Multi-Channel Auction Design in the Autobidding World

Over the past few years, more and more Internet advertisers have started using automated bidding for optimizing their advertising campaigns. Such advertisers have an optimization goal (e.g. to maximize conversions), and some constraints (e.g. a budget or an upper bound on average cost per conversion), and the automated bidding system optimizes their auction bids on their behalf. Often, these advertisers participate on multiple advertising channels and try to optimize across these channels. A central question that remains unexplored is how automated bidding affects optimal auction design in the multi-channel setting.

In this paper, we study the problem of setting auction reserve prices in the multi-channel setting. In particular, we shed light on the revenue implications of whether each channel optimizes its reserve price locally, or whether the channels optimize them globally to maximize total revenue. Motivated by practice, we consider two models: one in which the channels have full freedom to set reserve prices, and another in which the channels have to respect floor prices set by the publisher. We show that in the first model, welfare and revenue loss from local optimization is bounded by a function of the advertisers’ inputs, but is independent of the number of channels and bidders. In stark contrast, we show that the revenue from local optimization could be arbitrarily smaller than those from global optimization in the second model.

1 Introduction

Advertisers are increasingly using automated bidding in order to set bids for ad auctions in online advertising. Automated bidding simplifies the bidding process for advertisers – it allows an advertiser to specify a high-level goal and one or more constraints, and optimizes their auction bids on their behalf [17, 25, 23, 9]. A common goal is to maximize conversions or conversion value. Some common constraints include Budgets and TargetCPA (i.e. an upper bound on average cost per conversion). This trend has led to interesting new questions on auction design in the presence of automated bidders [5, 14, 8, 7].

One central question that remains unexplored is how automated bidding affects optimal auction design in the multi-channel setting. It is common for advertisers to show ads on multiple channels and optimize across channels. For example, an advertiser can optimize across Google Ads inventory (YouTube, Display, Search, Discover, Gmail, and Maps) with Performance Ads [3], or can optimize across Facebook, Instagram and Messenger with Automated Ad Placement [4], or an app developer can advertise across Google’s properties including Search, Google Play and YouTube with App campaigns [2]. With traditional quasi-linear bidders, the problem of auction design on each channel is independent of other channels’ designs. However, when advertisers use automated bidders and optimize across channels, the auction design of one channel creates externalities for the other channels through the constraints of automated bidders.

Motivated by this, we introduce the problem of auction design in the multi-channel setting with automated bidding across channels. In particular, we study the problem of setting reserve prices across channels. We consider two behavior models: Local and Global. In the Local model, each channel optimizes its reserve price to maximize its own revenue, while in the Global model, the channels optimize their reserve prices globally in order to maximize the total revenue across channels. The main question is: what is the revenue loss from optimizing locally, rather than globally?

We consider this question in two settings: one in which each channel has full control over its reserve prices, and one in which the channels have to respect an externally-imposed lower bound on the reserve prices. The first setting which we call Without Publisher Reserves is very common in practice and arises when the impressions are owned by the selling channel, or when the publisher leaves the pricing decisions to the selling channel. The second setting which we call With Publisher Reserves arises when the impressions are owned by a third-party publisher that sets a floor price for its impressions – this could come from an outside option for selling the impression. This is common in Display advertising where the selling channel is often different from the publisher who owns the impressions.

Model: Our model consists of channels, each selling a set of impressions. Each channel can set a uniform reserve price. The uniform reserve price is in the cost-per-unit-value space111See Section 7 for a discussion of uniform reserve prices in the cost-per-impression space (see Section 3.1 for details). This is motivated by the observation that, in practice, values are commonly known by the channels; values are usually click-through-rate or conversion-rate of an ad, as in [5], and the channels have good estimates for those. Besides the reserve prices set by channels, in the With Publisher Reserves setting, each impression could have a price floor set by the publisher who owns the impression. Each impression is sold in a Second-Price-Auction with a floor price that depends on the reserve price set by the selling channel and the price constraint set by the publisher. Bidders want to maximize their conversions (or some other form of value) subject to one of two types of constraints: (1) Budget, an upper bound on spend and (2) TargetCPA, an upper bound on the average cost per conversion. The model also allows standard quasi-linear bidders with no constraints. The game consists of two main stages: First, each channel simultaneously announces its reserve price; then, bidders bid optimally for the different impressions.

1.1 Our results

The paper’s main focus is to compare the revenue222See Section 7 for a brief discussion of welfare at equilibrium when channels optimize locally, i.e. each sets its reserve price(s) to maximize its own revenue, to the revenue where channels act globally and set their reserve prices to maximize the sum of the total revenue. We define the Price of Anarchy (PoA) as the worst-case ratio between the total revenue when the channels optimize locally compared to the case where the channels optimize globally. Our main goal is to bound the Price of Anarchy in the two settings: Without Publisher Reserves, and With Publisher Reserves.

Setting without Publisher Reserves

In order to bound the Price of Anarchy, we first bound the local and global revenue in terms of the optimal Liquid Welfare (see Section 3 for the definition). These revenue bounds are interesting in their own right and the proof methodology gives (non-polytime) algorithms for determining good reserve prices.

We first consider the worst-case revenue in the local model where each channel is optimizing for its own revenue, compared to the optimal Liquid Welfare. We show in Theorem 2 that the worst-case revenue is at least fraction of the optimal Liquid Welfare, where depends on the bidders’ inputs333 is the maximum of the ratio of the highest to lowest TargetCPA among TargetCPA bidders and a ratio defined (in Definition 5) for Budgeted bidders. and quantifies the heterogeneity of the pool of bidders. This lower bound on revenue trivially carries over to the setting where the channels are optimizing globally and to the single-channel setting. Next, we show that this bound is tight up to constant factors (Proposition 3). In particular, we give an example in the single-channel setting where the optimal revenue with a uniform reserve price is of the optimal Liquid Welfare. This upper bound also applies to the global and local models in the multi-channel setting. In other words, the upper bound and lower bounds on the gap between Liquid Welfare and revenue in each of these settings is . That naturally makes one wonder: Is optimizing locally as good for revenue as optimizing globally? If we look into the gap bounds, we find that they arise from trying to capture values of different scales with a uniform reserve price. And one might conjecture that since the source of the gap applies to both the global and local model, that even if there is a revenue gap between the two models, it should depend on different factors. Surprisingly, we show that the gap between optimizing locally and globally is exactly the same factor (Theorem 4). Note that in all the above settings, the revenue guarantee is independent of the number of channels and bidders and depends only on the heterogeneity of the bidders.

Setting with Publisher Reserves

In stark contrast to the setting without publisher reserves, we show that the PoA in this setting can be arbitrarily small even with one tCPA bidder (Theorem 6). The gap example depends heavily on the asymmetry between the different channels. Motivated by this, we consider the restricted setting where each channel sells a random sample of the impressions (see Section 6 for the exact details). For this case, with one tCPA bidder in the game, we show that under some mild constraint on the channels’ strategies, the PoA = , where is the number of channels. When the channels optimize globally, the equilibrium is efficient and all channels set low reserve prices. On the other hand, for the equilibrium in the local optimization model, the larger channels (in terms of the volume of impressions they own) set low reserve prices while small channels are extractive and set high reserve prices.

Hardness of Equilibrium Computation

To complement our Price of Anarchy results, we also study the computational complexity of computing the equilibrium of the game. We show an impossibility result – that it is PPAD-hard to compute the subgame equilibrium of the bidders (Theorem 1). To prove this result, we use gadget reduction from the problem of finding approximate Nash equilibrium for - bimatrix game, and we need to handle many difficulties unique to our subgame, which we explain with more details in Section 4 and Appendix B.

Key implications of our results

Our results have several implications for setting reserve prices in the multi-channel setting:

-

•

The revenue gap between local and global optimization depends heavily on whether there are publisher-imposed reserve prices.

-

•

Without publisher reserves, the worst-case gap between the revenue in the local model and the global model is , where captures the heterogeneity of the bidders’ inputs and is independent of the number of channels and bidders. Thus it is better to optimize globally when possible.

-

•

Without publisher reserves, it is possible to obtain a revenue of fraction of the optimal Liquid Welfare by setting uniform reserve prices. This observation is not surprising in the single-channel setting and for global optimization in the multi-channel setting, but it is remarkable that it holds even with local optimization, where the selfishness of a channel could have made it difficult for other channels to make revenue. We also note that the approximation can be improved by setting reserve prices at a more granular level, rather than a uniform reserve price. In that case, the approximation ratio will depend on the heterogeneity of bidders per slice.

