Unconditional Quantile Partial Effects via Conditional Quantile Regression††thanks: Alejo: IECON-Universidad de la Republica, Montevideo, Uruguay. E-mail: javier.alejo@fcea.edu.uy; Galvao: Department of Economics, Michigan State University, E-mail: agalvao@msu.edu; Martinez-Iriarte: Department of Economics, UC Santa Cruz. E-mail: jmart425@ucsc.edu; Montes-Rojas: IIEP-BAIRES-CONICET and Universidad de Buenos Aires. E-mail: gabriel.montes@economicas.uba.ar. We thank the Editor, Xiaohong Chen, the Associate Editor, anonymous referees, and Michael Jansson, Michael Leung, Jessie Li, Blaise Melly, Yixiao Sun, Takuya Ura, and seminar participants at UC Irvine, MSU, NY Camp Econometrics XVII, CFE-CMStatistics 2022, Econometric Society European Meeting 2023, SEA 93rd Annual Meeting, and 1st Workshop on Quantile Regression in Rome for very helpful and constructive comments. Computer programs to replicate the numerical analyses are available from the authors. All remaining errors are our own.

Abstract

This paper develops a semi-parametric procedure for estimation of unconditional quantile partial effects using quantile regression coefficients. The estimator is based on an identification result showing that, for continuous covariates, unconditional quantile effects are a weighted average of conditional ones at particular quantile levels that depend on the covariates. We propose a two-step estimator for the unconditional effects where in the first step one estimates a structural quantile regression model, and in the second step a nonparametric regression is applied to the first step coefficients. We establish the asymptotic properties of the estimator, say consistency and asymptotic normality. Monte Carlo simulations show numerical evidence that the estimator has very good finite sample performance and is robust to the selection of bandwidth and kernel. To illustrate the proposed method, we study the canonical application of the Engel’s curve, i.e. food expenditures as a share of income.

Keywords: Quantile regression, unconditional quantile regression, nonparametric regression.

JEL: C14, C21.

1 Introduction

Conditional quantile regression (CQR) is a general approach to estimate conditional quantile partial effects (CQPE), i.e., the effect of a covariate variable of interest (ceteris paribus) on the conditional quantile distribution of the outcome.111 See, e.g., Koenker and Bassett (1978); Koenker and Hallock (2001); Koenker (2005); Koenker, Chernozhukov, He, and Peng (2020) for comprehensive analyses of CQR. CQR is a useful way to represent heterogeneity using a set of parameters to characterize the entire conditional distribution of an outcome variable given a list of observable covariates.

Recently, unconditional quantile regression (UQR), proposed by Firpo, Fortin, and Lemieux (2009), has attracted interest in both applied and theoretical literatures. UQR is an important tool for practitioners since it provides a method to evaluate the impact of changes in the distribution of the explanatory variables on quantiles of the unconditional (marginal) distribution of the outcome variable. This method allows researchers to investigate important heterogeneity in the variable of interest. Naturally, UQR leads to the unconditional quantile partial effect (UQPE), which refers to the effect of a covariate (ceteris paribus) on the unconditional quantile distribution of the outcome variable.222Conditional here means that one is conditioning on a set of observable variables, while partial means that one is looking at the effect of one particular covariate controlling for the rest of the covariates. On the other hand, Conditional Quantile Regression (CQR) and Unconditional Quantile Regression (UQR) refer to two regression methodologies to estimate CQPE and UQPE, respectively. Sometimes the acronym of the method is informally interchanged with the parameter of interest, and, therefore, can be somewhat confusing if read lightly.

Firpo, Fortin, and Lemieux (2009) propose several ways to estimate the UQPE. The most popular approach is the recentered influence function (RIF) regression method, commonly referred to as RIF regression. It is a two-step procedure, where in the first stage one estimates the RIF, and in the second step, a standard OLS regression of the RIF on covariates estimates the UQPE. While the method is appealing due to its simplicity, it relies on ability of the researcher to specify a regression equation for the influence function, a relatively abstract object. Firpo, Fortin, and Lemieux (2009, p.959) also show an important theoretical result connecting CQPE and UQPE that, when considering a continuous covariate, the UQPE can be expressed as an unconditional weighted average of the CQPE. Derivation of this result relies on a function that matches the conditional quantile whose values are the closest to the unconditional quantile.

This paper builds on this relationship between CQPE and UQPE and suggests an alternative method for estimation of UQPE using simple CQR methods. The procedure is based on the identification result of UQPE that explores information contained in the CQPE. Since estimation of conditional density function is a high dimension object, we first slightly modify the result in Firpo, Fortin, and Lemieux (2009) to show that the UQPE can be written as a conditional average of the CQPE effects (evaluated where unconditional and conditional quantiles are equal), given the outcome variable (evaluated at the unconditional quantile). Hence, by starting with the common assumption of linearity of the quantile process, a simple reweighting of the CQR coefficients using a ratio of conditional and unconditional density functions delivers the UQPE.333In this paper we focus on a first stage quantile regression, but the model can be extended to non-linear models. An alternative is to employ distribution regression of Chernozhukov, Fernández-Val, and Melly (2013). Thus, a useful by-product of the CQR analysis is the ability to express UQPE, for a given quantile , as a function of CQR.444Other procedures where statistics of interest are based on a combination of CQR coefficients are the following: Bera, Galvao, Montes-Rojas, and Park (2016) propose to estimate a unique representative CQPE based on an asymmetric Laplace framework, and Lee (2021) considers a general weighted average quantile derivative using the CQR coefficients for a fixed quantile level.

We propose a new two-step semi-parametric estimator based on this identification result that employs CQR coefficients to estimate the UQPE. The practical implementation is simple and makes use of the usual practice in empirical research of estimating the CQR process, that is, many quantiles, to explore heterogeneity in conditional effects of a certain covariate. In the first step one uses standard linear QR methods to estimate CQPE from the conditional model of interest over a grid of -quantiles, and also estimates the unconditional -quantile of the outcome of interest. Then, for a given value of the covariates, a matching function can be applied to select coefficients such that unconditional and conditional quantiles are equal. This matching function estimator is analogous to the QR estimator of the conditional CDF proposed by Chernozhukov, Fernández-Val, and Melly (2013) in the context of counterfactual distributions. In the second step, one employs a nonparametric regression of the matched CQR coefficients on the outcome, and evaluates this at the unconditional -quantile. This is a one-dimensional (reverse) regression: the regressor is the outcome. Mild sufficient conditions are provided for the two-step estimator to have desired asymptotic properties, namely, consistency and asymptotic normality. We derive the convergence rate of the estimator and show that, as expected, it converges at a standard nonparametric rate.

The proposed method offers important advantages over available techniques to compute UQPE. First, an important motivation and advantage of this paper is to compare and contrast the conditional and unconditional quantile effects. Along these lines, the proposed methods do not require additional modeling assumptions to obtain the UQPE in addition to the CQPE conditions. Since UQPE is nonparametrically identified, the modeling assumptions for both cases would be the same, hence, while the results could still be affected by misspecification of the CQR model, potential differences between UQPE and CQPE results are not be driven by modeling choices.

Second, our framework provides the researcher with a simple structural conditional quantile model to study, which facilitates the understanding of identification. The conditional QR model in the first step allows for a simple and intuitive modelling framework. It is familiar to model the main output variable as a function of the covariates using CQR. On the other hand, in the second stage of RIF-OLS and RIF-Logit, one needs to model the effect of covariates on the conditional average of the RIF, which is difficult to conceptualize. There is, thus, a risk of misspecifying the regression in the second stage. In our proposed method, covariates enter the structural CQR in standard way, i.e., the dependent variable of interest is a function of covariates, in the first step. This approach may be simpler for the researcher since the CQR could be specified using the previous literature or the economic theory. Naturally, the price to be paid is the linearity of the CQR in the first step.

Finally, there have been considerable extensions on CQR modeling, such as, for example, models for panel data, endogeneity, and large number of covariates (see, e.g., Koenker, Chernozhukov, He, and Peng (2020)). Extensions of the proposed UQPE methods to encompass these situations might be simpler, relative to other existing methods, and are left for future research.

Related Literature. Although the literature on applications of UQR methods is extensive, the literature on theoretical developments is relatively small. Rothe (2010, 2012) generalize the method of Firpo, Fortin, and Lemieux (2009), for other recent developments, see, e.g., Inoue, Li, and Xu (2021), Sasaki, Ura, and Zhang (2022), Martinez-Iriarte, Montes-Rojas, and Sun (2022), Martinez-Iriarte and Sun (2022), and Martinez-Iriarte (2023). For a comprehensive survey on counterfactual distributions and decomposition methods, see Fortin, Lemieux, and Firpo (2011). Moreover, in a related work, Chernozhukov, Fernández-Val, and Melly (2013) propose to use distributional regression to compute conditional CDF and estimate general counterfactual distributions. It is possible to obtain the UQPE from this methodology by differentiating the estimated CDF, and then integrating the covariates. Another branch of the literature related to this paper uses a combination of standard CQR with simulation exercises to evaluate distributional effects, such as UQPE. While it is feasible to calculate the unconditional distribution of an outcome variable using CQR (see, e.g., Autor, Katz, and Kearney (2005), Machado and Mata (2005), Melly (2005), and Chernozhukov, Fernández-Val, and Melly (2013)), this task is not obvious, at least compared to the ordinary least-squares (OLS) for the conditional mean. Since an analogue of the law of iterated expectations does not hold in the case of quantiles (de Castro, Costa, Galvao, and Zubelli (2023)), the CQR analysis cannot be directly employed to analyze unconditional quantiles (see the discussion in Fortin, Lemieux, and Firpo, 2011).

The remaining of the paper is organized as follows. Section 2 presents the main result that motivates the UQPE estimator based on CQR. Section 3 proposes an estimator for the UQPE and Section 4 derives its asymptotic properties. Section 5 studies the estimator’s finite sample performance using Monte Carlo experiments. Section 6 provides an empirical application. Section 7 concludes.

2 Quantile Partial Effects

In this section we introduce the unconditional quantile partial effect (UQPE), and the conditional quantile partial effect (CQPE). Some developments appear in Firpo, Fortin, and Lemieux (2009) and we reproduce them here for completeness. The relationship between UQPE and CQPE is the foundation for the estimator we propose in the next section. In the following, the unconditional quantiles of are indexed by , while the conditional quantiles given are indexed by .

2.1 UQPE in terms of CQPE

Consider a general model , where . Here, is the dependent variable, is the target variable of interest and is a scalar, is a vector consisting of other observable covariates, and consists of unobservables. A leading example is the simple linear model such that the conditional -quantile of given is

| (1) |

The typical object of study of the standard conditional quantile regression (CQR) is the conditional quantile partial effect (CQPE) defined as

| (2) |

and corresponds to the marginal effect of on the conditional quantiles of the outcome when and . In the case of model (1), and estimation of this parameter follows from standard quantile regression methods.

To define an unconditional counterpart to , we follow Firpo, Fortin, and Lemieux (2009). To that end, consider the counterfactual outcome

where captures a small location change in the variable . is the outcome we would observe if every individual receives an additional quantity of , while keeping , , and the joint dependence between , and constant. Let be the unconditional -quantile of the random variable . The unconditional quantile partial effect (UQPE) is defined as555The UQPE can be defined for a vector of covariates as in Firpo, Fortin, and Lemieux (2009) resulting in a vector of UQPEs. Martinez-Iriarte, Montes-Rojas, and Sun (2022) provide an interpretation of the linear combination of UQPEs as a compensated counterfactual change.

| (3) |

The is the marginal effect of a location shift in on the unconditional -quantile of the outcome.

The interpretation of and are different. The amounts to manipulating locally at and evaluating a local impact on , i.e., it measures the effect of a marginal change in on the -conditional quantile of . In other words, it only concerns observations (i.e., individuals) with . The is obtained by what we may refer to as a global change in : everyone (not just those with covariates values) moves from to . Then, it looks at its associated impact on the -unconditional quantile of .666 Galvao and Wang (2015) study quantile treatment effects with a continuous treatment. When treatment is continuous, taking values , a subset of the real line, interest lies in the dose response function , which is the potential outcome associated with different levels of the treatment. The quantile dose response functions aims at estimating the quantiles of for different values of . This is different from here, where we estimates the effect on the quantiles of the observed outcome .

Firpo, Fortin, and Lemieux (2009) show that under some mild conditions the following identification result holds:

| (4) |

where is short for the joint distribution, . In a similar manner, assuming differentiability of , from (2) we have that

| (5) |

It is interesting to see that in equation (5) has a similar structure to in (4). Comparing the formulas in (4) and (5), one is able to see that even if the conditional quantile is equal to the corresponding unconditional, that is, , one is not able to recover from by simply integrating the latter over . Moreover, it is usually the case that . Thus, first we need to match conditional and unconditional quantiles, and then re-weight them appropriately to recover from .

The following matching map, introduced by Firpo, Fortin, and Lemieux (2009, p.959), is an important tool to relate the CQPE and UQPE:

| (6) |

The map corresponds to the quantile index(es) in the conditional model, , that produces the closest match with the unconditional quantiles for different values of . In Section 2.3 we analyze this map in detail. For now, we assume that is a singleton. Therefore, we have that, for every , . Under this condition, it is simple to formalize the relationship between CQPE and UQPE. Note that the in equation (5) evaluated at can be written as

Now, rearranging above and substituting into equation (4) yields

| (7) |

The result in equation (A.1) appears in Proposition 1(ii) of Firpo, Fortin, and Lemieux (2009).777Proposition 1(ii) is stated in Firpo, Fortin, and Lemieux (2009, p.959) as following: We can also represent as a weighted average of : , where , , and . One could think about estimating this unconditional expectation. However, notice that the conditional density is a high dimensional object, and might be difficult to estimate in practice. Thus, we rewrite this equation to obtain an alternative representation of the UQPE in terms of CQPE.

Note that, when is differentiable, weights in (A.1) can be rearranged as

Finally, using this weight equation (A.1) becomes a conditional expectation as

| (8) |

Equation (8) shows that the UQPE is in fact a local weighted average of CQPE effects “near” the unconditional -quantile of . As noted above, the -th unconditional quantile of interest may be different from the (random) -th conditional quantiles used inside the integral. The preceding informal discussion is summarized in the next lemma.

Lemma 1.

As mentioned above, sufficient conditions for are laid out in Firpo, Fortin, and Lemieux (2009). Regarding , see Assumption 1 stated below for sufficient conditions for to be singleton. The rest of the assumptions are customary regularity conditions.888 Rothe (2010) extends the identification of UQPE to nonseparable triangular models with endogenous regressors via a control variable approach.

