Analytic RFR Option Pricing with Smile and Skew

Current Version: )

Abstract

We extend the short rate model of Turfus and Romero-Bermúdez [2021] to facilitate accurate arbitrage-free analytic pricing of SOFR, SONIA or ESTR caplets, i.e. options on backward-looking compounded rates payments, in a manner consistent with the smile and skew levels observed in the market. These caplet pricing formulae and corresponding LIBOR or term-rate caplet results are translated into effective variance (implied vol) formulae, which are seen to be of a particularly simple form. They show that the model is essentially equivalent to imposing on a Hull-White model an effective variance which is a quadratic function of the moneyness parameter (rather than a constant) for any given maturity. Results are also illustrated graphically.

1 Introduction

The short rate model of Turfus and Romero-Bermúdez [2021] allows analytic pricing of caplets based on term rates such as LIBOR with smile and skew. We extend this model here to support analytic pricing of options on compounding risk-free rates (RFR) such as SOFR, SONIA or ESTR, in a manner consistent with the smile and skew levels observed in the market. Our approach is based on the observation that for small perturbations from equilibrium under this model the short rate is essentially a linear function of a (mean-reverting) Gaussian variable . This makes the situation similar to that captured by the model of Hull and White [1990]. An exact analytic pricing kernel for this model was derived by Van Steenkiste and Foresi [1999], Turfus [2019] and the extension of this kernel to address compounding rates by Turfus [2021a, 2022].

For a review of related work on options on compounded rates, the reader is referred to Turfus [2022], which follows the approach of Van Steenkiste and Foresi [1999] in introducing the integrated short rate as an additional state variable. Option prices are in this way derived analogous to the formulae of Henrard [2004], including taking account of delayed payment of the option premium. This work was extended to incorporate counterparty credit risk by Turfus [2021b] through a highly accurate asymptotic approximation.

In relation to analytic option pricing with smile and skew, the reader is referred to Turfus and Romero-Bermúdez [2021, 2022]. Their approach, which we extend below, is based on modelling the short rate as a function of a Gaussian Ornstein-Uhlenbeck process, which they argue is equivalent to assuming a quadratic dependence of the local volatility on the short rate. They make the point that little work has been done in this space, albeit that the Beta Blend model proposed by Horvath et al. [2017] interpolating between the model of Hull and White [1990] and that of Black and Karasinski [1991] can be viewed as allowing a term structure of skew to be specified. Also analytic LIBOR option and swaption prices incorporating smile and skew are available under the SABR model, as discussed by Antonov et al. [2019]. But this approach allows only one rate to be modelled at a time and does not constitute a short rate model capable of capturing multiple rates within a unified framework.

We single out for special mention here the work of Antonov and Spector [2011]. Like us they started out by considering Gaussian variables driven by Ornstein-Uhlenbeck dynamics and took the short rate to be a function thereof. One of the two cases they considered111The other case addressed was the well-known lognormal rates model of Black and Karasinski [1991] (see further §2 below). was a quotient of affine functions of exponentials of the Gaussian, under which assumption the short rate was constrained to lie between an upper and a lower limit. They did not like us attempt to capture volatility smile and skew explicitly. Nor did they consider a more general formulation involving an affine function of two exponentials with different exponents as we do here. Also, the (first-order) perturbation expansion they used to obtain analytic option prices was based on a small lognormal-volatility assumption, which limits the accuracy which can be obtained, particularly under low rates where lognormal volatilities can be quite high (in excess of 50%). We expect our expansion based on the smallness of the rates themselves to be more accurate, especially in circumstances of low rates.

We look to obtain analytic expressions for prices of SOFR options which take account of smile and skew by a method similar to that employed by Turfus and Romero-Bermúdez [2021] to price LIBOR caplets based on an extension of the Bachelier pricing kernel (for a Gaussian underlying). We do this by extending instead the Hull-White compounded rates kernel of Turfus [2022]. The challenge is that, as well as observing that the representations of the interest rate are similar (linear functions of a Gaussian variable) with and without smile or skew, we need to find a means of taking advantage of that observation systematically to obtain an explicit mathematical representation of the perturbation which must be applied to the known (Hull-White) analytic kernel. We do this using the operator expansion method expounded by Turfus [2021a].

We start off in §2 by setting out the pricing equation for our model. The associated pricing kernel is presented in §3 as a perturbation expansion based on a low-rates assumption, with a summary proof provided in Appendix A. The calibration of the model to the term structure of forward rates and volatility (with skew and smile) is considered in §4, where bond price formulae are also set out. The further application of the kernel to the pricing of forward rates and SOFR/ESTR caplets is considered in §5, with a proof of the latter in Appendix B. A LIBOR caplet pricing formula is also deduced providing more accuracy than that of Turfus and Romero-Bermúdez [2021]. The caplet prices are also give a convenient expression as implied volatilities, which simplifies calculation and helps ensure consistency of behaviour far from the money. Numerical calculations of caplet prices and implied volatility surfaces based on the formulae deduced are illustrated in §6. Conclusions are set out in §7.

