STEEL: Singularity-aware

Reinforcement Learning00footnotetext: Author

names are sorted alphabetically.

We thank Elynn Chen, Xi Chen, Max Cytrynbaum,

Lars Peter Hansen,

Clifford M. Hurvich, Max Tabord-Meehan, Chengchun Shi, Jin Zhou and other seminar participants at LSE, NYU Stern, University of Chicago for useful comments.

Abstract

Batch reinforcement learning (RL) aims at leveraging pre-collected data to find an optimal policy that maximizes the expected total rewards in a dynamic environment. Nearly all existing algorithms rely on the absolutely continuous assumption on the distribution induced by target policies with respect to the data distribution, so that the batch data can be used to calibrate target policies via the change of measure. However, the absolute continuity could be violated in practice especially when the state-action space is large or continuous. In this paper, we propose a new batch RL algorithm without requiring absolute continuity in the setting of an infinite-horizon Markov decision process with continuous states and actions. We call our algorithm STEEL: SingulariTy-awarE rEinforcement Learning. Our algorithm is motivated by a new error analysis on off-policy evaluation, where we use maximum mean discrepancy, together with distributionally robust optimization, to characterize the error of off-policy evaluation caused by the possible singularity and to enable model extrapolation. By leveraging the idea of pessimism and under some mild conditions, we derive a finite-sample regret guarantee for our proposed algorithm without imposing absolute continuity. Compared with existing algorithms, by requiring only minimal data-coverage assumption, STEEL significantly improves the applicability and robustness of batch RL. Extensive simulation studies and one (semi)-real experiment on personalized pricing demonstrate the superior performance of our method in dealing with possible singularity in batch RL.

1 Introduction

Batch reinforcement learning (RL) aims to learn an optimal policy using pre-collected data without further interacting with the environment. Recently, there is an increasing interest in studying batch RL, which has shown great potentials in many applications such as mobile health (Shi et al., 2020, 2021; Liao et al., 2022), robotics (Pinto & Gupta, 2016), digital marketing (Thomas et al., 2017), precision medicine (Kosorok & Laber, 2019), among many others.

Arguably, the biggest challenge in batch RL is the distributional mismatch between the batch data distribution and those induced by some candidate policies (Levine et al., 2020). It has been observed that, in practice, the distributional mismatch often results in an unsatisfactory performance of many existing algorithms, due to the insufficient coverage of the batch data (Fujimoto et al., 2019). From a theoretical standpoint, classical methods such as fitted q-iteration (Ernst et al., 2005) and policy iteration (e.g., Sutton et al., 1998) crucially rely on the full-coverage assumption for finding the optimal policy with the fixed dataset. The full-coverage assumption ensures that the distributions induced by all candidate policies can be well calibrated by the batch data generating process, using the change of measure, which could easily fail. To address this limitation, the recent literature (e.g., Kumar et al., 2019; Jin et al., 2021) has found that, by incorporating the idea of pessimism in the algorithm, the full-coverage requirement can be relaxed to only that the data cover the trajectories of an optimal policy, which is easier to satisfy. Here an optimal policy refers to either a globally optimal or an in-class optimal one.

Despite the recent progress, a key technical requirement for nearly all existing batch RL algorithms is the absolute continuity of the policy-induced distribution with respect to the batch data distribution. With this assumption, the change of measure is enabled and the concentrability coefficients (Munos, 2003) is used to characterize the deviation between the data distribution and the one induced by some target policy. However, in real applications, this assumption is not known a priori and could be easily violated. For example, when the action space is continuous, and all candidate policies are deterministic but the behavior one used to collect the batch data is stochastic, absolute continuity fails to hold and the singularity issue arises. Meanwhile, the concentrability coefficients is no longer well defined. Moreover, for many complex RL tasks such as robotic controls, the state and action spaces could be extremely large and high-dimensional. Due to the lack of interaction with the environment, some important state-action subspace induced by the optimal policy could be inevitably less explored by the behavior policy, which leads to an issue of a non-overlapping support. In this case, the requirement of absolute continuity cannot be satisfied either. Therefore, most existing batch RL algorithms cannot guarantee to obtain an optimal policy in both cases.

1.1 Our Contribution: A Provably Efficient RL Algorithm Allowing for Singularity

Motivated by the aforementioned issue, in this paper, we study batch RL with potential singularity. We consider an infinite-horizon Markov decision process (MDP) with continuous states and actions, despite that our idea is equally applicable to other setups. We propose an efficient policy-iteration-type algorithm, without requiring any form of absolute continuity. By saying an efficient algorithm, we refer to that the sample complexity requirement in finding an optimal policy is polynomial in terms of key parameters. We call our algorithm STEEL: SingulariTy-awarE rEinforcement Learning.

Our algorithm is motivated by a new error analysis on off-policy evaluation (OPE), which has been extensively studied in the recent literature. The goal of OPE is to use the batch data for evaluating the performance of other policies. By leveraging Lebesgue’s Decomposition Theorem, we decompose the error of OPE into two parts: the absolutely continuous part and the singular one with respect to the data distribution. For the absolutely continuous part, which can be calibrated by the behavior policy using the change of measure, standard OPE methods can be applied for controlling the error. For the singular part, we use the maximum mean discrepancy and leverage distributionally robust optimization to characterize its worst-case error measured by the behavior policy. Once we understand these two sources of the OPE error induced by any given target policy, a new estimating method for OPE without requiring absolute continuity can be formulated, based on which a policy iteration algorithm with pessimism is proposed.

From theoretical perspective, we show that under some technical conditions and without requiring absolute continuity, the regret of our estimated policy converges to zero at a satisfactory rate in terms of total decision points in the batch data. This novel result demonstrates that our method can be more applicable in solving batch RL problems, in comparison to existing solutions. More specifically, when the distribution induced by the optimal policy is covered by our batch data generating process in the usual manner, we recover the existing theoretical results given by those pessimistic RL algorithms (e.g., Xie et al., 2021; Fu et al., 2022). In contrast, when absolute continuity fails, our algorithm is provable to find an optimal policy with a finite-sample regret warranty. To the best of our knowledge, this is the first finite-sample regret guarantee in batch RL without assuming any form of absolute continuity. Moreover, our work can provide theoretical guidance on the existing algorithms aiming to find a deterministic optimal policy in a continuous action space. For example, our STEEL method and the related theoretical results can be helpful for improving the understanding of the celebrated deterministic policy gradient method (Silver et al., 2014).

To further demonstrate the effectiveness of our algorithm, we consider a contextual bandit problem and conduct extensive simulation studies. We show that compared with two existing baseline methods, under a possible singularity, our algorithm has a significantly better finite-sample performance. In particular, we observe that our algorithm converges faster and is more robust when the singularity arises. Lastly, we apply our method to a personalized pricing application using the data from a US auto loan company, and find that our method outperforms the existing baseline methods.

1.2 Relation to Existing Work

Classical methods on batch RL mainly focus on either value iteration or policy iteration (Watkins & Dayan, 1992; Sutton et al., 1998; Antos et al., 2008a). As discussed before, these methods require the full-coverage assumption on the batch data for finding the optimal policy, which is hard to satisfy in practice due to the inability to further interact with the environment. Failure of satisfying this condition often leads to unstable performance such as the lack of convergence or error magnification (Wang et al., 2021).

Recently, significant efforts from the empirical perspective have been made trying to address the challenge from the insufficient data coverage (e.g., Kumar et al., 2020; Fujimoto et al., 2019). The key idea of these works is to restrict the policy class within the reach of the batch dataset, so as to relax the stringent full-coverage assumption. To achieve this, the underlying strategy is to adopt the principle of pessimism for modeling the state-value function, in order to discourage the exploration over state-action pairs less-seen in the batch data. See Liu et al. (2020); Rashidinejad et al. (2021); Jin et al. (2021); Xie et al. (2021); Zanette et al. (2021); Zhan et al. (2022); Fu et al. (2022). Thanks to these pessimistic-type algorithms, the full-coverage assumption can be relaxed to the partial coverage or the so-called single-trajectory concentration assumption, i.e., the distribution induced by the (in-class) optimal policy is absolutely continuous with respect to the one induced by the behavior policy. This enhances the applicability of batch RL algorithms to some extent. However, this partial coverage assumptions still cannot be verified and hardly holds, especially when the state-action space is large or when the imposed policy class to search from is very complex (e.g., neural networks) that leads to unavoidable over-exploration. Our STEEL algorithm can address this limitation without assuming any form of absolute continuity, and can find an (in-class) optimal policy with a finite-sample regret guarantee. Thus, STEEL could be more generally applicable than existing solutions. The price to pay for this appealing property is a slightly stronger modeling assumption, i.e., Bellman completeness with respect to a smooth function class, which provides a desirable extrapolation property so that the singular part incurred by the distributional mismatch can be properly controlled.

