Distributionally Robust Optimization under Mean-Covariance Ambiguity Set and Half-Space Support for Bivariate Problems

Abstract

In this paper, we study a bivariate distributionally robust optimization problem with mean-covariance ambiguity set and half-space support. Under a conventional type of objective function widely adopted in inventory management, option pricing, and portfolio selection, we obtain closed-form tight bounds of the inner problem in six different cases. Through a primal-dual approach, we identify the optimal distributions in each case. As an application in inventory control, we first derive the optimal order quantity and the corresponding worst-case distribution, extending the existing results in the literature. Moreover, we show that under the distributionally robust setting, a centralized inventory system does not necessarily reduce the optimal total inventory, which contradicts conventional wisdom. Furthermore, we identify two effects, a conventional pooling effect, and a novel shifting effect, the combination of which determines the benefit of incorporating the covariance information in the ambiguity set. Finally, we demonstrate through numerical experiments the importance of keeping the covariance information in the ambiguity set instead of compressing the information into one dimension.

keywords:

robustness and sensitivity analysis , distributionally robust optimization , bivariate moment problem , mean-covariance ambiguity set , newsvendorWGMwgm\xspace \csdefQEqe\xspace \csdefEPep\xspace \csdefPMSpms\xspace \csdefBECbec\xspace \csdefDEde\xspace \usetikzlibraryshadows

[inst1]organization=School of Information Management and Engineering, Shanghai University of Finance and Economics,city=Shanghai, postcode=200433, country=P.R. China

[inst2]organization=School of Data Science, The Chinese University of Hong Kong, Shen Zhen,city=Shenzhen, Guangdong, postcode=518172, country=P.R. China

[inst3]organization=University of Science and Technology of China,city=Hefei, Anhui, postcode=230026, country=P.R. China

1 Introduction

In recent years, distributionally robust optimization (DRO) has become a popular approach to address optimization problems affected by uncertainty. Its applications have received considerable attention in various fields including economics, management science, and mathematical finance [3]. The appeal of distributionally robust optimization lies in its flexibility in specifying uncertainty beyond a fixed probability distribution, as well as in its ability to produce computationally tractable models [8]. We refer the readers to [34, 12, 17, 5, 35] for some comprehensive reviews for DRO problems.

The problem studied in distributionally robust optimization is as follows:

| (1) |

where is the realization of the uncertainty, is the decision taken before the realization, and is the objective function. Given the decision , the inner problem of (1) evaluates the worse-case objective:

| (2) |

where the ambiguity set, denoted by , characterizes a set of possible distributions may follow. In the literature, various characterizations of ambiguity set have been considered, such as support [14, 28], moments [34, 2], shape [29], and dispersions [20]. Among them, one of the most classical ambiguity sets is the mean-covariance ambiguity set given as follows:

| (3) |

where , are the mean and covariance of the distribution and is the support. If or , then we call the support of half-space or full-space respectively. The key advantage of the mean-covariance ambiguity set lies in its simplicity and computational tractability, especially under the full-space support. Generally speaking, the computational complexity of DRO problem depends on the complexity of solving the inner problem, which is a semi-infinite linear program on its probability measure, and NP-hard in general [2].

In this paper, we consider a class of widely-adopted loss functions for the inner problem as follows:

| (4) |

with , and . Such a loss function is adopted in a wide range of applications, including inventory management [34, 11], option pricing [28, 38, 41, 1], and portfolio selection [10, 27, 26, 40]. Regarding the ambiguity set, we focus on the mean-covariance ambiguity set, which is a common choice and has been studied in every application listed above (see, for instance, [28, 7, 34, 1, 38]). Furthermore, we consider the problem under the half-space support, which is of relevance under many situations (e.g., nonnegative demand in inventory control [18], nonnegative losses in a stop-loss contract [38]). Moreover, by incorporating the half-space information, the ambiguity sets shrink, resulting in a less conservative optimal solution.

However, for problems with a mean-covariance ambiguity set, the methodology for solving the DRO problem under half-space support is less well-studied than that under full-space support. Specifically, when considering the problems with objectives of a linear reward function under the full-space support, Popescu demonstrates a powerful projection property that can translate an dimensional multivariate inner problem into an equivalent univariate problem [30]. Unfortunately, it is not easy to incorporate half-space support information in such an approach. In fact, as shown in [1], even determining the feasibility of such a problem under half-space support is NP-hard. Therefore, given mean and covariance information, much research on incorporating half-space support into DRO focus on approximation algorithms. For example, Rujeerapaiboon et al. [33] study the upper Chebyshev bound of a product of non-negative random variables given their first two moments. They show that in order to obtain a tractable numerical procedure, the first two moments should follow a permutation-symmetric structure. Kong et al. [22] formulate a semidefinite programming relaxation for the appointment scheduling problem given the mean and covariance information for the nonnegative random service time variables. Natarajan et al. [28] provide a mathematically tractable lower bound for the expected piecewise linear utility function by taking a convolution of two problems that are computationally simple through relaxing either the half-space support to the full-space or the mean-covariance ambiguity set to the one with only mean information.

In this paper, we further shed light on the DRO problem under mean-covariance ambiguity set and half-space support. Particularly, we are able to derive an analytical solution to such a problem for the two-dimensional case. Two-dimensional problem has been extensively studied in the literature, as it is simple and useful to illustrate the relation between the optimal decisions and the correlations of two random variables. For example, two-dimensional problems are considered in the variations of newsvendor model including dual sourcing [39], two markets [23], and two products [24, 25]. Moreover, the stop-loss problem in option pricing typically involves two types of losses (i.e., property losses and liability losses) [38]. As far as we know, it is computationally challenging even to solve two-dimensional DRO problems with mean-covariance ambiguity set under half-space support. Specifically, a typical approach to solving those problems under half-space support is to relax the support to the full-space [18, 9, 1]. Moreover, as the projection theorem [30] cannot be applied to those problems, both works [9, 1] obtain numerical solutions to the relaxed problems. Govindarajan et al. achieve analytical solutions to the relaxed problem under strong assumptions [18]. Unlike the relaxation of the support, Tian relaxes the two-dimensional problem into a univariate one and applies the moment approach [38]. To sum up, the analytical result of a two-dimensional problem with mean-covariance ambiguity set under half-space support is largely missing in the literature, and our work fills in the gap with a conclusive answer.

We summarize the contributions of this paper as follows:

-

1.

We propose an analytical solution for the two-dimensional DRO problem with mean-covariance ambiguity set and loss function under half-space support. Specifically, the optimal value of this problem can be characterized by six different cases. To obtain the optimal solution in each case, we extend the primal-dual approach in [19], designed for the univariate moment problems, to our two-dimensional problems.

-

2.

