Jalan, Chakrabarti, and Sarkar

Incentive-Aware Models of Dynamic Financial Networks

Incentive-Aware Models of Financial Networks

Akhil Jalan \AFFDepartment of Computer Science, University of Texas at Austin, Austin, TX 78712, \EMAILakhiljalan@utexas.edu \AUTHORDeepayan Chakrabarti \AFFMcCombs School of Business, University of Texas at Austin, Austin, TX 78712, \EMAILdeepay@utexas.edu \AUTHORPurnamrita Sarkar \AFFDepartment of Statistics and Data Science, University of Texas at Austin, Austin, TX 78712, \EMAILpurna.sarkar@austin.utexas.edu

Financial networks help firms manage risk but also enable financial shocks to spread. Despite their importance, existing models of financial networks have several limitations. Prior works often consider a static network with a simple structure (e.g., a ring) or a model that assumes conditional independence between edges. We propose a new model where the network emerges from interactions between heterogeneous utility-maximizing firms. Edges correspond to contract agreements between pairs of firms, with the contract size being the edge weight. We show that, almost always, there is a unique “stable network.” All edge weights in this stable network depend on all firms’ beliefs. Furthermore, firms can find the stable network via iterative pairwise negotiations. When beliefs change, the stable network changes. We show that under realistic settings, a regulator cannot pin down the changed beliefs that caused the network changes. Also, each firm can use its view of the network to inform its beliefs. For instance, it can detect outlier firms whose beliefs deviate from their peers. But it cannot identify the deviant belief: increased risk-seeking is indistinguishable from increased expected profits. Seemingly minor news may settle the dilemma, triggering significant changes in the network.

financial networks; utility maximization; heterogeneous agents; dynamic games

1 Introduction

The financial crisis of showed the need for mitigating systemic risks in the financial system. There has been much recent work on categorizing such risks (Elliott et al. 2014, Glasserman and Young 2015, 2016, Birge 2021, Jackson and Pernoud 2021). While the causes of systemic risk are varied, they often share one feature. This shared feature is the network of interconnections between firms via which problems at one firm spread to others. One example is the weighted directed network of debt between firms. If one firm defaults on its debt, its creditors suffer losses. Some creditors may be forced into default, triggering a default cascade (Eisenberg and Noe 2001). Another example is the implicit network between firms holding similar assets. Sales by one firm can lead to mark-to-market valuation losses at other firms. These can snowball into fire sales (Caballero and Simsek 2013, Cont and Minca 2016, Feinstein 2020, Feinstein and Søjmark 2021).

The structure of inter-firm networks plays a vital role in the financial system. Small changes in network structure can lead to jumps in credit spreads in Over-The-Counter (OTC) markets (Eisfeldt et al. 2021). Network density, diversification, and inter-firm cross-holdings can affect how robust the networks are to shocks and how such shocks propagate (Elliott et al. 2014, Acemoglu et al. 2015). The network structure also affects the design of regulatory interventions (Papachristou and Kleinberg 2022, Amini et al. 2015, Calafiore et al. 2022, Galeotti et al. 2020).

Despite its importance, many prior works use simplistic descriptions of the network structure. For instance, they often assume that the network is fixed and observable. But only regulators may have access to the entire network. Furthermore, shocks or regulatory interventions can change the network. Others assume that the network belongs to a general class. For instance, Caballero and Simsek (2013) assume a ring network between banks. Amini et al. (2015) derive tractable optimal interventions for core-periphery networks. But financial networks can exhibit complex structure (Peltonen et al. 2014, Eisfeldt et al. 2021). Leverage levels, size heterogeneity, and other factors can affect the network topology (Glasserman and Young 2016). Hence, there is a need for models to help reason about financial networks.

In this paper, we design a model for a weighted network of contracts between agents, such as firms, countries, or individuals. The contracts can be arbitrary, and the edge weights denote contract sizes. In designing the model, we have two main desiderata. First, the model must account for heterogeneity between firms. This follows from empirical observations that differences in dealer characteristics lead to different trade risk exposures in OTC markets (Eisfeldt et al. 2021). Second, each firm seeks to maximize its utility and selects its contract sizes accordingly. In effect, each firm tries to optimize its portfolio of contracts (Markowitz 1952). The model must reflect this behavior. From this starting point, we ask the following questions:

-

1.

How does a network emerge from interactions between heterogeneous utility-maximizing firms?

-

2.

How does the network respond to regulatory interventions?

-

3.

How can the network structure inform the beliefs that firms hold about each other?

Next, we review the relevant literature.

Imputing financial networks. We often have only partial information about the structure of a financial network. For example, we may know the total liability of each bank in a network. From this, we want to reconstruct all the inter-bank liabilities (Squartini et al. 2018). One approach is to pick the network that minimizes KL divergence from a given input matrix (Upper and Worms 2004). Mastromatteo et al. (2012) use message-passing algorithms, while Gandy and Veraart (2017) use a Bayesian approach. But such random graph models often do not reflect the sparsity and power-law degree distributions of financial networks (Upper 2011). Furthermore, these models do not account for the utility-maximizing behavior of firms.

General-purpose network models. The simplest and most well-explored network model is the random graph model (Gilbert 1959, Erdös and Rényi 1959). Here, every pair of nodes is linked independently with probability . Generalizations of this model allow for different degree distributions and edge directionality (Aiello et al. 2000). Exponential random graph models remove the need for independence, but parameter estimation is costly (Frank and Strauss 1986, Wasserman and Pattison 1996, Hunter and Handcock 2006, Caimo and Friel 2011). Several models add node-specific latent variables to model the heterogeneity of nodes. For example, in the Stochastic Blockmodel and its variants, nodes are members of various latent communities. The community affiliations of two nodes determine their probability of linkage (Holland et al. 1983, Chakrabarti et al. 2004, Airoldi et al. 2008, Mao et al. 2018). Instead of latent communities, Hoff et al. (2002) assign a latent location to each node. Here, the probability of an edge depends on the distance between their locations.

All the latent variable models assume conditional independence of edges given the latent variables. But in financial networks, contracts between firms are not independent. Two firms will sign a contract only if the marginal benefit of the new contract is higher than the cost. This cost/benefit tradeoff depends on all other contracts signed with other firms. Unlike our model, existing general-purpose models do not account for such utility-maximization behavior.

Network games. Here, the payoffs of nodes are dependent on the actions of their neighbors (Tardos 2004). One well-studied class of network games is linear-quadratic games, with linear dynamics and quadratic payoff functions. Prior work has explored the stability of Nash equilibria (Guo and De Persis 2021) and algorithms to learn the agents’ payoff functions (Leng et al. 2020). But our model does not yield a linear-quadratic game except in exceptional cases. Instead, our process involves non-linear rational functions of the beliefs of firms. Thus, our setting differs from linear-quadratic games. Recently, network games have been extended to settings where the number of players tends to infinity (Carmona et al. 2022). However, we only consider finite networks.

Games to form networks. Several works study the stability of networks. In a pairwise-stable network, no pair of agents want to form or sever edges. This may be achieved via side-payments between agents, which our model also uses (Jackson and Wolinsky 2003). Pairwise stability has been extended to strong stability for networks (Jackson and Van den Nouweland 2005), and also to weighted networks with edge weights in (Bich and Morhaim 2020, Bich and Teteryatnikova 2022). We introduce an analogous notion called Higher-Order Nash stability against any deviating coalition. However, the weights in our network are not bounded in and can be negative. Furthermore, our edge weights denote contract size, requiring agreement from both parties. In contrast, prior works typically interpret edge weights as the engagement level in an ongoing interaction.

Sadler and Golub (2021) study a network game with endogenous network formation, whose stable points are both pairwise stable and Nash equilibria. We show similar results for our model. But they consider unweighted networks and focus on the case of separable games. In our setting, this corresponds to the case where all firms are uncorrelated. But in financial networks, correlations are widespread and help firms diversify their contracts.

Several authors study the effect of exogenous inputs on production networks (Herskovic 2018, Elliott et al. 2022). Acemoglu and Azar (2020) also model endogenous network formation but differ from our approach. Prices in their model equal the minimum unit cost of production. For us, prices are determined by pairwise negotiations between firms. Also, each firm in their model only considers a discrete set of choices among possible suppliers. In our model, firms can choose both their counterparties and the contract sizes.

Risk-sharing and exchange economies. The pricing of risk is a well-studied problem (Arrow and Debreu 1954, Bühlmann 1980, 1984, Tsanakas and Christofides 2006, Banerjee and Feinstein 2022). Most models typically price risk via a global market. However, in our model, all contracts are pairwise, and the contract terms and payments between a buyer and seller are bespoke. There is no global contract or global market price. Since contracts are pairwise, each firm under our model must consider counterparty risks and the correlations between them. A firm may make large payments and accept a negative reward for a contract with firm to diversify the risk from contracts with other firms. Finally, in our model, agents can hedge their risk by betting against one another. In contrast, Bühlmann equilibria always result in comonotonic endowments, which firms cannot use as hedges for each other (Banerjee and Feinstein 2022, Yaari 1987).

Network valuation adjustment. Some recent works price the risk due to exposure to the entire financial network (Banerjee and Feinstein 2022, Feinstein and Søjmark 2022). The network is usually treated as exogenous and fully known to all firms. In contrast, we consider endogenous network formation resulting from pairwise interactions between firms. The network valuation algorithm of Barucca et al. (2020) works with incomplete information, but is not designed for network formation, and it needs firms to share information not required to form their contracts.

Properties of equilibria. Another line of work considers the efficiency or social welfare of equilibria (Jackson and Pernoud 2021, Elliott and Golub 2022). Galeotti et al. (2020) show that welfare-maximizing interventions rely mainly on the top or bottom eigenvectors of the network. Elliott et al. (2022) show an efficiency-stability tradeoff for their model of supply network formation. Like prior work, we show that stable equilibria exist and are non-dominated. But our emphasis is on potentially valuable insights for regulators and firms. For instance, we show a negative result about the ability of regulators to infer the causes of changes to the network structure. The linkage between firms’ utilities and their beliefs, and its effect on stability, is not considered in prior work.

1.1 Our Contributions

We develop a new network model of contracts between heterogeneous agents, such as firms, countries, or individuals. Each agent aims to maximize a mean-variance utility parametrized by its beliefs. But for two agents to sign a contract, both must agree to the contract size. For a stable network, all agents must agree to all their contracts. We show that such constraints are solvable by allowing agents to pay each other. By choosing prices appropriately, every agent maximizes its utility in a stable network.

