Price impact in equity auctions: zero, then linear

Abstract

Using high-quality data, we report several statistical regularities of equity auctions in the Paris stock exchange. First, the average order book density is linear around the auction price at the time of auction clearing and has a large peak at the auction price. While the peak is due to slow traders, the order density shape is the result of subtle dynamics. The impact of a new market order or cancellation at the auction time can be decomposed into three parts as a function of the size of the additional order: (1) zero impact, caused by the discrete nature of prices, sometimes up to a surprisingly large additional volume relative to the auction volume (2) linear impact for additional orders up to a large fraction of the auction volume (3) for even larger orders price impact is non-linear, frequently super-linear.

I Introduction

Most electronic markets rely on auctions to start and end trading days in an orderly way. Because the volume involved during auctions is larger than the liquidity available at a given time in a typical open-market limit order book, auctions reduce price impact and fluctuations. The share of the closing auction in the total exchanged volume has significantly increased over the years [8], especially in European markets [34]. This increase highlights the importance of the auction mechanism in the price formation process.

In contrast to the abundant literature about open-market dynamics, work on auctions is scarce. On the theoretical side, Muni Toke [31] derives the distribution of the exchanged volume and the auction price using a stochastic order flow model during a standard call auction. In the same vein, Derksen et al. [21] propose a stochastic model for call auctions which produces a concave price impact function of market orders; in addition, Derksen et al. [22] build on the previous model to demonstrate the heavy-tailed nature of price and volume in closing auctions. Besides, Donier and Bouchaud [23] show that under sufficient regularity conditions (continuous price and time) and using a first-order Taylor expansion of supply and demand curves, price impact in Walrasian auctions is linear in the vicinity of the auction price.

Empirically, Pagano and Schwartz [32] find that introducing opening and closing call auctions improves market quality and lowers execution costs in the Paris stock exchange. Boussetta et al. [14] add that although opening volumes are decreasing and the market is fragmenting, the opening auction still improves market quality on Euronext Paris. They also report that slow brokers submit orders early, whereas high-frequency traders tend to act moments before the clearing. Challet and Gourianov [18] analyze US equities data and compute the auction price response functions conditional on the addition, and cancellation of an order. In addition, Challet [17] demonstrates that a strategic behavior of agents is needed to explain the antagonistic effects of activity acceleration and indicative price volatility decrease as the auction end approaches.

More recently, Jegadeesh and Wu [26] assess the robustness of closing auctions by comparing the price impact between NASDAQ and NYSE exchanges and find that the cost of trading during closing auctions is generally smaller than during trading hours. They also find that closing auctions mainly attract uninformed and passive investors, while informed traders prefer to act during continuous market hours. In the same spirit, Besson and Fernandez [7] analyze the closing auction in European markets and use a linear function to fit the impact of market orders; they report a smaller instantaneous impact for later submissions, and an overall cost of trading on close two to three times smaller than during trading hours.

Here, we characterize in detail the empirical properties of liquidity and price impact in equity auctions. At auction time, price impact is fully determined by the state of the order book, and we focus on the instantaneous impact caused by an order if sent just before the clearing. We do not find a straightforward linear impact: while adding or canceling a market (or marketable) order at the auction time has a linear component, the discreteness of the limit order book mechanically leads to zero price impact for small enough orders. These free-of-cost volumes can represent a fairly large fraction of the total matched volume. Before auction time, the order book shape yields a virtual/instantaneous price impact that can differ from that of actual submissions/cancellations. However, we find that the average impact of actual orders is of the same nature, i.e., linear. We argue that the opacity of limit order books during auctions causes the absence of selective liquidity taking, which results in turn in a linear impact.

This paper is organized as follows: first, we introduce a discrete-price auction mathematical framework (Section II) suitable to derive the conditions under which price impact is zero or linear. Next, we present the high-quality data used in this work: a large dataset from the European high-frequency financial (BEDOFIH) database (Section III). The main part consists in a detailed study of several statistical regularities of auctions, focusing on limit order book shapes and price impact during the auctions (Sections IV and V). Our main results are as follows:

-

1.

the average limit order book of buy (sell) orders has a skewed bell shape whose maximum is below (above) the auction price. Both distributions roughly mirror each other and can be considered linear in the vicinity of the auction price;

-

2.

there is an often large peak of volume at the auction price that builds up towards the end of the auction;

-

3.

breaking down the average limit order book densities by the agent latency (HFT, MIXED, NON) and their account type (own account, client account, market maker, parent company, retail market organization …) makes it clear that each category has a different behavior; the peak is not due to HFTs but to slower traders, and some traders post buy and sell orders asymmetrically;

-

4.

at any time during the auction, instantaneous price impact is zero for small enough volumes for both buy and sell orders simultaneously because of the discreteness of prices. The presence of a peak for both buy and sell limit order densities increases the importance of zero impact in auctions;

-

5.

for large enough volumes, instantaneous price impact is linear for most of the days and not only on average. This holds when the sum of the buy and sell order densities is constant as a function of the price around the indicative/auction price, which happens on most days. Using a change point detection algorithm, we characterize the linear impact price region day by day and asset by asset at the auction time;

-

6.

the average price impact of actual submissions/cancellations during the accumulation period is linear as well. This contrasts with open markets where the dependence of the average impact on the order size is much weaker. Since limit order books are not disseminated during auctions, selective liquidity taking is not possible;

-

7.

price impact at auction time is smaller during option expiry dates.

II A mathematical framework for auctions

In Euronext markets, equity auctions start with an accumulation period and end with a clearing process. During the accumulation period, participants send their orders (quantity, price, side, order type, …) to the exchange. Types of orders include market orders, limit orders, activated stop orders, and valid for auction orders. Modifications and cancellations are allowed, but transactions cannot occur. At any time during the accumulation process and at the end of the auction, the price that maximizes the matched volume and minimizes the imbalance is computed. At the auction time, buy (resp. sell) orders whose prices are larger (resp. smaller) than the auction price are executed, while limit orders whose price equals the auction price may be matched or remain in the order book after the auction.

Definition 1 (Supply and demand).

For an auction , where is the auction type (open, close, ) at date , we define the available supply and demand at a price and time as, dropping the for the sake of clarity,

| (1) | |||

where (resp. ) is the available sell volume (resp. buy volume) at a price and time .

Limit orders can only be submitted on a discrete price grid. Therefore, at any time , is a non-decreasing right-continuous step function, and is a non-increasing left-continuous step function.

Definition 2 (Auction price and volume).

For an auction , the auction volume noted is the one maximizing the exchanged quantity between buyers and sellers at the time of the clearing noted . For a given price at time , buyers and sellers can exchange a volume equal to at most. Thus

The auction price noted is the price that maximizes the exchanged quantity. As it may not be unique, we have

In this work we will always assume that supply and demand intersect, so that always exists and is unique. Note however that is often not uniquely defined by the maximization of the exchanged volume alone; this is why exchanges implement a complementary set of rules such that is always well defined. In the case of the Euronext markets used in this work, when multiple prices maximize the exchanged volume, the chosen is the one with the smallest imbalance. Then, if multiple prices with the highest executable volume and the smallest imbalance coexist, the auction price is the one closest to the reference price (last traded price).

Definition 3 (Indicative price and volume).

For an auction , the indicative price and the indicative volume at time are the hypothetical auction price and the total matched volume if the clearing took place at time .

Obviously, we have and . From now on, the time notation will be omitted when we work at time (e.g., stands for ). Note however that subsequent definitions and results can be stated for any time using time-dependent notations and substituting with and with .

Definition 4 (Buy and sell densities).

For an auction , we define the buy (resp. sell) density (resp. ) at a price as

| (2) |

where is the difference between the price and the next non-empty tick price when , and is the difference between and the previous non-empty tick price when .

To define a meaningful average density over a large number of days, volumes can be scaled by the auction volume at day , and prices can be substituted with log-price differences from the auction price .

