Robust and efficient Breusch-Pagan test-statistic: an

application of the -score Lagrange multipliers test for

non-identically distributed individuals

Nirian Martín, Complutense University of Madrid (nimartin@ucm.es)

Abstract

In Econometrics, the Breusch-Pagan test-statistic has become an iconic

application of the Lagrange multipliers (LM) test. We

shall introduce -score LM tests for heteroscedasticity in linear

regression models, which trades-off the degree of robustness and efficiency is

through a tuning parameter , being the

classical Breusch-Pagan test-statistic, the most efficient one under absence

of outliers. A very elegant expression is obtained, with an appealing least squares interpretation. The construction of the test-statistic is performed extending the

methodology of Basu et al. (2022) from identically distributed to

non-identically distributed individuals, for composite null hypotheses.

Detailed theoretical justifications about robustness and efficiency

properties are given, all of them under normality. A modified version is derived, the Koenker’s -score test-statistic.

The way of dealing, in practice, with new heteroscedasticity tests for linear

regression models is shown through a classical example.

JEL CLASSIFICATION: C01, C10;

KEYWORDS: Breusch-Pagan test, Composite null hypothesis,

Density power divergence, Heteroscedasticity, Lagrange multipliers test,

Linear Regression, Robustness.

1 Introduction

Majority of undergraduate textbooks of Econometrics, include the Breusch-Pagan

Lagrange Multipliers (LM) test as one of the most important tests for

heteroscedasticity in linear regression models. Authored by Breusch and Pagan

(1979), it was also obtained independently by Godfrey (1978a) under a stronger

assumption of multiplicative heteroskedasticity. Thereafter, Koenker (1981)

and Koenker and Basset (1982) developed a modified version of the test that

relaxes the assumption of normality in the error distribution, allowing for a

more general distribution. With a particular structure of the design matrix

for the type of heteroskedasticity, adding the cross-product of the

regressors, a test for heteroscedasticity was obtained in White (1980), but

Waldman (1983) clarified that White’s version of the test is a particular case

of the Breusch-Pagan or Koenker’s tests, depending on the normal ot non-normal

distributional assumption for errors. The mentioned tests suffer from lack of

robustness under outlying data. This issue is reported for example in Carrol

and Ruppert (1988, page 98), Green (page 314), Kmenta (1986, page 295), Lyon

and Tsay (1996, page 339) and Kalina (2011). Recently, Berenguer-Rico and

Wilms (2021) have suggested outlier removal for testing heterogeneity using

the White test-statistic, while Alih and Ong (2015) have proposed a robust

version of the Goldfeld-Quandt test-statistic replacing its non-robust component.

The robustness of many statistical procedures is often achieved at the price

of the loss of efficiency. The estimators and test-statistics constructed with

simultaneous asymptotic efficiency and robustness properties are very

attractive. This idea was firstly introduced, in the estimation setting, in

Beran (1977) through the Hellinger distance. The original notion of distance

(or divergence) between two probability distributions, constructed from a

sample, was introduced separately by Kolmogorov (1933) and Mahalanobis (1936),

in different ways. In parametric statistical inference, from the beginning and

in successive developments, the proposed new statistical distances were

focussed on the closeness of a empirical distribution and a model based

distribution , where is the

-dimensional parameter vector of interest. When the true distribution

belongs to the model based one, it is well-known that the Kullback-Leibler

(1951) divergence covers all the classical statistical theory related to the

maximum likelihood estimators (MLEs) and their associated test-statistics.

There is an extent family of -divergence measures, introduced by

Csiszár (1967), from which BAN (Best Asymptotically Normal) estimators are

obtained, i.e. estimators as efficient as the MLEs, asymptotically. The

aforementioned distances include as a particular class of distances, the so

called power divergences of Cressie and Read (1984) and the last ones at the

same time contain the Hellinger distance as a particular member. For more

details see Pardo (2006) and Basu et al. (2011). With the progress of the

literature, several new robust and efficient minimum distance procedures have

been proposed and among them, the density power divergence (DPD) measures of

Basu et al. (1998) have become very popular. Their novelty with respect to

the Hellinger distance was based on the bounded influence function of the

estimators as well as on the extension of their validity to continuous

populations apart from the discrete ones, mostly treated until this moment.

Thereafter, the DPDs have received a growing attention in statistical

inference being applied for estimation and testing in different parametric

models. For linear regression, from a conditional point of view or fixed

design matrix, Ghosh and Basu (2013) established for the first time formally

how to deal with DPDs in estimation when the observations in the sample are

independent and not-identically distributed. For robust testing through DPDs

in linear regression models, in Section 6.3. of Ghosh et al. (2016) -Wald test statistics were proposed, while in Qin and Priebe (2017) the

-likelihood ratio test statistics (L-likelihood-ratio-type tests)

were introduced. There is a sounded disadvantage of the -Likelihood

Ratio test statistics with respect to the -Wald test statistics, the

asymptotic distribution depends on weights to be calculated as eigenvalues of

matrices dependent of unknown parameters and except for scalar parameters this

issue affects the accuracy of the calculation of the test-statistics. Based on

Basu et al. (2022), it is expected that the -score LMs to be developed

in the current paper, will have the same asymptotic distribution as the

-Wald test statistics. In addition, as noted by Boos (1992), the

strength of the generalized score tests, where the -score LMs are

included, is the invariance property. This is in fact, what happens with the

Breusch-Pagan LM test, since it is valid for testing the presence of a general

type of heteroscedasticity. A unique expression of the test-statistic covers

different possible expressions of scedasticity function, which is not possible

with other types of test-statistics.

