Naïve Markowitz Policies††thanks: The first version of the paper was completed in 2017, and part of the results was included in the first author’s PhD thesis defended in 2020. The paper was finalized when the second author was on vacation in Las Vegas, a place arguably ideal for observing the “naïve” behaviors studied in the paper.

Abstract

We study a continuous-time Markowitz mean–variance portfolio selection model in which a naïve agent, unaware of the underlying time-inconsistency, continuously reoptimizes over time. We define the resulting naïve policies through the limit of discretely naïve policies that are committed only in very small time intervals, and derive them analytically and explicitly. We compare naïve policies with pre-committed optimal policies and with consistent planners’ equilibrium policies in a Black–Scholes market, and find that the former are mean–variance inefficient starting from any given time and wealth, and always take riskier exposure than equilibrium policies.

Key Words. Continuous time, mean–variance model, time inconsistency, naïve agent, pre-committed agent, consistent planner, equilibrium policies.

1 Introduction

The Markowitz mean–variance (MV) portfolio selection model (Markowitz, 1952 and Markowitz, 1959) is a monumental work in quantitative finance. The model formulates the investment problem as striving to achieve the best balance between return and risk, represented respectively by the mean and variance of the final portfolio worth. Its variants, extensions and implications have been passionately studied in theory and applied in practice to this day.

The original MV model is formulated for a static single period and solved by quadratic program. It is natural and necessary to extend it to the dynamic setting, both in discrete time and continuous time. However, a dynamic MV model is inherently time inconsistent; namely, any “optimal” policy for the present moment will generally not be optimal for the next moment.111Here a “policy” is a plan that maps any given time and state to an action (a portfolio in the MV model). It is also called a feedback control law in control theory. This inconsistency comes from the variance term that does not satisfy the tower rule: unlike the mean, there is no consistency over time in evaluating the same variance of the final wealth. As a result, in sharp contrast to the classical time-consistent models, there is no such notion as a dynamically optimal policy for a time-inconsistent model because any such policy, once planned for this moment, may need to be given up quickly (and instantly in a continuous-time setting) in favor of a different plan at the next moment. Technically, time-inconsistency poses fundamental challenges in “solving” – whatever “solving” means – the problem because the Bellman optimality principle, which is the very foundation of the classical dynamic programming for studying dynamic optimization problems, is no longer valid.

Economists have recognized and studied time-inconstancy since as early as the 1950s. The foundational paper Strotz (1956) describes three types of agents when facing time inconsistency. Type 1, a “naïveté” (or naïf), is unaware of the time inconsistency and at any given time and state of affairs seeks an “optimal” policy for that moment only, without knowing that he will not uphold that policy for long. As a result, his policies change all the times, and the eventual policy that is being actually carried out can be vastly and characteristically different from any of his short-lived “optimal” policies he originally planned to execute.222For instance, Barberis (2012) shows, in a casino gambling model (which is time-inconsistent in discrete time due to probability weighting), a naïve gambler’s initial plan was to gamble as long as possible when winning but to stop if he started accumulating losses, he actually ends up doing the opposite: he gambles as long as possible when losing and stops once he accumulates some gains. Similar behaviors are also observed, and indeed prevalent, in stock investment especially with retail investors. The next two types realize the issue of time inconsistency but act differently. Type 2 is a “precommitter” who solves the optimization problem only at time 0 and sticks to the resulting policy throughout (via some “commitment device” if necessary and available), recognizing that the original policy may no longer be optimal at later times. Type 3 is a “consistent planner” who is unable to precommit and realizes that her future selves may abandon whatever plans she makes now. Her resolution is to optimize taking the future deviations from the current plan as constraints, effectively leading to a game among selves at different times. The resulting policies are called equalibrium ones.

It is important to note that it is not meaningful to determine which type is superior than the others, simply because there are no uniform criteria to compare them. In this sense, the Strotzian approach to time-inconsistency is both normative (i.e. to advise people about the best course of actions, especially in Types 2 and 3) and descriptive (i.e. to describe what people are actually doing, as more with Type 1).

