Random matrices associated to Young diagrams

Abstract

We consider the singular values of certain Young diagram shaped random matrices. For block-shaped random matrices, the empirical distribution of the squares of the singular eigenvalues converges almost surely to a distribution whose moments are a generalisation of the Catalan numbers. The limiting distribution is the density of a product of rescaled independent Beta random variables and its Stieltjes-Cauchy transform has a hypergeometric representation. In special cases we recover the Marchenko-Pastur and Dykema-Haagerup measures of square and triangular random matrices, respectively. We find a further factorisation of the moments in terms of two complex-valued random variables that generalises the factorisation of the Marcenko-Pastur law as product of independent uniform and arcsine random variables.

1 Introduction

Let be a matrix whose entries are i.i.d. complex random variables. The nonnegative definite matrix is known as random covariance matrix, and it is arguably one of the most studied models in random matrix theory with varied applications in physics, statistics and other areas [14, 20, 26].

In this paper we consider a class of random matrices, that we dub -shaped random matrices. They can be thought of as a generalisation of random covariance matrices where has the ‘shape’ of a Young diagram. Instances of these matrix models in the special case of Gaussian entries were studied by Dykema and Haagerup [11] as a tool to construct certain non commutative random variables called DT-elements, and in the work of Féray and Sniady [12] in relation to Stanley’s character formula [31] of the symmetric group. Under various names and in disguised form, Gaussian -shaped matrices recently resurfaced in connection to biorthogonal ensembles, last passage percolation and free probability [1, 6, 7, 15, 27].

2 Partitions and Young diagrams

We begin by reviewing some of the basic terminology of integer partitons and Young diagrams. A standard reference is [21, Ch. I].

A partition is any (finite or infinite) sequence of weakly decreasing nonnegative integers, . It is convenient not to distinguish between two such sequences which differ only by a string of zeros at the end. Thus, for example, we regard , , as the same partition. We denote the set of partitions by . The number of nonzero elements of a partition is called number of parts or length of , denoted by ; the sum of the parts is the weight of , denoted by . If , we say that is a partition of and we write .

The Young diagram of a partition is the set of points . A Young diagram is drawn usually as a set of boxes, not of points. In drawing such diagrams we shall adopt the English convention, as with matrices, that the first coordinate (the row index) increases as one goes downwards, and the second coordinate (the column index) increases from left to right. With this convention the diagram can be visualised as a diagram of left-justified rows of boxes where the -th row contains boxes (hence each row is not longer than the row on top of it). For instance, the diagram of is:

It is customary to identify a partition and its Young diagram with boxes.

For , we shall write to mean that the diagram of contains the diagram of , i.e. that for all . We write to mean that the box is in the diagram of , i.e. . The conjugate of a partition is the partition whose diagram is the transpose of the diagram , i.e. the diagram obtained by reflection in the main diagonal.

It is possible to define an operation of left multiplication by positive integers on the set of Young diagrams. (In fact, it is possible to define a multiplication by positive real numbers using a natural identification between diagrams and their border path when drawing a partition in ‘Russian notation’ [9].) If and , then is the partition with parts given by

In other words

The Young diagram of is a dilation of the Young diagram of obtained by replacing each box in by a grid of boxes. Hence, if , then . For instance, if , then . Its diagram is:

We use the following pictorial notation. The square partition with parts all equal to is denoted . For the staircase partition we use the symbol .

3 -shaped random matrices

Fix a field , and a partition . We denote by the set of all matrices over with entries if . The set is a -vector space. These sets appeared in applied mathematics and computer science mostly when is a finite field. See [5] and references therein. We call matrices elements of , -shaped matrices.

In the present paper we will consider spectral properties of random matrices in defined as follows. Let a nested sequence in ,

| (1) |

Let be i.i.d. complex random variables with zero mean and second moment . For let be the -shaped matrix whose -th entry is if and otherwise.

Set and consider the complex Hermitian matrix

| (2) |

Denote the eigenvalues of by , and

| (3) |

the empirical distribution of the eigenvalues of . It is natural to ask whether the sequence converges in distribution. The limit, when it exists, will be referred to as the limiting spectral distribution of .

We begin by recalling two known cases.

