Optimal Robust Mechanism in Bilateral Trading

We consider a model of bilateral trade with private values. The value of the buyer and the cost of the seller are jointly distributed. The true joint distribution is unknown to the designer, however, the marginal distributions of the value and the cost are known to the designer. The designer wants to find a trading mechanism that is robustly Bayesian incentive compatible, robustly individually rational, budget-balanced and maximizes the expected gains from trade over all such mechanisms. We refer to such a mechanism as an optimal robust mechanism. We establish equivalence between Bayesian incentive compatible mechanisms (BIC) and dominant strategy mechanisms (DSIC). We characterise the worst distribution for a given mechanism and use this characterisation to find an optimal robust mechanism. We show that there is an optimal robust mechanism that is deterministic (posted-price), dominant strategy incentive compatible, and ex-post individually rational. We also derive an explicit expression of the posted-price of such an optimal robust mechanism. We also show the equivalence between the efficiency gains from the optimal robust mechanism (max-min problem) and guaranteed efficiency gains if the designer could choose the mechanism after observing the true joint distribution (min-max problem).

JEL Classification Number: D82, D40

Keywords: Distributionally robust mechanism, bilateral trade, posted-price mechanism, min-max theorem, DSIC-BIC equivalence.

1 Introduction

We consider a model of bilateral trading with private values. The valuation of the buyer and the cost of the seller are jointly distributed. The true joint distribution of valuation and cost is common knowledge among agents but is unknown to the designer. However, the designer knows the marginal distribution of valuation of the buyer and cost of the seller. The designer’s objective is to design a mechanism that is robust to this uncertainty of the designer. In particular, we want to design a mechanism that maximizes expected welfare guarantee. The expected welfare guarantee of a mechanism is the worst or minimum expected gains from trade, where the minimum is taken over all joint distributions consistent with the known marginals. Also, the mechanism must be implementable for all the possible joint distributions consistent with the marginal distribution of types as agents know the true joint distribution.

Consider a setting where the designer is a third party that is designing a platform for trade and its revenue is a function of efficiency gains. It is plausible that the third party does not have precise information about the joint distribution of value and cost. Another setting is that of a benevolent planner. In such situations, it is natural to seek distributional robustness. A similar approach was adopted by Carroll (2017) in the monopoly setting with the buyer having multi-dimensional demand. He and Li (2022) takes a similar approach in the auction environment and shows the second price auctions with no reserve price are asymptotically optimal. 111The approach adopted in the paper is one of the possible approaches and an extreme version. The set of possible joint densities could be restricted if more information is available. Also, the information to the designer can be modelled differently. For example, only moments of joint distribution could be known to designer Delage and Ye (2010); Suzdaltsev (2020).

We establish equivalence between Bayesian incentive compatible mechanisms (BIC) and dominant strategy mechanisms (DSIC). The equivalence result holds for robust efficiency gains for BIC and DSIC mechanisms along with the additional constraints on budget balancedness and individual rationality. The result implies it does not make a difference to the designer whether the joint distribution of valuations is known or unknown to the agents. The implementation of mechanisms and additional constraints over all the “consistent" joint distributions is quite demanding and results in dominant strategy implementation with additional ex-post constraints. It is an important result as it simplifies the problem of the designer significantly. Hagerty and Rogerson (1987) shows that a block mechanism implementable in dominant strategy, budget balanced and individually rational mechanism are implemented by “posted-price" mechanism. This result allows us to focus on this small class of mechanisms to find an optimal robust mechanism.

The main result on the equivalence between Bayesian strategy implementation and dominant strategy implementation is observed in many other settings. Bergemann and Morris (2005) finds environments in which the ex-post implementation is equivalent to interim implementation for all types; the equivalence holds for separable environments, e.g., implementation of social choice function, a quasi-linear environment with no restriction on transfers. Gershkov et al. (2013) and Chen et al. (2019) show such equivalence in the social choice environment. Manelli and Vincent (2010) shows the equivalence in a single unit, private values auction environment. The analysis in our paper is different from the above literature in two aspects: Firstly, we consider robustness in Bayesian incentive compatibility. Secondly, we also consider additional constraints on budget balancedness and individual rationality.

We characterize the worst joint distribution in terms of giving the least expected welfare guarantee for a given dominant strategy incentive compatible, ex-post individually rational, and budget-balanced deterministic mechanism. We use this to show that a deterministic posted price mechanism is an optimal robust mechanism.

Our result contributes to the growing literature on robust mechanism design pioneered by Bergemann and Morris. This literature tries to answer the Wilson critique (Wilson, 1987) of mechanisms that rely on the informational assumptions of the designer. Bergemann and Morris (2005) finds environments in which the ex-post implementation is equivalent to interim implementation for all types; the equivalence holds for separable environments, for example, implementation of social choice function, and a quasi-linear environment with no restriction on transfers.

Our paper adds to the long literature on the bilateral trading problem, which is inspired by the impossibility result in Myerson and Satterthwaite (1983). It assumes independent private values, and derives the expected welfare-maximizing mechanism – see also Chatterjee and Samuelson (1983) for a description of equilibria of a particular bilateral trading mechanism. While these papers assume common knowledge of priors, our paper follows the models in robust mechanism design literature and relaxes this assumption.