Mathematically, model formulations and solutions for deriving the three types of agent policies call for different treatments as they are very different from each other. The problems are also challenging due to the invalidity of the dynamic programming approach. In the last decade, there have been significant developments in studying time-inconsistent models analytically, mainly in three different settings: MV portfolio selection, and optimization problems involving non-exponential discounting or probability weighting; see He and Zhou (2022) for a recent survey on the related works. For the MV models, earlier works focused on Type 2, pre-committed agents; see, e.g., Richardson (1989); Hakansson (1971); Li and Ng (2000); Zhou and Li (2000); Lim and Zhou (2002); Bielecki et al. (2005); Xia (2005); Li and Zhou (2006), although most of these works did not spell out that their solutions were pre-committed ones. Later research gradually shifted to Type 3, consistent planners; see, e.g. Basak and Chabakauri (2010); Hu et al. (2012); Björk and Murgoci (2014); Björk et al. (2014); He and Jiang (2022).

In contrast to the rich literature on pre-committed agents and consistent planners, there are far fewer works on the general behaviors of naïve agents, and almost none in continuous time (not necessarily limited to MV models). Barberis (2012); Hu et al. (2022) study naïve strategies in casino gambling models which are inherently discrete time. As shown in these papers, finding naïve policies in discrete time is rather straightforward technically if the pre-committed polices are already available: at each discrete time point one solves and obtains the corresponding pre-committed policy, holds it until the next time point when one re-solves the pre-committed problem, and repeats these steps until the terminal time. The eventual naïve policy is then just to “paste” these piece-wise pre-committed policies together. This pasting approach, however, does not work for the continuous-time setting. Indeed, at each given time and state, say , a pre-committed policy is executed and instantaneously discarded, while a policy applied for just one single time–state initial point has no impact on the dynamics in continuous time. As a result, it is unclear how to paste these continuously changing policies and, even one found a way to do it, how to interpret the resulting policy.

We address this issue specific to continuous time and make two main contributions in this paper. First, to our best knowledge we are the first to define precisely the naïve policies in the original sprit of Strotz (1956) but adapted to the continuous-time setting, premised upon the notion that any continuous-time behavior is the limit of discrete-time behaviors when the time-step approaches zero.333An analogy here is that the Brownian motion is just the limit of a simple random walk when the step size diminishes to zero. We fix a set of discrete time points and consider a fictitious agent who only optimizes at each of these points and holds the resulting pre-committed policy until the next point. It is then natural to use the “limit” – in a certain sense – of these discretely naïve agents when the step size becomes asymptotically small to describe the naïve behavior in the original continuous-time model. One technical subtlety here is that policies are generally only measurable functions whose limit is difficult to analyze. We consider instead the limiting process of the wealth processes – which are analytically better behaved – of those discrete agents, and find the policy that generates this limiting process as the wealth process. A main advantage of our approach is that it is both general and constructive. It is general because the definition of a naïve policy applies readily to any time-inconsistent problems beyond MV (see Chen and Zhou, 2020 for an extension to the general stochastic linear–quadratic control problem), and it is constructive because the definition itself points to the direction of deriving a naïve policy.

The second contribution is to compare the naïve policies with the other Strotzian types of policies. Be mindful that it does not make much sense to use either mean or variance of the terminal wealth alone for comparison, as the essence of the MV model is to achieve a best trade-off between the two criteria. Instead, MV efficiency ought to be the primary criterion. Between a naïveté and a pre-committer, starting from any given point of time and state, the latter is MV efficient by definition while we show that the former is not (although he elevates the expected terminal wealth than he originally planned). To compare naïve and equilibrium policies which are both MV inefficient, we use an objective metric which is the risky weight defined as the fraction of dollar amount invested in stocks. We show that a naïveté always allocate strictly higher risky weight than the two types of consistent planners considered by Björk et al. (2014) and He and Jiang (2022) respectively. This in turn suggests that the naïve policies tend to be more risk-taking than their consistent planning counterparts.444An analogous result is proved in Hu et al. (2022) for a casino gambling model: a naïve gambler stops gambling no earlier than a gambler doing consistent planning.

Pendersen and Peskir (2017) introduce the notion of “dynamic optimality” in a continuous-time MV model, which seems to bear some relevance to naïve policies (although the paper stops short of commenting on it). Definition 2 therein defines a dynamically optimal policy as there being no other policy applied at present time could produce a more favourable value at the terminal time. However, as discussed earlier, in a time-inconsistent problem there is no such thing as “dynamic optimality”: as much as a naïveté attempts to reoptimize continuously over time, the resulting actual policy at any given time may significantly deviate from the pre-committed optimal one (and therefore is MV inefficient, and indeed not optimal in any sense). On the other hand, Pendersen and Peskir (2017) conjecture the analytical formula of such a “dynamically optimal” policy for a single stock Black–Scholes market without explaining where it comes from. Hence the solution method is ad hoc and it is unclear whether the existence of such a policy is prevalent and, if yes, how to extend the conjecture to a more general MV setting (e.g., one with more than one risky asset) or to other time-inconsistent problems (e.g. with non-exponential discounting or probability weighting). By contrast, our definition of naïve policies is general and our derivation of these policies is constructive.