-

•

With publisher reserves, the gap between the revenue in the local and global model can be arbitrarily large. This can happen even when only one of the channels has external pricing constraint.

Organization of the paper

We present a formal model of the problem in Section 3. Then, in Section 4, we show that it is PPAD-hard to compute the equilibrium of the sub-game. In Section 5, we study the setting without publisher reserves and present a tight bound on the Price of Anarchy, as well as on the gap between the revenue and optimal Liquid Welfare in the local and global models. In Section 6, we study the setting with publisher reserves and show the Price of Anarchy is 0. We also study a restricted version of this setting, and show a Price of Anarchy of for that version. Finally, in Section 7, we discuss extensions for welfare and for setting reserve prices in the cost-per-impression space.

2 Related Work

Autobidding. There has been a lot of recent interest in exploring questions related to automated bidding, including bidding algorithms and their equilibria [5], and auction design in the presence of automated bidding [14, 8, 7]. Aggarwal et al. [5] initiate the study of autobidding and find optimal bidding strategies for a general class of autobidding constraints. They also prove the existence of an equilibrium and prove a lower bound on liquid welfare at equilibrium compared to the optimal liquid welfare. Deng et al. [14] show how boosts can be used to improve welfare guarantees when bidders can have both TargetCPA and Budget constraints, potentially at the cost of revenue. Balseiro et al. [8] characterize the revenue-optimal single-stage auctions with either value-maximizers or utility-maximizers with TargetCPA constraints, when either the values and/or the targets are private. Similar to our paper, Balseiro et al. [7] also study reserve prices in the presence of autobidders, and show that with TargetCPA and Quasi-linear bidders, revenue and welfare can be increased by using (bidder-specific) reserve prices. They do not study budget-constrained bidders. All of the above papers are in the single channel setting.

Auction design with multiple channels. Most of this stream of literature have focused on models where multiple channels (auctioneers) compete to take captive profit-maximizers buyers [10, 16, 20]. The competition across channels leads to lower reserve prices, obtaining lower revenues and more efficient outcomes [24]. Our model differs from them in that our bidders are not captive but are instead are optimizing under their autobidding constraints. Interestingly, we show that in some cases the competition among channels leads to higher reserve prices, and at the same time, improves welfare (see Theorem 7.).

3 Model

Our baseline model considers a set of bidders (advertisers) interested in purchasing a set of impressions that are sold by different channels. The impressions that channel sells, , are sold using a second-price auction with a floor price. This floor price depends on the reserve price chosen by the channel and by the minimum price set by the publisher that owns the impression444The publisher might have an outside option to sell some of the impressions and sets a reserve price to account for that. These reserve prices are prechosen by the publishers and hence are fixed constants known to both channels and bidders..

3.1 Bidders

Motivated by the most common bidding formats that are used in practice, we assume that each bidder can be one of the following types: a tCPA bidder, a Budgeted bidder, or a Quasi-linear (QL) bidder. We denote by , and the set of bidders that are tCPA, Budgeted and QL bidders, respectively.

Each Bidder has a value (e.g. conversion rate) for impression and submits a bid for the impression. A bidder’s cost for buying impression is

| (1) |

where (note we use the notation for simplicity, even though does not depend on ) and (because ’s are fixed constants prechosen by the publishers, for simplicity we do not include them as variables). That is, a bidder’s cost for an impression is the maximum among (i) the bids of the bidders who bid above their own reserve prices, (ii) reserve price set by the channel which owns the impression, and (iii) reserve price set by the publisher. Also, note that the reserve prices and are multiplied by to get the final floor price of impression for bidder . In other words, the reserve prices are in the cost-per-unit-value space. We will refer to the final reserve price of impression for bidder by . Now we explain the bidder types.

QL bidder: This is a traditional profit-maximizing bidder with no constraint. The dominant strategy for such a Bidder is to bid her value for impression , regardless of how everyone else bids for that impression.

tCPA bidder: Such Bidder maximizes the number of conversions (i.e., the total value of the impressions which the bidder gets) subject to the constraint that the average cost per conversion is no greater than their tCPA . Namely, bidder solves the following maximization problem:

| s.t. | ||||

| (2) |

Budgeted bidder: Such Bidder maximizes the number of conversions subject to a budget constraint . Namely, Bidder solves the following maximization problem:

| s.t. | ||||

| (3) |

Notice that both tCPA bidder and Budgeted bidder are allowed to decide the fraction of an impression they get in case they are tied for that impression (we say that bidder is tied for an impression if ). This is in line with the standard approach in the literature (e.g., budget pacing equilibrium [13]) that endogenizes the tie-breaking rule as part of the equilibrium concept which we will define shortly. Moreover, in the following proposition, we show that given other bidders’ bids, it is optimal for a tCPA bidder (or a Budgeted bidder) to bid uniformly555Qualitatively, this is same as the well-known result of Aggarwal et al. [5]. They prove this by introducing small perturbations to bidders’ values. Instead, we take the approach that endogenizes the tie-breaking rule as part of the equilibrium concept, which is the standard approach in the literature for proving existence and computational complexity of equilibrium., i.e., the bids are characterized by a single bidding parameter as follows: .

Proposition 1.

The proof of Proposition 1 is provided in appendix.

3.2 Bidders’ Subgame

Bidders observe the reserve prices posted by the channels and decide their bids for each impression , and if a Bidder is tied for impression , they can also decide the fraction of impression they get. In the previous subsection, we have shown that for any bidder of any type, the best response given other bidders’ bids is bidding uniformly, and hence, we assume that each bidder uses uniform bidding with a bidding parameter .

Moreover, we assume that in the bidders’ subgame, bidders use the undominated uniform bidding strategies. Specifically, for a QL bidder, bidding less than their value is dominated by bidding their value, and for a tCPA bidder , using a bidding parameter less than is dominated by using a bidding parameter . To see the latter, notice that a tCPA bidder using a bidding parameter strictly less than cannot be tCPA-constrained since their cost for any impression they are winning cannot be more than their bid . Thus, their tCPA constraint, i.e., the first constraint in Problem (2), is not tight, and hence, by increasing their bidding parameter to , the bidder can only increase the total value without violating its tCPA constraint. In summary, we make the following assumption:

Assumption 1 (Uniform Undominated Bidding).

Each bidder uses uniform bidding, i.e., for some bidding parameter . Moreover, each QL bidder uses a bidding parameter , and each tCPA bidder uses a bidding parameter .

The equilibrium solution we adopt for the bidders’ subgame is a version of subgame perfection that takes into account endogenous tie-breaking rules, which is in line with the literature, e.g., the pacing equilibrium for Budgeted bidders [13] and the autobidding equilibrium for tCPA bidders [19].

Definition 1 (Subgame Bidding Equilibrium).

Consider the bidders’ subgame given reserve prices posted by the channels. An equilibrium for the subgame consists of bidders’ bidding parameters and probabilities of allocations of the impressions such that

-

(1)

Only a bidder whose bid is no less than the cost gets the impression: for , holds only if .

-

(2)

Full allocation of any item with a bid above the reserve price: for , must hold if there exists some such that .

-

(3)

Constraints are satisfied: for each , , and for each , .

-

(4)

For every Budgeted or tCPA bidder , even if they can decide the fraction of an impression they get in case they are tied for impression , increasing their bidding parameter would not increase their value without violating their budget/tCPA constraint.

The existence of subgame bidding equilibrium is a straightforward consequence by adapting the existence proofs of the pacing equilibrium for Budgeted bidders [13] and the autobidding equilibrium for tCPA bidders [19].

Proposition 2.

In the bidders’ subgame, the subgame bidding equilibrium always exists.

3.3 Channels

We focus on two models that depend on the objective functions the channels may have: the Local channels model and the Global channels model.

Local Channels Model: In this case, each channel sets its reserve price to maximize its own revenue given the other channels’ reserve prices . Thus, channel solves

Global Channels Model: In this case, the channels determine the reserve prices to maximize the sum of the revenue across all channels. Thus, they set reserve prices solving

3.4 The Full Game

We summarize the full game for the channels and the bidders as the following two-stage game:

-

(S0)

Each Channel chooses a uniform reserve price (in the cost-per-unit-value space) with finite precision666Note that assuming the reserve prices have finite precision is very natural for practice. for their impressions .