We extend the loss function defined in (4) to a generalized multi-piece quadratic objective function and provide a semi-definite programming reformulation for the DRO problem with mean-covariance ambiguity set and the generalized loss function.

-

3.

We apply our analytical result to inventory control problems, providing the optimal order quantity and the worst-case distribution, which is an extension of the result in [34]. Moreover, we find that under the DRO setting with mean-covariance ambiguity set, inventory pooling does not necessarily reduce the optimal total inventory, which contradicts with the conventional wisdom that pooling can reduce the total inventory. Furthermore, we identify two effects, a conventional pooling effect and a novel shifting effect, which together determine the benefit of incorporating the covariance information in the ambiguity set. Finally, we demonstrate through numerical experiments the importance of keeping the covariance information in the ambiguity set, instead of compressing the information in one dimension.

The rest of this paper is organized as follows. In Section 2, we introduce our model. In Section 3, we formally present the bivariate moment problem and its closed-form solution. We also demonstrate some properties of the worst-case distribution and provide a numerical approach for the generalized objectives. In Section 4, we study an inventory control problem as the outer problem and provide some managerial insights for adopting the mean-covariance DRO model for such problems compared to other approaches. We conclude the paper and point out some future research directions in Section 5.

2 Model

Consider the following distributionally robust optimization problem

| (5) |

with feasible region , ambiguity set , and loss function . The loss function depends both on the decision vector and the random vector .

We first investigate the inner worst-case expectation problem. For ease of notation, we suppress the dependence on the decision variable . Specifically, we consider the inner worst-case expectation problem of the form

| (6) |

where the loss function is a convex piecewise linear function with the following form

and is a nonnegative coefficient of the random vector . The ambiguity set of the distribution consists of nonnegative random vector with given mean and second-order moment , that is

| (7) |

The problem of form (6) is widely adopted in DRO. We provide the following two applications as examples.

Example 1. (Multi-dimensional Newsvendor Problem)

We consider a multi-dimensional distributionally robust newsvendor problem in a centralized inventory management setting (see [4]) as follows:

| (8) |

where we denote in the rest of this paper. Specifically, and are the order quantity and the critical ratio respectively, and represents the pooling of uncertain demands. Obviously, the worst-case expectation of the inner problem can be considered as a special case of problem (6) with , , and .

Example 2. (Mean-CVaR Portfolio Selection Problem)

We consider a capital market consisting of assets whose uncertain returns are captured by an dimensional random vector . A portfolio is encoded by an dimensional vector which has to satisfy some constraints . The distributionally robust mean-CVaR portfolio selection problem can be formulated as follows:

or equivalently,

where the equivalence is formally proved in [32]. Again, the worst-case expectation of the inner problem can be considered as a special case of problem (6) with , , and .

Without loss of generality, we assume in the rest of this paper. Otherwise, supposing , the loss function can be reduced to a linear function . As a result, problem (6) has a trivial solution as

In fact, with this assumption, we can simplify the formulation of problem (6) by the following proposition.

Proposition 1.

Suppose . We can reformulate the problem in (6) as follows:

with the transformed random variable and the transformed ambiguity set

where the notation denotes the Hadamard product.

This proposition demonstrates that it is sufficient to solve the simplified problem in the form of

| (9) |

so as to solve the original problem (6) with . We relegate the proof of Proposition 1 to Appendix A.

Generally speaking, even determining the feasibility of problem (9) is NP-hard as shown in [1]. For univariate case (), Scarf derives a closed-form solution in [34], which we state below for completeness.

Lemma 1 ([34]).

Let the ambiguity set .

-

1.

If , then the optimal value is

(10) with an optimal distribution .

-

2.

If , then the optimal value is

(11) with an optimal distribution , where .

3 Bivariate Moment Problem

In this section, we study the bivariate case () of problem (9) stated as follows:

| (12) |

where represents the moment information of random variables and . For simplicity, we denote for the rest of this paper, and consider the ambiguity set

| (13) |

Thus, we have the correlation and the covariance matrix

| (14) |

The nonemptyness of ambiguity set requires that the covariance matrix be positive semi-definite, which means , and . Note that and thus . To exclude trivial cases, we focus on . In all, without loss of generality, we assume that our input parameters satisfy the following assumption in the remaining part of this paper.

Assumption 1.

We assume , , and .

Next, we present the closed-form solution for the bivariate moment problem (12).

3.1 Closed-Form Solution

Before establishing our closed-form solution, we first define three terms that will be frequently used in this subsection:

In the following lemma, we present the conditions that correspond to six different optimal values of problem (12). Specifically, this lemma shows that such six conditions divide the feasible region into six disjoint sets.

Lemma 2.

Every feasible input of satisfies one and only one of the six conditions in the following table.

| Condition 1 | Condition 2 | Condition 3 | Condition 4 | Condition 5 | Condition 6 |

where and .

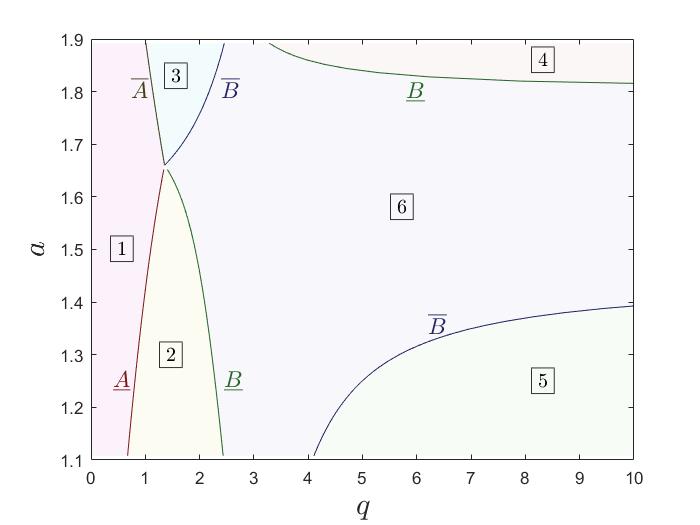

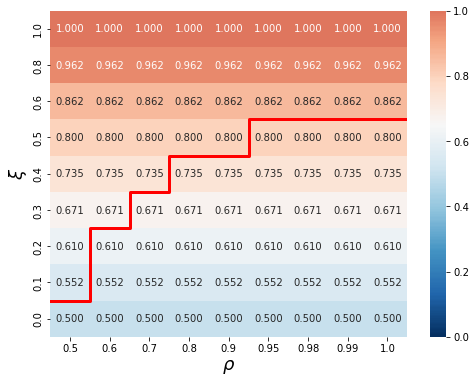

We relegate the proof of this lemma to Appendix B.1. Below we provide a sample plot as a graphical illustration.

