RiskProp: Account Risk Rating on Ethereum via De-anonymous Score and Network Propagation

Abstract.

As one of the most popular blockchain platforms supporting smart contracts, Ethereum has caught the interest of both investors and criminals. Differently from traditional financial scenarios, executing Know Your Customer verification on Ethereum is rather difficult due to the pseudonymous nature of the blockchain. Fortunately, as the transaction records stored in the Ethereum blockchain are publicly accessible, we can understand the behavior of accounts or detect illicit activities via transaction mining. Existing risk control techniques have primarily been developed from the perspectives of de-anonymizing address clustering and illicit account classification. However, these techniques cannot be used to ascertain the potential risks for all accounts and are limited by specific heuristic strategies or insufficient label information. These constraints motivate us to seek an effective rating method for quantifying the spread of risk in a transaction network. To the best of our knowledge, we are the first to address the problem of account risk rating on Ethereum by proposing a novel model called RiskProp, which includes a de-anonymous score to measure transaction anonymity and a network propagation mechanism to formulate the relationships between accounts and transactions. We demonstrate the effectiveness of RiskProp in overcoming the limitations of existing models by conducting experiments on real-world datasets from Ethereum. Through case studies on the detected high-risk accounts, we demonstrate that the risk assessment by RiskProp can be used to provide warnings for investors and protect them from possible financial losses, and the superior performance of risk score-based account classification experiments further verifies the effectiveness of our rating method.

1. Introduction

Ethereum (Wood, 2014) has the second-largest market cap in the blockchain ecosystem. The account model is adopted on Ethereum, and the native cryptocurrency on Ethereum is named Ether (abbreviated as “ETH”), which is widely accepted as payments and transferred from one account to another. It is known that Ethereum accounts are indexed according to pseudonyms, and the creation of accounts is almost cost-free. This anonymous nature and the lack of regulation result in the bad reputation of Ethereum and other blockchain systems for breeding malicious behaviors and enabling fraud, thereby resulting in large property losses for investors. As reported in a Chainalysis Crime Report, the illicit share of all cryptocurrency activities was valued at nearly USD 2.7 billion in 2020. These losses illustrate that Know-Your-Customer (KYC) and risk control of accounts are critical and necessary. Risk control (Möser et al., 2014) not only helps wallet customers identify risky accounts and avoid losses but also plays a vital role in the anti-money laundering of virtual asset service providers, such as cryptocurrency exchanges.

Therefore, a wealth of efforts have been expended in risk control on Ethereum in recent years. In September 2020, the Financial Action Task Force (FATF) published a recommendation report on virtual assets and released information on Red Flag Indicators (FATF, 2022) related to transactions, anonymity, senders or recipients, the source of funds, and geographical risks. In addition, researchers in the academic community have proposed various techniques from the perspectives of address clustering and illicit account classification. Address clustering techniques perform entity identification of anonymous accounts. For example, Victor (Victor, 2020) proposes several clustering heuristics for Ethereum accounts and clusters 17.9% of all active externally owned accounts. Illicit account detection techniques focus on training classifiers based on well-designed features extracted from transactions (Farrugia et al., 2020; Wu et al., 2022; Chen et al., 2020). Moreover, some researchers have developed methods for automatic feature extraction incorporating structural information (Weber et al., 2019; Yuan et al., 2020; Lin et al., 2020; Li et al., 2022).

However, there are still some limitations (L) associated with these techniques. L1: Account clustering techniques can only be applied to part of accounts and therefore have limited applicability, and most accounts beyond heuristic rules cannot thus be identified. L2: In the existing methods for illicit account detection, binary classifiers are usually trained via supervised learning. However, as only a very small percentage of risky nodes have clear labels, which are required for these methods, the vast majority of accounts that may be involved in malicious events are unlabeled. In particular, risky accounts with few transactions or unseen patterns are likely to be misidentified in practical use.

To address the limitations presented above, we explore risk control on Ethereum from a new perspective: Account risk rating. In traditional financial scenarios, credit scoring is usually conducted by authorized financial institutions, which perform audits on their customers to fully understand their identity, background, and financial credit standing. Similarly to credit scoring, risk rating on Ethereum can help us quantify the latent risk of a transaction or account with a quantitative score, thereby combating money laundering and identifying potential scams before new victims emerge. In terms of the abovementioned L1, in contrast to the traditional account clustering method, which can only de-anonymize a small number of accounts, the account risk method proposed in this paper can obtain quantitative risk indicators for all accounts. Regarding L2, the proposed risk rating method can achieve decent performance in an unsupervised manner without feeding labels. The output of the proposed method is risk values, which are provided continuously and allow evaluation of the severity of risk.

Compared with traditional financial scenarios, several unique challenges (C) are encountered in the task of account risk rating on Ethereum. C1: Nature of anonymity. Transactions on Ethereum do not require real-name verification. Even worse, perpetrators of some malicious activities deliberately enhance their anonymity to counter the impact of de-anonymizing clustering techniques (Weber et al., 2019). C2: Complex transaction relationship. Compared with traditional financial scenarios, a user or entity on Ethereum may control a large number of accounts at almost no cost, and the transaction relationship between accounts is also more complex. How to quantify the impact of trading behavior between accounts on account risk is a challenging core problem.

To overcome the challenges mentioned above, we propose a novel approach called Risk Propagation (RiskProp) for Ethereum account rating. It comprises two core designs, namely de-anonymous score and a network propagation mechanism. To resolve C1, de-anonymous score measures the degree to which transactions remain anonymous. For example, both the payer and the payee of an illicit transaction prefer to have a small number of transactions to ensure anonymity-preserving protection. In contrast, both sides of a licit transaction may participate in numerous interactions without evading the impact of the de-anonymized clustering algorithm. Afterward, to resolve C2, we model the massive transaction records as a directed bipartite graph and introduce a network propagation mechanism with three interdependent metrics, namely Confidence of the de-anonymous score, Trustiness of the payee, and Reliability of the payer. Intuitively, payees with higher trustiness receive transactions with higher de-anonymous scores, and payers with higher reliability will send transactions with higher confidence. Clearly, reliability, trustiness, and confidence are related to each other, so we define five items of prior knowledge that these metrics should satisfy and propose three mutually recursive equations to estimate the values of these metrics. To verify the effectiveness of the proposed risk rating method and further illustrate the significance of rating for risk control on Ethereum, we evaluate the effect of the risk rating system via experiments from two aspects, i.e., analysis of risk rating results and rating score-based illicit/licit classification.

Overall, our contributions are summarized as follows:

A new perspective for Ethereum risk control. This paper is the first to propose tackling the problem of Ethereum risk control via the perspective of account risk rating.

A novel risk metric for transactions. We creatively develop a metric called de-anonymous score for transactions, which measures the degree of de-anonymization to quantify the risk of a transaction.