The rest of the paper is organized as follows. In Section 2 we formulate the continuous-time MV portfolio selection model. In Section 3 we introduce the so-called -committed policies, which are commited only during a small interval of length , before reoptimization. We consider the limit of the wealth processes under these policies as , and define the policy that generates this limiting wealth process as a naïve policy. We then state the main result that expresses naïve policies analytically. In Section 4 we compare naïve policies with other types of policies in a Black–Scholes market. Section 5 concludes the paper. Proofs related to the main result are placed in Appendices.

2 A Continuous-Time Markowitz Model

In this section we review the continuous-time Markowitz MV model. We first introduce notations.

Throughout this paper, denotes the transpose of any vector or matrix , while all vectors are column vectors unless otherwise specified. A fixed filtered complete probability space is given along with a standard -adapted, -dimensional Brownian motion . We use or to denote the function , and to denote the function value of at . Likewise, we use or to denote a stochastic process . Given a Hilbert space and , we denote by the Hilbert space of -valued, square-integrable functions on endowed with the norm . Moreover, we denote by the Hilbert space of -valued, square-integrable and -adapted stochastic processes endowed with the norm , where is the norm in a Euclidean space.

A financial market has assets being traded continuously. One of the assets is a bank account whose price process is subject to the following equation:

| (1) |

where the interest rate function is deterministic. The other assets are stocks whose price processes , satisfy the following stochastic differential equations (SDEs):

| (2) |

where and , the appreciation and volatility rates functions respectively, are scalar-valued and deterministic. Set the excess rate of return vector function and the volatility matrix function respectively as

An agent has total wealth at time , where is a given terminal time of the investment horizon. Assuming that the trading of shares takes place in a self-financing fashion and that there are no transaction costs, the process satisfies the wealth equation

| (3) |

where each , denotes the total market value of the agent’s wealth in the -th asset, resulting in a portfolio , at time . The agent considers portfolio choice at time when her wealth is , where is given. The process is called an admissible portfolio (process) for if and the wealth equation (3) with initial condition admits a unique strong solution. Denote by the set of admissible portfolio processes for .

We focus on a portfolio policy which is a deterministic map from to . Such a policy specifies a portfolio when time is and wealth is .555In control theory, the policy here is also called the feedback control law, whereas the portfolio process corresponds to the open-loop control. In the classical, time-consistent setting, a policy is independent of the initial time–state pair , meaning that it is implemented no matter when and where one starts. Such policies are called time-consistent ones. A time-consistent policy is called admissible if for any , the following SDE obtained by substituting into the wealth equation (3)

| (4) |

admits a unique strong solution and, moreover, the resulting portfolio process where , . Note that the wealth–portfolio process pair depends on the initial , and we say is generated from the policy with respect to .

The classical verification theorem for time-consistent problems (e.g. Yong and Zhou, 1999) dictates that, under standard assumptions, there exists a time-consistent policy that generates optimal wealth–portfolio process pair for any given initial .

The following assumptions are in force throughout this paper.

(A1) and are uniformly bounded on .

(A2) a.e. and for some .

Given , the Markowitz mean–variance portfolio selection problem over is

| (5) |

| (6) |

where and denote respectively the variance and expectation conditional on and , and , is a given deterministic real-valued function satisfying . The number represents the desired growth factor over the time horizon . It is economically sensible to consider the expected mean target to be dependent of the initial , which is equivalent to the state-dependend risk aversion considered in Björk et al. (2014). He and Jiang (2022) consider a more general target instead of ; see also Section 4 of this paper.

We add an assumption on throughout this paper:

(A3) , , , and .

The second part of this assumption is natural, demanding the target return to be at least as great as the risk-free return.

Given , the relation between and , where is the optimal terminal wealth of the problem (5) – (6), is called an efficient frontier with respect to , which gives the best risk–return tradeoff for future investment when standing at .

The problem (5) – (6) has been solved explicitly in literature; see e.g. (Li and Zhou, 2006, Theorem 2.1),666The previous results such as (Li and Zhou, 2006, Theorem 2.1) are for the case when , but they extend readily to arbitrary initial because the underlying mathematical problem of the latter is the same. with the following unique optimal policy (conditional on and )

| (7) |

where

| (8) |

with

Note that l’Hôspital’s rule along with Assumptions (A2)-(A3) yield that is continuous at ; hence is uniformly bounded on .