Our STEEL algorithm is particularly useful for policy learning with a continuous action space, where the singularity arises naturally in the batch setting. This fundamental issue hinders the theoretical understanding of many existing algorithms such as deterministic policy gradient algorithms and their variants (e.g., Silver et al., 2014; Lillicrap et al., 2015). To the best of our knowledge, only Antos et al. (2008a); Kallus & Uehara (2020) in the RL literature tackle this problem. However, Antos et al. (2008a) imposes a strong regularity condition on the action space, which is hard to interpret and essentially implies that the -norm of any function over the action space is bounded by its -norm (multiplied by some constant). On the other hand, Kallus & Uehara (2020) used kernel smoothing techniques on the deterministic policy, which is known to suffer from the curse of dimensionality when the action space is large. Moreover, both Antos et al. (2008a) and Kallus & Uehara (2020) cannot address the possible singularity over the state space. In contrast, our STEEL algorithm can handle the singularity in both the state and action spaces with a strong theoretical guarantee. To the best of our knowledage, our paper is the first to address the aforementioned issue.

The rest of the paper is organized as follows. In Section 2, we introduce our setup, the discrete-time homogeneous MDP with continuous states and actions. We introduce related notations and also the problem formulation. Then, an illustrative example on the contextual bandit problem is presented in Section 3 for describing the challenge of policy learning without assuming absolute continuity. We also briefly introduce our solution in this section. In Section 4, we formally introduce the proposed method for finding an optimal policy when facing the possible singularity in batch RL. A comprehensive theoretical study of our algorithm is given in Section 5. Section 6 demonstrates the empirical performance of our methods using both simulation studies and a (semi-)real data application. Section 7 concludes this paper. All technical proofs can be found in the appendix.

2 Preliminaries and Notations

In this section, we briefly introduce the framework of the discrete-time homogeneous MDP and the related notations. Consider a trajectory , where denotes the state of the environment at the decision point , is the action and is the immediate reward received from the environment. We use and to denote the state and action spaces, respectively. Throughout this paper, we assume both and are continuous. It is worth mentioning that we allow to be a multi-dimensional action space, i.e., with , where is the space for -th coordinate of the action. Our method can also be applied in the general state-action space. The following two standard assumptions are imposed on the trajectory .

Assumption 1

There exists a time-invariant transition kernel such that for every , , and any set ,

where is the family of Borel subsets of and if . In addition, assume that for each , is absolutely continuous with respect to the Lebeque measure and thus there exists a probability density function associated with .

Assumption 2

The immediate reward is a known function of , i.e., for any , where . In addition, we assume is uniformly bounded, i.e., there exists a constant such that for every .

By Assumption 2, we define a reward function as for . The uniformly bounded assumption on the immediate reward is used to simplify the technical proofs and can be relaxed.

An essential goal of RL is to find an optimal policy that maximizes the expected discounted sum of rewards. A policy is a decision rule that an agent chooses her action based on the environment state at each decision point . In this paper, we focus on the stationary policy , which is a vector-valued function mapping from the state space into a probability distribution over the action space . Specifically, , where is a function mapping from into . For each policy , one can define a -function to measure its performance starting from any state-action pair , denoted by

| (1) |

where refers to the expectation that all actions along the trajectory follow the stationary policy . We evaluate the overall performance of a policy by the so-called policy value defined as

| (2) |

where is some known reference distribution. Here, for any function defined over , we define . Our goal in this paper is to search for an in-class optimal policy such that

| (3) |

where and is some pre-specified class of stationary policies for -th coordinate of . Some commonly used policy classes include linear decision functions, neural networks and decision trees. The sufficiency of focusing on the stationary policies is guaranteed by Assumptions 1 and 2. See Section 6.2 of Puterman (1994) for the justification. We also remark that stationary policy does not rule out the deterministic policy, which is a function mapping from the state space into the action space .

In this work, we focus on the batch setting, where the observed data consist of independent and identically distributed copies of up to decision points. For the -th trajectory, where , the data can be represented by . We aim to leverage the batch data to find an in-class optimal policy defined in (3). The following standard assumption is imposed on our batch data generating process.

Assumption 3

The batch dataset is generated by a stationary policy .

Next, we introduce the average visitation probability measure. Let be the marginal probability measure over at the decision point induced by the behavior policy . Then the average visitation probability measure across decision points is defined as

The corresponding expectation with respect to is denoted by . Similarly, we can define the discounted visitation probability measure over induced by a policy as

| (4) |

where is the marginal probability measure of induced by the policy with the initial state distribution . For notation simplicity, we also use and to denote their corresponding probability density function when there is no confusion.

Additional notations: For generic sequences and , the notation (resp. ) means that there exists a sufficiently large constant (resp. small) constant (resp. ) such that (resp. ). We use when and . For matrix and vector norms, we use to denote either the vector -norm or operator norm induced by the vector -norm, for , when there is no confusion. For any random variable , we use to denote the class of all measurable functions with finite -th moments for , where the underlying probability measure is . We may also write it as when there is no confusion about the underlying random vectors. Then the -norm is denoted by . We use to denote the point-wise sup-norm for a vector-valued function. For example, returns a vector with sup-norm on each coordinate for . In addition, we often use or to represent a generic transition tuple. We define the maximum mean discrepancy (MMD) between two probability distributions and as

| (5) |

where is a reproducing kernel Hilbert space (RKHS) with the kernel and the corresponding norm is denoted by . Lastly, we use when is absolutely continuous with respect to , and when is singular to .

3 An Illustrative Example: Contextual Bandit without Absolute Continuity

In this section, we use the offline contextual bandit problem (Manski, 2004) as an example to illustrate the challenge of policy learning without absolute continuity and our main idea to address it. Note that the contextual bandit problem is a special case of batch RL (i.e., ).

Suppose we have a batch dataset which contains i.i.d. copies from , where and is some unknown distribution. The target is to find an in-class optimal policy such that

| (6) |

Recall that .

Most existing methods for solving (6) rely on a key assumption that for all , under which one is able to use the batch data to calibrate and evaluate its performance via estimating for all . For instance, the regression-based approaches (Qian & Murphy, 2011; Bhattacharya & Dupas, 2012) consider a discrete action space, and require (i) is uniformly bounded away from 0 for all and , and (ii) . In this case, the absolute continuity holds. Meanwhile, the popular classification-based approaches (e.g., Zhao et al., 2012; Kitagawa & Tetenov, 2018; Athey & Wager, 2021; Mbakop & Tabord-Meehan, 2021; Kitagawa et al., 2022), which crucially rely on the inverse propensity weighting formulation, also have the same requirement. However, due to the distributional shift, such absolutely continuous assumption may not hold in general. There is a recent streamline of research studying contextual bandits under the framework of distributionally robust optimization such as Mo et al. (2021); Qi et al. (2022); Adjaho & Christensen (2022); Si et al. (2023) and the reference therein. These works investigate policy learning in the presence of distributional shifts in the covariates or rewards when deploying the policy in the future. In particular, Adjaho & Christensen (2022) considered to use Wasserstein distance for quantifying the distributional shift and can allow the singularity for such a shift. However, none of them study the policy learning when there is a singularity issue in terms of the policy during the training procedure. For example, when refers to some stochastic policy used to collect the data and is a class of deterministic policies, becomes singular to , i.e., for all . In this case, most existing methods may fail to find a desirable policy.

To address such singularity issue induced by the deterministic policy with respect to the stochastic one, existing solutions either adopt the kernel smoothing techniques on in order to approximately estimate (e.g., Chen et al., 2016) or impose some structure assumption on the reward function (e.g., Chernozhukov et al., 2019). The first type of approaches requires the selection of kernel and the tuning on the bandwidth for approximating all deterministic policies, while the latter one could suffer from the model mis-specification due to the strong (parametric) model assumption. It is also well-known that the performance of the kernel smoothing deteriorates when the dimension of the action space increases. In addition, these methods cannot handle general settings such as that is also singular to , i.e., there exists a covariate shift problem. This problem becomes more severe when considering the dynamic setting.