Specifically, we plot Figure 1 with and , when ranging and over and respectively. Figure 1 shows that the feasible region can be divided into six disjoint subsets, where borderlines are in the form of , , , , and that are functions of input defined in the proof of this lemma, see equation (B.5) in Appendix B.1.

For each condition, the following theorem presents a closed-form optimal value of the bivariate moment problem (12).

Theorem 1.

Given a non-empty ambiguity set and , the optimal value can be characterized as

We relegate the proof of this theorem to Appendix B. In this theorem, we characterize the optimal value of problem (12) by six different cases. To obtain the optimal distributions, we extend the primal-dual approach in [19], designed for the univariate moment problems, to our two-dimensional problems, and successfully identify a corresponding optimal distribution for each case stated in Lemma B.2.1-B.2.6.

There are several interesting observations of the optimal values in Theorem 1. First of all, the optimal value under condition 6 is the same as that in a univariate pooling problem. Specifically, let and we consider the univariate problem with the ambiguity set

We can verify that the optimal value under condition 6 is the same as that in this univariate pooling problem via (11) in Lemma 1.

Secondly, the optimal value under condition 2 and that under condition 3 are symmetric through replacing by and by . This symmetric property also applies to the optimal values under condition 4 and condition 5, while the optimal values under condition 1 and condition 6 are self-symmetric.

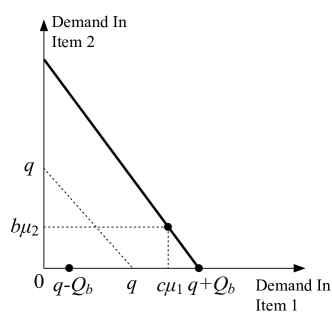

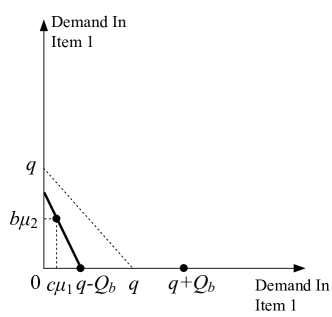

With respect to the optimal distributions, from Lemma B.2.2 and Lemma B.2.4 in Appendix B, we can see that the optimal distributions under condition 2 and condition 4 share the same formulation, though their optimal values are different. Specifically, both optimal distributions are in the form of

To illustrate, we plot the optimal distribution under condition 2 in Figure 2(a).

The points on the solid line together with are potential points in the optimal support, as they satisfy the complementary slackness conditions. In addition, condition 2 indicates that , so the objective value at point is strictly positive with . We also plot the optimal distribution under condition 4 in Figure 2(b). This condition indicates that , which implies a zero objective value at . In short, affects the objective value under condition 2 but not under condition 4.

In fact, the optimal distributions in other conditions can also be interpreted similarly. Note that the optimal distributions under conditions 3 and 5 also share the same formulation, as they are symmetric to those under condition 2 and condition 4 respectively. Furthermore, notice that the optimal distribution under condition 2 becomes invalid under condition 1, because , which contradicts the non-negativity of random variables. When shrinks from above to below , condition 2 is switched to condition 1, which is consistent with the illustration in Figure 1 with crossing . Consequently, the optimal distribution under condition 1 always takes in its optimal support from Lemma A.1. Lastly, as the optimal value under condition 6 is the same as that in the univariate pooling problem, it is not surprising to see each support point of optimal distributions lay on either or from Lemma B.2.6, which is consistent with the supporting points of the univariate pooling problem via (11) in Lemma 1.

3.2 Extension of the Loss Function

Beyond the two-piecewise linear objectives, recent literature also considers the multi-piece quadratic loss functions in newsvendor models [15, 16]. Specifically, quadratic losses are used to measure the cost severity of critical perishable commodities [15]. Moreover, such multi-piece quadratic functions are also employed in the robust portfolio selection problem to represent the lower partial moment as a measure of risk [7].

In this subsection, we study the bivariate moment problem under half-space support with a multi-piece quadratic objective function. As it is computationally challenging to obtain such a solution in closed form, we propose a numerical approach to solve this problem. Specifically, we provide a semi-definite programming (SDP) formulation by applying the sum-of-squares technique [31] to our dual problem. We relegate the proof to Appendix C.

Proposition 2.

Given a random vector with its ambiguity set defined in (13) and a matrix of coefficients for a piece-wise quadratic objective, we denote each piece as follows:

for . The following bivariate moment problem

can be solved by an SDP:

with and the matrix defined as follows:

where are the th column vectors of matrices , , respectively.

As far as we know, it is mathematically challenging to obtain an exact reformulation for piece-wise polynomial objectives with either a higher degree or more than two variables. This is because the sum-of-squares technique may no longer apply in these settings. Specifically, each dual constraint of our problem is to ensure that the corresponding polynomial is non-negative. Indeed, our analysis uses the result by Hilbert in 1888, who showed in [21] that every non-negative polynomial with variables and degree could be represented as sums of squares of other polynomials if and only if either or or and . Note that the formulation of our proposition is a bivariate polynomial () with fourth-order (). Therefore, the sum of squares technique can be applied. Similar challenges for a higher degree or more than two variables are also presented by Bertsimas and Popescu, who briefly review the computational tractability in moment problems [2].

4 The Bivariate Newsvendor Problem

In the previous section, we provided a closed-form solution for the inner bivariate moment problem. In this section, we study the outer DRO problem. Specifically, we consider the DRO newsvendor problem as follows:

| (15) |

where is the mean-covariance ambiguity set in (13), and the critical ratio is a given constant in .

In the following, we first propose an approach to solve this problem in Section 4.1, which also reveals the relation between the optimal order and the moment parameter in an analytical form. In Section 4.2, we analyze the benefit of incorporating the covariance information into the ambiguity set, as well as the impact on the total inventory. In Section 4.3, we show that it is important to keep the covariance information instead of compressing such information into one dimension.

4.1 Optimal Order Quantity

We introduce the following procedure in the box below to solve problem (15). In terms of the computational techniques to solve in (16), we first note that each essentially corresponds to an interval of , which can be solved from a quadratic equation. As a result, we obtain each in a closed form shown in Table B.2 in Appendix B.1. Furthermore, we note that is the sum of a linear term and a square root of a quadratic term of , which is strictly convex in . Therefore, it is not difficult to obtain the unique stationary points of (16) shown in Appendix E. Since an optimal solution locates at either a stationary point or a boundary point of the interval , (16) can be solved explicitly. To summarize, this framework is capable of solving the optimal order systematically.

1. Identify local solutions separately: for each condition of the six conditions in Theorem 1, solve

| (16) |

where .

