Lp Quasi-norm Minimization: Algorithm and Applications

Abstract

Sparsity finds applications in areas as diverse as statistics, machine learning, and signal processing. Computations over sparse structures are less complex compared to their dense counterparts, and their storage consumes less space. This paper proposes a heuristic method for retrieving sparse approximate solutions of optimization problems via minimizing the quasi-norm, where . An iterative two-block ADMM algorithm for minimizing the quasi-norm subject to convex constraints is proposed. For , , the proposed algorithm requires solving for the roots of a scalar degree polynomial as opposed to applying a soft thresholding operator in the case of . The merit of that algorithm relies on its ability to solve the quasi-norm minimization subject to any convex set of constraints. However, it suffers from low speed, due to a convex projection step in each iteration, and the lack of mathematical convergence guarantee. We then aim to vanquish these shortcomings by relaxing the assumption on the constraints set to be the set formed due to convex and differentiable, with Lipschitz continuous gradient, functions, i.e. specifically, polytope sets. Using a proximal gradient step, we mitigate the convex projection step and hence enhance the algorithm speed while proving its convergence. We then present various applications where the proposed algorithm excels, namely, matrix rank minimization, sparse signal reconstruction from noisy measurements, sparse binary classification, and system identification. The results demonstrate the significant gains obtained by the proposed algorithm compared to those via minimization.

Index Terms:

Sparsity, compressed sensing, rank minimization, ADMM, Proximal gradient method.I Introduction

I-A Motivation

In numerical analysis and scientific computing, a sparse matrix/array is the one with many of its elements being zeros. The number of zeros divided by the total number of elements is called sparsity. Sparse data is often easier to store and process. Hence, techniques for deriving sparse solutions and exploiting them have attracted the attention of many researchers in various engineering fields like machine learning, signal processing, and control theory.

The taxonomy of sparsity can be studied through the rank minimization problem (RMP). It has been lately considered in many engineering applications including control design and system identification. This is because the notions of complexity and system order can be closely related to the matrix rank. The RMP can be formulated as follows:

| (1) |

where and is a convex set. The problem (1) in its generality is NP-hard [1]. Therefore, polynomial time algorithms for solving large-scale problems of the form in (1) are not currently known. Hence, currently adopted methods for solving such problems are approximate and structured heuristics.

A special case of RMP is the sparse vector recovery (SVR) problem involving pseudo-norm minimization given by:

| (2) |

where , is a closed convex set and counts the number of the non-zero elements of its argument. From the definition of the rank being the number of non-zero singular values of a matrix, it can be easily realized that (1) is a generalized form of (2).

Various works – which will be discussed in the next section in more detail – have explored efficient solution techniques for the problems in (1) and (2) independently using Schatten-p and quasi-norm relaxations respectively. However, all of these methods either assume a specific structure for the convex set in (1) or only work for the special case in (2); hence, they lack generality. Using the fact that the Schatten-p quasi-norm is the quasi-norm of the matrix singular values, we aim to design an efficient heuristic method based on Schatten-p relaxation for solving both problems in a unified manner. To achieve this, we first propose an algorithm for solving quasi-norm relaxation of the SVR problem in (2), and next, exploiting the fact that (2) is a special case of (1), we then employ the derived quasi-norm minimization algorithm as a building block for the desired generalized algorithm for the rank minimization problem.

I-B Related work

I-B1 Sparse Vector Recovery

As discussed, a sparse solution is defined as the one having the minimum number of non-zero components while satisfying certain constraints such as a system of linear equations [2]. Since many signals are either sparse or compressible, SVR problem has found applications in object recognition, classification and compressed sensing problems, see, e.g.,[3, 4, 5]. In [6], the authors discussed the concept of the sparse representation of signals and systems, where they reviewed the theoretical and empirical results on sparse optimization, and discussed sufficient conditions needed for uniqueness, stability and computational practicability. Different applications for the SVR problem are explored in [6] and it is argued that in certain denoising and compression tasks, the methods for sparse optimization provide state of the art solutions.

The problem of constructing a sparse solution to undetermined linear systems has received great attention. In [7], the authors surveyed the existing algorithms for sparse approximation, namely; greedy methods [8, 9], the methods based on convex relaxation [4, 5, 10, 11], those involving non-convex optimization [12, 13], Bayesian framework [14, 15], and requiring brute force [16]. They also discussed the computational requirements of each algorithm and their relation to each other.

Sparse optimization problems of the form have been extensively studied in the literature, where is a sparsity inducing function, e.g., -norm, is a loss function on measurement errors, e.g., , and is a trade-off parameter between data-fidelity and sparsity. In [2], the authors considered sparse recovery problem from a set of corrupted measurements. For , they established a sufficient condition for the exact sparse signal recovery, i.e., restricted isometry property (RIP). Motivated by the fact that as , it is natural to consider the above problem with set to quasi-norm for . Hence, the authors in [17] presented theoretical results demonstrating the ability of the quasi-norm to recover sparse signals from noisy measurements. Under more relaxed RIP conditions, they showed that the quasi-norm provides better theoretical guarantees in terms of stability and robustness than the minimization. In [12], the problem of SVR via the quasi-norm minimization from small number of linear measurements of the target signal was considered. This setting is important in applications where data acquisition is difficult or expensive. However, the proposed approach in [12] has limited applicability due to its long reconstruction time compared to the norm. In [18], the authors exploited Fourier-based algorithms for convex optimization to solve sparse signals reconstruction problem via the quasi-norm minimization. They showed that their approach combines the construction abilities of the non-convex methods with the speed of the convex ones. In [19] the authors proposed an approach, for sparse reconstruction, replacing the non-convex function with a quadratic convex one. In [20], an alternating direction method of multipliers (ADMM) based algorithm that enforces both sparsity and group sparsity using non-convex regularization is presented. An iterative half thresholding algorithm for fast solution of the regularization is proposed in [21]. The authors proved the existence of the resolvent of gradient of , calculated its analytic expression, and derived a thresholding representation of solutions for regularization. In [22], the convergence of the iterative half thresholding algorithm is studied, where it was shown that, under certain conditions, the half thresholding algorithm converges, to a local minimizer of the regularized problem, with a linear convergence rate. Conditions for the convergence of an ADMM algorithm that solves the problem of minimizing the sum of a smooth function with a bounded Hessian and a non-smooth function are derived in [23]. In [24], the convergence of ADMM for minimizing a non-convex and possibly non-smooth objective function subject to equality constraints is analyzed. The developed convergence guarantee covers a variety of non-convex objectives including piece-wise linear functions, quasi-norm and Schatten- quasi-norm (), while allowing non-convex constraints as well.

I-B2 Rank minimization

In [25], the authors aimed at determining the least order dynamic output feedback, using same formulation as in (1), which stabilizes a given linear time invariant system. They found that minimizing the trace instead of the rank results in a Semi-Definite Program (SDP) that can be solved efficiently. However, their solution was only applicable for symmetric and square matrices. In [26], a generalization of the latter approach was introduced which is based on replacing the rank in the objective function with the summation of the singular values of the matrix, i.e., the nuclear norm. They showed that this leads to the convex envelope of the non-convex rank objective and boils down to the original trace heuristic when the decision matrix is a symmetric positive semi-definite (PSD) matrix. Finally, effectiveness of the approach was shown using a frequency domain system identification problem. In [27], another heuristic based on the logarithm of the determinant was presented as a surrogate for the rank minimization over the subspace of PSD matrices, and the authors showed that this formulation can be solved using a sequence of trace minimization problems. The authors also extended their heuristic to handle matrices that are not necessarily PSD. In [28], the authors also studied the existing trace and log determinant heuristics for approximating (1). They discussed the applications of these heuristics for computing a low-rank approximation of 1) covariance matrices for a given dataset so that one can obtain a simple data model, easy to interpret, which is especially important in statistics and signal processing; 2) Hankel matrices arising in system identification of a time invariant, low-order system for given output realizations; and 3) matrices appearing in various other problems including and reduced-order -synthesis with constant scaling and problems with inertia constraints.