In econometrics, there have been substantial contributions to assess

robustness while retaining little efficiency, based on minimum DPD estimators

(for example, see Lee and Song (2009), Kim and Lee (2013, 2017, 2018)). To the best of our knowledge, there

are no publications about testing using such estimators, except for goodness-of-fit setting (for example, Kim

(2018)).

Based on minimum DPD estimators, consistent estimators are considered, as well

as unbiased estimating equations. The proposal of this paper is proven to be

theoretically robust two-fold, in constructing the estimators and also the

test-statistic. The main feature of the methodology is on one hand in

achieving robustness through a bounded influence function for estimation and

testing and with an increasing gross error sensitivity as the tuning parameter

increases, while also ensuring an acceptable level of efficiency

through the same tuning parameter approaching . On the other hand,

the Pitman’s asymptotic relative efficiency (ARE) is obtained, which measures

the price, in terms of the relative sample size, to get a particular value of

the asymptotic power when dealing with pure data.

The paper is organized as follows. Based on a new framework of sampling, with

independent but non-identically observations, for composite hypothesis testing

is introduced and motivated in Section 2, by relating it to the

heteroscedastic linear regression model. The main theoretical results are

presented in Section 3, derived the Breusch-Pagan -score LM

tests in Section 4 and influence function analysis in Section

5. A modified version is derived in Section 6, the Koenker’s -score test-statistic.

In Section 7, a practical demonstration of how to handle new tests for heterogeneity in linear regression models is presented using a well-known example. Some concluding remarks are given in Section

8.

Most of the proofs are collected in the Appendix, at the end of the paper.

2 Basic model and testing specifications

Based on the conditional version of the linear regression, the predictors are considered fixed, so the sample of responses , , requires adapting the previous theory presented in Basu et al. (2002) for non-identically distributed individuals. In this setting, being

the true probability density function (p.d.f.) for

, and the p.d.f. under the

model with , the density power divergence of the whole sample is, according to Ghosh

and Basu (2013), given by , where

where is the common support for the sample of all the responses.

In practice, the unknown p.d.f. is approximated through the

empirical one, .

vs., with

(1)

where , with is a composite null hypothesis test. It is assumed the

function which defines to fulfill some regularity conditions,

exists and is continuous in and .

Definition 1

The minimum DPD estimator of , restricted to null

hypothesis established by (1), is obtained as

where

The restricted maximum likelihood estimator (MLE) of

is a member of the minimum DPD estimator, since

Proposition 1

The minimum DPD estimator of , restricted to null

hypothesis established by (1), is obtained as solution in

of the

following system of equations and unknown parameters

(2)

(3)

where is an -vector of Lagrange

multipliers, whose minimum DPD estimator is denoted by and

is the estimating function of the unrestricted minimum DPD estimator of

, where

(4)

The so-called scedastic function, , determines functionally the form of heteroscedasticity but it is not prefixed. It is assumed to be continuous,

to possess at least first and second derivarites and to verify

Definition 2

The conditional heteroscedastic linear regression model is given by

(5)

where and

includes most

of the schemes considered in the literature, for example, the additive scedastic model or the multiplcative scedastic model . The explanatory variables, , , , are assumed to be fixed, i.e.

non-random. In a full matrix notation, (5) is given by

(6)

where

For the heteroscedastic linear model, (5) or (6), the full

parameter vector is given by

(7)

and the hypothesis of homoscedasticity against heteroscedasticity

establishes

(8)

Proposition 2

For the heteroscedastic linear model (5) or (6), the estimating function for the unrestricted minimum DPD estimators

of is given by , where

with

(9)

with

(10)

(11)

Proof. From Martín (2021), taking and Theorem 6, the parameter vector , with , is taken into account. By

following the chain rule of differentiation, we get

where ,

(12)

and finally

with

Corollary 3

For the heteroscedastic linear model, (5) or

(6), the restricted minimum DPD estimators of ,

under homoscedastic null hypothesis, , is obtained as solution of

(13)

(14)

where

(15)

(16)

In addition, the corresponding restricted minimum DPD estimators of the LM

vector is given by

(17)

with

having columns (-vectors) linearly independent of .

Proof. (13) is a direct from Proposition 2, taking

and , while (17) comes

from

In this section we shall focus in a general model such as the one introduced in Section 2. For the particular case of identically distributed observations, the

asymptotic distribution of was known, from Basu et al. (2017). The

following result generalizes the previous one in two ways, extending to

non-identically distributed observations, and also by considering jointly

the estimator of the Lagrange multipliers. In what is to follow, it is assumed to be fulfilled

the regularity conditions given in Basu et al. (2017) based on a single

observation, as well as the existence of the limits of the following two

matrices based on the whole set of observations,

Restricted to the null hypothesis established by (1),

under the existence assumption of (18)-(19), it holds

where the normal distribution has singular variance-covariance with

(20)

(21)

(22)

and

Appendix A covers the proof of Theorem 4. The

original and classical Lagrange multipliers test, published by Aitchison and

Silvey (1958) and Silvey (1959), was for identically distributed

observation, in which taking into account that for ,

is the average Information matrix, the role of these matrices was played by

the Information matrix based on a unique observation. The asymptotic

distribution of is the cornerstone for the following

definition and generalizes the one given in Basu et al. (2022), from which

it is not possible to derive the Breusch-Pagan -score LM tests

presented in Section 4 of the current paper.

Definition 3

The -score Lagrange multipliers test for non-identically

distributed individuals is given by

(23)

where

(24)

is the “empirical sandwich matrix”.

Theorem 5

The asymptotic distribution of (23) is a chi-square

with degrees of freedom.

Large values of the test statistic, on the right hand side tail of , are interpreted as strong evidence against the null hypothesis.