Definition 5 (Scaled buy and sell densities).

For an auction , we define the scaled buy and sell densities as

| (3) |

where . Furthermore, if we substitute by a constant , we can compute for a given stock the average scaled density as

| (4) |

where denotes the average across days of the computed quantity at time .

Observe that this quantity is a discrete version of the continuous marginal supply and demand curves defined in Donier and Bouchaud [23], where and .

Definition 6 (Matched and remaining volumes).

For an auction , we define as the matched (executed) volume at a price and side , and as the remaining (non-executed) volume at a price and side . Hence, any limit volume at price is the sum of the matched and remaining volumes

| (5) |

Obviously, for any price , all the buy volume is matched and all the sell volume remains. Thus , , , and . Symmetrically, for any, price , we have , , , and . Consequently, can be non-zero only if .

Proposition 1.

Let be an auction with an auction price and an auction volume . The following equalities stand:

-

(a)

;

-

(b)

.

Proof.

(a): as the auction volume is the sum of all matched volumes, we have

(b) is proved by contradiction: if , then . This implies that a residual volume can be matched between buyers and sellers at the auction price and thus contradicts the fact that is maximizing the exchanged volume during the auction. ∎

Let us now introduce volumes scaled by the auction volume: given an integer volume of shares , we define the scaled volume .

Definition 7 (Price impact).

For an auction , for any , we define the price impact before the auction clearing of a buy (resp. sell) market order (resp. ) as the absolute change in the auction log-price immediately after submitting a buy (resp. sell) market order of size

| (6) |

where is the new auction price after injecting the market order.

Note that refers to the instantaneous impact of an order submission at auction time , i.e., assuming a market order is sent just before the clearing. In this case, the market can not react to this submission as the clearing happens right away, and no relaxation can occur. However, if a submission/cancellation is sent to the exchange way before the clearing, the corresponding price impact at with and refers to a virtual/instantaneous price impact that may differ from the price impact of an actual submission/cancellation since the market can still react to it.

Proposition 2.

Let be an auction with an auction price and an auction volume . We inject a market order of size before the auction clearing. The new auction price is . We have:

-

(a)

The function , for and , is a non-decreasing and right-continuous step function.

-

(b)

Let be the ordered points of discontinuity of . Then

(7) where is the non-empty price tick strictly greater than the auction price.

-

(c)

Let be the ordered points of discontinuity of . Then

(8) where is the non-empty price tick strictly lower than the auction price.

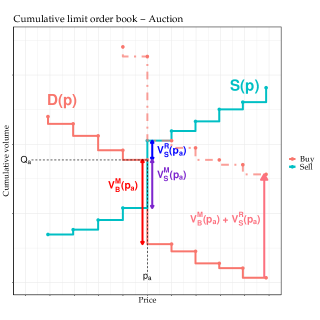

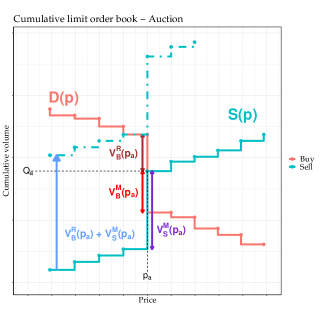

Obviously . Also, remark that if all price ticks contain non null volume (), then , where is the tick size. The proof of Proposition 2 is given in Appendix A. Proposition 2 allows us to compute the impact function at any time of a given auction, including during the accumulation period. In addition, the price impact of a new order is zero if its size is smaller than . Figure 1 provides a graphical explanation of formulas.

|

|

On the left panel for example, the buy volume at the auction price is totally matched ( and ). In this case, in order to shift the price, a buyer would need to execute a market buy order of minimal volume . Alternatively, a seller would need to execute a market sell order of minimal volume . The right panel of Figure 1 illustrates the symmetric case in which the sell volume at the auction price is totally matched ( and ). Moreover, observe that if a trader sends a market order of exact size , then both and maximize the auction volume. As explained above, the new auction price would be the one with the smallest imbalance, i.e. equal remaining volumes. If and have equal imbalances, then the new auction price is the closest to the reference price. Here, we assumed that whenever , the price automatically shifts to .

Also, by Proposition 2, for is the necessary volume to take the price from to . We therefore define for to denote this scaled incremental volume, with the convention that . Finally, notice that a cancellation of a buy market order of size affects the price in the same way as submitting a sell market order of the same size: in both cases the new price is a solution of . Similarly, cancelling a sell market order has the same effect as submitting a buy market order. Consequently, we only focus on the price impact of market order submissions in the following.

III Data

The dataset used in this work is part of the BEDOFIH database (Base Européenne de Données Financières à Haute-fréquence) built by the European Financial Data Institute (EUROFIDAI). The dataset provides detailed order data for all stocks traded on Euronext Paris between 2013 and 2017. For each stock and each trading day, information is provided in four files:

-

•

a history orders file that contains all the orders that remained in the central limit order book from the previous trading day ;

-

•

a current orders file that contains all submissions, modifications, and cancellations for the current trading day ;

-

•

a trades file that lists all the transactions that took place during the current trading day ;

-

•

an events file that lists special market events, if any, such as a delayed opening, a halt in trading, etc.

In addition to standard information such as time with microsecond precision, price, side (buy/sell), quantity, and price threshold for stop orders, we have access to additional order details in these files, some of which are computed ex-post. These include the order type and its temporal validity (market, limit, valid-for-auction, valid-for-closing, etc.), the high-frequency status of the market participant (HFT, NON-HFT, or MIXED), and the account type (own account, client account, market maker, parent company, retail liquidity provider, retail market organization).

In order to reconstruct the exact state of the limit order book (LOB) at any point during the auction, we combine the information from the four different files for each stock and each trading day to create a snapshot. We select the 34 most traded stocks on Euronext Paris between 2013 and 2017 and analyze 2 to 5 years worth of data for each stock, totaling stock-days. A small number of these stock-days result in errors or mismatches (e.g., dataset errors, non-crossing supply and demand for the opening auction, or half-day trading/halted trading before 17:30 for the closing auction). After removing these invalid snapshots, we are left with valid snapshots at the opening auction time and valid snapshots at the closing auction time.

Using these reconstructed snapshots just before the auction time, we compute reconstructed prices and volumes as per Euronext rules, i.e., by maximizing the exchanged volume and minimizing the imbalance. This boils down to finding the intersection of the reconstructed supply and demand curves. Table 1 reports the percentage of snapshots for which the reconstructed price (resp. volume) matches the actual auction price (resp. volume) among valid snapshots.

| Opening auction | Closing auction | |

|---|---|---|

| Number of valid snapshots | 34,971 | 34,820 |

| % snapshots matching the auction price | 99.6% | 99.9% |

| % snapshots matching the auction volume | 99.0% | 99.7% |

| % snapshots matching both | 98.9% | 99.6% |

The remaining discrepancies may be a result of using simplified rules to account for stop orders and occasional contradictions between recorded data in the orders file and the trades file. For these few unmatched snapshots, we note that the discrepancies between computed and actual quantities are small: less than 1 basis point on the absolute average difference from the auction price and 0.2% on the absolute average distance from the auction volume. These few unmatched auctions are discarded from the sample in the subsequent analysis, though they would not alter the outcome of our experiments.

IV Average shape of the auction limit order book

This section investigates the typical shape of the limit order book at auction time , what it implies for post-clearing price impact, and how the average LOB shape can be broken down by latency and account type of market participants.

