Nonlinear Optimization Filters for Stochastic Time-Varying Convex Optimization

Abstract

We look at a stochastic time-varying optimization problem and we formulate online algorithms to find and track its optimizers in expectation. The algorithms are derived from the intuition that standard prediction and correction steps can be seen as a nonlinear dynamical system and a measurement equation, respectively, yielding the notion of nonlinear filter design. The optimization algorithms are then based on an extended Kalman filter in the unconstrained case, and on a bilinear matrix inequality condition in the constrained case. Some special cases and variations are discussed, notably the case of parametric filters, yielding certificates based on LPV analysis and, if one wishes, matrix sum-of-squares relaxations. Supporting numerical results are presented from real data sets in ride-hailing scenarios. The results are encouraging, especially when predictions are accurate, a case which is often encountered in practice when historical data is abundant.

1 Introduction

We look at time-varying optimization problems of the form

| (1) |

where is a smooth strongly convex function in (for all ), parametrized over a time-varying data stream ( represents the continuous time), and is a closed convex and proper function (such as the indicator function, or an regularization).

Problem (1) appears naturally in a number of application scenarios, where optimal decisions have to be taken online and they change as new data arrive. Examples stem from video processing [1] to robot control [2], and to large-scale optimal management of smart infrastructures [3].

Solving Problem (1) means to find and track the optimizer trajectory , as changes and it is revealed. In order to accomplish this, in the standard time-varying literature, one can sample Problem (1) at discrete time instant , , with being the sampling time, and solve the sequence of time-invariant problems

| (2) |

as they are revealed in time. Then one can set up online algorithms that find approximate ’s, say ’s, that eventually converge to111Somebody could rather say: “track”. the solution trajectory, within an error bound. The reader is referred to the surveys [4, 5] for an ample treatment of the methods in both discrete and continuous time. One of the important aspects to keep in mind is that online algorithms are sought that are computationally frugal, so that one can approximate the solution of within the sampling time , and the key performance metric is how good the algorithms are with respect to an algorithm that has infinite computational time.

A tacit assumption in the above methods is that one wants to converge to the solution trajectory generated by the evolution of the data stream . However, this may be not the best course of action, since the data are often noisy and convergence to a noisy optimizer may be not advisable. A better angle is to ask whether we can set up algorithms to converge to a filtered version of the trajectory.

In this context, we re-interpret Problem (1) as a stochastic problem, where we would like to find and track the filtered solution trajectory as

| (3) |

where the expectation is with respect to the random variable , which is drawn from a time-varying probability distribution .

Were the probability distribution time-invariant, Formulation (3) would be common in stochastic optimization. With our setting, we are considering instead a gradual distribution shift of an unknown distribution, which renders the formulation less common and more challenging. Recent papers have started to look into this formulation [6, 7, 8]; especially the third one is the closest to our goal, however the authors “just” adapt the standard prediction-correction algorithms to the stochastic setting by properly tuning the prediction and the correction step sizes. Also they do not consider a non-smooth component as our function .

In this paper, we look from a different angle and ask whether we can use a perturbed version of the optimality condition as a suitable dynamical model to do filtering. This will have the advantage to combine prediction and correction in novel and more performant ways. To fix the ideas on this novel angle, consider the unconstrained problem:

| (4) |

with a strongly convex, doubly differentiable, and smooth function in . By perturbing the optimality condition , we can derive the ordinary differential equation that describes how the optimizer evolves as [9]:

| (5) | |||||

This is a nonlinear dynamical system. To derive a filter, we need to couple this model with a measurement equation, which tells us how far from the optimizer trajectory we are. We can thus use,

| (6) |

as a measurement equation (i.e., it will be different from zero at any point but on the optimizer trajectory, where ).

Armed with (5) and (6), we could design a dynamical filter to reconstruct based on a noisy data stream .

1.1 Contributions

Starting from the continuous-time intuition from (5) and (6), we develop discrete-time filters for unconstrained and constrained time-varying problems. In particular,

We derive an extended Kalman filter for unconstrained and differentiable convex problems in the discrete-time setting starting from an algorithmic viewpoint;

We generalize the filtering procedure for constrained and non-differentiable problems leveraging the nonlinear dynamical systems and nonlinear measurement equations coming from forward-backward algorithms and fixed-point residuals. We are then able to derive the optimal “Kalman-style” gain via both a worst-case approach and via dissipativity theory. We also present a possibly less conservative linear parameter-varying (LPV) methodology.

We showcase the benefit of the approach with respect to state-of-the-art prediction-correction methods (which our filters generalize), in numerical simulations stemming from a ride-hailing example with multiple companies in New York City.

1.2 Related work

Time-varying and stochastic optimization are vibrant research fields, and we do not plan to give an exhaustive account here. The reader is referred to [10, 4, 5] for the first and [11, 12, 13, 14] for a sub-sample of the second, and the many references therein. Jointly Stochastic and time-varying optimization is a less studied area, and as we have mentioned [6, 7, 8] scratch the surface in this direction. The celebrated [15] paper is also somewhat in the general area of interest, though their approach does not include prediction, it uses restart and is more directed at finding optimal regret rates for non-stationary objectives rather than noise.

We will build on techniques from dissipativity theory for analyzing and designing optimization algorithms. This is a recent and fertile area brought to fame by L. Lessard and collaborators’ seminal paper [16], and now gaining momentum [17, 18, 19, 20, 21, 22]. Our novel insight in this direction is to use the techniques to determine Kalman-style gains for optimization algorithms with errors. Finally, we use LPV techniques from [23, 24, 25], especially in the context of matrix sum-of-squares relaxations.

Organization. The remaining of the paper is organized as follows. Section 2 discusses formulation and main assumptions. We focus on the unconstrained case in Section 3, and on the general case in Section 4. Section 5 describes our gain design. We then conclude with some numerical simulations in Section 6. All proofs are given in the Appendix.

