Statistical Inference and A/B Testing for First-Price Pacing Equilibria

Abstract

We initiate the study of statistical inference and A/B testing for first-price pacing equilibria (FPPE). The FPPE model captures the dynamics resulting from large-scale first-price auction markets where buyers use pacing-based budget management. Such markets arise in the context of internet advertising, where budgets are prevalent.

We propose a statistical framework for the FPPE model, in which a limit FPPE with a continuum of items models the long-run steady-state behavior of the auction platform, and an observable FPPE consisting of a finite number of items provides the data to estimate primitives of the limit FPPE, such as revenue, Nash social welfare (a fair metric of efficiency), and other parameters of interest. We develop central limit theorems and asymptotically valid confidence intervals. Furthermore, we establish the asymptotic local minimax optimality of our estimators. We then show that the theory can be used for conducting statistically valid A/B testing on auction platforms. Numerical simulations verify our central limit theorems, and empirical coverage rates for our confidence intervals agree with our theory.

1 Introduction

A/B testing is a form of randomized controlled experiment, where each sample is assigned to one of two groups: the ‘A’ group or ‘B’ group, and a different treatment is applied to each group. For example, say a social media site wants to test whether a new layout will increase user engagement. A subset of users are sampled, and each user in the subset is randomly assigned the current layout (group A), or the new layout (group B). Now, if we ignore network effects, then we can measure whether the new layout increases user engagement by checking whether engagement in group B is higher than in group A with statistical significance. As of 2017, large internet companies such as Google and Microsoft each conduct more than 10,000 A/B tests annually (Kohavi & Thomke, 2017).

However, now consider a setting where advertisers also bid on their ads being shown to users. If we randomly assign users to groups A and B, then we get interference because an advertiser’s outcomes in group A affect their behavior when buying ads in group B. This is especially problematic if we are trying to measure something that directly pertains to ads (e.g. revenue changes, or user interest in the ads they are shown). In practice, a popular solution to this issue is to create two separate markets, one for group A and one for group B. Then, each advertiser participates in both markets, with half of their budget assigned to each market, and those budgets are then treated as separate budget constraints. We will refer to this as budget splitting. Despite the practical popularity of budget splitting, its statistical properties are not well-understood. A major obstacle to statistical inference with budget splitting is that we can no longer think of the mean user behavior as a sum of independent samples. Instead, we essentially have only two samples: a sample of a market under condition A, and a sample of a market under condition B. Thus, we need to understand when randomized assignment of users (which act as the supply of impressions) into separate markets can be used to make statistical inferences about market outcomes, given the effects of competition.

As stated at the beginning, we study this phenomenon in two important contexts: first-price pacing equilibria (FPPE), and Fisher markets. We will focus the majority of our writing on FPPE, because FPPE model the advertising auction setting faced by large internet companies. All our results carry over to Fisher markets, except results on revenue, which are not meaningful in the standard Fisher market model.

In an FPPE, a set of buyers compete in a set of first-price auctions, and each buyer has a budget. This models how impressions are sold in practice, where first or second-price auction generalizations are used: When a user shows up, an auction is run in order to determine which ads to show, before the page is returned to the user. This auction must run extremely fast. This is typically achieved by having each advertiser specify their target audience, their willingness-to-pay for an impression (or values per click, which are then multiplied by platform-supplied click-through-rate estimates), and a budget ahead of time. The control of the bids for individual impressions is then ceded to proxy bidders that are controlled by the ad platform. As a concrete example, to create an ad campaign on Meta Ads Manager, advertisers need to specify the following parameters: (1) the conversion location (how do you want people to reach out to you, via say website, apps, Messenger and so on), (2) optimization and delivery (target your ads to users with specific behavior patterns, such as those who are more likely to view the ad or click the ad link), (3) audience (age, gender, demographics, interests and behaviors), and (4) how much money do you want to spend (budget).

Given the above parameters reported by the advertiser, the (algorithmic) proxy bidder supplied by the platform is then responsible for bidding in individual auctions so as to maximize advertiser utility, while respecting the budget constraint. Two prevalent budget management methods are throttling and pacing. Throttling tries to enforce budget constraints by adaptively selecting which auctions the advertiser should participate in. Pacing, on the other hand, modifies the advertiser’s bids by applying a shading factor, referred to as a multiplicative pacing multiplier. Tuning the pacing multiplier changes the spending rate: the larger the pacing multiplier, the more aggressive the bids. The goal of the proxy bidder is to choose this pacing multiplier such that the advertiser exactly exhausts their budget (or alternatively use a multiplier of one in the case where their budget is not exhausted by using unmodified bids). In this paper we focus on pacing-based budget management systems.

In the case where each individual auction is a first-price auction, FPPE capture the outcomes of pacing-based budget-management systems. Conitzer et al. (2022a) introduced the FPPE notion, and showed that FPPE always exists and is unique. Moreover, FPPE enjoys lots of nice properties such as being revenue-maximizing among all budget-feasible pacing strategies, shill-proof (the platform does not benefit from adding fake bids under first-price auction mechanism) and revenue-monotone (revenue weakly increases when adding bidders, items or budget). Crucially for us, FPPE are fully characterized by a quasi-linear Eisenberg-Gale convex program (Conitzer et al., 2022a; Chen et al., 2007).

We remark that all the theory in the paper (CLT, inferential theory, and local asymptotic minimax theory) can be extended to Fisher market with quasilinear utility (Cole et al., 2017) given its equivalence to FPPE.

Given the above motivation, we study the question:

Suppose the auction platform operates at FPPE, i.e., at a market equilibrium. How can we quantify the variability in quantities of interest, and use this to perform A/B testing?

Our contributions are as follows.

A statistical model for first-price pacing equilibrium and A/B testing in auction markets.

We leverage the FPPE model of Conitzer et al. (2022a) and the infinite-dimensional Fisher market model of Gao & Kroer (2022) in order to propose a statistical model for first-price auction markets. In this model, we observe market equilibria formed with a finite number of items that are i.i.d. draws from some distribution, and aim to make inferences about several primitives of the limit market, such as revenue, Nash social welfare (a fair metric of efficiency), and other quantities of interest. More importantly, we lay the theoretical foundations for A/B testing in auction markets, which is a difficult statistical problem because buyers interfere with each other through the supply and the budget constraints, the first-price auction allocation, and so on. With the presence of equilibrium effects, traditional statistical approaches which rely on the i.i.d. or the SUTVA (stable unit treatment value assumption, Imbens & Rubin (2015)) assumption fail. The key lever we use to approach this problem is a convex program characterization of the first-price pacing equilibrium, called the Eisenberg-Gale (EG) program. With the EG program, the inference problem reduces to an -estimation problem (Shapiro et al., 2021; Van der Vaart, 2000) on a constrained non-smooth convex optimization problem.

Convergence and inference results for the limit market.

The technical challenges for developing inferential theory for FPPE are two-fold: (1) Nonsmoothness. The sample function in the convex program is non-differentiable on the constraint set almost surely as it involves the max operator (cf. Eq. P-DualEG). Such nonsmoothness results from the fact that the allocation produced by first-price auction is highly nonsmooth w.r.t. buyer’s pacing strategy. (2) The parameter-on-boundary issue: the optimal population solution might be on the boundary of the constraint set. Asymptotic convergence is established by showing that the EG convex program satisfies a set of regularity conditions from Theorem 3.3 by Shapiro (1989). The hardest condition to verify is stochastic equicontinuity (Cond. 8.c), which we establish by leveraging empirical process theory (Vaart & Wellner, 1996; Kosorok, 2008). For constrained -estimators, the asymptotic distribution might not be normal, causing challenges for inference. We discover sufficient conditions to ensure normality of the limit distributions. We also establish that the observed market is an optimal estimator of the limit market in the asymptotic local minimax sense (Van der Vaart, 2000; Le Cam et al., 2000; Duchi & Ruan, 2021). Finally, we provide consistent variance estimators, whose consistency is proved by a uniform law-of-large-numbers over certain function classes.

Statistically-valid inference for A/B testing.

Applying our theory, we develop an A/B testing design for item-side randomization that resembles practical A/B testing methodology. In the proposed design treatment and control markets are formed, and buyer’s budgets are split proportionally between them, while items are randomly assigned. Then, based on the equilibrium outcomes, we construct estimators and confidence intervals that enable statistical inference. A recipe for applying our theory is presented in Algorithm 1.

Notations. For a measurable space , we let (and , resp.) denote the set of (nonnegative, resp.) functions on w.r.t the integrating measure for any (including ). Given and , we let . We treat all functions that agree on all but a measure-zero set as the same. Denote by the -th unit vector. For a sequence of random variables , we say if for any there exists a finite and a finite such that for all . We say if converges to zero in probability. We say (resp. ) if (resp. ). The subscript is for indexing buyers and superscript is for items. Furthermore, we let be the Moore-Penrose pseudo inverse of a matrix . Given vectors and , let be the element-wise product.

In App. B we survey related works on A/B testing in two-sided markets, pacing equilibrum, -estimation when the parameter is on the boundary, and statistical inference with equilibrium effects.

2 Statistical Model for First-Price Pacing Equilibrium

Following Gao & Kroer (2022); Conitzer et al. (2022a), we consider a single-slot auction market with buyers and a possibly continuous set of items with an integrating measure . For example, one could take and the Lebesgue measure on . Defining first price pacing equilibrium requires the following elements.

-

•

The budget of buyer . Let .

-

•

The valuation for buyer is a function , i.e., buyer has valuation (value per unit supply) of item . Let , . We assume .

-

•

The supplies of items are given by a function , i.e., item has unit of supply. Without loss of generality, we assume a unit total supply . Given , we let and .

For buyer , an allocation of items gives a utility of . Let . The prices of items are modeled as ; the price of item is .

2.1 Definition and Interpretation of limit FPPE

Central to the notion of an FPPE is the pacing multiplier, which is a scalar such that buyer bids their “paced” value on a given item .

