Sizing Grid-Connected Wind Power Generation and Energy Storage with Wake Effect and Endogenous Uncertainty: A Distributionally Robust Method

Abstract

Wind power, as a green energy resource, is growing rapidly worldwide, along with energy storage systems (ESSs) to mitigate its volatility. Sizing of wind power generation and ESSs has become an important problem to be addressed. Wake effect in a wind farm can cause wind speed deficits and a drop in downstream wind turbine power generation, which however was rarely considered in the sizing problem in power systems. In this paper, a bi-objective distributionally robust optimization (DRO) model is proposed to determine the capacities of wind power generation and ESSs considering the wake effect. An ambiguity set based on Wasserstein metric is established to characterize the wind power and demand uncertainties. In particular, wind power uncertainty is affected by the wind power generation capacity which is determined in the first stage. Thus, the proposed model is a DRO problem with endogenous uncertainty (or decision-dependent uncertainty). To solve the proposed model, a stochastic programming approximation method based on minimum Lipschitz constants is developed to turn the DRO model into a linear program. Then, an iterative algorithm is built, embedded with methods for evaluating the minimum Lipschitz constants. Case studies demonstrate the necessity of considering wake effect and the effectiveness of the proposed method.

Index Terms:

sizing, wake effect, endogenous uncertainty, distributionally robust optimization, energy storageI Introduction

The large-scale integration of renewable energy is one of the worldwide efforts towards carbon neutrality [1]. Wind power, as one of the leading clean energy resources, has developed rapidly in recent years. However, wind resources are affected by weather conditions, leading to highly volatile and stochastic wind power, which threatens the power system operation. Energy storage systems (ESSs) that can shift energy over time are installed to better accommodate uncertain renewable generations. Therefore, the sizing of wind power generation and ESSs is an important problem to be addressed.

A vast literature has been devoted to the generation and ESS siting and sizing problems in renewable-integrated power systems. These studies can be divided into three categories based on stochastic programming (SP), robust optimization (RO), and distributionally robust optimization (DRO), respectively. The SP methods assume known probability distributions of the uncertainties, which are represented either by parametrized distributions or a set of scenarios. The sizing problem of generation and storage expansion [2], transmission and ESS capacities [3], and hybrid ESS systems [4] were studied using the SP method. In [5], the reduction of wind power prediction error caused by the aggregation effect was modeled by decision-dependent Gaussian distributions and further represented by generated scenarios. However, in practice, it is difficult to obtain the accurate uncertainty distribution in the planning stage, and an inexact empirical distribution may lead to infeasible or suboptimal results. To overcome this shortcoming, RO has been adopted, which optimizes the performance under the worst-case scenario within an uncertainty set. A tri-level robust model was proposed for ESS planning [6], where the uncertainties of wind power investment and coal-fired unit retirement were considered. Reference [7] jointly considered the short-term fluctuations and the long-term uncertainties of load and renewable growths in the ESS planning problem. However, as the worst case rarely happens, the RO method may lead to over-conservative sizing results.

DRO technique is in-between SP and RO methods, which optimizes decisions with respect to the worst-case distribution in a predefined ambiguity set. It can achieve a good tradeoff between optimality and robustness. DRO method has appeared in power system operation problems. Moments were used in [8] to construct the ambiguity set for distributionally robust energy management of energy hubs. The uncertain market price was modeled by ambiguity sets based on -divergence in the self-scheduling of compressed air energy storage in [9]. DRO method has also been adopted in power system sizing problems. Aiming at optimal generation expansion, a DRO model with risk constraints was put forward in [10] with an ambiguity set based on moments and unimodality. However, large numbers of data are needed to accurately estimate moments and different distributions may have the same moments. A DRO siting and sizing method for ESS was proposed in [11] based on -divergence, where the ESS lifespan model was considered. However, -divergence is only well-defined for discrete distributions supported on the range of the sample data. On the contrary, Wasserstein distance is able to measure the difference between general distributions. A distributionally robust chance-constrained model was proposed for clustered generation expansion in [12] with a Wasserstein-metric-based ambiguity set. However, none of the studies above considered the wake effect in a wind farm.

The wake effect in a wind farm refers to the decrease in gross energy production due to the changes in wind speed caused by the impact of wind turbines (WTs) on each other. To be specific, the wake from the upstream WTs decreases the wind’s kinetic energy and lowers the wind speed at the downstream WTs. Studies on wind farms have been aware of the wake effect and considered it in problems such as reliability evaluation [13], dynamic equivalent model [14], control strategy [15], maintenance scheduling [16], etc. As the wake effect can reduce the power output by about 20% [17], it is nonnegligible in wind farm planning. Currently, the wake effect is mainly considered in the layout design of wind farms. For instance, the wind farm layout was optimized in [18] considering the wake effect and the temporal correlation of wind speed. Another layout optimization approach was proposed in [19] based on an adaptive evolutionary algorithm with Monte Carlo tree search reinforcement learning. The comprehensive problem of wind farm area, shape, and layout decisions was studied in [20] and the method was applied to an offshore wind farm in the UK. The optimal ESS allocation inside the wind farm was investigated in [21] to better support frequency. However, the aforementioned studies did not consider the impact of wind power generation on power system operation. The SP method proposed in [22] planned wind farms in distribution systems, where the wake effect was integrated via simulations. The optimal solution was searched in an enumeration manner with an acceleration constraint, which may be computationally expensive for bulk power systems with a large number of WTs.

This paper proposes a distributionally robust optimization method with a decision-dependent ambiguity set for sizing wind power generation and energy storage considering the wake effect. The contributions are:

(1) Sizing Model. A distributionally robust optimization model is developed for the sizing of wind power generation and ESSs in power systems. The worst-case expected fuel cost in normal operation conditions is minimized while the worst-case expected load shedding in extreme conditions is upper bounded in the constraint. Distinct from the traditional models, the wake effect in a wind farm is considered. This makes the sizing model more practical. In particular, simulations are carried out to evaluate the wake effect. Based on this, a piecewise linear model showing how the available wind power generation changes with wind conditions and the capacity is developed. The model is then used for modeling wind power uncertainty via Wasserstein-metric-based ambiguity sets. Due to the wake effect, the size of the ambiguity set depends on the first-stage sizing decisions, and is thus decision-dependent. Therefore, the proposed model is a DRO problem with both endogenous/decision-dependent uncertainty (DDU) and exogenous/decision-independent uncertainty (DIU).

