Expectile hidden Markov regression models for analyzing cryptocurrency returns

Abstract

In this paper we develop a linear expectile hidden Markov model for the analysis of cryptocurrency time series in a risk management framework. The methodology proposed allows to focus on extreme returns and describe their temporal evolution by introducing in the model time-dependent coefficients evolving according to a latent discrete homogeneous Markov chain. As it is often used in the expectile literature, estimation of the model parameters is based on the asymmetric normal distribution. Maximum likelihood estimates are obtained via an Expectation-Maximization algorithm using efficient M-step update formulas for all parameters. We evaluate the introduced method with both artificial data under several experimental settings and real data investigating the relationship between daily Bitcoin returns and major world market indices.

Keywords: Asymmetric normal distribution, Cryptocurrencies, EM algorithm, Expectile regression, Markov switching models, Time series

1 Introduction

In the last ten years, investors have been increasingly attracted by the exploit of the cryptocurrency market, mostly because of its peculiar characteristics. Born merely as a peer-to-peer electronic cash system (Nakamoto, 2008), the billion increase in market capitalization (in particular Bitcoin during 2016-2017), enormous price jumps and levels of high volatility that were never seen before have made cryptos a new category of investment assets. Their unusual behavior makes them prone to some speculative bubbles that may in turn threaten the stability of financial markets (Cheah & Fry, 2015; Yarovaya et al., 2016). Being crucial to address the level of integration between cryptocurrencies and traditional financial assets, many contributions have analyzed the relationship with equities mainly relying on well-known econometric techniques such as GARCH models (Katsiampa et al., 2019; Guesmi et al., 2019), variance decomposition (Ji et al., 2018; Corbet et al., 2018; Yi et al., 2018) and Granger causality test (Bouri et al., 2020b). Part of the related literature has focused on extreme returns by using models capturing the tail behaviour, rather than inferring such occurrences from models based on conditional central tendency. For instance, Kristjanpoller et al. (2020) and Naeem et al. (2021) employ a multifractal asymmetric analysis, indicating the presence of heterogeneity in the cross-relationship between most cryptocurrencies and equity ETFs and showing different behaviors between upward and downward trends. Shahzad et al. (2022) investigate tail-based connectedness among major cryptocurrencies in extreme downward and upward market conditions using LASSO penalized quantile regressions, while Zhang et al. (2021) apply a risk spillover approach based on generalized quantiles, showing the existence of a downside risk spillover between Bitcoin and traditional assets.

In quantitative risk management, indeed, investigating the dynamic of extreme occurrences is of utmost importance for market participants and regulators. Among the different methods considered throughout the literature, quantile regression, introduced by Koenker & Bassett (1978), has represented a valid approach for modeling the entire distribution of returns while accounting for the well-known stylized facts, i.e., high kurtosis, skewness and serial correlation, that typically characterize financial assets. In the financial literature, the quantile regression framework has been positively applied to estimate and forecast Value at Risk (VaR) and quantile-based risk measures (Engle & Manganelli 2004; White et al. 2015; Taylor 2019; Merlo et al. 2021).

Several generalizations of the concept of quantiles have also been introduced over the years. One important extension is provided by the expectile regression (Newey & Powell 1987), which can be thought of as a generalization of the classical mean regression based on an asymmetric squared loss function. Similar to quantile regression, expectile regression allows to characterize the entire conditional distribution of a response variable, but possesses several advantages over the former. First, expectiles are more informative than quantiles since they rely on tail expectations whereas quantiles use only the information on whether an observation is below or above the predictor. Second, the squared loss is continuously differentiable which makes the estimators and their covariance matrix easier to compute using fast and efficient algorithms. For these reasons, expectile models have been implemented in several fields, such as longitudinal data (Tzavidis et al. 2016; Alfò et al. 2017; Barry et al. 2021), spatial analysis (Sobotka & Kneib 2012; Spiegel et al. 2020), life expectancy (Nigri et al. 2022), economics and finance (Taylor 2008; Kim & Lee 2016; Bellini & Di Bernardino 2017; Bottone et al. 2021). Especially in the context of risk management, expectiles have gained an important role as potential competitors to the VaR and the Expected Shortfall measures. Indeed, they possess several interesting properties in terms of risk measures (see for instance Bellini 2012, Bellini et al. 2014 and Ziegel 2016), and are the only risk measure that is both coherent (Artzner et al. 1999) and elicitable (Lambert et al. 2008).

Moreover, when modeling financial time series, returns often exhibit a clustering behavior over time which cannot be captured by traditional homogeneous regression models. Risk managers and regulators are increasingly interested in determining whether, and how, their temporal evolution can be influenced by hidden variables, e.g., the state of the market, during tranquil and crisis periods. In this context, Hidden Markov Models (HMMs, see MacDonald & Zucchini 1997; Zucchini et al. 2016) have been successfully employed in the analysis of time series data, with applications to asset allocation and stock returns as discussed in Mergner & Bulla (2008); De Angelis & Paas (2013); Nystrup et al. (2017) and Maruotti et al. (2019). Quantile regression methods have also been generalized to account for serial heterogeneity. For example, Liu (2016) consider a quantile autoregression in which the parameters are subject to regime shifts determined by the outcome of a latent, discrete-state Markov process, while Adam et al. (2019) propose a model-based clustering approach where groups are inferred from conditional quantiles; see also Ye et al. (2016), Maruotti et al. (2021) andMerlo et al. (2022) for other applications of regime-switching models to financial and environmental time series. In longitudinal data, Farcomeni (2012) and Marino et al. (2018) introduce linear quantile regression models where time-dependent unobserved heterogeneity is described through dynamic coefficients that evolve according to a homogeneous hidden Markov chain. Within a Bayesian framework, a quantile nonhomogeneous HMM for longitudinal data has been recently proposed by Liu et al. (2021). To the best of our knowledge, however, a HMM for estimating conditional expectiles has not yet been proposed in the literature.

Motivated by the advantages of expectiles and the versatility of HMMs, we develop a linear expectile hidden Markov regression model to analyze the tail relation between cryptocurrencies and traditional asset classes. The method introduced allows to examine the entire conditional distribution of returns given the hidden state and potential covariates, where the dynamics of returns over time is described by state-specific regression coefficients which follow a latent discrete homogeneous Markov chain. Inference about model parameters is carried out in a Maximum Likelihood (ML) approach using an Expectation-Maximization (EM) algorithm based on the asymmetric normal distribution of Waldmann et al. (2017) as working likelihood.

From a risk management standpoint, the proposed methodology contributes to identify and control for potential inherent risks related to the participation in crypto exchanges to develop appropriate policies and risk assessment procedures.

