An Axiomatic Characterization of CFMMs and Equivalence to Prediction Markets

Abstract.

Constant-function market makers (CFMMs), such as Uniswap, are automated exchanges offering trades among a set of assets. We study their technical relationship to another class of automated market makers, cost-function prediction markets. We first introduce axioms for market makers and show that CFMMs with concave potential functions characterize “good” market makers according to these axioms. We then show that every such CFMM on assets is equivalent to a cost-function prediction market for events with outcomes. Our construction directly converts a CFMM into a prediction market and vice versa.

Conceptually, our results show that desirable market-making axioms are equivalent to desirable information-elicitation axioms, i.e., markets are good at facilitating trade if and only if they are good at revealing beliefs. For example, we show that every CFMM implicitly defines a proper scoring rule for eliciting beliefs; the scoring rule for Uniswap is unusual, but known. From a technical standpoint, our results show how tools for prediction markets and CFMMs can interoperate. We illustrate this interoperability by showing how liquidity strategies from both literatures transfer to the other, yielding new market designs.

1. Introduction

A prediction market is designed to elicit forecasts, such as for elections or sporting events. Participants trade shares in securities, each tied to one of the possible outcomes, paying out $1 if that outcome occurs; the prices form a probability distribution over the outcomes representing an aggregate belief. To resolve thin market problems, Hanson (2003) and Chen and Pennock (2007) propose introducing automated market makers, mechanisms that offers to buy or sell any number of securities, with prices determined by the past history of transactions. A significant amount of research has investigated the design of such markets based on convex cost functions (Abernethy et al., 2013; Frongillo and Waggoner, 2018). To acquire a bundle of securities , the trader pays cash to the market maker, where is the total numbers of securities sold so far. A prominent example is the log market scoring rule (LMSR) due to Hanson (2003), given by for a liquidity parameter .

More recently, inspired by blockchain applications, there has been significant theoretical and practical interest in the design of decentralized financial markets (Capponi and Jia, 2021; Angeris et al., 2022). These markets allow trade between assets without a fixed unit of exchange (“cash”). Interestingly, like prediction markets, many decentralized exchanges also employ automated market makers, but for different reasons: automated market makers tend to have lower on-chain implementation costs than traditional order books (Jensen et al., 2021, §4.1). The dominant paradigm is the constant-function market maker (CFMM) based on a concave potential function . Here, if is the amount of market maker holdings or “reserves” in the assets, then a trade is accepted if , i.e., it keeps the potential function constant. One of the most popular CFMMs is Uniswap where .

Despite clear similarities between these two settings, prior work has considered prediction markets to be only analogous to CFMMs, but not technically related.111To give two examples, Angeris and Chitra (2020, §3.2) argue that the two market makers can diverge, and Bichuch and Feinstein (2022) state the following: “In a separate context, [automated market makers] for prediction markets were first proposed in (Hanson, 2003). Such a structure is fundamentally different from the constant function market makers considered herein insofar as a prediction market includes a terminal time at which bets are realized.” Indeed, there are obvious differences between the settings: prediction markets rely on “cash”, while CFMMs do not require a special unit of account; prediction markets only offer certain types of outcome-dependent securities (and can manufacture as many of these as they want), while CFMMs deal in arbitrary assets in limited supply; and so on. Furthermore, the goals of the two types of markets are very different: prediction markets seek to elicit information, whereas CFMMs seek to facilitate trade.

Nonetheless, we show a tight technical equivalence between prediction markets and CFMMs. We give straightforward reductions to transform a cost function for a prediction market into a potential function for a CFMM, and vice versa. The reductions give one-to-one correspondence between trades placed in both markets, while preserving the relevant market properties. An important implication is that markets designed to elicit information are also good at facilitating trade, and vice versa. We illustrate our results with several examples; among them, the prediction market equivalent to Uniswap, a new homogeneous CFMM from LMSR (Figure 1), and a close connection between Brier score and a hybrid CFMM. We hope our results can inspire new market designs and insights in both literatures.

1.1. Outline of results

We begin in § 2 with an axiomatic characterization of the class of constant-function market makers (CFMMs) of interest in this paper. Focusing on “vanilla” CFMMs that do not adapt liquidity, we show in Proposition 4 that an automated market maker satisfies a certain set of baseline axioms if and only if it can be represented by a CFMM with a concave, increasing . This result assumes the initial reserves are fixed; we give a similar result in Theorem 5 allowing any initial reserves where is quasiconcave and continuous.

We give our main equivalence in § 3. We first recall that cost-function prediction markets, where satisfies certain criteria, have been characterized by prior work as automated market makers satisfying a path independence axiom and an incentive-compatibility axiom (see Fact 1). We give a reduction from any such to a concave, increasing , resulting in a CFMM that satisfies desirable market-making axioms (Theorem 3). Then, we give a reduction from any concave, increasing to a convex satisfying the criteria, resulting in a prediction market with desirable incentive-compatibility axioms (Theorem 4). The conceptual implication is that design for good information-elicitation properties results in good market-making properties, and vice versa. In fact, an immediate corollary is that any CFMM defines a proper scoring rule, a function for eliciting truthful predictions (Corollary 5).

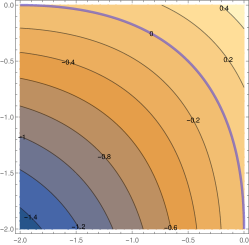

Our equivalence above is not fully satisfying in some cases, however, because for some initial conditions the resulting CFMMs can run out of their reserves. In § 4, we begin by characterizing markets that keep their reserves nonnegative in addition to our previous axioms. We then give a more sophisticated reserves-aware reduction from prediction markets to CFMMs, using the perspective transform technique from convex analysis. The result is a CFMM whose level sets are not parallel, as are those of cost functions (Figure 1(L)), but instead “stretched”, with curvature adapting to the amount of reserves available (Figure 1(M)). We show that every 1-homogeneous (scale-symmetric) potential function, the dominant CFMM design in practice, can be obtained via our construction.

We conclude in § 5 with a discussion of other practical considerations, mainly liquidity adaptation. In applications, CFMMs are designed to allow the reserves to grow (e.g. by lending), and the liquidity provided should grow as well (Angeris et al., 2020). Similarly, prediction-market research has studied how to automatically grow and adapt the liquidity of the market over time, again using the perspective transform (Abernethy et al., 2014). We begin an investigation of how these lines of research can inform each other.

1.2. Equivalence in a nutshell

Let us give the key intuition for our equivalence. First, to convert a prediction market into a CFMM, suppose we have cost function . We will turn it into a rule for pricing any set of assets, without money. Observe that a unit of cash is equivalent to the “grand bundle”, represented as the all-ones vector , containing one share of each security: exactly one of them will pay off $1, and the rest $0, so the grand bundle is worth exactly $1. We can therefore simulate transactions in a prediction market with only the assets (securities) and no cash: a trade of in exchange for units of cash can be expressed as the combined trade .

We can now simply set and, perhaps surprisingly, obtain a CFMM where valid trades are equivalent to those allowed by the original cost function. The negations resolve a difference in sign conventions (i.e., whether is interpreted as a gain or loss) and convert the convex to a concave . We will show that concavity is equivalent to the desirable trading axiom of demand responsiveness; and also satisfies other nice trading axioms, like liquidation: the trader can purchase any bundle of assets for some amount of any given asset. Perhaps surprisingly, these and other market-making axioms come “for free”, as long as is a good prediction-market cost function. One important exception is that ideally CFMMs do not deplete their reserves. As described above, we will fix this issue with a more sophisticated construction based on the perspective transform that guarantees nonnegative reserves. Figure 1 illustrates that construction applied to LMSR.

In the other direction, one can turn any CFMM into a prediction market with good elicitation properties. Given a CFMM with potential function , we show that it has an equivalent cost function defined as follows: Let for the constant satisfying where is the vector of initial reserves and again is grand bundle (the all-ones vector). For example, as we recover in § 3.5, the following cost function is equivalent to Uniswap when the initial reserves satisfy ,

| (1) |

In fact, by standard prediction market facts, this general result implies that every “good” CFMM can be converted into a proper scoring rule (Gneiting and Raftery, 2007); we derive the scoring rule for Uniswap in § 3.5.

