Structure-preserving eigenvalue modification of symplectic matrices and matrix pencils

Abstract

A famous theorem by R. Brauer shows how to modify a single eigenvalue of a matrix by a rank-one update without changing the remaining eigenvalues. A generalization of this theorem (due to R. Rado) is used to change a pair of eigenvalues of a symplectic matrix in a structure-preserving way to desired target values . Universal bounds on the relative distance between and the newly constructed symplectic matrix with modified spectrum are given. The eigenvalues Segre characteristics of are related to those of and a statement on the eigenvalue condition numbers of is derived. The main results are extended to matrix pencils.

1. Introduction

In numerical linear algebra and matrix analysis one occasionally encounters the necessity of modifying special eigenvalues of a matrix without altering its remaining eigenvalues. Techniques for changing certain eigenvalues of a matrix have, for instance, been applied to solve nonnegative inverse eigenvalue problems [13, 16] or, in form of deflation methods, to remove dominant eigenvalues in eigenvalue computations [14, Sec. 4.2]. Furthermore, the task of modifying eigenvalues of matrices is of interest in stability and feedback of linear systems [4, § 25], [3, Sec. 2.3] or for passivity and eigenvalue assignment in control design [1]. One basic result on how a single eigenvalue of a matrix may be changed without modifying any other eigenvalues is due to R. Brauer and can be found in [3, Sec. 1], [16].

Theorem 1 (Brauer).

Let have eigenvalues and let be an eigenvector for . Then, for any , the matrix has the eigenvalues .

This work is concerned with the purposive change of certain eigenvalues of matrices with symplectic structure. A complex matrix is called symplectic, if111Here and in the following, T denotes the transpose of a (maybe complex) matrix or vector, not its conjugate transpose.

| (1) |

Defining , we see that (1) is equivalent to . Therefore, a symplectic matrix is always nonsingular and . In consequence, as is similar222By definition, is similar to and by the Taussky-Zassenhaus Theorem [17], is similar to . to , the eigenvalues of a symplectic matrices arise in pairs , , where and have the same Segre characteristic. Recall that for an eigenvalue of , its Segre characteristic is the sequence of sizes of the Jordan blocks of with eigenvalue in non-increasing order [15]. We denote the Segre characteristic of an eigenvalue by . It is now immediate that Theorem 1 can in general not be used for a structure-preserving, symplectic change of eigenvalues. In fact, for a structure-preserving eigenvalue modification, the change of and must take place simultaneously.

Without any structure-preservation in mind, changing two (or more) eigenvalues simultaneously is possible with the following generalization of Theorem 1 attributed to R. Rado. It can be found in [13], see also [3, Sec. 3].

Theorem 2 (Rado).

Let have eigenvalues and let be linearly independent eigenvectors for . Set . Then, for any matrix , the matrix has the eigenvalues , where , , are the eigenvalues of .

In this work, we investigate how Theorem 2 can be utilized to change a pair of eigenvalues of a symplectic matrix (or a symplectic matrix pencil) to desired target values in a structure-preserving way without modifying any other eigenvalues of . Considering Theorem 2, the starting point of our discussion is thus the following question:

-

Let be symplectic with eigenvalues , , , linearly independent eigenvectors for and , respectively, and . How has to be chosen, such that is symplectic with eigenvalues for some given value ?

The above-mentioned problem will be discussed in Section 2. In Section 3 we investigate whether we can find an upper bound that only depends on and that assures the existence of a symplectic matrix with eigenvalues and relative distance . We derive distinguished matrices for which such a bound can be neatly expressed and related to the relative change in the eigenvalue, i.e. . We discuss commutativity relations between and in Section 4.1 and characterize the Segre characteristics of the eigenvalues of in Section 4.2. The results of Section 4.1 will come in handy here to find a condition on the simultaneous diagonalizability of and . In Section 6 we partially extend our results from Section 2 to symplectic matrix pencils.

1.1. Notation

The set of all matrices over (where we use either or ) is denoted by . Whenever we write instead of . For , see (1), we simply write and add the index whenever it is necessary to specify the size of . The range of a matrix is the vector space spanned by its columns and is denoted . For , we denote the Moore-Penrose pseudoinverse of by . In case and , we have so that , while for and , yields . The superscript H always denotes the conjugate transpose of a matrix or vector while T is used for the pure transposition. Whenever is some complex number, we denote by and its real and imaginary part, respectively. Complex conjugation of a number is denoted by a bar, i.e. .

2. Symplectic Eigenvalue Modification

Let be a symplectic matrix (see (1)) with eigenvalues , , and let be given. Furthermore, assume are linearly independent333If , then and are necessarily linear independent. Therefore, the linear independence is only a restrictive requirement if , i.e. . eigenvectors of for and , respectively, and define . In this section, our goal is to determine all possible matrices such that is again symplectic and has the eigenvalues . To this end, we will make use of Rado’s theorem and derive a structure-preserving version of Theorem 2 (see Theorem 3).