2 Model Description

We consider the short rate model of Turfus and Romero-Bermúdez [2021] which incorporates smile and skew into the Hull-White model through a variable transformation. We shall find it convenient to work with the reduced variable defined through the following Ornstein-Uhlenbeck process:

| (2.1) |

with a Wiener process for . This auxiliary variable is related to the short rate by where

| (2.2) |

Here are the instantaneous forward rate and a skewness function, respectively, and are functions representing volatility, mean reversion rate, a smile factor and a convexity adjustment factor, respectively, all assumed to be piecewise continuous and bounded. We further assume that , with the “as of” date for which the model is calibrated. The function is determined by calibration to the forward curve but will tend in the zero volatility limit to zero.222Strictly speaking, the function is the drift adjustment parameter which must be chosen to satisfy the no-arbitrage condition for a given choice of , so the latter should really be thought of as controlling the skew. However, the calculation of as a power series of nested integrals involving is much more convenient than attempting to perform the equivalent process in reverse, so in practice we consider to be inferred directly from the no-arbitrage condition, constructing the implied using the mathematical techniques expounded below. The formal no-arbitrage constraint which determines this function is as follows

| (2.3) |

under the martingale measure for , where is the longest maturity date for which the model is calibrated, and

| (2.4) |

is the -forward price of the -maturity zero coupon bond. This is to be contrasted with the Hull and White [1990] (H-W) model which is obtained by taking the limit as in (2.2):

and the Black and Karasinski [1991] (B-K) model which is obtained by choosing

Notably our model reverts to the first of these in the limit as .

Since we are interested in pricing options on daily-compounded rates payments, we introduce a new variable representing the integral of the short rate, making use of the fact that daily compounding can be to a good approximation captured by assuming continuous compounding. We shall make the choice

| (2.5) |

We consider the (stochastic) time- price of a European-style security which pays a cash amount at maturity , denoting this by . We note in particular that the price of a -maturity zero coupon bond is obtained by taking . We will look to derive the functional form of implied by our model in this case and in the process to determine the conditions on necessary to satisfy (2.3).

From the Feynman-Kac theorem we infer that emerges as the solution to the following backward Kolmogorov diffusion equation:

| (2.6) |

with given by (2.2), subject to the termiinal condition .

3 Pricing Kernel

We define at this point the following notation for future reference:

| (3.1) | ||||

| (3.2) | ||||

| (3.3) | ||||

| (3.4) | ||||

| (3.5) | ||||

| (3.8) | ||||

| (3.9) | ||||

| (3.10) | ||||

| (3.11) | ||||

| (3.12) |

We observe here that represents the impact of mean reversion and that of the counteracting dispersion from the mean induced by smile.

We look to obtain the pricing kernel or Green’s function for (2.6), defined as a (generalised) function such that the solution subject to the specified terminal condition can be obtained from the following convolution expression:

| (3.13) |

In the absence of exact analytic solutions, we seek the pricing kernel as a perturbation expansion in the limit that the deviations of the short rate from the forward rate curve are small under some suitable norm. To that end let us define the small parameter

| (3.14) |

and seek an asymptotic expansion of the pricing kernel in powers of . To allow of a skew adjustment that contributes at the same order of approximation as the smile adjustment we shall make the assumption that 333We have avoided being explicit about the range of over which the norms are assessed. A typical choice would be a weighted integral over for some finite . Let us further express asymptotically as

| (3.15) |

with .

To express our result conveniently, we introduce the functions

| (3.16) |

and shift operators defined for by

| (3.17) | ||||

| (3.18) | ||||

| (3.19) |

Using this notation we define also the following operators:

| (3.20) | ||||

| (3.21) | ||||

| (3.22) | ||||

| (3.23) |

Using the operator expansion method of Turfus [2021a] in the same manner as Turfus and Romero-Bermúdez [2021] we obtain the following result.

Theorem 3.1 (Pricing Kernel).

Making use of the above-defined notation, the pricing kernel for (2.6) can be written asymptotically in the limit as as

| (3.24) |

with the and in particular

| (3.25) | ||||

| (3.26) | ||||

| (3.27) | ||||

| (3.28) | ||||

| (3.29) | ||||

| (3.30) |

with

| (3.31) |

and a bivariate Gaussian probability density function with covariance .

Proof.

