Identification in a Binary Choice Panel Data Model

with a Predetermined Covariate

Abstract

We study identification in a binary choice panel data model with a single predetermined binary covariate (i.e., a covariate sequentially exogenous conditional on lagged outcomes and covariates). The choice model is indexed by a scalar parameter , whereas the distribution of unit-specific heterogeneity, as well as the feedback process that maps lagged outcomes into future covariate realizations, are left unrestricted. We provide a simple condition under which is never point-identified, no matter the number of time periods available. This condition is satisfied in most models, including the logit one. We also characterize the identified set of and show how to compute it using linear programming techniques. While is not generally point-identified, its identified set is informative in the examples we analyze numerically, suggesting that meaningful learning about may be possible even in short panels with feedback. As a complement, we report calculations of identified sets for an average partial effect, and find informative sets in this case as well.

JEL Codes: C23, C33

Keywords: Feedback, Panel Data, Incidental Parameters, Partial Identification.

1 Introduction

Empirical researchers utilizing panel data generally maintain the assumption that covariates are strictly exogenous: realized values of past, current, and future explanatory variables are independent of the time-varying structural disturbances or “shocks”.111Dependence between the covariates and the time-invariant heterogeneity – the so-called “fixed effects” – is, of course, allowed. In many settings this assumption is unrealistic. If the covariate is a policy, choice or dynamic state variable, then agents may adjust its level in response to past shocks (as when, for example, a firm adjusts its current capital expenditures in response to past productivity shocks).

When strict exogeneity is untenable, sequential exogeneity – sometimes called predeterminedness – may be palatable. A predetermined covariate varies independently of current and future time-varying shocks, but general feedback, or dependence on past shocks, is allowed. Assumptions of this type play an important role in, for example, production function estimation (Olley and Pakes, , 1996, Blundell and Bond, , 2000).

In two seminal papers, Arellano and Bond, (1991) and Arellano and Bover, (1995), Manuel Arellano and his collaborators presented foundational analyses of questions of identification, estimation, efficiency and specification testing in linear panel data models with feedback. Today such models are both well-understood and widely-used (see Arellano, (2003) for a textbook review).

In contrast, the properties of nonlinear models with feedback are much less well-understood. In this paper we study binary choice. Most existing work in this area focuses on the case where the covariate is either strictly exogenous or a lagged outcome. Under strict exogeneity, Rasch, (1960) and Andersen, (1970) show that the coefficient on the covariate is point-identified using two periods of data when shocks are logistic. Chamberlain, (2010) provides conditions under which the logit case is the only one admitting point-identification with two periods (Davezies et al., (2020) provide extensions of this result to the case of ). In the dynamic case, where the covariate is a lagged outcome, Cox, (1958), Chamberlain, (1985) and Honoré and Kyriazidou, (2000) derive conditions for point-identification of the coefficient on the lagged outcome in the logit case, while Honoré and Tamer, (2006) show how to compute bounds on coefficients for probit and other models.

Results for binary choice panel models with predetermined covariates are limited. Chamberlain, (2022) studies identification and semiparametric efficiency bounds in a class of non-linear panel data models with feedback; he provides both positive and negative results. In an hitherto unpublished section of an early draft of that paper (Chamberlain, , 1993), he proves that the coefficient on a lagged outcome is not point-identified in a dynamic logit model when only three periods of outcome data are available. Arellano and Carrasco, (2003) and Honoré and Lewbel, (2002) study binary choice models with predetermined covariates. Arellano and Carrasco, (2003) assume that the dependence between the time-invariant heterogeneity and the covariates is fully characterized by its conditional mean given current and lagged covariates. Honoré and Lewbel, (2002) assume that one of the covariates is independent of the individual effects conditional on the other covariates. In a recent contribution, Pigini and Bartolucci, (2022) show that one can accommodate specific forms of feedback while maintaining point-identification in binary choice models with pretermined covariates.222In this paper we focus on panel data with a fixed number of time periods. The large-T literature has also considered models with dynamics and feedback, see for example Carro, (2007), Hahn and Kuersteiner, (2002), and Fernández-Val, (2009).

In what follows we pose two questions. First, under what conditions is the coefficient on a predetermined covariate in a binary choice panel data model point-identified? Second, when the coefficient is only set-identified, how extreme is the failure of point-identification; i.e., what is the width of the identified set?

Our analyses leave the dependence between the (time-invariant) unit-specific heterogeneity and the covariates unrestricted. We focus on the special case of a single binary predetermined covariate, leaving the feedback process from lagged outcomes, covariates and the unit-specific heterogeneity onto future covariate realizations fully unrestricted. This is a substantial relaxation of the strict exogeneity assumption.

Regarding point-identification, we provide a simple condition on the model which guarantees that point-identification fails when periods of data are available (and is fixed). The condition is satisfied in most familiar models of binary choice, including the logit one. This finding contrasts with the prior work on logit models cited above, where point-identification typically holds for a sufficiently long panel. As a notable exception, the exponential binary choice model introduced by Al-Sadoon et al., (2017) does not satisfy our condition. In fact, point-identification holds in that case.

Regarding identified sets, we first show that sharp bounds on the coefficient can be computed using linear programming techniques. Our method builds on Honoré and Tamer, (2006), however, in contrast to their work, we allow for heterogeneous feedback. While the regressor coefficient is our main target parameter, we also derive the identified set for an average partial effect. This set can be computed using linear programming techniques as well.

Second, we numerically compute examples of identified sets. We find that, relative to the strictly exogenous case, allowing for a predetermined covariate tends to increase the width of the identified set. However, our calculations also suggest that the identified set can remain informative under predeterminedness, even in panels with as few as two periods, for both the coefficient and the average partial effect. Finally, as is true under strict exogeneity, the widths of the identified sets decrease quickly as the number of periods increases. These observations are based upon sets computed under a particular data generating processe (DGP). It is possible that identified sets may be larger under certain types of feedback.

The outline of the paper is as follows. In Section 2 we present the model. In Section 3 we provide a condition that implies that the common parameter in this model is not point-identified when . In Section 4 we show that our condition implies failure of point-identification for all (finite) . In Section 5 we show how to compute identified sets on coefficients and average partial effects, and we report the results of a small set of numerical illustrations. In Section 6 we describe potential restrictions one could impose on the feedback process. These restrictions may restore point-identification or shrink the identified set. We conclude in Section 7. Proofs are contained in the appendix. Lastly, replication codes are available as supplementary material.