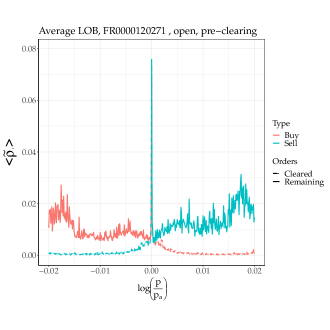

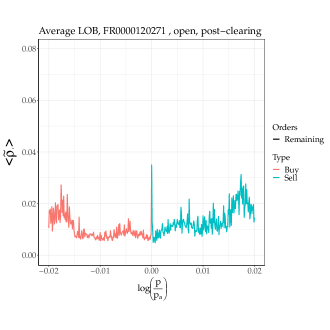

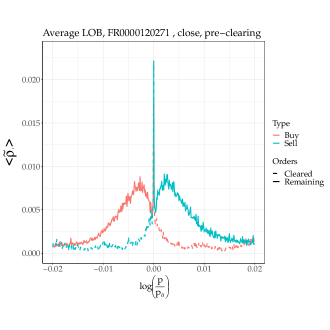

IV.1 Pre-clearing vs. post-clearing LOB shape

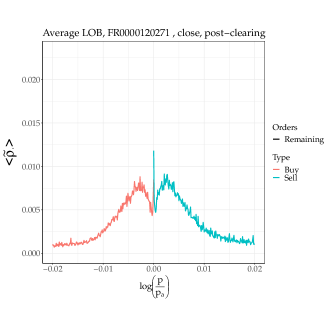

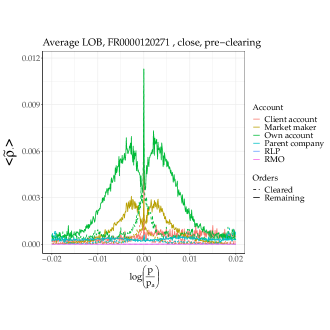

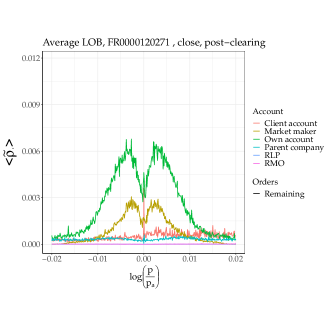

For each stock of the dataset, we compute the buy and sell average empirical densities (see Definition 5) as a function of the log-price difference . Figure 2 shows the average LOB density for the most traded stock in our dataset (ISIN FR0000120271, TTE.PA, TotalEnergies). We distinguish the orders that are cleared by the auction process (dotted lines) from the ones that remain in the LOB after the end of the auction (full lines). Average LOB densities are very similar across all the studied stocks.

Figure 2 shows the average LOB densities at the closing auction: the buy and sell densities have a skewed bell-shaped curve around the auction price. Opening and closing auctions have clearly different LOB densities. As expected, the average LOB density is noisier at the opening auction than at the closing auction which reflects the typical liquidity available at either auction [17]. However, the following remarks hold for both auctions:

-

•

there is a peak at the auction price, i.e. is larger than typical values taken near 0. This translates an accumulation of orders on on average at the time of the clearing ;

-

•

is linear around , i.e. .

As shown by Fig. 2, all buy orders with are cleared, and all buy orders with remain in the LOB after the auction as long as their temporal validity extends beyond the clearing; similarly, all sell orders with are cleared and all sell orders with remain in the LOB after the auction. For , some orders are matched, some are not. This explains why the peaks of buy and sell volumes at are reduced after the clearing. Finally, the auction-only orders are removed from the LOB after the clearing if they are not executed.

IV.2 Post-clearing instantaneous price impact

Let us briefly discuss the instantaneous post-clearing price impact during a continuous trading phase just after an auction. The following remarks are valid whenever there is a continuous trading phase right after the auction clearing (that is, after the open auction here). Consider the case of a trader sending a buy market order during the continuous trading phase just after auction clearing. This trader can expect to match up to all the remaining sell orders at without impacting the price. Once the liquidity at is consumed, sending an additional buy volume will result in a sub-linear price impact. Indeed, since has been observed to be linear around (peak excluded), we may write on this neighborhood so that we have on average

| (9) |

which implies

| (10) |

Hence, the post-clearing instantaneous price impact is sub-linear and ranges between a square root limit when and a linear impact limit . This reproduces in a stylized way the crossover between linear and square-root market impact observed in continuous double auctions [15]. The latter can be explained for example by assuming the existence of a hidden, latent LOB Tóth et al. [35], which is only partially revealed but whose shape largely determines that of market impact. At auction times instead, market participants are forced to reveal their intentions at least in the vicinity of , and one can relate the auction LOB with the latent LOB.

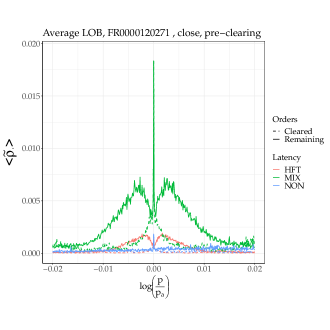

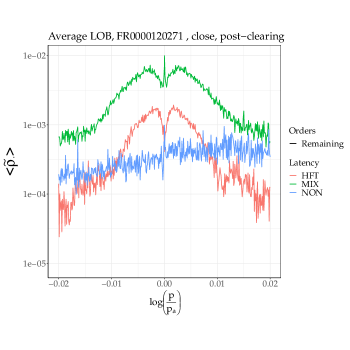

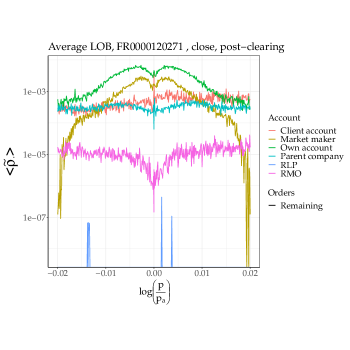

IV.3 Breakdown by market participant latency

Figure 3 displays a breakdown of the average empirical densities at the closing auctions by the speed of market participants. We used the latency flag in our data which specifies the HFT category of the order sender as per the AMF definition111A participant is considered a high-frequency trader (HFT) if he meets one of the two following conditions: • The average lifetime of its canceled orders is less than the average lifetime of all orders in the book, and it has canceled at least 100,000 orders during the year. • The participant must have canceled at least 500,000 orders with a lifetime of fewer than 0.1 seconds, and the top percentile of the lifetime of its canceled orders must be less than 500 microseconds. An investment bank meeting one of these conditions is described as mixed-HFT (MIX). If a participant does not meet any of the above conditions, it is a non-HFT (NON)..

Let us make three remarks regarding Figure 3. First, we notice that the MIX LOB has the same order of magnitude and shape as the total LOB (Fig. 2, bottom). This indicates that the contribution of traders flagged as fast (HFT) and slow (NON) to the liquidity provision of the closing auction (limit orders in the neighbourhood of the auction price) is smaller than the contribution of investment banks (flagged MIX). Second, the HFT LOB does not display an outstanding peak of volumes at the auction price. This suggests that this peak is actually caused by slow traders and may result in auction price pinning. Third, Figure 3 deals with the most liquid stock of the sample, but some stocks have a very small HFT-flagged LOB with the same order of magnitude as the low frequency LOB: HFT-flagged traders do not place sizeable limit orders in the closing auction of all stocks.

As stated in AMF [3], Benzaquen and Bouchaud [6], open markets are dominated by fast trading algorithms, which suggests considering the HFT LOB only (up to a multiplicative constant) when relating the auction LOB with the latent continuous-auction LOB. In this setting, the post-clearing price impact is much closer to a square root because of the sharp linear shape of the HFT LOB that vanishes around the current price.

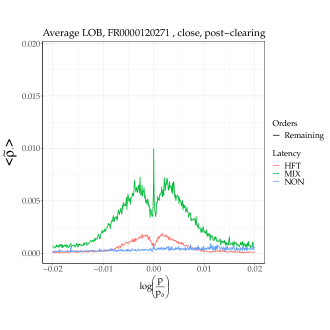

IV.4 Breakdown by account type

Figure 4 shows a breakdown of the average empirical densities at the closing auction by the account type. This particular flag tells on whose behalf an order was sent: client account, market marker, own account, parent company account, retail market organization (RMO), and retail liquidity provider (RLP).