Notation. Notation is wherever possible standard. For a differentiable function , we define a step of the gradient method starting from a point as , where is the step size and is the identity operator. Then, steps are indicated as,

| (7) |

We let also when needed.

We further indicate with the proximal operator,

| (8) |

Finally, spaces are indicated as , probability distributions are calligraphic, i.e., , matrices and vectors are boldfaced, e.g., , operators are in sans-serif, e.g., , constants are in standard roman.

2 Problem formulation and assumptions

Let us now consider the sequence of problems,

| (9) |

with a strongly convex, doubly differentiable and smooth cost function uniformly in and a generic convex function . Let us also introduce the shorthand notation , , and . Notice that, as done in stochastic optimization, the data point is supposed to be a random vector drawn from the distribution .

First, let us derive a discrete-time dynamical system on how the optimizers evolve in time. Quite naturally, one could be attempted at discretizing (5), but the presence of the inverse of the Hessian and the derivative of the data stream makes it quite cumbersome, especially if one has then to linearize it for an extended Kalman filter.

Instead we use a Bayesian approach, assuming that we have a (noisy) prior on how the data stream evolves, and we start from what we can be computed algorithmically. Let us denote with an approximation at time of . Noisy prior on how the data evolves and how the gradient evolves can come from linear filters, or more sophisticated neural network models, or kernel models (see also [26] for what they call predictable sequences). For now think about one of the simplest model: (obtained via an extrapolation technique [27]).

Then, we use an algorithmic view. At time , we would like to solve

| (10) |

yet it is not possible with data up to time . So, we introduce the noisy dynamical system

| (11) |

where means the application of the proximal gradient method of step size for times, and is the process error. The error comes both from a modelling error (truncating after iterations), and from the noisy predicted gradient . We will see how to characterize the error later, but for now it is useful to keep in mind that is not-zero mean in general. If the gradient were exact and , then Equation (11) would solve (10) with no noise ().

The “pseudo”-dynamical system (11) will be our computationally affordable nonlinear dynamical model.

In par with (11), we introduce a measurement equation,

| (12) | |||||

where is the number proximal gradient steps, is the correction step size, and is a noise term coming from the noisy character of and it is in general not zero-mean. Again, on the optimizer trajectory.

The right-hand side of (12) represents the fixed-point residual of our -steps proximal gradient method, that we use to compute the measurement.

2.1 Properties, requirements of the gradient approximators

Before going further, it is useful to understand a bit better the properties of the gradient approximations and . Both are attempting at approximating , but there are a few differences.

The first is based on data available up to time and it is in general a biased estimator. This is not a problem per se, since even in deterministic prediction-correction methods, the predicted gradient is in general a biased prediction.

Example 1 (Recurring stochastic example)

Consider the case in which is linear in (e.g., for linear models and Least-Squares estimators, for example when for a given matrix ), and more generally the case in which:

with strongly convex and smooth. In this case, let .

Further, suppose is generated by a nominal (doubly differentiable in ) trajectory to which we add a Gaussian zero-mean noise at each sampling time . And in particular, set , with for a given time-varying covariance matrix . We also know that , and we set .

Choose the extrapolation prediction: . Consider a nominal trajectory for which we assume the bounds:

| (13) |

Then, in the Appendix we show that:

∎

The second estimator, meaning using instead of , is evaluated with data coming at time and it is unbiased [11].

For the two approximations we require the following.

Assumption 1

Let the cost function be -strongly convex and -smooth in uniformly in (i.e., for all ). The chosen gradient predictor is then -strongly monotone and -Lipschitz in for all ’s.

Assumption 2

The noise processes and gradient prediction errors are bounded as follows:

for finite scalars and , for all , and (b) for all .

Assumption 1 is often required for time-varying optimization [5]. The assumption on the predictor is also reasonable, for instance is verified in Example 1, and with Taylor-based and extrapolation-based predictions [27].

For Assumption 2: Property is in par with some deterministic and stochastic assumptions appeared in past years. For example, it can be seen in parallel with the quality of the hint or predictable sequences in [26, 28]. In Example 1, Property is verified with . Stochastic versions of Property have appeared, e.g., in [8], with example-based constructions for determining a suitable . Property is also commonly asked in stochastic frameworks [6]. Usually, one asks that , but due to the convexity of and Jensen’s inequality, Property is implied by the squared one (in fact ). For us Property can be time-varying. In Example 1, Property is verified with . Finally, Property can be tightened to be valid only on the algorithm iterates , and interpret it as gradient noise with a small theoretical effort [7].

3 An extended Kalman filter

We are now ready to derive a filter to track the filtered optimizer trajectory . Since the linear system and the measurement equations are nonlinear, we will use an extended Kalman filter. For it, we require that both and are differentiable with respect to , and we will require knowledge of the covariance of the noise processes at all time instances. We will also assume that , to be able to differentiate, which puts us in an unconstrained differentiable problem setting, where we use gradient (the proximal operator is the identity in this case).

Recall the notation defined in (7), indicating the effect of steps of the gradient method, or an approximate gradient if is substituted with . Define the derivative quantities (we drop the mention to , since it does not exist in this case),

| (14) | |||||

| (15) |

We also let and be the covariance matrices of the noise processes and , respectively.

With this in place, the extended Kalman filter (TV-EKF) represented in Algorithm 1 is able to filter and track the optimizer trajectory . We notice that we have presented the filter with correction first, to highlight the standard workflow within a sampling period. We notice also that the filter can be extended to include a filtering process for the data stream , if a dynamical model for it is available.

Algorithmically, the presented TV-EKF requires several computations. In the correction step, it comprises the computation of the Hessian of at various points for determining and taking a matrix inverse for determining . The update for requires also gradient steps. In the prediction pass, the filter includes a process to determine any prediction , computing its derivatives, and gradient steps. Considering a -dimensional state, and letting be the computational effort to determine the gradient, Hessian, predicted gradient, and its derivatives, then the overall computational complexity of TV-EKF is .