Another strand of literature looks at robustness with respect to information structure (Bergemann et al., 2017; Brooks and Du, 2021; Carroll, 2018). In those environments, there is a “fixed" prior distribution over valuations that results from distribution over state spaces and the associated joint distribution over valuations. Then, there is an information structure that determines how the signals would be generated. The information structure affects the strategy of players as it affects the posterior beliefs about valuations. Our approach is different in the sense that only the information about priors is common knowledge, not the joint distribution. Secondly, they consider general information structures whereas we consider a particular information structure where the signal of each player reveals the true valuation of that player.

As part of the proof, we prove min-max theorem over deterministic posted price mechanisms that extends to then the class of Bayesian implementable mechanisms. It is similar to Brooks and Du (2021) that proves a strong min-max theorem but for informationally robust mechanism.

The paper is organized as follows. In section 2, we introduce the model and class of mechanisms that we are interested in. In section 3, we present the equivalence results. Section 4 contains the proofs of equivalence theorems, and Section 5 characterises the worst distribution for any (deterministic) posted price mechanism. Subsection 5.3 contains the result on optimal robust mechanism and min-max theorem.

2 Model

We consider a private values model of bilateral trading. There is a single object for trade, which the seller can produce and the buyer is willing to buy. The valuation of the buyer for the object and the cost of the seller for producing the object are jointly distributed according to a distribution . The marginal distribution of valuation of the buyer is denoted by and the marginal distribution of cost of the seller is denoted by . Though the true joint distribution is common knowledge among agents (the buyer and the seller), the designer does not know .222The assumption of common knowledge about among agents is least restrictive as it allows to look at ”robust” BIC mechanisms. The main result shows that we can focus on DSIC mechanisms without loss of generality. This assumption holds well in situations where the there large and number of agents who have more information about the characteristics of the good. However, she knows the marginal distributions and . We assume for simplification that the valuations of buyers lie in and costs lie in . We define 333In the proof of equivalence result, we prove the theorem for but it extends easily to type space with different supports (even unbounded) for marginal distributions of value of the buyer and cost of the seller.

We assume that marginal distribution of valuations, and are continuous i.e. there are no atoms.444Allowing for atoms does not affect the the equivalence results. To see this, note that we can approximate the problem with atoms to problem with continuous marginal by spreading mass at a point to a small square; the efficiency gains from arbitrary given mechanism will be close for the two problems. There are infinitely many possible joint distributions consistent with the given marginal distributions of agents. Note that the joint distribution affects the efficiency gains from a mechanism.

We focus attention on the direct revelation mechanisms.555 The designer can potentially attain information about from agents but we do not consider it as we are interested in situations where there are large number of buyers and sellers with different joint distributions. A (direct) mechanism is a triplet , where and for each . Here, denotes the probability of trade, is the payment made by the buyer and is the payment made to the seller at type profile .

2.1 Notions of incentive compatibility

We introduce two notions of incentive compatibility in this section. The first two notions are standard in the literature.

Definition 1

A mechanism is dominant strategy incentive compatible (DSIC) if for every

While DSIC is a prior-free notion, the weaker requirement of Bayesian incentive compatibility is not. In our model, the designer only knows the marginal distributions of types of individual agents. Hence, we require a robust version of Bayesian incentive compatibility.

A joint probability distribution of is consistent with if the marginal distribution of and are and respectively:

Let denote the set of all joint distributions consistent with . Note that the true distribution Since and are continuous functions666 and are absolutely continuous as continuous increasing functions are absolutely continuous., we can find well defined joint probability density function denoted by that generates joint distribution consistent with

Definition 2

A mechanism is Bayesian incentive compatible (BIC) with respect to a prior if

where denotes the conditional expectation of given valuation using joint distribution and denotes the conditional expectation of given cost using joint distribution A mechanism is marginal-consistent Bayesian incentive compatible (M-BIC) if it is BIC with respect to all priors

Clearly, a DSIC mechanism is BIC with respect to all priors. Hence, it is M-BIC.

2.2 Other desiderata

It is natural to impose two additional constraints on mechanisms in the bilateral trading problem: (a) participation constraint, and (b) budget-balance constraint.

Definition 3

A mechanism is ex-post individually rational (EIR) if for every

A weaker version of individual rationality is the following.

Definition 4

A mechanism is interim individually rational (IIR) with respect to a prior if

A mechanism is marginal-consistent interim individually rational (M-IIR) if it is IIR with respect to all priors .

The M-IIR participation constraint is the analogue of M-BIC incentive constraint we had introduced earlier. Since the designer is uncertain about the true prior, she wants to design mechanisms which satisfy these stronger notions of IC and IR constraints. Note that these are still weaker than DSIC and EIR constraints.

We also introduce two notions of budget-balance constraints.

Definition 5

A mechanism is

-

•

budget-balanced (BB) if for all ,

-

•

-budget-balanced (-BB) given , if for all , .

The proofs construct a DSIC and EIR mechanism, but a particular type of DSIC and EIR mechanism. We call it the block mechanism. For this, we divide the type space into squares for any positive integer .777We prove for for ease of notation. We do so in the usual way: for each , let . Then, a block is defined as:

with the usual convention that . Clearly, is different for different values of . But we suppress the dependence of on the value of for notational simplicity, unless it is necessary to be explicit.

