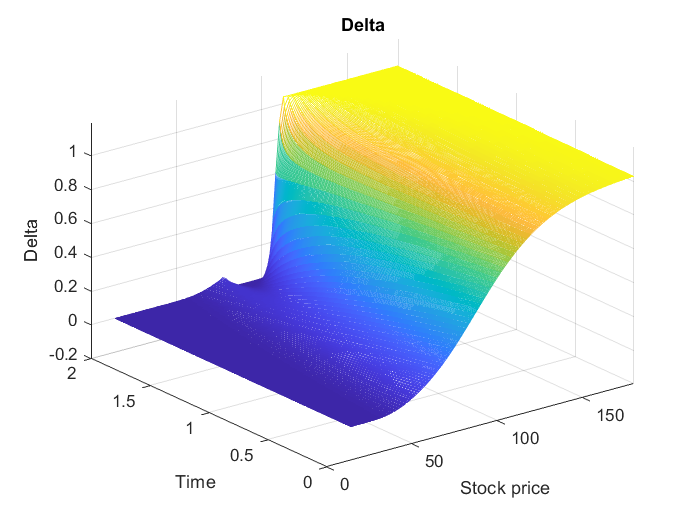

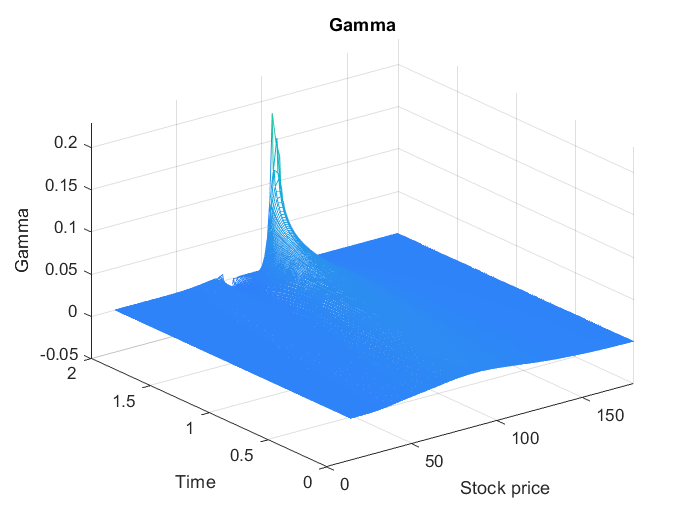

Keywords— TF model, Pricing convertible bonds, Finite element method, Finite difference method, Financial derivatives, Greeks.

1 Introduction

Convertible bond (CB) is a type of financial derivatives used in financial risk management and in trading by investors and the issuers [18, 27, 26]. It has become a popular choice of corporations as a stable investment vehicle.

Pricing financial derivatives for CBs is however a complicated problem. Tree methods (e.g., in [23]), Monte-Carlo simulation (e.g., [4]), and partial differential equations are among the widely used techniques in the literature.

One of the pioneering work using PDE modelling for CB pricing is due to Ignersoll [19], who developed a method for the determination of the optimal conversion and call policies for convertible securities using Black-Scholes [8] methodology. Brennan and Schwartz [9] extended Ignersoll’s model to incorporate callability and dividend payments. They later included stochastic interest rate, resulting in a two-factor model for CB pricing with callability and conversion strategies [10]. In the late 1990s, Tsiveriotis and Fernandes [28] proposed an innovative two-factor model for pricing CBs under callability, puttability and conversion provisions with hypothetical cash-only convertible bond (COCB) part, known as the TF model. Another model for pricing CBs with credit risk and default strategy was developed by Ayache et al. [6] based on a system of triple partial differential equations, called the AFV model.

Because of their complexity, the TF and AFV models have to be solved numerically. The review paper of Al Saedi and Tularam [1] provides a recent account on methodologies for option pricing under the Black-Scholes equation, such as the R3C scheme [5], cubic spline wavelets and multiwavelet bases methods [11], finite difference methods (FDM) [14], finite-volume methods (FVM) [22], and finite-element methods (FEM) [17, 7, 13, 20]. Due to their simplicity, FDM have become a popular numerical method in computational finance. In computational bond pricing, the authors of [9, 10, 28, 6] use FDM to solve their proposed model.