Characterization of stable networks (Section 2): We show that unique stable networks exist for almost all choices of agents’ beliefs. These networks are robust against actions by cartels, a condition that we call Higher-Order Nash Stability. The agents can also converge to the stable network via iterative pairwise negotiations. The convergence is exponential in the number of iterations. Hence, the stable network can be found quickly. Finally, we show how to infer the agents’ beliefs by observing network snapshots over time, under certain conditions.

The limits of regulation (Section 3): A financial regulator can observe the entire network but not the agents’ beliefs. Suppose firm changes its beliefs about firm . Then the contract size between and will change. Indirectly, other contracts will change too. We show empirically that in realistic settings, the indirect effects can be as significant as the direct effects. In such cases, the regulator cannot infer the underlying cause of changes in the network. Similarly, suppose the regulator intervenes with one firm, affecting its beliefs. The resulting network changes need not be localized to that firm’s neighborhood in the network. Thus, targeted interventions can have strong ripple effects. Broad-based interventions aimed at increasing stability can also have adverse effects. For instance, increasing margin requirements on contracts may even increase some contract sizes.

Outlier detection by firms (Section 4): A firm can observe its contracts with counterparties but not the entire network. Suppose another firm (say, a real-estate firm) has beliefs that are very different from its peers. Then, we prove that under certain conditions, ’s contract size with is also an outlier compared to other real-estate firms. So, firm can use the network to detect outliers and update its beliefs. But suppose all real-estate firms change their beliefs. This changes all their contract sizes without creating outliers. We show that cannot determine the cause of this change. For example, firm would observe the same change whether all real-estate firms had become more risk-seeking or profitable. However, firm may want to increase its exposure if they are more profitable but reduce exposure if they are more risk-seeking. Since the data cannot identify the proper action, firm remains uncertain. Exogenous, seemingly insignificant information may persuade firm one way or another. Thus, minor news may trigger drastic changes in the network.

Notation. We use lowercase letters, with or without subscripts, to denote scalars (e.g., ). Lowercase bold letters denote vectors (), and uppercase letters denote matrices (). We use to refer to the component of the vector , and for the cell of matrix . We use to denote the transpose of a vector , and to denote the norm of a vector or matrix. We say if is positive semidefinite, if it is positive definite, and if . The vectors denote the standard basis in , and is the identity matrix. If then denotes their tensor product: . For an appropriate matrix , calculates its trace, vectorizes by stacking its columns into a single vector, and vectorizes the upper-triangular off-diagonal entries of . For an integer , we use to denote the set of integers .

2 The Proposed Model

We consider a weighted network between agents (such as firms, countries, or individuals). The element represents the size of a contract between agents and . We make no assumptions about the content of the contract. For instance, the contract could be a interest rate swap, a stock swap, or an insurance contract. Since contracts need mutual agreement, . We take to represent ’s investment in itself. Note that a negative contract () is a valid contract that reverses the content of a positive contract. For example, if a positive contract is a derivative trade between two firms, the negative contract swaps the roles of the two firms.

Let denote the column of (i.e., for all ). Each agent would prefer to set its contract sizes to maximize its utility. But other agents will typically have different preferences. So, to achieve an agreement about the contract size , agents and can agree to adjust the terms of their contract. For example, may agree to pay an amount in cash at the beginning of the contract. Since payments are zero-sum and , we must have . More generally, we allow any adjustments that both agents consider to be equivalent to a cash transfer. For instance, in a loan contract, the borrower could pay extra interest over time, if the expected net present value of such interest payments is . We only consider adjustments where both agents agree on the expected net present value.

Each contract yields a stochastic payout, and agents have beliefs about these payouts. We represent agent ’s beliefs by a vector of expected returns and a covariance matrix . Thus, represents firm ’s perceived risk of trading with other firms, and includes both contract-specific risk and counterparty risk. Note that we do not assume that the contracts are zero-sum or that the beliefs are correct, even approximately. Thus, the overall expected return from all contracts of is , and the variance of the overall return is . We assume that each agent has a mean-variance utility (Markowitz 1952):

| (1) |

where is a risk-aversion parameter. In practice, we expect the set to be not too heterogeneous (Metrick 1995, Kimball et al. 2008, Ang 2014, Paravisini et al. 2017). Note that Eq. (1) ignores costs for contract formation; we will consider these in Section 3.1. Also, we assume that the contract adjustments do not change the perceived risk.

Example 2.1 (Loan contract)

Suppose borrower takes a loan of size from lender . Then, represents the lender ’s expected value for this loan, if it is under the “standard” terms. We allow each pair to define their own set of standard terms. The expected value depends on repayment schedule, the collateral, ’s estimate of the probability of default, the recovery rate in case of default, etc. The borrower’s expected value depends on the planned use of this loan. For example, if the loan is meant to purchase equipment, is the net present value of expected extra profits due to that equipment. Hence, may not be a function of . Now, to achieve agreement on the contract size, the borrower and lender may choose to deviate from the standard terms. For example, the loan may be callable, or have a higher interest rate than usual. Then is the net present value of these deviations for the lender .

Example 2.2 (Interest rate swap contract)

Suppose firm makes fixed-rate payments to firm , and receives floating-rate payments in return. Then, is the expected net present value of these payments for from a standard unit-sized contract. This value depends ’s forecast of future interest rates and need for floating-rate income, e.g., to match future liabilities. Hence, it may be quite different from . Now, firms and may adjust the standard terms. For example, firm could agree to pay firm a higher fixed rate than the standard rate. This corresponds to extra cash transfers over the contract’s lifetime with an expected net present value of .

Example 2.3 (Insurance Contract)

Suppose firm buys fire insurance from insurer . Then, is the buyer’s expected insurance payout minus the insurance premium. The expected payout depends on the probability of a fire, for which the buyer and insurer may have different estimates. Also, the insurance contract is negatively correlated with the buyer’s other contracts (reflected in ). This is because the buyer gains a payout from the insurer in case of a fire, but incurs losses on other contracts. Hence, the buyer may be willing to accept a contract with negative expected reward, and even pay a higher-than-usual premium per contract.

The model above allows contracts between all pairs of agents. But some edges may be prohibited due to logistical or legal reasons. For each agent , let denote the ordered set of agents with whom can form an edge. So, if (and hence ), we have . Similarly, if , then self-loops are prohibited (). We will encode these constraints in the binary matrix where if is the element of , and otherwise. In other words, is obtained from by deleting the rows corresponding to the prohibited counterparties of . Thus, for any , selects the elements of corresponding to . If all edges are allowed, we have for all .

Definition 2.4 (Network Setting)

A network setting captures the beliefs and constraints of agents. When there are no constraints (i.e., all edges are allowed), we drop the terms to simplify the exposition. Finally, we will use to denote a matrix whose column is , and to denote a diagonal matrix with .

2.1 Characterizing Stable Points

In the above model, every agent tries to optimize its own utility (Eq.(1)). We now characterize the conditions under which selfish utility-maximization leads to a stable network.

Definition 2.5 (Feasibility)

A tuple is feasible if , , and and obey the constraints encoded in .

Definition 2.6 (Stable point)

A feasible is stable if each agent achieves its maximum possible utility given prices :

Example 2.7

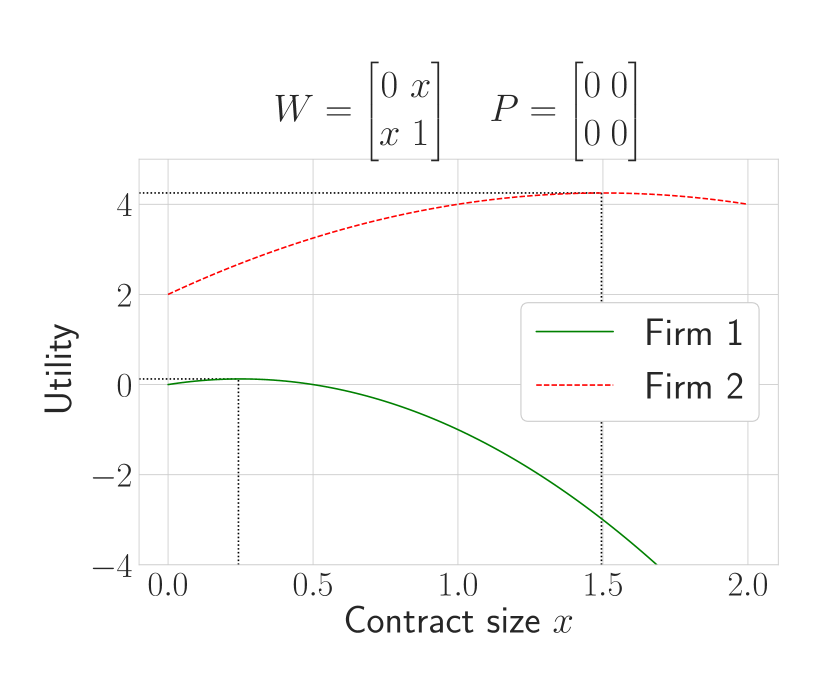

Suppose we only have two firms with the following setting:

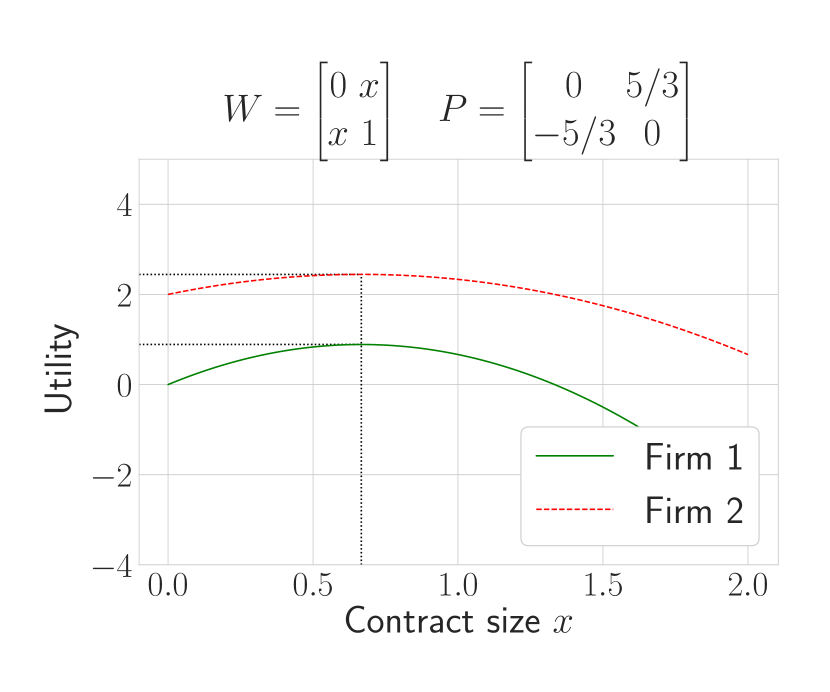

So, both firms perceive a benefit from trading (). If trading is disallowed, the optimum is diagonal with and (and is the zero matrix). The corresponding utilities are for firm and for firm . Suppose we allow trading but do not allow pricing (Figure 1(a)). Then, the two firms can each improve their utility by trading, but achieve their optimum utilities at different contract sizes. Hence, they may be unable to agree to a contract. In Figure 1(b), firm pays firm a specially chosen price of per unit contract. At this price, both firms achieve their optimum utilities at the same contract size . Hence, they can agree to a contract. By paying the price, firm shares some of its utility with firm to achieve agreement on the contract. This choice of and is a stable point (Figure 1(c)). The following results show that this is the only stable point.