The study period considered starts from September 2014 until October 2022, comprising numerous events that heavily impacted financial stability, as the Chinese stock market crash of 2015, the crypto currency bubble crisis in 2017-2018, the COVID-19 outbreak in 2020 and the Russian invasion of Ukraine at the beginning of 2022. Following Corbet et al. (2018), we model Bitcoin daily returns as a function of major stock and global market indices, including Crude Oil, Standard Poor’s 500 (SP500), Gold COMEX daily closing prices and the Volatility Index (VIX). Our results show that Bitcoin returns exhibit a clear temporal clustering behavior in calm and turbulent periods, and they are strongly associated with traditional assets at low and high expectile levels.

In concluding, we also evaluate the performance of our approach in a simulation study, generating observations from a two-state HMM under two different sample sizes and two different distributions for the error terms. Additional simulation studies with different error distributions, a higher number of hidden states and a less persistent transition probability matrix are illustrated in the Supplementary Materials.

The rest of the paper is organized as follows. Section 2 briefly reviews the expectile regression. In Section 3 we specify the proposed model with the EM algorithm for estimating the model parameters and the computational aspects. In Section 4, we evaluate the performance of our proposal in a simulation study. Section 5 shows the empirical analysis and discusses the results obtained while Section 6 concludes.

2 Expectile regression

Expectile regression has been proposed by Newey & Powell (1987) as a “quantile-like” generalization of standard mean regression based on asymmetric least-squares estimation. Similarly to quantile regression of Koenker & Bassett (1978), this is an alternative approach for characterizing the entire conditional distribution of a response variable where the quantile loss function is substituted with an asymmetric squared loss function. Formally, the expectile of order of a continuous response given the -dimensional vector of covariates , is defined as the minimizer, , of the following problem:

| (1) |

where is the asymmetric square loss and denotes the indicator function.

In a regression framework, for a given , a linear expectile model is defined as , where is the regression parameter vector. If , expectile regression reduces to the standard mean regression while for it allows to target the entire conditional distribution of the response given the covariates similarly to quantile regression. When we turn from quantiles to expectiles, the latter possess several advantages over the former. Particularly, we gain uniqueness of the ML solutions which is, indeed, not granted in the quantile context. From a computational standpoint, since the squared loss function is differentiable, the regression parameters can be estimated by efficient Iterative Reweighted Least Squares (IRLS), in contrast to algorithms used for fitting quantile regression models. Proofs of consistency, asymptotic normality and a robust estimator of the variance-covariance matrix of the regression coefficients for inference have been established in Newey & Powell (1987). These properties make the expectile regression versatile and computationally appealing from a statistical point of view.

In a likelihood approach, Gerlach & Chen (2015) and Waldmann et al. (2017) originally introduced the idea of expectile regression by employing a likelihood function that is based on the Asymmetric Normal (AN) distribution. The AN distribution can be thought of as a generalization of the normal distribution to allow for non-zero skewness, having the following density:

| (2) |

where is a location parameter corresponding to the -th expectile of , is a scale parameter and determines the asymmetry of the distribution. Particularly, when the density in (2) reduces to the well-known normal distribution, and and coincide with its mean and standard deviation, respectively. As discussed by Waldmann et al. (2017), the minimization of the asymmetric squared loss function in (1) is equivalent, in terms of parameter estimates, to the maximization of the likelihood associated with the AN density.

In the following section, we extend the expectile regression to the HMM setting by using the AN distribution as working likelihood.

3 Methodology

In this section we describe the expectile hidden Markov regression model in order to take into account the temporal evolution of the time series under analysis. We then show how inference about model parameters can be carried out in a ML approach using the AN distribution introduced in the previous section.

Formally, let be a latent, homogeneous, first-order Markov chain defined on the discrete state space . Let be the initial probability of state , , and , with and , denote the transition probability between states and , that is, the probability to visit state at time from state at time , and . More concisely, we collect the initial and transition probabilities in the -dimensional vector and in the matrix , respectively.

To build the proposed model, let denote a continuous observable response variable and be a vector of exogenous covariates, with the first element being the intercept, at time . For a given expectile level , the proposed linear Expectile Hidden Markov Model (EHMM) is defined as follows:

| (3) |

with being a state-specific coefficient vector that assumes one of the values depending on the outcome of the unobservable Markov chain and where is the error term whose conditional -th expectile is assumed to be zero.

Extending the approach of Waldmann et al. (2017) to the HMM setting, we use the AN distribution to describe the conditional distribution of the response given covariates and the state occupied by the latent process at time , whose probability density function is now given by

| (4) |

where the location parameter is defined by the linear model .

Following the work of Gassiat et al. (2016), to ensure sufficient conditions for model identifiability we state the following Proposition.

Proposition 1.

For any fixed expectile level , let’s assume that the number of hidden states K is known, that the matrix of transition probability between states has full rank and that the K’s conditional distributions of the response given covariates and the state occupied by the latent process are independent. Then, the model in (3)-(4) is identifiable from the distribution of three consecutive variables , up to label swapping of the hidden states.

The proof of this result can be obtained by adapting Theorem 1 in Gassiat et al. (2016).

In the following section we use the AN distribution as a working likelihood for estimating the model parameters in a regression framework.

3.1 Likelihood inference

In this section we consider a ML approach to make inference on model parameters. As is common for HMMs, and for latent variable models in general, we develop an EM algorithm (Baum et al. 1970) to estimate the parameters of the method proposed based on the observed data. To ease the notation, unless specified otherwise, hereinafter we omit the expectile level , yet all model parameters are allowed to depend on it.

For a given number of hidden states , the EM algorithm runs on the complete log-likelihood function of the model introduced, which is defined as

| (5) | ||||

where represents the vector of all model parameters, denotes a dummy variable equal to if the latent process is in state at occasion and 0 otherwise, and is a dummy variable equal to if the process is in state in and in state at time and otherwise.

To estimate , the algorithm iterates between two steps, the E- and M-steps, until convergence, as outlined below.

