Risk Sharing with Deep Neural Networks

Abstract

We consider the problem of optimally sharing a financial position among agents with potentially different reference risk measures. The problem is equivalent to computing the infimal convolution of the risk metrics and finding the so-called optimal allocations. We propose a neural network-based framework to solve the problem and we prove the convergence of the approximated inf-convolution, as well as the approximated optimal allocations, to the corresponding theoretical values. We support our findings with several numerical experiments.

Keywords: Risk Sharing; Deep Neural Networks; Risk Allocation; Inf-convolution; Universal Approximation Theorem.

JEL classification: C45, C63, G32.

1 Introduction

We consider the problem faced by economic agents, with reference risk measures , who want to share the risk carried by a certain financial position, represented by a random variable . The goal is to write as the sum of random variables so that the sum of the risk of the single agents, , is minimized. The problem is well known in the mathematical finance literature under the name of risk sharing, and it amounts to the calculation of the infimal convolution (inf-convolution) defined as follows:

| (1) |

The seminal paper (Barrieu & El Karoui, 2005), which introduced inf-convolutions in the context of (convex) risk measures, originated a vast offspring of literature. (Acciaio, 2007) and (Filipović & Svindland, 2008) studied the case without monotonicity assumptions on the , (Mastrogiacomo & Rosazza Gianin, 2015) considered the case of cash-subadditive and quasi-convex functionals, while multivariate risks are treated in (Carlier & Dana, 2013; Carlier et al., 2012). We also mention (Dana & Le Van, 2010), (Heath & Ku, 2004), (Tsanakas, 2009), (Weber, 2018), (Liebrich & Svindland, 2019) and (Embrechts et al., 2018, 2020) for further extensions and we refer to (Rüschendorf, 2013) for a comprehensive overview of the topic.

The most relevant results for our analysis were established by (Filipović & Svindland, 2008; Jouini et al., 2008) in the study of the so-called optimal allocations for , namely, the minimizers of the right-hand side of (1). For the case of law-invariant risk measures, it was demonstrated that comonotonicity plays a key role. In fact, optimal allocations can be found in the form for some non-decreasing, real-valued, maps , which sum up to the identity. This key aspect inspires the numerical framework that we propose in this paper. Indeed, it can be shown that the functions , for , are Lipschitz continuous functions, thus, they can be very well approximated by neural networks. Despite the abundance of theoretical results on the risk-sharing topic, we are not aware of a general framework for the numerical computation of the solutions which works under very little assumptions, such as law-invariance and convexity. Indeed, the aforementioned literature usually focused on the explicit (or semi-explicit) computation of the optimal allocations in some special cases. This operation obviously requires an exact computation of the inf-convolution and their minimizers, which needs to be worked out case-by-case. Some risk measures of interest, for which explicit solutions can be provided, are the entropic risk measure and expected shortfall among the family of convex risk measures and, more recently, the (Range) Value at Risk among the non-convex ones, see (Embrechts et al., 2018, 2020).

Using a suitable version of the Universal Approximation Theorem, we prove in Section 2 that

where is a suitable class of feed-forward neural networks. Deep neural networks (DNNs) have been proven to be very effective in solving a great variety of problems and in this paper, we show that this is the case also in a risk sharing context. The precise results are stated in Theorem 2.8 and in Theorem 2.11, which constitute the main results of the section. Note that the restriction to agents is dictated by the convenience of exposition, but the case can be covered similarly. Of course, we do not exclude that other methods could be successfully applied. In Appendix B, we discuss some possible alternative approaches.

In view of establishing a rigorous framework for our numerical experiments, we devote Section 3 to the convergence analysis of the historical estimators of the inf-convolution, as well as of their corresponding optimal allocations. Such estimators are constructed simply by applying the risk measures of the agents to the empirical distribution of a large sample of (see e.g. (Cont et al., 2010) for an overview). The main convergence result of the section is Theorem 3.3 which provides the theoretical justification of the experiments of Section 4. We test our findings in a series of numerical experiments with different risk measures, different architectures, and different distributions for (see Section 4.1 for the details about the framework) obtaining consistent results. As for the risk measures, we use the following:

-

1.

Entropic risk measure with parameter :

(2) -

2.

Expected Shortfall (ES) at level :

-

3.

Distortion risk measure for , see (Föllmer & Schied, 2016, Section 4.6):

(3)

The situation where all agents adopt an entropic risk measure, respectively ES, admits an explicit and simple solution for both the value of the inf-convolution and the optimal allocations. We test our numerical approximation in these cases only to confirm that the trained DNNs are converging to the known solutions. We then proceed in testing our algorithms in more complex situations. We cover the case of risk sharing between agents with distortion-type risk measures and between heterogeneous agents, that is, two agents using risk measures of different types — one has the entropic and the other adopts either the expected shortfall or a distortion risk measure. In all such cases, we confirm that the trained network is able to recover the expected form of the optimal allocations, known from (Embrechts et al., 2018) and (Jouini et al., 2008). In the last experiment, where we consider the convolution of an entropic risk measure with a distortion risk measure, we do not have any information about the solution.

We conclude this introduction with the frequently used notation. For a metric space , denotes the Borel -algebra and denotes the class of real-valued, Borel-measurable functions on . We define the following sets:

2 The theoretical framework

Let be a standard non-atomic probability space (see e.g. (Svindland, 2010) for details about the possibility of dropping the standardness assumption). The Banach space for is the set of -integrable random variables on , endowed with the norm . The Banach space is the set of essentially bounded random variables, endowed with the supremum norm . The order relation on such spaces is the one induced by the -a.s. ordering. We first recall the definition of monetary risk measures and some of their standard properties. We refer to the book (Föllmer & Schied, 2016) for a thorough presentation of the topic.

Definition 1.

Let and a functional.

-

•

is normalized if ;

-

•

is finite if for every ;

-

•

is monotone if , whenever -a.s.;

-

•

is cash additive if , for every and ;

-

•

is convex if , for every and .

Any normalized, finite, monotone, and cash-additive is called a monetary risk measure. If is also convex, it is called a convex risk measure.

-

•

is law-invariant if whenever ;

-

•

satisfies the Lebesgue Property if for any sequence and such that: there exists with -a.s. for all and -a.s. holds.

We next introduce the concept of infimal convolution (inf-convolution in short) of convex risk measures . For ease of exposition, we restrict ourselves to the case of , however, all the results generalize to the case of an arbitrary .

Definition 2.

Let . Given two functionals , their infimal convolution is defined as:

| (4) |

Every couple such that is called an allocation for . Additionally, we say that an allocation is

-

•

An optimal allocation if it is a minimizer of the right-hand side of (4);

-

•

A comonotonic allocation if it is of the form for some increasing111Increasing is understood in the non-strict sense. functions such that , where denotes the identity function .

The following well-known result, see (Filipović & Svindland, 2008) Theorem 2.5, shows that for lower semi-continuous (l.s.c.) law-invariant convex risk measures, optimal allocations can be found among the class of comonotonic allocations.

Theorem 2.1.

Let and be l.s.c. law-invariant convex cash additive functions. Then is a l.s.c. law-invariant convex cash additive function. Moreover, there exist increasing functions such that and

It is not difficult to see that the functions are necessarily Lipschitz continuous. Indeed, for , we can write and, using that both functions are increasing, we obtain the inequality for . For the case , the argument is analogous. In particular, it holds for , where

We also observe that, for monetary risk measures, if is an optimal allocation, the same is true for for an arbitrary . This is also called rebalancing of cash. Without loss of generality, the function can be therefore chosen to satisfy , while still preserving the Lipschitz property. Combining these two observations we obtain the following corollary to Theorem 2.1.

Corollary 2.2.

Under the assumptions of Theorem 2.1, we have

| (5) |

where

| (6) |

is the set of normalized Lipschitz allocations.

Any function induces the allocation . Indeed the sum equals by construction and, using the Lipschitz property, it is clear that if then as well. With a slight abuse of terminology, we call allocation also the pair of functions . By denoting the law of under , this terminology becomes accurate when we work on the probability space , as it will often be the case below. The following is a sufficient criterion for guaranteeing the uniqueness of optimal allocations, see (Filipović & Svindland, 2008) Proposition 3.1. For we use the notation for indicating that the difference is not a constant random variable.

Proposition 2.3.

Under the assumptions of Theorem 2.1, suppose additionally that is strictly convex in the sense that

| (7) |

Then the optimal allocation for is unique up to rebalancing of cash, namely, for any pair of optima , it holds for some with and for .

