An Effective Treatment Approach to Difference-in-Differences

with General Treatment Patterns††thanks:

The author is very grateful to Tadao Hoshino, Takuya Ishihara, and Ryo Okui for their helpful comments, which significantly improved the paper.

The author thanks Lei Qin for his excellent research assistance.

This work was supported by JSPS KAKENHI Grant Number 20K13469.

The author reports no other competing interests to declare.

The paper was previously circulated under the title “Doubly Robust Difference-in-Differences with General Treatment Patterns”.

Abstract

We consider a general difference-in-differences model in which the treatment variable of interest may be non-binary and its value may change in each period. It is generally difficult to estimate treatment parameters defined with the potential outcome given the entire path of treatment adoption, because each treatment path may be experienced by only a small number of observations. We propose an alternative approach using the concept of effective treatment, which summarizes the treatment path into an empirically tractable low-dimensional variable, and develop doubly robust identification, estimation, and inference methods. We also provide a companion R software package.

Keywords: dynamic treatment effects, effective treatment, event study, panel data, parallel trends

JEL Classification: C14, C21, C23

Abstract

Appendices A and B contain the proofs of the theorems and several lemmas. The discussion for aggregation parameters and the formal asymptotic investigations are given in Appendix C. In Appendix D, we report the results of Monte Carlo simulations.

1 Introduction

Difference-in-differences (DiD) is one of the most popular empirical strategies using panel data. Under the parallel trends assumption, one can identify meaningful treatment parameters by comparing the time evolution of the outcomes between the treatment and comparison groups. Most of the recent literature has been devoted to the development of methods in the staggered adoption setting, in which each unit continues to receive a binary treatment after the first treatment receipt (cf. de Chaisemartin and D’Haultfœuille, 2022c; Sun and Shapiro, 2022; Callaway, 2023; Roth et al., 2023).

Although staggered adoption is a typical setting in applied research, there are many empirical situations in which this is not the case.111 de Chaisemartin and D’Haultfœuille (2022a) conduct a survey of the 100 most-cited articles in the American Economic Review from 2015 to 2019. They document that 26 papers estimate a two-way fixed effects (TWFE) regression, but only 4 papers fit the standard staggered adoption setting. For example, Vella and Verbeek (1998) estimate the effect of union membership on wages. Approximately 28% of the individuals in their sample change union membership status at least twice, implying non-staggered treatment adoption. In another example, Deryugina (2017) examines the impact of being hit by a hurricane on the fiscal cost for a US county. In this scenario, the treatment variable of interest indicates whether (or the number of times) a county was hit by a hurricane in a year. This empirical situation also does not fit perfectly into the standard setting of staggered adoption because a county damaged by a hurricane this year is not necessarily hit by a hurricane in the following year.

We consider a general DiD model in which the treatment variable of interest may be non-binary and time-varying, in that the treatment realization of each unit may change in each period, which encompasses the staggered setting as a special case. It is generally difficult to estimate sensible treatment parameters using DiD methods conditional on the entire path of treatment adoption. This is because there may be a large number of treatment paths, so that each treatment path may be experienced by only a small set of observations. As a concrete example, in the dataset of Vella and Verbeek (1998), there are 95 different paths of union membership status, 53 of which are experienced by only one individual. In such a case, it is challenging to develop a DiD method that can accurately estimate meaningful treatment parameters.

We propose a DiD method using the concept of effective treatment, which converts the entire treatment path into an empirically tractable low-dimensional variable. In an influential study, Manski (2013) develops the concept of effective treatment to summarize potentially complicated treatment spillovers among individuals in the presence of social interactions.222 The effective treatment is also referred to as exposure mapping in the literature on causal inference under interference (cf., Aronow et al., 2021). Building on this idea, we propose an effective treatment approach to summarize the treatment path over time in the DiD setting, while assuming no interference between units. In particular, we consider the following effective treatment specifications useful for estimating the instantaneous and dynamic treatment effects: whether some treatment realization has been received at least once so far, the earliest period of receiving some treatment realization so far, and the number of treatment adoptions so far.

Given an effective treatment specification, we set our target parameter as the average treatment effect for movers (ATEM), who switch from the comparison group to receiving an effective treatment realization between two periods. We provide a set of sufficient conditions, including a conditional parallel trends assumption given observed covariates, under which the ATEM is identified by each of outcome regression (OR), inverse probability weighting (IPW), and doubly robust (DR) estimands. An important feature of our identification analysis is that it allows the chosen effective treatment specification to be “incorrect” in that the potential outcome is not well defined with respect to this effective treatment. This feature is empirically attractive, because researchers generally do not have prior knowledge of the true form of effective treatment. Furthermore, as the parallel trends assumption is key to our analysis, we also derive its testable implication, which suggests a “pre-trends” test similar to existing ones.

Based on the identification result using the DR estimand, we propose a two-step estimation procedure. First, we estimate the OR function for stayers and a generalized propensity score (GPS) under parametric assumptions. Then, we construct an ATEM estimator using the sample counterpart of the identification result. Desirably, the resulting ATEM estimator has the DR property: it is consistent and asymptotically normally distributed if either the parametric assumptions of the OR function or GPS are correct. We also consider a multiplier bootstrap inference procedure for constructing uniform confidence bands (UCB).

As an empirical illustration, we apply our methods to the dataset of Vella and Verbeek (1998). Using each effective treatment specification discussed above, we find no statistical evidence to support significant effects of union membership on current and future wages. Furthermore, the pre-trends testing result is consistent with the parallel trends assumption.

This study builds on a number of recent contributions, including de Chaisemartin and D’Haultfœuille (2020b), Goodman-Bacon (2021), Imai and Kim (2021), Sun and Abraham (2021), Wooldridge (2021), Athey and Imbens (2022), and Borusyak et al. (2023). Among them, our methods extend in particular Sant’Anna and Zhao (2020) and Callaway and Sant’Anna (2021), who develop the DiD methods using the DR estimands in the canonical two-period model and the staggered setting, to our situation with possibly non-binary time-varying treatment.