E-step:

In the E-step, at the generic -th iteration, the unobservable indicator variables and in (5) are replaced by their conditional expectations given the observed data and the current parameter estimates . To compute such quantities we require the calculation of the probability of being in state at time given the observed sequence

| (6) |

and the probability that at time the process is in state and then in state at time , given the observed sequence

| (7) |

The quantities in (6) and (7) can be obtained using the Forward-Backward algorithm of Welch (2003). Then, we use these to calculate the conditional expectation of the complete log-likelihood function in (5) given the observed data and the current estimates:

| (8) | ||||

M-step:

In the M-step we maximize in (8) with respect to to obtain the update parameter estimates . The maximization of can be partitioned into orthogonal subproblems, where the updating formulas for the hidden Markov chain and state-dependent regression parameters are obtained independently maximizing each of these terms. Formally, the initial probabilities and transition probabilities are updated using:

| (9) |

and

| (10) |

To update the regression coefficients, the first-order condition of (8) with respect to , , yields

| (11) |

so the M-step update expression for is

| (12) |

which can be computed using IRLS for cross-sectional data with appropriate weights. Similarly, from the first-order condition of (8) with respect to the scale parameters we obtain the following M-step update formula for :

| (13) |

The E- and M- steps are alternated until convergence, that is when the observed likelihood between two consecutive iterations is smaller than a predetermined threshold. In this paper, we set this threshold criterion equal to .

Following Maruotti et al. (2021) and Merlo et al. (2022), for fixed and we initialize the EM algorithm by providing the initial states partition, , according to a Multinomial distribution with probabilities . From the generated partition, the elements of are computed as proportions of transition, while we obtain and by fitting mean regressions on the observations within state . To deal with the possibility of multiple roots of the likelihood equation and better explore the parameter space, we fit the proposed EHMM using a multiple random starts strategy with different starting partitions and retain the solution corresponding to the maximum likelihood value.

Once we computed the ML estimate of the model parameters, to estimate the standard errors we employ the parametric bootstrap scheme of Visser et al. (2000). In practice, we refit the model to bootstrap samples and approximate the standard error of each model parameter with the corresponding standard deviation of the bootstrap estimates.

4 Simulation study

In this section we conduct a simulation study to validate the performance of our method under different scenarios in terms of: (i) recovering the true values of the parameters; (ii) assessing the classification behavior of the proposed model; (iii) evaluating the capability of penalized likelihood criteria in selecting the optimal number of hidden states . We analyze three sample sizes () and two distributions for the error term. For each scenario we conduct Monte Carlo simulations. We draw observations from a two state HMM () using the following data generating process:

| (14) |

with , where , and with and . We consider two distributions for the error terms in (14). In the first scenario, is generated from a Gaussian distribution with standard deviation 1, for . In the second one, is generated from a skew- distribution with 5 degrees of freedom and asymmetry parameter 2, for . Finally, the matrix of transition probabilities is set equal to , while the vector of initial probabilities is equal to . Additional simulation studies with different error distributions, a higher number of hidden states and a less persistent transition probability matrix are illustrated in the Supplementary Materials.

In order to assess the validity of the model we fit the proposed EHMM at five expectile levels, i.e., , and compute the bias and standard errors associated to the state-specific coefficients, averaged over the Monte Carlo replications, for each combination of sample size and error distribution. Tables 1 and 2 report the simulation outputs for the Gaussian and skew- distributions, respectively. As can be observed, as regards Gaussian distributed errors, the precision of the estimates is higher at the center of the distribution rather than on the tails, mainly due to the reduced number of observations at extreme expectile levels, but the bias always remains under control. Evidently, in Table 2 a higher standard deviation shows up for the skew- distribution due to the asymmetry and heavier tails than the Gaussian density, but both the bias and the standard deviation tend to decrease as the sample size increases, with some exception, probably related to Monte Carlo variability. Concerning the hidden process, given the true values of the transition probabilities in , we see that the coefficients corresponding to the first state are estimated with lower precision because fewer transitions occur from one state to the other, as expected.

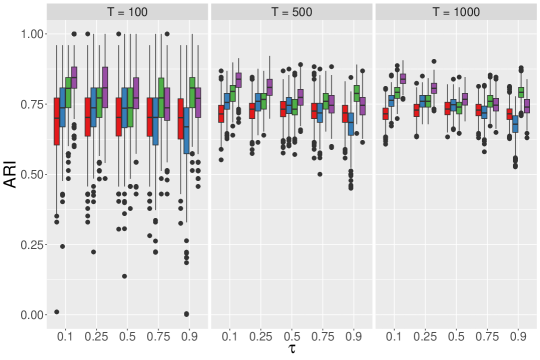

To evaluate the ability in recovering the true states partition we consider the Adjusted Rand Index (ARI) of Hubert & Arabie (1985). The state partition provided by the fitted models is obtained by taking the maximum, , posteriori probability for every , and report the box-plots of ARI for the classification obtained according to the posterior probabilities in Figure 1 for the four settings considered. As a benchmark, we also report box-plots of ARI related to the partitions obtained by considering the true model parameters. Firstly, we observe that the accuracy of estimating the true state partition is significantly influenced by distribution error, across all five expectile levels. The value of the asymmetry parameter and the tail-heaviness determine better results for the skew- in the left tail of the distribution, while exhibiting a comparatively inferior performance in the right tail with respect to the Gaussian distribution.

Secondly, the goodness of the clustering obtained partially depends on the specific expectile level as regards the Gaussian distribution, being the values slightly higher at the mean () than at the tails. Finally, when increasing the sample size from to and , results clearly improve reporting a lower variability for both error distributions. Overall, the proposed EHMM is able to recover the true values of the parameters and the true state partition highly satisfactory in all the cases examined. The last goal of this simulation exercise is to assess the performance of three widely employed penalized likelihood criteria for selecting the true number of hidden states , namely the AIC (Akaike 1998), the BIC (Schwarz et al. 1978) and the ICL (Biernacki et al. 2000). Following the work of Merlo et al. (2022), we use the same generating data process in (14), drawing observations from a two state HMM () with . We fit the EHMM with in order to select the best associated to the lowest penalized likelihood criteria over 300 Monte Carlo replicates. Table 3 reports the percentage frequency distributions of the selected for each of the three criteria at three expectile levels, i.e. , for Gaussian and skew- distributed errors (we do not show results for since it is never selected by any criteria). We can observe that the BIC and ICL work well at and for Gaussian distributed errors but, as we move towards the tails of the distribution of the response variable, ICL always outperforms the other criteria. These results suggest that, among the criteria considered, the ICL does well in terms of correctly identifying

the number of latent states across all considered scenarios,

capturing serial heterogeneity in the data in a more parsimonious manner.