Definition 6

A mechanism is an -block mechanism if for each block and for every , we have

We will impose these notions of budget-balancedness, individual rationality, and incentive compatibility to define three classes of mechanisms.

2.3 Three classes of mechanisms

We consider three classes of mechanisms. These mechanisms use different notions of IC, IR, and BB constraints.

| Then, for a given , define | ||||

We establish equivalence results for these classes of mechanisms in terms of robust efficiency gains888We have equivalence result between and the other classes but we can easily replace with mechanism that have budget surplus within margin.. Also, we define which forms an intermediate class of mechanisms and used to show equivalence between the three class of mechanisms defined above.

As a designer, we are interested in evaluating the worst efficiency of a mechanism in these classes. Formally, given a mechanism , its robust efficiency gain is

In each classes of these mechanism, we can then define the optimal robust mechanism. Given an , for any ,

Any mechanism in which attains worst case efficiency gain equal to will be an optimal robust mechanism in .

3 Equivalence results

There are two main equivalence results of the paper. The first theorem says that robust efficiency gain in the class of mechanisms can be made arbitrarily close to robust efficiency gain in class of prior-free mechanisms. The precise statement is the following.

Theorem 1

For every , there exists such that

Also, is such that

The second main theorem compares robust efficiency gains in with the class of mechanisms in .

Theorem 2

.

The proof of these theorems reveal that the equivalence results are stronger than what the statements suggest. For any given mechanism in , we can find a mechanism in that generates the gains from trade very close to that of mechanism in for all consistent joint distributions. As a result, it holds for worst distribution as well.

Since , Theorem 2 implies that . This establishes equivalence between the robust BIC and DSIC mechanisms with additional constraints in budget balancedness and individual rationality. Theorem 2 implies that we can focus on robust mechanism in the class of block mechanism implementable in dominant strategy, with ex-post individual rationality and budget balancedness. This simplifies the mechanism designer’s problem significantly since Hagerty and Rogerson (1987) showed that mechanisms in are implementable by random posted price mechanisms, which is a much simpler class of mechanisms.

4 Proofs of equivalence results

We construct - block mechanisms satisfying DSIC and EIR mechanisms to prove the equivalence theorems.

4.1 Proof of Theorem 1

For proof of Theorem 1, we construct a sequence of -block mechanisms starting from a mechanism in . We show that each of these block mechanisms is DSIC and EIR. The constructed block mechanism need not be BB. But, for sufficiently high value of , it is arbitrarily close to budget balancedness. 999In fact, the mechanism will have budget surplus for all by construction. We require close to budget balancedness for Theorem 2. For sufficiently high value of , can come arbitrarily close to the robust efficiency gain of the original mechanism.

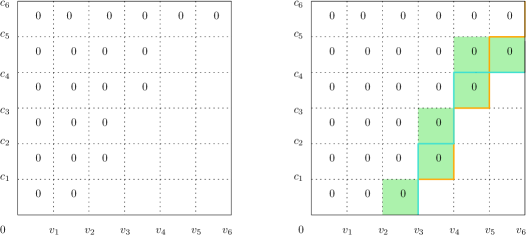

Given a mechanism and positive integer , define a new mechanism as follows. First, we define : for each block and for each

| (1) |

The allocation probabilities in new mechanism are average probabilities in a block, except for at most blocks.

The figure 1 illustrates how the allocation probabilities under the two mechanisms are different. The entry zero in block implies that the average allocation probability over the block is zero. The figure on the left has blocks with the same average probability as From this block mechanism, we can derive block mechanism, The average probabilities match for mechanism and on all but few blocks that coloured in green. The green coloured blocks have positive allocation probability for mechanism but zero allocation probability under mechanism .

The allocation function weakly decreases the allocation probability for each block and increases the number of blocks with zero probability of allocation, but this happens for only at max blocks out of blocks, for a general allocation function, . As increases, the share of such blocks would be insignificant and would have the same efficiency gains as the one from just averaging out the allocation probabilities.

It is clear that is feasible: for each . We show in the following lemma that is ex-post monotone: for each with and , and .

Lemma 1

Allocation rule is ex-post monotone.

Proof:

Step 1. In this step, we show that satisfies a ‘monotonicity’ property and the mechanism satisfies a version of the payoff equivalence formula. Fix a and . Define a joint density follows:

| (2) |

where is the marginal density of value of the buyer.

Note that coincides with everywhere except for . By construction, . Hence, the marginals of and coincide everywhere, implying .

Now consider a pair of M-BIC constraints for buyer: with . Consider the M-BIC prior constraints of mechanism for prior . We have

| (3) |

Analogously, the M-BIC constraint from to with prior gives

| (4) |

Since , we get for all ,

| (5) |

Analogously, for each , we get for all ,

| (6) |

We use this to prove ex-post monotonicity of in the next step.

Next, using (3) gives us for every and every ,

where

| (7) |

Rewriting

Hence, is convex in the first argument for every and is the subgradient of at . By the fundamental theorem of calculus, we can thus write for every and every

| (8) |

This payoff equivalence formula is useful and will be used later.