In the following, we present a brief description of our method for policy learning without requiring absolute continuity of the target distribution (i.e., ) with respect to the data distribution (i.e., ) in this contextual bandit problem. The idea relies on the following observation. Consider a fix policy . Let be any estimator for the reward function. It can be easily seen that

| (7) |

By leveraging Lebesgue’s Decomposition Theorem, we can always represent as

where and . Since and are finite measures, we normalize them and rewrite the above decomposition as

where and are two probability measures. In particular, if , the corresponding can be chosen as an arbitrary probability measure. Given this decomposition, one can further show that

In order to have an accurate estimation of , one needs to find an such that the absolutely continuous and singular parts in the above equality are minimized. For the absolutely continuous part, since is unknown, define as some class of symmetric functions and assume , we can show that

The right-hand side of the above inequality can be properly controlled using the batch data because now follows . To handle the singular part, we adopt the idea of distributionally robust optimization (e.g., a review paper by Rahimian & Mehrotra, 2019) with MMD. We can show that

Summarizing the above derivations together, we can quantify the error of using for estimating as

where the last inequality is given by Lemma 2 in the later section under some mild conditions. Moreover, it can be checked that if , the right-hand side of the above inequality vanishes. These facts motivate us to estimate the reward function and later via

| (8) | ||||

We remark that two terms: and are irrelevant to and could be estimated when is known. Once we are able to provide a valid estimation for , an optimization rountine can be implemented to estimate , where we incorporate the idea of pessimism. Specifically, for each given , we first implement the kernel ridge regression using for estimating . Denote the resulting estimator by . Note that is some candidate reward function. Then we propose to compute the optimal policy via solving the maximin problem

| (9) | ||||

| subject to | ||||

where is some pre-specified class of functions for modeling the true reward function and refers to the empirical average over the batch data . Two constants and are used to quantify the uncertainty for estimating and also control the degree of pessimism. We remark that the RKHS norm in (9) can be computed explicitly when kernel ridge regression is used in estimating . Under some technical conditions, with properly chosen and , we can show that the true reward function always belongs to the feasible set of (9). Therefore, by implementing the above algorithm, we search a policy that maximizes the most pessimistic estimation of its value within the corresponding uncertainty set. The proposed algorithm will produce a valid policy with regret guaranteed and without assuming absolute continuity. The details of our contextual bandit algorithm can be found in Section 6.

4 Policy Learning in Batch RL

In this section, we consider policy learning in batch RL and generalize the idea in the last section with more details. Our proposed algorithm for obtaining is motivated by the analysis of OPE.

4.1 Off-policy Evaluation with Potential Singularity

For any given policy , the target of OPE is to use the batch data to estimate the policy value defined in (2). Note that by the definition of the discounted visitation probability measure, we can show that

where recall that for any . A direct approach to perform OPE is via estimating defined in (1). Let be any estimator for and define the corresponding estimator for the policy value as . Then we have the following lemma to characterize the estimation error of to .

Based on Lemma 1, if , then by change of measure and assuming that , where recall that is a symmetric class of functions, we can obtain that

This naturally motivates a minimax estimating approach to learn and hence , i.e.,

which has been used in the literature of OPE (e.g., Jiang & Huang, 2020).

However, as discussed before, due to the potentially large state-action space, it is quite usual that some values of the state-action pairs induced by the target policy are not covered by the batch data generating process, causing the out of support issue. In addition, there are many applications where is a deterministic policy but the behavior one is stochastic (e.g., Silver et al., 2014; Lillicrap et al., 2015). In either of these cases, fails to hold and the above minimax estimating approach may no longer be valid for OPE as it cannot upper bound the estimation error of . Indeed, similar to the contextual bandit example discussed in the previous section, most of existing OPE (and policy learning) approaches in batch RL rely on this absolute continuity assumption, which could be illusive in practice.

Motivated by this gap, in the following, we do not assume the absolute continuity of with respect to , i.e., there exists a measurable subset such that but . Again, by Lebesgue’s Decomposition Theorem, with some abuse of notations, there always exist two finite measures and over such that

where and . By normalization, we can rewrite the above decomposition as

where and are two probability measures. Similar to the contextual bandit example, we can decompose the OPE error as

The absolutely continuous part can be properly controlled by using the above minimax formulation. However, the singularity of with respect to is the major obstacle that makes most existing OPE approaches not applicable. To address this issue, one must rely on the extrapolation ability of . As the difficulty of OPE largely comes from the distributional mismatch between and , we leverage the kernel mean embedding approach to quantifying the difference between and in order to control the singular part. See Lemma 6 in the appendix for the existence of kernel mean embeddings, which follows from Lemma 3 of Gretton et al. (2012).

Next, we present our formal result in bounding the OPE error of . Define the Bellman operator as

for any transition tuple . Since , by the Radon-Nikodym Theorem, we can define the Radon-Nikodym derivative as

for every . Recall that is a symmetric class of functions defined over . Without loss of generality, we assume that . We have the following key lemma for our proposal. For notation simplicity, let and denote .

Lemma 2

Given a policy , assume that the kernel is measurable with respect to both and , and . In addition, suppose and . Then the following holds.

| (11) |

Lemma 2 provides an upper bound for the estimation error of OPE using any estimator for . Moreover, it can be further checked that if , by Bellman equation,

Based on the above analysis, we propose to estimating by solving the following minimax problem.

| (12) | ||||

To use the above procedure for OPE, for each policy , one needs to estimate and first or find some constants that serve as upper bounds. This new method will serve as the foundation of our proposed algorithm developed below.

4.2 Policy Optimization under Potential Singularity

Recall that our goal is to leverage the batch data to estimate the in-class optimal policy . For any policy , we can implement the empirical version of (12) for obtaining the estimation of and hence perform the policy evaluation. This motivates us to develop a pessimistic policy iteration algorithm for finding .

Pessimism in batch RL serves as the main tool for efficient policy optimization by quantifying the uncertainty of the estimation and discouraging the exploration of the learned policy from visiting the less explored state-action pair in the batch data. The success of the pessimsitic-typed algorithms has been demonstrated in many applications (e.g., Kumar et al., 2019; Bai et al., 2022). In terms of the data coverage, instead of the full-coverage assumption (i.e., is uniformly bounded away from ) required by many classic RL algorithms, algorithms with a proper degree of pessimism only require that the in-class optimal policy is covered by the behavior one, which is thus more desirable. Adapting the pessimism idea to our setting without assuming absolute continuity, we expect to develop an algorithm that finds the optimal policy by at most requiring the data coverage assumption such that . This requirement is much weaker than those needed by all existing RL algorithms.

Let be some pre-specified class of functions over , which is used to model with . A key building block of our proposed algorithm is to construct the following two uncertainty sets for

| (13) | ||||

where and are some tuning parameters possibly depending on and , which will be specified later. Here

for any function , and is an estimator of to be specified later.

Based on the defined uncertainty sets , we propose to estimate the in-class optimal policy via

| (14) |

i.e., maximizing the worst-case policy value within the uncertainty sets. Note that our optimization problem (14) is free of and , compared with OPE using (12). Denote the resulting estimated policy as . In Section 5, we provide a regret guarantee for in finding under minimal data coverage assumption. The policy optimization problem (14), in its original form, may be difficult to solve because of the constraint set for , especially when and are highly complex such as neural networks. In the following, we propose to solve it via the dual formulation of the inner minimization problem in (14).

4.3 Dual Problem and Algorithm

Let be dual variables (i.e., Lagrange multipliers). Define a Lagrangian function as

| (15) | ||||

Based on the formulation of , we consider an alternative way to estimating the optimal policy by solving the equivalent optimization problem

| (16) |

where refers to the component-wise comparison. Note that compared with (14), Problem (16) can be solved in a more efficient manner as the optimization with respect to the two dual variables can be easily performed.

Denote the resulting estimated policy given by (16) as . By the weak duality, it can always be shown that

Therefore, solving Problem (16) can also be viewed as a policy optimization algorithm with pessimism. However, the strong duality for the primal and dual problems may not hold as the primal problem is not convex with respect to , which therefore leads to that in general. More seriously, the existence of the duality gap will result in a non-negligible regret of in finding . Nevertheless, in Section 5 below, we show that under one additional mild assumption, indeed can achieve the same regret guarantee as that of .

Now, to solve (16), we first estimate via kernel ridge regression. Specifically,

| (17) |

with the regularization parameter . Denote

Thanks to the representer theorem, we can show that

| (18) |

where is an identity matrix with the dimension .

Similarly, we use a RKHS to model . We set for some constant . We remark that a different kernel can be chosen for than the one used in the kernel ridge regression. By the representer property, we can obtain a closed-form optimal value for

which is given as

With these two choices, (16) is equivalent to

| (19) | ||||

Lastly, if letting and be any pre-specified functional classes such as neural network architectures, we can apply stochastic gradient decent to solve the primal-dual problem (19) and obtain . For the contextual bandit problem discussed in Section 3, we only need to let in (19) and input the data . See a pseudo algorithm of STEEL in Algorithm 1.

5 Theoretical Results

The performance of a policy optimization algorithm is often measured by the difference between the value of the (in-class) optimal policy and that of the estimated one, which is referred to as the regret. In our case, we evaluate the performance of any estimated policy via the regret defined as

| (20) |

Clearly, . In this section, we aim to derive the finite-sample upper bounds for both and . To begin with, we list several technical assumptions and discuss their corresponding implications.

5.1 Technical Assumptions

Assumption 4

The stochastic process induced by the behavior policy is stationary, exponentially -mixing. The -mixing coefficient at time lag satisfies that for and . The induced stationary distribution is denoted by .