1.3. Related work

The literature on CFMMs contains several axiomatic results in a spirit related to our work in §2, e.g. Angeris and Chitra (2020); Bichuch and Feinstein (2022); Schlegel et al. (2022). For example, Bichuch and Feinstein (2022) characterize the set of “ideal” CFMMs from among the class of all CFMMs and Schlegel et al. (2022) axiomatically characterize some sub-classes of CFMMs. A major difference between our axiomatic results in § 2 and the above works is that we do not take the structure of CFMMs as given, for example, existence of a potential/utility function or its concavity. We derive these attributes from the axioms directly.

Several authors have noted pieces of the equivalence we present. Most technically related is Chen and Pennock (2007), which proposes the constant-utility market maker for prediction markets. Their market maker accepts trades that, according to some subjective fixed belief (probability distribution) and risk-averse utility function, maintain its expected utility at a constant value. Intriguingly, they observe in their eq. (14) that such a market maker with log utility is equivalent to a cost function of the form (1), which turns out to be the result of our conversion of Uniswap to a prediction market; see § 3.5. We emphasize that Chen and Pennock (2007), unlike the current paper, focused only on prediction markets, i.e. do not show how to use their market maker for more general classes of assets. Within the prediction market context, they also only give equivalences to a certain class of cost functions, those corresponding to weighted pseudo-spherical scoring rules.

Other works have specifically connected market makers from decentralized finance and prediction markets. For example, Paradigm (2021) discusses how to apply the functional format of the LMSR as a potential function in a CFMM. Similarly, Manifold (2022) and Gnosis (2020) apply Uniswap to the case where assets are contingent securities, obtaining a prediction market. Such works can be described as applying a functional form from one context to a different context, without justifying why they will perform well in the new context. In contrast, this work shows how to convert any cost function to a CFMM and vice versa via a reduction that guarantees to preserve axiomatic properties of the original.

Other technical tools come from the prediction market literature. We rely specifically the cost-function market formulation (Chen and Pennock, 2007; Abernethy et al., 2013), axiomatic approaches to prediction markets (Abernethy et al., 2013, 2014; Frongillo and Waggoner, 2018), and the duality between prediction markets and scoring rules (Hanson, 2003; Abernethy et al., 2014). We also make use of constructions from the literature on financial risk measures, specifically obtaining a convex risk measure from a set of “acceptable” positions (Föllmer and Schied, 2008; Föllmer and Weber, 2015); the connection between risk measures and prediction markets has been noted several times (Chen and Vaughan, 2010; Agrawal et al., 2011; Frongillo and Reid, 2015).

1.4. Notation

Vectors are denoted in bold, e.g. . The all-zeros vector is and the all-ones vector is . The vector , i.e. all-zero except for a one in the position.

Comparison between vectors is pointwise, e.g. if for all , and similarly for . We say when for all and . Define , , et cetera.

Let . We will use the following conditions.

-

•

increasing: for all with .

-

•

convex: , .

-

•

concave: is convex.

-

•

quasiconcave: , the set is convex.

-

•

-invariant: for all , .

-

•

1-homogeneous (on ): for all and .

Given a list of vectors, e.g. , the sum is denoted . Concatenation of a new trade onto a history is denoted .

2. A Characterization of Fixed-Liquidity CFMMs

To lay a foundation, we consider market makers that have “fixed liquidity”: they do not accept loans nor charge transaction fees. The fixed-liquidity case allows for a simple, universal characterization: if one wants an automated market to satisfy certain natural axioms, it must be a CFMM as we show in Theorem 5.

2.1. Automated market makers for general asset markets

We consider automated market makers that process trades sequentially. There are assets . A trade or bundle represents net units of each asset being given to the market maker by a trader. A positive represents a net transfer from the trader to the market maker, and negative represents a net transfer from the market maker to the trader. A history is an ordered list of trades. The empty history is denoted .

A market maker is defined by a function that specifies, for any valid history , the set of valid trades that it is willing to accept from the next participant. For each arriving participant :

-

•

The current market history is .

-

•

The valid trades are given by .

-

•

Participant selects some trade .

-

•

The market history is now .

The market maker begins with some initial reserves . It will be convenient to include the initial reserves in the history, so in the above we would have . At any history , we define the notation

meaning the current reserves are equal to the sum of the trades in the history.

Given a market maker defined by and a history , we let denote the valid histories extending , i.e. all valid histories with as a prefix. Formally, is the smallest set containing such that, for all and all , we have . In particular, may be interpreted as the set of valid initial reserves for this market maker, and the set of valid histories. However, we abuse notation slightly in that is defined not to include itself, i.e. it only includes nonempty histories.

Examples and CFMMs.

The simplest example of an automated market maker is when is a constant set that does not depend on . Such a market maker would offer a fixed exchange rate between assets. However, we would like the exchange rates to adapt depending on demand. In the context of decentralized finance, a common approach is the following.

Definition 0 (CFMM).

A constant-function market maker (CFMM) is a market such that

for some function , called the potential function.

In a CFMM, the market maker accepts any trade keeping the potential of its reserves constant. Some common examples are Uniswap or the constant product market where , and its generalization Balancer or constant geometric mean market which has with .

2.2. Axioms

An axiom is a potentially desirable property for a market maker as defined by . We begin with a few intuitive axioms.

Axiom 1 (NoDominatedTrades).

For all , does not contain any dominated trade, i.e. an where, for some , we have .

Assuming all assets have nonnegative value, a rational trader would never select a dominated trade. Conversely, as typically , meaning a trader can chose not trade altogether, then under NoDominatedTrades no trader can take assets from the market maker without giving something in return. This latter property is the typical condition of no-arbitrage (within the system) in the finance literature.

Axiom 2 (PathIndependence).

For all , for all and , we have that .

PathIndependence ensures that a trader cannot profit by splitting a single large trade into two smaller sequential trades instead. By backward induction, it implies that any sequence of trades can just as well be made in a single bundle: if is a valid history, we must have .

Observation 1.

PathIndependence implies the following inductive version: for all and all , we have .

Axiom 3 (Liquidation).

For all and all , there exists such that .

In other words, a participant can supply any nonnegative bundle and specify a nonnegative demand bundle , and receive some multiple of in return for . The Liquidation axiom captures the point of a “market maker”, i.e., to offer to trade at some exhange rate between any pair of assets (or more generally, bundles).

Any market satisfying Liquidation and NoDominatedTrades must in particular offer the option to trade nothing; to see this set for any nontrivial bundle .

Observation 2.

Liquidation and NoDominatedTrades imply for all . Furthermore, any can be written where and satisfy .

Axiom 4 (DemandResponsiveness).

For all , if for some , and if there exist such that , then .

In other words, if a participant supplies in return for once, then the “exchange rate” should increase the second time in a row: more of is needed to buy a corresponding amount of .

2.3. Characterization of fixed-liquidity CFMMs

In this subsection we characterize automated market makers that satisfy the axioms above: CFMMs with increasing, concave potential functions. In addition to setting the stage for the equivalence with prediction markets, this result places limits on the design space of automated market makers, or at least shows what axioms must be relinquished to move beyond the concave-CFMM framework. We first prove that Liquidation, NoDominatedTrades, and PathIndependence already imply the market can be implemented as a CFMM for some potential function . DemandResponsiveness then gives concavity. Finally, we extend these results from fixed initial market reserves to show that, when considering multiple initial reserves, the market is still without loss of generality a CFMM for some quasiconcave potential.

Lemma 0.

Fix the initial reserves . If a market maker with satisfies Liquidation, NoDominatedTrades, and PathIndependence, then it is a CFMM for some potential function .

The key point of the proof is that there is a fixed set of reachable states of the market , and any of these is always reachable in a single trade regardless of the history. We can then define to vanish exactly on that set.

Proof.

Let be any valid history with initial reserves . We first prove that , by induction on the length of . The base case is immediate. For the inductive step, let and consider a trade . We show .

() Let . By Observation 1, .

() Let be some trade such that . By NoDominatedTrades, we must have , as otherwise would dominate or vice versa. By Liquidation, for some , . We will show , implying . By Observation 1, . If , this trade is dominated by or dominates . Therefore, by NoDominatedTrades, .