As it will become clear later, it seems appropriate to consider the situations and seperately. First, we assume that for the eigenvalues there exist eigenvectors such that (this immediately implies and to be linearly independent). In this case, we can assume w. l. o. g. , which can be achieved by a scaling of and/or . That is, we have . For the matrix to be symplectic, it has to hold that

| (2) |

Using , (2) is equivalent to the matrix equation

| (3) |

for the unknown matrix . Notice that (3) can be rewritten as

| (4) |

using . Since is a matrix of full rank, (4) immediately implies for any solution . Thus, for every satisfying (3), there is a matrix such that . Plugging this ansatz into (3), we obtain a equation for , namely

Replacing by this can be rewritten as

| (5) |

Finally, we may multiply (5) with the pseudo inverses from the left and with from the right to obtain

| (6) |

which is a matrix equation for of size that is equivalent to (5). As and are both skew-symmetric, their diagonals are identically zero. Comparing the entries of and in the (1,2) position, we obtain the condition

| (7) |

for (6) to hold (comparing the elements in the position certainly gives the same condition with a minus sign). In summary, a matrix of the form is symplectic if and only if for some matrix whose entries satisfy (7).

Next, to achieve the desired eigenvalue modification, according to Theorem 2 we need to assure that the eigenvalues of

| (8) |

become equal to and . To this end, recall that (by construction of ). Thus which, since , yields

| (9) |

The characteristic polynomial of is

which should, by Theorem 2, be equal to to achieve that will have the eigenvalues and . This gives two more conditions: one the one hand , i.e.

| (10) |

One the other hand, . The latter condition, however, is equal to condition (7) obtained for the symplectic structure above. Thus, additionally to (7), which is required for to be symplectic, the equation (10) has to hold to achieve that become eigenvalues of . In conclusion, we obtain the following version of Theorem 2 that answers the question stated in Section 1 on the eigenvalue modification for symplectic matrices.

Theorem 3.

Let be symplectic with eigenvalues and let be given. Let be eigenvectors for and , respectively, normalized such that for and set . Then the matrix

| (11) |

is symplectic and has the eigenvalues if and only if for some matrix whose entries satisfy the conditions

| (12) | ||||

| (13) |

Notice that the matrix in (11) can also be expressed as or as

| (14) |

according to the relation (where ). Furthermore, we see from (12) and (13) that there exist infinitely many possible choices for that realize the desired eigenvalue modification.

Next, we discuss the case that the eigenvectors of the symplectic matrix for and , respectively, satisfy and how this condition effects the result from Theorem 3. To this end, first notice that a symplectic matrix need in fact not have eigenvectors for and that satisfy A situation of this kind arises for the symplectic matrix

and its eigenvalue . The only eigenvectors for and are and , respectively, and we have . Thus, Theorem 3 cannot be applied. A simple sufficient (but not necessary) criterion to assure that eigenvectors with must exist, is that is a diagonalizable matrix, cf. [10, Lem. 3, Cor. 3.1] and Corollary 1 below.

Whenever are eigenvectors of for and with , then follows for . In this case, it follows from (3) that (4) takes the form

Again we obtain , so there has to exist some matrix such that . However, despite the concrete form of , analogously to (8) we obtain

since and . Thus, even if is chosen according to (13) such that is symplectic, no change in the eigenvalues can be achieved. In consequence, a change of an eigenvalue pair of a symplectic matrix by Rado’s theorem in a structure-preserving way is only possible if there exist eigenvectors and for and , respectively, such that . In the next section, we derive a universal criterion on the existence of such eigenvectors.

2.1. Applying Theorem 3: a criterion

We will now characterize those symplectic matrices , for which an eigenvalue adjustment according to Theorem 3 is possible. The condition derived below involves the Segre characteristic of the eigenvalue to be modified.

First, let and and . Now suppose at least one of both vectors, e.g. , belongs to a nontrivial444By nontrivial, we mean a Jordan chain of length while a trivial Jordan chain refers to a chain of length one. Jordan chain, that is, there is some such that (and possibly more generalized eigenvectors beside ). Then we have

| (15) | ||||

as and . In consequence, whenever are eigenvectors of for and , respectively, and at least one of them belongs to a nontrivial Jordan chain. In other words, we may have only in case both and belong to trivial Jordan chains. Next, we show that in case belongs to a trivial Jordan chain there must exist (also from a trivial Jordan chain) such that .