Our batch data consist of multiple trajectories, where observations in each trajectory follow a MDP and thus are dependent. Assumption 4 characterizes the dependency among those observations, instead of assuming transition tuples are all independent as in many previous works. This assumption has been used in recent works (e.g., Chen & Qi, 2022). The upper bound on the -mixing coefficient at time lag indicates that the dependency between and decays to 0 at least exponentially fast with respect to . See Bradley (2005) for the exact definition of the exponentially -mixing. Recall that we have let and denoted .

Assumption 5

The kernel is positive definite, and . For any , is measurable with respect to both and .

The bounded and measurable conditions on the kernel in Assumption 5 are mild, which can be easily satisfied by many popular kernels such as the Gaussian kernel. Assumption 5 ensures that the conditions in Lemma 6 of the appendix hold so that the kernel mean embeddings exist. Assumption 5 also indicates that is compactly embedded in , e.g., for any , . See Definition 2.1 and Lemma 2.3 of Steinwart & Scovel (2012) for more details. Define an integral operator as

| (21) |

Assumption 5 implies that the self-adjoint operator is compact and enjoys a spectral representation such that for any ,

| (22) |

where is referred to as the inner product in , is a non-increasing sequence of eigenvalues towards and are orthonormal bases of . See Theorem 2.11 of Steinwart & Scovel (2012) for a justification of such spectral decomposition. We will use to characterize the bias/approximation error induced by the regularization (17). Define an operator such that

| (23) |

for every . Consider the following class of vector-valued functions as

where . For , we use to denote . In the following, we quantify the complexities of function classes used in our policy optimization algorithm via the -covering number. See definition of the -covering number in C.1 of the appendix.

Assumption 6

The following conditions hold:

-

(a)

For any , . For any , , and ,

(24) In addition, for any , we have

(25) where is some constant.

-

(b)

For any , . In addition, for any , we have

(26) where is some constant.

-

(c)

The policy class is a class of deterministic policies, i.e., . The action space is bounded. In addition, for any and , we have

(27) where is some constant. Let

-

(d)

For any , for some constant . In addition, for any , we have

(28) where is some constant.

Assumption 6 imposes metric entropy conditions on function classes , , and . For simplicity, we consider uniformly bounded classes for deriving the exponential inequalities for both scalar-value and vector-value function classes (Van Der Vaart & Wellner, 1996; Park & Muandet, 2022). One can generalize Assumption 6 to include more complicated function classes such as neural networks. See Lemma 5 of Schmidt-Hieber (2020) for an example. We also remark that , , and could increase with respect to and . In practice, one can specify , and and compute its corresponding complexity. In the later section, we provide a sufficient condition for computing . The Lipschitz-typed condition in (24) is imposed so that the -covering number of the following class of functions:

could be properly controlled by the -covering numbers of for and (Van Der Vaart & Wellner, 1996).

Next, recall that is a non-increasing sequence of eigenvalues towards and are orthonormal bases of . Define a space as

Assumption 7

For any , , and some constant , . In addition, is closed.

Assumption 7 is called Bellman completeness, which has been widely imposed in the literature of batch RL (e.g., Antos et al., 2008b). Since is closed, Assumption 7 also implies that for by the contraction property of Bellman operator. In other words, there is no model misspecification error for estimating for every . That basically states that for any , , there exists such that . In the standard literature of the kernel ridge regression (e.g., Smale & Zhou, 2007; Caponnetto & De Vito, 2007), for fixed and , a similar type of the smoothness assumption is also imposed but only requires . Here we impose a slightly stronger condition for obtaining a faster rate in terms of . In addition, we strengthen this smoothness assumption by considering for all and , which is used for controlling the bias uniformly over and induced by the regularization in the kernel ridge regression (17). See more discussion related to this in Remark 2 of Theorem 2. It is worth mentioning that one can choose and modify Assumption 6 (a) accordingly.

Assumption 8

For any and , , where and . In addition, uniformly over and .

Then we have the following lemma.

5.2 Regret Bounds

To derive the regret bounds for and , we first show that for every , is a feasible solution to the inner minimization problem of (14) with a high probability. Let

Theorem 1

Theorem 1 is the key for establishing the regret bounds of our proposed algorithms. By showing (29), we can guarantee that for every , is bounded below by the optimal value of the inner minimization problem in (14) with a high probability. This verifies the use of pessimism in our algorithms, i.e., evaluating the value of each by a lower bound during the policy optimization procedure. Since we require , the smallest value that can be set is of the order . Based on Theorem 1, we have the following regret warranty for .

Theorem 2 (Regret warranty for )

Under Assumptions 1-7, the following statements hold.

- (a)

-

(b)

Suppose and , then with probability at least ,

(31) -

(c)

Suppose , then with probability at least ,

(32)

In addition, all statements above hold if Assumption 6 (d) is replaced by Assumption 8. Finally, when defined in Assumption 7 (i.e., ), then by letting , all statements above hold.

Remark 1

Among all assumptions we have made, Bellman completeness (i.e., Assumption 7) and with (implicitly imposed by Assumption 6 (b)), are two main conditions for our regret guarantee stated in Theorem 2. The first condition is related to the modeling assumption, while the second one is related to our batch data coverage induced by the behavior policy.

In the existing literature, the weakest data coverage assumption for establishing the regret guarantee is with , i.e., absolute continuity with a uniformly bounded Radon–Nikodym derivative. See for example Xie et al. (2021) and Zhan et al. (2022). In contrast, our proposed method remains valid without requiring the absolute continuity. For example, in Case (a) of Theorem 2, to achieve the regret guarantee of our proposed method, we only require the ratio of the absolutely continuous part of with respect to over , i.e., , is uniformly bounded above, and the MMD between the singular part of with respect to and , i.e., , is finite, which is ensured by Assumption 5. Therefore our method requires much weaker assumptions (essentially no assumptions) on the batch data coverage induced by the behavior policy, and is thus more applicable than existing algorithms from the perspective of the data coverage. However, our method requires a stronger condition on modeling , which could be regarded as a trade-off. We require Bellman completeness for modeling (i.e., Assumption 7), while some existing pessimistic algorithms (e.g., Jiang & Huang, 2020) only require the realizability condition on modeling (i.e., there is no misspecification error for ).

It is worth mentioning that, when as discussed in the Case (b) of Theorem 2, becomes , with . In this case, we recover the existing results such as Jiang & Huang (2020) on the regret bound by running our algorithm. However, compared with their results, we require a stronger condition, i.e., Assumption 7 for modeling instead of realizability condition on only. The main reason for requiring a stronger condition here is due to the unknown information that . When as discussed in Case (c) of Theorem 2, it can be seen that . We showcase that the regret of our estimated policy can still possibly converge to in a satisfactory rate without any data coverage assumption. To achieve this, we rely on the Bellman completenss and the smoothness condition for enabling the extrapolation property. To the best of our knowledge, this is the first regret guarantee in batch RL without assuming the absolute continuity. See Table 1 for a summary of our main assumptions for obtaining the regret of the proposed algorithm compared with existing ones. Finally, when the smoothness condition stated in Assumption 7 fails, i.e., , the upper bound on the regret of our estimated policy becomes a constant and our method may not guarantee to find an optimal policy asymptotically.

Remark 2

Our proposed algorithm is motivated by Lemma 2, which provides a careful decomposition on the estimation error of OPE without relying on the absolute continuity. The key reason for the possible success of our algorithm in handling insufficient data coverage (i.e., the singular part) relies on the smoothness condition we imposed on modeling , i.e., Assumption 7, which provides a strong extrapolation property for our estimated for and . Specifically, for any state-action pair , where is a measurable set such that but , by leveraging the convolution operator , the corresponding can be extrapolated by the kernel smoothing of for all . Therefore, can approximate well in terms of the RKHS norm. Such an extrapolation property is inherited by -function due to the Bellman equation that .

Remark 3

In Case (b) of Theorem 2, where , to achieve the desirable regret guarantee, by implementing our algorithm without using the constraint set , we indeed do not require our batch data to uniquely identify or for but only . Specifically, for a fixed policy , we allow that there exist two different and under the batch data distribution such that

In addition, because we do not require for modeled correctly or being uniformly bounded above, the above equality cannot ensure that

Thus for are not required to be identified by our batch data either if our proposed algorithm is implemented without incorporating . However, due to the unknown information on (e.g., whether Case (b) happens or not), our algorithm has to include the constraint set for handling the error induced by the possibly singular part, which implicitly imposes that and can be uniquely identified by our batch data for because of the strong RKHS norm used in . This is another trade-off for addressing the issue of a possible singularity. Lastly, we would like to emphasize and are only related to the in-class optimal policy .

Next, we develop a finite-sample regret bound for . Consider the following constrained optimization problem, which corresponds to the population counterpart of (30) with fixed and

where

Define the corresponding Lagrangian function as

| (33) | ||||

which could be roughly viewed as the population counterpart of . We ignore the dependency of on for notation simplicity. To proceed, we need one additional assumption.