We notice that traders operating on behalf of their own account, which includes a significant fraction of investment bank activities, and market markers provide most of the liquidity in the vicinity of the auction price. In addition, the density of orders sent on behalf of clients and slow traders have the same shape (see Fig. 3). This decomposition will be valuable in designing realistic agent-based models in addition to incorporating multi-time scale liquidity222There are only 126 authorized participants on the cash market (that includes equities) of Euronext Paris. See: https://live.euronext.com/en/resources/members-list..

V Price impact

This section investigates a set of statistical regularities of price impact in equity auctions focusing on closing auctions. In the first part, we study price impact at the auction time, which was fixed at 17:35:00 before the of September 2015, and then randomly between 17:35:00 and 17:35:30: we assume that a trader wishes to know by how much the auction price would have moved if she had sent a market order right before the clearing, supposing that she could know the clearing time in advance. In the second part, we study the behavior of price impact before the auction time. To this end, we examine the evolution of the virtual/instantaneous price impact throughout the accumulation period. Then, we relate the price impact at auction time with that at 17:35:00. Finally, we compute the average impact of actual submissions/cancellations during auctions and discuss why it is markedly different from that of open markets.

V.1 At the auction time

In this first part, we investigate the impact of a market order submitted (or canceled) to the exchange just before the clearing. We explicitly assume that the trader would have been able to insert or cancel her order just before the clearing process. In this setting, we highlight the existence of a significant zero impact volume below which the auction price would not have changed and explain why this zero impact is purely mechanical. We then show that any additional volume has a linear price impact over a volume range that we determine, not only on average but for most stocks and days. We also derive a simple formula for the impact slope that we validate empirically using a simplified optimization routine. Finally, we examine the influence of derivative expiry days on closing auctions.

V.1.1 Zero impact:

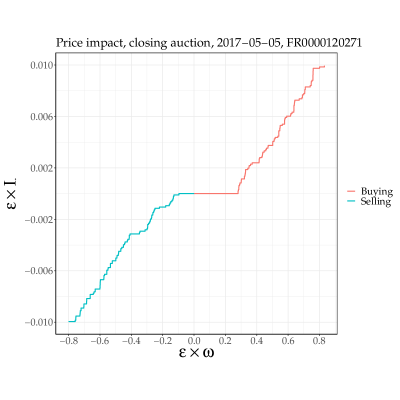

When inspecting the price impact function over several days and auctions, we observe that the minimal volume necessary to change the auction price ( using the notations of Proposition 2), can be much larger than the typical volumes needed to impact the price further ( , ). A compelling example is given by Figure 5, which shows the price impact function for TTE.PA at the closing auction of May 5, 2017, with the following quantities: €, , , and .

Hence, if sent just before , a buy order of a cash volume lower than million€ would not have resulted in an auction price change. Similarly a sell order of a cash volume lower than million€ would have had zero impact.

In our sample, zero price impact is present in more than 98% of the total processed days and sides. This means that in more than 98% of the time, sending one share, either on the buy or the sell side, will not change the auction price. In addition, and maybe more surprisingly, zero impact on both sides simultaneously is by far the most common situation. This comes from the fact that the prices are discrete and thus the cumulative buy and sell volumes and are step functions. At the auction price, these steps only overlap partially. To change the auction price, one needs to shift vertically either or in such a way that the overlap at the auction price disappears (see Figure 1 for an illustration). Thus, zero price impact only disappears when both and only have one share at most at .

Price impact can be zero for relatively large orders because of the peak of volume at : recall that the (scaled) zero-impact volume is the minimal volume needed to change the auction price; by the definition of in Proposition 2, having large matched buy and sell volumes at the auction price leads to large zero impact volumes on both sides (see Figure 1). This is confirmed empirically: we report in Table 2 the probability to send a market order of size just before the clearing without moving the closing price. For the stocks in our sample, this probability ranges from 46% to 74%. The randomization of the clearing time prevents fast agents from using their low latency to size their trades so as to have zero impact.

| ISIN | KS statistic | Observations | ||

|---|---|---|---|---|

| CH0012214059 | -0.559*** | 0.088* | 64% | 510 |

| FR0000031122 | -0.267*** | 0.056 | 67% | 1009 |

| FR0000045072 | -0.321*** | 0.035 | 65% | 1014 |

| FR0000073272 | -0.102** | 0.049 | 66% | 1015 |

| FR0000120073 | -0.210*** | 0.025 | 64% | 1014 |

| FR0000120172 | -0.156*** | 0.045 | 66% | 1268 |

| FR0000120271 | -0.048 | 0.022 | 46% | 1266 |

| FR0000120354 | -0.152*** | 0.088*** | 70% | 1014 |

| FR0000120404 | -0.089** | 0.052 | 69% | 1015 |

| FR0000120537 | -0.004 | 0.044 | 70% | 504 |

| FR0000120578 | -0.139*** | 0.054* | 48% | 1268 |

| FR0000120628 | -0.263*** | 0.043 | 64% | 1261 |

| FR0000120644 | -0.166*** | 0.027 | 60% | 1012 |

| FR0000120685 | -0.209*** | 0.044 | 68% | 1014 |

| FR0000121014 | -0.272*** | 0.021 | 68% | 1014 |

| FR0000121147 | -0.015 | 0.027 | 73% | 1013 |

| FR0000121261 | -0.225*** | 0.027 | 65% | 1013 |

| FR0000121501 | -0.311*** | 0.053 | 68% | 1014 |

| FR0000121667 | -0.338*** | 0.021 | 69% | 1012 |

| FR0000121972 | -0.095*** | 0.035 | 58% | 1264 |

| FR0000124141 | -0.288*** | 0.026 | 73% | 1012 |

| FR0000125007 | -0.14*** | 0.036 | 57% | 1265 |

| FR0000125338 | -0.172*** | 0.042 | 68% | 1012 |

| FR0000125486 | -0.132*** | 0.038 | 59% | 1013 |

| FR0000127771 | -0.248*** | 0.04 | 68% | 1015 |

| FR0000130338 | -0.098* | 0.033 | 74% | 613 |

| FR0000130809 | -0.061* | 0.032 | 56% | 1259 |

| FR0000131104 | -0.128*** | 0.049 | 53% | 1264 |

| FR0000131708 | -0.118** | 0.042 | 68% | 771 |

| FR0000131906 | -0.075** | 0.032 | 62% | 1269 |

| FR0000133308 | -0.242*** | 0.043 | 67% | 1012 |

| FR0010208488 | -0.271*** | 0.025 | 68% | 1010 |

| FR0013176526 | -0.349*** | 0.065 | 57% | 401 |

| NL0000235190 | -0.096*** | 0.035 | 61% | 1264 |

-

•

The symbols ***,**, and * indicate significance at the 0.1%, 1%, and 5% level, respectively.

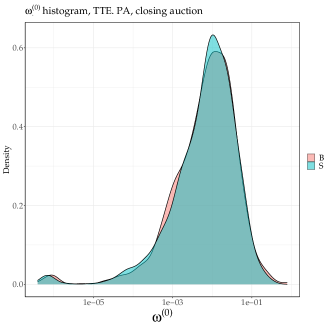

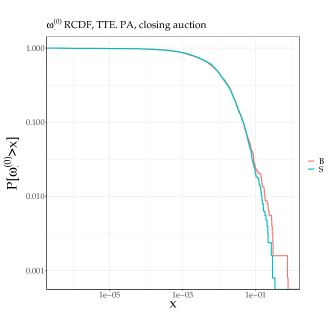

We also report several statistical observations on and . First, their statistical distribution can not be distinguished (as shown in Figure 6).

This is confirmed by a Kolmogorov-Smirnov test reported in Table 2, which also reports the empirical Spearman correlation between these two quantities: quite surprisingly, given the observation above, the correlation between and is rather weak, on average, and is non-significant for some very liquid stocks (e.g., TTE.PA the most traded stock in our dataset). This confirms that zero-impact is mostly a mechanical effect, not a strategic one.