2.2 Description of the procedure

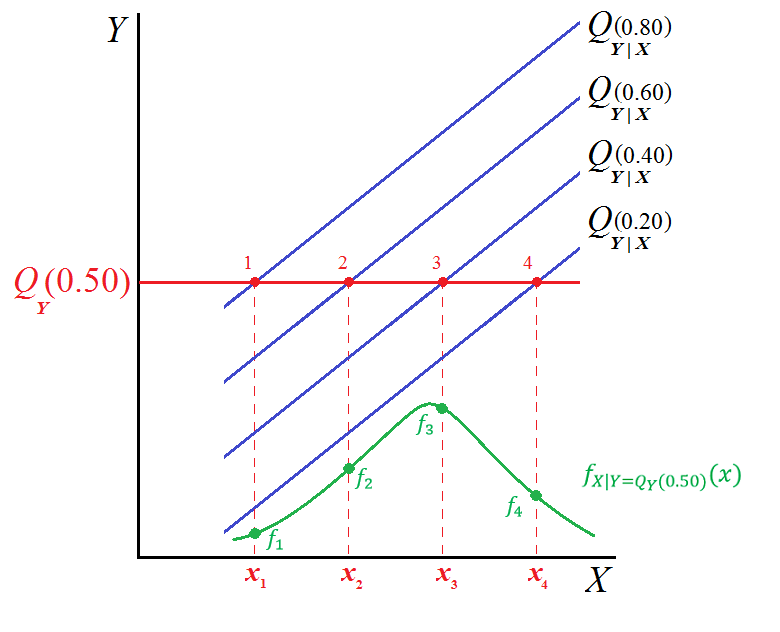

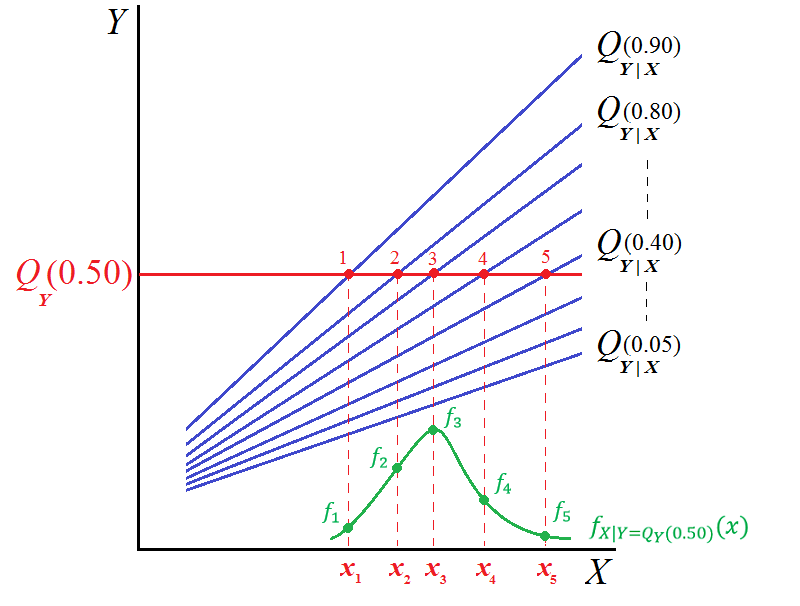

Given the discussion above, it is possible to compute the UQPE from CQPE using equation (8). Consider a linear conditional quantile model as in (1), then . This implies that becomes a weighted average of matched slopes. Figures 1(a) and 1(b) illustrate how the procedure works in two different linear cases. The figures plot both the unconditional quantile, (red line) and conditional quantiles, (blue lines), as well as the conditional density (green curve). An informal description is the following:

-

1.

Identify the unconditional quantile, , say as illustrated in the figures for the unconditional median, and drawn in a horizontal (red) line.

-

2.

Notice that for each , the conditional quantiles (blue lines) intersect the unconditional quantile (horizontal red line); in the figures, we illustrate this for values of that correspond to values respectively.

-

3.

The UQPE is the weighted average – with weights given by density (green curve) – of the intersected slopes on the conditional quantile models.

The figures are useful for analyzing the source of the variation in the UQPE across different unconditional quantiles. For example, in Figure 1(a), the CQPE slopes are the same across conditional quantiles , which implies that the CQPE is constant across quantiles. Even if the weights change with , this is irrelevant, because the slopes are constant.

On the other hand, in Figure 1(b), the CQPE slopes exhibit some variation across conditional quantiles . This heterogeneity can be present even if the weights are not a function of . The UQPE is then constructed as a weighted average of those. An additional source of variation is given by the potential different conditional densities of given . The UQPE will then be the based on the different CQPE and the corresponding density weights. Section 3 below formalizes the estimator.

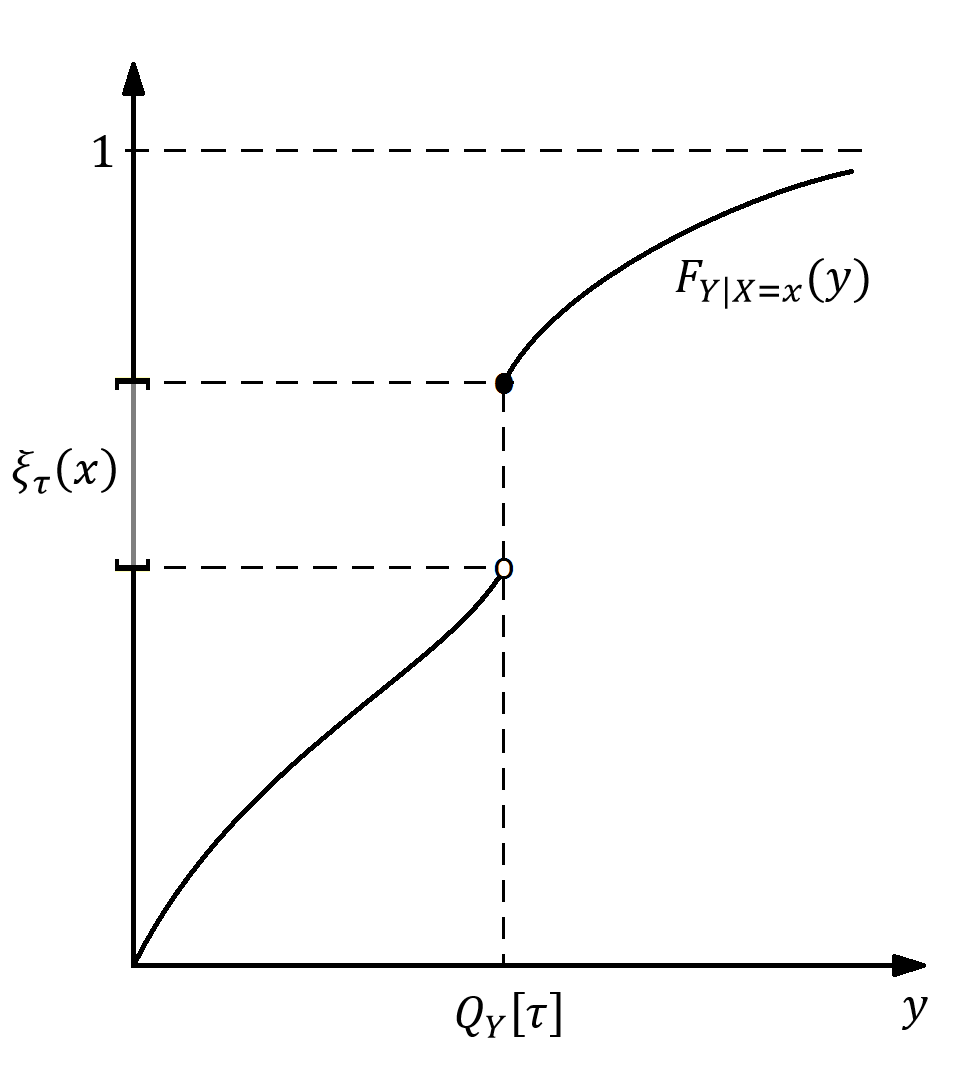

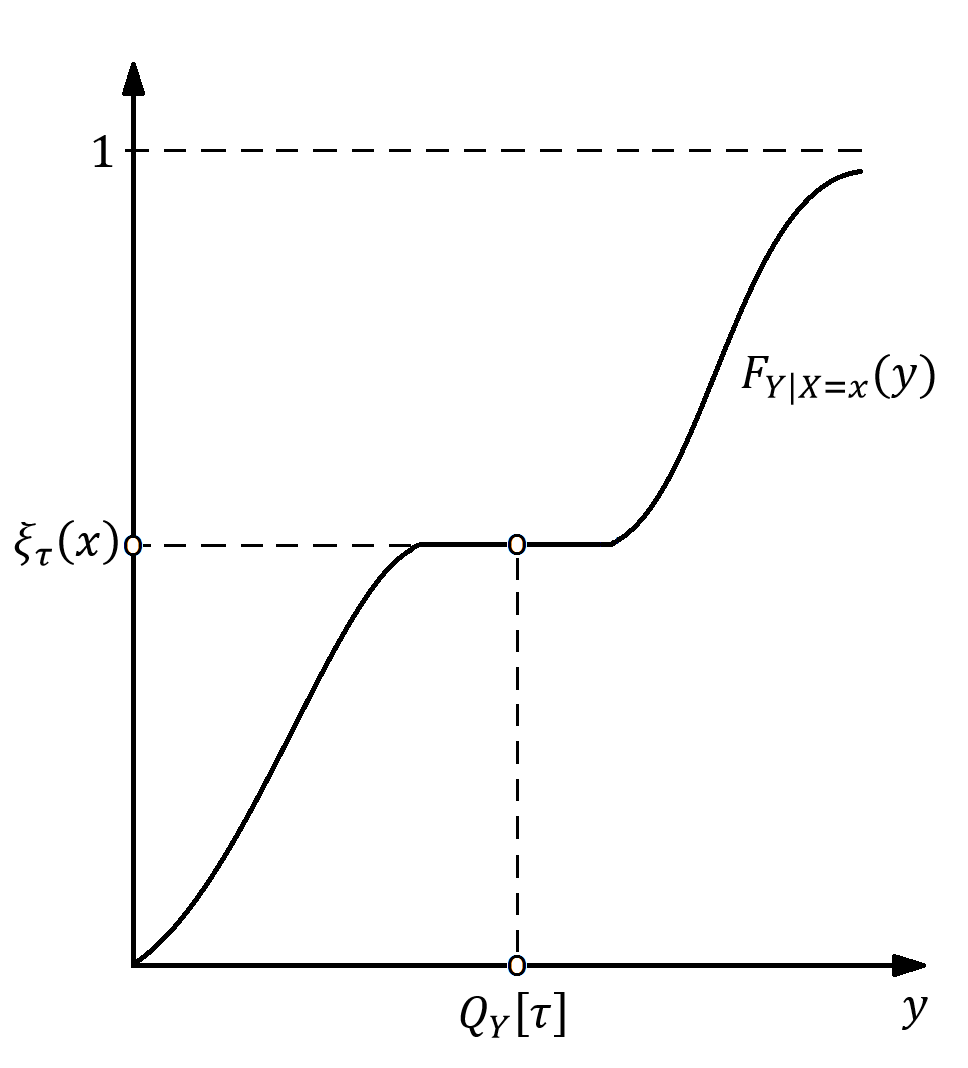

2.3 The matching map

Recall that the matching function selects the quantile that equates the unconditional quantile of with the corresponding conditional quantile, which may vary across values of . Equation (6) defined the map as

For a fixed covariate value , the map describes how the unconditional distribution maps on the conditional one. In general, may vary across the value of covariates as well. Note that it is entirely possible that .

For the purpose of this paper it is important that is unique. But, generally, three situations may occur. First, is unique when is strictly increasing. In this case, there can be at most one that satisfies equation (6). To see this, note that is identical to , so that is unique. Second, might be an interval. For example if has a jump discontinuity at , but it is otherwise continuous and strictly increasing, then . See Figure 2(a) below. Third, might be empty for some . For example, suppose that is continuous, and aside from a flat interval, it is strictly increasing. If is in the interior of the interval mapping to the flat interval, then we cannot have . This is illustrated in Figure 2(b) below.

Now we provide an example to illustrate the how to explicitly write matching function using a linear QR model.

Example 1.

Consider the model with . By standard computations, if , then . To find we need the level such that . Thus,

| (9) |

Remark 1.

If the matching function is the identity function: Then, by equation (8), can be written as

which is the parameter of interest of Lee (2021): a weighted average quantile derivative. Here the weight is . Note that the argument in is , which does not depend on , as opposed to general case when is evaluated at . If the matching function is not the identity, then our parameter is not covered by the methods of Lee (2021).

Since the estimation of the matching function is crucial for our results, we carry out many Monte Carlo simulations to asses the quality of the estimator proposed below in (14). In both the Monte Carlo simulations and the empirical application we plot the estimated matching function for different quantiles against the values of the of . The shape of the matching function can give an indication of the effect of on , as Example 1 shows.

2.4 -heterogeneity vs. -heterogeneity

Here we study how heterogeneity in the conditional effects across -quantiles propagates to heterogeneity in unconditional effects across -quantiles. We refer to the latter as -heterogeneity, and to the former as -heterogeneity. More precisely:

and

While the depends on (a fixed) , we keep this dependence implicit. Using the chain rule, we obtain the following marginal change in the unconditional quantile effect with respect to :

The first term averages across the -heterogeneity. In general, even if there is no -heterogeneity, we may still have non-zero -heterogeneity through the second term. An exception is when , since in this case, as given in equation (8). This is the case of Example 1 above, which we discuss in more details now.

Example 1 (Continued).

Here, . The -heterogeneity is governed by the parameter :

The unconditional effect is . It can be shown that

Now, if , there is no -heterogeneity, so the first term in the above expression for the -heterogeneity is 0. The second term is also 0, since :

provided we can interchange derivatives with integration. Thus, no -heterogeneity implies no -heterogeneity.

3 Estimator

In this section we describe a two-step estimator of , which is based on the conditional expectation in equation (8). The asymptotic properties are discussed in later sections.

Assume first that

| (10) |

where . Note that has to include a constant for correct specification. In this paper, we use the conditional quantile function in (10) to estimate the UQPE. Using this quantile regression model has advantages. First, it allows the researcher to directly model the outcome variable as a function of observable covariates , instead of modeling the recentered influence function. This is important because it may be simpler to relate the variable of interest directly from the economic theory or existing literature, than modeling the influence function. Second, practical estimation of (10) is simple, as we discuss below.