| 0.10 | 0.25 | 0.50 | 0.75 | 0.90 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | |

| Panel A: T=100 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.00622 | 0.33093 | 0.00955 | 0.12356 | -0.00565 | 0.11848 | -0.02963 | 0.13449 | -0.06976 | 0.17636 |

| = 2 | -0.01692 | 0.26157 | 0.00081 | 0.16778 | 0.00573 | 0.16098 | 0.01463 | 0.16816 | 0.03025 | 0.19427 |

| State 2 | ||||||||||

| = 1 | 0.08047 | 0.24807 | 0.04623 | 0.13363 | 0.01166 | 0.12077 | -0.01745 | 0.13365 | -0.04202 | 0.18725 |

| = -2 | 0.00566 | 0.30633 | -0.00625 | 0.17357 | -0.00682 | 0.16814 | -0.00495 | 0.18425 | -0.00012 | 0.22838 |

| Panel A: T=500 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.02575 | 0.07014 | 0.01263 | 0.05784 | 0.00044 | 0.05497 | -0.0171 | 0.06197 | -0.04871 | 0.0821 |

| = 2 | -0.01612 | 0.07496 | -0.00342 | 0.06725 | 0.00168 | 0.06623 | 0.00116 | 0.07122 | -0.00477 | 0.08286 |

| State 2 | ||||||||||

| = 1 | 0.05135 | 0.0778 | 0.01864 | 0.05887 | -0.00159 | 0.05347 | -0.0171 | 0.05688 | -0.03274 | 0.07033 |

| = -2 | 0.00684 | 0.08549 | 0.00288 | 0.07153 | 0.00269 | 0.0671 | 0.00642 | 0.07113 | 0.01655 | 0.08229 |

| Panel B: T = 1000 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.02282 | 0.04637 | 0.01032 | 0.03886 | -0.00241 | 0.03703 | -0.02037 | 0.04082 | -0.0507 | 0.05365 |

| = 2 | -0.01544 | 0.05691 | -0.00562 | 0.04951 | -0.00272 | 0.04693 | -0.00338 | 0.04991 | -0.00793 | 0.0589 |

| State 2 | ||||||||||

| = 1 | 0.04491 | 0.05364 | 0.01622 | 0.04135 | -0.00129 | 0.03711 | -0.01424 | 0.03884 | -0.02716 | 0.04679 |

| = -2 | 0.00666 | 0.06116 | 0.00151 | 0.05149 | 0.00003 | 0.0471 | 0.00278 | 0.04753 | 0.01253 | 0.05389 |

| 0.10 | 0.25 | 0.50 | 0.75 | 0.90 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | Bias | Std.Err | |

| Panel A: T=100 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.00815 | 0.1085 | -0.01061 | 0.10852 | -0.03357 | 0.18523 | -0.08009 | 0.32874 | -0.18035 | 0.48869 |

| = 2 | -0.00918 | 0.17167 | -0.00311 | 0.12744 | -0.00416 | 0.18517 | -0.03466 | 0.47901 | -0.11981 | 0.82864 |

| State 2 | ||||||||||

| = 1 | 0.01825 | 0.15049 | -0.00137 | 0.11403 | -0.0142 | 0.16168 | 0.04334 | 1.09454 | 0.11931 | 1.47897 |

| = -2 | 0.00479 | 0.23544 | 0.00591 | 0.14285 | -0.00152 | 0.4782 | 0.11121 | 0.96889 | 0.17729 | 0.64891 |

| Panel A: T=500 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.00483 | 0.04542 | -0.01193 | 0.04596 | -0.03978 | 0.06474 | -0.09664 | 0.11736 | -0.22504 | 0.25398 |

| = 2 | -0.00604 | 0.05776 | -0.00186 | 0.05428 | 0.00372 | 0.0682 | 0.02162 | 0.11595 | 0.093 | 0.27504 |

| State 2 | ||||||||||

| = 1 | 0.00974 | 0.04828 | -0.00616 | 0.04369 | -0.01681 | 0.05402 | -0.02279 | 0.0903 | 0.0038 | 0.19797 |

| = -2 | 0.00925 | 0.05833 | 0.00865 | 0.05523 | 0.01502 | 0.06355 | 0.03747 | 0.08278 | 0.06971 | 0.22292 |

| Panel B: T = 1000 | ||||||||||

| State 1 | ||||||||||

| = -1 | 0.00215 | 0.03171 | -0.01439 | 0.0314 | -0.04228 | 0.04483 | -0.10444 | 0.0845 | -0.2491 | 0.18266 |

| = 2 | -0.00609 | 0.03989 | -0.0021 | 0.03919 | 0.00261 | 0.04837 | 0.02072 | 0.08124 | 0.09536 | 0.19691 |

| State 2 | ||||||||||

| = 1 | 0.0108 | 0.03395 | -0.00527 | 0.0308 | -0.01522 | 0.03795 | -0.01847 | 0.06424 | 0.01649 | 0.14547 |

| = -2 | 0.00912 | 0.04106 | 0.00717 | 0.03911 | 0.01368 | 0.04379 | 0.03687 | 0.05688 | 0.0817 | 0.07759 |

| 0.10 | 0.50 | 0.90 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| AIC | BIC | ICL | AIC | BIC | ICL | AIC | BIC | ICL | |

| Panel A: Gaussian errors | |||||||||

| K = 2 | 0 | 0 | 100 | 57 | 91 | 95 | 0 | 0 | 100 |

| K = 3 | 0 | 27 | 0 | 31 | 4 | 5 | 0 | 25 | 0 |

| K = 4 | 100 | 73 | 0 | 12 | 5 | 0 | 100 | 75 | 0 |

| Panel B: skew- errors | |||||||||

| K = 2 | 0 | 0 | 57 | 0 | 0 | 92 | 0 | 0 | 52 |

| K = 3 | 0 | 0 | 42 | 0 | 0 | 8 | 0 | 0 | 47 |

| K = 4 | 100 | 100 | 1 | 100 | 100 | 0 | 100 | 100 | 1 |

5 Empirical application

In this section we apply the methodology proposed to analyze the Bitcoin daily returns as a function of global leading financial indices. Over the last decade, cryptocurrencies and in particular the Bitcoin market played a leading role, attracting attentions of researchers and investors. Their peculiar characteristics, such their extreme price volatility, driven by market speculation and technology applications, often lead to price bubbles, euphoria and market instability. In order to address these periods of upheaval, it is crucial to understand the association between Bitcoin and globally relevant market indices in such circumstances of financial turmoil. Consistently with Corbet et al. (2018), here we consider the Bitcoin, Crude Oil, Standard Poor’s 500 (SP500), Gold COMEX daily closing prices and the Volatility Index (VIX) from September 2014 to October 2022. All series are expressed in US dollars and have been downloaded from the Yahoo finance database. Daily returns with continuous compounding are calculated

taking the difference of the logarithms between closing prices in consecutive trading days and then multiplied by 100, i.e., , where is the closing price on day , for a total of observations.