3.1 Full matrices

Classical Wishart matrices fit naturally in the setting of -shaped random matrices. Let . We have

Then, the -shaped random matrix is simply a matrix with i.i.d. entries , so that is a Wishart matrix. Recall that the Catalan numbers are

| (4) |

Catalan numbers count hundreds of different combinatorial objects [32], such as rooted plane trees of vertices. It is a classical result that converges in distribution to a deterministic distribution function whose moments are the Catalan numbers

| (5) |

The limiting spectral distribution is called Marchenko-Pastur distribution [22]. It is supported on the interval with density

| (6) |

3.2 Triangular matrices

Let be the staircase partition of length . Again for all . Then, is a triangular random matrix (with entry if and otherwise). These matrices where first considered by Dykema and Haagerup [11] who proved the existence of the limiting spectral distribution whose moments are

| (7) |

The Dykema-Haagerup distribution comes from a density supported on the interval and defined by (see [11, Theorem 8.9])

| (8) |

This density can be also written in terms of Lambert function, see [6, Corollary 1] (arXiv version) and [15, Remark 3.9.].

3.3 Balanced shapes

We would like to study spectral properties of -shaped random matrices for more general increasing sequence of Young diagrams. This amounts to understand the large- limit of moments

| (9) |

where is defined is (2). We expect to find a nontrivial limiting spectral distribution if the sequence ‘converges’ to a limit shape (the ‘macroscopic shape’ of ). The first moment () calculation can makes this a bit more precise,

| (10) |

Therefore, in order to have a nontrivial limit distribution one needs (at least) the length of the partitions to scale like the square root of the weight

| (11) |

Young diagrams satisfying such a growth condition are called balanced Young diagrams [9]. If we view a Young diagram as a geometric object, Eq. (11) suggests to consider sequences that, after rescaling as , tend to a limit shape .

The easiest example of balanced Young diagrams is the sequence of dilations of a fixed partition. Let and consider the sequence . For such a sequence the ratio is constant.

4 Block-shaped random matrices

Fix a positive integer , consider the staircase partition of length . Define the sequence . In this case , and for all . The matrix is a block-shaped random matrix with nonzero blocks of size .

Example 1.

For , we have

Let be the empirical distribution (3) of the eigenvalues of .

Theorem 1.

Let . Then, the sequence converges, with probability , to the deterministic distribution with moments

| (12) |

The limiting moments (multiplied by ) have a combinatorial interpretation. They enumerate plane trees whose vertices are given labels from the set in such a way that the sum of the labels along any edge is at most . These combinatorial object were invented by Gu, Prodinger and Wagner [17], extending a previous definition by Gu and Prodinger [16].

Definition 1.

A -plane tree is a pair , where is a plane tree, and is a colouring such that whenever .

Proposition 1 (Gu, Prodinger and Wagner [17]).

The number of -plane trees on vertices is

| (13) |

For recent refined formulae see [29]. The integers are generalised Catalan numbers. Here are a few values of them.

The sequences for are the entries A000108, A007226, A007228, and A124724 in The On-Line Encyclopedia of Integer Sequences [28].

Remark 1.

For , the moments coincide with the Catalan sequence

| (14) |

For , is a ‘three-blocks’ matrix model studied by Flynn-Connolly [13] who proved that the moments are . The sequence entry A005132 in The On-Line Encyclopedia of Integer Sequences.

For large , we recover the moments (7) of the Dykema-Haagerup measure,

| (15) |

We now present a few results on the limiting measure. They are motivated by the observation (by Ledoux [18]) that a semicircular variable is equal in distribution to the product of the square root of a uniform random variable and an independent arcsine random variable. We denote by a random variable uniformly distributed in the interval , and simply by a random variable uniformly distribute in the unit interval . With we generally denote a beta random variable with parameters ; it has support in the interval , with density

| (16) |

where is the Euler Gamma function. Let be a random variable with Marchenko-Pastur distribution (6). Then, is equal in distribution to the product of a uniform random variable on the interval and an independent arcsine variable in the interval . In formulae:

| (17) |

This is equivalent to the above mentioned factorisation of semicircular variables [18]. Indeed, if are independent and uniformly distributed on , we can write

| (18) |

where . The random variable is the rescaled squared projection of a uniform point on the unit semicircle, hence an arcsine random variable. See [8] for a ‘semiclassical’ interpretation for Gaussian random matrices.

Proposition 2.

Let . Set .

-

1.

The Stieltjes-Cauchy transform of

(19) has the hypergeometric representation

(20) -

2.

If is a real random variable with distribution , then the following identity in distribution holds

(21) where the variables on the right are jointly independent.

-

3.

Let be independent and uniformly distributed on . Then,

(22) where .

Remark 2.

For the first values of we get

| (23) | ||||

| (24) | ||||

| (25) |

etc. For , Eq. (23) coincides with the factorisation (17). For , Eq. (24) is equivalent to a formula proved by Młotkowski and Penson [24, Proposition 3.1].

