1 Introduction

In this paper, we consider the random-coefficient autoregressive (RCA) model,

| (1) |

where is a random vector with and . Model (1) is a generalization of the usual AR(1) model, in that the autoregressive coefficient fluctuates over time around its mean with variance , instead of being constant at . Since Nicholls and Quinn (1982), much attention has been paid to the estimation and inference theory of model (1); see, for example, Hwang and Basawa (2005), Aue and Horváth (2011), Horváth and Trapani (2019) and references therein.

One aspect of the inferential theory for (1) that has attracted econometricians and statisticians is how to test the hypothesis of , that is, how to test the null hypothesis of the usual autoregressive specification against the RCA alternative. Nicholls and Quinn (1982) and Lee (1998) proposed test statistics for testing under the stationarity condition . Nagakura (2009a) showed the Lee (1998) test statistic has the same asymptotic null distribution when as when .222Nagakura (2009b) also showed the Lee (1998) test is consistent when and some other conditions hold. However, he did not show the test statistic has the same limiting null distribution when as when . The condition, , which these tests rest on, however, is restrictive and limits their applicability in practice, in view of the empirical analyses by Hill and Peng (2014) and Horváth and Trapani (2019). They applied model (1) to several macroeconomic variables and estimated to be near 1 for most of the variables, with estimated to be greater than 1 for some. For instance, the estimates obtained by Horváth and Trapani (2019) took values between 0.9884 and 1.0021. Their results indicate that nonstationary RCA models where and may be greater than 1 with near unity are empirically relevant, and thus testing procedures are required that are valid under these conditions. Horváth and Trapani (2019) proposed a test statistic for valid under the nonstationarity conditions (as well as under the stationarity conditions).

Another insight earlier studies provide is that the variation of the autoregressive root is smaller (if it exists) than assumed in the extant literature. For example, according to the empirical analysis conducted by Horváth and Trapani (2019), 4 variables out of 7 were estimated to have positive variance () in their coefficient, which is between and . However, Horváth and Trapani (2019) studied the finite-sample power of their test only for , which are of larger magnitude than observed in practice (as long as macroeconomic variables are concerned). 333Horváth and Trapani (2022) applied the RCA model to a cryptocurrency index and estimated to be around . Therefore, it is unclear whether their test performs well when is of small magnitude that seems to be typical in empirical studies. In fact, their test has almost no distinguishing power when is relatively small, as our simulation studies will reveal.

Given these observations, we consider model (1) with near unity and near zero and employ the following near unit root RCA model:

| (2) |

where and . When , (2) is the popular (conventional) local-to-unity AR(1) model. This specification has been useful in analyzing the power of unit root tests (Elliott et al., 1996) and in developing estimation and inference theory for models involving persistent variables (see, inter alia, Phillips, 1987; Stock, 1991; Campbell and Yogo, 2006; Phillips, 2014). The local-to-zero variance has been employed under by McCabe and Smith (1998) and Nishi and Kurozumi (2022) to derive and compare the local asymptotic power functions of unit root tests of against . Introducing the local-to-zero variance provides us with a convenient framework in which we can evaluate power functions of several tests against the alternatives that are close to the null of and seem relevant for empirical applications.444For example, when and , the variance takes values between 0 and . Model (2) integrates these two local-to-unit-root parametrizations, thereby rendering itself an empirically relevant random-coefficient model.

In the literature, testing procedures for have often been studied in the special case with . Such a model is called stochastic unit root (STUR) model. Test statistics for in the STUR model have been proposed by earlier studies, including McCabe and Tremayne (1995), Leybourne et al. (1996) and Distaso (2008). Moreover, McCabe and Smith (1998) and Nishi and Kurozumi (2022) analyzed the power properties of several tests for under the STUR modelling. On the one hand, the STUR model is a generalization of the pure unit root model, which is a main reason authors have paid much attention to it. But on the other hand, the assumption of exactly being unity is a restrictive condition that is unlikely to hold in empirical analysis. Our model, (2), generalizes the STUR model by allowing to take a value different from unity (but near it), which is a more realistic assumption given the empirical analyses conducted by earlier studies.

Nishi and Kurozumi (2022) revealed that, under the STUR () modelling with , the test for proposed by Lee (1998) and Nagakura (2009a) (hereafter, LN) has a higher local asymptotic power function than other tests. We will demonstrate that this is also the case when and . In this paper, however, it will be shown that the LN test can perform poorly when , for both the cases and . We will therefore propose several tests for whose power properties are robust to the value of . One of those tests turns out to be more powerful than the LN test for moderate to large values of . To the best of our knowledge, this study is the first to investigate how the value of affects the power properties of tests for , with the only exception of Su and Roca (2012), who analyzed through simulation this effect in finite samples under .

The other issue that this paper tackles is how to remove the effect of nuisance parameters from the null distributions of the test statistics mentioned above. As pointed out by Nagakura (2009a), the limiting null distribution of the LN test statistic depends on the correlation between and , , and so do the test statistics proposed in this article. If the true value of is known, the nuisance parameter can be removed straightforwardly by a similar way to the modification proposed by Nagakura (2009a), but this is not the case when the true is unknown. This problem is caused by the fact that the localizing parameter cannot be consistently estimated, as will be made clear later. As a solution for this problem, we propose a testing procedure based on the Bonferroni approach as Campbell and Yogo (2006) and Phillips (2014) did in the context of predictive regressions.

The remainder of this paper is organized as follows. In Section 2, we consider the local-to-unity model (2) with the true value of (or equivalently ) known, to uncover the effect has on power properties of tests for and propose new tests that have power functions robust to this effect. We also propose a modification to make these tests independent of , a nuisance parameter, under the null. In Section 3, we consider model (2) with unknown . Because the modification proposed in the preceding section cannot be directly applied in this case due to the fact that is not consistently estimable, we base our tests on the Bonferroni approach by constructing a confidence interval for . Section 4 analyzes the finite-sample properties of our tests and compares them with those of existing tests. In Section 5, we apply our tests to real data. Section 6 concludes.

2 The Case of Known

2.1 The effect of

In this section, we begin our analysis under the assumption that the true value of is known. This assumption will be relaxed in the next section. Our analysis for model (2) in this and the next section is conducted under the following assumption.

Assumption 1.

, where

Also, and . Moreover, .

Define and . Define also the partial sum process on by and . Then, it follows from the functional central limit theorem (FCLT) that under Assumption 1, as

in the Skorokhod space , where is a vector Brownian motion with the covariance coefficient

with . Note that and are not necessarily independent because of the covariance , and the Brownian motion satisfies the following equality in distribution:

| (3) |

where is a standard Brownian motion independent of . Following the argument by Nishi and Kurozumi (2022), we can show that under Assumption 1, the standardized process on constructed from (2) weakly converges to the Ornstein-Uhlenbeck (OU) process , where solves . We can also construct consistent estimators of variances, namely, and . Define . Then, the estimators and are consistent for and , respectively, which is proven in Appendix B.

Several tests of for model (2) have been proposed by earlier work such as LN. The LN test statistic is defined by

Nishi and Kurozumi (2022) found that the LN test has a high power function under the assumption that and .

As pointed out by Nishi and Kurozumi (2022), the LN test, which was originally derived as a locally best invariant test, can also be obtained as the t-test for under . To see this, note that from model (2), a simple calculation gives

| (4) |

where . Because and under Assumption 1 with , model (4) may be viewed as the linear regression model with playing the role of the disturbance, and the LN test statistic is obtained as the t-test for (with the variance estimator under the null used).

In view of this observation, the LN test seems to be a natural test for . However, this may not be the case when , because it results in , that is, endogeneity. In fact, as we will shortly show, the power of the LN test is crucially affected by the value of , and the greater the value of (in absolute value), the more poorly the LN test performs. Because we consider the localized model (2), the setup for analyzing the influence has is also a localized one. To derive relevant local asymptotic distributions, we localize the correlation (rather than the covariance ) between and in the following way:

Assumption 2.

.

Here, is interpreted as the correlation coefficient in the limit as . Under this localization, the LN test statistic has the following asymptotic distribution:

Note that when and (or ), the limit distribution reduces to the one Nishi and Kurozumi (2022) derived (their equation (19)). Nishi and Kurozumi (2022) found that the LN test performs better than other tests when . To see how the value of alters the LN test’s power properties, we simulate the asymptotic distribution in (5) by 100,000 replications. The replications are based on , so that , and . Note that the effect of on the limit distribution is symmetric when ; that is, and produce the identical distribution. This is because when , and hence in this case. Thus, in this simulation, and in the replications conducted later where holds, we only consider positive values of . Figure 1 shows the power functions of the LN test for under . One noticeable feature is that as gets larger, the power function gets lower and flatter for , while the power becomes greater for . Since the power gains over are obviously outweighed by the power losses over , we conclude that the LN test performs poorly when is large (in absolute value).555In our unreported simulations, we also found a similar tendency in the power function of Distaso (2008)’s LM test, which is based on the assumption of and being independent. The results are omitted to save space.

The LN test’s poor performance for large could be attributed to the endogeneity in (4). One solution for this endogeneity is to augment model (4) by adding as a regressor,

| (6) |

where and . Because this augmented model is free from the endogeneity, that is, under Assumption 1, we propose using the t-test for in model (6). We also propose using the Wald test for , because if and only if . To express the t and Wald test statistics, first regress , and on a constant:

| (7) |

where , and , and are defined similarly. Let , , , and . Then, model (7) can be expressed in matrix notation as

| (8) |

where and . The t and Wald test statistics are then given by

| and | |||

where , and and are the OLS variance and coefficient estimators of (8), respectively. We shall call the t and Wald tests in model (6) augmented t and Wald tests, respectively. The limiting distributions of these augmented test statistics are collected in the following theorem.

Theorem 2.

There are two points worth mentioning. First, the augmented t test statistic in model (6) has the asymptotic null distribution independent of . This is a direct result of the augmentation, which is intended to remove the endogeneity from the linearized model (4). When performing the augmented t test, we regress the endogenous regressor (and ) on . In the limit, this projection amounts to replacing in the limiting distribution of with , the residual from the linear projection of on in the Hilbert space (see, for example, Phillips and Ouliaris (1990)).

The second point is that the limiting null distributions of the augmented t and Wald test statistics are standard normal and chi square with 2 degrees of freedom, respectively, when . This will be seen immediately upon noting and are independent when (due to the independence between and ), and the limit distributions under conditional on are standard normal and chi square with 2 degrees of freedom (and so are they unconditionally). Along the lines of this argument, the asymptotic null distribution of the LN test statistic is seen to be standard normal when .

2.2 Removing from the limiting null distributions

Unless , the test statistics discussed thus far have asymptotic null distributions dependent on . Actually, this dependence stems from the strong persistence of the regressors and and the long run endogeneity present in the linearized models (4) and (6). To illustrate this, consider model (4) and the LN test. Under the null of , the model reduces to

| (11) |

where and . This model is free from endogeneity because . However, the regressor is, in a sense, “endogenous” in the limit as , because of the correlation between its innovation and the disturbance . Indeed, the LN test statistic becomes

where () is correlated with the differential (). This correlation originates from that between and , which is denoted by . Therefore, the correlation between the regressor’s innovation and the regression disturbance affects the test statistic’s behavior in the limit.

Interestingly, the situation we are in is analogous to the one that has been considered in the literature on predictive regressions. In predictive regressions, a main aim is typically to investigate whether stock returns () can be predicted by another economic or financial variable (). To test the predictability of , predictive regressions involve regressing on a constant and the lag of :

Here, represents the predictability of ; the stock return is not predictable by if . In the literature on predictive regressions, it has been well known that the usual t test for the hypothesis can be misleading when the regressor is persistent, or has a generating mechanism of the form with , and its innovation is correlated with the regression disturbance . The problem arising in such a case is that the asymptotic null distribution of the t statistic depends on and is not standard normal unless (see, for example, Campbell and Yogo, 2006). Our situation here is essentially the same: the regressor in (11) is persistent with the mechanism and its innovation is correlated with the regression disturbance , which results in the test statistic having the limiting null distribution dependent on the correlation .

