Efficient Liquidity Providing via Margin Liquidity

Abstract

The limit order book mechanism has been the core trading mechanism of the modern financial market. In the cryptocurrency market, centralized exchanges also adopt this limit order book mechanism and a centralized matching engine dynamically connects the traders to the orders of market makers. Recently, decentralized exchanges have been introduced and received considerable attention in the cryptocurrency community. A decentralized exchange typically adopts an automated market maker, which algorithmically arbitrates the trades between liquidity providers and traders through a pool of crypto assets. Meanwhile, the liquidity of the exchange is the most important factor when traders choose an exchange. However, the amount of liquidity provided by the liquidity providers in decentralized exchanges is insufficient when compared to centralized exchanges. This is because the liquidity providers in decentralized exchanges suffer from the risk of divergence loss inherent to the automated market making system. To this end, we introduce a new concept called margin liquidity and leverage this concept to propose a highly profitable margin liquidity-providing position. Then, we extend this margin liquidity-providing position to a virtual margin liquidity-providing position to alleviate the risk of divergence loss for the liquidity providers and encourage them to provide more liquidity to the pool. Furthermore, we introduce a representative strategy for the margin liquidity-providing position and backtest the strategy with historical data from the BTC/ETH market. Our strategy outperforms a simple holding baseline. We also show that our proposed margin liquidity is 8K times more capital efficient than the concentrated liquidity proposed in Uniswap V3.

Index Terms:

Decentralized finance, Margin liquidity, DEX, CEX, Market maker, Liquidity providerI Introduction

The cryptocurrency market has flourished remarkably over the recent years, with the daily trading volume to market cap ratio reaching higher than the stock market111The global cryptocurrency market cap is $ 1.26T and the daily trading volume in the cryptocurrency market is at $ 65.9B (2022-06-11, Coingecko.com) while the U.S. stock market cap is $43.8T and daily trading volume in the U.S. stock market is $ 534B (2022-06-13, Nasdaqtrader).. At the center of the cryptocurrency market lies centralized exchange (CEX), which adopts the traditional limit order book (LOB) mechanism that provides cryptocurrency trading with a centralized matching engine [24]. Market makers quote prices in a LOB, and the centralized matching engine dynamically connects the traders who want to buy or sell to the orders of market makers in the book, as illustrated in Figure 1(a). On the other hand, a new trading mechanism called automated market makers (AMM) has been proposed with the advent of decentralized exchange (DEX), which provides direct cryptocurrency tradings through the pools of crypto assets instead of the centralized matching engine in CEX [3, 4, 25, 13, 14, 30, 9, 20, 23, 10, 17, 29, 31]. In this paper, we denote a DEX that adopts AMM as DEX-AMM. AMM algorithmically arbitrates the trades between liquidity providers (LPs), who are market makers in DEX, and traders. LPs deposit their assets in the pools operated by AMM and traders swap their assets in the pools. Through the AMM, LPs receive swap fees from traders in return for providing liquidity, as shown in Figure 1(b)[27].

Liquidity in the exchange is one of the most significant factor when traders choose an exchange since traders can trade whenever they want only if the liquidity is sufficient [7, 5]. On the contrary, if the liquidity provided is insufficient, traders might experience an unexpectedly huge price impact or have to wait until a reasonable price comes. Liquidity in DEX-AMM is determined by the amount of liquidity the LPs provide. However, in current DEX-AMMs, the liquidity is not sufficiently provided by the LPs due to the risk of divergence loss inherent to the AMM system [10]. Divergence loss happens when the ratio of tokens deposited in the pool changes. We will describe the details of the divergence loss in Section II-E. To solve this problem, we introduce a new concept of liquidity, margin liquidity, and propose a margin liquidity-providing position that is highly profitable and can be applied to both CEX and DEX-AMM. Then, we extend this margin liquidity-providing position to a virtual margin liquidity-providing position to alleviate the risk of divergence loss of LPs in DEX-AMM and encourage them to provide more liquidity to the pool. Furthermore, we introduce a representative strategy for the margin liquidity-providing position and evaluate the strategy by backtesting it on the historical data of the ETH/BTC market with the Sharpe ratio[21], maximum drawdown (MDD)[22, 28], and the rate of return (ROR)[16]. We also show that our proposed margin liquidity is much more capital efficient than the concentrated liquidity of Uniswap V3 [4].

II Preliminary: Uniswap V2

Uniswap V2 [3] is the most popular DEX-AMM. LPs deposit two tokens in a Uniswap V2 pool and traders exchange a token for the other in the pool. To support this exchange mechanism, Uniswap V2 proposed CPMM (constant product market makers) where the product of the amount of two tokens is constant.

