Ruan, Chen, Ho

Risk-Averse MDPs under Reward Ambiguity

Risk-Averse MDPs under Reward Ambiguity

Haolin Ruan

\AFFSchool of Data Science, City University of Hong Kong, Kowloon Tong, Hong Kong

haolin.ruan@my.cityu.edu.hk \AUTHORZhi Chen

\AFFDepartment of Management Sciences, College of Business, City University of Hong Kong, Kowloon Tong, Hong Kong

zhi.chen@cityu.edu.hk

\AUTHORChin Pang Ho

\AFFSchool of Data Science, City University of Hong Kong, Kowloon Tong, Hong Kong

clint.ho@cityu.edu.hk

We propose a distributionally robust return-risk model for Markov decision processes (MDPs) under risk and reward ambiguity. The proposed model optimizes the weighted average of mean and percentile performances, and it covers the distributionally robust MDPs and the distributionally robust chance-constrained MDPs (both under reward ambiguity) as special cases. By considering that the unknown reward distribution lies in a Wasserstein ambiguity set, we derive the tractable reformulation for our model. In particular, we show that that the return-risk model can also account for risk from uncertain transition kernel when one only seeks deterministic policies, and that a distributionally robust MDP under the percentile criterion can be reformulated as its nominal counterpart at an adjusted risk level. A scalable first-order algorithm is designed to solve large-scale problems, and we demonstrate the advantages of our proposed model and algorithm through numerical experiments.

1 Introduction

Markov decision processes (MDPs) provide a powerful modeling framework for sequential decision-making problems and reinforcement learning in stochastic dynamic environments (puterman2014markov). Obtaining the model parameters of MDPs that perfectly reflect the environments, however, has always been a challenge in practice, as these parameters are estimated from limited data that are potentially contaminated (mannor2007bias). Moreover, these parameters, such as transition kernel and reward function, are often time-dependent or even uncertain, but they are approximated as fixed values in an overly simplified setting (mannor2016robust). Therefore, the output policies of MDPs are often disappointing in practice.

Robust MDPs address the aforementioned issues of parameter ambiguity, by allowing the unknown values of transition kernels and reward functions to lie in a given ambiguity set (behzadian2021optimizing, chen2019distributionally, clement2021DRMDP, delgado2016real). Then, robust MDPs seek for policies that maximize the worst-case expected return over all transition kernels and reward functions in the ambiguity sets. By specifying ambiguity sets that contain the unknown transition kernels with high confidence, the optimal policies of robust MDPs are robust to parameter ambiguity (iyengar2005robust).

In this paper, we focus on the case where the reward function is ambiguous, which sometimes is referred to as imprecise-reward MDPs (alizadeh2015approximate, regan2010robust, regan2011eliciting, regan2011robust, regan2012regret). This particular setting is also closely related to imitation learning, which trains an agent to learn a certain behavior of an expert, while only some demonstrated trajectories of her is available (chen2020bail, ho2016generative, osa2018algorithmic, rashidinejad2021bridging). When applying inverse reinforcement learning approach to learn the reward function that completely represents the expert’s preference (brown2020bayesian, choi2012nonparametric, ng2000algorithms), the yielded policies, which suffer from reward ambiguity, may perform poorly in practice.

To handle reward ambiguity, we utilize techniques from distributionally robust optimization (DRO) (derman2020distributional) and distributionally robust chance-constrained program (chen2007robust, postek2018robust), assuming that the true reward distribution resides in an ambiguity set. This approach does not require the reward function to be precisely specified. Instead, only the descriptions of common distribution information such as support, moments and shape in the ambiguity set are needed, which are often much easier to be obtained/estimated (hanasusanto2015distributionally, hanasusanto2017ambiguous, zymler2013distributionally). In this paper, we consider a Wasserstein ambiguity set for our distributionally robust models as in abdullah2019wasserstein, calafiore2006distributionally, xie2021distributionally. Unlike phi-divergence ambiguity sets which may contain too extreme member distributions, the closeness between points in the support set is incorporated in Wasserstein sets, thus their member distributions may be more reasonable (gao2022distributionally); on the other hand, Wasserstein sets are often a better choice than moment-based ambiguity sets when the number of samples is too small to obtain a reliable estimation on moments (yang2020wasserstein). We choose Wasserstein sets for these reasons, although other types of ambiguity sets such as nested ambiguity sets (xu2010distributionally, xu2012distributionally) and the ambiguity sets based on Prohorov metric (erdougan2006ambiguous) are also considered in literature. For our distributionally robust chance-constrained MDPs, we will furthermore show its equivalence with the nominal counterparts with an adjusted risk level. To the best of our knowledge, this is the first result in MDPs that establishes the mutual transformation between distributional ambiguity and risk.

Our return-risk model (RR) is a risk-averse MDP model that not only takes into account reward ambiguity, but also considers both the average and risk of the return. MDPs that minimize the risk of the return instead of the expected cost are called risk-aware MDPs (also called risk-sensitive or risk-averse MDPs) (ahmadi2021constrained, baauerle2017partially, carpin2016risk, haskell2015convex, huang2017risk). In risk-aware optimization, the objective function is taken as a risk measure, such as value-at-risk (VaR) (delage2007percentile, delage2010percentile, gilbert2017optimizing), conditional value-at-risk (CVaR) (bauerle2011markov, chow2017risk, huang2016minimum) and other spectral risk measures (bauerle2021minimizing), and variants of expected utility (bernard2022robust, jaimungal2022robust, pflug2007ambiguity).