An effective method and interesting insights. We implement a novel risk rating method called RiskProp and demonstrate its superior effectiveness and efficiency via experiments on a real-world Ethereum transaction dataset together with theoretical analysis. By analyzing the rating results and case studies on high-risk accounts, we obtain interesting insights into the Ethereum ecosystem and further show how our method could prevent financial losses ahead of blacklisting malicious accounts.

2. Preliminary

2.1. Ethereum Financial Background

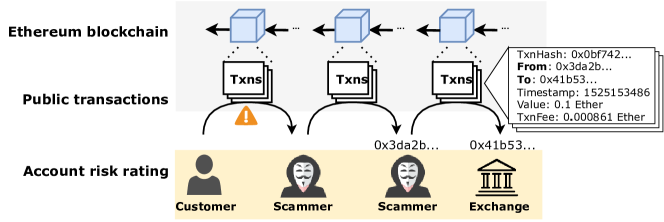

Ether is the native “currency” on Ethereum and plays a fundamental part in the Ethereum payment system. Ether can be paid or received in financial activities, just like currency in real life. In conventional financial scenarios, a Know Your Customer (KYC) check is the mandatory process to identify and verify a customer’s identity when opening an account and to periodically understand the legitimacy of the involved funds over time. However, unlike traditional transaction systems, where customers’ identity information is required and obtained in KYC checks, Ethereum accounts are designed as pseudonymous addresses identified by 20 bytes of public key information generated by cryptographic algorithms, for example, “0x99f154f6a393b088a7041f1f5d0a7cbfa795d301”.

Figure 1 depicts the risky scenario of Ether transfer in aspects of data acquisition. It includes three layers: 1) Ethereum blockchain. The Ethereum historical data are irreversible and publicly traceable on the chain. 2) Public transactions. The transaction denotes a signed data package from an account to another account, including the sending address, receiver address, transferred Ether amount, etc. 3) Account risk rating. Usually, the identities who control the accounts are not labeled. Customers may become involved in suspicious financial crimes or be vulnerable to frauds and scams. Furthermore, the illicit funds can be laundered and cashed out via exchanges. In this procedure, our proposed RiskProp is implemented to measure the risk of unlabeled accounts that may have ill intentions and alert customers when engaging in suspicious, potentially illegal transactions.

2.2. The Nature of Blockchain: Anonymity

It is known that the Ethereum account is identified as a pseudonymous address. However, if customers repeatedly use the same address as on-chain identification, the relationship between addresses becomes linkable via public transaction records. Accounts that participate in more transactions and connect with more accounts experience degrading anonymity (Weber et al., 2019). To reduce the likelihood of exposure, criminals naturally tend to initiate transactions with fewer accounts. Here is an example on Ethereum: The two accounts of transaction 0x9a9d have only three transactions and became inactive thereafter. These two accounts are considered suspicious and reported as relevant accounts of Upbit exchange hack. On the contrary, entities who do not deliberately take anonymity-preserving measures are likely to be normal (Weber et al., 2019). Thus, the transaction is scored based on the fact of whether the accounts are trying to hide or not, which is the de-anonymous score.

Definition 1 (De-anonymous score, abbreviated as “score”). The de-anonymous score of a transaction from account to where there is no intention to hide is defined as

| (1) |

where represents the outgoing transactions (payments) of payer , represents the incoming transactions (receptions) of payee , and denotes the size of a set. The minimum value of and is 1. Let and be the largest number of payments and receptions, respectively. The de-anonymous scores of a transaction range from (very high anonymity, abnormal) to 1 (very low anonymity, normal). Intuitively, the score of increases as the transaction numbers of either payer or payee grow. Note that tricky criminals may camouflage themselves by deliberately conducting low-anonymity transactions (Li et al., 2020).

2.3. Transaction Network Construction

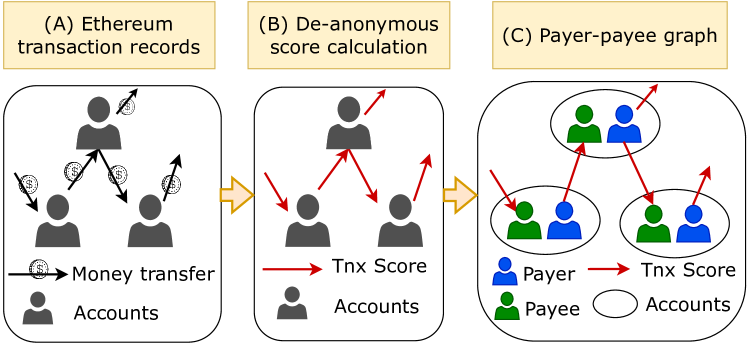

First, each transaction on Ethereum has one payer (i.e., sender) and one payee (i.e., receiver). Any account can be the role of payer or payee, just as a person in real life has different roles. The payee is a passive role and, therefore, we consider the incoming transactions to indicate the trustiness of an account. For instance, exchange accounts that receive more transactions are considered to be more trustworthy. In contrast, the payer is an active role and, thus, the outgoing transactions embody the intention of an account. For example, a scam account subjectively wants to transfer stolen money to its partners.

Next, the transaction records are modeled as a directed bipartite graph , where , , and represent the set of all payers, payees, and scores, respectively. A weighted edge denotes the transfer of Ethers from account to account with . The graph construction procedure is shown in Figure 2.

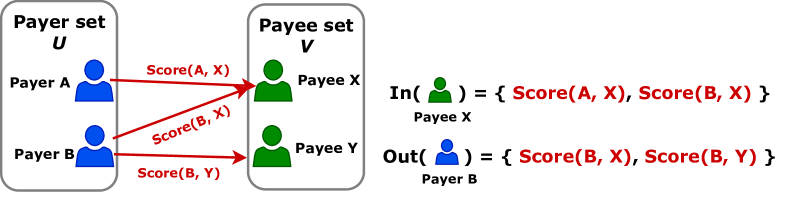

Then, the ego network of a payer is introduced. It is formed by its outgoing scores and corresponding payee neighbors, formulated as , where is the set of scores connected with . It is similar for the ego network of a payee, formulated as . Figure 3 shows an example in which there are two payers, two payees, and three transactions.

3. Model

In this section, we describe the prior knowledge that establishes the relationships among accounts and transactions and then propose risk propagation formulations that satisfy the prior knowledge. It is worth noticing that the proposed algorithm does not require handcraft feature engineering.

3.1. Problem Definition and Model Overview

Given raw transaction records of Ethereum, we model the transaction relationships between accounts as a directed bipartite graph with payers and payees as nodes and prepossessed de-anonymous scores as weights of edges. We believe that accounts have intrinsic metrics to quantify their reliability and trustworthiness and transactions have intrinsic metrics to measure the confidence of their calculated de-anonymous scores. Naturally, those metrics are interdependent and interplay with each other via the risk propagation mechanism:

Payers vary in terms of their Reliability, which indicates how motivated they are. A licit payer without malicious intent usually does not hide himself or disguise its intentions during transactions. Specifically, a reliable payer has harmless intentions regardless of whether it is transferring money to an exchange or to a scammer account (being gypped). In contrast, a perpetrator (e.g., a scammer) hopes to cover up its traces (Victor, 2020). The reliability metric of a payer lies in , . A value of 1 denotes a 100% reliable payer and 0 denotes a 0% reliable payer.