Define . When all edges are allowed, and . Let denote the ordered pairs where is allowed to be non-zero. Note that . For any matrix , let be a vector whose entries are the ordered set .

Theorem 2.8 (Existence and Uniqueness of Stable Point)

Define matrices , , and as follows:

Let be the matrix whose rows are the ordered sets . A stable point exists under if and only if lies in the column space of .

Theorem 2.8 shows that a full-rank is sufficient for the existence of a stable point (Appendix 7.2 shows an example). Furthermore, when the are random variables, we give a simple sufficient condition that a stable point exists and is unique with probability (see Appendix 7.3). Also, we provide closed-form formulas for the stable point when all agents have the same covariance ( for all ) (see Appendix 7.4). This occurs when the risk of a contract is primarily counterparty risk (so depends on and , not ) and there is reliable public data on such risks (say, via credit rating agencies).

Next, we consider some properties of the stable point. For two feasible tuples and , let dominate if for all , with at least one inequality being strict.

Theorem 2.9 (Stable points cannot be dominated)

Suppose a stable point exists. Then, there is no feasible that dominates .

The stable point obeys a strong form of robustness that we call Higher-Order Nash Stability. This strengthens the notions of pairwise stability (Hellmann 2013) and pairwise Nash (Calvó-Armengol and Ilkılıç 2009, Sadler and Golub 2021) by allowing for agent coalitions, instead of just considering pairs of agents. It is also closely related to the concept of Strong Nash equilibrium, which strengthens Nash equilibrium by requiring that no subset of agents can deviate at equilibrium without at least one agent being worse off (Mazalov and Chirkova 2019).

Definition 2.10 (Agent Action)

At a given feasible point , an “action” by agent is the ordered set , where is the set of permissible edges for agent . The action represents a set of proposed changes to ’s existing contracts. Each agent responds as follows:

-

1.

If the new raises ’s utility, then agrees to the revised contract and price.

-

2.

Otherwise, must either keep the existing contract or cancel it (). We assume that cancels the contract if and only if this strictly increases ’s utility.

We call the shifted the resulting network.

Definition 2.11 (Higher-Order Nash Stability)

A feasible is Higher-Order Nash Stable if:

-

1.

Nash equilibrium: No agent has an action such that the resulting network is strictly better for .

-

2.

Cartel robustness: For any proper subset of agents, there is no feasible point that differs from only for indices with such that all agents in have higher utility under than .

Theorem 2.12 (Higher-Order Nash Stability)

Any stable point is Higher-Order Nash Stable.

2.2 Finding the Stable Point via Pairwise Negotiations

To compute the stable point in Theorem 2.8, we must know the beliefs of all agents. But in practice, contracts are set iteratively by negotiations among pairs of agents. We will now formalize the process of pairwise negotiations and characterize the conditions under which such negotiations can converge to the stable point.

We propose a multi-round pairwise negotiation process. In round , every pair of agents and update the price to (and hence to ) as follows. First, they agree to a price between themselves, assuming optimal contract sizes with all other agents at the current prices . In other words, we assume that the other agents will accept the prices in and the contract sizes preferred by and . Under this condition, is the price at which ’s optimal contract size with is also ’s optimal size with . We provide an explicit formula for in Appendix 7.7. All pairs of agents calculate these prices simultaneously. We create a new price matrix from these prices. Then, we set , where is a dampening factor chosen to achieve convergence. Algorithm 1 shows the details.

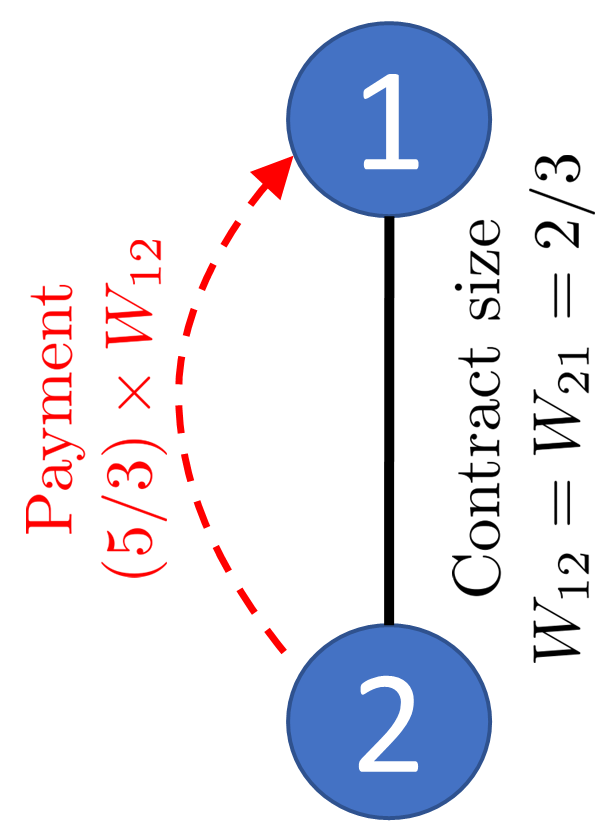

Example 2.13 (Pairwise negotations for loan contracts.)

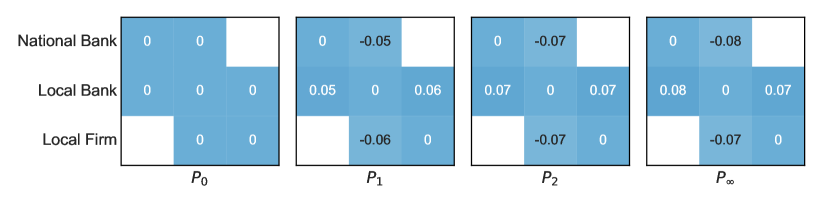

Consider a -firm loans network containing a national bank (firm 1), local bank (firm 2), and local firm (firm 3). Suppose that the local firm cannot access the national bank, so the edge between firms and is prohibited. The other parameters are:

Figure 2 shows how pairwise negotiations via Algorithm 1 quickly converge to the stable network.

Now, we will show that Algorithm 1 converges. First, we define global asymptotic stability (following Callier and Desoer (1994)).

Definition 2.14 (Global Asymptotic Stability)

The pairwise negotiation process is globally asymptotically stable for a given network setting and dampening factor if, for any initial price matrix , there exists a matrix such that the sequence of price matrices converges to in Frobenius norm: .

When pairwise negotiations are globally asymptotically stable, the limiting matrix must be skew-symmetric since each is skew-symmetric. Also, since prices are updated whenever two agents disagree on the size of the contract between them, all agents agree on their contract sizes at . Hence, must be a stable point for the given network setting.

Now, we show that for a range of , pairwise negotiations are globally asymptotically stable (Appendix 7.9 presents an example).

Theorem 2.15 (Convergence Conditions and Rate)

Let be defined as in Theorem 2.8. Define the following matrices:

| ( is diagonal). | ||||

Let denote the pseudoinverse of , and denote the principal submatrix of containing the rows/columns such that the edge is not prohibited. Let be the largest and smallest eigenvalues of the matrix respectively. Let . Then, we have:

-

1.

For all , pairwise negotiations with are globally asymptotically stable.

-

2.

For such an , the convergence is exponential in the number of rounds :

Here, is the stable point to which the negotiation converges.

2.3 Pairwise Negotiations under Random Covariances

So far we have made no assumptions about agents’ beliefs. In this section, we analyze the convergence of pairwise negotiations for “data-driven” agents. Specifically, each agent now estimates its covariance matrix. For this section only, we will call the covariance matrix instead of to emphasize that it is an estimated quantity.

Suppose each agent observes independent data samples. Each sample is a vector of the returns of unit contracts with all agents. The samples for agent are collected in a matrix , with one column per sample. The sample covariance of this data is .

We assume that all agents observe samples from the same return distribution, which has covariance . Under a wide range of conditions, in probability (Vershynin 2018). Hence, at convergence, the maximum allowed dampening rate in Theorem 2.15 would be a function of . But for finite sample sizes, each agent’s can be different. Hence, the maximum dampening may be less than . The smaller the , the worse the rate of convergence of pairwise negotiations. However, even with a few samples, is close to , as the next theorem shows.

Theorem 2.17 (Small Sample Sizes are Sufficient for Fast Convergence)

Suppose that and are with respect to and all edges are allowed. Also, suppose that each sample column of is drawn independently from a distribution, and let and . Let be the maximum dampening factor using as defined in Theorem 2.15. Let be the dampening factor if were replaced by for all . If , then for large enough , with probability at least .

Theorem 2.17 shows that data-driven agents using a broad range of dampening factors are still likely to find the stable point via pairwise negotiations. Furthermore, the amount of data they need is comparable to the number of agents (up to a logarithmic factor). We note that if firms use datasets of fixed sizes , then the conclusion of Theorem 2.17 still holds, as long as . For example, firms might use different look-back periods for covariance estimation.

2.4 Inferring Beliefs from the Network Structure

Suppose we are given a network that lies at a unique stable point as defined in Theorem 2.8. How can we infer the beliefs of the agents?

Non-identifiability of beliefs.