Among these risk measures, VaR and CVaR are arguably the most popular ones and have attracted the attention of many researchers (bauerle2011markov, chow2017risk, delage2007percentile, delage2010percentile, gilbert2017optimizing, huang2016minimum). By using CVaR, one aims to give a precise depiction of the extreme tail of the distribution (of the uncertain rewards), while VaR does not reflect the extreme scenerios exceeding VaR. It is well-known that CVaR is a coherent risk measure, which can be efficiently optimized by convex optimization tools (chen2021sharing); in contrast, VaR is a more challenging risk measure because it is not a coherent one.

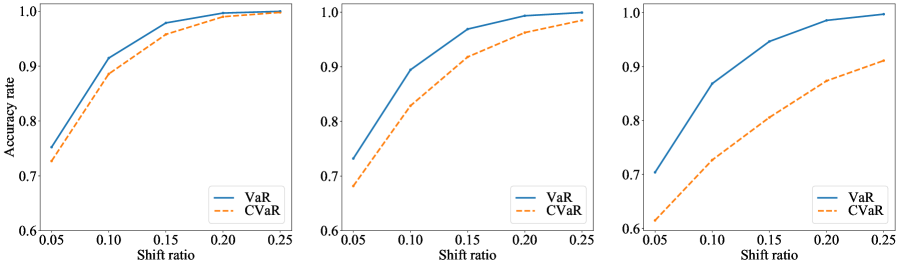

One remarkable advantage of VaR is its stability of estimation (especially under fat-tailed reward distribution (sarykalin2008value)), which is particularly important under data-driven settings where the number of samples are limited and decision makers evaluate models based on their out-of-sample performances (bertsimas2006robust, van2022data, zheng2016big). To demonstrate, we provide an example where we consider a one-step MDP with only 1 state and 2 actions and (sutton2018reinforcement). In this one-step MDP, the decision maker only makes one decision in each episode, and she aims to maximize her VaR/CVaR of rewards for these episodes. We consider uncertain rewards and where is a Student’s -distribution and we vary its degree of freedom . We set the shift ratios , and for testing the estimation accuracy w.r.t. VaR (resp., CVaR) (where we choose the risk threshold ), we set the shift quantity as (resp., ), where both risk measures can be efficiently calculated (see Appendix LABEL:apd:t_distribution for more details). We evaluate the decision maker’s accuracy rate as the proportion of testing samples where she has chosen the action with a higher VaR/CVaR of rewards (i.e., action ); for each pair of accuracy rate and shift ratio, following yamai2002comparative, 1000 random reward samples for each state-action pair are available for the decision maker, and we test her accuracy rate based on 10000 testing samples.

As illustrated in Figure 1, the accuracy rate increases with the shift ratio . As decreases, becomes more fat-tailed, and the accuracy rate of VaR is remarkably higher than that of CVaR, which indicates that the statistical inference on VaR would be more accurate than on CVaR. Therefore, VaR may be a more preferable choice when only small sample sets are available.

Our return-risk model is motivated by the soft-robust criterion/model, which optimizes a convex combination of the mean and a robust performance in the optimization literature (ben2010soft). MDPs with soft-robustness are also popular in recent years, where decision makers aim to maximize a weighted average of the mean and percentile performances (brown2020bayesian, lobo2020soft). Unlike these existing soft-robust MDPs, however, the proposed return-risk model is fundamentally different in two aspects: first, these existing soft-robust models have no consideration for reward ambiguity, while we utilize distributionally robustness to account for reward ambiguity, by which we can hedge against the most adversarial realization of the distribution of rewards (within the ambiguity set), thus our model is more robust to reward uncertainty (chen2019distributionally, xu2010distributionally); second, we choose VaR as the risk measure which has a direct interpretation to percentile performances, and, as illustrated above, tends to be more advantageous in data-driven optimization.

Our work concentrates on model-based setting, where our proposed models are motivated by the classical (dual formulation of) nominal MDPs (puterman2014markov) and the chance-constrained MDPs (delage2010percentile). It is worth noting that, beyond model-based setting, there are other inspiring and innovative researches on robust reinforcement learning, such as robust TDC algorithms and robust Q-learning (roy2017reinforcement, wang2021online), robust policy gradient (wang2022policy), least squares policy iteration (lagoudakis2003least) and sample complexity analysis (panaganti2022sample). Note that, though model-free reinforcement learning can be used to learn satisfactory policies for complex environment, the requirement of large amounts of interaction (with environment) may render the learning process slow (kaiser2019model), while high sample efficiency is one strong advantage of model-based learning (sutton2018reinforcement). We also note that MDPs with transition kernel ambiguity is another active research line where distributionally robustness is widely employed (clement2021first, shapiro2016rectangular, shapiro2021distributionally, xu2012distributionally).

We may summarize our contributions as follows (and we also compare our contributions to those of related works in Table LABEL:table:related_works in Appendix LABEL:apd:related_works).

(i) We show that the distributionally robust model of optimizing expected rewards can be reformulated as a convex conic program, which is equivalent to the nominal MDP with a convex regularization in the objective function.

(ii) For distributionally robust chance-constrained MDPs (DCC), we show that it can be reformulated as nominal chance-constrained MDPs at adjusted risk levels. This observation bridges the gap between risk and parameter ambiguity.

(iii) Combining the proposed models in (i) and (ii), we propose the return-risk MDP that maximizes the weighted average of the expectation and VaR of reward (both under distributionally robustness to reward uncertainty), which is flexible and can perform well under the criteria of mean and percentile returns.