Now we show the market is a CFMM. Define , the set of valid reserves after a single trade. We proved above that , which holds if and only if . Therefore, we can choose any potential function with as a level set, e.g. if and otherwise. ∎

In the proof of Lemma 2, consists of the level set containing , i.e. the set of valid reserves the market is willing to maintain starting from . In general, given a function and initial reserves , it will be useful to define the following notation:

Here, consists intuitively of valid reserves, plus all reserves that are weakly preferred by the market maker to some valid reserve. The key geometrical point is that, under DemandResponsiveness, is a convex set:

Lemma 0.

Fix the initial reserves . If a market maker with satisfies Liquidation, NoDominatedTrades, PathIndependence, and DemandResponsiveness, then it is a CFMM for some potential and, furthermore, is a convex set.

The proof of Lemma 3, as well as the rest of the claims in this section, can be found in Appendix A. We obtain that, for a fixed initial starting point, a market maker satisfying our axioms can always be implemented as a CFMM with a concave potential.

Proposition 0.

Fix the initial reserves . A market maker with satisfies Liquidation, NoDominatedTrades, PathIndependence, and DemandResponsiveness if and only if it can be implemented as a CFMM with an increasing, concave potential function .

If the market maker has multiple initial feasible reserves, then the market initiated from each one can be implemented as a CFMM with a concave potential. But it is not clear that there is a single concave potential function that implements all of these markets simultaneously. However, there at least exists a single quasiconcave potential function that implements the entire market as a CFMM simultaneously. This statement holds as long as we assume the slightly stronger axiom of StrongPathIndependence, which enforces a relationship between the market when starting at different initial reserves.

Axiom 5 (StrongPathIndependence).

For all with , we have . Furthermore, we have for all .

Theorem 5.

A market maker, with , satisfies Liquidation, NoDominatedTrades, StrongPathIndependence, and DemandResponsiveness if and only if it is a CFMM with an increasing, continuous, quasiconcave potential function .

As the potential functions in Proposition 4 are concave rather than continuous and quasiconcave, a weaker condition, one might ask whether this weaker condition is necessary in Theorem 5. We conjecture that the answer is yes, in the sense that there are CFMMs with continuous, quasiconcave potential functions which cannot be “concavified” by any monotone transformation; see e.g. Fenchel (1953); Connell and Rasmusen (2017).

3. Equivalence of CFMMs and Prediction Markets

The goal of CFMMs is to facilitate trade. In contrast, a prediction market is designed to to elicit and aggregate information about future events. We will now see that prediction markets (satisfying good elicitation axioms) are in a very strong sense equivalent to CFMMs (satisfying good trade axioms). We give direct reductions to convert each into the other. As a consequence, much existing research on design and properties of prediction markets can now transfer to CFMMs.

In § 3.1, we define cost function prediction markets and recall that they characterize automated market makers satisfying elicitation axioms. In § 3.2, we take the key step of converting them into “cashless prediction markets”. In § 3.3, we give the reductions and equivalence between prediction markets and CFMMs. § 3.4 discusses information-elicitation consequences, and § 3.5 gives examples.

3.1. Cost function prediction markets

To begin, let us briefly review prediction markets for Arrow–Debreu (AD) securities, which are designed to elicit a full probability distribution over a future event. Formally, let be a set of outcomes, and let be the future event, a random variable taking values in . For example, in a tournament with teams, can be the winner of the tournament, and is the outcome where team wins. The probability simplex on is denoted . The AD prediction market is a market with assets . When the outcome of is observed, each unit of pays off to the owner one unit of cash (some fixed currency, such as US dollars) if , and pays off zero otherwise.222In more general prediction markets than the Arrow–Debreu case described here, there can be any number of assets that each pay off according to an arbitrary function of . We allow traders to both buy and sell assets, including holding negative amounts, representing a short position.

By design, a trader’s fair price for is therefore the probability according to their belief. The current market prices for form a “consensus” prediction in the form of a probability distribution over .

A priori, as with general asset markets, it may seem that the valid trades and associated prices at each moment can be set in essentially any manner whatsoever. It may therefore be surprising that, in order to successfully elicit and aggregate information while maintaining path independence, a market for contingent securities must take the form of a cost-function market maker, as we define next. We then sketch the proof of this well-known characterization in Fact 1.

The classic cost-function market maker for Arrow–Debreu securities, slightly generalized for our setting, operates as follows.

Definition 0.

Let be convex, increasing, and -invariant. Let be an initial state. The AD market maker defined by , with initial state , operates as follows. At round

-

•

A trader can request any bundle of securities .

-

•

The market state updates to .

-

•

The trader pays the market maker in cash.

After an outcome of the form occurs, for each round , the trader responsible for the trade is paid in cash, i.e. the number of shares purchased in outcome .

When is differentiable, the instantaneous prices of the securities are given by . That is, the approximate cost of any bundle is given by . (The exact cost is given by integrating this trade from zero to , resulting in .) We can therefore regard as the market prediction. Because of -invariance, is always a probability distribution.

We can cast cost-function market makers as a special case of the automated market maker framework in § 2. Specifically, represent cash by an asset , and consider the assets . Then we can restate Definition 1 as the following asset market over . An important convention is that prediction markets interpret states and trades as net transfers to the trader, whereas our automated market maker follows the CFMM convention to interpret and as net amounts for the market maker. Therefore, a negative sign is always required to translate between the settings.

-

•

The initial reserves are .

-

•

Define .

In other words, consists of any bundle of securities to be sold, along with a payment in cash of . As mentioned, the input to is negated because expects as an argument the net bundle the market has sold rather than purchased.

A priori, the design space for prediction markets could include any automated market maker over any set of contingent securities. From this perspective, it is perhaps surprising that, to achieve “good” elicitation of predictions according to a standard set of axioms, one must use a cost-function market maker. That is, the following is known:

Fact 1 ((Frongillo and Waggoner, 2018; Abernethy et al., 2013)).

Let be any automated market maker offering contingent securities for cash and satisfying these axioms: (1) Path Independence; (2) Incentive Compatibility for predicting , in the sense that: (2a) Any history of the market defines a probability distribution over (the “market prediction”), and (2b) All possible predictions are achievable by some history, and (2c) A trader maximizes expected net payment by moving the market prediction match their belief . Then is a cost-function AD prediction market.

Fact 1 is essentially a characterization: any cost-function AD prediction market satisfies the above axioms, if is also differentiable with a certain set of gradients (Abernethy et al., 2013). For completeness, Appendix B includes a sketch of a proof. The key ideas, synthesized from (Frongillo and Waggoner, 2018; Abernethy et al., 2013), are these: Incentive Compatibility requires the market to use proper scoring rules, functions that induce truthful forecasts from individual experts (see Section 3.4). Path Independence then implies that market must use “chained” scoring rules as proposed by (Hanson, 2003). Finally, it is known that Hanson’s scoring-rule markets are equivalent to cost function based prediction markets via convex duality (Abernethy et al., 2013).

3.2. Cashless prediction markets

A key step to translating between prediction markets and CFMMs is this observation: without loss of generality, an AD prediction market can drop cash from its assets . Because exactly one of the outcomes of will occur, the “grand bundle” of securities is worth exactly one unit of cash to all traders; whichever outcome occurs, the th security will pay out one unit of cash and the rest will pay out zero.

Specifically, we can define a “cashless prediction market” for any cost function by taking a demand bundle which would have had a price , and subtracting units of each security, becoming the bundle . By -invariance, the cost of this new trade must be zero, eliminating the need for cash. With the negative sign to convert to the automated market maker framework, define for any cost function :

| (2) |

In Appendix C, we show the equivalence of and in more formality. The key step is the following lemma, which will be useful for converting to a CFMM:

Lemma 0.

.

Proof.

Let , and write with . Using ones-invariance, . Conversely, let be such that . Then, directly, , where we observe . ∎

3.3. Equivalence between CFMMs and prediction markets

We now show that, in a strong sense, CFMMs and AD cost-function market makers are equivalent. Specifically, every “good” prediction market mechanism for events on outcomes defines, in a straightforward manner, a “good” CFMM on assets; and vice versa. Here, a “good” prediction market is one that satisfies the elicitation axioms we introduced in Subsection 2.2, i.e. a cost-function market. A “good” CFMM is one that satisfies the trading axioms, i.e. is defined by a concave, increasing . Recall that is the market maker defined by the CFMM for , i.e. . Recall that was defined in Equation 2.

Theorem 3.