(2) Solution Method. To solve the proposed model, we first develop an SP approximation of it with the help of minimum Lipschitz constants. Then, an iterative algorithm embedded with methods for calculating the upper bounds of the minimum Lipschitz constants is established to solve the obtained SP problem. The proposed algorithm is novel in that it provides a systematic method for solving the Wasserstein-metric-based DRO model and can deal with DDUs that are seldom considered in previous work.

The rest of this paper is organized as follows. Section II establishes a linear approximation of available wind power function considering the wake effect. A distributionally robust wind-storage sizing model that takes into account the wake effect is proposed in Section III with solution method developed in Section IV. Case studies are reported in Section V. Finally, Section VI concludes the paper.

II Linearized Available Wind Power Function Considering Wake Effect

In this section, we characterize the available wind power in a wind farm considering the wake effect. First, the Jensen wake model is adopted to model the wake effect of a single WT. Simulations are carried out to calculate the available wind power in a wind farm under different total WT capacities and real-time wind conditions, whose relationship is a nonlinear function. Then, the nonlinear function is further linearized for computational tractability.

II-A Available Wind Power By Simulation

Jensen wake model is a widely used analytical wake model [23]. Suppose the wind direction is parallel to the line between two WTs, then according to the Jensen wake model, the wind speed at the downstream WT can be calculated as follows [24]:

| (1) | ||||

| (2) |

where and are the wind speed values at the upstream and downstream WTs, respectively; is the distance between the two WTs; the thrust factor , the turbine rotor diameter , the hub height , and the roughness length are parameters; is the wake decay constant. As (1) shows, the closer the two WTs to each other, the stronger the wake and the wind speed deficit.

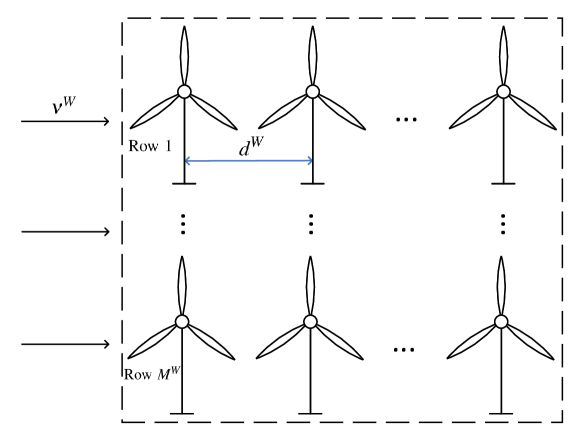

For simplicity, we consider the wind farm layout in Fig. 1 as an example: The wind farm will be built in a given rectangular area; all WTs have the same types and parameters and are placed evenly; the wind is blowing parallel to the rows of WTs; the distance between adjacent rows is fixed and large enough so that the wake effect between rows can be neglected. A similar assumption can be found in [24]. Nonetheless, other wind farm layouts as well as wake models can be used for simulation and the subsequent process from Section II-B to Section IV can still be carried out. Suppose the length of a row is and the number of WTs in a row is , then the distance between adjacent WTs is . The wind speed at the -th WT is

| (3) |

The available wind power of one WT can be calculated using the following function [25].

| (7) |

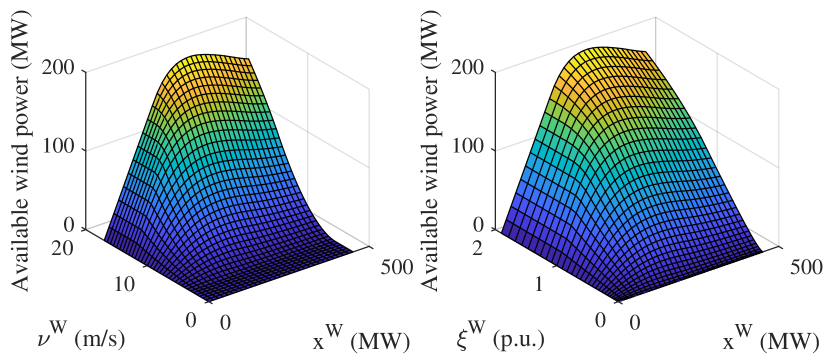

where is the available wind power and is the wind speed at this WT; the cut-in speed , cut-out speed , rated speed , and rated power are parameters. Sum up the available power of all WTs, then we have the available wind power of the wind farm , where is the number of rows. Given and the initial wind speed at the wind farm, the total capacity of WTs and the total available wind power can be uniquely determined. Hence, we can characterize the change of available wind power with and by simulations.

To be specific, let and denote the upper bounds of and , respectively. Use wind speed values for discretization. For and , calculate the corresponding and and get tuples for . The change of with and is shown in Fig. 2 (left). When is fixed, as varies from 0 to , first increases proportionally, but then its growth slows down; even decreases when is too large because of the severe wake effect. This shows the necessity of considering the wake effect in the sizing problem.

II-B Linearized Available Wind Power Function

Considering that the relationship between and is highly nonlinear, to facilitate the computation, we establish a piecewise linear approximation for the available wind power function. First, to eliminate the nonlinear term in (7), we introduce an auxiliary variable as follows.

| (10) |

Then, the available wind power can be viewed as a function of and , which is depicted in Fig. 2 (right). The actual wind power output can vary within 0 and , so the feasible region of wind power is the region below the plane in Fig. 2 and above zero, which can be approximated by its convex hull. Multi-Parametric Toolbox (MPT) 3.0 [26] can find the convex hull of a set of points, which is represented by its extreme point set or a linear inequality set describing the facets. We use MPT to find the convex hull of the feasible region of wind power and get a polyhedron as follows.

| (11) |

where , , and are the parameters of inequalities and is a piecewise linear approximation of the available wind power function.

There may be a large number of inequalities in (11). To improve the computational efficiency, we propose Algorithm 1 to select a representative subset of inequalities while maintaining acceptable precision. Algorithm 1 starts from a cuboid containing the original polyhedron, and adds the remaining most important inequality in each iteration until the approximation error is lower than a certain level. Algorithm 1 always converges because the number of inequalities is finite.