We will study the empirical performance of TV-EKF in Section 6, but we close here with some remarks.

Remark 1 (Prediction-Correction methods)

We can see how is updated as

| (16) |

and if we let , then we obtain back the standard prediction-correction methods.

Remark 2

The TV-EKF algorithms that is presented here could be extended to equality-constrained optimization problems, once formulated as saddle-points, but we leave this for future endeavors.

The TV-EKF algorithm that we have presented offers several advantages, and above all the ease of implementation. However, from an optimization perspective, it is lacking in good convergence guarantees222Besides the fact that the prediction and correction steps represent contractive operators for ., and from a noise perspective, we do not have a good intuition or recipe on how to set the covariances in meaningful ways.

This, combined with the fact that TV-EKF will not work for non-smooth costs, pushes us to look beyond to a more general setting. However, before moving on, we give some intuition on why the TV-EKF does perform well empirically in the numerical settings that are presented in Section 6.

Proposition 1 (Equivalence to a damped Newton’s step)

When the noise on the measurement is negligible, i.e., , and we take only one step of correction , then TV-EKF is a damped Newton’s method, with update

∎

Proposition 1 implies that TV-EKF includes second-order information and could be thought of as a stochastic quasi-Newton method. In this sense, if the noise covariances are well estimated, or small, then TV-EKF is expected to do better than standard prediction-correction methods that only use first-order information. This is not surprising, but the connection Kalman-Newton in optimization is interesting.

4 The general case

The standard extended Kalman filter can be easily derived when the cost is differentiable. We generalize now our filter design to the case in which one has also the term in the cost, modeling constraints and non-smooth regularizations.

Reconsider the dynamical system (11) in par with the measurement equation (12). Under Assumption 1, from standard operator theory, we know that if and are chosen small enough, and in particular333This is due to the fact that is -strongly monotone and -Lipschitz, but not a gradient per se. Sharper conditions can be derived if would be a gradient, like in the correction case, for which we can choose . , both the prediction and the correction represent contraction operators, which converge to their respectives unique fixed points. In particular, their contraction factors are [29]:

| (17) |

for prediction and correction operators, respectively.

4.1 A static gain filter

With our dynamical model (11) and measurement equation (12), we are now ready to build our filter. Here, since the model and the measurements are non-differentiable equations, we will focus on static gain filters, that can be computed off-line, before running the time-varying algorithm. We let .

Therefore, we start by considering the update equation

| (18) |

consisting of running a prediction and then correcting it via the correction . As mentioned in Remark 1, by setting , we obtain back the standard prediction-correction methods.

Algorithm 2 makes the update explicit along with all the involved computations, for a generic choice of and . As we can see the computational complexity here does not involve matrix inversions, but it adds proximal mapping computations. If the proximal step is easy to perform compared to the other computations, then the complexity is , which is better than TV-EKF, as expected.

As mentioned before, in this paper, we are interested in designing in such a way to reduce the tracking error of the sequence , and in particular: which would deliver the smallest ?

4.2 Scalar, worst-case convergence results

We start by analyzing the easier case of determining the best scalar gain , for the update,

| (19) |

While this is restrictive in practice, it will give us some intuition on the general problem. Also, by restricting in , we are considering all convex combinations of prediction and correction phases. The latter is important if represents a feasible set and we want the sequence to be feasible for every . We have the following Theorem.

Theorem 1

Let Assumptions 1-2 hold. Assume furthermore that the optimizer trajectory is bounded as,

| (20) |

Choose . Consider Algorithm 2 with the selection of , , leading to the update (19), and its sequence . Define functions and as:

Recall the contraction parameters (17) and choose the number of prediction and correction steps and such that . Then, by calling , the asymptotic error is upper bounded as,

| (21) |

with , and

Finally, under the setting of Example 1, , and . ∎

Theorem 1 captures the asymptotic tracking error of the proposed TV-CONTRACT algorithm, when . The requirement (20) is standard, assuring that the trajectory is regular enough to be tracked, see [5]. The condition is verified, whenever , since with the choice of .

For , Theorem 1 extends [27, Proposition 5.1] to stochastic settings and [8, Theorem 2.7] to settings with multiple prediction and correction steps.

The question we have for filter design is how to tune to lower the asymptotical error, given all the rest fixed?

4.3 Tuning

The filter design problem can be now formulated as,

| (22) |

Problem (22) is a linear-fractional programming, that can be solved by transforming it into a linear program, once all the coefficients are fixed. We do not give the details of this, since easily found in standard books [30, Ch. 4.3.2]. Nonetheless we report an interesting fact on the nature of the solution.

Proposition 2

The solution of the tuning problem (22) is either , , or in a special case, any . ∎

What Proposition 2 says is that from a worst-case perspective (i.e., from an asymptotic tracking error) we are better off to either just do predictions, or just do prediction-correction (and in a very special case, we can take any choice). The choice is made a priori, from the size of the prediction or correction errors (see the proof for exact conditions).

This is hardly satisfactory. We see next how to extend the above to a generic matrix gain , via dissipativity theory, which has a richer behavior.

5 Dissipativity theory and filter design

We move now to the general case of designing a matrix in an optimal fashion. We will be using recent tools from dissipativity theory applied to optimization algorithm design, and we were particularly inspired by [18, 19].

5.1 Filter design

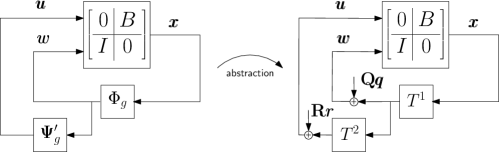

To start our filter design, we need to recast Algorithm 2 as a block diagram, where the optimization algorithmic updates are interpreted as nonlinear blocks and modeled as quadratic constraints. Consider then noisy algorithmic update,

| (23) |

where and are noise terms, whose expected norm is bounded, as we will see shortly, and are tuning matrices that can model the relative amount of error or correlations.