Although the nuclear norm is the tightest convex substitute for the non-convex rank function, one of its major shortcomings is that it treats all the singular values equally in order to be able to preserve the convexity. Therefore, this restricts its performance in applications where the singular values need to be treated differently, e.g., particularly in image denoising. In [29], the authors proposed an iterative re-weighted nuclear norm heuristic to avoid this problem and analyzed its convergence. They also proposed a gradient-based algorithm and applied it to a low-order system identification problem. Experimental results showed that the re-weighted nuclear norm leads to a lower order model than the nuclear norm itself. In [30], the solution of weighted nuclear norm (WNN) problem was analyzed under different circumstances where the weights could be in a non-ascending, arbitrary or a non-descending order. The authors applied their proposed WNN algorithm to an image denoising problem by exploiting the image non-local self-similarity. Numerical results showed that the proposed WNN algorithm outperforms many of the state of the art denoising methods in terms of both quantitative measures and visual quality.

Another method, inspired by the success of the quasi-norm for sparse signal reconstruction, is to enforce low-rank structure by using the Schatten-p quasi-norm, which is defined as the quasi-norm of the singular values. In [31], the authors considered the matrix completion problem, which deals with constructing a low-rank matrix, given a subset of its entries. Instead of minimizing the nuclear norm, the authors proposed a Schatten-p quasi-norm formulation, for which they came up with an algorithm and studied its convergence properties. In each iteration, the sub-problem that needs to be solved has a closed-form solution, which makes it fast and suitable for large-scale problems. To improve the robustness of the solutions to matrix completion problem, in [32] Schatten- quasi-norm for low-rank recovery was combined with quasi-norm of the prediction errors on the observed entries. The authors proposed an algorithm based on the ADMM, which performed better in their numerical experiments than other completion methods like fixed-point continuation and accelerated proximal gradient singular-value thresholding. In [33], the authors extended the theoretical recovery results previously developped for the nuclear norm to Schatten- quasi-norm using a weaker version of the RIP assumption; they showed that the minimum rank solution can be recovered by solving the Schatten- quasi-norm minimization problem. In [34], the authors developed an iterative re-weighted least squares algorithm to solve an unconstrained minimization problem. The algorithm, and analysis, are extended to include the low rank recovery problem. Another non-convex approaches for matrix optimization problems involving sparsity are developed, by means of a generalized shrinkage operation, in [35]. These approaches are applied to the decomposition of video into low rank and sparse components, which is able to separate moving objects from the stationary background better than in the convex case.

I-C Contributions

Despite the good performance of the various algorithms discussed in I-B1 and I-B2 for solving different relaxations of (2) and (1), they are all based on a specific structure of the considered convex constraint set; therefore, they are problem specific and lack generality. In this work, we present a general-purpose method based on projections onto the constraint set, for which we assume only closed convexity as the specific structure. [36] and [37] examine the characteristics of the projection on the constraint set. In the latter, the projection technique of every given point on balls is assumed to be known a priori, whereas in the former, the issue is solved while omitting an important coupling condition for the polynomial equations.

First, based on our previous work in [38], we propose an ADMM algorithm (pQN-ADMM) to solve the quasi-norm relaxation of (2). At each iteration, the bottleneck operation is to compute Euclidean projections on to some particular convex and non-convex sets. The proposed algorithm possesses two important properties: 1) Its computational complexity is similar to minimization algorithms except for the additional effort of solving for the roots of a polynomial; 2) No specific structure for the convex set is required. Numerical results, using a SVR and binary classification examples, are presented to show the competitive performance of our algorithm against the minimization approach. We then extend the proposed algorithm to solve the relaxation of (1) based on the Schatten- quasi-norm – here, we exploit the fact that minimizing the -norm of the vector of singular values is equivalent to minimizing the Schatten- quasi-norm. We consider two different numerical examples: 1) We formulate time domain system identification problem for minimum order system detection and solve it using the pQN-ADMM approach and compare our recovery results against the nuclear norm minimization approach of [26]; 2) We consider a matrix completion problem, where the goal is to recover an unknown low-rank matrix based on a small fraction of observed entries. Numerical results in both examples show that our method is competitive against some of the state-of-the-art algorithms in terms of both the detected system order (for the system identification problem) and the rank of the matrix recovered (for the matrix completion problem).

Finally, since the derived algorithm depends on a computationally expensive convex projection step in every iteration, we aim to develop a faster algorithm with a mathematical convergence guarantee. Considering only a subset of problems where the constraint set is a polytope, we utilize concepts from the proximal gradient (PG) method to derive a fast algorithm and prove that it converges with a rate , where is the iteration budget given to the algorithm.

II Notations and basic definitions

Unless otherwise specified, we denote vectors with lowercase boldface letters, i.e., , with -th entry as , while matrices are in uppercase, i.e. , with -th entry as . For an integer , . represents a vector of all entries equal to 1, while is an indicator function to the set , i.e., it evaluates to zero if its argument belongs to the set and is otherwise.

For a vector , the general norm is defined as

| (3) |

For convenience, we let be the well known euclidean norm, i.e., . When , the expression in (3) is termed as the quasi-norm satisfying the same axioms of the norm except the triangular inequality making it a non-convex function.

Definition 1.

Let be a linear operator between two normed spaces equipped with norm, . The induced -norm is defined as,

| (4) |

A special case of (4) is when , known as the spectral radius, which can be shown to be the square root of the maximum eigen value of , where is the complex conjugate of the transpose of , i.e., . In the rest of the analysis, we will drop the subscript 2 in the spectral norm notation and only refer to it with .

For a matrix , the entry-wise norm is defined as,

| (5) |

A special case of (5) is when , known as the Frobenius norm, which were refer to by .

Definition 2.

Let and be two separable Hilbert spaces and be a linear compact operator from to , the Schatten-p norm of is then defined as,

| (6) |

where is the -th singular value of the matrix .

When , equation (6) yields to the nuclear norm which is the convex envelope of the rank function. Throughout the paper, we consider a non-convex relaxation for the rank function, specifically , and compare its performance with the nuclear norm case in the results section.

We define as the ceiling operator, as a vector formed by stacking the columns of the matrix and as an operator that outputs a Hankel matrix constructed from the applied vector arguments.