III Distributionally Robust Sizing Model

In this section, we first propose models to evaluate the operation costs given the sizing strategies (capacities), and then build the ambiguity sets, based on which the distributionally robust sizing model is established.

III-A Operation Problems

First, we consider the operation stage with given wind power generation and ESS capacities and uncertainty realizations. Two models are developed to evaluate the operation cost under 1) normal conditions, where the total fuel cost is minimized and load shedding is not allowed; and 2) extreme conditions, where the total load shedding is minimized.

III-A1 Power System Operation Constraints

Let , , and be the set of periods, buses, and transmission lines, respectively. Denote the period length by . The power system operation constraints are as follows.

| (12a) | ||||

| (12b) | ||||

| (12c) | ||||

| (12d) | ||||

| (12e) | ||||

| (12f) | ||||

| (12g) | ||||

| (12h) | ||||

| (12i) | ||||

| (12j) | ||||

| (12k) | ||||

Constraints (12a)-(12d) constitute the model of traditional generators, where and denote the generation power and fuel cost of the traditional generator at bus in period , respectively. The fuel cost is modeled by the maximum of a set of linear functions in (12a), where are constant coefficients. Constraint (12b) stipulates the range of generation power. Constraints (12c) and (12d) consist of the lower bound and upper bound of ramp rates, where (12d) ensures continuous operation. Constraints (12e)-(12h) compose the model of ESSs, where , are the charging and discharging power of the ESS at bus in period , respectively; is the stored energy at the end of period . The power and energy capacities of the ESS at bus are denoted by and , respectively. Constraint (12e) limits the charging/discharging power. Constraints (12f) and (12g) are for the dynamics of the stored energy, with charging and discharging efficiencies and . Constraint (12h) stipulates the lower bound and upper bound of ESSs’ state-of-charge. The complementary constraint preventing simultaneous charging and discharging is omitted according to Proposition 1 in [27], in the sense that the minimized fuel cost or load shedding values will not be affected. The DC power flow model is used in (12i), where is the active power flow from node to node in period , and are the reactance and capacity of the line, respectively, and denotes the voltage angle. The load demand, load shedding, and the power curtailment at bus in period are denoted by , , and , respectively. Their bounds are in (12j). Constraint (12k) is the nodal power balance equation, in which is the wind power generation at bus in period .

III-A2 Operation Problem in Normal Conditions

In normal conditions, the goal is to minimize the total fuel cost of traditional generators.

| (13a) | ||||

| s.t. | (13b) | |||

| (13c) | ||||

The objective (13a) minimizes the total fuel cost. The fuel cost model in (12a) can be equivalently transformed into inequalities in (13b) thanks to the minimization operation in the objective. The remaining constraints in the power system model are included and the load shedding is forced to be zero in (13c) since no load shedding is allowed in normal conditions. Let denote the capacity variable and be the uncertainty realization. When changes, the optimal objective value (13a) changes accordingly, which is denoted by .

III-A3 Operation Problem in Extreme Conditions

In extreme conditions, the goal is to minimize the total load shedding.

| (14a) | ||||

| s.t. | (14b) | |||

The total load shedding in (14a) is minimized subject to the power system constraints in (14b). Fuel cost is not considered since it is not a major concern in extreme conditions. Similarly, the optimal objective value is a function of and denoted by , showing the total load shedding under given .

III-B Decision-Dependent Ambiguity Sets

We use ambiguity sets to model uncertainties, formed by a set of distributions around the empirical distribution with distances measured by Wasserstein metric.

III-B1 Empirical Distributions

Suppose we have some empirical data of wind and load demand in extreme conditions, where is the index set of extreme scenarios. Then the available wind power is

| (15) |

where is the linearized approximation obtained by Algorithm 1; is a theoretical upper bound for the available wind power without considering the wake effect and the cut-out wind speed, which can be seen in (7) and (10). The notation is to emphasize that the available wind power is decision-dependent. Thus, the data of scenario are . Based on the data, the empirical probability distribution in extreme conditions is

where is the number of scenarios in , denotes the Dirac distribution with unit mass at the subscript point, and represents the product operation of distributions. Therefore, probability is assigned to each available wind power sample under the empirical distribution . Denote the index set of normal scenarios by , then similarly the corresponding empirical distribution can be defined.

III-B2 Range of Uncertain Variables

For the wind farm at bus , the range of the wind power output in extreme conditions is built by

The wind power cannot exceed the bounds obtained in Algorithm 1 as well as the capacity . Again we denote the wind power range by to emphasize the decision-dependent feature.

The range of load demand in extreme conditions is given by , where is the maximum possible load demand at bus .

For normal conditions, the range is defined as the convex hull of the corresponding scenarios. Then the range of wind power in normal conditions is

where are the coefficients of convex combination; all the convex combinations of are contained in . The range of load demand in normal conditions has a similar form. Compared with normal conditions, the range of uncertain variables in extreme conditions is larger to include the possible extreme scenarios, i.e., and .

III-B3 Wasserstein Metric and Ambiguity Set

Wasserstein metric is a way to measure the distance between two distributions [28]. For distributions and defined on , the 1-norm Wasserstein metric between them is

| (16) | |||

where is the 1-norm. It can be regarded as the minimum cost of transporting the mass distribution to , in which the transport way is represented by the joint distribution .

Inspired by the definition of Wasserstein metric, we propose the following ambiguity set for uncertain variable in extreme conditions.

| (17) |

The distributions in are the average of the product distributions of and . denotes the set of all the distributions supported on the range in the bracket. is a joint distribution with marginals and the empirical distribution . The Wasserstein metric between them is no larger than , where is a parameter controlling the size of the ambiguity set. Since larger capacity leads to larger fluctuation of wind power, we use the product as the bound. The constraints of load demand distribution have a similar bound . Let , then the ambiguity set contains for all non-negative and it becomes a singleton when , the zero vector.

The ambiguity set in normal conditions can be defined similarly by replacing , , , , and by , , , , and , respectively. Both the ambiguity sets are decision-dependent.

There are theoretical results about the convergence rate of empirical distributions under Wasserstein metric [29], which guide the proper selection of the Wasserstein metric bounds and . Roughly speaking, the bound should be proportional to and , where is the number of data and is the dimension.