Substituting the policy (7) into the wealth equation (3) we obtain that the corresponding optimal wealth process is determined by the following SDE:

| (9) |

Finally, the efficient frontier at is

| (10) |

In sharp contrast to the time-consistent setting, the policy given by (7) now depends on the initial pair explicitly. If the agent sticks to this policy during the entire future time period without subsequently altering it, then it is the so-called optimal pre-committed policy. If the agent is naïve à la Strotz who reoptimizes at every subsequent time moment, then the policy (7) will be abandoned immediately (indeed instantaneously) at any . More precisely, suppose the agent carries out (7) for a (little) while and reaches the state at time . Now the current initial time becomes and the current initial state is . If the agent reoptimizes the problem for the remaining duration , then the corresponding policy at is (conditional on )

| (11) |

Clearly, the two policies (7) and (11) are generally different as two functions on .

So, problem (5) – (6) admits a policy (7) that is optimal for the current only. In other words, the pre-committed optimal policy depends inherently on , which in turn causes the time-inconsistency of the policy and hence that of the problem, as discussed above. A time-inconsistent policy of the type (7) is defined only for the given .

3 Naïve Policies

A naïvetè (“he”) always “reoptimizes” under current information; as a result he devises policies and then instantly abandons them in the continuous-time setting. Although at each given time he tries to follow the pre-committed optimal policy (7) but his eventual policy due to the constant changes could be completely different from (7). In this section, we define naïve policies rigorously, and then derive them in analytical form for the MV problem (5)–(6).

3.1 A -committed agent

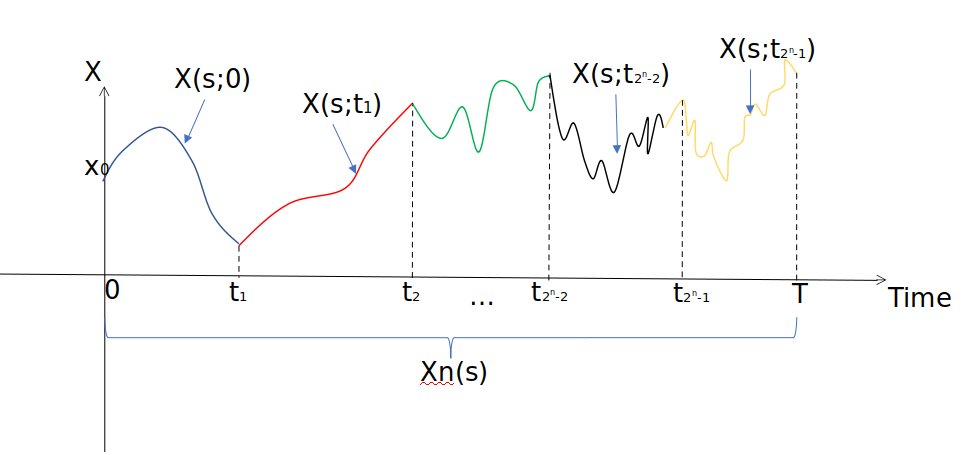

As discussed earlier, the difficulty of defining and analyzing naïve policies lies in the continuous-time setting of the problem. We overcome this difficulty by introducing an auxiliary agent, named the -committed agent, to approximate the behavior of the naïvetè.

A -committed agent (“she”) is one who behaves “in between” a pre-committer and a naïvetè. Specifically, she partitions the time horizon into equal-length intervals, with the partitioning points being where . She first solves problem (5)-(6) with to obtain the pre-committed optimal policy defined by (7). She implements and commits to this policy until time when her wealth becomes , at which she resolves problem (5)-(6) with and switches to the policy . She commits to this new policy until before changing it to . She then repeats these steps until time . Figure 1 illustrates the resulting wealth process under this construction.

Denote by the above wealth process in the time interval , with . By (9), these processes , , can be determined by the following SDEs recursively:

| (12) |

where is defined as .

Now, by “pasting” , , we obtain the following process:

| (13) |

which is the wealth process of the -committed agent, visualized by Figure 1. Obviously, this process is adapted and continuous on .

3.2 Naïve policies

While this -committed agent behaves somewhere between a pre-committed agent and a naïve one, she is closer to the latter when becomes larger. Therefore, we define a naïve policy through the limit (in certain sense) of the -committed wealth process as .

