Generalizing Impermanent Loss on Decentralized Exchanges with Constant Function Market Makers

Abstract

Liquidity providers are essential for the function of decentralized exchanges to ensure liquidity takers can be guaranteed a counterparty for their trades. However, liquidity providers investing in liquidity pools face many risks, the most prominent of which is impermanent loss. Currently, analysis of this metric is difficult to conduct due to different market maker algorithms, fee structures and concentrated liquidity dynamics across the various exchanges. To this end, we provide a framework to generalize impermanent loss for multiple asset pools obeying any constant function market maker with optional concentrated liquidity. We also discuss how pool fees fit into the framework, and identify the condition for which liquidity provisioning becomes profitable when earnings from trading fees exceed impermanent loss. Finally, we demonstrate the utility and generalizability of this framework with simulations in BalancerV2 and UniswapV3.

Keywords Liquidity Provider Decentralized Exchange Automated Market Maker Impermanent Loss

1 Introduction

Decentralized finance (DeFi) aims to provide a trustless system of finance by replacing third-parties who control liquidity flows with smart contracts that manage rules for issuing debt and trading. Between 2019 and 2021, the industry has grown to manage over $150 billion of assets. The largest applications within the DeFi ecosystem are decentralized exchanges (DEXs), which coordinate large-scale trading of digital assets in a non-custodial manner. This is achieved through automated algorithms, as opposed to a centralized exchange (CEX) which requires an intermediary to facilitate the transfer and custody of funds.

There are two types of agents that can interact with a DEX, liquidity providers (LPs) and liquidity takers (LTs). LPs provide their digital assets to a liquidity pool which acts as the counterparty for LTs. For every trade by an LT, the pool takes a portion of the trade as a fee, which is then distributed amongst the LPs and protocol treasury. In this way, LPs are motivated to participate with the incentive of generating a passive income in a way not accessible on CEXs. The more liquidity provided to a liquidity pool, the better the trade dynamics for LTs (e.g. lower slippage), therefore attracting more trade activity. Therefore, a big effort is made by DEXs to attract LPs to their platforms, typically in the form of financial incentives such as liquidity mining.

A major barrier for many LPs is impermanent loss (IL). IL is the opportunity cost of providing assets in a liquidity pool instead of holding those same assets over the investment period. Cartea et al. (2022) have shown that for convex constant product market makers, . Therefore, liquidity provisioning is only profitable when trading and liquidity mining fees compensate for this loss. Research by Loesch et al. (2021) revealed that over 50% of LPs on UniswapV3 suffer IL which is not compensated by fee earnings. They also showed that the most popular strategy is to passively invest, with 30% of LPs holding their positions for longer than a month. Furthermore, each DEX can operate with a different market maker algorithm, fee structure and (concentrated) liquidity dynamics, and the current absence of any formal general framework makes it difficult to easily analyze IL across exchanges. This work aims to establish the missing general framework and employs it to consider different forms of IL over UniswapV3 and BalancerV2.

2 Fundamentals of Constant Function Market Maker Pools

Consider a pool of assets. Each asset is characterized by its quantity in the pool, given by the number of the respective token, and its internal instantaneous price with respect to the other assets in the pool. Denote the quantities of the assets in the pool as and the internal instantaneous price of asset with respect to asset as , meaning one unit of asset is exchangeable for units of asset .

There are two events that can trigger a change in pool state: a trade and a quote. A trade occurs when an LT exchanges assets with the liquidity pool. Unlike a swap which is constrained to an exchange of two assets (Bichuch and Feinstein (2022)), a trade allows for an exchange of up to assets. Suppose that the LT wants to add and/or remove assets from the pool in exchange for asset , then a trade can be defined as

| (1) |

where represents the change in the -th asset quantity from the perspective of the pool. The quantites are given by the trader, and only needs to be solved for by the pool.