III Sparse Vector Recovery Algorithm

III-A Problem Formulation

This section develops a method for approximating the solution of (2) using the following relaxation,

| (7) |

where and is a closed convex set. Problem (7) is convex for ; hence, can be solved to optimality efficiently. However, the problem becomes non-convex when . An epigraph equivalent formulation of (7) is obtained by introducing the variable :

| (8) | ||||||

Let denote the epigraph of the scalar function , i.e., , which is a non-convex set for . Then, (8) can be cast as

| (9) |

ADMM exploits the structure of the problem to split the optimization over the variables via iteratively solving fairly simple subproblems. In particular, we introduce auxiliary variables and and obtain an ADMM equivalent formulation of (9) given by:

| (10) | ||||||

where is the -sublevel set of , i.e., . The dual variables associated with the constraints and are and , respectively. Hence, the Lagrangian function corresponding to (10) augmented with a quadratic penalty on the violation of the equality constraints with penalty parameter , is given by:

| (11) |

Considering the two block variables and , ADMM [39] consists of the following iterations:

| (12) | |||||

| (13) | |||||

| (14) | |||||

| (15) |

According to the expression of the augmented Lagrangian function in (III-A), it follows from (12) that the variables and are updated via solving the following non-convex problem

| (16) |

Exploiting the separable structure of (16), one immediately concludes that (16) can be split into independent 2-dimensional problems that can be solved in parallel, i.e., for each ,

| (17) |

where denotes the Euclidean projection operator onto the set . Furthermore, (III-A) and (13) imply that and are independently updated as follows:

| (18) | |||||

| (19) |

Algorithm 1 summarizes the proposed ADMM algorithm. It is clear that , , and merit closed-form updates. However, updating requires solving non-convex problems. Our strategy for dealing with this issue is presented in the section that follows.

III-B Non-convex Projection

In this part, we present the method used to tackle the non-convex projection problem required to update and .

Among the advantages of the proposed algorithm is that it is amenable to decentralization. As it is clear from (17), and can be updated element-wise via performing a projection operation onto the non-convex set , one for each . The projection problems can be run independently in parallel. We now outline the proposed idea for solving one such projection, i.e., we suppress the dependence on the index of the entry of and . For , entails solving

| (20) |

If , then trivially . Thus, we focus on the case in which . The following proposition states the necessary optimality conditions for (20).

Proposition 1.

Let , and be an optimal solution of (20). Then, the following properties are satisfied

-

(a)

,

-

(b)

,

-

(c)

,

-

(d)

.

Proof.

We prove the statements by contradiction as follows:

-

(a)

Suppose that , then

(21) i.e., . Hence, . Moreover, the feasibility of implies that . Thus, is feasible and attains a lower objective value than that attained by . This contradicts the optimality of .

-

(b)

Assume that . Then,

(22) Furthermore, by the feasibility of , we have . Thus, is feasible and attains a lower objective value than that attained by . This contradicts the optimality of .

-

(c)

Suppose that , i.e.,

(23) We now consider two cases, and . First, let . Then, we have by and (23) that . Since , i.e., , therefore and hence, . Pick such that , i.e., . Then clearly, . Thus, we have

(24) where the last inequality follows the just proven identity that . Moreover, we have by . Thus, is feasible and attains a lower objective value than that attained by . This contradicts the optimality of . On the other hand, let . Then, we have by and (23) that . Since , i.e., , then , i.e., . Therefore, Pick such that , i.e., . Then, (24) also holds when . Note that by . Thus, is feasible and attains a lower objective value than that attained by . This contradicts the optimality of .

-

(d)

The feasibility of eliminates the possibility that . Now let and pick . Then, , where the first inequality follows from . Then, . Thus, we have

(25) Furthermore, the feasibility of follows trivially from the choice of . Thus, is feasible and attains a lower objective value than that attained by . This contradicts the optimality of .

This concludes the proof. ∎

We now make use of the fact that for (20), an optimal solution satisfies and hence, (20) reduces to solving

| (26) |

The first order necessary optimality condition for (26) implies the following:

| (27) |

By the symmetry of the function , without loss of generality, assume that and let for some . A change of variables plugged in (27) shows that finding an optimal solution for (20) reduces to finding a root of the following scalar degree polynomial:

| (28) |

Thus, to find , solve for a root of the polynomial in (28) such that minimizes . Algorithm 2 summarizes the method we use to solve problem (20). In case , we set . If the set is empty, we set and .

III-C Convex Projection

The convex projection for y-update in (18) can be formulated as the following convex optimization problem

| (29) |

where is the euclidean norm. Convex problems can be solved by a variety of contemporary methods including bundle methods [40], sub-gradient projection [41], interior point methods [42], and ellipsoid methods [43]. The efficiency of optimization techniques rely mainly on exploiting the structure of the constraint set. As mentioned in I-C, to be general, we aim to solve the problem in (7) with no assumptions on the set , other than it being closed and convex. That said, if possible, through exploiting the structure of , one should be able to reduce the computational complexity of solving (29).

Remark 1.

As per our knowledge, none of the existing literature considered the convergence of an ADMM algorithm for solving the general problem in (7). As discussed in I-B1, on one hand, the work in [23] studied the convergence of ADMM under mild assumptions. However, assuming has a particular form, these assumptions hold only if the function defining the the constraint set in (7) is Lipschitz differentiable. On the other hand, [44] studied the convergence of a non ADMM algorithm to solve (7) while assuming that the global optimal for each update step can be found efficiently.

IV Rank Minimization Algorithm

We consider the same problem as in (1) and propose a method for approximating its solution efficiently. The Schatten-p heuristic of (1) can be written as

| (30) |

where and is the th singular value of . When , problem (30) is a convex one which is eventually the nuclear norm heuristic. We consider a non-convex case where , which has the corresponding epi-graph form,

| (31) | ||||

| s.t. |

such that . Defining the epi-graph set for the function , where , the problem in (31) can be written as,

| (32) |

In order to structure the problem in a from that ADMM can exploit, we introduce the auxiliary variables and which makes the problem in (32) be,

| (33) | ||||

| s.t. |

such that , are the dual variables associated with and respectively. Similar to (III-A), the Lagrangian function associated with (33) augmented with a quadratic penalty for the equality constraint violation with a parameter , is

| (34) | ||||

where is the trace operator. Considering the 2-tuples and , the ADMM iterations is,

| (35) | |||

| (36) | |||

| (37) | |||

| (38) | |||

| (39) |

IV-A update

By completing the square and with some simple algebra, it can be shown that the problem in (35) is equivalent to

| (40) | ||||

| s.t. |

where and . For an ease of notations, we will drop the iteration index . Assume that and is the singular value decomposition (SVD) of and respectively. Where are diagonal matrices with the singular values associated and while and are the unitary matrices. By applying the same steps as in Theorem 3 of [45], we can write the first term of (40) after dropping as,

| (41) | ||||

where (a) is because with being an identity matrix of size , and exploiting the circular property of the trace while (b) holds is from the main result of [46]. In order to make achieve its derived lower bound, we set and .

Henceforth, the problem in (40) will be equivalent to,

| (42) | ||||

| s.t. |

where and are the vectors of singular values of the matrices and respectively. The optimal solution for (40) can be calculated by finding the optimal of (42) and then , where diag and diag is an operator that converts a vector to its corresponding diagonal matrix. Since the problem in (42) is separable, we drop the index and only consider solving

| (43) |

IV-B update

V Proximal Gradient Algorithm

The SVR algorithm deals with the relaxation of (2) without assuming any specific structure for , other than being closed and convex. Indeed, the algorithm only requires the Euclidean projections onto as in (29). However, this approach suffers from two pitfalls: 1) high computational complexity per iteration as a result of solving (29) in every iteration, and 2) the lack of convergence guarantees.

In this section, we consider a sub-class of problems with a specific structure for the convex set of the form , where for some given , and . Note that is a convex function with Lipschitz continuous gradient. i.e., is -smooth: for all and . Specifically, in order to solve

| (46) |

we aim to develop an efficient algorithm with some convergence guarantees for the following Lagrangian relaxation:

| (47) |

where is the dual multiplier that captures the trade-off between solution sparsity and fidelity.