What has effectively been achieved here is that representations of the drift and diffusion associated with and the Hull-White stochastic discounting, as captured by , are subtracted out of the time-ordered exponential operator in (A.9) and incorporated directly into the modified Gaussian kernel on which it acts. In this way a zeroth order operator is replaced by the first order operator in (A.16). Only by use of this device does the asymptotic expansion of the (modified) operator become possible.

It will be observed that the leading-order contribution () is in its functional form identical to the Hull-White kernel of Turfus [2022], with the caveat that the mean reversion function is adjusted up (reducing its impact) by inclusion of the smile factor in (3.9), with no impact from skew. This means that solutions based on our expansion are likely to retain better accuracy even at longer maturities than those of Turfus and Romero-Bermúdez [2021]. Note that we could have expressed our results as a perturbation operator acting on the Hull-White kernel but choose, for reasons of convenience of use, to multiply by the stochastic discounting operator in the ansatz (3.24) after applying the perturbation operators term-by-term.

4 Fitting to the Forward Curve

Let us further define for future notational convenience

| (4.1) | ||||

| (4.2) | ||||

| (4.3) |

Note that -shifts apply in the integral term in (4.3), but can in practice be ignored, since they give rise to terms impacting at higher than second order; also that, in deriving (4.2), we have made use of the identity (A.27).

The calibration of our model to the forward interest rate market is achieved by considering zero coupon bond prices.

Theorem 4.1 (Calibration).

Applying (3.24) to a unit payoff at , the -maturity zero coupon bond price associated with the pricing kernel (3.24) is seen to be given asymptotically by

| (4.4) |

Differentiating the calibration condition w.r.t. , applying this to second order accuracy and setting gives rise to the requirement that the first two terms of (3.15) are given by

| (4.5) | ||||

| (4.6) | ||||

| (4.7) | ||||

| (4.8) |

where for ,

| (4.9) |

We observe that, excluding the bracketed expression which provides the main skew-smile adjustment, (4.4) is essentially a Hull-White representation of the bond price making use of a modified mean reversion factor in place of the usual as the integrand in (3.9). A first-order representation which should suffice for many purposes, is obtained by neglecting in (4.4). Provided the leading-order skew-smile correction terms remain small, the approximation should be a good one: the variable would have to take on improbably large values for this not to be the case. Note that these results are, up to second order, equivalent to those presented in Turfus and Romero-Bermúdez [2021], as might be expected since the model is unchanged here, only the method of building the expansion slightly different.

5 Applications

5.1 Forward Rates

An expression for forward rates is easily deduced from our zero coupon bond formula.

Corollary 5.1 (Instantaneous Forward Rate).

The instantaneous forward rate is given by

| (5.1) | ||||

| (5.2) |

with as given by Theorem 4.1. The corresponding first order version of this result is obtained by ignoring the second two terms in parentheses and taking a first order representation of .

Proof.

This result is obtained by noting that the instantaneous forward rate is given by where

and making use of (4.4). ∎

5.2 Option Pricing

We assume below that, in option pricing, the interest rate that is used as the underlying is the same one that is used in the discounting of cash flows. If, particularly in the case of LIBOR, there is a spread over the risk-free rate, this situation can effectively be managed by calibrating the model to the risk-free rate and subtracting the (assumed deterministic) spread off of the strike (or coupon rate).

Compounded Rate Caplet Pricing

RFR cap and caplet prices are obtained to leading order from the following theorem.

Theorem 5.1 (RFR Caplet Price).

Consider a caplet based on the compounded risk-free rate over a payment period and a payoff with strike at time of

| (5.3) | ||||

| (5.4) |

where , and , with providing the relevant year fraction. Using the above-defined notation and defining the critical value of at which the option comes into the money as

| (5.5) |

the caplet PV will be given asymptotically with relative errors by

| (5.6) | ||||

| (5.7) | ||||

| (5.8) | ||||

| (5.9) |

with a cumulative normal distribution function, the corresponding density and the Heaviside step function, where we define

| (5.10) | ||||

| (5.11) | ||||

| (5.12) |

and is defined analogously to above except in that we re-define

| (5.13) | ||||

| (5.14) |

Proof.

The proof of this result is set out in Appendix B. Cap prices are of course obtained as an algebraic sum of caplet prices. ∎

LIBOR Caplet Pricing

LIBOR or term-rate cap and caplet prices are obtained similarly.

Theorem 5.2 (LIBOR Caplet Price).

Consider a caplet based on the term rate over a payment period and a payoff with strike at time of

| (5.15) |

where . This gives rise to a -value of

Using the above-defined notation, the caplet PV will be given asymptotically with relative errors by

| (5.16) | ||||

| (5.17) | ||||

| (5.18) | ||||

| (5.19) |

where we define additionally

| (5.20) | ||||

| (5.21) |

Proof.