We denote the amount of each token deposited in the Uniswap V2 pool at time as for two exchangeable tokens and . Concretely, CPMM satisfies for all time , where is the conservative constant and denotes the liquidity of the pool. increases when LPs deposit their assets and decreases when LPs withdraw their assets. In Uniswap V2, swap fees distributed to LPs are reinvested, and increases. However, in this paper, we assume swap fees are collected individually as in the Uniswap V3 [4].

II-A LP mechanism: add liquidity and remove liquidity

LPs of the Uniswap V2 pool require a certain ratio of the amount of and to deposit in the Uniswap V2 pool. We call this operation as adding liquidity. When LPs withdraw, they receive and in a certain ratio. We call this operation as removing liquidity.

The ratio of the amount of and LPs deposit or withdraw is the same as the ratio of the amount of and deposited in the Uniswap V2 pool. Concretely, where and are the amount of and an LP deposits or withdraws at time , respectively.

The liquidity of the pool, , increases when an LP deposits of and of . If the ratio of assets deposited by LPs to assets deposited in the pool is , increases to . Concretely,

where .

II-B Exchange mechanism

The exchange ratio is determined by the CPMM mechanism. When traders sell of , of are distributed to LPs in proportion to the amount LPs deposit and of are added on the pool, where is set close to . Then, where is the amount of extracted to the trader. Concretely,

For simplicity, we set in this paper.

II-C Marginal price

The price of the token in Binance, which is the largest CEX, can be globally measured by stablecoin, USDC. On the other hand, the price of each token in the Uniswap V2 pool is measured by the other token. In this regard, we define the exchange ratio of a very small amount of to as the marginal price of with respect to . The marginal price of with respect to can be represented with the amount of and deposited in the Uniswap V2 pool as in Proposition II.1.

Proposition II.1.

The marginal price of with respect to at time is the ratio of the amount of and deposited in the Uniswap V2 pool. As a corollary, the marginal price of with respect to at time is the ratio of the amount of and LPs deposit or withdraw in the Uniswap V2 pool at time .

Proof.

We first denote the marginal price of with respect to at time as . Then, by the definition. Therefore,

As noted in Section II-A, the ratio of the amount of and an LP deposit or withdraw is the same as the ratio of the total amount of and deposited in the Uniswap V2 pool. Concretely, where and are the amount of and the LP deposit or withdraw at time , respectively. Therefore, . ∎

The amount of , and the amount of , can be represented by the marginal price of with respect to , as follows:

| (1) |

The ratio of marginal price between time and time can be represented by the amount of at time and . Concretely,

| (2) |

II-D Interpretation as an order book

The trade amount in LOB is quoted at a certain price while the trade amount in DEX-AMM is quoted in the price range. To be more specific, the quoted amount of between can be written as

In Uniswap V2, by Equation 1. Note, the sum of quoted amount between price ranges is proportional to the liquidity, .

II-E Divergence loss

Divergence loss, also known as impermanent loss, is the opportunity cost for providing a pair of assets to the pool compared to simply holding them. The divergence loss is strictly determined by swap fees from traders to LPs and the difference between a deposited asset and a withdrawn asset. In this paper, however, we consider the profits from swap fees apart from the divergence loss for simplicity. The divergence loss is the value difference between a deposited asset and a withdrawn asset when LPs withdraw their assets.

Suppose an LP deposits the asset at time and withdraws at time . We denote the asset of the LP as a tuple of the amount of and . For example, we denote the deposited asset of the LP at time and the withdrawn asset of the LP at time as and , respectively.

The value of a withdrawn asset with respect to is where is the marginal price of with respect to at time . On the other hand, suppose the LP holds the asset without deposit. Then, the value of the held asset with respect to at time is .

The difference between the value of a withdrawn asset with respect to at time , , and the value of the deposited asset with respect to at time , is the divergence loss with respect to and we denote the divergence loss as . is strictly negative as shown in Proposition II.2.

Proposition II.2.

The divergence loss with respect to at time , is where is the withdrawn at time and is the deposited at time .

Proof.

The divergence loss, is the difference between the value of a withdrawn asset with respect to at time and the value of the deposited asset with respect to at time or . First, by Proposition II.1. Therefore,

The product of the amount of two tokens should be constant in CPMM. Therefore, and .

∎

LPs can still make a profit despite the divergence loss since the LPs are rewarded with swap fees paid by traders. Because divergence loss increases quadratically as marginal price deviates from the initial value, rational market participants will only provide liquidity in DEX only when they expect a sideways market.

III Method

We propose a novel position to reduce the risk of divergence loss for LPs in DEX-AMM. We first introduce a new concept called margin liquidity. We then propose a highly profitable position that attracts market participants by utilizing this margin liquidity. Finally, we introduce a modified version of the proposed position that is still highly profitable but at the same time reduces the risk of divergence loss.

III-A Margin liquidity

Can we provide more liquidity than the assets we have? Similar to margin trading, we define margin liquidity as the liquidity introduced by borrowing assets from lenders with collateral. If the divergence loss of the lent liquidity exceeds the collateral, the lent liquidity and collateral are automatically withdrawn to lenders.