Under (10), . Equation (8) then has the convenient form

| (11) |

Our proposed estimator is a nonparametric regression of on evaluated at . To implement this method in practice we are required to estimate and .

To estimate we first use CQR methods, and estimate for a grid of values of ’s given by , . In the standard linear case we have that for a given value of and a sample , we simply apply standard quantile regression methods as

| (12) |

where is the Koenker and Bassett (1978) check function. We also estimate the unconditional quantile by

| (13) |

To find the matched coefficients , we employ the two previous estimates as following. Let

| (14) |

for . We note that the estimation of the matching function procedure in equation (14) is analogous to the estimation of the conditional CDF in equation (3.7) of Chernozhukov, Fernández-Val, and Melly (2013, p.2219) using instead of .999The above estimator relies on monotonicity of CQR such that there is only one match. In practice, this needs to be checked in small samples as multiple crossings may occur if is very different from . Then an algorithm could be implemented such as taking the average of the selected or a rearrangement of estimated quantiles (see, for instance, Chernozhukov, Fernández-Val, and Galichon (2010) for a discussion about quantile crossings). Alternatively, one could employ distribution regression to estimate this matching function.

Finally, to estimate the , we use a Nadaraya-Watson type-estimator, using the preliminary estimators:

| (15) |

where is the rescaled kernel . The estimator in (15) avoids the curse of dimensionality because it is a nonparametric regression on just one regressor: . Indeed, the dimension of enters in the CQR estimation and in the matching function.

Equation (15) highlights the main benefit of our proposed approach: obtaining the unconditional effect is an easy follow-up from the conditional effects. If the researcher, as is usually the case, has estimated a grid of CQR coefficients, then, after they are “matched” according to (14), they can be averaged following (15) to yield the unconditional effect for the desired quantile level. Moreover, notice that the second nonparametric step in equation (15) does not suffer from the curse of dimensionality, in the sense that it is a reverse regression where the one-dimensional outcome is the regressor.101010The RIF-nonparametric approach is potentially subject to the curse of dimensionality since multiple regressors may enter the nonparametric second step.

Remark 2.

An alternative approach to estimating based on (11) is a linear regression of on a constant and . The predicted fit at is an easy-to-compute approximation to . Yet another option is to do a local linear regression. This estimator may help reduce the bias in lower and higher quantiles. The estimator is , where solve

A study of the properties of this estimator in this particular setting is left for future research.

Next we provide a concise algorithm to compute the UQPE estimator for a given .

Note that this procedure is based on the initial estimate of a QR process for , a typical output in QR analysis, and the unconditional quantile of . Then, for each observation compute the estimated conditional quantile functions for (point 3). The matching function involves a simple binary argument from the results in point 3. Then the algorithm needs to retrieve the corresponding QR coefficient (already estimated in point 2) delivered by the match. Finally compute a weighted average using the kernels as weights (point 5). Importantly, if several values of are to be computed, then points 1, 2 and 3 do not have to be redone.

4 Asymptotic Theory

This section derives the asymptotic properties of the two-step estimator. First, we study the first step, and establish an asymptotic linear representation and rate of convergence for the conditional quantile regression coefficients as a function of the matched quantiles. Second, we study the asymptotic properties of the nonparametric regression in the second step.

4.1 Structural QR and Matched Quantiles

The following assumptions are needed to establish that , where is computed according to (14).

Assumption 1.

Let be a random sample of independent and identically distributed (iid) observations with a scalar and that satisfy the following properties:

-

1.

The conditional quantiles are linear: , , , with and .

-

2.

For every in the support of , is bounded away from zero.

-

3.

The conditional quantile regression estimators satisfy

uniformly in , , and has uniformly bounded derivatives.

-

4.

The unconditional quantile estimator satisfies

-

5.

The grid of quantiles , , satisfies as for , and and for a small .

Assumption 1.1 imposes linearity of the quantile process.111111There is a large set of examples using linear specification of quantiles over the entire conditional distribution as, among others, treatment effects, endogeneity, high-dimensional, stochastic dominance, censoring, as well as most of the theoretical papers providing statistical foundations for the quantile regression process (see, e.g., among many others, Gutenbrunner and Jurečková (1992), Koenker and Machado (1999), Koenker and Xiao (2002), Knight (2002), Chernozhukov and Fernández-Val (2005), Angrist, Chernozhukov, and Fernández-Val (2006), Belloni and Chernozhukov (2011), Portnoy (2012), Volgushev, Chao, and Cheng (2019), and He, Pan, Tan, and Zhou (2022)). Condition 1.2 is very standard in the QR literature, see, e.g., Koenker (2005). Assumptions 1.1 and 1.2, allow us to write , so that , where is the Jacobian vector: the derivative of the map . This quantity appears in the denominator of the influence function of . Moreover, Assumption 1.2 states that is bounded away from zero. This in turn implies that is strictly increasing. Assumption 1.3 is a uniform Bahadur representation for the QR estimator. It is established in Lemma 3 in Ota, Kato, and Hara (2019). See also Theorem 3 in Angrist, Chernozhukov, and Fernández-Val (2006). It implies and the stochastic equicontinuity of the process on . Condition 1.4 is a simple linear representation for the unconditional quantile. Sufficient conditions for Assumption 1.4 are given in Serfling (1980). Finally, Assumption 1.5 requires that the grid for the matching function becomes denser as the sample size increases. This condition has appeared in the QR literature. Chernozhukov, Fernández-Val, and Melly (2013, Remark 3.1 p.2220) provide a similar condition when computing counterfactual distributions.

The next result provides a rate of convergence and a linear representation for , and for .

Theorem 1.

Under Assumption 1, the CQR coefficient of evaluated at the random quantile can be represented as

where

Moreover, they are both and asymptotically normal.

4.2 Nadaraya-Watson Estimator

Our parameter of interest given in (11) is

and we propose the following nonparametric regression Nadaraya-Watson-type estimator:

The unfeasible (oracle) version is denoted by

We maintain the following assumptions.

Assumption 2.

is a symmetric function around 0 that satisfies: (i) ; (ii) For , when , and ; (iii) ; (iv) as for j=1,…,r+1; (v) and ; (vi) and .

Remark 3.

The Gaussian kernel is (ignoring the constants) . It’s first derivative is . To show that is Lipschitz, we need to show that there exist a constant , independent of and , such that . We can use the mean value theorem, since the second derivative is uniformly bounded. It is given by and . Therefore, by the mean value theorem, is Lipschitz continuous.

Assumption 3.

As , the bandwidth satisfies with .

Remark 4.

If a second order Kernel is chosen, and Assumption 3 requires that the admissible bandwidth satisfies for .

Assumption 4.

(i) The density of is times continuously differentiable, with uniformly bounded derivatives; (ii) The joint density is times continuously differentiable, with uniformly bounded derivatives for every in the support of .

Assumption 5.

(i) The remainder in the expression for holds uniformly over , the support of ; (ii) , and .

Remark 5.

Assumption 5.(i) is implied by Condition D in Chernozhukov, Fernández-Val, and Melly (2013, p.2224). It pertains to a uniform central limit theorem for the estimator of the conditional CDF. For primitive conditions, we refer the reader to Chernozhukov, Fernández-Val, and Melly (2013), where they provide details on this verification.

This theorem states that the preliminary estimators of the CQR slopes, the matched quantiles and the unconditional quantile of vanish asymptotically because they converge at a faster rate: as opposed to . Moreover, the asymptotic distribution of the unfeasible estimator is well-known and can be readily established.

The following assumption is customary in order to apply the Lindeberg-Feller Central Limit Theorem.

Assumption 6.

(i) For , and , a.s. for some ; (ii) ; (iii) The map is times continuously differentiable, with uniformly bounded derivatives; (iv) The map is continuous.

Remark 6.

The practical computation of the asymptotic variance-covariance matrix in Corollary 1 is difficult due to the presence of preliminary estimators in the nonparametric regression. Thus, in practice, we employ resampling approach for inference. There is an extensive literature on constructing nonparametric confidence bands for functions. We refer the reader to Härdle and Bowman (1988) and Hall and Horowitz (2013) and references therein for resampling methods.

We describe now the implementation of the pairwise bootstrap procedure.

-

1.

Estimate for a given grid and , then compute using the sample .

-

2.

Compute samples with replacement , for , and estimators for , and .

-

3.

Compute the standard deviation from the bootstrap sample,

where .

-

4.

Compute the confidence interval using the ordered statistics of the bootstrap sample.

5 Monte Carlo experiments

This section presents several simulation exercises to study the finite sample performance of the proposed estimator. First, we assess the matching function estimator. Second, we evaluate the unconditional quantile partial effect (UQPE) estimation.

The first data generating process (DGP) we consider is as following:

| (16) |

where and is a random variable with , and independent of . The distribution of is specified below as either standard Gaussian or (standardized) Chi-squared with 1 degree of freedom. The parameter controls the type of effect of the covariate on the distribution of : when the effect is a location shift, and if is a location-scale shift. In the former case the conditional quantile regression (CQR) effects are constant across quantiles, while in the latter case they vary.

Second, we use a DGP with an additional covariate

| (17) |

where we consider two cases: (i) (independent of ; (ii) , where we make correlated with .