This result can be understood as a special case of Theorem 5.1 when a zero value is assigned to the volatility for . ∎

Swaption Pricing

Swaption prices are obtained similarly.

Theorem 5.3 (Swaption Price).

Consider a payer swaption based on a LIBOR or compounded-rate swap with payment periods for and a fixed coupon with payoff at time given by the swap value at time if this is in the money.

Using the above-defined notation, the swaption PV will be given asymptotically with relative errors by

| (5.22) | ||||

| (5.23) | ||||

| (5.24) | ||||

| (5.25) | ||||

| (5.26) | ||||

| (5.27) | ||||

| (5.28) | ||||

| (5.29) |

where we define additionally for

| (5.30) |

where is the value of at which the swap comes into the money.

Proof.

The proof of this result is analogous to that provided in Appendix B. This follows from the similarity of the swaption payoff:

with Eq. (5.15). A key observation is that the value of a risk-free interest rate payment stream, starting at with final payment at and discounted at the risk-free interest rate is , i.e. the difference between the value of a unit payment at time and one at time . We note further that this observation is equally true of compounded-rate and term-rate swaptions, since the term-rate payment is by definition the expected value of a compounded-rate payment, observed on its initial fixing date. ∎

5.3 Implied Volatility Formulae

We look to translate the formulae set out in (5.9) and (5.19) above into expressions for effective/implied Hull-White term variances. This has the advantage of making it more intuitively obvious how the smile and skew impact on the caplet pricing as a function of moneyness. Indeed, one of the first things practitioners typically want to do with option prices is to translate them into effective/implied volatility equivalents. A second advantage is that if, rather than using our asymptotic formulae directly, we use the Hull-White formulae with our best estimate of the effective variance substituted for the Hull-White variance, we naturally obtain better extrapolated behaviour far from the money, with arbitrage avoided.444The quadratic expressions (5.41) and (5.47) obtained below may arguably give rise for values of of order unity to effective variance specifications which are negative. But such circumstances are of no practical relevance and would in any event compromise the asymptotic approach entirely, not just the implied volatility specification.

We note in passing that one of the main reasons for the popularity of the SABR model of Hagan et al. [2002] was precisely that the asymptotic representation of option prices was explicitly as a formula for the implied Black-Scholes volatility. The approach we take is along the lines of that made use of by Alòs et al. [2015].

Effective Compounded Rates Variance

Starting with the expression (5.9) for the compounded caplet price, we look to re-express this as

| (5.31) |

with relative errors , where

| (5.32) | ||||

| (5.33) |

for some variance adjustment function defined against a baseline compounded-rate term variance

| (5.34) |

so that the effective variance is

| (5.35) |

To determine the appropriate functional form for , we expand (5.9) and (5.31) as Taylor expansions and equate terms. To that end we note expanding (5.31) to first order in terms of the small parameter that

| (5.36) |

with given by , while the expansion of (5.9) gives rise with relative error to

where

| (5.37) | ||||

| (5.38) | ||||

| (5.39) |

with

| (5.40) |

and defined by (4.9) above.

Equating terms in the two expansions, we conclude that we must have

| (5.41) |

from which we deduce an effective compounding rate caplet term variance given by (5.35) with relative error. It is at this point evident how the linear term involving gives rise to the skew and the quadratic term involving to the smile. We suggest on this basis that taking the parameter to be given here by would furnish a good guide as to the level of accuracy of the first order effective variance expansion, with relative errors being expected to be of magnitude .

Effective LIBOR Variance

Starting instead with the expression (5.19) for the LIBOR or term-rate caplet price, we look to re-express this as

| (5.42) |

with relative errors , where

| (5.43) | ||||

| (5.44) |

for some variance adjustment function defined against a baseline LIBOR term variance

| (5.45) |

so that the effective variance is

| (5.46) |

By a calculation analogous to the above, we conclude that we must have

| (5.47) |

with given by and

| (5.48) | ||||

| (5.49) | ||||

| (5.50) |

with

| (5.51) |

Effective Swaption Variance

Starting instead with the expression (5.29) for the swaption price, we look to re-express this as

| (5.52) |

with relative errors , where

| (5.53) |

for some variance adjustment function with , with the effective short rate term variance taken to be

| (5.54) |

Defining to be the result obtained by setting in (5.53), we can expand (5.52) as

| (5.55) | ||||

| (5.56) |

where we have made use of the fact that

| (5.57) |

with

| (5.58) |

and the Kronecker delta. We observe that the sum in the second line of (5.55) can be written more compactly as

Expanding (5.29) as in the previous cases leads to the conclusion that the second line in (5.55) must be equated with

This can be written asymptotically, making use of (5.57), as

which we write more compactly as

Asymptotic matching then requires that be chosen to satisfy

| (5.59) |

As can be seen, the effective term variance is on this occasion not quite quadratic in its dependence on log-moneyness. Further, the form of the denominator will cause it to give rise to singular behaviour for values of sufficiently far from the ATM level. However, since the model would not in any event be calibrated to give credible results in such extreme cases, this ought not to be a significant limitation in practice.