The considered timespan is marked by numerous crises that may have impacted cross-market integration patterns, including the Chinese stock market crash of 2015, the cryptocurrency bubble crisis in 2017-2018, the COVID-19 pandemic and the Russian invasion of Ukraine at the beginning of 2022, which have caused unprecedented levels of uncertainty and risk.

In Table 4 we report the list of examined variables and the summary statistics for the whole sample. First thing to notice is that Bitcoin is generally much more volatile than the other assets, having the highest standard deviation. The Bitcoin returns also show very high negative skewness and very high kurtosis, as well as SP500. The highest level of kurtosis is reported by Crude Oil, probably determined by the prices’ fluctuations after the COVID-19 outbreak. On the other side, the large positive skewness of VIX indicates longer and fatter tails on the right side of the distribution, highlighting the well-known inverse relationship with the SP500.

In concluding, the Augmented Dickey-Fuller (ADF) test Dickey & Fuller (1979) shows that all daily returns are stationary at the level of significance. Following these considerations, and motivated by the reforms considered by markets authorities to protect investors and preserve stability in response to cryptocurrencies’ downturns, the proposed EHMM can provide insights into the temporal evolution of Bitcoin returns and describe how this is affected by rapid changes in markets volatility.

| Minimum | Mean | Maximum | Std.Err. | Skewness | Kurtosis | Jarque-Bera test | ADF test | |

|---|---|---|---|---|---|---|---|---|

| Bitcoin | -46.4730 | 0.1859 | 22.5119 | 4.6165 | -0.6817 | 8.7172 | 6568.469 | -11.117 |

| Crude Oil | -28.2206 | 0.0280 | 31.9634 | 3.1077 | 0.0942 | 21.1219 | 37645.730 | -10.324 |

| S&P500 | -12.7652 | 0.0316 | 8.9683 | 1.1716 | -0.9033 | 16.3473 | 22823.380 | -12.390 |

| Gold | -5.1069 | 0.0152 | 5.7775 | 0.9358 | -0.0698 | 4.1741 | 1471.712 | -12.292 |

| VIX | -29.9831 | 0.0379 | 76.8245 | 8.3414 | 1.2683 | 6.6648 | 4290.737 | -14.209 |

To this end, we consider the following linear EHMM:

| (15) |

with corresponding to the -th conditional expectile of Bitcoin return at time in state , while denotes the return of the same date for Crude Oil, and similarly for the other indices.

As a first step of the empirical analysis, in order to select the number of latent states we fit the proposed EHMM for different values of varying from 2 to 5.

To model large negative and positive returns, we focus on three expectile levels .

To compare models with differing number of states, Table 5 reports three widely employed penalized likelihood selection criteria for , namely the AIC (Akaike 1998), the BIC (Schwarz et al. 1978) and the ICL (Biernacki et al. 2000). As one can see, the AIC selects 5, or more, states, while BIC chooses for all three expectile levels. This should not be surprising since the AIC tends to overestimate the true number of hidden states. On the contrary, ICL favors a more parsimonious choice as is always considered to be the optimal number of states at , and . For these reasons, and in order to clearly identify high and low volatility market conditions we thus consider the proposed EHMM with states for all three levels.

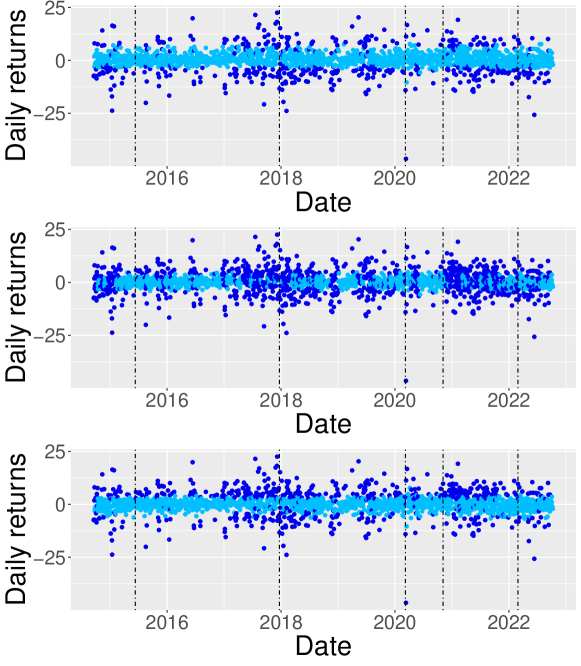

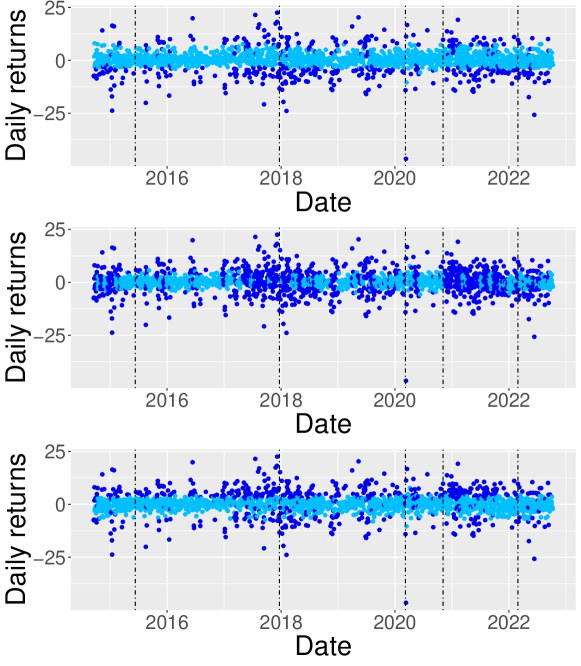

For the selected models, we report the clustering results in Figure 2 at the investigated expectile levels for Bitcoin daily returns, colored according to the estimated posterior probability of class membership, , with the vertical dashed lines representing globally relevant events such as the Chinese stock market crash in 2015, the cryptocurrencies crash at the beginning of 2018, the COVID-19 market crash in March 2020, Biden’s election at the USA presidency in November 2020 and the Russian invasion of Ukraine at the beginning of 2022. Here we clearly see that the latent components can be associated to specific market regimes characterized by low and high volatility periods. Specifically, light-blue points (State 1) tend to identify low returns, while dark-blue ones (State 2) correspond to periods of extreme positive and negative returns. When targeting the conditional mean (), as expected the level of separation among high and low volatility periods becomes less clear. However, as the focus of our work lies especially at the tails of the returns distribution ( and ), the classification obtained with is more clear and it allows us to distinguish low and high volatility periods. As a robustness check, we also used the Viterbi algorithm for the estimation of clustering partition (see Figure 3 in the Appendix). By comparing the results with those obtained with the MAP rule in Figure 2, the two assignment rules give the same results more than of the time.