This proposition generalizes to the case when all but one of the initial risk measures are strictly convex (see e.g. the discussion after Corollary 11.14 in (Rüschendorf, 2013)). An example of strictly convex risk measure is the entropic risk measure of (2). We observe here that, for a given , uniqueness can be obtained via a small perturbation of by guaranteeing, at the same time, that the value of the infimal convolution is close.

Lemma 2.4.

Let be law-invariant convex risk measures on , for . Let be a strictly convex risk measure on . For every , the risk measure is a strictly convex risk measure. Moreover, for every and , there exists such that .

Proof.

It is easy to see that all the properties of and are inherited by . As for the second statement, in view of Corollary 2.2 it is enough to show that, defining , , we have . To see this, observe that

Since , and by monotonicity and finiteness of we get , and . The same argument applies to , from which we deduce for some constant depending only on . Since the right-hand side does not depend on , the claim is proved. ∎

Towards the aim of approximating the infimal convolutions using neural networks, we need some continuity of the risk functionals. For risk measures on , the continuity is a consequence of the monotonicity and cash additivity properties. For the case , the Extended Namioka-Klee Theorem (see (Biagini & Frittelli, 2010)) guarantees that any proper convex and monotone functional on is continuous with respect to the -norm, on the interior of its domain. Thanks to the finiteness property, convex risk measures as in Definition 1 are norm continuous for every on the whole space. Throughout the paper, we will therefore make the following standing assumption.

Assumption 2.5.

and are law-invariant convex risk measures.

2.1 Approximation of inf-convolutions via neural networks

In this section, we show that the inf-convolution of two risk measures in (5) can be approximated using neural networks in the construction of the allocations. This is achieved by means of appropriate versions of the universal approximation theorem (UAT). We first note that we can reduce our focus to . Consider indeed a functional which is law-invariant. Since the underlying space is non-atomic, for every probability measure (or for ), there exists such that . Using the law invariance of , the functional given by

| (8) |

is well defined and it inherits the properties listed in Definition 1 from . A similar procedure has been considered by (Frittelli & Maggis, 2018), although with a totally different aim. We stress some key consequences.

Proposition 2.6.

Proof.

The equality (9) is simply Corollary 2.2. The first equality in (10) is given by definition of in (8) and the fact that any satisfies , thanks to the Lipschitz continuity. The last equality in (10) does not immediately follow from Corollary 2.2, since we do not know if is non-atomic. The inequality is clear. Using (8), we can rewrite

which concludes the proof of the equality chain in (9), (10). The last statement follows from (8).

∎

Remark 1.

The second equality in (10) holds, more generally, if we replace with an arbitrary . Indeed, since the space is non atomic, is the law of some . For such a it also holds that .

We next introduce the class of neural networks that we intend to use.

Definition 3.

Let , with , let an activation function and for any , let an affine function. A (feed-forward) neural network is a function defined as

where the activation function is applied componentwise.

We denote by the vector space generated by the class of neural networks from determined by a fixed activation function , continuous, nonconstant and bounded. Notice that is a vector subspace of , and is, in particular, a convex cone. Moreover, imposing in the above definition, contains the functions generated by only one hidden layer and only one output unit as considered in (Hornik, 1991). A simple argument based on the classical UAT of (Hornik, 1991) (Theorem 1) yields the approximation result that we need, at least for the case . The case is not covered by this theorem and we need a slightly different approach.

Theorem 2.7.

Let be continuous, bounded, and nonconstant. Then is norm dense in for any finite measure and .

The original theorem is stated for networks with two layers (). Since contains this particular class, the density result also holds as stated in Theorem 2.7. The following is our first approximation result.

Theorem 2.8.

Let . Let be law-invariant convex risk measures. Then,

| (11) |

Proof.

Let . Let be the law of under . We claim that

Indeed, from Corollary 2.2, attains the minimum over the set of allocations with . Since , for every , the first equality follows. The second equality is by (8). Notice now that and are law-invariant convex risk measures, which are -continuous by the Extended Namioka-Klee Theorem in (Biagini & Frittelli, 2010). From Theorem 2.7, applied with , we have

which in turns yields, by norm continuity, that (11) holds. ∎

The UAT does not provide uniform approximations and, in particular, it does not cover the case. We use here an approach based on weighted spaces in order to obtain Theorem 2.10, which is inspired by the forthcoming paper (Cuchiero et al., 2023). This theorem is only instrumental for our main results and it is certainly not the first time that the theory of weighted spaces has been exploited in Universal Approximation results (see for example (Kratsios, 2021; Cuchiero et al., 2023) and the references therein). We will also add a short proof for the sake of completeness. Let be a continuous function with compact sublevels and define

The space is a Banach lattice when endowed with the norm . This can be easily verified following verbatim the argument for the standard case of bounded continuous functions with the supremum norm. We introduce the following sets:

Proposition 2.9.

is a Banach space and for every continuous linear functional there exists a unique such that . Conversely, every defines a continuous linear functional in in the same way.

Proof.

This follows from (Dörsek & Teichmann, 2010), see Theorem 2.4 and Theorem 2.7. ∎

Theorem 2.10.

Let be continuous, bounded, and non-constant. Let be a fixed integer and take . Then the family in Definition 3 is -dense in .

Proof.

As commented above, it is enough to prove the result for networks with two layers. By (Hornik, 1991, Theorem 5), is discriminatory, meaning that for any we have

Let be the weak closure of in with respect to the topology , where the pairing is given by the integration and is well defined from Proposition 2.9. Recall that, for a cone , is called the polar cone of . Since is discriminatory, . By the bipolar theorem, we have . Since in Definition 3 is convex, we have , the latter being the -closure of . This proves that , as desired. ∎

The following is our second general approximation result.

Theorem 2.11.

Let be law-invariant convex risk measures. Then,

| (12) |

Proof.

Let and its law under . From Proposition 2.6, we can rewrite

Note that for with . We thus deduce,

where in the second inequality we have used that has compact support and is continuous, whereas, in the third inequality we used again the law invariance. Finally, the last equality is a consequence of Proposition 2.6. This shows that all the above inequalities are actually equalities. From Theorem 2.10, , so that

We conclude using the continuity of with respect to the uniform convergence. ∎

Remark 2.

Note that if we replace with and , the same arguments with the choice of yields that (12) holds for every . The proof presented for Theorem 2.8 is however more direct and it does not require extra integrability on . The advantage of the approach of Theorem 2.11 is that the extra equality

shows that the elements in the closure are approximated by the neural networks uniformly also for the case of .

3 Convergence results

Let , for some . Consider an i.i.d. sequence with common distribution and let denote the corresponding sequence of empirical cumulative distribution functions: for , is defined as

Denote by the random measure associated to the empirical c.d.f. , namely

| (13) |

Finally, for , let be the -Wasserstein distance on induced by the Euclidean norm, namely,

We refer to the book (Villani, 2009) for a thorough presentation of the topic.

Lemma 3.1.

Let and . Then , -a.s., where denotes the weak convergence of probability measures. If , it holds additionally

Proof.

The first statement follows from the Glivenko-Cantelli theorem. As for the second statement, Theorem 6.9 in (Villani, 2009) shows that convergence in is equivalent to together with the convergence of the -th moments. The latter follows from the law of large numbers and the integrability of , so that, . ∎

We aim at proving the convergence of the optimal values, namely,

| (14) |

and the convergence of the corresponding minimizers. We will need to establish some joint continuity results for the map , defined in (8), on the spaces and . Some preliminary topological considerations are useful.

Remark 3.

The space is used for the case. Indeed, for and an i.i.d. sequence with common law , we obviously have -a.s.. Thus, the measure satisfies for -a.e. and for .

We endow with the -topology, for and with the weak topology. We endow with the topology induced by the metric:

| (15) |

One can verify that is a complete metric space and metrizes the uniform convergence on compact sets. As a consequence of the Ascoli-Arzelà theorem, we have that is compact with respect to the topology induced by , as we prove next.

Lemma 3.2.

Let be a sequence in . There exists and a subsequence such that .

Proof.

Recall that for every , . In particular, for every , any family of functions in , restricted to , is equicontinuous and equibounded. We first construct a sequence of functions in the following iterative way. For we apply the Ascoli-Arzelà theorem to restricted to . This yields a subsequence, that we relabel again as , and a continuous function on such that converges uniformly to on . Note that is continuous on , being uniform limit of continuous functions, and satisfies , since and for any . At the step we repeat the same argument to the sequence obtained at step . Note that the limiting function satisfies on , since converges uniformly to on . Similarly as above, is continuous on and satisfies .