6 Numerical Calculations

Caplets

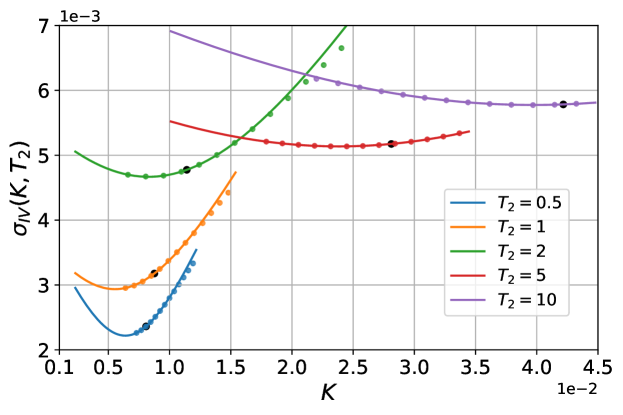

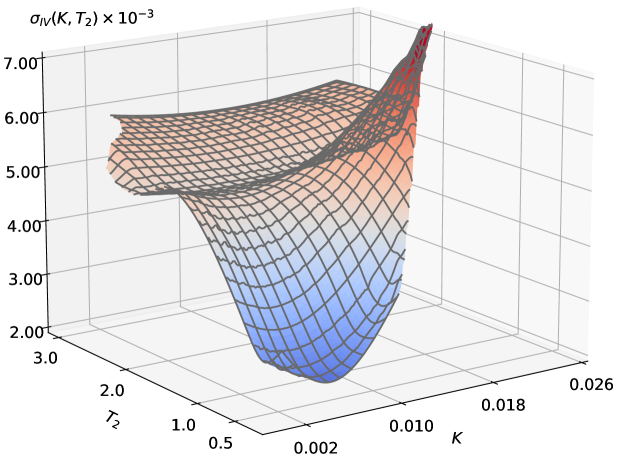

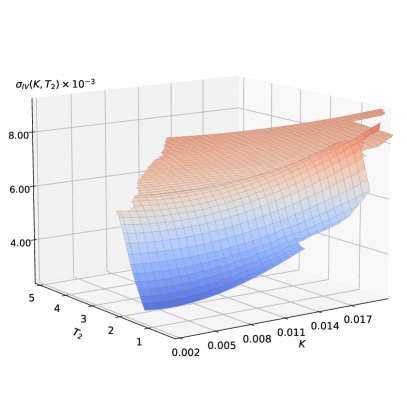

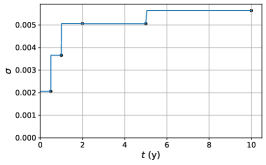

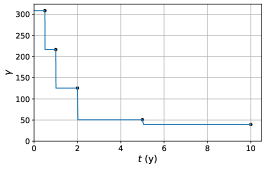

The above model has been calibrated to caplet market data capturing the skew and smile for SAR 6M LIBOR rates in May 2021. For the mean reversion, we choose a representative fixed value of . Choosing other values made little difference to the results obtained. Since the model has three other disposable parameters (, and ) it should be possible making use of (5.41) to match the ATM level, smile and skew of the implied volatility surface at each maturity for which market data are provided. Indeed this is found to be the case.555In fact the fitting was done to LIBOR caplet data treated as compounded-rate caplets, since the latter were not available and this approach satisfied the exigency of convenient presentation of numerical results for compounded-rate formulae. In any event, it was found to be no more difficult to calibrate the model interpreting the data as being for LIBOR caplets. The resulting fit is illustrated in Fig. 1 and is seen to be excellent. Results are expressed as , the constant value of which would have to be inserted in the Hull-White formula to replicate the price of a (6M tenor) caplet with strike and maturity . For the smile, calibrated values of ranged from around 300 at the short end to 40 for y while, for the skew, the corresponding values of were 0.5 and 0.08. The corresponding implied volatility surface is illustrated in Fig. 2.