2 The model

Available to the econometrician is a random sample of units, each of which is followed for time periods. We focus on short panels, and keep fixed. The sampling process asymptotically reveals the joint distribution of .

For any sequence of random variables and any non-stochastic sequence , we use the shorthand notation and . In addition, we simply denote and when the subsequence starts in the first period.

Let and denote a binary outcome and a binary covariate, respectively. We assume that

where is a scalar individual effect, is a known differentiable cumulative distribution function, and is a scalar parameter.

Let denote the distribution of heterogeneity given the initial condition ; i.e., the distribution of . We leave this distribution unrestricted on . When is a discrete subset of the real line, belongs to the unit simplex on , however it is otherwise unrestricted. We denote as the collection of all , for all and .

For each , let

denote the feedback process through which lagged outcomes, past covariates and heterogeneity affect the current covariate. We leave this distribution unrestricted as well. We denote as the collection of all , for all , , , and .

The (integrated) likelihood function conditional on the first period’s covariate is

| (1) |

for some (discrete or continuous) measure on .

A key feature of a model with predetermined covariates is the dependence of the feedback process on lagged outcomes, as reflected in the dependence of on in (1). When this dependence is ruled out, the covariate is strictly exogenous, and the likelihood function simplifies.333Under strict exogeneity, the likelihood function factors as where denotes the distribution of heterogeneity given all periods’ covariates . Dynamic responses of covariates to lagged outcome realizations are central to many economic models, including those where is a choice variable, policy, or a dynamic state variable.

For any , and any , let denote the right-hand side of (1). Moreover, let denote the vector collecting all those elements, for all . Finally, let denote the vector stacking and . For a given (population) , we define the identified set of as

| (2) |

The set in (2) includes all where, for that , it is possible to find a heterogeneity distribution , and a feedback process , such that the resulting conditional likelihood assigns the same probability to each of the possible data outcomes as the true one (given both and ).

In the first part of the paper, we provide conditions on the model under which is not a singleton. This corresponds to cases where is not point-identified. In the second part of the paper, we report numerical calculations of under particular DGPs.

Our focus on is motivated by the extensive literature on the identification of coefficients in binary choice models. However, in applications, average effects may also be of interest. In the second part of the paper, we will also report numerical calculations of identified sets for an average partial effect associated with a change in the binary predetermined covariate.

3 Failure of point-identification in two-period panels

We first present an analysis of point-identification in the two-period case, since this leads to simple and transparent calculations. In the next section, we will then generalize this result to accommodate periods.

3.1 Assumptions and result

To keep the formal analysis simple, in this section and the next we assume that takes a finite number of values, with known support points.

Assumption 1.

, where are known, and , where denotes the Dirac measure at .

Assumption 1 makes the model fully parametric. However this is not a limitation as our aim in this section and the next is to derive conditions under which point-identification fails. The conditions we provide will require sufficiently many support points.444The analysis is essentially unchanged if one instead assumes that , for some .

We rely on the parameterization given by the vector , where, for all , and . The vector is unrestricted, except for the fact that , for , belongs to the unit simplex. This parameterization handles the fact that probability mass functions sum to one.

We next impose the following assumption on the population parameters.

Assumption 2.

, , and are all interior, and for all and .

Assumption 2 places restrictions on the underlying parametric binary choice model and heterogeneity distribution. It rules out heterogeneity distributions that induce a point mass of “stayers” (i.e., units with such extreme values of that they either always take the binary action or they never do).555In some microeconometric datasets a substantial fraction of units never alter their value of . For example, in Card, (1996) few workers join or leave a union during the sample period. Assumption 2 also rules out the “staggered adoption” design common in difference-in-differences analyses. Exploring the implications of non-interior feedback processes is left for future work.

Finally, we assume that the parameter point is regular in the sense of Rothenberg, (1971).

Assumption 3.

is a regular point of the Jacobian matrix , in the sense that the rank of is constant for all in an open neighborhood of .

The assumption of regularity is standard in the literature on the identification of parametric models (Rothenberg, , 1971). If is analytic, the irregular points of (i.e., the points such that Assumption 3 is not satisfied) form a set of measure zero (Bekker and Wansbeek, , 2001). Thus, Assumption 3 is satisfied almost everywhere in the parameter space in many binary choice models, including the probit and logit ones.

We aim to provide a simple condition under which point-identification of fails when . We start by observing that, when , the model outcome probabilities given are

which, given the structure of the model, coincide with

| (11) |

With this notation in hand we present the following lemma.

Lemma 1.

Let . Suppose that Assumptions 1, 2 and 3 hold, and that is point-identified. Then, there exists and a non-zero function such that:

(i) for all and ,

(ii) for all and ,

The proof of Lemma 1 exploits the fact that, if is point-identified, then it is also locally point-identified. Together with the assumption that the parameter is regular, this allows us to apply a result of Bekker and Wansbeek, (2001) regarding the identification of subvectors, which guarantees the existence of some such that does not belong to the range of the matrix . We then show, using (11), that this implies the existence of such that (LABEL:eq_1) and (LABEL:eq_2) hold.

When the population parameter is point-identified, Lemma 1 suggests a method-of-moments approach to estimation. In such settings, will generally be a non-trivial function of . Let be this function. Next, note that condition in Lemma 1 corresponds to the conditional moment restriction

| (14) |

while – continuing to maintain – equation implies the additional requirement that

| (15) |

Analog estimators in point-identified models with feedback, based on these observations, are explored in our companion paper (Bonhomme et al., , 2022).

This formulation clarifies that a necessary condition for point-identification of is the existence of a non-zero moment function, , with a mean that is invariant to given and the past (i.e., the first period’s covariate and outcome). Such a moment function is “feedback robust”, in the sense that it remains valid across all possible feedback processes. This is the content of condition in Lemma 1, while imposes a similar invariance to the distribution of unobserved heterogeneity.

To show that point-identification fails, our focus here, we need to show that no such non-zero moment function exists. It turns out that there is a very simple condition for this in our model. Specifically, from Lemma 1 we obtain the following corollary.

Corollary 1.