Appendix B covers the proof of Theorem 5.

Theorem 6

Consider the test vs., with

given by (9) and let a sequence of local Pitman-type alternatives be

defined by , with

given by

(25)

being fixed . Under the sequence , the asymptotic distribution of the -score LM

test-statistic for non-identically distributed individuals, (23), is

a chi-square with degrees of freedom and non-centrality parameter

(26)

where

(27)

is the “theoretical sandwich matrix”, the

asymptotic variance-covariance matrix of . The corresponding asymptotic power function, given the nominal

level , is

(28)

where is the Marcum -function (see details in Nuttal, 1975).

From the previous result, the Breusch-Pagan test is consistent under Pitman

alternatives since taking , we get .

The Pitman asymptotic relative efficiency (ARE) of the -score LM

test to the classical LM test is given by

(29)

based on similar ideas taken from Hannan (1956) and Koenker and Bassett

(1982).

As particular case of Definition 3, we get the following version.

Proposition 7

Let us consider the particular case of and , with and

being asymptotically independent

and is a proportional

matrix, with respect to ,

within the block correspondent to . Then, the -score Lagrange multipliers test for non-identically distributed individuals,

given in (23), has the following simpler expression

(30)

where

4 Derivation of the Breusch-Pagan -score LM tests

Focussed on the matrix version of Definition 3, let us consider the extended design matrix of the scedasticity function,

and the corresponding rows,

, . We shall assume that

,

and

(31)

where denotes the minimum eigenvalue of a matrix.

Using the full parameter given in (7), the hypothesis of

homoscedasticity against heteroscedasticity, (8), belongs to the

particular case of Theorem 7 with playing

the role of and the role of . The current section is

mainly devoted to calculate and .

Theorem 8

For the heteroscedastic linear model, (5) or (6),

under homoscedastic null hypothesis, it holds

can be obtained from Martín 2020, Corollary 4. Finally, from the desired expression of (32) is obtained. The expression of (33) is obtained in a similar way.

Remark 1

The assumptions given in (31) arise as application of the multivariate

Lindeberg Central Limit Theorem (CLT) to the estimators obtained as solution of the

estimating equations given in Proposition 2, with weaker

assumptions for the errors, just only considering null mean and finite variance.

Theorem 9

The Pitman ARE of the Breusch-Pagan -score LM

test-statistic (with respect to the classical one, ) for the

heteroscedastic linear model (5) or (6) is given by

(37)

Proof. From Theorem 8 and equation (29), we get the ARE to be .

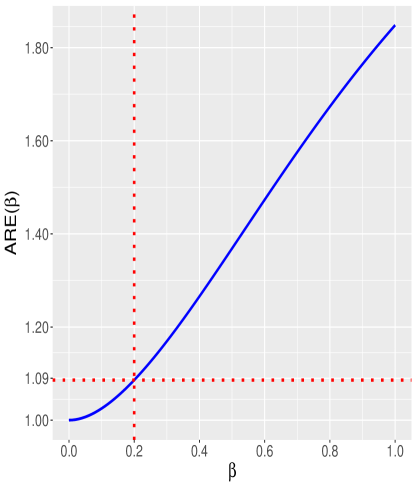

The expression given in (37), for pure normally distributed data, depends only on

(there is no dependence on , or

), being actually increasing on (see Figure

1). This means that, as it happens usually with the minimum DPD estimators,

the most efficient test-statistics are the ones closer in the value of

to the classical one, . It is observed that the ARE is at

, hence for , needs about additional

observations to get the same power as .

Figure 1: Asymptotic Relative

Efficiency for the Breusch-Pagan -score LM test-statistic.

Corollary 10

The Breusch-Pagan -score LM test-statistic for the

heteroscedastic linear model, (5) or (6), is given by

(38)

with given by (16). Once the two conditions established by (31) are verified,

the test-statistic, (38), is asymptotically a chi-square random

variable with degrees of freedom under homoscedastic null hypothesis.

Proof. From Theorem 7, we can use (30) rather than

(23). The matrix of the quadratic form to be inverted needs a

previous block matrix inversion and selection of its upper-left

block, i.e.

with

according to Lu and Shiou (2002, Theorem 2.1.-(ii)). From (16) and

(17), we have

and the final expression (38) is followed from Theorem A.45 in Rao

et al. (2008, page 503).

Remark 2

The classical Breusch-Pagan LM test-statistic (),

(39)

matches (5.17) of Godfrey (1989, page 128). This expression justifies the

two-fold ordinary least squares (OLS) regression procedure for the computation

of the classical Breusch-Pagan LM test-statistic. The most general

interpretation for the new proposal is also easily deducted. The value of the

Breusch-Pagan -score LM test-statistic is based on a projection of

, a vector

constructed from the vector of squared standardized -residuals,

, taking

as response to be adjusted in the linear regression model,

with as design matrix. Such a projection is on the vector

space of dimension , generated by the columns of , whenever . The practical procedure is as follows:

“The value of (38) can be calculated as the

explained sum of squares from the OLS regression of the response

over the matrix of

explanatory variables , multiplied by ”.

5 Influence Function Analysis

The influence function approach was introduced in Hampel (1968, 1974) for

estimators, being in essence based on the Gateaux derivative of a

functional. It was fully developed in Hampel et al. (1986). It is the most

important tool to analyze the robustness of statistical procedures, due to

its adaptability to analyze either robustness of estimators or

test-statistics.