-

(S1)

Each Bidder observes the reserve prices posted by the channels (and the reserve prices prechosen by the publishers), and then they choose a bidding parameter and submit their bids according to (see Assumption 1). If Bidder is tied for impression , they can also decide the fraction of impression they get.

By Proposition 2, given any fixed in the support of the channels’ mixed strategies, stage (S1) has a subgame equilibrium between the bidders. We assume that stage (S1) always results into one such equilibrium deterministically, i.e., henceforth, we assume that in stage (S1) is always a fixed subgame equilibrium given (as defined in Definition 1).

Channels are allowed to use mixed strategies in stage (S0), i.e., sampling their reserve price from a distribution . Notice that the game for the channels is a finite game between finite players, and hence, there always exists a mixed-strategy equilibrium by the celebrated Nash’s theorem [21].

Additionally, we assume the game is complete-information. That is, are known to the channels and the bidders.

3.5 Important Concepts

We now present the main concepts which we will use to compare the outcomes of the local channels model to the global channels model.

Definition 2 (Liquid Welfare).

The liquid welfare of a fractional allocation is

and the optimal liquid welfare is .

This concept of liquid welfare has been previously studied in e.g., Aggarwal et al. [5] and Azar et al. [6], and it was first introduced by Dobzinski and Paes Leme [15]. It is well-known that optimal liquid welfare is an upper bound on the sum of the revenues of all channels. More precisely, optimal liquid welfare is greater or equal than the sum of the channels’ revenues, which we denote by , regardless of the reserve prices they choose:

Fact 1.

For any , .

Thus, we use the optimal liquid welfare as the benchmark to measure performance of the revenue in the local and global models. We let LocalEQ denote the set that contains every mixed-strategy equilibrium for the channels in the local channel model, and we define the revenue guarantees in the local and global models as follows:

Definition 3 (Revenue Guarantee).

The revenue guarantees for the local and global models are defined as

Note that any reserve prices in the support of any in the local model is also feasible in the global model, thereby giving us the following fact.

Fact 2.

Furthermore, to compare the outcomes of the two models, we use the standard notion of the Price of Anarchy [18].

Definition 4 (Price of Anarchy).

The Price of Anarchy (PoA) of the local model compared to the global model is

4 Hardness of equilibrium computation

In this section, we study the computational complexity of computing equilibrium of our game. Our main result in this section is that we show that even just finding the subgame equilibrium (Definition 1) for the bidders’ subgame is already computationally hard:

Theorem 1.

Finding the subgame equilibrium (Definition 1) is PPAD-hard.

We prove this by reduction from the problem of finding an approximate Nash equilibrium for the 0-1 bimatrix game, which was shown to be PPAD-hard in [12]. The basic idea of the proof is similar to that of the hardness result for finding a pacing equilibrium for budget-constrained quasi-linear bidders [11]. However, we have to handle many difficulties that are unique to tCPA bidders. Most notably, in contrast to budget-constrained quasi-linear bidders, whose bidding parameters are at most , tCPA bidders do not have a natural upper bound for their bids, and their bidding parameters can be arbitrarily high when their tCPA constraints are not tight. We construct new gadgets that force tCPA bidders’ bidding parameters to stay bounded but still leave a controlled amount of ”slack” for them, so that they can bid on impressions that are more expensive than their tCPA but not win all of them. We provide the full reduction in the appendix.

Despite the computational hardness, we are able to prove tight revenue guarantees that channels can achieve in the equilibrium, which we will present in the subsequent sections.

5 Revenue and Price of Anarchy with no Publisher Reserves

In this section, we focus on the setting where impressions do not have publisher-chosen reserve prices, i.e. for every . We study the revenue guarantees that the channels can achieve in the local model where each channel chooses their reserve price out of their own self-interest vs. the global model where the channels cooperatively choose the reserve prices to maximize their total revenue.

Our main results in this section are the following:

- •

-

•

Moreover, we prove that our revenue guarantee in the local model is tight even for the global model (Proposition 3).

- •

5.1 Revenue Guarantees

We begin by proving the main technical result of this section, which establishes a revenue guarantee for the local model. It is PPAD-hard to actually compute the equilibrium, as shown in Theorem 1. Nevertheless, we will show that each channel can set a certain reserve price in order to guarantee itself a decent amount of revenue, irrespective of the reserve prices set by other channels.

To do this, we will show that each channel can set a reserve price which ensures that its revenue is at least a certain fraction of the total budget of unconstrained Budgeted bidders (Lemma 1 and Corollary 1). Then, we will show that each channel can set a reserve price which ensures that its revenue is at least a certain fraction of its contribution to the optimal liquid welfare (Definition 2) from tCPA and QL bidders (Lemma 2 and Corollary 2). Finally, we will put these together to get the final revenue guarantee (Theorem 2).

The main difficulty in this proof comes from Budgeted bidders who are unconstrained, i.e. not spending their budget, at the equilibrium of the local model. The contribution to optimal Liquid Welfare from tCPA and QL bidders can be easily attributed to different channels (see the definition of and in Lemma 2) and there is a natural way for a channel to obtain a good fraction of its contribution as revenue (see Lemma 2). However, there is no obvious attribution for the contribution of Budgeted bidders to different channels, and no obvious lower bound on the bid of Budgeted bidders. In order to get a handle on unconstrained Budgeted bidders, we define the notion of Budget-fraction.

Definition 5 (Budget-fraction and , ).

For a Budgeted bidder , define their budget-fraction as , i.e., the ratio of their budget to the sum of their values of all impressions. Also, define and .

Intuitively, the budget-fraction for a Budgeted bidder plays a role similar to the tCPA of a tCPA bidder. With this, we are ready to prove some key technical claims that will help establish a lower bound on the bids of unconstrained Budgeted bidders, which in turn will help us find a good reserve price for these bidders.

Key Claims

Claim 1.

In a subgame equilibrium (Definition 1), if a Budgeted bidder is unconstrained, i.e. not spending all its budget, then they must be winning all impressions with and cannot be tied with another unconstrained Budgeted bidder on those impressions.

Proof.

Suppose for contradiction that a Budgeted bidder is unconstrained but does not fully win certain impression (i.e., ) such that . Notice that Bidder can increase the bidding parameter without increasing the total spend until Bidder is tied for (but does not fully win) some impression with . Such tie must occur, because otherwise, as Bidder increases , at some point Bidder will be tied for the impression . However, this contradicts item (4) of Definition 1, because Bidder can strictly increase the utility by increasing by a sufficiently small amount such that their budget constraint is not violated. ∎

The next claim follows directly from Claim 1.

Claim 2.

In a subgame equilibrium, for any impression , there can be at most one unconstrained Budgeted bidder with .

Next we prove the following claim, which will be helpful in bounding revenue against the optimal Liquid Welfare from unconstrained Budgeted bidders.

Claim 3.

If the final reserve price of an impression for a Budgeted bidder satisfies that , then impression will be sold for a cost at least in the subgame equilibrium.

Proof.

We first show that unless impression is fully sold to bidder (in which case the statement holds trivially because the cost of impression is at least its reserve price ), Bidder will bid for impression .

Suppose for contradiction. Recall that denotes the bidding parameter of Bidder . Since is assumed to be less than , we get . Moreover, because the total amount spent by Bidder is at most the sum of their bids, we have that

Thus, Bidder is unconstrained. By Claim 1, this bidder must be winning all its impressions.

The following claim, analogous to the claim above, will be used to bound revenue against the optimal Liquid Welfare from tCPA and QL bidders.

Claim 4.

If the final reserve price (i.e., in the cost space) of impression for a tCPA bidder (recall this is denoted by in the model section) satisfies that , then impression will be sold for a cost of at least in the subgame equilibrium. Similarly, if the final reserve price of impression for a QL bidder satisfies that , then impression will be sold for a cost of at least in the subgame equilibrium.

Proof.

Next, we first lower bound each channel’s revenue against the optimal Liquid Welfare contribution from Budgeted bidders (Lemma 1 and Corollary 1), and then we lower bound each channel’s revenue against the welfare contribution from tCPA and QL bidders (Lemma 2 and Corollary 2). Finally, we will put these together to get a lower bound on the revenue guarantee (Theorem 2).

Welfare from Budgeted Bidders

Lemma 1.

Let be any subgame equilibrium given any reserve prices. Define the following:

-

•

Let be the subset of Budgeted bidders who are constrained, i.e. are spending their entire budget in the equilibrium .