Let define an AD cost-function prediction market. Then the function defined by

is concave and increasing, i.e. defines a CFMM. Furthermore, .

Proof.

As is the negative of a convex function, it is concave. Because is increasing, is increasing. By Lemma 2, . ∎

Theorem 4.

Let be concave and increasing, defining a CFMM. For any , the function defined by

| (3) |

is convex, increasing, and ones-invariant, i.e., defines an AD cost-function prediction market. Furthermore, for all , we have .

Proof.

The key observations come from the financial risk-measure literature, specifically “constant-risk” market makers (Frongillo and Reid, 2015, §2.1) (Chen and Pennock, 2007) and standard constructions extending convex functions to be ones-invariant (Föllmer and Weber, 2015). Specifically, is increasing because is increasing, and ones-invariant immediately by construction. We observe that the infimum is always achieved because , a concave function defined on all of , is continuous. For convexity, given and , let . Let and . Then by concavity, . Because , we have , as desired.

Now, if and only if by Lemma 2. Because , inductively we obtain . By construction of and because is increasing, . And by definition of a CFMM, . ∎

3.4. CFMMs and scoring rules

Recall that a scoring rule is a function that evaluates the prediction given an observed outcome . A scoring rule is proper if for all probability distributions , the expected score when is maximized by report . It is strictly proper if is the unique maximizer. It is well-known (see e.g. Gneiting and Raftery (2007)) that a scoring rule is proper if and only if it can be written as an affine approximation to a particular convex generating function .

One implication of the above equivalence is that CFMMs are closely linked to proper scoring rules. This connection emphasizes the surprising nature of the equivalence between cost functions and CFMMs, namely that CFMMs, while designed for a very different context than probabilistic forecasting, characterize the properties needed for eliciting forecasts.

Corollary 0.

Every CFMM for a concave, increasing and initial reserves is associated with a proper scoring rule.

The corollary follows immediately from known prediction-market equivalences between cost functions and scoring rules, discussed in Appendix B.1. Briefly, every cost function corresponds to the scoring rule generated by , the convex conjugate of , and vice versa.

As alluded to above, for strict properness, one needs additional conditions on , namely that (1) is differentiable, so that there is a unique market price at any given state, and (2) the set of gradients is equal to the probability simplex, so that any given market price/prediction is achievable by some set of trades. These carry over into corresponding conditions on , as we explore in Appendix B.2.

3.5. Examples

We now present two examples to illustrate our equivalence thus far. We discuss these examples again in § 4.5 along with others.

LMSR CFMM

As a warm-up, let us see how the most popular cost function, the LMSR , can be interpreted as a CFMM. Letting , we have , where is the initial reserves. If , then is a valid trade if and only if . For two assets, this equation reduces to (cf. (Paradigm, 2021)). See § 4.5 for a version which scales the liquidity depending on .

Uniswap cost function / scoring rule

One of the most iconic CFMMs is Uniswap, with the potential function given by . Interestingly, is not defined on all of , and is only increasing on ; as such, typically one restricts to the latter space. As we will see in § 4, this restriction to is typical for CFMMs used in practice, and does not pose a barrier for our equivalence. Briefly, as long as we require , the market reserves will stay within , and the characterization from Theorem 5 and equivalence from Theorem 4 will still apply.

Let and set . Applying Theorem 4, we obtain the cost function from eq. (1),

Let us verify the construction. One can easily check that is -invariant and increasing. Consequently, it suffices to verify a single level set of ; we will show .

We conclude that, indeed, , as promised by Theorem 4. In other words, a prediction market run using would behave exactly the same as Uniswap.

As discussed in § 1, the expression for appears in Chen and Pennock (2007, eq. (14)). There they show that a market maker keeping constant utility assuming the binary outcome would be drawn from the uniform distribution . Moreover, as observed by Bichuch and Feinstein (2022) and Othman (2021), constant expected log utility under the uniform distribution gives rise to Uniswap: . (Changing this distribution gives rise to more general forms of Uniswap, such as Balancer, which takes the form .) Amazingly, it appears that no one has yet made these two connections together, that Uniswap is equivalent to a cost-function prediction market.

In light of Corollary 5, each level set of Uniswap must therefore be equivalent to a scoring rule market for some choice of proper scoring rule. Let us now derive this family of scoring rules. Taking the convex conjugate of , we obtain the convex generating function

The corresponding scoring rule is

where . This scoring rule is exactly the boosting loss of Buja et al. (2005), negated and scaled by . (This scoring rule also appears in a shifted form as “” in Ben-David and Blais (2020).) Interestingly, while in general each level set of could have corresponded to an entirely different scoring rule, instead each level set merely scales the same scoring rule. In fact, as we will see in § 4.4, this phenomenon is shared by all 1-homogeneous CFMMs.

4. Bounded reserves and liquidity

CFMMs are defined in terms of the current reserves , the vector of asset quantities available to trade. Naturally, one might like to ensure at every state of the market, i.e., that the market maker can only trade assets it has, and not go short on any asset. We now make this restriction explicit.

Axiom 6 (BoundedReserves).

and for all , .

A version of the BoundedReserves axiom appeared in Angeris et al. (2022), emphasizing its importance as most common potential functions are 1-homogeneous. In this section, we first characterize all market makers satisfying BoundedReserves in addition to our other four axioms (Theorem 2). We then explore the relationship between BoundedReserves and bounded worst-case loss from the prediction market literature, finding the former to be a stronger condition. In fact, CFMMs constructed from cost functions in our previous equivalence, Theorem 3, can essentially never satisfy BoundedReserves. Instead, we present a new construction leveraging a liquidity parameter from the prediction market literature, to convert any cost function to a CFMM satisfying BoundedReserves. As we will see, this construction recovers every 1-homogeneous CFMM potential function, including nearly all CFMMs used in practice. Moreover, leveraging Corollary 5, these 1-homogeneous CFMMs are associated with a unique scoring rule, thus allowing us to convert between proper scoring rules and CFMMs satisfying BoundedReserves.

4.1. Characterizing bounded reserves

We begin with an observation about CFMMs satisfying BoundedReserves: with Liquidation and NoDominatedTrades, the reserves of each asset must be strictly positive at all valid histories.

Lemma 0.

A market maker satisfying BoundedReserves, Liquidation and NoDominatedTrades must have for all .

Proof.

Assume that for a history , we have for some . For any quantity of asset an agent offers, Liquidation states that the market maker would have to quote a price for it in terms of asset . As the market maker does not have any of asset , it must quote a price of zero to satisfy BoundedReserves. If the agent asks to trade quantity of asset , the market maker can still only give zero units of asset . This trade of for zero units of therefore dominates for zero, violating NoDominatedTrades. Hence the reserves for an asset can never be empty. ∎

We will now characterize CFMMs satisfying all of our axioms. In light of Lemma 1, for any CFMM that satisfies these axioms, it must be the case that and together imply . Intuitively, it follows that we may restrict attention to the strictly positive orthant . While will be increasing on , however, it might not be on its boundary . In fact, a prominent example is Uniswap, , where for . Yet the behavior of in a neighborhood of turns out to be the key to whether Liquidation is satisfied. To state our results, therefore, we restrict without loss of generality, and then use the limits to control the behavior of near .

Theorem 2.

A market maker satisfies Liquidation, NoDominatedTrades, StrongPathIndependence, DemandResponsiveness, and BoundedReserves if and only if the following hold: (a) , (b) the market maker is a CFMM with an continuous, increasing, quasiconcave potential function , and (c) for all .

Proof.

First consider the forward direction, and assume we are given a market maker satisfying all 5 axioms. For (a), we have by BoundedReserves and the reverse inclusion from Lemma 1. For (b), we make use of the Lemma 5, a more general version of the foreward direction for Theorem 5 (see § A). Leveraging (a), the lemma states that the first 4 axioms imply a CFMM with an continuous, increasing, quasiconcave potential .

Finally, consider (c). Denote for ; the limit exists as is increasing. Then condition (c) can be succinctly written: for all . A fact we will use is that for and , we have . (Take ; as is increasing and by definition of , we have .) As is increasing, we have . Now suppose for a contradiction we had some with . By definiton of a limit, there exists sufficiently small so that . Let so that . Then by the fact above we have . By continuity of , there exists satisfying . Let be an asset such that . Now let us apply Liquidation at to bundles and , giving some such that . Let be the resulting history. Then by (b). By Lemma 1, we must have , which implies . As , we therefore have , as the th coordinate is and all other coordinates are at least 1. By the fact above, , a contradiction.