(iv) When only considering deterministic policies, we show that our return-risk model can also account for risk from uncertain transition kernel, and we derive its equivalent reformulation as a mixed-integer second-order cone program (MISOCP).

(v) To solve the proposed return-risk model, we design a first-order method that is more scalable than the MOSEK solver, thus is faster with large-size problems.

(vi) In the simulation and empirical experiments, we adopt a data-driven setting, where the decision maker aims at maximizing the expectation and VaR of the random reward. We compare the performances of distributionally robust MDPs (DRMDPs), DCC, RR, robust MDPs (RMDPs) (delage2010percentile) and BROIL (brown2020bayesian), and results show that the third one performs the best under both expectation and different VaR’s (with risk thresholds and ), which showcases its advantages and adjustability to the decision makers’ changeable preferences between return and risk.

The remainder of this paper is organized as follows. We introduce the background in Section 2. In Sections 3 and 4, we study DRMDPs as well as the DCC model, respectively, and we derive their tractable reformulations. Combining these proposed models, we propose the RR model in Section 5. The designed first-order algorithm for the RR model is detailed in Section 6. We compare the performances of DRMDP, DCC, RR, RMDP and BROIL, and demonstrate the advantage of our proposed algorithm in Section 7. Conclusion is drawn in Section 8.

2 Background

We consider an infinite-horizon MDP with a finite state space and a finite action space . Let be the transition probability kernel such that is denoted to be the transition probability of transiting to state when action is chosen in state ; thus, is the transition probability distribution for every . Given the state-action pair , an agent will receive an expected reward . To simplify our notation, we denote the reward function as a vector .

We seek for the optimal stationary randomized policy with for all , where an action will be taken in state with probability . A nominal MDP that maximizes the expected reward can be formulated (puterman2014markov) as

| (1) |

where the feasible set is given by Here the coefficient matrices with all-ones vectors and with for all . For each , we denote the subvector of as ; its component can be interpreted as the total discounted probability one occupying state and choosing action when applying the policy (puterman2014markov)111By puterman2014markov, any admits such interpretation, thus we can retrieve our policies of all the proposed models in this paper in this way.. We have a discount factor and the initial distribution of the initial states. Problem (1) is a linear program that can be efficiently solved by simplex method and interior-point method (nocedal2006numerical). One can also compute the optimal policy efficiently by applying value iteration or policy iteration to solve the associated Bellman equation of this problem (bertsekas1995neuro, puterman2014markov).

The nominal MDP (1) does not account for uncertainty in either rewards or transition kernel. To account for reward uncertainty, delage2010percentile assume that the random reward vector follows a known Gaussian distribution and propose a chance-constrained MDP model as follows:

| (2) |

In fact, the above chance-constrained model maximizes the VaR (at the risk level ) of the reward with respect to the distribution . Since is assumed Gaussian, by theorem 10.4.1 in prekopa2013stochastic, one can reformulate problem (2) as a second-order cone program as follows:

where is the inverse of the cumulative density function of the Gaussian distribution and is the covariance matrix of . Second-order cone programs allow efficient solutions by state-of-the-art commercial solvers such as CPLEX, Gurobi and MOSEK (see, e.g., ben2001lectures). Despite its tractability, the chance-constrained MDP (2) requires the precise underlying reward distribution as input. Moreover, the above reformulation does not hold for generic distribution .

3 Distributionally Robust MDPs

In many real-world situations, the true distribution of the uncertain reward is hard (if not impossible) to obtain. Instead, we may have some firm knowledge, such as moments and shape about it. As one of the most efficacious treatments for such situations, the DRO approach models uncertainty as a random variable governed by an unknown probability distribution residing in an ambiguity set. Facing distributional ambiguity, a decision maker seeks for solutions that hedge against the most adversarial distribution from within the ambiguity set. To be specific, in our context, we assume that the true distribution of the uncertain reward resides in a Wasserstein ball of radius around some reference distribution :

| (3) |

Here is the set of all probability distributions on , and the Wasserstein distance between two distributions and , equipped with a general norm in , is given by where is the set of all joint distributions with marginal distributions and that govern and , respectively.

The random parameter in the nominal MDP (1) is the expectation of reward, which in practice, is often estimated by the average of historical samples. However, when the sample size is small, such a sample average is not close to the expectation but rather, is known to be optimistically biased (see, e.g., smith2006optimizer). Hence, the nominal MDP (1) based on samples may yield an unsatisfactory policy that does not perform well out-of-sample. For this reason, a possible alternative is to maximize instead the worst-case expected reward as in the following distributionally robust MDP:

| (4) |

The following proposition offers an equivalent conic program for (4).

Proposition 3.1

The distributionally robust MDP (4) can be reformulated a conic program

It is not hard to observe that the distributionally robust MDPs can be viewed as a convex regularization of the nominal MDP (4) under the reference distribution . In particular, the convex regularizing term in the distributionally robust MDP is , which is sized by the Wasserstein radius . Interestingly, we have also found that an (distributionally) optimistic MDP can be reformulated as a reverse conic program with a (concave) regularization term . We relegate this result to Appendix LABEL:apd:optimistic_MDPs.

We remark that, problem (4) is indeed a special case of the robust optimization problem considered in jaimungal2022robust, where we consider the expected utility framework. Compared to the policy gradient methods provided in jaimungal2022robust where convergence is not established, we have derived its equivalent reformulation as a tractable conic program which can be efficiently solved by state-of-the-art commercial solvers such as Gurobi, Mosek and CPLEX, and can also be seamlessly incorporated in the tractable reformulation of our proposed return-risk model in Section 5.