We are now able to construct the limiting . For every , we extend to in an arbitrary way outside . We set , for every and note that coincides with on every . In particular, we deduce that .

Finally, we construct the convergent subsequence of the original sequence. From the Ascoli-Arzelà argument above, for every, , there exists such that

For every and , using that on , we obtain

which implies the uniform convergence of the subsequence to on every interval . An application of Dominated Convergence Theorem then yields

∎

We state now our main convergence result. We need the following functional, which is an almost sure version of the distance . For a measure on and , -measurable functions,

| (16) |

where in the above -norm we made explicit the dependence on the reference measure in order to avoid ambiguity in what follows.

Theorem 3.3.

Let . Let be law-invariant convex risk measures. Suppose that is strictly convex in the sense of (7). Only in the case of suppose that and satisfy the Lebesgue property. Then,

Furthermore, let and be optimal allocations in , corresponding to and respectively. Then,

The rest of the section is devoted to the proof of this theorem. We will need a number of auxiliary results, which are of independent interest. The first result is essentially (Delbaen, 2021, Proposition 1) or (Shapiro, 2013, Theorem 2.1), adapted to our context.

Lemma 3.4.

Consider again a generic atomless probability space .

-

1.

Let . Suppose and . Then, there exists a sequence in and such that for every , and .

-

2.

Let . Suppose and . Then there exists a sequence in and such that for every , , -a.s. and .

Proof.

For every , by the Skorokhod Theorem (as in (Billingsley, 1999, Theorem 25.6)), there exist random variables such that , for every and -a.s. For item 2, it is enough to additionally note that .

As for item 1, by the characterization of -convergence in (Villani, 2009, Theorem 6.9), we have

Now we proceed as in (Delbaen, 2021) Proposition 1: by Scheffé’s lemma we conclude that converges in to . Hence is a uniformly integrable sequence. Indeed,

Since converges to zero -a.s., the proof is complete. ∎

Proposition 3.5.

Let and be a law-invariant convex risk measure. For the map of (8) is continuous on . If, on the other hand and additionally satisfies the Lebesgue property on , then is continuous on , for every .

Proof.

We start covering the case . Since is a metric space, we check continuity along sequences. Take a convergent sequence in . Take any subsequence. We prove that it admits a further subsequence for which , which yields the convergence of the original sequence. The first extracted subsequence will be relabelled with the index . Since , we can apply Lemma 3.4. Since

up to taking a further subsequence (and relabeling again with ) we might suppose that there exists a with , -a.s. By Dominated Convergence Theorem, since -a.s., we get

Now, since is real-valued, hence norm continuous by Extended Namioka-Klee Theorem, we deduce

| (17) |

and the desired continuity follows.

For the second statement, the argument is very similar. Take a convergent sequence in . Take any subsequence. We prove that it admits a further subsequence for which . Use Lemma 3.4 item 2 to obtain the sequence . Since , we have which is finite by Lemma 3.4 item 2. Since converges to uniformly on compact intervals by definition, we deduce -a.s. Using the Lebesgue property we conclude that (17) holds true, providing continuity. ∎

Proof of Theorem 3.3.

Consider first the case . We prove something stronger, namely, that the thesis holds for every such that instead of only for and . First, observe that by Proposition 3.5 the function

is continuous on , and is compact by Lemma 3.2. Berge’s Theorem (see (Aliprantis & Border, 2006) Theorem 17.31) guarantees that

and that the correspondence defined by

is upper hemicontinuous. Consider now the numerical sequence . Take an arbitrary subsequence and relabeled it again by . Using the upper hemicontinuity of (see (Aliprantis & Border, 2006) Theorem 17.20) and the convergence of to , the sequence has a limit point in , that we call . Up to passing to a further subsequence and relabeling, we may assume that converges to with respect to the distance . By definition of , induces an optimal allocation under and for with we get, and using Proposition 2.6,

Since is strictly convex, the minimizer is unique by Proposition 2.3 (recall that we fixed 222As a consequence of translation invariance, we can assume, without loss of generality, that gives positive mass to every neighborhood of . Then, given two optimal allocations , Proposition 2.3 implies that -a.s., for some . However, the definition of necessarily implies .). Thus, , or equivalently . The latter -a.s. equality property yields . Note now that, by construction, . We conclude that

We have shown that starting from an arbitrary subsequence of there exists a further subsequence converging to . This shows the desired property. For the case , the argument is exactly the same. Note only that for applying Proposition 3.5 we need to require the Lebesgue continuity.

The claims in the statement follow now from Lemma 3.1. ∎

The case of spectral risk measures

The convergence (14) can be established in the context of spectral risk measures by proving a stronger result.

Definition 4.

Let . A functional is called a spectral risk measure if

| (18) |

for some non-increasing function , called spectral density, satisfying .

We refer to (Pichler, 2013a, b) for a thorough analysis of the topic. In particular, the properties of ensure that is convex, monotone, and cash additive. Moreover, due to the properties of , is also law invariant and positive homogeneous. Whenever and are both finite spectral risk measures on , (which is the case for suitably integrable spectral densities as shown in (Pichler, 2013b, Proposition 5 and Theorem 11)), Assumption 2.5 is thus satisfied. For , and also satisfy the Lebesgue property if the spectral densities are such that and are well defined and finite on for some big enough, by the Extended Namioka-Klee Theorem. This translates into an integrability requirement on , see (Pichler, 2013b, Proposition 5 and Theorem 11), and holds true for example if are bounded themselves. In both cases, we are in the exact setup of Theorem 3.3. However, we can provide an explicit estimate for the convergence (14), as detailed below.

Proposition 3.6.

Let and be law-invariant spectral convex risk measures, with possibly different spectral densities . Then,

| (19) |

In particular, (14) holds.

4 Numerical experiments

In this section, we illustrate the results of a number of numerical experiments that showcase the usefulness of the approximation developed in Section 2. We first test our findings in the case of entropic risk measures and expected shortfall, where simple explicit formulas for the optimal allocations and for the value of the inf-convolutions are known. We then consider the more complex case of distortion risk measures and, to conclude, we treat the case of heterogeneous agents adopting risk measures in two different classes, i.e. entropic and distortion-type.

4.1 Description of the framework

We model two agents with reference risk measures and as those in the introduction. For the sake of comparison, we consider a financial position , as it belongs to the domain of each of those risk measures. The objective is to approximate optimal allocations for the inf-convolution of and , which takes the form

To model the functions and , we use two Fully Connected Deep Neural Networks (DNNs) and , respectively. We observe that, while and explicitly parametrize and by design, the functions and are proxies for and respectively.

Let be a sample of of size with its empirical measure. For , we denote by the historical risk measures associated to and , namely, . Since we aim at finding allocations that realize an inf-convolution value as close as possible to , we need to find an appropriate and robust estimate of such a quantity. While we could use the explicit parametrizations of and of and minimize , another valid alternative is to use the implicit parametrizations and minimize . To have a more robust estimate, we use their arithmetic average which leads to the following loss function

| (20) |

and to the following parameterizations of and

Not only these are more robust estimates, but as they sum up to the identity, they provide acceptable allocations by construction. Theorem 3.3 guarantees the convergence of the induced optimal allocations for the risk-sharing problem.

To train the neural networks and obtain the estimators of the theoretical optimum , we minimize (20) with the optimizer Adam (Kingma & Ba, 2015). The precise choices of the learning rate, batch size, the number of training epochs, and other implementation details are reported in the Appendix. To ensure a robust framework, we train the DNNs multiple times and use their average as the final estimate. To be more explicit, we train and for times each starting from a different initialization. We obtain couples of neural networks and use their arithmetic averages

to estimate and , respectively. In all our experiments we chose .

To have a flexible framework, we allow the networks to have three types of different activation functions:

While the non-linear activation functions Tanh and ReLu are standard choices in deep learning, the reason for including the linear one will be apparent below. We incidentally note that, since is bounded, we have no issues in allowing for unbounded activation functions. We report a review of possible methodological and architectural enhancements in Appendix A.1.

To verify the stability and reliability of our framework, we test our results with three different distributions

-

1.

, where is the uniform distribution;

-

2.

, where is the normal distribution;

-

3.

, where is the distribution.

The uniform distribution is the most basic example and it provides an easy setup to test our framework. A more interesting example is the normal distribution because of its well-known financial relevance. We note that in our experiments we restricted to in order to have a distribution with bounded support. Finally, the distribution presents skewness and rare events, modeling the scarcity of data for extreme losses. We chose the opposite of a distribution in order to represent the financially more relevant case of pure losses.