Suppose we are given a network that is generated using a single covariance . We want to infer the agents’ beliefs . By Corollary 7.8,

Clearly, the agents’ beliefs can only be specified up to an appropriate scaling of , , and . But even if we specify a scale (e.g., ), for any valid choice of and we can find a corresponding . Thus, even in the simple setting of identical covariance and fixed scale, the network cannot be used to select a unique combination of the parameters . By a similar argument, we cannot identify the underlying beliefs even if we observe multiple networks generated using the same and (but different ). Thus, we need further assumptions in order to infer beliefs.

Consider a sequence of networks over timesteps . We assume that (a) and for all , (b) for all , varies independently according to a Brownian motion with the same parameters for all , and (c) .

The first assumption is motivated by the observations in portfolio theory that errors in mean estimation are far more significant than covariance estimation errors (Chopra and Ziemba 2013). So, accounting for variations in may be less important than variations in (but see Remark 2.19 below). The homogeneity of risk aversion was noted in Section 2, and this justifies setting . The second assumption is common in the literature on pricing models (Geman et al. 2001, Bianchi et al. 2013). The third assumption fixes the scale, as discussed above.

Proposition 2.18

Finding the maximum likelihood estimator of under Assumption 2.4 is equivalent to the following Semidefinite Program (SDP):

Remark 2.19 (Generalization to time-varying )

Instead of a constant covariance , the time range may be split into intervals, with covariance in interval . Then, we can add a regularizer for some to the objective of the SDP to penalize differences between successive covariances. This allows the covariance to evolve while keeping the objective convex. The time intervals can be tuned based on heuristics or prior information.

3 Insights for Regulators

A financial regulator can observe the network but does not know the firms’ beliefs. The regulator may ask: what changes in beliefs caused recently observed changes in the network? What are the side effects of different regulatory interventions? To answer these questions, we need to know how changes in firms’ beliefs or utility functions affect the network. That is the subject of this section.

3.1 Effect of Friction in Contract Formation

Our model imposes no costs for contract formation. This is reasonable for large firms where the fixed costs associated with contract negotiations may be small relative to the contract sizes. However, in an overheating market, a regulator may impose frictions by penalizing large contracts, for example by increasing margin requirements.

We model contract costs via an adding a penalty term to the utility of agent in Eq. (1):

| (2) |

Theorem 3.1

Consider a network setting where and all edges are allowed. Suppose that for each firm , the function is twice differentiable, and there exist strictly increasing functions such that for all , . Then, there exists a unique stable point.

Example 3.2

By imposing frictions, the regulator may increase the sizes of certain contracts. For example, let for some . Thus, the cost of inter-firm trades scales with the square of the contract size (we assume ). Consider a network setting with firms, with , , and . Then, without frictions (when ) but for .

3.2 Effect of Changes in Firms’ Beliefs

Regulatory actions can change the risk and expected return perceptions of firms. The next theorem shows the effect of such belief changes on the stable point.

Theorem 3.3

Suppose for all firms, and let be the matrix of expected returns.

-

1.

Change in beliefs about expected returns: Let have the eigendecomposition . Then for ,

(3) In particular, is monotonically increasing with respect to .

-

2.

Risk scaling: If the covariance changes to (), then changes to .

-

3.

Increase in perceived risk: Suppose for all , and the covariance increases to . Let and be the stable points under and respectively. Then,

This shows that, in general, an increase in risk leads to a decrease in the weighted average of the contract sizes. The weights are given by the expected return beliefs of the firms. However, individual contracts between firms can increase, as can the norm . This is because increases in the covariance may also increase correlations, which can offer better hedging opportunities. By hedging some risks, larger contract sizes can be supported.

Theorem 3.3 also shows that a change in the perceived expected return affects all contracts . Can we trace the changes in back to the underlying changes in ? For instance, consider the following problem.

Definition 3.4 (Source Detection Problem)

Suppose that a financial regulator observes two networks and , with the only difference being a small change in a single entry of (say, ). Can the regulator identify the pair ?

One approach is to try to infer all beliefs of all firms, and then identify the changed belief. But, as discussed in Section 2.4, the beliefs are only identifiable under extra assumptions and more data. An alternative approach for the source detection problem is to find the entry with the largest change . The intuition is that a change in has a direct effect on and (hopefully weaker) indirect effects on other contracts. Thus, the source detection problem is closely tied to the following:

Definition 3.5 (Targeted Intervention Problem)

Can a regulator induce a small change in a single entry of (say, ) such that the change in is significantly larger than changes in other entries of ?

When all eigenvalues of are equal (that is, ), a change in only affects , as can be seen from Corollary 7.8. But when the eigenvalues are skewed, the terms in Eq. (3) corresponding to the smallest eigenvalues have greater weight. In such circumstances, the indirect effect of a change in on other can be significant. The following empirical results show that this is indeed the case.

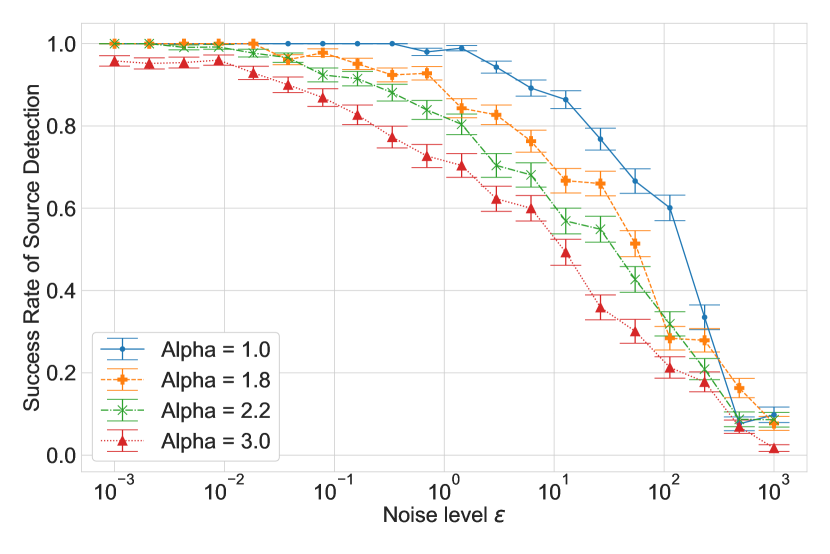

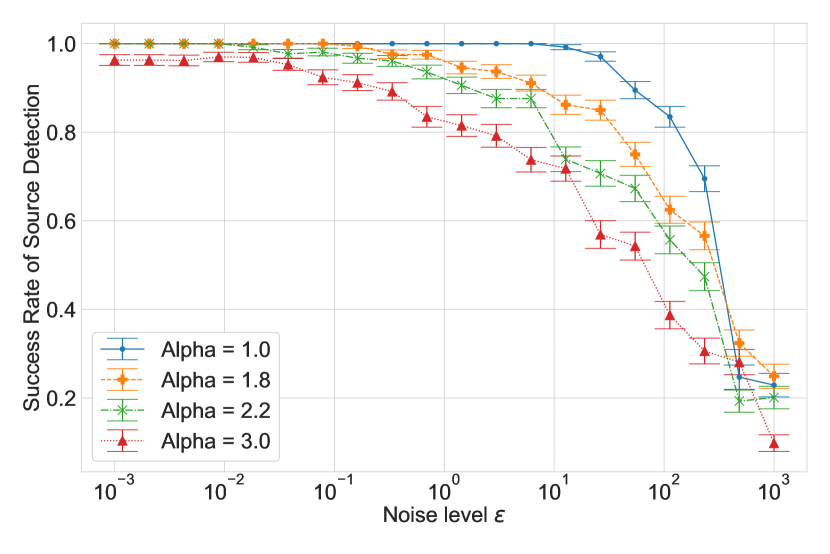

Empirical Results for the Source Detection Problem (Simulated Data). Here, we set the covariance , where is a diagonal matrix, a correlation matrix, and a noise matrix. If , then would be the variance of firm . We set according to a power law: for an . Larger values of correspond to greater skew in the variances. We choose to be an equi-correlation matrix with along the diagonal and everywhere else. We draw the error matrix from a scaled Wishart distribution: for some chosen the noise level . As increases, the noise dominates .

Figure 3 shows the success rate of source detection over experiments for various values of for and . As increases, the variances become more skewed and the source detection can fail even with noise. When grows, the success rate for the source detection problem goes to zero. This suggests that skew combined with noise makes source detection difficult. These trends occur even if we only test whether the source belongs to the most changed contracts (Figure 3(b)), as opposed to single largest change (Figure 3(a)). We observe similar results for real-world choices of , as we show next.