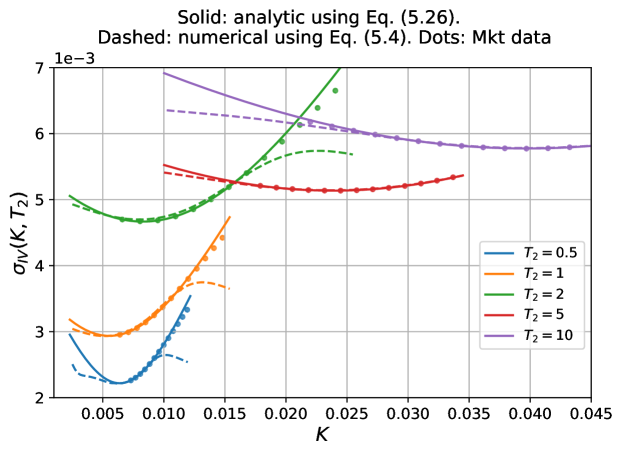

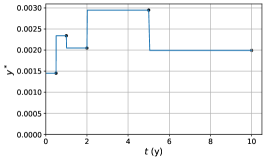

Values of were also explicitly backed out from the compounded-rate caplet price formula (5.9). These are shown for comparison in Fig. 3. As can be seen, the fit is similarly good close to the money but the asymptotic caplet price formula clearly becomes unreliable for more extreme strikes so caution should be exercised in its direct use to calculate prices. Rather, the use of an asymptotic representation of the implied volatility surface, embedding as it does the avoidance of arbitrage (negative option prices) for any reasonable strikes, is to be preferred.666For the same reason analytic option prices under the SABR model are always constructed indirectly from asymptotic representation of implied volatilities.

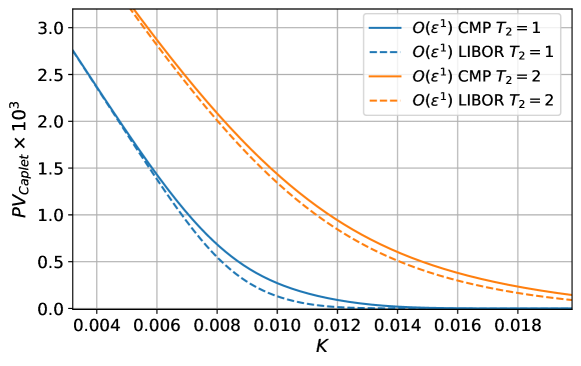

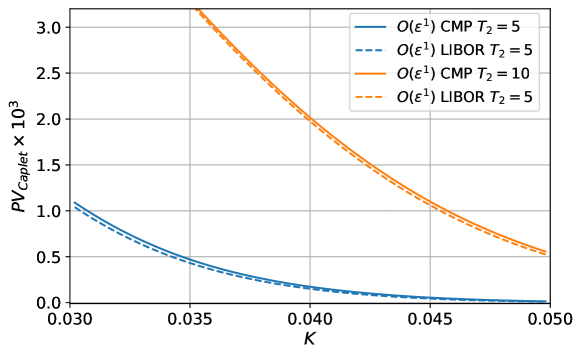

It is of interest to consider how much impact results from use of a compounded rate rather than a term rate as the caplet underlying. This is illustrated in Figs. 4 and 5 where PVs based on formulae (5.31) and (5.42) are compared. As is evident, the impact is much greater for shorter maturities where is comparable with , and becomes rather insignificant when

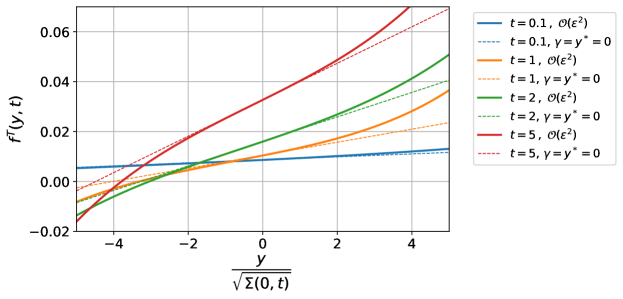

For completeness we also looked at instantaneous forward rates calculated in accordance with (5.1), with fixing date . Results are shown in Fig. 6. Since these results incorporate second order terms, unlike the caplet results shown above, they are expected to be highly accurate. The impact of the skew/smile can be inferred by comparing with the dashed lines (Hull-White). As expected, the model is seen to behave just like Hull-White with forward rates linear in the underlying Gaussian variable when this is small in magnitude.

Swaptions

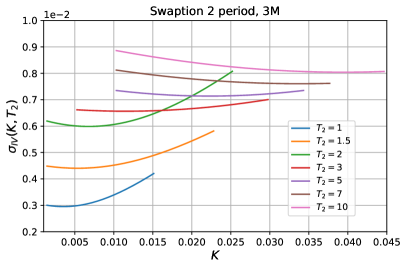

The implied volatility surface of swaptions with two payment periods of 3 months is shown in Fig. 7.