4.2 Initial tests: entropic and expected shortfall case

To begin with, we test our framework in the well-known cases of entropic risk measures and expected shortfalls, for which explicit formulas are known. We start by recalling that, as in Examples 2.8 and 2.9 in (Filipović & Svindland, 2008),

| (21) |

This means that we can directly compute the theoretical value of the inf-convolution and compare it with the value obtained by the DNNs. Additionally, we can calculate the error (under ) between the estimated and and the theoretical ones. As we show below, we found that the values of the inf-convolutions achieved by all our trained networks converge to the theoretical values and that approximates up to a negligible error, for .

-

•

For the entropic case, we chose and which yield the optimal allocation and ;

-

•

For the case, we chose and . It is clear from (21) that and is an optimal allocation.

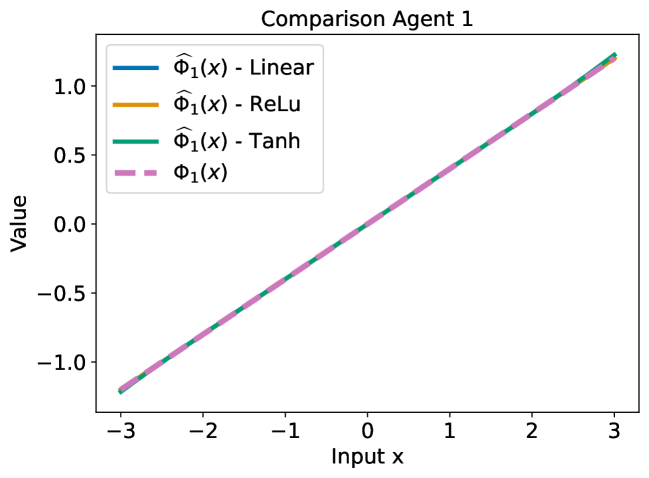

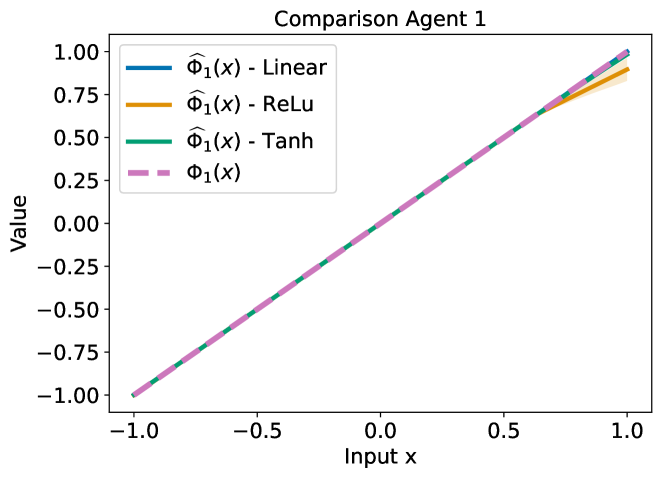

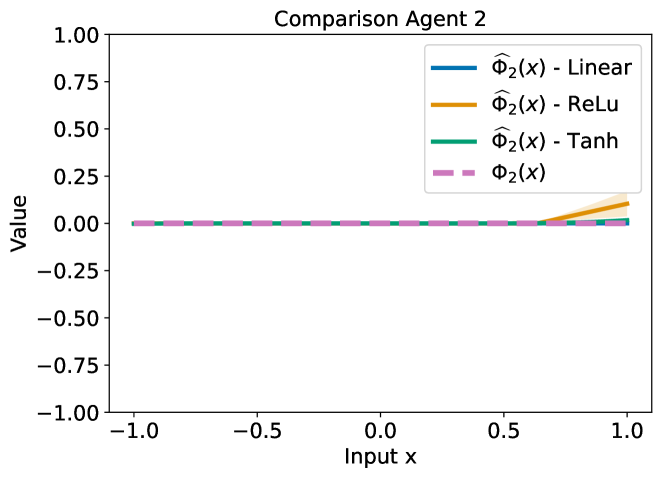

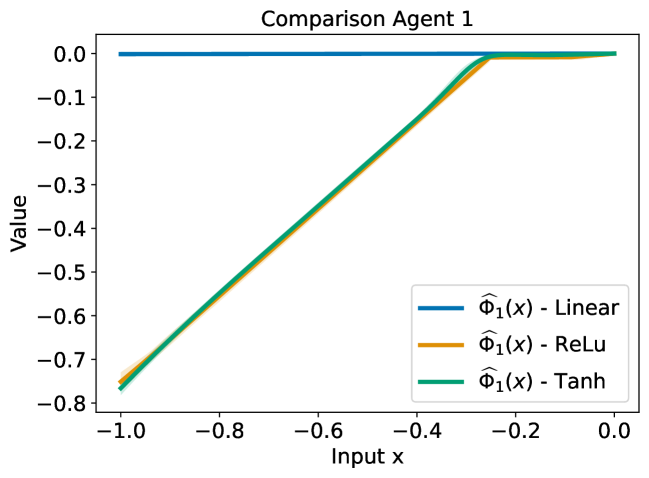

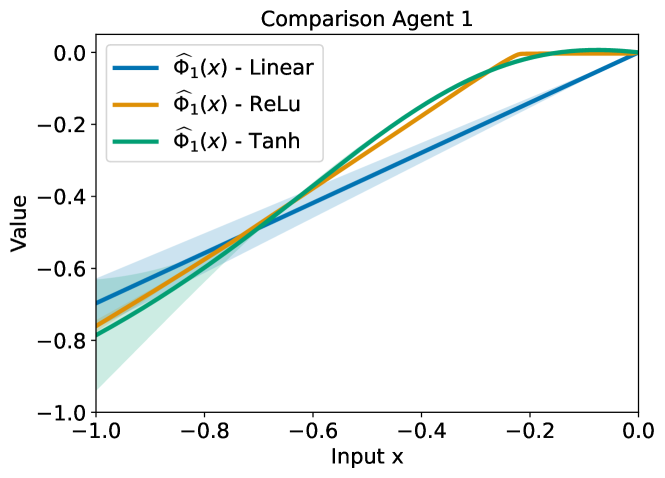

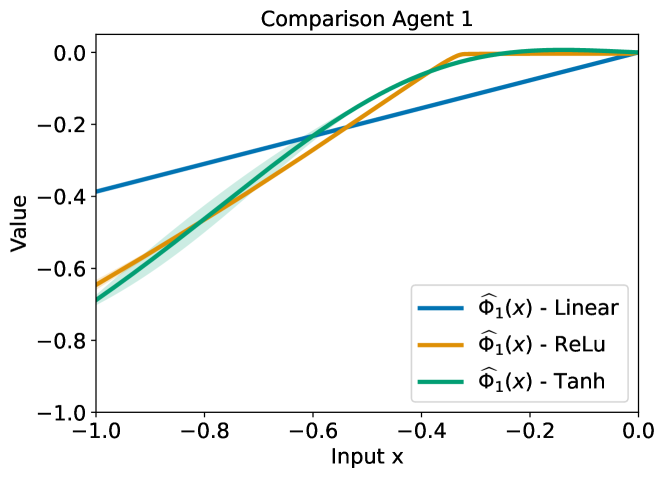

We start by discussing the entropic case. Figure 1 shows the comparison between the theoretical optimal allocations and the average predicted and for the normal distribution case and for the three activation functions. Every trained DNN seems to match perfectly the theoretical allocations. Indeed, we point out that the average predicted allocations in Figure 1 are plotted with their respective standard deviation bands across the networks. In particular, for this case, we notice that the uncertainty bands are invisible as they are almost null.