Payees vary in their trustworthiness level, measured by a metric called Trustiness, which indicates how trustworthy they are. Intuitively, a cryptocurrency service provider with a better reputation will receive more licit transactions (with higher scores) from well-motivated payers. Trustiness of a payee ranges from 0 (very untrustworthy) to 1 (very trustworthy) .

De-anonymous scores vary in terms of Confidence, which reflects the confidence in the estimated risk probability of a transaction. The confidence metric ranges from 0 (lack of confidence) to 1 (very confident).

The connection between the reliability and risk of accounts: We define Reliability to characterize the risk rating of accounts because an account’s intention can be inferred by its (active) sending behavior, rather than by its (passive) receiving behavior. A scammer transferring stolen money to its gang is a better reflection of its evil intention than the receipt of stolen money from victims. In the later section, we calculate the risk rating of accounts based on the Reliability of payer roles.

3.2. Network Propagation Mechanism

Given a cryptocurrency payer–payee graph, all intrinsic metrics are unknown but are interdependent. Here, we introduce five items of prior knowledge that establish the relationships and how the network propagation mechanism is specially designed for our problem. The first two items of prior knowledge reflect the interdependency between a payee and the de-anonymous scores that they receive.

[Prior knowledge 1] Payees with higher trustiness receive transactions with higher de-anonymous scores. Intuitively, a payee receiving transactions with high de-anonymous scores is more likely to be trustworthy. Formally, if two payees and have a one-to-one mapping, and , then .

[Prior knowledge 2] Payees with higher trustiness receive transactions with more positive confident scores. For two payees and with identical de-anonymous score networks, if the confidence of the in-transactions of payee is higher than that of payee , the trustiness of payee should be higher. Formally, if two payees and have a one-to-one mapping, and , then .

According to the above prior knowledge, we develop the Trustiness formulation for of our RiskProp algorithm:

| (2) |

The next item of prior knowledge defines the relationship between the score of a transaction and the connected payer–payee pair using the anonymous nature of cryptocurrency.

[Prior knowledge 3] Confident de-anonymous scores of transactions are closely linked with the connected payee’s trustiness. Formally, if two scores and are such that , , and , then .

We imply that different transactions sent by the same payers can have different intentions and anonymity. Even scammers on Ethereum can have transactions that seem normal.

[Prior knowledge 4] Transactions with higher confidence de-anonymous scores are sent by more reliable payers. Formally, if two scores and are such that , , and , then .

This prior knowledge incorporates the payer’s intention in measuring the confidence of transaction scores. In this way, payees may have different confidence in receiving transactions with the same anonymity. For instance, exchanges on Ethereum receive funds from payers with different motivations—some are ordinary investors and some are suspicious accounts.

Below, we propose the Confidence formulation that satisfies the above items of prior knowledge:

| (3) |

Then, we describe how to quantify the Reliability metric of a payer by the transactions it sends.

[Prior knowledge 5] Payers with higher reliability send transactions with higher confidence. For two payers and with equal scores, if payer has higher confidence for all out transaction scores than , then payer has a higher reliability. Formally, if two payers and have and , then . The corresponding formulation of Reliability metric for is defined as

| (4) |

Finally, the risk rating of an account is calculated by . The pseudo-code of RiskProp network propagation is described in Algorithm 1. Let , , be initial values and be the number of interactions. In the beginning, we have initial reliability , initial trustiness , and initial confidence for all transactions. Then, we keep updating metrics using Equations 2–4 until is less than 0.01.

RiskProp+: A Semi-supervised Version

Sometimes, we have partial information about the labels of fraudulent accounts (verified, phishing scams, etc.) and licit accounts. We can take advantage of such prior information and incorporate them into our approach in a semi-supervised manner. In the semi-supervised RiskProp+, we initialize the Reliability metrics only for the training accounts. According to the risk levels of services reported by Chainalysis (Team, 2021), we set for ICO wallet, Converter, and Mining, for Exchange, for Gambling, for Phish/Hack, and set for testing accounts. The reliability values of labeled illicit accounts are unchanged during the training procedure.

Example

Here, we use a small real-world dataset on Ethereum to intuitively show the results of RiskProp+ after interactions. We collect transactions of 10 accounts (6 for training and 4 for testing), including 28,598 accounts and 52,733 transactions in total. Table 1 shows how the reliability of the 4 testing accounts varies over interactions (we omit trustiness and confidence for brevity). These testing accounts have the same reliability values at the beginning (). After convergence, accounts labeled as “phish/hack” get a lower value of reliability, and other licit accounts get higher reliability. Confirming our intuition, RiskProp learns that accounts 0xebdc and 0xfe34 are high-risk accounts that investors need to be aware of.

Workflow for Account Risk Rating

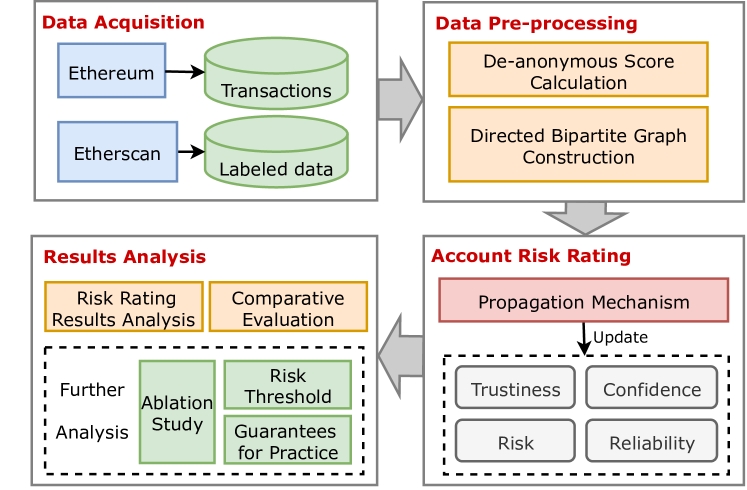

Figure 4 shows the workflow of account risk rating on Ethereum, which contains four modules: (i) Data acquisition collects accounts, transactions, and labels from Ethereum and Etherscan. Only a few labels are provided, and these labels are not available in the unsupervised setting. (ii) Data pre-processing of raw transaction data described in Figure 1 is conducted in two steps: de-anonymous score calculation and directed bipartite graph construction (i.e., payer–payee network). (iii) Account risk rating recursively calculates the Reliability, Trustiness of accounts, and Confidence of transaction scores until convergence, updated by the propagation mechanism. (iv) Results analysis contains risk rating results analysis, comparative evaluation, and further analysis.