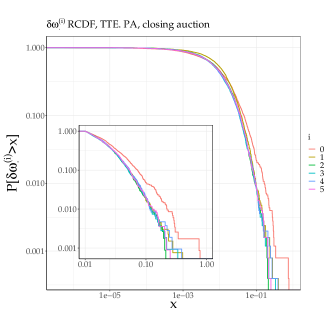

Let us finally compare , the minimal scaled volume needed to move the auction price, to , , the minimal scaled volumes needed to take the price from to (see Proposition 2). Table 3 presents results for the stock TTE.PA of pairwise Kolmogorov-Smirnov tests on the empirical distribution functions of and . For the sake of brevity, results are presented for , but the statistical testing has actually been conducted up to .

| 0.091*** | |||||||||||

| 0.047** | 0.08*** | ||||||||||

| 0.063*** | 0.103*** | 0.034 | |||||||||

| 0.057*** | 0.105*** | 0.033 | 0.023 | ||||||||

| 0.053** | 0.089*** | 0.02 | 0.026 | 0.028 | |||||||

| 0.055** | 0.112*** | 0.04* | 0.021 | 0.028 | 0.032 | ||||||

| 0.068*** | 0.117*** | 0.044* | 0.019 | 0.026 | 0.031 | 0.024 | |||||

| 0.043* | 0.086*** | 0.02 | 0.03 | 0.03 | 0.018 | 0.037. | 0.037 | ||||

| 0.047** | 0.091*** | 0.019 | 0.025 | 0.021 | 0.02 | 0.032 | 0.036 | 0.016 | |||

| 0.042* | 0.081*** | 0.022 | 0.04* | 0.037 | 0.022 | 0.043* | 0.041* | 0.016 | 0.023 |

-

•

The symbols ***, **, and * indicate significance at the 0.1%, 1%, and 5% level, respectively.

We clearly observe that and have specific statistical properties, while the distributions of the incremental volumes for could hardly be distinguished as the null hypothesis could not be rejected at the 1% significance level. Figure 7 shows smoothed histograms and empirical reverse cumulative distribution function for , .

This observation is not easily generalized to all stocks since additional factors come into play: small tick vs. large tick stocks and the randomization of the clearing time. These factors have a non-negligible influence on the distribution of s across different stocks and over the years.

V.1.2 Linear impact:

According to [23], in a Walrasian auction with continuous prices, average volumes around the auction price are non-null, which leads to a linear impact (in a first-order expansion), while in a continuous double auction, average volumes vanish around the current price and lead to a square root impact.

It is useful to first assume that price is continuous in order to derive a simple condition for the price impact to be strictly linear. If we send a buy market order of size before the auction clearing, and assuming we work in a log-price frame of reference in a continuous price setting, we have

| (11) |

hence,

| (12) |

Donier and Bouchaud [23] perform a first-order expansion to write

| (13) |

and approximate

| (14) |

However, instead, we use equation (12) to find exactly

| (15) |

thus

| (16) | ||||

Having a linear impact requires that and are linear functions, therefore that is constant.

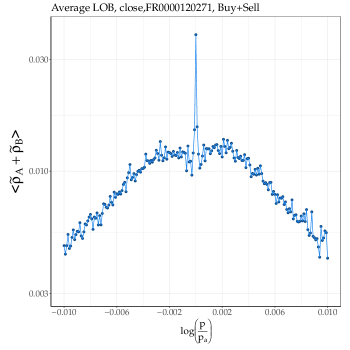

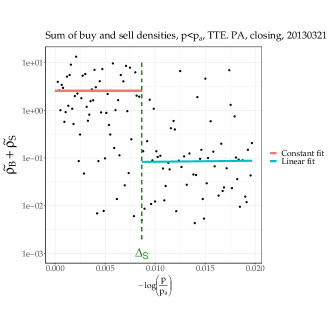

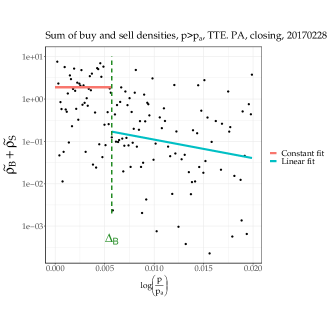

Figure 8 shows the average empirical density of the sum of buy and sell volumes for the most liquid stock in the sample. It strongly suggests the existence of a price interval, on each side of the auction price, in which the sum of buy and sell volumes can be well approximated by a constant.

We now include this observation in the discrete-price theoretical framework introduced Section II and we prove in Proposition 3 that if buy and sell densities sum up to a constant around the auction price (removing the zero-impact part), price impact is linear.

Proposition 3.

If is constant on some intervals and , then the price impact is linear. More precisely, if positive constant for all and positive constant for all , then for all such that , we have

| (17) |

where we omitted the notation from , , and . Recall that is the first non empty price tick after (resp. before) the auction price when (resp. when ), as in Proposition 2.

The proof of Proposition 3 is given in Appendix B. Notice that represents a constant scaled liquidity around . Also, since and are both scaled by , the price impact as written in the right-hand side of equation (17) does not depend on the auction volume . For large-tick stocks, if constant around , then the scaled liquidity is given by , where is the tick size. For small-tick stocks, one can obtain an approximation by substituting with a fraction of the average spread.

Following Proposition 3, we want to characterize the intervals in which can be considered constant. Therefore we need to find and for , such that

| (18) | ||||

For symmetry reasons, we focus on and : the problem is to find and for a given day by resorting to a simple change point detection algorithm. This method minimizes the residual sum of squared errors between and its mean for plus the residual sum of errors of a linear fit of for . We choose to work with logarithms, since errors are multiplicative. The resulting cost function is

| (19) | ||||

where is the linear regression estimate of over for , and is the number of non-null observations for . We then define

| (20) |

This definition means that for , the sum of the logarithm of the sum of scaled empirical buy and sell densities is better approximated by its mean than by a non-constant (linear) fit, whereas for , the opposite holds. Then, we calculate as the mean of for in order to avoid an underestimation due to the convexity of the exponential function. Finally, we define as the maximum scaled volume of a market order that would result in a null or linear impact, i.e.,

| (21) |

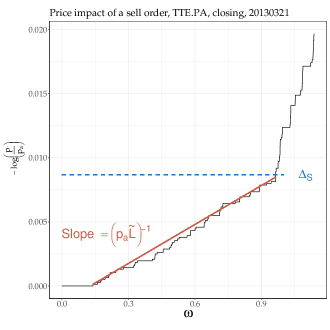

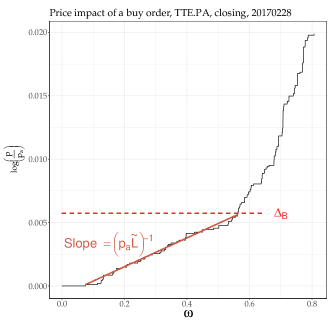

Figure 9 shows examples for detection using the previous optimisation for two different days at the closing auction, and plots in each case the theoretical impact given by Proposition 3 with respect to the actually observed impact function.

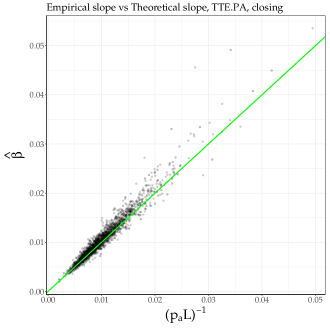

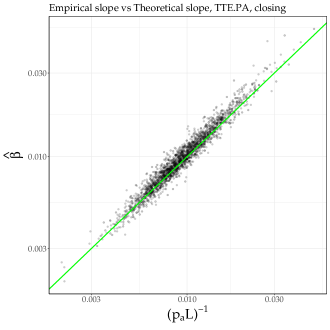

One sees that the estimated cut-off , as well as the slope estimate , fit very well the actual slope and domain of the linear price impact. This is actually the case of most days, as shown by Figure 10, where we plot the observed slope against the theoretical slope.