5.1 Matching function estimator

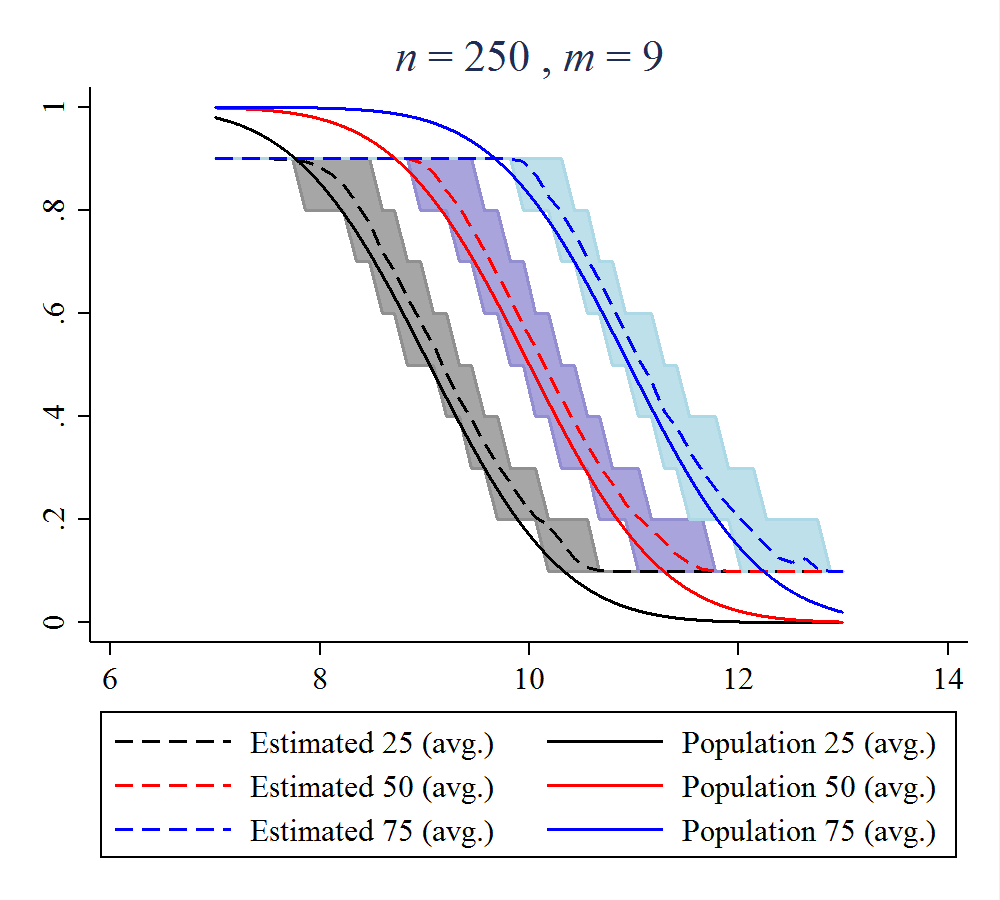

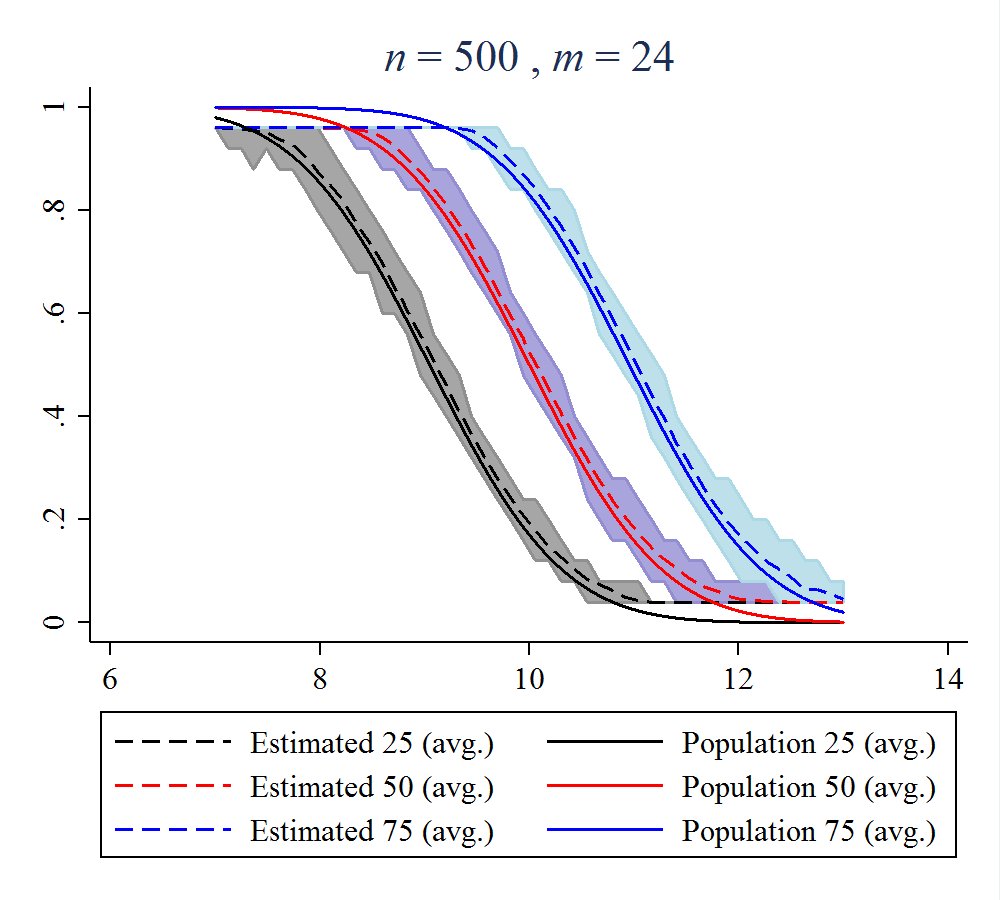

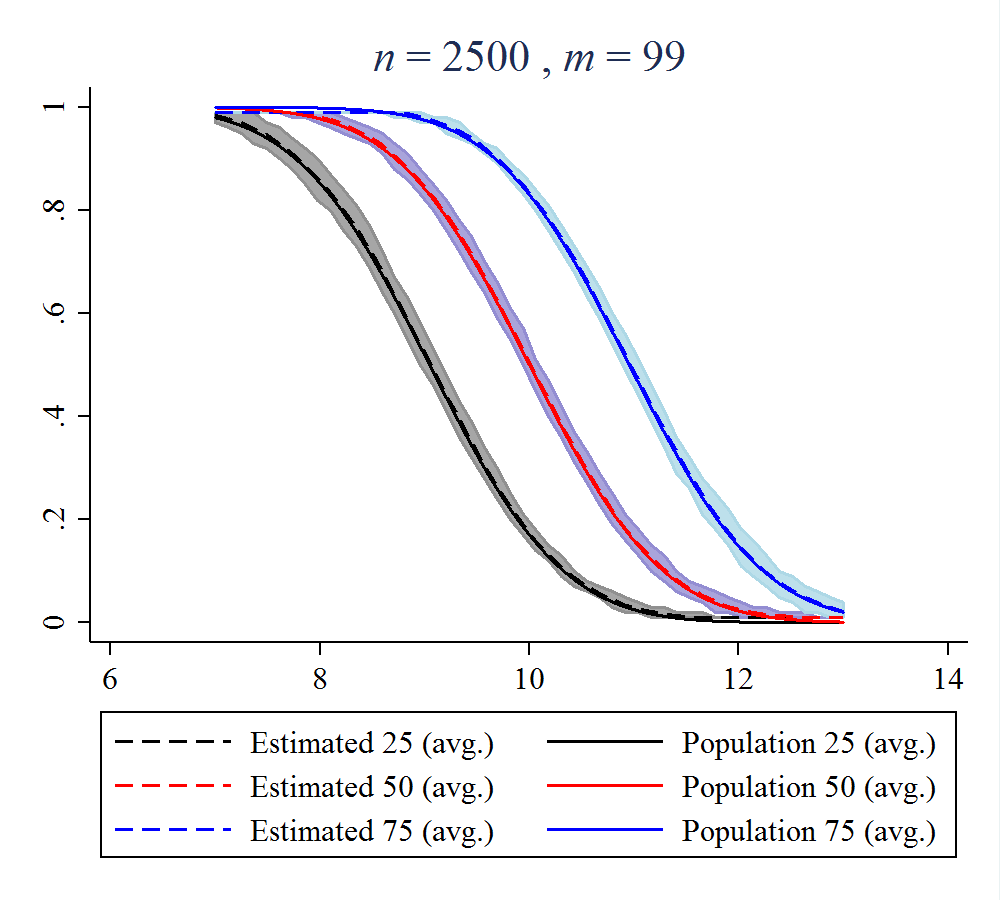

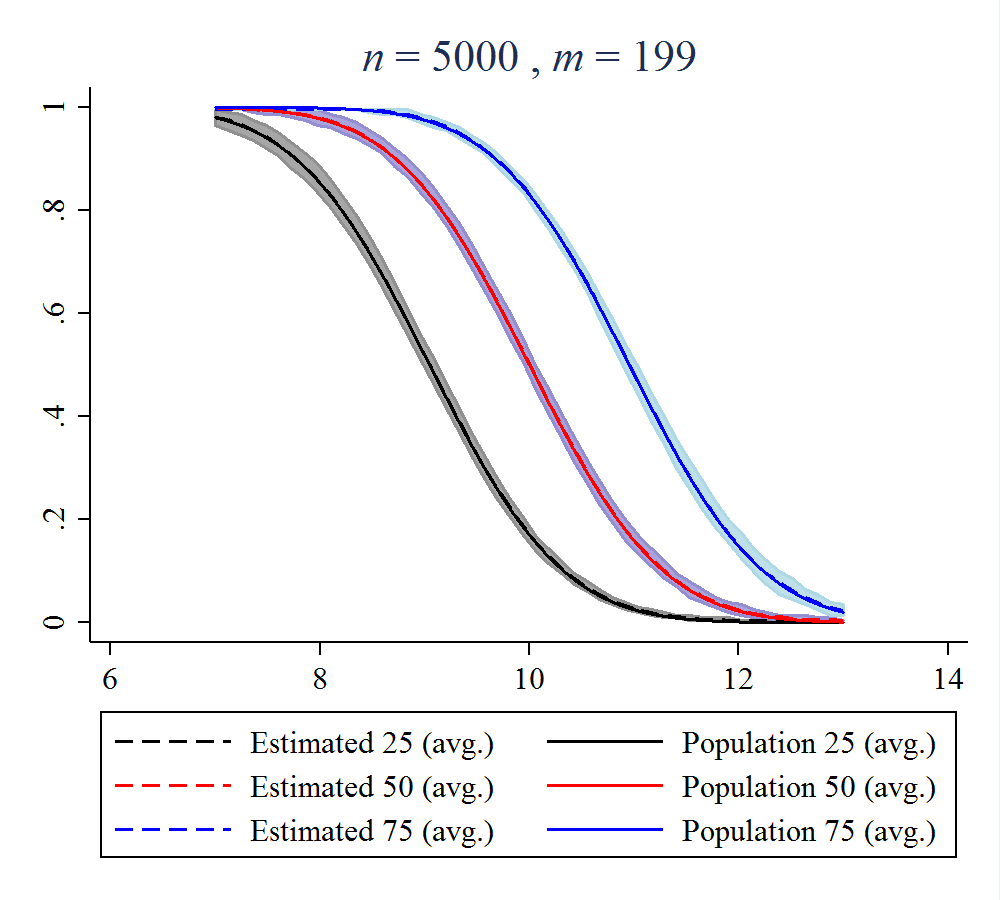

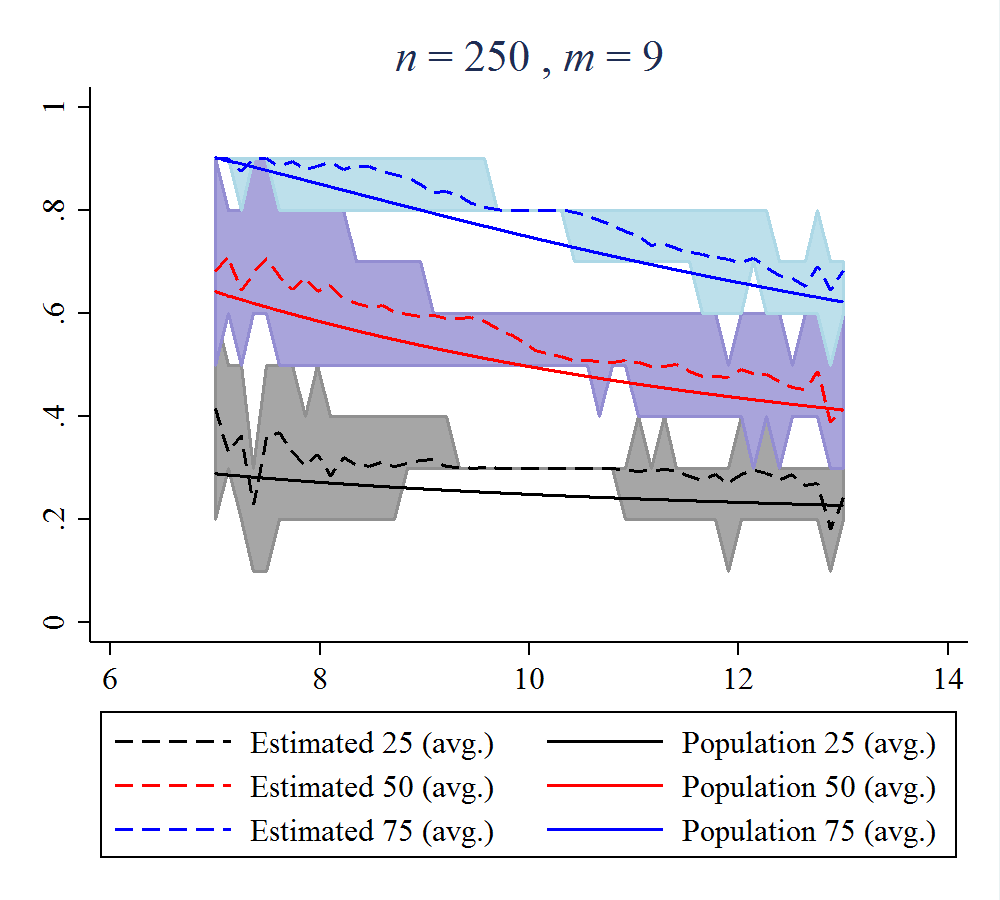

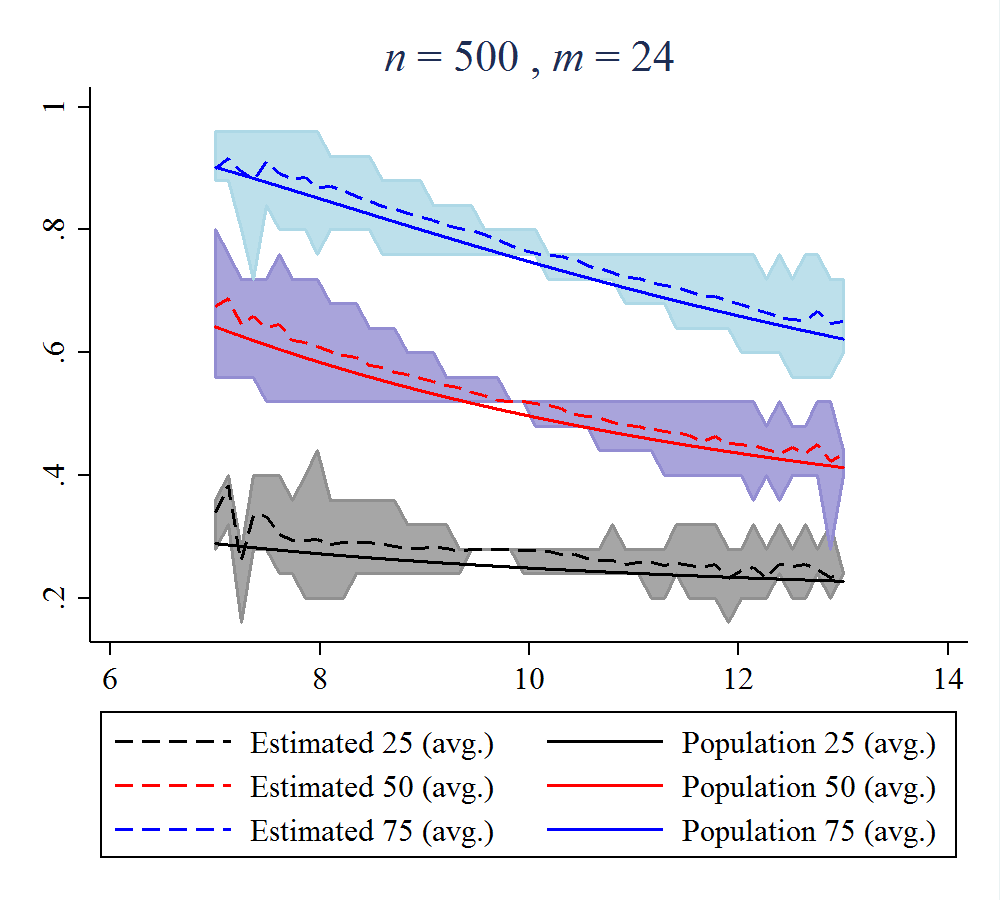

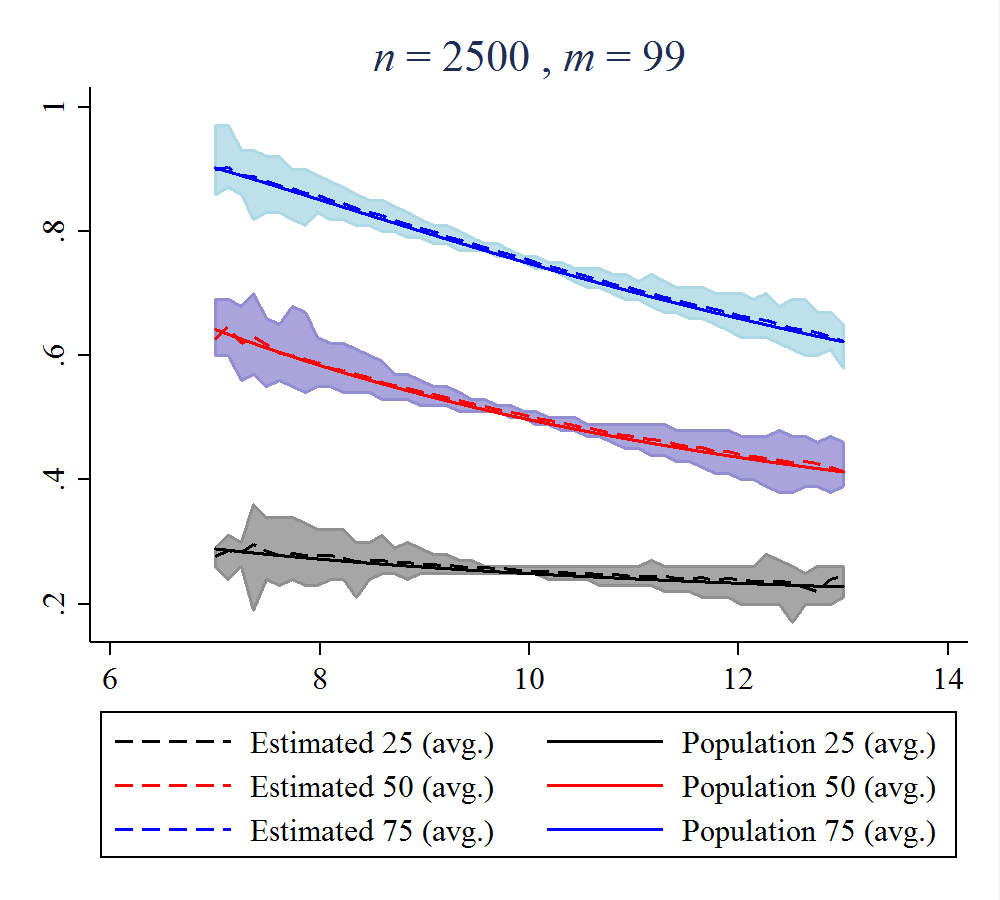

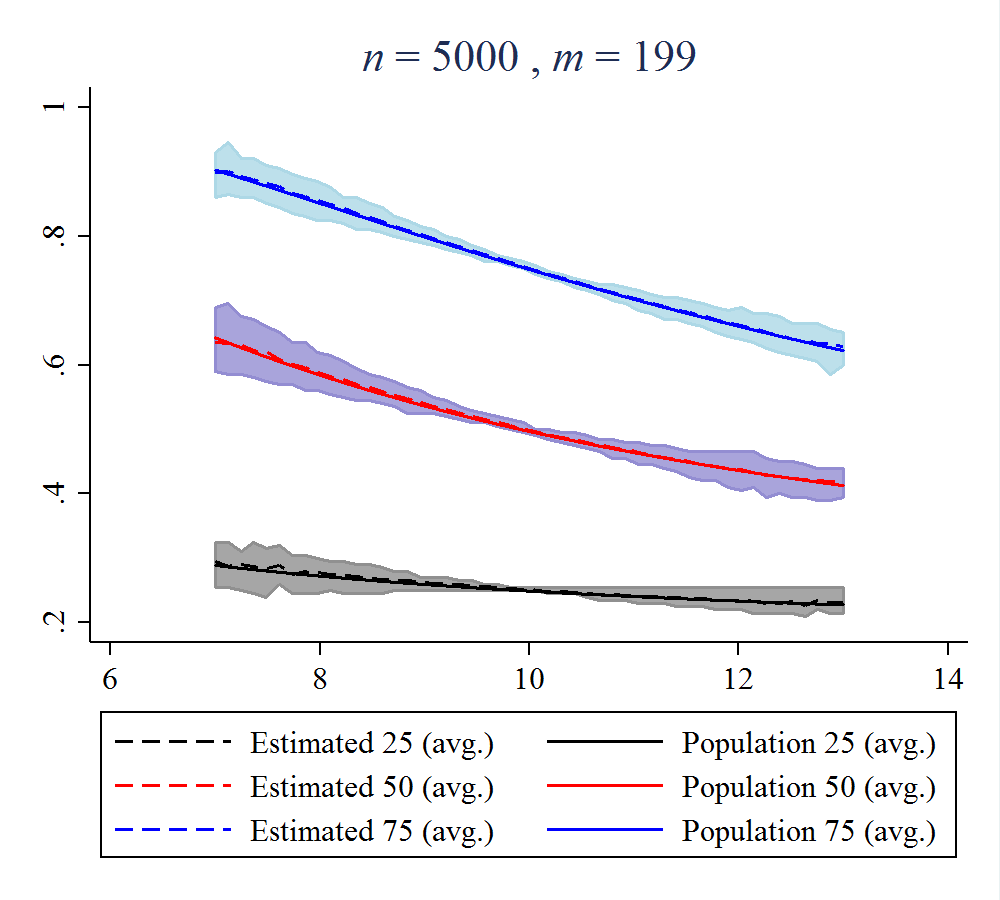

The proposed UQPE estimator relies on the estimator of the matching function for the quantiles, . This subsection presents simulations exercises for assessing the accuracy of the matching estimator as given in equation (14). Recall from Example 1, equation (9), that in the simple linear case we have an explicit formula for the population matching function, . Thus, we are able to use simulations to assess the finite sample performance of the estimator.

We consider experiments using DGP model in (16) for a pure location model, , as well as a location-scale model, . We use and . Each experiment has 100 simulations of the DGP with sample sizes , and quantile grid sizes , respectively. We consider three quantiles . Figure 3 reports results for the location case, and Figure 4 displays results for the location-scale case. In each figure, we plot the parameter of interest (the true value of the matching function), the estimates (average estimates over the number of simulations), as well as the 95% empirical confidence interval.121212These are computed as the 2.5-th and 97.5-th empirical percentiles of estimates across simulations.

Simulation results show evidence that the matching function estimator provides an approximately asymptotically unbiased estimator for both the pure location and location-scale models with a better performance of sample sizes of . Point estimates are close to the populations counterparts even for small samples and grids. As sample size and grid increase together, point estimates become very close to the population and confidence intervals shrink.

|

|

|

|

Notes: The shaded areas are 95% empirical confidence intervals estimated using 100 simulations.

|

|

|

|

Notes: The shaded areas are 95% empirical confidence intervals estimated using 100 simulations.

5.2 UQPE estimation

Now we investigate the finite sample performance of the proposed UQPE estimator as in equation (15). In what follows, We label this estimator as Nadaraya-Watson (NW). For comparison, we also implement the RIF regression model for UQR for each unconditional quantile using the rifvar STATA command (Rios-Avila, 2020). In this case, the UQPE is estimated by OLS with a cubic polynomial model of the RIF for each quantile as a function of (or as a function of and for the model with additional covariates). Although not reported the cubic model overperforms the linear and quadratic implementation, available from the Authors upon request. Finally we also implement the RIF-Logit model suggested by Firpo, Fortin, and Lemieux (2009).

Each experiment has 1,000 simulations of the DGP with sample sizes , and quantiles grid sizes , respectively. We consider three quantiles . Moreover, we use a bandwidth and the Gaussian kernel function. To evaluate the procedures we report the empirical bias, variance, and mean-squared error (MSE).

Table 1 presents results for the baseline model for the simple location-shift model (i.e. ) and Gaussian covariate and innovation. Both RIF models and NW estimators have a good performance in terms of bias, variance and MSE. These three statistics decrease for both estimators as sample size increases, for all three quantiles.

Tables 2 and 3 present simulations results for Gaussian and Chi-squared innovations, respectively, for the location-scale shift model (i.e. ) with a Gaussian covariate. For all cases we observe that for the proposed NW estimator the bias and variance reduces as increases. The relative performance to the RIF models varies depending on the simulation exercises, but in most cases either the NW estimator outperforms the RIF one.

Tables 4 and 5 collect simulation results for cases where there is an additional covariate, . The former case uses an independent additional covariate and in the latter case is correlated with . In both cases we use the model with and . The results are also in line with previous ones, highlighting a good performance of the NW estimator in terms of bias, variance, and MSE.

Overall, these simulation results indicate that our proposed method produces a consistent estimator, where both bias and variance reduce as increases. In some cases, however, the bias improvement applies only for .