To this end, assume that is an eigenvalue of the symplectic matrix with ones in its Segre characteristic (that is, there are Jordan blocks of size , i.e. trivial Jordan chains, and possibly other Jordan blocks of size ). Then there exists a matrix transforming to the following Jordan form

| (16) |

where the upper-left block is and contains all other Jordan blocks (note that there might also be other Jordan blocks for of size contained in ). Now define

| (17) |

Then is a right eigenvector of for () and is a left eigenvector of for (). Certainly, . Now we define . Then we have

| (18) | ||||

It follows that is an eigenvector of for . Now we obtain

In conclusion, for any eigenvector of for belonging to a trivial Jordan chain, there always exists an eigenvector of for such that Recall from our observation (15) above, that must also be a vector from a trivial Jordan chain. We conclude our findings in the following theorem.

Theorem 4.

Let be symplectic with and let be given. Then Theorem 3 is applicable to for and , i.e. there exist eigenvectors for and , respectively, with , if and only if the Segre characteristic of for contains a one, that is, it has the form . In particular, eigenvectors for and for with always belong to trivial Jordan chains of .

Do not overlook that Theorem 4 applies also for , i.e. . In this case necessarily has an even multiplicity and an even number of Jordan blocks of the same size, so a Segre characteristic of the form implies that there appears at least another one, i.e. . Then the reasoning in (16), (17) and (18) applies in the same way. If is diagonalizable, the Segre characteristic of for any eigenvalue consists only of ones. So we immediately obtain the following corollary.

Corollary 1.

Let be symplectic with and let be given. Then Theorem 3 is applicable to for and if is diagonalizable.

3. Bounding the relative change

Let be symplectic. For the matrix in (11) we immediately obtain a bound on its (absolute or relative) change in norm with respect to . That is,

| (19) |

hold for any submultiplicative and unitarily invariant matrix norm . In this section, we intend to derive explicit bounds of the relative distance between and for certain choices of . To this end, we assume so that holds and the upper bound in (19) reduces to .

To bound the relative change with respect to consider again (12) and (13). The solution set to (12) is an affine subspace of and all solutions may be parameterized as

| (20) |

Plugging these expressions for and into (13) yields a polynomial in , i.e.

| (21) |

Thus, depending on and (which can both be arbitrary), in (21) there are always two solutions of and, in consequence, two matrices

| (22) |

To find some that yields a small norm and thus a small bound in (19), it seems natural to consider the case , in particular 555Certainly, choosing and gives the same roots of in (21), and thus the same values for and , but a larger Frobenius norm of than choosing .. The two possible roots of for are and . The matrices and that arise according to (22) are thus given by

| (23) |

Using and in (23), explicit bounds can be found on . According to (19) and (23) such a bound only depends on , and the eigenvectors of for and and guarantees the existence of a symplectic matrix that solves the problem from Section 1 with . To formulate these bounds, we impose a condition on to estimate without computing the norm. In particular, we assume the eigenvectors of for and , respectively, to be normalized, i.e. and to be of the form

| (24) |

Then holds and it follows that

| (25) |

The value has a nice interpretation whenever is a simple eigenvalue of and holds. To see this, recall that, whenever has a simple eigenvalue (i.e. its algebraic multiplicity equals one), then

is called its condition number, where and are right and left eigenvectors of for (i.e. and ). It is a measure on how sensitive reacts to small changes in the matrix , see [14, Sec. 3.3]. As we have seen in (18) above, whenever satisfies . Thus, for simple (which implies that is simple as well) we can choose and so that

since and . We can now formulate the following theorem which follows directly from the bound in (19), the observation in (25) and the Frobenius norms of the matrices in (23).

Theorem 5.

As the following example shows, similar easy bounds can be found with the use of and when is considered. In fact, in the 2-norm, such a bound can be sharp.

Example 1.

For a symplectic matrix , the bound (19) for with respect to can easily be determined as

| (28) |

It can be seen for with that the bound in (28) can be sharp. In particular, with eigenvectors for , respectively, and we have

with nonzero entries in the first and st position. As and we obtain under the assumption

and so if is the largest eigenvalue of in absolute value (i.e. ). On the other hand, for we certainly have and thus, whenever , the bound on the right hand side in (28) also reduces to .

3.1. Improved distance bounds

Although the bound in (26) nicely relates to the relative value change and the condition number , it can be quite bad666The same is true for the bound in (27)., see e.g. Fig. 1 in Section 5. In this section we derive sharper bounds under the additional assumption that is known.

As before, let be symplectic with eigenvectors for , respectively, such that (and set ). As seen in (14), we have for and that satisfies (12) and (13)

and therefore . Whenever () from (23), then

according to (20). Recall the solutions of in (21), i.e. (corresponding to ) and (corresponding to ). Instead of estimating by we now intend to estimate directly. To this end, assume that has the form (24) and , . Then we have for

Now we further obtain

| (29) |

Note that as and are normalized. Furthermore, , and we may now derive upper (and lower) bounds for (29) depending on whether this term is positive or negative.