In this paper, we discuss and expanded the existing literature on numerical solutions of the TF model for CB pricing with credit risk and without dividends by implementing finite-element methods.

The TF model for convertible bond pricing is based on the system of partial differential equations (PDEs)

|

|

|

(1) |

|

|

|

(2) |

for the time and the underlying stock price , with being the value of the CB, the value of hypothetical COCB, the risk-free rate, the growth rate, which can be counted as risk-free rate (see [18]), the credit spread reflecting payoff default risk, be volatility, and the maturity time.

The terminal condition at the maturity time means that once the CB is expired, no one can call or put it back. Holder of the CB will get as much as possible depending on the conversion ratio and stock price. There is however a minimum based on the face value and the coupon payment , yielding the terminal condition:

|

|

|

(3) |

and

|

|

|

(4) |

Throughout its lifetime, however, the CB can be converted to the underlying stock at the value , and issuer should pay the principal value to the holder, if the issuer has not converted until maturity time. These rights lead to three conditions that constrain the CB price:

-

1.

Upside constraint due to conversion of bonds: for ,

|

|

|

(5) |

|

|

|

(6) |

-

2.

Upside constraint due to callability with the call price : for , with the earliest time the bond issuer is allowed to call back the bond,

|

|

|

(7) |

|

|

|

(8) |

-

3.

Downside constraint due to putability with the put price : for , with the earliest time the investor is allowed to put the bond back,

|

|

|

(9) |

|

|

|

(10) |

Following [6], the call and put price in the callability and puttability constraints include the effect of future’s coupon payment and the underlying interest as follows. Let , the set of the coupon payment time, with . Then

|

|

|

(11) |

where

|

|

|

(12) |

the accrued interest at any time between the time of the last coupon payment and the time of the next (pending) coupon payment . Note that the constraints (5) and (9) can be combined to . In this way, the constraints for can be rewritten as

|

|

|

|

(13) |

|

|

|

|

(14) |

with

|

|

|

|

(15) |

|

|

|

|

(16) |

Two boundary conditions need to be supplemented to the PDEs (1) and (2). At , the PDEs are reduced to

|

|

|

|

(17) |

and

|

|

|

|

(18) |

with the terminal conditions (see Eqs. (3) and (4)).

The other boundary condition is associated with the situation when the the stock price increases unboundedly, under which the CB is converted into stock. Therefore,

|

|

|

(19) |

After spatial discretization using, for instance, FDM or FEM, the initial-boundary value problems (IBVP) with constraints given by (1)–(19) can be solved by using a time-integration method, such as Crank-Nicolson, in combination with projected SSOR (PSSOR) method to tackle the nonlinearity. In our paper, however, we shall consider a formulation of the above-stated IBVP in a penalty PDE to explicitly include some constraints in the PDEs, and apply FEM and Crank-Nicolson method on the resulting penalty PDE.