4. Experiments

To investigate the effectiveness of RiskProp, we conduct experiments on a real-world Ethereum transaction dataset. As risk rating is an issue without any ground truth, we verify the effectiveness and significance of the risk rating results of RiskProp via three tasks: 1) risk rating analysis, which includes distribution of risk rating results and case studies of transaction pattern; 2) comparative evaluation, which reports on the classification performance of labeled accounts compared with various baselines; and 3) further analysis, which contains ablation study, impact of risk threshold, and guarantees for practical use. RiskProp is open source and reproducible, and the code and dataset are publicly available after the paper is accepted.

4.1. Data Collection

We first obtain 803 ground truth account labels from an official Ethereum explorer and then include all the accounts and transactions that are within the one-hop and two-hop neighborhood of each labeled account. Next, we filter out the zero-ETH transactions and construct the records into a graph, retaining the largest weakly connected component for experiments. As a result, there are 1.19 million accounts and 4.13 million transactions in the network. In the dataset, 0.02 percent (243) are labeled illicit (e.g., phishing scam), whereas 0.05 percent (560) are labeled licit (e.g., exchanges). The remaining unknown accounts are not labeled with regards to licit versus illicit.

4.2. Effectiveness of De-anonymous Score

We use one-way analysis of variance (ANOVA) to assess whether there is a significant difference between illicit and licit transactions in the proposed de-anonymous score in Equation (1). We consider a transaction as illicit (versus licit) if its payer is marked as illicit (versus licit). Table 2 shows that compared with the random score, our proposed score achieves a larger mean square (MS) between groups and smaller MS within groups; in addition, our proposed score has a higher F value, and the -value equals . These results suggest that the de-anonymous score is a useful metric for assessing the quality of transactions.

| Random scores | De-anonymous score | |||||

|---|---|---|---|---|---|---|

| Src of var. | MS | F | -value | MS | F | -value |

| Between groups | 0 | |||||

| Within groups | - | - | - | - | ||

4.3. Analysis of Risk Rating Results

The principal task of RiskProp is to rate Ethereum accounts based on how ill-disposed they are. Given the account risk rating obtained by RiskProp, we first review the results and investigate the capability of RiskProp in discovering new risky accounts. Then, we dig deeper into the predicted high-risk accounts and obtain some insights.

4.3.1. Distribution of risk rating results

The risk value of an account ranges from 0 (low risk) to 10 (high risk). The distribution of the predicted risk scores is as follows: 33.58% are located at (0,2], 63.45% are located at (2,4], 2.03% are located at (4,6], 0.78% are located at (6, 8], and 0.19% are located at (8, 10]. This is consistent with expectations: The risk value of the Ethereum transaction network meets the power distribution law, indicating that the overwhelming majority of accounts act normally, and only very few accounts have abnormal behaviors. We are interested in whether the high-risk accounts predicted by RiskProp are actually questionable. Thus, we first manually check the top 150 accounts with the highest risk (with both in-coming and out-going transactions). The finding is that 119 out of 150 (approximately 80%) accounts have abnormal behaviors. Among these 119 illicit accounts, 43 accounts are already labeled as “phish/hack” by Etherscan, whereas the remaining 76 are newly discovered suspicious accounts that are not marked in the existing label library. This result indicates the capabilities of RiskProp in predicting undiscovered risky accounts and reducing financial losses.

4.3.2. Case studies of transaction pattern

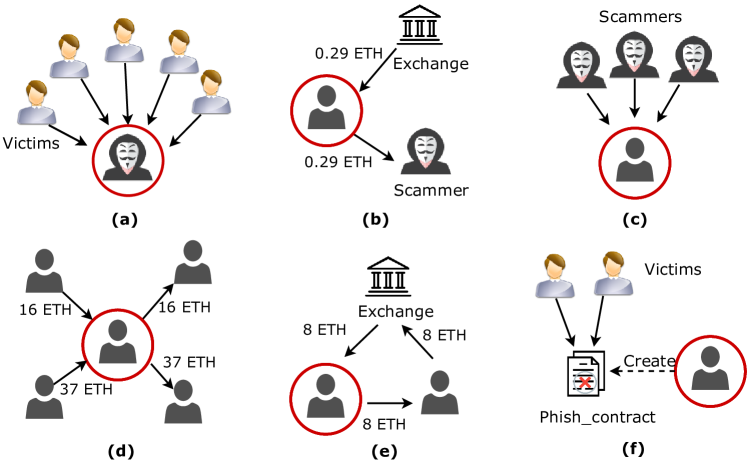

We then manually verified the predicted risky accounts by investigating their abnormal behaviors and find that there are many suspicious transaction patterns in the network. In order to save space, we show 6 typical patterns in Figure 5. These patterns are summarized from the real-world Ethereum transaction data and guided by current research and recommendation reports.

(a) Hacking scammers are a list of addresses related to phishing and hacks. Figure 5(a) shows a pattern of phishing accounts reported by users who suffered financial loss. A typical phishing scam on Ethereum is the “Bee Token ICO Scam” attack, in which the phishers sent fake emails to the investors of an ICO with a fake Ethereum address to deposit their contributions into. For example, account 0xe336 has been confirmed to be part of this “Bee Token” scam, and 243 ETH has been sent to this address by 165 victims.

(b) Fund source of hacking scammers are the upstream accounts of the known illicit accounts, which are collusion scam accounts to attract victims or provide money for hacking. As shown in Figure 5(b), the behaviors of collusion scam accounts may look similar to victims. Nevertheless, we find that the upstream collusion accounts appear to participate in fewer transactions with shorter time intervals, and there are attempts to transfer the entire ETH balance of the scammers according to the Red Flag Indicators of FATF (FATF, 2022).

(c) Money laundering of scammers are the downstream accounts of the known illicit accounts, which are collusion scam accounts to accept and transfer the stolen money, obfuscating the true sources. As shown in Figure 5(c), account 0x78f1 received stolen funds from several known hacking scammers, appearing to be the account used in the “placement” stage of money laundering. Another example is 0xcfdd, which receives stolen funds from the Fake Starbase Crowdsale Contribution account 0x122c. (d) Zero-out middle accounts are the middle accounts that serve as a bridge defined by Li et al. (Li et al., 2020). As shown in Figure 5(d), most of the received funds will be transferred out in short succession (such as within 24 hours). See 0x126e for an example.

(e) Round transfers among exchanges denote a pattern that an account withdraws ETH without additional activity to a private wallet and then deposits back to the exchange, as shown in Figure 5(e). Account 0x886e withdraws 0.4 ETH from Cryptopia exchange and then deposits the same amount of ETH back to Cryptopia, which is an unnecessary step and incurs transaction fees (FATF, 2022). Such a phenomenon indicates that the exchange is misused as a money-laundering mixer or is conducting wash trading (Victor and Weintraud, 2021).

(f) Creators of illicit contracts are often the manipulators behind the scenes. The Origin Protocol phishing scam contact account 0x9819 was created by account 0xff1a. After victims deposited money into the phishing contract, the creator transfers the stolen funds back to himself via internal transactions, which deliberately enhances anonymity.