A quote occurs when an LP provides or withdraws liquidity from the liquidity pool. A quote can be defined as

| (2) |

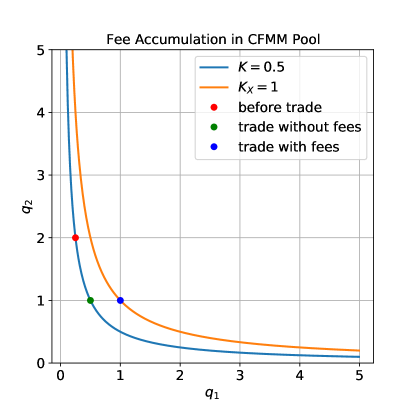

At all times, the assets of a pool satisfy the automated market maker (AMM), which dictates new asset quantities given an event. The most common type of AMM implemented in DEXs is the constant function market maker (CFMM) of the form

| (3) |

where is a continuous map, is the depth of the pool and are any further parameters.

The instantaneous price of asset with respect to asset is defined by the quantity of asset that can be traded for an infinitesimally small quantity of asset . For a trade where one of and is negative and the other is positive, the instantaneous price is given by

| (4) |

where the relationship between and is derived via the CFMM formula in (3). Assuming that , then the CFMM is constrained by the condition . Furthermore, given the pool should always sell at a higher price than it buys, the CFMM should be convex with respect to the asset quantities (Cartea et al. (2022)).

Finally, each asset has an associated weight, , which is defined as the proportion of value in the pool held in the -th asset, that is

| (5) |

3 Uniform Pool Mechanics

In a uniform liquidity pool, LPs provide liquidity over the entire price range for LTs to make trades with. An LP therefore only needs to decide which pools to provide liquidity for based on the assets held within. An example of the dynamics described here can be found in Section 7.2.

3.1 Solving an Event

For simplicity, this section will ignore fees. When a trade occurs, the CFMM equation in (3) can be solved to obtain the final asset quantities. Given a trade, the amount of asset to be deposited or withdrawn, , needs to solved for:

| (6) |

On the other hand, when a quote occurs, a new depth parameter, , needs to be calculated from the new asset quantities; the new depth calculation is given by

| (7) |

3.2 Pool Share

Each LP has a share of the pool they are invested in. This is tracked by LP tokens, where each LP owns a proportion of these tokens and they are created and destroyed to affect the total supply as LPs provide or withdraw liquidity. Let be the quantity of asset owned by the -th LP. The pool share of the -th LP, , is defined by asset quantities, not prices, and is given by

| (8) |

3.3 Pool Fees

For every trade with a pool, a percentage of the inbound assets to the pool is taken as a fee and distributed amongst the LPs and protocol treasury. Denote by the total fee paid by LTs and by the protocol fee, that is, the percentage of the total fee designated to the protocol treasury. The trade quantities for the -th asset including fees, , can then be derived from the trade quantities excluding fees, , which are solved for in (6), to give

| (9) |

Given a trade including fees, the quantities of inbound assets can be defined as

| (10) |

and the total fees for all LPs generated from the trade, , is given by

| (11) |

These fees are generally reinvested into the LP position, although in some cases they can an also be kept in a separate account. Either way, the LP receives their fees on top of their underlying position in the pool once they exit their position. Furthermore, the -th LP specific fees, , can be derived from the total fees generated by the pool and the LP pool share as

| (12) |

Assuming trading fees are collected in the pool, the CFMM dynamics are affected in the event of a trade since a new pool depth, , needs to be computed for the new trade quantities, given as

| (13) |

Liquidity mining is a feature in many DEXs, and allows LPs to stake their LP tokens for extra rewards; generally, this is used to incentivize LPs to keep their positions for longer time periods. Each DEX handles this differently, but these rewards are also collected once an LP exits their position; in the meantime, these are generally kept in a separate account.

4 Concentrated Pool Mechanics

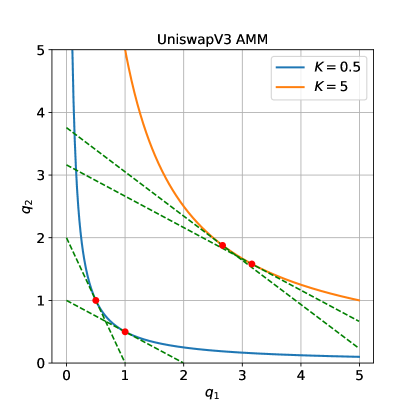

Concentrated liquidity (CL) allows LPs to specify an instantaneous price range for the liquidity they want to provide. In practice, the continuous price space is discretized into ticks such that LPs can provide liquidity in a range between any two ticks which need not be adjacent. An example of the dynamics described here can be found in Section 7.1.