In this section we are going to introduce the second order influence

function of the -score LM test-statistics for non-identically

distributed observation. The following scheme will be followed. We will

calculate first the influence function of the minimum DPD estimator of the

LM, under the null hypothesis, and based on it, later, the influence

function of the -score LM test-statistics is obtained. To fully

justify the robustness of the test-statistic, in principle it is not enough

with analyzing the raw influence function, it requires to prove in addition

the stability of the significance level and power of the -score LM

test-statistics under data contamination.

Let denote funcional associated with

, where is the vector of true distribution

observation-by-observation in the sample, , . Under the

assumption that the true distribution belongs to the parametric model

associated with the homoscedastic linear regression, the same vector is

denoted by .

Theorem 11

The -score LM tests for non-identically distributed

individuals, has the usual first-order influence function equals zero, and

its second-order influence function, or self standardized IF of , is given by

(40)

where

(41)

Taking into account that is bounded, for any , then it is fulfilled

that for any , is bounded with respect to the -th observation for , and the higher the value of , the outliers suffer

from a greater down-weighting effect. For the classic score tests (), is

unbounded because is

unbounded. The influence function of all the observations is bounded if only

if the influence functions associated with pairs of individuals are all

bounded, i.e. the influence function of all the observations is bounded if

only if . The gross-error sensitivity (GES) of for a sample of non-identically

distributed observations is defined as

where the GES of for

the -th individual, , matches the square of the so-called self

standardized GES of , , or . A finite (an

infinite) GES implies a bounded (an unbounded) second order influence

function of . Different

parameterizations yield a unique value of , self standardized IF and self standardized GES

(introduced for the first time in Krasker and Welsch, 1982). This is the

so-called invariance property of the Rao-type test statistics, not fulfilled

by other commonly used test-statistics such as the likelihood ratio and Wald

type tests.

Corollary 12

In the particular case of and ,

the -score LM test for non-identically distributed individuals,

given in (23), has the second-order influence function (40),

where

(42)

and

Based on , with , we shall consider the -contaminated distribution

function under a sequence of local Pitman-type alternatives, with respect to

the degenerated distribution function, ,

Theorem 13

For the -contaminated distribution

function and under a sequence of local Pitman-type alternatives , with given by (25), the -score LM test-statistics for non-identically

distributed individuals, , is asymptotically a chi-square random variable with degrees of freedom an noncentrality parameter

by (40). Moreover, the corresponding asymptotic power function, given the

nominal level , is

(45)

where is the Marcum -function.

The (asymptotic) power IF is defined as

Theorem 14

For the -contaminated distribution function and

under a sequence of local Pitman-type alternatives , with given by (25),

the power inflluence function of the -score LM test-statistics for

non-identically distributed individuals, , with nominal level ,

is given by

We may observe that the boundedness of the PIF is equivalent to the

boundedness of the IF of the minimum DPDs of parameter . In fact, it is well-known, that the IF is bounded for and

unbounded for .

Taking and , since , based on , we shall consider to be the -contaminated distribution function under the null hypothesis and

In this setting, , which indicates a null IF of the

significance level.

Example 15

For the Breusch-Pagan -score LM test-statistics, the second order

influence function is

where

It is fulfilled that for any , is bounded with respect to ,

but unbounded for the classical Breusch-Pagan score LM test (). In

addition, leverages do not affect negatively on the second order influence

function for the Breusch-Pagan -score LM tests since the first

factor is bounded with respect to and the second

factor is also bounded with respect to . In particular,

for the simple linear regression, with , ((31) is verified), , , , being the true

model, we get

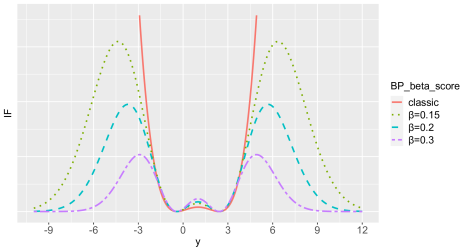

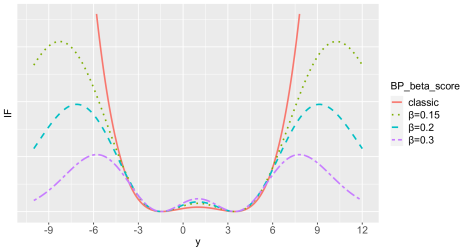

In Figure 2 the second order IFs are plotted when , ,and . On the left and right

hand tails of the curves associated with , the down-weighting

effect is clearly visualized while for the curve increases

indefinitely. The maximum of the curves is reached at a double solution on of , concluding

(46)

a decreasing function on , being finite only for . Since for , the stability of the classical Breusch-Pagan LM test-statistic

breaks down completely with outliers, while robustness of the Breusch-Pagan -score LM test-statistic increases (GES decreases) as

increases.

(a)Case:

(b)Case:

Figure 2: for the Breusch-Pagan -score LM

tests of a simple linear regression.

6 Koenker’s -score test-statistic

Koenker (1981) extended the Breusch-Pagan test-statistic to make

it applicable also for non-normally distributed errors. Multiplying the

original Breusch-Pagan test-statistic by a constant, the new proposal was

found to have the same asymptotic distribution, with a new OLS interpretation

and relationship with the sample kurtosis. Similarly, we shall extend the

Breusch-Pagan -score LM test in what we call the Koenker’s -score test. For the classical Breusch-Pagan test (), the average of

the cross-product of the estimating function is

where is a

consistent estimator of the theoretical Kurtosis coefficient of the -th

error (under the null hypothesis of homoscedasticity), i.e. . In the genuine linear homoscedastic

regression, i.e. when , it holds the theoretical Kurtosis coefficient to be .