Another closely related study is de Chaisemartin and D’Haultfœuille (2022a), who propose DiD estimation for certain instantaneous and dynamic treatment effects in a setting similar to ours. They begin by showing that commonly used TWFE regressions produce biased estimates for treatment effects. Importantly, this negative result is applicable to our situation, and thus, we cannot recover sensible treatment parameters from such TWFE regressions. See de Chaisemartin and D’Haultfœuille (2020b, 2022b), Goodman-Bacon (2021), and Ishimaru (2022) for related results. de Chaisemartin and D’Haultfœuille (2022a) then propose an event study estimation method by defining the “event” as the period in which the unit receives a treatment realization for the first time. In comparison, we consider general forms of effective treatment, and our methods have an empirically attractive DR property in the same spirits as Sant’Anna and Zhao (2020) and Callaway and Sant’Anna (2021).

This study is also related to several recent works that propose DiD methods when the treatment variable of interest is non-binary. Callaway et al. (2021) and de Chaisemartin et al. (2022) consider settings in which the treatment variable has continuous realizations. de Chaisemartin and D’Haultfœuille (2022b) study DiD estimation in the presence of several binary treatment variables with staggered adoption. These studies are tailored to specific forms of treatment realizations, whereas our effective treatment approach handles essentially arbitrary treatment realizations.

The rest of this paper is organized as follows. In Section 2, we introduce the setup and formalize the concept of effective treatment. Sections 3 and 4 develop the identification and estimation methods. Section 5 presents the testable implication for parallel trends. Section 6 provides the empirical illustration. The supplementary appendix contains technical proofs and simulation results. A companion R package is available from the author’s website.

2 Setup and Effective Treatment

We have panel data , where and are the outcome and treatment, respectively, for unit in period , is a vector of unit--specific covariates, and and denote the sets of units and periods, respectively. Some unobserved factors may be correlated with and , implying the possible treatment endogeneity.

The treatment may be binary, discrete, continuous, or multidimensional. When , unit receives no treatment in period (throughout the paper, for notational simplicity, we write a generic vector of zeros by ). By contrast, with indicates that unit receives treatment intensity in period . The realization of can vary over time in that each unit can move into and out of receiving each treatment intensity in each period. For each , let .

Let denote the potential outcome given the entire treatment path . This notation makes explicit that the current outcome may depend on past, current, and future treatment intensity. For example, denotes the potential outcome in period if unit has never been treated in periods. By construction, .

Remark 1 (No anticipation).

The no-anticipation condition is commonly assumed in the literature, under which the current outcome does not depend on future treatment adoption. Then, the potential outcome in period given is well defined. We will reflect our belief in no anticipation when choosing the functional form of effective treatment.

In general, it is difficult to estimate treatment parameters defined with respect to . This is because the number of units that follow a specific treatment path may be small in practice, especially when there is much variation in treatment intensity or when the length of the time series is not very small. For example, when has discrete realizations, there may be potential outcomes for each and . In such a situation, only a limited number of units would experience , making it difficult to obtain precise causal estimates.

To circumvent this problem, we adopt the concept of effective treatment, which converts the treatment path into an empirically tractable low-dimensional variable that researchers believe to be relevant to the outcome in period . Specifically, for each , consider a user-specified function , where denotes the range of . Here, the functional form of may change depending on . We call the effective treatment function, the corresponding realization the realized effective treatment for unit in period , and the values in the effective treatment intensity. When , we consider unit in period as the comparison unit under this . We write the set of nonzero realizations of as .

The following is a set of examples of the functional form of effective treatment.

Example 1 (name = The once specification, label = ex:once).

If we are interested in the relationship between the outcome and whether the unit has received some treatment intensity at least once so far, we may consider

| (2.1) |

The set of nonzero realizations is .

Example 2 (name = The event specification, label = ex:event).

When the period so far in which each unit is treated for the first time is relevant to the outcome, we may use the following specification:

| (2.2) |

We call and the event date and event time, respectively (cf. Miller, 2023). The set of nonzero realizations in period is .

Example 3 (name = The number specification, label = ex:number).

When the number of treatment adoptions so far matters for the outcome, we set

| (2.3) |

with the corresponding .

Remark 2 (Limited anticipation).

Under limited anticipation, there is some known such that the outcome in period is determined from the path of treatment adoptions over periods (cf. Callaway and Sant’Anna, 2021). We can easily incorporate our belief in it into the functional form of effective treatment. For example, (2.1) can be modified to .

Next, we formalize the correctness of the effective treatment specification. The following definition builds on the treatment effects literature on cross-unit interference (cf., Manski, 2013; Vazquez-Bare, 2022; Hoshino and Yanagi, 2023b).

Definition 2.1.

Consider effective treatment functions and .

-

(i)

is correct if for all and , implies .

-

(ii)

is coarser than if there is a surjective mapping such that for any .

-

(iii)

A correct is true if is coarser than any other correct specification.

There may be several correct specifications. For example, if one of (2.1)–(2.3) is correct, so is the identity mapping , which is the “finest” correct specification. As the identity mapping is always correct, the true specification always exists, which may or may not equal the identity mapping.

Example 4.

Since , the once specification is coarser than the event and number specifications. In general, there is no relationship between the coarseness of the event and number specifications.

Throughout the paper, we write the true effective treatment function as , which is generally unknown to researchers. Let denote the realized true effective treatment for unit in period . From the definition of the correct specification, we can define the potential outcome for unit in period given , that is, for any such that . For example, denotes the potential outcome when unit in period is a comparison unit under the true . The individual treatment effect in period can be written as , where and , which may be heterogeneous across , , and .

Ideally, we would like to adopt the true effective treatment function for the DiD analysis to obtain meaningful causal estimates. In reality, however, we generally have no prior knowledge of the true specification, unless the canonical two-period model or the staggered case. Furthermore, even if we know a correct specification, such as identity mapping, it may be too “fine” to obtain accurate DiD estimates. Thus, instead of pursing the true specification, we explicitly allow for potential misspecification and aim to obtain relatively precise DiD estimates equipped with sensible causal interpretation. Similar approaches have been advocated in the literature of causal inference in the presence of treatment spillovers (Aronow and Samii, 2017; Leung, 2022; Vazquez-Bare, 2022; Hoshino and Yanagi, 2023a).

3 Identification Analysis

We begin by imposing the following condition:

Assumption 3.1 (Effective treatment 1).

Let be a user-specified effective treatment function.

-

(i)

For each , is a finite set on .

-

(ii)

For any and , implies .

Assumption 3.1(i) requires the pre-specified to have discrete realizations. Under Assumption 3.1(ii), any comparison unit under the pre-specified is a comparison unit even under the true . This should be a mild requirement, because each unit should be considered as a comparison unit when or when with some .

