Maragno et al.

Finding Regions of Counterfactual Explanations via Robust Optimization

Finding Regions of Counterfactual Explanations via Robust Optimization

Donato Maragno, Jannis Kurtz, Tabea E. Röber, Rob Goedhart, Ş. İlker Birbil, Dick den Hertog

\AFFAmsterdam Business School, University of Amsterdam, 1018TV Amsterdam, Netherlands

\EMAILd.maragno@uva.nl j.kurtz@uva.nl t.e.rober@uva.nl r.goedhart2@uva.nl

s.i.birbil@uva.nl d.denhertog@uva.nl

Counterfactual explanations play an important role in detecting bias and improving the explainability of data-driven classification models. A counterfactual explanation (CE) is a minimal perturbed data point for which the decision of the model changes. Most of the existing methods can only provide one CE, which may not be achievable for the user. In this work we derive an iterative method to calculate robust CEs, i.e., CEs that remain valid even after the features are slightly perturbed. To this end, our method provides a whole region of CEs allowing the user to choose a suitable recourse to obtain a desired outcome. We use algorithmic ideas from robust optimization and prove convergence results for the most common machine learning methods including decision trees, tree ensembles, and neural networks. Our experiments show that our method can efficiently generate globally optimal robust CEs for a variety of common data sets and classification models.

counterfactual explanation; explainable AI; machine learning; robust optimization

1 Introduction

Counterfactual explanations, also known as algorithmic recourse, are becoming increasingly popular as a way to explain the decisions made by black-box machine learning (ML) models. Given a factual instance for which we want to derive an explanation, we search for a counterfactual feature combination describing the minimum change in the feature space that will lead to a flipped model prediction. For example, for a person with a rejected loan application, the counterfactual explanation (CE) could be “if the annual salary would increase to 50,000$, then the loan application would be approved.” This method enables a form of user agency and is therefore particularly attractive in consequential decision making, where the user is directly and indirectly impacted by the outcome of the ML model.

The first optimization-based approach to generate CEs has been proposed by Wachter et al. (2018). Given a trained classifier and a factual instance , the aim is to find a counterfactual that has the shortest distance to , and has the opposite target. The problem to obtain can be formulated as

| (1) | ||||

| subject to | (2) |

where is a distance function, often chosen to be the -norm or the -norm, and is a given threshold parameter for the classification decision.

Others have built on this work and proposed approaches that generate CEs with increased practical value, primarily by adding constraints to ensure actionability of the proposed changes and generating CEs that are close to the data manifold (Ustun et al. 2019, Russell 2019, Mahajan et al. 2019, Mothilal et al. 2020, Maragno et al. 2022). Nonetheless, the user agency provided by these methods remains theoretical: the generated CEs are exact point solutions that may remain difficult, if not impossible, to implement in practice. A minimal change to the proposed CE could fail to flip the model’s prediction, especially since the CEs are close to the decision boundary due to minimizing the distance between and . As a solution, prior work suggests generating several CEs to increase the likelihood of generating at least one attainable solution. Approaches generating several CEs typically require solving the optimization problem multiple times (Russell 2019, Mothilal et al. 2020, Kanamori et al. 2021, Karimi et al. 2020), which might heavily affect the optimization time when the number of explanations is large. Maragno et al. (2022) suggest using incumbent solutions, however, this does not allow to control the quality of sub-optimal solutions. On top of that, the added practical value may be unconvincing: each of the CEs is still sensitive to arbitrarily small changes in the actions implemented by the user (Dominguez-Olmedo et al. 2021, Pawelczyk et al. 2022, Virgolin and Fracaros 2023).

This problem has been acknowledged in prior work and falls under the discussion of robustness in CEs. In the literature, the concept of robustness in CEs has different meanings: (1) robustness to input perturbations (Slack et al. 2021, Artelt et al. 2021) and generating explanations for a group of individuals Carrizosa et al. (2021), (2) robustness to model changes (Rawal et al. 2020, Forel et al. 2022, Upadhyay et al. 2021, Ferrario and Loi 2022, Black et al. 2021, Dutta et al. 2022, Bui et al. 2022), (3) robustness to hyperparameter selection (Dandl et al. 2020), and (4) robustness to recourse (Pawelczyk et al. 2022, Dominguez-Olmedo et al. 2021, Virgolin and Fracaros 2023). The latter perspective, albeit very user-centered, has so far received only a little attention. Our work focuses on the latter definition of robustness in CEs, specifically, the idea of robustness to recourse. This means that a counterfactual solution should remain valid even if small changes are made to the implemented recourse action. In other words, we aim to define regions of counterfactual solutions that allow the user to choose any point within that region to flip the model prediction. This extends the idea of offering several explanations for the user to choose from, such that not only the suggested point is a counterfactual, but every point in the defined region. Returning to the example we used above, a final explanation may be “if the annual salary would increase to anywhere between 50,000$ and 54,200$, then the loan application would be approved.” While existing research has tackled this problem, their solutions are not comprehensive and have room for further improvements. In the remainder of this section, we will explore the related prior work and present our own contributions to this field.

Pawelczyk et al. (2022) introduce the notion of recourse invalidation rate, which amounts to the proportion of recourse that does not lead to the desired model prediction, i.e., that is invalid. They model the noise around a counterfactual data point with a Gaussian distribution and suggest an approach that ensures the invalidation rate within a specified neighborhood around the counterfactual data point to be no larger than a target recourse invalidation rate. However, their work provides a heuristic solution using a gradient-based approach, which makes it not directly applicable to decision tree models. Additionally, it only provides a probabilistic robustness guarantee. Dominguez-Olmedo et al. (2021) introduce an approach where the optimal solution is surrounded by an uncertainty set such that every point in the set is a feasible solution. They also model causality between (perturbed) features to obtain a more informative neighborhood of similar points. Given a structural causal model (SCM), they model such perturbations as additive interventions on the factual instance features. The authors design an iterative approach that works only for differentiable classifiers and does not guarantee that the generated recourse actions are adversarially robust. Virgolin and Fracaros (2023) incorporate the possibility of additional intervention to contrast perturbations in their search for CEs. They make a distinction between the features that could be changed and those that should be kept as they are, and introduce the concept of C-setbacks; a subset of perturbations in changeable features that work against the user. Rather than seeking CEs that are not invalidated by C-setbacks, they seek CEs for which the additional intervention cost to overcome the setback is minimal. Perturbations to features that should be kept as they are according to a CE are orthogonal to the direction of the counterfactual, and Virgolin and Fracaros (2023) approximate a robustness-score for such features. A drawback of this method is that it is only applicable in situations where additional intervention is possible, and not in situations where (e.g., due to time limitations) only a single recourse is possible.

Our work addresses robustness to recourse by utilizing a robust optimization approach to generate regions of CEs. For a given factual instance, our method generates a CE that is robust to small perturbations. This gives the user more flexibility in implementing the recourse and reduces the risk of invalidating it. In this work we consider numerical features, ensuring that small perturbations do not affect the recourse validity, while categorical features are treated as immutable based on user preferences. Additionally, the generated CEs are optimal in terms of their objective distance to the factual instance. The proposed algorithm is proven to converge, ensuring that the optimal solution is reached. This is different from prior work that provides only heuristic algorithms which are not provably able to find the optimal (i.e., closest) counterfactual point with a certain robustness guarantee (e.g., Pawelczyk et al. 2022, Dominguez-Olmedo et al. 2021). Unlike prior research in this area, our approach is able to provide deterministic robustness guarantees for the CEs generated. Furthermore, our method does not require differentiability of the underlying ML model and is applicable to the tree-based models, which, to the best of our knowledge, has not been done before.

In summary, we make the following contributions:

-

•

We propose an iterative algorithm that effectively finds global optimal robust CEs for trained decision trees, ensembles of trees, and neural networks.

-

•

We prove the convergence of the algorithm for the considered trained models.

-

•

We demonstrate the power of our algorithm on several datasets and different ML models. We empirically evaluate its convergence performance and compare the robustness as well as the validity of the generated CEs with the prior work in the literature.

-

•

We release an open-source software called RCE to make the proposed algorithm easily accessible to practitioners. Our software is available in a dedicated repository111https://github.com/donato-maragno/robust-CE through which all our results can be reproduced.

2 Robust Counterfactual Explanations

We consider binary classification problems, i.e., we have a trained classifier that assigns a value between zero and one to each data point in the data space . A point is then predicted to correspond to class , if and to class , otherwise. Here is a given threshold parameter which is often chosen to be . Given a factual instance which is predicted to be in class , i.e., , the robust CE problem is defined as

| (3) | ||||

| subject to | (4) |

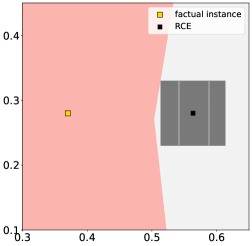

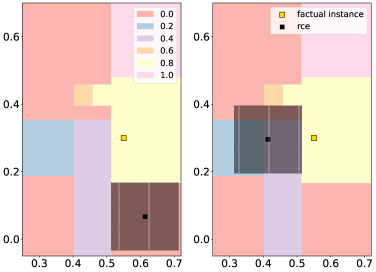

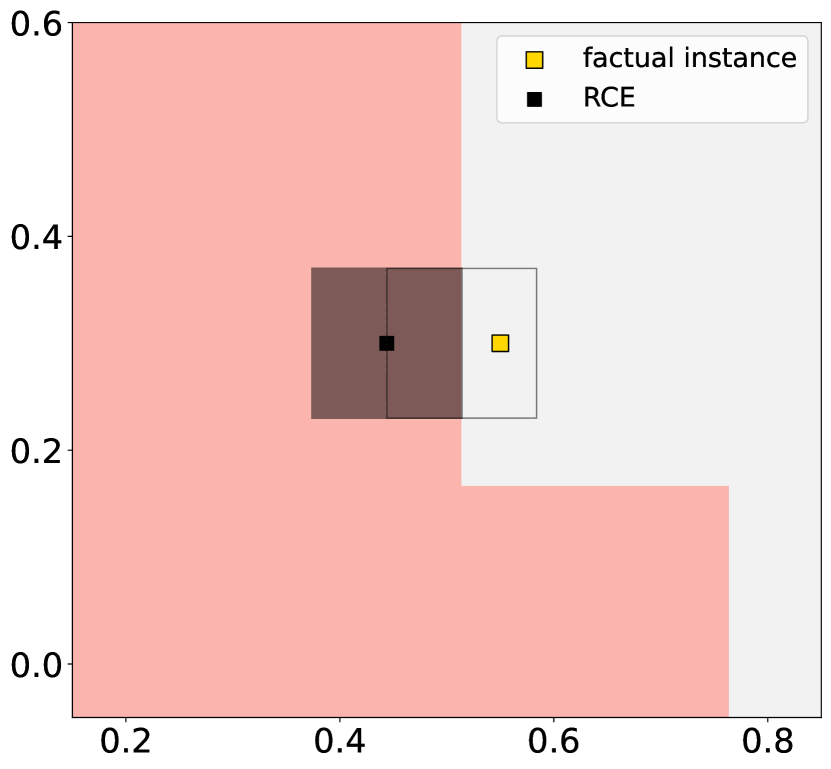

where the represents a distance function, e.g., induced by the -, - or -norm, and is a given uncertainty set. The idea of the problem is to find a point that is as close as possible to the factual instance such that for all perturbations , the corresponding point is classified as which is enforced by constraints (4); see Figure 1. This results in a large set of counterfactual explanations.