We observe that many illicit accounts are outside the label library and are still considered risk-free. Based on the results, we infer that our RiskProp is able to expose unlabeled illicit accounts. This is crucial on Ethereum, which lacks authorized and effective regulation. In addition, the newly identified illicit accounts can complete the current label collection for additional analysis.

4.4. Comparative Evaluation Settings

To further evaluate the performance of our method and show the potential application, we employ the rating scores to conduct classification experiments that divide Ethereum accounts into illicit and licit accounts, and we compare the results with the existing baseline methods for further verification. We wish to investigate if RiskProp can give a higher risk rating for the known illicit accounts and a lower rating for known licit accounts.

4.4.1. Compared Methods

As mentioned earlier, RiskProp is the first algorithm that explores the risk rating of blockchain accounts. We chose a variety of methods (unsupervised and supervised) as baselines, which are similar to the problem we want to solve. We compare unsupervised RiskProp with (i) web page ranking, such as PageRank (Brin and Page, 1998), and (ii) bipartite graph-based fraud detection, such as FraudEagle (Akoglu et al., 2013), BIRDNEST (Hooi et al., 2016a), and REV2 (Kumar et al., 2018), which are also unsupervised methods.

The (semi-)supervised approaches are as follows. (i) Machine learning methods, e.g., logistic regression (LR), naïve Bayes (NB), decision tree (DT), support vector machine (SVM), random forest (RF), extreme gradient boosting (XGBoost), and LightGBM. These methods are used by (Al-E’mari et al., 2021; Agarwal et al., 2021; Chen et al., 2020; Li et al., 2022) for detection of abnormal Ethereum accounts. (ii) Traditional graph neural network, including DeepWalk, Node2Vec, and graph convolutional network (GCN) were conducted by Chen et al. (Chen et al., 2021) for detection of Ethereum phishing scams. (iii) Graph neural network for graphs with heterophily, such as CPGNN (Zhu et al., 2021). The application of this type of algorithms is a recent research advancement in the task of Ethereum account classification (Huang et al., 2022).

4.4.2. Evaluation Metrics

To evaluate the performance of the models, we calculate the following metrics: , , , , and . As we know, there are only 6 out of 10,000 (0.067 percent) accounts labeled in the entire dataset. To measure the order of the risk rating, we employ and to evaluate the ranking order of the algorithm ( means the top accounts). All baseline methods are tested using the original codes published by the authors. We repeat experiments 10 times and report the average results.

4.4.3. Implementation Details

We evaluate the methods with binary labeled accounts (illicit verse licit) and, thus, we assume accounts in the top 1% to be the illicit accounts (corresponding threshold: 6 for RiskProp). The reason for this threshold and percentage setting is discussed in Section 4.7. The split of the dataset in the (semi-)supervised setting is .

4.5. Comparative Evaluation Results

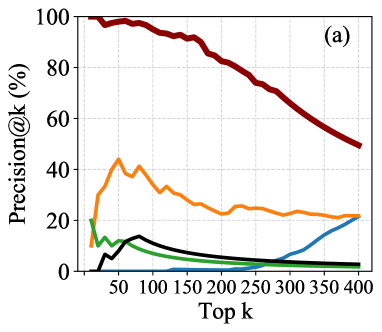

We report the and curves of the compared algorithms, as shown in Figure 6. We observe that RiskProp obtains superior precision and recall than that of baseline with different . Up to , the precision of RiskProp is almost 1 for illicit account prediction, which is surprising for an unsupervised setting. The curve of RiskProp is significantly higher than the compared methods, and also increases steadily with . Table 3 shows the performance of unsupervised and supervised methods separately. We observe that RiskProp remarkably outperforms the unsupervised graph rating baselines in terms of accuracy and AUC, improving by 38.90% and 34.16%, respectively. Meanwhile, for the licit account prediction, we observe that RiskProp beats the best baseline (FraudEagle) with a 10.48% improvement in its F1-score. These demonstrate the effectiveness of our account risk rating method without labeling information.

Next, we turn our attention to the results of the semi-supervised RiskProp+ compared with the existing (semi-)supervised classification in Table 3, from which we derive the following conclusions: 1) RiskProp+ outperforms all baseline methods by 12.32% in terms of F1-score, 13.62% in terms of AUC, and 10.56% in terms of accuracy. 2) The precision of licit accounts prediction is improved from 82.52% (i.e., the average precision in baselines) to 93.33%, which means more licit accounts can be correctly identified. 3) The superior performance of RiskProp is more significant in the prediction of illicit accounts. The recall of illicit accounts prediction is improved from 60.56% (i.e., the average recall of illicit accounts prediction in baselines) to 84.78%. This shows the effectiveness of our framework in the prediction of both illicit and licit accounts.

| Illicit account | Licit account | Total | ||||||

| Methods | P | R | F1 | P | R | F1 | Acc. | AUC |

| PageRank | 29.13 | 67.49 | 40.69 | 67.08 | 28.75 | 40.25 | 40.47 | 48.12 |

| FraudEagle | 12.28 | 2.88 | 4.670 | 68.36 | 91.07 | 78.10 | 64.38 | 46.98 |

| BIRDNEST | 22.24 | 47.32 | 30.26 | 55.24 | 28.21 | 37.35 | 34.00 | 37.77 |

| REV2 | 14.10 | 4.527 | 6.854 | 68.00 | 88.04 | 76.73 | 62.76 | 46.28 |

| RiskProp | 71.48 | 71.48 | 76.15 | 91.44 | 85.89 | 88.58 | 84.56 | 83.69 |

| Illicit account | Licit account | Total | ||||||

| Methods | P | R | F1 | P | R | F1 | Acc. | AUC |

| LR | 65.67 | 74.58 | 69.84 | 83.87 | 77.23 | 80.41 | 76.25 | 75.90 |

| NB | 59.79 | 98.31 | 74.36 | 98.41 | 61.39 | 75.61 | 75.00 | 79.85 |

| DT | 62.66 | 54.07 | 58.04 | 75.79 | 81.19 | 78.40 | 71.75 | 68.39 |

| SVM | 90.00 | 45.76 | 60.67 | 75.38 | 97.03 | 84.85 | 78.12 | 71.40 |

| RF | 71.52 | 53.39 | 61.14 | 75.55 | 86.93 | 80.84 | 74.00 | 69.40 |

| XGBoost | 67.35 | 55.95 | 61.11 | 76.58 | 84.16 | 80.19 | 70.05 | 73.75 |

| LightGBM | 75.77 | 65.19 | 69.93 | 84.23 | 92.57 | 88.21 | 81.86 | 77.75 |

| DeepWalk | 66.85 | 66.30 | 66.54 | 86.48 | 86.75 | 86.61 | 83.13 | 81.03 |

| Node2Vec | 62.36 | 63.26 | 62.76 | 85.10 | 84.56 | 84.82 | 78.13 | 72.78 |

| GCN | 20.83 | 27.78 | 23.81 | 79.46 | 68.99 | 73.86 | 60.63 | 47.40 |

| CPGNN | 52.17 | 61.54 | 56.47 | 86.84 | 81.82 | 84.26 | 76.88 | 71.68 |

| RiskProp+ | 70.91 | 84.78 | 77.23 | 93.33 | 85.96 | 89.49 | 85.63 | 85.37 |

4.6. Ablation Study

To further validate the contribution of each component of the proposed RiskProp+, we conduct an ablation study as follows.