Some literature on Wasserstein-metric-based DRO uses the ambiguity sets that only contain the discrete distributions supported on the sample data sets [30], which are not suitable for wind power and load demand uncertainties because they can change continuously. In contrast, the Wasserstein-metric-based ambiguity sets constructed in this paper contain general distributions including both continuous and discrete ones.

III-C Sizing Model

Suppose , , and are the upper bounds of , , and , respectively. Then the feasible set of capacity variable is as follows.

where means that the operation problem (13) is feasible for all normal scenarios; in other words, load shedding will not arise in normal conditions. Since is the optimal value of a linear program (LP), it is a convex function on its domain [31].

The bi-objective sizing model is established below.

| (18a) | ||||

| s.t. | (18b) | |||

| (18c) | ||||

where in (18a) the first objective is to minimize the total investment cost, and the second objective function defined in (18c) represents the worst-case fuel cost expectation when the distribution varies within the ambiguity set for normal conditions. Constraint (18b) stipulates an upper bound for the worst-case load shedding expectation in extreme conditions. The worst-case distributions in normal and extreme conditions are different. In (18), the wind farm capacities are approximated by continuous variables. If the obtained capacity is not divisible by the capacity of a single WT, we round the obtained capacity to the nearest integer multiples of the WT capacity to ensure the number of WTs is an integer. For large-scale wind farms, this simplification would not significantly affect the optimality, as will be examined in Section V.

The sizing model (18) is hard to solve due to three reasons: 1) There are distributionally robust expectations in the model. 2) The ambiguity sets are decision-dependent. 3) The functions and are defined as the optimal values of LP problems. To overcome these difficulties, we develop a solution method in the next section.

IV Solution Method

We first transform the DRO sizing model (18) into a SP problem, and then propose an iterative algorithm to solve it.

IV-A Approximate Stochastic Programming Problem

First, we use Lipschitz constants to transform the distributionally robust expectations into the expectations with respect to the empirical distributions plus compensation terms, as in the following theorem.

Theorem 1.

For any and ,

| (19) |

where is the minimum Lipschitz constant of regarded as a function of , and is the minimum Lipschitz constant of regarded as a function of . 111For example,

The proof of Theorem 1 can be found in Appendix A. The distributionally robust expectation in normal conditions has a similar property with minimum Lipschitz constants and .

By the sample average approximation (SAA) technique, . Thus, the following SP problem is an approximation of the sizing model (18).

| (20a) | ||||

| s.t. | (20b) | |||

| (20c) | ||||

| (20d) | ||||

| (20e) | ||||

| (20f) | ||||

| (20g) | ||||

| (20h) | ||||

where (20b) and (20f) contain the requirement ; and are auxiliary variables representing and , respectively. As will be examined in Section V, the approximate problem is not over-conservative with suitable parameters and .

IV-B Solution Algorithm

To solve the SP problem (20), we still need to address two issues: 1) what are the minimum Lipschitz constants , , , and ; 2) how to solve the bi-objective optimization.

For the first issue, though the minimum Lipschitz constants are hard to calculate accurately, it is easy for us to obtain their upper bounds based on the fact that functions and are defined by LPs whose dual variables can reflect their changing rates in . Denote the upper bounds by , , , and , respectively. The detailed procedure for getting the upper bounds is presented in Appendix B. According to the procedure, we can find that calculating and involves solving a KKT condition embedded optimization while calculating and only requires solving some LP problems. To accelerate the computation, we use uniform upper bounds for and , i.e., ; and -dependent upper bounds for and , i.e., and .

For the second issue, we adopt the -constraint method [32] to handle the two objectives. Particularly, the investment cost objective is replaced with a budget constraint, and the new model only minimizes the fuel cost expectation as follows.

| s.t. | ||||

| (21) |

where is the budget. With a varying budget, the Pareto frontier of the bi-objective sizing model can be obtained, which is the advantage of the -constraint method compared with summing the two objective functions together. The uniform upper bounds and are calculated in advance and used in the solution process of (IV-B), which is shown in Algorithm 2. The algorithm finds an approximate solution in an iterative way: in each iteration , use the and in the current iteration to approximate the upper bounds of minimum Lipschitz constants in the next iteration by letting , , .

| s.t. | |||

V Case Studies

This section first uses a modified IEEE 30-bus system to test the proposed method. The influence of the wake effect on the sizing results is examined and the proposed method is compared with the traditional SP and RO methods. Sensitivity analysis is also conducted. Moreover, the scalability of the proposed method is verified via a modified IEEE 118-bus system. All experiments are performed on a laptop equipped with Intel i7-12700H processor and 16 GM RAM. The LPs and mixed-integer linear programs (MILPs) are solved by GUROBI 9.5 in MATLAB.

V-A Benchmark

The benchmark case study is based on a modified IEEE 30-bus system, whose data can be found in [33] and some parameters are listed in TABLE I. There are candidate wind farms at buses 13 and 27, where the WT parameters are from [34]. The candidate wind farms are built on square areas with 25 and 20 rows, respectively. The wind speed data are generated based on the weather data in Qinghai province, China [35]. There are candidate ESSs at buses 13, 23, and 27. They all have capacity bounds GW and GWh. The load demand data are generated by normal distributions with bounds. We generate 365 groups of data in total. By analyzing the load demand and wind conditions, we select 89 groups from them to represent extreme conditions, and another 272 groups are for normal conditions. In the benchmark case, and groups of data are used for sizing. In the out-of-sample tests, and groups of data are used for validation, representing the distributions of extreme conditions and normal conditions, respectively. The parameters and controlling the size of the ambiguity sets are set as

where 20 is the number of buses with load, and is an auxiliary scalar parameter to control and .