We consider uncertainty sets of the type

| (5) |

where is a given norm. Popular choices are the -norm, resulting in a box with upper and lower bounds on features, or the -norm, resulting in a circular uncertainty set. We refer to Ben-Tal et al. (2009a) for a discussion of uncertainty sets. From the user perspective, choosing the -norm has a practical advantage since the region is a box, i.e., we obtain an interval for each attribute of . Each attribute can be changed in its corresponding interval independently, resulting in a counterfactual explanation. Hence, the user can easily detect if there exists a CE in the region that can be practically reached. The choice of the robustness budget greatly depends on the specific domain. Larger values of are associated with CEs that are more robust but can have a larger distance to the factual instance. However, our approach outlined in the subsequent sections is designed to minimize the proximity to the factual instance for a given robustness parameter . If the perturbation applied to the CE adheres to a known distribution, it becomes feasible to determine in a way that offers a probabilistic guarantee of CE robustness. We refer to Appendix 6 for a comprehensive guide on how to determine the appropriate value for .

2.1 Comparison Against Model-Robustness

There are several works that study the robustness of counterfactual explanations regarding changes in the parameters of the trained machine learning model; see e.g. (Rawal et al. 2020, Forel et al. 2022, Upadhyay et al. 2021, Ferrario and Loi 2022, Black et al. 2021, Dutta et al. 2022, Bui et al. 2022). As a motivation to study this concept the re-training of ML models is often mentioned, where after re-training a model the model-parameters can change.

Consider a classifier where is the vector of model parameters that was determined during the training process. In the case of a neural network, this vector contains all weights of the neural network, or in the case of a linear classifier, contains all weight parameters of the linear hyperplane separating the two classes.

Translated into the robust optimization setting we study in this work, a model-robust CE is a point, which remains a CE for all parameter values , where is a given uncertainty set which contains all possible model parameters which have distance at most to the original weights of the classifier. In other words, if is a counterfactual point for the original classifier, i.e., then for each classifier where this must also be the case, i.e., . Note that defining model-robustness for decision tree models is much more elaborate since a decision tree is not only defined by the parameters of its split-hyperplanes but also by the tree structure which can change after re-training the model. So, defining is not as straightforward as it is for linear models.

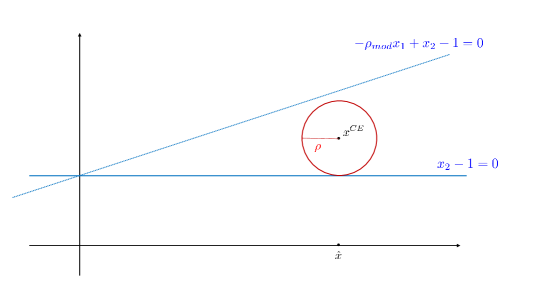

However, a natural question arises: Are the two concepts, model-robustness and recourse-robustness, equivalent? In this case concepts from both fields could profit from each other. Unfortunately, this is not the case, which we show in the following example.

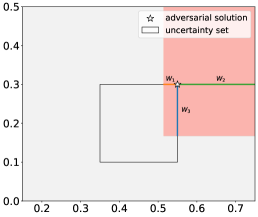

Consider the linear classifier given by the hyperplane , i.e., every point where is classified as and all others as . Then, for every there exists a recourse-robust CE with radius which is not model-robust with radius .

The construction works as follows: Let and define the factual instance . Then the closest recourse-robust CE for radius is for all relevant norms used in (5); see Figure 2. Now consider the -perturbed hyperplane . For , it holds

Hence is not a counterfactual point for the perturbed model.

While the latter example shows that the equivalence of both robustness types does not hold, there can be special cases of models where both concepts are related. However, we place this interesting analysis on our future research agenda.

2.2 Algorithm

We note that the model in (3)-(4) has infinitely many constraints. One approach often used in robust optimization is to rewrite constraints (4) as

and dualize the optimization problem on the left hand side. This leads to a problem with a finite number of constraints. Unfortunately, strong duality is required to perform this reformulation, which does not hold for most classifiers involving non-convexity or integer variables222See Appendix 7 for the well-known dual approach applied to linear models.. In the latter case, we can use an alternative method popular in robust optimization where the constraints are generated iteratively. This iterative approach to solve problem (3)-(4) is known as the adversarial approach. The approach was intensively used for robust optimization problems; see Bienstock and Özbay (2008), Mutapcic and Boyd (2009). In Bertsimas et al. (2016) the adversarial approach was compared to the classical robust reformulation.

The idea of the approach is to consider a relaxed version of the model, where only a finite subset of scenarios is considered:

| (MP) | ||||

| (6) |

This problem is called the master problem (MP), and it only has a finite number of constraints. Note that the optimal value of (MP) is a lower bound of the optimal value of (3)-(4). However, an optimal solution of (MP) is not necessarily feasible for the original problem, since there may exist a scenario in that is not contained in for which the solution is not feasible. More precisely, it may be that there exists an such that , and hence, is not a robust counterfactual.

In this case, we want to find such a scenario that makes solution infeasible. This can be done by solving the following, so called, adversarial problem (AP):

| (AP) |

The idea is to find a scenario such that the prediction of classifier for point is , i.e., . If we can find such a scenario and add it to the set in the MP, then cannot be feasible anymore for (MP). To find the scenario with the largest impact, we maximize the constraint violation in the objective function in (AP). If the optimal value of (AP) is positive then is classified as , and the optimal solution is added to , and we calculate a solution of the updated (MP). We iterate until no violating scenario can be found, that is, until the optimal value of (AP) is smaller or equal to zero. Note that in this case holds for all , which means that is a robust counterfactual. Algorithm 1 shows the steps of our approach, and Figure 3 shows its iterative behaviour. Each time a new scenario is found by solving the AP, it is added to the uncertainty set , and the new solution moves to be feasible also for the new scenario. This is repeated until no scenario can be found anymore, i.e., until the full box lies in the correct region. Note that instead of checking for a positive optimal value of (AP), we use an accuracy parameter in Algorithm 1. In this case, we can guarantee the convergence of our algorithm using the following result.

Theorem 2.1 (Mutapcic and Boyd, 2009)

If is bounded and if is a Lipschitz continuous function, i.e., there exists an such that

for all . Then, for any tolerance parameter value , Algorithm 1 terminates after a finite number of steps with a solution such that

for all .

Indeed without Lipschitz continuity, the convergence of Algorithm 1 cannot be ensured. We elaborate on this necessity in the following example, for which Algorithm 1 does not terminate in a finite number of steps.

Example 2.2

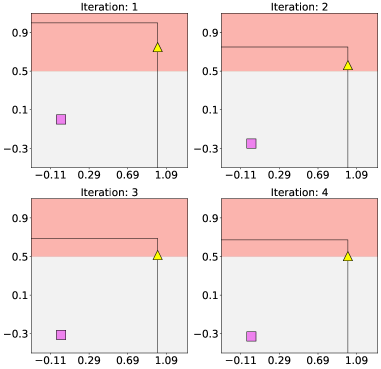

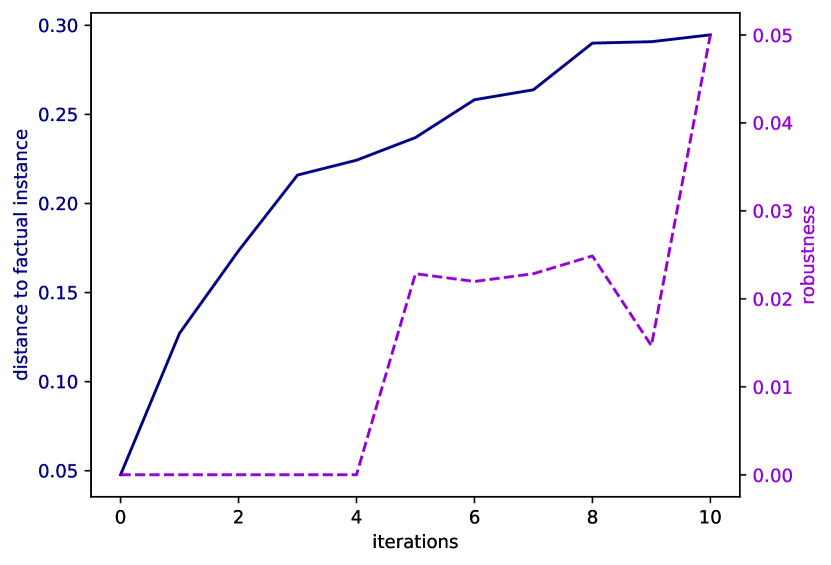

Consider a classifier with , if and , otherwise. The threshold is , i.e., a point is classified as , if and as , otherwise. The factual instance is , which is classified as . Furthermore, the uncertainty set is given as . We can warm-start Algorithm 1 with the (MP) solution . Now, assume that in iteration the optimal solution returned by (AP) is . Note that in the first iteration lies on the boundary of and is classified as , i.e., it is an optimal solution of (AP). We are looking now for the closest point to such that is classified as , that is, it has a second component of at most . This is the point which must be the optimal solution of (MP). Note that is again on the boundary of and is classified as . Hence, is an optimal solution of (AP). We can conclude inductively that the optimal solution of (MP) in iteration is and that is an optimal solution of (AP) in iteration . Note that the latter is true, since the value of is constant in the negative region, and hence, each point in the uncertainty set is an optimal solution of (AP). If the latter solutions are returned by (AP), then the sequence of solutions converges to the point which follows from the limit of the geometric series. However, is not a robust CE regarding , since for instance, is classified as . Consequently, Algorithm 1 never terminates. This example is illustrated in Figure 4.

One difficulty is modeling the constraints of the form for different trained classifiers. For decision trees, ensembles of decision trees, and neural networks, these constraints can be modeled by mixed-integer linear constraints as we present in the following section. Another difficulty is that is discontinuous for decision trees and ensembles of decision trees. To handle these models, we have to find Lipschitz continuous extensions of with equivalent predictions to guarantee convergence of Algorithm 1.

3 Trained Models

The main contribution of this section is modeling MP and AP for different types of classifiers by mixed-integer programming formulations. Furthermore, to prove convergence we need to assure that all studied classifiers are Lipschitz continuous, which is not the case for tree-based models. Hence we introduce a Lipschitz continuous classifier for tree-based models and derive the MP and AP for it.

We give reformulations for (MP) and (AP) for decision trees, tree ensembles, and neural networks that satisfy the conditions needed in Theorem 2.1 for convergence.

3.1 Decision Trees

A decision tree (DT) partitions the data samples into distinct leaves through a series of feature splits. A split at node is performed by a hyperplane . We assume that can have multiple non-zero elements, in which we have the hyperplane split setting – if there is only one non-zero element, this creates an orthogonal (single feature) split. Formally, each leaf of a decision tree is defined by a set of (strict) inequalities

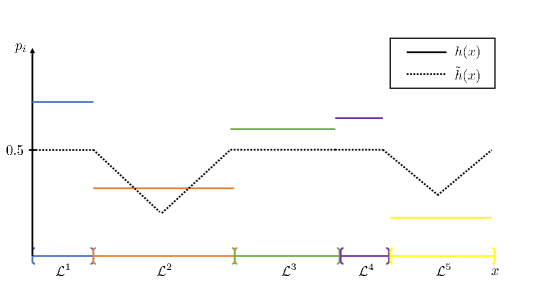

where and contain all split parameters of the leaf for the corresponding inequality type. For ease of notation in the following, we do not distinguish between strict and non-strict inequalities and define . Furthermore, it holds that where is the index set of all leaves of the tree. Each leaf is assigned a weight , which is usually determined by the fraction of training data of class inside the leaf. The classifier is a piecewise constant function , where if and only if is contained in leaf . Since, is a discontinuous step-function, and it is not Lipschitz continuous. To achieve convergence of our algorithm, we have to find a Lipschitz continuous function assigning the same classes to each data point as . To this end we define the function

We choose this function to have a constant value of for all leaves with while for a point in one of the other leaves, we subtract from the minimum slack-value of the point over all leaf-defining constraints. Since the minimum slack on the boundary of the leaves is zero, is a continuous function and it holds in the interior of the latter leaves. Note that the value of decreases if a point is farther away from the boundary of the leaf. Figure 5 illustrates this construction on a one-dimensional feature space.