Moving on to the state-specific model parameters, Table 6 shows the parameter estimates along with the standard errors (in brackets) computed by using the parametric bootstrap technique illustrated in Section 3.1 over resamples. First, consistently with the quantile regression literature, the intercepts are increasing with , with State 1 having lower values than State 2 for all s. Second, it is interesting to observe that in the not-at-risk state (State 1) the SP500, Gold and the VIX index positively influence extreme left-tail () movements of Bitcoin returns, while only SP500 and Gold significantly influence the right-tail () expectiles of the cryptocurrency, exposing a connection during high volatility periods between traditional financial markets and Bitcoin both for negative and positive returns. At , instead, Bitcoin can be considered as a weak hedge during high volatility periods since it is not statistically associated with all the assets considered (Bouri, Jalkh, Molnár & Roubaud, 2017; Bouri, Molnár, Azzi, Roubaud & Hagfors, 2017). In the at-risk state (State 2) we observe a positive influence of the SP500 and Gold across the conditional distribution of returns. Also, one can see that Crude Oil is negatively associated with the crypto returns at the -th expectile. This finding is in line with Bouri et al. (2020a) but it is contrary to the works of Dyhrberg (2016) and Corbet et al. (2018), which may be due to the events and crises occurred in the last years.

Finally, the estimated state-dependent scale parameter reflects more stable periods for the first state, meanwhile contemplates rapid (positive and negative) peak and burst returns for the second state, confirming the graphical analysis conducted in Figure 2.

| AIC | |||

|---|---|---|---|

| 11347.4122 | 11231.4286 | 11389.7954 | |

| 11210.6074 | 11126.1327 | 11204.4727 | |

| 11109.3930 | 11051.9556 | 11115.4655 | |

| 11055.7980 | 11014.8696 | 11079.7912 | |

| BIC | |||

| 11431.6121 | 11315.6285 | 11473.9953 | |

| 11356.5539 | 11272.0791 | 11350.4192 | |

| 11328.3127 | 11270.8753 | 11334.3852 | |

| 11358.9175 | 11317.9892 | 11382.9108 | |

| ICL | |||

| 12784.4362 | 12787.4471 | 12926.5182 | |

| 13490.5599 | 13406.8221 | 13616.8609 | |

| 13880.2346 | 13487.8461 | 13759.7332 | |

| 14111.8066 | 13511.4108 | 13908.7362 |

| Intercept | Crude Oil | S&P500 | Gold | VIX | ||

|---|---|---|---|---|---|---|

| State 1 | ||||||

| -1.036 (0.280) | 0.024 (0.021) | 0.595 (0.096) | 0.189 (0.072) | 0.029 (0.012) | 1.433 (0.040) | |

| 0.122 (0.158) | 0.031 (0.072) | 0.409 (0.383) | 0.263 (0.249) | 0.009 (0.036) | 1.695 (0.062) | |

| 1.297 (0.061) | -0.009 (0.020) | 0.589 (0.088) | 0.134 (0.065) | 0.014 (0.011) | 1.335 (0.041) | |

| State 2 | ||||||

| -6.52 (0.060) | -0.256 (0.096) | 2.072 (0.476) | 1.032 (0.320) | -0.055 (0.058) | 4.964 (0.157) | |

| 0.242 (0.092) | -0.056 (0.055) | 1.087 (0.357) | 0.613 (0.214) | -0.025 (0.026) | 6.164 (0.169) | |

| 6.244 (0.229) | 0.017 (0.079) | 0.948 (0.291) | 0.835 (0.249) | -0.002 (0.041) | 4.692 (0.128) |

6 Conclusions

The increasing popularity and importance of Bitcoin in the financial landscape have made scholars and practitioners interrogated about its properties and its relation to other assets. In this regard, we contribute to the existing literature in two ways. From a theoretical standpoint, we develop a linear expectile hidden Markov model for the analysis of time series where temporal behaviors of the data are captured via time-dependent coefficients that follow an unobservable discrete homogeneous Markov chain. The proposed method enables us to model the entire conditional distribution of asset returns and, at the same time, to grasp unobserved serial heterogeneity and rapid volatility jumps that would otherwise go undetected. From a practical point of view, we analyze the association between Bitcoin and a collection of global market indices, not only at the average, but also during times of market stress.

Empirically, we find evidence of strong and positive interrelations among Bitcoin returns and SP500 and Gold, and, at the same time, we observe the capacity of the Bitcoin of working as a weak hedge during high volatility periods, contributing to the existing strands of literature on the subject (Baur et al., 2018; Corbet et al., 2018, 2019). Its partial capacity of being a weak hedge but not a safe haven it is consistent with the excess volatility of Bitcoin and indications that assets with no history as a safe haven are unlikely to be considered “safe” in an economic or financial crisis (Baur et al., 2018).

As a possible next step, our methodology could be extended to the hidden semi-Markov model setting where the sojourn-distributions, that is, the distributions of the number of consecutive time points that the chain spends in each state, can be modeled by the researcher using either parametric or non-parametric approaches instead of assuming geometric sojourn densities as in HMMs.

Appendix

Figures

References

- (1)

- Adam et al. (2019) Adam, T., Langrock, R. & Kneib, T. (2019), Model-based clustering of time series data: a flexible approach using nonparametric state-switching quantile regression models, in ‘Proceedings of the 12th Scientific Meeting on Classification and Data Analysis’, pp. 8–11.

- Akaike (1998) Akaike, H. (1998), Information theory and an extension of the maximum likelihood principle, in ‘Selected papers of Hirotugu Akaike’, Springer, pp. 199–213.

- Alfò et al. (2017) Alfò, M., Salvati, N. & Ranallli, M. G. (2017), ‘Finite mixtures of quantile and M-quantile regression models’, Statistics and Computing 27(2), 547–570.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. & Heath, D. (1999), ‘Coherent measures of risk’, Math. Finance 9(3), 203–228.

- Barry et al. (2021) Barry, A., Oualkacha, K. & Charpentier, A. (2021), ‘A new GEE method to account for heteroscedasticity using asymmetric least-square regressions’, Journal of Applied Statistics pp. 1–27.

- Baum et al. (1970) Baum, L. E., Petrie, T., Soules, G. & Weiss, N. (1970), ‘A maximization technique occurring in the statistical analysis of probabilistic functions of Markov chains’, The Annals of Mathematical Statistics 41(1), 164–171.