Definition 1 (Limit FPPE).

Given , a limit FPPE (denoted ) is a tuple such that

-

1.1

(First-price) For all item , . Moreover, implies for all and .

-

1.2

(Supply and budget feasible) For all , . For all , .

-

1.3

(Market clearing) For all , implies . For all , implies .

By Conitzer et al. (2022a), the limit FPPE exists and is unique. Next we unpack Def. 1. The constraint is natural since a rational buyer should not bid more than their value. Cond. 1.1 captures the fact that FPPE is a model for first-price auctions, where pacing is used to manage budgets. The scalar controls the expenditure of buyer , and the constraint ensures that the price is equal to the highest bid, and that only buyers tied for highest are allocated a non-zero amount. Cond. 1.2 ensures that the budget and supply constraints are satisfied. Cond. 1.3 ensures that the solution satisfies no unnecessary pacing, meaning that we should only scale down a buyer’s bids in case their budget constraint is binding. Secondly, it ensures that if a good is demanded by any buyers, then it must be fully allocated.

Fact 1 (Buyer’s satisfaction, Theorem 2 from Conitzer et al. (2022a)).

Let . For all , it holds where the utility of a buyer is

where the first term is utility from the allocated items, the second term is the leftover budget.

This means FPPE is a competitive equilibrium. In the first-price auction context, each buyer’s allocated items maximize their utility (item utility + leftover budget) among all budget-feasible allocations, given the price.

From now on we use to denote limit FPPE quantities. Given an FPPE , we define by

| (1) |

the leftover budget, the item utility and the total utility of buyer . Let be the vectors that collect these quantities for all buyers. It is well-known that are unique in equilibrium, but might not be unique. Later we will see that for statistical inference we need conditions to ensure uniqueness of . The following equations about limit FPPE (Gao & Kroer, 2022) are important.

| (2) |

We want to estimate the following quantities in the limit FPPE. (1) Revenue. The revenue in the limit FPPE is It measures the profitability of the auction platform. When the platform operates at the limit FPPE, is the maximum revenue the platform could extract from the buyers over the space of budget-feasible pacing strategies Conitzer et al. (2022a). (2) Nash social welfare (NSW). The (logarithm of) NSW is defined as The NSW at equilibrium measures total utility of the buyers and, when used as a summary metric of the efficiency of the auction platform, is able to promote fairness better than the utilitarian social welfare, that is, the sum of buyer utilities (Bertsimas et al., 2012; Caragiannis et al., 2019). (3) Individual utilities at limit FPPE, . (4) Pacing multipliers . Pacing multiplier has a two-fold interpretation. First, through the equation , it is the ratio of budget and utility. Second, is the pacing policy employed by the buyers in first-price auctions, a quantity of natural interest.

As we will see next, counterparts of these quantities in the observed market are good estimators of the limit quantities.

2.2 The Observed FPPE

Let be a sequence of observed items drawn from the distribution in an i.i.d. manner. Assume each item has the same supply of units. Most of the time we take to ensure total supply agrees with the limit market.

Definition 2 (Observed FPPE, informal).

Given , the observed FPPE contains tuples such that the conditions in Def. 1 hold with the following modifications: and where is a point mass on .

A formal definition and further properties of FPPE can be found in App. C. Here is the fractional allocation of item to buyer . The mechanism of forming the observed FPPE is exactly the same as the limit FPPE in Def. 1, except now the price , the supply and the allocation reduce to vectors in as opposed to functions.

To emphasize dependence on the item sequence , we use to denote equilibrium quantities in . We let be an observed FPPE with . The leftover budget , item utility and total utility are defined similarly. Let be the vectors that collect these quantities for all buyers. The observed revenue is , and NSW is .

Having observed an FPPE with a finite number of items, our goal is to estimate the quantities of interest in the limit FPPE.

2.3 Convex Programs for FPPE

Before we present the main statistical theories for FPPE, we review convex program characterization of FPPE, which are at the core of the paper. These convex characterization results reduce the FPPE inference problem to the one on a constrained nonsmooth convex program.

The limit FPPE pacing multiplier can be recovered through the population dual Eisenberg-Gale (EG) program

| (P-DualEG) |

where , ,

It is known that the FPPE is the unique solution to Eq. P-DualEG, and any FPPE belongs to the set of optimal solutions to the population primal EG program (to be presented in App. C).

The observed FPPE has a similar convex program characterization. By taking and replacing with the empirical measure in Eq. P-DualEG, it can be shown that the observed FPPE pacing multiplier solves the sample dual EG program

| (S-DualEG) |

To develop inferential theory for FPPE, we study the concentration of the dual EG programs. The study of the convergence “” reduces to the one of

As mentioned previously, the difficulty of analyzing the above convex programs lies in the nonsmoothness of the sample function and that the population optimum could lie on the boundary of . We define the set of constraints that are active/inactive at by

| (3) |

3 Statistical Inference

For statistical inference we need the limit market to behave smoothly around the optimal pacing multipliers . To that end, we make the following assumption.

Assumption 1 (SMO).

Assume the map is in a neighborhood of the limit FPPE pacing multiplier .

For a given , the quantity is the price of item in the first-price auction. The assumption requires that the revenue, , when viewed as a function of , changes smoothly around . The assumption implies that , defined in Eq. P-DualEG, is also at .

Assumption 1 implies a number of nice regularity conditions. One is that the set of items that are tied at the limit FPPE is -measure zero. The set of tied items is

Lemma 1.

(SMO). is a joint assumption on value functions and the supply function . Lower level conditions on and that imply (SMO). were derived by Liao et al. (2022b). For example, if the distribution of the values is smooth, then (SMO). holds. If we impose functional structure on , such as and with , ’s distinct, and is uniform, then (SMO). also holds. If the gap between the highest and the second-highest bid is large for most items in the limit FPPE, (SMO). also holds. For a precise statement, we refer readers to Theorem 7 from Liao et al. (2022b).

In order to state our main CLT results, we define

| (4) |

Under (SMO)., is unique and well-defined. Clearly .

In the unconstrained case, classical -estimation theory says that, under regularity conditions, an -estimator is asymptotically normal with covariance matrix (Van der Vaart, 2000, Chap. 5). However, in the case of FPPE which is characterized by a constrained convex problem, the Hessian matrix needs to be adjusted to take into account the geometry of the constraint set at the optimum . We let be an “indicator matrix” of buyers whose , and define the projected Hessian

| (5) |

It will be shown that the asymptotic variance of is .

Assumption 2 (SCS).

Strict complementary slackness holds: implies .

(SCS). can be viewed as a non-degeneracy condition from a convex programming perspective, since corresponds to a Lagrange multiplier on . From a market perpective, (SCS). requires that if a buyer’s bids are not paced (), then the leftover budget must be strictly positive. This can again be seen as a market-based non-degeneracy condition: if then the budget constraint of buyer is binding, yet would imply that they have no use for additional budget. If (SCS). fails, one could slightly increase the budgets of buyers for which (SCS). fails, i.e., those who do not pace yet have exactly zero leftover budget, and obtain a market instance with the same equilibrium, but where (SCS). holds.

From a technical viewpoint, (SCS). is a stronger form of the first-order optimality condition. Note (cf. App. C). The usual first-order optimality condition is

| (6) |

where is the normal cone with if and if for . Then Eq. 6 translates to the condition that implies . On the other hand, when written in the form that resembles optimality condition, (SCS). is equivalent to

Given that , (SCS). is obviously a stronger form of first-order condition. The (SCS). condition is commonly seen in the study of statistical properties of constrained -estimators (Duchi & Ruan (2021, Assumption B) and Shapiro (1989)). In the proof of Thm. 1, (SCS). forces the critical cone to reduce to a hyperplane and thus ensures asymptotic normality of the estimates. Without (SCS)., the asymptotic distribution of could be non-normal.

3.1 Central Limit Theorems

We now show that the observed pacing multipliers and the observed revenue converge to the limit market quantities in probability, and satisfy central limit theorems. Define the influence functions

| (7) | ||||

Theorem 1.

The functions and are called the influence functions of the estimates and because they measure the change in the estimates caused by adding a new item to the market (asymptotically).

Thm. 1 implies fast convergence rate of for whose constraint is tight in the limit market. To see this, we suppose wlog. that , i.e. the first buyers are the ones with . Then the pseudo-inverse of projected Hessian where is the lower right block of . Consequently, entries of (resp. ) are zeros except those on the lower right blocks (resp. ). This result shows that the constraint set “improves” the covariance by zeroing out the entries corresponding to the active constraints . Consequently, and are of order for , and thus converging faster than the usual rate. The fast rate phenomenon is empirically investigated in Sec. G.1.

By (SCS). we have , i.e., is the set of buyers with positive leftover budgets, and , i.e., is the set of buyers who exhaust their budgets. 222Without (SCS)., it only holds and by complementary slackness Eq. 2. In the context of first-price auctions, the fast rate implies that the platform can identify buyers that are unpaced in the limit FPPE even when the market size is small.

The proof of Thm. 1 proceeds by showing that FPPE satisfy a set of regularity conditions that are sufficient for asymptotic normality (Shapiro, 1989, Theorem 3.3); the conditions are stated in Lemma 8 in the appendix. Maybe the hardest condition to verify is the so called stochastic equicontinuity condition (Cond. 8.c), which we establish with tools from the empirical process literature. In particular, we show that the function class whose functions map an item to the first-price auction allocation of items, is VC-subgraph, which implies stochastic equicontinuity. (SCS). is used to ensure normality of the limit distribution.

Finally, we remark that the CLT result for revenue holds true even if . If for all , then all buyers’ budgets are exhausted in the observed FPPE, and so we have if By the convergence , we know that with high probability for all large if . In that case, it must be that the asymptotic variance of revenue equals zero. Our result covers this case because one can show using Euler’s identify for homogenous functions and that if ; see Lemma 6.