Theoretically, other function classes than piecewise linear functions could be used to connect the leaf values, as long as these functions are Lipschitz continuous on each leaf region. However, this would lead to non-linear problem formulations for the adversarial problem (see below), which would increase the computational effort of our method.

Unfortunately, due to imposed continuity, the predictions on the boundaries of the leaves can be different than the original predictions of . We show in the following lemma that is Lipschitz continuous and, except on the leaf boundaries, the same class is assigned to each data point as it is done by the original classifier .

Lemma 3.1

The function is Lipschitz continuous on and , where int denotes the interior of the set.

Proof 3.2

Proof. We first show, that is Lipschitz continuous. To this end, let . Consider the following three cases.

Case 1: Both points are contained in a leaf with prediction , i.e., and with . In this case we have

| (7) |

Case 2: Point is in a leaf with prediction , and point is in a leaf with prediction , i.e., and with and . Since is not contained in , there must be split parameters (without loss of generality, we assume that it is related to a non-strict inequality) such that and . It holds , and we obtain

| (8) | ||||

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) |

where the first inequality follows from , the second inequality follows from , and for the last inequality we apply the Cauchy-Schwarz inequality.

Case 3: Both points are contained in a leaf with prediction , i.e., and with . First assume that . Without loss of generality, we also assume that . In this case, we have

| (14) |

which follows from for all . We can prove Lipschitz continuity in this case by following the same steps as in Case 2. When , we designate as the parameters which attain the minimum in

| (15) |

Then, we have

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) |

where we use for the first inequality, and the Cauchy-Schwarz inequality for the last one.

Following the three cases above, we show that is Lipschitz continuous with Lipschitz constant .

We now show the second part of the result. First, assume for that . This implies that is contained in a leaf with , and hence, showing the second inclusion. For the first inclusion, let now be a point in the interior of the set . Assume the contrary of the statement, i.e., it is contained in a leaf with . We can assume that the leaf is full-dimensional, since otherwise the interior is empty. Then, by definition of , it must hold that

| (20) |

That is, there is a such that . Since the leaf is a full-dimensional polyhedron, there exists a and a direction such that for all and all . Consequently, for all . This implies that cannot be in the interior of the set , which is a contradiction. Thus, must be contained in a leaf with which proves the result. \Halmos

We can now derive the formulations for (MP) and (AP) for our tree model. By using Lemma 3.1, we can use instead of to model Constraints (6) in (MP). Then, we can adapt the decision tree formulation proposed by Maragno et al. (2022) and reformulate Constraint (6) of (MP) as

| (21) | |||

| (22) | |||

| (23) | |||

| (24) | |||

| (25) |

where is a predefined large-enough constant. The variables are binary variables associated with the corresponding leaf and scenario , where , if solution is contained in leaf . Constraints (23) ensure that each scenario gets assigned to exactly one leaf. Constraints (21) and (22) ensure that only if leaf is selected for scenario , i.e., , then has to fulfill the corresponding constraints of while the constraints for all other leaves can be violated, which is ensured by the big- value. Note that in our computational experiments we use an -accuracy parameter to reformulate the strict inequalities as non-strict inequalities. Finally, Constraints (24) ensure that the chosen leaf has a weight which is greater than or equal to the threshold . We can remove all variables and constraints of the problem related to leaves with together with constraint (24), since only leafs which correspond to label can be chosen to obtain a feasible solution.

Using the Lipschitz continuous function , (AP) can be reformulated as

| (26) |

Optimizing over is equivalent to iterating over all leaves with and maximizing the same function over the corresponding leaf. The problem is formulated as:

| maximize | (27) | |||

| subject to | (28) | |||

| (29) | ||||

| (30) |

for each such leaf. Using a level-set transformation and substituting the latter problem in (26) leads to

| maximize | (31) | |||

| subject to | (32) | |||

| (33) | ||||

| (34) | ||||

| (35) |

which is equivalent to maximizing the minimum slacks of the constraints corresponding to the leaves. Geometrically this means that we try to find a perturbation such that is as deep as possible in one of the negative leaves; see Figure 6. Note that the problems (31) are continuous optimization problems that can be solved efficiently by state-of-the-art solvers, such as, Gurobi Gurobi Optimization, LLC (2022) or CPLEX Cplex (2009).

Heuristic Variant.

Using Algorithm 1 can be computationally demanding, since it requires solving (MP) and (AP) many times in an iterative manner. An alternative and more efficient approach can be conducted, where we try to find a CE that is robust only regarding to one leaf of the tree. More precisely, this means that is contained in the same leaf for all . This is an approximation, since for each scenario , the point could be contained in a different neighboring leaf leading to better CEs; see Figure 8. Hence, the solutions of the latter approach may be non-optimal. When restricting to one leaf, we can iterate over all possible leaves with and solve the resulting (MP):