Assumption 9

is a convex set.

Assumption 9 is imposed so that together with Assumptions 1, 2 and 6 (a), the following strong duality holds so that

This implies that there is no duality gap between and

asymptotically, which is essential for us to derive a finite-sample bound for the regret of given below.

Remark 4

The implications behind Theorem 3 are the same as those of Theorem 2. The benefit of considering mainly comes from the computational efficiency. However, assuming convex could be restrictive. Therefore it will be interesting to study the behavior of duality gap when is modeled by a non-convex but “asymptotically” convex set. This will allow the use of some deep neural network architectures such as Zhang et al. (2019) in practice. We leave it for future work.

6 Numerical Studies

6.1 Simulation

In this section, we use Monte Carlo (MC) experiments to systematically study the proposed method in terms of the convergence of our algorithm, the effect of pessimism in finding the optimal policy, and the robustness to the covariate shift. For simplicity, we only consider the contextual bandit problem.

For all numerical studies, we compare our method with two popular continuous-action policy optimization methods. The regression-based approach first estimates the reward function as by running a regression method, and then estimates the value of any given policy with the plug-in estimator , where the expectation is approximated via MC sampling of . Recall that is known in advance. Given such a policy value estimator, we implement the off-the-shelf optimization algorithm to estimate the optimal policy within a given policy class. The kernel-based approach (Chen et al., 2016; Kallus & Zhou, 2018) is similar to the regression approach but first estimates the policy value using the inverse probability weighting with kernel smoothing. Specifically, we estimate the value of any given policy by

where is a kernel function, is the bandwidth parameter, and is referred as to the generalized propensity score in this setting.

Next, we describe the data generating process in our simulation study. We consider the mean reward function , where the state-value has dimension , the action-value has dimension , the parameter matrix , and is a negative definite matrix. We randomly sample every entry of from . We construct , where every entry of is sampled from the standard normal. Our reward is generated following , where the independent noise . Therefore, the optimal policy for every , regardless of the state distribution.

The training dataset is generated as follows. The state is uniformly sampled from , which is the same as the reference distribution. Except for the case where we study the effect of covariate shift, values of learned policies in this section are evaluated over the same distribution as the training distribution. The action is sampled following a behavior policy such that , where . Therefore, a larger indicates that the behavior policy is more different from the optimal one and also implies that the action space is explored more in the training data.

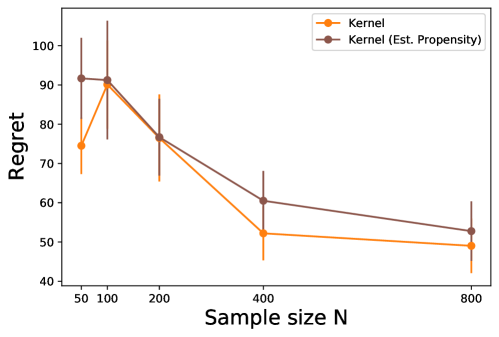

For all three methods, we search the optimal policy within the class of linear deterministic policies . For the kernel-based method, we assume the true value of the generalized propensity score is known, instead of plugging-in the estimated value. Although the latter is known to be asymptotically more efficient in the causal inference literature, we observe that its empirical performance is close or sometimes worse than the oracle version in the studied setting, given the challenge to estimating a multi-dimensional conditional density function (See Appendix D). We tune the bandwidth for the kernel-based method and use the best one for it. To implement the optimization problems in two baseline methods, we adopt the widely used L-BFGS-B optimization algorithm following Liu & Nocedal (1989). Regarding estimating the reward function , we use a neural network of three hidden layers with units for each layer and ReLU as the activation function. For STEEL, we use the Laplacian kernel in both the kernel ridge regression and the modeling of , where the bandwidth is picked based on the popular median heuristic, i.e., set as the median of . For the other tuning parameters, we set , , and .

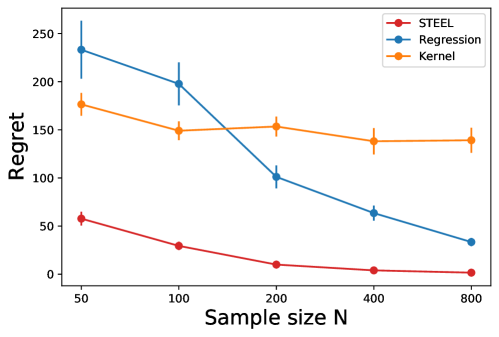

For each setting below, we run repetitions and report the average regret of each method as well as its standard error. Except for when we study the convergence of three methods in terms of the sample size, we fix data points for each repetition.

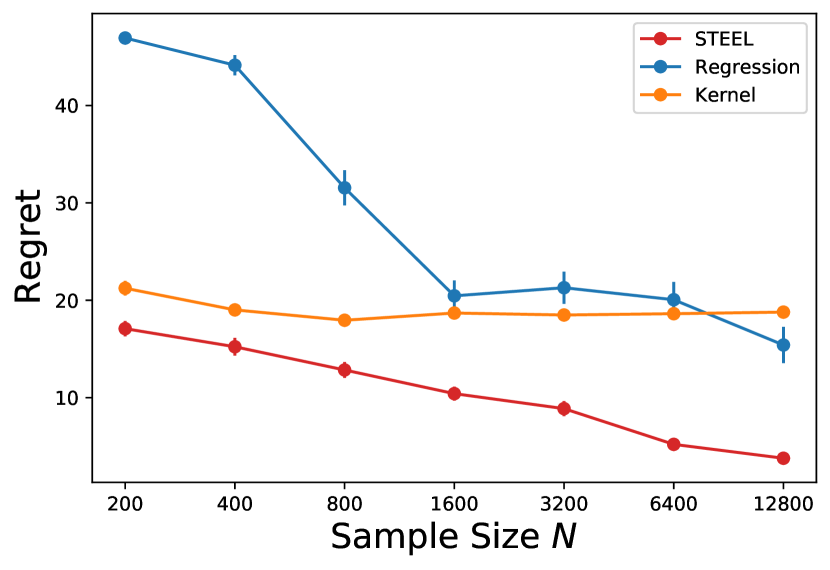

Convergence. We first study the convergence of all three methods, by increasing the training sample size . The results when are presented in Figure 1. Overall, we observe that our method yields a desired convergence with the regret decaying to zero very quickly. The regression-based method also improves as the sample size increases, despite that the finite-sample performance is worse compare with ours. The kernel-based method suffers from the curse of dimensionality of the action space and the regret does not decay very significantly. Results under a few other settings are reported in the appendix, with similar findings.

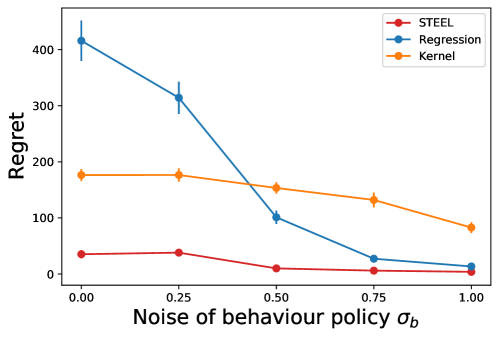

Effect of pessimism. Next, recall that controls the degree of exploration in the training data. It is known that a well-explored action space in the training dataset is beneficial for policy learning, in the sense that we can accurately estimate the values of most candidate policies. In contrast, when is small (i.e., the behavior policy is close to the optimal one), although the value estimation of the optimal policy may be accurate, that of a sub-optimal policy suffers from a large uncertainty and by chance the resulting estimator could be very large, which leads to returning a sub-optimal policy. Our method is designed with addressing such a large uncertainty in mind, by utilizing the pessimistic mechanism.

In Figure 2, we empirically study the effect of on different methods. The results are based on data points and different values of . It can be seen clearly that, our method is fairly robust, when the training data is either well explored or not. In contrast, the performance of the two baseline methods deteriorates significantly when is small.

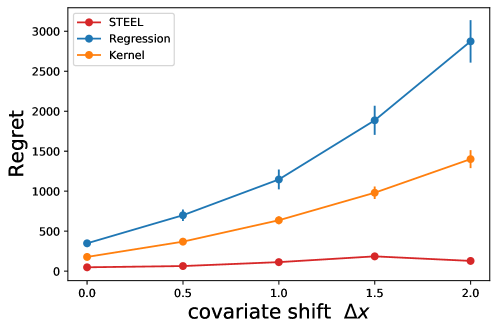

Robustness to covariate shift. Recall that the singularity may be caused by the covariate shift as well. Motivated by this, we also study the robustness of different methods to such a shift. Specifically, the policy will be tested when the covaraites are sampled uniformly from . A larger value of hence indicates a larger degree of covariate shift.

The results when and are presented in Figure 3. It can be seen clearly that our method shows a desired robustness. This is by design, as it accounts for such a shift explicitly. In contrast, the regret of the other two methods increase significantly when the testing state distribution of becomes more different from that in the training data.