2. Obtain global solutions jointly: solve

4.2 The Effects of Inventory Pooling

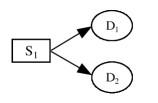

Inventory pooling is frequently employed as an operational strategy to mitigate demand uncertainty: combining inventory allows the company to decrease demand variability, cut operational costs, and boost profits, especially if the component market demands are negatively correlated [37]. The pooling strategy often results in a centralized inventory system [4, 13, 36]. We illustrate the difference between centralized and decentralized structures of inventory systems through Figure 3. In Figure 3(a), we show a single supplier serving two demand streams, which we call the centralized system; in Figure 3(b), we show two suppliers deciding order quantities separately, which we call the decentralized system.

From the perspective of pooling, we consider our model in (15) as a bivariate centralized model (BCM). In the following, we compare the centralized model with the decentralized model. We first denote individual ambiguity sets of demands and by

as the marginal ambiguity sets of in (15). Note that these marginal ambiguity sets neglect the covariance information in the original ambiguity set . Now we are ready to propose the bivariate decentralized model (BDM) as follows:

| (17) |

where and are the optimal values of

respectively. Note that we can decompose the BDM to be the sum of two marginal univariate DRO problems, i.e.,

Therefore, the optimal solution of the BDM can be obtained through applying Scarf’s result [34] on each individual univariate problem with

for .

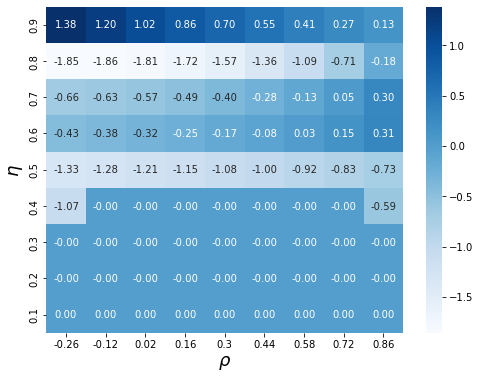

In the rest of this subsection, we compare the optimal values and optimal solutions between the BCM and the BDM. By doing so, we demonstrate the role of the correlation coefficient in the BCM over various critical ratios . With regard to the optimal values, the BCM always outperforms the BDM. Intuitively, the BDM is inclined to adopt an overly conservative decision, since this model neglects the correlation between demands. As an illustration, we plot the relative gap of optimal values between the BCM and the BDM over correlation coefficient and critical ratio in Figure 4, when fixing the other moment information with . Specifically, this relative gap is defined as the ratio:

where and are optimal values of the BCM and the BDM, respectively.

In Figure 4, it is not surprising to see is relatively large when is small. This phenomenon is consistent with the well-known pooling effect, i.e., inventory pooling can significantly reduce operational costs when demands are negatively correlated. Moreover, when is small, both models tend to accept a zero inventory so that is zero as expected.

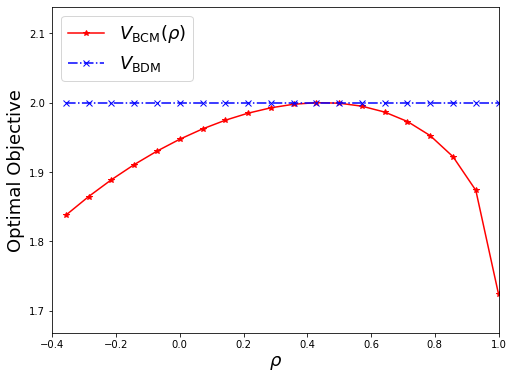

An unexpected observation is that the BCM also enjoys an advantage when is close to 1 and is in the intermediate range. This is due to another effect which we call the shifting effect. Before introducing the shifting effect, we first illustrate this observation with a concrete example through further fixing . In such a case, we obtain . For , by the method introduced in Section 4.1, we have

As shown in Figure 5,

is a concave function on 111If , then Assumption 1 will be violated. with the optimal value obtained at . The increase of over , as expected, is because of the pooling effect. On the other hand, the shifting effect dominates the pooling effect over , resulting in a decrease in the objective function of . To explain the shifting effect, we first introduce the following proposition with , whose proof is relegated to Appendix D.

Proposition 3.

Suppose that two nonnegative random variables and satisfy

and assume without loss of generality. If and are perfectly correlated with , then it must be .

From this proposition, we can see that a perfect correlation with still benefits the BCM by shifting the restriction of uncertain demand from to , which is considered as the shifting effect. Consequently, this effect tightens the ambiguity set and thus results in a less conservative decision.

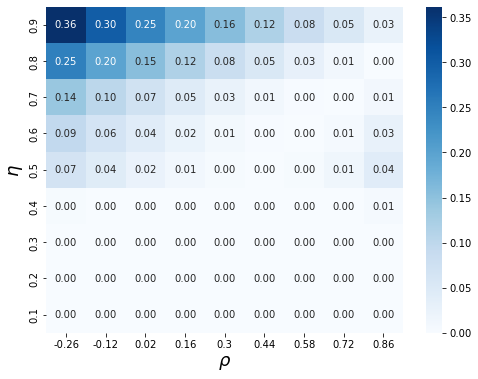

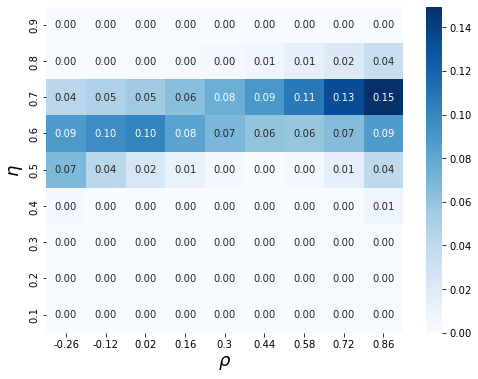

To further illustrate the shifting effect, we note that a large benefits the BCM by reducing the probability of occurrences of a small demand realization, thus tightening the ambiguity set and making the decision less conservative. As an illustration, we plot the upper bound of probability over correlation in Figure 6, when fixing the same parameters with . On the upper left of the red dividing line, the values of remain the same as . On the lower right of this red line, we observe that

and the shifting effect takes place. Besides, for , the shifting effect keeps getting stronger as the value of increases. In the extreme case when and , Figure 6(a) shows that , which verifies Proposition 3.

Another counter-intuitive observation is that a centralized system does not necessarily reduce the optimal total order quantity,

i.e., the optimal order quantity may be larger than with . We illustrate this observation in Figure 7 with the same set of moment parameters as in Figure 6. In Figure 7, a very large (e.g., ) results in the worst-case demand distribution taking condition 6 in Theorem 1. In such a case, the conventional pooling effects dominate [4, 13]. For an instance with , , the centralized optimal order , whereas the decentralized orders are and respectively and pooling indeed reduces the optimal total order quantity. However, for a medium-large , the individual optimal order quality could become 0 under sufficiently large demand uncertainty. For an instance with , the centralized optimal order , whereas the decentralized orders are and respectively. In some sense, demand pooling can reduce demand variability and smooth the change of the optimal orders along with different critical ratios , and during this process, the optimal total order quantity under the centralized system may be larger than that under the decentralized system.