Definition 1

Some remarks on this definition are in order. First, this definition applies to more general time-consistent problems instead of just the current Markowitz problem. As such, we intentionally leave vague the precise sense in which converge to in order to make the definition general and applicable to other problems. For the present problem, we will see momentarily that the convergence is in the weak- sense. Second, a naïve policy in itself must be time-consistent, meaning that it can no longer depend on any initial and, in particular, on , even though each is indeed constructed starting from a specific pair . Finally, we do not define a naïve policy as simply the limit of -committed policies, because policies are in general only measurable and they may not converge and are hard to analyze. Instead, we consider the limit of wealth processes that are much better behaved, and then use the limiting wealth equation to recover the corresponding naïve policy.

The following proposition, whose proof is deferred to Appendix A, indicates that the -committed wealth processes , , are uniformly bounded in .

Proposition 1

It holds that

Moreover, is uniformly bounded in .

Due to Proposition 1, the sequence is uniformly bounded in the Hilbert space , and hence is weakly compact. So there exists a weakly convergent subsequence (still denoted as without loss of generality) and a process such that

The following theorem is the main result of the paper, which characterizes this limiting process and, consequently, the naïve policy.

Theorem 1

The weakly limiting process satisfies the following SDE:

| (14) |

Moreover, the following is the naïve policy:

| (15) |

Note that the explicitly presented policy (15) indeed does not depend on any initial pair and, in particular, on . This means that even if the wealth process of the -committed is constructed from an arbitrarily different initial pair , it will lead to the same naïve policy (15). On the other hand, it generates as its wealth process for the given initial .

4 Comparison between Naïve and Other Types of Policies

In the continuous-time MV literature, two types of equilibrium policies by consistent planners have been introduced and studied: the weak equilibrium policies by Björk et al. (2014) and the regular equilibrium policies by He and Jiang (2022). In this section, we compare the naïve policies with these two types of equilibrium policies as well as the pre-committed ones, in a Black–Scholes market.

4.1 Weak and regular equilibrium policies

We first review the two types of equilibrium strategies, whose definitions can be found, in slight variants of the MV formulation, in Björk et al. (2014) and He and Jiang (2022) respectively.

Given , Björk et al. (2014) consider the following problem:

| (16) |

| (17) |

In the objective function of this problem, there is a risk-aversion term that depends on the initial time and initial state ; see Björk et al. (2014) for the many discussions on the motivation of such a varying risk-aversion term.777Björk et al. (2014) consider only the state-dependent risk aversion , but the method and results therein readily extend to the time–state dependent case presetned here. The problem is again time-inconsistent. Björk et al. (2014) study the behavior of a consistent planner by considering the equilibrium policies defined as follows. Given an admissible (time-consistent) policy , construct a new policy by

| (18) |

where , and are aribitrarily given. Let and be respectively the portfolio processes generated by and starting from . We say that is a weak equilibrium policy if the pertubed policy is admissible and

| (19) |

for all and .

On the other hand, He and Jiang (2022) formulate the following problem:

| (20) |

| (21) |

where indicates the expected terminal wealth target when the initial pair is .888In the original formulation of He and Jiang (2022), the expected terminal wealth constraint is , which is equivalent to the equality constraint formulated here. When , the problem (20)–(21) reduces to the problem (5)–(6). He and Jiang (2022) also study a consistent planner, except that they use the notion of regular equilibrium policies which is very different from that of the weak equilibrium policies. Specifically, an admissible, time-consistent policy is called a regular equilibrium policy if for any , any such that constructed by (18) is admissible for sufficeintly small , we have999Here, the term “admissible” requires the corresponding portfolio processes generated by the relevant policies for to also satisfy the expectation constraint in (21).

| (22) |

for sufficiently small , where and are the terminal wealth values, both starting from and under and respectively.

The difference between the problems (16)–(17) and (20)–(21) is that the former uses a weighting coefficient in its objective function while the latter takes in its constraint. The two problems are related via the Lagrange multiplier method. As a result, if we choose and in a certain way, then the respective pre-committed optimal polices for the two problems coincide, as stipulated in the following proposition.

Proposition 2

Proof.