Step 2. Fix for some . If , for with , we argue that . Suppose and . If , we are done since . So, implies . Then,

where we used (6) for the second inequality.

Now, suppose for some . We show that for all . Suppose and . If , we are done since . Else, . Hence, . Since , this means for all . If , we are done. Else, we repeatedly apply this procedure to get .

This shows that for all and all . An analogous proof using (5) can be done to show that for all and for all .

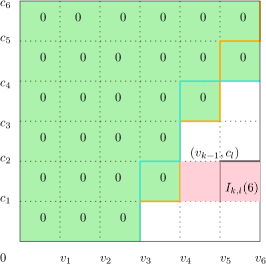

By Lemma 1, since is monotone, we can define an EIR and DSIC mechanism using standard revenue equivalence techniques: payments at the lowest types are set to zero and local incentive constraints bind to give payments at all types. In particular, for every ,

| (9) |

Similarly, for every ,

| (10) |

The payment of buyer and seller is such that the agents with valuation at boundary of squares in the block are indifferent between reporting their true valuation and misreporting valuation in next block as shown in the figure 2. The corresponding blocks are shown in pink colour. Thus, we have a DSIC and EIR mechanism and gives the next lemma.

Lemma 2

is DSIC and EIR mechanism.

As grows infinitely, the budget surplus for a pair approaches that of original mechanism, which is budget balanced. We get the following lemma as a result.

Lemma 3

As we have for all

Lemma 4

The efficiency gains generated by sequence of mechanism converges to efficiency gains from mechanism ,

Proof:

The efficiency gains of mechanism is given by

We would use the following lemma directly at this point. It will be proved in Section 7.

Lemma 5

For any block , we have

| (11) |

where is allocation for block mechanism with blocks.

Summing over in equation (11), we get

The last inequality follows from the fact that and is a probability measure. Thus, as and we have

Note that we had partitioned the entire space of valuation into squares. Choosing , we can see that for all , as , efficiency gains of converges to efficiency gains of mechanism

By combining Lemma 2, Lemma 3 and Lemma 4, for all and for all ,

For every , for all , there exists such that , for large and

Taking infimum over , we get that for every and for all , there exists such that and for large , we have and

Taking supremum over all and using the fact that , we get that for every , there exists such that and

4.2 Proof of Theorem 2

Lemma 6

As , we have

Proof: We start by mentioning two results for -block mechanisms implementable in dominant strategy. The proof of the following observations is provided in Section 7.

Observation 1

For an -block mechanism implementable in dominant strategy, for we have

| (12) |

Observation 2

The constructed -block mechanism, has the property that for all , for any we have .

Hagerty and Rogerson (1987) shows that a block mechanism which is DSIC, BB and EIR is implementable by posted price mechanism. In particular, such a mechanism with blocks can be represented by a vector where element, where 101010See Corollary 3 in Hagerty and Rogerson (1987) for details. Also, for any , we have

Consider a constructed -block mechanism . Here is the smallest number such that for every , the constructed -block mechanism lies in We construct from a block mechanism which is DSIC, BB and EIR using the result in Hagerty and Rogerson (1987). Let vector be the corresponding vector for the block mechanism, and be defined as

Here is a carefully chosen constant. We will define it later.

We show that allocation function is well defined and in three steps.

Step 1. The allocation function is well defined iff From Observation 1, for , we have 111111For the concerned block mechanisms,

Iteratively replacing the expression of allocation rules on the right hand side of the above equation, and using Observation 2, we get

| (13) |

where

We choose Note that The first equality follows from the definition of and the second equality follows from equation (13).

Since it must be true that .

Step 2.

We find the expression for for all Fix and a utility profile Note that corresponding to depend on .

Case 1. For where for all From Observation 2, it follows that In Hagerty and

Rogerson (1987), the construction from vector is such that Thus,

Case 2. For : By construction of , we have

| (14) |

Case 3. For where As , we have . We then get

| (15) |

Step 3. We show that

If is bounded as , it is easy to see that as , and are finite.

Let us consider the situation where as . Note that we will have and such that and .

We use the following observations to finding the bound on value of where are arbitrary. In particular, we show that .

Observation 3

For , we have

| (16) |

Observation 4

For all we have

By Observation 4, for all we have

| (17) |

By Observation 3, we have

The last equality follows from (17). However, since is non-negative, we get

| (18) |

We use equation (18) to find an upper bound on . For Case 2, from equation (14), we have

which follows from equation (18).

5 Optimal robust mechanism

We introduce additional notations to ease the analysis. Instead of using marginal distributions, we would use marginal density of valuation from now on as it is easier to work with. Since marginal distributions of value and cost are continuous, there exist marginal density functions of value of buyer and cost of seller, and are denoted by and , respectively.

A joint probability density of is consistent with if the marginal density of and are and respectively:

Let denote the set of all joint densities consistent with .

We can redefine the objective of designer in terms of joint density. The designer would find a mechanism that maximises robust efficiency gains in a class of mechanisms where robust efficiency gains of a mechanism is given as

Recall that is the class of mechanisms satisfying dominant strategy incentive compatibility, budget balancedness and ex-post individual rationality. Hagerty and Rogerson (1987) shows that mechanism in class of block mechanisms, any mechanism in can be implemented by posted price mechanisms- randomisation of the deterministic posted price mechanisms. This combined with Theorem 2 implies that the designer can focus without loss of generality on the class of posted price mechanisms.