3.2 Asymptotic Local Minimax Optimality

Given the asymptotic normality of observed FPPE, it is desirable to understand the best possible statistical procedure for estimating the limit FPPE. One way to discuss the optimality is to measure the difficulty of estimating the limit FPPE when the supply distribution varies over small neighborhoods of the true supply , asymptotically. When an estimator achieves the best worst-case risk over these small neighborhoods, we say it is asymptotically locally minimax optimal. For general references, see Vaart & Wellner (1996); Le Cam et al. (2000). More recently Duchi & Ruan (2021, Sec. 3.2) develop asymptotic local minimax theory for constrained convex optimization, and we rely on their results.

Given the central limit results for and REV, we will show that the observed FPPE estimates are optimal in a asymptotic local minimax sense. To make this precise we introduce a few more notations to parametrize neighborhoods of the supply . Let be a direction along which we wish to perturb the supply . Given a vector signifying the magnitude of perturbation, we want to scale the original supply of item by and then obtain a perturbed supply distribution by appropriate normalization. To do this we define the perturbed supply by 333 In Duchi & Ruan (2021) they allow more general classes of perturbations, we specialize their results for our purposes.

| (8) |

with a normalizing constant . As , the perturbed supply effectively approximates

Asymptotic local minimax optimality for .

We first focus on estimation of pacing multipliers. For a given perturbation , we let , and be the limit FPPE pacing multiplier, price and revenue under supply distribution . Clearly for any and similarly for and . Let be any symmetric quasi-convex loss. 444A function is quasi-convex if its sublevel sets are convex. In asymptotic local minimax theory we are interested in the local asymptotic risk: given a sequence of estimators ,

If we ignore the limits and consider a fixed , then roughly measures the worst-case risk for the estimators . Note that is a -dimensional vector, and thus the shrinking norm-balls depend on the choice of , and the expectation is taken w.r.t. the -fold product of the perturbed supply. As an immediate application of Theorem 1 from Duchi & Ruan (2021), it holds that

where the expectation is taken w.r.t. a normal specified above. Moreover, the lower bound is achieved by the observed FPPE pacing multipliers according to the CLT result in Thm. 1.

Asymptotic local minimax optimality for revenue estimation.

More interesting is the asymptotic minimax result of revenue estimation. Given a symmetric quasi-convex loss , we define the local asymptotic risk for any procedure that aims to estimate the revenue:

Proof in Sec. F.3. In the proof we calculate the derivative of revenue w.r.t. , which in turns uses a perturbation result for constrained convex program from Duchi & Ruan (2021); Shapiro (1989). Again, the lower bound is achieved by the observed FPPE revenue according to the CLT result in Thm. 1. Similar optimality statements can be made for and NSW by finding the corresponding derivative expressions.

3.3 Inference

In order to perform inference, we need to construct estimators for the influence functions Eq. 7. We show how each component can be estimated by the observed FPPE.

Given a sequence of smoothing parameters , we estimate by For the same sequence , we introduce a numerical difference estimator for the Hessian matrix , whose -th entry is with , and is defined in Eq. S-DualEG. Then is a natural estimator of . Also, will be estimated by . Let be the proportion of allocated to buyer and be the price.

Mirroring the definitions in Eq. 7, we define the following influence function estimators

Given that the asymptotic variance of (resp. ) is (resp. ), plug-in estimators of the (co)variance are naturally

| (9) |

For any , the -confidence region/interval for and are

| (10) | |||

| (11) |

where is the -th quantile of a chi-square distribution with degree , is the unit ball in , and is the -th quantile of a standard normal distribution. The coverage rate of is empirically verified in Sec. G.3.

Theorem 3.

The theorem suggests choosing smoothing parameter for ; see Sec. G.2 for a numerical study on how affects Hessian estimation. Variance estimators for , and NSW can be constructed similarly.

4 A/B Testing for First-Price Auction Platforms

Consider an auction market with buyers with a continuum of items with supply function . To model treatment application we introduce the potential value functions

If item is exposed to treatment , then its value to buyer will be .

Suppose we are interested in estimating the change in the auction market when treatment 1 is deployed to the entire item set . In this section we describe how to do this using A/B testing, specifically for estimating the treatment effect on revenue. We discuss other quantities like Nash social welfare in App. D. Formally, we wish to look at the difference in revenues between the markets

where is the market with treatment 1, and is the one with treatment 0. The treatment effects on revenue is defined as

where is revenue in the equilibrium .

We will refer to the experiment design as budget splitting with item randomization. Step 1. Budget splitting. We replicate buyers by splitting their budgets and form two markets with the same set of buyers. For each buyer we allocate of their budget to the market with treatment , and the remaining budget, , to the market with treatment . Step 2. Item randomization. Let be i.i.d. draws from the supply distribution . For each sampled item, it is applied treatment with probability and treatment with probability . The total A/B testing horizon is . When the end of horizon is reached, two observed FPPEs are formed. Assume each item has a supply of in the 1-treated market and in the 0-treated market. The is the scaling required for our CLTs and the factor ensures the budget-supply ratio agrees with the limit market; see Lemma 5 regarding scale-invariance of FPPE.

Let be the number of -treated items, and be the number of -treated items. Conditional on the total number of items , the random variable is a binomial random variable with mean . Let be the set of -treated items, and similarly . The total item set . Compactly, the observables in the described A/B testing experiment are

both defined in Def. 2. Let denote the observed revenue in the -treated market. The estimator of revenue treatment effect is

For fixed , the variance in Thm. 1 is a functional of the value functions. We will use to represent the revenue variance in the equilibrium . Each variance can be estimated using Eq. 9.

Theorem 4 (Revenue treatment effects CLT).

Based on the theorem, an A/B testing procedure is the following. Compute the revenue variance as Eq. 9 for each market, obtaining and , and form the confidence interval

| (12) |

If zero is on the left (resp. right) of the CI Eq. 17, we conclude that the new feature increases (resp. decreases) revenue with confidence. If zero is inside the interval, the effect of new feature is undecided. See Sec. G.4 for a numerical study verifying the validity of this procedure. Algorithm 1 presents a step-by-step procedure for using the above results.