Corollary 1 shows that a necessary condition for identification of is that , , and , for , are linearly dependent. This condition arises directly from condition (LABEL:eq_1), which requires the existence of a moment function that is robust to unknown feedback. Indeed, one can show that , , and are linearly dependent if and only if there exists a non-constant function such that

| (16) |

However, the condition that , , and be linearly dependent is restrictive, as we show in the next subsection.666While here we focus on a discrete under Assumption 1, note that, when and is strictly increasing on , , , and , for , cannot be linearly dependent. If that were the case, then for some non-zero triplet we would have for all . This would imply, by taking that and , which would then imply and contradict the assumption that is non-zero.

3.2 The logit model

Consider the logit model with a binary predetermined covariate, which corresponds to . In this case, the linear dependence condition of Corollary 1 requires that, for some non-zero triplet ,

However, this implies

which is a quadratic polynomial equation in . Therefore, provided that there are values in , this implies

which, provided that , entails

contradicting the assumption that is non-zero.

We have thus proved the following corollary.

Corollary 2.

3.3 The exponential model

Suppose now that, for , . This corresponds to the exponential binary choice model of Al-Sadoon et al., (2017). Note that here the support of is a strict subset of the real line. In this case, letting

we have

Hence the non point-identification condition of Corollary 1 is not satisfied in the exponential binary choice model.

4 Failure of point-identification in -period panels for

In this section we generalize our analysis to an arbitrary number of periods and state our main result.

4.1 Main result

The arguments laid out in the previous section extend to an arbitrary number of time periods, . Indeed, using a similar strategy to the proof of Lemma 1 and proceeding by induction, we obtain the following lemma.

Lemma 2.

Let . Suppose that Assumptions 1, 2 and 3 hold, and that is point-identified. Then, there exists and a non-zero function such that:

(i) for all , , , ,

| (18) |

does not depend on ;

(ii) for all and ,

| (19) |

Similarly to Lemma 1, Lemma 2 implies the existence of a moment function, with (generally) non-trivial dependence on , which is “feedback robust”, in the sense that, for all ,

while also requiring that

From Lemma 2 we obtain the following corollary, which we also prove by induction. This is our main result.

4.2 Logit model

Using that, when , , , and , for , are linearly independent in the logit model, Corollary 3 implies that in the logit model with a binary predetermined covariate, is not point-identified irrespective of the number of time periods available.

Corollary 4.

This non point-identification result contrasts with prior work on logit panel data models. Under strict exogeneity, Rasch, (1960) and Andersen, (1970) have established that is point-identified under mild conditions on whenever . In the dynamic logit model when , Chamberlain, (1993) shows that is not point-identified when (a result also obtained as an implication of Corollary 1). However, Chamberlain, (1985), and Honoré and Kyriazidou, (2000) in a model with covariates, show that is point-identified under suitable conditions whenever .777Since in the dynamic logit model is a lagged outcome, (respectively, ) requires that individual outcomes be available for at least three (resp., four) periods. By contrast, Corollary 4 shows that, when the feedback process through which current covariates are influenced by lagged outcomes is unrestricted, the failure of point-identification is pervasive irrespective of , despite the logit structure.

5 Characterizing identified sets

The previous sections show that point-identification often fails in binary choice models with a predetermined covariate. In this section, we explore the degree of identification failure by presenting numerical calculations of the identified set for specific parameter values. In the last part of the section we present calculations of the identified set for an average partial effect.

5.1 Linear programming representation

We show that the identified set , defined by set (2) above, can be represented as a set of values for which a certain linear program has a solution. This characterization facilitates numerical computation of the identified set.

To present our construction, let us first focus on the case, and suppose that Assumption 1 holds, so has discrete support. For any hypothetical values , we define

| (20) |

The right-hand-side of (20) is determined by the unknown heterogeneity distribution, the parametric likelihood for (given and ), and the unknown feedback process for . Finding essentially involves repeatedly asking whether, for a given , there exists a valid feedback process and heterogeneity distributions consistent with the observed data distribution (and the parametric part of the model).

Specifically we first require that is a valid probability mass function:

| (21) |

Second, we check that it is consistent with the parametric likelihood model for given and :

| (22) |

Finally, we conclude that if and only if

| (23) |

for some vectors also satisfying (21) and (22) for . Condition (23) ensures compatibility with the likelihood contribution for the period outcome, .

Since all of the equalities and inequalities in (21), (22) and (23) are linear in , it follows that one can verify whether by checking the existence of a solution to a finite-dimensional linear program.888Note that, to compute the identified set under the assumption of strict exogeneity, one can simply modify this approach by adding to (21), (22) and (23) the additional restriction which is also linear in . The fact that, under strict exogeneity, can be computed using linear programming was first established by Honoré and Tamer, (2006). We provide details about computation in Appendix H.

The characterization of in (21), (22) and (23) remains valid when Assumption 1 does not hold, and has continuous support. In that case, one needs to interpret in (20) as the product between the density of conditional on and the probability of , both of them conditional on and for hypothetical parameter values. The resulting linear program is infinite-dimensional in that case.

The linear programming representation of extends to any number of periods. To see this, let, for some ,

with a similar definition when the support of is not discrete and Assumption 1 does not hold. In Appendix G we derive the following characterization of the (sharp) identified set .

Proposition 1.

(Identified Set) if, and only if,

| (24) |

for some integrable functions , , satisfying

| (25) |

and, for all ,999For , restriction (26) should be read as also satisfying

| (26) |

Proposition 1 shows that one can verify whether by checking the feasibility of a (finite- or infinite-dimensional) linear program. In a setting with lagged outcomes and strictly exogenous covariates, Honoré and Tamer, (2006) provided an analogous linear programming representation of the identified set. By contrast, in Proposition 1 we characterize the identified set of in the general predetermined case where the Granger condition fails; i.e., when may depend on , a situation that Honoré and Tamer, (2006) did not consider but anticipated in their conclusion.

5.2 Numerical illustration

In this section we compute identified sets in logit and probit models for a set of example data generating processes (DGPs). In the DGPs, follows a Bernoulli distribution on with probabilities , independent over time, and takes values with probabilities closely resembling those of a standard normal (a specification we borrow from Honoré and Tamer, , 2006), and is drawn independently of . In the logit case, , and in the probit case, for the standard normal cdf. Lastly, we vary between and . Note that is strictly exogenous in this data generating process. We characterize identified sets in two scenarios: assuming that are strictly exogenous, and only assuming that are predetermined.