| minimize | (36) | |||

| subject to | (37) | |||

| (38) | ||||

| (39) |

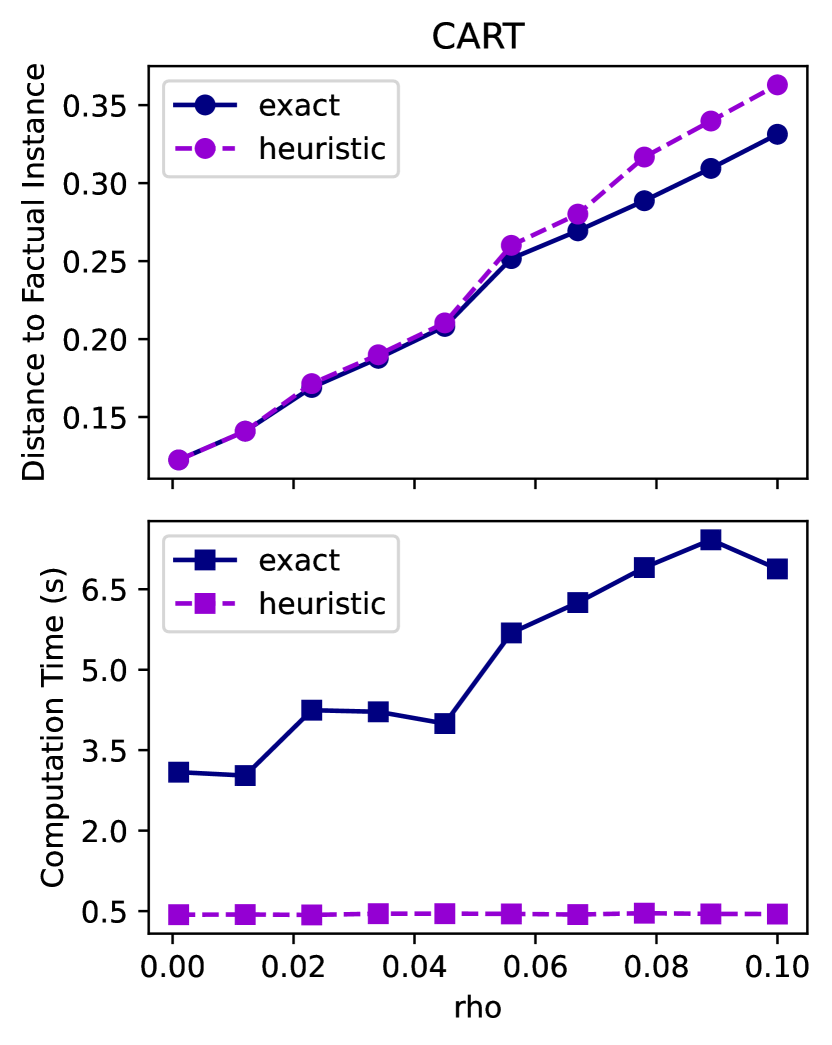

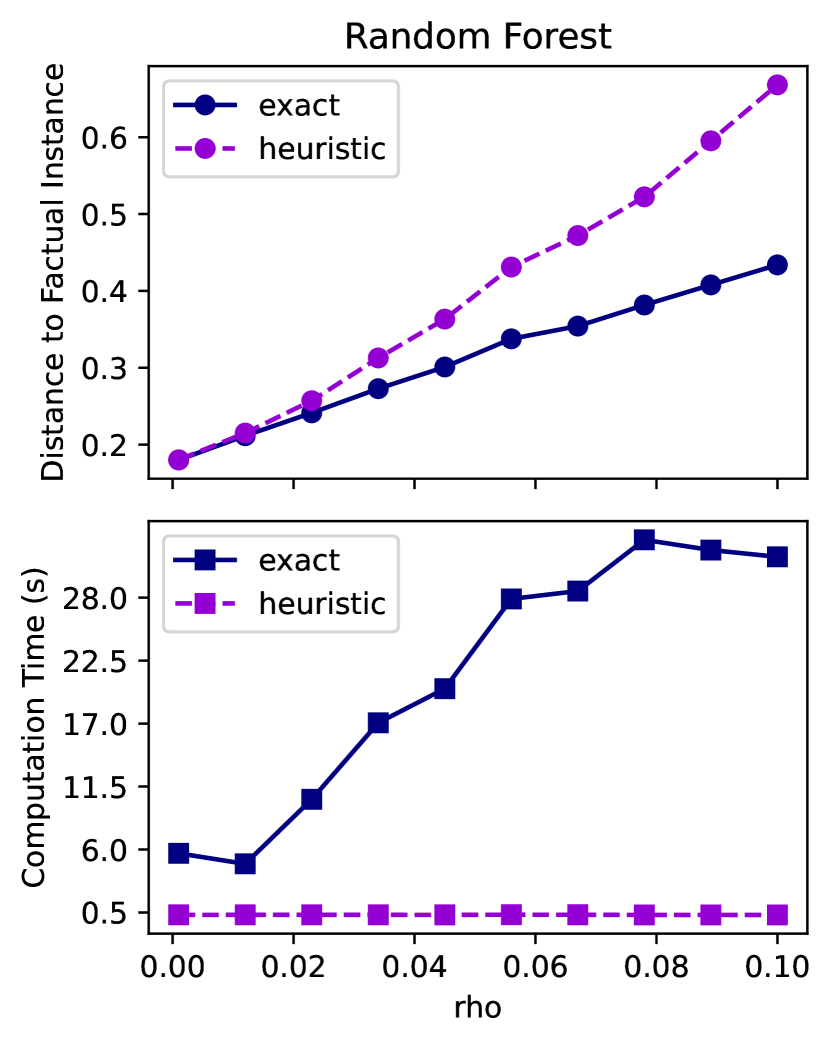

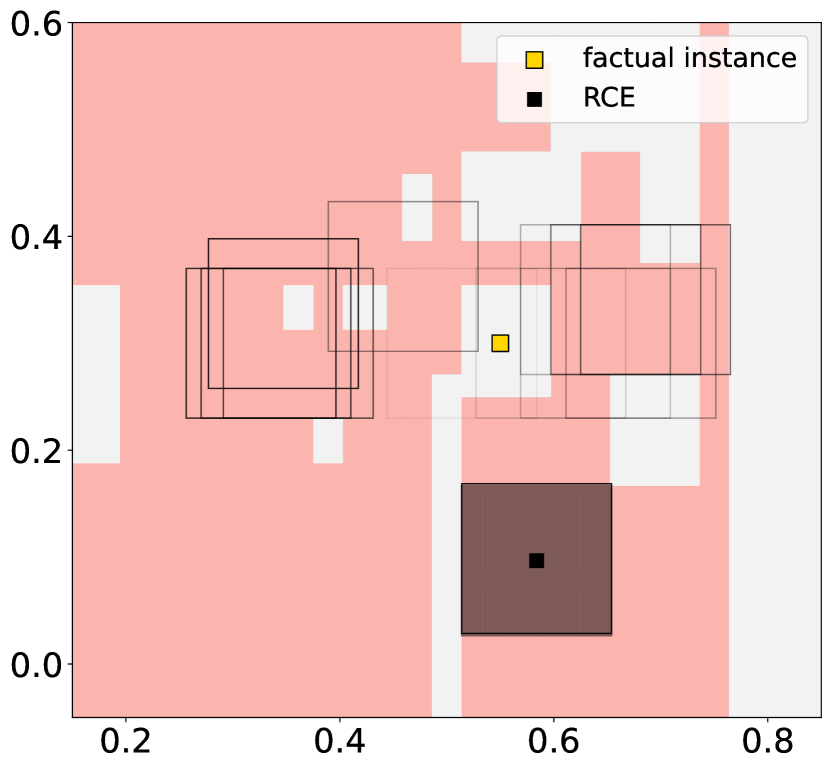

and choose the solution for the leaf which yields the best optimal value. Note that, in that case, we do not need binary assignment variables anymore, since we only consider one leaf for (MP). Alternatively, we can obtain the same result modelling the entire decision tree using auxiliary binary variables, one for each leaf with . In Figure 7, we present the computation time and the distance of the calculated CE to the factual instance using both the heuristic and the (exact) adversarial algorithm. The results show that the heuristic approach outperforms the exact method in terms of speed, and its computation time remains unaffected by the robustness budget . However, it is noteworthy that the CEs generated through the heuristic method have a larger distance to the factual instance where the difference to the optimal distance provided by our exact algorithm increases with increasing .

3.2 Tree Ensembles

In the case of tree ensembles like random forest (RF) and gradient boosting machines (GBM), we model the validity constraints by formulating each base learner separately. Assume we obtain base learners. Since each base learner is a decision tree, we can use the construction of the constraints (21)-(25) and apply them to all base learners separately. Then, we add the constraints to the master problem, where each base learner gets a separate copy of the assignment variables and has its own set of node inequalities given by and . Additionally, we have to replace constraint (24) by

| (40) |

where is the weight of leaf in base learner . This constraint forces the average prediction value of the tree ensemble to be larger than or equal to . Note that to model a majority vote, we can use . Since a random forest is equivalent to a decision tree, the same methodology for (AP) can be used as in Section 3.1. Note that for classical DTs we may iterate over all leaves and solve Problem (31). However, deriving the polyhedral descriptions of all leaves for an ensemble of trees is very time consuming. Instead (AP) can be reformulated as

| maximize | (41) | |||

| subject to | (42) | |||

| (43) | ||||

| (44) | ||||

| (45) |

where contain the split parameters of the nodes of tree as defined in Section 3.1 and we use to denote the set of the first positive integers, that is .

Finally, note that since the classifier of an ensemble of trees is equivalent to a classical decision tree classifier, the convergence analysis presented in Section 3.1 holds also for the ensemble case.

3.3 Neural Networks

In the case of neural networks convergence of Algorithm 1 is immediately guaranteed when we consider ReLU activation functions. More precisely, the evaluation function of a trained neural network with rectified linear unit (ReLU) activation functions is Lipschitz continuous, since it is a concatenation of Lipschitz continuous functions; see Appendix 8 for a formal proof.

Moreover, neural networks with ReLU activation functions belong to the MIP-representable class of ML models (Grimstad and Andersson 2019, Anderson et al. 2020), and we adopt the formulation proposed by Fischetti and Jo (2018). The ReLU operator of a neuron in layer is given by

| (46) |

where is the coefficient vector for neuron in layer , is the bias value and is the output of neuron of layer . Note that in our model the input of the neural network can be a data point perturbed by a scenario , i.e., all variables depend on the perturbation . The input in the first layer is and the output of layer is denoted as . The ReLU operator (46) can then be linearly reformulated as

| (47) | ||||

| (48) | ||||

| (49) | ||||

| (50) | ||||

| (51) |

where and are big-M values.

The following is a complete formulation of the master problem (MP) in the case of neural networks with ReLU activation functions:

| (52) | ||||

| subject to | (53) | |||

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) | ||||

| (59) |

where represents the number of layers with and the set of neurons in layer . The first layers are activated by a ReLU function except for the output layer, which consists of a single node that is a linear combination of the node values in layer . The variable is the output of the activation function in node , layer , and scenario .

4 Experiments

In this section, we aim to illustrate the effectiveness of our method by conducting empirical experiments on various datasets. The mixed-integer optimization formulations of the ML models used in our experiments are based on Maragno et al. (2021). In our experiments, we consistently set to 1e-7 and utilize a big value of 1e3 for decision trees and tree ensembles, while for neural networks, we employ a big value of 100. The experiments were conducted on a computer with an Apple M1 Pro processor and 16 GB of RAM. For reproducibility, our open-source implementation can be found at our repository333https://github.com/donato-maragno/robust-CE. It is important to note that, to the best of our knowledge, the present work is the first approach that generates a region of CEs for a range of different models, involving non-differentiable models. Therefore, a comparison to prior work is only possible for the case of neural networks with ReLU activation functions. In the last part of the experiments, we compare our method against the one proposed by Dominguez-Olmedo et al. (2021) in terms of CE validity and robustness.

| BANKNOTE AUTHENTICATION | DIABETES | IONOSPHERE | ||||||||

| 4 features | 8 features | 34 features | ||||||||

| Model | Specs | Comp. time (s) | # iterations | # early stops | Comp. time (s) | # iterations | # early stops | Comp. time (s) | # iterations | # early stops |

| Linear | ElasticNet | 0.25 (0.01) | – | – | 0.23 (0.01) | – | – | 0.25 (0.01) | – | – |

| max depth: 3 | 1.53 (0.04) | 1.00 (0.00) | – | 1.66 (0.07) | 1.20 (0.09) | – | 1.66 (0.07) | 1.10 (0.07) | – | |

| max depth: 5 | 1.86 (0.09) | 1.10 (0.07) | – | 2.29 (0.11) | 1.20 (0.09) | – | 1.96 (0.08) | 1.10 (0.07) | – | |

| DT | max depth: 10 | 3.90 (0.88) | 2.00 (0.58) | – | 5.77 (0.48) | 1.40 (0.13) | – | 2.86 (0.16) | 1.20 (0.09) | – |

| # est.: 5 | 3.50 (0.36) | 1.75 (0.22) | – | 5.89 (1.98) | 2.60 (0.83) | – | 3.79 (0.24) | 1.70 (0.13) | – | |

| # est.: 10 | 6.74 (1.03) | 2.60 (0.40) | – | 7.20 (0.94) | 2.35 (0.29) | – | 8.76 (0.89) | 2.85 (0.33) | – | |

| # est.: 20 | 21.21 (4.61) | 4.55 (0.99) | – | 33.55 (7.48) | 6.15 (0.79) | – | 22.33 (2.83) | 4.40 (0.51) | – | |

| # est.: 50 | 115.79 (34.35) | 7.80 (1.65) | – | 110.24 (32.43) | 6.47 (1.39) | 3 ( = 0.007) | 137.26 (33.37) | 8.20 (1.20) | – | |

| RF∗ | # est.: 100 | 214.38 (65.07) | 6.44 (1.31) | 2 ( = 0.009) | 274.09 (71.93) | 8.87 (1.49) | 5 ( = 0.004) | 285.62 (95.57) | 8.27 (2.02) | 9 ( = 0.004) |

| # est.: 5 | 2.70 (0.22) | 1.20 (0.14) | – | 2.76 (0.22) | 1.85 (0.17) | – | 2.37 (0.15) | 1.60 (0.13) | – | |

| # est.: 10 | 3.20 (0.30) | 1.45 (0.15) | – | 2.72 (0.29) | 1.50 (0.24) | – | 4.35 (0.44) | 2.75 (0.30) | – | |

| # est.: 20 | 5.94 (0.50) | 2.60 (0.23) | – | 4.25 (0.45) | 2.15 (0.28) | – | 9.01 (1.11) | 3.85 (0.50) | – | |

| # est.: 50 | 18.38 (1.62) | 4.05 (0.35) | – | 24.60 (8.21) | 5.85 (1.41) | – | 81.33 (28.39) | 8.90 (1.36) | – | |

| GBM∗∗ | # est.: 100 | 87.11 (26.24) | 7.28 (0.77) | 2 ( = 0.006) | 164.32 (42.12) | 11.63 (2.00) | 1 ( = 0.004) | 137.98 (22.74) | 10.33 (0.97) | 2 ( = 0.007) |

| (10,) | 1.63 (0.04) | 1.00 (0.00) | – | 1.55 (0.06) | 1.00 (0.00) | – | 2.22 (0.19) | 1.80 (0.21) | – | |

| (10, 10, 10) | 2.98 (0.15) | 1.15 (0.08) | – | 2.40 (0.12) | 1.15 (0.08) | – | 13.01 (3.57) | 2.30 (0.40) | – | |

| (50,) | 2.60 (0.14) | 1.00 (0.00) | – | 2.09 (0.12) | 1.05 (0.05) | – | 5.75 (0.75) | 1.20 (0.12) | – | |

| NN | (100,) | 3.53 (0.15) | 1.00 (0.00) | – | 4.36 (0.62) | 1.10 (0.07) | – | 61.31 (33.11) | 1.50 (0.22) | 10 ( = 0.000) |

| Linear | ElasticNet | 0.13 (0.00) | – | – | 0.15 (0.01) | – | – | 0.14 (0.00) | – | – |

| max depth: 3 | 1.00 (0.06) | 1.70 (0.15) | – | 1.09 (0.07) | 1.60 (0.15) | – | 1.02 (0.07) | 1.30 (0.15) | – | |

| max depth: 5 | 1.18 (0.11) | 1.80 (0.22) | – | 1.63 (0.13) | 2.05 (0.22) | – | 1.33 (0.10) | 1.60 (0.18) | – | |

| DT | max depth: 10 | 2.22 (0.41) | 2.95 (0.61) | – | 8.84 (1.49) | 4.45 (0.59) | – | 3.68 (2.14) | 2.95 (1.49) | – |

| # est.: 5 | 2.85 (0.47) | 3.25 (0.54) | – | 4.29 (0.73) | 5.25 (0.86) | – | 2.27 (0.19) | 2.35 (0.23) | – | |