Next, Table 6 presents simulation exercises where we consider different bandwidth choices. In particular, we use , and . We consider the location-scale model with and Gaussian errors. The results show evidence that there are only small differences across bandwidths which suggest that the estimator is robust to these choices. For the empirical researcher this suggests that our proposed estimator can be combined with different nonparametric implementations.

| Estimator | RIF-OLS (cubic) | RIF-Logit | NW | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | Bias | Variance | MSE | ||

| 25 | 250 | 0.02470 | 0.01559 | 0.01620 | 0.02547 | 0.01736 | 0.01800 | -0.00405 | 0.00458 | 0.00459 |

| 500 | 0.02432 | 0.00876 | 0.00935 | 0.01837 | 0.00960 | 0.00994 | 0.00019 | 0.00241 | 0.00241 | |

| 2500 | 0.01299 | 0.00202 | 0.00219 | 0.00924 | 0.00224 | 0.00233 | -0.00104 | 0.00046 | 0.00046 | |

| 5000 | 0.00866 | 0.00122 | 0.00129 | 0.00595 | 0.00136 | 0.00140 | -0.00049 | 0.00022 | 0.00022 | |

| 50 | 250 | 0.04550 | 0.01215 | 0.01422 | 0.03407 | 0.01344 | 0.01460 | -0.00017 | 0.00419 | 0.00419 |

| 500 | 0.03899 | 0.00736 | 0.00888 | 0.02971 | 0.00815 | 0.00903 | 0.00222 | 0.00219 | 0.00219 | |

| 2500 | 0.02319 | 0.00166 | 0.00220 | 0.01701 | 0.00188 | 0.00217 | -0.00050 | 0.00043 | 0.00043 | |

| 5000 | 0.01764 | 0.00090 | 0.00121 | 0.01287 | 0.00103 | 0.00119 | -0.00005 | 0.00020 | 0.00020 | |

| 75 | 250 | 0.03803 | 0.01592 | 0.01737 | 0.02125 | 0.01714 | 0.01759 | 0.00242 | 0.00503 | 0.00504 |

| 500 | 0.02561 | 0.00846 | 0.00911 | 0.01772 | 0.00920 | 0.00952 | 0.00400 | 0.00261 | 0.00263 | |

| 2500 | 0.01217 | 0.00219 | 0.00234 | 0.00856 | 0.00242 | 0.00249 | 0.00015 | 0.00047 | 0.00047 | |

| 5000 | 0.01135 | 0.00120 | 0.00133 | 0.00852 | 0.00136 | 0.00143 | 0.00045 | 0.00023 | 0.00023 | |

Notes: Monte Carlo experiments based on 1000 simulations.

| Estimator | RIF-OLS (cubic) | RIF-Logit | NW | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | Bias | Variance | MSE | ||

| 25 | 250 | -0.00459 | 1.01506 | 1.01508 | 0.00897 | 0.97017 | 0.97025 | 0.14868 | 0.80311 | 0.82522 |

| 500 | 0.02808 | 0.47673 | 0.47752 | 0.02558 | 0.46631 | 0.46696 | 0.09142 | 0.42411 | 0.43246 | |

| 2500 | -0.00302 | 0.09242 | 0.09242 | -0.00503 | 0.09132 | 0.09135 | 0.00379 | 0.08527 | 0.08528 | |

| 5000 | 0.00355 | 0.04448 | 0.04449 | 0.00239 | 0.04412 | 0.04413 | 0.00602 | 0.04154 | 0.04157 | |

| 50 | 250 | 0.05602 | 0.86653 | 0.86967 | 0.04100 | 0.81673 | 0.81841 | 0.11159 | 0.68532 | 0.69778 |

| 500 | 0.07079 | 0.43029 | 0.43530 | 0.05600 | 0.41888 | 0.42201 | 0.06935 | 0.35727 | 0.36208 | |

| 2500 | 0.01198 | 0.08004 | 0.08018 | 0.00445 | 0.07946 | 0.07948 | 0.00249 | 0.06978 | 0.06978 | |

| 5000 | 0.01055 | 0.03963 | 0.03974 | 0.00541 | 0.03937 | 0.03940 | -0.00108 | 0.03341 | 0.03341 | |

| 75 | 250 | 0.07899 | 1.06619 | 1.07243 | 0.06986 | 0.97638 | 0.98126 | 0.19632 | 0.82485 | 0.86339 |

| 500 | 0.04227 | 0.50446 | 0.50625 | 0.03024 | 0.49447 | 0.49538 | 0.09177 | 0.42507 | 0.43349 | |

| 2500 | 0.03413 | 0.10107 | 0.10223 | 0.02793 | 0.10136 | 0.10214 | 0.02224 | 0.08093 | 0.08143 | |

| 5000 | 0.02322 | 0.04809 | 0.04863 | 0.01820 | 0.04827 | 0.04860 | 0.01541 | 0.03744 | 0.03768 | |

Notes: Monte Carlo experiments based on 1000 simulations.

| Estimator | RIF-OLS (cubic) | RIF-Logit | NW | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | Bias | Variance | MSE | ||

| 25 | 250 | 0.38010 | 0.12921 | 0.27369 | 0.29658 | 0.10312 | 0.19108 | 0.04724 | 0.05433 | 0.05656 |

| 500 | 0.31075 | 0.05070 | 0.14727 | 0.24543 | 0.04069 | 0.10093 | 0.01919 | 0.02012 | 0.02049 | |

| 2500 | 0.18007 | 0.00637 | 0.03880 | 0.13126 | 0.00527 | 0.02250 | 0.01149 | 0.00315 | 0.00328 | |

| 5000 | 0.13945 | 0.00289 | 0.02234 | 0.09669 | 0.00240 | 0.01175 | 0.00796 | 0.00157 | 0.00163 | |

| 50 | 250 | -0.07688 | 0.22020 | 0.22611 | -0.08321 | 0.20770 | 0.21463 | 0.08695 | 0.34549 | 0.35305 |

| 500 | -0.08876 | 0.10207 | 0.10995 | -0.08481 | 0.10242 | 0.10961 | 0.03118 | 0.14885 | 0.14982 | |

| 2500 | -0.08059 | 0.02002 | 0.02652 | -0.06304 | 0.02133 | 0.02531 | 0.00559 | 0.02382 | 0.02385 | |

| 5000 | -0.06959 | 0.01075 | 0.01559 | -0.05158 | 0.01150 | 0.01416 | -0.00212 | 0.01240 | 0.01240 | |

| 75 | 250 | -0.05772 | 1.39024 | 1.39357 | -0.03968 | 1.40400 | 1.40557 | 0.24080 | 1.95959 | 2.01758 |

| 500 | -0.08805 | 0.70950 | 0.71725 | -0.06975 | 0.72037 | 0.72524 | 0.04520 | 0.81321 | 0.81526 | |

| 2500 | -0.02743 | 0.14136 | 0.14211 | -0.02110 | 0.14339 | 0.14384 | 0.01590 | 0.13451 | 0.13477 | |

| 5000 | -0.03405 | 0.06550 | 0.06666 | -0.02846 | 0.06630 | 0.06711 | -0.00672 | 0.05988 | 0.05992 | |

Notes: Monte Carlo experiments based on 1000 simulations.