5 Experiment

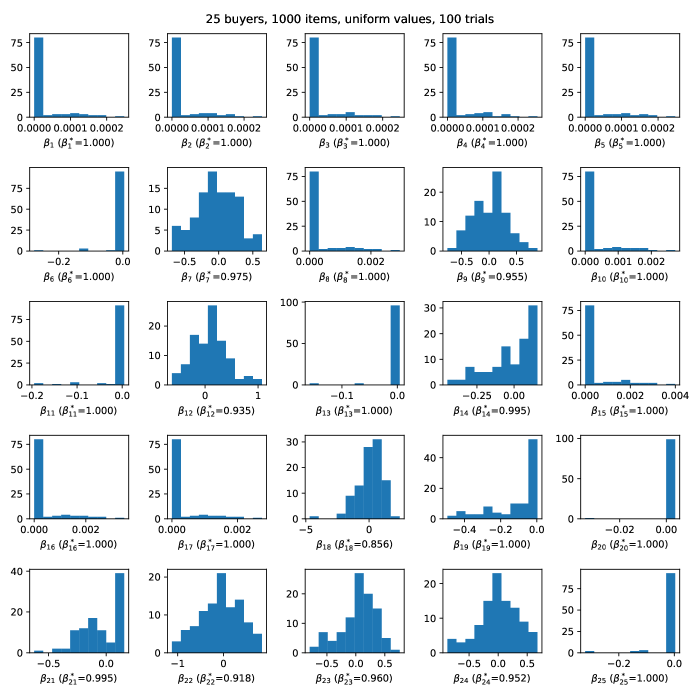

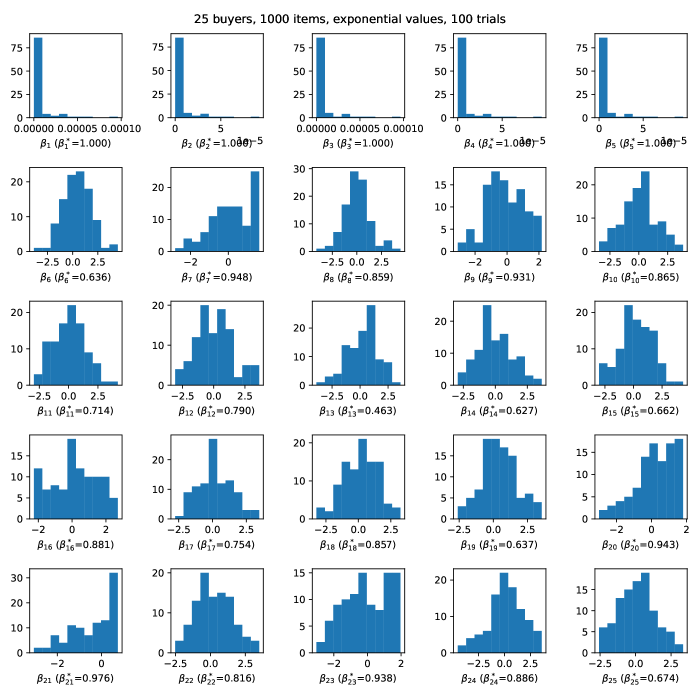

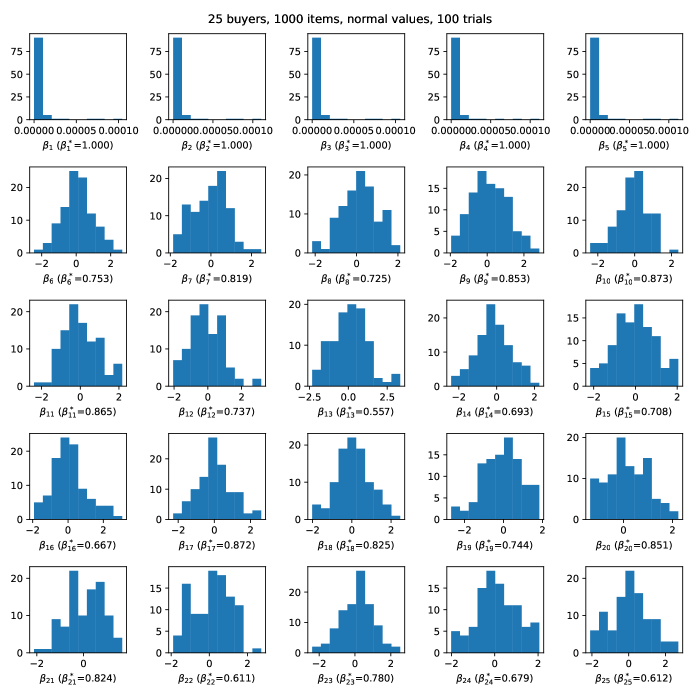

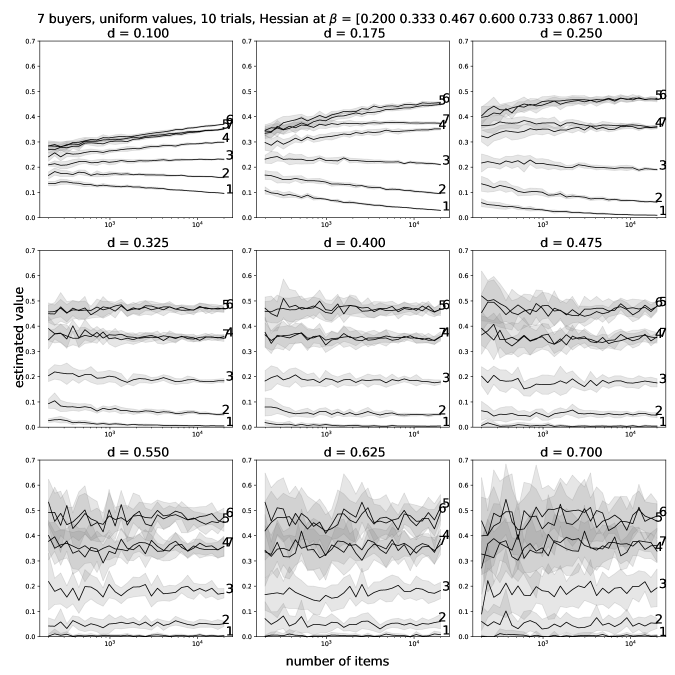

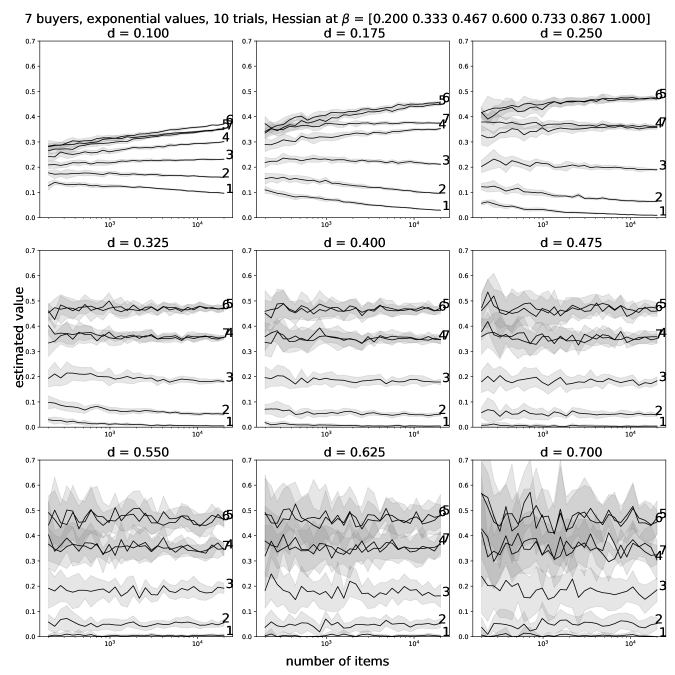

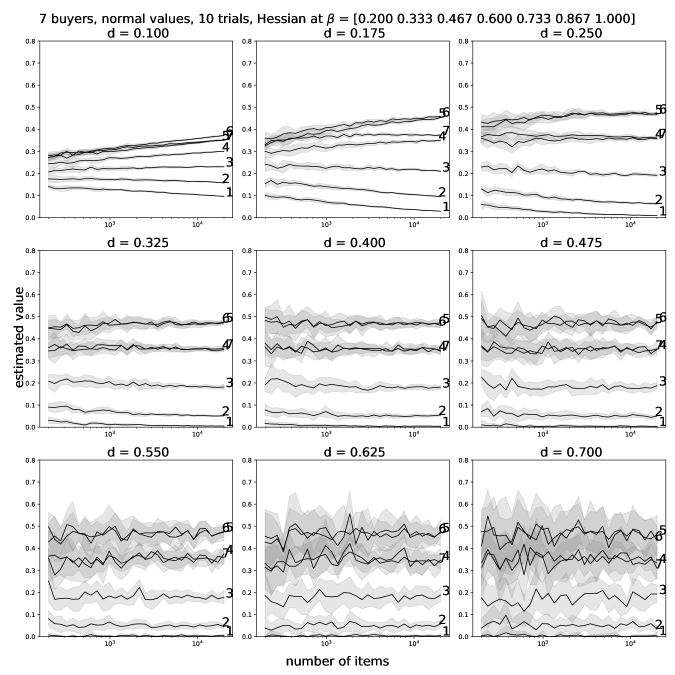

In App. G we conduct simulations to investigate asymptotic normality for and fast convergence rate for , the effect of smoothing parameter on Hessian estimation, the coverage rate of the CI for revenue, and the coverage rate of the treatment effect CI for revenue. Through these experiments, we confirm that the finite sample of converges to a normal distribution, with fast convergence in the entries whose constraints are tight. We confirm that for Hessian estimation, a suitable choice of of smoothing parameter sequence is for . Finally, the revenue confidence intervals in Thm. 3 and Eq. 17 attain the nominal coverage rate.

Acknowledgements

This research was supported by the Office of Naval Research under grants N00014-22-1-2530 and N00014-23-1-2374, and the National Science Foundation award IIS-2147361.

References

- Andrews (1994) Andrews, D. W. Asymptotics for semiparametric econometric models via stochastic equicontinuity. Econometrica: Journal of the Econometric Society, pp. 43–72, 1994.

- Andrews (1999) Andrews, D. W. Estimation when a parameter is on a boundary. Econometrica, 67(6):1341–1383, 1999.

- Andrews (2001) Andrews, D. W. Testing when a parameter is on the boundary of the maintained hypothesis. Econometrica, 69(3):683–734, 2001.

- Aronow & Samii (2017) Aronow, P. M. and Samii, C. Estimating average causal effects under general interference, with application to a social network experiment. The Annals of Applied Statistics, 11(4):1912–1947, 2017.

- Athey & Haile (2007) Athey, S. and Haile, P. A. Nonparametric approaches to auctions. Handbook of econometrics, 6:3847–3965, 2007.

- Athey et al. (2018) Athey, S., Eckles, D., and Imbens, G. W. Exact p-values for network interference. Journal of the American Statistical Association, 113(521):230–240, 2018.

- Bajari et al. (2021) Bajari, P., Burdick, B., Imbens, G. W., Masoero, L., McQueen, J., Richardson, T., and Rosen, I. M. Multiple randomization designs. arXiv preprint arXiv:2112.13495, 2021.

- Balseiro et al. (2021) Balseiro, S., Kim, A., Mahdian, M., and Mirrokni, V. Budget-management strategies in repeated auctions. Operations research, (3):859–876, 2021.

- Balseiro & Gur (2019) Balseiro, S. R. and Gur, Y. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019.

- Balseiro et al. (2015) Balseiro, S. R., Besbes, O., and Weintraub, G. Y. Repeated auctions with budgets in ad exchanges: Approximations and design. Management Science, 61(4):864–884, 2015.

- Basse et al. (2016) Basse, G. W., Soufiani, H. A., and Lambert, D. Randomization and the pernicious effects of limited budgets on auction experiments. In Artificial Intelligence and Statistics, pp. 1412–1420. PMLR, 2016.

- Bertsekas (1973) Bertsekas, D. P. Stochastic optimization problems with nondifferentiable cost functionals. Journal of Optimization Theory and Applications, 12(2):218–231, 1973.

- Bertsimas et al. (2012) Bertsimas, D., Farias, V. F., and Trichakis, N. On the efficiency-fairness trade-off. Management Science, 58(12):2234–2250, 2012.

- Blake & Coey (2014) Blake, T. and Coey, D. Why marketplace experimentation is harder than it seems: The role of test-control interference. In Proceedings of the fifteenth ACM conference on Economics and computation, pp. 567–582, 2014.

- Bojinov & Gupta (2022) Bojinov, I. and Gupta, S. Online experimentation: Benefits, operational and methodological challenges, and scaling guide. Harvard Data Science Review, 4(3), 2022.

- Bojinov & Shephard (2019) Bojinov, I. and Shephard, N. Time series experiments and causal estimands: exact randomization tests and trading. Journal of the American Statistical Association, 114(528):1665–1682, 2019.

- Bojinov et al. (2022) Bojinov, I., Simchi-Levi, D., and Zhao, J. Design and analysis of switchback experiments. Management Science, 2022.

- Borgs et al. (2007) Borgs, C., Chayes, J., Immorlica, N., Jain, K., Etesami, O., and Mahdian, M. Dynamics of bid optimization in online advertisement auctions. In Proceedings of the 16th international conference on World Wide Web, pp. 531–540, 2007.

- Caragiannis et al. (2019) Caragiannis, I., Kurokawa, D., Moulin, H., Procaccia, A. D., Shah, N., and Wang, J. The unreasonable fairness of maximum nash welfare. ACM Transactions on Economics and Computation (TEAC), 7(3):1–32, 2019.