Hence, it is almost straightforward to see that if we replace by

in the

denominator of (39), we get the Koenker’s test-statistic

(47)

In the same vein, the Koenker’s -score test-statistic is defined as

(48)

where

Corollary 16

The Koenker’s -score test-statistic for the

heteroscedastic linear model (5) or (6), given by

(48), follows asymptotically a chi-square distribution with

degrees of freedom.

Proof. From the Weak Law of the Large Numbers (WLLN) and taking into account that

, it holds

(49)

where , with

being the moment generating function of

, valid among other values, for

, and under normality of the errors. Taking into account that

(49) implies

with Corollary 10 and the Slutsky’s theorem, the desired result

is obtained.

The calculation of (48) can be made though a proper

interpretation of the least squared method as follows. It is times the

determination coefficient calculated from the linear regression of

, as response, over

explanatory variables given by . Hence, it remains

having the original appealing interpretation for the classical Koenker’s

test-statistic. In Corollary 16, the validity of its asymptotic

distribution has been justified for normally distributed errors, in a similar

way done in Koenker (1981). Taking into account that the classical Koenker’s

test, for non-normally distributed observations, was proven in a quantile

regression framework (see Koenker, 1982), the most general validity of the

asymptotic distribution of (48) will be now justified. The

normality assumption of the error, (11), of the linear regression model, (5), can

be weakened to any centered distribution with finite variance, having second

order derivative of the moment generating function for the square of the

standardized errors.

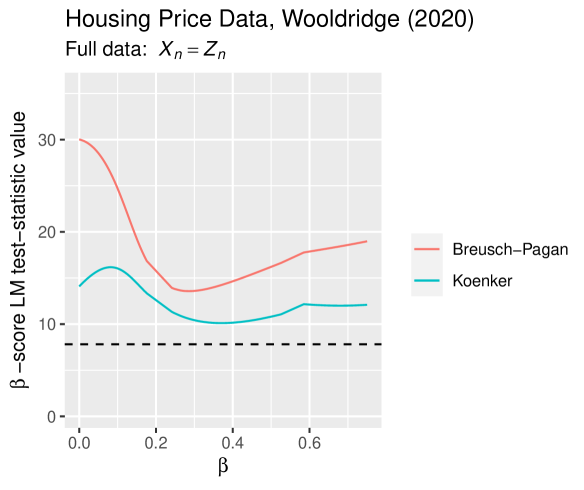

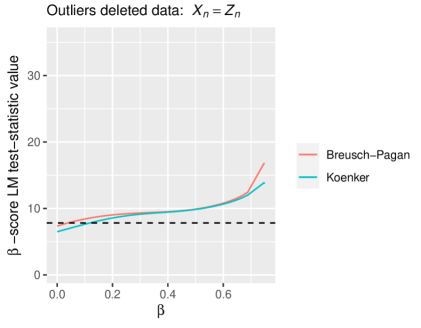

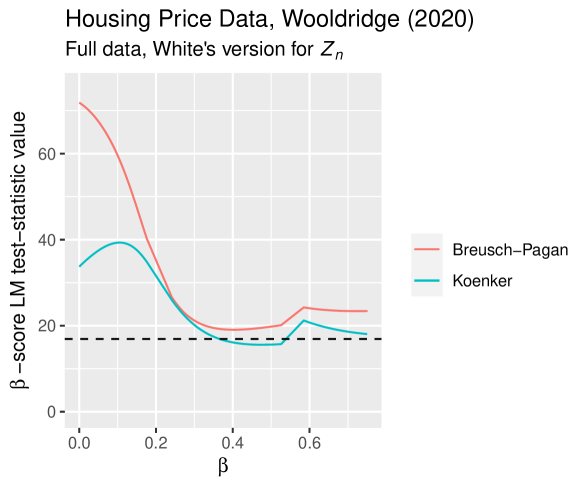

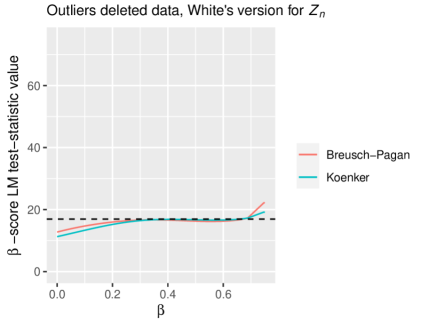

7 Example: Housing Price Data

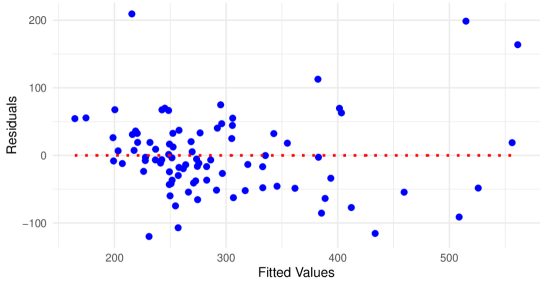

Within the wooldridgeR package, the dataframe hprice1 is related to a well-known example in Econometrics from Wooldridge (2020), which is referred to as the Housing Price Data. The dataset includes observations of 88 individuals and contains 10 variables, representing housing characteristics and sales information for houses sold in the Boston area, and it was collected from a publicly available database, published in 1990. We consider the heteroscedastic linear model (5), price bdrmslotsizesqrft, where price is the house price, in thousands of dollars (), bdrms, the number of bedrooms (), lotsize, the size of lot in square feet (), sqrft, the size of house in square feet (). Figure 3 suggests the presence of three outliers with the largest value of residuals, the observations with identification numbers , and in the dataframe.

Figure 3: Residual plot for the Housing Price Data for estimation under OLS or MLEs ().