| # est.: 10 | 13.51 (3.03) | 8.95 (1.60) | – | 14.71 (3.53) | 8.35 (1.24) | – | 7.41 (1.22) | 5.15 (0.67) | – | |

| # est.: 20 | 13.86 (3.58) | 5.53 (0.92) | 1 ( = 0.041) | 89.00 (28.17) | 14.00 (2.28) | 2 ( = 0.045) | 47.44 (26.35) | 9.50 (2.52) | – | |

| # est.: 50 | 101.21 (24.90) | 11.37 (1.53) | 1 ( = 0.048) | 303.27 (93.95) | 16.73 (2.55) | 9 ( = 0.034) | 307.72 (72.52) | 19.31 (3.15) | 7 ( = 0.044) | |

| RF∗ | # est.: 100 | 156.28 (33.21) | 8.70 (1.02) | – | 453.67 (111.27) | 15.43 (2.19) | 13 ( = 0.032) | 156.45 (116.11) | 5.75 (2.29) | 16 ( = 0.029) |

| # est.: 5 | 1.57 (0.15) | 1.75 (0.24) | – | 1.50 (0.10) | 2.05 (0.20) | – | 1.97 (0.32) | 2.65 (0.50) | – | |

| # est.: 10 | 4.84 (0.58) | 3.55 (0.46) | – | 8.87 (4.44) | 8.55 (3.21) | – | 11.76 (6.51) | 8.85 (3.27) | – | |

| # est.: 20 | 12.72 (2.22) | 8.28 (0.85) | 2 ( = 0.038) | 41.81 (17.86) | 17.05 (4.37) | 1 ( = 0.025) | 19.20 (6.32) | 9.45 (1.80) | – | |

| # est.: 50 | 73.23 (27.00) | 13.76 (1.82) | 3 ( = 0.039) | 223.87 (125.98) | 19.86 (4.23) | 13 ( = 0.027) | 139.18 (56.80) | 16.31 (3.03) | 7 ( = 0.023) | |

| GBM∗∗ | # est.: 100 | 274.22 (51.40) | 17.25 (1.57) | 4 ( = 0.040) | – | – | 20 ( = 0.022) | 537.13 (295.04) | 15.00 (2.08) | 17 ( = 0.022) |

| (10,) | 0.90 (0.01) | 1.00 (0.00) | – | 1.00 (0.04) | 1.15 (0.08) | – | 2.96 (0.23) | 3.00 (0.25) | – | |

| (10, 10, 10) | 1.48 (0.03) | 1.00 (0.00) | – | 2.02 (0.26) | 1.65 (0.21) | – | 229.69 (104.80) | 4.90 (0.67) | 10 ( = 0.039) | |

| (50,) | 1.39 (0.06) | 1.00 (0.00) | – | 1.75 (0.13) | 1.35 (0.11) | – | 19.06 (6.63) | 2.37 (0.24) | 1 ( = 0.049) | |

| NN | (100,) | 1.83 (0.05) | 1.00 (0.00) | – | 5.88 (1.19) | 1.80 (0.16) | – | 289.62 (125.61) | 2.70 (0.30) | 10 ( = 0.000) |

| * max depth of each decision tree equal to 3.; ** max depth of each decision tree equal to 2. | ||||||||||

| BANKNOTE AUTHENTICATION | DIABETES | IONOSPHERE | ||||||||

| 4 features | 8 features | 34 features | ||||||||

| Model | Specs | Comp. time (s) | # iterations | # early stops | Comp. time (s) | # iterations | # early stops | Comp. time (s) | # iterations | # early stops |

| Linear | ElasticNet | 0.24 (0.01) | – | – | 0.24 (0.01) | – | – | 0.26 (0.01) | – | – |

| max depth: 3 | 2.09 (0.11) | 1.45 (0.11) | – | 2.18 (0.13) | 1.70 (0.15) | – | 5.54 (0.38) | 1.20 (0.09) | – | |

| max depth: 5 | 2.64 (0.14) | 1.53 (0.12) | 1 ( = 0.000) | 4.21 (0.39) | 2.00 (0.23) | – | 10.17 (0.78) | 1.56 (0.16) | 4 ( = 0.000) | |

| DT | max depth: 10 | 4.61 (0.88) | 2.70 (0.58) | – | 14.17 (2.64) | 2.63 (0.50) | 1 ( = 0.000) | 21.75 (2.58) | 2.06 (0.26) | 2 ( = 0.000) |

| # est.: 5 | 5.20 (0.62) | 2.35 (0.34) | – | 7.96 (1.65) | 3.17 (0.55) | 2 ( = 0.004) | 69.94 (10.77) | 4.41 (0.54) | 3 ( = 0.006) | |

| # est.: 10 | 10.83 (2.68) | 3.41 (0.78) | 3 ( = 0.006) | 15.20 (3.17) | 4.20 (0.68) | – | 237.03 (41.12) | 5.50 (0.70) | 4 ( = 0.003) | |

| # est.: 20 | 22.59 (7.10) | 4.15 (1.22) | 7 ( = 0.004) | 104.42 (27.35) | 9.81 (1.78) | 4 ( = 0.007) | 370.21 (41.84) | 7.33 (0.73) | 5 ( = 0.004) | |

| # est.: 50 | 61.93 (14.29) | 3.89 (1.22) | 11 ( = 0.004) | 137.37 (39.96) | 6.50 (1.51) | 10 ( = 0.004) | 570.88 (111.94) | 9.70 (1.61) | 10 ( = 0.001) | |

| RF∗ | # est.: 100 | 103.33 (31.75) | 3.20 (0.89) | 10 ( = 0.004) | 177.47 (41.01) | 3.80 (0.86) | 15 ( = 0.002) | 531.13 (121.00) | 6.17 (0.98) | 14 ( = 0.001) |

| # est.: 5 | 4.50 (0.50) | 2.50 (0.34) | – | 4.67 (0.47) | 2.45 (0.26) | – | 11.47 (1.48) | 4.42 (0.66) | 8 ( = 0.002) | |

| # est.: 10 | 6.87 (0.88) | 3.15 (0.42) | – | 6.11 (1.04) | 2.70 (0.48) | – | 42.68 (6.67) | 6.88 (0.86) | 3 ( = 0.001) | |

| # est.: 20 | 14.02 (1.09) | 4.40 (0.34) | – | 10.97 (1.45) | 3.65 (0.49) | – | 58.16 (7.01) | 9.62 (1.00) | 4 ( = 0.004) | |

| # est.: 50 | 34.03 (3.15) | 5.21 (0.44) | 1 ( = 0.010) | 76.04 (33.09) | 9.35 (2.21) | – | 192.70 (42.52) | 14.77 (2.47) | 7 ( = 0.006) | |

| GBM∗∗ | # est.: 100 | 133.53 (24.40) | 8.50 (0.98) | 6 ( = 0.007) | 201.13 (77.68) | 12.08 (2.92) | 8 ( = 0.005) | 415.96 (80.09) | 17.29 (3.36) | 13 ( = 0.003) |

| (10,) | 1.64 (0.09) | 1.00 (0.00) | – | 1.73 (0.05) | 1.00 (0.00) | – | 4.73 (0.57) | 1.27 (0.19) | 9 ( = 0.004) | |

| (10, 10, 10) | 2.54 (0.15) | 1.00 (0.00) | – | 2.04 (0.10) | 1.00 (0.00) | 6 ( = 0.000) | 282.24 (193.65) | 1.50 (0.50) | 18 ( = 0.003) | |

| (50,) | 2.42 (0.14) | 1.00 (0.00) | – | 2.00 (0.08) | 1.00 (0.00) | 1 ( = 0.000) | 48.13 (12.76) | 2.40 (0.51) | 15 ( = 0.008) | |

| NN | (100,) | 3.57 (0.14) | 1.00 (0.00) | – | 5.28 (0.83) | 1.15 (0.11) | – | 352.64 (153.96) | 1.09 (0.09) | 9 ( = 0.000) |

| Linear | ElasticNet | 0.15 (0.00) | – | – | 0.34 (0.02) | – | – | 0.26 (0.01) | – | – |

| max depth: 3 | 1.72 (0.17) | 2.25 (0.19) | – | 6.71 (0.65) | 2.40 (0.24) | – | 4.40 (1.35) | 2.60 (0.90) | – | |

| max depth: 5 | 2.69 (0.52) | 3.95 (0.74) | 1 ( = 0.026) | 20.28 (2.88) | 5.00 (0.68) | 1 ( = 0.000) | 5.91 (1.09) | 2.26 (0.40) | 1 ( = 0.000) | |

| DT | max depth: 10 | 4.44 (0.80) | 4.95 (0.93) | – | 178.35 (34.48) | 9.11 (1.30) | 1 ( = 0.045) | 20.91 (10.20) | 5.05 (1.51) | – |

| # est.: 5 | 4.49 (0.64) | 4.40 (0.64) | – | 117.95 (28.96) | 9.63 (1.82) | 1 ( = 0.049) | 28.79 (2.76) | 6.35 (0.51) | – | |

| # est.: 10 | 12.39 (2.57) | 6.82 (1.14) | 3 ( = 0.048) | 200.39 (69.46) | 12.92 (2.93) | 7 ( = 0.043) | 232.63 (36.46) | 10.79 (1.36) | 1 ( = 0.042) | |

| # est.: 20 | 51.29 (18.03) | 10.17 (2.32) | 8 ( = 0.049) | 149.39 (46.57) | 12.75 (2.78) | 12 ( = 0.042) | 450.46 (68.06) | 8.50 (1.06) | 10 ( = 0.027) | |

| # est.: 50 | 93.18 (51.21) | 7.78 (2.17) | 11 ( = 0.048) | 560.78 (–) | 6.00 (–) | 19 ( = 0.031) | 510.69 (341.34) | 7.50 (3.50) | 18 ( = 0.021) | |

| RF∗ | # est.: 100 | 108.47 (29.76) | 5.25 (0.80) | 8 ( = 0.047) | 868.10 (–) | 4.00 (–) | 19 ( = 0.024) | 495.03 (268.88) | 9.00 (2.08) | 17 ( = 0.014) |

| # est.: 5 | 2.67 (0.33) | 3.55 (0.47) | – | 8.89 (1.29) | 3.68 (0.53) | 1 ( = 0.000) | 11.38 (1.83) | 5.74 (0.68) | 1 ( = 0.029) | |

| # est.: 10 | 5.77 (0.45) | 5.55 (0.44)) | – | 46.46 (14.33) | 12.00 (3.12) | – | 72.15 (15.31) | 15.19 (2.62) | 4 ( = 0.005) | |

| # est.: 20 | 23.89 (3.55) | 10.41 (1.00) | 3 ( = 0.046) | 153.43 (43.11) | 18.76 (3.73) | 3 ( = 0.036) | 156.17 (19.16) | 16.42 (1.71) | 8 ( = 0.005) | |

| # est.: 50 | 123.75 (51.10) | 18.14 (4.47) | 6 ( = 0.044) | 243.24 (80.72) | 24.50 (6.31) | 14 ( = 0.029) | 894.23 (100.35) | 32.50 (6.50) | 18 ( = 0.013) | |

| GBM∗∗ | # est.: 100 | 389.06 (124.83) | 20.25 (3.32) | 12 ( = 0.044) | – (–) | – (–) | 20 ( = 0.020) | – (–) | – (–) | 20 ( = 0.010) |

| (10,) | 0.91 (0.00) | 1.00 (0.00) | – | 4.13 (0.13) | 1.00 (0.00) | – | 36.34 (5.22) | 1.68 (0.19) | 1 ( = 0.000) | |

| (10, 10, 10) | 1.45 (0.03) | 1.00 (0.00) | – | 8.02 (0.86) | 1.31 (0.18) | 4 ( = 0.024) | 328.70 (72.59) | 2.38 (0.35) | 4 ( = 0.012) | |

| (50,) | 1.36 (0.03) | 1.00 (0.00) | – | 11.27 (1.10) | 1.50 (0.15) | – | 57.07 (7.28) | 1.22 (0.10) | 2 ( = 0.000) | |

| NN | (100,) | 2.26 (0.04) | 1.00 (0.00) | – | 26.82 (3.39) | 1.30 (0.13) | – | 111.85 (26.18) | 1.44 (0.24) | 11 ( = 0.001) |

| * max depth of each decision tree equal to 3.; ** max depth of each decision tree equal to 2. | ||||||||||