Let be the collection of all posted price mechanisms. The objective of the designer is to find optimal mechanism , where

5.1 Worst distributions

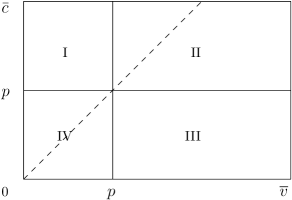

Now we restrict our attention to deterministic posted price mechanisms. In such mechanisms, there is a posted price . If the valuation of buyer, is greater than the posted price, and valuation of seller, is less than posted price, , then the trade occurs with certainty and price, will be charged as payment. If the valuation of buyer, is less than the posted price, or valuation of seller, is greater than posted price, , then trade does not occur with certainty and no payment is made.

A deterministic posted price mechanism, is defined as follows

When or , the tie between trading and not trading can be broken in anyway we want.

The efficiency gains of for true joint probability density is given by

| (19) |

Consider Figure 3. The value of the buyer and the cost of the seller is represented horizontally and vertically, respectively. Given a posted price mechanism , the trade occurs only in region III of Figure 3, and will be referred as trade region. Note that the efficiency gains of a mechanism depends only on the marginal distribution of value of buyer and cost of seller within the trade region.

For a given deterministic posted price mechanism, we characterise the set of joint distributions satisfying the marginal distribution of valuations that minimises the efficiency gains. To do that, we would use the concept of redistributing the mass which is explained in the next section.

5.1.1 Redistribution of mass

Consider a joint probability density, such that rectangles and have same mass, say in the corresponding regions. We introduce the idea of redistribution of mass from and to and . The redistribution would reduce the mass in regions and to zero whereas the mass in regions and will increase by mass, .

For a given , consider a new joint probability density

| (20) |

The above joint probability density is constructed such that marginal density of a valuation restricted to just the rectangles and collectively remains unchanged. Since , we get To be more specific, the marginal density of over rectangle and marginal density of over rectangle is shifted to rectangle . The marginal density of over rectangle and marginal density of over rectangle is shifted to rectangle . This gives us the marginal densities over each of the rectangles.

Given the marginal densities over a rectangle, we can construct a joint probability density function where the random variables are independent. Suppose and are the marginal densities over a rectangular region, . A possible joint probability density, where the random variables are independent in rectangular region is given by . Using this fact, we get

Notice that such a redistribution will decrease the mass in trade region and reduce the efficiency gains of mechanism . We will use the redistributions of the above form to characterise the worst distribution for a given posted price mechanism.

5.2 Characteristics of worst distribution for a given posted price mechanism

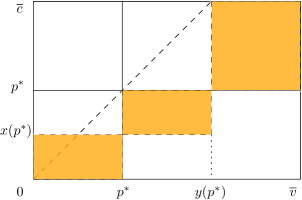

Fix mechanism We define . It is the minimum mass from a joint distribution that must lie in the trade region in order to meet the requirement of mass imposed by the marginal distributions of valuations. Note that is a parameter and depends on just the given marginal distributions.

If there is a possibility where the entire mass can be distributed such that mass in region corresponding to efficiency gains is zero. This possibility is shown in Figure 5.

Since efficiency gains is a non-negative number, for the given posted price mechanism, the robust efficiency gain must be 0.

Now we characterise the worst distribution when . Note that if this is the case, a distribution depicted in Figure 5 is not feasible. Thus, any distribution consistent with given marginal distribution of valuations must have positive mass in trade region.

Let be the worst distribution for mechanism . We define For we must have . Such a situation is depicted in Figure 6.

We prove few useful lemmas that characterise the worst case distribution, given a deterministic posted price mechanism, .

Lemma 7

If , then .

Proof:

Suppose not for contradiction. If and , then we can find rectangle and rectangle with mass as shown in Figure 7.

Redistribute mass from and to and in the manner described by equation (20). As a result, efficiency gains will decrease, contradicting the assumption that we started with worst distribution.

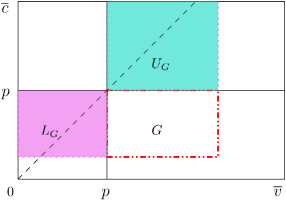

To further characterise the worst case distribution, we define the set as the smallest open rectangle with vertex and diagonally opposite vertex, where and , such that

Formally,

let . We have

where

We define two rectangles,

and

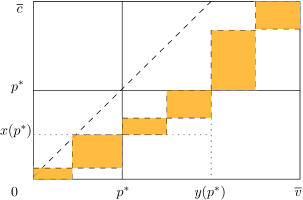

is the rectangle to the left of and is a rectangle upward as depicted in the Figure 8. The dotted red rectangle shows the boundary of set . In the next lemma, we show that mass of area to the left, and above, is zero.

Lemma 8

For worst distribution mass in region and is zero, i.e.,

Proof: We start with the proof for region.