4.1 Price Surface

Given a pool with assets, an LP must provide liquidity in any instantaneous price range, , for an asset pair , with bounds for pairs:

| (14) |

From the perspective of the pool, the price ticks form a price surface, that is, a grid in dimensions with ticks in the -th dimension.

A unit price range, , defines a price range bounded by adjacent ticks such that the space cannot be subdivided further given a price surface

| (18) |

The active price range defines the unit price range in which the current instantaneous prices reside such that at any time

| (19) |

4.2 Virtual Pool

Denote by the quantity of asset provided by the -th LP in the price range and let each unit price range in the pool have -th asset quantity . Given liquidity providers in the pool, the asset quantities in a unit price range can be defined as a transformation of the LP quantities

| (20) |

where is the indicator function of interval .

In practice, these real asset quantities are not used to define pool behavior, but instead, a virtual pool with virtual quantities and virtual depth is defined over the active price range (Adams et al. (2021)). Specifically, the active price range only needs to hold enough assets to cover an instantaneous price movement to a tick boundary. To achieve this, the CFMM specified in (3) is translated such that the position is solvent exactly within the active range. A virtual pool can be defined over any finite price range. Denote by the real quantity of the -th asset over the price range , by the virtual quantity of the -th asset over the same range, and by the virtual depth. Then

| (21) | |||

| (22) |

4.3 Solving an Event

Given a new quote, the new quantities in each unit price range can be computed as in (20).

Given a trade, , if the active range does not change, the CFMM equation looks very similar to (6), just using the fixed virtual depth and virtual asset quantities to solve for , that is

| (23) |

However, suppose a trade causes the instantaneous rate to cross separate price ticks, then the order is executed as separate transactions with the respective values for the virtual depths. A tick is crossed once the real quantities of any asset in the unit range are depleted. However, the boundary condition can also be calculated using the virtual pool in the active range. Define by the control, the fraction of a trade that has been completed taking into account all quantity changes the trader has control over. In other words, given a trade needs to be solved for a quantity , is applied as a fraction to the trade for as

| (24) |

where can be solved for by the CFMM equation

| (25) |

Therefore, the instantaneous price at some time into the trade, , can be represented as a function of the control , in the form

| (26) |

and so given some active price range, the expression can be solved to find and , that is, the controls that push the instantaneous rate of asset pair to the lower and upper bound of the active range.

| (27) |

4.4 Pool Share

In pools with CL, LPs own a share of the liquidity in each unit price range. Similarly to uniform pools, this is defined by asset quantities. Given a unit price range , the -th LP with liquidity in the price range owns

| (28) |

4.5 Pool Fees

Given a trade over active price ranges and controls such that , the incoming assets to the pool over each active range is

| (29) |

so that the pool fee over each active range are

| (30) |

The total fees paid by LTs are distributed amongst the LPs who own liquidity in the active ranges of the trade. Therefore, the -th LP will receive

| (31) |

In CFMMs with CL, fee income is not automatically reinvested in the pool because LPs can provide liquidity in various ranges simultaneously, so the distribution and reinvestment of fees across different ranges is a choice made by the LP. This is in contrast to the fee structure for CFMMs without CL as described in Section 3.3 where fees are more commonly automatically compounded into the LP position (not including liquidity mining fees).

5 Arbitrage

Let the external FIAT prices of the assets in a pool be represented by . A difference between the external FIAT price and the internal instantaneous price of assets in a pool leads to arbitrage trades, which alter the quantities of assets. The trades continue until the new instantaneous prices reflect the current FIAT prices. This process is referred to as equilibration of the pool. In an equilibrated pool, the instantaneous prices match the external FIAT prices of the assets. This price balance condition (PBC) can be encoded by equations, in the form

| (32) |

If equation (32) does not hold, the pool is not in equilibrium and an arbitrage opportunity exists which LTs can take advantage of. Let a specific arbitrage, refer to the arbitrage opportunity of an asset with respect to an asset , that is