-

Suppose . Then follows and, since , we can estimate from (29), setting ,

On the other hand, changing the sign of we certainly have

-

Suppose . Then follows and we can estimate from (29), setting again ,

while on the other hand, with a change of sign, we obtain

Before we state our findings in the next theorem, notice that there are neat expressions for the terms , , arising above, i.e.

As it turns out, also can be rewritten in a similar fashion as

| (30) |

Finally, the two conditions to be checked in and above can be simplified. For one finds, after some reformulations,

where we used the first expression for in (30) in the second-last equation.

Thus holds if and only if , which is the case if and only if as and are located in the same half plane. For we obtain analogously

and so holds if and only if . This, in turn, holds if and only if . In conclusion, we have proven the following theorem.

Theorem 6.

Let be symplectic with and let be given. Let be normalized eigenvectors for and , respectively, with and as in (24). Define

It is shown in Section 5 (see Fig. 1) that the bounds in Theorem 6 are significantly sharper compared to the bounds in (26) and (27).

Remark 1.

For any matrix that satisfies the conditions (12) and (13) the bounds in (19) can easily be calculated. However, there are several reasons for not considering other choices of (beside and from (23)) in this section in detail:

-

(a)

If , there are two possibilities for whose entries and of depend on through (one of) the zeros of , see (21). Thus, and involve the expression of a complex square root and there is no neat and compact expression for compared to (26) and (27) or to the formulas in Theorem 6. Furthermore, minimizing with respect to the entries of under the side conditions (12) and (13) results in a difficult complex optimization problem for which the author is not aware of a closed form solution.

- (b)

- (c)

4. Segre characteristics and commutativity relations

In this section we discuss how the Segre characteristics of eigenvalues are effected by a change of a symplectic matrix to according to Theorem 3. In particular, we will show that the Segre characteristics of the eigenvalues of and are either the same or connected in a direct way. Furthermore, we make a statement on eigenvectors of and that remain unchanged. Notice that, in the context of Theorem 2, the eigenvectors of and are in general all different and not related in an immediate fashion [3] if no further restrictions are imposed on the form of . In this section we show that, in the structure-preserving context of Theorem 3, the particular form of allows for some explicit statements. Furthermore, we derive statements on the diagonalizability of and the simultaneous diagonalizability of and . To this end, we begin in Section 4.1 with a result on the commutativity of and .

4.1. The Commutativity of and

Recall that the matrix in (11) can also be expressed as

| (31) |

Since and are both symplectic, the matrix is symplectic, too. As for any the matrices and always have the same eigenvalues [9], beside , we may also define the symplectic matrix that solves the eigenvalue modification problem stated in Section 1. A question naturally arising is whether there is a connection between from (31) and . Such a connection is revealed in Theorem 7 which shows a distinguishing feature of the matrices from (23) among all matrices that satisfy (12) and (13), see Remark 1 (b). The result from Theorem 7 will be used when the diagonalizability of is investigated in Section 4.2.

Theorem 7.

Proof.

First, notice that is equivalent to

| (33) |

Multiplying both equations with (from the right) and using the relations (where ) and yields Moreover, and, equivalently to (33), it suffices to investigate the equation

| (34) |

Now, as has full rank, (34) is (by the multiplication with from the left and from the right) equivalent to , that is, . For we obtain

This shows that holds, in case , if and only if . The two possibilities for that satisfy the conditions (12) and (13) when are the matrices in (23). Furthermore, if , the equation always holds. This completes the proof. ∎

4.2. Segre characteristics

Let be symplectic with eigenvalues and let be given. To analyse the consequences of the change on the Segre characteristics of the eigenvalues of and , we discuss the cases of (the eigenvalues that are changed), (the values and are changed to) and all other eigenvalues (which are the same for and ) separately. As before, let be eigenvectors for and , respectively, normalized such that for and assume has been constructed as in Theorem 3.

We first consider eigenvalues different from and . These eigenvalues and their algebraic multiplicities are the same for and and we show that their eigenspaces and Jordan chains (thus, in consequence, their Segre characteristics) remain completely unchanged. To prove this, we need the following fact about the matrix and its (generalized) eigenvectors (see also [10, Sec. 2]): assume that is some eigenvalue of different from and and let () be a Jordan chain for and , i.e. it holds that and for . Then follows for any To see this, first consider the eigenvector of for . We have

This shows that if . Similarly, follows for . Now assume that holds for and . For we thus obtain

Therefore, again follows whenever . With the same reasoning we obtain for . In conclusion we have for any whenever

Lemma 1.

Let be symplectic with and let be given. Suppose that has been constructed according to Theorem 3. Then for any which is neither equal to or nor equal to or the Segre characteristics of as an eigenvalue of and and their corresponding Jordan chains, respectively, are identical.

Proof.