The algorithmic choice (26) is an abstraction of Algorithm 2, as we can see in Figure 1, where and are the ideal operators representing the ideal prediction and correction steps, respectively, and both with fixed point . The fact that, technically, one should consider , and the noise terms and are in fact correlated, since should depend on a noisy prediction, can be ignored here, since we will only look at worst-case performance guarantees, from bounded errors to bounded output.

Under Assumptions 1 and 2, with the same notation of Theorem 1 and from the proof of [27, Proposition 5.1] with , we can bound,

| (24) |

On the other hand,

| (25) |

so we can look at bounded errors as and .

Similarly for the error term , we can look only for bounded errors as .

In particular, we consider , and model the matrices to have their largest singular value at and , respectively.

For the sake of ease of notation, in (26), we define matrices , and the nominal input and error signal as,

| (26) | |||

| (27) |

and . We also introduce point-wise-in-time quadratic constraints for and as,

| (28) |

| (29) |

with and , which are due to the contracting properties of and , respectively. With this in place, convergence and asymptotic tracking error performance can be formulated as follows.

Theorem 2

Consider Algorithm 2 and its abstraction (27), to find and track the filtered optimizer trajectory of the time-varying stochastic optimization problem . Assume that the optimizer trajectory varies in a bounded way as , for all and . Let Assumptions 1-2 hold as well.

Introduce matrix and , scalars , in addition to supporting scalars , and consider the tuning matrix . For any fixed scalar , by solving the convex problem444For readability, we indicate in blue the decision variables.

| (30c) | |||||

| subject to | (30o) | ||||

then Algorithm 2 with generates a sequence that converges as,

| (31) |

Furthermore, for any fixed , solving Problem (30) diminishes the asymptotical error . ∎

Theorem 2 describes how to best tune the matrix to minimize the asymptotic tracking error. In particular, doing a grid search on , one can identify the best that minimizes the worst-case asymptotical error bound. Two remarks are in order.

First the convex problem (30) grows linearly in the dimension of the problem . However, if the matrices and have some particular structure (i.e., diagonal, block diagonal), we can reduce the problem size considerably. In the case of , , then choosing , the problem becomes independent of the problem size , as it happens in other examples [22].

Second, the matrices and are gateways through which one can include variable correlations and dependency, which is not present in a standard prediction-correction algorithm, nor in the scalar worst-case convergence tuning .

5.2 LPV filter design

The presented filter design, captured by the conditions in Theorem 2, could suffer from conservatism, since the matrices and are selected as worst cases. For example, we have modeled at having its largest singular value at . In practice, one could wish to model these matrices as parameter-varying, and directly dependent on how the data changes in time.

We propose here an LPV filter design that accomplishes this task and reduce conservatism of the design process. We focus on a simplified setting to convey the basic ideas, and the reader is left to generalize the approach.

Consider the change in time of the data , and let be a normalized parameter that capture this change. For example, we let . We then consider as an affine parameter-varying matrix: . We consider here a static for simplicity, thereby assuming that the change in the data only affects the prediction accuracy, which is reasonable to assume (and easy to lift if needed).

In parallel, we will be looking for an affine parameter-varying Lyapunov matrix , and a parameter-varying filter gain matrix . The following theorem is then in place.

Theorem 3

Consider Algorithm 2 and its abstraction (27), to find and track the filtered optimizer trajectory of the time-varying stochastic optimization problem . Assume that the optimizer trajectory varies in a bounded way as , for all and . Let Assumptions 1-2 hold as well.

Introduce matrix function and , scalars , in addition to supporting scalars , and consider the tuning matrix function . Assume that and that the value of at subsequent time step is upper bounded as . For any fixed scalar , by solving the problem

| (32c) | |||||

| subject to | (32s) | ||||

then Algorithm 2 with generates a sequence that converges as,

| (33) |

Furthermore, for any fixed , solving Problem (30) diminishes the asymptotical error . ∎

Theorem 3 describes parametric conditions for Algortihm 2 to converge to the optimizer trajectory in expectation and within an error ball. We remark here the extra constraint , which requires some explanation.

As one can see in the proof of Theorem 3, the key step in proving convergence of the algorithm is to ensure that a Lyapunov function decreases at subsequent times. The Lyapunov function that we consider is , and therefore we have to deal with matrices at subsequent times. By imposing , we can write however,

from which we can derive Theorem 3 and this renders the derivation of a solvable program easier.

The constraint induces conservatism in the design, but in all our numerical simulations we found it to be redundant (meaning that the optimal was with or without the constraint), and therefore not conservative in our application. We remark that a more correct approach would be to consider both extremes ( and ) as done in [25] and remove , but this would lead to an ambiguous definition of and an harder problem to solve.

Another possible approach is to remove and to consider only slowly changing parameters, for which . Since in our simulations , we have preferred to focus on the former approach. Finally, note that considering a is not totally unreasonable, since we can assume that increasing , the convergence performance would be negatively affected.

For fixed , the problem to be solved is infinite dimensional (yet convex once is fixed). We recall that the constraints in (32s) are quadratic in , due to the product with .

A possible way to solve problem (32) is to discretize the domain with a uniform grid and impose (32s) for all the points of the grid. Another possible way is to introduce another variable , and render affine (32s). A more sophisticated way to proceed is to introduce a more conservative yet convex condition in , hinging on the concept of matrix sum of squares.

Definition 1

Let be a symmetric matrix of polynomials of degree up to in the variable . A matrix is sum of squares (MSOS) if there exists a finite number of symmetric matrices of polynomials such that

The decomposition implies that for all . The constraint “ is MSOS” is convex.