7 Conclusions

We have successfully extended the short rate model of Turfus and Romero-Bermúdez [2021] to address the pricing of SOFR/SONIA/ESTR caplets based on compounded rates. This we achieved by expressing the result as a perturbation of the analytic kernel of Turfus [2022]. The model is seen to have the following properties:

-

1.

Convenient analytic representations are available for bond and option prices.

-

2.

A single calibration addresses options of any maturity and tenor.

-

3.

Option pricing takes account of volatility skew and smile.

-

4.

Prices can be calculated for LIBOR or term-rate options as well as for options on backward-looking compounded rates.

We believe our model to be unique in satisfying all of the above criteria.

The asymptotic expansion developed here provides the further benefit of pricing forward rates and LIBOR caplets more accurately than that of Turfus and Romero-Bermúdez [2021]. The expression for forward rates is (5.1). Caplet prices are best calculated noting that the effective Hull-White term variance is given by (5.35) and (5.41) for a compounded-rate caplet and by (5.46) and (5.47) for a LIBOR or term-rate caplet.

Appendix A Proof of Pricing Kernel Result

We offer a sketch of the proof that (3.24) represents the pricing kernel for (2.6). We follow Turfus [2019, 2021a] in introducing the following definitions and notation.

Definition A.1.

The time-ordered exponential or Dyson series defined for a linear operator by

| (A.1) | ||||

| (A.2) | ||||

| (A.3) |

generalises the exponentiation of the integral of a function to the case of a time-dependent linear operator .

Definition A.2.

We define the commutator of an operator with an operator where both operators act on the same function space by the following operator:

| (A.4) |

We will have need to combine these two ideas in computing the time-ordered exponential of a commutator operator, interpreted as follows:

| (A.5) |

Proof of Theorem 3.1.

We start by observing that, although , the term is so prevents direct use of a naïve perturbation expansion. Noting however that for small we can subtract out the asymptotic representation and look to handle it separately. To that end we write the evolution operator associated with (2.6) as where

| (A.6) | ||||

| (A.7) |

Following Turfus and Romero-Bermúdez [2021] who apply the exponential expansion formula of Turfus [2021a] to a closely analogous evolution operator, we can write the Green’s function solution of (2.6) as

| (A.8) |

where777Observe that the only difference at this stage compared to their result is in the inclusion of the derivative w.r.t. in (A.9). However there is an important difference in the solution strategy. By subtracting out of (A.19) below a Hull-White (linear) representation of the discounting rate in addition to the -drift, we are able to incorporate both directly into the analytic kernel. So, rather than the stochastic discounting being represented by a perturbation as in Turfus and Romero-Bermúdez [2021], it is only the difference between that and the Hull-White representation thereof which is so represented.

| (A.9) |

with

| (A.10) |

Let us define

| (A.11) | ||||

| (A.12) |

We deduce

| (A.13) | ||||

| (A.14) | ||||

| (A.15) | ||||

| (A.16) |

Next defining

| (A.17) | ||||

| (A.18) | ||||

| (A.19) |

we deduce

| (A.20) | ||||

| (A.21) | ||||

| (A.22) | ||||

| (A.23) |

where

| (A.24) | ||||

| (A.25) |

We observe, making use of the identity888This is readily proved by differentiating both sides w.r.t. .

| (A.27) |

that

| (A.28) |

whence we deduce

Applying to the Gaussian kernel, so increasing its dimension from 1 to 2, gives rise to

| (A.29) |

with defined by (3.25) above. It is convenient to move the exponential function to the left of this expression. To this end we note that the exponential of a derivative acts as a shift operator, whence

We obtain

| (A.30) | ||||

| (A.31) | ||||

| (A.32) |

with defined by (3.16), where we have made use of the fact that

Expanding as a power series in (A.30) and making use of the above identities, we obtain (3.24), with (3.25)–(3.30) as the first three terms, as claimed. This completes the proof. ∎

Appendix B Proof of RFR Caplet Pricing Result

Proof of Theorem 5.1.

Making use of (3.24), the first order caplet value as of time with and will be

| (B.1) | ||||

| (B.2) | ||||

| (B.3) | ||||

| (B.4) |

We see the -dependence drops out at this stage. Letting denote the result of applying to the th order contribution to , we find

with and defined by (5.10) and (5.11), respectively. Applying the first-order operator and making use of the identity

| (B.6) |

yields at first order999We use the convention here that the integration in the operator expression is applied after the operator has been applied to the operand; likewise for the assignment of the -value.