We can apply this concept of margin liquidity to any AMM where divergence loss exists [3, 4, 13, 25]. In this paper, we instantiate margin liquidity on top of the Uniswap V2 framework. We suppose MLPs in Uniswap V2 provide when the collateral is and the leverage ratio is . The ratio of and should be fixed as the current marginal price of with respect to by Proposition II.1.

III-B Margin liquidity-providing position

We propose a margin liquidity-providing position using the concept of margin liquidity. This position requires lenders to lend assets to market participants who open the position. Lenders can be the exchange or other market participants. When market participants open the margin liquidity-providing position, market participants borrow the assets from the lenders with collateral and provide liquidity by depositing the lent assets.

We refer to the market participant who opens margin liquidity-providing positions as the margin liquidity provider (MLP). MLPs receive swap fees from traders in return for providing liquidity when a margin liquidity-providing position opens. The interactions between market participants (MLP, lender, and trader) are illustrated in Figure 1(c).

The margin liquidity-providing position is liquidated when the divergence loss exceeds the collateral. The position can also be closed by the action of the MLP. When the margin liquidity-providing position closes, the deposited assets are withdrawn and returned to the lenders, along with a portion of the collateral corresponding to the divergence loss. Therefore, from the perspective of the lender, the value of the lent asset is equal to the value of the returned asset when the asset is returned. In detail, Proposition III.1 states the ratio of the divergence loss to the collateral when the position closes. It also states the condition when the marginal liquidity-providing position is liquidated. Furthermore, Figure 2 illustrates the rate of marginal price change where the marginal liquidity-providing position is not liquidated for each leverage ratio.

Proposition III.1.

Suppose a margin liquidity-providing position opens when the marginal price is . When the marginal price is , the ratio of the divergence loss to the collateral is . As a corollary, the margin liquidity-providing position is liquidated if the rate of marginal price change, is bigger than or less than .

Proof.

Suppose an MLP opens a margin liquidity-providing position when the marginal price is by depositing as liquidity when the collateral is and the leverage ratio is . When the marginal price is , the divergence loss is , where is the deposited asset of the position. Note, . If the margin liquidity-providing position closes when the marginal price is , the portion of the collateral corresponding to the divergence loss is returned to the lender. We denote the ratio of the divergence loss to the collateral as . Concretely,

| (by Proposition II.2) | ||||

| (by Proposition II.1) | ||||

| (by Equation 2) |

The position is not liquidated when the portion . Concretely,

The margin liquidity-providing position is liquidated if the rate of marginal price change (=) is bigger than or less than . ∎

Margin liquidity-providing position can be applied to both DEX and CEX. In DEX, a margin liquidity-providing position provides liquidity within a specific price range as shown in the liquidity curve of Figure 3(a). Liquidity in the price range is increased by the margin liquidity-providing position. The position yields a similar effect in CEX by facilitating market-making in the order book within the price range.

Note that margin liquidity-providing positions can be interpreted as betting on the sideways market while traditional margin trading bets on the bull market or bear market. Margin liquidity-providing positions have no potential danger of cascading liquidation as in long and short positions of margin trading since closing the margin liquidity-providing positions just reduces the liquidity in exchange without price change.

III-C Virtual Margin liquidity-providing position

Although the introduction of the margin liquidity-providing position increases the total liquidity of the market by attracting risk-taking market participants, traditional LPs still have to suffer from divergence loss, which is the main source of the liquidity shortage in DEX-AMM. To address this issue, we propose a virtual margin liquidity-providing position to lower the risk of divergence loss. Virtual margin liquidity-providing position borrows liquidity from LPs while margin liquidity-providing position borrows liquidity from lenders.

While a margin liquidity-providing position increases the actual liquidity provided to the market, a virtual margin liquidity-providing position does not change the actual liquidity provided to the market. This is because the liquidity provided by the virtual liquidity-providing position comes from the liquidity previously provided by LPs in the same DEX pool. Figure 3 illustrates this difference between a margin liquidity-providing position and a virtual liquidity-providing position.

We name the market participants who open this position virtual margin liquidity providers (VMLP). VMLPs take ownership of the liquidity provided by LPs and are rewarded with swap fees based on their ownership. However, when VMLPs close their positions, VMLPs compensate LPs for any divergence loss of the lent liquidity incurred during the loan period with their collateral. As a result, the virtual margin liquidity-providing positions are liquidated when the divergence loss of the lent liquidity exceeds the collateral.

LPs are rewarded by position fees from VMLPs proportional to the loan period, while the divergence loss of the lent liquidity is compensated. Therefore, their assets increase if the value of assets goes sideways. The interactions between the introduced market participants (VMLP, LP, and trader) are illustrated in Figure 1(c).