Assume is neither equal to or nor equal to or . By construction of , is an eigenvalue of both and with the same algebraic multiplicities. Whenever is an eigenvector of for it is also an eigenvector of for since , which implies

| (35) |

Next, let be a Jordan chain for and . Then

since for any , , from the Jordan chain. Inductively, this shows that remains to be a Jordan chain of for . Therefore, the Segre characteristic for of and and the corresponding Jordan chains are the same. ∎

Next we consider and . When is transformed to and (one instance of) is replaced by and , the Segre characteristic of for is necessarily different from its Segre characteristic for due to the eigenvalue modification that has taken place (if is a simple eigenvalue of , then it is not even an eigenvalue of anymore). However, if the algebraic multiplicity of as an eigenvalue of is , then the Segre characteristics of as an eigenvalue of and are connected in an easy fashion (see Theorem 8 below). This is obviously false in the general context of Rado’s Theorem, where nontrivial Jordan blocks may arise, as the following counterexample for and shows:

In this example, the Segre characteristic of is while it is for .

Theorem 8.

Let be symplectic with and let be given. Suppose that has been constructed according to Theorem 3. Then the following hold:

-

If the Segre characteristic of as an eigenvalue of is

(36) with777Notice that for Theorem 3 to be applicable to , is a necessary condition according to Theorem 4. If , then implies since then Jordan blocks of a particular size must appear an even number of times in the Jordan structure of . , then the Segre characteristic of as an eigenvalue of is . Moreover, if and (36) is its Segre characteristic of with7 , then the Segre characteristic of as an eigenvalue of is .

-

Let . Then the Segre characteristic of as an eigenvalue of is always if . If its Segre characteristic is if and only if or from (23), otherwise it is .

Proof.

We first assume . According to the Segre characteristic of there are Jordan blocks of sizes . As let be the corresponding eigenvector. We denote the generalized eigenvectors corresponding to the -th Jordan block by and set and Since has the same Segre characteristic as , there are also Jordan blocks of for of sizes . Let , and be defined analogously from the (generalized) eigenvectors for . We now define the matrix . Then the matrix can be written as

As for we therefore obtain and thus . Now set and notice that the third to last row of are identically zero (due to the form of ). Therefore, the form of can be explicitly determined (with indicating zero or nonzero entries that are not of further interest):

| (37) |

Now, its is easily seen that are part of the Jordan structure of , hence they also arise in the Jordan structure of . This shows that the Segre characterstic of and is both . If the proof follows the same lines without the use of . To prove we note that the upper-left block of is exactly from (9), hence its eigenvalues are . If , then is semisimple. Therefore, we obtain the Segre characteristic of and as eigenvalues of both as . On the other hand, if , then is semisimple if and only if its minimal polynomial is . Now

Thus, for we must have and the only possible choices for to be semisimple are and from (23). It is easy to check that in fact both choices result in . This proves that the Segre characteristic of as an eigenvalue of is if and that it has to be otherwise. ∎

Finally, assume that was already an eigenvalue of and Theorem 3 is applied for . Then the arguments of the proof of Lemma 1 apply to (as an ’old’ eigenvalue of ) as well as the result from Theorem 8 (for as the ’new’ eigenvalue appearing in the spectrum of ). Thus, the Segre characteristic of is its old Segre characteristic from extended by one of the cases described in Theorem 8 .

As another consequence of Theorem 8 it follows that, if is semisimple for , then remains semisimple for is case its multiplicity was . Moreover, assume the symplectic matrix is diagonalizable (i.e. all its eigenvalues are semisimple) and let be constructed according to Theorem 3. As a consequence of Lemma 1 and Theorem 8, the diagonalizability of can then only be circumvented in case a Jordan block arises for . As seen above, a Jordan block for will arise if is different from and . In other words, if or from (23) are chosen in Theorem 3, the matrix will be semisimple in case was. In fact, this is the only situation in which and are simultaneously diagonalizable since the simultaneous diagonalizability of and is only possible if and commute. According to Theorem 7 this is the case if and only if are chosen. We summarize this result in the following corollary.

Corollary 2.

Example 2 below shows how the simultaneous diagonalization looks like if or are used to construct .

Example 2.

Whenever with and and , then for with from (23) we have

where and . In fact, for being diagonal, and are the only possible choice such that is diagonal, too.

4.3. A note on condition numbers

We conclude this section with a result on eigenvalue condition numbers. It is a surprising fact, that we can apply Theorem 3 to a symplectic matrix without changing any eigenvalue condition number (for simple eigenvalues) at all. For Rado’s theorem this is not true: an unstructured application of Theorem 2 typically changes all eigenvalue condition numbers, even those of eigenvalues that remain unchanged. The main result on the behavior of condition numbers is stated in Theorem 9. For its proof, we need the following well-known fact that we state without proof in Lemma 2.

Lemma 2.