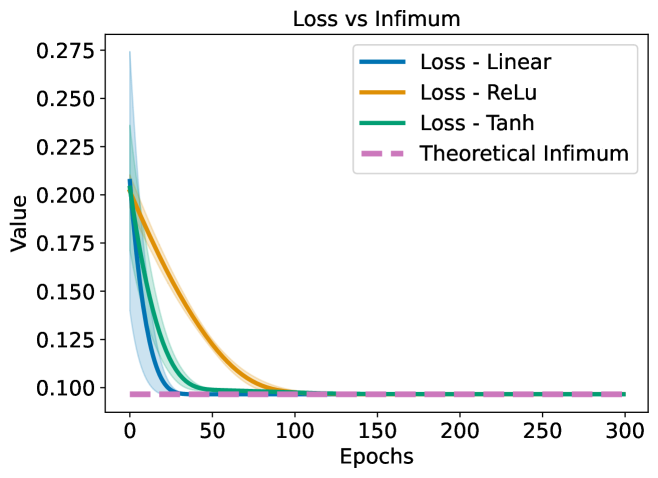

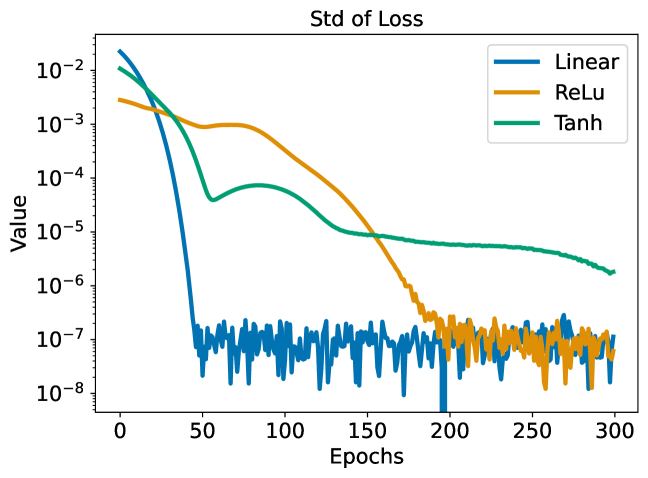

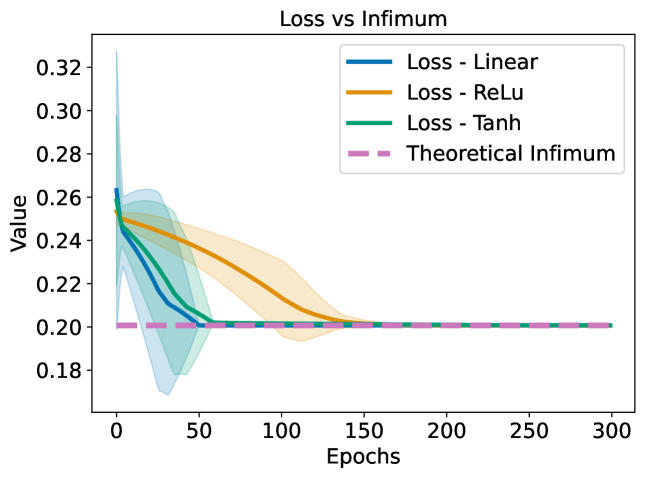

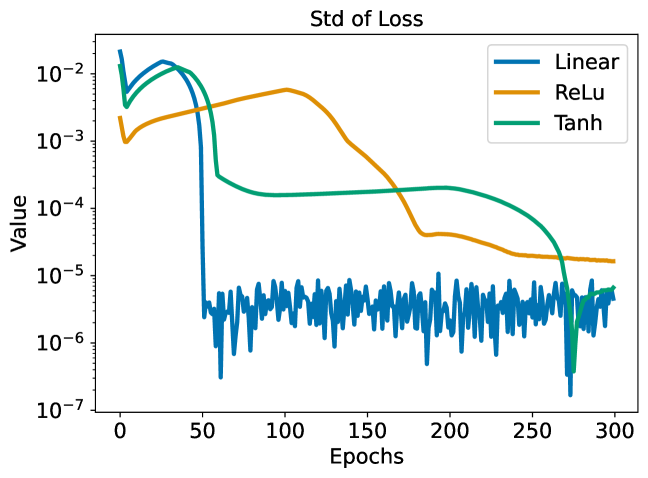

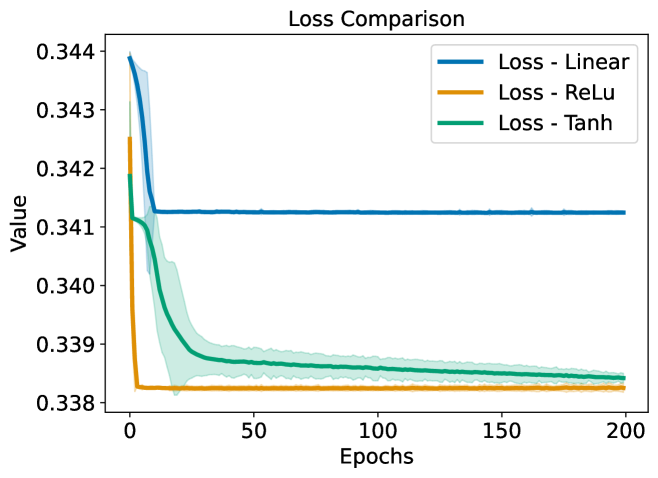

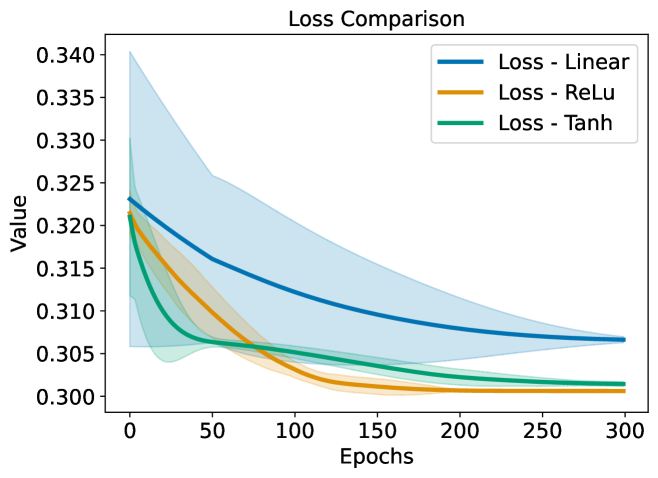

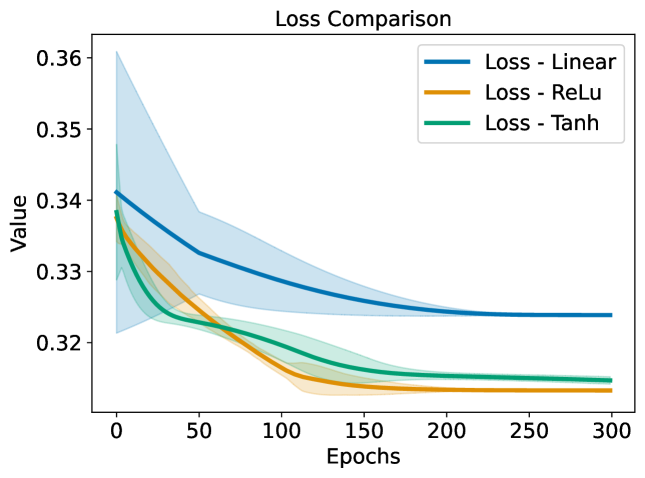

In Figure 2(a), we show the comparison between the average loss functions, along with the respective standard deviation shaded band, and the theoretical infimum calculated using (21). All three types of NNs achieve a loss that is close to the theoretical value of the inf-convolution, up to a negligible error. In Figure 2(b), for each model, we plot the standard deviation of the loss function (20). Since the variance of the three losses is decreasing, we are observing a stable convergence.

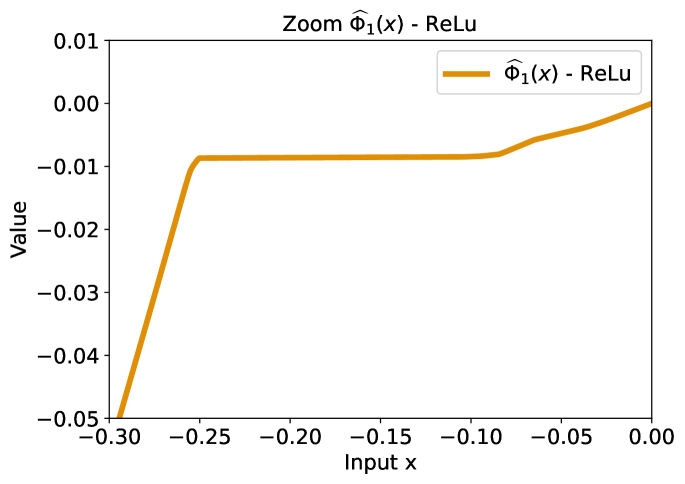

Table 1 collects the data regarding the errors for the experiment with the standard normal distribution. We computed the average relative error with respect to the theoretical infimum, together with its standard deviation, and the error of with respect to the theoretical . Table 6 reports the same figures also for the cases of uniform and distributions. We observe that the errors are all close to zero, meaning that all our NNs reached convergence and they exhibited low uncertainty, which is an indication of stable learning. Observe that for the entropic case (as well as for ) the optimal allocation is a linear function, therefore, it belongs to the span of the linear-activated DNN. We thus expect the linear activation to achieve the best performance. As we can appreciate in Table 1, this result is confirmed by our experiments. Additionally, we notice that also ReLu and Tanh are providing satisfactory performances.