3.1 Target parameter and its causal interpretation

For periods and such that , a user-specified effective treatment function , and effective treatment intensity , the ATEM is defined by

| (3.1) |

where indicates whether unit is a mover who moves from the comparison group to receiving effective treatment intensity between periods and .

The next theorem is our first main result, which shows that the causal interpretation of is determined from the relationship between the pre-specified and true .

Theorem 3.1.

Suppose that Assumption 3.1 holds.

-

(i)

If ,

where .

-

(ii)

If is not the true but a correct specification, there is a surjective such that

-

(iii)

Assume that has discrete realizations (for exposition purposes). If is incorrect,

Result (i) considers the case where the pre-specified is actually true. In this case, the ATEM indicates the ATE of receiving the true effective treatment intensity for movers defined with the true .

Result (ii) corresponds to the situation where the pre-specified is correct but “finer” than the true . Then, the ATEM can be interpreted as the ATE of receiving the true effective treatment intensity for movers in terms of the pre-specified

Result (iii) allows for the possibility that the pre-specified is neither true nor correct. Even in this case, the ATEM has causal interpretation as a weighted average of the ATE conditional on both the “true mover” () and the “pre-specified mover” (). The weight function is , that is, the probability of being the true mover conditional on being the pre-specified mover. Importantly, this weight function is non-negative and sums up to one so that the ATEM satisfies the so-called no-sign-reversal property. More precisely, is positive (resp. negative) if the individual treatment effect is almost surely (a.s.) positive (resp. negative) for all . Thus, in conjunction with the identification results given in the next subsection, our methods do not suffer from the negative weighting or sign-reversal problem, unlike commonly used TWFE regressions (cf. de Chaisemartin and D’Haultfœuille, 2020b, 2022a, 2022b; Goodman-Bacon, 2021; Ishimaru, 2022).

Remark 3 (Test of significance).

If there is no treatment effect heterogeneity across units and true effective treatment intensity such that with some non-stochastic , we have for any . In particular, this result holds for . Thus, in practice, we can test for the significance of treatment effects by performing statistical inference for even when the pre-specified is incorrect.

The choice of the effective treatment function , periods , and effective treatment intensity determine what measures more specifically.

Example 5 (continues = ex:once).

Let , where . By setting , we have

which captures the composition of the instantaneous and dynamic treatment effects, that is, the effect of receiving some treatment intensity at least once between periods and for those who did not receive the treatment in the first period.

Example 6 (continues = ex:event).

Let , where with and . Setting , we have

This indicates the ATE in period for those who received some treatment intensity for the first time in period . In the same manner as in the staggered case, estimating this ATEM over a set of allows us to understand the instantaneous and dynamic treatment effects separately. Specifically, with (resp. with ) is informative about the instantaneous (resp. dynamic) effect of the first treatment receipt in period .

Example 7 (continues = ex:number).

Define , where with and . When we set , we have

This ATEM recovers the ATE in period for those who were not treated in the first period and received treatment times in periods. By estimating this ATEM over a set of , we can separately assess the instantaneous and dynamic effects of the number of treatment adoptions.

Remark 4 (Relationship between different specifications).

Interestingly, can be obtained from aggregating or in a certain way. See the supplementary appendix for more details.

Remark 5 (Practical recommendations).

It is common practice to perform event study analyses prior to formal DiD estimation (cf. Miller, 2023). Given this, it would be natural to take the event specification as a good starting point and to plot over a set of , including “pre-trends” to assess the validity of parallel trends (see Figure 2 in the empirical illustration section). It would then be desirable to further examine treatment effect heterogeneity with other effective treatment functions, such as the number specification. Finally, to obtain more precise estimates, it would be recommended to estimate and its time-series average as useful aggregation parameters, that is,

| (3.2) |

3.2 Identification of ATEM

Let indicate a stayer who remains in the comparison group in periods and . Define the GPS by

which is the probability of being a mover with receiving effective treatment intensity between periods and conditional on and on being either a mover or a stayer between periods and . Let denote a set of triplets at which we would like to identify .

Assumption 3.2 (Overlap).

For each , there exists a constant such that and a.s.

Assumption 3.3 (Parallel trends).

For any ,

Assumption 3.2 is an overlap condition under which there are non-negligible proportions of stayers and movers. This is a common requirement, but clearly restricts the data generating process and functional form of effective treatment. For instance, it will be violated if there are few treated units in each period or if is time invariant (i.e., for all ).

The parallel trends condition in Assumption 3.3 is essential for our analysis. This assumption states that the evolution of the untreated potential outcome is mean-independent of the entire treatment path, conditional on the unit-specific covariates. Note that this is a condition on the data generating process and does not restrict the specification of effective treatment. For a better understanding, consider the following specific model:

where is a non-stochastic coefficient vector, represents a treatment choice equation, is a unit FE, and are non-stochastic time FEs, and and are idiosyncratic error terms that vary across both and . The essential requirement is that is additively separable from the other components in the untreated potential outcome equation. If the treatment status in is deterministic, then is determined from given . Then, Assumption 3.3 is fulfilled if are independent of conditional on . Importantly, this situation allows for the endogenous treatment choice in that can be correlated with both and .

As the second main result in this paper, the next theorem shows that the ATEM is identifiable from each of OR, IPW, and DR estimands. For a generic and periods , denote . Define

| (3.3) |

where

In words, is the OR function for stayers, is the ratio of GPS, and and are weights for movers and stayers, respectively.

Remark 6 (Identification in the absence of covariates).

If the identification conditions are fulfilled without covariates, the identification result reduces to

In Theorem 3.2, the three estimands serve the same role from the perspective of identification analysis, but we prefer the DR estimand for estimation purposes. This is because only it has the DR property. To see this, we introduce parametric models for the OR function and GPS, say and . Here, and are functions known up to the finite-dimensional parameters and . Let and denote the pseudo-true values. The DR estimand under these parametric specifications is given by

| (3.4) |

where

| (3.5) |

Assumption 3.4 (Parametric model).

For each , either condition is satisfied.

-

(i)

There exists a unique such that a.s.

-

(ii)

There exists a unique such that a.s.

Theorem 3.3.

This result, in turn, ensures that the ATEM can be consistently estimated via the DR estimand if either the OR function or GPS is correctly specified.

4 Estimation and Statistical Inference

We consider estimation and inference methods based on the identification result using the DR estimand in (3.4). We focus on the following data generating process:

Assumption 4.1 (DGP).

The panel data are independent and identically distributed (IID) across .