We can use the decomposition (21) to write ‘explicit’ expressions for the densities . For small values of we have

| (26) | ||||

| (27) |

The first is the Marchenko-Pastur distribution . The second is equivalent to formula in [24, Theorem 3.1] proved by Mellin inversion. For generic values of , a ‘direct’ way to numerically compute is by applying the Stieltjes inversion formula

| (28) |

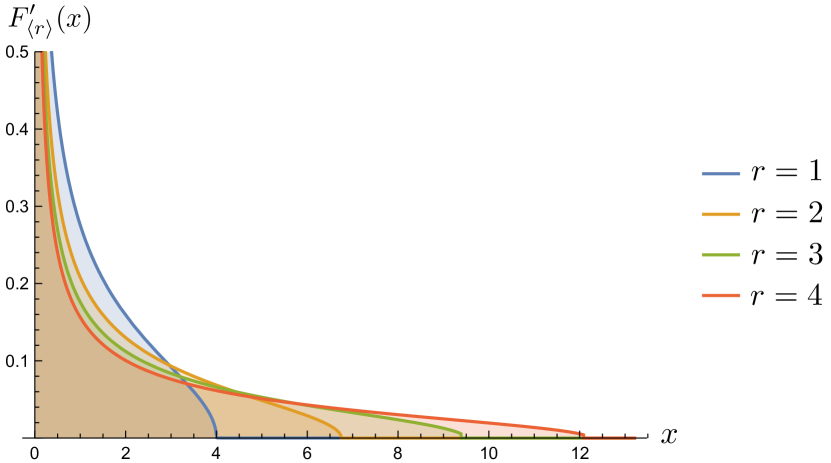

to Equation (20). This is how we made the numerical plots shown in Fig. 1.

In fact, one could, as in [30], write as the inverse Mellin transform of the moments. Since the moments are products of ratios of Pochhammer symbols, the resulting density would be a Mejier-G function (see the note by Dunkl [10]). In fact, from the previous proposition we can get some precise information on the support of and on its behavior at the edges.

Corollary 1.

The measure has a density, with support

| (29) |

Moreover at the edges of the support the density behaves as

| (30) |

for some constants .

The density vanishes as a square root at the ‘soft edge’ . At the ‘hard edge’ the density has an integrable singularity . For (Wishart matrices) this is the classical divergence, but for the singularity is stronger.

Remark 3.

The generalised Catalan numbers

| (31) |

are related to the most known Fuss-Catalan sequences

| (32) |

The Fuss-Catalan sequences also appear in random matrix theory and free probability as limiting moments of products of independent Wishart matrices [2, 19, 23]. As shown by Penson and Życzkowski [30], the Fuss-Catalan numbers are the moment sequence of a distribution whose density is a Meijer G-function, with support on the interval .

5 Proofs

Theorem 1 was discovered by a combination of experimenting and guessing, and the proof is based on matrix moments calculations combined with the exact solution for the enumeration of -plane trees (Proposition 1).

Proof of Theorem 1.

Let

| (33) |

Claim 1.

Each has moments of all order.

Claim 2.

For all , the moment sequence converges to , almost surely.

Claim 3.

The sequence uniquely determine the distribution .

By the moment method, the three claims imply Theorem 1. Note that corresponds to a random measure with finite support. Hence, Claim 1 is immediate. Claim 3 can be showed by checking Riesz’s condition [4, Lemma B.2],

| (34) |

Indeed, Stirling’s approximation formula implies

| (35) |

It remains to prove Claim 2:

| (36) |

Note that

| (37) |

We may first assume that the entries are uniformly bounded. Under this assumption we can prove the following two Lemmas.

Lemma 1.

Let . Then, for all ,

| (38) |

Lemma 2.

Let . Then, for all ,

| (39) |

Lemma 1 states the convergence in expectation of the moments. Lemma 2 implies, through Borel-Cantelli, the almost sure convergence (36).

We now show that the Theorem holds true under the sole hypothesis of finite second moment . This is done by the standard procedure of truncation. Fix a constant and consider the symmetric matrix whose elements satisfy, for

| (40) |

The matrix is a truncated and standardised version of . Denote by the empirical spectral distribution of .