Risk-averse market participants would prefer LP with low-risk and low returns. On the other hand, risk-taking market participants would prefer VMLP with high-risk and high returns.

IV Related works

IV-A Uniswap V3

Uniswap V2 provides liquidity uniformly across the whole price range . Hence, most of the liquidity is provided in the price range far from the current price. To deal with this problem, Uniswap V3 proposes concentrated liquidity which allows LPs to provide liquidity only on the bounded price range close to the current price. Therefore, the LPs in Uniswap V3 can provide the same liquidity to the market with a smaller capital.

Margin liquidity provides liquidity on a bounded price range like Uniswap V3. However, margin liquidity provides much more liquidity in the same price range than the concentrated liquidity in Uniswap V3 as shown in Section VI-B.

IV-B dYdX

dYdX DEX [18] provides perpetual margin tradings in DeFi. We call market participants who open the position for margin trading as margin traders. Margin traders buy or sell assets by leveraging their loans. On the other hand, MLPs leverage their loan to provide liquidity for other traders.

dYdX protocol buys or sells tokens using third-party DEX with the assets of lenders when margin traders open a long or short position with their collaterals. On the other hand, our margin liquidity-providing position does not require any third-party DEX to buy or sell tokens.

IV-C Aave V3

Aave provides a pool-based crypto lending service in DeFi. In the Aave lending pool, lenders deposit crypto assets, and users can borrow the assets with their collaterals when Loan-to-Value (LTV) is below the limit set by the Aave protocol[8, 12, 15, 2, 1]. Unlike margin tradings or margin liquidity, the value of the collaterals is usually higher than the value of borrowed assets[19].

Aave requires a third party to liquidate the assets of users when LTV approaches the limit[26]. On the other hand, the position is liquidated without any support from a third party in the margin liquidity-providing position.

V Application

We propose a representative strategy for MLPs who open and close the margin liquidity-providing position to maximize their profit. We backtest[6] an MLP that opens and closes a margin liquidity-providing position to provide liquidity on the pool of and .

V-A Price

We denote the USD price of and at time as and , respectively. For the backtesting, we bring the historical data of , , and from Binance. In detail, there are open price, close price, high price, and low price for each timestamp in OHLCV data. , , are set as the open price in this paper.

We evaluate the asset of an MLP at time in USD terms. Then, we denote the value of the MLP’s asset at time as USD. Concretely, if the MLP has of and of , then .

V-B Opening criteria

The margin liquidity-providing position yields the maximum profit in a sideways market. Therefore, we define the price trend slope at time as in Definition V.1 and determine whether the market is in the uptrend, downtrend, or sideways market at each time with this measure. Note that indicates the market is in an uptrend, while indicates the market is in a downtrend. In this regard, we assume the MLP judges the market is in the sideways market when for a fixed hyperparameter and opens the margin liquidity-providing position.

Definition V.1 (Price trend slope).

We define the price trend slope at time as the slope of the linear trend line for the price data of the last time. Concretely, the price trend slope at time , , is defined as

We assume the MLP opens margin liquidity-providing position at time with the whole asset . Then, the MLP buys of and of for the collateral at the price and , respectively according to Proposition V.2. For simplicity, we suppose MLP buys of and of . Then, MLP deposits with the collateral .

Proposition V.2.

When the asset of MLP is USD at time , MLP can buy of and of as collateral where the marginal price of with respect to is , and the marginal price of and are and , respectively.

Proof.

When the asset of the MLP is , suppose the MLP buys of and of . Then, . Also, by Proposition II.1. Therefore,

∎

V-C PNL analysis

We can estimate the profit and loss (PNL) for the MLP position by 1) estimating the swap fees from trading volumes on the provided liquidity by deposited assets and 2) computing the divergence loss due to the change of marginal price.

V-C1 Swap fees

Swap fees returned to the MLP are proportional to the trade volume on the liquidity provided by the MLP. We denote the liquidity provided by the MLP as , which is computed as .

We track the trade volume on the liquidity provided by the MLP since the margin liquidity-providing position opens at time . We denote the trade volume from both to and to since as and , respectively. Then, where is the trade volume from to at time on the liquidity provided by the MLP. Similarly, where is the trade volume from to at time on the liquidity provided by the MLP. Proposition V.3 states the lower bound and for each time . In the backtesting, we suppose the and are equal to the lower bound in Proposition V.3. Then, we can compute the profit from the swap fees. The MLP receive of and of until time as the swap fees. These fees are worth USD.

Proposition V.3.

The lower bound of trade volume from to at time on the liquidity provided by MLP () can be written as below:

| (3) |

Similarly, the lower bound of the trade volume from to at time on the liquidity provided by MLP () can be written as below:

| (4) |

Proof.