-

•

Let be the subset of Budgeted bidders who are unconstrained, i.e. are spending strictly less than their budget in the equilibrium .

-

•

For Channel and Budgeted bidder , let be the ratio of the total value of impressions in for Bidder to the total value of all impressions in for Bidder .

Then, for any ,

-

1.

in the equilibrium , the total revenue of all the channels from a Bidder is no less than their budget ,

-

2.

and moreover, if Channel could set bidder-specific reserve prices for each Budgeted bidder (recall is the budget-fraction in Definition 5), then regardless of other channels’ reserve prices, in the resulting subgame equilibrium (this is not necessarily ), Channel can obtain a revenue of at least

-

3.

and furthermore, Channel can set a uniform reserve price which is independent of such that regardless of other channels’ reserve prices, in the resulting subgame equilibrium (not necessarily ), Channel will obtain a revenue of at least

Proof.

-

1.

Since bidders are spending their entire budget in (by definition of ), the total revenue of all channels from them is equal to their budget.

-

2.

Consider any equilibrium resulting from Channel ’s bidder-specific reserve prices given in the statement and arbitrary reserve prices of other channels (note is unrelated to ). Consider any impression . Since Channel has set a bidder-specific reserve price of for each Budgeted bidder , the reserve price of impression for Budgeted bidder is . Then, by Claim 3, each impression is sold for a price of at least in the equilibrium for any . That is,

(4) Now let denote the set of the impressions such that . By Claim 2, if and are two bidders unconstrained in the equilibrium , then and are disjoint.

-

3.

The high-level idea for setting a good uniform reserve price is to bucketize the reserve prices and pick the one with the highest revenue potential. Specifically, we divide Budgeted bidders into the following buckets:

for (recall are the largest and smallest budget-fractions respectively defined in Definition 5). We observe that if Channel sets its uniform reserve price to , then for bidders , it holds that for all impressions . Thus, by Claim 3, each impression will get sold for a price of at least (the inequality is by bucketization) in the subgame equilibrium that results from Channel setting a uniform reserve price of and arbitrary reserve prices set by other channels. Thus, the revenue of Channel from setting a uniform reserve price to

(9) Now let denote the set of impressions such that . Then, by Claim 2, and are disjoint for two unconstrained Budgeted bidders in the equilibrium . Hence, we have that

(10) where the last inequality follows from the same derivation as in Inequalities (5-8).

Finally, let . Then, we have that the revenue of Channel by setting a uniform reserve price (notice is indeed independent of ) is

(By Inequality (9)) (By definition of )

∎

Item (3) in Lemma 1 implies the following corollary:

Corollary 1.

Define as in Lemma 1. Let be any mixed-strategy equilibrium of the channels’ game (i.e., S0), and let be the subgame equilibrium given any reserve prices in the support of the channels’ mixed strategies. Then, the expected revenue of Channel in the mixed-strategy equilibrium is at least

Welfare from tCPA and QL Bidders

Lemma 2.

Let be a welfare maximizing allocation (i.e., is s.t. in Definition 2) and

-

•

let be the liquid welfare generated by the impressions in allocated to tCPA bidders in , i.e.,

-

•

and let be the liquid welfare generated by the impressions in allocated to quasi-linear bidders in , i.e.,

Then, for any ,

-

1.

if Channel could set the bidder-specific reserve prices (also in the cost-per-unit-value space) for each tCPA or QL bidder as follows:

then Channel obtains a revenue at least regardless of what other channels do,

-

2.

and moreover, we let and let , and then Channel can set a uniform reserve price s.t. Channel obtains a revenue at least

regardless of what other channels do.

Proof.

-

1.

Fix Channel ’s bidder-specific reserve prices as in the assumption and consider any subgame equilibrium. For any impression , let Bidder , and let Bidder . Since , it follows from Claim 4 that impression will be sold for a cost of at least . Similarly, since , it follows from Claim 4 that impression will be sold for a cost of at least . Moreover, note that the contribution of impression to is at most , and we have shown impression will be sold for at least -fraction of this amount, it follows that channel ’s revenue is at least .

-

2.

The high-level idea for setting a good uniform reserve price is again to bucketize the bidder-specific reserve prices used above and set the uniform reserve price to the lower end of the bucket that has the highest revenue potential. Specifically, we divide all the tCPA bidders into the following buckets:

for .

As before, for any impression , let bidder and bidder , and notice that the contribution of impression to is at most .

If , let be such that . Suppose Channel sets a reserve price of which is strictly less than because of the bucketization. Then, by Claim 4, impression will be sold at a cost at least in the subgame equilibrium, where the inequality is because of the bucketization.

If , suppose Channel sets a reserve price . Then, by Claim 4, impression will be sold at a cost at least in the subgame equilibrium.

Now we put these two cases together. Let be the revenue of Channel at the subgame equilibrium if Channel sets a uniform reserve price (regardless of the reserve prices of other channels). Then, summing over all the buckets , we have

because as we have shown in the above case analysis, all the buckets together cover at least -fraction of the liquid welfare of each impression’s contribution to .

Let . Then, by setting a reserve price of , Channel can get a revenue of at least

∎

If Channel can always get certain amount of revenue by setting a particular uniform reserve price regardless of what other channels do, then Channel ’s revenue at any mixed-strategy equilibrium of the channels’ game (i.e., stage (S0) of the full game) is at least the same amount (because otherwise Channel will deviate to the uniform reserve price ). Thus, item (2) in Lemma 2 implies the following corollary:

Corollary 2.

Let and be defined as in Lemma 2 above. Then, for any , at any mixed-strategy equilibrium of the channels’ game (S0), the expected revenue of channel is at least

The Final Revenue Guarantee

Theorem 2.

For any ,

Proof.

Let be any mixed-strategy equilibrium of the channels’ game, and let denote the subgame equilibrium given any reserve prices in the support of the channels’ mixed strategies. Let be the liquid welfare maximizing allocation (i.e., is s.t. ).

By Corollary 2, the expected revenue of Channel in the equilibrium , denoted by , is

where and are defined as in Lemma 2.

Thus, the expected total revenue of all channels, denoted by , is

| (11) |

where and denote the total contributions of tCPA and QL bidders to the liquid welfare of respectively.

Also, by item (1) of Lemma 1, we have that

| (13) |

Corollary 3.

For any ,

Finally, we show that the above revenue guarantees in the local and global models are both tight up to a constant factor by constructing an example using the well-known ”equal-revenue” trick.

Proposition 3.

For the single-channel setting, there is an instance where .

Proof.

Since there is only one channel, .

Consider tCPA bidders with tCPAs for , each interested in a unique impression with a value of (i.e. their value for every other impression is 0, and everyone else’s value for their impression is 0). Similarly, there are Budgeted bidders with budgets for , each interested in a unique impression with a value of (i.e. their value for every other impression is 0, and everyone else’s value for their impression is 0). Optimal liquid welfare is obtained by giving everyone their unique impression. The best uniform reserve price cannot get a revenue more than . This shows that . ∎

5.2 Price of Anarchy

In this subsection, we study how much total revenue the channels lose in the local model where they set their uniform reserve prices out of their own self-interest compared to the global model where they choose the reserve prices cooperatively. Specifically, we consider the standard notion – price of anarchy (Definition 4). First, we observe that the revenue guarantee from Theorem 2 immediately implies a lower bound for the :

Theorem 3.

For any ,

Proof.

Next, we show that the lower bound in Theorem 3 is tight (up to a constant factor).

Theorem 4.

There is an instance with two channels such that .

The high-level idea:

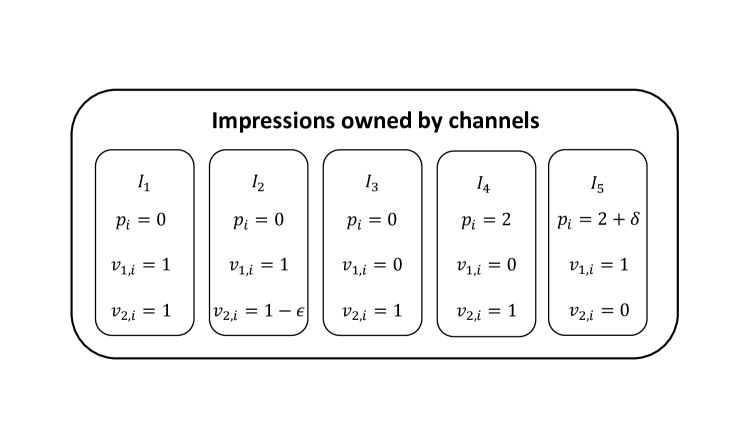

We first construct an “equal-revenue” instance (which consists of many tCPA bidders with geometrically decreasing tCPAs, each interested in a unique impression owned by Channel ) as in the proof of Proposition 3. For this “equal-revenue” instance, Channel cannot simultaneously get good revenues from all the bidders in by setting a uniform reserve price.