Here the effect of the shift operators is to transform

where

| (B.7) |

Combining this with the leading-order term (and noting that there is no first-order payoff contribution), we obtain . Taking this in turn as the payoff at and valuing as of time gives rise to

| (B.8) | ||||

| (B.9) |

The -integration is in this case trivial. In particular we have the quasi-Hull-White result

| (B.10) |

whence

| (B.11) |

Considering next the action of the first-order Green’s function term on the leading-order term, we obtain

| (B.12) | ||||

| (B.13) |

Setting , we find

| (B.14) | ||||

| (B.15) |

Considering next the action of the leading-order Green’s function term on the first-order term , we obtain

| (B.16) | ||||

| (B.17) | ||||

| (B.18) | ||||

| (B.19) | ||||

| (B.20) | ||||

| (B.21) | ||||

| (B.22) | ||||

| (B.23) |

with relative errors, where

| (B.24) |

We conclude, making use of the fact that , that

| (B.25) | ||||

| (B.26) | ||||

| (B.27) | ||||

| (B.28) |

We make use here of the identity that, for ,

where

| (B.29) | ||||

| (B.30) |

We neglect this subdominant adjustment factor in our asymptotic estimate, arguing that the result would otherwise not be consistent with the price of deep in-the-money forward contracts. Combining all terms and simplifying gives rise to (5.9). This completes the proof. ∎

Appendix C Calibration to Caplet market data

The calibration of the forward curve has already been explained in Sec. 4. As mentioned before, for the mean reversion, we choose a representative fixed value of . The calibration of , and follows from matching the analytical implied volatility formula to the implied volatilities quoted in the market for 6-month caps. We take piece-wise parametrisations for these parameters and calibrate on the available maturities. The result of the calibration is given in Fig. 9.

References

- Alòs et al. [2015] E. Alòs, R. De Santiago, and J. Vives. Calibration of stochastic volatility models via second-order approximation: the Heston case. International Journal of Theoretical and Applied Finance, 18(6):1550036, 2015.

- Antonov and Spector [2011] A. Antonov and M. Spector. General Short-Rate Analytics. Risk, April:66–71, 2011.

- Antonov et al. [2019] A. Antonov, M. Konikov, and M. Spector. Modern SABR Analytics: Formulas and Insights for Quants, Former Physicists and Mathematicians. Springer, 2019. ISBN 978-3030106553.

- Black and Karasinski [1991] F. Black and P. Karasinski. Bond and Option Pricing when Short Rates are Lognormal. Financial Analysts Journal, 47(4):52–59, 1991.

- Hagan et al. [2002] P. S. Hagan, D. Kumar, A. S. Lesniewski, and D. E. Woodward. Managing Smile Risk. Wilmott Magazine, July:84–108, 2002.

- Henrard [2004] M. P. A. Henrard. Overnight Indexed Swaps and Floored Compounded Instrument in HJM One-Factor Model. Research paper, University Library of Munich, 2004. URL https://ideas.repec.org/p/wpa/wuwpfi/0402008.html.

- Horvath et al. [2017] B. Horvath, A. Jacquier, and C. Turfus. Analytic Option Prices for the Black-Karasinski Short Rate Model. Research Paper, SSRN, 2017. URL https://ssrn.com/abstract=3253833.

- Hull and White [1990] J. Hull and A. White. Pricing Interest Rate Derivative Securities. The Review of Financial Studies, 3:573–592, 1990.

- Turfus [2019] C. Turfus. Closed-Form Arrow-Debreu Pricing for the Hull-White Short Rate Model. Quantitative Finance, 19(12):2087–2094, 2019.

- Turfus [2021a] C. Turfus. Perturbation Methods in Credit Derivatives: Strategies for efficient risk management. Wiley Finance, 2021a. ISBN 978-1-119-60961-2.

- Turfus [2021b] C. Turfus. Risky Caplet Pricing with Backward-Looking Rates. Risk, August, 2021b.

- Turfus [2022] C. Turfus. Caplet Pricing with Backward-Looking Rates. Wilmott Magazine, September:106–109, 2022.

- Turfus and Romero-Bermúdez [2021] C. Turfus and A. Romero-Bermúdez. Analytic Short Rate Model with Smile and Skew. Research paper, SSRN, 2021. URL https://ssrn.com/abstract=3840044.

- Turfus and Romero-Bermúdez [2022] C. Turfus and A. Romero-Bermúdez. What Short Rate Model Should I Use? Wilmott Magazine, March:28–38, 2022.

- Van Steenkiste and Foresi [1999] R. J. Van Steenkiste and S. Foresi. Arrow-Debreu prices for affine models. Research Paper, SSRN, 1999. URL http://dx.doi.org/10.2139/ssrn.158630.