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| 24 | h | ||

| CNY/MW | CNY/MWh | ||

| CNY/MW | MWh |

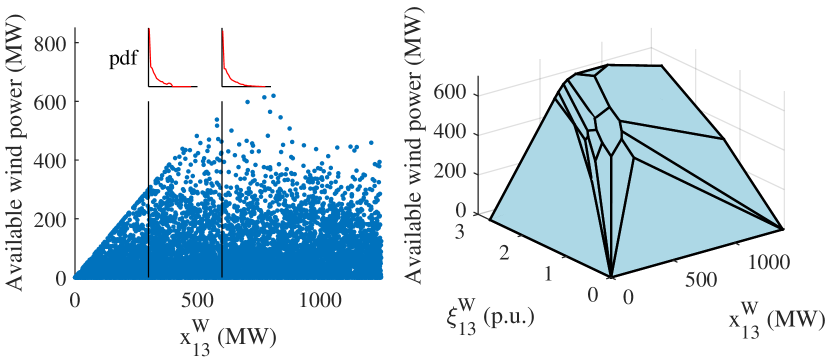

To visualize the endogenous uncertainty, we draw the available wind power sample points in Fig. 3 (left), where the points with the same horizontal coordinate reflect the distribution and probability density function (pdf) of the available wind power under a specific wind power capacity. It is clear that the distributions change as the capacity varies. The linearized available wind power function proposed in Section II is shown in Fig. 3 (right). The total computation time is within 1 s. The errors between the available wind power model (15) and the simulation value are about 5% on average, mainly from the convex hull approximation.

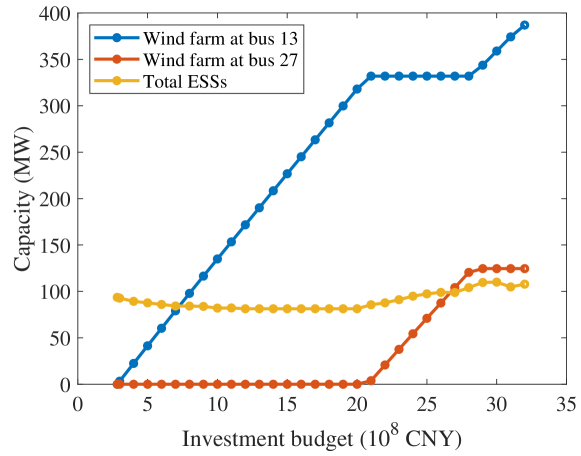

The sizing results with different investment budgets are shown in Fig. 4. The minimum investment is CNY to equip ESSs and ensure the reliable supply of load demand. When the investment budget increases, the capacities of the wind power generation become larger because renewable power can help reduce fuel costs. The wind power generation capacity accounts for about % of the total generation capacity when the investment budget is CNY. The total capacity of ESSs does not change much when wind power penetration is relatively low, but starts to grow with more wind power generation due to the flexibility requirement in the power system. We compare the results before and after the obtained capacity is rounded to integer multiples of the single WT capacity, and the error is below 0.5%. Therefore, we can optimize with continuous capacity variables and then round the results without perceptible loss of optimality. Moreover, all fuel costs and load shedding in this section have been verified to remain the same after adding the charging and discharging complementarity constraints to the power system model (12).

V-B Comparison With Traditional Methods

In order to show the impact of the wake effect and the advantage of the DRO technique, we compare the proposed method with traditional methods:

-

•

DRO: The proposed method.

-

•

SP1: Traditional SP method that does not consider the wake effect. In this method, the empirical distributions are regarded as the real distributions, i.e., and are replaced by and , respectively. The wake effect is not considered, so the available wind power in (15) becomes . The sizing model can be equivalently transformed into an LP following a similar solution method to that described in Section IV.

-

•

SP2: Traditional SP method considering the wake effect. This method is similar to SP1 except that the available wind power is still computed according to (15).

-

•

RO: RO method considering the wake effect. This method optimizes over the worst cases in and . The sizing model is

s.t.

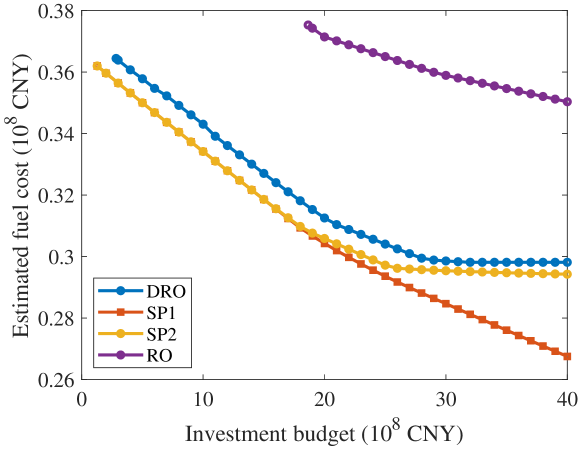

Their Pareto frontiers are depicted in Fig. 5. First, we compare the impact of wake effect. The Pareto frontiers of SP1 and SP2 almost coincide when the investment budget is below CNY because the capacities of wind power generation are relatively small and the wake effect is not obvious, as shown in Fig. 3. As the investment budget gets higher, the difference between the Pareto frontiers of SP1 and SP2 enlarges. The estimated fuel cost of SP1 becomes remarkably lower than that of SP2, showing that neglecting wake effect results in an over-optimistic estimate of fuel cost. Therefore, it is necessary to consider the wake effect in future power systems that will have large-scale wind power.

Then, we compare SP2, RO, and DRO. They all take into account the wake effect but use different optimization techniques to deal with uncertainties. The Pareto frontier of DRO is above SP2 and below RO. The minimum feasible investment budget of DRO is also in-between those of SP2 and RO. This shows the results of DRO are much less conservative than RO though a little bit more costly than SP2.

In order to compare the different methods in more detail, we list the sizing results under the investment budget CNY in TABLE II, where the estimated and are obtained from the corresponding optimization methods, while the tested and are average values given by the out-of-sample tests. In terms of the estimated fuel cost , we have SP1 SP2 DRO RO, from the most optimistic to the most conservative methods. Following this order, the total capacity of ESSs increases, and that of wind power generation decreases. This is because low-cost wind power generation brings uncertainties to the system while the ESSs can provide flexibility. The estimated load shedding is within the upper bound MWh under all the methods, but the tested of SP1 exceeds the bound. The tested of DRO is MWh, which is higher than that of RO but much lower than those of SP1 and SP2. The tested of SP1 and SP2 are higher than the estimated value because the distribution represented by the test data is different from the empirical distribution but the SP-based methods neglect the possible inexactness of empirical distribution. On the contrary, the tested under DRO is lower than the estimated one because this method already considers the inexactness of empirical distribution and the test distribution is better than the worst-case distribution. For the tested , we have SP2 DRO SP1 RO. Considering that the DRO method performs better in load shedding than SP2 and has a lower cost than RO, DRO stands out among others in that it achieves a good balance between optimality and robustness.