Now the key idea is to introduce another Channel and another tCPA bidder , such that Channel only owns one impression, for which only bidder has strictly positive value. Moreover, Bidder has a value for each impression in channel , and Bidder ’s value for impression is carefully chosen to be proportional to the tCPA of the bidder in who is interested in impression . Thus, if Bidder makes a uniform bid (in the cost-per-unit-value space), it results into non-uniform bids (in the cost space) for the impressions in Channel , which are proportional to the tCPAs of bidders in . We can think of these non-uniform bids as non-uniform bidder-specific reserve prices for bidders in , which are proportional to their tCPAs. Thus, we are able to extract the full revenue from all the bidders in (similar to item (1) of Lemma 2).

Finally, we just need to argue the above idea can only be successfully applied in the global model but not in the local model. This is because in the local model, Channel sets a high reserve price for its sole impression in order to profit more from bidder , and as a result, Bidder does not have enough “slack” to make a sufficiently high uniform bid to incur sufficiently high bidder-specific reserve prices for bidders in .

The construction of the instance with Budgeted bidders uses essentially the same idea as above. The full proof is provided in Appendix C.

Theorem 5 (Price of Anarchy).

.

6 Price of Anarchy with Publisher Reserves

This section studies the general version of the model where a publisher, owning impression , sets a minimum price for the impression to be sold.777Recall that the price is also in the cost-per-unit-value space. The main finding we obtain is that Theorem 5 dramatically depends on not having publisher prices. We show that with publisher prices and general channels, in the worst case (Theorem 6).

We then restrict our attention to an important subclass of instances where channels are scaled copy of each other. That is, channels share a set of a homogeneous set of impressions and differ on the revenue share each owns. In this context, we show that has non-trivial lower bound only if there is one bidder in the auction. In this case, , and hence, depends on the number of channels in the game in contrast to our results in Section 5.

General Channels

We now present the main result of the section for the general case when channels can have arbitrary asymmetries for the impressions they own with arbitrary publisher reserve prices.

Theorem 6.

If publishers can set arbitrary minimum prices on their impressions, then there is an instance for which .

Proof.

Consider the following instance with two channels and one bidder who is a tCPA bidder with a target constraint . Channel 1 has only one impression to sell. This impression does not have any publisher pricing constraint (). Channel 2 has impressions to sell, each of these impressions has the same publisher pricing constraint . The bidder’s valuation for all impressions is the same, i.e., for all .

We assert that in the global model, it is optimal to set reserve prices equal to zero for both channels. Indeed, with no reserve prices, the bidder can purchase all impressions since she gets a value of for a total cost of . This is the optimal solution for the global model as the total revenue is exactly the optimal liquid welfare.

On the other hand, in the local model, it is a strictly dominant strategy for Channel 1 to set a uniform reserve : if , Channel 1 gets zero revenue. If , the bidder purchases its impression, which leads to a revenue of . Thus, Channel 1 strictly prefers to set a reserve price of . Because of , the bidder cannot afford to buy any impression of Channel 2 since the cost of each impression is at least . Thus, in this equilibrium, the bidder submits a uniform bid of , gets only the impressions sold by Channel 1, and the global revenue is .

Therefore from this instance we have that . We conclude the proof by taking . ∎

The intuition behind the previous result comes from instances where some of the channels have high publisher prices relative to the bidder’s tCPA targets while some other channels do not have publisher prices. In these instances, in the global model, channels benefit by keeping low reserve prices in the cheap channels (without publisher reserves) as they provide subsidy to the tCPA bidders to buy impressions from the expensive channels. However, when the cheap channels are myopic, they would like to raise their reserve prices to increase their local revenue. This local behavior negatively impacts the revenue of the expensive channels, which in turn, is negative for all channels.

Given that the reason for the previous negative result is the asymmetry of the publisher prices on the different channels, in what follows we restrict our analysis for a special subclass where channels are scaled versions of each other.

Scaled Channels

The scaled channels model consists of weights 888 is the unit simplex in so that Channel owns a fraction of each impression .999For simplicity of the exposition we assume that impressions are divisible. A similar model with non-divisible impressions would assume that each impression is duplicated so that Channel owns a fraction of those duplicates.

The first result shows that, surprisingly, so long as there are more than one bidder participating in the auctions, then in the worst case.

Theorem 7.

For the scaled channels models if there are two or more bidders participating in the auctions, then there is an instance for which .

The instance we construct (deferred to Appendix D) consists of two channels and two tCPA bidders. The idea of the instance is that the main source of revenue for the channels comes from Bidder 1 buying the expensive impressions, those with high publisher reserve price. Bidder 1 needs enough slack to be able to purchase those expensive impressions. Thus, Bidder 1 needs to buy enough cheap impressions. However, the cheap impressions may have a high price if Bidder 2 sets a high bid. Bidder 2 can only set a high bid if, instead, it has enough slack from (other) cheap impressions. The crux of the argument is that, in the global model, by setting a sufficiently high reserve price, the channels can avoid Bidder 2 to have enough slack. This, in turn, allows Bidder to have slack to buy the expensive impressions. On the contrary, for the local models, there is an equilibrium where both channels set a low reserve. This prevents Bidder 1 to buy expensive impressions because Bidder 2 is setting a high bid and removing Bidder 1’s slack.

As a corollary of this instance, we show that in the autobidding framework setting a high reserve price like in the global model not only increases revenue but also increases the welfare. This contrasts with the classic profit-maximizing framework where there is a negative correlation between high reserve prices and welfare.

We finish this section by showing that for the case of only one bidder participating across all channels the is always strictly positive (for pure-strategy equilibria).

Theorem 8.

If there is only a single bidder, then for pure-strategy equilibria we have that , where is the number of channels in the game.

7 Further Discussion

In this paper, we have established tight bounds on revenue guarantees and Price of Anarchy when the reserve prices are set in the cost-per-unit-value space. Two natural follow-up questions are:

- •

Can we obtain similar bounds for welfare of the bidders?

- •

What are the revenue guarantees if the channels set reserve prices in the cost-per-impression space?

We briefly discuss how to extend some of our results to answer these questions. We defer the details to the full paper.

Bounds for Welfare

Most of our revenue and Price of Anarchy results carry over to welfare. In particular for the setting without publisher reserves, we can get bounds similar to the the revenue bounds in Theorem 2 and Proposition 3 and the Price of Anarchy bound in Theorem 5 for welfare (see Appendix E for a proof sketch). Many of the results in the setting without publisher reserves also carry over to welfare. We defer the details to the full paper.

We also observe an interesting phenomena – in contrast to the quasi-linear setting, using a higher reserve price can sometimes increase the welfare (see the discussion after Theorem 7).

Uniform cost-per-impression reserve prices

We can obtain a revenue guarantee analogous to Theorem 2 when channels set uniform cost-per-impression reserve prices (i.e., value-independent and the same for all bidders and impressions). We can do this by adapting the bucketization arguments in Section 5 to bucketize instead of for tCPA bidders, bucketize for Quasi-linear bidders, and bucketize instead of for Budgeted bidders.

References

- [1]

- About App campaigns [[n. d.]] About App campaigns [n. d.]. About App campaigns. https://support.google.com/google-ads/answer/6247380?hl=en. Accessed: 2022-02-08.

- About Performance Max campaigns [[n. d.]] About Performance Max campaigns [n. d.]. About Performance Max campaigns. https://support.google.com/google-ads/answer/10724817?hl=en. Accessed: 2022-02-08.

- About the Delivery System: Placements [[n. d.]] About the Delivery System: Placements [n. d.]. About the Delivery System: Placements. https://www.facebook.com/business/help/965529646866485?id=802745156580214. Accessed: 2022-02-08.