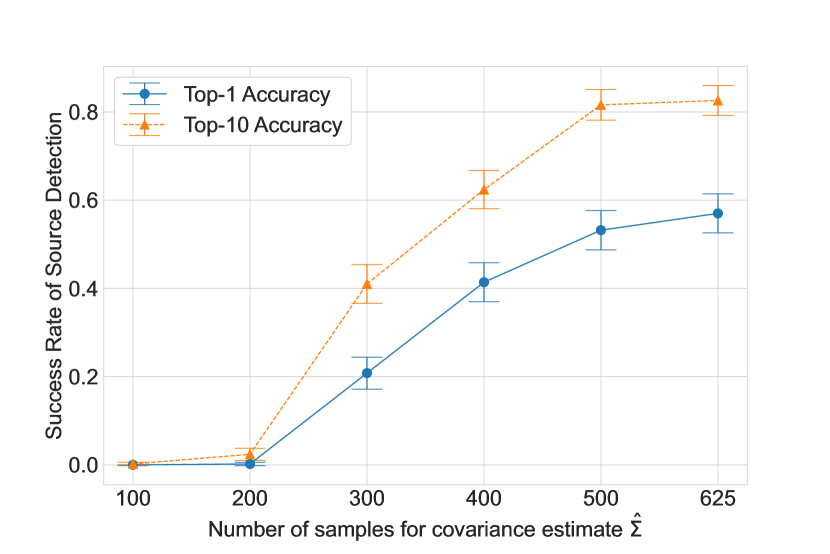

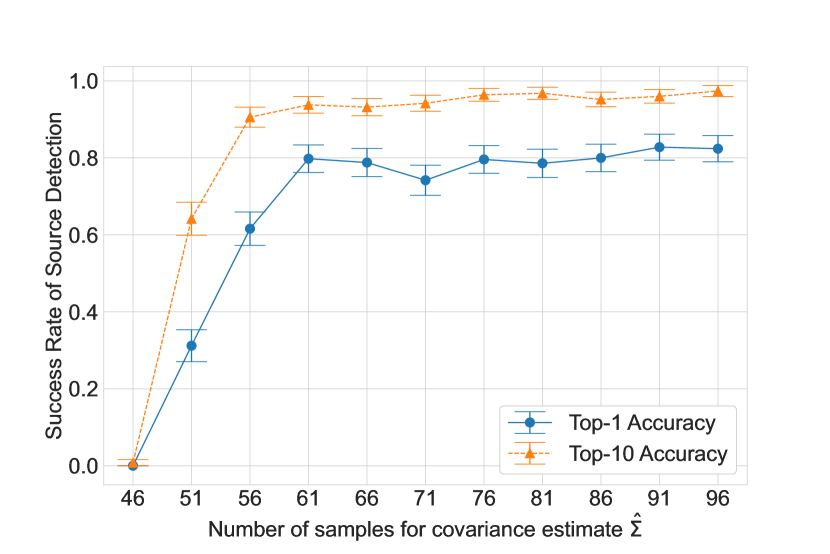

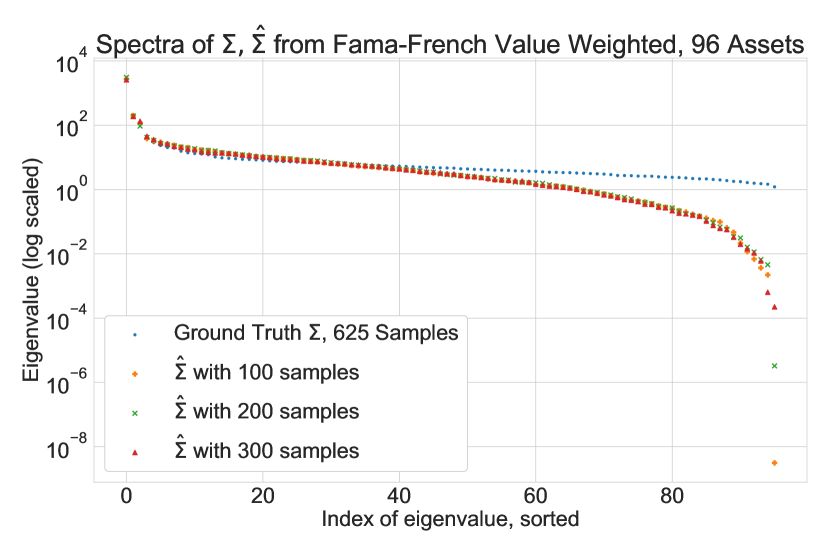

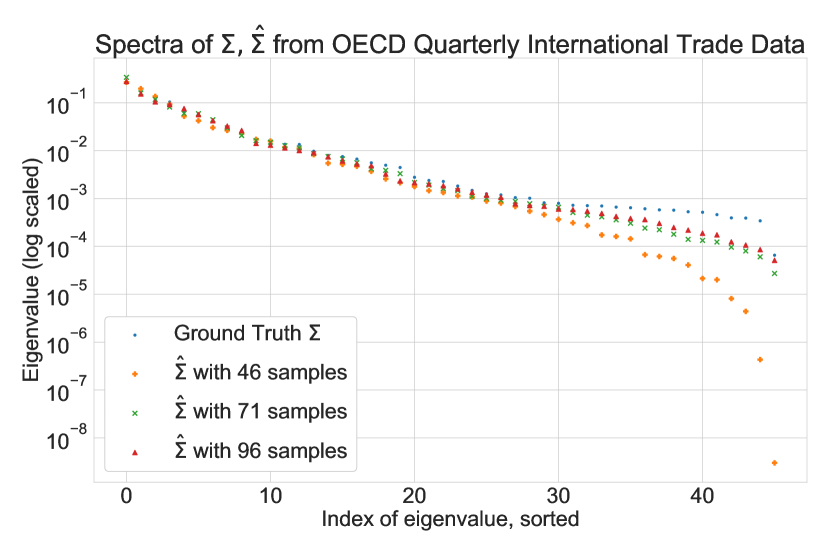

Empirical Results for the Source Detection Problem (Real-World Data). We consider two datasets: (a) a trade network between large economies (OECD 2022), and (b) a simulated network between portfolio managers following various Fama-French strategies Fama and French (2015). For each dataset, we construct a “ground-truth” covariance using all available data (the details are in in Appendix 8). Then, using independent samples , we build a “data-driven” covariance , where is the sample mean. We use this to construct the financial network.

Figure 4 shows the success rate over experiments for various choices of the sample size . The success rate increases monotonically with . The reason for this behavior lies in the spectra of and . We find that in both datasets, the largest and smallest eigenvalues of are separated by several orders of magnitude. This gap becomes even more extreme in the data-driven ; the fewer the samples , the greater the gap (see Figure 5). In fact, we observe that the smallest eigenvalue of is much smaller than the second-smallest eigenvalue: . Zhao et al. (2019) make similar observations.

In summary, the experiments on both simulated and real-world datasets highlight the difficulty of source detection and targeted intervention in realistic networks. The reason is the skew in the eigenvalues coupled with noise, which affects the eigenvectors. Skewed eigenvalues correspond to trade combinations (eigenvectors) that are seemingly low-risk. Hence, firms use such trades to diversify. This implies that these eigenvectors have an outsized effect on the network, and how it responds to local changes. Intuitively, if these eigenvectors are “random,” the effect of a changed belief affects the rest of the network randomly. Hence, the direct effects on may be less than the indirect effects on other . We explore this theoretically in Appendix 7.14.

4 Insights for Firms

Until now, we have treated the beliefs of firms as fixed and exogenous. In this section, we consider how a firm can use its contracts to gain insights into other firms and update its beliefs.

For instance, suppose a firm faces a crisis, e.g., a looming debt payment that may make it insolvent. The firm may then become risk-seeking (i.e., lower its ), hoping that the risks pay off. Another firm may be unaware of the crisis, so ’s risk perceptions (perhaps based on historical data) would be outdated. Can firm infer the lower , solely from ’s contracts with all firms? What if a group of firms become risk-seeking, and not just one firm?

4.1 Detecting Outlier Firms

Intuitively, firm will try to answer these questions by comparing the behavior of firm against other similar firms. We formalize this by assuming that each firm belongs to a community , e.g., banking, or real-estate, or insurance, etc. The community of each firm is publicly known. Firms in the same community are perceived to have similar return distributions:

| (4) |

for some unknown deterministic functions , , and and random error terms and . We also assume that all firms use the same covariance .

Now, suppose one firm is an outlier, with very different beliefs from other firms in its community. For firm to detect the outlier firm , the contract size should deviate from a cluster of contracts of other firms from the same community as firm . Now, outlier detection methods often assume independent datapoints. In our model, all contracts are dependent. But we can still do outlier detection if the contracts are appropriately exchangeable. We prove below this is the case.

Definition 4.1

An intra-community permutation is a permutation such that implies that .

Proposition 4.2

Suppose exhibit community structure (Eq. (4)), and all the error terms and are independent and identically distributed. Let be any intra-community permutation, and let be the corresponding column-permutation matrix: . Then, and are identically distributed.

Corollary 4.3

Let belong to the same community: . Suppose the conditions of Proposition 4.2 hold. Then, for any , the joint distribution of is exchangeable.

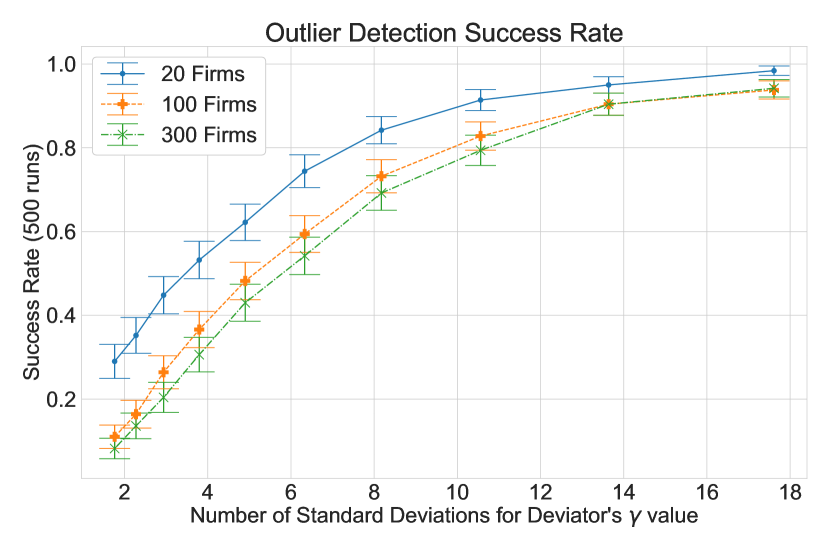

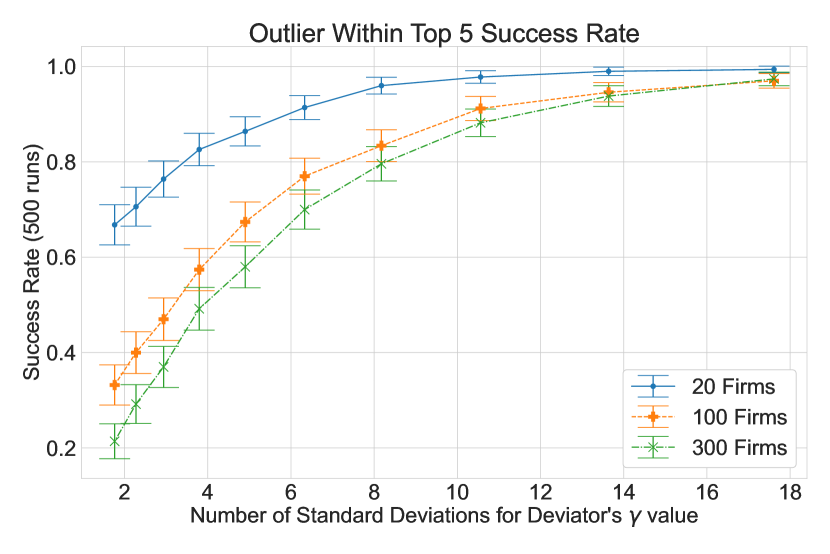

Empirical Results for Outlier Detection. We generate community-based networks (Eq. (4)) such that truncated to . The smaller the , the more closely the values cluster around . For the outlier risk-seeking firm, we set . For clarity of exposition, we set everywhere.