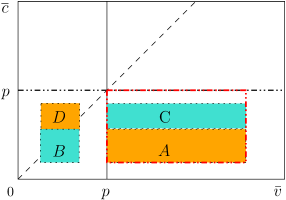

Suppose for contradiction that there exists a rectangle, with non-zero mass in region Let be the rectangle in with mass, .121212Without loss of generality, we could have considered . Now, consider rectangle defined as follows:

Since has positive mass, Note that we can find and such that and have same mass, , and To find these and , one can find a horizontal line cutting regions and . As the horizontal line moves upward, the mass below the line in rectangle will increase and mass above the line in rectangle will decrease.131313For any line passing through , the mass of region is strictly positive; it follows from definition of . As a result, one can choose horizontal line for region close to the bottom boundary of set and keep it moving upward until the mass equalises in region above the horizontal line in rectangle and region below horizontal line in rectangle .

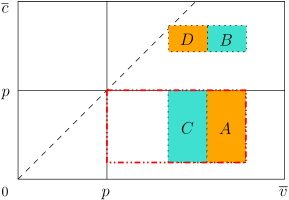

Now consider redistribution from and to and as per equation (20). Notice that as a result, the efficiency gains will decrease, contradicting the assumption that we started with worst distribution. Analogously, we could argue for upper rectangle . The redistribution corresponding to this case is shown in Figure 10:

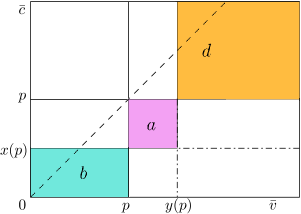

When , for consistency with the marginals and the lemmas 7 and 8, we will have regions with mass and as shown in Figure 11.

Here,

| (21) | ||||

Note that here, 141414For For by definition, and the efficiency gains is zero.

From the analysis above, depending upon , we will have either of the two distributions as worst distribution. When , the efficiency gains is zero. Whenever the equations (21) are satisfied and , irrespective of how the mass is distributed within three rectangles, the efficiency gains are same, and given by

where

This gives us the first proposition of our paper.

Proposition 1

The optimal robust mechanism within the class of deterministic posted price mechanism is mechanism with posted price , where is solution to

where and

Let . This represents the robust efficiency gains corresponding to optimal robust mechanism, and we will use it later.

Proposition 1 characterized that the optimal robust mechanism in the class of deterministic mechanisms. Our main result will show that this mechanism is also the optimal robust mechanism if we allowed for random mechanisms.

5.3 Results on optimal robust mechanism

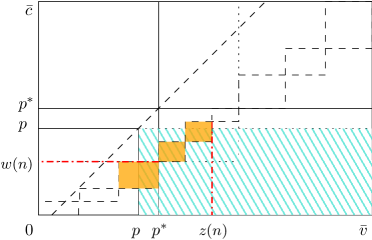

In this section, we show that the mechanism discussed in Proposition 1 is in fact the optimal robust mechanism. We use the observation that for a collection of consistent joint distributions , mechanism is the optimal mechanism and as a result, is optimal robust mechanism. 151515For all , the efficiency gains of mechanism, from the associated worst distribution cannot exceed the one corresponding to by an amount more than

For posted price mechanism , there is a worst distribution of the form that we found in Sub-section 5.2. In that form, we have three rectangles with positive mass. Consider the collection of consistent joint distributions having finer mass distribution than the obtained worst distribution. For illustration, consider Figure 12. Three segments of buyer’s valuation further divided into two equal parts. Given the six segments for buyer’s valuation, we will have six segments of valuation of seller ensuring consistency in marginal distribution. Now, we will have six smaller rectangles with mass. Such a finer mass distribution ensures that efficiency gains by mechanism, for these joint distributions is same as the guaranteed efficiency gains associated with mechanism as these finer distributions are of the form of worst distribution associated with

Consider any posted price mechanism with distribution function over prices. The efficiency gains from for a finer distribution can possibly be greater than . But as we make the distributions finer and finer, the efficiency gains converges to the robust efficiency gains from .161616The limiting distribution will be such that entire mass is on line, given by equation . As a result, the efficiency gains from the posted price mechanism is convex combination of robust efficiency gains of mechanisms, . Since is the optimal robust mechanism in the class of deterministic posted price mechanisms , the robust efficiency gains corresponding to will be greater than those corresponding to posted price mechanism. It follows that is optimal robust mechanism in

Theorem 3

The posted price mechanism is an optimal robust mechanism.

The theorem implies that if we are interested in optimal robust mechanisms in bilateral trading setting, we can restrict ourselves to a very simple class of mechanism–deterministic posted price mechanism.

We have considered the max-min problem till now, where designer wants to design an optimal robust mechanism and the efficiency gains associated with optimal robust mechanism gives the lower bound on the efficiency gains that can be realised if the designer optimally chooses the mechanism. The alternate lower bound for efficiency gains will be the one in which there is uncertainty about the true joint probability density but after the realised value of joint probability density, the designer can optimally choose mechanism. We would expect that the efficiency gains in such a situation will be higher as the designer gets to choose mechanism after realisation of true joint probability density in comparison to choosing the mechanism before realisation in case of max-min problem. However, as we see in the following theorem, these lower bounds actually coincide.