A canonical problem for the regularized risk minimization has the following form:

| (48) |

where is an -smooth loss function and is a a regularizer term. When both and are convex, the proximal gradient (PG) algorithm [47] can compute a solution to (48) through iteratively taking PG steps, i.e., where , for some constant . When is convex, prox operation is well-defined; thus, the PG step can be computed.

Comparing both (47) and (48), the convexity assumption of in (48) is not satisfied for in (47). When the regularizer is a continuous nonconvex function, the proximal map may not exist, let alone it can be computed in closed form. On the other hand, for , using similar arguments for the non-convex projection step introduced in subsection III-B, we aim to derive an analytical solution that can be computed efficiently. Indeed, assuming is a positive rational number, the proposed method for computing the proximal map of involves finding the roots of a polynomial of order , where such that for some .

Since is -smooth, for all , we have

| (49) |

Given , replacing with the upper bound in (49) for , the prox-gradient operation naturally arises as follows:

| (50) | ||||

By completing the square, (50) yields to

| (51) |

Defining , (51) can be rewritten as

| (52) | ||||

which is clearly a separable structure in the entries of . Therefore, for each , we have

| (53) |

where such that for some positive rational .

Next, we consider a generic form of (53), i.e., given some , we would like to compute

| (54) |

The first-order optimality condition for (54) can be written as

| (55) |

Using similar arguments with those in section III-B for Proposition 1, we can conclude that the optimal solution attains the property that . Without loss of generality, exploiting the symmetry of the function , we only consider the case when ; hence, the optimal solution is the smallest positive root of the following polynomial:

| (56) |

As in (28), suppose for some . Using the change of variables , (56) reduces to finding the roots of a polynomial of degree :

| (57) |

To efficiently solve (46), we will use Algorithm 3, which is an implementation of nonconvex inexact accelerated proximal gradient (APG) descent method proposed in [48, Algorithm 2]. To summarize, [48, Algorithm 2] is designed to solve composite problems of the form in (48) assuming that is -smooth and is proper lower-semicontinuous such that is bounded from below and coercive, i.e., – note that there is no assumption regarding neither nor to be convex. The key points enhancing both practical behavior of and theoretical guarantees for [48, Algorithm 2] can be summarized as given below:

-

•

An extrapolation is generated as introduced in [49] for the APG algorithm (step 3).

-

•

Steps 4 through 9 allow non monotone update of the objective. is checked with respect to the maximum of the latest objective values. The gradient step is adjusted according to this (step 9). This permits to occasionally increase the objective and makes be less than the maximum of the objective value of the latest iterations.

-

•

Steps 11 and 12 are the solution of the PG step using the non-convex projection method.

In the next part, we show that algorithm 3 converges to a critical point and it exhibits a convergence rate of , where is the iteration budget that is given to the algorithm.

Definition 3.

Definition 4.

([50]) is a critical point of if .

By comparing (48) and (47), it can be realized that the functions and in definition 4 are equal to and respectively.

Theorem 1.

Proof.

It can easily be verified that our problem in (47) satisfies all required assumptions for Algorithm 3. Indeed,

-

1.

The function is a proper and lower semi-continuous function.

-

2.

The gradient of is -Lipschitz smooth, i.e., for all , with .

-

3.

is bounded from below, i.e., .

-

4.

.

-

5.

The introduced non-convex projection method is an exact solution for the proximal gradient step. This is because it is based on finding the roots of a polynomial of order in equation (57).

Therefore, the assumptions required for theorem 4.1 for critical point convergence and proposition 4.3 for the rate of convergence in [48] are satisfied which then completes the proof. ∎

Remark 2.

The global convergence of several exact iterative methods that solve (48) has been explored, under the framework of Kurdyka–Lojasiewicz (KL) theory, in various additional literature including [51, 50, 52, 53, 54]. Other work (see [55] and references therein) considered the linear convergence of non-exact algorithms with relaxations on the assumptions of KL theory, however, it is difficult to verify that the sequence generated by algorithm 3 satisfies the relaxed assumptions stated in [55].

VI Numerical Results for SVR Problem

In this section, we present two numerical examples for the p-quasi-norm ADMM (pQN-ADMM) from algorithm 1 and the non-convex projection from algorithm 2. For both examples, the pQN-ADMM algorithm result is compared with the objective function solution from MOSEK solver [56]. The two examples include; i) Sparse signal reconstruction from noisy measurements, where the pQN-ADMM algorithm is also compared with another quasi-norm minimization based algorithm, named -FL, described in [57]. ii) Binary classification using support vector machines (SVM).

VI-A Sparse Signal Reconstruction

Let and , randomly construct the sparse binary matrix, , with a few number of ones in each column. The number of ones in each column of is generated independently and randomly in the range of integers between and , and their locations are randomly chosen independently for each column. Let , which is the vertical concatenation of the matrix M and its negative. Following the same setup in [58], the column orthogonality in is not satisfied. Let be a reference signal with , where the non-zero locations are chosen uniformly at random with the values following a zero mean, unit variance Gaussian distribution. Let be the allowable measurement, where is a Gaussian random vector with zero mean and co-variance matrix , where is the identity matrix. The sparse vector is reconstructed from v by solving (7) with .

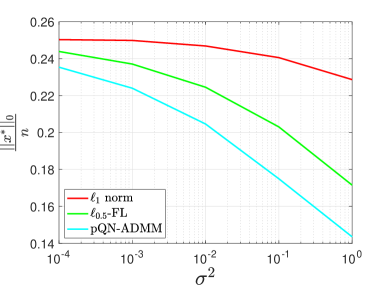

Figure 1 plots the relation between the sparsity level and the noise variance for norm minimization, -FL quasi-norm and pQN-ADMM solutions. A threshold value of was used where the threshold is a value below which the entry of the solution vector is considered to be zero. Depending on the noise variance , the value of was chosen to make the problem feasible. The reported result is the average of 100 independent random runs. It can be realized that pQN-ADMM algorithm produces a sparser solution than its counter baselines for different values of . On increasing , the sparsity level for all methods decreases. This is due to the increased scarcity of information on the original signal in the realization vector which makes the reconstruction process less accurate.

VI-B Binary Classification

In this part, we build an email spam classifier based on support vector machines. We use a subset of the training set used in the SpamAssassin Public Corpus [59]. Let be the training set of feature vectors with corresponding labels identifying whether the email is spam or not. We highlight the effectiveness of our method in designing an email spam detector using the least number of words. Following [60], we maintain a dictionary of words. For a given email , the th entry of is 1 if word of the dictionary is in email , and is 0 otherwise. We aim to build a linear classifier with the decision rule , where is the feature vector of the email in question and is a vector of the classifier coefficients with the first entry being the bias term. The main aim is to build a classifier that detects whether an email is a spam or not, using the least number of words from the dictionary and achieving a high training data accuracy. To achieve this objective, we solve (7) with }.

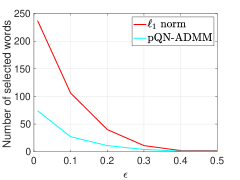

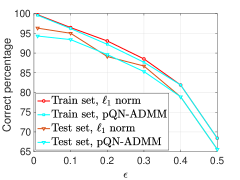

It can be clearly realized that the training set accuracy is controlled by . Algorithm 1 was run for , 2000 training emails and various values for . For each value of , the algorithm was terminated after 100 iterations and performance tested on 1000 emails. For comparison purpose, the problem was also solved with the norm convex relaxation under the same setup. In figure 2(a), we plot the number of non-zero entries in the optimal classifier from both the pQN-ADMM and solutions vs different values of .