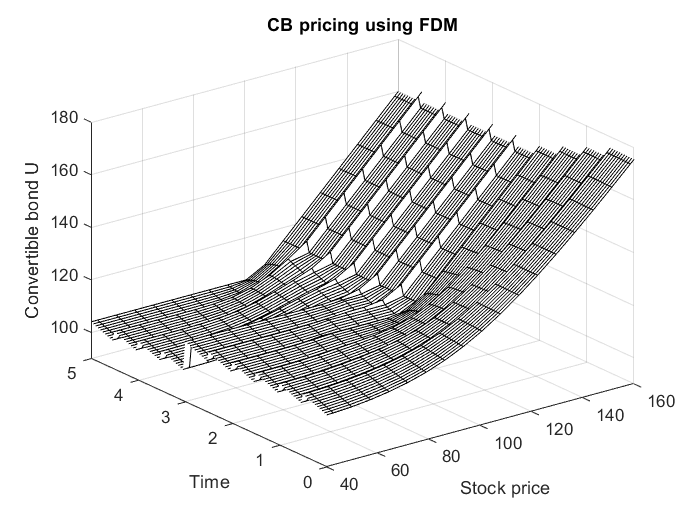

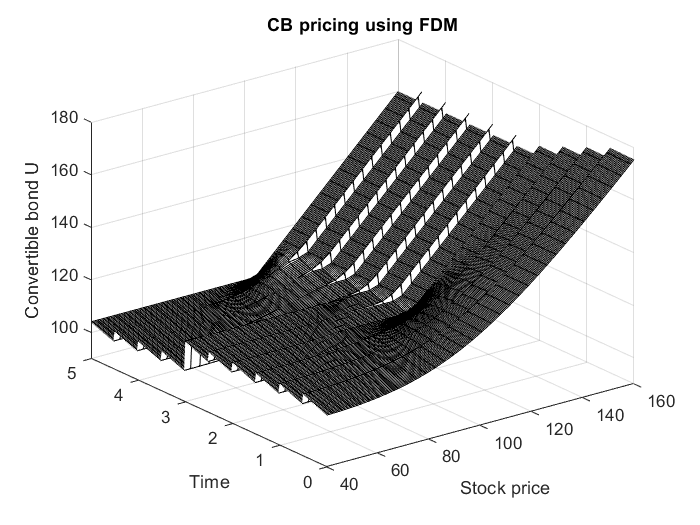

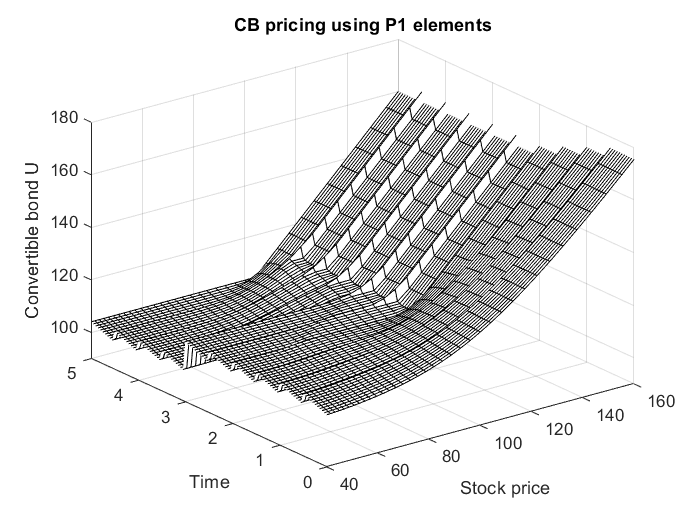

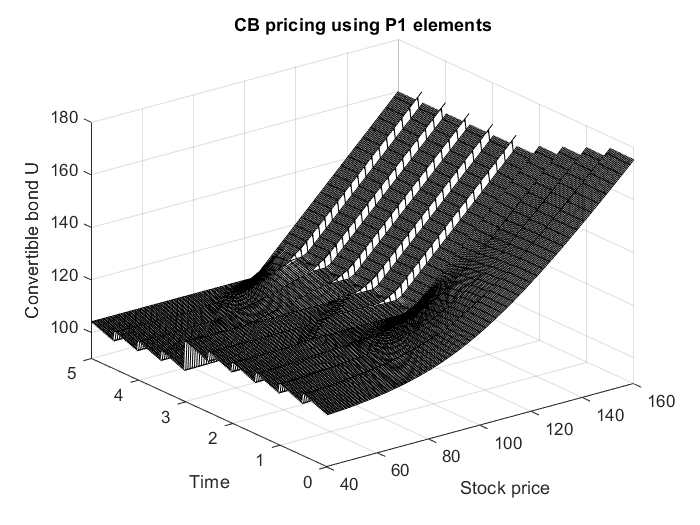

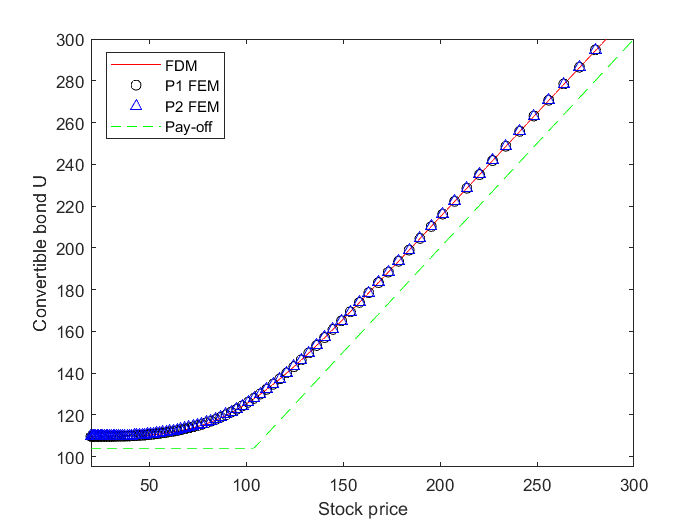

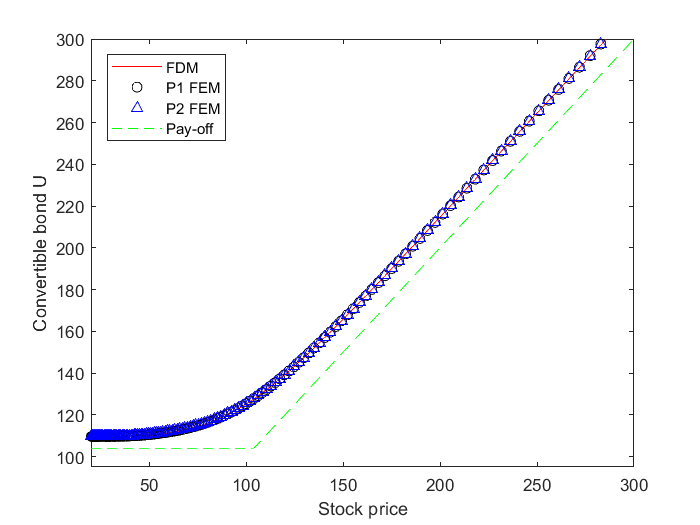

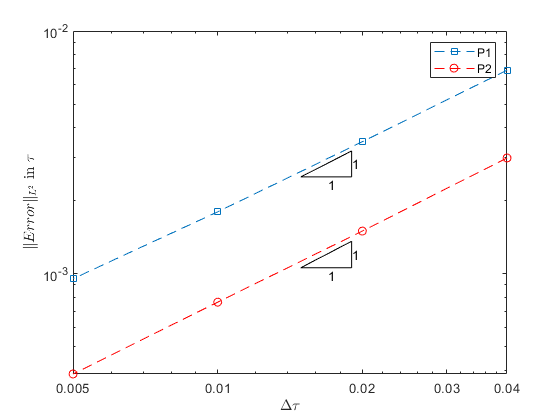

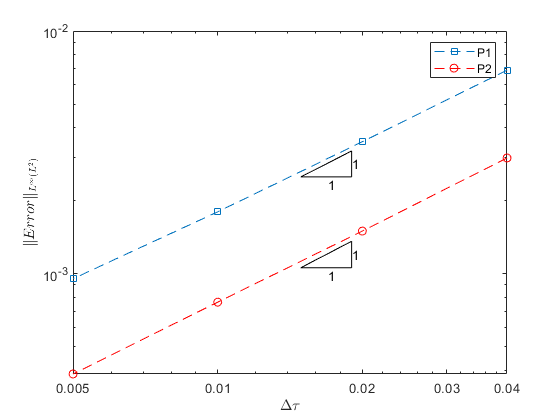

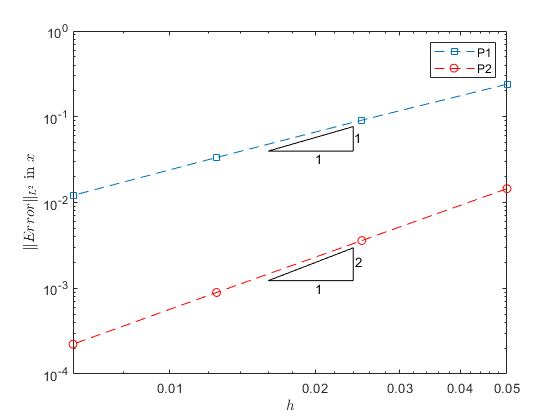

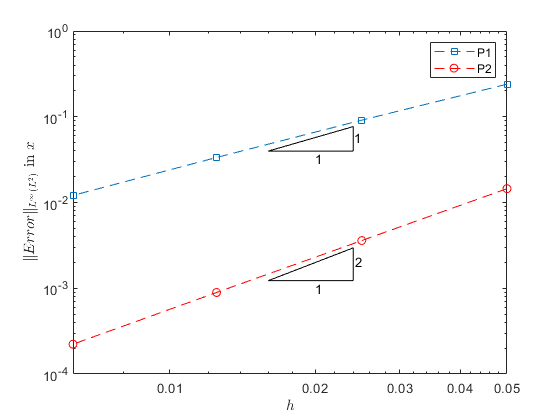

The paper is organized as follows. In Section 2, transformation of the TF model with penalty in a suitable form for numerical method is presented to implement our numerical schemes. Finite element formulation for the penalty TF model is established in Section 3. We detail the time-integration method for solving the resulting differential algebraic equation in Section 4. Section 5 presents numerical results and discussions on the convergence of the FEM method. We finish up the paper by drawing some conclusion and remarks in Section 6.

2 The transformed TF model

The standard procedure for solving the Black-Scholes-type PDEs requires transformation of the terminal-boundary value problem to an initial-boundary value problem, on which many numerical methods can be devised. Let and ,