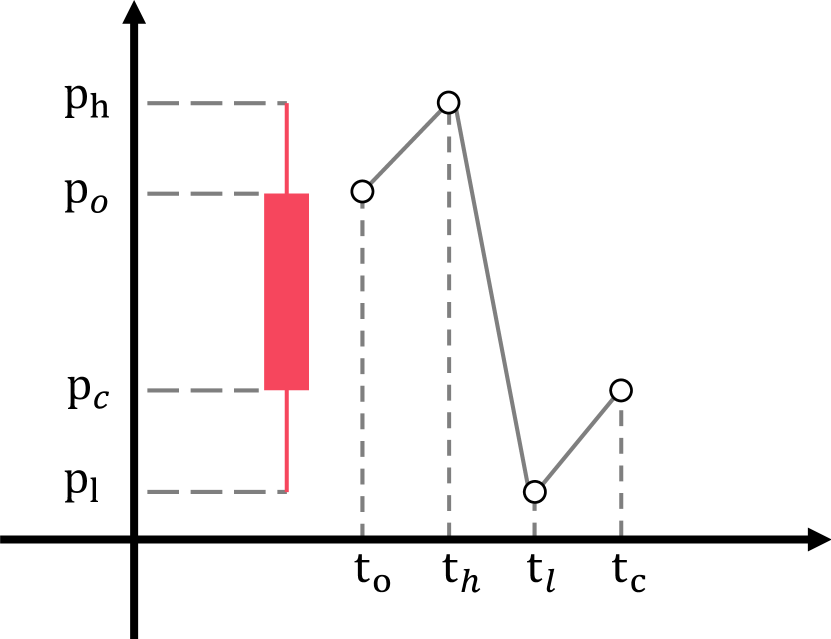

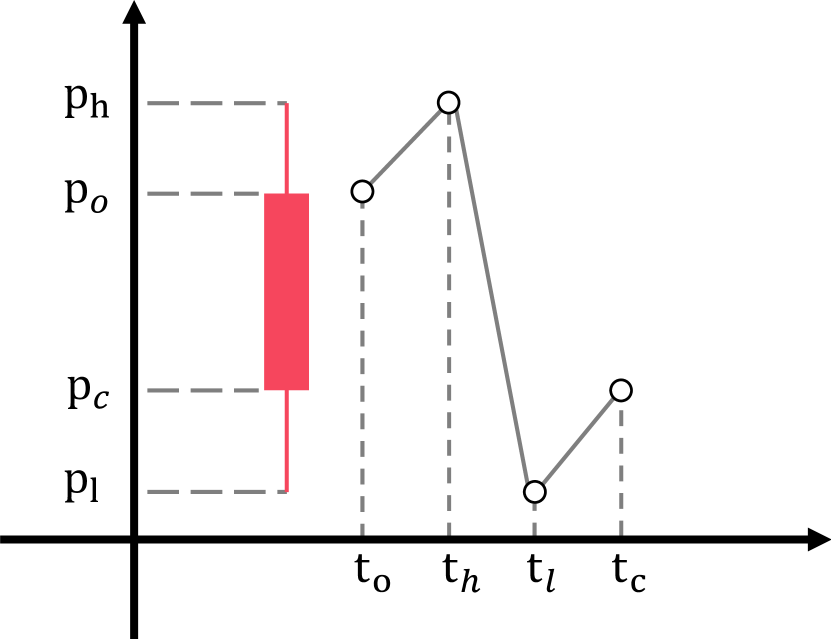

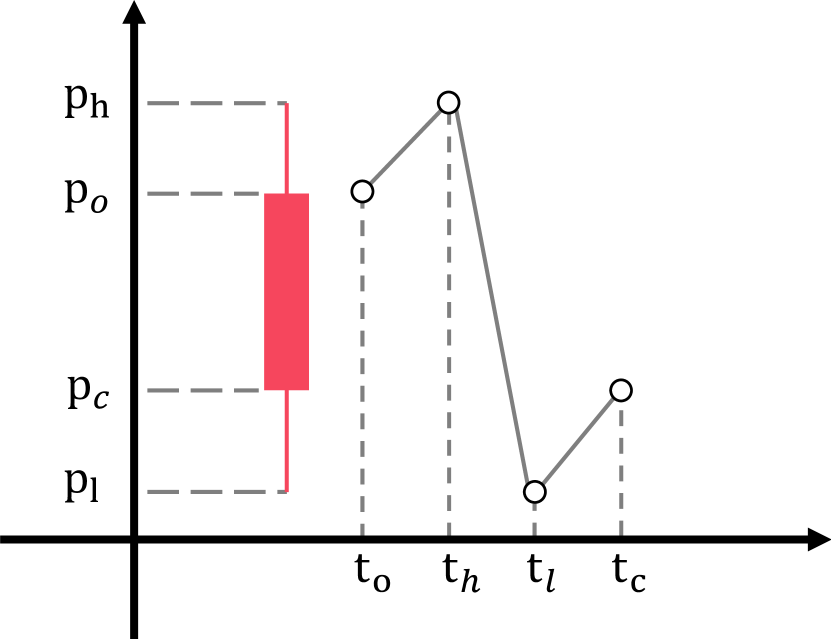

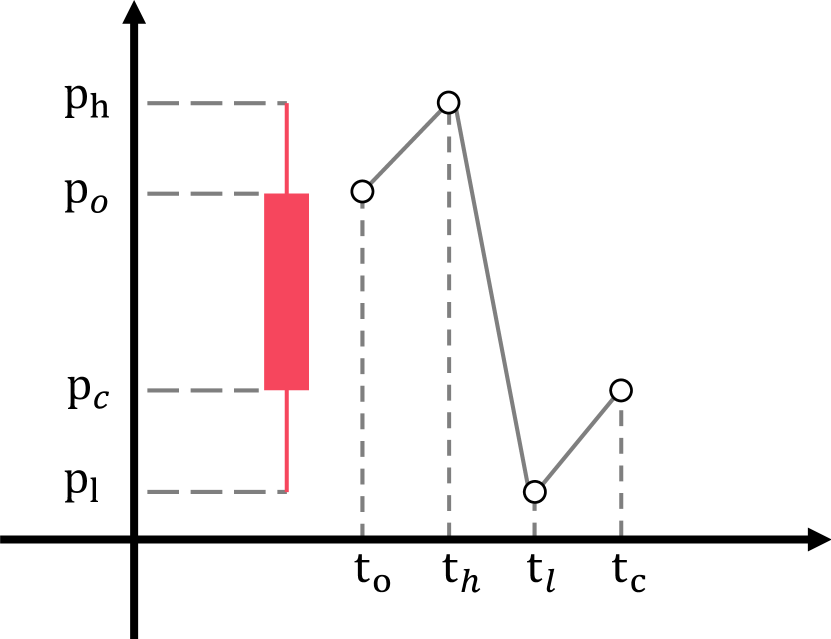

We first denote the reference time for the open price , close price , high price , and low price as , , , and , respectively. By the definition of OHLCV, . Therefore, we can divide OHLCV into four possible cases according to two criteria: 1) or else and 2) or else as in Figure 4.

The marginal price increase means traders swap to . On the contrary, the marginal price decrease means traders swap to . Note that when the price changes, the trade volume is at least the amount changed in the pool which can be represented by the marginal price by Equation 1.

-

•

In Figure 4(a) and Figure 4(c),

(5) -

•

In Figure 4(b) and Figure 4(d),

(6)

Figure 4(a) and Figure 4(b) are indistinguishable from OHLCV data. Therefore, we estimate and by the lower bound of Equation 5 and Equation 6. ∎

V-C2 Divergence loss

Suppose the MLP closes the margin liquidity-providing position at time . The portion of collateral corresponding to the divergence loss is returned to the lender. We evaluate the value of the collateral left in the margin liquidity-providing position at time as the value of the withdrawn asset to the MLP if the position closes at time . We denote the ratio of deposited collateral corresponding to the divergence loss at time as . Concretely,

by Proposition III.1. Then, the withdrawn asset is if the margin liquidity position closes at time . Therefore, the value of the collateral left in the margin liquidity-providing position at time is .

V-C3 PNL