We used a threshold of , where the threshold is defined as in section VI-A. It can be realized from figure 2(a) that the pQN-ADMM solution outperforms the in terms of the number of words used for legitimacy detection. When the value of increases, the number of required words decreases for both and problems. This outlines the trade-off between the sparsity level of the classifier and its accuracy, i.e., small values of enforces a low classification error in expense of a less sparse solution. The corresponding training and test set accuracies for the obtained classifiers are plotted in Fig. 2(b). Both figures 2(a) and 2(b) depict the performance of the pQN-ADMM solution from algorithm 1 in terms of the sparsity level while maintaining nearly the same level of accuracy as the solution for both the training and test sets.

VII Numerical Results for RMP Problem

VII-A Time domain system identification

In this part, we apply the derived pQN-ADMM approach on a time domain system identification example. In that example, input is applied to randomly generated systems with a known order. Using the outputs corresponding to these systems, the minimum rank/order system is derived and results are compared to nuclear norm heuristic in [26].

We consider a discrete time stable Single Input Single Output (SISO) system with an input , where represents the number of input samples, i.e., input time span. We assume an impulse response of a fixed number of samples . The corresponding system output is . However, we assume that only noisy realizations, , of the output can be considered, such that; , where is the system’s original impulse response, is a random vector with entries drawn independently from samples of a uniform distribution on the range , i.e., , while denotes the convolution operator. From the window property of the convolution, . Assume that , and are the th components of the vectors , and respectively. The three components are related to each other by convolution through which is a linear relation. Hence, let be the Toeplitz matrix formed by the input , it can be easily seen that . Assume that is an impulse response variable and let be a Hankel matrix formed by the entries of . From [29, 61, 62, 63], the minimum order time domain system identification problem can be formulated as,

| (60a) | ||||

| s.t. | (60b) | |||

| (60c) | ||||

(60b) ensures that is a Hankel matrix and (60c) holds to make the result by applying the input, , to the optimal impulse response, , fit the available noisy data, , in a non-trivial sense. Defining the convex set , (60) can be cast as,

| (61) |

which is clearly identical to the problem in (1). The problem was solved using the same pQN-ADMM approach discussed in section IV.

We let and . Note that , which is a reasonable assumption as in some practical applications, one is allowed only a specific window to realize the output. We consider the simulation for 10 different original system orders, i.e., . An input vector, , is generated, where the elements of are independent and follow a uniform distribution on the interval . For each ; 1) 50 random stable systems are generated using the command ’drss’ in MATLAB. 2) The generated input is applied to each system to get the corresponding noisy output . 3) Given the output , the problem in (60) is solved and the corresponding system’s rank is calculated using singular value decomposition. 4) The results are averaged out to get the corresponding average rank to each original .

| =2 | =6 | =10 | |

|---|---|---|---|

| Nuclear norm | 2.3907 | 6.6668 | 7.2572 |

| pQN-ADMM | 0.5292 | 0.9042 | 1.0861 |

| =2 | =6 | =10 | |

|---|---|---|---|

| Nuclear norm | 6.9877 | 11.2638 | 11.7854 |

| pQN-ADMM | 0.5325 | 0.9113 | 1.0861 |

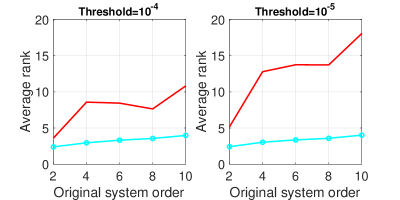

Figure 3 shows the average rank for the the nuclear norm and pQN-ADMM heuristics. The results are for two different values of thresholds, where the threshold is defined as the value below which the singular value is considered to be zero. It can be realized that the introduced pQN-ADMM approach outperforms the nuclear norm one for both values of thresholds. Moreover, when the threshold value decreases from to , the behavior of the pQN-ADMM remains the same. However, the average rank for the nuclear norm increases. This proves the robustness of the derived pQN-ADMM in comparison to the nuclear norm one. Tables I and II show the standard deviation of the algorithms. It can be seen that the standard deviation is the same for the pQN-ADMM when changing the threshold, however, it increases for the nuclear norm as the threshold value decreases.

VII-B Matrix Completion Example

In this section, we apply our algorithm (pQN-ADMM) to a matrix completion example and compare the result to the matrix iterative re-weighted least squares (MatrixIRLS) [64, 65], truncated iterative re-weighted unconstrained Lq (tIRucLq) [34] and iterative re-weighted least squares (sIRLS-p IRLS-p) [66] algorithms. The matrix completion problem is a special case of the low rank minimization where a linear transform takes a few random entries of an ambiguous matrix . Given only these entries, the goal is to approximate and find the missing ones. The matrix completion problem with low rank recovery can be approximated by,

| (62) |

where is a linear map with and . In order to apply the mentioned algorithms, the linear transform will be rewritten as , where and is a vector formed by stacking the columns of the matrix .

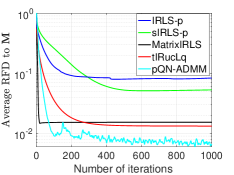

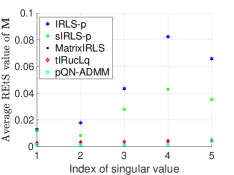

A random matrix with rank is created using the following method: 1) , where and . 2) The entries of both and are i.i.d Gaussian random variables with zero mean and unit variance. Let , where is a Gaussian noise with each entry being an i.i.d Gaussian random variable with zero mean and variance . The vector is then created by selecting random elements from . Since , one can easily construct the matrix which is a sparse matrix where each row is composed of a value 1 at the index of the corresponding selected entry in the vector while the rest are zeros. We set , and . Let denotes the dimension of the set of rank matrices and define as the sampling ratio. We assume that which yields to . It can be realized that . We set and let the algorithms terminate if a budget of 1000 iterations is reached. In order to compare the results from different algorithms, we consider the average of 50 runs for two measures: a) the relative Frobenius distance (RFD) to the matrix , b) the relative error to singular (REtS) values of .

In figures 4(a) and 4(b), we report the average RFD and REtS values for all the algorithms. Despite that all the baselines are designed to exploit the specific structure of the matrix completion problem, described in (62), while the proposed pQN-ADMM doesn’t, it is competitive against them all. This in turns shows the effectiveness of the pQN-ADMM algorithm in solving the rank minimization problems without requiring any prior information about the structure of the associated convex set.

VIII Numerical Results for the nonconvex Accelerated Proximal Gradient (APG) Algorithm

In this subsection, we present numerical results for the APG method, displayed in Algorithm 3. Following the same procedure in [67], we first generate the target signal through

| (63) |

where the design parameters , and for are chosen as follows:

-

1.

the index set is constructed by selecting a subset of with cardinality uniformly at random;

-

2.

are independent, identically distributed (IID) Bernoulli random variables taking values with equal probability;

-

3.

are IID uniform random variables.

The measurement matrix is a partial Discrete Cosine Transform (DCT) matrix with rows corresponding to frequency, where these indices are chosen uniformly at random from . The noisy measurement vector is then set to be , where and are the input and realization noises.