- Aggarwal et al. [2019] Gagan Aggarwal, Ashwinkumar Badanidiyuru, and Aranyak Mehta. 2019. Autobidding with Constraints. In Web and Internet Economics - 15th International Conference, WINE 2019, New York, NY, USA, December 10-12, 2019, Proceedings (Lecture Notes in Computer Science, Vol. 11920), Ioannis Caragiannis, Vahab S. Mirrokni, and Evdokia Nikolova (Eds.). Springer, 17–30. https://doi.org/10.1007/978-3-030-35389-6_2

- Azar et al. [2017] Yossi Azar, Michal Feldman, Nick Gravin, and Alan Roytman. 2017. Liquid price of anarchy. In International Symposium on Algorithmic Game Theory. Springer, 3–15.

- Balseiro et al. [2021a] Santiago Balseiro, Yuan Deng, Jieming Mao, Vahab Mirrokni, and Song Zuo. 2021a. Robust Auction Design in the Auto-bidding World. Advances in Neural Information Processing Systems 34 (2021).

- Balseiro et al. [2021b] Santiago R. Balseiro, Yuan Deng, Jieming Mao, Vahab S. Mirrokni, and Song Zuo. 2021b. The Landscape of Auto-Bidding Auctions: Value versus Utility Maximization. Association for Computing Machinery, New York, NY, USA, 132–133. https://doi.org/10.1145/3465456.3467607

- Bidding on Twitter Ads [[n. d.]] Bidding on Twitter Ads [n. d.]. Bidding on Twitter Ads. https://business.twitter.com/en/help/troubleshooting/bidding-and-auctions-faqs.html. Accessed: 2022-02-08.

- Burguet and Sákovics [1999] Roberto Burguet and József Sákovics. 1999. Imperfect Competition in Auction Designs. International Economic Review 40 (1999), 231–247.

- Chen et al. [2021] Xi Chen, Christian Kroer, and Rachitesh Kumar. 2021. The Complexity of Pacing for Second-Price Auctions. In Proceedings of the 22nd ACM Conference on Economics and Computation (EC ’21). Association for Computing Machinery, 318.

- Chen et al. [2007] Xi Chen, Shang-Hua Teng, and Paul Valiant. 2007. The approximation complexity of win-lose games. In SODA, Vol. 7. Citeseer, 159–168.

- Conitzer et al. [2021] Vincent Conitzer, Christian Kroer, Eric Sodomka, and Nicolas E Stier-Moses. 2021. Multiplicative pacing equilibria in auction markets. Operations Research (2021).

- Deng et al. [2021] Yuan Deng, Jieming Mao, Vahab Mirrokni, and Song Zuo. 2021. Towards Efficient Auctions in an Auto-Bidding World. Association for Computing Machinery, New York, NY, USA, 3965–3973. https://doi.org/10.1145/3442381.3450052

- Dobzinski and Paes Leme [2014] Shahar Dobzinski and Renato Paes Leme. 2014. Efficiency guarantees in auctions with budgets. In International Colloquium on Automata, Languages, and Programming. Springer, 392–404.

- Ellison et al. [2004] Glenn Ellison, Drew Fudenberg, and Markus Möbius. 2004. Competing Auctions. Journal of the European Economic Association 2, 1 (03 2004), 30–66. https://doi.org/10.1162/154247604323015472 arXiv:https://academic.oup.com/jeea/article-pdf/2/1/30/10312861/jeea0030.pdf

- Google Ads Help Center: About automated bidding [[n. d.]] Google Ads Help Center: About automated bidding [n. d.]. Google Ads Help Center: About automated bidding. https://support.google.com/google-ads/answer/2979071?hl=en. Accessed: 2020-02-08.

- Koutsoupias and Papadimitriou [1999] Elias Koutsoupias and Christos Papadimitriou. 1999. Worst-Case Equilibria. In Proceedings of the 16th Annual Conference on Theoretical Aspects of Computer Science (Trier, Germany) (STACS’99). Springer-Verlag, Berlin, Heidelberg, 404–413.

- Li and Tang [2022] Juncheng Li and Pingzhong Tang. 2022. Auto-bidding Equilibrium in ROI-Constrained Online Advertising Markets. arXiv preprint arXiv:2210.06107 (2022).

- McAfee [1993] R. Preston McAfee. 1993. Mechanism Design by Competing Sellers. Econometrica 61, 6 (1993), 1281–1312. http://www.jstor.org/stable/2951643

- NAs [1951] JF NAs. 1951. Non-cooperative games. Annals of mathematics 54, 2 (1951), 286–295.

- Rankin [1968] RA Rankin. 1968. Real and Complex Analysis. By W. Rudin. Pp. 412. 84s. 1966.(McGraw-Hill, New York.). The Mathematical Gazette 52, 382 (1968), 412–412.

- Tiktok Business Help Center: About App Event Optimization [[n. d.]] Tiktok Business Help Center: About App Event Optimization [n. d.]. Tiktok Business Help Center: About App Event Optimization. https://ads.tiktok.com/help/article?aid=179845248081724490. Accessed: 2022-02-08.

- Virág [2010] Gábor Virág. 2010. Competing auctions: Finite markets and convergence. Theoretical Economics 5, 2 (2010), 241–274. https://doi.org/10.3982/TE538 arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.3982/TE538

- Your Guide to Meta Bid Strategies [[n. d.]] Your Guide to Meta Bid Strategies [n. d.]. Your Guide to Meta Bid Strategies. https://www.facebook.com/business/m/one-sheeters/facebook-bid-strategy-guide. Accessed: 2022-02-08.

Appendix A Bidding Uniformly is Optimal

Proof of Proposition 1.

We prove the proposition using a greedy-exchange argument. We will maintain the invariant . Initially, we let and , and then we update them using a greedy procedure: Until the first constraint in Problem (2) (or (3) resp.) is tight for solution or (i.e., bidder has already won every impression for which they have strictly positive value), do the following

-

1.

if bidder is tied for an impression and (when there are multiple such impressions, choose an arbitrary one), increase until or the stop condition is met,

-

2.

and if there is no such impression, increase until bidder is tied for a new impression and go to Step 1.

Notice that whenever the above procedure increases for an impression in Step 1, two things must hold: (i) for any impression such that , we have (because for any such , in the the above procedure, bidder would have been tied for before , and the above procedure would have already increased to ), and (ii) (because the procedure only increases when bidder is tied for impression ). Therefore, at any moment when the above procedure is increasing for some impression , impression must be the current “best bang for the buck”, i.e., among all the impressions such that , impression has the smallest cost-per-unit-value for bidder .

Now we let be the solution to Problem (2) (or (3) resp.) that the above greedy procedure converges to and let be any feasible solution to Problem (2) (or (3) resp.), and we want to show that is not worse than .

To this end, we rank all the impressions in according to their cost-per-unit-value for bidder in the increasing order , i.e., is a permutation over such that for any . Let be the smallest number such that . It must hold that . To see this, notice that if , because the greedy procedure prioritize increasing over any other for until the first constraint in Problem (2) (or (3) resp.) is tight, and for all by definition of , we must have (otherwise should violate the first constraint). If , then holds trivially. Since in both cases we have , and we assumed that , it follows that .

Let be such that . There must exist such WLOG, because otherwise it is obvious that is the better solution. Now consider the overall cost-per-unit-value and the total cost . Because , if we decrease by and increase by for , then neither nor can increase, and the total value does not change. (Note that such change for and is feasible after changing the bids and appropriately.)

Furthermore, we can repeat the above argument whenever there exists such that to make , which shows that achieves better (or equal) total value than . ∎

Appendix B Proof of Hardness of Finding Subgame Equilibrium

In this section, we prove that it is PPAD-hard to find the subgame equilibrium (Definition 1) even when the subgame only consists of tCPA bidders and does not have reserve prices. Since we only consider tCPA bidders and no reserve prices in this section, we first simplify the notion of the subgame equilibrium by restricting to tCPA bidders in the following subsection.

B.1 Subgame Equilibrium for tCPA Bidders

Without reserve prices, the subgame equilibrium for tCPA bidders can be simplified as the following uniform-bidding equilibrium, which is essentially same as the autobidding equilibrium in [19], and hence, we also refer to the subgame for tCPA bidders as uniform-bidding game in this section.

Definition 6 (Uniform-Bidding Equilibrium for tCPA Bidders).

In the subgame with items (impressions) and tCPA bidders with tCPAs , let be the vector of the bidders’ bidding parameters, where , and let be the vector of the allocations of the items, where is the fraction of item being allocated to bidder , and thus , and let be the second highest bid for item , and thus bidder pays for item . We say is a uniform-bidding equilibrium if

-

(1)

Only the bidder with highest bid gets the item: only if for all .