For the predictive regression model, there is an extensive literature on this problem, and numerous solutions have been proposed (Campbell and Yogo, 2006; Phillips and Lee, 2013; Phillips, 2014; Kostakis et al., 2015). For our case, fortunately, one of those solutions can be applied. Specifically, following Campbell and Yogo (2006), we modify the test statistics (LN, augmented t and augmented Wald) so that their asymptotic null distributions are standard normal and chi square with 2 degrees of freedom, irrespective of the value of . To explain the idea, take the LN test as an example. Note that under the null of , in the numerator of the LN test statistic may be asymptotically expressed as

given the distributional equivalence (3). This observation leads us to propose the following modification to remove the effect of :

| (12) |

where is an estimator of .666In fact, Campbell and Yogo (2006) proposed the modification based on the optimality argument. In Appendix B, we show that is consistent. Note that is used as a proxy for . With the replacement given in (12), the modified LN test statistic is defined by

The modified augmented t and Wald tests are based on the following regression model:

| (13) |

where with . The modified augmented test statistics are

| and | |||

where and are the OLS variance and coefficient estimators of (13), respectively.

Theorem 3.

It should be noticed that the modified test statistics have pivotal asymptotic null distributions (standard normal and chi square with 2 degrees of freedom), thanks to the independence between and . Also note that the limiting distributions are unaffected by our modification when (cf. Theorems 1 and 2).