In the first part of the experiments, we analyze our method using three well-known datasets: Banknote Authentication, Diabetes, and Ionosphere (Dua and Graff 2017). Before training the ML models, we scaled each feature to be between zero and one. None of the datasets contain categorical features, which otherwise would have been considered immutable or fixed according to the user’s preference. We apply our algorithm to generate robust CEs for 20 factual instances randomly selected from the dataset. We use -norm as uncertainty set with a radius () of 0.01 and 0.05. The distance function adopted is the -norm, which can be linearly expressed within the optimization model. For each instance, we use a time limit of 1000 seconds. Although less practical from a user’s perspective, we also report the results using -norm as uncertainty set in Table 2. The datasets used in our analysis do not require any additional constraints, such as actionability, sparsity, or data manifold closeness. However, it is important to note that these types of constraints can be added to our master problem when needed by using constraints like the ones proposed in (Maragno et al. 2022). The accuracy of each trained ML model is provided in Appendix 9.

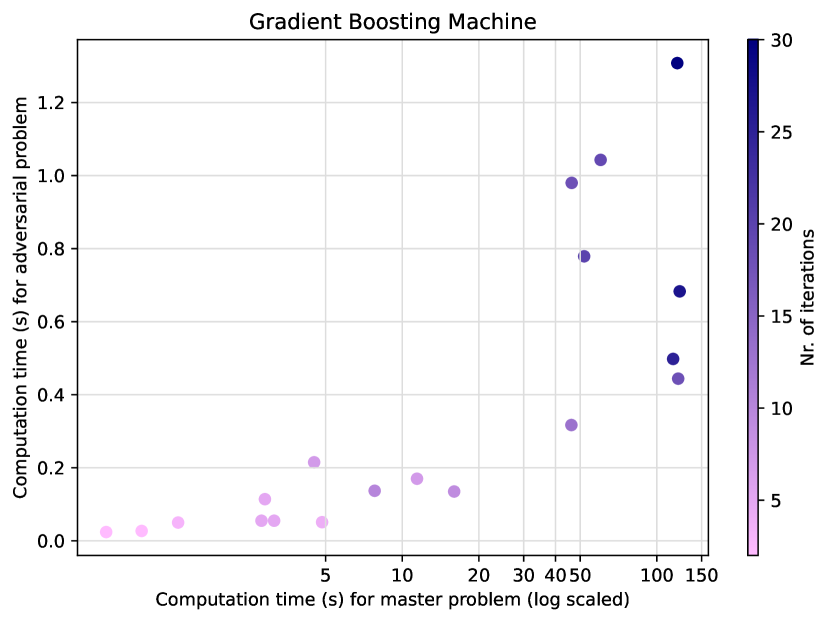

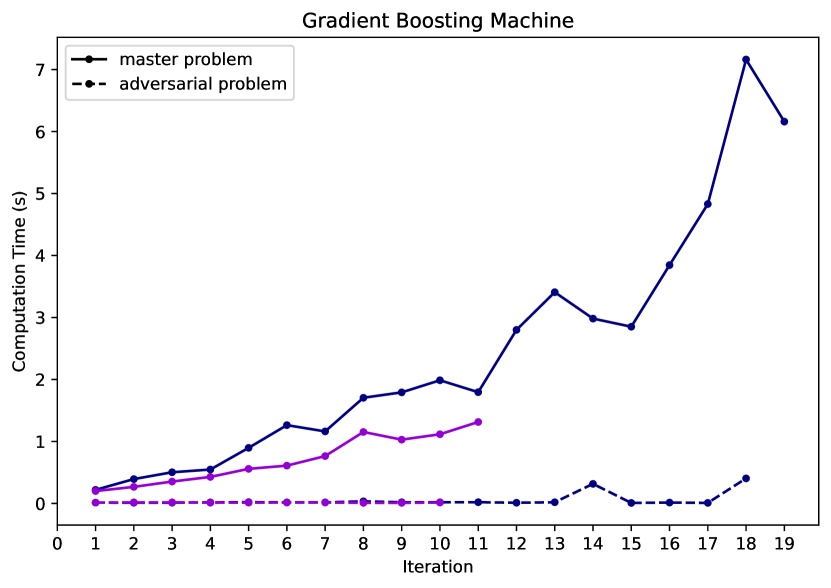

In Table 1, we show (from left to right) the type of ML model, model-specific hyperparameters, and for each dataset, the average computation time (in seconds), the number of iterations performed by the algorithm, and the number of instances where the algorithm hits the time limit without providing an optimal solution. For the computation time and the number of iterations, we show the standard error values in parentheses. For the early stops, we show the (average) maximum radius of the uncertainty set, which is feasible for the generated counterfactual solutions in each iteration of the algorithm. The latter value gives a measure for the robustness of the returned solution. As for hyperparameters, we report the maximum tree depth for DT, the number of generated trees for RF and GBM, and the depth of each layer in the NN. The results indicate that the computation time and the number of iterations increase primarily due to the complexity of the ML models rather than the number of features in the datasets. We further inspect the computation time by looking at the time needed to solve the MP and AP at each iteration. To do so, we use the Diabetes dataset and train a GBM with 100 estimators. In Figure 9(a) we plot the overall computation time of the AP versus the overall computation time of the MP for 20 instances. In Figure 9(b) we inspect the time required per iteration for two of those instances. We can see that the time required to solve the AP remains small and stable while the time required to solve the MP increases exponentially with each iteration, i.e., as more scenarios are added.

Decision trees tend to overfit as their depth increases. In Figure 10, we show iterations for a decision tree with maximum depths of (a) 10 and (b) 3. We observe that the more complex model substantially increases the number of iterations, and hence the computation time.

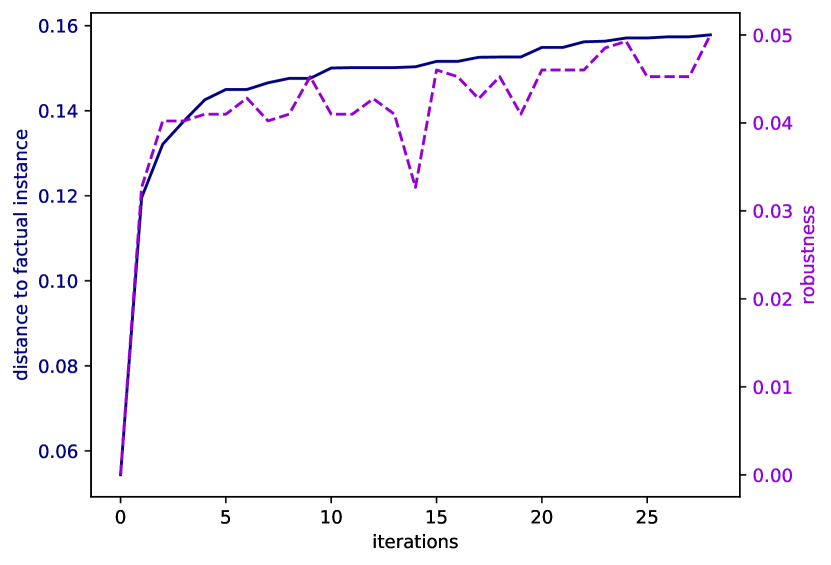

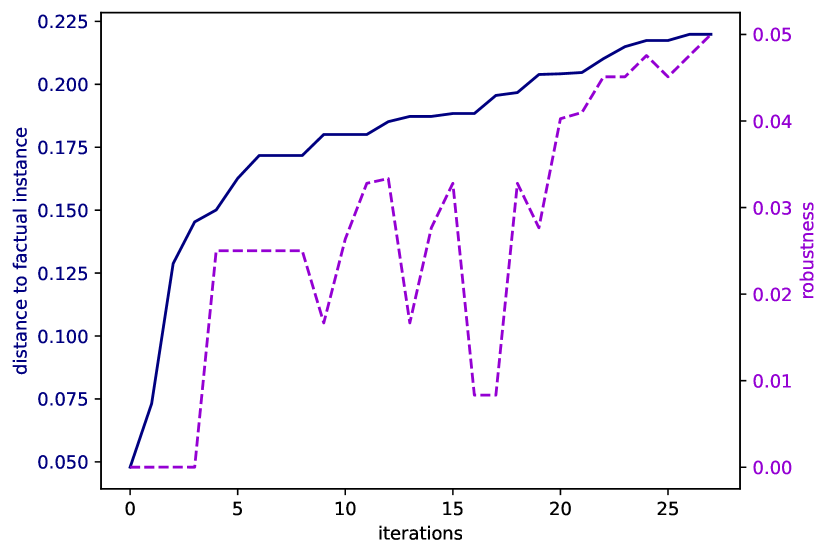

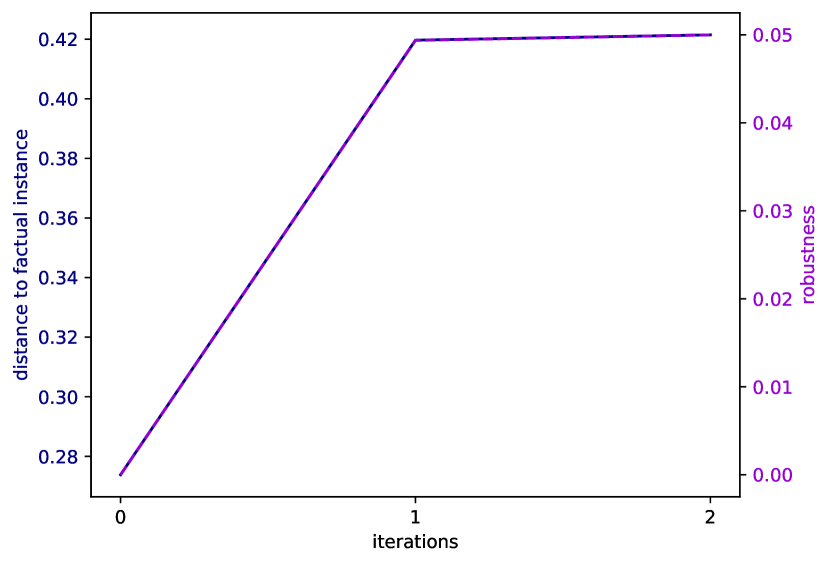

When the time limit is reached, we can still provide a list of solutions generated by solving the (MP) at each iteration. Each one of these solutions comes with information on the distance to the actual instance and the radius of the uncertainty set for which the model predictions still belong to the desired class for all perturbations. Therefore, the decision-makers still have the chance to select CEs from a region, albeit slightly smaller than intended. Overall the algorithm converges relatively quickly, however, our experiments show that it converges slower when using -norm as uncertainty set; see Table 2. Furthermore, as expected, for a smaller radius of we reach the global optimum faster. Figure 11 shows the convergence behavior of various predictive models trained on the Diabetes dataset and evaluated on a specific instance. Although the distance to the factual instance (solid line) follows a monotonic increasing trend, the robustness (dashed line) exhibits both peaks and troughs. This behavior can be attributed to the objective function of (MP), which seeks to minimize the distance between the CE and the factual instance. With each iteration of our algorithm, a new scenario/constraint is introduced to (MP), resulting in a worse objective value (higher), but not necessarily an improvement in robustness.