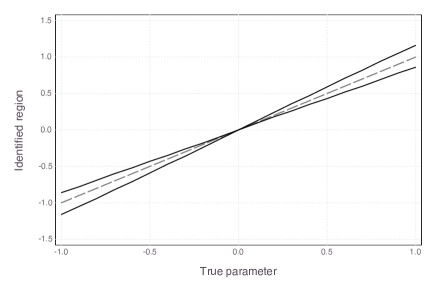

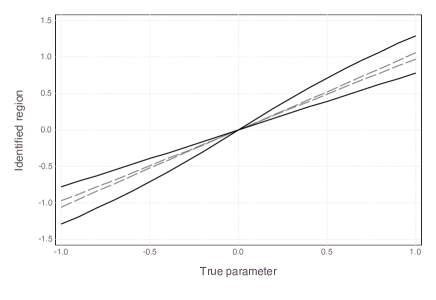

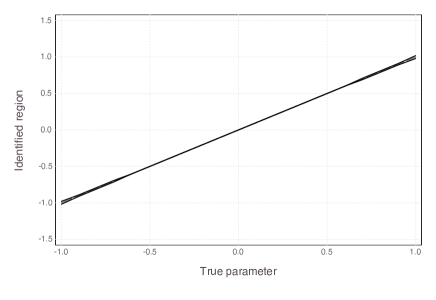

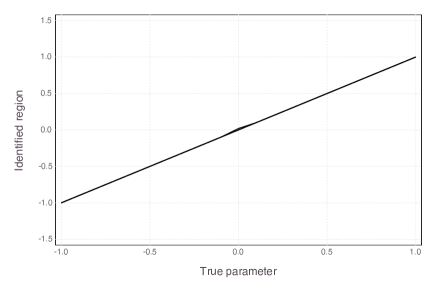

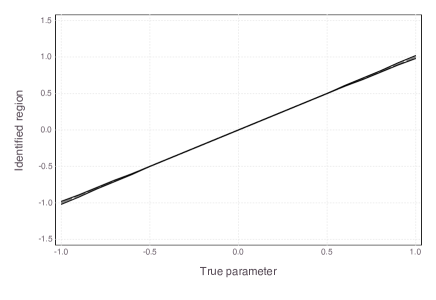

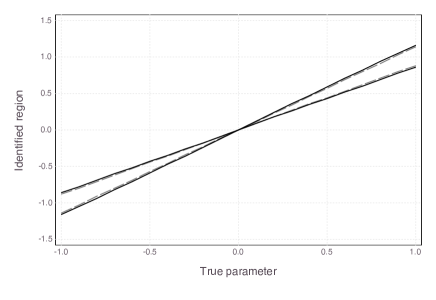

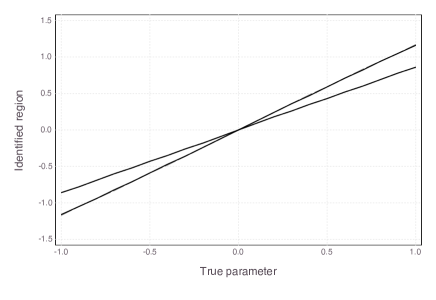

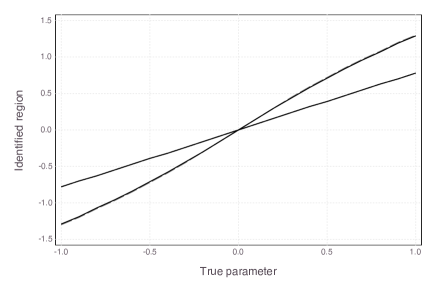

In Figure 1 we report our numerical calculations of the identified set for the logit model (in the left column panels) and for the probit model (in the right column panels). The three vertical panels correspond to the cases, respectively. In each graph, we report two sets of upper and lower bounds: those computed while maintaining the strict exogeneity assumption (in dashed lines) and those computed maintaining just predeterminedness (in solid lines). We report the true parameter on the x-axis. To compute the sets, we assume that has the same points of support as in the DGP. We also experimented with fewer and additional support points, as we report below.

| LOGIT MODEL | PROBIT MODEL |

|

|

|

|

|

|

Notes: Upper and lower bounds of the identified set in a logit model (left column) and a probit model (right column), for . The identified sets under strict exogeneity are indicated by the dashed lines, the sets under predeterminedness are indicated by the solid lines. The population value of is given on the x-axis.

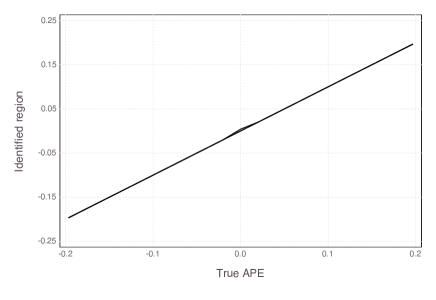

Focusing first on the logit case, shown in the left column of Figure 1, we see that the identified set under strict exogeneity is a singleton for any value of and irrespective of . This is not surprising since is point-identified in the static logit model. In contrast, the upper and lower bounds of the identified set do not coincide in the predetermined case, consistent with our non point-identification result. At the same time, the identified sets appear rather narrow, even when , and the width of the set tends to decrease rapidly when increases to three and four periods. This is qualitatively similar to the observation of Honoré and Tamer, (2006), who focused on dynamic probit models and found that the width of the identified set tends to decrease rapidly with .

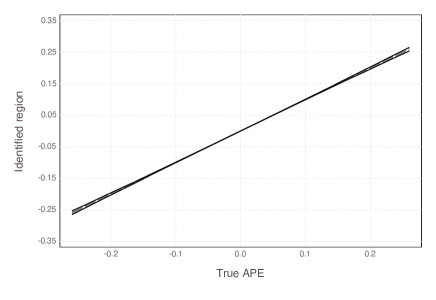

Focusing next on the probit case, shown in the right column of Figure 1, we see that the identified set under strict exogeneity is not a singleton. Moreover, allowing the covariate to be predetermined increases the width of the identified set. However, as in the logit case, the sets appear rather narrow, even when , and their widths decrease quickly as increases. Of course, these observations are specific to a particular data-generating process and the corresponding bounds may be wide for other DGPs.