For the reverse direction, let satisfying conditions (a), (b), and (c) be given. Let be defined as above. We first show that we may assume without loss of generality that is continous on . Let for all . Then is monotone increasing and continuous, and has a monotone increasing and continuous inverse. Thus, satisfies conditions (a), (b), and (c) as well. Moreover, satisfies for all ; in other words, follows the construction of Theorem 5. Now as by the above, and for all by (c), Crouzeix (2005, Proposition 4.1) states that is continuous on . As on , we have continuity on .

BoundedReserves is trivially satisfied as is only defined (or equivalently, equal to ) outside of , so and immediately implies . It follows that the proofs for DemandResponsiveness, NoDominatedTrades, and StrongPathIndependence in Theorem 5 immediately extend to the case where the domain is restricted to , since they all begin with given elements of . (The second condition of StrongPathIndependence also follows immediately from .)

It remains therefore to show Liquidation. We will use the fact that for all , which follows by a similar argument to the above: letting , we have . Now let and . Then as is defined only on , giving as well. Thus . Now let be the unique real value such that . By (c), we have . Thus . By continuity of on (see above), we have some such that . As , we have . Thus as well, giving , as desired. ∎

In Appendix A, we prove a more general version of some key steps of Theorem 2 for more general restrictions on the reserves other than . While from BoundedReserves this is perhaps the most interesting case, the entire theorem could in principle be generalized to other which are “dominant domains” (Definition 4); for example, condition (c) in the theorem would replace with .

4.2. Connection to worst-case loss and liquidity

When assets are contingent securities, it is perhaps more natural to ask how much money the market maker could lose in some run of the market and some outcome of nature, rather than tracking the number of securities “in reserve”. This interpretation gives the following axiom, which is commonly found in the literature on prediction markets (Chen and Pennock, 2007; Abernethy et al., 2013, 2014; Cummings et al., 2016; Frongillo and Waggoner, 2017). Here we regard “money” as the grand bundle (cf. § 3.2).

Axiom 7 (WorstCaseLoss).

For all , there exists such that for all with , we have .

The BoundedReserves axiom can be regarded as a special case of WorstCaseLoss, where , but the converse does not hold. Indeed, essentially any interesting -invariant cost function satisfying WorstCaseLoss does not satisfy BoundedReserves. To see why, let and be any non-dominated trade, i.e., with . In other words, start with one of each asset, and take any nontrivial trade. Let be an asset with , and now consider where . Then by -invariance, we still have , yet now , meaning the market maker is negative in its reserves of asset . Moreover, as our previous construction from Theorem 3) gives a -invariant market, we have yet to see how to convert a prediction market to a CFMM that respects the reserves regardless of where the market is initialized.

Fortunately, we can borrow ideas from the prediction market literature to make our construction reserves-aware. Specifically, we will use the relationship between worst-case loss and liquidity, roughly the amount of assets available to buy or sell around a given price, which has been extensively studied (Chen and Pennock, 2007; Abernethy et al., 2013, 2014; Cummings et al., 2016; Frongillo and Waggoner, 2017). In the cost-function formulation, there is a simple and direct tradeoff: more liquidity leads to a higher worst-case loss.

Furthermore, there is a simple transformation from convex analysis that changes any given cost function’s liquidity: the perspective transform. Given a convex function , its perspective transform by is the function .333Often the perspective transform is given by , a form we will use in Proposition 5. For example, for , the perspective transform is . As , the liquidity increases: the gradient of , i.e. the price, changes more slowly in response to a change in quantity . But the worst-case loss increases as well. One way to see the latter is via the convex duality relationship to proper scoring rules: the perspective transform on is equivalent to a simple scaling of its corresponding proper scoring rule by .

4.3. CFMM construction satisfying bounded reserves

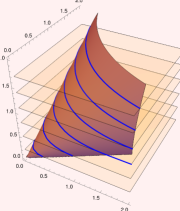

Using the ideas above, we now provide a construction taking any cost function to a CFMM that satisfies BoundedReserves. The magic is in “wrapping up” the level sets of for different into a single function , so that starting at implies a liquidity of . Furthermore, we ensure that as , so that a market starting with very low initial reserves quickly moves the price so as not to run out.

Construction 1.

Let be a convex, increasing, -invariant cost function satisfying . Then define by where .

The assumption is without loss of generality; otherwise, add a sufficiently large constant to . Similarly, while this construction centers around the level set , other level sets may be taken be shifting by a constant.

Before arguing that this construction is well-defined and satisfies all our axioms, let us verify that it is behaving as we would hope. Define , which is but with “liquidity level” . Then by definition the -level set of matches the -level set of , i.e., . (See Figure 2(L) for a visualization.) If satisfies for , then we have . In other words, indeed has liquidity level when . Moreover, if , then , so indeed the liquidity level drops to as , thereby protecting the reserves. This scaling property is known as 1-homogeneity, and plays a large role in our analysis; see Lemma 4 and § 4.4.

Lemma 0.

The function from Construction 1 is well-defined.

Proof.

We must show that exists and is unique on . Let . First, define . By -invariance, . Let and . Define and . We have . Because is increasing, . Because is convex and defined on , it is continuous. Therefore, is continuous in for . So there exists such that . Furthermore, because is strictly decreasing in , this solution to is unique. ∎

A useful fact about Construction 1 is that the resulting potential function is 1-homogeneous. Recall that a function is 1-homogeneous if for all and we have . Such functions have useful symmetry for market making (Othman et al., 2010); in particular, since their gradients are 0-homogeneous (invariant under scaling), the instantaneous exchange rates between any two assets remain constant when scaling up the reserves. In part because of this appealing scale invariance, nearly all popular CFMM potential functions used in practice are 1-homogeneous (Angeris et al., 2022).

Lemma 0.

Any resulting from Construction 1 is 1-homogeneous, concave, and increasing.

Proof.

Let be the given cost function.

(Homogeneous) Let , and . Then by definition of and the fact that it is well defined (Lemma 3). Further, for any , we have , which implies .

(Increasing) Let . Let , so that . As is increasing, and , we have . Now let , so that . Clearly due to uniqueness in Lemma 3, and if , we would have yet , contradicting being increasing. We conclude , or equivalently, , as desired.

(Concave) It is well-known that the map is convex, as the perspective transform of the convex function . Thus, is a convex set as a sublevel set of a convex function. Yet this set is precisely the hypograph of , as , so . As the hypograph of is convex, is a concave function.

∎

Proposition 0.

Let satisfy the conditions of Construction 1 as well as . Then the resulting defines a CFMM satisfying Liquidation, NoDominatedTrades, PathIndependence, DemandResponsiveness, and BoundedReserves.

Proof.

We will establish conditions (a), (b), and (c) from Theorem 2 and then apply the result. Part (a) is implied by the domain of . Part (b) follows from Lemma 4. It thus suffices to show (c).

Let be the concave closure of . Then is continuous on ; see the proof of Theorem 2. As is 1-homogeneous from Lemma 4, we have . Now let with for some . Suppose for a contradiction that . Let be a sequence in converging to , so that . Then letting , we have . By definition of , each point is an element of . As is closed (by continuity of ), we must have . Yet by assumption, , a contradiction as (recall that ). We conclude that . As on , by continuity we also have . Thus , giving (c). ∎

4.4. Homogeneous CFMMs and unique scoring rules

As essentially all CFMMs used in practice are 1-homogeneous (Angeris et al., 2022), it is natural to ask whether Construction 1 could have produced them. We now show the answer is yes: every 1-homogeneous (increasing, concave) potential function is the result of Construction 1 for some choice of cost function.

Proposition 0.

A potential is the result of applying Construction 1 if and only if is 1-homogeneous, increasing, and concave.

Proof.

We have already shown in Lemma 4 and the proof of Proposition 5 that any potential resulting from the construction is 1-homogeneous, increasing, and concave. Now let be a given 1-homogeneous, increasing, and concave potential. As in Theorem 4, define . Then for any , we have . Now apply Construction 1 to and obtain . Then . We conclude . As both and are 1-homogeneous, they are fully determined by any level set, so must now be equal; formally, for any , letting , we have . ∎

As a result of Proposition 6, through Corollary 5, every 1-homogeneous CFMM can be associated with a unique proper scoring rule; the various level sets of the potential merely correspond to scaling up the underlying scoring rule. As we will see in § 4.5, this fact can be used to construct useful CFMMs from the vast literature on proper scoring rules.