Theorem 4

The values of max-min and min-max of efficiency gains are equal for the class of DSIC mechanisms with BB and IR, 171717The equality holds even for more general setting of BIC mechanisms satisfying BB and interim individual rationality. i.e.,

| (22) |

The above theorem holds because restricted to collection maximises efficiency gains. Restricted to these joint densities, had we chosen the mechanism optimally for true joint probability density, the guaranteed efficiency gains is . Combined with the fact that min-max is not less than max-min in any problem, we get the value of max-min and min-max of efficiency gains equal.

6 Concluding remarks

We studied distributionally robust mechanism design in bilateral trade setting. We focused on max-min version of robustness for joint distribution and found that there is no loss of generality in restricting attention to DSIC mechanisms. This allows us to use characterisation result for implementable mechanisms in the class of block mechanisms in Hagerty and Rogerson (1987) and just focus on posted price mechanisms.

We use the idea of redistribution of mass to characterise the worst distribution for deterministic posted price. For all deterministic posted price mechanism, maximally correlated distribution gives the worst expected gains from the trade. This feature is critical in proving optimality of deterministic posted price, and equivalence between max-min and min-max exercise.

Our analysis can be extended to an auction setting. He and Li (2022) have considered this setting in auction environment but they focused on asymptotically optimal auction. Unlike the bilateral trade setting, in an auction setting, the worst distribution depends on the auction. This makes it more challenging to find the worst distribution.

Acknowledgement

I am grateful to my supervisor, Debasis Mishra for the guidance. I appreciate Jeffrey Mensch and Hemant Mishra for their suggestions. I would also like to thank Aditya Vikram, Arunava Sen, Li Jiangtao, and seminar participants at Stony Brook International Conference on Game Theory and Royal Economic Society Conference (2021) for useful comments.

References

- Bergemann et al. (2017) Bergemann, D., B. Brooks, and S. Morris (2017): “First-Price Auctions With General Information Structures: Implications for Bidding and Revenue,” Econometrica, 85, 107–143.

- Bergemann and Morris (2005) Bergemann, D. and S. Morris (2005): “Robust Mechanism Design,” Econometrica, 73, 1771–1813.

- Brooks and Du (2021) Brooks, B. and S. Du (2021): “On the Structure of Informationally Robust Optimal Auctions,” Tech. rep., Working Paper.

- Carroll (2017) Carroll, G. (2017): “Robustness and Separation in Multidimensional Screening,” Econometrica, 85, 453–488.

- Carroll (2018) ——— (2018): “Information games and robust trading mechanisms,” Unpublished manuscript, Stanford Univ., Stanford, CA.

- Chatterjee and Samuelson (1983) Chatterjee, K. and W. Samuelson (1983): “Bargaining under incomplete information,” Operations research, 31, 835–851.

- Chen et al. (2019) Chen, Y.-C., W. He, J. Li, and Y. Sun (2019): “Equivalence of Stochastic and Deterministic Mechanisms,” Econometrica, 87, 1367–1390.

- Delage and Ye (2010) Delage, E. and Y. Ye (2010): “Distributionally robust optimization under moment uncertainty with application to data-driven problems,” Operations research, 58, 595–612.

- Gershkov et al. (2013) Gershkov, A., J. K. Goeree, A. Kushnir, B. Moldovanu, and X. Shi (2013): “On the equivalence of Bayesian and dominant strategy implementation,” Econometrica, 81, 197–220.

- Hagerty and Rogerson (1987) Hagerty, K. M. and W. P. Rogerson (1987): “Robust trading mechanisms,” Journal of Economic Theory, 42, 94–107.

- He and Li (2022) He, W. and J. Li (2022): “Correlation-robust auction design,” Journal of Economic Theory, 200, 105403.

- Manelli and Vincent (2010) Manelli, A. M. and D. R. Vincent (2010): “Bayesian and Dominant-Strategy Implementation in the Independent Private-Values Model,” Econometrica, 78, 1905–1938.

- Myerson and Satterthwaite (1983) Myerson, R. B. and M. A. Satterthwaite (1983): “Efficient mechanisms for bilateral trading,” Journal of economic theory, 29, 265–281.

- Suzdaltsev (2020) Suzdaltsev, A. (2020): Essays in Robust Mechanism and Contract Design, Stanford University.

- Wilson (1987) Wilson, R. (1987): Game-theoretic analyses of trading processes, Cambridge University Press, 33–70, Econometric Society Monographs.

7 Appendix

7.1 Proof of Lemma 3

We start by defining the following functions:

-

1.

-

2.

We define . Consider arbitrary . By definition of , and , it follows that if we have and .181818Note that iff Thus, we have budget balancedness for such values.