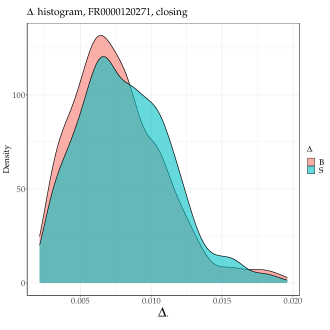

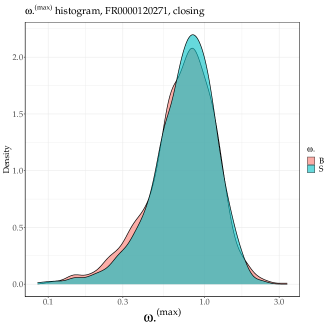

We also plot the smoothed histograms of and issued by our detection algorithm for the stock TTE.PA between 2013 and 2017 ( stock-days and two sides (buy and sell)) (see Fig. 11) .

Note that we truncated the closing auction snapshots at a maximum log-price distance , which is twice the average impact of a market order of a size equal to the auction volume . In addition, only fits with a number of points are kept, which happens in about of the days and sides: this shows that the price impact is linear for most of the days with an average value of above 50 basis points. Finally, : this means that a trader has 73% chance to execute 50% of the total auction volume just before the close clearing and still result in zero or linear impact.

Appendix C reports empirical properties of the impact slope at auction time computed for every asset, which may be of some use in transaction cost analysis.

V.1.3 Influence of derivatives expiry dates

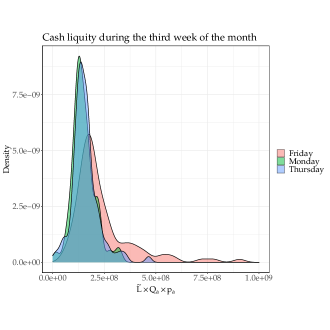

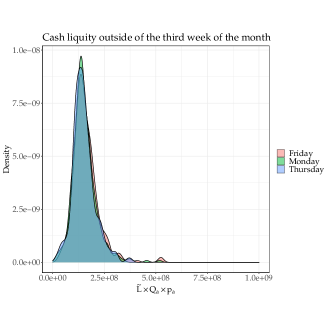

When there is no derivatives expiry, the liquidity in currency units defined by whether on Friday or other days of the week (Fig. 12, right panel) seem to be drawn from the same distribution, as we could not reject the null hypothesis associated with Kolmogorov-Smirnov tests for any pair of weekdays outside the third week of the month.

However, on expiry days (third Fridays of the month), liquidity in currency units is typically larger than for other weekdays during the same week and seems to be drawn from a different shifted distribution to the right (Fig. 12, left panel). This finding is confirmed by one tailed Kolmogorov-Smirnov tests for Friday and any other weekday during third weeks of a month. Therefore, the impact slope is typically smaller during expiry days and the final auction order book is more resistant to price changes.

V.2 Before the auction time

In this second part, we study price impact before the auction time. First, we examine the evolution of virtual price impact throughout the accumulation period by looking at the evolution of liquidity as well as the maximum volume resulting in a linear impact. Second, we assume that traders have means to infer the impact slope at 17:35:00, which is the latest time that ensures not missing the clearing with certainty. We then relate zero impacts and the impact slope at 17:35:00 with those at the auction time. Finally, we study the average impact on the indicative price of actual submissions/cancellations between 17:30:30 and the auction time by means of response functions.

V.2.1 Price impact evolution

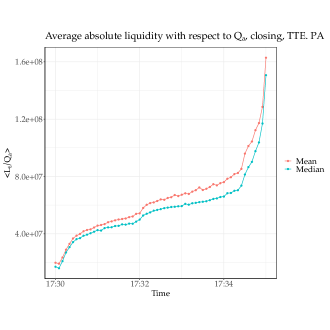

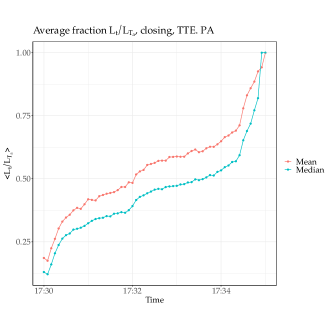

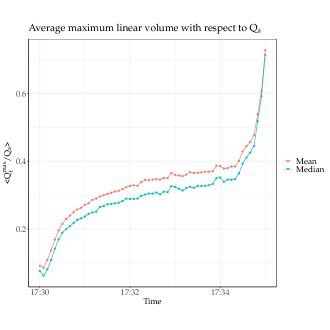

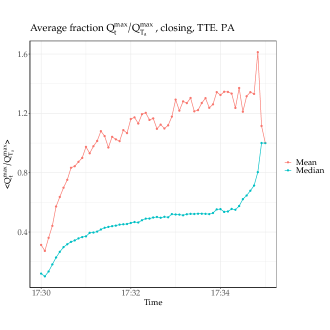

We investigate how the virtual price impact behaves throughout the accumulation period. We construct successive snapshots at 5-second intervals for TTE.PA at the closing auction. Then, we compute the (virtual/ instantaneous) price impact for with and . We define the absolute liquidity as the (constant) sum of buy and sell empirical densities at time : (Recall that the buy and sell densities sum up to a constant around the current indicative price). Similarly, we define as the maximum (absolute) volume that results in a null or linear impact time .

Figure 13 shows that averages of both the absolute liquidity (w.r.t. to ) and the fraction of the final liquidity follow the same pattern, i.e., a strong concave monotonicity at the start of the accumulation period followed by strong convex evolution as the clearing nears. Likewise, the average of the maximum linear volume with respect to the final volume has the same shape. Nonetheless, the average mean of has a more complex pattern and suggests a strong effect of cancellations.

V.2.2 Impact at auction time vs. 17:35:00

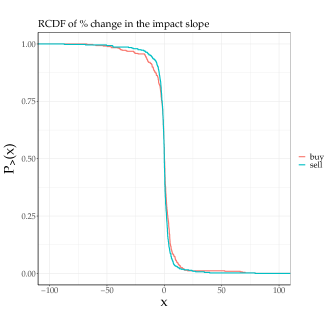

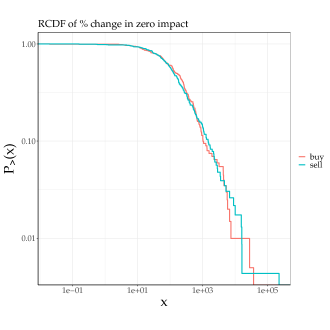

Let us now relate the virtual market impact at 17:35:00 and at auction time after the introduction of the randomized clearing time. Because the limit order book is not disseminated, traders have no direct way to estimate its shape, hence their virtual impact, at either time. However, sending a large market order and gradually cancelling it is a way around, and is observed at times.

The relationship between the two parts of price impact (zero, then linear) at both times is markedly different. The relative change of zero impact volumes is distributed over several orders of magnitude (see Fig. 14); agents do have an incentive to send zero-impact orders between 17:35:00 and the auction time. On the contrary, the slopes of the linear impact part are closely related: in 90% of the days, the relative change in the impact slope is smaller than 12% in absolute value (see Fig. 14). This means that the auction book stabilizes after 17:35:00 as one can expect since the clearing can occur at any time after 17:35:00. For TotalEnergies stock, the average absolute price change between 17:34:55 and 17:35:00 is 7 basis points. It is only 1.6 basis points between 17:35:00 and the auction time.