4.1 Estimation procedure

We propose a two-step estimation procedure. First, we estimate the finite-dimensional parameters and using parametric estimation methods. For instance, may be estimated by running a linear regression with the dependent variable and the explanatory vector using the observations satisfying . Meanwhile, using observations with , we can estimate using the parametric maximum likelihood method, such as logit or probit estimation, in which the binary response variable is and the explanatory vector is . Let denote the vector of the first-step estimators.

In the second step, we compute the sample analog of the DR estimand in (3.4) as follows:

| (4.1) |

where for generic and

Remark 7 (Overview of the asymptotic properties).

When tends to infinity and is fixed, under a set of mild regularity conditions, we can show that the proposed ATEM estimator is -consistent and asymptotically normally distributed. More precisely, we can prove the following influence function representation:

where denotes the pseudo-true parameter vector in the first-stage parametric estimation and is an influence function, which has a zero mean and a finite variance. See the supplementary appendix for the formal asymptotic analysis.

4.2 Multiplier bootstrap inference

Let be an estimator of obtained by replacing the pseudo-true parameter value and population mean with the first-step estimator and sample mean , respectively. Let be a set of IID bootstrap weights independent of the original sample such that , , and for some . A common choice is Mammen’s (1993) weight, such that and with . The bootstrap analog of the ATEM estimator is defined by

We consider the following multiplier bootstrap inference procedure, which is similar to those of Belloni et al. (2017) and Callaway and Sant’Anna (2021).

Procedure 4.1 (Multiplier bootstrap).

-

1.

Generate . Compute and . Repeat this step times.

-

2.

Construct the bootstrap standard error for by the empirical interquartile range of rescaled with the interquartile range of :

where is the empirical -quantile of and is the -quantile of .

-

3.

Construct the UCB for as follows:

where the bootstrap critical value is obtained by the empirical -quantile of the maximum of the bootstrapped test statistics defined as .

It can be shown that the bootstrap distribution mimics the asymptotic distribution of the ATEM estimator. The proof is analogous to Theorem 3 of Callaway and Sant’Anna (2021) and thus is omitted here. This result, in turn, ensures the asymptotic validity of the multiplier bootstrap inference procedure. More precisely, the coverage error of the UCB vanishes asymptotically:

5 Testable Implication for Parallel Trends: Pre-trends Test

To begin with, we add a mild requirement to the pre-specified . The following assumption states that a comparison unit in the current period should be a comparison unit even in past periods.

Assumption 5.1 (Effective treatment 2).

For any , implies .

The basic idea is as follows. For a period such that , we denote . Under the parallel trends condition in Assumption 3.3, we can show that

| (5.1) |

Thus, it is necessary for parallel trends that, in any “pre-effective treatment” period , the outcome evolution for movers should follow the same path as the outcome evolution for stayers. If we find statistical evidence against (5.1), the parallel trends assumption would be implausible.

The next theorem formalizes this idea using the DR estimand. For each and , define

and

where is the OR function in period for stayers between periods and . Note that for reduces to in (3.1).

Theorem 5.1.

This testable implication suggests the following procedure for assessing parallel trends. First, we construct the UCB for using the multiplier bootstrap. Then, the parallel trends assumption should be refuted if a number of the resulting confidence bands exclude zeros.

It should be cautious that “passing” this type of test does not necessarily ensure the validity of parallel trends. This is because the testable implication in (5.2) is merely a necessary condition for parallel trends. Indeed, recent studies point out that this type of test often has low power against the violation of parallel trends (cf., Roth, 2022).

6 Empirical Illustration: Union Wage Premium

Vella and Verbeek (1998) find a positive effect of union membership status on wages by estimating a dynamic selection model. In the DiD literature, de Chaisemartin and D’Haultfœuille (2020b) revisit the same dataset and demonstrate that current union membership may not significantly influence current wages. Here, we complement these previous results with the proposed methods, which enable the estimation of both the instantaneous and dynamic treatment effects.

The data record 545 full-time working males taken from the National Longitudinal Survey (Youth Sample) for 1980–1987.333 The data set is available through the Inter-university Consortium for Political and Social Research (de Chaisemartin and D’Haultfœuille, 2020a). The binary treatment indicates the union membership status of individual in year , reflecting whether is covered by a collective bargaining agreement. The outcome is the logarithm of the hourly wages for individual in year . As the set of unit-specific covariates , we consider race, years of schooling, and years of labor market experience in the first period.