-

(2)

Full allocation of any item with a positive bid: if for some .

-

(3)

tCPAs are satisfied: for each , .

-

(4)

Every bidder’s bidding parameter is such that even if they can decide the fraction of an item they get in case of a tie, increasing their bidding parameter would not increase their total value without violating their tCPA constraint.

B.2 Hardness of Finding the Uniform-Bidding Equilibrium

We reduce computing an (approximate) mixed-strategy Nash equilibrium of a 0-1 (win-lose) bimatrix game to computing a uniform-bidding equilibrium of the uniform-bidding game for tCPA bidders. The basic idea of the reduction is similar to that of the hardness result for finding uniform-bidding equilibrium for budget-constrained quasi-linear bidders [11]. However, we do have to handle many difficulties that are unique to the tCPA constraints. Most notably, in contrast to budget-constrained quasi-linear bidders, whose bidding parameter is at most , tCPA bidders do not have a natural upper bound for their bids, and their bidding parameters can be arbitrarily high when their tCPA constraints are not binding.

We start by defining the 0-1 bimatrix game and the approximate Nash equilibrium of this game.

Definition 7 (0-1 bimatrix game ).

In a 0-1 bimatrix game, there are two players, and they both have strategies to choose from. Player 1’s cost matrix is , i.e., player 1’s cost is if player 1 plays the -th strategy, and player 2 plays the -th strategy. Similarly, player 2’s cost matrix is , i.e., player 2’s cost is if player 1 plays the -th strategy, and player 2 plays the -th strategy..

Definition 8 (-approximate Nash equilibrium).

In a 0-1 bimatrix game , suppose that player 1 plays mixed strategy s.t. , and player 2 plays mixed strategy s.t. . Then, we say is an -approximate Nash equilibrium if it holds for all s.t. that

Finding an approximate Nash equilibrium for 0-1 bimatrix game was shown to be PPAD-hard [12].

Lemma 3 (Chen et al. [12, Theorem 6.1]).

For any constant , finding -approximate Nash equilibrium for 0-1 bimatrix game is PPAD-hard.

Now, given a 0-1 bimatrix game with arbitrary cost matrices and , we construct a uniform-bidding game for tCPA bidders as follows.

B.2.1 Construction of Hard Instance

- Bidders:

-

For each player and each strategy , we introduce two tCPA bidders and . In addition, we have two more tCPA bidders and .

- Items:

-

For each and each , we construct an expensive item , a cheap item , a set of normalized items , and a set of expenditure items for bidder , and moreover, we construct a cheap item for bidder . Furthermore, we have a special item for bidders and and a cheap item for bidder .

- Valuations:

-

We first give an informal description of the valuations, and then we provide the formal definition. Let and .

Bidder has high values (i.e., ) for the items and , medium values (i.e., ) for their own normalized items , low values (i.e., ) for their own expenditure items , normalized item , and bidder ’s -th normalized item , and negligible values (i.e., ) for bidder ’s -th expenditure item . Bidder ’s valuation is analogous.

On the other hand, bidder has the same value (i.e., ) as bidder for bidder ’s -th normalized item and value for their own item .

Bidder has the same value (i.e., ) as bidder for bidder ’s expensive item and value for the item . Bidder has the same value (i.e., ) for the item as bidder and value for their own item .

Formally, we use the notation to denote a bidder’s value of an item. For all , all distinct and all , we let

Moreover, we let for all and , and . For any other pair that did not appear above, .

- tCPAs:

-

Bidder ’s tCPA is , and bidder ’s tCPA is . For all and , bidder ’s tCPA is , and

B.2.2 Proof of Hardness

Theorem 9.

It is PPAD-hard to find a uniform-bidding equilibrium in uniform-bidding game for tCPA bidders.

We prove Theorem 9 by showing that if we find a uniform-bidding equilibrium for our hard instance , then we also find a -approximate Nash equilibrium for the 0-1 bimatrix game (the theorem follows by Lemma 3). We split the proof of the theorem into a series of lemmata.

Lemma 4.

In any uniform-bidding equilibrium of , for all and , bidder ’s bidding parameter is at least .

Proof.

Suppose for contradiction bidder ’s bidding parameter is strictly less than . Then, bidder does not get any fraction of the item , because bidder has the same value for the item as bidder , and bidder ’s bidding parameter is at least bidder ’s tCPA, which is . Now let us upper bound the CPA (cost-per-acquisition, i.e., bidder’s total payment divided by bidder’s total value) of bidder .

First, the total value that bidder gets is at least the value of the item , which is , because no one other than has positive value for , and hence always wins for free.

Moreover, the total payment that bidder makes is at most ’s bidding parameter times ’s total value of the items except and , because does not get any fraction of and gets for free. It is straightforward to verify that by construction of , ’s total value of the items except and is less than . Since we assume for contradiction that ’s bidding parameter is less than , the total payment makes is less than .

Thus, bidder’s ’s CPA is less than , which is much less than ’s tCPA. Next, we show that this contradicts the fourth property in Definition 6. Specifically, we can first assume WLOG that bidder does not tie for any item, because otherwise can increase the bidding parameter by an arbitrarily small amount such that gets the full item which ties for, and would still be an upper bound of ’s total payment (by the same argument as before), which contradicts the fourth property in Definition 6. Then, we notice there exist items for which bidder has positive value such as . Therefore, if raises the bidding parameter until the first time ties for a new item for which has positive value, then because already gets positive value with a CPA that is much less than ’s tCPA, can afford at least a fraction of that new item (which contradicts the fourth property in Definition 6). ∎

Lemma 5.

In any uniform-bidding equilibrium of , bidder ’s bidding parameter is equal to bidder ’s bidding parameter, and bidder ’s bidding parameter is equal to bidder ’s bidding parameter for all and .

Proof.

First, we show that in a uniform-bidding equilibrium, bidder ’s bidding parameter is equal to bidder ’s bidding parameter. Notice that no one other than bidder has positive value for the item , and thus, gets with value for free, which gives the flexibility to afford certain fraction of the item regardless of its price, because bidder ’s tCPA is positive. Since bidder has the same value (i.e., ) for the item as bidder and can always afford a fraction of , it follows by the fourth property in Definition 6 that in a uniform-bidding equilibrium, ’s bidding parameter should be no less than ’s bidding parameter. On the other hand, if ’s bidding parameter is strictly greater than ’s bidding parameter, which is at least , then will win the full item for a price that is at least , and it follows that ’s CPA is at least , which is much higher than ’s tCPA (i.e., ). Thus, ’s bidding parameter is no greater than (and hence equal to) ’s bidding parameter.

The proof of the equivalence between bidder ’s bidding parameter and bidder ’s is similar. Specifically, also has a free item with value , and also has a positive but tiny tCPA (i.e., ), and thus, can afford certain fraction of the item . Notice that and have the same value (i.e., ) for the item , and ’s bidding parameter is no less than ’s tCPA (). The rest of the proof is same as the proof above for bidder and bidder . ∎

Lemma 6.

In any uniform-bidding equilibrium of , bidder ’s bidding parameter is .

Proof.

’s bidding parameter is at least , because ’s tCPA is . It suffices to prove that ’s bidding parameter is at most .

Now suppose for contradiction, bidder ’s bidding parameter is strictly greater than . In the proof of Lemma 5, we have shown that bidder ’s bidding parameter is equal to ’s bidding parameter and that can not afford the full item . Therefore, must get a fraction of by the second property of Definition 6, and the payment per value makes for is exactly ’s bidding parameter, which is strictly greater than by our assumption for contradiction. Moreover, for all and , (i) by Lemma 4, bidder ’s bidding parameter is at least , and (ii) bidder has the same value for the item as bidder by construction of . Hence, if bidder wins any fraction of the item for any and , the payment per value makes for is at least . Therefore, overall, bidder ’s CPA is strictly greater than and thus violates ’s tCPA, which is a contradiction. ∎

Lemma 7.

In any uniform-bidding equilibrium, for all and , bidder wins at least fraction of the item .

Proof.

Bidder and bidder tie for the item , because they have the same value for this item and the same bidding parameter by Lemma 5. Thus, the payment per value for the item is equal to ’s bidding parameter which is . Since the only other item bidder gets is (value and zero cost), and has tCPA , it follows by straightforward calculation that can afford no more than fraction of the item . By the second property in Definition 6, wins at least fraction of . ∎

Lemma 8.