4.3 The Effects of Ambiguity Pooling

For bivariate moment problems, a straightforward technique of relaxation, often considered in the literature, is to model the problem as a univariate problem [38]. Such relaxation can simplify the problem definition, reduce the solution complexity, and ease the analysis. More precisely, this technique of relaxation results in a univariate centralized model (UCM) as follows:

| (18) |

where we treat with , , and define

Unlike the BDM which neglects the covariance, the UCM compresses the uncertainty of mean and covariance into information in the one-dimensional space. We call such a maneuver ambiguity pooling.

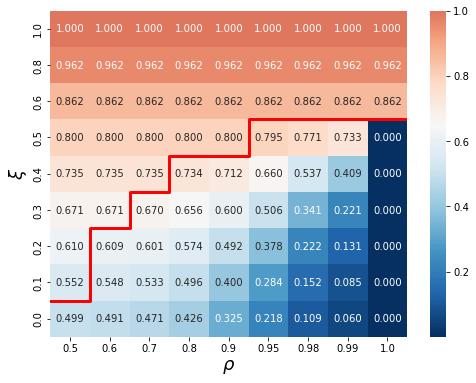

In the rest of this subsection, we demonstrate the effects of ambiguity pooling by comparing the optimal value and ambiguity sets of the BCM and the UCM. In Figure 8, we plot the relative gap between the optimal values through fixing the same part of moment parameters with .

As shown in Figure 8, the BCM enjoys a performance improvement with a medium to large . It is not surprising to see that the relative gap is zero when is small or very large: when is small, both models will adopt a zero inventory, thus the gap is zero; when is very large, condition 6 in Theorem 1 holds, resulting in the same optimal values for both models.

An essential observation is that the ambiguity pooling process may lead to a loss of information on the uncertainty under half-space support. To be precise, we consider the following ambiguity set

and the UCM can be reformulated as follows:

It is obvious that , which means the ambiguity pooling process potentially results in a more conservative decision. Next, we shall provide an example to demonstrate that the optimal distribution of problem does not belong to ; in other words, is a proper subset of . We take as an example, in which and . Based on the Scarf bound in Lemma 1, a class of optimal distributions for problem with total mass points can be described as follows:

with and for all . To show by contradiction, we first assume . Thus, the following constraints must hold for :

As a result, the second moment of must satisfy

This contradicts with . Therefore, .

Lastly, we remark that the assumption on the half-space support plays an important role in the above result. If the half-space support is replaced by the full-space support for both the BCM and the UCM, then the two models will result in the same optimal values by the projection theorem in [30].

5 Conclusion and Further Discussion

To summarize, we study a bivariate distributionally robust optimization problem with the mean-covariance ambiguity set and half-space support. For a class of widely-adopted objective functions in inventory management, option pricing, and portfolio selection, we obtain closed- form tight bounds and optimal distributions of the inner problem. Furthermore, we show that under the distributionally robust setting, a centralized inventory system does not always reduce the optimal total inventory. This contradicts with the belief that a centralized inventory system can reduce the total inventory. In addition, we identify two effects, a conventional pooling effect and a novel shifting effect. Their combination determines the benefit of incorporating the covariance information in the ambiguity set. Finally, we demonstrate the importance of keeping the covariance information in the ambiguity set instead of compressing the information into one dimension through numerical experiments.

It is worth mentioning that our result of the bivariate moment problem is also useful to derive a closed-form upper bound of the multivariate moment problem in (6) with . Such multivariate problem is known to be computationally challenging, and Natarajan et al. provide a mathematically tractable upper bound for the expected piecewise linear utility function in a numerical way [28]. In consideration of our results, we treat the -dimensional random variable as consisting of a sequence of low-dimensional random variables with and . In turn, we can decompose the ambiguity set into corresponding marginal ambiguity sets . Based on such a decomposition, we obtain an upper bound of the multivariate problem as follows:

for all possible and satisfying and . Therefore, if for all , we can provide a closed-form upper bound. In terms of numerical algorithms, we can incorporate and as two constraints to obtain a better upper bound. Note that the estimation of the covariance matrix is usually unreliable in practice if is large enough. Our approach relies on only a number of marginal well-estimated covariance submatrices, which is considered to be robust against data perturbations. On the other hand, the weakness of our approach is that we only incorporate submatrices at most. The open question is how to make more use of the covariance information so as to provide a better bound for this multivariate moment problem.

Another possible research direction is to incorporate the shape of distributions including symmetry, unimodality, or convexity into the ambiguity set in order to provide less conservative decisions appropriate to their respective scenarios, which we also leave for further study.

References

- Bertsimas and Popescu, [2002] Bertsimas, D. and Popescu, I. (2002). On the relation between option and stock prices: A convex optimization approach. Operations Research, 50(2):358–374.

- Bertsimas and Popescu, [2005] Bertsimas, D. and Popescu, I. (2005). Optimal inequalities in probability theory: A convex optimization approach. SIAM Journal on Optimization, 15(3):780–804.

- Bertsimas et al., [2019] Bertsimas, D., Sim, M., and Zhang, M. (2019). Adaptive distributionally robust optimization. Management Science, 65(2):604–618.

- Bimpikis and Markakis, [2016] Bimpikis, K. and Markakis, M. G. (2016). Inventory pooling under heavy-tailed demand. Management Science, 62(6):1800–1813.

- Breton and El Hachem, [1995] Breton, M. and El Hachem, S. (1995). Algorithms for the solution of stochastic dynamic minimax problems. Computational Optimization and Applications, 4(4):317–345.

- Casella and Berger, [2002] Casella, G. and Berger, R. L. (2002). Statistical inference. Cengage Learning.

- Chen et al., [2011] Chen, L., He, S., and Zhang, S. (2011). Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research, 59(4):847–865.

- Chen et al., [2019] Chen, Z., Sim, M., and Xu, H. (2019). Distributionally robust optimization with infinitely constrained ambiguity sets. Operations Research, 67(5):1328–1344.

- Cox et al., [2010] Cox, S. H., Lin, Y., Tian, R., and Zuluaga, L. (2010). Bounds for probabilities of extreme events defined by two random variables. Variance, 4(1):47–65.

- Doan et al., [2015] Doan, X. V., Li, X., and Natarajan, K. (2015). Robustness to dependency in portfolio optimization using overlapping marginals. Operations Research, 63(6):1468–1488.