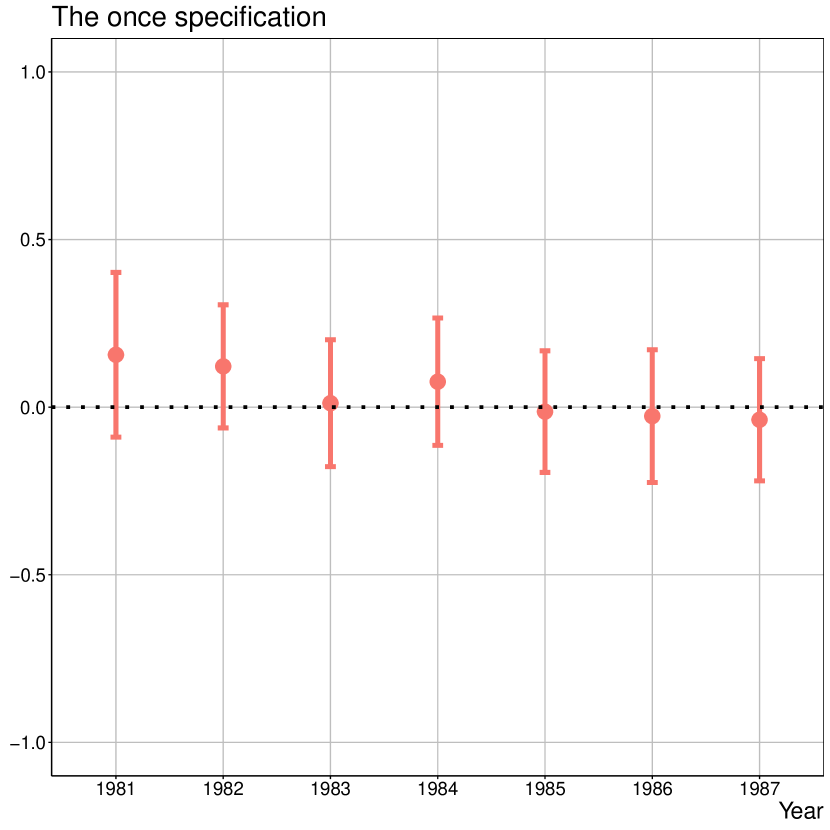

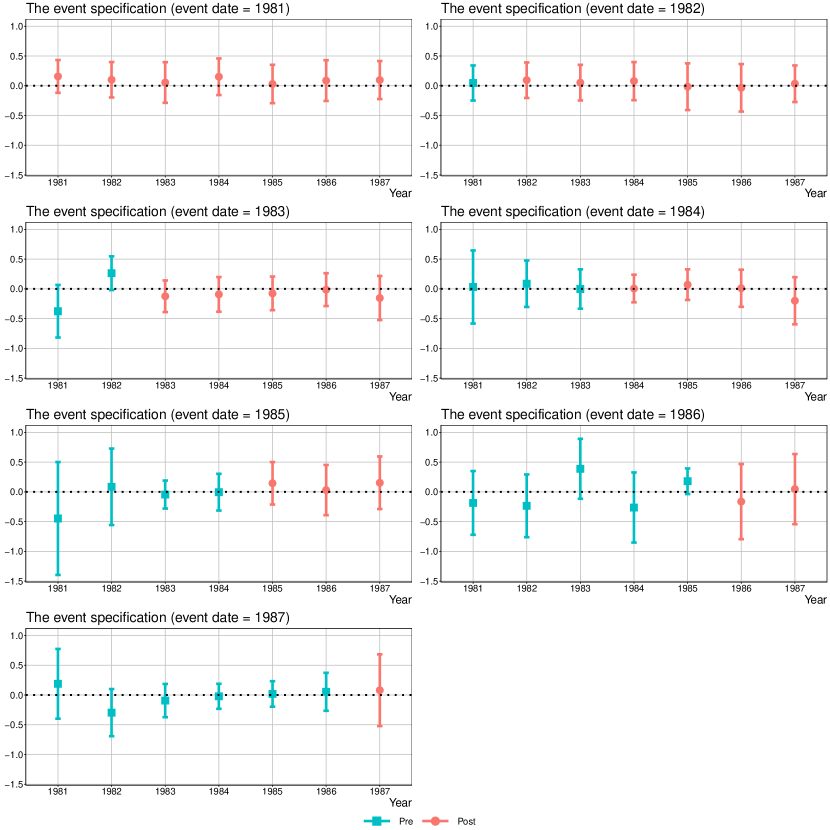

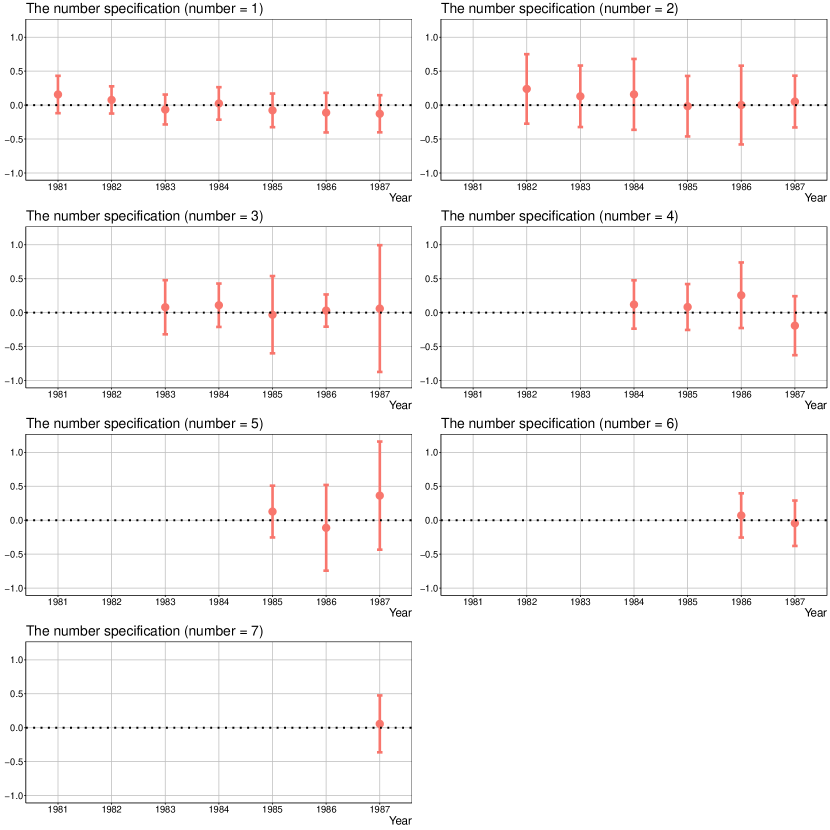

Figures 1, 2, and 3 present the estimates of the three ATEM parameters in Examples LABEL:ex:once, LABEL:ex:event, and LABEL:ex:number with the corresponding 95% UCBs obtained from 5,000 bootstrap replications using Mammen’s (1993) weight. For the first-step estimation, we estimate the OR function for stayers and GPS using the method of least squares and logit estimation, respectively. We can see that there are both positive and negative estimates, but many of them are small in the absolute sense. Indeed, all the resulting UCBs include zeros, that is, we find no statistical evidence for current and future union wage premiums. We also find a statistically insignificant estimate of the aggregation parameter defined in (3.2). Specifically, the estimate is and the 95% confidence interval is .

The pre-trends testing result for the event specification is shown in Figure 2. No UCBs for “pre-effective treatment” periods exclude zeros, which is consistent with the parallel trends in Assumption 3.3.

Accordingly, our DiD analysis suggests that union membership might not substantially improve current and future wages, which is in line with the finding of de Chaisemartin and D’Haultfœuille (2020b).

References

- Aronow et al. (2021) Aronow, P.M., Eckles, D., Samii, C., and Zonszein, S., 2021. Spillover effects in experimental data, in: J. Druckman and D.P. Green, eds., Advances in Experimental Political Science, Cambridge University Press, chap. 16, 289–319.

- Aronow and Samii (2017) Aronow, P.M. and Samii, C., 2017. Estimating average causal effects under general interference, with application to a social network experiment, The Annals of Applied Statistics, 11 (4), 1912–1947.

- Athey and Imbens (2022) Athey, S. and Imbens, G.W., 2022. Design-based analysis in difference-in-differences settings with staggered adoption, Journal of Econometrics, 226 (1), 62–79.