We are now ready for the following result.

Theorem 4

Theorems 3 and 4 describe an LPV design strategy for our filter gain design. This is a particular choice due to the affine parameter-varying and static . More complex choices can be made (relatively) straightforwardly following the same pattern of the presented theorems. We now look at some numerical simulations.

6 Numerical simulations

We focus now on showcasing the performance of the proposed algorithms on a real dataset and problem stemming from ride-hailing. We obtain trips data from the New York City dataset555Open data from the NYC Taxi and Limousine Commission Data Hub. for the yellow taxi cab in the month of November 2019, totalling over millions trips. We group the trips in minutes intervals and divide the trip requests among different ride-hailing companies (such as taxi cab, Uber, Lyft, etc.). The trip requests are divided randomly among the companies in a way that different companies do not have the same number of requests.

In the modern context of mobility as a service with ride-hailing orchestration [31], it makes sense for the city to provide software platforms to decide caps on the number of vehicles that each company can put on the streets depending on trading-off satisfying the demand and limiting traffic. A natural optimization problem that a city can formulate is

| (35) |

where for each represents the upper limit on vehicles on the roads for company . The constraint represents box constraints on the number of allowed vehicles. The term multiplies the trip requests for company at time , to be able to match most of the requests as possible. The logistic term with is a regularization to make the cost non-quadratic but still convex and favor a smaller number of vehicles on the roads. Finally, the coupling term is set to have a similar regulation among different companies. For the sake of the simulations, we take , and we sample Problem (35) at every minutes. We simulate also the ground truth considering a smoothed version of the data.

6.1 Unconstrained case

We start by considering the unconstrained case, where , and we look at different noise regimes and algorithms.

As for the algorithms, we consider our TV-EKF (Algorithm 1), a standard prediction-correction [27], and the stochastic prediction-correction version of [8]. For the latter, with their optimal choice of window size and weights for two-point evaluation, we can see that it is equivalent to the AGT algorithm of [32], i.e., exact prediction with Hessian inversion, but with a finite difference evaluation of .

For the three algorithms, we consider different choices of prediction steps and correction steps . For the stochastic prediction-correction version of [8], prediction is exact, so is not a free parameter. We simulate three noise regimes:

The case of very good prediction . For this, generates as predictive signal a random signal around the ground truth with variance . We use for the correction the true data stream. This case represents a realistic scenario of having a very good predictor (based on accurate historical data and, e.g., on a periodic Kernel method). This could be typical in ride-hailing systems.

The case of poor prediction . For this, generates as predictive signal a random signal around the ground truth with variance . We use for the correction a convex combination of the true data stream and the ground truth (weighting the true data ). This case represents a potential scenario of situation in which the system transitions (e.g., a lock-down happens) and we have poor prediction. This is in general less typical, since prediction can be built online on current data, based, e.g., on extrapolation, but still interesting to analyze.

The case of generated by the true data based on an extrapolation-based prediction [27], and correction also based on true data. We label this case . The error between the true data and the ground truth has variance , and the prediction . We design and accordingly, also taking into account that the data streams are correlated, and therefore are full.

Table 1 displays the results obtained in these settings. As we can see, Algorithm 1 performs the best by a significant margin, when prediction is accurate (). When prediction is poor (), then Algorithm 1 behaves close to a damped Newton’s method, which significantly outperforms a standard prediction-correction algorithm, but it is in par with its stochastic version (since the latter still uses the very accurate data stream to built its exact prediction).

Finally, for the setting of , then all the three methods perform very similarly, which is almost expected since taking prediction, or prediction and then correction incur the same “error”, so any combination could achieve similar results. In this case, Algorithm 1 chooses a .

The results in Table 1 support Algorithm 1 as an algorithm that can automatically tune prediction and correction; based on this tuning it can be significantly better than the competitors; and in the worst case it performs as state-of-the-art methods. We finally remark that the good prediction case is considered to be typical in this application scenario, and that the method from [8] could also be updated by designing an EKF for it, in the same way we did for the standard prediction-correction.

| Regime | Algorithm | |||||||||

| Extrap. P-C, [27], | Stoch. P-C [8], | TV-EKF: Algortihm 1, | ||||||||

| 80.0 | 47.2 | 134.0 | 118.9 | 160.1 | 151.1 | 70.1∗ | 10.8∗ | 61.2∗ | 14.0∗ | |

| 26.3 | 17.0 | 49.7 | 44.7 | 59.9 | 56.0 | 20.2 | 3.8 | 17.7 | 4.6 | |

| 111.3 | 64.7 | 183.9 | 163.5 | 219.1 | 206.6 | 107.1 | 14.9 | 90.8 | 19.3 | |

| 90.5 | 195.7 | 19.4 | 48.6 | 11.2 | 8.0 | 7.5 | 7.6 | 7.5 | 7.5 | |

| 66.3 | 148.7 | 12.7 | 32.2 | 4.1 | 2.9 | 2.8 | 2.9 | 2.8 | 2.8 | |

| 109.3 | 236.4 | 23.8 | 60.6 | 14.3 | 10.6 | 10.4 | 10.4 | 10.5 | 10.5 | |

| 135.0 | 162.4 | 144.7 | 149.5 | 160.1 | 151.1 | 141.7 | 152.4 | 149.5 | 150.2 | |

| 47.8 | 60.9 | 53.6 | 55.5 | 59.9 | 56.0 | 52.0 | 56.4 | 56.4 | 56.4 | |

| 185.7 | 225.9 | 198.0 | 204.3 | 219.1 | 206.6 | 193.4 | 210.6 | 205.0 | 206.0 | |

6.2 Constrained case

We analyze now the constrained case, for which we set and . These constraints are not overly restrictive, but the point here is to see how our BMI-based method performs with respect to a standard prediction-correction method in different scenarios. Here, the stochastic variant [8] cannot be applied, but one could use the methods in [5] with exact prediction and finite-difference computations for . We do not look into that, since typically these methods are more computationally demanding.