| Entropic case - - Infimum = | |||

|---|---|---|---|

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

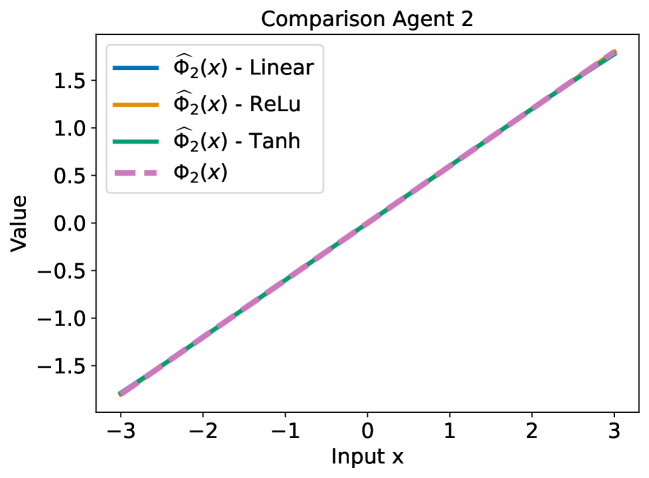

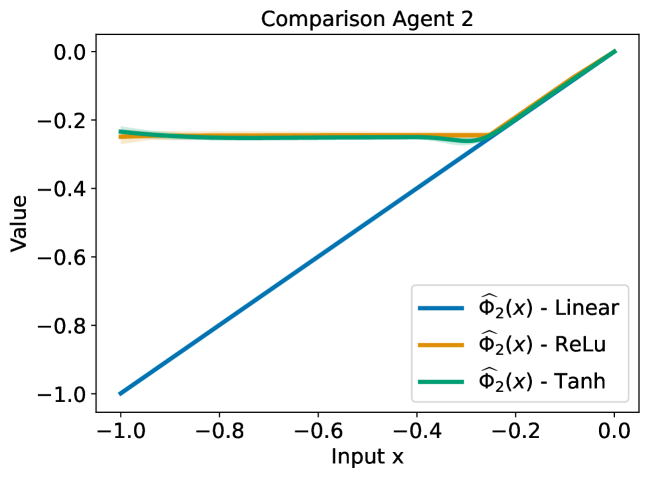

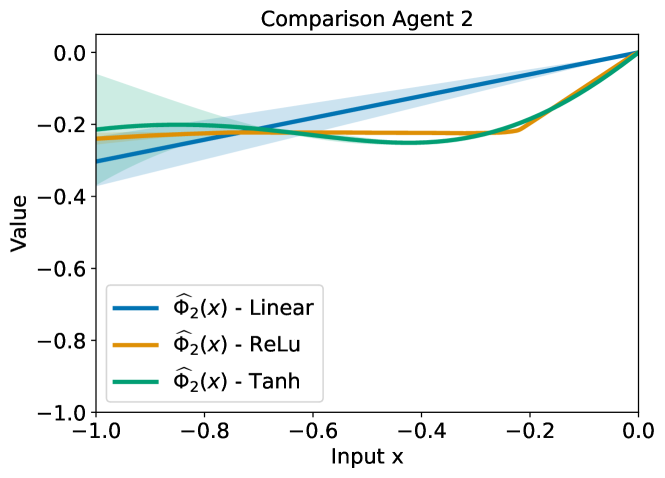

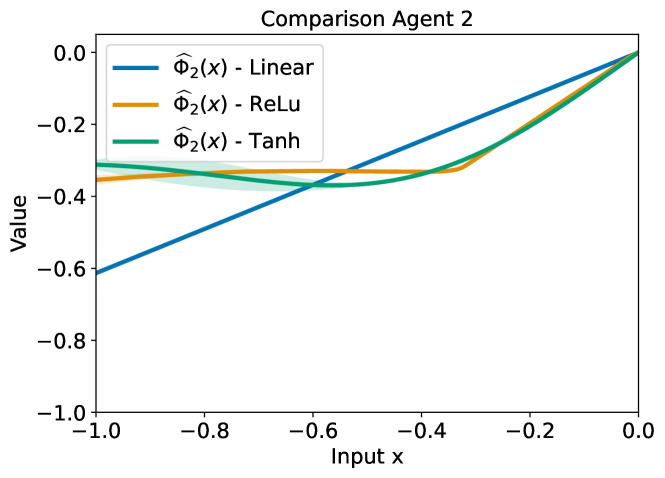

Similar considerations apply to the case of and we obtain qualitatively and quantitatively the same results. As an example, in Figure 3 we show the results for the uniform distribution case. Regarding the convergence analysis, we observe in Figure 4 that all three types of NNs achieve a loss that is only marginally distant from the theoretical value of the inf-convolution. Additionally, we notice that the convergence to such a value takes place with decreasing variance of the losses, indicating a stable convergence. In Figure 3 we present the comparison between the average predicted and , along with their respective standard deviation shaded band, and the theoretical optimal allocations for the uniform distribution case. A consideration, which is specific to the case, is now due. The optimal allocation is of the form and , and the DNN needs to learn the constant function in the latter case. Consistently with the known fact that using nonlinear functions for the (unsupervised) learning of constant functions is a challenging task, we find that ReLu and Tanh underperform with respect to the linear DNN.

In Table 2, we finally present the average relative error with respect to the theoretical infimum, its standard deviation, and error of with respect to . Table 7 reports the same figures also for the case of normal and distributions.

| Expected Shortfall - - Infimum = | |||

|---|---|---|---|

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

4.3 Convolution of distortion risk measures

We here consider the case where both and are distortion risk measures, as in (3), with respect to some discrete probabilities , . Let , be two given integers, and consider the risk measures

where with and for and for . Some semi-explicit expressions of the optimal allocations are known for this case, in particular, an optimal allocation can be found as a linear combination of ReLu functions, possibly composed with translation maps — see Example 3.1 in (Jouini et al., 2008) and also Appendix A of (Embrechts et al., 2018) for a more general case333We thank an anonymous referee for pointing out this fact.. Hence, we expect the ReLu-activated DNN to achieve the best performance.

Differently from the entropic and cases, the problem has a non-linear solution and we expect the linear-activated DNN to perform poorly. Nevertheless, for the sake of consistency in our tests, we included the linear activation in all experiments. As an example, we chose

Figure 5 shows the average predicted and for the case of the distribution and for the three activation functions. As we can observe, the DNNs trained with non-linear activation functions agree on the shape of the solution, whereas the linear-activated one is clearly different.

As anticipated before, we expect the optimal allocations to be linear combinations of ReLu activations. Consistently with the theory, if we look at the average predicted for the case of ReLu, as in Figure 6(b), we observe that such expected behavior is captured. Figure 6(a) shows the average loss functions as a function of the training epochs. First of all, we notice that the linear NN achieves a loss level that is sensibly larger than those achieved by the ReLu and the Tanh DNNs, confirming the expectations of it poor performance. Secondly, we notice that the loss decreases with decreasing variance, indicating a stable convergence with low uncertainty in all three cases.

Finally, in Table 3, we present the average achieved losses, together with the uncertainty of their estimates, for all activation functions and for all distributions. In line with the theoretical predictions, the DNN activated with a ReLu function is the one performing best in terms of average loss: all three loss values are, by construction, greater or equal to the theoretical infimum, and the best performance is understood in the sense of achieving the lowest value. The Tanh-activated DNN is comparably reliable. From Table 3, we can see that in some cases the linear-activated DNN shows the most stable convergence, namely the lowest standard deviation of losses. However, it converges to a loss value that is significantly higher than the other two. This is not unexpected since, by design, the linear-activated DNN is unable to represent a nonlinear function and, therefore, exhibits poorer performances.

| Distortion Measure - | ||

|---|---|---|

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Distortion risk measures - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Distortion Measure - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

4.4 Heterogeneous agents

In our last experiments, we consider two heterogeneous agents, in the sense that one adopts an entropic risk measure while the other one opts for a distortion-type risk measure. In the first of such experiments, the risk measures are

| (22) |

From (Jouini et al., 2008) Proposition 3.2 or (Rüschendorf, 2013) Theorem 11.22, the optimal allocation is known to be induced by for some (non-explicit) constant . In line with the previous subsections, we show an example of the average predicted and . In Figure 7, we plot the predicted allocations for the distribution, for the three different activation functions. Once again, we expect the solution to be non-linear and we can observe that the optimal allocations found by ReLu and Tanh-activated DNNs are comparable, whereas the one found by the linear-activated DNN differs significantly. In Figure 8(b) we isolated the allocation found by the ReLu DNN which, as we will see below, is the one that performed best. We notice that the desired behavior of the optimal allocations is well-captured.