In any uniform-bidding equilibrium of , for all and , bidder ’s bidding parameter is strictly less than .

Proof.

We prove the lemma for bidder (the case of bidder is analogous). Suppose for contradiction bidder ’s bidding parameter is at least , we show that ’s tCPA must be violated. To this end, we count the total value gets and the total payment makes.

First, bidder is the only bidder who has postive value for the item . Thus, bidder gets value from the item with zero payment.

Notice that bidder and bidder have the same value for the item , and by Lemma 6, bidder ’s bidding parameter is which is strictly less than bidder ’s bidding parameter (), and hence, bidder wins the full item with payment and gets value .

Bidder and bidder have the same value for the item . Lemma 5 shows that bidder ’s bidding parameter is equal to bidder ’s bidding parameter (). Therefore, the price per value of the item is at least . By Lemma 7, gets at least fraction of the item and hence pays at least for that fraction of . That is, gets at most value from (because ’s value for the full item is ) and pays at least .

The other items for which bidder has positive value are , , and .

Because bidder has value for the item , and by Lemma 4 ’s bidding parameter is at least , if bidder wins the full item , the payment makes is at least . For and , because bidder has value for the item , and ’s bidding parameter is at least by Lemma 4, if bidder wins the full item , the payment makes is at least . We can assume WLOG that gets the full value of (i.e., ) with payment for each and gets the full value of (i.e., ) with payment for each , because these are the best payments per value can hope for these items, and these payments per value are much lower than ’s tCPA (). Namely, if ’s CPA does not exceed ’s tCPA, giving the items and to and charging the above payments per value will not violate ’s tCPA. Therefore, WLOG bidder gets value from the items and and pays .

On the other hand, because bidder has value and bidder has value for the item , and by Lemma 4 ’s bidding parameter is at least , if bidder wins any fraction of the item , the payment per value makes is at least (or bidder never wins any fraction of this item if ). For and , because bidder has value and bidder has value for the item , and ’s bidding parameter is at least by Lemma 4, if bidder wins any fraction of the item , the payment per value makes is at least . Notice that the payments per value for these items are all much higher than ’s tCPA, and hence, we can assume WLOG does not win any fraction of these items. Namely, if bidder ’s CPA does not exceed ’s tCPA, taking the items and away from bidder will not violate ’s tCPA. Therefore, WLOG bidder gets zero value from the items and and pays zero.

At the end of each paragraph above, we stated the values bidder gets from different items and the associated payments. In summary, bidder ’s total value is at most , and the total payment is at least . Thus, ’s CPA exceeds ’s tCPA, which is a contradiction. ∎

Lemma 9.

In any uniform-bidding equilibrium, for all , there exists such that bidder ’s bidding parameter is strictly greater than .

Proof.

We prove the lemma for (the case of is analogous). Suppose for contradiction that for all , bidder ’s bidding parameter is in (we know that it is at least by Lemma 4), we upper bound bidder ’s CPA.

First, bidder gets the item for free, since there is no competition for this item. Moreover, bidder can get a fraction of the item , since and have the same value for this item, and by Lemma 6 ’s bidding parameter is which is no larger than ’s. Let denote the fraction of the item which bidder wins, and hence gets value from and pays . Furthermore, For each , bidder gets the full item and pays at most , because bidder has value for this item, and ’s bidding parameter is less than by Lemma 8. For each and , bidder gets the full item and pays at most , because bidder has value for this item, and ’s bidding parameter is by our assumption. Finally, by Lemma 7, wins at least fraction of and pays at most (because ’s bidding parameter times ’s value for the full item is ). In addition, it is easy to verify that with bidding parameter , bidder can not get any fraction of the items and .

In summary, bidder gets total value at least and makes total payment at most . Therefore, the resulting upper bound of bidder ’s CPA is maximized when , and the maximum is

which is strictly less than ’s tCPA. Therefore, if raises the bidding parameter until the first time ties for a new item (such item exists, e.g., ), can afford a fraction of that item, which contradicts the fourth property in Definition 6. (One might notice that raising ’s bidding parameter will break the tie for the item between and , but this is not an issue, because in the above calculation for the upper bound of the total payment made by , we already take the payment for the full item into account.) ∎

Now we let denote bidder ’s bidding parameter and let denote a bidder ’s bidding parameter in a uniform-bidding equilibrium. We define a probability vector which corresponds to a mixed strategy for player 1 and a probability vector which corresponds to a mixed strategy for player 2 in the bimatrix game as follows

Note that is a valid probability vector, because for all , by Lemma 4, and there exists such that by Lemma 9. Similarly, is also a valid probability vector. The next lemma implies that is an -approximate Nash equilibrium of , which proves Theorem 9, because obviously can be computed efficiently from the uniform-bidding equilibrium of , and finding an -approximate Nash equilibrium of is PPAD-hard in general by Lemma 3.

Lemma 10.

For all , if bidder ’s bidding parameter is strictly greater than , then the -th strategy is a -approximate best response101010We say a pure strategy is an -approximate best response to the other player’s mixed strategy if the expected cost of this pure strategy is at most the expected cost of any other pure strategy plus . for player to player 2’s mixed strategy in the 0-1 bimatrix game . Similarly, if bidder ’s bidding parameter is strictly greater than , then the -th strategy is a -approximate best response for player to player 1’s mixed strategy in .

Proof.

We prove the first part of the lemma, i.e., if , then the -th strategy is an -approximate best response to . (The other part is analogous.) Formally, we want to show for all and , . By definition of , this inequality is equivalent to

By Lemma 4 and Lemma 9, is at least . Hence, it suffices to prove that for all and ,

| (14) |

First of all, we show that for all , bidder ’s tCPA must be binding WLOG. Specifically, by Lemma 8, bidder ’s bidding parameter is less than , which implies that does not get any fraction of the items . However, if ’s tCPA is not binding, can raise the bidding parameter and afford certain fraction of those items, which contradicts the fourth property in Definition 6. The only exception is that might have only won a fraction of the item because of a tie with bidder (or the item in case of a tie with bidder ), and then raising the bidding parameter might violate ’s tCPA constraint if can not afford the full item. However, in this case, we can simply increase the fraction of the item (or respectively) that gets and decrease the fraction that (or respectively) gets in the allocation vector of the uniform-bidding equilibrium until ’s tCPA is binding, and the result is still a uniform-bidding equilibrium. Thus,

It follows that

| (15) |

Next, we calculate bidder ’s and bidder ’s total payment and total value respectively to get different bounds for their CPAs.

First, for any (including and ), since except , only bidder bids on the item ( is ’s bidding parameter, and is ’s value for ), and by Lemma 8, (which is less than bidder ’s bid ), it follows that bidder wins all the items and pays . Moreover, by Lemma 7, bidder wins at least fraction of (and at most the full item), and because bidders and have the same bidding parameter by Lemma 5 and the same value for , pays at least (and at most ) for . Moreover, since except , only bidder bids on the item ( is ’s bidding parameter, and is ’s value for ), and by Lemma 8, (which is less than bidder ’s bid for ), it follows that bidder wins all the items and pays . Furthermore, bidder wins the item for free since there is no competition for this item. In addition, it is easy to verify that with bidding parameter , bidder can not get any fraction of the items and .

Finally, we calculate ’s value and cost for the item . To this end, we need to do case analysis for and (because although bidder ’s bidding parameter by our assumption, bidder ’s bidding parameter could be or exactly ). Since is the only bidder other than bids on the item ( is ’s value for , and is ’s bidding parameter by Lemma 6), it follows that wins by paying . Similarly, also bids on the item . However, since can be or exactly , we only know that bidder wins at least a fraction of the item . Let denote the fraction of which wins, and then pays for this item.

In summary, bidder gets total value at most and makes total payment at least . Thus,

| bidder ’s CPA | |||

Bidder gets total value at least and makes total payment at most . Thus,

| (because the first upper bound is maximized when ) | |||

Combining our lower bound of bidder ’s CPA and upper bound of bidder ’s CPA, we get

| (16) |

Putting Eq. (15) and Eq. (16) together, we have that

which implies that

This is exactly Eq. (14), which completes the proof. ∎

Appendix C Proof of Upper Bound of Price of Anarchy

Proof of Theorem 4.

We will construct two instances such that for the first instance, and for the second instance. The theorem follows by picking the instance with worse upper bound from those two instances (depending on which of and is larger). We let .