The estimated value of the MLP’s asset at time is the sum of the value of collateral left in the margin liquidity position and the value of swap fees from traders. Concretely,

PNL at time is the difference between the estimated value of the MLP’s asset at time and . We denote the PNL at time as . Then, .

V-D Closing criteria

There are three closing conditions for the margin liquidity-providing position. If one of the conditions is satisfied, the margin liquidity-providing position is voluntarily closed or liquidated. Firstly, if the absolute value of the price trend slope is larger than a fixed hyperparameter which is larger than , MLP judges the market converts from a sideways market to a trend market and closes the position. Secondly, if the PNL exceeds the stop loss, the MLP voluntarily closes the position. We denote the ratio of stop loss to the initial asset as . Then, the MLP closes the position when . Finally, if the divergence loss exceeds collateral or , the position is liquidated.

VI Experiments

period Method Sharpe ratio MDD ROR 20Q1 Baseline -0.21 0.67 0.95 Ours () 3.31 0.32 1.84 Ours () 3.32 0.32 1.84 Ours () 3.53 0.33 1.91 Ours () 1.80 0.79 2.07 20Q3 Baseline 1.82 0.29 1.39 Ours () 2.20 0.21 1.84 Ours () 2.22 0.21 1.84 Ours () 2.35 0.22 1.91 Ours () -2.11 0.89 2.07 21Q1 Baseline 3.72 0.31 2.31 Ours () 4.04 0.30 2.55 Ours () 4.06 0.30 2.52 Ours () 4.11 0.32 2.28 Ours () -3.42 0.92 0.42

VI-A Backtesting for representative strategy

We proposed our representative strategy in Section V. In this section, we backtest our representative strategy with historical data from several periods (20Q1, 20Q3, 21Q1). We consider the margin liquidity-providing strategy on the ETH/BTC market and utilize ‘5m’ Binance OHLCV data for ETH/USDC, BTC/USDC, and ETH/BTC.