Figure 8(a) shows the average loss functions as a function of the training epochs, together with their uncertainty-shaded bands. We notice that all networks exhibit stable convergence. However, the linear-activated network achieves a loss level that is sensibly larger than those achieved by the ReLu and Tanh-activated ones. From the picture, it is already clear that Relu is the one performing best in this case. This is confirmed by the data that we collect in Table 4, namely, the average achieved loss together with the uncertainty of their estimates. Nevertheless, we note that while the Tanh NN underperforms with respect to the ReLu one, it provides comparable performances.

| Case Eq. (22) - | ||

|---|---|---|

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Case Eq. (22) - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Case Eq. (22) - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

In our last experiment, we consider a case where, to the best of our knowledge, no theoretical information is available. Again, we consider two heterogeneous agents, the first one opting for a distortion risk measure, and the second one adopting an entropic risk measure. More precisely, the risk measures are

| (23) |

In Figure 9 we plot the average predicted and for the beta distribution, for the three different activation functions. As in the cases in Section 4.3 and in the previous heterogeneous case, we anticipate a non-linear behavior, which translates into linear activated DNNs underperforming significantly. We can observe that the optimal allocations found by ReLu and Tanh-activated DNNs are comparable. In Figure 10 we isolated the allocation found by the ReLu DNN which, as in the previous heterogeneous case of Section 4.4, is the one that performed best, which is confirmed by Table 5.

| Case Eq. (23) - | ||

|---|---|---|

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Case Eq. (23) - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

| Case Eq. (23) - | ||

| Avg. Loss | Std. Loss | |

| Linear | ||

| ReLu | ||

| Tanh | ||

All networks exhibit stable convergence. Still, as expected, the linear-activated DNN achieves a far larger loss level. The Tanh NN underperforms with respect to the ReLu one, yet still provides comparable performances.

References

- Acciaio (2007) Acciaio, B. Optimal risk sharing with non-monotone monetary functionals. Finance Stoch., 11(2):267–289, 2007.

- Aliprantis & Border (2006) Aliprantis, C. D. and Border, K. C. Infinite Dimensional Analysis: a Hitchhiker’s Guide. Springer, Berlin; London, 2006.

- Barrieu & El Karoui (2005) Barrieu, P. and El Karoui, N. Inf-convolution of risk measures and optimal risk transfer. Finance Stoch., 9(2):269–298, 2005.

- Biagini & Frittelli (2010) Biagini, S. and Frittelli, M. On the Extension of the Namioka-Klee Theorem and on the Fatou Property for Risk Measures, pp. 1–28. Springer Berlin Heidelberg, Berlin, Heidelberg, 2010.

- Billingsley (1999) Billingsley, P. Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999.

- Brown et al. (2020) Brown, T., Mann, B., Ryder, N., Subbiah, M., Kaplan, J. D., Dhariwal, P., Neelakantan, A., Shyam, P., Sastry, G., Askell, A., et al. Language models are few-shot learners. Advances in neural information processing systems, 33:1877–1901, 2020.

- Carlier & Dana (2013) Carlier, G. and Dana, R.-A. Pareto optima and equilibria when preferences are incompletely known. J. Econom. Theory, 148(4):1606–1623, 2013.

- Carlier et al. (2012) Carlier, G., Dana, R.-A., and Galichon, A. Pareto efficiency for the concave order and multivariate comonotonicity. J. Econom. Theory, 147(1):207–229, 2012.

- Clevert et al. (2016) Clevert, D.-A., Unterthiner, T., and Hochreiter, S. Fast and accurate deep network learning by exponential linear units (elus). ICLR 2016, 2016.

- Compagnoni et al. (2023a) Compagnoni, E. M., Orvieto, A., Biggio, L., Kersting, H., Proske, F. N., and Lucchi, A. An sde for modeling sam: Theory and insights. ICML 2023, 2023a.

- Compagnoni et al. (2023b) Compagnoni, E. M., Scampicchio, A., Biggio, L., Orvieto, A., Hofmann, T., and Teichmann, J. On the effectiveness of randomized signatures as reservoir for learning rough dynamics. IJCNN 2023, 2023b.

- Cont et al. (2010) Cont, R., Deguest, R., and Scandolo, G. Robustness and sensitivity analysis of risk measurement procedures. Quant. Finance, 10(6):593–606, 2010.

- Cuchiero et al. (2023) Cuchiero, C., Schmocker, P., and Teichmann, J. Global universal approximation of functional input maps on weighted spaces. arXiv preprint arXiv:2306.03303, 2023.

- Dana & Le Van (2010) Dana, R. A. and Le Van, C. Overlapping sets of priors and the existence of efficient allocations and equilibria for risk measures. Math. Finance, 20(3):327–339, 2010.

- Daniels & Velikova (2010) Daniels, H. and Velikova, M. Monotone and partially monotone neural networks. IEEE Transactions on Neural Networks, 21(6):906–917, 2010.

- Delbaen (2021) Delbaen, f. Law of large numbers for risk measures. Preprint: arXiv:2109.10612v1, 2021.

- Dörsek & Teichmann (2010) Dörsek, P. and Teichmann, J. A semigroup point of view on splitting schemes for stochastic (partial) differential equations. arXiv preprint arXiv:1011.2651, 2010.

- Embrechts et al. (2018) Embrechts, P., Liu, H., and Wang, R. Quantile-based risk sharing. Oper. Res., 66(4):936–949, 2018.

- Embrechts et al. (2020) Embrechts, P., Liu, H., Mao, T., and Wang, R. Quantile-based risk sharing with heterogeneous beliefs. Math. Program., 181(2, Ser. B):319–347, 2020.

- Filipović & Svindland (2008) Filipović, D. and Svindland, G. Optimal capital and risk allocations for law- and cash-invariant convex functions. Finance Stoch., 12(3):423–439, 2008.

- Föllmer & Schied (2016) Föllmer, H. and Schied, A. Stochastic Finance. An introduction in discrete time. De Gruyter Graduate. De Gruyter, Berlin, fourth revised and extended edition, 2016.

- Frittelli & Maggis (2018) Frittelli, M. and Maggis, M. Disentangling price, risk and model risk: V&r measures. Mathematics and Financial Economics, 12(2):219–247, 2018.

- Heath & Ku (2004) Heath, D. and Ku, H. Pareto equilibria with coherent measures of risk. Math. Finance, 14(2):163–172, 2004.

- Hendrycks & Gimpel (2016) Hendrycks, D. and Gimpel, K. Gaussian error linear units (gelus). arXiv preprint arXiv:1606.08415, 2016.

- Hornik (1991) Hornik, K. Approximation capabilities of multilayer feedforward networks. Neural Networks, 4(2):251–257, 1991.

- Jouini et al. (2008) Jouini, E., Schachermayer, W., and Touzi, N. Optimal risk sharing for law invariant monetary utility functions. Math. Finance, 18(2):269–292, 2008.

- Kailath & Weinert (1975) Kailath, T. and Weinert, H. An rkhs approach to detection and estimation problems–ii: Gaussian signal detection. IEEE Transactions on Information Theory, 21(1):15–23, 1975.

- Kingma & Ba (2015) Kingma, D. P. and Ba, J. Adam: A method for stochastic optimization. ICLR 2015, 2015.

- Kratsios (2021) Kratsios, A. The universal approximation property: characterization, construction, representation, and existence. Ann. Math. Artif. Intell., 89(5-6):435–469, 2021.

- Liebrich & Svindland (2019) Liebrich, F.-B. and Svindland, G. Risk sharing for capital requirements with multidimensional security markets. Finance Stoch., 23(4):925–973, 2019.

- Liu et al. (2020) Liu, X., Han, X., Zhang, N., and Liu, Q. Certified monotonic neural networks. Advances in Neural Information Processing Systems, 33:15427–15438, 2020.

- Mastrogiacomo & Rosazza Gianin (2015) Mastrogiacomo, E. and Rosazza Gianin, E. Pareto optimal allocations and optimal risk sharing for quasiconvex risk measures. Math. Financ. Econ., 9(2):149–167, 2015.