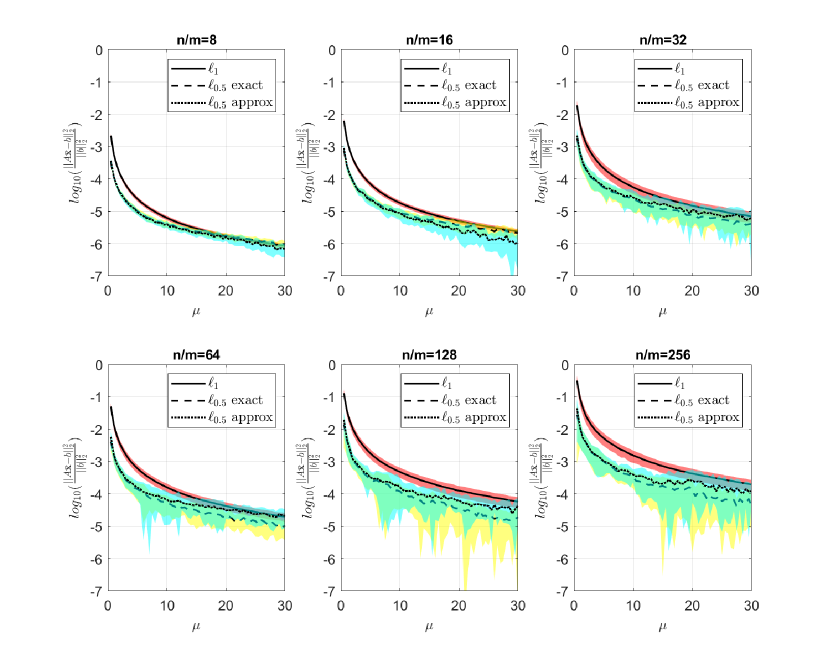

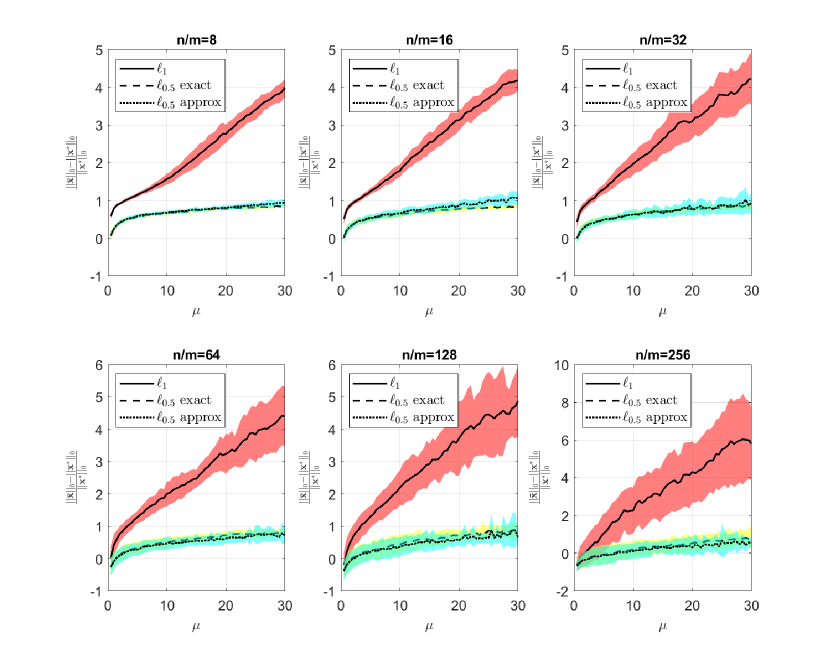

In our experiments, , and the PG algorithm memory to 5, i.e., . Following the medium noise setup in [68], we set , .

For , we have . We perform our experiment for various values of , i.e., number of noisy measurements, and , i.e., trade-off parameter, see (47). For each selection, in order to capture the inherent statistical variation of the problem, we generate 20 random instances of the triplet and each random instance is solved by Algorithm 3. We reported the average performance. We terminated Algorithm 3 when the relative error between consecutive iterates satisfies for the first time.

In our experiments, we compared solving (47) for against , i.e., against -optimization for sparse recovery. On one hand, when , i.e., for minimization, we solve (47) using Algorithm 3, called exact, and using the algorithm 2 of [69], which we call approx. On the other hand, when , -minimization problem is a convex one and we adopt the FISTA algorithm of [70]. The solution is denoted by while the target signal, from (63), by . In Algorithm 3, is set to a zero vector while is the norm solution.

Figures 5 and 6 highlight the relation between the average error and sparsity vs for different values of . It can be realized that the average error (sparsity) decreases (increases) on increasing . For small values of , more weight is given to the loss function, which emphasizes the quasi-norm minimization, and hence the sparsity level, as in figure 6, is low. However, for high values of , more weight is assigned to the minimization of the regularization term, which solves , and hence the error decreases, as shown in figure 3, with a corresponding increase in the sparsity. It can be realized that the solutions always outperforms the one with very slight difference between the exact and the approximate ones.

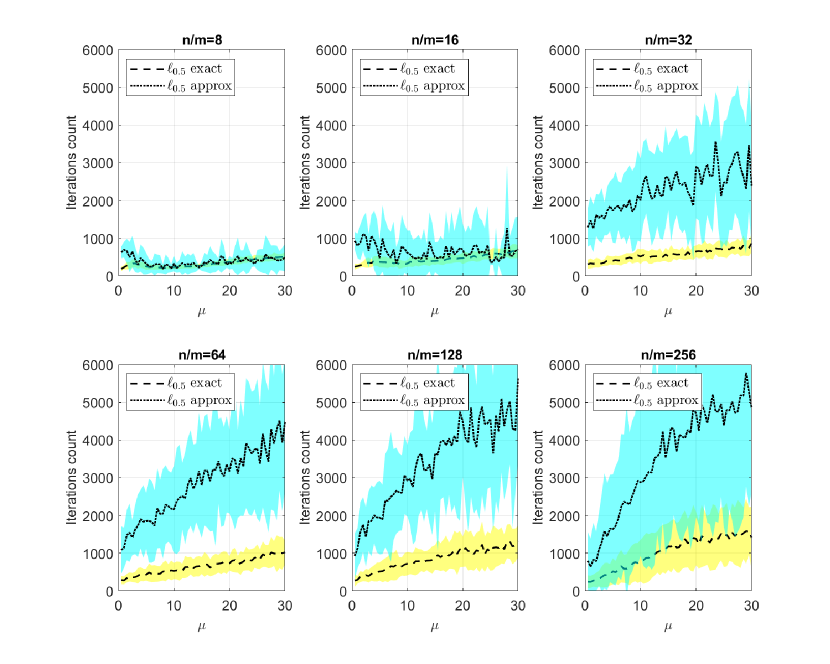

Figure 7 highlights the statistics of the number of iterations used until convergence for both the exact and approximate algorithms. It can be realized that with a sufficient number of available realizations, and , both algorithms approximately consume the same number of iterations. However, when the number of available realizations decreases, and higher, our exact proximal solution requires significantly less number of iterations to converge. This conclusion, along with figures 5 and 6 findings, indicates that our algorithm not only finds a similar solution to the approximate method, but also converges with a fewer number of iterations.