Corollary 0.

Every CFMM for a 1-homogeneous, concave, increasing is associated with a unique proper scoring rule.

Before moving to examples, let us briefly remark on connections to convex geometry. Construction 1 can be regarded geometrically as a gauge function (also known as a Minkowski functional) on a star set, which is known to be a characterization of 1-homogeneous functions. For any set , the gauge function (Minkowski functional) of is defined as . Letting , we have .

4.5. Examples

Uniswap

Let us perform Construction 1 on the cost function we derived from Uniswap, , given some level set :

First, let us check that satisfies the condition of Construction 1: indeed, . From § 3.5, we have . Thus . Thus, the construction yields , which is exactly when , and a scaled version for other values.

LMSR

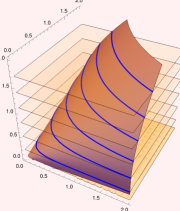

Let be LMSR. Unlike our choice from § 3.5, let us now consider a “reserves-aware” version, which will automatically scale liquidity with . As , Construction 1 applies, giving a potential . See Figure 2(M) for a visualization. Moreover, the condition of Proposition 5 is also satisfied, as for all . So the CFMM with potential satisfies all five of our axioms. Unfortunately, unlike Uniswap, this does not permit a closed-form expression. Nonetheless, as we discuss in § 5, we believe it could be practical to deploy in real markets.

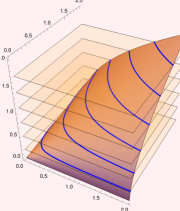

CFMM from Brier score

Let us see how to take one of the most popular scoring rules, the Brier (or quadratic) score,

| (4) |

and convert it to a CFMM using our chain of equivalences. The corresponding convex generating function is . The associated cost function , the convex conjugate of , does not have a convenient closed form in general; for assets it can be written

| (5) |

From this form, one can see that is not always increasing, as e.g. the price for asset 2 becomes 0 when . The resulting market therefore does not satisfy NoDominatedTrades, as selling asset 2 for a price of 0 is dominated by doing nothing.

It turns out, however, that we may still apply Construction 1 to obtain a sensible CFMM; in this case, for , we obtain

| (6) |

the sum of the geometric and arithmetic means; see Figure 2(R). In fact, this potential function is a hybrid CFMM appearing already in the literature, e.g. Angeris et al. (2022, § 2.4).

Curve

Finally, let us consider Curve (Egorov, 2019), given by . As noted by Angeris et al. (2022), this potential is not 1-homogeneous, and thus could not be produced by Construction 1. As a result, its level sets are not merely scaled copies of each other, but change as the value of grows. (For instance, its 0-level set is the same as Uniswap with , but no other level set is in common with Uniswap.) Nonetheless, we may still apply Theorem 2 to see that satisfies all five of our axioms; to check condition (c), note that on .

5. Adaptive Liquidity and Other Future Directions

The literature on automated market makers for decentralized exchanges has largely proceeded somewhat removed from the expansive literature on prediction markets. We believe the results presented here will allow for these independent lines of research to merge and inform each other. To conclude, we briefly discuss several avenues for future work, with a focus on liquidity adaptation.

Transaction fees

In practice, CFMMs often allow liquidity to change over time, in two ways: (1) they may charge a “transaction fee”, wherein traders must contribute directly to the reserves in addition to their trade, and (2) they may allow liquidity providers to contribute to the reserves in exchange for a dividend. Let us first discuss the transaction fee.

Here the market designer chooses a parameter , where lower corresponds to a higher fee. The market maker then accepts any trade keeping the potential function constant after discounting the bundle given to the market maker by . Formally, we can write

| (7) |

where and . To state this set of valid trades more naturally in terms of transaction fees, relative to the no-fee for the vanilla CFMM, we may write

| (8) |

where for . That is, a trader may choose any trade keeping constant, but then must also add to the reserves.

Now suppose is increasing, concave, and 1-homogeneous, as is commonly the case, and as guaranteed by Construction 1. Then as , and is increasing, we will have . As we saw in § 4, represents the liquidity level when the reserves are , so we conclude that the liquidity increases after each trade. Moreover, as the fee-less CFMM satisfies BoundedReserves, and is increasing, it is easy to verify that BoundedReserves will still be satisfied with the transaction fee. Thus, the transaction fee successsfully subsidizes the liquidity increase of the market without risking depleting the reserves.

Implicitly defined potential functions

Recall that the from Construnction 1 is only implicitly defined, as the solution to for the given cost function . Thus, even if is given explicitly, may not have a closed form. While sometimes one can solve for explicitly, as we saw in § 4.5, this is the case for the 1-homogeneous CFMM potential we derived from LMSR. The lack of a closed form poses a challenge, as the transaction fee causes to change, and thus the value of would need to be recalculated rather than being fixed ahead of time.

We now propose a straightforward workaround using the fact that is still implicitly defined by a known cost function . Suppose the current value is publicly known, and a trader wishes to purchase , i.e., such that . We will ask the trader to announce , as well as the value , up to some error tolerance. As is monotone in , the trader can easily compute within the desired accuracy given an expression for . Moreover, the two relevant conditions can be checked on-chain: by , and by .

To illustrate, let be LMSR, and the result of Construction 1. From the condition , the level set is . The validity of and can be checked, via and . Thus, by asking a trader to compute a valid trade, as well as approximating the next value of , the market can proceed even without a closed form for .

Other forms of liquidity adaptation

The prediction market literature offers many other forms of transaction fees and schemes for liquidity adaptation; see e.g. Othman et al. (2010); Othman and Sandholm (2012); Li and Vaughan (2013). Using the equivalence developed in this work, these market makers can be readily transformed into those for decentralized exchanges. It would be particularly interesting to study the CFMM transaction fee within the volume-parameterized market (VPM) framework of Abernethy et al. (2014); we conjecture that it fails to satisfy their shrinking spread axiom (for any choice of volume function) but satisfies their others. Conversely, the perspective market from that same paper may be of interest to the decentralized finance community.

Other directions

As mentioned above, many CFMMs allow liquidity providers to directly contribute to the reserves. In light of our results, it would be interesting and potentially impactful to study the elicitation implications of these protocols from the side of liquidity providers. Finally, while the above focuses on potential contributions from the prediction market literature to decentralized finance, contributions in the direction are likely to be fruitful as well.

Acknowledgements

We thank David Pennock, Daniel Reeves, and Anson Kahng for collaboration in working out the cost function and proper scoring rule corresponding to Uniswap. We also thank Scott Kominers, Ciamac Moallemi, Abe Othman, Tim Roughgarden, and Christoph Schlegel for helpful discussions. This material is based upon work supported by the National Science Foundation under Grant No. IIS-2045347.

References

- Abernethy et al. [2013] Jacob Abernethy, Yiling Chen, and Jennifer Wortman Vaughan. Efficient market making via convex optimization, and a connection to online learning. ACM Transactions on Economics and Computation, 1(2):12, 2013. URL http://dl.acm.org/citation.cfm?id=2465777.

- Abernethy et al. [2014] Jacob D. Abernethy, Rafael M. Frongillo, Xiaolong Li, and Jennifer Wortman Vaughan. A General Volume-parameterized Market Making Framework. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, EC ’14, pages 413–430, New York, NY, USA, 2014. ACM. ISBN 978-1-4503-2565-3. doi: 10.1145/2600057.2602900. URL http://doi.acm.org/10.1145/2600057.2602900.

- Agrawal et al. [2011] Shipra Agrawal, Erick Delage, Mark Peters, Zizhuo Wang, and Yinyu Ye. A unified framework for dynamic prediction market design. Operations research, 59(3):550–568, 2011. URL http://pubsonline.informs.org/doi/abs/10.1287/opre.1110.0922.

- Angeris and Chitra [2020] Guillermo Angeris and Tarun Chitra. Improved price oracles: Constant function market makers. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, pages 80–91, 2020.

- Angeris et al. [2020] Guillermo Angeris, Alex Evans, and Tarun Chitra. When does the tail wag the dog? curvature and market making, 2020. URL https://arxiv.org/abs/2012.08040.