RiskProp+ (Full model): All components of the model and label data are included.

w/o label: Labels are unavailable in the learning procedure, and the model is trained in an unsupervised manner.

w/o network propagation (NP): Remove the NP procedure and calculate the average de-anonymous scores () for each accounts’ outgoing transactions (payer role). An account is predicted as abnormal if its .

w/o de-anonymous score (DS): Replace DS with random scores, ranging from 1 to 1.

| Methods | Precision | Recall | F1-score |

|---|---|---|---|

| RiskProp+ | 0.7091 | 0.8478 | 0.7723 |

| RiskProp+ (w/o label) | 0.7148 | 0.8148 | 0.7615 |

| RiskProp+ (w/o NP) | 0.3811 | 0.9959 | 0.5513 |

| RiskProp+ (w/o DS) | 0.4737 | 0.1957 | 0.2769 |

We derive the following findings from Table 4: 1) Without the labels, the F1-score drops only slightly, indicating that our RiskProp does not rely on label data and can obtain good results in an unsupervised manner. To our surprise, the full model outperforms the RiskProp (w/o label), with a 3.3% increase in recall and 0.51% decrease in precision. This may be possibly explained by the reliability values of labeled illicit accounts remaining unchanged during training in the supervised setting. 2) RiskProp (w/o NP) has a only lower precision but a greatly improved recall, revealing that most of the illicit accounts are correctly predicted as illicit but that some licit accounts are misjudged to be illicit. This result demonstrates that de-anonymous score is an effective indicator of illicit transactions but their confidence varies among transactions. This result also confirms why we need to consider the confidence of the score in the propagation mechanism. 3) RiskProp (w/o DS) yields low precision (47.37%) and severely low recall (19.57%). This result demonstrates that, even if the network propagation model is retained, the wrong scores of transactions will be spread throughout the entire Ethereum transaction network, resulting in poor prediction results.

4.7. Risk Threshold of RiskProp

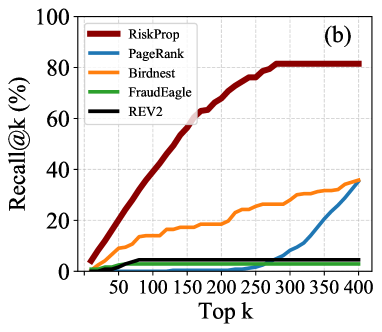

Given accounts in the reversed order of their risk ratings, a natural question is how to classify licit or illicit accounts according to their risk ratings for the classification task? One possible option is to determine the percentage of known illicit labels in the dataset and set the risk value of this percentage as a demarcation line for account classification. However, the percentage is imprecise because some of the illicit accounts remain unrevealed according to the experimental results in Section 4.3.2. Therefore, we try to establish a suitable risk threshold () of RiskProp by conducting classification experiments. Figure 7(a) demonstrates the results of illicit account prediction with different risk thresholds, ranging from 1 to 10. As expected, the precision increases while the recall decreases with increasing . In addition, F1, accuracy, and AUC first increase and then decrease with the increase in . The best performance for F1 and AUC is when . Thus, we set the risk threshold for RiskProp.

4.8. Guarantees for Practical Use

Here, we present guarantees for RiskProp in practical use regarding the following aspects: 1) guarantee of convergence; 2) time complexity; and 3) linear scalability.

Convergence and Uniqueness. We present the theoretical properties of RiskProp, including the proofs of prior knowledge, convergence, and uniqueness of the proposed metrics, i.e., reliability, trustiness, and confidence. Proofs are shown in the Appendix due to lack of space.

Time complexity. In each interaction, the RiskProp updates the reliability, Trustiness metrics of accounts and Confidence metric of transactions. Therefore, the complexity of each iteration is , is the total edges in the payer–payee network. Thus, for iterations, the total running time is .

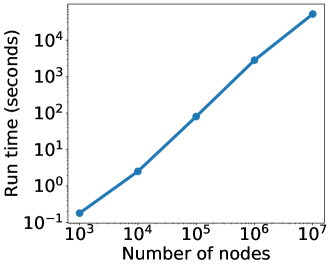

Linear scalability. We have shown that RiskProp is linear in running time in the number of nodes. To show this experimentally as well, we create random networks of an increasing number of nodes and edges and compute the running time of the algorithm until convergence. Figure 7(b) shows that the running time increases linearly with the number of nodes in the network. Therefore, we can conclude that RiskProp is a scalable rating method that is suitable for applications on large-scale transaction networks.

Analysis of incorrect predictions. Furthermore, the results of the RiskProp+ experiment showed that 39 out of 46 (85%) phishing accounts were correctly predicted as illicit accounts. To understand why the remaining accounts failed to be detected as illicit by our model, we manually checked their transactions and neighbors and obtained the following results: (i) For one of the accounts, we have a risk score of 5.72, and in practice, the system will also warn about such accounts that are close to the risk threshold (). (ii) One account is set as the default risk value because the phishing account has no outgoing transactions for the time being, and in practice, we can make correct predictions as soon as the phishing account starts laundering money. (iii) Among the remaining five accounts, one account has a high transaction volume of 154. The remaining four accounts have a high volume of transactions along with withdrawals of ETH from exchanges, which directly contributed to the high de-anonymity score of transactions. However, there are two sides to the story: regulation and fraud are a game of confrontation. For hackers, reusing accounts reduces the probability of being identified as high risk and, at the same time, reusing accounts and withdrawing money from exchanges increase the risk of exposure and fund freezing.

5. Related Work

Risk control studies in cryptocurrency. In recent years, there has been growing interest in account clustering and detecting illicit activities (e.g., financial scams, money laundering) in cryptocurrency transaction networks (Wu et al., 2021). Victor (Victor, 2020) is the first to propose clustering heuristics for the Ethereum’s account model, including deposit address reuse, airdrop multi-participation, and self-authorization. A recent review of the literature on cryptocurrency scams (Bartoletti et al., 2021) showed that the existing methods (e.g., (Chen et al., 2018), (Farrugia et al., 2020), and (Ibrahim et al., 2021)) are mainly based on supervised classifiers fed with handcrafted features. Many attempts have been made (Tam et al., 2019; Weber et al., 2019; Wu et al., 2022) to incorporate structural information by learning the latent representations of accounts. Some researchers have investigated and modeled the money flow from a network perspective (Lin et al., 2020; Lal et al., 2021) to better identify illicit activities. After all, there is still a black area regarding the estimation of the risk value of Ethereum accounts, which is the key task in alerting about suspicious accounts and transactions on the chain.