V.2.3 The linear impact of market order submission/cancellation before the auction

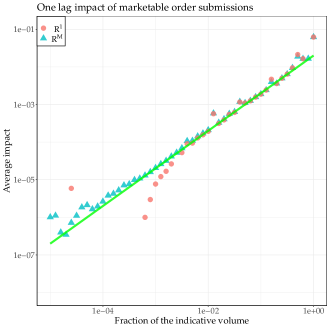

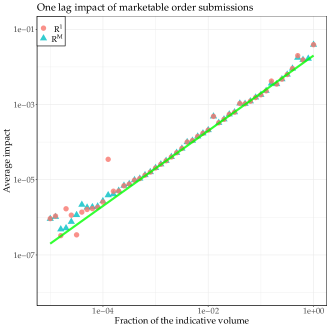

Finally, we evaluate the average impact of actual submissions/cancellations during the accumulation period. To this end, we compute the one lag response function for marketable orders (market orders and limit orders with an aggressive limit price) conditional on the order (scaled) size

| (22) |

where, is the indicative price just before the arrival of marketable order submission, for a buy, for a sell, and the time is incremented at each marketable order submission. Additionally, we compute the one lag mechanical response function conditional on the order (scaled) size

| (23) |

where is the indicative price just after the marketable order arrival.

In contrast to open markets where is sub-linearly dependent on the volume [29, 33, 13], we observe in Fig. 15 that scales linearly with for marketable orders larger than a certain threshold . For , values of can be negative indicating a strong mean reversion of the price, with values smaller than a tenth of a basis point in absolute value. For , we have essentially indicating that the price impact of individual orders is mostly mechanical and linear in . As agents can not access the full order book during auctions, there is no selective liquidity taking: this is confirmed as and scale linearly with . Incorporating marketable order cancellations with for sell cancellations and for buy cancellations yields , as we account for almost all price-changing events (right panel of Fig. 15).

These results imply that the nature of price impact is the same during the accumulation time and at the auction time, and contrasts with results for open markets, where selective liquidity taking causes very different shapes between the average virtual impact (using the instantaneous shape of the book) and market impact of actual trades [36, 12].

VI Conclusion

The discrete nature of prices in limit order books mechanically causes the price impact at auction time to be zero at first, sometimes for quite a substantial fraction of the total exchanged volume. Surprisingly, zero price impact happens most of the time simultaneously on both sides of the auction book, for additional sell and buy market orders or equivalently for cancellations of buy or sell market orders. For volumes larger than zero-impact ones, price impact at auction time is linear in a limited price range around the auction price not only on average but for more than 90% of days. The theoretical work of Donier and Bouchaud [23] shows the linearity of the auction impact locally around the auction price using a first-order expansion and under strong regularity assumptions of supply and demand in a continuous price setting. Here, we showed that the linearity of auction impact is due instead to the fact that the sum of buy and sell volumes around the auction price is constant.

While this work mainly describes the final result of the order accumulation process and characterizes the limit order book at the auction time, a more microscopic description of the dynamics of order submission, cancellation, and perhaps diffusion (price update) is needed. Even though market orders submitted during the accumulation period do not play a significant role in shaping the price response of the final limit order book, the action-reaction game between market orders and limit orders throughout the auction [34, 7] is probably a major driver of its dynamics. Similarly, the interplay between the various categories of agents (HFTs, market markers, agents trading on their behalf, or agents trading on behalf of their clients, …) is clearly of great interest. For example, Boussetta et al. [14] show that HFTs submit their orders in a markedly different way than slow traders. A good starting point would be a substantial modification of the model of Donier and Bouchaud [23] in the spirit of the work done by Lemhadri [28].

Acknowledgements

This publication stems from a partnership between CentraleSupélec and BNP Paribas.

The authors would like to acknowledge the support of the“Equipex PLADIFES ANR-21-ESRE-0036 (France 2030)” responsible for the EUROFIDAI BEDOFIH’s database.

References

- Alfi et al. [2007] Valentina Alfi, Giorgio Parisi, and Luciano Pietronero. Conference registration: how people react to a deadline. Nature Physics, 3(11):746–746, 2007.

- Alfi et al. [2009] Valentina Alfi, Andrea Gabrielli, and Luciano Pietronero. How people react to a deadline: time distribution of conference registrations and fee payments. Open Physics, 7(3):483–489, 2009.

- AMF [2017] AMF. Study of the behaviour of high-frequency traders on Euronext Paris. 2017. Available at https://www.amf-france.org/en/news-publications/publications/reports-research-and-analysis/study-behaviour-high-frequency-traders-euronext-paris.

- Avellaneda and Lipkin [2003] Marco Avellaneda and Michael D. Lipkin. A market-induced mechanism for stock pinning. Quantitative Finance, 3(6):417, 2003.

- Avellaneda et al. [2012] Marco Avellaneda, Gennady Kasyan, and Michael D. Lipkin. Mathematical models for stock pinning near option expiration dates. Communications on Pure and Applied Mathematics, 65(7):949–974, 2012.

- Benzaquen and Bouchaud [2018] Michael Benzaquen and Jean-Philippe Bouchaud. Market impact with multi-timescale liquidity. Quantitative Finance, 18(11):1781–1790, 2018.

- Besson and Fernandez [2021] Paul Besson and Raphaël Fernandez. Better trading at the close thanks to market impact models. 2021. Euronext quantitative research report.

- Blackrock [2020] Blackrock. A global perspective on market-on-close activity. 2020. Available at https://www.blackrock.com/corporate/literature/whitepaper/viewpoint-aglobal-perspective-on-market-on-close-activity-july-2020.pdf.

- Bouchaud et al. [2002] Jean-Philippe Bouchaud, Marc Mézard, and Marc Potters. Statistical properties of stock order books: empirical results and models. Quantitative finance, 2(4):251, 2002.

- Bouchaud et al. [2003] Jean-Philippe Bouchaud, Yuval Gefen, Marc Potters, and Matthieu Wyart. Fluctuations and response in financial markets: the subtle nature of random price changes. Quantitative finance, 4(2):176, 2003.

- Bouchaud et al. [2006] Jean-Philippe Bouchaud, Julien Kockelkoren, and Marc Potters. Random walks, liquidity molasses and critical response in financial markets. Quantitative finance, 6(02):115–123, 2006.

- Bouchaud et al. [2009] Jean-Philippe Bouchaud, J Doyne Farmer, and Fabrizio Lillo. How markets slowly digest changes in supply and demand. In Handbook of financial markets: dynamics and evolution, pages 57–160. Elsevier, 2009.

- Bouchaud et al. [2018] Jean-Philippe Bouchaud, Julius Bonart, Jonathan Donier, and Martin Gould. Trades, quotes and prices: financial markets under the microscope. Cambridge University Press, 2018.

- Boussetta et al. [2017] Selma Boussetta, Laurence Daures-Lescourret, and Sophie Moinas. The role of pre-opening mechanisms in fragmented markets. In Paris December 2017 Finance Meeting EUROFIDAI-AFFI, 2017.

- Bucci et al. [2019] Frédéric Bucci, Michael Benzaquen, Fabrizio Lillo, and Jean-Philippe Bouchaud. Crossover from linear to square-root market impact. Physical review letters, 122(10):108302, 2019.

- Budish et al. [2015] Eric Budish, Peter Cramton, and John Shim. The high-frequency trading arms race: Frequent batch auctions as a market design response. The Quarterly Journal of Economics, 130(4):1547–1621, 2015.

- Challet [2019] Damien Challet. Strategic behaviour and indicative price diffusion in Paris Stock exchange auctions. In New Perspectives and Challenges in Econophysics and Sociophysics, pages 3–12. Springer, 2019.

- Challet and Gourianov [2018] Damien Challet and Nikita Gourianov. Dynamical regularities of US equities opening and closing auctions. Market microstructure and liquidity, 4(01n02):1950001, 2018.

- Challet and Stinchcombe [2001] Damien Challet and Robin Stinchcombe. Analyzing and modeling 1+ 1d markets. Physica A: Statistical Mechanics and its Applications, 300(1-2):285–299, 2001.

- Dall’Amico et al. [2019] Lorenzo Dall’Amico, Antoine Fosset, Jean-Philippe Bouchaud, and Michael Benzaquen. How does latent liquidity get revealed in the limit order book? Journal of Statistical Mechanics: Theory and Experiment, 2019(1):013404, 2019.