| Method | DRO | SP1 | SP2 | RO |

|---|---|---|---|---|

| (MW) | ||||

| (MW) | ||||

| (MWh) | ||||

| Estimated (MWh) | ||||

| Tested (MWh) | ||||

| Estimated ( CNY) | ||||

| Tested ( CNY) |

V-C Sensitivity Analysis

In the sensitivity analysis, we investigate the impacts of the scalar parameter of ambiguity set size, maximum acceptable load shedding expectation in extreme conditions, and the unit cost of ESS. In this subsection, we set an upper bound CNY for the estimated and minimize the investment cost. The results under different are shown in TABLE III. Larger leads to larger ambiguity sets and more conservative results, which can be seen from the increasing investment and decreasing tested and . Note that the tested exceeds the upper bound when and , which indicates that the ambiguity sets are not large enough to include the distribution represented by the test data. Proper parameters should be selected to establish an ambiguity set with a suitable size so that the sizing results are robust but not over-conservative.

| (MW) | ||||

|---|---|---|---|---|

| (MW) | ||||

| (MWh) | ||||

| Investment ( CNY) | ||||

| Tested (MWh) | ||||

| Tested ( CNY) |

TABLE IV shows the results under different . The larger the is, the smaller the investment cost becomes. The capacities of ESSs change much while that of wind power generation are almost the same. The reason is that larger ESSs help to enhance reliability. Note that the tested is always lower than and the tested is within the bounds, which shows the proposed method is effective.

| (MWh) | ||||

|---|---|---|---|---|

| (MW) | ||||

| (MW) | ||||

| (MWh) | ||||

| Investment ( CNY) | ||||

| Tested (MWh) | ||||

| Tested ( CNY) |

We investigate the impact of the ESS unit cost by multiplying and by a constant . The results under different are listed in TABLE V. As increases, the investment cost becomes larger, while the capacities of wind power generation and ESSs do not change much, indicating that ESSs and wind power play different roles in the system and they can hardly substitute each other even when the unit cost changes.

| (MW) | ||||

|---|---|---|---|---|

| (MW) | ||||

| (MWh) | ||||

| Investment ( CNY) |

V-D Scalability

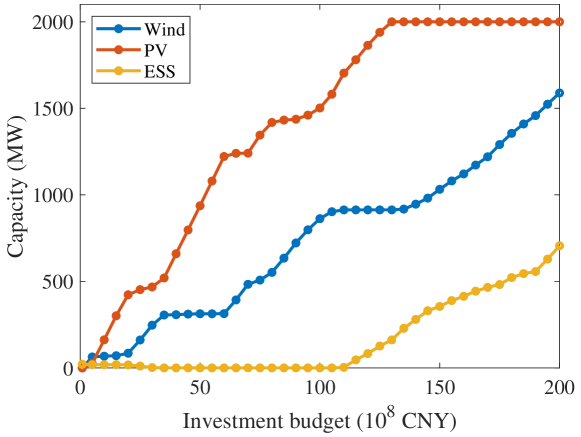

To show the scalability of the proposed method, a modified IEEE 118-bus system is tested, where candidate components are wind farms, PV stations, and ESSs. The PV stations are treated in a similar way but without wake effect. The sizing results are shown in Fig. 6. ESSs will be invested when the renewable capacity is large. TABLE VI shows the computation time of Algorithm 2 under different settings. Overall, the computation efficiency is acceptable for planning purposes.

| Number of scenarios | ||||

|---|---|---|---|---|

| 30-bus | s | s | s | s |

| 118-bus | s | s | s | s |

VI Conclusion

This paper studies the sizing problem of wind power generation and energy storage in power systems considering the wake effect, which is cast as a DRO model with DDU. A solution methodology consisting of the SP approximation based on minimum Lipschitz constants, evaluations of the Lipschitz constants, and an iterative algorithm, is developed. Simulations on the modified IEEE 30-bus and 118-bus systems show the effectiveness and scalability of the proposed method, and reveal the following findings: 1) The impact of wake effect becomes more significant when the wind power capacity grows in a limited area. 2) The DRO model outperforms the traditional SP and RO models in terms of balancing optimality and robustness. Our future work aims at considering the long-term uncertainties from society, economy, and technology.

References

- [1] X. Wei, Y. Xu, H. Sun, and H. Zhao, “Bi-level hybrid stochastic/robust optimization for low-carbon virtual power plant dispatch,” CSEE Journal of Power and Energy Systems, 2022.

- [2] M. Cañas-Carretón and M. Carrión, “Generation capacity expansion considering reserve provision by wind power units,” IEEE Transactions on Power Systems, vol. 35, no. 6, pp. 4564–4573, 2020.

- [3] S. Bhattacharjee, R. Sioshansi, and H. Zareipour, “Benefits of strategically sizing wind-integrated energy storage and transmission,” IEEE Transactions on Power Systems, vol. 36, no. 2, pp. 1141–1151, 2020.

- [4] C. Wan, W. Qian, C. Zhao, Y. Song, and G. Yang, “Probabilistic forecasting based sizing and control of hybrid energy storage for wind power smoothing,” IEEE Transactions on Sustainable Energy, vol. 12, no. 4, pp. 1841–1852, 2021.

- [5] W. Yin, Y. Li, J. Hou, M. Miao, and Y. Hou, “Coordinated planning of wind power generation and energy storage with decision-dependent uncertainty induced by spatial correlation,” IEEE Systems Journal, pp. 1–12, 2022.

- [6] D. Liu, S. Zhang, H. Cheng, L. Liu, Z. Wang, D. Sang, and R. Zhu, “Accommodating uncertain wind power investment and coal-fired unit retirement by robust energy storage system planning,” CSEE Journal of Power and Energy Systems, vol. 8, no. 5, pp. 1398–1407, 2020.

- [7] C. Yan, X. Geng, Z. Bie, and L. Xie, “Two-stage robust energy storage planning with probabilistic guarantees: A data-driven approach,” Applied Energy, vol. 313, p. 118623, 2022.

- [8] J. Cao, B. Yang, S. Zhu, C. Ning, and X. Guan, “Day-ahead chance-constrained energy management of energy hubs: A distributionally robust approach,” CSEE Journal of Power and Energy Systems, vol. 8, no. 3, pp. 812–825, 2021.