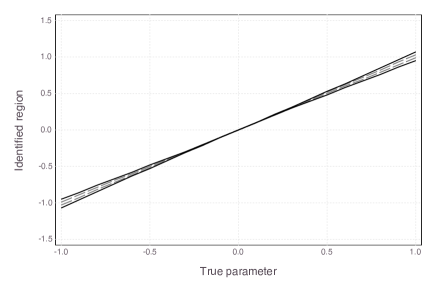

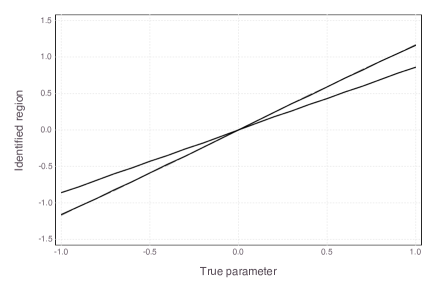

The results in Figure 1 are obtained by assuming that the researcher knows the (finite) support of . This approach is similar to the one in Honoré and Tamer, (2006). Alternatively, one may wish to characterize the identified set in a class of models where is continuous, e.g., when and is the Lebesgue measure. Doing so, as noted earlier, requires approximating an infinite-dimensional linear program. In Appendix Figure 1, we go take a heuristic step in this direction by reporting numerical approximations to the identified sets, for , obtained by taking , , and points of support for , respectively, where the points of support are equidistant percentiles of a standard normal distribution. We find very minor differences compared to the case that we report in Figure 1. While we do not provide a formal analysis of numerical approximation properties, this suggests that identified sets under continuous may not be markedly different from the ones in Figure 1.

Overall, these calculations suggest that, while relaxing strict exogeneity tends to increase the widths of the bounds, the identified sets under predeterminedness can be informative even when the number of periods is very small. To reiterate, these conclusions are based on a particular set of example DGPs.

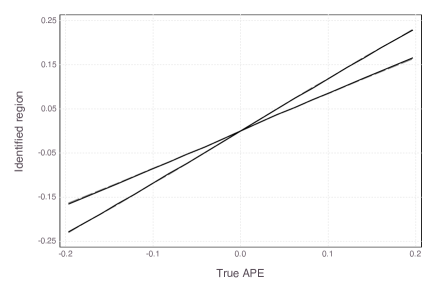

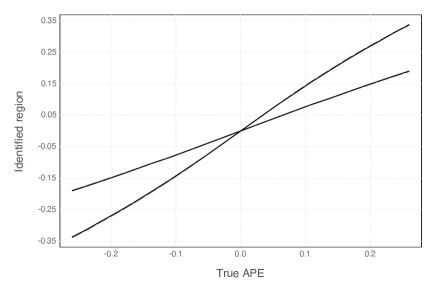

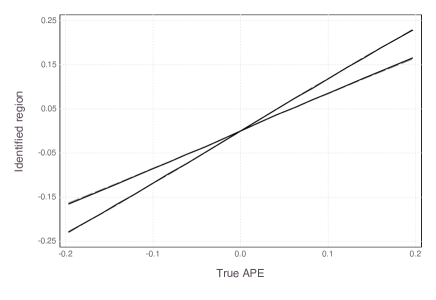

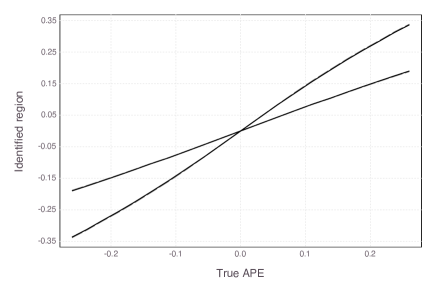

5.3 Average partial effect

Although our focus in this paper is on the parameter , in applications researchers are often interested in average partial effects such as

| (27) |

where the expectation is taken with respect to the distribution of .

The identified set for can also be characterized as the solution to a linear program. Indeed, it follows from Proposition 1 that is in the identified set of if and only if there exists , and such that (24), (25), and (26) hold, and

| (28) |

where . For any given , we can therefore compute the set of parameters in the identified set by solving a linear program. We provide details about computation in Appendix H.

| LOGIT MODEL | PROBIT MODEL |

|

|

|

|

|

|

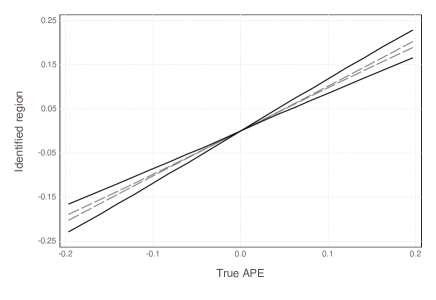

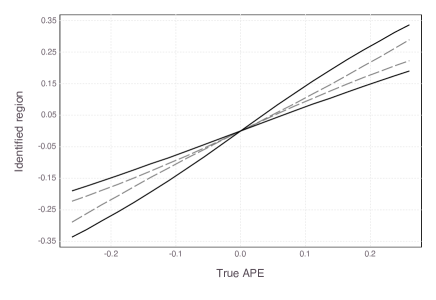

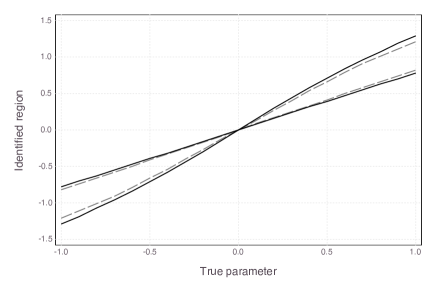

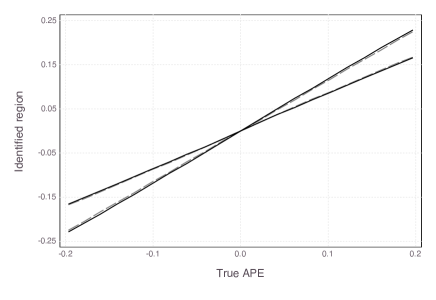

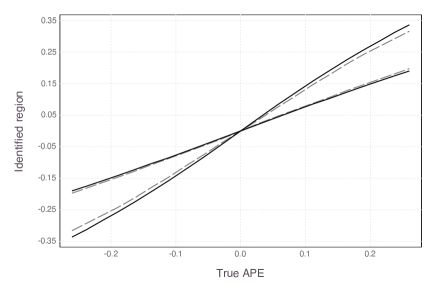

Notes: Upper and lower bounds of the identified set for the average partial effect in a logit model (left column) and a probit model (right column), for . The identified sets under strict exogeneity are indicated by the dashed lines, the sets under predeterminedness are indicated by the solid lines. The population value of the average partial effect is given on the x-axis.