- Belloni et al. (2017) Belloni, A., Chernozhukov, V., Fernández-Val, I., and Hansen, C., 2017. Program evaluation and causal inference with high-dimensional data, Econometrica, 85 (1), 233–298.

- Borusyak et al. (2023) Borusyak, K., Jaravel, X., and Spiess, J., 2023. Revisiting event study designs: Robust and efficient estimation, arXiv preprint arXiv:2108.12419.

- Callaway (2023) Callaway, B., 2023. Difference-in-differences for policy evaluation, in: K.F. Zimmermann, ed., Handbook of Labor, Human Resources and Population Economics, Springer International Publishing, 1–61.

- Callaway et al. (2021) Callaway, B., Goodman-Bacon, A., and Sant’Anna, P.H., 2021. Difference-in-differences with a continuous treatment, arXiv preprint arXiv:2107.02637.

- Callaway and Sant’Anna (2021) Callaway, B. and Sant’Anna, P.H., 2021. Difference-in-differences with multiple time periods, Journal of Econometrics, 225 (2), 200–230.

- de Chaisemartin and D’Haultfœuille (2020a) de Chaisemartin, C. and D’Haultfœuille, X., 2020a. Data and code for: Two-way fixed effects estimators with heterogeneous treatment effects, Inter-university Consortium for Political and Social Research [distributor], 2020-08-26. https://doi.org/10.3886/E118363V2.

- de Chaisemartin and D’Haultfœuille (2020b) de Chaisemartin, C. and D’Haultfœuille, X., 2020b. Two-way fixed effects estimators with heterogeneous treatment effects, American Economic Review, 110 (9), 2964–96.

- de Chaisemartin and D’Haultfœuille (2022a) de Chaisemartin, C. and D’Haultfœuille, X., 2022a. Difference-in-differences estimators of intertemporal treatment effects, Tech. rep., National Bureau of Economic Research.

- de Chaisemartin and D’Haultfœuille (2022b) de Chaisemartin, C. and D’Haultfœuille, X., 2022b. Two-way fixed effects and differences-in-differences estimators with several treatments, Tech. rep., National Bureau of Economic Research.

- de Chaisemartin and D’Haultfœuille (2022c) de Chaisemartin, C. and D’Haultfœuille, X., 2022c. Two-way fixed effects and differences-in-differences with heterogeneous treatment effects: A survey, The Econometrics Journal, forthcoming.

- de Chaisemartin et al. (2022) de Chaisemartin, C., D’Haultfœuille, X., Pasquier, F., and Vazquez-Bare, G., 2022. Difference-in-differences estimators for treatments continuously distributed at every period, Available at SSRN.

- Deryugina (2017) Deryugina, T., 2017. The fiscal cost of hurricanes: Disaster aid versus social insurance, American Economic Journal: Economic Policy, 9 (3), 168–98.

- Goodman-Bacon (2021) Goodman-Bacon, A., 2021. Difference-in-differences with variation in treatment timing, Journal of Econometrics, 225 (2), 254–277.

- Hoshino and Yanagi (2023a) Hoshino, T. and Yanagi, T., 2023a. Causal inference with noncompliance and unknown interference, arXiv preprint arXiv:2108.07455.

- Hoshino and Yanagi (2023b) Hoshino, T. and Yanagi, T., 2023b. Randomization test for the specification of interference structure, arXiv preprint arXiv:2301.05580.

- Imai and Kim (2021) Imai, K. and Kim, I.S., 2021. On the use of two-way fixed effects regression models for causal inference with panel data, Political Analysis, 29 (3), 405–415.

- Ishimaru (2022) Ishimaru, S., 2022. What do we get from a two-way fixed effects estimator? implications from a general numerical equivalence, arXiv preprint arXiv:2103.12374.

- Leung (2022) Leung, M.P., 2022. Causal inference under approximate neighborhood interference, Econometrica, 90 (1), 267–293.

- Mammen (1993) Mammen, E., 1993. Bootstrap and wild bootstrap for high dimensional linear models, The Annals of Statistics, 21 (1), 255–285.

- Manski (2013) Manski, C.F., 2013. Identification of treatment response with social interactions, The Econometrics Journal, 16 (1), S1–S23.

- Miller (2023) Miller, D.L., 2023. An introductory guide to event study models, Journal of Economic Perspectives, 37 (2), 203–30.

- Roth (2022) Roth, J., 2022. Pretest with caution: Event-study estimates after testing for parallel trends, American Economic Review: Insights, 4 (3), 305–22.

- Roth et al. (2023) Roth, J., Sant’Anna, P.H., Bilinski, A., and Poe, J., 2023. What’s trending in difference-in-differences? a synthesis of the recent econometrics literature, Journal of Econometrics, forthcoming.

- Sant’Anna and Zhao (2020) Sant’Anna, P.H. and Zhao, J., 2020. Doubly robust difference-in-differences estimators, Journal of Econometrics, 219 (1), 101–122.

- Sun and Abraham (2021) Sun, L. and Abraham, S., 2021. Estimating dynamic treatment effects in event studies with heterogeneous treatment effects, Journal of Econometrics, 225 (2), 175–199.

- Sun and Shapiro (2022) Sun, L. and Shapiro, J.M., 2022. A linear panel model with heterogeneous coefficients and variation in exposure, Journal of Economic Perspectives, 36 (4), 193–204.

- Vazquez-Bare (2022) Vazquez-Bare, G., 2022. Identification and estimation of spillover effects in randomized experiments, Journal of Econometrics.

- Vella and Verbeek (1998) Vella, F. and Verbeek, M., 1998. Whose wages do unions raise? a dynamic model of unionism and wage rate determination for young men, Journal of Applied Econometrics, 13 (2), 163–183.

- Wooldridge (2021) Wooldridge, J., 2021. Two-way fixed effects, the two-way mundlak regression, and difference-in-differences estimators, Available at SSRN 3906345.

Note: Circles and bars indicate ATEM estimates and corresponding 95% UCBs, respectively.

Note: Circles (resp. boxes) and bars indicate ATEM estimates and corresponding 95% UCBs for “post-effective treatment” (resp. “pre-effective treatment”) periods.

Note: Circles and bars indicate ATEM estimates and corresponding 95% UCBs, respectively.

Online Appendix for:

An Effective Treatment Approach to Difference-in-Differences with General Treatment Patterns

Takahide Yanagi†

† Graduate School of Economics, Kyoto University.