| Estimator | RIF-OLS (cubic) | RIF-Logit | NW | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | Bias | Variance | MSE | ||

| 25 | 250 | -0.01793 | 0.96720 | 0.96752 | -0.01313 | 0.90922 | 0.90940 | 0.11521 | 0.76408 | 0.77735 |

| 500 | 0.02157 | 0.52336 | 0.52383 | 0.01794 | 0.51131 | 0.51163 | 0.08835 | 0.40504 | 0.41285 | |

| 2500 | 0.00591 | 0.09537 | 0.09541 | 0.00476 | 0.09394 | 0.09396 | 0.01958 | 0.08337 | 0.08375 | |

| 5000 | -0.00026 | 0.04463 | 0.04463 | -0.00131 | 0.04433 | 0.04433 | 0.00394 | 0.03924 | 0.03926 | |

| 50 | 250 | 0.00228 | 0.93384 | 0.93384 | -0.02212 | 0.87770 | 0.87819 | 0.07071 | 0.68265 | 0.68765 |

| 500 | 0.04824 | 0.41277 | 0.41510 | 0.03867 | 0.39961 | 0.40110 | 0.06020 | 0.32478 | 0.32840 | |

| 2500 | 0.00705 | 0.08055 | 0.08060 | 0.00002 | 0.07976 | 0.07976 | -0.00757 | 0.07035 | 0.07041 | |

| 5000 | -0.00166 | 0.03845 | 0.03846 | -0.00712 | 0.03802 | 0.03807 | -0.01254 | 0.03165 | 0.03181 | |

| 75 | 250 | -0.00581 | 1.01975 | 1.01979 | -0.01927 | 0.98074 | 0.98112 | 0.10028 | 0.86565 | 0.87570 |

| 500 | 0.04783 | 0.45838 | 0.46066 | 0.03623 | 0.45086 | 0.45217 | 0.05986 | 0.37305 | 0.37663 | |

| 2500 | 0.01022 | 0.10191 | 0.10201 | 0.00445 | 0.10232 | 0.10234 | 0.00708 | 0.07831 | 0.07836 | |

| 5000 | -0.00166 | 0.04808 | 0.04808 | -0.00545 | 0.04845 | 0.04848 | -0.01037 | 0.03879 | 0.03889 | |

Notes: Monte Carlo experiments based on 1000 simulations.

| Estimator | RIF-OLS (cubic) | RIF-Logit | NW | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | Bias | Variance | MSE | ||

| 25 | 250 | -0.09324 | 2.05569 | 2.06438 | -0.06573 | 1.96614 | 1.97046 | 0.04637 | 1.61066 | 1.61281 |

| 500 | -0.02007 | 0.98728 | 0.98769 | -0.02275 | 0.96771 | 0.96823 | 0.04168 | 0.78219 | 0.78393 | |

| 2500 | -0.02730 | 0.17002 | 0.17077 | -0.02856 | 0.16783 | 0.16864 | -0.01622 | 0.14786 | 0.14813 | |

| 5000 | -0.01900 | 0.08653 | 0.08689 | -0.02042 | 0.08588 | 0.08630 | -0.01659 | 0.07614 | 0.07642 | |

| 50 | 250 | 0.00075 | 1.90333 | 1.90334 | -0.02501 | 1.82672 | 1.82735 | 0.06789 | 1.42734 | 1.43195 |

| 500 | 0.03006 | 0.82247 | 0.82337 | 0.01738 | 0.79296 | 0.79326 | 0.02777 | 0.65445 | 0.65522 | |

| 2500 | -0.01982 | 0.15795 | 0.15834 | -0.02668 | 0.15681 | 0.15752 | -0.02519 | 0.13293 | 0.13356 | |

| 5000 | -0.00523 | 0.07573 | 0.07576 | -0.01103 | 0.07484 | 0.07497 | -0.01642 | 0.06310 | 0.06337 | |

| 75 | 250 | 0.00633 | 2.04659 | 2.04663 | -0.01486 | 1.92153 | 1.92175 | 0.12363 | 1.62417 | 1.63946 |

| 500 | 0.04492 | 1.03865 | 1.04067 | 0.03612 | 1.02019 | 1.02150 | 0.07378 | 0.78689 | 0.79233 | |

| 2500 | 0.01423 | 0.19626 | 0.19646 | 0.00868 | 0.19582 | 0.19590 | 0.02220 | 0.15084 | 0.15134 | |

| 5000 | 0.00299 | 0.09886 | 0.09887 | -0.00072 | 0.09855 | 0.09855 | -0.00242 | 0.07764 | 0.07764 | |

Notes: Monte Carlo experiments based on 1000 simulations.

| Bias | Variance | ECM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Kernel | |||||||||||

| Gauss | 25 | 250 | 0.14894 | 0.14868 | 0.14849 | 0.80470 | 0.80311 | 0.80181 | 0.82688 | 0.82522 | 0.82386 |

| 500 | 0.09184 | 0.09142 | 0.09108 | 0.42566 | 0.42411 | 0.42300 | 0.43409 | 0.43246 | 0.43130 | ||

| 2500 | 0.00411 | 0.00379 | 0.00359 | 0.08542 | 0.08527 | 0.08516 | 0.08544 | 0.08528 | 0.08517 | ||

| 5000 | 0.00629 | 0.00602 | 0.00585 | 0.04160 | 0.04154 | 0.04150 | 0.04164 | 0.04157 | 0.04153 | ||

| 50 | 250 | 0.11349 | 0.11159 | 0.11028 | 0.68763 | 0.68532 | 0.68358 | 0.70051 | 0.69778 | 0.69574 | |

| 500 | 0.07096 | 0.06935 | 0.06825 | 0.35794 | 0.35727 | 0.35668 | 0.36298 | 0.36208 | 0.36133 | ||

| 2500 | 0.00308 | 0.00249 | 0.00201 | 0.06978 | 0.06978 | 0.06975 | 0.06979 | 0.06978 | 0.06975 | ||

| 5000 | -0.00071 | -0.00108 | -0.00144 | 0.03340 | 0.03341 | 0.03340 | 0.03340 | 0.03341 | 0.03341 | ||

| 75 | 250 | 0.19834 | 0.19632 | 0.19488 | 0.82528 | 0.82485 | 0.82442 | 0.86462 | 0.86339 | 0.86239 | |

| 500 | 0.09263 | 0.09177 | 0.09123 | 0.42418 | 0.42507 | 0.42552 | 0.43276 | 0.43349 | 0.43384 | ||

| 2500 | 0.02237 | 0.02224 | 0.02228 | 0.08078 | 0.08093 | 0.08107 | 0.08128 | 0.08143 | 0.08156 | ||

| 5000 | 0.01525 | 0.01541 | 0.01558 | 0.03740 | 0.03744 | 0.03750 | 0.03763 | 0.03768 | 0.03774 | ||

Notes: Monte Carlo experiments based on 1000 simulations.

5.3 UQPE bootstrap inference

Finally, we evaluate the finite sample performance of the pairwise bootstrap procedure discussed above for practical inference of the proposed NW estimator. For this we report empirical coverages for a nominal coverage of the 95% confidence intervals for three models considered above with one covariate as in eq. (16): DGP 1: and (as in Table 1); DGP 2: and (as in Table 2); and DGP 3: and (as in Table 3). In particular, we consider the Gaussian confidence interval, constructed using times the estimated bootstrap variance, and the percentile bootstrap that uses the 0.025 and 0.975 percentiles of the bootstrapped distribution.

The results for empirical coverage are presented in Table 7. The coverage is accurate for all cases, being close to the nominal 0.95. There is no systematic difference between Gaussian and percentile bootstrap, thus indicating that both work in a similar fashion.

| DGP 1 | DGP 2 | DGP 3 | |||||

|---|---|---|---|---|---|---|---|

| Gaussian | Percentile | Gaussian | Percentile | Gaussian | Percentile | ||

| 25 | 500 | 0.949 | 0.941 | 0.942 | 0.953 | 0.920 | 0.932 |

| 1000 | 0.940 | 0.937 | 0.941 | 0.941 | 0.936 | 0.939 | |

| 50 | 500 | 0.954 | 0.936 | 0.945 | 0.948 | 0.928 | 0.937 |

| 1000 | 0.940 | 0.934 | 0.940 | 0.945 | 0.931 | 0.939 | |

| 75 | 500 | 0.949 | 0.945 | 0.935 | 0.947 | 0.922 | 0.940 |

| 1000 | 0.939 | 0.935 | 0.930 | 0.934 | 0.934 | 0.942 | |

Notes: Monte Carlo experiments based on 1000 simulations. Bootstrap with 100 replications. Coverage corresponding to 95% confidence intervals.

6 Empirical Application

This section illustrates the UQPE estimator with an analysis of Engel’s curves. The original concept corresponds to Ernst Engel (1857, cited in Koenker (2005), pp. 78-79) who studied the European working class households consumption in the 19th century. Engel curves describe how household expenditures on particular goods and services depend on household income. The analysis of Engel curves has a long history of estimating the expenditure-income relationship. An empirical result commonly referred to as “Engel’s law” states that the poorer a family is, the larger the budget share it spends on food. Other categories of expenditure present a less robust pattern. Hence, we investigate the hypothesis that food expenditure constitutes a declining share of household income.131313There is a large literature on empirical applications of the Engel’s curve, see, e.g., for example, among many others, Lewbel (1997, 2008), Blundell, Chen, and Kristensen (2007), Charles, Hurst, and Roussanov (2009), Heffetz (2011), Perez-Truglia (2013), Chernozhukov, Fernández-Val, and Kowalski (2015), Atkin, Faber, Fally, and Gonzalez-Navarro (2020) and Li (2009). We follow a regression approach to model the conditional effects. In this paper, for simplicity, we do not consider endogeneity issues that potentially arise from simultaneous decisions on income and expenditures.

We apply this framework to household expenditures in Argentina using the national survey of expenditures (Encuesta Nacional de Gasto de los Hogares, known as ENGHO 2017-2018), implemented by the Instituto Nacional de Estadística y Censos (INDEC). The survey was carried out between November 2017 and November 2018. The ENGHO 2017-2018 surveys the households’ living conditions in terms of their access to goods and services, as well as their income. The data contains information about household expenditures on different goods and services. About 21,547 households were randomly selected and participated on the survey. We consider both food household expenditures and total non-durable consumption for comparison.141414In particular, the sample has information on: food and non-alcoholic beverages, alcoholic beverages and tobacco, clothing and footwear, housing, water, electricity, gas and other fuels, home equipment and maintenance, health, transportation, communications, recreation and culture, education, restaurants and hotels, and miscellaneous goods and services. Both expenses and income are transformed to represent monthly values. Since the monetary values of each household are expressed in current currency at the time of the survey, an inflation adjustment was made to transform them into constant currency for December of the fourth quarter of 2018 using the Consumer Price Index (CPI) computed by national statistical office, INDEC.

We estimate both UQPE and CQPE. The former analysis corresponds to evaluating effect of an increase in income for every household in a uniform pattern on the unconditional quantile of food expenditure while focusing on the entire distribution of expenditure. The latter effect corresponds to the study of how expenditure changes when marginally increasing income conditional on income. For comparison, we also provide estimate results for the RIF regression and RIF-Logit of Firpo, Fortin, and Lemieux (2009). We use both income and expenditures in logarithm, so that the coefficient estimates can be interpreted as an elasticity. Confidence intervals are computed using 200 bootstrap replications.

| Quantile Partial Effect | |||||

| 10 | 25 | 50 | 75 | 90 | |

| Conditional distribution | |||||

| CQR | 0.383*** | 0.407*** | 0.408*** | 0.408*** | 0.425*** |

| (0.000571) | (0.000422) | (0.000246) | (0.000278) | (0.000336) | |

| Unconditional distribution | |||||

| RIF-OLS (linear) | 0.367*** | 0.388*** | 0.427*** | 0.396*** | 0.393*** |

| (0.0285) | (0.0170) | (0.0139) | (0.0130) | (0.0181) | |

| RIF-OLS (quadratic) | 0.360*** | 0.383*** | 0.427*** | 0.403*** | 0.406*** |

| (0.0275) | (0.0166) | (0.0140) | (0.0129) | (0.0182) | |

| RIF-OLS (cubic) | 0.370*** | 0.394*** | 0.440*** | 0.415*** | 0.412*** |

| (0.0279) | (0.0169) | (0.0143) | (0.0137) | (0.0183) | |

| RIF-Logit | 0.327*** | 0.395*** | 0.434*** | 0.403*** | 0.427*** |

| (0.0373) | (0.0260) | (0.0234) | (0.0242) | (0.0316) | |

| NW | 0.395*** | 0.405*** | 0.408*** | 0.409*** | 0.410*** |

| (0.0166) | (0.0111) | (0.00851) | (0.00810) | (0.00868) | |

| Observations | 21,017 | 21,017 | 21,017 | 21,012 | 21,017 |

Notes: The CQR analysis corresponds to a regression of log food expenditures on log income. UQPE estimates the effect of a marginal change in log income on the unconditional distribution of log food expenditures. Standard errors in parentheses (analytical for CQR, bootstrap with 200 replications for RIF and NW). * indicates significance at 10 %, ** at 5 % and *** at 1 %.

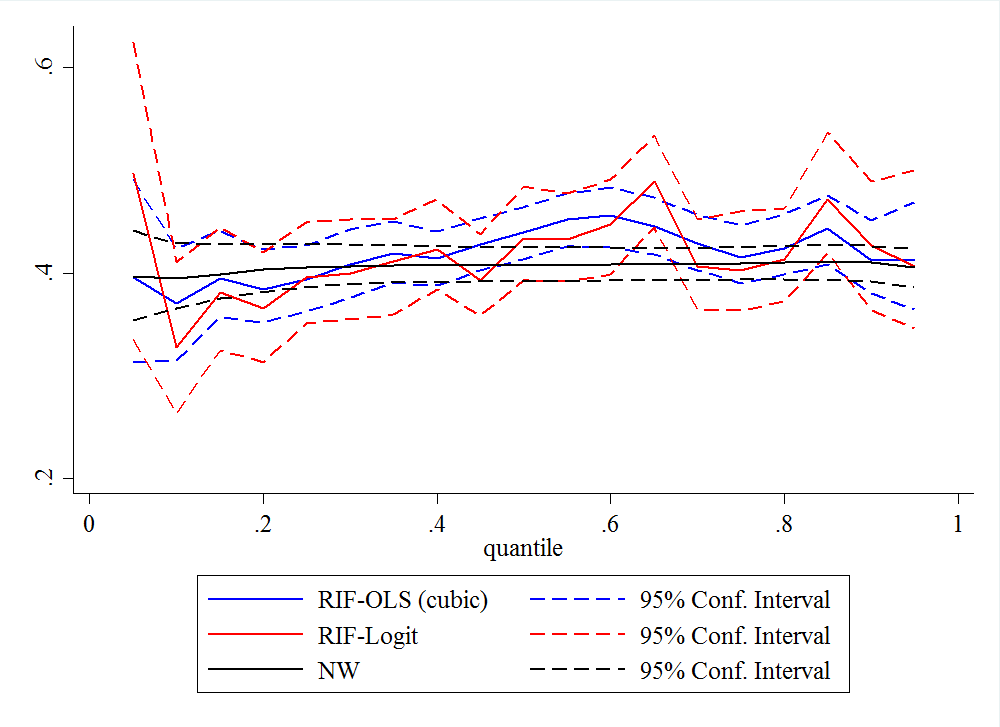

Notes: UQPE NW (black), RIF-OLS (cubic polynomial, blue) and RIF-Logit (red) estimates together with 95% confidence intervals estimated using bootstrap with 200 replications.