To detect outliers under exchangeability (Corollary 4.3), we can use methods based on conformal prediction (Guan and Tibshirani 2022). Here, we use a simpler approach: pick the firm with the largest contract size as the outlier; . To test sensitivity to false negatives, we also test whether the outlier is among the 5 largest contracts in . We run experiments for each choice of , and count the frequency with which the outlier firm is detected via its contract size. Further details are presented in Appendix 8.3.

Figure 6 shows the results. We characterize the degree of outlierness by how many standard deviations away is from the baseline of . The smaller the , the more the outlierness. The success rate increases with increasing outlierness, as expected. It also increases when the number of firms is reduced. This is because contract sizes depend on the values of all firms; fewer firms reduces the chances of any one firm attaining large contract sizes due to randomness.

4.2 Risk-Aversion versus Expected Returns

The discussion above shows that a firm can detect outlier counterparties. However, the firm cannot determine why the counterparty is an outlier, as the following theorem shows.

Theorem 4.4 (Non-identifiability of risk-aversion versus expected returns)

Consider two network settings and which differ only in the risk-aversions of firms . Then, there exists a setting such that for all and the stable networks under and are identical.

Thus, one cannot determine if an outlier is more risk-seeking than its community or expects higher profits. But risk-seeking behavior may be indicative of stress, while higher profits than similar firms are unlikely. Hence, in either case, the firm detecting the outlier may choose to reduce its exposure to the outlier. However, this approach fails if an entire community shifts its behavior. The following example illustrates the problem.

Example 4.5

Consider two communities numbered and , with and firms respectively. Let the setting of Theorem 4.4 correspond to

Now, suppose that under setting , for some small for all nodes in community . The change in the network would be the same if we had updated the columns corresponding to community in the matrix instead (setting ):

Thus, a firm from community cannot determine if the network change was due to a change in or . For instance, when , an increase in risk-seeking () looks the same as an increase in trading benefits (). In the former case, firms in community should reduce their exposure to community firms. But in the latter case, they should increase exposure. Since the data cannot be used to choose the appropriate action, the behaviors of firms may be guided by their prior beliefs or inertia. When such beliefs change due to external events (e.g., due to news about one firm in community ), the resulting change in the network may be drastic.

5 Conclusions

We have proposed a model of a weighted undirected financial network of contracts. The network emerges from the beliefs of the participant firms. The link between the two is utility maximization coupled with pricing. For almost all belief settings, our approach yields a unique network. This network satisfies a strong Higher-Order Nash Stability property. Furthermore, the firms can converge to this stable network via iterative pairwise negotiations.

The model yields two insights. First, a regulator is unable to reliably identify the causes of a change in network structure, or engage in targeted interventions. The reason is that firms seek to diversify risk by exploiting correlations. We find that in realistic settings, there are often combinations of trades that offer seemingly low risk. Hence, all firms aim to use such trades. The over-dependence on a few such combinations leads to a pattern of connections between firms that thwarts targeted regulatory interventions.

The second insight is that firms can use the network to update their beliefs. For instance, they can identify counterparties that behave very differently from their peers. However, the cause of the outlierness remains hidden. If all firms in one line of business become more risk-seeking, the result is indistinguishable from that business becoming more profitable. Innocuous events (such as a news story) may cause beliefs to change suddenly, leading to drastic changes in the network. In addition to identifying risky counterparties, firms may use the network to update their mean and covariance beliefs. For example, a firm that suffers significant losses on its current trades may be judged by others to be a riskier counterparty for future trades. We leave this for future work.

Our work focuses on mean-variance utility, but some of our results are applicable in other settings too. A second-order Taylor approximation of a twice-differentiable concave utility matches the form of a mean-variance utility. Hence, results based on mean-variance utility can be useful guides for small perturbations around a stable point. Some of our results for pairwise negotiations and targeted interventions are based on such perturbation arguments.

6 Acknowledgments

The authors thank Stathis Tompaidis, Marios Papachristou, Kshitij Kulkarni, and David Fridovich-Keil for valuable discussions and suggestions. This work was supported by NSF grant 2217069, a McCombs Research Excellence Grant, and a Dell Faculty Award.

References

- Acemoglu and Azar (2020) Acemoglu D, Azar PD (2020) Endogenous production networks. Econometrica 88(1):33–82.

- Acemoglu et al. (2015) Acemoglu D, Ozdaglar A, Tahbaz-Salehi A (2015) Systemic risk and stability in financial networks. American Economic Review 105(2):564–608.

- Aiello et al. (2000) Aiello W, Chung F, Lu L (2000) A random graph model for massive graphs. Proceedings of the 32nd Annual ACM Symposium on Theory of Computing (STOC ’00), 171–180.

- Airoldi et al. (2008) Airoldi EM, Blei DM, Fienberg SE, Xing EP (2008) Mixed membership stochastic blockmodels. Journal of Machine Learning Research 9:1981–2014.

- Amini et al. (2015) Amini H, Minca A, Sulem A (2015) Control of interbank contagion under partial information. SIAM Journal on Financial Mathematics 6(1):1195–1219.

- Ang (2014) Ang A (2014) Asset management: A systematic approach to factor investing.

- Arrow and Debreu (1954) Arrow KJ, Debreu G (1954) Existence of an equilibrium for a competitive economy. Econometrica: Journal of the Econometric Society 265–290.

- Banerjee and Feinstein (2022) Banerjee T, Feinstein Z (2022) Pricing of debt and equity in a financial network with comonotonic endowments. Operations Research 70(4):2085–2100.

- Barucca et al. (2020) Barucca P, Bardoscia M, Caccioli F, D’Errico M, Visentin G, Caldarelli G, Battiston S (2020) Network valuation in financial systems. Mathematical Finance 30(4):1181–1204.

- Bianchi et al. (2013) Bianchi S, Pantanella A, Pianese A (2013) Modeling stock prices by multifractional brownian motion: an improved estimation of the pointwise regularity. Quantitative finance 13(8):1317–1330.

- Bich and Morhaim (2020) Bich P, Morhaim L (2020) On the existence of pairwise stable weighted networks. Mathematics of Operations Research 45(4):1393–1404.

- Bich and Teteryatnikova (2022) Bich P, Teteryatnikova M (2022) On perfect pairwise stable networks. Journal of Economic Theory 105577.

- Birge (2021) Birge JR (2021) Modeling investment behavior and risk propagation in financial networks. Available at SSRN 3847443 .

- Bühlmann (1980) Bühlmann H (1980) An economic premium principle. ASTIN Bulletin: The Journal of the IAA 11(1):52–60.

- Bühlmann (1984) Bühlmann H (1984) The general economic premium principle. ASTIN Bulletin: The Journal of the IAA 14(1):13–21.

- Caballero and Simsek (2013) Caballero RJ, Simsek A (2013) Fire sales in a model of complexity. The Journal of Finance 68(6):2549–2587.

- Caimo and Friel (2011) Caimo A, Friel N (2011) Bayesian inference for exponential random graph models. Social Networks 33(1):41–55.

- Calafiore et al. (2022) Calafiore GC, Fracastoro G, Proskurnikov AV (2022) Control of dynamic financial networks. IEEE Control Systems Letters .

- Callier and Desoer (1994) Callier FM, Desoer CA (1994) Linear System Theory (Springer Verlag).

- Calvó-Armengol and Ilkılıç (2009) Calvó-Armengol A, Ilkılıç R (2009) Pairwise-stability and nash equilibria in network formation. International Journal of Game Theory 38(1):51–79.

- Carmona et al. (2022) Carmona R, Cooney DB, Graves CV, Lauriere M (2022) Stochastic graphon games: I. The static case. Mathematics of Operations Research 47(1):750–778.

- Chakrabarti et al. (2004) Chakrabarti D, Zhan Y, Faloutsos C (2004) R-MAT: A recursive model for graph mining. Proceedings of the 4th SIAM International Conference on Data Mining (SDM ’04), 442–446.

- Chopra and Ziemba (2013) Chopra VK, Ziemba WT (2013) The effect of errors in means, variances, and covariances on optimal portfolio choice. Handbook of the fundamentals of financial decision making: Part I, 365–373.

- Cont and Minca (2016) Cont R, Minca A (2016) Credit default swaps and systemic risk. Annals of Operations Research 247(7):523–547.

- Eisenberg and Noe (2001) Eisenberg L, Noe TH (2001) Systemic risk in financial systems. Management Science 47(2):236–249.

- Eisfeldt et al. (2021) Eisfeldt AL, Herskovic B, Rajan S, Siriwardane E (2021) OTC intermediaries. Research Paper 18-05, Office of Financial Research.

- Elliott and Golub (2022) Elliott M, Golub B (2022) Networks and economic fragility. Annual Review of Economics 14:665–696.

- Elliott et al. (2014) Elliott M, Golub B, Jackson MO (2014) Financial networks and contagion. American Economic Review 104(10):3115–53.

- Elliott et al. (2022) Elliott M, Golub B, Leduc MV (2022) Supply network formation and fragility. American Economic Review 112(8):2701–47.

- Erdös and Rényi (1959) Erdös P, Rényi A (1959) On random graphs I. Publicationes Mathematicae 6:290–297.

- Fama and French (2015) Fama EF, French KR (2015) A five-factor asset pricing model. Journal of financial economics 116(1):1–22.

- Feinstein (2020) Feinstein Z (2020) Capital regulation under price impacts and dynamic financial contagion. European Journal of Operational Research 281(2):449–463.

- Feinstein and Søjmark (2021) Feinstein Z, Søjmark A (2021) Dynamic default contagion in heterogeneous interbank systems. SIAM Journal on Financial Mathematics 12(4):SC83–SC97.

- Feinstein and Søjmark (2022) Feinstein Z, Søjmark A (2022) Endogenous network valuation adjustment and the systemic term structure in a dynamic interbank model. arXiv preprint arXiv:2211.15431 .

- Frank and Strauss (1986) Frank O, Strauss D (1986) Markov Graphs. Journal of the American Statistical Association 81(395):832–842.

- Galeotti et al. (2020) Galeotti A, Golub B, Goyal S (2020) Targeting interventions in networks. Econometrica 88(6):2445–2471.

- Gandy and Veraart (2017) Gandy A, Veraart LA (2017) A Bayesian methodology for systemic risk assessment in financial networks. Management Science 63(12):4428–4446.

- Geman et al. (2001) Geman H, Madan DB, Yor M (2001) Asset prices are brownian motion: only in business time. Quantitative Analysis In Financial Markets: Collected Papers of the New York University Mathematical Finance Seminar (Volume II), 103–146.

- Gilbert (1959) Gilbert EN (1959) Random Graphs. The Annals of Mathematical Statistics 30(4):1141–1144.