4 Distributionally Robust Chance-Constrained MDPs

In this section, we turn from optimizing the expectation of reward to its tailed performance, by exploring chance-constrained MDPs. In particular, we still consider Wasserstein ambiguity sets (3) to account for distributional ambiguity, meanwhile specifying the reference distribution and the norm in the definition of the Wasserstein distance.

For the former, we focus on an elliptical reference distribution = 222Note that results in Section 3 hold for a general reference distribution. throughout this section, whose probability density distribution is given by where is a positive normalization scalar, is a mean vector, is a positive definite matrix and is a generating function. We emphasize that this assumption on is mild as this is only the center of the ambiguity set. In particular, our proposed distributionally robust chance-constrained MDPs can account for all types of distributions (as long as they are inside the ambiguity set) and they are not restricted to be all elliptical. As we shall see, such specifications lead to tractable reformulation of our proposed models. Preliminaries on elliptical distributions are relegated to Appendix LABEL:apd:elliptical_distributions.

For the latter, we adopt the Mahalanobis norm associated with the positive definite matrix , captured by . Note that the dual norm of a Mahalanobis norm is another Mahalanobis norm that is defined by the inverse matrix .

In a distributionally robust chance-constrained MDP, we hope that even in the worst-case, with a high confidence the reward is no less than a lower bound, and we aim at maximizing such a lower bound by solving

| (5) |

Quite notably, the worst-case chance constraint in the pessimistic chance-constrained MDP (5) is equivalent to a nominal chance constraint in (2) with a higher risky level.

Lemma 4.1

Suppose in the Wasserstein ambiguity set (3), the reference distribution is an elliptical distribution and the Wasserstein distance is equipped with a Mahalanobis norm associated with the positive definite matrix . The distributionally robust chance constraint

| (6) |

is satisfiable if and only if where with that can be computed via bisection method which searches for the smallest that satisfies

Equipped with Lemma 4.1, it then turns out that the distributionally robust chance-constrained MDP (5) is equivalent to a nominal chance-constrained MDP (2) at a higher risky level. Consequently, the distributionally robust chance-constrained MDP (5) can be reformulated into a conic program, or more precisely, a second-order cone program owing to our choice of the Mahalanobis norm.

Proposition 4.2

Suppose in the Wasserstein ambiguity set (3), the reference distribution is an elliptical distribution and the Wasserstein distance is equipped with a Mahalanobis norm associated with the positive definite matrix . If the risk threshold satisfies , then the distributionally robust chance-constrained MDP (5) is equivalent to the second-order cone program

where with being the smallest that satisfies

Similar to the distributionally robust MDPs in Section 3, the distributionally robust chance-constrained MDPs also admit an optimistic counterpart, which is equivalent to the nominal chance-constrained MDPs with a larger risk threshold. We relegate this result to Appendix LABEL:apd:optimistic_CC.