The settings we investigate are similar to the unconstrained case, with the difference that we use our second algorithm TV-CONTRACT with a static generated via Problem (30), and uniform grid-search on . We also consider two cases for , the first has and , the second and . In both cases, as before, are full.

In Table 2, we displays the results obtained in these settings. As we can see, Algorithm 2 has the best advantage when prediction is accurate and can be chosen different from . In general, the performance of Algorithm 2 is comparable with the competition, unless there is a clear advantage to choose a different from gain. In this latter case, the performance gain can be significant. In Table 2, we have also added the selected best , which is full whenever we use the sign, with diagonal elements close to the indicated values.

The results in Table 2 support Algorithm 2 as an algorithm that can automatically tune prediction and correction; based on this tuning it can be better than the competitors; and in the worst case it performs in par with state-of-the-art methods. We finally remark that the good prediction case is considered to be typical in this application scenario.

For display purposes, Figure 2 illustrates the different trajectories for one of the five companies during Thanksgiving week of the selected month of November 2019, for the case and .

| Regime | Algorithm | ||||||||

| Extrapolation P-C, [27], | TV-CONTRACT: Algorithm 2, | ||||||||

| 68.7 | 58.2 | 84.3 | 79.7 | 71.1 | 51.3∗ | 73.0∗ | 54.6∗ | ||

| 25.3 | 20.3 | 33.5 | 32.6 | 32.8 | 9.0 | 28.9 | 15.5 | ||

| 102.4 | 93.1 | 122.1 | 117.1 | 103.1 | 94.4 | 106.3 | 92.4 | ||

| 88.6 | 143.2 | 54.5 | 66.9 | 88.6 | 143.2 | 54.5 | 66.9 | ||

| 58.1 | 80.3 | 16.4 | 34.1 | 58.1 | 80.3 | 16.4 | 34.1 | ||

| 119.6 | 200.2 | 95.5 | 99.1 | 119.6 | 200.2 | 95.5 | 99.1 | ||

| 85.4 | 93.3 | 87.7 | 89.2 | 85.3 | 94.2 | 87.7 | 89.2 | ||

| 32.5 | 34.4 | 34.2 | 34.9 | 32.3 | 34.4 | 34.2 | 34.9 | ||

| 118.8 | 135.6 | 126.3 | 128.8 | 118.7 | 137.7 | 126.3 | 128.8 | ||

| 68.3 | 58.9 | 84.1 | 79.3 | 68.3 | 56.8 | 84.1 | 68.7∗ | ||

| 25.3 | 23.0 | 33.3 | 32.2 | 27.1 | 22.1 | 33.3 | 28.1 | ||

| 101.5 | 92.2 | 122.0 | 116.7 | 101.3 | 91.6 | 122.0 | 103.1 | ||

| Regime | Algorithm | ||||

| TV-CONTRACT-LPV: Algorithm 2, | |||||

| 85.5 | 93.9 | 87.3† | 89.8 | ||

| 32.0 | 34.3 | 33.7 | 35.1 | ||

| 118.6 | 136.7 | 125.4 | 129.2 | ||

| 70.9 | 56.9 | 74.4†∗ | 65.3† | ||

| 32.7 | 22.5 | 29.3 | 26.6 | ||

| 102.7 | 94.2 | 108.9 | 99.5 | ||

6.3 Variable case

We finish the simulation assessment showing the tracking results obtained solving Problem (32) for an affine parametric-varying . In particular, we let and , where is numerically defined as before, and run Algorithm 2 on all the four cases that we have looked at in Table 2. We solve Problem (32) by uniform gridding with points. As mentioned, in our case .

In Table 3, we report the results for the cases, since we do not observe any substantial difference for the other cases of Table 2. We indicate in bold if we have a gain w.r.t. a static gain, and with a dagger, if we have also a gain w.r.t. the state of the art. We also report how the maximal element of the diagonal of changes in time in a selected week.

As we can see, the results are very similar to the static results, but the gains can be important in some cases. As we see, the filter gain does not change over a wide range. However, it appears that even these small changes are enough to reduce the asymptotical error in selected scenarios, and behaving in par with the static approach in the others. As one can infer, parametric-varying gain design does depend on the modelling choices for and , and one could expect possibly more performant results in the case of more complex dependencies on . We leave this analysis for future endeavors.

7 Conclusions

We have discussed several methods to generalize time-varying optimization algorithms to the case of noisy data streams. The methods are rooted in the intuition that prediction and correction can be seen as a nonlinear dynamical system and a nonlinear measurement equation, respectively. This leads to extended Kalman filter formulations as well as contractive filters based on bilinear matrix inequalities (BMI’s). Numerical results are promising, even when using possibly conservative BMI conditions.

Appendix A Proofs

A.1 An additional example

Example 2 (Deterministic example)

Consider a deterministic method with an extrapolation predictor [27], meaning: , where now is deterministic. Assume is strongly convex and smooth, uniformly in , assume that the Hessian of does not depend on , and assume the following bounds on data and mixed derivatives:

| (36) |

Then we have that

∎

Proof.

By using the higher-derivatives Faà di Bruno’s chain rule:

| (38) |

from which the thesis follows. ∎

A.2 Derivations for Example 1

We choose to write as a short-hand notation, in this proof only.

By linearity of with respect to the parameter , and the linearity of the expectation, we can write

We now use the Triangle inequality, the result (38), and the mean value theorem for the nominal trajectory, to upper bound the last inequality as

from which the first claim is proven.

For the second,

as claimed. ∎

A.3 Proof of Proposition 1

Consider in Algorithm 1, as well as a negligible . Then, we can simplify the Kalman gain as:

Therefore, the state update reads

from which the thesis is proven. ∎

A.4 Supporting results for Theorem 1

Lemma 1

Proof.