Let and suppose is a right eigenvector of for (i.e. ) and is a left eigenvector of for (i.e. ). Then if .

Theorem 9.

Proof.

Under the assumption and the simplicity of , it follows that or for some . Assume w. l. o. g. that and let be some corresponding eigenvector of . According to Lemma 1, holds. Next suppose is some left eigenvector of for , i.e. . Then

as according to Lemma 2. Thus the left and right eigenvectors for of and coincide, which directly implies .

Now assume for in (23) and suppose . The condition implies to be simple for . If are eigenvectors of for and , respectively, then one directly obtains

(similarly, follows). Analogously we have , which follows from (see (18)). Thus, the left and right eigenvectors of for and those of for coincide and the statement follows. The proof is analogous for . ∎

Remark 2.

One can proceed as in the above proof to see that, if is used,

In fact, it is easy to show that now and hold.

5. Experiments

To perform numerical experiments in Matlab R2021b, we used the code available in [8]. To obtain symplectic matrices , a symplectic matrix constructed from [8], was modified as

| (38) |

and are random numbers: rand(1) + 1i*rand(1). Compared to , has a more widespread spectrum ranging in magnitude from about to .

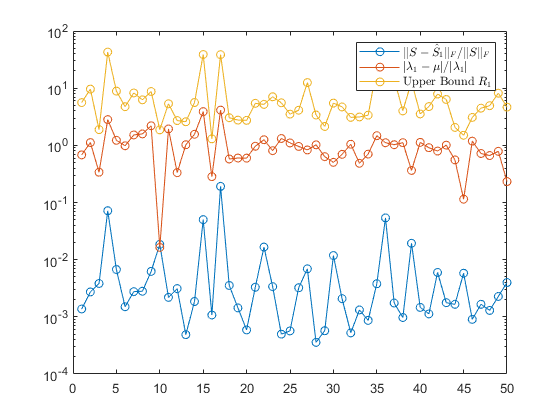

In Figure 1, 50 examples are shown where a randomly selected eigenvalue of has been changed to , where is a random complex number with and . Therefore, . The plot shows the relative change , the coarse bound in (26), the upper and lower bounds from Theorem 5 and the relative change in the eigenvalue . The plots show clearly that the bounds from Theorem 5 are significantly sharper than the bound from (26). If is used instead of the plots do not alter essentially.

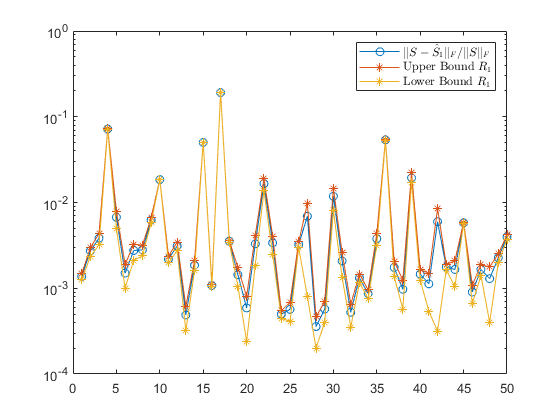

The most significant difference between using and can be seen when an eigenvalue is subject to a small or large relative change compared to its absolute value. This is shown in Figure 2 where the experimental set-up is the same as before but now (left plot) and (right plot) are chosen. Both plots show the relative change for and the relative change in the eigenvalue . It is seen that for a small change in the eigenvalue , the relative change is significantly smaller than . However, when undergoes a large change, then there is no big difference in using or .