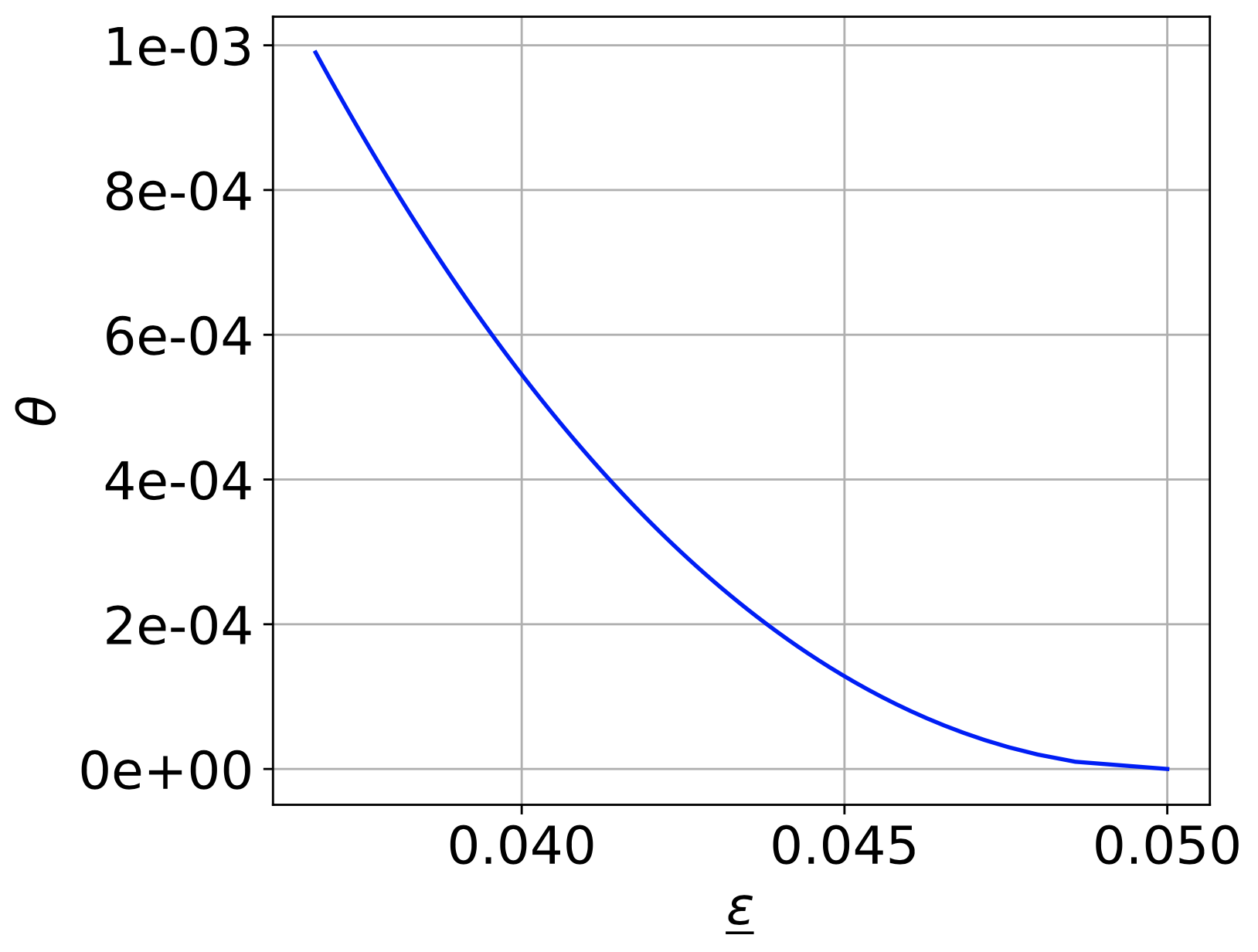

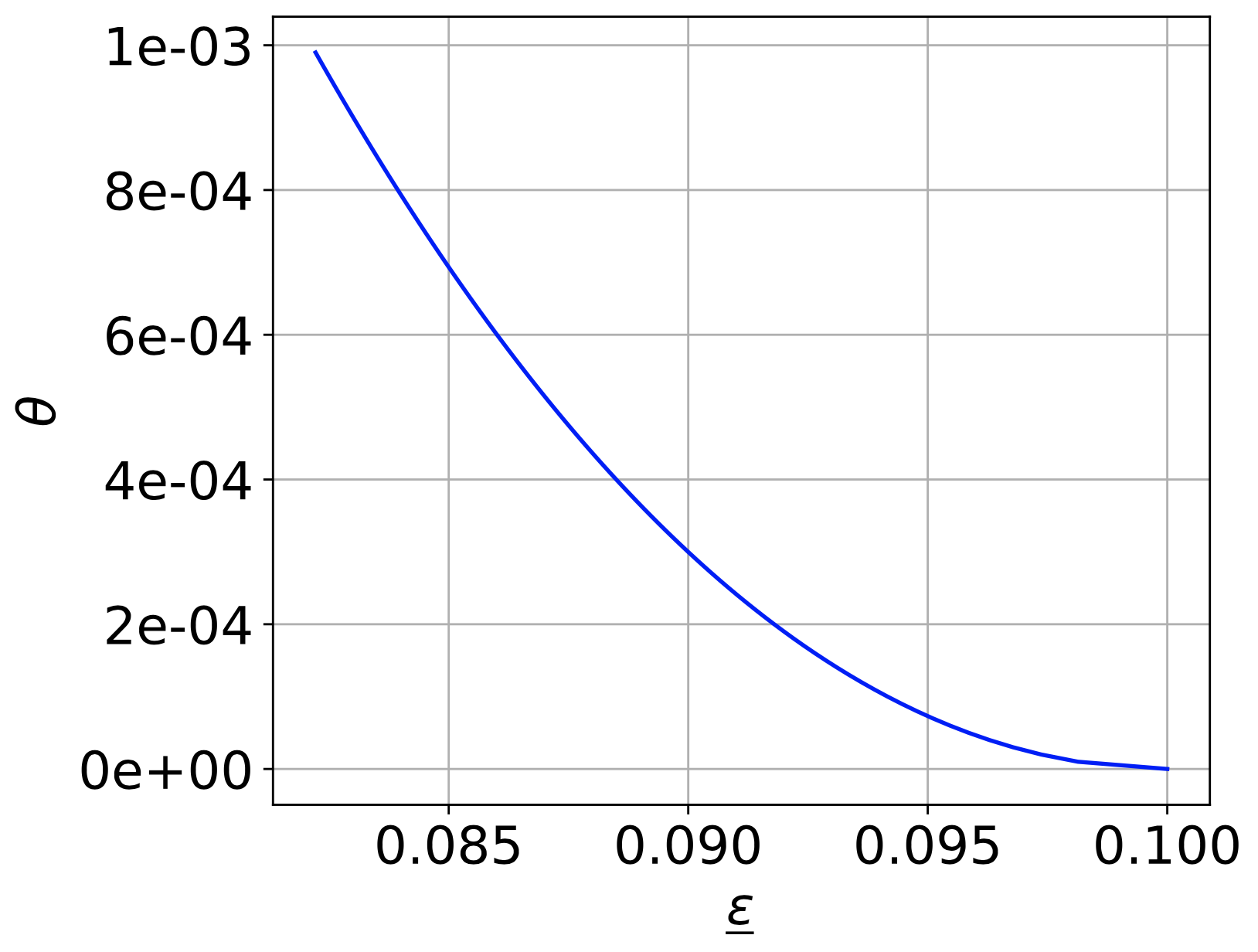

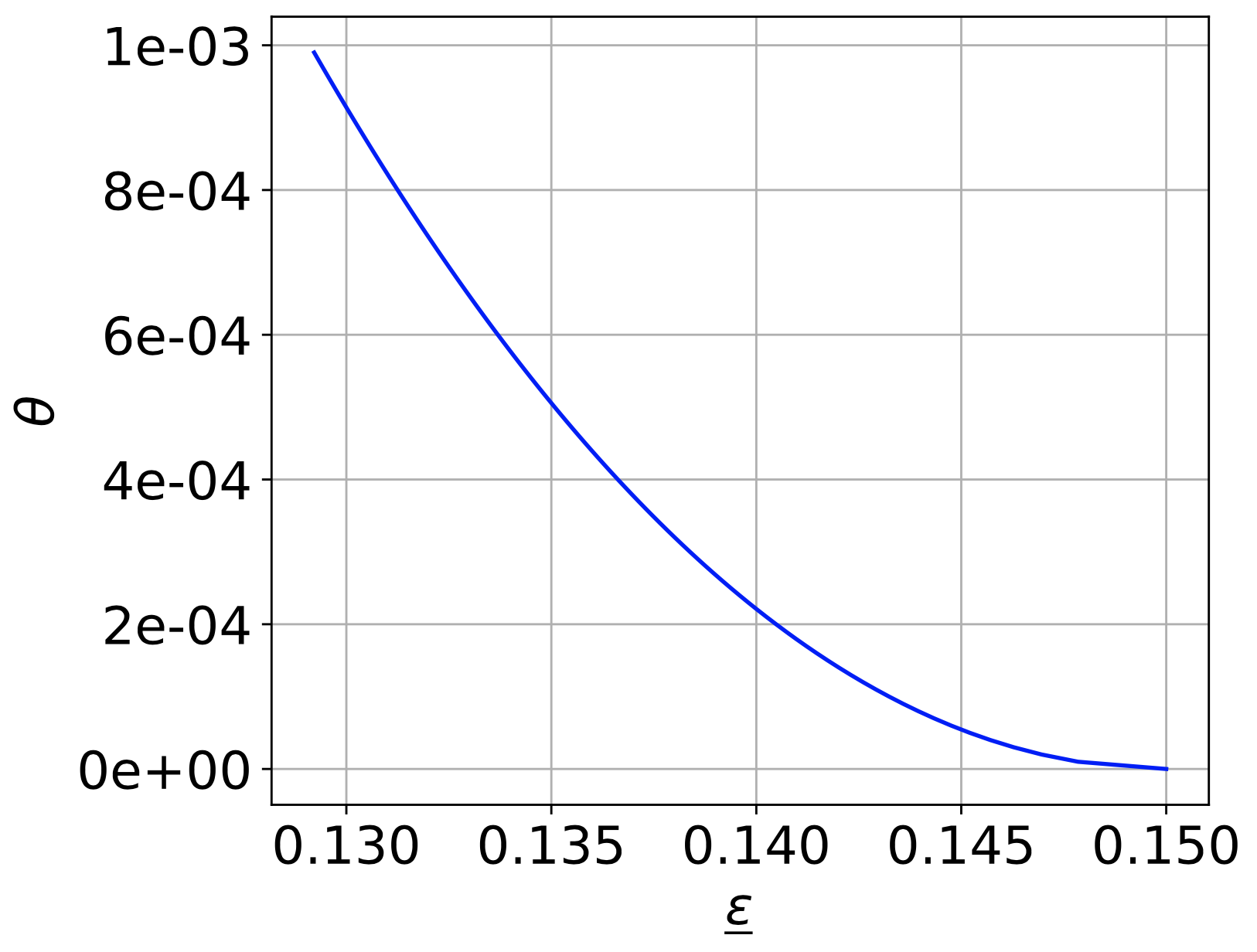

To conclude this section, we present in Figure 2 the relations between and . Indeed, for any fixed , there is a one-to-one correspondence between the risk threshold and the Wasserstein radius . Following from this fact, for the chance-constrained model in our numerical experiments (Section 7), we only calibrate the risk threshold rather than the Wasserstein radius.

5 Return-Risk MDP

For rational decision makers, two types of rewards are their chief concerns: the average and the worst-case rewards. However, the risk-averse models often can not achieve decent average return on which the model put no emphasis (carpin2016risk, delage2010percentile, jiang2018risk). To take both concerns into considerations, we leverage the established DRMDPs and DCC model in Sections 3 and 4 as ingredients and propose the return-risk MDP that maximizes the weighted average of the worst-case expectation and VaR of reward as follows:

| (7) |

Here the Wasserstein ball is assumed equipped with a general reference distribution and an -norm in the definition of the Wasserstein distance, while an elliptical reference distribution and a Mahalanobis norm associated with the positive definite matrix are assumed for . It is not hard to see that the return-risk MDP (7) takes the distributionally robust MDP (4) and the distributionally robust chance-constrained MDP (5) in as special cases by varying , and . Furthermore, by choosing a fractional , the return-risk model enables one to tailor a balance between risk and return. Proposition 5.1 below provides an equivalent second-order cone program for the return-risk MDP (7) under these assumptions.

Proposition 5.1

Suppose in (7) the Wasserstein ball (resp., ) is equipped with a general distribution (resp., an elliptical reference distribution ) and the norms in the definitions of the Wasserstein distances of and are an -norm and the Mahalanobis norm associated with , respectively. Assume that the risk threshold satisfies , then the return-risk MDP (7) is equivalent to a second-order cone program

| (8) |

where with being the smallest that satisfies and it could be computed via bisection method.

5.1 Risk-Awareness for Uncertain Transition Kernel

By adopting the static soft-robust framework in lobo2020soft, one can indeed also account for the uncertainty in transition kernel in our return-risk model. As in lobo2020soft, suppose we have finite samples of transition kernel with weights that are generated by MCMC (see, e.g., kruschke2010bayesian). Our proposed model is then as follows:

| (9) |

Here the objective function in (9) is again soft-robust against the uncertainty (in transition kernel), with the weight as the controller for the robustness and is the risk threshold (w.r.t. the uncertain transition kernel). The weighted empirical distribution and the function

represents the optimal value of the return-risk model with the additional constraint that the optimal policy should be the input and with as the coefficient matrix corresponding to the input transition kernel .