- Doan and Nguyen, [2020] Doan, X. V. and Nguyen, T.-D. (2020). Robust newsvendor games with ambiguity in demand distributions. Operations Research, 68(4):1047–1062.

- Dupačová, [1987] Dupačová, J. (1987). The minimax approach to stochastic programming and an illustrative application. Stochastics: An International Journal of Probability and Stochastic Processes, 20(1):73–88.

- Eppen, [1979] Eppen, G. D. (1979). Note—Effects of centralization on expected costs in a multi-location newsboy problem. Management Science, 25(5):498–501.

- Ghaoui et al., [2003] Ghaoui, L. E., Oks, M., and Oustry, F. (2003). Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 51(4):543–556.

- Ghosh and Mukhoti, [2022] Ghosh, S. and Mukhoti, S. (2022). Non-parametric generalised newsvendor model. Annals of Operations Research, pages 1–26.

- Ghosh et al., [2021] Ghosh, S., Sahare, M., and Mukhoti, S. (2021). A new generalized newsvendor model with random demand and cost misspecification. In Strategic Management, Decision Theory, and Decision Science, pages 211–245. Springer.

- Gilboa and Schmeidler, [2004] Gilboa, I. and Schmeidler, D. (2004). Maxmin expected utility with non-unique prior. In Uncertainty in Economic Theory, pages 141–151. Routledge.

- Govindarajan et al., [2021] Govindarajan, A., Sinha, A., and Uichanco, J. (2021). Distribution-free inventory risk pooling in a multilocation newsvendor. Management Science, 67(4):2272–2291.

- Guo et al., [2022] Guo, J., He, S., Jiang, B., and Wang, Z. (2022). A unified framework for generalized moment problems: A novel primal-dual approach. arXiv preprint arXiv:2201.01445.

- Hanasusanto et al., [2017] Hanasusanto, G. A., Roitch, V., Kuhn, D., and Wiesemann, W. (2017). Ambiguous joint chance constraints under mean and dispersion information. Operations Research, 65(3):751–767.

- Hilbert, [1888] Hilbert, D. (1888). Über die darstellung definiter formen als summe von formenquadraten. Mathematische Annalen, 32(3):342–350.

- Kong et al., [2013] Kong, Q., Lee, C.-Y., Teo, C.-P., and Zheng, Z. (2013). Scheduling arrivals to a stochastic service delivery system using copositive cones. Operations Research, 61(3):711–726.

- Kouvelis and Gutierrez, [1997] Kouvelis, P. and Gutierrez, G. J. (1997). The newsvendor problem in a global market: Optimal centralized and decentralized control policies for a two-market stochastic inventory system. Management Science, 43(5):571–585.

- Lau and Lau, [1988] Lau, A. H.-L. and Lau, H.-S. (1988). Maximizing the probability of achieving a target profit in a two-product newsboy problem. Decision Sciences, 19(2):392–408.

- Li et al., [1991] Li, J., Lau, H.-S., and Lau, A. H.-L. (1991). A two-product newsboy problem with satisficing objective and independent exponential demands. IIE Transactions, 23(1):29–39.

- Liu et al., [2022] Liu, W., Yang, L., and Yu, B. (2022). Kernel density estimation based distributionally robust mean-CVaR portfolio optimization. Journal of Global Optimization, pages 1–25.

- Mohajerin Esfahani and Kuhn, [2018] Mohajerin Esfahani, P. and Kuhn, D. (2018). Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1):115–166.

- Natarajan et al., [2010] Natarajan, K., Sim, M., and Uichanco, J. (2010). Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 20(4):695–731.

- Popescu, [2005] Popescu, I. (2005). A semidefinite programming approach to optimal-moment bounds for convex classes of distributions. Mathematics of Operations Research, 30(3):632–657.

- Popescu, [2007] Popescu, I. (2007). Robust mean-covariance solutions for stochastic optimization. Operations Research, 55(1):98–112.

- Powers and Wörmann, [1998] Powers, V. and Wörmann, T. (1998). An algorithm for sums of squares of real polynomials. Journal of Pure and Applied Algebra, 127(1):99–104.

- Rockafellar and Uryasev, [2000] Rockafellar, R. T. and Uryasev, S. (2000). Optimization of conditional value-at-risk. Journal of Risk, 2:21–42.

- Rujeerapaiboon et al., [2018] Rujeerapaiboon, N., Kuhn, D., and Wiesemann, W. (2018). Chebyshev inequalities for products of random variables. Mathematics of Operations Research, 43(3):887–918.

- Scarf, [1958] Scarf, H. (1958). A min-max solution of an inventory problem. Studies in the Mathematical Theory of Inventory and Production.

- Shapiro and Kleywegt, [2002] Shapiro, A. and Kleywegt, A. (2002). Minimax analysis of stochastic problems. Optimization Methods and Software, 17(3):523–542.

- Su, [2008] Su, X. (2008). Bounded rationality in newsvendor models. Manufacturing & Service Operations Management, 10(4):566–589.

- Swinney, [2012] Swinney, R. (2012). Inventory pooling with strategic consumers: Operational and behavioral benefits. In Stanford University Stanford CA Working Paper.

- Tian, [2008] Tian, R. (2008). Moment problems with applications to Value-at-Risk and portfolio management. PhD thesis, Georgia State University.

- Tomlin and Wang, [2005] Tomlin, B. and Wang, Y. (2005). On the value of mix flexibility and dual sourcing in unreliable newsvendor networks. Manufacturing & Service Operations Management, 7(1):37–57.

- Zhu and Fukushima, [2009] Zhu, S. and Fukushima, M. (2009). Worst-case conditional value-at-risk with application to robust portfolio management. Operations Research, 57(5):1155–1168.

- Zuluaga et al., [2009] Zuluaga, L. F., Peña, J., and Du, D. (2009). Third-order extensions of Lo’s semiparametric bound for european call options. European Journal of Operational Research, 198(2):557–570.

Appendix A: Proof of Proposition 1

Rewrite the loss function

Let , then and . Thus, the ambiguity set of random vector is equivalent to the ambiguity set of random vector . Therefore,

Appendix B: Proof of Theorem 1

As proved in [1], problem is NP-hard for general cases. In this paper, we study the bivariate case (). Specifically, we consider the following bivariate moment problem

| (B.1) |

where and the ambiguity set is described as follows

| (B.2) |

For simplicity, we denote for the rest of the Appendix. Thus, the covariance matrix and correlation can be represented by

| (B.3) |

Note that parameters , and follow Assumption 1, which characterizes the feasibility of the primal problem (B.1). To exclude the trivial cases in which the ambiguity set only contains the distribution with a fixed single-point marginal distribution, without loss of generality, we assume that and in the remaining discussion.