- Cen & Shah (2022) Cen, S. H. and Shah, D. Regret, stability & fairness in matching markets with bandit learners. In International Conference on Artificial Intelligence and Statistics, pp. 8938–8968. PMLR, 2022.

- Chen et al. (2007) Chen, L., Ye, Y., and Zhang, J. A note on equilibrium pricing as convex optimization. In International Workshop on Web and Internet Economics, pp. 7–16. Springer, 2007.

- Chen et al. (2003) Chen, X., Linton, O., and Van Keilegom, I. Estimation of semiparametric models when the criterion function is not smooth. Econometrica, 71(5):1591–1608, 2003.

- Clarke (1990) Clarke, F. H. Optimization and Nonsmooth Analysis. Society for Industrial and Applied Mathematics, January 1990. doi: 10.1137/1.9781611971309. URL https://doi.org/10.1137/1.9781611971309.

- Cole et al. (2017) Cole, R., Devanur, N. R., Gkatzelis, V., Jain, K., Mai, T., Vazirani, V. V., and Yazdanbod, S. Convex program duality, fisher markets, and Nash social welfare. In 18th ACM Conference on Economics and Computation, EC 2017. Association for Computing Machinery, Inc, 2017.

- Conitzer et al. (2022a) Conitzer, V., Kroer, C., Panigrahi, D., Schrijvers, O., Stier-Moses, N. E., Sodomka, E., and Wilkens, C. A. Pacing equilibrium in first price auction markets. Management Science, 2022a.

- Conitzer et al. (2022b) Conitzer, V., Kroer, C., Sodomka, E., and Stier-Moses, N. E. Multiplicative pacing equilibria in auction markets. Operations Research, 70(2):963–989, 2022b.

- Dai & Jordan (2021) Dai, X. and Jordan, M. Learning in multi-stage decentralized matching markets. In Ranzato, M., Beygelzimer, A., Dauphin, Y., Liang, P., and Vaughan, J. W. (eds.), Advances in Neural Information Processing Systems, volume 34, pp. 12798–12809. Curran Associates, Inc., 2021. URL https://proceedings.neurips.cc/paper/2021/file/6a571fe98a2ba453e84923b447d79cff-Paper.pdf.

- Duchi & Ruan (2021) Duchi, J. C. and Ruan, F. Asymptotic optimality in stochastic optimization. The Annals of Statistics, 49(1):21–48, 2021.

- Dupačová (1991) Dupačová, J. On non-normal asymptotic behavior of optimal solutions for stochastic programming problems and on related problems of mathematical statistics. Kybernetika, 27(1):38–52, 1991.

- Dupacová & Wets (1988) Dupacová, J. and Wets, R. Asymptotic behavior of statistical estimators and of optimal solutions of stochastic optimization problems. The annals of statistics, 16(4):1517–1549, 1988.

- Durrett (2019) Durrett, R. Probability: theory and examples, volume 49. Cambridge university press, 2019.

- Fradkin (2019) Fradkin, A. A simulation approach to designing digital matching platforms. Boston University Questrom School of Business Research Paper Forthcoming, 2019.

- Gao & Kroer (2022) Gao, Y. and Kroer, C. Infinite-dimensional fisher markets and tractable fair division. Operation Research, Forthcoming, 2022.

- Gao et al. (2021) Gao, Y., Kroer, C., and Peysakhovich, A. Online market equilibrium with application to fair division. arXiv preprint arXiv:2103.12936, 2021.

- Geyer (1994) Geyer, C. J. On the asymptotics of constrained -estimation. The Annals of statistics, pp. 1993–2010, 1994.

- Giné & Nickl (2021) Giné, E. and Nickl, R. Mathematical foundations of infinite-dimensional statistical models. Cambridge university press, 2021.

- Glynn et al. (2020) Glynn, P. W., Johari, R., and Rasouli, M. Adaptive experimental design with temporal interference: A maximum likelihood approach. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H. (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 15054–15064. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/abd987257ff0eddc2bc6602538cb3c43-Paper.pdf.

- Guo et al. (2021) Guo, W., Kandasamy, K., Gonzalez, J. E., Jordan, M. I., and Stoica, I. Online learning of competitive equilibria in exchange economies. arXiv preprint arXiv:2106.06616, 2021.

- Hong & Li (2020) Hong, H. and Li, J. The numerical bootstrap. The Annals of Statistics, 48(1):397–412, 2020.

- Hsieh et al. (2022) Hsieh, Y.-W., Shi, X., and Shum, M. Inference on estimators defined by mathematical programming. Journal of Econometrics, 226(2):248–268, 2022.

- Hu & Wager (2022) Hu, Y. and Wager, S. Switchback experiments under geometric mixing. arXiv preprint arXiv:2209.00197, 2022.

- Hu et al. (2022) Hu, Y., Li, S., and Wager, S. Average direct and indirect causal effects under interference. Biometrika, 2022.

- Hudgens & Halloran (2008) Hudgens, M. G. and Halloran, M. E. Toward causal inference with interference. Journal of the American Statistical Association, 103(482):832–842, 2008.

- Imbens & Rubin (2015) Imbens, G. W. and Rubin, D. B. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Jagadeesan et al. (2021) Jagadeesan, M., Wei, A., Wang, Y., Jordan, M., and Steinhardt, J. Learning equilibria in matching markets from bandit feedback. Advances in Neural Information Processing Systems, 34:3323–3335, 2021.

- Johari et al. (2022) Johari, R., Li, H., Liskovich, I., and Weintraub, G. Y. Experimental design in two-sided platforms: An analysis of bias. Management Science, 2022.

- Knight (1999) Knight, K. Epi-convergence in distribution and stochastic equi-semicontinuity. Unpublished manuscript, 37(7):14, 1999.

- Knight (2001) Knight, K. Limiting distributions of linear programming estimators. Extremes, 4(2):87–103, 2001.

- Knight (2006) Knight, K. Asymptotic theory for -estimators of boundaries. In The Art of Semiparametrics, pp. 1–21. Springer, 2006.

- Knight (2010) Knight, K. On the asymptotic distribution of the analytic center estimator. Nonparametrics and Robustness in Modern Statistical Inference and Time Series Analysis: A Festschrift in honor of Professor Jana Jurecková, pp. 123, 2010.

- Kohavi & Thomke (2017) Kohavi, R. and Thomke, S. The surprising power of online experiments. Harvard business review, 95(5):74–82, 2017.

- Kosorok (2008) Kosorok, M. R. Introduction to empirical processes and semiparametric inference. Springer, 2008.

- Larsen et al. (2022) Larsen, N., Stallrich, J., Sengupta, S., Deng, A., Kohavi, R., and Stevens, N. Statistical challenges in online controlled experiments: A review of a/b testing methodology. arXiv preprint arXiv:2212.11366, 2022.

- Le Cam et al. (2000) Le Cam, L., LeCam, L. M., and Yang, G. L. Asymptotics in statistics: some basic concepts. Springer Science & Business Media, 2000.

- Leung (2020) Leung, M. P. Treatment and spillover effects under network interference. Review of Economics and Statistics, 102(2):368–380, 2020.

- Li et al. (2022) Li, H., Zhao, G., Johari, R., and Weintraub, G. Y. Interference, bias, and variance in two-sided marketplace experimentation: Guidance for platforms. In Proceedings of the ACM Web Conference 2022, pp. 182–192, 2022.

- Li (2022) Li, J. The proximal bootstrap for constrained estimators. 2022.

- Li & Wager (2022) Li, S. and Wager, S. Random graph asymptotics for treatment effect estimation under network interference. The Annals of Statistics, 50(4):2334–2358, 2022.

- Liao et al. (2022a) Liao, L., Gao, Y., and Kroer, C. Nonstationary dual averaging and online fair allocation. arXiv preprint arXiv:2202.11614v1, 2022a.

- Liao et al. (2022b) Liao, L., Gao, Y., and Kroer, C. Statistical inference for fisher market equilibrium. In arXiv preprint arXiv:2209.15422v1, 2022b. URL https://arxiv.org/abs/2209.15422.

- Liu et al. (2021a) Liu, L. T., Ruan, F., Mania, H., and Jordan, M. I. Bandit learning in decentralized matching markets. J. Mach. Learn. Res., 22:211–1, 2021a.

- Liu et al. (2021b) Liu, M., Mao, J., and Kang, K. Trustworthy and powerful online marketplace experimentation with budget-split design. In Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery & Data Mining, pp. 3319–3329, 2021b.

- Liu et al. (2022) Liu, Z., Lu, M., Wang, Z., Jordan, M., and Yang, Z. Welfare maximization in competitive equilibrium: Reinforcement learning for markov exchange economy. In International Conference on Machine Learning, pp. 13870–13911. PMLR, 2022.

- Min et al. (2022) Min, Y., Wang, T., Xu, R., Wang, Z., Jordan, M. I., and Yang, Z. Learn to match with no regret: Reinforcement learning in markov matching markets. arXiv preprint arXiv:2203.03684, 2022.

- Munro et al. (2021) Munro, E., Wager, S., and Xu, K. Treatment effects in market equilibrium. arXiv preprint arXiv:2109.11647, 2021.

- Newey & McFadden (1994) Newey, W. K. and McFadden, D. Large sample estimation and hypothesis testing. Handbook of econometrics, 4:2111–2245, 1994.

- Pakes & Pollard (1989) Pakes, A. and Pollard, D. Simulation and the asymptotics of optimization estimators. Econometrica: Journal of the Econometric Society, pp. 1027–1057, 1989.

- Sahoo & Wager (2022) Sahoo, R. and Wager, S. Policy learning with competing agents. arXiv preprint arXiv:2204.01884, 2022.

- Self & Liang (1987) Self, S. G. and Liang, K.-Y. Asymptotic properties of maximum likelihood estimators and likelihood ratio tests under nonstandard conditions. Journal of the American Statistical Association, 82(398):605–610, 1987.