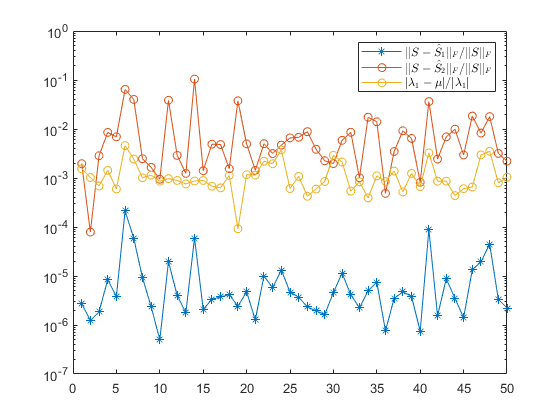

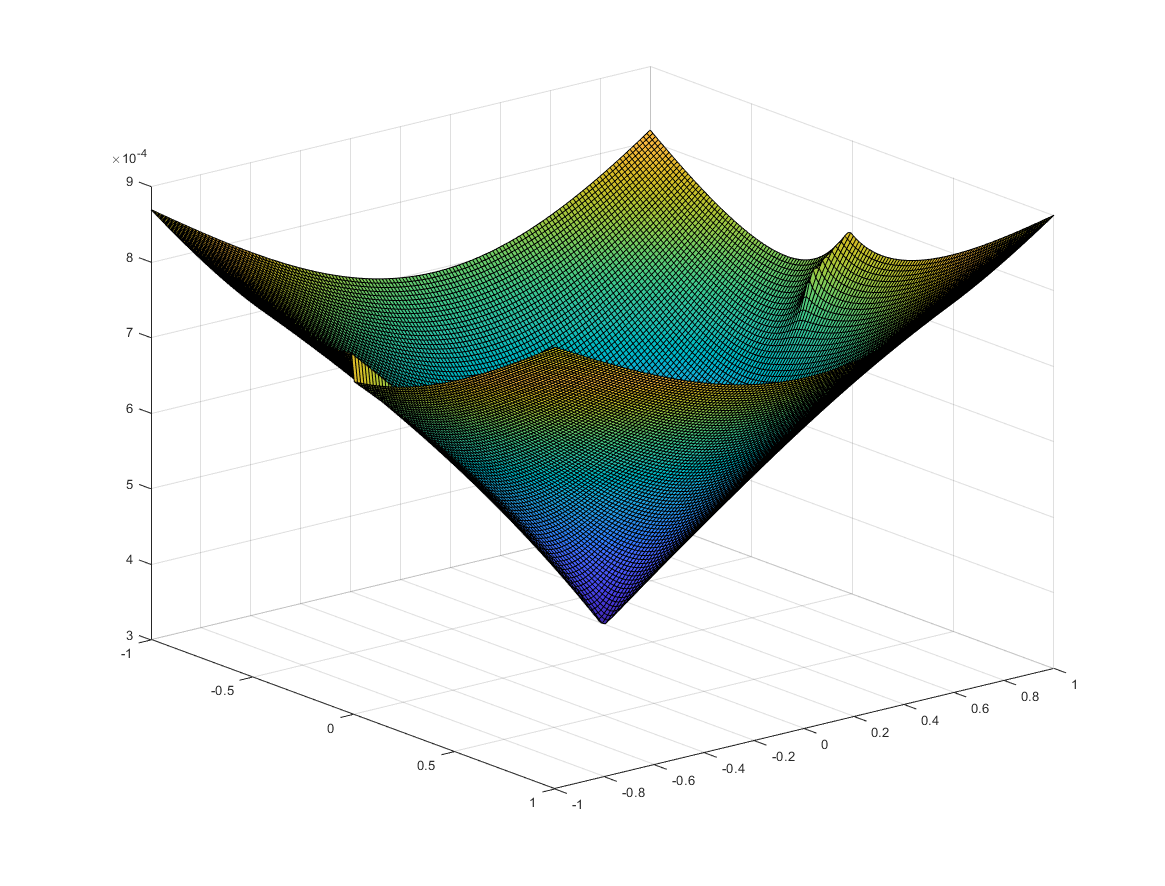

In Figure 3 we show the use of matrices different from and in (23). To this end, we fix a symplectic matrix and an eigenvalue of that is to be modified by a relativ change of . We consider a mesh grid on with 150 discretization points in each direction. Each point is associated with the complex number from which we made up . The values for and are found according to (20) and (21) so that we obtain two different matrices and . The matrices , , where constructed and in Figure 3 the minimum of is shown for each point . The plot indicates that the minimum numerically found among all values is attained for , i.e. . Thus, the minimum is obtained for one of the matrices in (23). In most examples that have been considered a plot similar to the one in Figure 3 arose. However, seldom the numerical minimum was detected somewhere near .

6. Symplectic Matrix Pencils

In this section we analyse the eigenvalue modification problem of Section 1 for symplectic matrix pencils. We call a matrix pencil , symplectic (see [6, Sec. 2.1.1]) if it holds that

| (39) |

From (39) it follows that for a symplectic pencil either and are both regular or singular, cf. [6, Sec. 2]. A scalar is called an eigenvalue of if there exists some nonzero with , i.e. [2, Sec. 2]. Eigenvalues of symplectic pencils also arise in pairs [6]. In particular, if and are singular, it is also possible to have as an eigenvalue of which implies that is also an eigenvalue of (see, e.g., [5] for more information on the finite and infinite eigenstructure of matrix pencils). In the following, we focus on symplectic pencils where both and are regular. Thus, has neither the eigenvalue zero nor the eigenvalue infinity.

In general, for an arbitrary matrix pencil , , where is nonsingular, we can easily derive an adapted version of Rado’s theorem.

Theorem 10.

Let , and nonsingular, be a matrix pencil with eigenvalues . Let be eigenvectors for such that for . Furthermore, let be arbitrary. Then the matrix pencil

has the eigenvalues , where are the eigenvalues of the matrix with .

Proof.