Rating and ranking on graph data. The aim of ratings and rankings on graph data is to provide a score or an order for each node in a graph. Currently, the main solutions are based on link analysis technique (Sangers et al., 2019), Bayesian model (Hooi et al., 2016a), and iterative learning (Hooi et al., 2016b), etc. Similarly to the proposed RiskProp algorithm, (Kumar et al., 2018) proposed axioms and iterative formulations to establish the relationship between ratings. In (Mishra and Bhattacharya, 2011), the authors measured the bias and prestige of nodes in networks based on trust scores. In (Kurshan and Shen, 2020), the authors highlighted that graph-based approaches provide unique solution opportunities for financial crime and fraud detection. A review on this topic (Akoglu et al., 2015) described the problems in current studies: lack of ground truths, imbalanced class, and large-scale network. These challenges also exist in our risk rating problem on Ethereum transaction networks.

6. Conclusions and Future Work

In this paper, we present the first systematic study to assess the account risk via a rating system named RiskProp. In RiskProp, we modeled transaction records of Ethereum as a bipartite graph, proposed a novel metric called de-anonymous score to quantify the transaction risk, and designed a network propagation mechanism based on transaction semantics. By analyzing the rating results and manually checking the accounts with high risk, we evaluated the performance of RiskProp and obtained new insights about transaction risks on Ethereum. In addition, we employed the obtained risk scores to conduct illicit/licit account classification experiments on labeled data, and the superiority of this method over baseline methods further verified the effectiveness of RiskProp in risk estimation. For future work, we plan to integrate the transaction amounts and temporal information in our model, develop a web page or online tool for querying risk values of accounts, and share the details of risky cases with the Ethereum community.

References

- (1)

- Agarwal et al. (2021) Rachit Agarwal, Shikhar Barve, and Sandeep Kumar Shukla. 2021. Detecting malicious accounts in permissionless blockchains using temporal graph properties. Applied Network Science 6, 1 (Dec. 2021), 9.

- Akoglu et al. (2013) Leman Akoglu, Rishi Chandy, and Christos Faloutsos. 2013. Opinion fraud detection in online reviews by network effects. In Proceedings of the International AAAI Conference on Web and Social Media, Vol. 7. 2–11.

- Akoglu et al. (2015) Leman Akoglu, Hanghang Tong, and Danai Koutra. 2015. Graph based anomaly detection and description: A survey. Data Mining and Knowledge Discovery 29, 3 (2015), 626–688.

- Al-E’mari et al. (2021) Salam Al-E’mari, Mohammed Anbar, Yousef Sanjalawe, and Selvakumar Manickam. 2021. A Labeled Transactions-Based Dataset on the Ethereum Network. Communications in Computer and Information Science 1347 (2021), 61–79.

- Bartoletti et al. (2021) Massimo Bartoletti, Stefano Lande, Andrea Loddo, Livio Pompianu, and Sergio Serusi. 2021. Cryptocurrency scams: Analysis and perspectives. IEEE Access 9 (2021), 148353–148373.

- Brin and Page (1998) Sergey Brin and Lawrence Page. 1998. The anatomy of a large-scale hypertextual Web search engine. Computer Networks and ISDN Systems 30, 1 (1998), 107–117.

- Chen et al. (2021) Liang Chen, Jiaying Peng, Yang Liu, Jintang Li, Fenfang Xie, and Zibin Zheng. 2021. Phishing Scams Detection in Ethereum Transaction Network. ACM Transactions on Internet Technology 21, 1 (Feb. 2021), 1–16.

- Chen et al. (2020) Weili Chen, Xiongfeng Guo, Zhiguang Chen, Zibin Zheng, and Yutong Lu. 2020. Phishing scam detection on Ethereum: Towards financial security for blockchain ecosystem. In IJCAI. 4506–4512.

- Chen et al. (2018) Weili Chen, Zibin Zheng, Jiahui Cui, Edith Ngai, Peilin Zheng, and Yuren Zhou. 2018. Detecting ponzi schemes on Ethereum: Towards healthier blockchain technology. In WWW. ACM, 1409–1418.

- Farrugia et al. (2020) Steven Farrugia, Joshua Ellul, and George Azzopardi. 2020. Detection of illicit accounts over the Ethereum blockchain. Expert Systems with Applications 150 (Jul. 2020), 113318.

- FATF (2022) FATF. 2022. Money Laundering and Terrorist Financing Red Flag Indicators Associated with Virtual Assets. http://www.fatf-gafi.org/publications/fatfrecommendations/documents/Virtual-Assets-Red-Flag-Indicators.html.

- Hooi et al. (2016a) Bryan Hooi, Neil Shah, Alex Beutel, Stephan Günnemann, Leman Akoglu, Mohit Kumar, Disha Makhija, and Christos Faloutsos. 2016a. Birdnest: Bayesian inference for ratings-fraud detection. In ICDM. SIAM, 495–503.

- Hooi et al. (2016b) Bryan Hooi, Hyun Ah Song, Alex Beutel, Neil Shah, Kijung Shin, and Christos Faloutsos. 2016b. FRAUDAR: Bounding graph fraud in the face of camouflage. In SIGKDD. ACM, 895–904.

- Huang et al. (2022) Tao Huang, Dan Lin, and Jiajing Wu. 2022. Ethereum Account Classification Based on Graph Convolutional Network. IEEE Transactions on Circuits and Systems II: Express Briefs 69, 5 (2022), 2528–2532.

- Ibrahim et al. (2021) Rahmeh Fawaz Ibrahim, Aseel Mohammad Elian, and Mohammed Ababneh. 2021. Illicit account detection in the Ethereum blockchain using machine learning. In ICIT. IEEE, 488–493.

- Kumar et al. (2018) Srijan Kumar, Bryan Hooi, Disha Makhija, Mohit Kumar, Christos Faloutsos, and V.S. Subrahmanian. 2018. REV2: Fraudulent user prediction in rating platforms. In WSDM. ACM, 333–341.

- Kurshan and Shen (2020) Eren Kurshan and Hongda Shen. 2020. Graph computing for financial crime and fraud detection: Trends, challenges and outlook. International Journal of Semantic Computing 14, 4 (2020), 565–589.

- Lal et al. (2021) Banwari Lal, Rachit Agarwal, and Sandeep Kumar Shukla. 2021. Understanding money trails of suspicious activities in a cryptocurrency-based blockchain. arXiv preprint arXiv:2108.11818 (2021).

- Li et al. (2022) Sijia Li, Gaopeng Gou, Chang Liu, Chengshang Hou, Zhenzhen Li, and Gang Xiong. 2022. TTAGN: Temporal Transaction Aggregation Graph Network for Ethereum Phishing Scams Detection. In Proceedings of the ACM Web Conference. ACM, 661–669.