Notes: Matched coefficients for estimates together with 95% confidence intervals estimated using bootstrap with 200 replications.

| Quantile Partial Effect | |||||

| 10 | 25 | 50 | 75 | 90 | |

| Conditional distribution | |||||

| CQR | 0.778*** | 0.784*** | 0.776*** | 0.738*** | 0.662*** |

| (0.000359) | (0.000265) | (0.000211) | (0.000283) | (0.000295) | |

| Unconditional distribution | |||||

| RIF-OLS (linear) | 0.700*** | 0.706*** | 0.761*** | 0.768*** | 0.731*** |

| (0.0295) | (0.0194) | (0.0216) | (0.0229) | (0.0292) | |

| RIF-OLS (quadratic) | 0.674*** | 0.693*** | 0.765*** | 0.792*** | 0.769*** |

| (0.0278) | (0.0183) | (0.0217) | (0.0251) | (0.0338) | |

| RIF-OLS (cubic) | 0.683*** | 0.719*** | 0.801*** | 0.817*** | 0.774*** |

| (0.0267) | (0.0183) | (0.0217) | (0.0229) | (0.0275) | |

| RIF-Logit | 0.622*** | 0.641*** | 0.755*** | 0.794*** | 0.811*** |

| (0.0471) | (0.0329) | (0.0434) | (0.0475) | (0.0542) | |

| NW | 0.774*** | 0.773*** | 0.760*** | 0.732*** | 0.700*** |

| (0.0140) | (0.0102) | (0.00839) | (0.00863) | (0.0103) | |

| Observations | 21,461 | 21,461 | 21,461 | 21,461 | 21,461 |

Notes: The CQR analysis corresponds to a regression of log non-durable expenditures on log income. UQPE estimates the effect of a marginal change in log income on the unconditional distribution of log non-durable expenditures.

Standard errors in parentheses (analytical for CQR, bootstrap with 200 replications for RIF and NW). * indicates significance at 10 %, ** at 5 % and *** at 1 %.

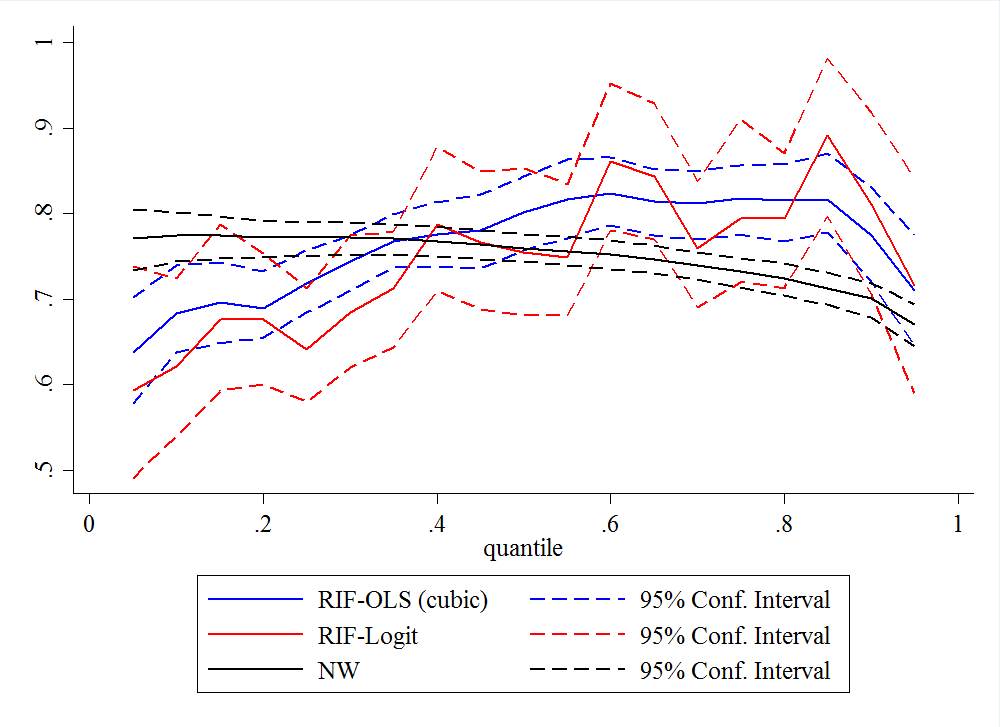

Notes: UQPE NW (black), RIF-OLS (cubic polynomial, blue) and RIF-Logit (red) estimates together with 95% confidence intervals estimated using bootstrap with 200 replications).

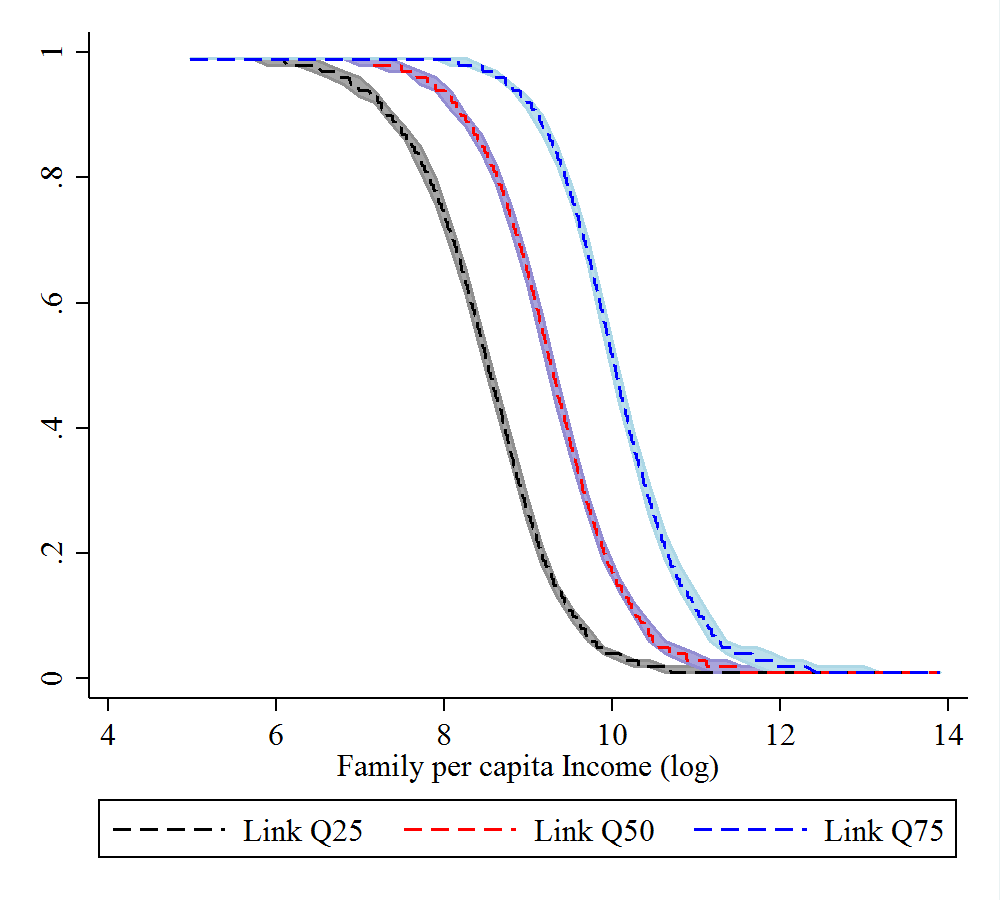

Notes: Matched coefficients for estimates together with 95% confidence intervals estimated using bootstrap with 200 replications.

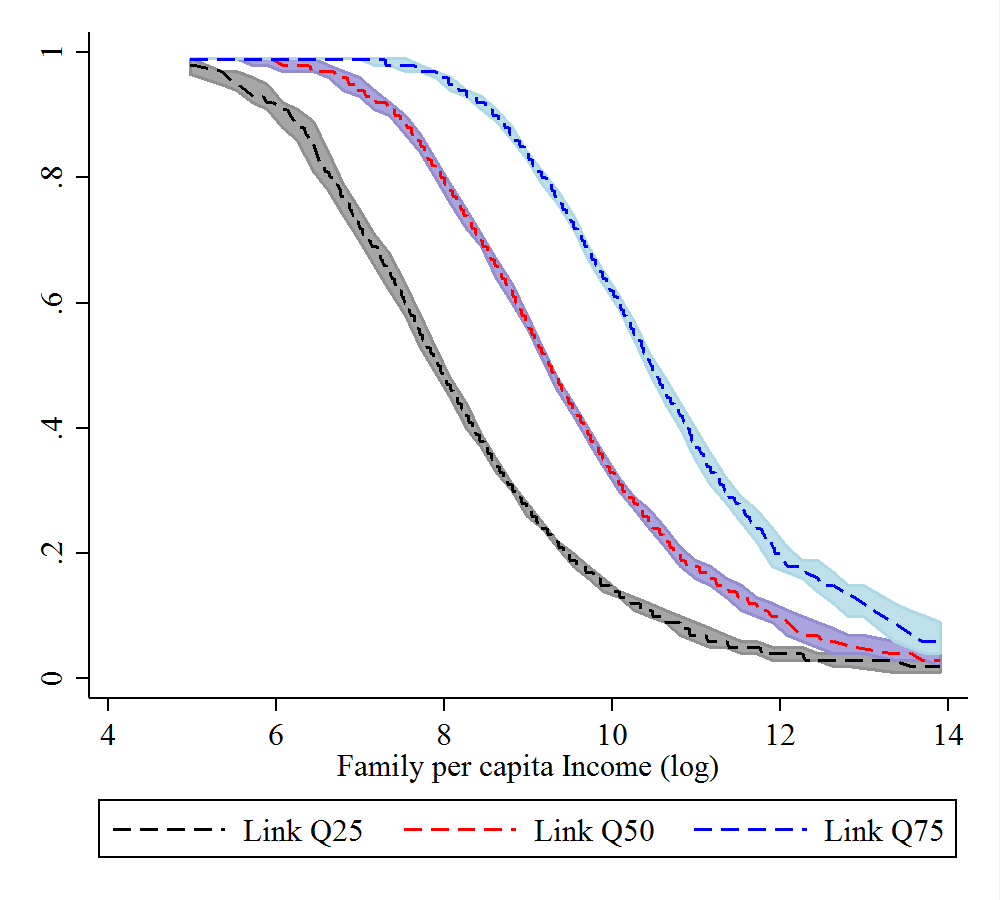

We estimate these models for different quantiles. The results are collected in Table 8 and Figure 5 for food expenditures, and Table 9 and Figure 7 for total non-durable expenditures. In order to explore the results in more detail, we also plot the by-product of this analysis that is the matching quantile function. This was implicitly used for the estimation of the UQPE NW estimator. Figures 6 and 8 plot the estimated match for for different values of log income, for food and non-durable expenditures, respectively. The last figures illustrate that for each there is a full range of variation in the corresponding CQPE model indexed by .

The results for food expenditures show evidence that CQR coefficients are roughly constant across , although mildly increasing. The proposed UQPE NW estimator is then also roughly constant across . The RIF estimates also have this pattern although they are estimated in a less precise manner. In all cases, the estimated effects can be interpreted as elasticities, implying that a 1% increase in income increase food consumption in less than 1%, about 0.4%. Moreover, since the CQR coefficients are mildly increasing, the variation in the UQPE has to be coming from the variation in the density of given . As increases, for the UQPE to increase, higher CQR coefficients must be getting higher weight. This happens if the density of “income|food” is moving to the right.

For the case of non-durable expenditures, the RIF estimates are increasing along , while the UQPE NW estimator is decreasing. The fact that RIF estimates have a larger range of variation than CQR and that it gives the counter-intuitive increasing pattern suggest that it might be misspecified. That is, if we assume that richest families have a higher saving rate than the poorer ones, the unconditional estimates should not increase along the quantiles.

A take away note from this example is that the empirical researcher should be aware of different modelling choices. RIF and UQPE NW estimators both rely on different assumptions to estimate the same parameter. As such, it may be a good procedure to report different alternatives and to highlight if differences occur.

7 Conclusion

This paper considers the use of conditional quantile regression analysis to estimate unconditional quantile partial effects. The proposed methodology is based on a matching and reweighting result to link the unconditional effects to the conditional ones. This method thus benefits from the usual conditional quantile regression estimation techniques, and suggests a two-step estimator for the unconditional effects. In the first step one estimates a structural quantile regression model, and in the second step a nonparametric regression is applied. We establish the asymptotic properties of the estimator. Monte Carlo simulations show evidence that the estimator has good finite sample performance and is robust to the selection of bandwidth and kernel. To illustrate the proposed methods, we study Engel’s curves in Argentina.

The current paper can be extended in several directions. First, the proposed model uses a simple linear quantile regression framework and is based on its coefficient estimators. The current framework can be applied to any other -consistent estimation procedure. In particular, as an example, instrumental variables quantile regression and/or panel data models deliver consistent estimators for the conditional effects in several related statistical models. The current methodology could be extended to evaluate unconditional effects, starting from any initial consistent conditional estimation procedure. Second, the current proposed framework can be used to evaluate any other functional analysis related to the unconditional quantile regression one. In other words, to recover general distributional effects. Third, the Nadaraya-Watson estimator is the first approximation to a larger family of estimators that can be used to estimate the unconditional effects. Local linear regression models is a proposed refinement to obtain possibly better asymptotic properties. Fourth, we leave optimal bandwidth choice for future research. Finally, the analysis may be extended in formalizing the resampling procedure and studying to practically construct uniform confidence bands.

Appendix A

A.1 Proof of Lemma 1

Recall that , , and and are one-dimensional. First we show that , defined in (2) as

can be written in the way of (5) as

By definition of quantiles, we have that this identity holds for all for a given fixed :

Differentiating both sides with respect to , we obtain

Since , then the result follows by solving for . Since the matching is a singleton, then for every , and any , we have . Thus, we evaluate at to yield

Given the identification result for in equation (4), we have that

which is the result in (A.1). Since and are non-zero, then

Therefore, we obtain (8):

A.2 Proof of Theorem 1

Let

Here, and are fixed, and the criterion function is the map for . Under Assumption 1.2, is strictly increasing, and hence has a unique zero given by . This shows that is -conditional quantile of . By Assumption 1.1, this can be written as .

Now we will show consistency: . The matching function is defined to be the (approximate) zero of the random criterion function :

The computational procedure outlined in equation (14) implicitly defines as for some in such that

We want to show that this, together with Assumption 1.5 that ensures , imply that . For a given , let , that is

We focus on the difference . We write

For the last term, we can write because the derivative is bounded by Assumption 1.3. To alleviate notation, define:

which is differentiable with bounded derivative by 1.3. Using Assumption 1.3 we have that

so that

By Assumption 1.2, is bounded away from zero, so that is bounded. We focus first on the difference in the sums.