It follows from the equations (5.12), (5.1) and (6.7) in Zhou and Li (2000) that the pre-committed optimal policy of (16)–(17) is

| (24) |

where

On the other hand, it follows from (Li and Zhou, 2006, Theorem 2.1) that the precommitted strategy of (20)–(21) is

| (25) |

where

It is now evident that if (23) is satisfied, then leading to . ∎

The condition (23) ensures that the pre-committed solutions of the two problems coincide. As a result, the naïve policies of the two problems are also identical because they are obtained via the limit of pre-committed policies. However, (23) does not necessarily lead to the same weak/regular equilibrium policies of the two problems, because equilibrium policies are not based on pre-committed ones.

4.2 Comparisons

We now compare the naïve policies with the weak/regular equilibrium policies and the pre-committed polices, in a Black–Scholes market for simplicity. Specifically, there is a risk-free asset and only one risky asset (i.e. ) with , , . As a result, .

We carry out the comparison for two cases. In Subsection 4.2.1, we choose for some constant in the problem (16)–(17), which is also a case examined closely in Björk et al. (2014). Subsection 4.2.2 studies the case when for some constant in the problem (20)–(21). In each case, we choose , and in such a way (e.g. to satisfy (23)) that the different formulations of the MV problem are consistent in their respective pre-committed optimal policies.

4.2.1 The case

When , the corresponding according to (23) is

| (26) |

whereas the corresponding is

| (27) |

It is easy to check that this satisfies Assumption (A3). By Theorem 1, the naïve policy is

| (28) |

Substituting the expression of in (27) into the above and going through some simple computation, we finally get

| (29) |

The risky weight function of this policy, defined as the ratio between the dollar amount in the stock and the total wealth and denoted by , is thereby

| (30) |

which turns out to be a function of only.

On the other hand, when , Theorem 4.6 in Björk et al. (2014) gives the weak equilibrium policy of the problem (16)–(17) as

| (31) |

where is the unique solution to the following integral equation

| (32) |

Similarly, is the risky weight function of the weak equilibrium policy.

Applying Theorem 1-i in He and Jiang (2022) and noting that the solution to the problem (2.10) therein is , we obtain the regular equilibrium policy for (20)–(21) to be

| (35) |

where

| (36) |

is the risky weight of this equilibrium policy at .

The following proposition shows that the naïve policy allocates strictly more weight to the risky asset than the two equilibrium policies at any time before .

Proposition 3

In the Black–Scholes market, if , then we have

for any .

Proof.

Let us first prove . We have the obvious inequality

| (37) |

because . Recalling that satisfies (32), we deduce

| (38) | ||||

Next, we prove . Indeed

The proof is complete.

∎

So naïve policies take more risk exposure than the two types of equilibrium policies. It is interesting to compare the naïvetè also with a pre-committer, realizing that the former strives to follow the latter at every initial pair . Take for example. The pre-committer’s expected terminal wealth is

| (39) |

noting (27). Although the naïvetè’s original expected target return was also at , he changes mind all the time subsequently so his actual target return at can be significantly deviate from the original one. To see this, plugging in the naïve policy (29) to the wealth equation (3) to obtain

| (40) |

Taking the integral form of this SDE and applying expectation on both sides, we get an ODE in terms of . Solving this ODE we arrive at

| (41) |

Recall that is the risk aversion coefficient, and the smaller the less risk averse the agent is. Comparing (41) with (39) and noting that always holds, the naïvetè’s expected terminal wealth is larger than the pre-committer’s when is small, and the former grows exponentially fast while the latter does only linearly in as . So a naïve policy ends up achieving a much higher expected terminal wealth than a pre-committed one which is also his originally planned target.101010This also reconciles with the previously proved fact that naïve policies are more exposed to the stock than equilibrium ones. However, this by no means implies that the former is superior to the latter because in an MV model there are two criteria and the variance is as important as the return. Indeed, it is straightforward to check that the naïve policy (28) is different from the unique pre-committed optimal policy (7) under the new expected terminal wealth (41), hence must be MV inefficient.111111Alternatively, one can calculate and show that it is strictly larger than the right hand side of (10) with the expected terminal wealth given by (41) and . In other words, lies off the efficient frontier (10). Details are left to interested readers. In other words, the naïve policy (28) takes more risk than it needs to - as dictated by the efficient frontier – in order to achieve a higher expected terminal wealth (41).

To sum, in the current MV setting, a naïve policy is more risk-loving than the other types of polices while expecting higher terminal wealth. Although at every it tries to follow the pre-committed optimal policy, the actual policy turns out to be very different. It is MV inefficient and certainly not “dynamically optimal” in any sense at any given .