Choosing and under Assumption 1, we know that the prediction is a contractive operator and its fixed point exists and it is unique. By implicit function theorems, see for instance [33, Theorem 2F.9] and [27, Theorem B.1 and Lemma 4.1], being careful to being strongly monotone and not generally the gradient of a strongly convex function, then,

| (39) |

Passing in expectations, and by using Assumption 2, the first thesis follows.

As for the second statement, it follows from the derivations of Example 1. ∎

Lemma 2

Let Assumptions 1-2 hold. Choose . Consider the prediction update with prediction steps, and the correction update with correction steps. Let the contraction factors be defined as in (17). Then, the following error bounds are in place.

| (40) | |||||

| (41) |

where .

Furthermore, under the setting of Example 1, and . ∎

Proof.

Choosing and under Assumption 1, we know that the prediction and correction are contractive operators and their fixed points are unique.

For the prediction part, by using Equation (39), we obtain,

| (42) | |||||

and passing in expectation with Assumption 2 the claim is proven.

For the second claim, we can write

| (43) |

Call . Then each proximal gradient step will incur in an additive error, where will be different at each step:

| (44) |

Passing in expectation, with Assumption 2 and the sum of geometric series, the second claim is also proven. ∎

A.5 Proof of Theorem 1

The proof follows the one of [27, Proposition 5.1], combining Lemma 1 and Lemma 2. Start by considering , so a classical prediction-correction method. We can use [27, Proposition 5.1], with , and the correction with an additional error term to say,

| (45) |

Looking at prediction only, , we obtain instead,

| (46) |

For a generic , we can combine the errors as

| (47) |

Then, we can recursively compute the error via geometric series summation. By passing through expectations, the claim follows.

A.6 Proof of Proposition 2

For Problem (22), we look at the minimum of the curve,

| (48) |

For our problem , , while can be positive, negative, or zero. Since function is a linear-fractional function in one dimension, for , function is monotone. In particular, for the function is decreasing (increasing), leading to the optimal choices of . The condition means,

For the special case , and any is optimal. ∎

A.7 Proof of Theorem 2

To impose convergence and performance, we look at the following matrix condition, featuring semidefinite matrix , the scalar , and matrix which is implicit in :

| (49) |

where means that what is post-multiplied is also pre-multiplied transposed and , . Condition (49) combines the system, the quadratic constraints (i.e., the contractivity) via an -procedure, and the performance criterion.

We now develop the multiplications, we let , and pre and post multiply with the vector and we obtain,

| (50) |

Define the error and the drift , then

| (51) |

Taking the square root of both sides, since

| (52) |

Let , also note that since . Since we impose without loss of generality (since the problem remains unchanged for any scalar scaling), then and . Here the equality sign is due to the fact that we minimize over .

Similarly, . Then, iterating on , and taking the expectations, we obtain,

| (53) | |||

| (54) |

As such, for any fixed , minimizing minimizes the asymptotic tracking error. Furthermore, since for , we know that . So our cost majorizes the asymptotical error and therefore by minimizing our cost, we diminish the latter (notice, we do not minimize the latter, in general, since we have a constrained problem).

To finish the proof, we need to transform (49) into (30o). We develop the matrix multiplications, and we observe that the resulting matrix is block diagonal. The first block is . The second block is

| (55) |

Expand into and introduce the variable . Then, taking the Schur’s complement, we obtain , from which the thesis. ∎

A.8 Proof of Theorem 3

The proof follows the proof of Theorem 2. We focus here on the different parts.

Starting from Eq. (49), we adapt the first term to:

| (56) |

The bottom diagonal leads to conditions

| (57) | |||

| (58) |

which needs to be valid for the extreme points , since affine in . However, given the constraint , the above simplify into (32s) and (32s), respectively.

Bu using again the constraint , the upper diagonal can be upper bounded as,

| (59) |

so imposing a condition on the latter, would imply a condition on the former. In particular, adapting (55), the condition

| (60) |

would imply a similar condition on , thus the upper diagonal of (56), and for proof of Theorem 2, convergence of the algorithm as indicated in Theorem 3.

Condition (60) leads to condition (32s), by Schur complement and dropping the now-redundant subscript .

We remark here the importance of the constraint , without which we would need two upper bounds in (59), one for and one for , which would render the substitution ambiguous, and determining harder.

∎

A.9 Proof of Theorem 4

The condition is equivalent to . Then we apply the generalized -procedure as in [25].

∎

References

- [1] T. H. Hamam and J. Romberg, “Streaming solutions for time-varying optimization problems,” IEEE Transactions on Signal Processing, vol. 70, pp. 3582–3597, 2022.

- [2] M. M. Zavlanos, A. Ribeiro, and G. J. Pappas, “Network Integrity in Mobile Robotic Networks,” IEEE Transactions on Automatic Control, vol. 58, no. 1, pp. 3 – 18, 2013.

- [3] E. Dall’Anese and A. Simonetto, “Optimal Power Flow Pursuit,” IEEE Transactions on Smart Grid, vol. 9, no. 2, pp. 942 – 952, 2018.

- [4] E. Dall’Anese, A. Simonetto, S. Becker, and L. Madden, “Optimization and learning with information streams: Time-varying algorithms and applications,” IEEE Signal Processing Magazine, vol. 37, pp. 71–83, 2020.

- [5] A. Simonetto, E. Dall’Anese, S. Paternain, G. Leus, and G. B. Giannakis, “Time-Varying Convex Optimization: Time-Structured Algorithms and Applications,” Proceedings of the IEEE, vol. 108, no. 11, 2020.

- [6] J. Zhang, H. Lin, S. Das, S. Sra, and A. Jadbabaie, “Stochastic optimization with non-stationary noise,” arXiv:2006.04429v2, 2020.