As , the eigenvalues of coincide with those of the matrix . In particular, does not have as an eigenvalue. Assume that with we obtain and Theorem 2 implies that has the eigenvalues , where are the eigenvalues of the matrix . As and the matrix pencil have the same eigenvalues, the statement follows. ∎

Now let be a symplectic matrix pencil according to (39) with nonsingular and eigenvalues . We set

and intend to determine such that is again symplectic and has the eigenvalues for a given value . A direct calculation reveals that (39) is equivalent to being a symplectic matrix, i.e. . Thus, Theorem 3 can be applied to the matrix that has the same eigenvalues as . Now suppose

i.e. are generalized eigenvectors for and , respectively. Furthermore, assume . Then

is symplectic with eigenvalues provided that is chosen according to the conditions in Theorem 3 for . Then, the matrix pencil , i.e.

| (40) |

has the same eigenvalues as [5, Sec. 3.1]. In fact, is again a symplectic pencil. To show this, we have to check that

holds. To this end, it only remains to prove that

| (41) | ||||

since holds by assumption. Using this relation, (41) simplifies to

which can be rewritten as . As in Section 2 this relation holds if and only if . As for any we have , it follows that the condition is equivalent to (6). Therefore, since was constructed according to (13) so that holds, this finally shows that (41) is true, so is symplectic. As already mentioned above, and have the same eigenvalues, so the eigenvalues of are .

Notice that in (40) can be rewritten in various ways, e.g.

| (42) | ||||

| (43) |

using the relation that follows from being symplectic in (42) and in (43). Using and exchanging with in (42) yields

| (44) |

which is an expression for similar to (14). We conclude our finding in the following theorem.

Theorem 11.

7. Summary

In this work we showed how to modify a pair of eigenvalues of a symplectic matrix to desired target values for a symplecitc matrix in a structure-preserving way. Universal bounds on the relative distance between and with modified spectrum were given. The eigenvalues Segre characteristics of were related to those of and some statements on eigenvalue condition numbers have been derived. The main results have been extended to matrix pencils.

8. Acknowledgement

The author is grateful to Thomas Richter as this work was in parts developed during the authors employment in Thomas Richter’s group at the Otto-von-Guericke-Universität Magdeburg.

References

- [1] A. T. Alexandridis, H. E. Psillakis. The inverse optimal LQR problem and its relation to passivity and eigenvalue assignment. International Journal of Tomography & Statistics, Vol. 5, 2007.

- [2] T. Betcke, N. J. Higham, V. Mehrmann, C. Schröder, F. Tisseur. NLEVP: A Collection of Nonlinear Eigenvalue Problems. ACM Transactions on Mathematical Software, Vol. 39(2), 2013.

- [3] R. Bru, R. Canto, R. L. Soto and A. M. Urbano A Brauer’s theorem and related Results. Cent. Eur. J. Math. 10(1), 2012.

- [4] D. F. Delchamps. State Space and Input-Output Linear Systems. Springer Verlag, New York, USA, 1988.

- [5] F. De Terán, F. M. Dopico, D. S. Mackey. Spectral equivalence of matrix polynomials and the Index Sum Theorem. Linear Algebra Appl., Vol. 459, 2014.

- [6] H. Fassbender. Symplectic Methods for the Symplectic Eigenproblem. Kluwer Academic Publishers, New York, USA, 2002.

- [7] R. A. Horn, C. R. Johnson. Matrix Analysis (Second Edition). Cambridge University Press, New York, USA, 2013.

- [8] D. P. Jagger. MATLAB Toolbox for Classical Matrix Groups. Masters thesis, University of Manchester, 2003. MIMS EPrint 2007.99.

- [9] C. R. Johnson, E. A. Schreiner. The Relationship between and . The American Mathematical Monthly, Vol. 103(7), 1996.

- [10] A. J.Laub, K. Meyer. Canonical Forms for Symplectic and Hamiltonian Matrices. Celestial Mechanics, Vol. 9, 1974.

- [11] D. G. Luenberger. Optimization by Vector Space Methods. John Wiley & Sons, Inc., New York, USA, 1969.

- [12] T. Lyche. Numerical Linear Algebra and Matrix Factorizations. Springer Nature, Cham, Switzerland, 2020.

- [13] H. Perfect. Methods of constructing certain stochastic matrices. II Duke Math. J. 22(2), 1955.

- [14] Y. Saad. Numerical Methods for Large Eigenvalue Problems (Revised Edition). Society for Industrial and Applied Mathematics, Philadelphia, USA, 2011.

- [15] H. Shapiro. Linear Algebra and Matrices. Topics for a Second Course. American Mathematical Society, Providence, USA, 2015.

- [16] R. L. Soto and O. Rojo. Applications of a Brauer theorem in the nonnegative inverse eigenvalue problem. Linear Algebra Appl. 416(2-3), 2006.

- [17] O. Taussky, H. Zassenhaus. On the similarity transformation between a matirx and its transpose. Pacific J. Math. 9(3), 1959.