Quite notably, when focusing on deterministic policies, one can reformulate (9) as an MISOCP.

Proposition 5.2

We remark that, though deterministic policies seem to be restricted compared to the randomized ones, they actually are more favored under some situations; for example, they may be a more suitable choice in some medical domains where randomized policies are unworkable for practical and philosophical reasons (rosen2006defense). Also, randomized policies may be difficult to be evaluated after they have been deployed and may have poor reproducibility (lobo2020soft).

6 First-Order Method

In this section, we introduce an efficient first-order algorithm to solve the equivalent formulation (8) of our return-risk model. Our algorithm is based on an alternating direction linearized proximal method of multipliers (AD-LPMM) algorithm (beck2017first, shefi2014rate), which is a variant of the alternating direction method of multiplier (ADMM) algorithm and also has a convergence rate of (here is the number of iterations) proved by beck2017first. The proposed splitting allows efficient update of variables in AD-LPMM (where the solutions are analytical or can be retrieved by an efficient bisection method).

For the primal update of the ADMM algorithm, one needs to solve minimization problems with a quadratic term involved (in its objective function); in AD-LPMM, this quadratic term can be linearized by adding a proximity term to the objective function, which could render the primal update much easier. To implement our AD-LPMM algorithm, first we will introduce auxiliary variables and rewrite (8) (as a minimization problem) as follows:

| (10) |

where, in the spirit of AD-LPMM, we can split the decision variables into two groups and update them separately. The augmented Lagrangian function of (10) is:

Based on our splitting method, we will update the two groups of variables and separately. For the update of , we define two primal update operators

and while for the update of (i.e., the second group of variables), we define

where and (equipped with a positive semi-definite matrix ) is a weighted vector norm such that . As we shall see in Section 6.3, the update of is fast (where an analytical solution is available) with the proximity term added. Note that when , the update in AD-LPMM degenerates to an ADMM’s one.

We now introduce our AD-LPMM in Algorithm 1. Basically, the most time-consuming computations lie in the primal update phase, where the updates are carried out by solving a minimization problem with other variables fixed at values after their last updates. As shall be detailed soon, owing to our variable splitting method, the primal updates are also quite fast, where analytical solutions or solutions obtained by bisection are available. Here we choose a stepsize that is increasing in every iteration (with a growth rate ), which in practice accelerates the convergence.

6.1 Subproblem in Step 1: Proximal Mapping and Projection

To solve , first we would utilize the technique of proximal mapping and establish the following equivalences:

| (11) |

where is the proximal mapping operator and

| (12) |

is the operator of projection on the unit ball Here, the first equality in (11) holds by the definition of the proximal mapping operator, and the second equality follows from,e.g., example in beck2017first. Indeed, problem (12) allows an efficient solution obtained by a bisection method to locate its optimal dual solution (after which the optimal primal solution can be retrieved immediately), where the upper bound of the bisection is provided in Lemma LABEL:lemma:bisect_ub relegated to Appendix LABEL:apd:proof_of_adlpmm. The time complexity of the solution process (11), as well as the pseudocode for the bisection method, are provided in the following proposition.

Proposition 6.1

Problem can be solved in time , where is the desired precision of the bisection method.

6.2 Subproblem is Step 2: Componentwise Update

Problem can be decomposed into single-variable quadratic programming problems, each allowing an analytical solution. We summarize the time complexity and details in the following proposition.

Proposition 6.2

Problem can be solved in time .

6.3 Subproblem in Step 3: Linearization and Proximal Mapping

Compared to the update in ADMM, in our AD-LPMM, a proximity term is added to the objective function of the update in step . By choosing as mentioned in Section 6, we can linearize all the quadratic terms in , thus the solution can be obtained analytically by the technique of proximal mapping (meanwhile assuring the positive semi-definiteness of in every iteration of Algorithm 1). This solution process, as well as its time complexity, is provided in the following proposition.

Proposition 6.3

Problem can be solved in time .

7 Numerical Experiments

In this section, we conduct two numerical experiments to compare the performances of DRMDPs (4), CC (2)333As we demonstrated in Section 4, a DCC is equivalent to a nominal chance-constrained one with an adjusted risk level, thus here we simply choose the latter as the benchmark., RR (7), RMDPs (delage2010percentile) and BROIL (brown2020bayesian) (please see Appendices LABEL:apd:RMDP and LABEL:apd:BROIL for more details for the last two models). In both experiments, we train our reward functions with different sample sizes (100,200,300,400,500). For each sample size, performance of each model is evaluated for 100 times. The performance of each model is evaluated by expectation and VaR with risk thresholds . Cross validations are conducted for parameter selection (please see Appendix LABEL:apd:parameter for details).

In Section 7.1, we conduct a simulation study where MDPs are generated randomly as in regan2012regret; In Section 7.2, we study a machine replacement problem introduced in delage2010percentile. As implied in our proofs, in this section, the Wasserstein ambiguity set of DRMDPs (4) will be equipped with a general reference distribution and an -norm for the Wasserstein distance; as for RR (7), we use a general reference distribution and an -norm in the definition of the Wasserstein distance for the Wasserstein ambiguity set , while for , we use an elliptical reference distribution and the Mahalanobis norm associated with the positive definite matrix for the Wasserstein distance. All optimization problems are solved by MOSEK on a GHz processor with GB memory.