- Angeris et al. [2022] Guillermo Angeris, Akshay Agrawal, Alex Evans, Tarun Chitra, and Stephen Boyd. Constant Function Market Makers: Multi-asset Trades via Convex Optimization, pages 415–444. Springer International Publishing, Cham, 2022. ISBN 978-3-031-07535-3. doi: 10.1007/978-3-031-07535-3˙13. URL https://doi.org/10.1007/978-3-031-07535-3_13.

- Ben-David and Blais [2020] Shalev Ben-David and Eric Blais. A new minimax theorem for randomized algorithms. In 2020 IEEE 61st Annual Symposium on Foundations of Computer Science (FOCS), pages 403–411. IEEE, 2020.

- Bichuch and Feinstein [2022] Maxim Bichuch and Zachary Feinstein. Axioms for automated market makers: A mathematical framework in fintech and decentralized finance, 2022. URL https://arxiv.org/abs/2210.01227.

- Buja et al. [2005] Andreas Buja, Werner Stuetzle, and Yi Shen. Loss functions for binary class probability estimation and classification: Structure and applications. Working draft, November, 3:13, 2005. URL pdfs.semanticscholar.org/d670/6b6e626c15680688b0774419662f2341caee.pdf.

- Capponi and Jia [2021] Agostino Capponi and Ruizhe Jia. The adoption of blockchain-based decentralized exchanges. arXiv preprint arXiv:2103.08842, 2021.

- Chen and Pennock [2007] Y. Chen and D.M. Pennock. A utility framework for bounded-loss market makers. In Proceedings of the 23rd Conference on Uncertainty in Artificial Intelligence, pages 49–56, 2007.

- Chen and Vaughan [2010] Y. Chen and J.W. Vaughan. A new understanding of prediction markets via no-regret learning. In Proceedings of the 11th ACM conference on Electronic commerce, pages 189–198, 2010.

- Connell and Rasmusen [2017] Chris Connell and Eric B Rasmusen. Concavifying the quasiconcave. Journal of Convex Analysis, 24(4):1239–1262, 2017.

- Crouzeix [2005] Jean-Pierre Crouzeix. Continuity and differentiability of quasiconvex functions. Handbook of generalized convexity and generalized monotonicity, pages 121–149, 2005.

- Cummings et al. [2016] Rachel Cummings, David M Pennock, and Jennifer Wortman Vaughan. The possibilities and limitations of private prediction markets. In Proceedings of the 17th ACM Conference on Economics and Computation, EC ’16, pages 143–160. ACM, 2016.

- Egorov [2019] Michael Egorov. Stableswap-efficient mechanism for stablecoin liquidity. Retrieved Feb, 24:2021, 2019.

- Fenchel [1953] W. Fenchel. Convex Cones, Sets, and Functions. Princeton University, Department of Mathematics, Logistics Research Project, 1953. URL https://books.google.com/books?id=qOQ-AAAAIAAJ.

- Frongillo and Reid [2015] Rafael Frongillo and Mark D. Reid. Convergence Analysis of Prediction Markets via Randomized Subspace Descent. In Advances in Neural Information Processing Systems, pages 3016–3024, 2015. URL http://papers.nips.cc/paper/5727-convergence-analysis-of-prediction-markets-via-randomized-subspace-descent.

- Frongillo and Waggoner [2017] Rafael Frongillo and Bo Waggoner. Bounded-loss private prediction markets, 2017. URL https://arxiv.org/abs/1703.00899.

- Frongillo and Waggoner [2018] Rafael Frongillo and Bo Waggoner. An Axiomatic Study of Scoring Rule Markets. In Anna R. Karlin, editor, 9th Innovations in Theoretical Computer Science Conference (ITCS 2018), volume 94 of Leibniz International Proceedings in Informatics (LIPIcs), pages 15:1–15:20, Dagstuhl, Germany, 2018. Schloss Dagstuhl–Leibniz-Zentrum fuer Informatik. ISBN 978-3-95977-060-6. doi: 10.4230/LIPIcs.ITCS.2018.15. URL http://drops.dagstuhl.de/opus/volltexte/2018/8361.

- Föllmer and Schied [2008] Hans Föllmer and Alexander Schied. Convex and coherent risk measures. October, 8:2008, 2008. URL http://alexschied.de/Encyclopedia6.pdf.

- Föllmer and Weber [2015] Hans Föllmer and Stefan Weber. The Axiomatic Approach to Risk Measures for Capital Determination. Annual Review of Financial Economics, 7(1), 2015.

- Gneiting and Raftery [2007] Tilmann Gneiting and Adrian E. Raftery. Strictly proper scoring rules, prediction, and estimation. Journal of the American Statistical Association, 102(477):359–378, 2007.

- Gnosis [2020] Gnosis. Automated market makers for prediction markets. https://docs.gnosis.io/conditionaltokens/docs/introduction3/, 2020.

- Hanson [2003] R. Hanson. Combinatorial Information Market Design. Information Systems Frontiers, 5(1):107–119, 2003.

- Jensen et al. [2021] Johannes Rude Jensen, Victor von Wachter, and Omri Ross. An introduction to decentralized finance (defi). Complex Systems Informatics and Modeling Quarterly, (26):46–54, 2021.

- Li and Vaughan [2013] Xiaolong Li and Jennifer Wortman Vaughan. An axiomatic characterization of adaptive-liquidity market makers. In ACM EC, 2013.

- Manifold [2022] Manifold. Maniswap. https://www.notion.so/Maniswap-ce406e1e897d417cbd491071ea8a0c39, 2022.

- Othman and Sandholm [2012] A. Othman and T. Sandholm. Profit-charging market makers with bounded loss, vanishing bid/ask spreads, and unlimited market depth. In ACM EC, 2012.

- Othman et al. [2010] A. Othman, T. Sandholm, D. M Pennock, and D. M Reeves. A practical liquidity-sensitive automated market maker. In Proceedings of the 11th ACM conference on Electronic commerce, pages 377–386, 2010.

- Othman [2021] Abraham Othman. New invariants for automated market making, 2021. URL https://github.com/shipyard-software/market-making-whitepaper/blob/main/paper.pdf.

- Paradigm [2021] Paradigm. Uniswap v3: The universal amm. https://www.paradigm.xyz/2021/06/uniswap-v3-the-universal-amm, 2021.

- Schlegel et al. [2022] Jan Christoph Schlegel, Mateusz Kwaśnicki, and Akaki Mamageishvili. Axioms for constant function market makers, 2022. URL https://arxiv.org/abs/2210.00048.

Appendix A Omitted Proofs for CFMM Characterization

To prove Lemma 3, we separate out the following lemma, which will be useful later.

Lemma 0.

Suppose the CFMM defined by satisfies PathIndependence, NoDominatedTrades, Liquidation, and DemandResponsiveness. For any , let and let . Then is convex.

Proof.

We show that for any , any convex combination is in . The lemma then follows because for any of the form , with , the convex combination is , which is in .

So let , let , and define . Then . Let and taken pointwise, so that . By Liquidation, there exists such that . By NoDominatedTrades, as otherwise would be dominated by trade . Let . Then , because . Therefore, by DemandResponsiveness, , implying .

Observe that . Because , , and , we have . ∎

Proof of Lemma 3.

Proposition 4 will be proven by the following two lemmas.

Lemma 0.

Fix the initial reserves . If a market maker with satisfies Liquidation, NoDominatedTrades, PathIndependence, and DemandResponsiveness, then it can be implemented as a CFMM with an increasing, concave potential function .

Proof.

Given a market satisfying the axioms, Lemma 3 implies it has a potential such that is convex. Again, for convenience, write and . Define

This is a well-known construction in theory of risk measures [Föllmer and Schied, 2008, Föllmer and Weber, 2015]; we provide a proof that is increasing and concave for completeness. First, is well-defined, i.e. the supremum is over a nonempty set: for example, taking , we find that , i.e. , so .

Second, it implements as a CFMM. By definition of the set of legal reserves , we have . So we must show . First, for any , including , we have . This follows because , but would violate NoDominatedTrades, as we would have , which implies some trade in strictly dominates . Second, if , then , and cannot dominate any member of (else ), so it must be in . We have shown .