- Baur et al. (2018) Baur, D. G., Hong, K. & Lee, A. D. (2018), ‘Bitcoin: Medium of exchange or speculative assets?’, Journal of International Financial Markets, Institutions and Money 54, 177–189.

- Bellini (2012) Bellini, F. (2012), ‘Isotonicity properties of generalized quantiles’, Statistics & Probability Letters 82(11), 2017–2024.

- Bellini & Di Bernardino (2017) Bellini, F. & Di Bernardino, E. (2017), ‘Risk management with expectiles’, The European Journal of Finance 23(6), 487–506.

- Bellini et al. (2014) Bellini, F., Klar, B., Müller, A. & Rosazza Gianin, E. (2014), ‘Generalized quantiles as risk measures’, Insurance Math. Econom. 54, 41–48.

- Biernacki et al. (2000) Biernacki, C., Celeux, G. & Govaert, G. (2000), ‘Assessing a mixture model for clustering with the integrated completed likelihood’, IEEE Transactions on Pattern Analysis and Machine Intelligence 22(7), 719–725.

- Bottone et al. (2021) Bottone, M., Petrella, L. & Bernardi, M. (2021), ‘Unified Bayesian conditional autoregressive risk measures using the skew exponential power distribution’, Statistical Methods & Applications 30(3), 1079–1107.

- Bouri, Jalkh, Molnár & Roubaud (2017) Bouri, E., Jalkh, N., Molnár, P. & Roubaud, D. (2017), ‘Bitcoin for energy commodities before and after the december 2013 crash: diversifier, hedge or safe haven?’, Applied Economics 49(50), 5063–5073.

- Bouri et al. (2020a) Bouri, E., Lucey, B. & Roubaud, D. (2020a), ‘Cryptocurrencies and the downside risk in equity investments’, Finance Research Letters 33, 101211.

- Bouri et al. (2020b) Bouri, E., Lucey, B. & Roubaud, D. (2020b), ‘The volatility surprise of leading cryptocurrencies: Transitory and permanent linkages’, Finance Research Letters 33, 101188.

- Bouri, Molnár, Azzi, Roubaud & Hagfors (2017) Bouri, E., Molnár, P., Azzi, G., Roubaud, D. & Hagfors, L. I. (2017), ‘On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier?’, Finance Research Letters 20, 192–198.

- Cheah & Fry (2015) Cheah, E.-T. & Fry, J. (2015), ‘Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin’, Economics Letters 130, 32–36.

- Corbet et al. (2019) Corbet, S., Lucey, B., Urquhart, A. & Yarovaya, L. (2019), ‘Cryptocurrencies as a financial asset: A systematic analysis’, International Review of Financial Analysis 62, 182–199.

- Corbet et al. (2018) Corbet, S., Meegan, A., Larkin, C., Lucey, B. & Yarovaya, L. (2018), ‘Exploring the dynamic relationships between cryptocurrencies and other financial assets’, Economics Letters 165, 28–34.

- De Angelis & Paas (2013) De Angelis, L. & Paas, L. J. (2013), ‘A dynamic analysis of stock markets using a hidden Markov model’, Journal of Applied Statistics 40(8), 1682–1700.

- Dickey & Fuller (1979) Dickey, D. A. & Fuller, W. A. (1979), ‘Distribution of the estimators for autoregressive time series with a unit root’, Journal of the American Statistical Association 74(366a), 427–431.

- Dyhrberg (2016) Dyhrberg, A. H. (2016), ‘Hedging capabilities of Bitcoin. Is it the virtual gold?’, Finance Research Letters 16, 139–144.

- Engle & Manganelli (2004) Engle, R. F. & Manganelli, S. (2004), ‘CAViaR: conditional autoregressive Value at Risk by regression quantiles’, Journal of Business & Economic Statistics 22(4), 367–381.

- Farcomeni (2012) Farcomeni, A. (2012), ‘Quantile regression for longitudinal data based on latent markov subject-specific parameters’, Statistics and Computing 22(1), 141–152.

- Gassiat et al. (2016) Gassiat, É., Cleynen, A. & Robin, S. (2016), ‘Inference in finite state space non parametric hidden markov models and applications’, Statistics and Computing 26, 61–71.

- Gerlach & Chen (2015) Gerlach, R. & Chen, C. W. (2015), ‘Bayesian expected shortfall forecasting incorporating the intraday range’, Journal of Financial Econometrics 14(1), 128–158.

- Guesmi et al. (2019) Guesmi, K., Saadi, S., Abid, I. & Ftiti, Z. (2019), ‘Portfolio diversification with virtual currency: Evidence from Bitcoin’, International Review of Financial Analysis 63, 431–437.

- Hubert & Arabie (1985) Hubert, L. & Arabie, P. (1985), ‘Comparing partitions’, Journal of Classification 2(1), 193–218.

- Ji et al. (2018) Ji, Q., Bouri, E., Gupta, R. & Roubaud, D. (2018), ‘Network causality structures among bitcoin and other financial assets: A directed acyclic graph approach’, The Quarterly Review of Economics and Finance 70, 203–213.

- Katsiampa et al. (2019) Katsiampa, P., Corbet, S. & Lucey, B. (2019), ‘Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis’, Finance Research Letters 29, 68–74.

- Kim & Lee (2016) Kim, M. & Lee, S. (2016), ‘Nonlinear expectile regression with application to Value-at-Risk and Expected Shortfall estimation’, Computational Statistics & Data Analysis 94, 1–19.

- Koenker & Bassett (1978) Koenker, R. & Bassett, G. (1978), ‘Regression quantiles’, Econometrica: Journal of the Econometric Society 46(1), 33–50.

- Kristjanpoller et al. (2020) Kristjanpoller, W., Bouri, E. & Takaishi, T. (2020), ‘Cryptocurrencies and equity funds: Evidence from an asymmetric multifractal analysis’, Physica A: Statistical Mechanics and Its Applications 545, 123711.

- Lambert et al. (2008) Lambert, N. S., Pennock, D. M. & Shoham, Y. (2008), Eliciting properties of probability distributions, in ‘Proceedings of the 9th ACM Conference on Electronic Commerce’, ACM, pp. 129–138.

- Liu et al. (2021) Liu, H., Song, X., Tang, Y. & Zhang, B. (2021), ‘Bayesian quantile nonhomogeneous hidden Markov models’, Statistical Methods in Medical Research 30(1), 112–128.