An extensive study of the performance of the Breusch-Pagan and Koenker’s -score LM test-statistics, and respectively with tuning parameter interval , has been performed taking in consideration either the full data or the outliers deleted data, dropping the three observations mentioned previously. We shall focus our attention on two different sources of heteroscedasticity depending on the choice of , . The case , (), is the one considered in Figure 4 and the left hand sides of Tables 1-2, while in Figure 5 and the right hand sides of Tables 1-2 the White’s additive heteroscedastic model is taken into account,

with , being the half vectorization of matrix , and . In the last section of the Appendix several computational details are given, useful for both estimation and test-statistics. Based on the quantile of the with being or depending on the choice of source of heteroscedasticity, the dashed line In Figures 4-5 is indicating the threshold for rejection of the test, considering the asymptotic distribution.

The motivation behind this example is the suspicion of being made a non-appropriate decision with the classical tests, the ones with . With both classical tests under consideration, the null hypothesis of homoscedasticity is clearly rejected, while it is accepted when deleting outliers. Our purpose is to provide further insight in the decision to be made, based on the study of the newly proposed test-statistics along the complete tuning parameter interval . The strength of and , when , is their damping effect in presence of outliers, and therefore avoiding the deletion of outliers. It is however, for illustrative purposes, interesting to analyze and compare the behaviour of the test-statistics when dropping outliers.

In view of the plots shown in Figure 4 and the left hand sides of Tables 1-2, we find enough evidence to reject the null hypothesis of homoscedasticity with significance level but in view of Figure 5 and the right hand sides of Tables 1-2 it is not so clear for both test-statistics since the Koenker’s -score

LM test-statistic, when , is in the acceptance region. However, if we consider significance level, both test-statistics are in favour of the same decision of rejecting along the whole tuning parameter interval . This decision is not consistent with the one made in Berenguer-Rico and Wilms (2021). Indeed, the approach behind their proposal is different as well, since the method is constructed under the preference of dropping outliers from data.

case

White’s version of

1.364e-06

3.501e-03

4.6799e-04

6.559e-12

1.179e-02

0.0128

2.782e-03

1.526e-02

6.9919e-03

9.952e-05

1.684e-02

0.0137

Table 1: p-values of the Breusch-Pagan and Koenker’s -score

LM test-statistics, with full Housing Price Data.

case

White’s version of

0.0615

0.0252

0.0041

0.1743

0.0550

0.0618

0.0898

0.0275

0.0138

0.2576

0.0582

0.0548

Table 2: p-values of the Breusch-Pagan and Koenker’s -score

LM test-statistics, with outliers deleted Housing Price Data.

Figure 4: Breusch-Pagan and Koenker’s -score LM test-statistics for the Housing Price Data and the case .

Figure 5: Breusch-Pagan and Koenker’s -score LM test-statistics for the Housing Price Data and White’s version of .

8 Concluding remarks

This paper proposes Breusch-Pagan -score LM tests for heterogeneity

in linear regression models. Prior to the proposal, the needed general

theory for its derivation has been developed over a framework of composite

null hypothesis with independent but non-identically distributed

observations, since Basu et al. (2022) did only consider identically

distributed observations. The Breusch-Pagan -score LM

test-statistics depend on a tuning paramater and the case is obtained as a limit of from the cases

. This family of test-statistics considers the classical

Breusch-Pagan LM test (Breusch and Pagan, 1979) as a particular case, being

just the case . Efficiency and the robustness can be balanced

through the tuning parameter , being the most

efficient one, useful in case of having clean data free from outliers, while

robustness in the test-statistic is gained by increasing the value of , convenient in case of having outliers. A compromise between efficiency

and the robustness is reached by selecting properly an appropriate value of

the tuning parameter.

Since Koenker (1981) published a modified version, robust against normality

assumption, this one remains being a reference of robustness, but our paper

fill the gap of proposing a specific test robust from outliers. The

challenge of generalizing our proposed -score LM tests for

heterogeneity to be resistant from both simultaneously, normality assumption

and outliers, has been in addition addressed through the Koenker’s -score test.

When outliers are present in the data, in order to avoid results derived

from a biased and inefficient version of the classical Breusch-Godfried LM

test, based on Breusch (1978) and Godfrey (1978b), we are currently involved

in an ongoing paper which proposes -score LM tests for testing

autocorrelation in the errors of a linear regression models. Apart from the aforementioned open problem, and based on the ideas

inherited from Breusch and Pagan (1980), the current paper could be the key

and reference for further challenging research on new applications of the -score LM test for non-identically distributed individuals, useful in

Econometrics. In this regards, recently Halunga et al. (2017) have proposed

a robust version, against heteroscedasticity, of the Breusch-Pagan test for the null hypothesis of

zero cross-section correlation in dynamic panel data. Even though the model is

different and also the robust technique compared with our proposal, they comment “If

the null is not rejected by the test, it would be more confidently concluded

that the rejection is not due to the heteroscedasticity, and OLS estimation

would be preferred. If the null is rejected, then a suitable estimation

procedure should be pursued”, which suits quite perfectly

in the context of the model in our paper and -score LM tests could

be an attractive alternative methodology.

References

[1] Alih, E. and Ong, H.C. (2015). An outlier-resistant test for

heteroskedasticity in linear models. Journal of Applied Statistics,

42, 1617–1634.

[2] Aitchison, J. and Silvey, D.S. (1958). Maximum-Likelihood

Estimation of Parameters Subject to Restraints. The Annals of

Mathematical Statistics, 29, 813–828.

[3] Athreya, K.B. and Lahiri, S.N. (2006). Measure Theory

and Probability Theory. Springer-Verlag.

[4] Basu, A., Ghosh, A., Martin, N., and Pardo, L. (2022). A

Robust Generalization of the Rao Test. Journal of Business & Economic

Statistics, 40, 868–879.