In the latter part of the experiment, we train a neural network with one hidden layer containing 50 nodes using the same three datasets. For the Ionosphere dataset, we also trained another neural network with one hidden layer containing 10 nodes. To generate robust counterfactuals, we used the -norm uncertainty set and tested our algorithm against the one proposed by Dominguez-Olmedo et al. (2021) on 10 instances. In Table 3, we report the percentage of times each algorithm was able to find a counterfactual that was at least distant from the decision boundary (robustness) and the percentage of times the counterfactual was valid (validity). We test values of 0.1 and 0.2 for each dataset. Our approach consistently generated counterfactual explanations that were optimal in terms of distance to the factual instance and valid. In the Diabetes dataset, our algorithm reached the time limit without finding a counterfactual with robustness of at least 0.2 in 20% of cases. Nevertheless, the generated counterfactuals were still valid, with a value smaller than 0.2. In contrast, the algorithm proposed by Dominguez-Olmedo et al. (2021) often returned solutions that were not entirely robust with respect to , particularly with the increase in and the complexity of the predictive model. Even more concerning, their algorithm generated invalid solutions in 10% of the cases for the Ionosphere dataset. Note that our experiments only cover neural network models since the method in (Dominguez-Olmedo et al. 2021) cannot be used for non-differentiable predictive models.

| Dominguez-Olmedo et al. (2021) | Our algorithm | |||

| robustness | validity | robustness | validity | |

| Banknote NN(50) | ||||

| 0.1 | 80% | 100% | 100% | 100% |

| 0.2 | 0% | 100% | 100% | 100% |

| Diabetes NN(50) | ||||

| 0.1 | 60% | 100% | 100% | 100% |

| 0.2 | 0% | 100% | 80% | 100% |

| Ionosphere NN(10) | ||||

| 0.1 | 70% | 90% | 100% | 100% |

| 0.2 | 40% | 90% | 100% | 100% |

| Ionosphere NN(50) | ||||

| 0.1 | 50% | 100% | 100% | 100% |

| 0.2 | 30% | 100% | 100% | 100% |

5 Discussion and Future Work

In this paper, we propose a robust optimization approach for generating regions of CEs for tree-based models and neural networks. We have also shown theoretically that our approach converges. This result has also been supported by empirical studies on different datasets. Our experiments demonstrate that our approach is able to generate explanations efficiently on a variety of datasets and ML models. Our results indicate that the proposed method scales well with the number of features and that the main computational challenge lies in solving the master problem as it becomes larger with every iteration. Overall, our results suggest that our proposed approach is a promising method for generating robust CEs for a variety of machine learning models.

As future work, we plan to investigate methods for speeding up the calculations of the master problem by using more efficient formulations of the predictive models, such as the one proposed by Parmentier and Vidal (2021) for tree-based models. Additionally, we aim to evaluate the user perception of the robust CEs generated by our approach and investigate how the choice of the uncertainty set affects the quality of the solution. Another research direction is the implementation of categorical and immutable features into the model. In the current version, categorical features are considered immutable, following user preferences. Adhering to user preferences by keeping some feature values constant, whether they are categorical or numerical, offers a practical strategy for generating sparse counterfactual explanations. This approach assumes that only a subset of the features (the ones that are not considered immutable) is susceptible to perturbations. Considering mutable categorical features would require a reformulation of the uncertainty set to account for the different feature types. This would lead to non-convex, discrete, and lower-dimensional uncertainty sets. However, this change would only affect the adversarial problem, while the master problem remains the same.

This work was supported by the Dutch Scientific Council (NWO) grant OCENW.GROOT.2019.015, Optimization for and with Machine Learning (OPTIMAL).

6 How to choose the robustness budget

When determining the robustness budget , it is essential to weigh the balance between the distance of the resulting CE to the factual instance and its robustness against small perturbations. When the underlying distribution of the CE perturbations is known, we can select such that a certain probabilistic guarantee is satisfied. However, in many real-world situations, we do not have access to distributional information regarding the perturbations. In this case, decision-makers can derive a Pareto front based on the CE’s proximity to the factual instance and its robustness against changes.

6.1 Probability guarantee

Probability guarantees regarding the invalidation of recourse depend on both the specific predictive model and the type of uncertainty set in use. For a comprehensive overview of robust reformulations with probabilistic guarantees in the context of linear models, we refer to (Ben-Tal et al. 2009b). In this section, we present a more generic formulation that is applicable to both linear and nonlinear models. However, it should be noted that it is a more conservative approach since it only considers the probability that the realized recourse will be in the uncertainty set while (large) part(s) of the uncertainty set may not be near the decision boundary, depending on the model structure.

If we assume that the realized/actual perturbation is distributed according to , where is the identity matrix, then we can approach the probabilistic guarantee from three angles:

-

1.

What is the probability () that the realized recourse is in the defined uncertainty set , given and ?

-

2.

What value of is required to have probability that the realized recourse is in the uncertainty set , given and ?

-

3.

How large can the standard deviation of the perturbations () be to have probability of the realized recourse being in the uncertainty set , given and ?

These answers depend on the chosen norm for the uncertainty set. Note that a prediction region with probability for is given by (Chew 1966), such that for the norm the questions above boil down to

| (68) | |||

| (69) | |||

| (70) |

where and is the quantile-function for the probability for the chi-square distribution with degrees of freedom, is the dimension (number of features) of , and is the cumulative distribution function for the chi-square distribution with degrees of freedom.

For the -norm, first note that is a vector of i.i.d. variables. The probability that the realized recourse is in the defined uncertainty set for this norm is then equal to the probability that all variables are between and , i.e.: , where represents the standard normal cumulative distribution function. Equating to then yields:

| (71) | |||

| (72) | |||

| (73) |

where represents the inverse of the standard normal cumulative distribution function.

6.2 Pareto front

The Pareto front represents a set of CE solutions that cannot be improved in one objective without degrading performance in the other. In our context:

-

•

Objective 1: Proximity of the CE to the Factual Instance – This measures the -norm distance between the CE and the factual instance.

-

•

Objective 2: Robustness () - This quantifies the robustness of the CE against perturbations.

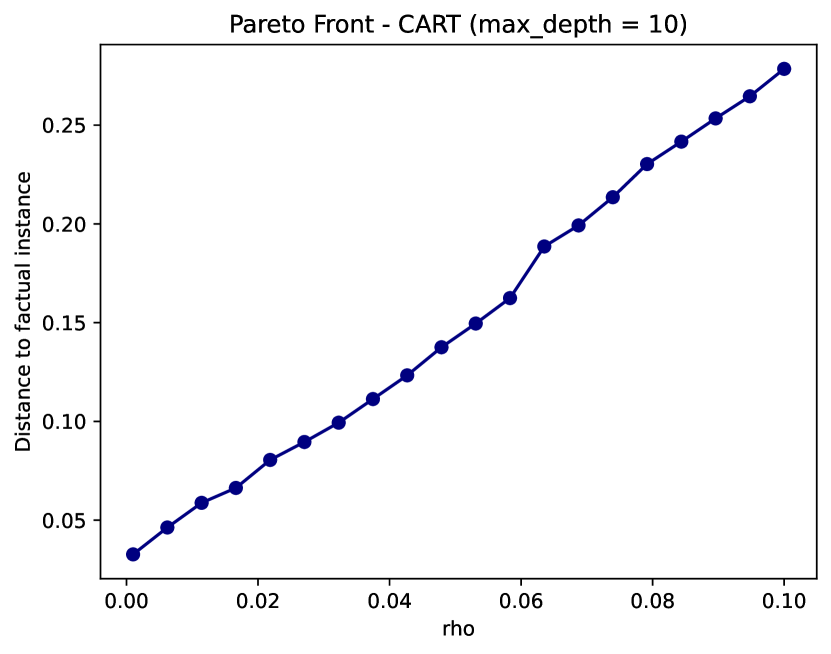

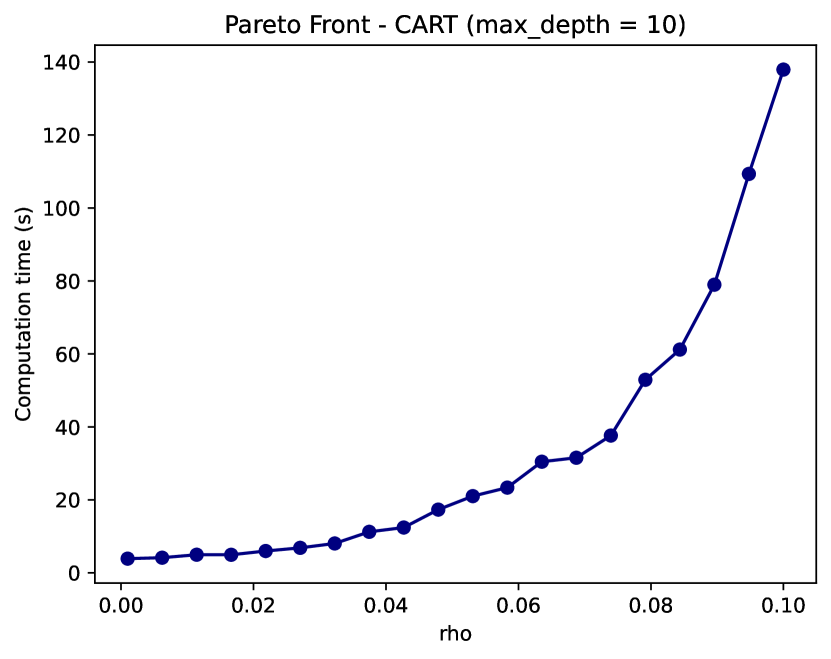

In Figure 12(a), we report the Pareto front for a decision tree with a max depth of 10 and -norm uncertainty set. The outcomes are averaged across 20 different cases. When we increase the value of , the distance to the factual instance also increases, occasionally experiencing jumps, see for example the jump in distance for values of around 0.06, which can be attributed to changes in the leaf nodes. Also, the computation time increases with given the increasing difficulty in finding a region that is large enough to contain the -robust CE, see Figure 12(b).

7 Linear Models

Although Algorithm 1 could still be used for the linear models, there is a well-known easier, and more efficient dual approach to solve model (3)-(4). We review this approach briefly here for the completeness of our discussion.

In the case of linear models, such as logistic regression (LR) or linear support vector machines (SVM), the validity constraint (4) can be formulated as

| (74) |

where is the coefficient vector and is the intercept. Then, these constraints can be equivalently reformulated as

Since is given in the form (5), the latter is equivalent to

| (75) |

where is the dual norm of the norm used in the definition of . The constant term ensures that the constraint (74) holds for all . Note that constraint (75) remains linear in independently of . For more details see, e.g., Dominguez-Olmedo et al. (2021), Bertsimas et al. (2019), Xu et al. (2008).