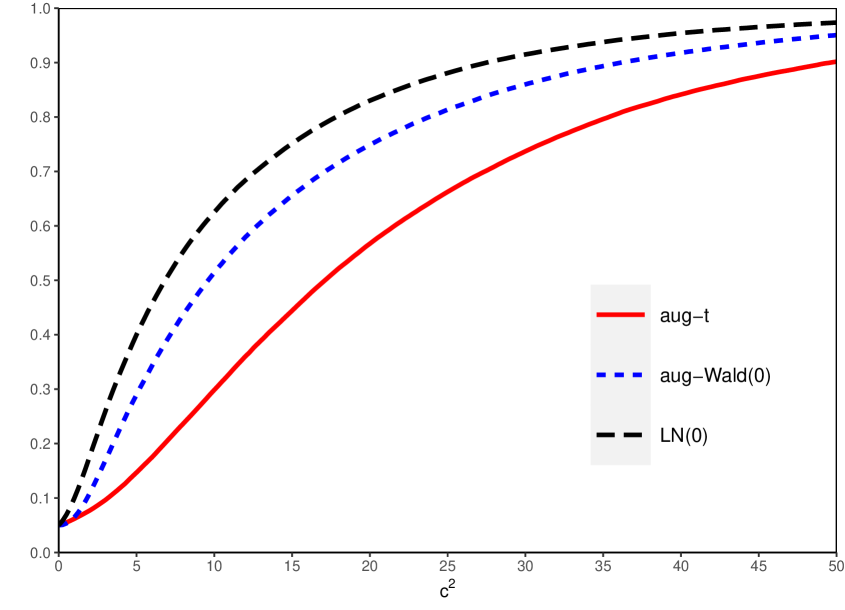

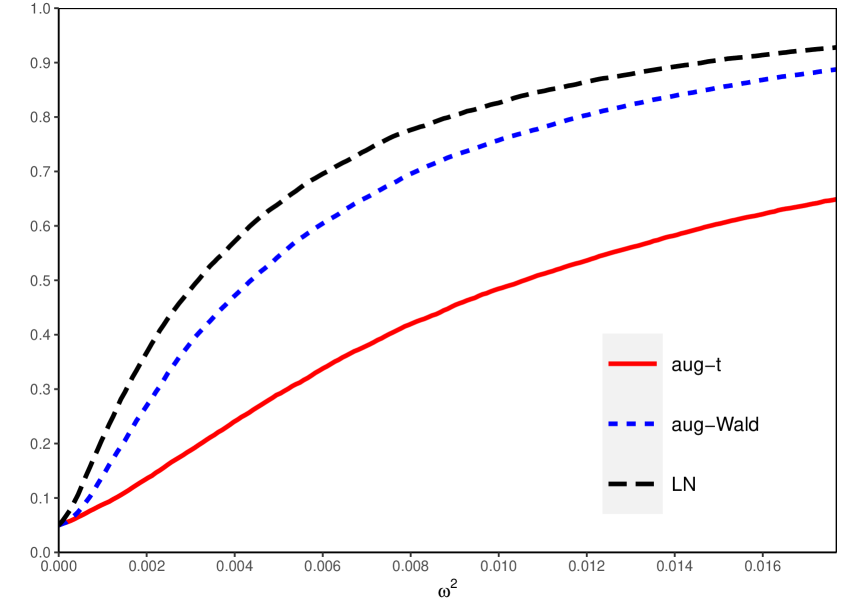

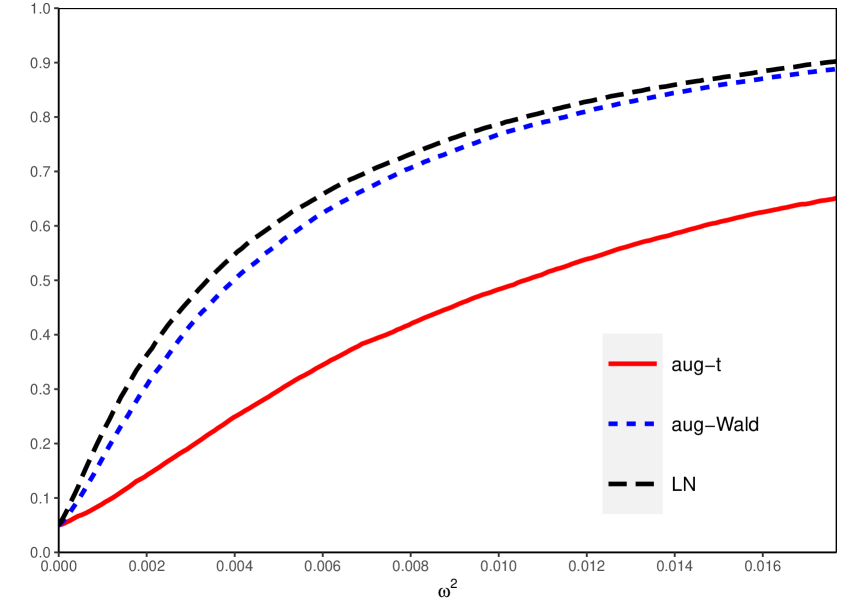

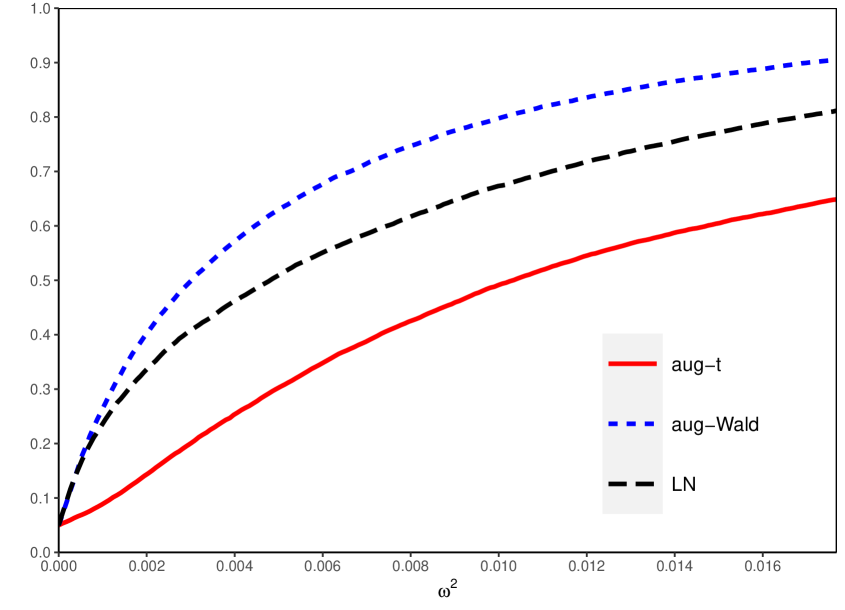

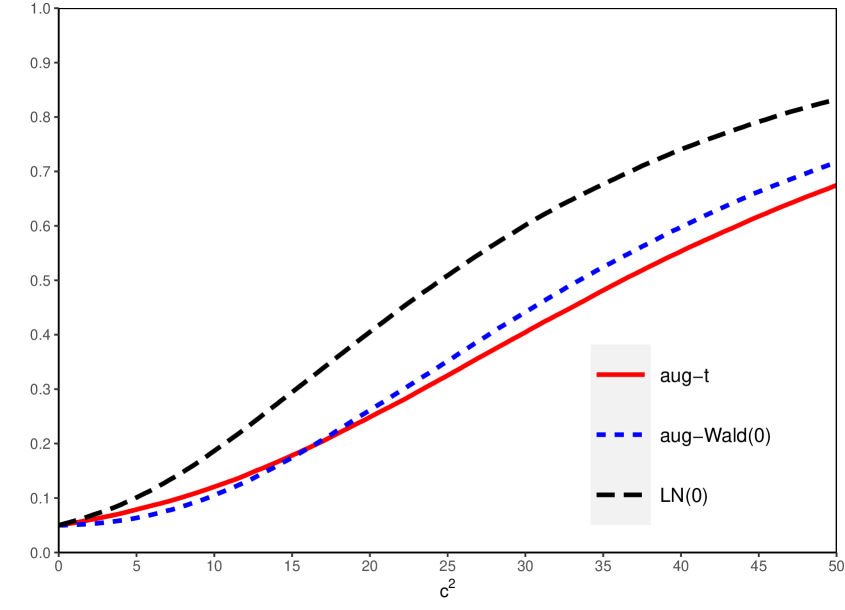

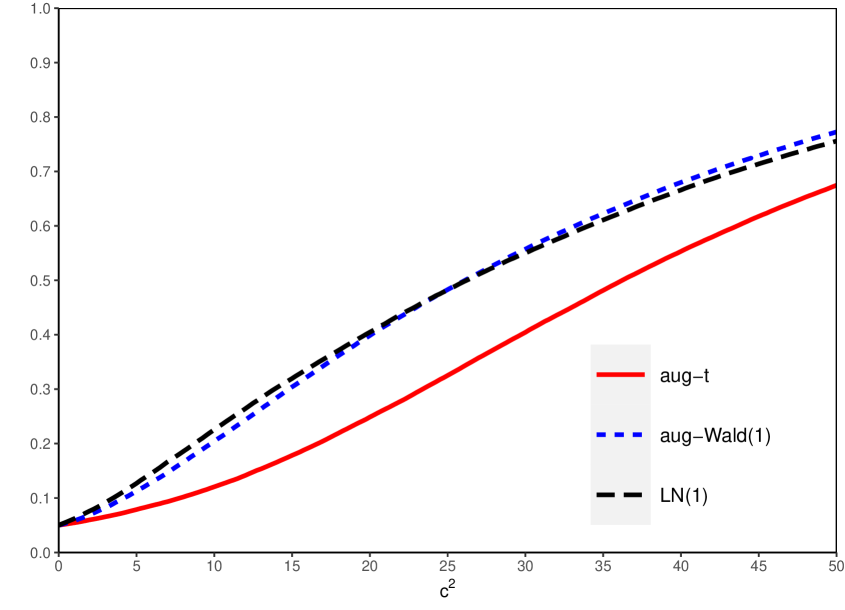

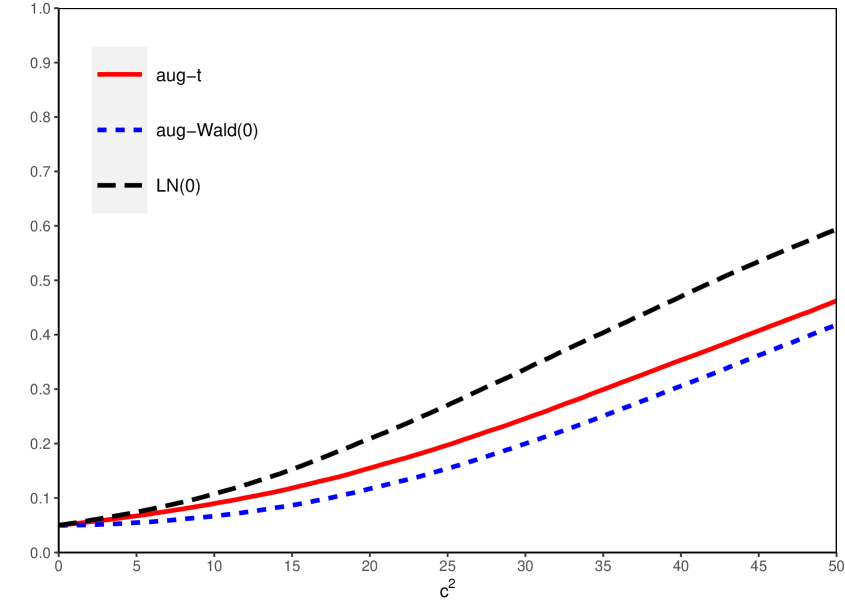

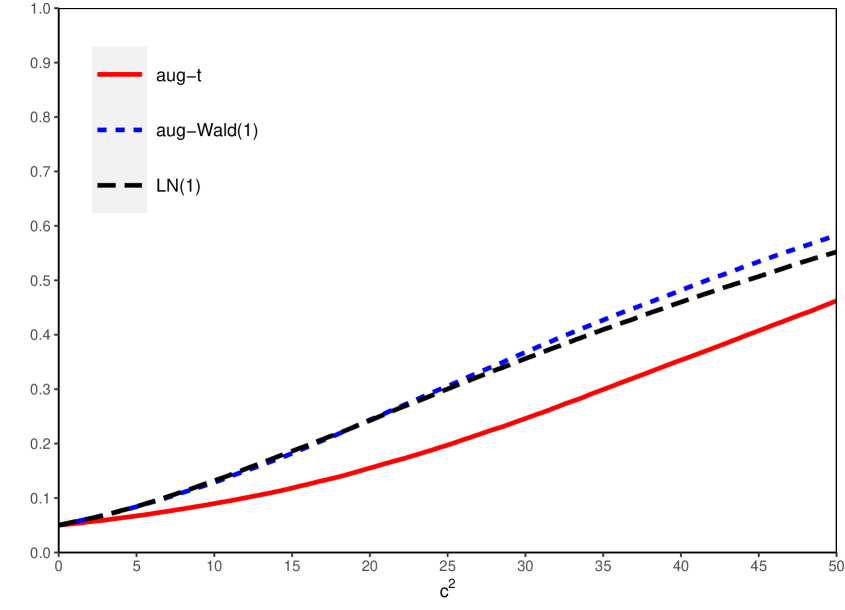

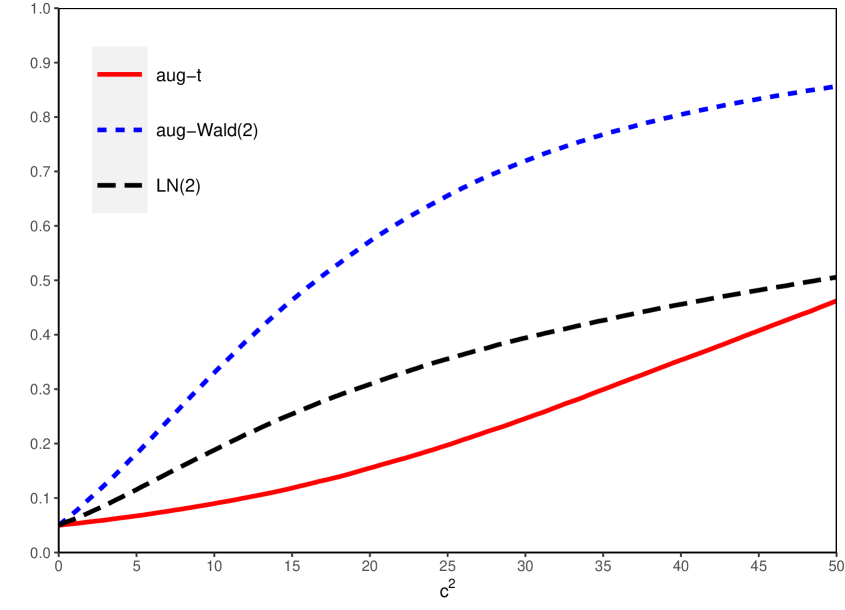

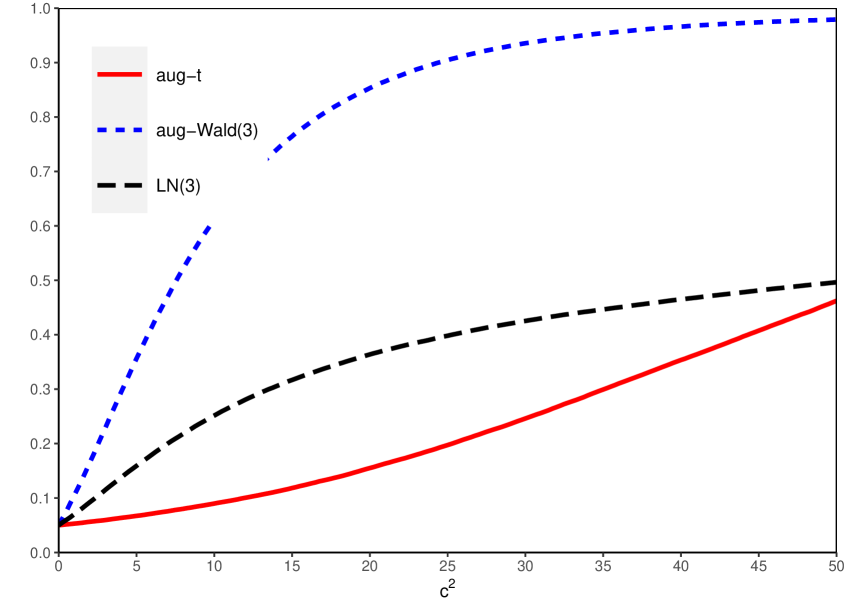

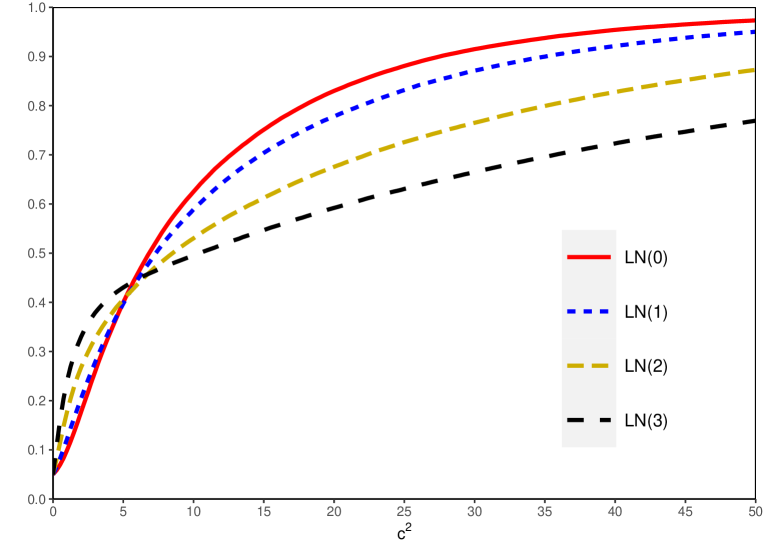

Figure 2 compares the asymptotic power functions of the modified LN, augmented t and augmented Wald tests under and with . When , the LN test performs best, and the Wald test’s power function is slightly below the LN test’s. As for the comparison between the augmented t and Wald tests, the Wald test has better power properties than the t test. When , the Wald test outperforms the LN test (and the augmented t test) with the greater dominance by the Wald test for larger . To translate these results into finite-sample ones, consider for example the case of , in which case . Based on the results from the local asymptotic case, it is expected that the augmented Wald test performs more poorly than the LN test if , or in this case, and outperforms the LN test otherwise. To see whether this reasoning gives a good approximation of finite-sample results, we present the size-adjusted power functions for in Figure 3. The calculation of these power functions are based on 20,000 replications where , , and so that under . Figure 3 shows the local asymptotic analysis can well predict the finite-sample results: the LN test performs slightly better than the augmented Wald test when , but the latter test outperforms the former otherwise.