- Shapiro (1988) Shapiro, A. Sensitivity analysis of nonlinear programs and differentiability properties of metric projections. SIAM Journal on Control and Optimization, 26(3):628–645, 1988.

- Shapiro (1989) Shapiro, A. Asymptotic properties of statistical estimators in stochastic programming. The Annals of Statistics, 17(2):841–858, 1989.

- Shapiro (1990) Shapiro, A. On differential stability in stochastic programming. Mathematical Programming, 47(1):107–116, 1990.

- Shapiro (1991) Shapiro, A. Asymptotic analysis of stochastic programs. Annals of Operations Research, 30(1):169–186, 1991.

- Shapiro (1993) Shapiro, A. Asymptotic behavior of optimal solutions in stochastic programming. Mathematics of Operations Research, 18(4):829–845, 1993.

- Shapiro (2000) Shapiro, A. On the asymptotics of constrained local -estimators. Annals of statistics, pp. 948–960, 2000.

- Shapiro et al. (2021) Shapiro, A., Dentcheva, D., and Ruszczynski, A. Lectures on stochastic programming: modeling and theory. SIAM, 2021.

- Sneider et al. (2018) Sneider, C., Tang, Y., and Tang, Y. Experiment rigor for switchback experiment analysis. URL: https://doordash. engineering/2019/02/20/experiment-rigor-for-switchback-experiment-analysis, 2018.

- Vaart & Wellner (1996) Vaart, A. W. and Wellner, J. A. Weak convergence. In Weak convergence and empirical processes, pp. 16–28. Springer, 1996.

- Van der Vaart (2000) Van der Vaart, A. W. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Wager & Xu (2021) Wager, S. and Xu, K. Experimenting in equilibrium. Management Science, 67(11):6694–6715, November 2021. doi: 10.1287/mnsc.2020.3844. URL https://doi.org/10.1287/mnsc.2020.3844.

- Wainwright (2019) Wainwright, M. J. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press, 2019.

- Xiao (2010) Xiao, L. Dual averaging methods for regularized stochastic learning and online optimization. Journal of Machine Learning Research, 11:2543–2596, 2010.

Appendix A Notations

| Symbol | Meaning |

|---|---|

| Notations in First-Price Pacing Equilibrium | |

| pacing multiplier | |

| , | price and revenue |

| utility generated from items | |

| leftover budget | |

| total utility = utility from items + leftover budgets | |

| allocation | |

| supply (a probability density) | |

| budget | |

| valuations | |

| Notations in Eisenberg-Gale Grogram | |

| , , and | see Eq. P-DualEG |

| objective function of Eisenberg-Gale convex programs | |

| the domain of and | |

| the Hessian matrix of at | |

| matrix whose diagonal = | |

| , | partition of buyers into those with and those not |

Appendix B Related Works

A/B testing in two-sided markets. Empirical studies by Blake & Coey (2014); Fradkin (2019) demonstrate bias in experiments due to marketplace interference. Basse et al. (2016) study the bias and variance of treatment effects under two randomization schemes for auction experiments. Bojinov & Shephard (2019) study the estimation of causal quantities in time series experiments. Some recent state-of-the-art designs are the multiple randomization designs (Liu et al., 2021b; Johari et al., 2022; Bajari et al., 2021) and the switch-back designs (Sneider et al., 2018; Hu & Wager, 2022; Li et al., 2022; Bojinov et al., 2022; Glynn et al., 2020). The surveys by Kohavi & Thomke (2017); Bojinov & Gupta (2022) contain detailed accounts of A/B testing in internet markets. See Larsen et al. (2022) for an extensive survey on statistical challenges in A/B testing. Our paper focuses on A/B testing in first-price auction markets with the consideration of equilibrium effects, to the best of our knowledge this is the first work to consider market equilibrium effects in A/B testing.

Pacing equilibrium. Pacing and throttling are two prevalent budget-management methods on ad auction platforms. Here we focus on pacing methods since that is our setting. In the first-price setting, Borgs et al. (2007) study first price auctions with budget constraints in a perturbed model, whose limit prices converge to those of an FPPE. Building on the work of Borgs et al. (2007), Conitzer et al. (2022a) introduce the FPPE model and discover several properties of FPPE such as shill-proofness and monotonicity in buyers, budgets and goods. There it is also established that FPPE is closely related to the quasilinear Fisher market equilibrium (Chen et al., 2007; Cole et al., 2017). Gao & Kroer (2022) propose an infinite-dimensional variant of the quasilinear Fisher market, which lays the probability foundation of the current paper. Gao et al. (2021); Liao et al. (2022a) study online computation of the infinite-dimensional Fisher market equilibrium. In the second-price setting, Balseiro et al. (2015) investigate budget-management in second-price auctions through a fluid mean-field approximation; Balseiro & Gur (2019) study adaptive pacing strategy from buyers’ perspective in a stochastic continuous setting; Balseiro et al. (2021) study several budget smoothing methods including multiplicative pacing in a stochastic context; Conitzer et al. (2022b) study second price pacing equilibrium, and shows that the equilibria exist under fractional allocations.

-estimation when the parameter is on the boundary There is a long literature on the statistical properties of -estimators when the parameter is on the boundary (Geyer, 1994; Shapiro, 1990, 1988, 1989, 1991, 1993, 2000; Andrews, 1999, 2001; Knight, 1999, 2001, 2006, 2010; Dupacová & Wets, 1988; Dupačová, 1991; Self & Liang, 1987). Some recent works on the statistical inference theory for constrained -estimation include Li (2022); Hong & Li (2020); Hsieh et al. (2022). Our work leverages Shapiro (1989), which develops a general set of conditions for CLTs of constrained -estimators when the sample function is nonsmooth. Working under the specific model of FPPE, we build on and go beyond these contributions by deriving sufficient condition for asymptotic normality in FPPE, establishing local asymptotic minimax theory and developing valid inferential procedures.

Statistical learning and inference with equilibrium effects Wager & Xu (2021); Munro et al. (2021); Sahoo & Wager (2022) take a mean-field game modeling approach and perform policy learning with a gradient descent method. Liao et al. (2022b) consider statistical inference in the Fisher market equilibrium which is useful for fair and efficient resource allocations. Statistical learning and inference has been investigated for other equilibrium models, such as general exchange economy (Guo et al., 2021; Liu et al., 2022) and matching markets (Cen & Shah, 2022; Dai & Jordan, 2021; Liu et al., 2021a; Jagadeesan et al., 2021; Min et al., 2022). Our work is also related to the rich literature of inference under interference (Hudgens & Halloran, 2008; Aronow & Samii, 2017; Athey et al., 2018; Leung, 2020; Hu et al., 2022; Li & Wager, 2022). In the FPPE model, the interference among buyers is caused by the supply and budget constraint and the revenue-maximizing incentive of the platform. In the economic literature, researchers have studied how to estimate auction market primitives from bid data; see (Athey & Haile, 2007) for a survey.

Appendix C Omitted properties of FPPE

Definition 3 (Observed FPPE, formal).

Given , an observed FPPE is a tuple such that

-

•

(First-price) For all , . Moreover, implies for all and .

-

•

(Supply and budget feasible) For all , . For all , .

-

•

(Revenue maximizing and market clearing) For all , implies . For all , implies .

We start by listing a number of known properties of the limit FPPE that we will use in our proofs.

A limit FPPE allocation and the limit FPPE pacing multiplier can be recovered through the convex programs, the population primal EG

| (P-EG) | |||

and the population dual EG

| (P-DualEG) |

where , and .

Lemma 2 (FPPE EG).

The limit FPPE is the unique solution to Eq. P-DualEG, and any limit FPPE belongs to the set of optimal solutions to Eq. P-EG (Gao & Kroer, 2022).

Lemma 3 (First-order conditions of limit FPPE, Theorem 10 from Gao & Kroer (2022)).

Given , the limit FPPE satisfies the following.

-

•

all .

-

•

all .

-

•

all .

-

•

all .

-

•

all .

-

•

all .

Lemma 4 (From EG to FPPE).

Recall the definition of in Eq. P-DualEG. Under (SMO).

Lemma 5 (Scale-invariance).

Scaling the budget and values at the same time does not change the market equilibrium. Scaling the value and the supply inversely does not change the market equilibrium. That is, given a positive scalar , if , then

Similarly, for a given observed FPPE defined in Def. 2, and any positive scalar , if , then

| (13) | |||

| (14) |

Lemma 6.

Let . Assume (SMO). holds. Then for all implies .

Proof.

If for all , then . By definition and (SMO)., and . It suffices to show , or equivalently . Recall is homogenous, i.e., for any positive scalar . By the Euler’s identity for homogenous functions, we have

Taking derivative again, we have for all . Finally, note , we have , where the second equality holds by the first-order condition that , and the third by the fact that for all implies . So . ∎

As for the limit FPPE, the observed FPPE is characterized by primal and dual convex programs:

| (15) | |||

| (16) |

See Conitzer et al. (2022a, Sec. 5) and Gao & Kroer (2022) for more details on the convex program characterization of observed FPPE. As with the limit FPPE, the observed FPPE has an analogous set of properties.

Lemma 7 (First-order conditions of observed FPPE, from EG to FPPE).

Given , the observed FPPE satisfies the following.

-

•

all .

-

•

all .

-

•

all .

-

•

all .

-

•

all .

-

•

all .

Moreover, recall the definition of in Eq. S-DualEG. Then

C.1 Proof of Lemma 1

Proof of Lemma 1.

The proof follows a similar argument as in Liao et al. (2022b) for non-quasilinear Fisher market (recall that an FPPE is a quasilinear Fisher market). Recall . We define

where is the second-highest entry (which could possibly be equal to the highest entry). For example, .

Note is differentiable at if and only if , since this holds if and only if the subdifferential is a singleton at . Let and . Then

By Proposition 2.3 from Bertsekas (1973) we know is differentiable at if and only if is measure one.