Recall that [3, Appendix C] the space of probability measures on equipped with the weak topology is metrizable with the Lévy distance, defined for any pair of distribution functions as:

| (41) |

For the reader’s convenience, we state explicitly a bound that can be extracted from the book of Bai and Silverstein [4, Equations (3.1.3)-(3.1.4)-(3.1.5) on p. 48]. For large enough ,

| (42) |

almost surely. The above inequality is an application of classic matrix inequalities and the strong law of large numbers. Note that the right-hand side of the inequality can be made arbitrarily small, by choosing large, uniformly in . From the fact that weak convergence is equivalent to convergence with respect to the Lévy metric, we conclude that and have the same limit in distribution. (See also [3, Theorem 2.1.21].) ∎

It remains to prove the combinatorial lemmas. We follow the scheme of proof of [4, Theorem 3.7], and its variant by Cheliotis [6] (arXiv version).

Proof of Lemmas 1 and 2.

We start from the exact formula

| (43) |

Now, we group row and column indices within the same block as follows

| (44) | ||||

(We use the standard notation .) We introduce the following subset of multiindices

| (45) |

If , then the corresponding word in the summation (43) contains a letter identically zero.

For two -tuples , we associate the bipartite graph with vertex set

(its cardinality is not necessarily because of possible repetitions), and set of edges

with the convention . Two graphs and are said isomorphic if one becomes the other by renaming the vertices, that is if , and for some permutations .

With this notation, we write

where we encode the word

| (46) |

in the bipartite graph . From we generate its skeleton by identifying edges with equal ends. Formally, has vertex set , and edge set

Note that if contains an edge that does not appear at least twice, than because the ’s are independent and centred. Thus we have at most edges in the skeleton and so at most vertices. The number of isomorphic graphs with vertices is . Thus the contribution to the expectation of these terms is which vanishes as , unless . In the latter case is a tree.

Therefore, the indices that contribute in the large- limit of (43) are those for which

-

1.

;

-

2.

the associated has exactly vertices;

-

3.

the closed path

traverses each edge of the tree exactly twice.

In fact, such a pair defines a plane tree, that is, a tree on which we have specified an order among the children of each vertex. (Among two vertices with common parent, we declare smaller the one that appears first in the sequence , that is, the one that is visited first in the path.) So the graph can be identified with a plane tree with vertices. Since the ’s are independent and have unit variance, the corresponding word has expectation , if . Each label can be written as for a unique choice of ‘block index’ and ‘inner index’ . Therefore, for any choice of block indices, there are ways to choose multiindices and corresponding to the same plane tree up to isomorphism. The condition is the colouring condition on that makes it a -plane tree:

| (47) |

We now recall Proposition 1

| (48) |

and conclude the proof of Lemma 1.

Proof of Proposition 2.

To prove i) we assume that can be expanded in a neighbourhood of

| (50) |

(It can be verified, a posteriori, that this expansion holds true for .) When computing the ratio of consecutive terms of the series we identify the claimed hypergeometric representation (20).

In order to prove ii), recall the moments of Beta and uniform random variables,

| (51) |

A little calculation shows that

| (52) |

Compare now with (51) to conclude the proof.

Finally, for point iii) we notice that

| (53) |

Now change coordinates to get

| (54) |

∎

Proof of Corollary 1.

By Proposition 2, the density is the Mellin (multiplicative) convolution of the densities of :

| (55) |

where

| (56) |

is the characteristic function of the interval , and . Since the beta random variables are supported on , we see immediately that is zero for . Assume that . Then, we can rewrite (57) as

| (57) |

For , the leading contribution to the integral comes from the singular part of the integrand at . Therefore, for we have

| (58) |

For , the leading contribution to the integral comes instead from the vicinity of , picking the singular part of the integrand for . Therefore, for we have

| (59) |

∎

6 Outlook

We conclude with some exercises and further food for thought.

-

1.

Show that adding/removing a finite number of boxes independent of to the dilation of the staircase partition does not change the limiting spectral distribution .

-

2.

Prove Theorem 1 using the Stieltjes transform method. One should first identify the algebraic equation whose solution (decaying at infinity as ) is .

-

3.

Investigate the microscopic statistics of the eigenvalues of block-shaped random matrices.

-

4.

For -shaped random matrices one expects a relation between the limit shape and the limiting spectral distribution. Find new examples, for which the limit of can be computed explicitly.

References

References

- [1] Adler M, Van Moerbeke P, Wang D, Random matrix minor processes related to percolation theory, Random Matrices: Theory and Applications 2, 1350008 (2013).

- [2] Alexeev N, Götze F and Tikhomirov A, Asymptotic distribution of singular values of powers of random matrices, Lithuanian Math. J. 50, 121 (2010).