| (33) |

Further, let arbitrage, be a reduction of the specific arbitrage such that it defines the total arbitrage opportunity in asset given by

| (34) |

6 Impermanent Loss

Impermanent loss (IL) is the difference between the value of assets provided as liquidity in a pool and the value of those same assets had the LPs simply held them instead of providing liquidity. Given a pool with assets, let there be trades, , and quotes, , in the time range . Further, denote by the sum of all quotes in the time range as

| (35) |

The strict definition of IL for a pool ignoring fees is given in a FIAT currency by

| (36) |

However, it can also be given in terms of an asset as

| (37) |

6.1 Relative Value

Relative value (RV) is a measure that has a more intuitive meaning than IL, and is defined as the ratio between the value of assets provided as liquidity and the value of those same assets had the LP simply held them instead of providing liquidity. Again, there are two ways to define RV depending on the frame of reference: either with respect to external FIAT prices or internal instantaneous prices. The RV with respect to the external FIAT price ignoring fees is defined as

| (38) |

and the RV with respect to asset in the pool ignoring fees is defined as

| (39) |

If , then the pool is in equilibrium, else there is an arbitrage opportunity that can be exploited by LTs.

A change in RV (and IL) only arises when there is a trade in the pool. Assume there are no trades and only quotes in the time range , then

| (40) |

6.2 Fee-Adjusted Relative Value

Fee-adjusted relative value (FARV) measures the relative value of a pool taking into account the fees generated by trades that are allocated to LPs. For clarity, denote by the quantity of the -th asset in the pool without fees, the set by the fees generated from each of the trades, and by the sum of the fees as

| (41) |

The FARV with respect to FIAT prices and with respect to asset are defined as

| (42) | |||

| (43) |

In the event of a quote, FARV behaves in the same way as RV since no fees are collected, so that .

6.3 Liquidity Provider Profitability Condition

For a pool with a CFMM as defined in (3), due to the convexity of the CFMM (Cartea et al. (2022)). The LP profitability condition defines the space where the value of fees earned by an LP outweigh the value of IL suffered. For pools without CL, IL maps linearly from the pool to an individual LP via the pool share ratio. The LP profitability condition is given for pools without CL as

| (44) |

This is not the case for pools with CL because the IL of the pool does not map linearly with the IL of an individual LP. Therefore, the FARV of the individual LP, , should be more explicitly considered. Consider a time range , denote by the quantity of asset owned by a single LP and by the final quantity of asset owned by a single LP ignoring fees. Further, let denote the total quote of asset given by the LP and the total fees allocated to the LP in asset over the time period. Then the LP profitability condition can be defined for a pool with CL as

| (45) |

7 Examples

This section demonstrates the utility of the framework discussed here over different DEXs.

7.1 UniswapV3

At the time of writing, UniswapV3 was the second largest DEX by liquidity with $3.49b TVL and $4.11b trade volume (7 day). It features concentrated liquidity and has a common type of CFMM known as a constant product market maker (CPMM), constrained to two assets with time-invariant weights , that is

| (46) |

From this market maker, the instantaneous price can be derived as

| (47) |

Further, the virtual pool with virtual quantities and virtual depth in the price range with real quantities is defined as (Adams et al. (2021))