We note first that since , by definition of quantiles, . This means that if , then , and if , then either , or . Thus, the difference

is either 1 or 0. Using this, we have

Now, for the second term, we note that

where is between and . Therefore, we have that

Since is a Z-estimator, we follow Theorem 5.9 in van der Vaart (1998). We need to show that the criterion function converges uniformly in probability:

| (A.1) |

and that the zero is well-separated: for any

To show (A.1), we note that by Assumption 1.1

where is the Euclidean norm, and the bounds follow from Assumptions 1.3 and 1.4. To show that the zero is well-separated, we note that by Assumption 1.2, is strictly increasing, so that for any , if , then by the mean-value theorem

where is between and . Now, . Moreover, if , then , so that , where we take small enough such that . The same analysis can be carried out for , in which case: . Therefore,

where we have used that is bounded away from zero. Finally, we can invoke Theorem 5.9 in van der Vaart (1998), since we also showed that , therefore, .

Having shown consistency, we now prove it is actually -consistent. To that end, we use Assumption 1.5:

| (A.2) | ||||

By Assumptions 1.1, 1.2, we have that , so that , so that we can do a first order term-by-term Taylor expansion to obtain

Here, is the Jacobian vector: the derivative of the map and is a vector of residuals of the expansion. Plugging this into the previous display, we obtain

| (A.3) |

Here the term is scalar-valued and collects all the terms from . Now, by Assumption 1.4. Also, by Assumption 1.3 . Therefore, since , we have that .

A.3 Proof of Theorem 2

To alleviate notation, we write:

Thus, our estimator of can be written as

The unfeasible version is then

Consider the difference

| (A.4) |

First we focus on the second term of (A.3). We note that

is an estimator of the density of evaluated at , the estimator of ; while

is an estimator of the density of evaluated at . The next lemma, proved below, will be useful.151515We thank an anonymous referee for pointing us in this direction.

Under the above lemma, we can write

| (A.5) |

which implies that .

Now we focus on the first term of (A.3). For the numerator, consider the following decomposition

| (A.6) |

First we will show that . We do a first order Taylor expansion to obtain

| (A.7) |

Consider the first term. Let denote the -th partial derivative of with respect to . The expected value is

where we used Assumption 4 to expand the joint density. The properties of the kernel of Assumption 2 yield

Therefore, the bias is of order :

For the variance, we have

We take care of each term at a time.

For the other term, we have

Combining the bias and variance results, we obtain

Now we show that in (A.3) satisfies

We use the following decomposition, similar to the one in Theorem 1:

We have

Here we use and to conclude that the first term is . For the second term, we use the mean value theorem and Theorem 1 to get

| (A.8) | ||||

where is the remainder of the expansion of in Theorem 1, which, by Assumption 5, is over the support of . Now, by Assumption 5, , are bounded. Moreover, . All these facts together imply that in the above display, the order of the terms are , , and respectively. Therefore, we can conclude that .

A.4 Proof of Lemma 2

We have for some random ,

| (A.10) |

We focus on the difference .

The terms comes from the continuity of the first derivative which follows from Assumption 4. Now we derive the uniform rate of the estimator of the first derivative. We follow the exposition in Section 1.12 of Li and Racine, and modify it to the case of the derivative. We write

| (A.11) |

and take care of each term at a time. We start with the second term, the bias term. The first derivative of the kernel estimator is

We will use the fact that, by Assumption 2, , , for , and . In the following, denotes the -th derivative.

Since, by Assumption 4, the derivatives are bounded, then in the compact set , the bias is

Now we address the first term in (A.11). As usual, since is a compact set, we can pick a finite number of intervals centered at for and length that cover . We write

We start with . Write

Then, for some ,

| (A.12) |

Using Markov’s inequality161616 for . we aim to bound uniformly . We write

| (A.13) |

for some . By Assumption 2, is a bounded function then,

for some that does not depend on . Let , be such that

for all , for sufficiently large. Since for , then

so that

because , and for . Thus, going back to (A.4), we have for , and sufficiently large, that

| (A.14) |

Now, the second moment of is bounded by

by doing the change of variable , where does not depend on because by Assumption 4, and are bounded. Going back to (A.4), we obtain

| (A.15) |

and this holds uniformly, so that

Therefore, going back to (A.4), the bound is

To utilize the Borel-Cantelli lemma,171717If , then almost surely. we need to choose a sequence , such that , and such that the bound is summable. We can take

so that

and the bound is

Therefore, by choosing the order of and sufficiently large so that is sufficiently small (negative), then the right-hand side of the above display will be summable. This means that, by the Borel-Cantelli lemma, almost surely.

Now, for the term , we have

Here we use the Lipschitz continuity of , which is guaranteed by Assumption 2 by the second derivative being bounded. For some ,

where is the common length of the intervals. Since the bound is independent of , then

Thus, we choose to be of the same order as :

which implies we need . Therefore,

Finally, for the term , we have

Here we have

so that, as with , we have

Therefore, the order of is

Going back to (A.4), we have

Now we show that under Assumption 3, the order of the remainder is . We need the bandwidth to satisfy

which means we need

So we have that we need with . This is also ensures , and . Now, the bias in the estimation is of order , so that we need the following undersmoothing rate

which means we need , or , which implies . For example, for , we have . Therefore,

A.5 Proof of Corollary 1

Recall that by equation (11), we have that

and that we defined

and, by construction, a.s. and, by Assumption 6, for every in the support of . Moreover, for , we have

| (A.16) |

We focus on

| (A.17) |

Consider the first term:

For this term we use the Lindberg-Feller CLT. First we compute the variance of the sum.

because and are continuous, and are bounded. The conclusion follows from the dominated convergence theorem. We write

To apply the Lindberg-Feller CLT, we define

We need to show that, for some ,

We have

It will be sufficient to focus on

which goes to 0 since and is continuous at . We have used the bound of the higher order conditional expectation of : a.s., and that . Therefore,

| (A.18) |

since .

The second term in the expansion of is a bias term. We now find its rate of convergence. We start with the numerator.

We do a Taylor expansion on the density and the conditional expectation and we use the fact that , when , and . Let denote the -derivative with respect to of the product evaluated at . The first term is

since the derivatives are uniformly bounded. Now, for the other term we do a similar expansion of the density.

Therefore, we obtain that the bias is of order :

Now, for the variance we have

This implies that

Therefore, we obtain that

Under Assumption 3, this term is , since

since , and as Therefore, the bias term is

References

- (1)

- Angrist, Chernozhukov, and Fernández-Val (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val (2006): “Quantile Regression under Misspecification, with an Application to the U.S. Wage Structure,” Econometrica, 74, 539–563.

- Atkin, Faber, Fally, and Gonzalez-Navarro (2020) Atkin, D., B. Faber, T. Fally, and M. Gonzalez-Navarro (2020): “A New Engel on Price Index and Welfare Estimation,” NBER Working Paper No. 26890.

- Autor, Katz, and Kearney (2005) Autor, D. H., L. S. Katz, and M. S. Kearney (2005): “Rising Wage Inequality: The Role of Composition and Prices,” NBER Working Paper 11628.

- Belloni and Chernozhukov (2011) Belloni, A., and V. Chernozhukov (2011): “l1-Penalized Quantile Regression in HIgh-Dimensional Sparse Models,” Annals of Statistics, 39, 82–130.

- Bera, Galvao, Montes-Rojas, and Park (2016) Bera, A., A. Galvao, G. Montes-Rojas, and S. Park (2016): “Asymmetric Laplace Regression: Maximum Likelihood, Maximum Entropy and Quantile Regression,” Journal of Econometric Methods, 5(1), 79–101.

- Blundell, Chen, and Kristensen (2007) Blundell, R., X. Chen, and D. Kristensen (2007): “Semi-Nonparametric IV Estimation of Shape-Invariant Engel Curves,” Econometrica, 75(6), 1613–1669.

- Charles, Hurst, and Roussanov (2009) Charles, K., E. Hurst, and N. Roussanov (2009): “Conspicuous Consumption and Race,” Quarterly Journal of Economics, 124, 425–467.

- Chernozhukov and Fernández-Val (2005) Chernozhukov, V., and I. Fernández-Val (2005): “Subsampling inference on quantile regression processes,” Sankhya, 67, 253–276.

- Chernozhukov, Fernández-Val, and Galichon (2010) Chernozhukov, V., I. Fernández-Val, and A. Galichon (2010): “Quantile and Probability Curves Without Crossing,” Econometrica, 78(3), 1093–1125.

- Chernozhukov, Fernández-Val, and Kowalski (2015) Chernozhukov, V., I. Fernández-Val, and A. E. Kowalski (2015): “Quantile Regression with Censoring and Endogeneity,” Journal of Econometrics, 186(1), 201–221.

- Chernozhukov, Fernández-Val, and Melly (2013) Chernozhukov, V., I. Fernández-Val, and B. Melly (2013): “Inference on Counterfactual Distributions,” Econometrica, 81(6), 2205–2268.

- de Castro, Costa, Galvao, and Zubelli (2023) de Castro, L., B. N. Costa, A. F. Galvao, and J. P. Zubelli (2023): “Conditional Quantiles: An Operator-Theoretical Approach,” Bernoulli, forthcoming.

- Firpo, Fortin, and Lemieux (2009) Firpo, S., N. Fortin, and T. Lemieux (2009): “Unconditional Quantile Regression,” Econometrica, 77(3), 953–973.

- Fortin, Lemieux, and Firpo (2011) Fortin, N., T. Lemieux, and S. Firpo (2011): “Decomposition Methods in Economics,” in Handbook of Labor Economics, ed. by O. Ashenfelter, and D. Card, vol. 4, pp. 1–12. Amsterdam: Elsevier.

- Galvao and Wang (2015) Galvao, A., and L. Wang (2015): “Uniformly Semiparametric Efficient Estimation of Treatment Effects With a Continuous Treatment,” Journal of the American Statistical Association, 110, 1528–1542.

- Gutenbrunner and Jurečková (1992) Gutenbrunner, C., and J. Jurečková (1992): “Regression rank scores and regression quantiles,” Annals of Statistics, 20, 305–330.

- Hall and Horowitz (2013) Hall, P., and J. Horowitz (2013): “A Simple Bootstrap Method For Constructing Nonparametric Confidence Bands For Functions,” Annals of Statistics, 41, 1892–1921.

- Härdle and Bowman (1988) Härdle, W., and A. Bowman (1988): “Bootstrapping in Nonparametric Regression: Local Adaptive Smoothing and Confidence Bands,” Journal of the American Statistical Association, 83, 1892–1921.

- He, Pan, Tan, and Zhou (2022) He, X., X. Pan, K. M. Tan, and W.-X. Zhou (2022): “Scalable Estimation and Inference for Censored Quantile Regression Process,” Annals of Statistics, 50, 2899–2924.

- Heffetz (2011) Heffetz, O. (2011): “A Test of the Conspicuous Consumption: Visibility and Income Elasticities,” Review of Economics and Statistics, 93(4), 1101–1117.

- Inoue, Li, and Xu (2021) Inoue, A., T. Li, and Q. Xu (2021): “Two Sample Unconditional Quantile Effect,” ARXIV: https://arxiv.org/pdf/2105.09445.pdf.

- Knight (2002) Knight, K. (2002): “Comparing Conditional Quantile Estimators: First and Second Order Considerations,” Working Paper.

- Koenker (2005) Koenker, R. (2005): Quantile Regression. Cambridge University Press, Cambridge.

- Koenker and Bassett (1978) Koenker, R., and G. W. Bassett (1978): “Regression Quantiles,” Econometrica, 46, 33–49.

- Koenker, Chernozhukov, He, and Peng (2020) Koenker, R., V. Chernozhukov, X. He, and L. Peng (2020): Handbook of Quantile Regression. Chapman and Hall/CRC.

- Koenker and Hallock (2001) Koenker, R., and K. Hallock (2001): “Quantile Regression,” Journal of Economic Perspecives, 15 (4), 143–156.

- Koenker and Machado (1999) Koenker, R., and J. A. F. Machado (1999): “Godness of Fit and Related Inference Processes for Quantile Regression,” Journal of the American Statistical Association, 94, 1296–1310.

- Koenker and Xiao (2002) Koenker, R., and Z. Xiao (2002): “Inference on the Quantile Regression Process,” Econometrica, 70, 1583–1612.

- Lee (2021) Lee, Y.-Y. (2021): “Nonparametric Weighted Average Quantile Derivative,” Econometric Theory, pp. 1–39.

- Lewbel (1997) Lewbel, A. (1997): “Consumer Demand Systems and Household Equivalence Scales,” Handbook of Applied Econometrics, 2, 167–201.

- Lewbel (2008) (2008): “Engel Curves,” The New Palgrave Dictionary of Economics, 2.

- Li (2009) Li, N. (2009): “An Engel Curve for Variety,” Review of Economics and Statistics, 103(1), 72–87.

- Machado and Mata (2005) Machado, J. A. F., and J. Mata (2005): “Counterfactual Decomposition of Changes in Wage Distributions Using Quantile,” Journal of Applied Econometrics, 20, 445–465.

- Martinez-Iriarte (2023) Martinez-Iriarte, J. (2023): “Sensitivity Analysis in Unconditional Quantile Effects,” Working Paper.

- Martinez-Iriarte, Montes-Rojas, and Sun (2022) Martinez-Iriarte, J., G. Montes-Rojas, and Y. Sun (2022): “Unconditional Effects of General Policy Interventions,” Working Paper.

- Martinez-Iriarte and Sun (2022) Martinez-Iriarte, J., and Y. Sun (2022): “Identification and Estimation of Unconditional Policy Effects of an Endogenous Binary Treatment,” Working Paper.

- Melly (2005) Melly, B. (2005): “Decomposition of Differences in Distribution Using Quantile Regressions,” Labour Economics, 12, 577–590.

- Ota, Kato, and Hara (2019) Ota, H., K. Kato, and S. Hara (2019): “Quantile Regression Approach to Conditional Mode Estimation,” Electronic Journal of Statistics, 13, 3120–3160.

- Perez-Truglia (2013) Perez-Truglia, R. (2013): “A Test of the Conspicuous-Consumption Model Using Subjective Well-Being Data,” Journal of Socio-Economics, 45, 146–154.

- Portnoy (2012) Portnoy, S. (2012): “Nearly Root-N Approximation for Regression Quantile Process,” Annals of Statistics, 40, 1714–1736.