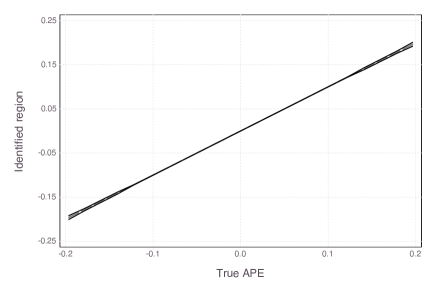

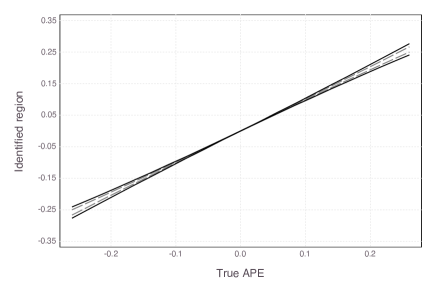

In Figure 2 we report our computations of the identified set for the average partial effect , relying on the same parameter values and DGP as before. Focusing first on the logit case, shown in the left column of the figure, we see that the identified set under strict exogeneity is not a singleton, except when the true and are equal to zero. This is not surprising, since average partial effects generally fail to be point-identified in binary choice models, even when covariates are strictly exogenous. Yet, the sets seem rather narrow, even when . Allowing the covariate to be predetermined increases the widths of the sets, however the increase is relatively moderate. Moreover, the sets under predeterminedness are very tight whenever .

Focusing next on the probit case, shown in the right column of Figure 2, we see that although the sets appear wider than in the logit case, relaxing strict exogeneity only moderately increases the widths of the sets, especially when .

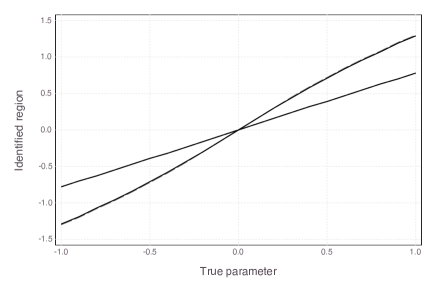

Lastly, while we compute the sets in Figure 2 under the assumption that has the same points of support as in the DGP, in Appendix Figure 2 we report approximations of the sets, for , obtained using , , and points of support for . The sets appear very similar to the ones based on points of support shown in Figure 2. However, in this case as well, we do not formally analyze the numerical approximation of the identified sets under continuous .

6 Restrictions on the feedback process

Our analysis suggests that failures of point-identification are commonplace in binary choice models with a predetermined covariate. In this section we describe possible restrictions on the model that can strengthen its identification content. We focus on restrictions on the feedback process, since restrictions on individual heterogeneity are rarely motivated by the economic context.

6.1 Homogeneous feedback

In some applications one may want to restrict the feedback process to not depend on time-invariant heterogeneity; that is, to impose that

| (29) |

is independent of . For example, in structural dynamic discrete choice models, researchers may be willing to model the law of motion of state variables such as dynamic production inputs as homogeneous across units. Kasahara and Shimotsu, (2009) show how this assumption can help identification in these models. Here we study how a homogeneity assumption can lead to tighter identified sets in our setting.

To proceed, we focus on the case where . Given (29), the likelihood function takes the form

where the likelihood factors due to the fact that the feedback process does not depend on . Hence, under Assumption 2 (which avoids division by zero) we have

| (30) |

A key observation to make about (30) is its right-hand-side coincides with the likelihood function of a binary choice model with a strictly exogenous covariate (where in addition is independent of given ). In turn, the left-hand side is weighted by the inverse of the feedback process. This is similar to the inverse-probability-of-treatment-weighting approach to dynamic treatment effect analysis in Jamie Robins’ work (e.g., Robins, , 2000), with the difference that here we focus on panel data models with fixed effects.

The similarity between (30) and the strictly exogenous case directly delivers point-identification results and consistent estimators. For example, suppose that is logistic. Given that the left-hand side of (30) is point-identified, it follows from standard arguments (Rasch, , 1960, Andersen, , 1970) that is point-identified. Moreover, a consistent estimator of is obtained by maximizing the weighted conditional logit log-likelihood

with weights

for a consistent estimate of the homogeneous feedback probabilities.101010The analysis in this subsection is not restricted to the binary covariate case. However, when are continuous, demonstrating consistency of would generally require imposing rate-of-convergence and other requirements on the first-step estimation of the weights.

6.2 Markovian feedback

Another possible restriction on the feedback process is a Markovian condition, such as

| (31) |

is independent of . Such a condition may be natural in models where is the state variable in the agent’s economic problem (as in Rust, , 1987 and Kasahara and Shimotsu, , 2009, for example).

In order to characterize the identified set with the Markovian condition (31) added, we augment the restrictions (24), (25) and (26) with the fact that, for all ,

does not depend on .111111When , this requires that does not depend on .

A difficulty arises in this case since this additional set of restrictions is not linear in . As a result, one would need to use different techniques to characterize the identified set in the spirit of Proposition 1, and to establish conditions for (the failure of) point-identification in the spirit of Corollary 3. Given this, we leave the analysis of identification in models with Markovian feedback processes to future work.

7 Conclusion

In this paper we study a binary choice model with a binary predetermined covariate. We find that failures of point-identification are widespread in this setting. Point-identification fails in many binary choice models, with apparently only a few exceptions (such as the exponential model). At the same time, our numerical calculations of identified sets suggest that the bounds on the parameter can be narrow, even in very short panels. This suggests that, while the strict exogeneity assumption has identifying content, models with predetermined covariates and feedback may still lead to informative empirical conclusions, both for the coefficients of the covariates and for average partial effects.

Our analysis of models with a binary covariates can easily be extended to handle general discrete covariates with finite support. In particular, for to be regularly point-identified there need to exist in the support of such that , , and , for , are linearly dependent. This condition fails in many popular specifications such as the logit. In turn, when has finite, non-binary support, the identified set can still be computed as a solution to a linear program, analogously to Proposition 1. However, the extension to continuous covariates is not straightforward in our setting, in particular since the notion of regularity maintained by Assumption 3 no longer applies.