- [3] Anderson G W, Guionnet A and Zeitouni O, An Introduction to Random Matrices, Cambridge University Press, 2010.

- [4] Bai Z, Silverstein J W, Spectral Analysis of Large Dimensional Random Matrices, 2dn Edition, Springer, 2010.

- [5] Ballico E, Linear subspaces of matrices associated to a Ferrers diagram and with a prescribed lower bound for their rank, Linear Algebra and its Applications 483, 30-39 (2015).

- [6] Cheliotis D, Triangular random matrices and biorthogonal ensembles, Statistics and Probability Letters 134, 36-44 (2018); arXiv:1404.4730v1.

- [7] Collins B, Gawron P, Litvak A E, Życzkowski K, Numerical range for random matrices, J. Math. Anal. Appl. 418, 516-533 (2014).

- [8] Cunden F D, Majumdar S N, O’Connell N, Free fermions and -determinantal processes, J. Phys. A: Math. Theor. 52, 165202 (2019).

- [9] Dolega M, Féray V, Śniady P, Explicit combinatorial interpretation of Kerov character polynomials as numbers of permutation factorizations, Adv. Math. 225, 81-120 (2010).

- [10] Dunkl C F, Products of Beta distributed random variables, arXiv:1304.6671.

- [11] Dykema K and Haagerup U, DT-operators and decomposability of Voiculescu’s circular operator, Amer. J. Math. 126(1),121-189 (2004).

- [12] Féray V, Śniady P, Asymptotics of characters of symmetric groups related to Stanley character formula, Ann. Math. 173, 887-906 (2011).

- [13] Flynn-Connolly O, Random matrices, genus expansions and the symmetric group, UCD Summer Research Project 2018 - Final report, 2018.

- [14] Forrester P J, Log-gases and random matrices, London Mathematical Society Monographs Series, 34, Princeton University Press, Princeton, 2010.

- [15] Forrester P J, Wang D, Muttalib-Borodin ensembles in random matrix theory - realisations and correlation functions, Electron. J. Probab. 22 , 1-43 (2017).

- [16] Gu N S S, Prodinger H, Bijections for -plane trees and ternary trees, European J. Combin. 30 (4), 969-985 (2009).

- [17] Gu N S S, Prodinger H, Wagner S, Bijections for a class of labeled plane trees, European J. Combin. 31, 720-732 (2010).

- [18] Ledoux M, Differential operators and spectral distributions of invariant ensembles from the classical orthogonal polynomials. The continuous case, Elec. J. Probab. 9, 177-208 (2004).

- [19] Liu D-Z, Song C, Wang Z-D, On explicit probability densities associated with Fuss-Catalan numbers, Proc. AMS 39, (2011).

- [20] Livan G, Novaes M, Vivo P, Introduction to Random Matrices - Theory and Practice, SpringerBriefs in Mathematical Physics (2018).

- [21] Macdonald I G, Symmetric Functions and Hall Polynomials, 2nd Ed., Oxford Mathematical Monographs, 1995.

- [22] Marchenko V A and Pastur L A, Distribution of eigenvalues for some sets of random matrices, Matematicheskii Sbornik, 114(4), 507-536(1967).

- [23] Młotkowski W, Fuss-Catalan numbers in noncommutative probability, Documenta Mathematica 15, 939-955, (2010).

- [24] Młotkowski W, Penson K A, The probability measure corresponding to 2-plane trees, Probability and Mathematical Statistics 33 (2), 255-264 (2013).

- [25] Młotkowski W, Penson K A, Probability distributions with binomial moments, Inf. Dim. Analysis, Quantum Prob. and Related Topics 17/2 (2014).

- [26] Muirhead R J, Aspects of multivariate statistical theory, John Wiley & Sons (2009).

- [27] Nakashima H, Graczyk P, Wigner and Wishart Ensembles for graphical models, arXiv:2008.10446.

- [28] OEIS Foundation Inc. (2023), The On-Line Encyclopedia of Integer Sequences, Published electronically at http://oeis.org.

- [29] Okoth I O, Wagner S, Refined enumeration of -plane trees and -noncrossing trees, arXiv:2205.01002.

- [30] Penson K A and Życzkowski K, Product of Ginibre matrices: Fuss-Catalan and Raney distributions, Phys. Rev. E 83, 061118 (2011).

- [31] Stanley R P, Irreducible Symmetric Group Characters of Rectangular Shape Séminaire Lotharingien de Combinatoire 20, Article B50d (2004).

- [32] R. Stanley R P, Catalan Numbers, Cambridge University Press, 2015.