Now we just need to show -budget balancedness for . Formally, we show that as , we have We start by finding relation between and

We simplify the second term in right hand side of above equation using integration by parts. It gives

| (25) |

Substituting (25) in (24), and multiplying the resultant equation by , we get

Iteratively using relation between of consecutive blocks from equation (9), we get

| (26) | ||||

| (27) |

where 191919It is well defined function as and by definition of , whenever lie on boundary of grid,

We will simplify the above expression by using following observations. By definition of and individual rationality of , we have

| (28) | ||||

| (29) |

Using (28) and (29) in (26) gives

| (30) |

Thus, we have

| (31) |

where

| (32) |

From boundedness of , we have

| (33) |

Using M-IIR of , we have

| (34) |

Using this along with boundedness of in equation (32), we get

| (35) |

Using (33) and (35) in (31) we get that for ,

| (36) |

Analogously, for each such that we have

| (37) |

Subtracting (37) from (36), for and , we get

| (38) |

The last equality follows from budget balancedness of

We have thus shown that for the -budget balancedness holds for a large enough . From budget balancedness for and -budget balancedness for , we get that for all ,

7.2 Proof of Lemma 5

Step 1. We define an allocation rule where

Recall the following definitions:

-

1.

-

2.

We show the convergence between probability of allocation for the given mechanism, and .

Let and

Notice that for a given , for squares, containing a point in . In particular, restricted to , the values differ over only. It follows directly from the definition of We show this below.

Suppose for contradiction that there exists and .

Note that implies that .

Since , we have and for all 202020 The inequalities are strict as . Also, by definition of , implies that or . Combining with the fact , we get or for some which is a contradiction.

Using the above fact, for all we have

The first equality comes from partioning each block into blocks. The first inequality follows from the fact that for all and that is non-negative. The last inequality follows from the fact that by definition. Thus, for all , as we have

Alternatively, for all , as we have

Step 2. We show the convergence between probability of allocation for the given mechanism and , which would later be used to prove Lemma 4.

To simplify notations, we consider two measures on the Borel sigma algebra: Lebesgue measure, and given probability measure, We use the concept of simple functions to show convergence in probabilities.

Consider a rectangle, . We can divide it into equal sized blocks by cutting each side into equal parts. We define as the collection of these equal sized blocks.

Let be a simple function defined as where is indicator function, are disjoint measurable sets and for all Also, we have

Fix collection of measurable sets, . Since is a measurable set, for every , there exists collection of blocks (squares) (for large enough ) such that

-

(i)

-

(ii)

and

-

(iii)

Choose This ensures that above conditions hold simultaneously for all

Note that

| (39) |

The first equality follows from additivity of measure for disjoint sets. The strict inequality follows from definition of and sub-additivity of measure The last equality follows from the fact that

Now consider arbitrary collection such that , and we have

| (40) | ||||

| (41) |

This follows from the fact that and and equation (39). This is explained below.

Analogously, we get the expression for as presented in (40). We use use this equation in this proof later.

Now we show that as

We start by finding expected over arbitrary

Consider arbitrary For , we have

| (42) |

The equality follows from the definition of . The first inequality follows from definition of function of and the last inequality follows from definition of max. Thus,

| (43) |

We partition the set on the basis of whether intersects measurable sets other than or not, with positive measure. Consider For , by equation (42), we get This implies

| (44) |

For , we have

| (45) | ||||

| (46) |

The last strict inequality uses equation (40) and the fact that we are considering number of measurable sets. Adding (44) and (46), we get that

Summing over , we get

As the above equation holds for all , we get

| (47) |

Now we will show similar result for simple functions approaching from below.

Consider be a simple function defined as where is indicator function, are disjoint measurable sets, and Also, we have

Analogously, we can show that as Since is integrable with respect to we have

Using the above fact with lower and upper bound for , we get that as ,

Step 3. We use the observations in Step 1 and Step 2 to prove lemma.

Combining the convergences in Step 1 and Step 2,

| (48) |

Let and be the projection of a set on axis and axis, respectively. Note that

| (49) |

It follows from the fact that and .

7.3 Proof of observations in proof of Theorem 2

Proof of Observation 1

Proof of Observation 2

Fix a and . Define a joint density as follows:

By M-IIR of

The inequality holds for all . By integrating over from to , we get

| (50) |

Analogously, by BB of , we get

| (51) |

Combining the inequalities (50) and (51), we get

| (52) |

For , we have for all . To satisfy the above inequality, we must have a.e.

Thus, for , we have by definition of

Proof of Observation 3

We prove this observation by induction. For , it holds true. Suppose the inequality holds for all where and . We show that it holds for all where Consider arbitrary with

To simplify notation in the proof, let . By the definition of , we have

As the observation holds for where , and depends only on we get

7.4 Proof of Theorem 3

For , we define a collection of consistent joint densities . It has distributions that are finer than the worst distribution for deterministic posted price mechanism depicted in Figure 11. In particular, the mass in each of the three rectangles is redistributed into some rectangles such that length of rectangles is same within each of the three rectangles. Formally,

We use to denote the joint probability density with partitions in each of three rectangles.

An element of collection is depicted in Figure 13.

Notice that there are sets and such that there is mass only in rectangles of form where

We will show that arbitrary mechanism generates robust efficiency gains less than .

Consider an arbitrary joint probability density, From equation (19), we know that just the marginal density in the region of trade matters for calculation of efficiency gains. Thus, the efficiency gains for posted price mechanism- is upper bounded by

where

The Figure 13 depicts and for an example.

Note that

Since and are strictly decreasing in , we have

The efficiency gains of posted price mechanism is given by

Since the above relation holds for arbitrary posted price mechanism, we get

As , we get

However, we have

Thus, we get and is an optimal robust mechanism in