where is the stock price at the initial time . With this change of variables, it can be shown that the PDEs (1)–(2) are transformed to

|

|

|

|

(20) |

|

|

|

|

(21) |

with .

The terminal conditions at now become initial conditions at , given by

|

|

|

(22) |

and

|

|

|

(23) |

Furthermore, the constraints for are transformed into

|

|

|

|

(24) |

|

|

|

|

(25) |

where

|

|

|

|

(26) |

and

|

|

|

|

(27) |

with and, for ,

|

|

|

(28) |

The constraints for now read

-

1.

for ,

|

|

|

(29) |

-

2.

for ,

|

|

|

(30) |

-

3.

for ,

|

|

|

(31) |

For the boundary conditions, we note here that is not defined at . As in the actual numerical computation we set as close as possible to , we assume that (17) also holds at the proximity of , which corresponds to in the -space. This results in the boundary conditions at

|

|

|

|

(32) |

|

|

|

|

(33) |

Transformation of the boundary conditions at is straightforward: at ,

|

|

|

|

(34) |

|

|

|

|

(35) |

As stated in Section 1, our focus in this paper is on the the penalty TF model. We therefore need to reformulate the model into a PDE model with penalty terms associated with some constraints. In particular, as in practice we are mainly concerned with the CB price , not , we shall reformulate the CB PDE (20) with the associated constraints (24) and (25) into a penalty PDE. To this end, note that the linear complementarity problem (LCP) for (20)

with constraints (24) and (25) is given by [6]

|

|

|

(36) |

where .

The penalty PDE for the bond valuation can be constructed from the LCP (36):

|

|

|

where is the penalty parameter, which typically is set very large. By rewriting and , with

|

|

|

(37) |

the CB PDE can be reformulated into

|

|

|

(38) |

3 Finite element method

In this section, we construct finite-element methods to approximately discretize the penalty CB PDE (38) and the COCB PDE (21) in the transformed TF model. To apply finite element spatial discretization to the PDEs, the domain is approximated by the bounded domain in the following:

Suppose that the solution of the bond PDEs are functions of the following class:

|

|

|

Consider two test functions , where . The weak formulation of the penalty PDE (38) and (21) reads

|

|

|

|

|

|

|

|

where the integration is carried out along the -direction ( is not indicated to save space).