6.2 Real Data

In this section, we apply our method to personalized pricing with a real dataset. The dataset is from an online auto loan lending company in the United States 111The dataset is available at https://business.columbia.edu/cprm upon request.. It was first studied by Phillips et al. (2015) and we follow similar setups as in subsequent studies (Ban & Keskin, 2021).

The dataset contains all auto loan records (208085 in total) in a major online auto loan lending company from July 2002 to November 2004. For each record, it contains some covariates (e.g., FIFO credit score, the term and amount of loan requested, etc.), the monthly payment offered by the company, and the decision of the applicant (accept the offer or not). We refer interested readers to Phillips et al. (2015) for more details of the dataset.

The monthly payment (together with the loan term) can be regarded as the offered price (action) and the binary decision of the applicant reflects the corresponding demand. Specifically, we follow Ban & Keskin (2021) and Bastani et al. (2022) to define the price as

which considers the net present value of future payments. Here, the prime rate is the interest rate that the company itself needs to pay. We filter the dataset to exclude the outlier records (defined as having a price higher than $10,000), and data points remain in the final dataset.

In our notations, the price is hence the action . Let the binary decision of the applicant be . The reward is then naturally computed as . We use the same set of features which are identified as significant in Ban & Keskin (2021) to construct our feature vector : it contains the FICO credit score, the loan amount approved, the prime rate, the competitor’s rate, and the loan term.

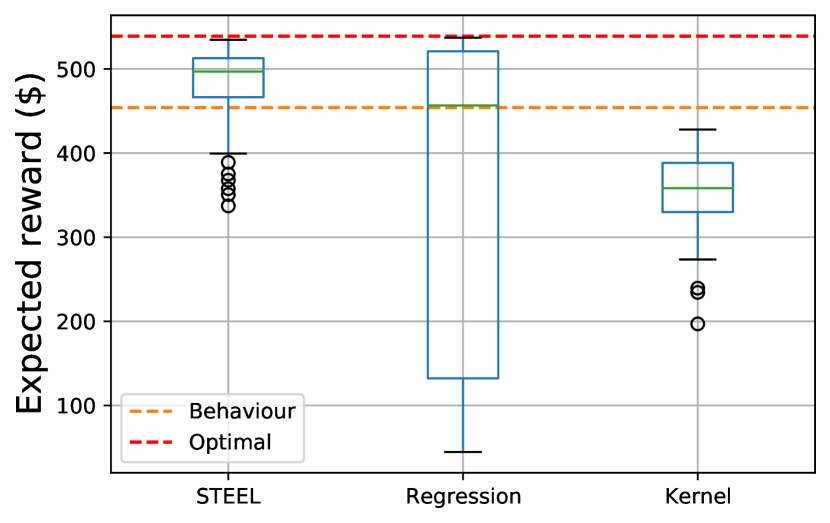

When running offline experiments for problems with discrete action spaces, to compared different learned policies, the standard procedure is to find those data points where the recorded actions are consistent with the recommendations from a policy that we would like to evaluate. However, with a continuous action space, such a procedure is typically impossible, as it is difficult for two continuous actions to have exactly the same value. Therefore, it is well acknowledged that, offline experiments without any model assumption is infeasible. We closely follow Bastani et al. (2022) to design a semi-real experiment, where we fit a linear demand function from the real dataset and use it to evaluate the policies learned by different methods. The linear regression uses the concatenation of (which describes the baseline effect) and (which describes the interaction effect) as the covariate vector. To evaluate the statistical performance of the three methods considered in Section 6.1, we repeat for random seeds, and for each random seed we sample data points for policy optimization.

The implementation and tuning details of the three methods are almost the same with Section 6.1. The main modification is that, for the reward function class used in our method and the regression-based method, we use the neural network to model the demand function (instead of the expected reward itself), which multiplies with the action (price) gives the expected reward. Such a modification utilizes the problem-specific structure. All covariates are normalized and we always add an intercept term. For tuning parameters, we set , , and .

In Figure 4(a), we increase from to and report the average regrets. We find that our method consistently outperforms the other two methods and its regret decays to zero. In Figure 4(b), we zoom into the case where , and report the values of the learned policies across the random seeds. We observe that, although the regression-based method can outperform the behaviour policy in about half of the random replications, it can perform very poor in the remaining replicates. In contrast, our method has an impressive performance and the robustness of our methods is consistent with our methodology design. The kernel-based method does not perform well in most settings. A deep dive shows that this is because this method over-estimates the values of some sub-optimal policies that assign many actions near the boundaries where we have few data points. The over-estimation is due to its poor extrapolation ability and the lack of the pessimism mechanism (i.e., it is not aware of the uncertainty).

Finally, we randomly pick a policy learned by our method (with the first random seed we used) and report its coefficient to provide some insights. Recall that we use a linear policy, mapping from the five features to the recommended price. The coefficients are overall aligned with the intuition: the learned personalized pricing policy offers a higher price when the FICO score is lower, the loan amount approved is higher, the prime rate (the interest rate that the company itself faces) is higher, the competitor’s rate is higher (implying a consensus on the high risk of this loan), and the term is longer.

| FICO score | Loan amount approved | Prime rate | Competitor’s rate | Term |

| -0.135 | 0.041 | 0.180 | 0.027 | 0.514 |

7 Conclusion

In this paper, we study batch RL in the presence of singularities and propose a new policy learning algorithm to tackle this issue. Our proposed method finds an optimal policy without requiring absolute continuity on the distribution of target policies with respect to the data distribution. Both theoretical guarantees and numerical evidence are presented to illustrate the superior performance of our proposed method, compared with existing works. In the current proposal, we leverage the MMD, together with distributionally robust optimization, to enable the extrapolation. Future research could involve studying the algorithm under the Wasserstein distance and exploring model-based solutions for addressing the singularity issue in batch RL.

References

- (1)

- Adjaho & Christensen (2022) Adjaho, C. & Christensen, T. (2022), ‘Externally valid treatment choice’, arXiv preprint arXiv:2205.05561 .

- Antos et al. (2008a) Antos, A., Szepesvári, C. & Munos, R. (2008a), Fitted q-iteration in continuous action-space mdps, in ‘Advances in neural information processing systems’, pp. 9–16.

-

Antos et al. (2008b)

Antos, A., Szepesvári, C. & Munos, R. (2008b), ‘Learning near-optimal policies with bellman-residual

minimization based fitted policy iteration and a single sample path’, Machine Learning 71(1), 89–129.

http://link.springer.com/10.1007/s10994-007-5038-2 - Antos et al. (2008c) Antos, A., Szepesvári, C. & Munos, R. (2008c), ‘Learning near-optimal policies with bellman-residual minimization based fitted policy iteration and a single sample path’, Machine Learning 71(1), 89–129.

- Athey & Wager (2021) Athey, S. & Wager, S. (2021), ‘Policy learning with observational data’, Econometrica 89(1), 133–161.

- Bai et al. (2022) Bai, C., Wang, L., Yang, Z., Deng, Z., Garg, A., Liu, P. & Wang, Z. (2022), ‘Pessimistic bootstrapping for uncertainty-driven offline reinforcement learning’, arXiv preprint arXiv:2202.11566 .

- Ban & Keskin (2021) Ban, G.-Y. & Keskin, N. B. (2021), ‘Personalized dynamic pricing with machine learning: High-dimensional features and heterogeneous elasticity’, Management Science 67(9), 5549–5568.

- Bastani et al. (2022) Bastani, H., Simchi-Levi, D. & Zhu, R. (2022), ‘Meta dynamic pricing: Transfer learning across experiments’, Management Science 68(3), 1865–1881.

- Berbee (1979) Berbee, H. C. (1979), ‘Random walks with stationary increments and renewal theory’, MC Tracts .

- Bhattacharya & Dupas (2012) Bhattacharya, D. & Dupas, P. (2012), ‘Inferring welfare maximizing treatment assignment under budget constraints’, Journal of Econometrics 167(1), 168–196.

- Bradley (2005) Bradley, R. C. (2005), ‘Basic properties of strong mixing conditions. a survey and some open questions’, Probability Surveys 2, 107–144.

- Caponnetto & De Vito (2007) Caponnetto, A. & De Vito, E. (2007), ‘Optimal rates for the regularized least-squares algorithm’, Foundations of Computational Mathematics 7(3), 331–368.

- Chen et al. (2016) Chen, G., Zeng, D. & Kosorok, M. R. (2016), ‘Personalized dose finding using outcome weighted learning’, Journal of the American Statistical Association 111(516), 1509–1521.

- Chen & Qi (2022) Chen, X. & Qi, Z. (2022), ‘On well-posedness and minimax optimal rates of nonparametric q-function estimation in off-policy evaluation’, arXiv preprint arXiv:2201.06169 .