[5] Basu, A, Harris, I.R., Hjort, N.L. and Jones, M.C. (1998).

Robust and efficient estimation by minimising a density power divergence.

Biometrika, 85, 549–559.

[6] Basu, A., Mandal, A., Martin, N., and Pardo, L. (2017).

Testing Composite Hypothesis Based on the Density Power Divergence. Sankhya B. 80, 222–262.

[7] Basu, A., Shioya, H., and Park C. (2011). Statistical

Inference: The Minimum Distance Approach. Boca Raton, CRC Press

[8] Beran, R. J. (1977). Mínimum Hellinger distance

estimates for parametric models. The annals of Statistics, 5, 445–463.

[9] Berenguer-Rico, V. and Wilms, I. (2021).

Heteroscedasticity testing after outlier removal. Econometric Reviews, 40, 51–85.

[10] Bickel, P.J. (1978). Using residuals robustly I: Tests for

heteroscedasticity and non-linearity. Annals of Statistics, 6,

266–291.

[11] Breusch, T. S. (1978). Testing for Autocorrelation in Dynamic

Linear Models. Australian EconomicPapers, 17, 334–355.

[12] Breusch, T.S. and Pagan, A.R. (1979). A simple test for

heteroscedasticity and random coefficient variation. Econometrica,

47, 1287–1294.

[13] Breusch, T.S., and Pagan, A.R. (1980). The Lagrange

multiplier test and its applications to model specification in econometrics.

The Review of Economic Studies, 47, 239–253.

[14] Boos, D. D. (1992). On Generalized Score Tests. The

American Statistician, 46, 327–333.

[15] Carrol, R.J. and Ruppert, D. (1988). Transformation

and Weighting in Regression. CRC Press.

[16] Cook, R. D. and Weisberg, S. (1983). Diagnostics for

heteroscedasticity in regression. Biometrika, 70, 1–10.

[17] Cressie, N. and Read, T.R.C. (1984). Multinomial

goodness-of-fit tests. Journal of the Royal Statistical Society.

Series B, 46, 440–464.

[18] Csiszár, I. (1967). Information-type measures of

difference of probability distributions and indirect observations. Studia Scientiarum Mathematicarum Hungarica, 2, 299–318.

[19] Ghosh, A. and Basu, A. (2013). Robust estimation for

independent non-homogeneous observations using density power divergence with

applications to linear regression. Electronic Journal of Statistics,

7, 2420–2456.

[20] Ghosh, A., Mandal, A., Martín, N. and Pardo, L.

(2016). Influence analysis of robust Wald-type tests. Journal of

Multivariate Analysis, 147, 102–126.

[21] Godfrey, L.G. (1978a). Testing for multiplicative heteroscedasticity.

Journal of Econometrics, 8, 227-236.

[22] Godfrey, L.G. (1978b). Testing Against General

Autoregressive and Moving Average Error Models when the Regressors Include

Lagged Dependent Variables. Econometrica, 46, 1293–1301.

[23] Godfrey, L. G. (1989). Misspecification Tests in

Econometrics: The Lagrange Multiplier Principle and Other Approaches.

Cambridge University Press, New York.

[24] Halunga, A.G., Orme, C.D, Yamagata, T. (2017). A

heteroskedasticity robust Breusch-Pagan test for Contemporaneous correlation

in dynamic panel data models. Journal of Econometrics. 198, 209–230.

[25] Hampel, F.R. (1968). Contribution to the theory of

robust estimation. Ph.D. Thesis, University of California, Berkeley.

[26] Hampel, F.R. (1974). The influence curve and its role in

robust estimation. Journal of the American Statistical Association,

69, 383–393.

[27] Hampel, F.R., E.M. Ronchetti, P.J. Rousseeuw, and W.A.

Stahel (1986). Robust Statistics: The Approach Based on lnfluence

Functions. Wiley, New York.

[28] Hannan, E.J. (1956). The Asymptotic Powers of Certain Tests

Based on Multiple Correlations. Journal of the Royal Statistical

Society. Series B, 18, 227–233.

[29] Honda, Y. (1988). A size correction to the Lagrange

multiplier test for heteroskedasticity. Journal of Econometrics,

38, 375–386.

[30] Kalina, J. (2011) Testing heteroscedasticity in robust

regression. Research Journal of Economics Business and ICT, 4, 25–28.

[31] Kim, B. and Lee, S. (2013). Robust estimation for copula Parameter in SCOMDY

models. Journal of Time Series Analysis, 34, 302–314.

[32] Kim, B. and Lee, S. (2017). Robust estimation for zero-inflated Poisson

autoregressive models based on density power divergence. Journal of

Statistical Computation and Simulation, 87, 2981–2996.

[33] Kim, B. and Lee, S. (2020). Robust estimation for general integer-valued time

series models. Annals of the Institute of Statistical Mathematics, 72(6), 1371-1396.

[34] Kim, B. (2018). Robust maximum entropy test for GARCH models based on a

minimum density power divergence estimator. Economics Letters, 162, 93–97.

[35] Lee, S. and Song, J. (2009). Minimum density power divergence estimator for

GARCH models. TEST 18, 316–341.

[36] Koenker, R. (1981). A note on Studentizing a test for

heteroscedasticity. Journal of Econometrics, 17, 107–112.

[37] Koenker, R. and Bassett, G. (1982). Robust tests for

heteroscedasticity based on regression quantiles. Econometrica,

50, 43–61.

[38] Koenker, R., and Bassett, G. (1982). Tests of Linear

Hypotheses and Estimation. Econometrica, 50,

1577–1583.