Appendix A Proofs

A.1 Proof of Theorem 3.1

To begin with, recall the definition of the ATEM parameter:

Result (i).

When the pre-specified is actually true so that , we have . Since conditional on , it holds that

Result (ii).

When the pre-specified is not true but correct, the true is coarser than , and there is a surjective mapping such that . Noting that , we have

Result (iii).

Using the law of iterated expectations, we have

where we used Assumption 3.1(ii) and the definitions of and in the third and last equalities, respectively.

∎

A.2 Proof of Theorem 3.2

The OR estimand.

Let . Using the law of iterated expectations and Lemma B.2, we have

The IPW estimand.

The DR estimand.

A.3 Proof of Theorem 3.3

We focus on proving result (i) only, because result (ii) can be shown by the same arguments as in the proof of the third result of Theorem 3.2. Owing to the first result in Theorem 3.2, it suffices to show that

Fix arbitrary . Using the law of iterated expectations, the left-hand side can be written as

From the definition of and the correctly specified , it is easy to see that

This completes the proof. ∎

A.4 Proof of Theorem 5.1

Appendix B Lemmas

Lemma B.1.

Proof.

Using the law of iterated expectations, we have

where the first equality follows from the fact that is determined from and the second equality follows from Assumption 3.3. The same argument shows that

∎

Let

Appendix C Additional Results

C.1 Aggregation parameters

Given Theorems 3.2 and 3.3, a number of aggregation parameters can be recovered as weighted averages of . We discuss the specific aggregation schemes by continuing Examples LABEL:ex:event and LABEL:ex:number.

Example 8 (continues = ex:event).

Define

| (C.1) |

where . This is the ATE for those who were not treated in the first period but received some treatment intensity between periods 2 and . From the law of iterated expectations and the fact that implies that , we can observe that

where . Note that the weight function is identifiable from data and sums up to one.

Example 9 (continues = ex:number).

Define

| (C.2) |

where indicates whether unit , who did not receive the treatment in the first period, received some treatment intensity until period . Using the law of iterated expectations, we can see that this aggregation parameter can be recovered from

where denotes the set of non-zero realizations of and is an identifiable weight function that is non-negative and sums up to one.

The aggregation parameters in (C.1) and (C.2) are closely related to the ATEM parameter discussed in Example LABEL:ex:once. Specifically, it is straightforward to see that

Thus, we recommend that researchers obtain sensible aggregation parameters by estimating and its time-series average, that is,

We can perform the statistical inference for by the multiplier bootstrap in a similar manner to Procedure 4.1.

C.2 Asymptotic investigations

We study the asymptotic properties of the proposed ATEM estimator in (4.1). We consider the asymptotic regime where grows to infinity and is fixed.

The following assumption comprises mild regularity conditions for the first-step estimation, which is similar to Assumption 7 of Callaway and Sant’Anna (2021). Let denote a generic notation that indicates or with or , respectively. We write the Frobenius norm of a generic matrix as .

Assumption C.1 (First-step estimation).

The following conditions are satisfied for each .

-

(i)

The parameter space of , , is a compact set on .

-

(ii)

is a.s. continuous in on .

-

(iii)

There exists a unique pseudo-true parameter value .

-

(iv)

There exists a neighborhood of , , on which is a.s. twice continuously differentiable in with bounded derivatives.

-

(v)

The first-step estimator satisfies and

where is a vector of influence functions such that , is positive definite, and .

-

(vi)

There exists some such that for all , a.s.

To state the next assumption, we introduce the following notation. Letting be a vector of the first-step parameters, define

| (C.3) |

where

with

and

Here, it is easy to see that . Also note that arises from the fact that we estimate the unknown in the first-stage parametric estimation.

Assumption C.2 (Moments).

-

(i)

for each such that with some .

-

(ii)

for each .

The next theorem presents the joint asymptotic normality result for defined in (4.1). The proof is relegated to the end of this section. Let and denote the vectors stacking and , respectively, over . Similarly, for each , let be a vector that collects over .

Theorem C.1.

This theorem implies that the asymptotic variance of is given by , which depends critically on the inverse of . Thus, a more precise ATEM estimation can be generally achieved with a coarser effective treatment specification, such as the once specification, as a coarser one can generally induce more movers between two periods.

C.3 Proof of Theorem C.1

Observe that

For , we first note that

by the Lindeberg–Lévy central limit theorem (CLT). Applying Taylor’s theorem to in around and using the above equations, we have

where we used Assumptions 3.2 and 4.1 in the second equality to evaluate the remainder term. Thus,

Similarly, we can obtain the following results:

and

and

Consequently, we obtain

which completes the proof of asymptotic linear representation. Then, using the CLT, it is easy to obtain the joint asymptotic normality result for . ∎

Appendix D Monte Carlo Experiment

We evaluate the finite-sample performance of the proposed methods through Monte Carlo simulations.

Setting for all , we generate a time-varying binary treatment for each , where the unit-specific covariate , unit FE , and idiosyncratic error term are mutually independent standard normal variables, and is the non-stochastic time effect. We set the untreated potential outcome equation as with the standard normal and another time effect . The observed outcome is generated by , where . The true effective treatment is the event specification in (2.2), and the true ATEM corresponds to . The coefficient parameters are set to , , , and . We consider three patterns of sample sizes .

In the first-step estimation, we estimate the OR function by regressing on the constant and using observations satisfying . In this simulation setup, with and ; thus, the OR function is correctly specified. Meanwhile, we estimate the GPS using logit estimation, implying that the specification of GPS is incorrect. In the second-step estimation, we estimate the three ATEM parameters considered in the empirical illustration. For the multiplier bootstrap inference, we use Mammen’s (1993) weight, and the number of bootstrap replications is set to 5,000.

Tables S1, S2, and S3 present the simulation results obtained with 10,000 simulation repetitions. Each table reports the bias, root mean squared error (RMSE), point-wise coverage probability (PW.CP) and uniform coverage probability (U.CP) of the 95% UCB, and average length of confidence interval (CI.L) for each effective treatment specification.