4.2.2 The case

We now consider the case when , where (otherwise the problem (20)–(21) is trivial). The corresponding is which satisfies Assumption (A3). Substituting this into (28) we obtain the naïve policy

where the risky weight is

| (42) |

Next, it follows from (23) that the corresponding

| (43) |

where . Again, by Theorem 4.6 in Björk et al. (2014) we get the weak equilibrium policy of the problem (16)–(17) to be

where uniquely solves

| (44) |

Finally, by Theorem 1-i in He and Jiang (2022), the regular equilibrium policy for (20)–(21) is

where

| (45) |

Proposition 4

In the Black-Scholes market, if , then we have

for any .

Proof.

It follows from (44) that

| (46) | ||||

where we have utilized (37) to get the second inquality and noted the definition of to obtain the second to the last equality.

Next, applying the general inequality

we deduce

The proof is complete. ∎

We can also show that the naïve policy is not MV efficient with respect to any initial in the current case. Because the analysis is similar to that in the previous subsection, we omit the details here.

5 Conclusions

In this paper we define precisely and derive rigorously the policies implemented by a naïve agent, a notion originally put forth by Strotz (1956), for a continuous-time Markowitz model that is intrinsically time inconsistent. Such an agent attempts to optimize at any given time but, since optimal policies depend on when and where one makes them in a time-inconsistent problem, in effect constantly changes his policies. Ironically, the policy a naïveté actually executes may be anything but he originally desired. At any given time and state he sets an expected investment target and wants to achieve mean–variance efficiency but we show that his final policy ends up with a (much) higher target return and an even higher variance that overall becomes mean–variance inefficient. Moreover, naïve policies are universally riskier than their consistent planning counterparts.

Studying naïve behaviors in continuous-time problems is a nearly uncharted research area. From a behavioral economics perspective, it is fascinating to inquire and understand how an originally well-intended policy may go wrong or even go opposite when one insists on optimizing all the time. The definition of naïve policies and the approach to derive them in this paper is generalizable to other types of problems such as those with non-exponential discounting and probability weighting. As such, we hope the paper has also set a stage for further study of these problems.

Appendices

Appendix A Proof of Proposition 1

The main idea of the proof is to find a deterministic function to bound , which is stated in the following lemma.

Lemma 5

Let satisfying the following ODE

| (47) |

where

Then, we have, for every ,

Proof.

By Assumptions (A1)–(A3), it is clear that and .

Recall satisfies the SDE (12) on for . Applying Itô’s formula to and then taking conditional expectation on we obtain the (-wise) ODE

| (48) |

Consider a new stochastic process which satisfies the ODE on for :

| (49) |

Because , , a comparison theorem of ODEs yields

| (50) |

Now, we construct another stochastic process on for :

| (51) |

It follows from (49) that increases in ; hence for . Then, we get

| (52) | ||||

Comparing (51) and (52), we conclude from the Grownwall inequality that

| (53) |

To finish the proof we use mathematical induction on . When , , it follows from (50) and (53) that

| (54) |

Now, assume that when , the following holds:

| (55) |

| (56) | ||||

where the initial value of on is . However, (55) gives , whereas and satisfy the same ODE on . Thus on . Combining with (56), we get the desired result. ∎

Appendix B Proof of Theorem 1

Denote

which are all finite due to the boundedness assumptions in (A1) and (A2).

In order to prove Theorem 1, we need the following lemma.

Lemma 6

The process defined by (13) satisfies

Proof.

For , we bound the term as follows:

| (60) | ||||

For bounding the first term on the right side of the above, we have by the Cauchy–Schwartz inequality

| (61) | ||||

where the last inequality follows from Lemma 5 and the fact that is increasing in .

For the second term, by virtue of Itô’s isometry, we similarly have

| (62) |

Combining the above, we obtain

| (63) |

Thus,

as . ∎

Because , it follows from Mazur’s lemma that for each integer , there exists a positive integer and a convex combination , where and , such that

| (64) |

By the definition of , it satisfies the SDE

| (65) |

where

Consider the linear SDE

| (66) |

We now prove that

| (67) |

To this end, we first analyze . We have

| (68) | ||||

As a result,

| (69) |

We proceed to analyze and , respectively. First

| (70) | ||||

By the strong convergence of to , the first term above converges to as . For the second term,

| (71) | ||||

Now,

| (72) | ||||

where the last inequality follows from the convexity of the function . Because is continuous on , it is uniformly continuous. Hence, for any there is such that whenever with . For , we then have

| (73) | ||||

where the second inequality is by Lemma 5 and the proof of Lemma 6. Taking and then , we obtain

| (74) |

Combining (70), (71) and (74) yields

| (75) |

Moreover, according to the above analysis the bound of does not depend on ; thus the dominated convergence theorem gives

| (76) |

Employing Itô’s isometry we can derive similarly

| (77) |

By plugging (76) and (77) into (69) we establish (67), namely, . Thus, except on a zero measure set in the space of . It follows that satisfies the same SDE as or, equivalently, satisfies (14). Moreover, it is immediate that this wealth equation is generated by the feedback policy (15). The proof is complete.