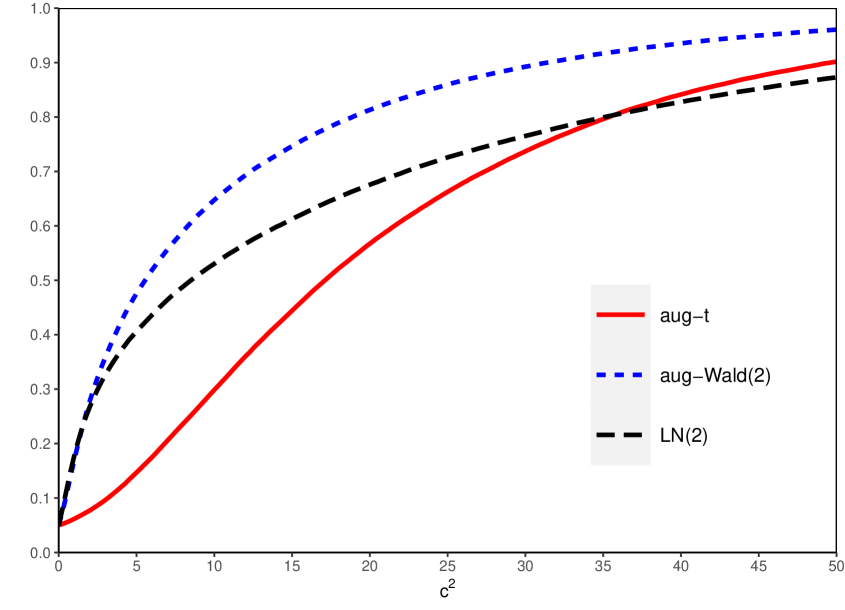

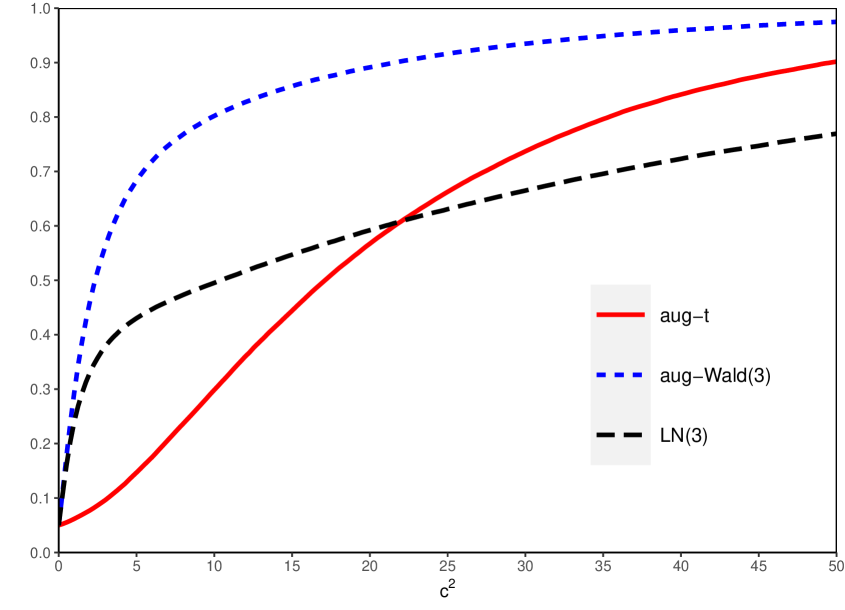

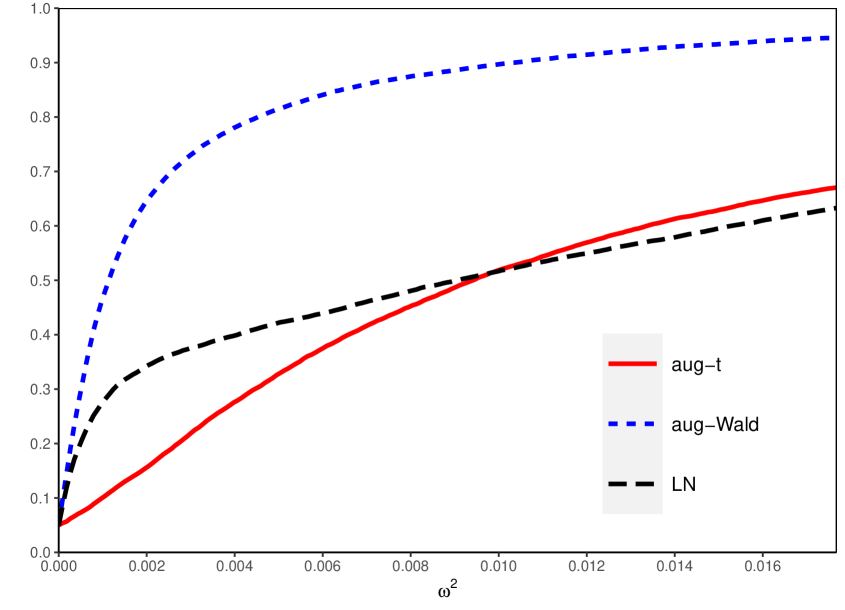

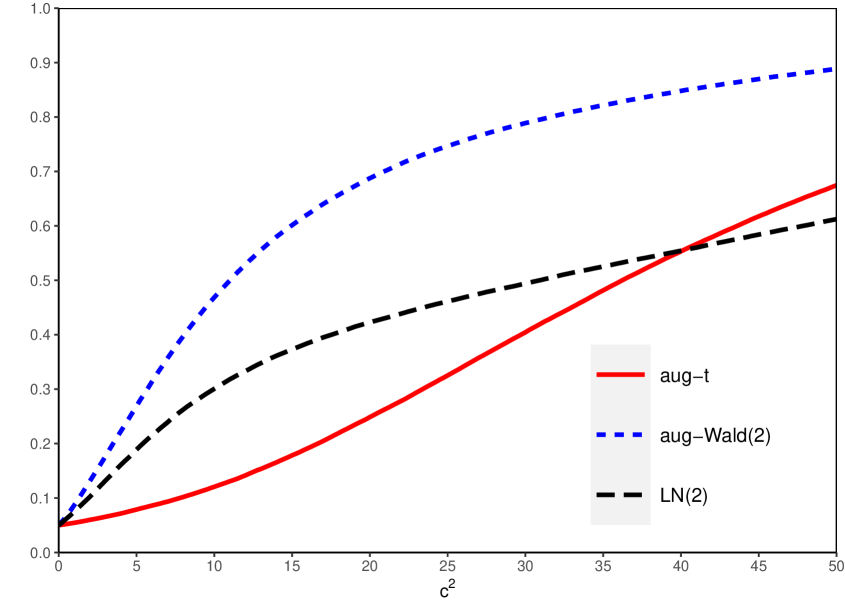

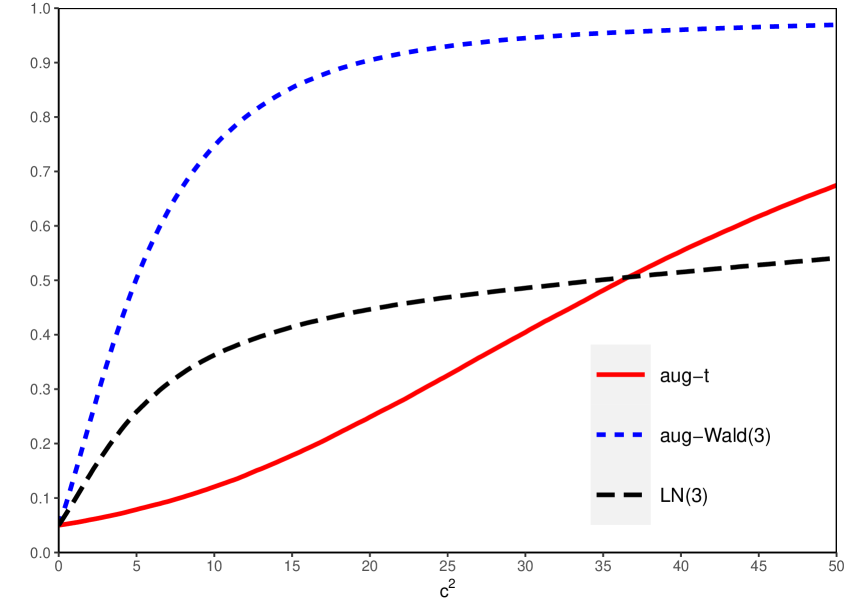

We also compute the asymptotic power functions under , to investigate the effect of the value on the power properties. The computed power functions are displayed in Figures 4 and 5. When , the general pattern of the power properties is the same as when : the LN test performs best for small , and the Wald test performs best for moderate to large . However, the powers of all the tests we consider get lower as deviates from 0 (as long as ).777According to the results of our simulation studies given later, deviations from 0 by positive seem to lead to higher powers. A similar tendency of the power properties of tests for has been observed through simulation by earlier work such as Nagakura (2009a) and Horváth and Trapani (2019). Nonetheless, even when , the Wald test’s power function is increasing in while the LN test’s is decreasing in . This renders the Wald test preferable in empirical applications, where in general the degree of the correlation between the random coefficient and disturbance is unknown to practitioners.

Although all the above results are based on the assumption that the true is known so that the tests discussed so far are infeasible, they suggest the potential of the augmentation to enhance the ability to detect the nonzero variance of the autoregressive root.

3 The Case of Unknown

In this section, we consider model (2) with the true unknown. To deal with the uncertainty about , we use the OLS estimator of , which is defined by . In Appendix C, we show that is consistent, and that other estimators defined in the preceding section such as remain consistent if they are computed using instead of the true . Given these consistency results, one may expect that the asymptotic behaviors of , and are the same as those of , and . Unfortunately, however, this is not the case. Indeed, it can be shown that the limiting null distributions of the test statistics, if calculated using , are no longer normal or chi square. This is essentially because is not consistently estimable, which has been well known in the literature (Campbell and Yogo, 2006).

To deal with this problem, following Cavanagh et al. (1995) and Campbell and Yogo (2006), we base our tests on the Bonferroni approach by using a confidence interval for instead of its point estimate . The Bonferroni-based test consists of two steps: first, construct a confidence interval for , and then repeat either of the tests considered above using all the hypothetical values belonging to the confidence interval. Specifically, letting denote either the modified LN, augmented t or augmented Wald test statistic (calculated using ), the testing procedure based on the Bonferroni approach is described as follows:

-

Step 1.

Given the data , calculate for each hypothetical (on some grid) the t statistic , to construct the (equal-tailed) confidence interval for , denoted by . That is, is the collection of all the that satisfies with and denoting the lower and upper quantiles of the asymptotic distribution of derived under the assumption that .

-

Step 2.

For each , calculate and compare its value with the critical value with significance level (based on the standard normal or chi square distributions). Reject the null only if all the calculated () exceed the critical value.

We shall call tests following these two steps Bonferroni tests.

Remark 1.

-

1.

The asymptotic distribution of under is . The quantiles and can be found through simulation.

-

2.

By the Bonferroni inequality, the resulted test is (asymptotically) a test with significance level : under ,

-

3.

Campbell and Yogo (2006) constructed the confidence interval for by inverting the Dickey-Fuller type t statistic, which is calculated by centering by unity rather than . However, it has been known in the literature on predictive regressions that the use of the Dickey-Fuller type t ratio leads to severe size distortion (Phillips, 2014). We found in our unreported simulations that our Bonferroni tests also suffer from the same problem when it is based on the Dickey-Fuller t ratio. Following the theoretical analysis by Phillips (2014), we here construct the confidence interval for using the t statistic centered by hypothetical ’s.

Although the Bonferroni test defined above is a valid test with significance level , the test’s type 1 errors (dependent on ) can be quite smaller than , as pointed out by Cavanagh et al. (1995) and Campbell and Yogo (2006). To make the type 1 errors close to the desired nominal level, (say), they proposed using a pair with which the Bonferroni test’s type 1 errors are close to the given . Theoretically, we would find such numerous pairs by changing both the values of and . To simplify the searching process, we fix and set , following Campbell and Yogo (2006). In this study, we consider the case , giving the Bonferroni test with significance level 0.05. Then, for each , we numerically find the value of such that under the null , and this probability is as close to 0.05 as possible, for all on some grid. The simulation process to find the values is described in Appendix A.

Table 1 displays the significance level of the confidence interval for along with corresponding intervals of values.888We assign values to each interval of instead of each single (on some grid) for computational ease of the Bonferroni-test. Given the good asymptotic performance by the modified Wald test, we report in Table 1 values for the case of being the modified augmented Wald test statistic. When performing the Bonferroni-Wald test, first estimate by its consistent estimator , and then select the value of based on Table 1. For example, if , is selected. With the selected value, one can perform the Bonferroni-Wald test following the two-step testing procedure outlined before. The finite-sample performances of the Bonferroni-Wald test are investigated through simulation in the next section.

4 Finite-Sample Performance

As described in Appendix A, the simulation exercise to determine the values of is based on the asymptotic procedure. Thus, we need to verify whether the Bonferroni-Wald test we have proposed performs well in finite samples.