- Glasserman and Young (2015) Glasserman P, Young HP (2015) How likely is contagion in financial networks? Journal of Banking & Finance 50:383–399.

- Glasserman and Young (2016) Glasserman P, Young HP (2016) Contagion in financial networks. Journal of Economic Literature 54(3):779–831.

- Guan and Tibshirani (2022) Guan L, Tibshirani R (2022) Prediction and outlier detection in classification problems. Journal of the Royal Statistical Society. Series B, Statistical Methodology 84(2):524.

- Guo and De Persis (2021) Guo M, De Persis C (2021) Linear quadratic network games with dynamic players: Stabilization and output convergence to Nash equilibrium. Automatica 130:109711.

- Hellmann (2013) Hellmann T (2013) On the existence and uniqueness of pairwise stable networks. International Journal of Game Theory 42(1):211–237.

- Herskovic (2018) Herskovic B (2018) Networks in production: Asset pricing implications. The Journal of Finance 73(4):1785–1818.

- Hoff et al. (2002) Hoff PD, Raftery AE, Handcock MS (2002) Latent space approaches to social network analysis. Journal of the American Statistical Association 97(460):1090–1098.

- Holland et al. (1983) Holland PW, Laskey KB, Leinhardt S (1983) Stochastic blockmodels: First steps. Social Networks 5(2):109–137.

- Horn and Johnson (2008) Horn R, Johnson C (2008) Topics in matrix analysis (Cambridge University Press).

- Hunter and Handcock (2006) Hunter DR, Handcock MS (2006) Inference in Curved Exponential Family Models for Networks. Journal of Computational and Graphical Statistics 15(3):565–583.

- Jackson and Pernoud (2021) Jackson MO, Pernoud A (2021) Systemic risk in financial networks: A survey. Annual Review of Economics 13:171–202.

- Jackson and Van den Nouweland (2005) Jackson MO, Van den Nouweland A (2005) Strongly stable networks. Games and Economic Behavior 51(2):420–444.

- Jackson and Wolinsky (2003) Jackson MO, Wolinsky A (2003) A strategic model of social and economic networks. Networks and groups, 23–49.

- Kimball et al. (2008) Kimball MS, Sahm CR, Shapiro MD (2008) Imputing risk tolerance from survey responses. Journal of the American statistical Association 103(483):1028–1038.

- Leng et al. (2020) Leng Y, Dong X, Wu J, Pentland A (2020) Learning quadratic games on networks. International Conference on Machine Learning, 5820–5830.

- Mao et al. (2018) Mao X, Sarkar P, Chakrabarti D (2018) Overlapping clustering models, and one (class) SVM to bind them all. Advances in Neural Information Processing Systems, volume 31.

- Markowitz (1952) Markowitz H (1952) Portfolio selection. Journal of Finance 7(1):77–91.

- Mastromatteo et al. (2012) Mastromatteo I, Zarinelli E, Marsili M (2012) Reconstruction of financial networks for robust estimation of systemic risk. Journal of Statistical Mechanics: Theory and Experiment .

- Mazalov and Chirkova (2019) Mazalov V, Chirkova JV (2019) Networking games: network forming games and games on networks (Academic Press).

- Metrick (1995) Metrick A (1995) A natural experiment in “Jeopardy!”. The American Economic Review 240–253.

- OECD (2022) OECD (2022) OECD statistics. URL https://stats.oecd.org/.

- Papachristou and Kleinberg (2022) Papachristou M, Kleinberg J (2022) Allocating stimulus checks in times of crisis. Proceedings of the ACM Web Conference 2022, 16–26.

- Paravisini et al. (2017) Paravisini D, Rappoport V, Ravina E (2017) Risk aversion and wealth: Evidence from person-to-person lending portfolios. Management Science 63(2):279–297.

- Peltonen et al. (2014) Peltonen TA, Scheicher M, Vuillemey G (2014) The network structure of the CDS market and its determinants. Journal of Financial Stability 13:118–133.

- Sadler and Golub (2021) Sadler E, Golub B (2021) Games on endogenous networks. arXiv preprint arXiv:2102.01587 .

- Sandberg and Willson (1972) Sandberg I, Willson A Jr (1972) Existence and uniqueness of solutions for the equations of nonlinear DC networks. SIAM Journal on Applied Mathematics 22(2):173–186.

- Squartini et al. (2018) Squartini T, Caldarelli G, Cimini G, Gabrielli A, Garlaschelli D (2018) Reconstruction methods for networks: the case of economic and financial systems. Physics Reports 757:1–47.

- Tardos (2004) Tardos E (2004) Network games. Proceedings of the thirty-sixth annual ACM symposium on Theory of computing, 341–342.

- Tsanakas and Christofides (2006) Tsanakas A, Christofides N (2006) Risk exchange with distorted probabilities. ASTIN Bulletin: The Journal of the IAA 36(1):219–243.

- Upper (2011) Upper C (2011) Simulation methods to assess the danger of contagion in interbank markets. Journal of financial stability 7(3):111–125.

- Upper and Worms (2004) Upper C, Worms A (2004) Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? European Economic Review 48:827–849.

- Vershynin (2018) Vershynin R (2018) High-dimensional probability: An introduction with applications in data science, volume 47 (Cambridge University Press).

- Wasserman and Pattison (1996) Wasserman S, Pattison P (1996) Logit models and logistic regressions for social networks: I. An introduction to Markov graphs and p. Psychometrika 61(3):401–425.

- Yaari (1987) Yaari ME (1987) The dual theory of choice under risk. Econometrica: Journal of the Econometric Society 95–115.

- Zhao et al. (2019) Zhao L, Chakrabarti D, Muthuraman K (2019) Portfolio construction by mitigating error amplification: The bounded-noise portfolio. Operations Research 67(4):965–983.

7 Proofs

7.1 Proof of Theorem 2.8

Recall that , , and is a vector whose entries are the ordered set .

Note that is positive definite, since it is a principal submatrix of the positive definite matrix . We shall prove an expanded version of Theorem 2.8.

[Expanded Version of Theorem 2.8]. Define matrices , , and as follows:

Let be the matrix whose rows are the ordered sets . Then, we have the following:

-

1.

A stable point under exists if and only if lies in the column space of .

-

2.

If a stable point exists, then .

-

3.

A unique stable point always exists if is full rank.

Proof 7.1

Proof. For clarity of exposition, we first prove the result when all edges are allowed, and then consider the case of disallowed edges.

(1) All edges allowed. Here, , and we use and to refer to and in the theorem statement. For any price matrix with , consider the matrix whose column has the utility-maximizing contract sizes for agent :

The tuple ) is stable if . So, for all , we require

| (5) | ||||

| (6) |

Since , we must have , where is upper-triangular with zero on the diagonal. Hence, using , we have

where we used the upper-triangular nature of in the last step. Plugging into Eq. (6), a stable point exists if and only if there is an appropriate vector such that for all , . This is equivalent to . If such a solution vector exists, then by definition it corresponds to a matrix via and .

(2) Disallowed edges. If is a prohibited edge then , so , so . Also, so . Therefore, the equality is achieved for any solution vector if is a prohibited edge. We can therefore reduce the linear system from part (1) by deleting rows of corresponding to prohibited edges.

Similarly, since the system is constrained by for prohibited edges , the columns of corresponding to such edges have no effect on the solution set.

We conclude that the linear system in (1) is equivalent to the (unconstrained) reduced system . Each solution corresponds to a skew-symmetric by construction. Finally, if has full rank then the unique reduced solution is . \Halmos

7.2 Example of Stable Network

To illustrate Theorem 2.8, consider the following example.

Example 7.2 (Stable points)

Consider a -firm network where the only allowed edges are given by . Suppose firms share the same covariance belief matrix , but have different mean beliefs and risk aversions. The firms’ beliefs are:

Then the matrices in Theorem 2.8 are given as:

Hence

Therefore, and . Since is full-rank, there exists a unique stable point for this network setting.

7.3 Stable Points are Common

Lemma 7.3

Proof 7.4

Now, we consider the ’s (and hence the ’s) to be random variables. Any distribution of induces a distribution on , where . Define , where is the minimum of union of the (nonzero) eigenvalues of all the ’s. A distribution over corresponds to a distribution over .

Proposition 7.5

If the distribution of given is continuous, then a unique stable point exists with probability .

Proof 7.6

Proof of Proposition 7.5. Let be the matrix generated from , and the corresponding matrix for . By Lemma 7.3, . Hence, , where denote the set of eigenvalues of . Since is a function of and is continuous given , the eigenvalues of are non-zero with probability . Hence, by Theorem 2.8, a unique stable point exists for with probability . \Halmos

Note that we require no condition on the distribution of . The condition of Proposition 7.5 is satisfied if the joint distribution of the is continuous and all edges are permitted, as shown in the following example.

Example 7.7

Fix some . Suppose the joint distribution of the is continuous and all edges are permitted. Then so the joint distribution of is continuous. By Bayes’ rule, . Since is continuous, we conclude is continuous.

7.4 Stable Network for the Shared Covariance Case

In the case of a shared covariance matrix for all agents, we can give a closed form expression for the stable network.

Corollary 7.8 (Shared , all edges allowed)

Suppose and for all . Let denote the eigenvalue and eigenvector of . Then, the network can be written in two equivalent ways:

The prices can be written as:

Proof 7.9

Proof. We first prove the identity with .

For each agent the optimal set of contracts is given as . Since for all , we obtain . Hence . Using and for a stable feasible point , we obtain .

Vectorization implies . It remains to show that is invertible.

Let for shorthand. Notice . Let . Since is invertible it suffices to show is invertible.

Properties of Kronecker products imply that if a matrix has strictly positive eigenvalues then counting mutiplicities (Horn and Johnson 2008). Let . Then, since and we obtain . Hence , so is invertible and hence is invertible. This proves the first identity.

Next, we prove the second identity. Properties of Kronecker products imply that has eigendecomposition .

Therefore, since we obtain:

Finally, the formulas for and follow from similar reasoning, using and . \Halmos

7.5 Proof of Theorem 2.9

[Restatement of Theorem 2.9]. Let be a stable feasible point. Then there is no feasible such that .

Proof 7.10

Proof of Theorem 2.9. Case 1: . First, consider a feasible such that . Then . Since is stable, by definition each agent optimizes contracts with respect to , so no agent is worse off under then . Hence .

Case 2: . Second, suppose that . Let . It follows that . Let be defined as . Then .