References

- Barberis (2012) Barberis, N. A model of casino gambling. Management Science, 58:35–51, 2012.

- Basak and Chabakauri (2010) Basak, S. and Chabakauri, G. Dynamic mean-variance asset allocation. Review of Financial Studies, 23:2970–3016, 2010.

- Bielecki et al. (2005) Bielecki, T., Jin, H., Pliska, S., and Zhou, X. Continuous-time mean-variance portfolio selection with bankruptcy prohibition. Mathematical Finance, 15:213–244, 2005.

- Björk and Murgoci (2014) Björk, T. and Murgoci, A. A theory of markovian time-inconsistent stochastic control in discrete time. Finance and Stochastics, 18:545–592, 2014.

- Björk et al. (2014) Björk, T., Murgoci, A., and Zhou, X. Mean-variance portfolio optimization with state-dependent risk aversion. Mathematics Finance, 24:1–24, 2014.

- Chen and Zhou (2020) Chen, L. and Zhou, X. Naive strategies in a general linear quadratic model. Working Paper, 2020.

- Hakansson (1971) Hakansson, N. Multi-period mean-variance analysis: Toward a general theory of portfolio choice. The Journal of Finance, 26:857–884, 1971.

- He and Jiang (2022) He, X. and Jiang, Z. Mean–variance portfolio selection with dynamic targets for expected terminal wealth. Mathematics of Operations Research, pages 587–615, 2022.

- He and Zhou (2022) He, X. and Zhou, X. Who are I: Time inconsistency and intrapersonal conflict and reconciliation. Stochastic Analysis, Filtering, and Stochastic Optimization, Yin, G., Zariphopoulou, T. (eds), pages 177–208, 2022.

- Hu et al. (2022) Hu, S., Obloj, J., and Zhou, X. A casino gambling model under cumulative prospect theory: Analysis and algorithm. Management Science, page to appear, 2022.

- Hu et al. (2012) Hu, Y., Jin, H., and Zhou, X. Time-inconsistent stochastic linear-quadratic control. SIAM Journal on Control and Optimization, 50:1548–1572, 2012.

- Li and Ng (2000) Li, D. and Ng, W. Optimal dynamic portfolio selection: Multiperiod mean-variance formulation. Mathematical Finance,, 10:387–406, 2000.

- Li and Zhou (2006) Li, X. and Zhou, X. Continuous-time mean–variance efficiency: The 80% rule. Annals of Applied Probability, 16:1751–1763, 2006.

- Lim and Zhou (2002) Lim, A. E. B. and Zhou, X. Quadratic hedging and mean-variance portfolio selection with random parameters in a complete market. Mathematics of Operations Research, 27:101–120, 2002.

- Markowitz (1952) Markowitz, H. Portfolio selection. Journal of Finance, 7:77–91, 1952.

- Markowitz (1959) Markowitz, H. Portfolio Selection: Efficient Diversification of Investment. Wiley, New York, 1959.

- Pendersen and Peskir (2017) Pendersen, J. L. and Peskir, G. Optimal mean-variance portfolio selection. Mathematics and Financial Economics, 11:137–160, 2017.

- Richardson (1989) Richardson, H. R. A minimum variance result in continuous trading portfolio optimization. Management Science, 35:1045–1055, 1989.

- Strotz (1956) Strotz, R. H. Myopia and inconsistency in dynamic utility maximization. The Review of Economic Studies, 23:165–180, 1956.

- Xia (2005) Xia, J. Mean-variance portfolio choice: Quadratic partial hedging. Mathematical Finance, 15:533–538, 2005.

- Yong and Zhou (1999) Yong, J. and Zhou, X. Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer, New York, 1999.

- Zhou and Li (2000) Zhou, X. and Li, D. Continous-time mean-variance portfolio selection:a stochastic lq framework. Applied Mathematics, 42:19–33, 2000.