4.1 Empirical size

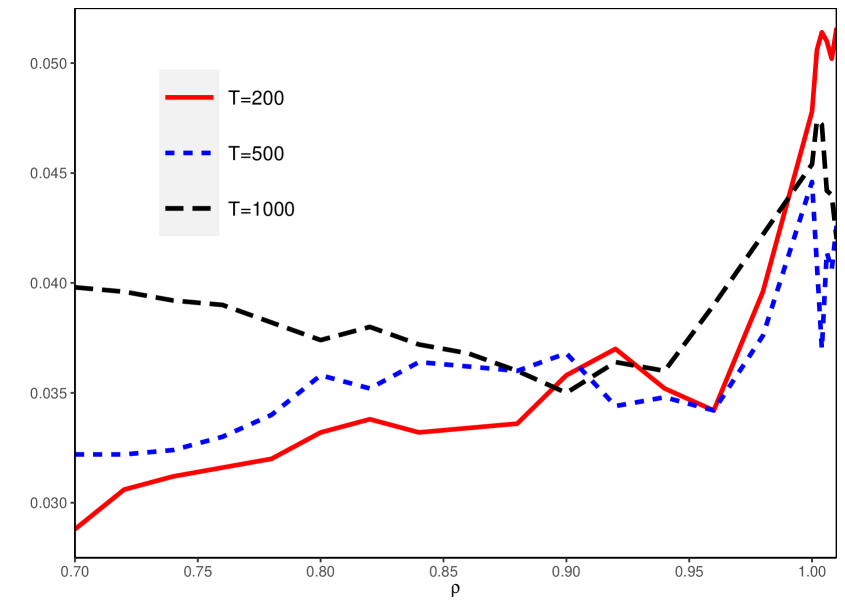

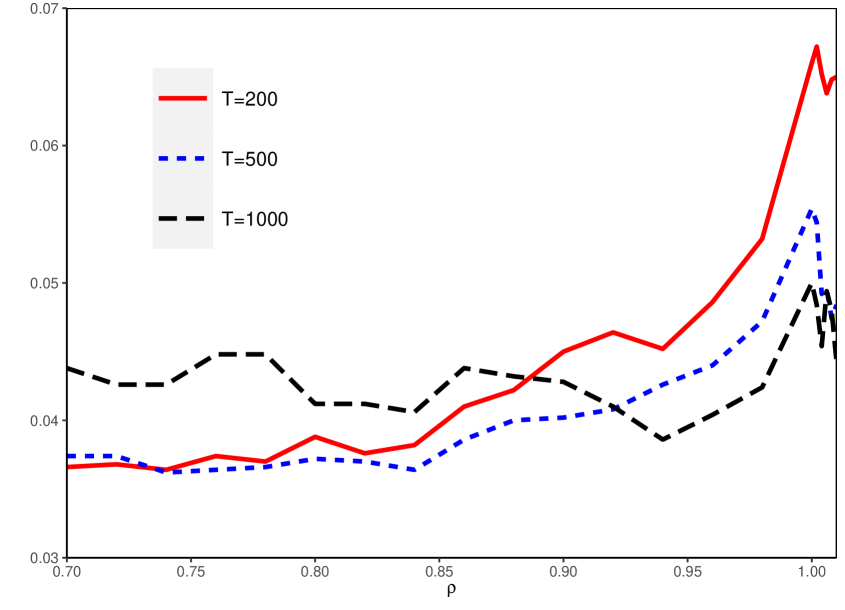

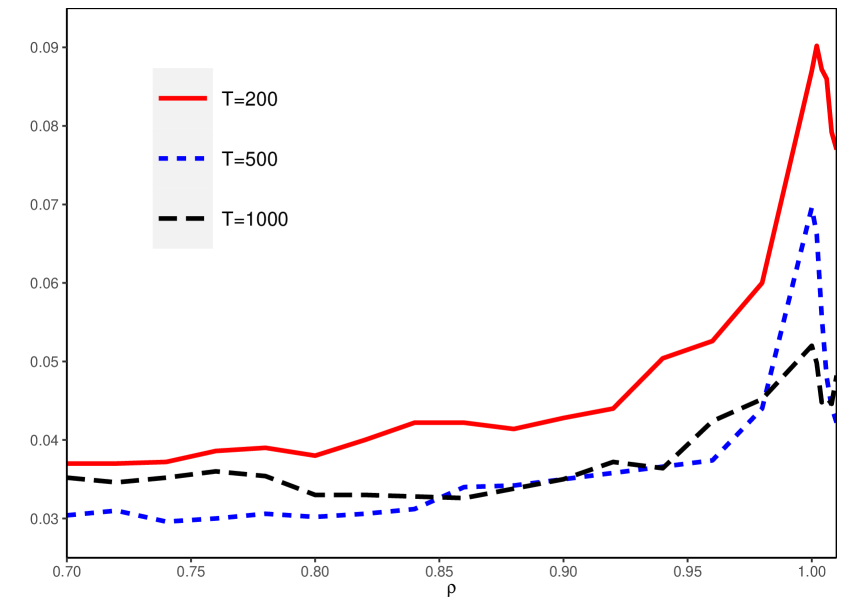

Following Nagakura (2009a), we employ three data generating mechanism to evaluate empirical sizes: (i) , so that , (ii) , so that , and (iii) , so that . For each case, we set . The sample size we use is , and the number of replications is 5,000. The values are fixed across , and we consider . The simulation results are collected in Figure 6. The general pattern is that the empirical rejection rates under are relatively small when and tend to be greater than the nominal level 0.05 when is near unity. As for the normal case (Figure 6(a)), rejection rates are stable around 0.05 over , with them approaching 0.05 as increases. As for the chi square cases (Figure 6(b) and (c)), rejection rates stay around the nominal level, but they get farther away from 0.05 when is larger, is smaller and is near 1. In particular, when and , the rejection rates can be as large as 0.09 (around ), although they approach 0.05 as increases. A similar tendency can be observed in the finite-sample behavior of modified LN tests proposed by Nagakura (2009a) according to his simulation results. One possible cause of this phenomenon would be the finite-sample bias involved in the estimation of when the value is large. One may be advised to use a more conservative Bonferroni-Wald test (with smaller values) when the estimate is large and the sample size is not so large.