- Chernozhukov et al. (2019) Chernozhukov, V., Demirer, M., Lewis, G. & Syrgkanis, V. (2019), ‘Semi-parametric efficient policy learning with continuous actions’, Advances in Neural Information Processing Systems 32.

- Dedecker & Louhichi (2002) Dedecker, J. & Louhichi, S. (2002), Maximal inequalities and empirical central limit theorems, in ‘Empirical process techniques for dependent data’, Springer, pp. 137–159.

- Ernst et al. (2005) Ernst, D., Geurts, P. & Wehenkel, L. (2005), ‘Tree-based batch mode reinforcement learning’, Journal of Machine Learning Research 6, 503–556.

-

Fu et al. (2022)

Fu, Z., Qi, Z., Wang, Z., Yang, Z., Xu, Y. & Kosorok, M. R.

(2022), ‘Offline reinforcement learning with

instrumental variables in confounded markov decision processes’.

Working Paper, Northwestern University, Evanston, IL.

https://arxiv.org/abs/2209.08666 - Fujimoto et al. (2019) Fujimoto, S., Meger, D. & Precup, D. (2019), Off-policy deep reinforcement learning without exploration, in ‘International conference on machine learning’, PMLR, pp. 2052–2062.

- Gretton et al. (2012) Gretton, A., Borgwardt, K. M., Rasch, M. J., Schölkopf, B. & Smola, A. (2012), ‘A kernel two-sample test’, The Journal of Machine Learning Research 13(1), 723–773.

- Jiang & Huang (2020) Jiang, N. & Huang, J. (2020), ‘Minimax value interval for off-policy evaluation and policy optimization’, Advances in Neural Information Processing Systems 33, 2747–2758.

- Jin et al. (2021) Jin, Y., Yang, Z. & Wang, Z. (2021), Is pessimism provably efficient for offline rl?, in ‘International Conference on Machine Learning’, PMLR, pp. 5084–5096.

- Kallus & Uehara (2020) Kallus, N. & Uehara, M. (2020), ‘Doubly robust off-policy value and gradient estimation for deterministic policies’, Advances in Neural Information Processing Systems 33, 10420–10430.

- Kallus & Zhou (2018) Kallus, N. & Zhou, A. (2018), Policy evaluation and optimization with continuous treatments, in ‘International conference on artificial intelligence and statistics’, PMLR, pp. 1243–1251.

- Kitagawa & Tetenov (2018) Kitagawa, T. & Tetenov, A. (2018), ‘Who should be treated? empirical welfare maximization methods for treatment choice’, Econometrica 86(2), 591–616.

- Kitagawa et al. (2022) Kitagawa, T., Wang, W. & Xu, M. (2022), ‘Policy choice in time series by empirical welfare maximization’, arXiv preprint arXiv:2205.03970 .

- Kosorok & Laber (2019) Kosorok, M. R. & Laber, E. B. (2019), ‘Precision medicine’, Annual review of statistics and its application 6, 263–286.

- Kumar et al. (2019) Kumar, A., Fu, J., Soh, M., Tucker, G. & Levine, S. (2019), Stabilizing off-policy q-learning via bootstrapping error reduction, in ‘Advances in Neural Information Processing Systems’, pp. 11784–11794.

- Kumar et al. (2020) Kumar, A., Zhou, A., Tucker, G. & Levine, S. (2020), ‘Conservative q-learning for offline reinforcement learning’, arXiv preprint arXiv:2006.04779 .

- Levine et al. (2020) Levine, S., Kumar, A., Tucker, G. & Fu, J. (2020), ‘Offline reinforcement learning: Tutorial, review, and perspectives on open problems’, arXiv preprint arXiv:2005.01643 .

- Liao et al. (2022) Liao, P., Qi, Z., Wan, R., Klasnja, P. & Murphy, S. A. (2022), ‘Batch policy learning in average reward markov decision processes’, The Annals of Statistics 50(6), 3364–3387.

- Lillicrap et al. (2015) Lillicrap, T. P., Hunt, J. J., Pritzel, A., Heess, N., Erez, T., Tassa, Y., Silver, D. & Wierstra, D. (2015), ‘Continuous control with deep reinforcement learning’, arXiv preprint arXiv:1509.02971 .

- Liu & Nocedal (1989) Liu, D. C. & Nocedal, J. (1989), ‘On the limited memory bfgs method for large scale optimization’, Mathematical programming 45(1-3), 503–528.

- Liu et al. (2020) Liu, Y., Swaminathan, A., Agarwal, A. & Brunskill, E. (2020), ‘Provably good batch off-policy reinforcement learning without great exploration’, Advances in neural information processing systems 33, 1264–1274.

- Luenberger (1997) Luenberger, D. G. (1997), Optimization by vector space methods, John Wiley & Sons.

- Manski (2004) Manski, C. F. (2004), ‘Statistical treatment rules for heterogeneous populations’, Econometrica 72(4), 1221–1246.

- Mbakop & Tabord-Meehan (2021) Mbakop, E. & Tabord-Meehan, M. (2021), ‘Model selection for treatment choice: Penalized welfare maximization’, Econometrica 89(2), 825–848.

- Mo et al. (2021) Mo, W., Qi, Z. & Liu, Y. (2021), ‘Learning optimal distributionally robust individualized treatment rules’, Journal of the American Statistical Association 116(534), 659–674.

- Munos (2003) Munos, R. (2003), Error bounds for approximate policy iteration, in ‘ICML’, Vol. 3, Citeseer, pp. 560–567.

- Munos & Szepesvári (2008) Munos, R. & Szepesvári, C. (2008), ‘Finite-time bounds for fitted value iteration’, Journal of Machine Learning Research 9(May), 815–857.

- Park & Muandet (2022) Park, J. & Muandet, K. (2022), ‘Towards empirical process theory for vector-valued functions: Metric entropy of smooth function classes’, arXiv preprint arXiv:2202.04415 .

- Phillips et al. (2015) Phillips, R., Şimşek, A. S. & Van Ryzin, G. (2015), ‘The effectiveness of field price discretion: Empirical evidence from auto lending’, Management Science 61(8), 1741–1759.

- Pinto & Gupta (2016) Pinto, L. & Gupta, A. (2016), Supersizing self-supervision: Learning to grasp from 50k tries and 700 robot hours, in ‘2016 IEEE international conference on robotics and automation (ICRA)’, IEEE, pp. 3406–3413.

- Puterman (1994) Puterman, M. L. (1994), Markov Decision Processes: Discrete Stochastic Dynamic Programming, John Wiley & Sons, Inc.

- Qi et al. (2022) Qi, Z., Pang, J.-S. & Liu, Y. (2022), ‘On robustness of individualized decision rules’, Journal of the American Statistical Association pp. 1–15.

- Qian & Murphy (2011) Qian, M. & Murphy, S. A. (2011), ‘Performance guarantees for individualized treatment rules’, Annals of statistics 39(2), 1180.

- Rahimian & Mehrotra (2019) Rahimian, H. & Mehrotra, S. (2019), ‘Distributionally robust optimization: A review’, arXiv preprint arXiv:1908.05659 .

- Rashidinejad et al. (2021) Rashidinejad, P., Zhu, B., Ma, C., Jiao, J. & Russell, S. (2021), ‘Bridging offline reinforcement learning and imitation learning: A tale of pessimism’, Advances in Neural Information Processing Systems 34, 11702–11716.

- Rivasplata et al. (2018) Rivasplata, O., Parrado-Hernández, E., Shawe-Taylor, J. S., Sun, S. & Szepesvári, C. (2018), ‘Pac-bayes bounds for stable algorithms with instance-dependent priors’, Advances in Neural Information Processing Systems 31.

- Schmidt-Hieber (2020) Schmidt-Hieber, J. (2020), ‘Nonparametric regression using deep neural networks with relu activation function’, The Annals of Statistics 48(4), 1875–1897.

- Shi et al. (2021) Shi, C., Wan, R., Chernozhukov, V. & Song, R. (2021), ‘Deeply-debiased off-policy interval estimation’, arXiv preprint arXiv:2105.04646 .

- Shi et al. (2020) Shi, C., Zhang, S., Lu, W. & Song, R. (2020), ‘Statistical inference of the value function for reinforcement learning in infinite horizon settings’, arXiv preprint arXiv:2001.04515 .

- Si et al. (2023) Si, N., Zhang, F., Zhou, Z. & Blanchet, J. (2023), ‘Distributionally robust batch contextual bandits’, Management Science .

- Silver et al. (2014) Silver, D., Lever, G., Heess, N., Degris, T., Wierstra, D. & Riedmiller, M. (2014), Deterministic policy gradient algorithms, in ‘International conference on machine learning’, PMLR, pp. 387–395.

- Smale & Zhou (2005) Smale, S. & Zhou, D.-X. (2005), ‘Shannon sampling ii: Connections to learning theory’, Applied and Computational Harmonic Analysis 19(3), 285–302.