- Derksen et al. [2020] Mike Derksen, Bas Kleijn, and Robin De Vilder. Clearing price distributions in call auctions. Quantitative Finance, 20(9):1475–1493, 2020.

- Derksen et al. [2022] Mike Derksen, Bas Kleijn, and Robin De Vilder. Heavy tailed distributions in closing auctions. Physica A: Statistical Mechanics and its Applications, 593:126959, 2022.

- Donier and Bouchaud [2016] Jonathan Donier and Jean-Philippe Bouchaud. From Walras’ auctioneer to continuous time double auctions: A general dynamic theory of supply and demand. Journal of Statistical Mechanics: Theory and Experiment, 2016(12):123406, 2016.

- Donier et al. [2015] Jonathan Donier, Julius Bonart, Iacopo Mastromatteo, and Jean-Philippe Bouchaud. A fully consistent, minimal model for non-linear market impact. Quantitative finance, 15(7):1109–1121, 2015.

- Euronext [2020] Euronext. Euronext rule book, Book 1: Harmonised Rules. 2020. Available for download at https://www.euronext.com/en/regulation/euronext-regulated-markets.

- Jegadeesh and Wu [2022] Narasimhan Jegadeesh and Yanbin Wu. Closing auctions: Nasdaq versus NYSE. Journal of Financial Economics, 143(3):1120–1139, 2022.

- Kyle [1985] Albert S. Kyle. Continuous auctions and insider trading. Econometrica: Journal of the Econometric Society, pages 1315–1335, 1985.

- Lemhadri [2019] Ismael Lemhadri. Price impact in a latent order book. Market Microstructure and Liquidity, 5(01n04):2050004, 2019.

- Lillo et al. [2003] Fabrizio Lillo, J. Doyne Farmer, and Rosario N. Mantegna. Master curve for price-impact function. Nature, 421(6919):129–130, 2003.

- Mastromatteo et al. [2014] Iacopo Mastromatteo, Bence Toth, and Jean-Philippe Bouchaud. Agent-based models for latent liquidity and concave price impact. Physical Review E, 89(4):042805, 2014.

- Muni Toke [2015] Ioane Muni Toke. Exact and asymptotic solutions of the call auction problem. Market microstructure and liquidity, 1(01):1550001, 2015.

- Pagano and Schwartz [2003] Michael S. Pagano and Robert A. Schwartz. A closing call’s impact on market quality at Euronext Paris. Journal of Financial Economics, 68(3):439–484, 2003.

- Potters and Bouchaud [2003] Marc Potters and Jean-Philippe Bouchaud. More statistical properties of order books and price impact. Physica A: Statistical Mechanics and its Applications, 324(1-2):133–140, 2003.

- Raillon [2020] Franck Raillon. The growing importance of the closing auction in share trading volumes. Journal of Securities Operations & Custody, 12(2):135–152, 2020.

- Tóth et al. [2011] Bence Tóth, Yves Lemperiere, Cyril Deremble, Joachim De Lataillade, Julien Kockelkoren, and Jean-Philippe Bouchaud. Anomalous price impact and the critical nature of liquidity in financial markets. Physical Review X, 1(2):021006, 2011.

- Weber and Rosenow [2005] Philipp Weber and Bernd Rosenow. Order book approach to price impact. Quantitative Finance, 5(4):357–364, 2005.

Appendix A Proof of Proposition 2

Proof.

We only prove the proposition for an additional buy market order resulting in a price impact denoted by . The case of a sell market order resulting in an impact is symmetric. By definition, is a non-decreasing right-continuous step function; the same holds for . Obviously and if and only if . Since denotes the first point of discontinuity of , by monotonicity, the condition is equivalent to . In the original auction with auction price and auction volume , we have

| (24) |

All these quantities are fixed by the original auction setting. If we add a buy market order of size in this setting, the new auction price satisfies

| (25) |

where and are the original supply and demand functions, and (resp. ) is the remaining sell quantity (resp. buy quantity) at price in the new setting. These volumes depend clearly on .

Let us now determine the first point of discontinuity . It is clear that the first price change due to the addition of a market order of size occurs when , , and the new auction price is the first non empty price tick after in the sense of , i.e., the first tick price strictly greater than the auction price which contains buy or sell shares. (see Figure 1 to build an intuition). Equation (25) yields

| (26) |

Using the fact that and we obtain

| (27) |

hence, using equation (24), one finds

| (28) |

Using , we obtain

| (29) |

which yields

| (30) |

Let us now determine , : which is the point of discontinuity of . We proceed similarly: the price change due to the injection of a market order occurs when , , and is the non empty price tick greater than (in the sense of ). Equation (25) yields

| (31) |

| (32) |

| (33) |

Using equation (24), we obtain

| (34) |

Finally,

| (35) |

Thus,

| (36) |

which leads to

| (37) |

∎

Appendix B Proof of Proposition 3

Appendix C Empirical properties of impact slopes at auction time

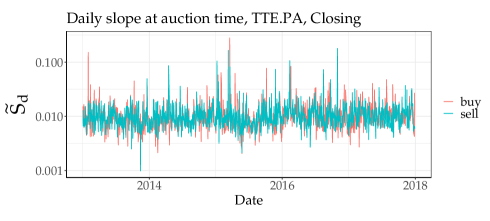

In this appendix, we report empirical observations on the impact slope at auction time on day defined as

| (39) |

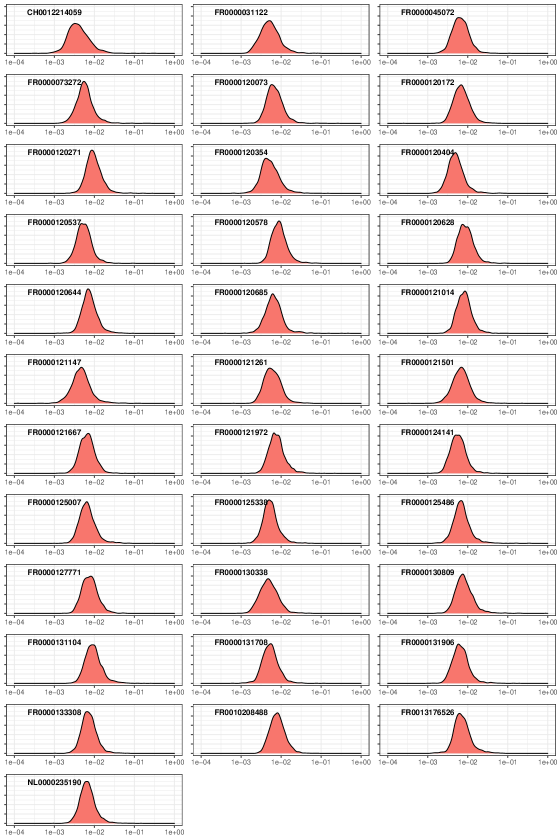

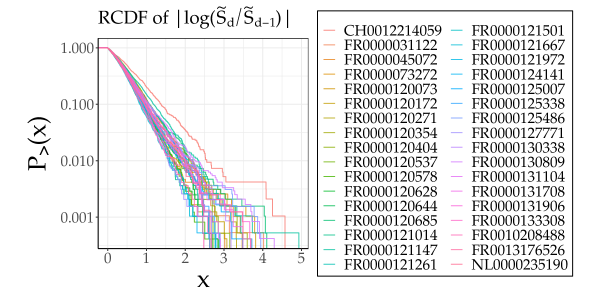

Figure 16 plots for TotalEnergies as a function of time. It oscillates around a typical value and has a positive autocorrelation over a few days. The distribution of for the 34 stocks is reported in Fig. 17: while its shape is similar for all the assets, its parameters depend on each stock.

We also report the distribution of the absolute value log-changes of the slopes in Fig. 18, which clearly appear to be exponentially distributed. Its one-step autocorrelation is negative.