[39] Krasker, W.S. and Welsch, R.E. (1982). Efficient bounded

influence regression estimation. Journal of the American Statistical

Association, 77, 595–604.

[40] Kolmogorov, A. N. (1933). Sulla determinazione empirica

di una legge di distribuzione. Giornale dell’Istituto Italiano degli

Attuari, 4, 83-91.

[41] Kmenta, J. (1986). Elements of Econometrics.

Macmillan.

[42] Lyon, J. D. and Tsai, C.L. (1996). A Comparison of Tests for

Heteroscedasticity. Journal of the Royal Statistical Society. Series D

(The Statistician), 45, 337–349.

[43] Lu, T. T. and Shiou, S. H. (2002). Inverses of

block matrices. Computers & Mathematics with Applications, 43, 119–129.

[45] Mahalanobis, P. C. (1936). On the generalized distance

in statistics. Proceedings of the National Institute of Science of

India, 2, 49–55.

[46] Markatou, M., Karlis, D., and Ding, Y. (2021).

Distance-Based Statistical Inference. Annual Review of Statistics and

Its Application, 8, 301–327.

[47] A. Nuttall (1975). Some integrals involving the function. IEEE Transactions on Information Theory, 21,

95–96.

[48] Pardo, L. (2006). Statistical inference based on divergence

measures. Chapman and Hall/CRC.

[49] Rao, C. R., Toutenburg, H., Shalabh and Heumann, C. (2008).

Linear Models and Generalizations. Least Squares and Alternatives.

Springer.

[50] Salibian-Barrera, M., Van Aelst, S. and Yohai, V.J.

(2016). Robust tests for linear regression models based on -estimates. Computational Statistics & Data Analysis, 93,

436–455.

[51] Silvey, S.D. (1959). The Lagrangian Multiplier Test. The Annals of Mathematical Statistics, 30, 389–407.

[52] Waldman, D.M. (1983). A note on algebraic equivalence of White’s test and a

variation of the Godfrey/Breusch-Pagan test for heteroscedasticity.

Economics Letters, 13, 197–200.

[53] White. H. (1980). A heteroscedasticity-consistent covariance matrix estimator

and a direct test for heteroscedasticity. Econometrica, 48, 817-838.

We shall follow a similar scheme to Davidson and MacKinnon (2021, page 275),

in Section 8.9 devoted to the classical LM test, but adapted to independent

and non-identical individuals and DPD based estimating functions. We may

start by considering the Taylor expansion of at the point for

we get

This yields

Adjusting the left hand side expression according to (2) and taking

into account the Markov’s WLLN

it holds

(50)

On the other hand, from the Taylor expansion of at the point ,

and under the existence assumption of (18)-(19) it is

also verified the the following the multivariate version of the Lindeberg CLT for independent non-identically

distributed observations,

(53)

In view of the expression given in Definition 3 for , this is just the estimator of

the variance for a centered sample, which is justified as follows

where , . The expression , is straightforward from

established in Basu et al. (1998) for identically distributed observations.

Finally, from (52)-(53) the desired result is obtained.

The influence function associated with all the individuals for the Lagrange

multiplier, is given by a function such that

where

(56)

i.e.

Appendix E Computational considerations for obtaining the Breusch-Pagan and Koenker’s -score test-statistics

In this section we provide some details about the followed methodology for computation, taking in consideration some mathematical tools as well as some details about the R code.

E.1 Case:

E.1.1 MLE of ,

Let us consider the Cholesky decomposition of , i.e. where is an lower triangular matrix . Considering the system of

equations

(57)

to be solved in two steps

being the first one forward substitution and the second one backward

substitution.

E.1.2 Classical Breusch Pagan and Koenker’s test-statistics

Let us consider , , and . We must derive an ANOVA of

where

is the element wise product of two vectors, is the solution of . Then

are respectively the classical Breusch Pagan and Koenker’s test-statistics,

which are asymptotically a chi-square random variable with degrees of

freedom (number of columns of full rank matrix ). Under

non-normal errors, the same asymptotic distribution of remains being valid but does not need to tend to almost surely. The value of is an estimation of the Kurtosis minus of the errors distribution.

E.2 Case:

E.2.1 Minimum DPD estimation of ,

The solution of

(58)

where

will be recursively obtained. (58) will be solved in the same way as

(57), taking

In each iteration is updated solving in terms of , i.e. , where

(59)

will be updated.

The -th iteration is just to get or . The -th iteration consists on

updating

and , solving the

system of equations (based on , ) to get , update of solving a non-linear equation with a unique variable and checking

whether the norm of is less than a pre-specified tolerance level.

If so, the sequence of iterations stops, if not the sequence goes ahead. The

system of linear equations can be efficiently solved using the base R

function solve() to solve linear equations, once the Cholesky

decomposition is properly suited according to the indications given

previously:

The non-linear equation can be efficiently solved utilizing the R

package nleqslv (Klein and Sporleder (2020), version 0.8-2,

installed on 2020-12-01.), as it enables the attainment of a solution within

a minimal number of iterations. It needs providing (59) and

E.2.2 Breusch-Pagan and Koenker’s -score

test-statistic

In a similar way done for the classical ones, we get

Therefore, once we have calculated , the scheme to be followed is exactly the same as the one we have followed for

the classical tests and it is easily calculated from the well-known ANOVA

for OLS, hence the ln() function and related ones of R can be used.

Appendix References

[1] Davidson, R., and MacKinnon, J. G. (2021). Estimation and Inference in Econometrics. Oxford University Press, New York.

[2] Klein, S. and Sporleder, C. (2020). nleqslv: Solve Nonlinear

Equations and systems of Equations. R package version 0.8-2. https://CRAN.R-project.org/package=nleqslv