Integration by parts and applying the vanishing property of the function and at the boundary results in the weak formulation

|

|

|

|

|

|

|

|

To build our finite-element approximation, we consider the finite dimensional subspace , spanned by the basis . The finite-element approximation to the solution is the function

|

|

|

where are additional functions needed to interpolate the given solutions at the boundaries. A similar form of approximation to is devised, namely

|

|

|

The use of the above approximations results in the weak formulation in the finite-dimensional space:

|

|

|

|

(39) |

|

|

|

|

|

|

|

|

|

|

|

|

where and ,

and

|

|

|

|

(40) |

|

|

|

|

|

|

|

|

In the Galerkin method [21], the test function and are chosen to coincide with the basis function . Imposing this condition for , results in the system of equations

|

|

|

|

(41) |

|

|

|

|

|

|

|

|

|

|

|

|

where is with be replaced by and similarly for , and

|

|

|

|

(42) |

|

|

|

|

|

|

|

|

In practice, systems of equations (41) and (42) are constructed via an assembly process using (local) element matrices, whose structures depend on the choice of the basis functions . The common choice for the basis functions is a class of functions satisfying the nodal condition

|

|

|

(43) |

where is the nodal point. This choice leads to global systems of linear equations with sparse and banded coefficient matrices.

3.1 Linear polynomial bases

Consider partition of the spatial domain into non-overlapping elements , with , , , the nodal points, and . In the basic element , we define two linear interpolation basis functions

|

|

|

|

|

|

|

|

resulting in the P1 finite element (P1-FEM). Evaluating the integrals in (41) and (42) using the above-stated basis functions over the element results in the following local (element) matrices:

-

•

For the term, the element matrix reads

|

|

|

-

•

For the term, the element matrix reads

|

|

|

-

•

For the term, the element matrix reads

|

|

|

3.2 Quadratic polynomial bases

In this approach, we add a midpoint in the basic element , giving three nodal points: , , and , and define three quadratic interpolation polynomials satisfying the nodal condition (43):

|

|

|

|

(44) |

|

|

|

|

(45) |

|

|

|

|

(46) |

resulting in P2-FEM. The local element matrices are as follows:

-

•

the term:

|

|

|

-

•

the term:

|

|

|

-

•

the term:

|

|

|

3.3 Treating the constraints by Penalty method

We now turn to the two nonlinear penalty terms in (38) and construct a finite-element approximation to them. We in particular apply group finite element [15] to deal with the nonlinearity. We shall discuss the construction for ; construction of finite element approximation for is done in the same way.

We assume that the term is approximated by

|

|

|

where . Therefore, for , , we have

|

|

|

|

|

|

|

|

(47) |

Each integral in the above-equation is evaluated element-wise, resulting in the local element matrices , , and , given in Sections 3.1 and 3.2.

By using the same argument,

|

|

|

(48) |

4 Time integration scheme

The global finite-element system obtained from assembling the local finite-element matrices can be represented by the differential algebraic equations (DAEs):

|

|

|

|

|

|

|

|

(49) |

|

|

|

|

(50) |

where , , and

|

|

|

|

(51) |

|

|

|

|

(52) |

are the boundary condition vectors.

Time integration of the DAEs (49) and (50) is carried out by applying the -scheme on both equations, which results in the systems, with , , and the number of time steps,

|

|

|

|

|

|

or

|

|

|

|

|

|

|

|

|

|

|

|

(53) |

|

|

|

|

(54) |

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let the solutions and be known. The solutions at the next time level can in principle be computed by first solving (54) for . The solution is then computed via (53) using the known , , and . This procedure however requires knowledge of the solutions at the boundaries at the time level .

4.1 Boundary solutions

At , with , , etc, the boundary conditions with penalty in can be written as follows:

|

|

|

(55) |

Note that , with

|

|

|

and , with

|

|

|

Application of the -scheme on (55) leads to the discrete equations:

|

|

|

|

|

|

|

|

(56) |

|

|

|

|

(57) |

Let the boundary solution be known. Then can be computed from (57). With , , and now known, (56) becomes a nonlinear function of , which can be solved approximately using Newton’s method. First of all we assume that the penalty term in (56) is approximated in a fully implicit way at the new time level . This results in the equation

|

|

|

(58) |

where

|

|

|

With

|

|

|

(59) |

Newton’s method for finding satisfying (58) can be written as follows: with an initial guess , compute , for .