- [9] Z. Li, L. Chen, W. Wei, and S. Mei, “Risk constrained self-scheduling of aa-caes facility in electricity and heat markets: A distributionally robust optimization approach,” CSEE Journal of Power and Energy Systems, 2021.

- [10] F. Pourahmadi and J. Kazempour, “Distributionally robust generation expansion planning with unimodality and risk constraints,” IEEE Transactions on Power Systems, vol. 36, no. 5, pp. 4281–4295, 2021.

- [11] J. Le, X. Liao, L. Zhang, and T. Mao, “Distributionally robust chance constrained planning model for energy storage plants based on kullback–leibler divergence,” Energy Reports, vol. 7, pp. 5203–5213, 2021.

- [12] B. Chen, T. Liu, X. Liu, C. He, L. Nan, L. Wu, X. Su, and J. Zhang, “A wasserstein distance-based distributionally robust chance-constrained clustered generation expansion planning considering flexible resource investments,” IEEE Transactions on Power Systems, 2022.

- [13] Z. Ren, H. Li, W. Li, X. Zhao, Y. Sun, T. Li, and F. Jiang, “Reliability evaluation of tidal current farm integrated generation systems considering wake effects,” IEEE Access, vol. 6, pp. 52 616–52 624, 2018.

- [14] A. P. Gupta, A. Mitra, A. Mohapatra, and S. N. Singh, “A multi-machine equivalent model of a wind farm considering lvrt characteristic and wake effect,” IEEE Transactions on Sustainable Energy, vol. 13, no. 3, pp. 1396–1407, 2022.

- [15] X. Lyu, Y. Jia, and Z. Xu, “A novel control strategy for wind farm active power regulation considering wake interaction,” IEEE Transactions on Sustainable Energy, vol. 11, no. 2, pp. 618–628, 2019.

- [16] W. Yin, X. Peng, and Y. Hou, “A decision-dependent stochastic approach for wind farm maintenance scheduling considering wake effect,” in 2020 IEEE PES Innovative Smart Grid Technologies Europe (ISGT-Europe). IEEE, 2020, pp. 814–818.

- [17] X. Gao, H. Yang, and L. Lu, “Optimization of wind turbine layout position in a wind farm using a newly-developed two-dimensional wake model,” Applied Energy, vol. 174, pp. 192–200, 2016.

- [18] Y. Ma, K. Xie, Y. Zhao, H. Yang, and D. Zhang, “Bi-objective layout optimization for multiple wind farms considering sequential fluctuation of wind power using uniform design,” CSEE Journal of Power and Energy Systems, vol. 8, no. 6, pp. 1623–1635, 2021.

- [19] F. Bai, X. Ju, S. Wang, W. Zhou, and F. Liu, “Wind farm layout optimization using adaptive evolutionary algorithm with monte carlo tree search reinforcement learning,” Energy Conversion and Management, vol. 252, p. 115047, 2022.

- [20] D. Cazzaro, A. Trivella, F. Corman, and D. Pisinger, “Multi-scale optimization of the design of offshore wind farms,” Applied energy, vol. 314, p. 118830, 2022.

- [21] L. Xiong, S. Yang, S. Huang, D. He, P. Li, M. W. Khan, and J. Wang, “Optimal allocation of energy storage system in dfig wind farms for frequency support considering wake effect,” IEEE Transactions on Power Systems, vol. 37, no. 3, pp. 2097–2112, 2021.

- [22] O. Sadeghian, A. Oshnoei, M. Tarafdar-Hagh, and M. Kheradmandi, “A clustering-based approach for wind farm placement in radial distribution systems considering wake effect and a time-acceleration constraint,” IEEE Systems Journal, vol. 15, no. 1, pp. 985–995, 2020.

- [23] J. S. González, M. B. Payán, J. M. R. Santos, and F. González-Longatt, “A review and recent developments in the optimal wind-turbine micro-siting problem,” Renewable and Sustainable Energy Reviews, vol. 30, pp. 133–144, 2014.

- [24] A. E. Feijoo and J. Cidras, “Modeling of wind farms in the load flow analysis,” IEEE transactions on power systems, vol. 15, no. 1, pp. 110–115, 2000.

- [25] D. Villanueva, J. L. Pazos, and A. Feijoo, “Probabilistic load flow including wind power generation,” IEEE Transactions on Power Systems, vol. 26, no. 3, pp. 1659–1667, 2011.

- [26] M. Herceg, M. Kvasnica, C. Jones, and M. Morari, “Multi-Parametric Toolbox 3.0,” in Proc. of the European Control Conference, Zürich, Switzerland, July 17–19 2013, pp. 502–510, http://control.ee.ethz.ch/~mpt.

- [27] R. Xie, W. Wei, M. Li, Z. Dong, and S. Mei, “Sizing capacities of renewable generation, transmission, and energy storage for low-carbon power systems: A distributionally robust optimization approach,” Energy, vol. 263, p. 125653, 2023.

- [28] L. V. Kantorovich and S. Rubinshtein, “On a space of totally additive functions,” Vestnik of the St. Petersburg University: Mathematics, vol. 13, no. 7, pp. 52–59, 1958.

- [29] N. Fournier and A. Guillin, “On the rate of convergence in wasserstein distance of the empirical measure,” Probability Theory and Related Fields, vol. 162, pp. 707–738, 2015.

- [30] F. Luo and S. Mehrotra, “Distributionally robust optimization with decision dependent ambiguity sets,” Optimization Letters, vol. 14, pp. 2565–2594, 2020.

- [31] S. Boyd and L. Vandenberghe, Convex optimization. Cambridge university press, 2004.

- [32] H. Mavalizadeh, O. Homaee, R. Dashti, J. M. Guerrero, H. H. Alhelou, and P. Siano, “Robust switch selection in radial distribution systems using combinatorial optimization,” CSEE Journal of Power and Energy Systems, vol. 8, no. 3, pp. 933–940, 2021.

- [33] R. Xie, “Wind farm planning considering wake effect,” https://github.com/xieruijx/wind-farm-planning-considering-wake-effect, 2022.

- [34] K. Yang, G. Kwak, K. Cho, and J. Huh, “Wind farm layout optimization for wake effect uniformity,” Energy, vol. 183, pp. 983–995, 2019.