Now we show is increasing. Let and . Let such that contains . Then also contains, by upward closure, . This proves , as the supremum is taken over a superset. Furthermore, if , then we claim , i.e. is increasing. If , then , but then the trade is dominated by the trade , both in , contradicting NoDominatedTrades.

Finally, for concavity, let and . Let . Then also contains , proving that . ∎

Lemma 0.

Fix the initial reserves . If a market maker with is a CFMM with an increasing, concave potential function , then it satisfies Liquidation, NoDominatedTrades, PathIndependence, and DemandResponsiveness.

Proof.

Let and, for short, let .

(DemandResponsiveness) Assume , where , and assume where . We must prove . As these are feasible trades, we have that the value of the CFMM is same at those points i.e. . Let . By concavity of we have that

As is an increasing function, this implies we cannot have . Thus we cannot have . We conclude , and thus , which proves DemandResponsiveness.

PathIndependence is immediately satisfied by a CFMM, as and imply , which implies .

Assume NoDominatedTrades is not satisfied i.e. with . This implies that , violating that is increasing.

For Liquidation, let . Concavity of implies that at current reserves , there exists a supergradient444A supergradient is defined as any that satisfies the inequality . of , say . We show that as is increasing, . This should hold for . Since is increasing, . Therefore, and .

For any , . Hence from the supergradient inequality, , from which we have . As is increasing, we also have that . Hence by continuity of , which follows from concavity, we can say that s.t. which proves Liquidation.

∎

Theorem 5 will be proven by the following two lemmas. We show Lemma 5 on a slightly more general space called dominant domain, which we define below. The two primary examples of dominant domains are itself and the strictly positive orthant .

Definition 0.

We call a subset of a dominant domain if it is an open, convex set that is closed under dominance, i.e. .

Lemma 0.

If a market maker, where is a dominant domain , satisfies Liquidation, NoDominatedTrades, StrongPathIndependence, and DemandResponsiveness, then it is implemented by a CFMM for some increasing, continuous, quasiconcave .

Proof.

Let a market satisfying the axioms be given. For any , define

If there is no such that , then leave undefined.

We first show that is a well-defined function on . Let and . Observe by StrongPathIndependence. Let and let , noting that . By Liquidation applied to and , there exists such that contains . We take . Furthermore, is unique, as is unique by NoDominatedTrades.

We will show that implements as a CFMM. Then, we will show that it is increasing, continuous, and quasiconcave.

To begin, we first show that has “level set structure”. Specifically, we will show that is a well-defined equivalence relation. Combining this statement with the fact that is well-defined, we will have for all .

As StrongPathIndependence implies PathIndependence, results only assuming the latter apply. For all , let be the set from Lemma 2, so that . Substituting into the above, the following claim shows that as defined above is indeed an equivalence relation.

Claim 1.

For all , .

Proof.

We first show . Let such that . Let . Let . Note since by assumption and thus . Observe so StrongPathIndependence applies. From Lemma 2 and StrongPathIndependence, we have . For the reverse implication, if , we have , completing the proof. ∎

We can now see that implements . Let . Then from StrongPathIndependence, . It remains to show that is continuous, increasing, and quasiconcave.

Before we show properties of , we introduce another construction of a “cost function”. Let such that . Observe that this construction is ones-invariant i.e. for any constant . We first show that this is continuous for any .

Suppose that is not continuous at a particular . Thus such that , such that and . Given an , take , and let be given satisfying the above. Let , so that and . As , we have . Assume without loss of generality that ; then . Now . We have now contradicted NoDominatedTrades as but .

(Increasing) Suppose for a contradiction that we have two vectors such that and . If then , violating NoDominatedTrades as . Otherwise, . As we saw from above that are continuous functions, so is the function . Observe that as . Thus, . On the other hand, . If , then but by definition of , violating NoDominatedTrades. Thus, . As is continuous, by the intermediate value theorem we have some such that , implying . From the definition of and , we have and . From Claim 1, which is contradiction of NoDominatedTrades.

(Quasiconcave) We claim that the superlevel sets of are exactly the sets of the form for some . Then Lemma 1 implies that each such set is convex, which proves quasiconcavity. To show these are the superlevel sets: for one direction, because is increasing, we have . For the other direction, suppose . We show for some . Specifically, use Liquidation starting at reserves to trade for units of , where is chosen large enough that the trade vector is positive. Receiving for some , the new reserves are . By definition of a CFMM, we have . And because , and is increasing, we must have .

(Continuous) Let . We will show that is continuous at . By Crouzeix [2005, Proposition 4.1], as is increasing with respect to , and is in the interior of , it suffices to show continuity of the function at . Observe that is increasing. We use the formulation of continuity.

Let and let such that , which exists as is open. Let ; by definition, . Let so that . Applying Liquidation with and bundles and , we have some such that . This condition is in turn equivalent to . By the same argument for , we have some such that .

We have , , and . As is increasing, we must have . Let . Then . In particular, again as is increasing, for all , we have . Thus, whenever , giving continuity of at and completing the proof. ∎

Lemma 0.

Let a CFMM be given for a quasiconcave, increasing, continuous , with . Then it satisfies DemandResponsiveness, Liquidation, NoDominatedTrades and PathIndependence.

Proof.

Let and, for short, let .

(DemandResponsiveness) Assume , where , and assume where . We must prove . As these are feasible trades, we have that the value of the CFMM is same at those points i.e. . Let . By quasiconcavity of we have that

As is an increasing function, this implies we cannot have . Thus we cannot have . We conclude , and thus , which proves DemandResponsiveness.

(StrongPathIndependence) , if then which is also . We also trivially have for all .

(NoDominatedTrades) Assume that the axiom is not satisfied, i.e., we have with . This implies that , violating that is increasing.

(Liquidation) Quasi-concavity of implies that at current reserves , there exists a supporting hyperplane555A supporting hyperplane of a set would satisfy the inequality , for all of super-level set666 A super-level set of for level is defined as of . The existence of a supporting hyperplane at stems from as we will show now. We take a slight detour to show that . Lets assume the contrary that there exists a such that . Let for an such that , which is possible as is continuous. As , this gives us which is a contradiction as and is in the super-level set.

The supporting hyperplane inequality should hold for for some . Since is increasing and defined on all of , we have and hence and . Therefore, and as it folds for any , .

Let and let be a constant. Then and . Hence from the supporting hyperplane inequality, , from which we have , again using the fact that is defined at the latter point. As is increasing, we also have that . Hence by continuity of , we can say that s.t. which proves Liquidation. ∎

Appendix B Information Elicitation

B.1. Sketch for Fact 1

We recall that a scoring rule is a function , assigning a score to each prediction when the obeserved outcome is . The scoring rule is proper if the expected score, with respect to any given belief , is maximized by reporting . It is strictly proper if uniquely maximizes the expected score. Examples of strictly proper scoring rules are the log score and the Brier or quadratic score .

We now sketch the proof of Fact 1 for completeness.

Proof sketch for Fact 1.

The first key step is Theorem 3.1 of [Frongillo and Waggoner, 2018], which states that any market maker satisfying Path Independence and Incentive Compatibility must in fact be representable as a “scoring rule market”. A scoring rule market, in our terminology, is an automated market maker including an asset of cash where must map one-to-one to predictions , and the net payoff for moving the market prediction from to must be given by the formula of [Hanson, 2003]:

where is a strictly proper scoring rule. The intuition is that Incentive Compatibility is characterized by use of a strictly proper scoring rule in each round, while Path Independence imposes the requirement of “telescoping sums” for sequences of predictions, giving the above formula.

The second key step is given by classic results of [Chen and Pennock, 2007, Abernethy et al., 2013] stating that scoring-rule markets are equivalent to cost-function markets. In particular, a strictly proper scoring rule corresponds via convex duality to a convex cost function such that

(Also, is differentiable and has a certain set of gradients, namely the probability simplex.) Here convex duality gives a one-to-one correspondence between market states and predictions , such that the trade with is equivalent to the prediction update . In other words, the cost-function interface to the market is equivalent to the scoring-rule interface.777There is a difference in timing, because as usually implemented, a cost function collects the cash payment at the time of trade while the securities pay off at the end; the scoring rule assesses all payments at the end. For Fact 1, we must either wait to collect the payment until the end, or assume that one unit of cash has constant utility over time (the usual assumption).