8 Proof of Lipschitz Continuity of Neural Networks

Suppose that we have a trained -layer neural network constructed with ReLU activation functions. If we denote the resulting functional by , then we can write

| (76) |

where , stands for the vectorized ReLU functions, and , for , are the weight matrices. This shows that is simply the composition of linear and component- as well as piece-wise linear functions.

Given any two Lipschitz continuous functions and with respective Lipschitz constants and , the composition is Lipschitz continuous with Lipschitz constant . This simply follows from observing for a pair of vectors that

| (77) |

Next, for any , we have

| (78) |

where is the spectral norm. As the Lipschitz constant for any vectorized ReLU function is one, we obtain the desired result by

| (79) |

for any pair . \Halmos

9 Performances of Predictive Models

| CART | RF | GBM | NN | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| LR | 3 | 5 | 10 | 5 | 10 | 20 | 50 | 100 | 5 | 10 | 20 | 50 | 100 | (10) | (10, 10, 10) | (50) | (100) | |

| Banknote | ||||||||||||||||||

| Train | 0.97 | 0.94 | 0.98 | 1.00 | 0.96 | 0.97 | 0.96 | 0.97 | 0.97 | 0.99 | 0.99 | 1.00 | 1.00 | 1.00 | 0.98 | 0.99 | 1.00 | 1.00 |

| Test | 0.96 | 0.89 | 1.00 | 1.00 | 0.96 | 0.93 | 0.93 | 0.96 | 0.93 | 0.96 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Diabetes | ||||||||||||||||||

| Train | 0.77 | 0.77 | 0.84 | 0.97 | 0.77 | 0.77 | 0.79 | 0.80 | 0.80 | 0.80 | 0.83 | 0.87 | 0.93 | 0.99 | 0.78 | 0.79 | 0.80 | 0.82 |

| Test | 0.72 | 0.77 | 0.72 | 0.69 | 0.72 | 0.69 | 0.69 | 0.67 | 0.71 | 0.59 | 0.67 | 0.69 | 0.59 | 0.62 | 0.69 | 0.64 | 0.73 | 0.77 |

| Ionosphere | ||||||||||||||||||

| Train | 0.88 | 0.93 | 0.97 | 1.00 | 0.93 | 0.95 | 0.94 | 0.96 | 0.96 | 0.99 | 1.00 | 1.00 | 1.00 | 1.00 | 0.98 | 0.99 | 0.99 | 0.99 |

| Test | 0.83 | 0.88 | 0.83 | 0.83 | 0.88 | 0.92 | 0.92 | 0.92 | 0.92 | 0.88 | 0.88 | 0.92 | 0.92 | 0.92 | 0.89 | 0.92 | 0.88 | 0.88 |

Table 4 displays the accuracy score of each predictive model employed in the experiments, with their performance being reported for both the training and testing sets.

References

- Anderson et al. (2020) Anderson R, Huchette J, Ma W, Tjandraatmadja C, Vielma JP (2020) Strong mixed-integer programming formulations for trained neural networks. Mathematical Programming 183(1-2):3–39, ISSN 14364646, URL http://dx.doi.org/10.1007/s10107-020-01474-5.

- Artelt et al. (2021) Artelt A, Vaquet V, Velioglu R, Hinder F, Brinkrolf J, Schilling M, Hammer B (2021) Evaluating robustness of counterfactual explanations. 2021 IEEE Symposium Series on Computational Intelligence (SSCI) 01–09, URL http://dx.doi.org/10.1109/ssci50451.2021.9660058.

- Ben-Tal et al. (2009a) Ben-Tal A, El Ghaoui L, Nemirovski A (2009a) Robust Optimization (Princeton University Press), ISBN 9781400831050, URL http://dx.doi.org/10.1515/9781400831050.

- Ben-Tal et al. (2009b) Ben-Tal A, Ghaoui L, Nemirovski A (2009b) Robust Optimization. ISBN 9781400831050, URL http://dx.doi.org/10.1515/9781400831050.

- Bertsimas et al. (2019) Bertsimas D, Dunn J, Pawlowski C, Zhuo YD (2019) Robust classification. INFORMS Journal on Optimization 1(1):2–34.

- Bertsimas et al. (2016) Bertsimas D, Dunning I, Lubin M (2016) Reformulation versus cutting-planes for robust optimization: A computational study. Computational Management Science 13:195–217.

- Bienstock and Özbay (2008) Bienstock D, Özbay N (2008) Computing robust basestock levels. Discrete Optimization 5(2):389–414.

- Black et al. (2021) Black E, Wang Z, Fredrikson M, Datta A (2021) Consistent counterfactuals for deep models. URL http://dx.doi.org/10.48550/ARXIV.2110.03109.

- Bui et al. (2022) Bui N, Nguyen D, Nguyen VA (2022) Counterfactual plans under distributional ambiguity.

- Carrizosa et al. (2021) Carrizosa E, Ramırez-Ayerbe J, Morales DR (2021) Generating collective counterfactual explanations in score-based classification via mathematical optimization. Generating Collective Counterfactual Explanations in Score-Based Classification via Mathematical Optimization .

- Chew (1966) Chew V (1966) Confidence, prediction, and tolerance regions for the multivariate normal distribution. Journal of the American Statistical Association 61(315):605–617.

- Cplex (2009) Cplex II (2009) V12. 1: User’s manual for CPLEX. International Business Machines Corporation 46(53):157.

- Dandl et al. (2020) Dandl S, Molnar C, Binder M, Bischl B (2020) Multi-objective counterfactual explanations. Bäck T, Preuss M, Deutz A, Wang H, Doerr C, Emmerich M, Trautmann H, eds., Parallel Problem Solving from Nature – PPSN XVI, 448–469 (Cham: Springer International Publishing), ISBN 978-3-030-58112-1.

- Dominguez-Olmedo et al. (2021) Dominguez-Olmedo R, Karimi AH, Schölkopf B (2021) On the adversarial robustness of causal algorithmic recourse. URL http://dx.doi.org/10.48550/ARXIV.2112.11313.

- Dua and Graff (2017) Dua D, Graff C (2017) UCI machine learning repository. URL http://archive.ics.uci.edu.

- Dutta et al. (2022) Dutta S, Long J, Mishra S, Tilli C, Magazzeni D (2022) Robust counterfactual explanations for tree-based ensembles. Chaudhuri K, Jegelka S, Song L, Szepesvari C, Niu G, Sabato S, eds., Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, 5742–5756 (PMLR).

- Ferrario and Loi (2022) Ferrario A, Loi M (2022) The robustness of counterfactual explanations over time. IEEE Access 10:82736–82750, URL http://dx.doi.org/10.1109/ACCESS.2022.3196917.

- Fischetti and Jo (2018) Fischetti M, Jo J (2018) Deep neural networks and mixed integer linear optimization. Constraints 23(3):296–309, URL http://dx.doi.org/10.1007/s10601-018-9285-6.

- Forel et al. (2022) Forel A, Parmentier A, Vidal T (2022) Robust counterfactual explanations for random forests. URL http://dx.doi.org/10.48550/ARXIV.2205.14116.

- Grimstad and Andersson (2019) Grimstad B, Andersson H (2019) ReLU networks as surrogate models in mixed-integer linear programs. Computers and Chemical Engineering 131:106580, ISSN 00981354, URL http://dx.doi.org/10.1016/j.compchemeng.2019.106580.

- Gurobi Optimization, LLC (2022) Gurobi Optimization, LLC (2022) Gurobi optimizer reference manual. URL https://www.gurobi.com.

- Kanamori et al. (2021) Kanamori K, Takagi T, Kobayashi K, Ike Y, Uemura K, Arimura H (2021) Ordered counterfactual explanation by mixed-integer linear optimization. Proceedings of the AAAI Conference on Artificial Intelligence 35(13):11564–11574.

- Karimi et al. (2020) Karimi AH, Barthe G, Balle B, Valera I (2020) Model-agnostic counterfactual explanations for consequential decisions. Chiappa S, Calandra R, eds., Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, 895–905 (PMLR).

- Mahajan et al. (2019) Mahajan D, Tan C, Sharma A (2019) Preserving causal constraints in counterfactual explanations for machine learning classifiers. URL http://dx.doi.org/10.48550/ARXIV.1912.03277.

- Maragno et al. (2022) Maragno D, Röber TE, Birbil I (2022) Counterfactual explanations using optimization with constraint learning. OPT 2022: Optimization for Machine Learning (NeurIPS 2022 Workshop), URL https://openreview.net/forum?id=mcjDldTC3F2.

- Maragno et al. (2021) Maragno D, Wiberg H, Bertsimas D, Birbil SI, den Hertog D, Fajemisin A (2021) Mixed-integer optimization with constraint learning. URL http://dx.doi.org/10.48550/ARXIV.2111.04469.

- Mothilal et al. (2020) Mothilal RK, Sharma A, Tan C (2020) Explaining machine learning classifiers through diverse counterfactual explanations. Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency 607–617.

- Mutapcic and Boyd (2009) Mutapcic A, Boyd S (2009) Cutting-set methods for robust convex optimization with pessimizing oracles. Optimization Methods & Software 24(3):381–406.

- Parmentier and Vidal (2021) Parmentier A, Vidal T (2021) Optimal counterfactual explanations in tree ensembles. Meila M, Zhang T, eds., Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, 8422–8431 (PMLR).

- Pawelczyk et al. (2022) Pawelczyk M, Datta T, van-den Heuvel J, Kasneci G, Lakkaraju H (2022) Probabilistically robust recourse: Navigating the trade-offs between costs and robustness in algorithmic recourse. URL http://dx.doi.org/10.48550/ARXIV.2203.06768.

- Rawal et al. (2020) Rawal K, Kamar E, Lakkaraju H (2020) Algorithmic recourse in the wild: Understanding the impact of data and model shifts. URL http://dx.doi.org/10.48550/ARXIV.2012.11788.

- Russell (2019) Russell C (2019) Efficient search for diverse coherent explanations. Proceedings of the Conference on Fairness, Accountability, and Transparency 20–28.

- Slack et al. (2021) Slack D, Hilgard A, Lakkaraju H, Singh S (2021) Counterfactual explanations can be manipulated. Ranzato M, Beygelzimer A, Dauphin Y, Liang P, Vaughan JW, eds., Advances in Neural Information Processing Systems, volume 34, 62–75 (Curran Associates, Inc.).

- Upadhyay et al. (2021) Upadhyay S, Joshi S, Lakkaraju H (2021) Towards robust and reliable algorithmic recourse. Ranzato M, Beygelzimer A, Dauphin Y, Liang P, Vaughan JW, eds., Advances in Neural Information Processing Systems, volume 34, 16926–16937 (Curran Associates, Inc.).

- Ustun et al. (2019) Ustun B, Spangher A, Liu Y (2019) Actionable recourse in linear classification. Proceedings of the Conference on Fairness, Accountability, and Transparency 10–19.

- Virgolin and Fracaros (2023) Virgolin M, Fracaros S (2023) On the robustness of sparse counterfactual explanations to adverse perturbations. Artificial Intelligence 316:103840.

- Wachter et al. (2018) Wachter S, Mittelstadt B, Russell C (2018) Counterfactual explanations without opening the black box: automated decisions and the GDPR. Harvard Journal of Law and Technology 31(2):841–887.

- Xu et al. (2008) Xu H, Caramanis C, Mannor S (2008) Robust regression and lasso. Advances in Neural Information Processing Systems 21.