4.2 Finite-sample power comparison

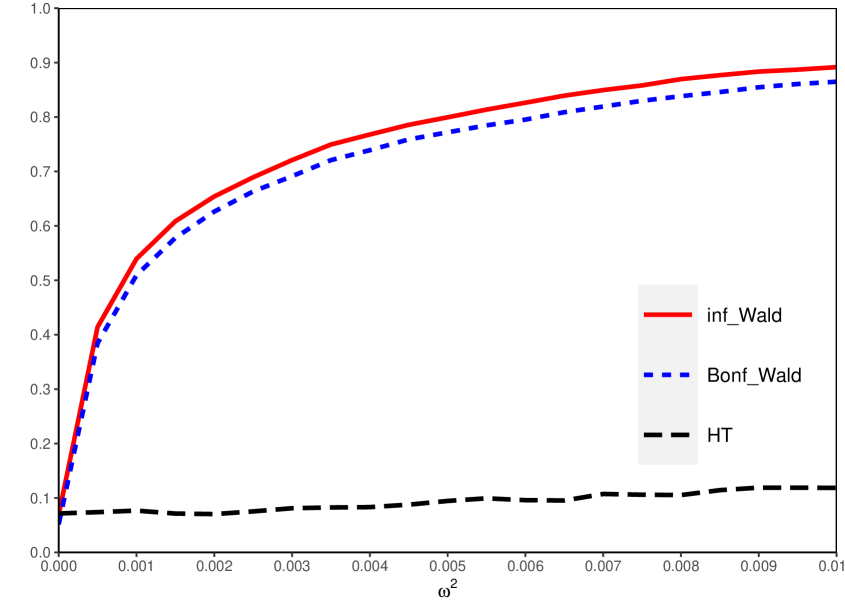

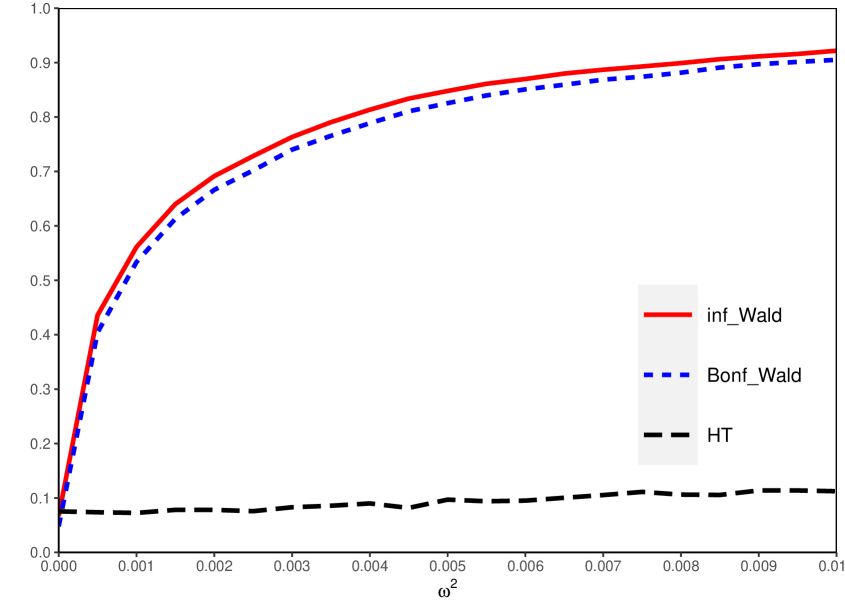

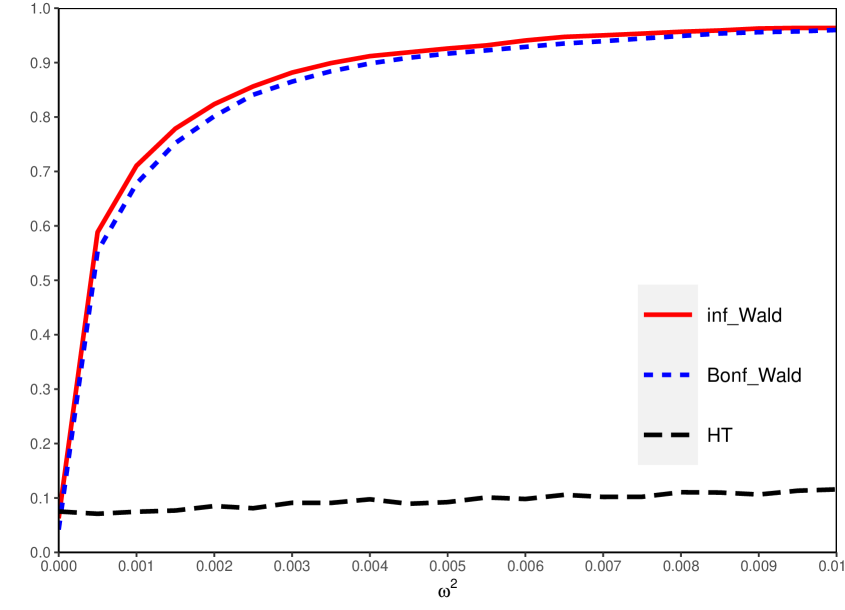

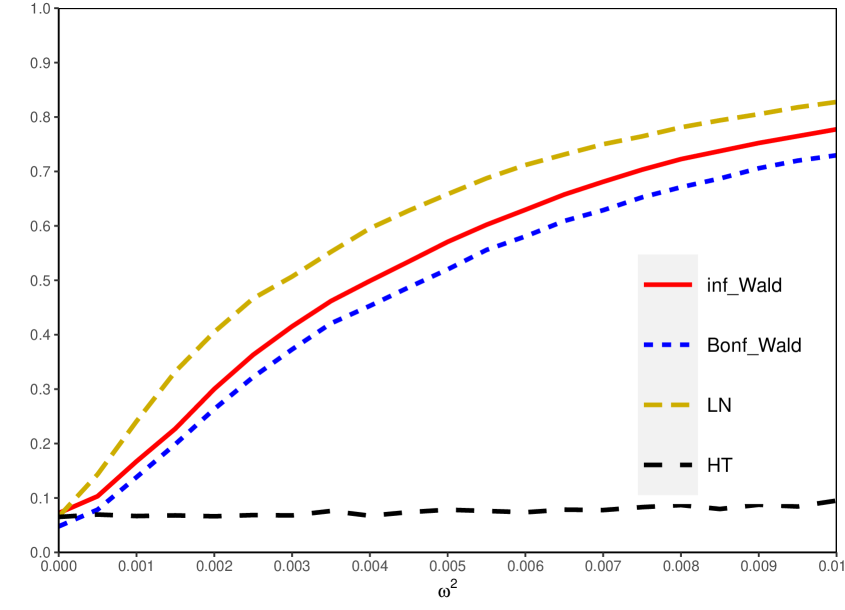

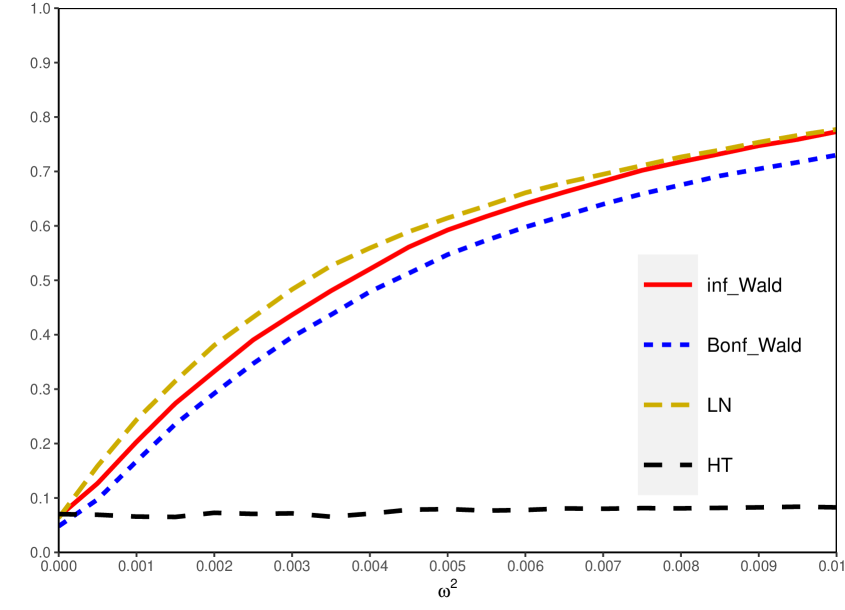

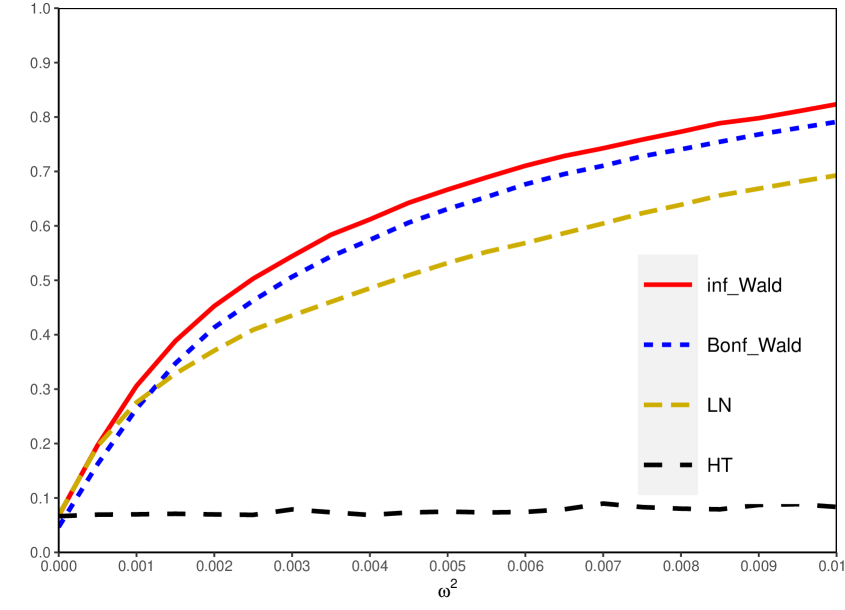

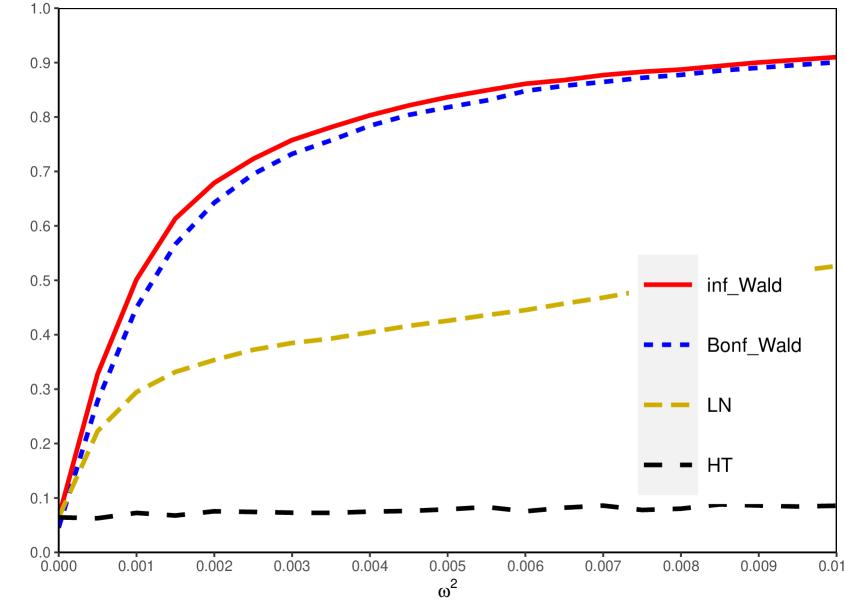

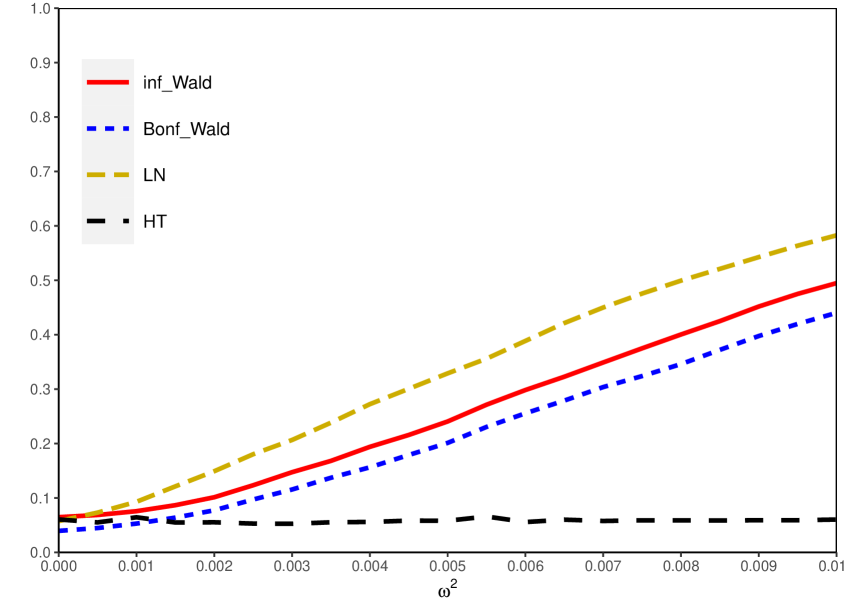

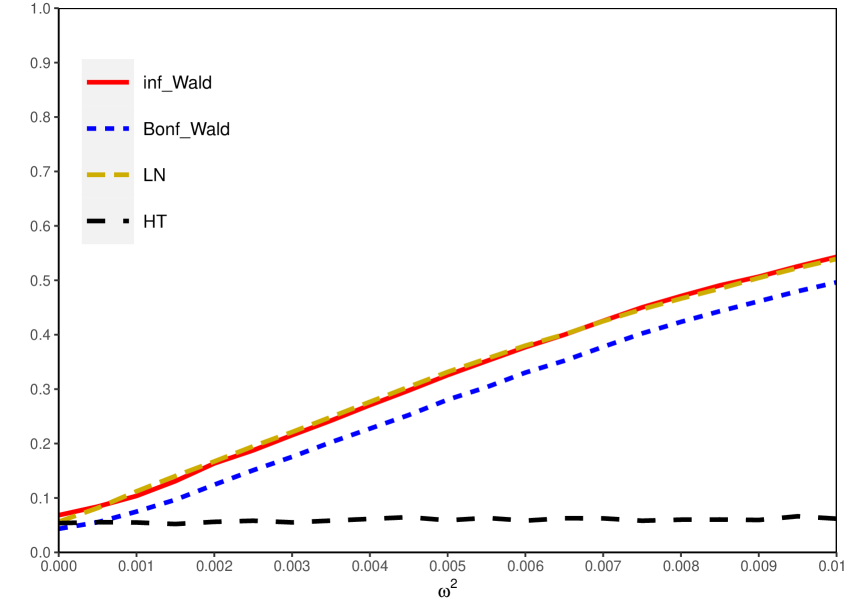

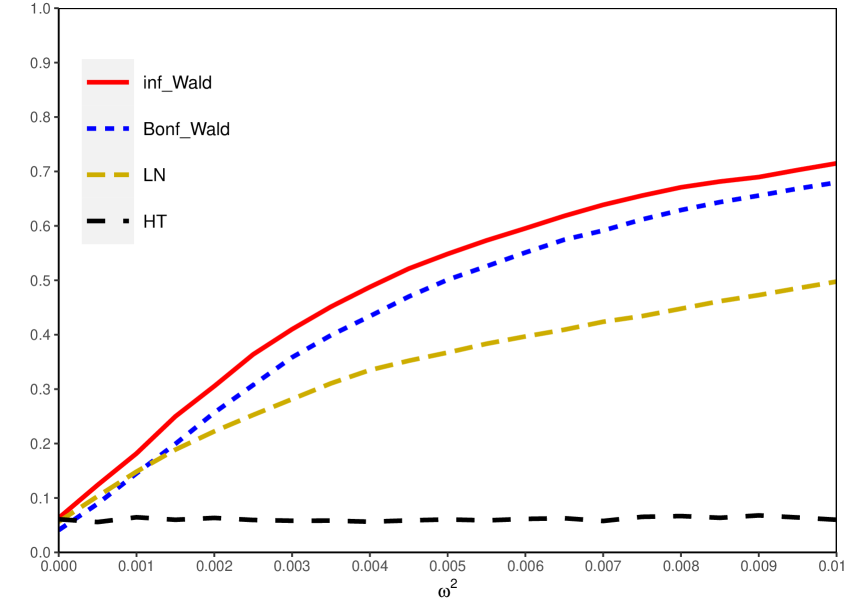

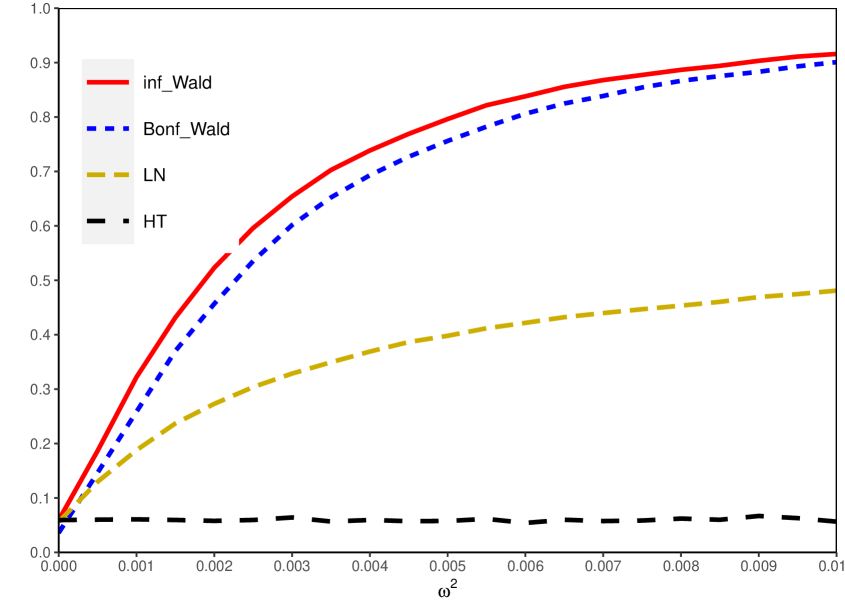

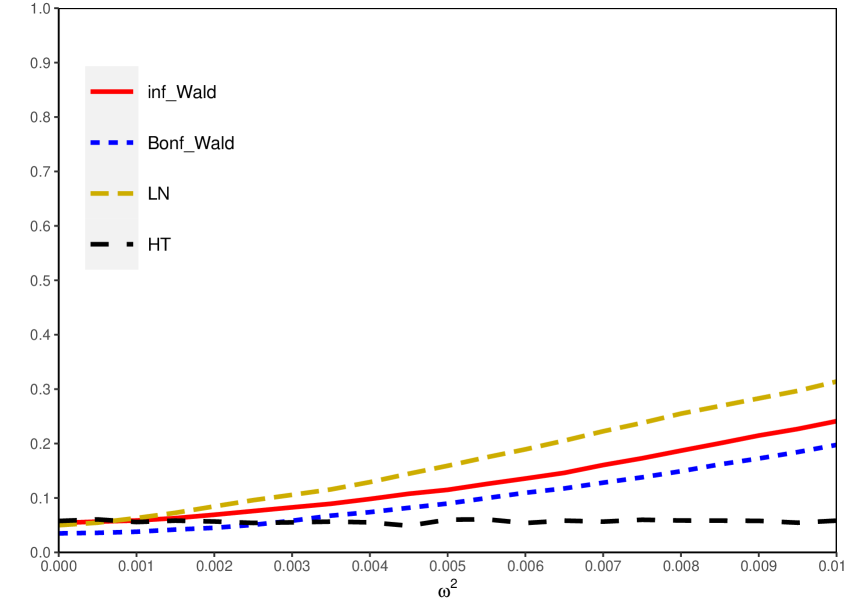

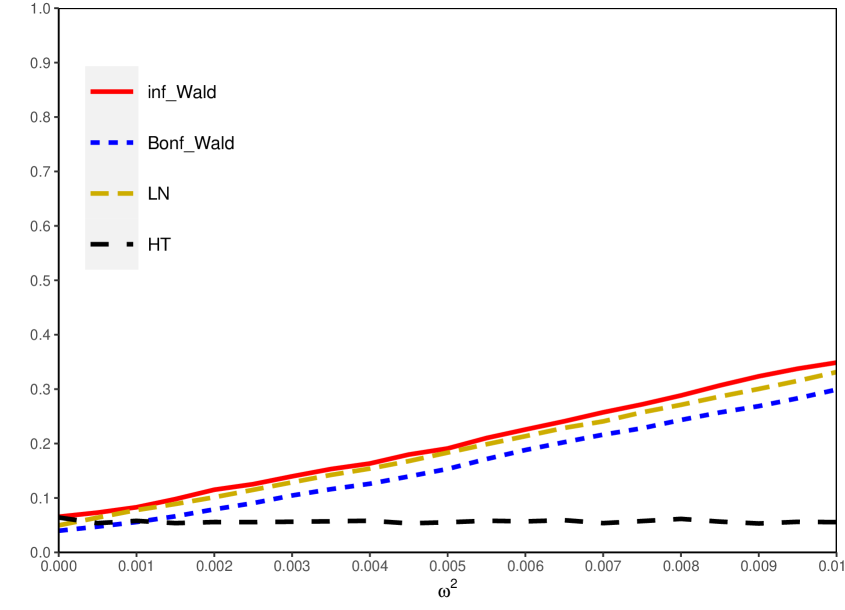

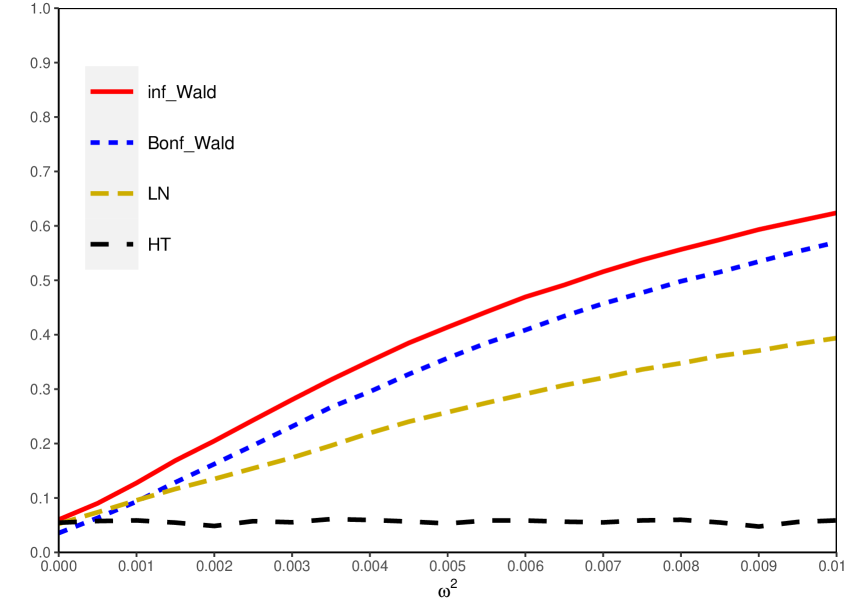

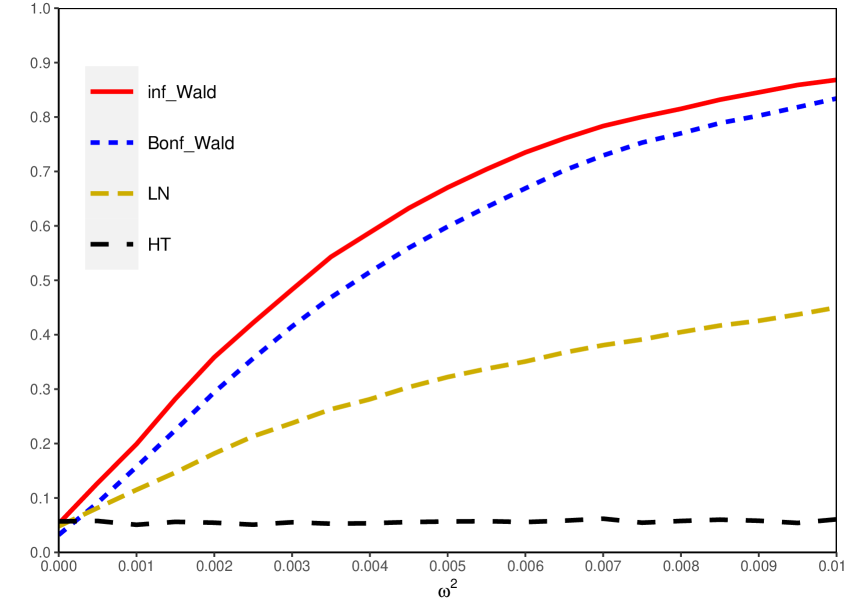

Next, we investigate tests’ ability to detect the nonzero variance in the autoregressive root. The simulation design is as follows: , and with , , and (corresponding to ). The tests we consider here are the Bonferroni-Wald test, the infeasible modified Wald test (calculated using the true ), and one of the modified LN tests proposed by Nagakura (2009a), which is denoted by in his notation. The infeasible Wald test is taken as a benchmark, and thereby we can evaluate the power loss originating from using the confidence interval for to perform the Bonferroni-Wald test. Nagakura (2009a)’s modified LN test statistic is designed to converge in distribution under to the standard normal irrespective of the value, under the data generating mechanism with fixed (i.e., independent of ). Because Nagakura (2009a) did not show its asymptotic null distribution remains standard normal when , we do not perform it for the case . We also consider the test proposed recently by Horváth and Trapani (2019) (hereafter HT). The HT test is a randomized one, and their test statistic (in their notation) converges in distribution to the chi square with one degree of freedom, for almost all realizations.999The HT test needs a tuning parameter, , to be performed, and they stated their test’s performance is insensitive to the choice of the value and set . However, in our simulation, their test’s performance is somehow affected by the choice of . Thus, we set , to obtain simulation results similar to those of HT. The HT test is not originally proposed under the local-to-unity specification, but it will be informative to practitioners to reveal the performance of the test under this setting.

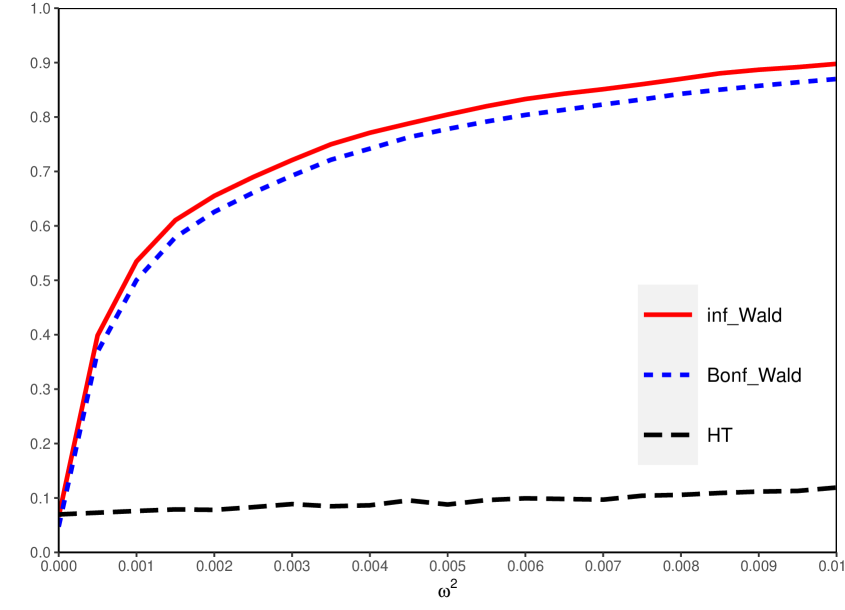

The simulation results are shown in Figures 7 through 10. For the case , where all but the LN test are performed, the infeasible and Bonferroni-Wald tests have good power, and the discrepancy between their power functions is small. The latter result is due to the refinement on the construction of the confidence interval for . In contrast, the power function of the HT test stays around the nominal level 0.05 over , which implies it has almost no distinguishing power for these alternatives. Indeed, HT conjectured (based on some theoretical analysis) that their test would have no power when and , which is of larger magnitude than our local-to-zero variance .101010Nishi and Kurozumi (2022) showed that under the STUR specification, the LN and some other tests are consistent when , from which they concluded that this case should be regarded as capturing stochastic “moderate” departures from a unit root rather than local departures. Our simulation results corroborate their statement.

Turning to the cases , it is noticeable that for each , the LN test performs well for small values of , but Wald type tests outperform the LN test otherwise. In particular, the greater value of leads to the greater dominance by the Wald type tests. The power function of HT test, again, stays around the nominal level for these cases. Overall, the Bonferroni-Wald test performs better than the LN and HT tests for moderate to large values of (irrespective of the value) and performs almost as efficiently as its ideal, infeasible counterpart.

5 Empirical Application

In this section, we apply the Bonferroni-Wald test along with the LN and HT tests111111Based on our simulation results, we set the tuning parameter for the HT test. to several U.S. macroeconomic and financial time series, following Hill and Peng (2014) and HT. The dataset includes CPI, real GDP, industrial production, M2, S&P500, the 3 month Treasury bill rate and the unemployment rate. We take the logarithm of the first 5 series before detrending all the series. All data have been extracted from Federal Reserve Economic Data. The data description and testing results are displayed in Tables 2 and 3, respectively.