IX Conclusion

In this study, we presented a non-convex ADMM algorithm (pQN-ADMM) to solve the norm minimization problem. The algorithm has a similar complexity to that of the minimization in addition to solving the roots of a polynomial for the non-convex projection. Our algorithm can also be considered as a general procedure for solving problems as no specific structure for the convex constraint set was assumed and a convex projection on that set was done for variables update. Applying sparse signal recover and binary classification examples, our method was found to outperform the minimization in terms of the sparsity of the generated solution. In addition, we studied the problem of solving a non-convex relaxation of RMPs using Schatten-p quasi-norm. This relaxation was shown to be the minimization of the singular values of the variable matrix and hence the primary developed algorithm could be used. Showing the numerical results, the pQN-ADMM was found to be less sensitive to the threshold decrease in time domain system identification problems. Additionally, the pQN-ADMM method was shown to be competitive against various other baselines when solving the matrix completion problem.

References

- [1] L. Vandenberghe and S. Boyd, “Semidefinite programming,” SIAM Review, vol. 38, no. 1, pp. 49–95, 1996.

- [2] E. J. Candes and T. Tao, “Decoding by linear programming,” IEEE Transactions on Information Theory, vol. 51, no. 12, pp. 4203–4215, 2005.

- [3] J. Wright, A. Y. Yang, A. Ganesh, S. S. Sastry, and Y. Ma, “Robust face recognition via sparse representation,” IEEE Transactions on Pattern Analysis and Machine Intelligence, vol. 31, no. 2, pp. 210–227, 2009.

- [4] E. J. Candes, J. Romberg, and T. Tao, “Robust uncertainty principles: exact signal reconstruction from highly incomplete frequency information,” IEEE Transactions on Information Theory, vol. 52, no. 2, pp. 489–509, 2006.

- [5] D. L. Donoho, “Compressed sensing,” IEEE Transactions on Information Theory, vol. 52, no. 4, pp. 1289–1306, 2006.

- [6] A. M. Bruckstein, D. L. Donoho, and M. Elad, “From sparse solutions of systems of equations to sparse modeling of signals and images,” SIAM review, vol. 51, no. 1, pp. 34–81, 2009.

- [7] J. A. Tropp and S. J. Wright, “Computational methods for sparse solution of linear inverse problems,” Proceedings of the IEEE, vol. 98, no. 6, pp. 948–958, 2010.

- [8] S. G. Mallat and Zhifeng Zhang, “Matching pursuits with time-frequency dictionaries,” IEEE Transactions on Signal Processing, vol. 41, no. 12, pp. 3397–3415, 1993.

- [9] J. A. Tropp, “Greed is good: algorithmic results for sparse approximation,” IEEE Transactions on Information Theory, vol. 50, no. 10, pp. 2231–2242, 2004.

- [10] S. S. Chen, D. L. Donoho, and M. A. Saunders, “Atomic decomposition by basis pursuit,” SIAM review, vol. 43, no. 1, pp. 129–159, 2001.

- [11] R. Tibshirani, “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society: Series B (Methodological), vol. 58, no. 1, pp. 267–288, 1996.

- [12] R. Chartrand, “Exact reconstruction of sparse signals via nonconvex minimization,” IEEE Signal Processing Letters, vol. 14, no. 10, pp. 707–710, 2007.

- [13] R. Chartrand and W. Yin, “Iteratively reweighted algorithms for compressive sensing,” in 2008 IEEE International Conference on Acoustics, Speech and Signal Processing, pp. 3869–3872, IEEE, 2008.

- [14] D. P. Wipf and B. D. Rao, “Sparse bayesian learning for basis selection,” IEEE Transactions on Signal Processing, vol. 52, no. 8, pp. 2153–2164, 2004.

- [15] P. Schniter, L. C. Potter, and J. Ziniel, “Fast bayesian matching pursuit,” in 2008 Information Theory and Applications Workshop, pp. 326–333, 2008.

- [16] A. Miller, Subset selection in regression. CRC Press, 2002.

- [17] R. Saab, R. Chartrand, and O. Yilmaz, “Stable sparse approximations via nonconvex optimization,” in 2008 IEEE International Conference on Acoustics, Speech and Signal Processing, pp. 3885–3888, 2008.

- [18] R. Chartrand, “Fast algorithms for nonconvex compressive sensing: MRI reconstruction from very few data,” in 2009 IEEE International Symposium on Biomedical Imaging: From Nano to Macro, pp. 262–265, 2009.

- [19] N. Mourad and J. P. Reilly, “Minimizing nonconvex functions for sparse vector reconstruction,” IEEE Transactions on Signal Processing, vol. 58, no. 7, pp. 3485–3496, 2010.

- [20] R. Chartrand and B. Wohlberg, “A nonconvex ADMM algorithm for group sparsity with sparse groups,” in 2013 IEEE International Conference on Acoustics, Speech and Signal Processing, pp. 6009–6013, 2013.

- [21] Z. Xu, X. Chang, F. Xu, and H. Zhang, “ regularization: A thresholding representation theory and a fast solver,” IEEE Transactions on Neural Networks and Learning Systems, vol. 23, no. 7, pp. 1013–1027, 2012.

- [22] J. Zeng, S. Lin, Y. Wang, and Z. Xu, “ regularization: Convergence of iterative half thresholding algorithm,” IEEE Transactions on Signal Processing, vol. 62, no. 9, pp. 2317–2329, 2014.

- [23] G. Li and T. K. Pong, “Global convergence of splitting methods for nonconvex composite optimization,” SIAM Journal on Optimization, vol. 25, no. 4, pp. 2434–2460, 2015.

- [24] Y. Wang, W. Yin, and J. Zeng, “Global convergence of ADMM in nonconvex nonsmooth optimization,” Journal of Scientific Computing, vol. 78, no. 1, pp. 29–63, 2019.

- [25] M. Mesbahi, “On the semi-definite programming solution on the least order dynamic output feedback synthesis,” 1999.

- [26] M. Fazel, H. Hindi, and S. P. Boyd, “A rank minimization heuristic with application to minimum order system approximation,” in Proceedings of the 2001 American Control Conference. (Cat. No.01CH37148), vol. 6, pp. 4734–4739 vol.6, 2001.

- [27] M. Fazel, H. Hindi, and S. P. Boyd, “Log-det heuristic for matrix rank minimization with applications to hankel and euclidean distance matrices,” in Proceedings of the 2003 American Control Conference, 2003., vol. 3, pp. 2156–2162 vol.3, 2003.

- [28] M. Fazel, H. Hindi, and S. Boyd, “Rank minimization and applications in system theory,” in Proceedings of the 2004 American Control Conference, vol. 4, pp. 3273–3278 vol.4, 2004.

- [29] K. Mohan and M. Fazel, “Reweighted nuclear norm minimization with application to system identification,” in Proceedings of the 2010 American Control Conference, pp. 2953–2959, 2010.

- [30] S. Gu, L. Zhang, W. Zuo, and X. Feng, “Weighted nuclear norm minimization with application to image denoising,” in 2014 IEEE Conference on Computer Vision and Pattern Recognition, pp. 2862–2869, 2014.

- [31] F. Nie, H. Huang, and C. Ding, “Low-rank matrix recovery via efficient Schatten p-norm minimization,” in Twenty-sixth AAAI conference on artificial intelligence, 2012.

- [32] F. Nie, H. Wang, H. Huang, and C. Ding, “Joint schatten -norm and norm robust matrix completion for missing value recovery,” Knowledge and Information Systems, vol. 42, no. 3, pp. 525–544, 2015.

- [33] L. Liu, W. Huang, and D.-R. Chen, “Exact minimum rank approximation via Schatten p-norm minimization,” Journal of Computational and Applied Mathematics, vol. 267, pp. 218–227, 2014.