- Li et al. (2020) Xiangfeng Li, Shenghua Liu, Zifeng Li, Xiaotian Han, Chuan Shi, Bryan Hooi, He Huang, and Xueqi Cheng. 2020. Flowscope: Spotting money laundering based on graphs. In AAAI, Vol. 34. 4731–4738.

- Lin et al. (2020) Dan Lin, Jiajing Wu, Qi Yuan, and Zibin Zheng. 2020. Modeling and understanding Ethereum transaction records via a complex network approach. IEEE Transactions on Circuits and Systems II: Express Briefs 67, 11 (2020), 2737–2741.

- Mishra and Bhattacharya (2011) Abhinav Mishra and Arnab Bhattacharya. 2011. Finding the bias and prestige of nodes in networks based on trust scores. In WWW. ACM, 567–576.

- Möser et al. (2014) Malte Möser, Rainer Böhme, and Dominic Breuker. 2014. Towards risk scoring of Bitcoin transactions. In FC. Springer, 16–32.

- Sangers et al. (2019) Alex Sangers, Maran van Heesch, Thomas Attema, Thijs Veugen, Mark Wiggerman, Jan Veldsink, Oscar Bloemen, and Daniël Worm. 2019. Secure multiparty pageRank algorithm for collaborative fraud detection. In FC. Springer, 605–623.

- Tam et al. (2019) Da Sun Handason Tam, Wing Cheong Lau, Bin Hu, Qiu Fang Ying, Dah Ming Chiu, and Hong Liu. 2019. Identifying illicit accounts in large scale e-payment networks – A graph representation learning approach. arXiv preprint arXiv:1906.05546 (2019).

- Team (2021) Chainalysis Team. 2021. Report: Key Players of the Cryptocurrency Ecosystem. Retrieved January 11, 2022 from https://go.chainalysis.com/rs/503-FAP-074/images/Key-players-in-crypto-report.pdf

- Victor (2020) Friedhelm Victor. 2020. Address clustering heuristics for Ethereum. In FC. Springer, 617–633.

- Victor and Weintraud (2021) Friedhelm Victor and Andrea Marie Weintraud. 2021. Detecting and quantifying wash trading on decentralized cryptocurrency exchanges. In WWW. ACM, 23–32.

- Weber et al. (2019) Mark Weber, Giacomo Domeniconi, Jie Chen, Daniel Karl I. Weidele, Claudio Bellei, Tom Robinson, and Charles E. Leiserson. 2019. Anti-money laundering in Bitcoin: Experimenting with graph convolutional networks for financial forensics. arXiv preprint arXiv:1908.02591 (2019).

- Wood (2014) Gavin Wood. 2014. Ethereum: A secure decentralised generalised transaction ledger. Ethereum Project Yellow Paper 151 (2014), 1–32.

- Wu et al. (2021) Jiajing Wu, Jieli Liu, Yijing Zhao, and Zibin Zheng. 2021. Analysis of cryptocurrency transactions from a network perspective: An overview. Journal of Network and Computer Applications 190 (2021), 103139.

- Wu et al. (2022) Jiajing Wu, Qi Yuan, Dan Lin, Wei You, Weili Chen, Chuan Chen, and Zibin Zheng. 2022. Who are the phishers? Phishing scam detection on Ethereum via network embedding. IEEE Transactions on Systems, Man, and Cybernetics: Systems 52, 2 (2022), 1156–1166.

- Yuan et al. (2020) Zihao Yuan, Qi Yuan, and Jiajing Wu. 2020. Phishing detection on ethereum via learning representation of transaction subgraphs. In Blocksys. Springer, 178–191.

- Zhu et al. (2021) Jiong Zhu, Ryan A Rossi, Anup Rao, Tung Mai, Nedim Lipka, Nesreen K Ahmed, and Danai Koutra. 2021. Graph neural networks with heterophily. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 35. 11168–11176.

Appendix A Appendix

A.1. Proof for Prior Knowledge

In this part, we provide proofs that the proposed metrics, i.e., Reliability, Trustiness, and Confidence satisfy Prior knowledge 1 - 5. Prior knowledge 1 in the main paper is the following:

[Prior knowledge 1] Payees with higher trustiness receive transactions with higher de-anonymous scores. Formally, if two payees and have a one-to-one mapping, and , then .

The formulation to be used to show that the prior knowledge is satisfied is Equations 2, 3, and 4 in the main paper.

Proof.

To prove the Prior Knowledge 1, let us take two payees and that have identically ego networks and a one-to-one mapping , such that , , and .

According to Equation 2, we have

As , so

As 0 because Confidence are non-negative,

The other items of prior knowledge have very similar and straightforward proof. ∎

A.2. Proof for Convergence

Before the proof of convergence, we first discuss the boundary of proposed metrics. At the end of iteration of Algorithm 1, and by equation 2, 3, and 4, we get,

are their final values after convergence.

Lemma A.1.

(Boundary discussion) Set the maximum score in the transaction network as , namely:

then .

The difference between a payee ’s final Trustiness and its Trustiness after the first iteration is

Similarly,

Proof.

First, we state that is strictly less than 1 in practice. According to the formulation of of the main paper, we can see that when and , it is an extreme situation where the largest number of payments and receptions of the entire network appears in one transaction. The other case is when that and at the same time. This situation presents to be some isolated transactions, however, they do not propagate risk and thus do not influence convergence. These situations are out of our consideration. So we get is strictly smaller than 1.

Then, we prove that is bounded during the iterations:

Since , we get,

Since , we have,

| (5) |

Since , and , we get,

Next, we conduct the proof on :

Again, since , we get,

| (6) |

Similarly, since , we have,

Finally, we calculate the bound of :

Since , we have

Since , it follows that,

| (7) |

Since , and, we get,

For convenience, we let . Since , then .

∎

Theorem A.2.

Convergence of Propagation: The difference during iterations is bounded as as (), . As increases, the difference decreases and converges to . Similarly, , .

Proof.

First, we will prove the convergence of Confidence using mathematical induction.

Base case of induction.

When , as we proved in Lemma A.1, we get:

Induction step.

We assume by hypothesis that

which is consistent with the base case already.

Then, by substituting Equations 9 and 10 into Equation 8, for the case in the next iteration where time is , we have,

Therefore, .

As discussed in the Lemma A.1. we know that is strictly smaller than 1, then we have . As increases, and , so after t iterations, , , and , the algorithm converges.

∎

A.3. Proof for Uniqueness

In this part, we provides proofs that Reliability, Trustiness, and Confidence are unique.

Theorem A.3.

Confidence, Reliability, and Trustiness converge to the unique value.

Proof.

First, we consider the uniqueness of Confidence using mathematical contradiction.

Let the converges to different values. So, let be the transaction with maximum Confidence difference, (with ), between its two possible and .

According to Equation 8, we get,

| (11) |

| (12) |

| (13) |

Thus, by solving and with the condition that , we obtain . Then, and converge value of Confidence is unique. The uniqueness of Trustiness and Reliability have similar proof.

∎