Before discussing main results, it should be recalled from our simulation results that the Bonferroni-Wald test can be oversized when is not large, is large and is near unity (see Section 4). Thus, we need to check whether all the three conditions hold for our series or not. According to Table 3, all the estimates are near unity, as expected. We also have obtained moderate estimates of for the CPI and S&P500 series, but the sample sizes for them are large enough that it is unlikely the Bonferroni-Wald test is oversized for these series. As for GDP, the sample size is but the estimate is near zero, and hence we expect the Bonferroni-Wald test is not severely oversized for this series. Overall, all the three conditions for the potential oversize problem do not jointly hold.

For GDP and T-bill rate, we have obtained consistent results from all the three tests: the null of is not rejected for these series. This coincidence could be viewed as evidence for nonrandomness of the autoregressive root for these series. As for CPI, industrial production and S&P500, it is observed that the Bonferroni-Wald and LN tests reject the null while the HT test does not. This result will be attributed to the fact that the former two tests are much more powerful than the latter one. Finally, as for M2 and unemployment rate, only the Bonferroni-Wald test rejects the null. This outcome will be due to the fact that the Bonferroni-Wald test tends to be the most powerful among the three tests.

In Table 3, we also present the estimates proposed by Horváth and Trapani (2019) (denoted by ). They showed this estimator is consistent under the non-local RCA models (with and fixed). The values of seem to support our testing results. For instance, we have a negative for T-bill rate, for which none of the tests reject the null. Moreover, for the other series, takes values around to , magnitudes of the coefficient randomness with which the HT test tends to be powerless under the sample size given in Table 3. For example, for M2, the sample size is , and is , translating into estimate of the localizing coefficient . According to our simulation results, the HT test has almost no power against the alternative of this magnitude, hence the testing result given in Table 3.

Given these findings, our empirical application illustrates the merit in choosing our Bonferroni-Wald test over existing ones.

6 Conclusion and Discussion

Given the results of empirical analyses conducted by earlier studies, the local-to-unity RCA models, which extend the STUR modelling, are empirically relevant. Under this setting, we can analyze the effect of the correlation between the random coefficient and disturbance on the power properties of tests for coefficient randomness. Theoretical and simulation analyses reveal that tests proposed by earlier studies can perform poorly when the degree of the correlation is moderate to large and the coefficient randomness is local to zero, while the augmented-Wald test we have proposed performs well even in such cases. Our test is also independent of the nuisance parameter , the correlation between the disturbance and its square, so that it is implementable without the knowledge about the value of . To deal with the uncertainty about the mean of the autoregressive root, we have proposed using a confidence interval for , leading to the Bonferroni-Wald test, where the significance level for the confidence interval is selected according to the value of the estimate. Embedding this selection process into the Bonferroni-Wald test helps stabilize the test’s size and improve the test’s power.

Several directions for future research are possible. First, from the similarity in the construction of test statistics between our model and predictive regressions, it is expected that the theory developed by numerous studies on predictive regressions can be applied to testing for coefficient randomness in local-to-unity autoregressions. For example Phillips and Lee (2013, 2016) proposed the use of the so-called IVX procedure for predictability testing (see also Kostakis et al., 2015). This procedure leads to good size and power properties and also requires less computational burden for implementation than the Bonferroni approach employed by Campbell and Yogo (2006). The use of the IVX approach may facilitate testing for coefficient randomness in local-to-unity autoregressions. The analysis of tests’ performance when is distant from unity will also be of interest. In such a case, more preferable tests might be available than the Bonferroni-Wald test, which is based on the local-to-unity asymptotics.