Proof of is measure zero. Recall . The claim follows from the fact that the SMO assumption implies differentiability, which implies that the complement of is measure one.

Proof of uniqueness of . By Lemma 3, we know only if for all other . Under the pacing profile , for all (but a measure-zero set of) items there is only one winning bidder, i.e., for almost all there is a unique such that and for all . Coupled with the limit FPPE first-order condition that we know is unique. This immediately implies uniqueness of as well.

Proof of existence of . By the assumption that is twice continuously differentiable at , there is a neighborhood such that is continuously differentiable on . By the same argument as for being measure zero, is measure zero for each .

∎

Appendix D More A/B testing estimands

We remark that the potential value functions are suitable for modeling either item-side or buyer-side treatments. In the context of ad auctions, item-size treatment are, for example, positions of the ads in the browser, whether links are attached to the ads and so on. Buyer-side treatments are, for example, a new layout of the ad campaign setup portal for the advertisers. The following discussion centers around item-side treatments since they are more prominent in practice, but readers should keep in mind that our theory extends to buyer-side treatments.

As discussed in Sec. 2.3, each FPPE has a convex program characterization. If the market is given treatment , then the limit FPPE pacing multipliers can be recovered by Let be the unique solution to the above program and also the unique FPPE pacing multiplier. The FPPE prices and revenue are and . The utility vector under treatment is . The NSW is .

Other metrics of treatment effects could be (i) treatment effects on revenue: , (ii) treatment effects on Nash social welfare: , (iii) treatment effects on pacing multiplier: , and (vi) treatment effects on utilities: . The estimators of treatment effects are and

For given , the (co)variances in Thm. 1 and Corollary 1 are functionals of the value functions. We will use to represents the (co)variances in the market formed with value functions . Each variance can be estimated the same way as in Sec. 3.3. Let , and denote the observed FPPE quantities for treatment .

Theorem 5 (Treatment effects CLT).

Step 1. Experiment. Choose the new feature assignment probability . Perform A/B testing with budget splitting and item randomization. Form two first-price pacing equilibria.

Step 2. Collect data. Observe the equilibrium data from the two markets, including prices, item allocations, pacing multipliers, leftover budgets, and values of the observed items.

Step 3. Compute CI. Compute the revenue variance as Eq. 11 for each market, obtaining and , and form the confidence interval

| (17) |

Appendix E Technical Lemmas

E.1 A CLT for constrained -estimator

We introduce a CLT result from (Shapiro, 1989) that handles -estimation when the true parameter is on the boundary of the constraint set. Throughout this section, when we refer to assumptions A1, A2, B2, etc, we mean those assumptions in Shapiro (1989).

Let be a probability space. Consider and a set . Let be a sample of independent random variables with values in having the common probability distribution . Let , and . Let be the unique minimizer of over (Assumption A4 in Shapiro (1989)). Let and be an optimal solution.

We begin with some blanket assumptions. Suppose the geometry of at is given by functions (Assumption B1), i.e., there exists a neighborhood such that

where and are finite index sets and the constraints in are active at , meaning for all . Assume the functions , are twice continuously differentiable in a neighborhood of (Assumption B2). Define the Lagrangian function by Let be the set of optimal Lagrange multipliers, i.e., iff (assuming differentiability) and .

Lemma 8 (Theorems 3.1 and 3.2 from Shapiro (1989)).

Assume there exists a neighborhood of such that the following holds.

-

8.a

Conditions on the sample function and the distribution .

-

•

(Assumption A1 in the original paper) For almost every , is a continuous function of , and for all , is a measurable function of .

-

•

(Assumption A2) The family , is uniformly integrable.

-

•

(Assumption A4) For all , there exist a positive constant such that for all .

-

•

(Assumption A5) For each fixed is continuously differentiable at for almost every .

-

•

(Assumption A6) The family , is uniformly integrable.

-

•

(Assumption D) The expectation is finite.

-

•

(Assumption B4) The function is twice continuously differentiable in a neighborhood of .

-

•

-

8.b

Conditions on the optimal solution.

-

•

(Assumption B3) A constraint qualification, the Mangasarian-Fromovitz condition: The gradient vectors , are linearly independent, and there exists a vector such that and

-

•

(Assumption B5) Second-order sufficient conditions: Let be the cone of critical directions

(18) The assumption requires that for all nonzero ,

-

•

-

8.c

Stochastic equicontinuity, a modified version of Assumption C1 in the original paper. For any sequence , the variable

(19) as . Here the supremum is taken over such that exists.

Then it holds that . Let

| (20) |

and

| (21) |

Then

Furthermore, suppose for all the function has a unique minimizer over . Then

Remark 1 (The stochastic equicontinuity condition).

By inspecting the proof, the original Assumption C1, , which requires uniform convergence over a fixed neighborhood , can be relaxed to the uniform convergence in a shrinking neighborhood of . The shrinking neighborhood condition is in fact standard, see, e.g., Pakes & Pollard (1989); Newey & McFadden (1994).

Remark 2.

Hessian matrix estimation at the optimum can be done via the numerical difference method.

Lemma 9 (Hessian estimation via numerical difference, adapted from Theorem 7.4 from Newey & McFadden (1994)).

Recall , and . We are interested in the Hessian matrix . Let be any point and let be an estimate of . Assume

-

9.a

;

-

9.b

is twice differentiable at with non-singular Hessian matrix ;

-

9.c

for some matrix ;

-

9.d

for any positive sequence , the stochastic equicontinuity condition Eq. 19 holds.

Suppose and . Then , where is the numerical difference estimator whose -th entry is

Proof of Lemma 9.

We provide a proof sketch following Theorem 7.4 from Newey & McFadden (1994) and Lemma 3.3 in Shapiro (1989). By Cond. 9.a and we know for any vector , it holds . Let . By a mean value theorem for locally Lipschitz functions (see Clarke (1990); the lemma is also used in the proof of Lemma 3.3 in Shapiro (1989)), there is a (sample-path dependent) on the segment joining and such that

for some . Then

| (by Cond. 9.d ) | ||||

| (by Cond. 9.c ) | ||||

| (22) |

Next by Cond. 9.b we have a quadratic expansion

| (23) |

Let , and . Then and . Applying the above bounds with , recalling the definition of , we have

| (by Eq. 22) | ||||

| (by Eq. 23) | ||||

In the above we use , and similarly for other terms. This completes the proof of Lemma 9. ∎

E.2 Showing stochastic equicontinuity via VC-subgraph function classes

Next we review classical results from the empirical process literature (Vaart & Wellner, 1996; Giné & Nickl, 2021).

We begin with the notions of Donsker function class and stochastic equicontinuity.

Let be a probability space. Let be a class of measurable functions of finite second moment. The class is called -Donsker if a certain central limit theorem holds for the class of random variables , where where ’s are i.i.d. draws from . Because Donskerness will be used as an intermediate step that we will not actually need to show directly or utilize directly, we refer the reader to Definition 3.7.29 from Giné & Nickl (2021) for a precise definition.

Lemma 10 (Donskerness stochastic equicontinuity, Theorem 3.7.31 from Giné & Nickl (2021)).

Let and consider the pseudo-metric space . Assume satisfies the condition for all . Then the following are equivalent

-

•

is -Donsker.

-

•

is totally bounded, and stochastic equicontinuity under the L2 function norm holds, i.e., for any ,

as , where .

Lemma 10 reduces the problem of showing stochastic equicontinuity under the L2 function norm to showing Donskerness. In order to show Donskerness, we will show that our function class is VC-subgraph, which implies Donskerness. At the end, we will connect stochastic equicontinuity under the L2 function norm to the stochastic equicontinuity that we need (see Lemma 16).

Let be a class of subsets of a set . Let be a finite set. We say that shatters if every subset of is the intersection of with some set . The subgraph of a real function on is the set

Definition 4 (VC-subgraph function classes, Definition 3.6.1 and 3.6.8 from Giné & Nickl (2021)).

A collection of sets is a Vapnik-Červonenkis class is if there exists such that does not shatter any subsets of of cardinality . A class of functions is -subgraph if the class of sets is .

Lemma 11 (VC subgraph + envelop square integrability Donskerness, Theorem 3.7.37 from Giné & Nickl (2021)).

If is VC-subgraph, and there exists a measurable such that for all with , then is -Donsker.

Since VC-subgraph implies Donskerness which is equivalent to stochastic equicontinuity, our problem reduces to showing the VC-subgraph property. The following lemmas show how to construct complex VC-subgraph function classes from simpler ones, and will be used in our proof.

Lemma 12 (Preservation of VC class of sets, Lemma 2.6.17 from Vaart & Wellner (1996)).

If and are VC classes of sets. Then is VC.

Lemma 13 (Preservation of VC-subgraph function classes, Lemma 2.6.18 from Vaart & Wellner (1996)).

Let and be -subgraph classes of functions on a set and be a fixed function. Then , , is VC-subgraph for fixed , and are VC-subgraph;

Lemma 14 (Problem 9 Section 2.6 from Vaart & Wellner (1996)).

If a collection of sets is a VC-class, then the collection of indicators of sets in is a VC-subgraph class of the same index.

In general, the VC-subgraph property is not preserved by multiplication, whereas Donskerness is. Thus, our proof will use the VC-subgraph property up until a final step where we need to invoke multiplication, which will instead be applied on the Donskerness property.

Lemma 15 (Corollary 9.32 from Kosorok (2008)).

Let and be Donsker, then is Donsker if both and are uniformly bounded.

For parametric function classes, if the parametrization is continuous in a certain sense, then stochastic equicontinuity holds w.r.t. the norm in the parameter space.

Lemma 16 (From -norm to parameter norm, Lemma 2.17 from Pakes & Pollard (1989); see also Lemma 1 from Chen et al. (2003)).

Suppose the function class , , is -Donsker, with an envelope such that . Suppose as . Then for any positive sequence , it holds

| (24) |

Lemma 17 (Andrews (1994)).