Define six conditions of in Table B.1,

| Condition 1 | Condition 2 | Condition 3 | Condition 4 | Condition 5 | Condition 6 |

where and , and

For simplicity of the later proof, we denote

| (B.5) |

where

| (B.6) |

and

| (B.7) |

Note that and are symmetric if we replace by and by .

We also present four terms that will be frequently employed for the later analysis:

| (B.8) | |||

| (B.9) | |||

| (B.10) | |||

| (B.11) |

where . Because of the condition in Assumption 1, it is easy to prove that .

In Appendix B.1, we prove parameters must satisfy one and precisely one of six conditions in Table B.1. Then we provide the worst-case distributions for every condition and prove the optimality in Appendix B.2. Through the analyses of the worst-case distribution for each condition, Theorem 1 can be proved.

Appendix B.1. Proof of Lemma 2

To show that every feasible input satisfies one and exactly one of six conditions, we first show that conditions in Table B.1 are equivalent to those in (B.12-B.17). By simple algebra, we can verify the following equivalency with

Thus, we can rewrite conditions in Table B.1 as follows:

| (B.12) | |||

| (B.13) | |||

| (B.14) | |||

| (B.15) | |||

| (B.16) | |||

| (B.17) |

Furthermore, according to the conditions in (B.12-B.17), we will discuss the feasible region of under each condition based on the input in different cases. The results are summarized in Table B.2.

| condition 1 | ||||||

| condition 2 | - | - | - | |||

| condition 3 | - | - | - | |||

| condition 4 | - | - | - | - | - | |

| condition 5 | - | - | - | - | - | |

| condition 6 | ||||||

Through this table, we can clearly see that the intersection of feasible regions of in each column is empty, and the union of those is . In addition, as the six cases of input are also mutually exclusive, every feasible input satisfies one and exactly one of six conditions. Now, we are ready to see how to obtain feasible regions of in each case.

Case (): In this case, we have based on in Assumption 1, and we can first verify that

| (B.18) |

Condition 1 in (B.12) can be rewritten as

According to Hlder’s inequality, we have , i.e.,

| (B.19) |

Thus, and due to (B.19) and . In all, condition 1 can be represented as , as .

Condition 3 in (B.14) can be rewritten as

because of in (B.18) and . According to (B.8), we have

| (B.20) |

due to in (B.18) and in Assumption 1. In addition, we can verify that due to (B.18) and in (B.7). In all, condition 3 can be simplified as .

Condition 6 in (B.17) can be written as

due to inequality (B.18). Moreover, we have , as by equation (B.11) and inequality (B.18). In all, condition 6 can be represented as .

Similar to the previous analysis, the feasible region of under condition 2 in (B.13) and that under condition 4 in (B.15) are empty with . Due to in (B.20), we know that and together are incompatible, which means that the feasible region of under condition 5 in (B.16) is also empty.

In summary, the space is fulfilled by condition 1, condition 3, and condition 6 in this case, and all feasible regions are mutually exclusive, which are summarized in the first column of Table B.2.

Case (): Note that the condition on the input under case 2 () is symmetric to that under case 1 () in the sense of swapping and . In fact, condition 2 and condition 3 are symmetric; condition 4 and condition 5 are symmetric; condition 1 and condition 6 are self-symmetric. Therefore, by the same analysis in case 1, we summarize the result in the second column of Table B.2.

Condition 1 in (B.12) can be rewritten as

due to . As holds by (B.21) and , condition 1 can be represented as .

Condition 3 in (B.14) can be written as

because of and . According to (B.8), we have due to in this case and in Assumption 1. In addition, we can verify that due to in (B.7) and in this case. Thus, . In all, the condition can be simplified as .

Condition 6 in (B.17) can be written as

due to . Moreover, we have , as by equation (B.11) and . In all, condition 6 can be simplified as .

Similar to the previous analysis, we can verify that . Thus we know that and together are incompatible, which means that the feasible region of under condition 2 in (B.13) and condition 4 in (B.15) are empty. In addition, due to , we know that and together are incompatible, which means that the feasible region of under condition 5 in (B.16) is also empty.

In summary, the space is fulfilled by condition 1, condition 3, and condition 6 in this case, and all feasible regions are mutually exclusive, which are summarized in the third column of Table B.2.

Case (): In this case, we first prove that by contradiction. Assume and , i.e., and . If we cancel and , it leads to , which contradicts the feasibility requirement in Assumption 1.

Furthermore, we can verify that

By the same analysis in case 3, the feasible regions of under condition 1 and condition 3 are the same as those in case 3.

Condition 4 in (B.15) can be written as

because of and . According to (B.9), we have that due to in this case and in Assumption 1. In addition, we verify that due to in (B.7) and together with in this case. In all, condition 4 can be simplified as .

Condition 6 in (B.17) can be written as

because of and . Moreover, we have , as by equation (B.11) and . In all, condition 6 can be simplified as .

Similar to the previous analysis, due to , we know that and together are incompatible, which means that the feasible region of under condition 2 in (B.13) is empty. In addition, due to , we know that and together are incompatible, which means that the feasible region of under condition 5 in (B.16) is empty.

In summary, the space is fulfilled by condition 1, condition 3, condition 4, and condition 6 in this case, and all feasible regions are mutually exclusive, which are summarized in the fourth column of Table B.2.

Case (): Note that the condition about the input under case 5 () is symmetric to that under case 3 (). As the symmetry of condition 2 and condition 3 and the self-symmetry of condition 1 and condition 6, by the same analysis in case 3, we summarize the result in the fifth column of Table B.2.

Case (): Note that the condition about the input under case 6 () is symmetric to that under case 4 (). Note that condition 2 and condition 3 are symmetric; condition 4 and condition 5 are symmetric; condition 1 and condition 6 are self-symmetric. Therefore, by the same analysis in case 4, we summarize the result in the last column of Table B.2.

Appendix B.2. Proof of Theorem 1

In this subsection, we provide the optimal values and optimal distributions under each condition in Lemma B.2.1-B.2.6, and Theorem 1 follows immediately from these lemmas.

Before diving into details, we first present our intuitions on how to derive the optimal distribution under each condition. Let be the dual optimal solution, so the dual feasibility implies and for all in (B.4). Moreover, the complementary slackness conditions indicate that or for every in optimal support. Instead of focusing on and directly, geometrically, we consider a curved surface with

and a folded hyperplane with

Accordingly, is equivalent to above , and or is equivalent to touching . Through this interpretation, we can quickly analyze the characteristics of optimal support. Based on these characteristics, we successfully identify an optimal distribution under each condition. In this derivation, although we are motivated by the framework for solving univariate moment problems introduced in [19], it also requires a lot of trial and error to obtain an optimal distribution of our bivariate moment problem. As an illustration, we plot and with parameters in Figure B.1. In this figure, the points of the solid line together with are touching points of and . In fact, the curved surface is a paraboloid.