References

- (1)

- Aue and Horváth (2011) Aue, A. and L. Horváth (2011) Quasi-Likelihood Estimation in Stationary and Nonstationary Autoregressive Models with Random Coefficients. Statistica Sinica, 21 (3), 973–999.

- Campbell and Yogo (2006) Campbell, J. Y. and M. Yogo (2006) Efficient Tests of Stock Return Predictability. Journal of Financial Economics, 81 (1), 27–60.

- Cavanagh et al. (1995) Cavanagh, C. L., G. Elliott, and J. H. Stock (1995) Inference in Models with Nearly Integrated Regressors. Econometric Theory, 11 (5), 1131–1147.

- Distaso (2008) Distaso, W. (2008) Testing for Unit Root Processes in Random Coefficient Autoregressive Models. Journal of Econometrics, 142 (1), 581–609.

- Elliott et al. (1996) Elliott, G., T. J. Rothenberg, and J. H. Stock (1996) Efficient Tests for an Autoregressive Unit Root. Econometrica, 64 (4), 813–836.

- Hansen (1992) Hansen, B. E. (1992) Convergence to Stochastic Integrals for Dependent Heterogeneous Processes. Econometric Theory, 8 (4), 489–500.

- Hill and Peng (2014) Hill, J. and L. Peng (2014) Unified Interval Estimation for Random Coefficient Autoregressive Models. Journal of Time Series Analysis, 35 (3), 282–297.

- Horváth and Trapani (2019) Horváth, L. and L. Trapani (2019) Testing for Randomness in a Random Coefficient Autoregression Model. Journal of Econometrics, 209 (2), 338–352.

- Horváth and Trapani (2022) Horváth, L. and L. Trapani (2022) Changepoint Detection in Heteroscedastic Random Coefficient Autoregressive Models. Journal of Business & Economic Statistics (forthcoming).

- Hwang and Basawa (2005) Hwang, S. Y. and I. V. Basawa (2005) Explosive Random-Coefficient AR(1) Processes and Related Asymptotics for Least-Squares Estimation. Journal of Time Series Analysis, 26 (6), 807–824.

- Kostakis et al. (2015) Kostakis, A., T. Magdalinos, and M. P. Stamatogiannis (2015) Robust Econometric Inference for Stock Return Predictability. The Review of Financial Studies, 28 (5), 1506–1553.

- Lee (1998) Lee, S. (1998) Coefficient Constancy Test in a Random Coefficient Autoregressive Model. Journal of Statistical Planning and Inference, 74 (1), 93–101.

- Leybourne et al. (1996) Leybourne, S. J., B. P. M. McCabe, and A. R. Tremayne (1996) Can Economic Time Series Be Differenced to Stationarity? Journal of business & economic statistics, 14 (4), 435.

- McCabe and Smith (1998) McCabe, B. P. M. and R. J. Smith (1998) The Power of Some Tests for Difference Stationarity under Local Heteroscedastic Integration. Journal of the American Statistical Association, 93 (442), 751–761.

- McCabe and Tremayne (1995) McCabe, B. P. M. and A. R. Tremayne (1995) Testing a Time Series for Difference Stationarity. The Annals of Statistics, 23 (3), 1015–1028.

- Nagakura (2009a) Nagakura, D. (2009a) Testing for Coefficient Stability of AR(1) Model When the Null Is an Integrated or a Stationary Process. Journal of Statistical Planning and Inference, 139 (8), 2731–2745.

- Nagakura (2009b) Nagakura, D. (2009b) Asymptotic Theory for Explosive Random Coefficient Autoregressive Models and Inconsistency of a Unit Root Test against a Stochastic Unit Root Process. Statistics & Probability Letters, 79 (24), 2476–2483.

- Nicholls and Quinn (1982) Nicholls, D. F. and B. G. Quinn (1982) Random Coefficient Autoregressive Models: An Introduction, 11 of Lecture Notes in Statistics, New York, NY Springer US.

- Nishi and Kurozumi (2022) Nishi, M. and E. Kurozumi (2022) Stochastic Local and Moderate Departures from a Unit Root and Its Application to Unit Root Testing.Technical Report 2022-02, Graduate School of Economics, Hitotsubashi University.

- Phillips (1987) Phillips, P. C. B. (1987) Towards a Unified Asymptotic Theory for Autoregression. Biometrika, 74 (3), 535–547.

- Phillips (2014) Phillips, P. C. B. (2014) On Confidence Intervals for Autoregressive Roots and Predictive Regression. Econometrica, 82 (3), 1177–1195.

- Phillips and Lee (2013) Phillips, P. C. B. and J. H. Lee (2013) Predictive Regression under Various Degrees of Persistence and Robust Long-Horizon Regression. Journal of Econometrics, 177 (2), 250–264.

- Phillips and Lee (2016) Phillips, P. C. B. and J. H. Lee (2016) Robust Econometric Inference with Mixed Integrated and Mildly Explosive Regressors. Journal of Econometrics, 192 (2), 433–450.

- Phillips and Ouliaris (1990) Phillips, P. C. B. and S. Ouliaris (1990) Asymptotic Properties of Residual Based Tests for Cointegration. Econometrica, 58 (1), 165–193.

- Stock (1991) Stock, J. H. (1991) Confidence Intervals for the Largest Autoregressive Root in U.S. Macroeconomic Time Series. Journal of Monetary Economics, 28 (3), 435–459.

- Su and Roca (2012) Su, J.-J. and E. Roca (2012) Examining the Power of Stochastic Unit Root Tests without Assuming Independence in the Error Processes of the Underlying Time Series. Applied Economics Letters, 19 (4), 373–377.

Appendix A: Procedure to Determine Values for the Bonferroni-Wald Test

In this appendix, we describe the procedure to determine the values for the confidence interval for explained in Section 3. The procedure is based on simulating asymptotic distributions with 5,000 replications. In each replication, we first generate by the mechanism

| (A.1) |

with , , and . Then, with given , we conduct the two-step procedure for the Bonferroni-Wald test explained in Section 3 and calculate the frequency of being rejected for the .

Note that used in (A.1) satisfies . To calculate the false rejection frequencies for other values, we artificially produce an environment where the Wald test statistic depends on . Noting that under the null,

and (combined with ) determines the value of on which the asymptotic distribution of depends, we artificially replace with , obtaining

in view of the distributional equivalence and the fact that and . In this replacement, the newly crafted variable takes over the role of , satisfying , and by construction. This replacement can be justified by the fact that under the null, the Wald test statistic asymptotically depends only on (and ) and is not dependent on any other moment. It follows that the Bonferroni-Wald test statistic using in place of asymptotically depends on , so that we can calculate the false rejection frequencies for any value of .

For each on some grid, we calculate the false rejection rates of the Bonferroni-Wald test with moving over a grid on and determine the value of for the given such that the false rejection rate is less than or equal to 0.05 for all .

Appendix B: Proofs of Results in Section 2

In this appendix, we prove the theorems stated in Section 2.

Lemma B.1.

Proof. The proof is essentially the same as that of Lemma 1(a) of Nishi and Kurozumi (2022) and hence is omitted. ∎

Proof. The proofs of parts (a) and (b) are identical to those of Lemma 1(b) and (c) of Nishi and Kurozumi (2022) and hence are omitted. To prove part (c), it suffices to show

A simple calculation gives

where

The first term of satisfies

say, because is i.i.d with zero mean and finite variance. Similarly, we can prove that the other terms of is . Thus

∎

For later reference, we give several results on the weak convergence of components of test statistics.

Lemma B.3.

Proof. For part (a), a straightforward calculation gives

where

| and | ||||

It is straightforward to show , using Lemma B.1 and Theorem 2.1 of Hansen (1992). As for , we have

where the last convergence follows from Lemma B.1 and the continuous mapping theorem (CMT). By a similar argument, we obtain

Therefore, we arrive at

as desired.

Part (b) can be proven in a similar fashion. Write as

where , , and . Then, it is straightforward to show

| and | ||||

Combining the above results completes the proof of part (b).

To prove part (c), we define and write as

| (B.1) |

The first term of (B.1) becomes

The second term of (B.1) satisfies

| (B.2) |

Hence, we obtain , as desired.

To prove part (d), let . Then, is expressed as

which yields

| (B.3) |

where , , and . Since is , we have already proven in part (c) that

| (B.4) |

In view of equation (8), becomes

As for the first term of , we have

We can also show that the second term of is in the same way as we did in (B.2). Thus, we get

| (B.5) |

Lastly, becomes

| (B.6) |

Substituting (B.4) through (B.6) into (B.3) and applying Lemma B.2, we deduce

∎

Proof of Theorem 2. First, by Lemma B.3(c) and the CMT, the denominator of divided by becomes

where and . Next, applying Lemma B.3, the numerator of divided by is seen to satisfy

Combining the above results gives

To derive the asymptotic distribution of , note that

Then, applying Lemma B.3 and the CMT, we get

completing the proof. ∎

To prove Theorem 3, we use the following lemma.

Proof. To prove part (a), note that

where and . By Lemma B.3(a), satisfies

As for , a straightforward calculation yields

Hence, we obtain

in view of (3). This proves part (a). The proof of part (b) is similar and thus is omitted. ∎

Proof of Theorem 3. The proof for is essentially the same as that of Theorem 1 except that we consider in the numerator of the test statistic. Dividing both the numerator and denominator by and applying Lemma B.4(a) leads to the desired result. The proof for the augmented tests goes along the same lines as those of Theorem 2 if we replace with and apply Lemmas B.3(d) and B.4. ∎

Appendix C: Proofs of Results in Section 3

In this appendix, we prove the asymptotic results mentioned in Section 3: namely, the asymptotic distribution of and the consistency of , and .

Proof. From the definition of , we have

∎

Proof. As for part (a), satisfies

for which we have , by Lemma C.1 and the CMT, and

Therefore

given Lemma B.2(a).

To prove part (b), write as

| (C.1) |

The first term is

Straightforward calculations reveal

which gives

Substituting this and into (C.1), we arrive at

by Lemma B.2(b).

To prove part (c), it suffices to show , given that and . Now, we have

in view of the last line of the proof of Lemma B.2(c). ∎

| 0.09 | 0.42 | ||

| 0.17 | 0.38 | ||

| 0.23 | 0.35 | ||

| 0.31 | 0.31 | ||

| 0.38 | 0.26 | ||

| 0.45 | 0.22 | ||

| 0.5 | 0.17 | ||

| 0.48 | 0.11 | ||

| 0.46 | 0.05 | ||

| 0.44 | |||

-

a.

Entries in the second and fourth columns are the significance level of the equal-tailed confidence interval for when the significance levels of the Bonferroni-Wald test () and individual modified Wald test () are 0.05.

-

b.

To determine the value for the interval , we actually computed type 1 errors over .

| Series | Frequency | Sample period | |

|---|---|---|---|

| CPI (1982-1984=100) | Monthly | Jan. 1913-Dec. 2019 | 1284 |

| Real GDP (2012 chained) | Quarterly | Q1 1947-Q4 2019 | 292 |

| Industrial production (2017=100) | Monthly | Jan. 1919-Dec. 2019 | 1212 |

| M2 | Weekly | Nov. 3, 1980-Dec. 30, 2019 | 2044 |

| S&P 500 | Daily | Dec. 3, 2012-Dec. 31, 2019 | 1782 |

| 3 month T-bill rate | Daily | Dec. 3, 2012-Dec. 31, 2019 | 1770 |

| Unemployment rate | Monthly | Jan. 1948-Dec. 2019 | 864 |

| Series | Bonf-Wald | LN () | HT () | ||||

| CPI | 1284 | 0.999 | 0.211 | Yes | Yes | - | |

| GDP | 292 | 0.994 | -0.065 | - | - | - | |

| Industrial production | 1212 | 0.998 | 0.054 | Yes | Yes | - | |

| M2 | 2044 | 0.995 | 0.066 | Yes | - | - | |

| S&P 500 | 1782 | 0.984 | -0.258 | Yes | Yes | - | |

| T-bill rate | 1770 | 0.999 | 0.108 | - | - | - | |

| Unemployment rate | 864 | 0.993 | 0.142 | Yes | - | - |

-

•

For entries in the last three columns, “Yes” (“-”) signifies the rejection (nonrejection) of the null by the corresponding test with 5% significance level.

(The values in the parentheses denote the values of .)