- [35] I. Staffell and S. Pfenninger, “Using bias-corrected reanalysis to simulate current and future wind power output,” Energy, vol. 114, pp. 1224–1239, 2016.

- [36] D. Bertsekas, Convex optimization theory. Athena Scientific, 2009, vol. 1.

- [37] P. M. Esfahani and D. Kuhn, “Data-driven distributionally robust optimization using the wasserstein metric: performance guarantees and tractable reformulations,” Mathematical Programming, vol. 171, pp. 115–166, 2018.

- [38] A. Shapiro, On Duality Theory of Conic Linear Problems. Boston, MA: Springer US, 2001, pp. 135–165.

- [39] S. Pineda and J. M. Morales, “Solving linear bilevel problems using big-ms: not all that glitters is gold,” IEEE Transactions on Power Systems, vol. 34, no. 3, pp. 2469–2471, 2019.

- [40] B. T. Nguyen and P. D. Khanh, “Lipschitz continuity of convex functions,” Applied Mathematics & Optimization, vol. 84, pp. 1623–1640, 2021.

Appendix A Proof of Theorem 1

We omit function variable in the proof since it can be regarded as a fixed parameter of the function. We investigate the properties of the function first and then transform the distributionally robust expectation.

A-A Load Shedding Function

The definition of in (14) can be written in a compact form as follows.

| s.t. | (A.1) |

where , , , and are coefficient matrices or vectors; denotes the operation variables. Since represents the minimum load shedding, it is always nonnegative and no larger than the total load demand. Thus, the LP problem (A.1) has a finite optimal value. Then by the strong duality of LP [31], we have

| s.t. |

Because the optimal value can be reached at some vertex if it is finite,

| (A.2) |

with polyhedron and its vertex set . Then is a finite set and is convex [31] and continuous. For each , let

then it is either empty or closed, and .

Claim 1: For , if , then it is convex.

Proof: Suppose and . Then

| (A.3) | ||||

| (A.4) | ||||

| (A.5) |

where (A.4) follows from the convexity of and (A.5) is due to (A.2). Since (A.3) and (A.5) are the same, the inequalities are actually equations, so and therefore is convex. ∎

Let be a subset of defined by

In addition, define a new function as follows, where is the dimension of .

| (A.6) |

We prove that is an extension of .

Claim 2: .

Proof: Denote the Lebesgue measure by . For any , if , then contains some open set since it is convex. Additionally, , so . Thus, and it is finite since is bounded. Note that is convex, on , and they are continuous, so . ∎

Because is proper, convex, and continuous, according to the property of conjugate function [36], , which is the bi-conjugate function, i.e.,

where the conjugate function and .

Claim 3: , i.e., the convex hull of .

Proof: (1) Prove that .

For any , there exist and subject to , and , so

and then

which means . Thus, .

(2) Prove that .

Assume . Since is a finite set, is closed and convex. Then and can be strictly separated [31], i.e., there are vector and constant such that . Then for any , we have

then

which means . Thus, . ∎

Claim 4: , where denotes the projection of to the component corresponding to the wind farm at bus .

Proof: directly follows from and that is finite. We prove .

(1) Prove that .

There is a such that

According to the definition of , there is an open set . For , and . Since is open, we can choose and so that , for any and

due to the property of dual norm. Then by the definition of , we have .

(2) Prove that .

For arbitrary subject to and for any , there are and so that

so

and then

Since and are arbitrary, we have . ∎

Similarly, .

Remark: The fuel cost function can be handled in a similar way when the dimension of is .

A-B Distributionally Robust Expectation

The proof in this subsection is analogous to that in [37].

By the definition of in (III-B3), the distributionally robust expectation is

| (A.7) |

where ; (A.7) follows from the linearity of expectation and the definitions of Dirac distribution and joint distribution.

Using the duality technique, we have

| (A.8) | ||||

| (A.9) | ||||

| (A.10) |

From (A.8) to (A.9), the “” direction uses the max-min inequality, and the opposite direction follows from the strong duality result of moment problems [38]. The Dirac distribution for can be regarded as a product of Dirac distributions on and , so (A.10) holds.

Appendix B Calculating Lipschitz Constants

The methods of calculating Lipschitz constants are different for and since their domains are defined in different ways.

B-A Lipschitz Constants of the Load Shedding Function

The definition of load shedding function in (14) can be written in the following compact form:

| (B.1a) | ||||

| s.t. | (B.1b) | |||

| (B.1c) | ||||

where , , , , , , , , and are coefficient matrices or vectors; represents the operation variables. The dual problem of (B.1) is

| (B.2a) | ||||

| s.t. | (B.2b) | |||

Because the LP problem (B.1) has a finite optimal value for any and , the strong duality holds [31]. Then for dual optimal solution , we have

which shows that the value of reflects how changes as varies.

For fixed , in order to find a Lipschitz constant , we solve the following optimization problem.

| (B.3a) | ||||

| s.t. | (B.3b) | |||

| (B.3c) | ||||

| (B.3d) | ||||

where the decision variables are , , , , and . In (B.3a), represents a component corresponding to . Any such component works because all lead to equivalent problems, which can be observed from (14) and the power system operation constraints. Since larger wind power output results in smaller load shedding, is maximized in (B.3a). Constraints (B.3c) and (B.3d) form the KKT condition of problem (B.1), where (B.3c) can be linearized by the big-M technique [39], so that (B.3) is transformed into an MILP problem. It can also be solved directly as a bilinear program using solvers. Its optimal value or any upper bound can be the desired .

We can also find a uniform bound so that by the optimization problem below.

| (B.4a) | ||||

| s.t. | (B.4b) | |||

which is modified from (B.3) by allowing to vary within . This problem can still be either directly solved as a bilinear program or transformed into an MILP problem and then solved.

B-B Lipschitz Constants of the Fuel Cost Function

The definition of the fuel cost function can also be written in the form of (B.1), and so is the dual problem (B.2). When is fixed, is a convex and piecewise linear function of . According to the relation of Lipschitz continuity and local Lipschitz continuity [40], the maximum local Lipschitz constant at is also a Lipschitz constant on . Therefore, solve the dual problem (B.2) at each to find the dual optimal solutions , where emphasizes that they are dependent on . Then calculate , extract the component corresponding to , and denote it by . Note that is a vector with dimensions. Then can be estimated by . The Lipschitz constant can be estimated in a similar way.