7.1 Simulation Study

In this experiment, we follow the experiment setup in regan2012regret where the number of reachable next-states and the transition kernel are randomly generated (both of which are known to decision makers). More details of the experiment setting are relegated to Appendix LABEL:apd:simulation.

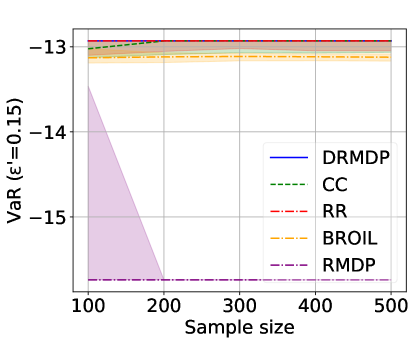

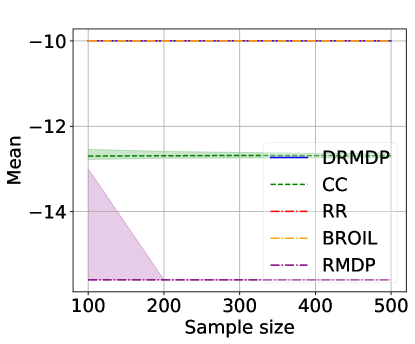

As illustrated in Figures 5 and LABEL:fig:simulation_05_10 (where the latter for VaR with is relegated to Appendix LABEL:apd:simulation_results), when the decision maker aims to optimize her tailed performances, CC is a preferable choice compared to DRMDPs; on the contrary, when pursuing optimizing the average return, DRMDPs perform much better than CC. Observe that the RR model, which includes both DRMDPs and the DCC model as special cases, remains as the best model under all criteria. In particular, one can observe that, RR achieves higher percentile returns than BROIL (that is a model without robustness), which demonstrates the benefits of distributionally robustness and the advantage of the risk measure VaR for percentile performance optimization. As expected, RMDPs end up yielding over-conservative policies; as a result, it performs poorly in most instances under all criteria.

7.2 Machine Replacement Problem

In this experiment, we follow the experiment setup in delage2010percentile and consider the case where a factory holds an extensive amount of machines, each of which is subject to the same underlying MDP (more details of the experiment setting can be found in Appendix LABEL:apd:simulation). Our setting is similar to delage2010percentile except for the follows: we use a data-driven setting as described above, and we evaluate our (policies of) models by looking at the various performance measures as in Section 7.1.

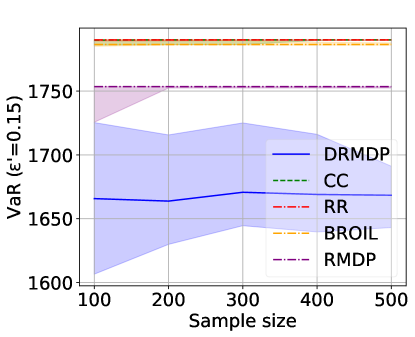

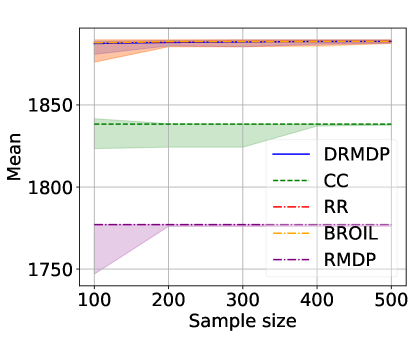

We report the overall performances of the five models in Figures 4 and LABEL:fig:empirical_05_10 (where the latter for VaR with is relegated to Appendix LABEL:apd:empirical_results). Similar to the previous experiment, RR always performs better than or equal to the best model between CC and DRMDPs, and it provides the best performance under all criteria, which again manifest the merit of taking both the expected and worst-case performances into consideration and distributionally robustness.

7.3 Computation Times of Different Algorithms

| S=A | Runtimes | Relative gaps | |

|---|---|---|---|

| MOSEK | AD-LPMM | ||

| 40 | 0.60 | 2.79 | 0.1 |

| 70 | 5.58 | 4.81 | 0.1 |

| 100 | 25.50 | 19.98 | 0.2 |

| 130 | 93.54 | 66.17 | 0.1 |

| 160 | 444.06 | 168.34 | 0.4 |

In this section, we compare the computation times of our AD-LPMM algorithm with the state-of-the-art solver MOSEK. Table 1 reports the runtimes of the the AD-LPMM and MOSEK when solving problem (8) at different problem sizes. Results indicate that, though our AD-LPMM is slower than the MOSEK solver when problem size is small, it showcases its strong scalability and become much faster than MOSEK with large-size problems (while always maintaining high solution quality), where the advantage is more notable when the problem scales up.

8 Conclusion

We consider risk-aware MDPs with ambiguous reward functions and propose the return-risk model, which is versatile and can optimize any weighted combination of the average and quantile performances of a policy. This model generalizes and combines the advantage of distributionally robust MDPs and distributionally robust chance-constrained MDPs, thus is powerful in both average and percentile performances optimization. In particular, risk from uncertain transition kernel can also be captured by the return-risk model when output policies are deterministic. Tractable reformulations are provided for all our proposed models, and

Algorithm 1

we design an AD-LPMM algorithm for the return-risk model, which is well scalable and faster than the MOSEK solver with large-scale problems. Experimental results showcase the versatility of the return-risk model as well as