- Liu (2016) Liu, X. (2016), ‘Markov switching quantile autoregression’, Statistica Neerlandica 70(4), 356–395.

- MacDonald & Zucchini (1997) MacDonald, I. L. & Zucchini, W. (1997), Hidden Markov and other models for discrete-valued time series, Vol. 110, CRC Press.

- Marino et al. (2018) Marino, M. F., Tzavidis, N. & Alfò, M. (2018), ‘Mixed hidden Markov quantile regression models for longitudinal data with possibly incomplete sequences’, Statistical Methods in Medical Research 27(7), 2231–2246.

- Maruotti et al. (2021) Maruotti, A., Petrella, L. & Sposito, L. (2021), ‘Hidden semi-Markov-switching quantile regression for time series’, Computational Statistics & Data Analysis 159, 107208.

- Maruotti et al. (2019) Maruotti, A., Punzo, A. & Bagnato, L. (2019), ‘Hidden Markov and semi-Markov models with multivariate leptokurtic-normal components for robust modeling of daily returns series’, Journal of Financial Econometrics 17(1), 91–117.

- Mergner & Bulla (2008) Mergner, S. & Bulla, J. (2008), ‘Time-varying beta risk of Pan-European industry portfolios: A comparison of alternative modeling techniques’, The European Journal of Finance 14(8), 771–802.

- Merlo et al. (2022) Merlo, L., Maruotti, A., Petrella, L. & Punzo, A. (2022), ‘Quantile hidden semi-Markov models for multivariate time series’, Statistics and Computing 32(4), 1–22.

- Merlo et al. (2021) Merlo, L., Petrella, L. & Raponi, V. (2021), ‘Forecasting VaR and ES using a joint quantile regression and its implications in portfolio allocation’, Journal of Banking & Finance p. 106248.

- Naeem et al. (2021) Naeem, M. A., Bouri, E., Peng, Z., Shahzad, S. J. H. & Vo, X. V. (2021), ‘Asymmetric efficiency of cryptocurrencies during COVID19’, Physica A: Statistical Mechanics and its Applications 565, 125562.

- Nakamoto (2008) Nakamoto, S. (2008), ‘Bitcoin: A peer-to-peer electronic cash system’, Decentralized Business Review p. 21260.

- Newey & Powell (1987) Newey, W. K. & Powell, J. L. (1987), ‘Asymmetric least squares estimation and testing’, Econometrica: Journal of the Econometric Society pp. 819–847.

- Nigri et al. (2022) Nigri, A., Barbi, E. & Levantesi, S. (2022), ‘The relationship between longevity and lifespan variation’, Statistical Methods & Applications 31(3), 481–493.

- Nystrup et al. (2017) Nystrup, P., Madsen, H. & Lindström, E. (2017), ‘Long memory of financial time series and hidden Markov models with time-varying parameters’, Journal of Forecasting 36(8), 989–1002.

- Schwarz et al. (1978) Schwarz, G. et al. (1978), ‘Estimating the dimension of a model’, The Annals of Statistics 6(2), 461–464.

- Shahzad et al. (2022) Shahzad, S. J. H., Bouri, E., Ahmad, T. & Naeem, M. A. (2022), ‘Extreme tail network analysis of cryptocurrencies and trading strategies’, Finance Research Letters 44, 102106.

- Sobotka & Kneib (2012) Sobotka, F. & Kneib, T. (2012), ‘Geoadditive expectile regression’, Computational Statistics & Data Analysis 56(4), 755–767.

- Spiegel et al. (2020) Spiegel, E., Kneib, T. & Otto-Sobotka, F. (2020), ‘Spatio-temporal expectile regression models’, Statistical Modelling 20(4), 386–409.

- Taylor (2008) Taylor, J. W. (2008), ‘Estimating Value at Risk and Expected Shortfall using expectiles’, Journal of Financial Econometrics 6(2), 231–252.

- Taylor (2019) Taylor, J. W. (2019), ‘Forecasting Value at Risk and Expected Shortfall using a semiparametric approach based on the asymmetric Laplace distribution’, Journal of Business & Economic Statistics 37(1), 121–133.

- Tzavidis et al. (2016) Tzavidis, N., Salvati, N., Schmid, T., Flouri, E. & Midouhas, E. (2016), ‘Longitudinal analysis of the strengths and difficulties questionnaire scores of the Millennium Cohort Study children in England using M-quantile random-effects regression’, Journal of the Royal Statistical Society: Series A (Statistics in Society) 179(2), 427–452.

- Visser et al. (2000) Visser, I., Raijmakers, M. E. & Molenaar, P. C. (2000), ‘Confidence intervals for hidden Markov model parameters’, British Journal of Mathematical and Statistical Psychology 53(2), 317–327.

- Waldmann et al. (2017) Waldmann, E., Sobotka, F. & Kneib, T. (2017), ‘Bayesian regularisation in geoadditive expectile regression’, Statistics and Computing 27(6), 1539–1553.

- Welch (2003) Welch, L. R. (2003), ‘Hidden Markov models and the Baum-Welch algorithm’, IEEE Information Theory Society Newsletter 53(4), 10–13.

- White et al. (2015) White, H., Kim, T.-H. & Manganelli, S. (2015), ‘VAR for VaR: Measuring tail dependence using multivariate regression quantiles’, Journal of Econometrics 187(1), 169–188.

- Yarovaya et al. (2016) Yarovaya, L., Brzeszczyński, J. & Lau, C. K. M. (2016), ‘Intra-and inter-regional return and volatility spillovers across emerging and developed markets: Evidence from stock indices and stock index futures’, International Review of Financial Analysis 43, 96–114.

- Ye et al. (2016) Ye, W., Zhu, Y., Wu, Y. & Miao, B. (2016), ‘Markov regime-switching quantile regression models and financial contagion detection’, Insurance: Mathematics and Economics 67, 21–26.

- Yi et al. (2018) Yi, S., Xu, Z. & Wang, G.-J. (2018), ‘Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency?’, International Review of Financial Analysis 60, 98–114.

- Zhang et al. (2021) Zhang, Y.-J., Bouri, E., Gupta, R. & Ma, S.-J. (2021), ‘Risk spillover between bitcoin and conventional financial markets: An expectile-based approach’, The North American Journal of Economics and Finance 55, 101296.

- Ziegel (2016) Ziegel, J. F. (2016), ‘Coherence and elicitability’, Mathematical Finance 26(4), 901–918.

- Zucchini et al. (2016) Zucchini, W., MacDonald, I. L. & Langrock, R. (2016), Hidden Markov models for time series: an introduction using R, Chapman and Hall/CRC.