The bias is satisfactorily small even when is small. The RMSE is approximately halved as increases from 250 to 1,000 or from 1,000 to 4,000, as expected from the consistency of the ATEM estimator. The PW.CP tends to be larger than the nominal level of 0.95, whereas the U.CP is closer to the desired level, which is a common feature of the uniform inference. As expected, the CI.L becomes shorter as increases. Overall, the RMSE and U.CP for the once specification are more desirable than those for the others, due to the fact that the once specification can induce more movers than the others.

| Bias | RMSE | PW.CP | U.CP | CI.L | |||||

|---|---|---|---|---|---|---|---|---|---|

| 250 | 4 | 2 | 1 | 1 | -0.004 | 0.343 | 0.975 | 0.905 | 1.541 |

| 250 | 4 | 3 | 1 | 1 | -0.008 | 0.383 | 0.965 | 0.905 | 1.652 |

| 250 | 4 | 4 | 1 | 1 | 0.001 | 0.433 | 0.958 | 0.905 | 1.820 |

| 1000 | 4 | 2 | 1 | 1 | -0.002 | 0.173 | 0.979 | 0.936 | 0.798 |

| 1000 | 4 | 3 | 1 | 1 | -0.002 | 0.191 | 0.978 | 0.936 | 0.878 |

| 1000 | 4 | 4 | 1 | 1 | -0.001 | 0.219 | 0.977 | 0.936 | 0.989 |

| 4000 | 4 | 2 | 1 | 1 | -0.001 | 0.086 | 0.982 | 0.948 | 0.403 |

| 4000 | 4 | 3 | 1 | 1 | -0.002 | 0.096 | 0.982 | 0.948 | 0.449 |

| 4000 | 4 | 4 | 1 | 1 | -0.002 | 0.108 | 0.981 | 0.948 | 0.511 |

| Bias | RMSE | PW.CP | U.CP | CI.L | |||||

|---|---|---|---|---|---|---|---|---|---|

| 250 | 4 | 2 | 1 | 2 | -0.004 | 0.343 | 0.989 | 0.888 | 1.775 |

| 250 | 4 | 3 | 1 | 2 | -0.011 | 0.445 | 0.981 | 0.888 | 2.143 |

| 250 | 4 | 4 | 1 | 2 | 0.000 | 0.547 | 0.971 | 0.888 | 2.478 |

| 250 | 4 | 3 | 2 | 3 | -0.002 | 0.413 | 0.990 | 0.888 | 2.172 |

| 250 | 4 | 4 | 2 | 3 | 0.004 | 0.466 | 0.988 | 0.888 | 2.400 |

| 250 | 4 | 4 | 3 | 4 | 0.000 | 0.493 | 0.988 | 0.888 | 2.566 |

| 1000 | 4 | 2 | 1 | 2 | -0.002 | 0.173 | 0.993 | 0.931 | 0.924 |

| 1000 | 4 | 3 | 1 | 2 | -0.003 | 0.224 | 0.991 | 0.931 | 1.177 |

| 1000 | 4 | 4 | 1 | 2 | -0.001 | 0.289 | 0.989 | 0.931 | 1.438 |

| 1000 | 4 | 3 | 2 | 3 | -0.001 | 0.204 | 0.992 | 0.931 | 1.101 |

| 1000 | 4 | 4 | 2 | 3 | -0.002 | 0.231 | 0.991 | 0.931 | 1.239 |

| 1000 | 4 | 4 | 3 | 4 | 0.001 | 0.239 | 0.992 | 0.931 | 1.297 |

| 4000 | 4 | 2 | 1 | 2 | -0.001 | 0.086 | 0.993 | 0.941 | 0.467 |

| 4000 | 4 | 3 | 1 | 2 | -0.002 | 0.114 | 0.994 | 0.941 | 0.611 |

| 4000 | 4 | 4 | 1 | 2 | -0.002 | 0.144 | 0.993 | 0.941 | 0.775 |

| 4000 | 4 | 3 | 2 | 3 | 0.001 | 0.103 | 0.992 | 0.941 | 0.554 |

| 4000 | 4 | 4 | 2 | 3 | 0.000 | 0.115 | 0.993 | 0.941 | 0.627 |

| 4000 | 4 | 4 | 3 | 4 | -0.004 | 0.119 | 0.992 | 0.941 | 0.651 |

| Bias | RMSE | PW.CP | U.CP | CI.L | |||||

|---|---|---|---|---|---|---|---|---|---|

| 250 | 4 | 2 | 1 | 1 | -0.004 | 0.343 | 0.987 | 0.874 | 1.688 |

| 250 | 4 | 3 | 1 | 1 | -0.004 | 0.359 | 0.985 | 0.874 | 1.794 |

| 250 | 4 | 4 | 1 | 1 | 0.002 | 0.393 | 0.986 | 0.874 | 1.960 |

| 250 | 4 | 3 | 1 | 2 | -0.012 | 0.538 | 0.967 | 0.874 | 2.332 |

| 250 | 4 | 4 | 1 | 2 | -0.002 | 0.506 | 0.977 | 0.874 | 2.329 |

| 250 | 4 | 4 | 1 | 3 | 0.006 | 0.712 | 0.943 | 0.874 | 2.770 |

| 1000 | 4 | 2 | 1 | 1 | -0.002 | 0.173 | 0.988 | 0.923 | 0.871 |

| 1000 | 4 | 3 | 1 | 1 | -0.001 | 0.178 | 0.987 | 0.923 | 0.907 |

| 1000 | 4 | 4 | 1 | 1 | 0.001 | 0.193 | 0.991 | 0.923 | 0.987 |

| 1000 | 4 | 3 | 1 | 2 | -0.003 | 0.284 | 0.985 | 0.923 | 1.337 |

| 1000 | 4 | 4 | 1 | 2 | -0.003 | 0.252 | 0.985 | 0.923 | 1.242 |

| 1000 | 4 | 4 | 1 | 3 | -0.002 | 0.409 | 0.974 | 0.923 | 1.739 |

| 4000 | 4 | 2 | 1 | 1 | -0.001 | 0.086 | 0.989 | 0.942 | 0.439 |

| 4000 | 4 | 3 | 1 | 1 | -0.001 | 0.089 | 0.991 | 0.942 | 0.455 |

| 4000 | 4 | 4 | 1 | 1 | -0.002 | 0.096 | 0.990 | 0.942 | 0.495 |

| 4000 | 4 | 3 | 1 | 2 | -0.003 | 0.147 | 0.988 | 0.942 | 0.723 |

| 4000 | 4 | 4 | 1 | 2 | -0.002 | 0.125 | 0.990 | 0.942 | 0.640 |

| 4000 | 4 | 4 | 1 | 3 | -0.002 | 0.219 | 0.987 | 0.942 | 1.036 |