Finally, although we have analyzed a binary choice model, our techniques can be used to study other models with stronger identification content, such as models for count data (e.g., Poisson regression, Wooldridge, , 1997, Blundell et al., , 2002) and models with continuous outcomes (e.g., censored regression, Honoré and Hu, , 2004, and duration models, Chamberlain, , 1985). Deriving sequential moment restrictions in such nonlinear models was considered by Chamberlain, (2022) and is further explored in our companion paper (Bonhomme et al., , 2022).

References

- Al-Sadoon et al., (2017) Al-Sadoon, M. M., Li, T., and Pesaran, H. (2017). Exponential class of dynamic binary choice panel data models with fixed effects. Econometric Reviews, 36(6-9).

- Andersen, (1970) Andersen, E. B. (1970). Asymptotic properties of conditional maximum-likelihood estimators. Journal of the Royal Statistical Society: Series B (Methodological), 32(2):283–301.

- Arellano, (2003) Arellano, M. (2003). Panel data econometrics. OUP Oxford.

- Arellano and Bond, (1991) Arellano, M. and Bond, S. (1991). Some tests of specification for panel data: Monte carlo evidence and an application to employment equations. The review of economic studies, 58(2):277–297.

- Arellano and Bover, (1995) Arellano, M. and Bover, O. (1995). Another look at the instrumental variables estimation of error-component models. Journal of Econometrics, 68(1):29 – 51.

- Arellano and Carrasco, (2003) Arellano, M. and Carrasco, R. (2003). Binary choice panel data models with predetermined variables. Journal of Econometrics, 115(1):125 – 157.

- Bekker and Wansbeek, (2001) Bekker, P. and Wansbeek, T. (2001). Identification in parametric models. A companion to theoretical econometrics, pages 144–161.

- Blundell and Bond, (2000) Blundell, R. and Bond, S. (2000). Gmm estimation with persistent panel data: an application to production functions. Econometric Reviews, 19(3):321 – 340.

- Blundell et al., (2002) Blundell, R., Griffith, R., and Windmeijer, F. (2002). Individual effects and dynamics in count data models. Journal of econometrics, 108(1):113–131.

- Bonhomme et al., (2022) Bonhomme, S., Dano, K., and Graham, B. (2022). Sequential moment restrictions in nonlinear panel data models. Working Paper.

- Card, (1996) Card, D. (1996). The effect of unions on the structure of wages: a longitudinal analysis. Econometrica, 64(4):957 – 979.

- Carro, (2007) Carro, J. M. (2007). Estimating dynamic panel data discrete choice models with fixed effects. Journal of Econometrics, 140(2):503–528.

- Chamberlain, (1985) Chamberlain, G. (1985). Heterogeneity, duration dependence and omitted variable bias. Longitudinal Analysis of Labor Market Data. Cambridge University Press New York.

- Chamberlain, (1993) Chamberlain, G. (1993). Feedback in panel data models. Working Paper.

- Chamberlain, (2010) Chamberlain, G. (2010). Binary response models for panel data: Identification and information. Econometrica, 78(1):159–168.

- Chamberlain, (2022) Chamberlain, G. (2022). Feedback in panel data models. Journal of Econometrics, 226(1):4 – 20.

- Cox, (1958) Cox, D. R. (1958). The regression analysis of binary sequences. Journal of the Royal Statistical Society B, 20(2):215 – 242.

- Davezies et al., (2020) Davezies, L., D’Haultfoeuille, X., and Mugnier, M. (2020). Fixed effects binary choice models with three or more periods. arXiv preprint arXiv:2009.08108.

- Fernández-Val, (2009) Fernández-Val, I. (2009). Fixed effects estimation of structural parameters and marginal effects in panel probit models. Journal of Econometrics, 150(1):71–85.

- Hahn and Kuersteiner, (2002) Hahn, J. and Kuersteiner, G. (2002). Asymptotically unbiased inference for a dynamic panel model with fixed effects when both n and t are large. Econometrica, 70(4):1639–1657.

- Honoré and Hu, (2004) Honoré, B. E. and Hu, L. (2004). Estimation of cross sectional and panel data censored regression models with endogeneity. Journal of Econometrics, 122(2):293–316.

- Honoré and Kyriazidou, (2000) Honoré, B. E. and Kyriazidou, E. (2000). Panel data discrete choice models with lagged dependent variables. Econometrica, 68(4):839–874.

- Honoré and Lewbel, (2002) Honoré, B. E. and Lewbel, A. (2002). Semiparametric binary choice panel data models without strictly exogeneous regressors. Econometrica, 70(5):2053–2063.

- Honoré and Tamer, (2006) Honoré, B. E. and Tamer, E. (2006). Bounds on parameters in panel dynamic discrete choice models. Econometrica, 74(3):611–629.

- Kasahara and Shimotsu, (2009) Kasahara, H. and Shimotsu, K. (2009). Nonparametric identification of finite mixture models of dynamic discrete choices. Econometrica, 77(1):135–175.

- Olley and Pakes, (1996) Olley, S. and Pakes, A. (1996). The dynamics of productivity in the telecommunications equipment industry. Econometrica, 64(6):1263–1297.

- Pigini and Bartolucci, (2022) Pigini, C. and Bartolucci, F. (2022). Conditional inference for binary panel data models with predetermined covariates. Econometrics and Statistics, 23:83–104.

- Rasch, (1960) Rasch, G. (1960). Studies in mathematical psychology: I. Probabilistic models for some intelligence and attainment tests. Nielsen & Lydiche, New York.

- Robins, (2000) Robins, J. M. (2000). Marginal structural models versus structural nested models as tools for causal inference. In Statistical models in epidemiology, the environment, and clinical trials, pages 95–133. Springer.

- Rothenberg, (1971) Rothenberg, T. J. (1971). Identification in parametric models. Econometrica: Journal of the Econometric Society, pages 577–591.

- Rust, (1987) Rust, J. (1987). Optimal replacement of gmc bus engines: An empirical model of harold zurcher. Econometrica: Journal of the Econometric Society, pages 999–1033.

- Wooldridge, (1997) Wooldridge, J. M. (1997). Multiplicative panel data models without the strict exogeneity assumption. Econometric Theory, 13(5):667–678.

APPENDIX

Appendix A Proof of Lemma 1

For any matrix , we will denote as

the range of ,

the null space of , and the Moore-Penrose generalized inverse of .