| (48) | |||

| (49) | |||

| (50) |

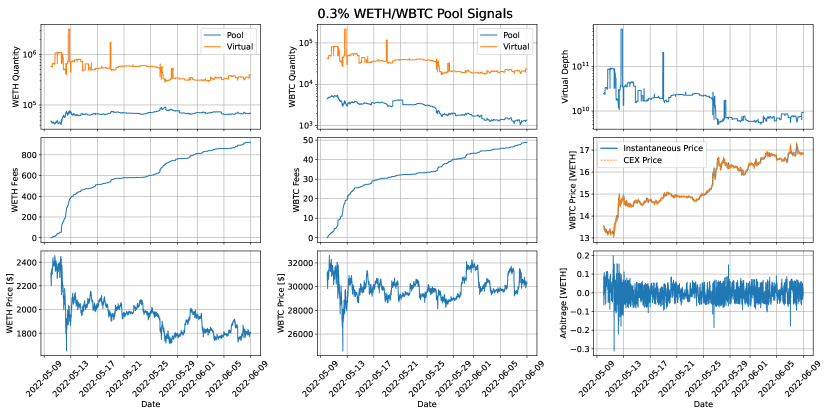

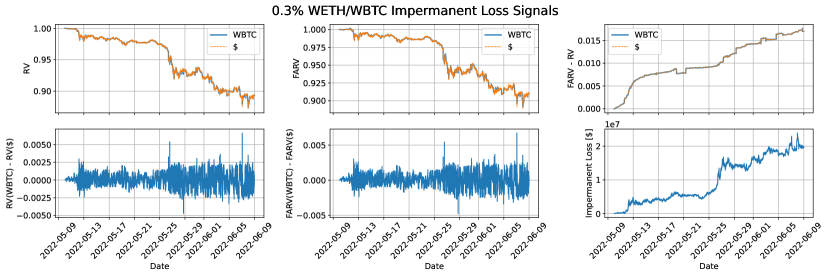

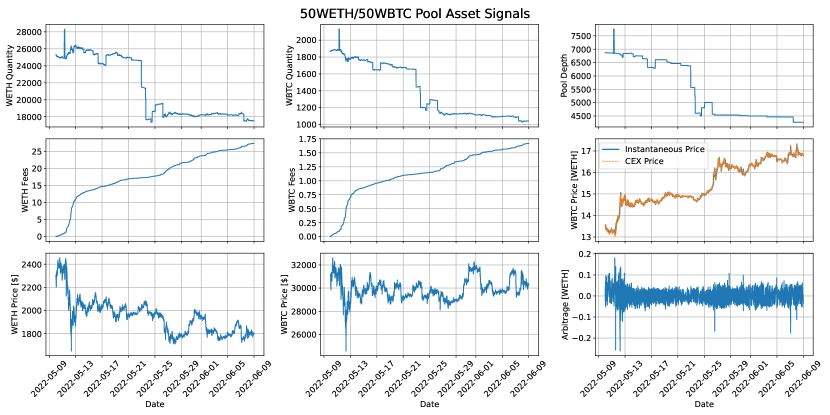

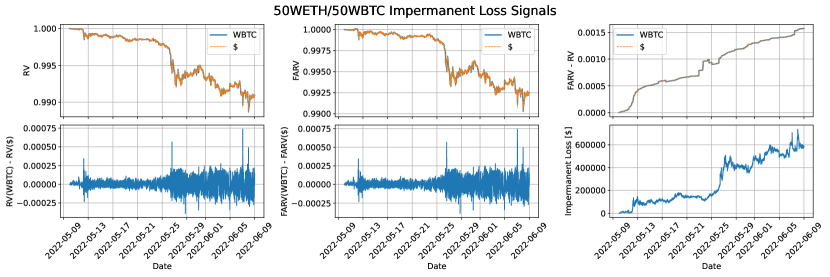

In UniswapV3, the pool fees are fixed to a discrete set such that each asset pair has a unique pool for each fee tier. The figures in this section analyze pool address 0xCBCdF9626bC03E24f779434178A73a0B4bad62eD over a month with a sampling period of one minute. This pool contains WETH and WBTC with a 0.3% pool fee. Figure 3 shows the evolution of the quantities of assets in the pool, and the fees generated from trades and arbitrage, while Figure 4 shows how the variants of IL change over time.

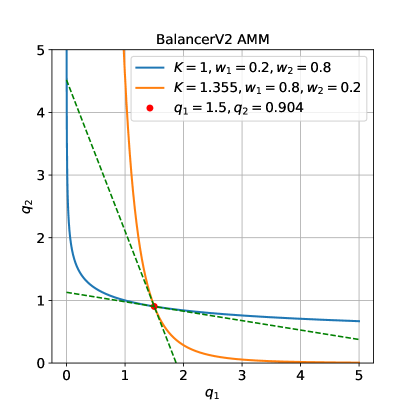

7.2 BalancerV2

At the time of writing, BalancerV2 was one of the top 5 DEX by liquidity with $1.2b TVL and $963m trade volume (7 day). It does not feature concentrated liquidity and has a generalized constant product market maker for assets known as a constant mean market maker (CMMM) given by (Angeris et al. (2019))