- Pichler (2013a) Pichler, A. Evaluations of risk measures for different probability measures. SIAM J. Optim., 23(1):530–551, 2013a.

- Pichler (2013b) Pichler, A. The natural Banach space for version independent risk measures. Insurance Math. Econom., 53(2):405–415, 2013b.

- Rahimi & Recht (2007) Rahimi, A. and Recht, B. Random features for large-scale kernel machines. In Platt, J., Koller, D., Singer, Y., and Roweis, S. (eds.), Advances in Neural Information Processing Systems, volume 20. Curran Associates, Inc., 2007.

- Rahimi & Recht (2008) Rahimi, A. and Recht, B. Uniform approximation of functions with random bases. In 2008 46th annual allerton conference on communication, control, and computing, pp. 555–561. IEEE, 2008.

- Rüschendorf (2013) Rüschendorf, L. Mathematical risk analysis. Springer Series in Operations Research and Financial Engineering. Springer, Heidelberg, 2013. Dependence, risk bounds, optimal allocations and portfolios.

- Schölkopf & Smola (2018) Schölkopf, B. and Smola, A. J. Learning with kernels: support vector machines, regularization, optimization, and beyond. MIT press, 2018.

- Schölkopf et al. (2015) Schölkopf, B., Muandet, K., Fukumizu, K., Harmeling, S., and Peters, J. Computing functions of random variables via reproducing kernel hilbert space representations. Statistics and Computing, 25:755–766, 2015.

- Shapiro (2013) Shapiro, A. Consistency of sample estimates of risk averse stochastic programs. Journal of Applied Probability, 50(2):533–541, 2013.

- Svindland (2010) Svindland, G. Continuity properties of law-invariant (quasi-)convex risk functions on . Math. Financ. Econ., 3(1):39–43, 2010.

- Theodoridis & Koutroumbas (2006) Theodoridis, S. and Koutroumbas, K. Pattern recognition. Elsevier, 2006.

- Tsanakas (2009) Tsanakas, A. To split or not to split: capital allocation with convex risk measures. Insurance Math. Econom., 44(2):268–277, 2009.

- Villani (2009) Villani, C. Optimal Transport: Old and New, volume 338 of Grundlehren der Mathematischen Wissenschaften Fundamental Principles of Mathematical Sciences. Springer-Verlag, Berlin, 2009.

- Weber (2018) Weber, S. Solvency II, or how to sweep the downside risk under the carpet. Insurance Math. Econom., 82:191–200, 2018.

- Wen et al. (2023) Wen, K., Ma, T., and Li, Z. How sharpness-aware minimization minimizes sharpness? In ICLR 2023, 2023.

Appendix A Implementation details and additional experimental results

All code is implemented in Python and the Deep Learning library used is PyTorch. In each experiment, the dataset is of size , while the batch size is . All the neural networks have hidden layers of neurons each and have been optimized with Adam. More precisely, the learning rate is while all other settings of Adam are as per default setting. We remind that it is a very well-known result of convex optimization that the learning rate has to be smaller than twice the inverse of the largest eigenvalue of the loss function for Gradient Descent to converge. In practice, this is a valuable indication also in nonconvex optimization. Even if our choice for the learning rate might seem unusual, such a low value was necessary for our experiments, as we observed that higher ones would lead to instability in the optimization process. This is oftentimes an indication that the optimization problem at hand is rather nonlinear and the loss landscape is irregular, together with its derivatives. To make the convergence even more stable, we used the ReduceLROnPlateau scheduler for the learning rate, with patience equal to and threshold equal to , while all other parameters are as per default specification. Finally, all experiments have been run for a number of epochs equal to , apart from those for the Distortion Measures where the number of epochs is . The optimal hyperparameters are the result of fine-tuning via extensive grid search.

We finally complete the exposition of the numerical results for the entropic risk measure and expected shortfall experiments. Table 6 and 7 contain the average relative error with respect to the theoretical infimum, together with its standard deviation, and the error of with respect to the theoretical for all distributions and activation functions.

In our experiments, we observe that both ReLu and Tanh activation functions performed well in all cases, even when the solution was known to be linear. ReLu seemed to perform better in most of the cases. This is due to the fact that in some cases the semi-explicit solution has a piecewise linear behavior.

A.1 Possible Enhancements

The deep learning literature offers a variety of architectural and methodological enhancements that could be used to further push the results that we obtained.

One could include several other activation functions, such as GELU (Hendrycks & Gimpel, 2016) or ELU which obtained recent success in NLP (Brown et al., 2020) and Image Classification (Clevert et al., 2016), respectively. Similarly, one could try different optimizers which may converge to more stable regions of the loss landscape. For example, recent optimizers that found great success in NLP and Computer Vision are SAM and its variants. As detailed in (Wen et al., 2023) and (Compagnoni et al., 2023a), this class of optimizers drives the dynamics towards flatter regions of the landscapes which result in provenly more stable DNNs. Other possibilities include standard techniques such as Batch Normalization and Residual Connections which are proven to stabilize the optimization process.

Finally, since the functions we are learning are monotonic, an interesting approach, suggested by an anonymous referee, would be to enforce the monotonicity of the approximating functions. This could be attained by leveraging specific network structures such as in (Daniels & Velikova, 2010) or suitable penalization terms (Liu et al., 2020). While all our experiments reached convergence without the need of imposing monotonicity, this might be necessary in other cases where convergence is more elusive. As a side note, we remark that not enforcing a priori monotonicity allows for a further sanity check in the experiments, as we can check if the monotone behavior of the optima is learned without any external enforcement.

It is worth noting that, for all the architectural changes that would alter the DNNs, one should of course provide the proof of suitable versions of the Theorems 2.8, 2.11 and Theorem 3.3 for this very specific class of NNs. Since our experiments already achieved satisfactory results, there is no compelling reason to do so at the moment, and we leave these for future research.

| Entropic case - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

| Entropic case - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

| Entropic case - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

| Expected Shortfall - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

| Expected Shortfall - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

| Expected Shortfall - - Infimum = | |||

| Avg. Rel. Error | Std. Rel. Error | Avg. Error | |

| Linear | |||

| ReLu | |||

| Tanh | |||

Appendix B Modeling Alternatives

As suggested by an anonymous referee, there might be other possible ways to successfully model the functions and , for example, using a basis-based approach, such as Random Feature Models, (Rahimi & Recht, 2008) or using Kernel functions (Schölkopf & Smola, 2018).

In the basis-based approach, it is required to fix (or randomly generate) a number of representations of the input and then to linearly combine them to fit the output via a linear layer. These techniques have proven to be effective and computationally cheap in many fields (Rahimi & Recht, 2007). However, the key to their success is a careful design and selection of the (possibly random) features, an operation which is not always straightforward (Compagnoni et al., 2023b). Much differently, DNNs are able to learn and adapt the features during the optimization procedure.

The second approach is based on Reproducing Kernel Hilbert Space (RKHS), also known in the Machine Learning community as kernel methods. This is a very powerful set of techniques that maps the input data into a higher (possibly infinite) dimensional space, in which it is easier to separate data points respect to their native space. These methods found success in many applications (Schölkopf & Smola, 2018) such as in Classification, Signal Detection (Kailath & Weinert, 1975), and Function Emulation (Schölkopf et al., 2015). However, we find that the kernel trick (Theodoridis & Koutroumbas, 2006) at the basis of these methods does not allow us to find a closed-form solution for our problem. Therefore, while this would allow us to face a convex optimization problem, we would still have to rely on an optimizer such as SGD (or Adam) to actually find the unique solution. In this regard, we recall that using RKHS requires calculating the Gramian matrix, which has a complexity of , where is the number of data points. Therefore, even just evaluating the loss function in Eq. (20) has a complexity of , for each training epoch. This cost is additional to the computation of gradients and the update of the parameters in the optimization step, therefore, we expect a much higher computational cost and less scalability of RKHS-based techniques compared to that of DNN. From a theoretical point of view, consistency results for RKHS-based techniques in the literature are only available for the Supervised Learning case and it is not clear if they would be easily adapted to our Unsupervised Learning setting.

To conclude, while many alternatives are present, many of them present criticalities such as higher computational cost and design challenges, that DNNs easily avoid.

Disclosure statement: The authors report there are no competing interests to declare.

Acknowledgements: The authors thank two anonymous referees for precious comments, and F.-B. Liebrich for addressing them to the reference (Shapiro, 2013) and for pointing out the delicate point of the standardness requirements on the underlying probability space.