockafellar and S. Uryasev, Optimization of Conditional Value-at-Risk, J. Risk, 2 (2000), pp. 21-42.

- Rockafellar and Uryasev [2002] R. T. Rockafellar and S. Uryasev, Conditional Value-at-Risk for General Loss Distributions, J. Bank. Finance, 26 (2002), pp. 1443-1471.

- Rockafellar et al. [2002] R. T. Rockafellar, S. Uryasev, and M. Zabarankin, 2002. Deviation Measures in Risk Analysis and Optimization, SSRN Electronic Journal, 10.2139/ssrn.365640.

- Rockafellar et al. [2006] R. T. Rockafellar, S. Uryasev, and M. Zabarankin, 2006. Optimality Conditions in Portfolio Analysis with Generalized Deviation Measures, Math. Program., 108, pp. 515-540.

- Rockafellar and Uryasev [2014] R. T. Rockafellar and S. Uryasev, 2013. The Fundamental Risk Quadrangle in Risk Management, Optimization and Statistical Estimation, Surv. Oper. Res. Manag. Sci., 18, pp. 33-53.

- Rockafellar et al. [2014] R. T. Rockafellar, O. R. Johannes, and S. I. Miranda, 2014. Superquantile Regression with Applications to Buffered Reliability, Uncertainty Quantification and Conditional Value-at-Risk, European J. Oper. Res., 234, pp. 140-154.

- Rossi [2016] M. Rossi, 2016. The Capital Asset Pricing Model: A Critical Literature Review, Glob. Bus. Econ. Rev., 18, pp. 604.

- Ruszczynski [2011] A. Ruszczynski, 2011. Nonlinear Optimization, Princeton University Press.

- Sharpe [1964] W. F. Sharpe, 1964. Capital Asset Prices: A Theory of Market Equilibrium under Condition of Risk, J. Finance, 19, pp. 425-442.

- Sharpe [1992] W. F. Sharpe, 1992. Asset allocation: Management Style and Performance Measurement, J. Portf. Manag., 18, pp. 7-19.

- Testuri and Uryasev [2004] C. Testuri and S. Uryasev, 2004. On Relation Between Expected Regret and Conditional Value at Risk, S. Rachev (Ed.) Handbook of Computational and Numerical Methods in Finance, Birkhauser, pp. 361-373.

- Yang and Le Cam [2000] G. L. Yang and L. Le Cam, 2000. Asymptotics in Statistics: Some Basic Concepts, Berlin: Springer.

- Zabarankin et al. [2014] M. Zabarankin, P. Konstantin, and S. Uryasev, 2014. Capital Asset Pricing Model (CAPM) with Drawdown Measure, European J. Oper. Res., 234, pp. 508-517.