Now, we are ready to present six lemmas corresponding to each condition. In each proof, we first verify the primal feasibility. Then, we provide a dual solution and show its feasibility. Lastly, we verify the zero duality gap and thus the optimality.

Lemma B.2.1.

Suppose that , and Assumption 1 holds. The optimal distribution for problem B.1 can be characterized as follows

(i) if ,

| (B.22) |

(ii) if ,

| (B.23) |

For both cases, the optimal values are all .

Proof of Lemma B.2.1.

Recall the inequality in (B.19). We now further assume .

First, we shall verify the feasibility of the primal solution (B.22). Due to and , we can verify the non-negativity of the primal supporting points and . Besides, it is easy to verify that . In addition, we can confirm the following moment constraints hold, . In all, the primal solution (B.22) is feasible for problem (B.1).

Second, we shall verify the dual feasibility of the following dual solution with

| (B.24) |

We consider two dual constraint functions and . Since and , then the Hessian matrix is positive semidefinite, which means that both functions are convex. Next, we take the derivative of functions and ,

| (B.25) |

and

| (B.26) |

Define , , . Substitute into equation (B.25), and we have

Since and in Assumption 1, in condition 1, and inequality (B.19), then we have

Note that is a convex function, which implies for any ,

For function , substitute into equation (B.26), and we have

Note that the function is convex, which implies for any ,

In all, we prove that the dual solution is feasible for problem (B.4).

Lastly, it is easy to verify the objective values for the feasible primal-dual pair are all equal to . Hence, the zero duality gap implies the optimality of the feasible primal-dual pair.

Lemma B.2.2.

Suppose that and Assumption 1 hold. Then an optimal distribution for primal distribution for problem B.1 can be characterized as

| (B.27) |

where . The optimal value is .

Proof of Lemma B.2.2.

First, we shall verify the feasibility of the primal solution (B.27). Since in Assumption 1, we have , and it further leads to

With , we get and . Now we rewrite and to be

Thus, is due to , and is due to . Besides, holds obviously. Furthermore, by straightforward calculations, we can also verify that the following constraints hold, , . In all, the primal solution (B.27) is feasible for problem (B.1).

Second, we shall verify the dual feasibility of the following dual solution

We consider two dual constraint functions and . Since and , then the Hessian matrix is positive semidefinite, which means that both functions are convex. Next, we define , and . Then, we have

Since is a convex function, for any , we have For function , substitute into equation (B.26), and we have . Thus . In all, we prove that the dual solution is feasible for problem (B.4).

Lastly, it is easy to verify the objective values for the feasible primal-dual pair are all equal to

. Hence, the zero duality gap implies the optimality of the feasible primal-dual pair. ∎

Lemma B.2.3.

Suppose that and Assumption 1 hold. Then an optimal distribution for primal distribution for problem B.1 can be characterized as

| (B.28) |

where . The optimal value is .

Proof of Lemma B.2.3.

Lemma B.2.4.

Suppose that and Assumption 1 hold. Then an optimal distribution for primal distribution for problem B.1 can be characterized as

| (B.29) |

where . The optimal value is .

Proof of Lemma B.2.4.

First, we observe that the optimal primal solution is the same as that in Lemma B.2.2, so the primal feasibility of this solution holds.

Second, we shall verify the dual feasibility of the following dual solution

We consider two dual constraint functions and . Note that and , then the Hessian matrix is positive semidefinite, which means that both functions are convex. Next, we construct and . Then we have

Since is a convex function, for any , we have For function , substitute into equation (B.26), and we have . Thus, . In all, and hold for all .

Lastly, it is easy to verify the objective values for the feasible primal-dual pair equal to . Hence, the zero duality gap implies the optimality of the feasible primal-dual pair. ∎

Lemma B.2.5.

Suppose that and Assumption 1 hold. Then an optimal distribution for primal distribution for problem B.1 can be characterized as

| (B.30) |

where . The optimal value is .

Proof of Lemma B.2.5.

Lemma B.2.6.

Proof of Lemma B.2.6.

First, we shall verify the feasibility of the primal solution (B.31). Because of the condition 6 with , we have immediately. Moreover, we also have due to . Thus, the distribution (B.31) has positive support and probability. As

we conclude the primal solution (B.31) is a well-defined distribution. To verify this distribution satisfies corresponding constraints, we state two useful equations that will be frequently employed. Specially, we have

In all, the primal feasibility holds.

Second, we shall verify the dual feasibility of the following dual solution

By straightforward calculations, we have and . Thus, is a dual feasible solution.

Lastly, it is easy to verify the objective values for the feasible primal-dual pair equal to . Hence, the zero duality gap implies the optimality of the feasible primal-dual pair. ∎

Appendix C: Proof of Proposition 2

From Theorem 2.1 in [35], the bivariate moment problem

| (C.1) |

is equivalent to its dual problem

for all . Let and , and then we have

The left-hand-side of the inequality can be represented by the sum of squares of polynomials, that is, the above inequality is equivalent to

for some and . Therefore, the original problem (C.1) can be reformulated by

with and the matrix defined as follows:

where are the th column vectors of matrices , , respectively.

Appendix D: Proof of Proposition 3

From Theorem 4.5.7 in book [6], we know that if and only if there exists numbers and such that . If and are perfectly correlated with , we have the following moment constraints due to and :

From these equations, and should satisfy and Then we can obtain and and thus . Moreover, note that we assume , then . From the nonnegativity of , we know that .

Appendix E: Closed-Form Solution of the DRO Newsvendor Problem

We study the DRO newsvendor problem as follows:

where is the mean-covariance ambiguity set in (B.2), and the critical ratio is a given constant in .

We explain the procedure of solving the closed-form solution introduced in Section 4.1. Firstly, each locates at either a stationary point of or a boundary point of the interval . The formulation of each interval is discussed in Table B.2. Thus, we study the stationary point of

in each interval . For simplicity, we denote

For condition 2 as an example, we have

with its derivative

Thus, the stationary point is obtained as follows by setting :

which exists only if .

The stationary points under other conditions can be derived by the same approach shown under condition 2. We provide Table E.1 to summarize the closed-form stationary points in all cases. Lastly, we remark that the stationary point shown in this table for each condition may be out of the interval . In all, given this table, it is not difficult to obtain the closed-form expressions of the optimal solutions.

| Conditions | Stationary Points | Feasible |

| condition 1 | is linear in | |

| condition 2 | , | |

| condition 3 | , | |

| condition 4 | , | |

| condition 5 | , | |

| condition 6 | , |