In this paper, is chosen to be solution of the unconstrained boundary problem given by (17). Since we expect that computed in this way is a better approximation than, e.g., , we can use this value as well to evaluate the conditions to constraint .

The complete algorithm for computing and is as follows:

Algorithm 1: Computing the boundary solutions

-

1.

input , ;

-

2.

compute and ;

-

3.

compute from (57);

-

4.

compute from (56) without penalty terms;

-

5.

apply constraints on using ;

-

6.

set ;

-

7.

for until convergence

-

7.1.

compute using (58);

-

7.2.

compute using (59);

-

7.3.

;

-

8.

apply constraints on using ;

-

9.

if

-

9.1

;

-

9.2

;

At we need to compute and via (19), apply the constraints, and pay the coupon if .

We remark here that solution of Newton’s method exists if the derivative . This condition however cannot be theoretically guaranteed. In this regard, for the tuple and nonnegative , , , and ,

-

1.

if , then ;

-

2.

if , we have two situations:

-

(a)

if and , then ;

-

(b)

if and , then if .

Since the penalty parameter is taken very large (e.g., in this paper), vanishing is very unlikely to happen under a reasonable choice of the time step . For instance, using the simulation parameters in Table 1 in Section 5, the vanishing situation outlined in Point 2(b) above may occur if is chosen to be in the order of , which makes the time-integration process extremely impractical.

4.2 Interior solutions

With solutions at the boundaries available at and , all related boundary vectors in (53) and (54) are known. We are thus now in the position to compute the solutions and . is readily computed from (54). With known, (53) reduces to a nonlinear function of . As we do for the boundary equations, we assume that the penalty terms in (54) are approximated in a fully implicit way, resulting in the equation

|

|

|

|

|

(60) |

where

|

|

|

(61) |

The nonlinear equation (60) is solved iteratively using Newton’s method. Starting from an initial guess of the solution , the solution is approximated using the iterands

|

|

|

where is the Jacobian of , given by

|

|

|

(62) |

The initial guess is chosen such that it solves unconstrained CB PDE, which is equivalent to solving (53) without penalty terms. We shall also use this unconstrained solution to constrain the initially computed prior to the start of Newton’s iterations. The procedure for computing the solutions in the interior after one -scheme step is summarized in the following algorithm:

Algorithm 2: Computing the interior solutions

-

1.

input , ;

-

2.

compute and ;

-

3.

compute from (54);

-

4.

compute from (53) without penalty terms;

-

5.

apply constraints on using ;

-

6.

set ;

-

7.

for until convergence

-

7.1.

compute using (60);

-

7.2.

compute using (62);

-

7.3.

;

-

8.

apply constraints on using ;

-

9.

if

-

9.1

;

-

9.2

;

The existence of a solution of Newton’s method requires nonsingularity of the Jacobian . Like in the case with Newton’s method for computing boundary solutions, there may exist values of parameters , , , , , and such that the Jacobian is singular. Quantification of such conditions requires analysis, which is beyond the scope of this paper. Numerical tests using various realistic values of parameters exhibit no convergence issues with the methods, suggesting nonsingularity of .

4.3 Summary of the time integration method

By including Algorithm 1 and 2 in the -scheme, the complete time stepping procedure to compute the solutions and is shown in Algorithm 3.

Algorithm 3: -scheme for time integration with constraints

-

1.

input the initial solution at : , , , , , and ;

-

2.

for

-

2.1.

Compute and ;

-

2.2.

Compute and by performing Step 3–9 of Algorithm 1;

-

2.3.

Compute and ;

-

2.4.

Apply the conversion-callability-puttability constraints on and .

-

2.5.

if

-

2.5.1.

;

-

2.5.2.

;

-

2.6.

Compute and by performing Step 3–9 of Algorithm 2;

For increased stability, it is possible to initiate the time integration using Rannacher’s step [24]. In this case, for , the solutions , , , , , and are computed using the initial conditions using Step 2.1–2.6 but with a smaller time step than (e.g, , where ). Since we did not see stability issues when , we did not implement Rannacher’s step to obtain numerical results presented in Section 5.