We evaluate our representative strategy with Sharpe ratio, MDD, and ROR. Note that we suppose the risk-free rate in the Sharpe ratio is computed for the case where the USD is deposited in the bank with an annual interest rate of . For the baseline, we propose an ETH and BTC holding position as baseline, where the ratio of the holding amount of ETH and BTC is the marginal price of ETH with respect to BTC following Proposition II.1 [11]. Table I shows that our strategy can outperform the baseline with a higher Sharpe ratio, a smaller MDD, and a higher ROR if leverage ratio is set appropriately. For example, in 20Q1, the Sharpe ratio, MDD, and ROR for our strategy when are , , and , while the baseline achieves , , and .

VI-B Capital efficiency comparison

In this paper, we use the term capital efficiency to denote how much liquidity can be provided with the same amount of assets. We aim to compare the capital efficiency of our proposed margin liquidity with the concentrated liquidity in Uniswap V3. Note that our proposed margin liquidity and concentrated liquidity are both extensions of Uniswap V2.

VI-B1 Capital efficiency of concentrated liquidity

We first suppose liquidity is provided in the price range in the Uniswap V3. Then,

where and are the number of tokens and tokens, respectively. Also, the marginal price of token with token can be computed as in Equation 7.

| (7) |

Then, , when the marginal price is and , when the marginal price is . Therefore, Uniswap V3 provides of token and of token in .

Suppose the deposited assets in the Uniswap V3 pool are withdrawn at the marginal price and are redeposited to the Uniswap V2 pool. For brevity, let’s denote the as . Then, the assets amount of are withdrawn and redeposited to the Uniswap V2 pool. The liquidity of the Uniswap V2 pool becomes

We denote the liquidity of the Uniswap V2 pool as . Similarly in the Uniswap V3, , when the marginal price is and , when the marginal price is by Equation 1. Therefore, Uniswap V2 provides of token and of token in the price range .

The ratio of and represent the ratio of the number of tokens provided by the Uniswap V2 pool and Uniswap V3 pool in the price range :

The ratio above implies that concentrated liquidity in Uniswap V3 is more capital efficient than Uniswap V2.

VI-B2 Capital efficiency of Margin liquidity

Suppose we open a margin liquidity-providing position instead of re-depositing the asset to the Uniswap V2 pool. We set the leverage ratio of margin liquidity-providing position as such that the position remains open without liquidation in the price range . This in turn means that and by Proposition III.1. Then, the maximum leverage ratio possible is .

Margin liquidity is more capital efficient than Uniswap V2 since times more assets are deposited in the margin liquidity. In the best case, margin liquidity is more capital efficient than Uniswap V2.

Figure 5 shows the capital efficiency of Uniswap V3 and margin liquidity using the results above. In particular, When , concentrated liquidity in Uniswap V3 is times more efficient than Uniswap V2 while margin liquidity is times more efficient than Uniswap V2.

VII Conclusion

Liquidity is one of the most crucial factors when traders choose an exchange, regardless of whether the exchange operates in a centralized or decentralized manner. However, the inherent risk of divergence loss in DEX-AMM hinders the market participants from providing enough liquidity. In this regard, we introduce a new concept of liquidity, margin liquidity, and propose a highly profitable liquidity-providing position, which can be applied to both CEX and DEX, to attract risk-taking market participants. Also, we extend this position to hedge the risk of divergence loss of LPs so that LPs can provide more liquidity. Furthermore, we introduce a representative strategy for market participants who want to provide liquidity with our proposed position. Our representative strategy outperforms a simple holding baseline with a higher ROR and a lower MDD in the backtest on the historical data of the ETH/BTC market. Also, we show that our margin liquidity is 8K more capital efficient than the concentrated liquidity proposed by Uniswap V3.

References

- [1] Aave, “Aave/aave-protocol: Aave protocol version 1.0 - decentralized lending pools.” [Online]. Available: https://github.com/aave/aave-protocol

- [2] ——, “Aave/protocol-v2: Aave protocol v2.” [Online]. Available: https://github.com/aave/protocol-v2

- [3] H. Adams, N. Zinsmeister, and D. Robinson, “Uniswap v2 core,” 2020.

- [4] H. Adams, N. Zinsmeister, M. Salem, R. Keefer, and D. Robinson, “Uniswap v3 core,” 2021.

- [5] J. Aoyagi and Y. Ito, “Coexisting exchange platforms,” 2021.