If for any Eq. 24 holds, then for any random elements such that , it holds

Lemma 18.

Given any fixed functions , , the following two function classes

are VC-subgraph and Donsker. Here and

Proof of Lemma 18.

We show is VC-subgraph. For each , the class is VC-subgraph (Proposition 4.20 from Wainwright (2019), and Example 19.17 from Van der Vaart (2000)). By the fact the VC-subgraph function classes are preserved by pairwise maximum (Lemma 13), we know is VC-subgraph. Moreover, the required envelop condition holds since for all , so is Donsker by Lemma 11.

We now show is VC-subgraph. For a vector-valued function class, we say it is VC-subgraph if each coordinate is VC-subgraph. First, the class of sets is VC, for all . By Lemma 12, we know the class of sets is VC. By Lemma 14, we obtain that the class is VC-subgraph. Finally, multiplying all functions by a fixed function preserves VC-subgraph classes (Lemma 13), and so is VC-subgraph. Repeat the argument for each coordinate, and we obtain that is VC-subgraph. Moreover, the required envelop condition holds since for all , and so is Donsker by Lemma 11. We conclude the proof of Lemma 18. ∎

Appendix F Proofs for Main Theorems

F.1 Proof of Thm. 1

Proof of Thm. 1.

We verify all the conditions in Lemma 8. Recall is the set of active constraints. The local geometry of at is described by the constraint functions , .

First, we verify the conditions on the probability distribution and the sample function. A1 holds obviously for the map . A2 holds by . A4 holds with Lipschitz constant . A5 holds since by (SMO). there is a neighborhood of such that for all , the set is measure zero (cf. Lemma 1). A6 holds by . B4 holds by (SMO)..

Second, we verify the conditions on the optimality. B3 holds since the constraint functions are , , whose gradient vectors are obviously linear independent. Moreover, the set is nonempty. B5 holds by being positive definite.

Finally, we verify the stochastic equicontinuity condition. Recall the definitions of the following two function classes from Lemma 18

Here . For any we have . In Lemma 18 we show that is VC-subgraph and Donsker. By Lemma 11 we know that a stochastic equicontinuity condition w.r.t. the norm holds, i.e.,

| (25) |

where , , . Next, we note for (almost every) fixed , by is measure zero (a condition implied by (SMO).). Moreover, note

where the exchange of limit and expectation is justified by bounded convergence theorem, and by Lemma 16, we can replace with in Eq. 25. Finally, note , and if is differentiable at , then for all . Then

| (26) | |||

| (by Eq. 25) |

and thus the required stochastic equicontinuity condition holds.

Now we are ready to invoke Lemma 8. We need to find the three objects, as in the lemma that characterize the limit distribution. The critical cone is

| ( (SCS).) |

where whose rows are . From here we can see the role of (SCS). is to ensure the critical cone is a hyperplane, which ensures asymptotic normality of .

If , i.e., lies in the interior of , then is identity matrix, and the limit distribution is ture.

Now assume . Note is an identity matrix of size and . The optimal Lagrangian multiplier is unique and so the piecewise quadratic function is . Finally, the gradient error term is

| (27) |

The unique minimizer of over is where

For completeness, we provide details for solving this quadratic problem. By writing down the KKT conditions, the optimality condition is

where is the Lagrangian multiplier. By a matrix equality, for any symmetric positive definite of size and of rank , it holds

| (28) |

with . We conclude that the asymptotic expansion

| (29) |

holds, where

and that the asymptotic distribution of is with . Note .

One could further write out the expression. Assume . Let . Then the matrix and where is the variance of winned item value of buyer .

Proof of . This follows from Lemma 8.

Proof of CLT for pacing multiplier . This follows from the above discussion.

Proof of CLT for revenue REV. We use a stochastic equicontinuity argument. Given the item sequence , define the (random) operator

where , . Note , , and we obtain the decomposition

For the term , it can be written as . By the linear representation for in Eq. 29, applying the delta method, we get the linear representation result

We will show . The difficulty lies in that the operator and the pacing multiplier depend on the same batch of items. This can be handled with the stochastic equicontinuity argument. The desired claim follows by verifying that the function class (same as that defined in Lemma 18) is VC-subgraph and Donsker. This is true by Lemma 18. By Lemma 10 we know for any ,

| (30) |

where . Noting that for all , it holds , we know that as . Then by Lemma 16, we know Eq. 30 holds with replaced with . Combined with the fact that , by Lemma 17 we know .

To summarize, we obtain the linear expansion

| (31) |

We complete the proof of Thm. 1.

∎

F.2 Proof of Corollary 1

Full statement of Corollary 1. Under the same conditions as Thm. 1, , and are asymptotically normal with (co)variances , , and , respectively.

Proof of Corollary 1.

Proof of CLT for individual utility . We use the delta method; see Theorem 3.1 from Van der Vaart (2000). Note with . By Eq. 29, it holds

| (32) |

Finally, noting we complete the proof.

Proof of CLT for Nash social welfare NSW. We use the delta method. Note with . By Eq. 29 it holds

| (33) |

Finally, noting we complete the proof of Corollary 1.

Proof of CLT for leftover budget . This is a direct consequence of Theorem 4.1 in Shapiro (1989). By that theorem, it holds that

with

where and . By a matrix equality, noting matrix ’s rows are distinct basis vectors, it holds

Moreover, for other entries of , i.e., , their asymptotic variance will be zero. The matrix is zero at the -th entry if or . Summarizing, the asymptotic variance of is .

An alternative proof is by the delta method and a stochastic equicontinuity argument. It holds and the linear expansion

| (34) |

holds. In the case where , i.e., for all , we have and so . ∎

F.3 Proof of Thm. 2

Proof of Thm. 2.

Based on Le Cam’s local asymptotic normality theory (Le Cam et al., 2000), to establish the local asymptotic minimax optimality of a statistical procedure, one needs to verify two things. First, the class of perturbed distributions (the class in our case) satisfies the locally asymptotically normal (LAN) condition (Vaart & Wellner, 1996; Le Cam et al., 2000). This part is completed by Lemma 8.3 from Duchi & Ruan (2021) since our construction of perturbed supply distributions follows theirs. Second, one should verify the asymptotic variance of the statistical procedure equals to the minimax optimal variance. To calculate this quantity, one needs to find the derivative of the map at . For this part we present a formal derivation below.

For a given perturbation , we let and be the limit FPPE price and revenue under supply distribution . Let be the score function. Obviously with our parametrization of we have by Eq. 8. We next find the derivative of at . Recall is defined in Eq. P-DualEG and the price is produced by the highest bid, i.e., .

Above we exchange the gradient and the expectation and then apply the chain rule. By a perturbation result by Lemma 8.1 and Prop. 1 from Duchi & Ruan (2021), under (SMO). and (SCS).,

with . Plugging in , (see App. C) and , we obtain

Now we have the two components required to invoke the local minimax result. Given a symmetric quasi-convex loss , we recall the local asymptotic risk for any procedure that aims to estimate the revenue:

Following the argument in Duchi & Ruan (2021, Sec. 8.3) it holds

We complete the proof of Thm. 2.

∎

F.4 Proof of Thm. 3

Proof of Thm. 3.

We first show by verifying conditions in Lemma 9. All conditions are easy to verify except the stochastic equicontinuity condition. By Lemma 18 we know the SE condition holds. We conclude .

Next we show . Recall indicates the set of inactive constraints. For such that , we know by the central limit theorem results Thm. 1 (actually the strong result holds). Then

| (by ) |

using the smoothing rate condition . For such that , we know by consistency of . Then

| (by and ) |

We conclude .

We now show . For any ,

| (by ) |

Next we show can be consistently estimated by

Define for

where

is a fixed selection of an element from the subgradient set, is a neighborhood of such that for all , the set is measure zero; see Lemma 1. 555 Note this is different from the condition there is a neighborhood such that the set is measure one. The map is defined on , and yet the set might not be measure one. This is the reason we use subgradients in the definition of . We also assume the subgradient selection coincides with the observed FPPE allocation selection, i.e.,

Noting and , we see that and are constructed so that and . Moreover, for any fixed , it holds (Bertsekas, 1973, Prop. 2.2). Next we use a decomposition of

We now argue that both terms converges in probability uniformly on . For the first term, consider a fixed , we know

which is measure zero, and that is continuous on by (SMO).. By Theorem 7.53 of Shapiro et al. (2021) (a uniform law of large number result for continuous random functions), it holds and . To summarize we have

Combined with the fact that we have . From this we conclude .

Proof of . We rewrite as

Proof of . In Lemma 18 we have shown both and are VC-subgraph, and thus a uniform law of large number holds. We rewrite

and

We have by invoking Lemma 18, applying a uniform LLN and using the fact that . And holds by , and , and applying Slutsky’s theorem. Finally, by is Donsker by Lemma 15 and thus a uniform law of large number holds, and that .

We complete the proof of Thm. 3. ∎

F.5 Proof of Thm. 4

Proof of Thm. 4.

By the EG characterization of FPPE, we know that , the pacing multiplier of the observed FPPE , solves the following dual EG program

| (35) |

The major technical challenge is that the number of summands in the first summation is also random. Given a fixed integer and a sequence of items , define

Here where and are the projected Hessian in Eq. 5, item utility function in Eq. 4, and total item utility vector in Eq. 1 in the limit market . Note . Note since scaling the supply and the budget at the same time does not change the equilibrium pacing multiplier. We introduce the following asymptotic equivalence results:

Lemma 19.

Here is the greatest integer less than or equal to . A similar result holds for the market limit and the influence function is defined similarly.

Proof of CLT for . It follows from the above discussion.

Proof of CLT for . We begin with the linear expansion Eq. 32 and repeat the same argument.

Proof of CLT for . We begin with the linear expansion Eq. 31 and repeat the same argument.

Proof of CLT for . We begin with the linear expansion Eq. 33 and repeat the same argument.

We complete the proof of Thm. 4. ∎