- Smale & Zhou (2007) Smale, S. & Zhou, D.-X. (2007), ‘Learning theory estimates via integral operators and their approximations’, Constructive approximation 26(2), 153–172.

- Steinwart & Scovel (2012) Steinwart, I. & Scovel, C. (2012), ‘Mercer?s theorem on general domains: On the interaction between measures, kernels, and rkhss’, Constructive Approximation 35(3), 363–417.

- Sutton et al. (1998) Sutton, R. S., Barto, A. G. et al. (1998), Introduction to reinforcement learning, Vol. 135, MIT press Cambridge.

- Thomas et al. (2017) Thomas, P. S., Theocharous, G., Ghavamzadeh, M., Durugkar, I. & Brunskill, E. (2017), Predictive off-policy policy evaluation for nonstationary decision problems, with applications to digital marketing, in ‘Twenty-Ninth IAAI Conference’.

- Van Der Vaart & Wellner (1996) Van Der Vaart, A. W. & Wellner, J. A. (1996), Weak convergence, in ‘Weak convergence and empirical processes’, Springer, pp. 16–28.

- Van Der Vaart & Wellner (2011) Van Der Vaart, A. & Wellner, J. A. (2011), ‘A local maximal inequality under uniform entropy’, Electronic Journal of Statistics 5(2011), 192.

- Wang et al. (2021) Wang, R., Wu, Y., Salakhutdinov, R. & Kakade, S. (2021), Instabilities of offline rl with pre-trained neural representation, in ‘International Conference on Machine Learning’, PMLR, pp. 10948–10960.

- Watkins & Dayan (1992) Watkins, C. J. & Dayan, P. (1992), ‘Q-learning’, Machine learning 8(3), 279–292.

- Xie et al. (2021) Xie, T., Cheng, C.-A., Jiang, N., Mineiro, P. & Agarwal, A. (2021), ‘Bellman-consistent pessimism for offline reinforcement learning’, Advances in neural information processing systems 34, 6683–6694.

- Zanette et al. (2021) Zanette, A., Wainwright, M. J. & Brunskill, E. (2021), ‘Provable benefits of actor-critic methods for offline reinforcement learning’, Advances in neural information processing systems 34, 13626–13640.

- Zhan et al. (2022) Zhan, W., Huang, B., Huang, A., Jiang, N. & Lee, J. (2022), Offline reinforcement learning with realizability and single-policy concentrability, in ‘Conference on Learning Theory’, PMLR, pp. 2730–2775.

- Zhang et al. (2019) Zhang, H., Shao, J. & Salakhutdinov, R. (2019), Deep neural networks with multi-branch architectures are intrinsically less non-convex, in ‘The 22nd International Conference on Artificial Intelligence and Statistics’, PMLR, pp. 1099–1109.

- Zhao et al. (2012) Zhao, Y., Zeng, D., Rush, A. J. & Kosorok, M. R. (2012), ‘Estimating individualized treatment rules using outcome weighted learning’, Journal of the American Statistical Association 107(499), 1106–1118.

Appendix A Proof of Regret

Proof of Theorem 2: By Theorem 1, with probability at least , the regret can be decomposed as

where the first inequality is based on Theorem 1 and the second one relies on our policy optimization algorithm (14). The last line of the above inequalities transforms the regret of into the estimation error of OPE for using . Lastly, by leveraging results in Lemma 2, as long as , we obtain that

where we use results in Lemmas 4-5 for the last inequality. When , by slightly modifying the proof, Theorem 1 holds with . Then we have the last result of Theorem 2. This concludes our proof.

Proof of Theorem 3: Denote the solution of

by , where . As shown in Theorem 1, with probability at least , for every ,

Then with probability at least , we have the following regret decomposition for any constant .

where the first inequality is due to , the second inequality holds as we minimize over and by Assumption 7, , the third inequality is based on the optimization property of (16), and the last one holds because of the restriction on the dual variable . By results in Lemmas 4-5, we can further obtain that

with probability at least . Consider the following constraint optimization problem.

where

It can be verified that the objective function is convex functional with respect to and the constraint set is constructed by convex mapping of under the Assumption 9. Moreover, when by Assumption 7, the inequality is strictly satisfied due to the Bellman equation, which implies that is the interior point of . Lastly, by Assumption 6 (a), the objective function is always bounded below. Then by Theorem 8.6.1 of Luenberger (1997), strong duality holds. Therefore

In the following, we show that

for some . For every , let be the optimal dual variables, i.e.,

| (34) |

By the strong duality and complementary slackness, one must have that

where is the optimal primal solution. Since the optimal value for the primal problem is always finite duo to Assumption 6 (a), we claim that are finite. We can show this statement by contradiction. Without loss of generality, if and is finite, one must have

so that is an optimal solution of

with the optimal value . This violates the complementary slackness. Therefore, there always exists an optimal dual solution such that some constant of the above dual problem. This further indicates that

By leveraging the above equality, we obtain that

where the last inequality is given by Lemma 2 and the definition of . For the last part of the proof, see a similar argument in the proof of Theorem 2. This concludes our proof.

Appendix B Supporting Lemmas

Proof of Lemma 1: Without loss of generality, assume is the probability density function of the discounted visitation probability measure over . Then by the backward Bellman equation, we can show that for any ,

Multiplying and integrating out over on both sides gives that

| (35) |

By using the Bellman equation for , i.e., for every ,

| (36) |

we can conclude our proof by showing that Equation (35) can be simplified to that

Proof of Lemma 2: By Lebesgue’s decomposition theorem, we can show that

where the last equality uses the change of measure. By the conditions that and is symmetric, we can derive an upper bound for the first term in the above inequality, i.e.,

Furthermore, under the conditions in Lemma 6 and , we have that

where the first equality is based on Lemma 1. Furthermore, by Cauchy–Schwarz inequality, we can show that

| (37) | ||||

| (38) |

where the equality in the last line holds if for or = 0. Therefore we can conclude that

By a similar argument, we can show that

and note that

Summarizing two upper bounds together gives that for every

If additionally , then we can obtain that

Proof. We apply Lemma 7 to show the statement. Define

By Assumption 6, we can show that

Then by applying Lemma 7, we can show that with probability at least ,

Proof of Lemma 3: Recall that we define the following class of vector-valued functions as

where . Next, we show that for any , , i.e., the envelop function of is uniformly bounded above. Since for any , by Assumption 6 (a), we can show that for any ,

where the second inequality is based on Assumption 2 and the following argument.

where the second inequality is based on the condition that and . In the following, we calculate the uniform entropy of with respect to any empirical probability measure, i.e., . Then, for any , it can be seen that for any , and ,

where the first inequality is based on Assumption 5, the second one is given by Lipschitz condition stated in Assumption 6 (a), and the last one is due to the linearity of the operator . For the second term in the above inequality, we can show that

where the first inequality is based on Assumption 5. The second and third lines hold because of Assumption 7 and the spectral decomposition of . The last inequality holds because of the Lipschitz condition in Assumption 8. The third inequality is based on the following argument.

where the inequality holds as is non-decreasing towards and . Now we focus on the last term . Similar as before, we can show that

Therefore, we can show that

Proof. Recall that we define an operator such that

| (39) |

for every . It can be seen that

where is the identity operator. In order to bound , we first decompose it as

We then derive an upper bound for Term (II), which is the “bias” term for estimating . We follow the proof of Theorem 4 in Smale & Zhou (2005) and extend their pointwise results to the uniform covergence over and . Specifically, under Assumption 7, for every and , there exists such that . Recall that

and thus

By the definition of , we can show that for every and ,

Then for , we have

which implies that for any and ,

which further gives that

Next, we derive an upper bound for the “variance” of , i.e., Term (I). Following the result of Smale & Zhou (2007), we define the sampling operator with batch data over as

for any function defined over . The adjoint of the sampling operator is defined as such that

Then we have

where

and is an identity matrix with the dimension . It can be seen that for any and ,

where the last equation is based on the definition of the sampling operator, its adjoint and the closed form of . Now we can show that

Note that for any and , by Assumption 4,

To bound the above empirical process for vector-valued functions, we leverage the result developed in Lemma 8. By Lemma 8, we can show that with probability at least ,

Summarizing Terms (I) and (II) gives that

By choosing , we optimize the right-hand-side of the above inequality and obtain that

Appendix C Additional Definitions and Supporting Lemmas

We define the -covering number below, which is used in the main text.

Definition C.1 (-covering number)

An -cover of a set with respect to some semi-metric is a set of finite elements such that for every , there exists such that . An -covering number of a set denoted by is the infimum of the cardinality of -cover of .

The following lemma provides a sufficient condition for the existence of mean embeddings for both and . For notation simplicity, let and denote .

Lemma 6

If the kernel is measurable with respect to both and and , then there exist mean embeddings such that for any