- [6] D. H. Bailey, J. Borwein, M. Lopez de Prado, and Q. J. Zhu, “The probability of backtest overfitting,” Journal of Computational Finance, forthcoming, 2016.

- [7] A. Barbon and A. Ranaldo, “On the quality of cryptocurrency markets: Centralized versus decentralized exchanges,” arXiv preprint arXiv:2112.07386, 2021.

- [8] M. Bartoletti, J. H.-y. Chiang, and A. L. Lafuente, “Sok: lending pools in decentralized finance,” in International Conference on Financial Cryptography and Data Security, 2021.

- [9] M. Bartoletti, J. H.-y. Chiang, and A. Lluch-Lafuente, “A theory of automated market makers in defi,” in International Conference on Coordination Languages and Models, 2021.

- [10] A. Capponi and R. Jia, “The adoption of blockchain-based decentralized exchanges,” arXiv preprint arXiv:2103.08842, 2021.

- [11] R. Cont, “Empirical properties of asset returns: stylized facts and statistical issues,” Quantitative Finance, 2001.

- [12] S. Cousaert, J. Xu, and T. Matsui, “Sok: Yield aggregators in defi,” in 2022 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2022.

- [13] M. Egorov, “Stableswap-efficient mechanism for stablecoin liquidity,” Retrieved Feb, 2019.

- [14] M. Egorov and C. Finance, “Automatic market-making with dynamic peg,” Technical report, Curve Finance, Tech. Rep., 2021.

- [15] E. Frangella and L. Herskind, “Aave/aave-v3-core: This repository contains the core smart contracts of the aave v3 protocol.” [Online]. Available: https://github.com/aave/aave-v3-core

- [16] B. T. Gale, “Market share and rate of return,” The review of economics and statistics, 1972.

- [17] J. Han, S. Huang, and Z. Zhong, “Trust in defi: an empirical study of the decentralized exchange,” Available at SSRN 3896461, 2021.

- [18] A. Juliano, “dydx: A standard for decentralized margin trading and derivatives,” URl: https://whitepaper. dydx. exchange, 2018.

- [19] A. Klages-Mundt, D. Harz, L. Gudgeon, J.-Y. Liu, and A. Minca, “Stablecoins 2.0: Economic foundations and risk-based models,” in Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, 2020.

- [20] B. Krishnamachari, Q. Feng, and E. Grippo, “Dynamic curves for decentralized autonomous cryptocurrency exchanges,” arXiv preprint arXiv:2101.02778, 2021.

- [21] A. W. Lo, “The statistics of sharpe ratios - andrew lo.” [Online]. Available: https://alo.mit.edu/wp-content/uploads/2017/06/The-Statistics-of-Sharpe-Ratios.pdf

- [22] M. Magdon-Ismail and A. F. Atiya, “Maximum drawdown,” Risk Magazine, 2004.

- [23] S. Malamud and M. Rostek, “Decentralized exchange,” American Economic Review, 2017.

- [24] T. N. S. Market, “Exhibit e-tab1-systems description-sec.” [Online]. Available: https://www.sec.gov/pdf/nasd1/systems.pdf

- [25] F. Martinelli and N. Mushegian, “A-non-custodial-portfolio-manager, liquidity provider, and price sensor,” URl: https://balancer.finance/whitepaper, 2019.

- [26] K. Qin, L. Zhou, P. Gamito, P. Jovanovic, and A. Gervais, “An empirical study of defi liquidations: Incentives, risks, and instabilities,” Jun 2021. [Online]. Available: https://arxiv.org/abs/2106.06389v1

- [27] Stastny, Reuptaken, Devinwalsh, AndyForman, moto22, Danhsiu, and Research, “Alastor uniswap fee switch report,” 2022. [Online]. Available: https://gov.uniswap.org/t/alastor-fee-switch-report/18020

- [28] O. Van Hemert, M. Ganz, C. R. Harvey, S. Rattray, E. S. Martin, and D. Yawitch, “Drawdowns,” The Journal of Portfolio Management, 2020.

- [29] S. M. Werner, D. Perez, L. Gudgeon, A. Klages-Mundt, D. Harz, and W. J. Knottenbelt, “Sok: Decentralized finance (defi),” arXiv preprint arXiv:2101.08778, 2021.

- [30] J. Xu, K. Paruch, S. Cousaert, and Y. Feng, “Sok: Decentralized exchanges (dex) with automated market maker (amm) protocols,” arXiv preprint arXiv:2103.12732, 2021.

- [31] L. Zhou, X. Xiong, J. Ernstberger, S. Chaliasos, Z. Wang, Y. Wang, K. Qin, R. Wattenhofer, D. Song, A. Gervais, and et al., “Sok: Decentralized finance (defi) attacks,” Sep 2022. [Online]. Available: https://arxiv.org/abs/2208.13035