| (51) |

From this market maker the instantaneous price can be derived as (Martinelli and Mushegian (2019))

| (52) |

For weighted math pools (pools that contain a non-stablecoin asset), the weights are set at pool creation and are time-invariant. Therefore, given the AMM and pool fee percentage are static, the LP profitability condition is used to calculate whether the LP fees overcome IL for any trade in isolation. In BalancerV2, a trade is constrained between 2 assets, given by asset and asset , and fees accumulate in the pool. Denote by the trade without fees, by the total fees of asset collected by the pool, and by fees of asset allocated to the LPs in the pool as

| (53) | |||

| (54) |

where and are defined as in Section 3.3.

There are three pool asset quantities to consider: represents the starting quantity of asset before the trade, represents the quantity of asset after the trade without fees, and represents the quantity of asset after the trade with fees. The final instantaneous price of asset with respect to asset after the trade with fees is denoted , with the hat symbol to emphasize its existence on a new AMM curve as

| (55) |

These parameters can be used to solve the LP profitability condition for and to identify the space of trades that are profitable for LPs to participate in, as given by

| (56) |

The AMM itself can be used to define the second equation to solve for the two unknowns (Martinelli and Mushegian (2019))

| (57) |

Now, suppose the trade deposits asset to the pool in exchange for asset such that and , then

| (58) |

The figures in this section analyze pool address 0xA6F548DF93de924d73be7D25dC02554c6bD66dB5 over a month with a sampling period of one minute. This pool is a weighted math pool on BalancerV2 containing WETH and WBTC with weights and fees . Given these pool parameters, (58) can be reduced as

| (59) |

Over the month period in Figure 7, 2472 out of 2622 individual trades would be profitable for an active LP to participate in. That is, ignoring gas fees, an LP participating in single trades would be profitable for roughly 94% of the trades as defined by the LP profitability condition.

8 Conclusion

This paper provides a general framework to understand asset pool dynamics for any constant product market maker, fee structure and optional concentrated liquidity. We introduce relative value as a more intuitive measure than impermanent loss, and define fee-adjusted relative value as a measure for LP profitability. The framework itself is validated with simulations in UniswapV3 and BalancerV2, where in both cases we observe that the passive pool suffers more from impermanent loss than it gains in fees. However, the LP profitability condition in BalancerV2 indicates that more active LPs have the potential to be profitable over the same period, with 94% of individual trades fulfilling the LP profitability condition. Unfortunately, the most popular LP strategy is to passively invest, with 30% of positions on UniswapV3 being held for over a month (Loesch et al. (2021)). Therefore, Compass Labs recommends LPs to invest more actively, and proposes that DEXs should market make more dynamically too, as opposed to the static pools currently observed.

References

- Cartea et al. [2022] Álvaro Cartea, Fayçal Drissi, and Marcello Monga. Decentralised finance and automated market making: Predictable loss and optimal liquidity provision. 2022. doi:http://dx.doi.org/10.2139/ssrn.4273989.

- Loesch et al. [2021] Stefan Loesch, Nate Hindman, Mark B Richardson, and Nicholas Welch. Impermanent loss in uniswap v3, 2021. URL https://arxiv.org/abs/2111.09192.

- Bichuch and Feinstein [2022] Maxim Bichuch and Zachary Feinstein. Axioms for automated market makers: A mathematical framework in fintech and decentralized finance, 2022. URL https://arxiv.org/abs/2210.01227.

- Adams et al. [2021] Hayden Adams, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. Uniswap v3 core. 2021. URL https://uniswap.org/whitepaper-v3.pdf.

- Angeris et al. [2019] Guillermo Angeris, Hsien-Tang Kao, Rei Chiang, Charlie Noyes, and Tarun Chitra. An analysis of uniswap markets, 2019. URL https://arxiv.org/abs/1911.03380.

- Martinelli and Mushegian [2019] Fernando Martinelli and Nikolai Mushegian. A non-custodial portfolio manager, liquidity provider, and price sensor. 2019. URL https://balancer.fi/whitepaper.pdf.