We now proceed to prove Lemma 1. Since is point-identified, it is locally point-identified. Since is a regular point of by Assumption 3, it follows from Theorem 8 in Bekker and Wansbeek, (2001) that

| (A1) |

Therefore, there must exist such that

| (A2) |

and in the rest of the proof we will fix this value.

Let denote the projection of onto the orthogonal complement of the vector space spanned by the columns of ; that is,

It follows from (A2) that . Moreover, since , where denotes a conformable vector of ones, we have

| (A3) |

It follows that , implying that cannot be constant.

Now, since for all , we have

Next, let be the vector with elements

for . Since , we have, for all ,

where we have used the fact that .

Let us define the following demeaned version of :111The vector represents a function . With some abuse of terminology we sometimes refer to as a vector and sometimes as a function.

Note that, since is not constant, it follows that . Moreover, using (A2) and (A3) we have

from which it follows that

We are now going to use (i) and (ii) to show (LABEL:eq_1)-(LABEL:eq_2). From (ii) we get, for all ,

Lastly, from (i) we get, for all ,

which can be equivalently written as

Now, using (LABEL:eq_1), this implies that, for all ,

which coincides with (LABEL:eq_2).

Appendix B Proof of Corollary 1

The proof is by contradiction. Suppose that is point-identified. Then by (LABEL:eq_1) we have, for some , and for all and ,

Since , , and , for , are linearly independent, we thus have, for all ,

| (A4) |

Next, using (LABEL:eq_2) at we have

Using (A4) then gives

Now, since and , for , are linearly independent, it follows that

Using (A4) then also gives

Lastly, repeating the same argument starting with (LABEL:eq_2) at gives

It follows that , which leads to a contradiction.

Appendix C Proof of remark 1 (sign identification of )

Note that

| (A5) | ||||

If , (A5) implies that . Moreover, since is strictly increasing, it follows that (respectively, ) and (resp., ) are equivalent. This implies that . A similar argument applied to implies that .

Appendix D Identification in the exponential model

Let

We show that is the unique solution to the equation

Since , the result will follow if one can show that, for any , is strictly monotonic.

Let with . For , we have

which shows that is strictly increasing. If , then

which shows that is strictly decreasing.

Appendix E Proof of Lemma 2

In what follows we assume , having already proved the validity of the claim for in Lemma 1.

Since is point-identified it is locally point-identified. Additionally, since is a regular point of by Assumption 3, we can appeal to Theorem 8 in Bekker and Wansbeek, (2001) and follow the same line of arguments as in the proof of Lemma 1 to conclude that there exists and a vector such that

Let us start with (18). Given , let denote the statement that, for all and ,

does not depend on .

Base case:

Condition (ii) implies that

or equivalently that

Using Assumption 2, this simplifies to

which implies that

does not depend on .

Thus, is true.

Induction step:

Suppose that are true for . We are going to show that is true.

Condition (ii) implies that

If , this corresponds to

While if , this corresponds to

Using Assumption 2 this gives, for all ,

| (A6) |

Let denote the left-hand side of (A6). Exploiting successively the fact that are true, alongside the property that, for all ,

| (A7) |

it is easy to see that

Recalling that is true, this implies that

does not depend on . Hence, is true. This concludes the proof of (18).

Appendix F Proof of Corollary 3

In what follows we assume , having already proved the validity of the claim for in Corollary 1.

The proof is by contradiction. Suppose that is point-identified. We will show that this necessarily leads to , which will contradict Lemma 2. To that end, we will first prove via finite induction that must be a constant function.

For , let denote the statement that there exists a function such that, for all and , we have

Base case:

By (18), the quantity

| (A8) |

does not depend on . Hence

By linear independence of , , and , this implies that

does not depend on . Hence is true.

Induction step

Suppose that is true for . Let us show that is true.

Since is true, we know that

there exists a function such that

Thus, by (18), the quantity:

does not depend on . Therefore,

Since , , and are linearly independent, this implies .

It follows from the previous induction argument that there exists a function such that, for all ,

Using (18), the quantity

does not depend on . Therefore,

Since , , and are linearly independent, this implies that there exists a function such that, for all ,

Lastly, (19) implies

Linear independence of , , and thus implies

Therefore, must be the null function, a contradiction.

Appendix G Proof of Proposition 1

Next, using (26) we have, for all ,

so, for all , the conditional distributions of given induced by coincide with the ones under the model; i.e., with .

Lastly, using (A9) we have

so the conditional distribution of given induced by also coincides with the one under the model.

This implies that .

Appendix H Computation of identified sets

In this section we describe the practical implementation of the linear programming approach for the computation of identified sets for two types of target parameters: , and average partial effects. For simplicity of exposition we discuss the case , but the construction is analogous for larger .

H.1 Parameter

In Proposition 1, we established that a candidate parameter lies in the identified set if and only if one can find functions verifying equations (21), (22) and (23). A useful observation is that these conditions can be viewed as the constraints of a linear program. Thus, determining whether is equivalent to determining the feasibility of a linear optimization problem. In the numerical illustration, we specifically consider:

where the constraints are that satisfy equations (21), (22) and (23). The additional constraints for the strictly exogenous case are that also verify the relationship presented in footnote 5.

H.2 Average partial effect

In addition to , a quantity of interest is the average partial effect

which is generally not point-identified. Yet, for a given , one can compute a lower bound and an upper bound on the range of possible average partial effects as solutions to the following linear optimization problem:

subject to satisfying equations (23), (21), and (22). Under the assumption of strict exogeneity, and have to satisfy the additional constraint discussed in footnote 5. The sharp bounds for are then obtained as

| LOGIT MODEL | PROBIT MODEL |

|

|

|

|

|

|

Notes: Approximate upper and lower bounds of the identified set in a logit model (left column) and a probit model (right column) with based on a discretization of unobserved heterogeneity with support points respectively. The true identified set is depicted by the solid lines while the approximations are indicated by the dashed lines. The population value of is given on the x-axis.

| LOGIT MODEL | PROBIT MODEL |

|

|

|

|

|

|

Notes: Approximate upper and lower bounds of the identified set for average partial effects in a logit model (left column) and a probit model (right column) with using a discretization of unobserved heterogeneity with support points respectively. The true identified set is depicted by the solid lines while the approximations are indicated by the dashed lines. The population value is given on the x-axis.