- [7] J. Cutler, D. Drusvyatskiy, and Z. Harchaoui, “Stochastic optimization under time drift: iterate averaging, step-decay schedules, and high probability guarantees,” in Advances in Neural Information Processing Systems. Advances in Neural Information Processing Systems, 2021.

- [8] S. Maity, D. Mukherjee, M. Banerjee, and Y. Sun, “Predictor-Corrector Algorithms for Stochastic Optimization under Gradual Distribution Shift,” arXiv:2205.13575, 2022.

- [9] B. T. Polyak, Introduction to Optimization. Optimization Software, Inc., 1987.

- [10] M. Fazlyab, S. Paternain, V. Preciado, and A. Ribeiro, “Prediction-Correction Interior-Point Method for Time-Varying Convex Optimization,” IEEE Transactions on Automatic Control, vol. 63, no. 7, 2018.

- [11] A. Flaxman, A. Kalai, and H. McMahan, “Online Convex Optimization in the Bandit Setting: Gradient Descent without Gradient,” in Proceedings of the ACM-SIAM Symposium on Discrete Algorithms. Vancouver, Canada: Proceedings of the ACM-SIAM Symposium on Discrete Algorithms, January 2005, pp. 385 – 394.

- [12] J. Duchi, E. Hazan, and Y. Singer, “Adaptive subgradient methods for online learning and stochastic optimization,” J. Mach. Learn. Res., vol. 12, p. 2121–2159, 2011.

- [13] M. Schmidt, N. Le Roux, and F. Bach, “Minimizing finite sums with the stochastic average gradient,” Mathematical Programming, vol. 162, no. 1, pp. 83–112, 2017.

- [14] J. Duchi, Introductory lectures on stochastic optimization. The mathematics of data, 2018.

- [15] O. Besbes, Y. Gur, and A. Zeevi, “Non-stationary Stochastic Optimization,” Operations research, vol. 63, no. 5, pp. 1227 – 1244, 2015.

- [16] L. Lessard, B. Recht, and A. Packard, “Analysis and design of optimization algorithms via integral quadratic constraints,” SIAM Journal on Optimization, vol. 26, no. 1, pp. 57–95, 2016.

- [17] Z. E. Nelson and E. Mallada, “An integral quadratic constraint framework for real-time steady-state optimization of linear time-invariant systems,” in 2018 Annual American Control Conference (ACC). 2018 Annual American Control Conference (ACC), 2018, pp. 597–603.

- [18] M. Colombino, E. Dall’Anese, and A. Bernstein, “Online optimization as a feedback controller: Stability and tracking,” IEEE Transactions on Control of Network Systems, 2019.

- [19] S. Hassan-Moghaddam and M. R. Jovanović, “Proximal gradient flow and Douglas–Rachford splitting dynamics: Global exponential stability via integral quadratic constraints,” Automatica, vol. 123, p. 109311, 2021.

- [20] C. Scherer and C. Ebenbauer, “Convex synthesis of accelerated gradient algorithms,” SIAM Journal on Control and Optimization, vol. 59, no. 6, pp. 4615–4645, 2021.

- [21] S. Michalowsky, C. Scherer, and C. Ebenbauer, “Robust and structure exploiting optimisation algorithms: an integral quadratic constraint approach,” International Journal of Control, vol. 94, no. 11, pp. 2956–2979, 2021.

- [22] L. Lessard, “The analysis of optimization algorithms: A dissipativity approach,” IEEE Control Systems Magazine, vol. 42, no. 3, pp. 58–72, 2022.

- [23] F. Wu and S. Prajna, “SOS-based solution approach to polynomial LPV system analysis and synthesis problems,” International Journal of Control, vol. 78, no. 8, pp. 600–611, 2005.

- [24] C. W. Scherer and C. W. J. Hol, “Matrix Sum-of-Squares Relaxations for Robust Semi-Definite Programs,” Mathematical Programming, vol. 107, no. 1, pp. 189–211, 2006.

- [25] P. Massioni, L. Bako, and G. Scorletti, “Stability of uncertain piecewise-affine systems with parametric dependence,” IFAC-PapersOnLine, vol. 53, no. 2, pp. 1998–2003, 2020, 21st IFAC World Congress.

- [26] A. Rakhlin and K. Sridharan, “Online learning with predictable sequences,” in COLT, PMLR. COLT, PMLR, 2013.

- [27] N. Bastianello, A. Simonetto, and R. Carli, “Primal and dual prediction-correction methods for time-varying convex optimization,” arXiv:2004.11709, 2020.

- [28] A. Jadbabaie, A. Rakhlin, S. Shahrampour, and K. Sridharan, “Online Optimization: Competing with Dynamic Comparators,” in Proceedings of the Eighteenth International Conference on Artificial Intelligence and Statistics, PMLR, no. 38. Proceedings of the Eighteenth International Conference on Artificial Intelligence and Statistics, PMLR, 2015, pp. 398 – 406.

- [29] Y. Nesterov, Introductory Lectures on Convex Optimization, ser. Applied Optimization. Springer, 2004.

- [30] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge University Press, 2004.

- [31] V. Pandey, J. Monteil, C. Gambella, and A. Simonetto, “On the needs for MaaS platforms to handle competition in ridesharing mobility,” Transportation Research Part C: Emerging Technologies, vol. 108, pp. 269–288, 2019.

- [32] A. Simonetto, A. Mokhtari, A. Koppel, G. Leus, and A. Ribeiro, “A Class of Prediction-Correction Methods for Time-Varying Convex Optimization,” IEEE Transactions on Signal Processing, vol. 64, no. 17, pp. 4576 – 4591, 2016.

- [33] A. L. Dontchev and R. T. Rockafellar, Implicit Functions and Solution Mappings. Springer, 2009.