- [34] M.-J. Lai, Y. Xu, and W. Yin, “Improved iteratively reweighted least squares for unconstrained smoothed minimization,” SIAM Journal on Numerical Analysis, vol. 51, no. 2, pp. 927–957, 2013.

- [35] R. Chartrand, “Nonconvex splitting for regularized low-rank + sparse decomposition,” IEEE Transactions on Signal Processing, vol. 60, no. 11, pp. 5810–5819, 2012.

- [36] M. D. Gupta and S. Kumar, “Non-convex p-norm projection for robust sparsity,” in 2013 IEEE International Conference on Computer Vision, pp. 1593–1600, 2013.

- [37] S. Bahmani and B. Raj, “A unifying analysis of projected gradient descent for -constrained least squares,” Applied and Computational Harmonic Analysis, vol. 34, no. 3, pp. 366–378, 2013.

- [38] M. E. Ashour, C. M. Lagoa, and N. S. Aybat, “Lp quasi-norm minimization,” in 2019 53rd Asilomar Conference on Signals, Systems, and Computers, pp. 726–730, 2019.

- [39] S. Boyd, N. Parikh, and E. Chu, Distributed optimization and statistical learning via the alternating direction method of multipliers. Now Publishers Inc, 2011.

- [40] C. Helmberg and F. Rendl, “A spectral bundle method for semidefinite programming,” SIAM Journal on Optimization, vol. 10, no. 3, pp. 673–696, 2000.

- [41] A. Beck and M. Teboulle, “Mirror descent and nonlinear projected subgradient methods for convex optimization,” Operations Research Letters, vol. 31, no. 3, pp. 167–175, 2003.

- [42] Y. Nesterov and A. Nemirovskii, Interior-point polynomial algorithms in convex programming. SIAM, 1994.

- [43] A. Ben-Tal and A. Nemirovski, Lectures on modern convex optimization: analysis, algorithms, and engineering applications. SIAM, 2001.

- [44] Y. Xu and W. Yin, “A globally convergent algorithm for nonconvex optimization based on block coordinate update,” Journal of Scientific Computing, vol. 72, no. 2, pp. 700–734, 2017.

- [45] Z. Zha, X. Zhang, Y. Wu, Q. Wang, X. Liu, L. Tang, and X. Yuan, “Non-convex weighted nuclear norm based ADMM framework for image restoration,” Neurocomputing, vol. 311, pp. 209–224, 2018.

- [46] L. Mirsky, “A trace inequality of John von Neumann,” Monatshefte für mathematik, vol. 79, no. 4, pp. 303–306, 1975.

- [47] N. Parikh and S. Boyd, “Proximal algorithms,” Foundations and Trends in optimization, vol. 1, no. 3, pp. 127–239, 2014.

- [48] Q. Yao, J. T. Kwok, F. Gao, W. Chen, and T.-Y. Liu, “Efficient inexact proximal gradient algorithm for nonconvex problems,” arXiv preprint arXiv:1612.09069, 2016.

- [49] A. Beck and M. Teboulle, “A fast iterative shrinkage-thresholding algorithm for linear inverse problems,” SIAM journal on imaging sciences, vol. 2, no. 1, pp. 183–202, 2009.

- [50] H. Attouch, J. Bolte, and B. F. Svaiter, “Convergence of descent methods for semi-algebraic and tame problems: proximal algorithms, forward–backward splitting, and regularized Gauss–Seidel methods,” Mathematical Programming, vol. 137, no. 1, pp. 91–129, 2013.

- [51] H. Attouch, J. Bolte, P. Redont, and A. Soubeyran, “Proximal alternating minimization and projection methods for nonconvex problems: An approach based on the Kurdyka-Lojasiewicz inequality,” Mathematics of operations research, vol. 35, no. 2, pp. 438–457, 2010.

- [52] J. Bolte, S. Sabach, and M. Teboulle, “Proximal alternating linearized minimization for nonconvex and nonsmooth problems,” Mathematical Programming, vol. 146, no. 1, pp. 459–494, 2014.

- [53] M. Razaviyayn, M. Hong, and Z.-Q. Luo, “A unified convergence analysis of block successive minimization methods for nonsmooth optimization,” SIAM Journal on Optimization, vol. 23, no. 2, pp. 1126–1153, 2013.

- [54] P. Tseng and S. Yun, “A coordinate gradient descent method for nonsmooth separable minimization,” Mathematical Programming, vol. 117, no. 1, pp. 387–423, 2009.

- [55] Y. Hu, C. Li, K. Meng, and X. Yang, “Linear convergence of inexact descent method and inexact proximal gradient algorithms for lower-order regularization problems,” Journal of Global Optimization, vol. 79, no. 4, pp. 853–883, 2021.

- [56] M. ApS, The MOSEK optimization toolbox for MATLAB manual. Version 9.0., 2019.

- [57] S. Foucart and M.-J. Lai, “Sparsest solutions of under-determined linear systems via -minimization for ,” Applied and Computational Harmonic Analysis, vol. 26, no. 3, pp. 395–407, 2009.

- [58] D. Ge, X. Jiang, and Y. Ye, “A note on the complexity of minimization,” Mathematical programming, vol. 129, no. 2, pp. 285–299, 2011.

- [59] SpamAssassin Public Corpus, http://spamassassin.apache.org.

- [60] Andrew Ng, Machine learning MOOC, https://www.coursera.org/learn/machine-learning.

- [61] M. Sznaier, M. Ayazoglu, and T. Inanc, “Fast structured nuclear norm minimization with applications to set membership systems identification,” IEEE Transactions on Automatic Control, vol. 59, no. 10, pp. 2837–2842, 2014.

- [62] Z. Liu and L. Vandenberghe, “Semidefinite programming methods for system realization and identification,” in Proceedings of the 48h IEEE Conference on Decision and Control (CDC) held jointly with 2009 28th Chinese Control Conference, pp. 4676–4681, 2009.

- [63] M. Fazel, T. K. Pong, D. Sun, and P. Tseng, “Hankel matrix rank minimization with applications to system identification and realization,” SIAM Journal on Matrix Analysis and Applications, vol. 34, no. 3, pp. 946–977, 2013.

- [64] C. Kümmerle and C. Mayrink Verdun, “Escaping saddle points in ill-conditioned matrix completion with a scalable second order method,” in Workshop on Beyond First Order Methods in ML Systems at the International Conference on Machine Learning, 2020.

- [65] C. Kümmerle and C. Mayrink Verdun, “A scalable second order method for ill-conditioned matrix completion from few samples,” in International Conference on Machine Learning (ICML), 2021.

- [66] K. Mohan and M. Fazel, “Iterative reweighted algorithms for matrix rank minimization,” Journal of Machine Learning Research, vol. 13, no. 110, pp. 3441–3473, 2012.

- [67] N. S. Aybat and G. Iyengar, “A first-order augmented Lagrangian method for compressed sensing,” SIAM Journal on Optimization, vol. 22, no. 2, pp. 429–459, 2012.

- [68] E. T. Hale, W. Yin, and Y. Zhang, “A fixed-point continuation method for l1-regularized minimization with applications to compressed sensing,” CAAM TR07-07, Rice University, vol. 43, p. 44, 2007.

- [69] C. O’Brien and M. D. Plumbley, “Inexact proximal operators for -Quasi-norm minimization,” in 2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pp. 4724–4728, 2018.

- [70] A. Beck and M. Teboulle, “A fast iterative shrinkage-thresholding algorithm for linear inverse problems,” SIAM journal on imaging sciences, vol. 2, no. 1, pp. 183–202, 2009.