Next, notice that . Therefore, . Hence, either for all , or there exists such that .

Case 2(i). Suppose there exists such that . Then . By case , we have . Therefore agent is strictly worse off, so .

Case 2(ii). Suppose for all . Then for all . By case , we have . Therefore no agent is better off, so . \Halmos

7.6 Proof of Theorem 2.12

[Restatement of Theorem 2.12] Any stable point is Higher-Order Nash Stable.

Proof 7.11

Proof of Theorem 2.12. First, we argue is a Nash equilibrium. Suppose that agent wants to shift some of their contracts at the stable feasible point . Suppose they propose for . Let denote the new feasible point that occurs if all changes are accepted. By Theorem 2.9 we know that , so at least one agent does not prefer . Since the only changes are to edges , there must exist a who does not prefer . Therefore, they will reject the proposal of agent to shift to .

Then, agent can choose to either maintain the existing contract or delete the edge . We claim that agent prefers to keep the edge, since they could have chosen to set during the network formation process, no matter what price was offered. But at equilibrium . By stability of we know is the optimal choice for agent at prices . Therefore, after agent rejects , it follows that the edge remains at .

Since was arbitrary, we conclude that at equilibrium, agent cannot propose any set of changes that result in a strictly better network for them. Therefore, their optimal action at is to not deviate from the equilibrium.

Next, we show cartel robustness. Suppose is a strict subset and is a feasible point differing only at indices such that . By Theorem 2.9, we know cannot dominate , so there is some agent that does not prefer to . Since only changes contracts where both members are in , the utility of agents in must be unchanged. Therefore , and hence not all members of the cartel have higher utility under . \Halmos

7.7 Price Update Rule for Pairwise Negotiations

We give an explicit formula for the updated price of a unit contract after a pairwise negotiation.

Proposition 7.12 (Price after Pairwise Negotiation)

Consider a network setting . Let be as in Theorem 2.8. Given a price matrix and a pair of firms that are permitted to trade, let be another skew-symmetric price matrix such that (a) differs from only in the cells and , (b) and both maximize their utility at the same contract size under , and (c) and can choose their optimal contract sizes with all other agents given these prices. Then,

Proof 7.13

Proof. Let for . Since and is a principal submatrix, we know is real symmetric and positive definite, and hence its inverse is as well. Therefore is real symmetric and PSD. (It is not full rank in general, unless ). Since is a permitted edge, and . Therefore since is positive definite. So, and similarly .

Now, the optimal contracts for agent under prices are given by . Note that . Since both and maximize their utility at the same contract size, we have:

7.8 Proof of Theorem 2.15

First, we characterize pairwise negotiation dynamics as linear in the price updates.

Theorem 7.14

Consider a network setting . Define as in Theorem 2.8. Let if is a permitted edge and otherwise. Let be diagonal matrices such that and , and be the pseudoinverse of . Let , where is the price matrix at time step of pairwise negotiations. Then,

Proof 7.15

Proof. Let be a permitted edge. From Proposition 7.12, we obtain:

We assumed that was a permitted edge above, but notice the identity is also true for prohibited since both the numerator and denominator become , and we can define their ratio to be . Defining , and recalling the definitions of and from the theorem statement, the above formula becomes

| (7) |

We show next that , where is defined in the theorem statement. Let denote the trace operator. Then,

where we used .

Hence we need to show . Letting denote the Kronecker delta, we obtain:

| (8) |

Now, we observe that is the vectorization of a matrix whose column is , i.e., the matrix . Similarly, is the vectorization of a matrix whose row is , i.e., the matrix . Hence, , as desired.

Plugging into Eq. (7),

where we used the facts that for disallowed edges, and and , which can be easily confirmed by inspection of these diagonal matrices. \Halmos

We use Lyapunov theory to analyze the convergence of pairwise negotiation dynamics. In particular, we need the the discrete Lyapunov equation, also called the Stein equation.

Theorem 7.16 (Callier and Desoer (1994) 7.d)

For the discrete-time dynamical system , with , the following are equivalent:

-

1.

The system is globally asymptotically stable towards .

-

2.

For any positive definite , there exists a unique solution to the equation

-

3.

For any eigenvalue of , .

Pairwise negotiation dynamics can be described as a discrete-time linear system in , where is the price difference at time . Clearly, the system converges iff approaches zero. Therefore, we can use the Stein equation to prove global asymptotic stability conditions.

We will also need the commutation matrix.

Lemma 7.17 (Horn and Johnson (2008))

Let be a permutation matrix (called the commutation matrix) defined as . Then for any , we have

Recall that for a linear operator that denotes the eigenvalues of . We are ready to prove Part 1 of Theorem 2.15.

Proposition 7.18 (Part 1 of Theorem 2.15)

Let be defined as in Theorem 7.14. For a matrix let denote the principal submatrix of corresponding to the nonzero rows/columns of . Define . Then, for any , is globally asymptotically stable towards .

Proof 7.19

Proof of Proposition 7.18. Let . By Theorem 7.16, the dynamics are globally asymptotically stable towards iff for all , we have .

From Eq. (8) for a prohibited edge , we see that , since . Hence, . Taking transposes and noting that both and are symmetric, we find . Hence, , where we used . Thus, is zero except for the principal submatrix corresponding to the nonzero columns of . So, to apply Theorem 7.16, we only require for .

For clarity of exposition we will first consider the case where (no prohibited edges). Then, the eigenvalues of equal , where by a similarity transformation. Also, , where and . The matrix is block diagonal with positive-definite blocks , so . By Lemma 7.17, is similar to via a permutation matrix, so . Hence, , and . So, the eigenvalues of are real and positive. Hence, we have convergence iff for all , we have . i.e., . Hence, as required.

Now we consider the prohibited edges setting (). Here, convergence occurs iff for all . Since and , we have . Arguing as above, it suffices to show that . We claim where is a block diagonal matrix with block equal to , and is similar to via Lemma 7.17. Hence and the expression for follows. \Halmos

Proposition 7.20 (Part 2 of Theorem 2.15)

Proof 7.21

Proof. Let denote the greatest eigenvalue in absolute value of . From Theorem 7.14, we have . Recall that denote largest and smallest eigenvalues of the matrix respectively. Since , it follows that .

Then,

Since we are done. \Halmos

7.9 Example of Convergence Conditions and Rate

Example 7.22 (Convergence Conditions and Rate)

In the setting of Example 7.2, we have

Hence

Also, is the diagonal matrix with for . Since the permitted edges are , and so . Hence , and .

It follows that pairwise negotiations with are globally asymptotically stable. Suppose that . Then . Hence after rounds, the distance of to shrinks by a factor of .

7.10 Proof of Theorem 2.17

We will use a series of Lemmas to reduce the result of Theorem 2.17 to a matrix concentration inequality in each of the .

Lemma 7.23

Let be as in Theorem 2.17. Suppose all edges are permitted.

Suppose that for all , we have . Then, .

Proof 7.24

Proof. Let be as in Theorem 2.17, but built using instead of . Let be defined similarly to but using in place of all .

Then and .

Let be such that and . We will bound .

Let be defined as in Theorem 2.8, so and . Let . Notice , so .

First, since is diagonal, .

Second, let where are defined analogously to in the proof of Theorem 2.15. Letting be the commutation matrix of Lemma 7.17, we know , so . Since are block diagonal with blocks respectively, it follows . Hence .

Third, notice that since and are assumed to be that and . So,

We conclude that , so . \Halmos

Lemma 7.25

Suppose for , we have . Then .

Proof 7.26

Proof. Weyl’s inequality implies that . Therefore,

The last step follows from the fact . \Halmos

The hypothesis of Lemma 7.25 follows from a standard argument on the concentration of random covariance matrices.

Theorem 7.27

Under the setting of Theorem 2.17, with probability at least , we have for all .

Proof 7.28

Proof of Theorem 7.27. Let be the samples. Let , and . Then, . Hence,

Now, , so . By Vershynin (2018) (4.7.3 and 2.8.3), there exist constants such that for any ,

Now we set and for some constant . Then, when , we have Then, with probability at least , we have

| and | |||

Choosing large enough and , this statement holds for all with probability greater than . \Halmos

Theorem 2.17 follows easily.

Proof 7.29

Proof of Theorem 2.17 When all edges are permitted, the proof follows from Theorem 7.27, Lemma 7.23, and Lemma 7.25.

If there are prohibited edges, then we must use matrix concentration to bound instead of . Notice that prohibited edges have the effect of simply zeroing out certain rows and columns of , so that , rather than . Therefore, we can use Theorem 7.27 to bound for all , and then prove the appropriate analogue of Lemma 7.23. In particular, the sample size requirement remains the same. \Halmos

7.11 Proof of Proposition 2.18

[Restatement of Proposition 2.18.] Finding the maximum likelihood estimator of under Assumption 2.4 is equivalent to the following SDP:

Recall that in Assumption 2.4 we assumed that varies independently according to a Brownian motion with the same parameters for all . To avoid ambiguity, we recall the definition of a standard Brownian motion as follows.

Definition 7.30 (Brownian Motion)

For , a -dimensional Brownian motion with scale parameter is a stochastic process such that for all , the components of are independent, and for all ,

i) The process has independent increments.

ii) For , the increment is distributed as .

iii) With probability , the function is continuous on .

We can derive the SDP of Proposition 2.18 as follows.

Proposition 7.31

Under Assumption 2.4, the maximum likelihood estimator for is the unique such that and

-

•

Consistency: For all ,

-

•

Minimum mean shift: The resulting minimize the objective

Proof 7.32

Proof of Proposition 7.31.

The proof of Proposition 2.18 follows easily.

Proof 7.33

Proof of Proposition 2.18. By Proposition 7.31, we obtain the SDP

under the assumptions of and . Since the Frobenius norm is invariant under transposes, we have

We can replace with for all to obtain the equivalent objective function (up to a constant). This substitution enforces the fixed point equation for all , so the conclusion follows. \Halmos

Remark 7.34 (The prohibited edges setting.)

Proposition 2.18 generalizes straightforwardly to the setting of prohibited edges. Let denote the set of permitted edges. Then minimum mean shift assumption is equivalent to minimizing . In words, the objective just zeroes out prohibited edges, since mean estimates for prohibited edges have no effect on the network. For a network setting , some algebra gives . Notice is a diagonal matrix with if and zero otherwise. Therefore, it is clear that upon substitution, the objective is an SDP in with the same constraints.

7.12 Proof of Theorem 3.1

[Restatement of Theorem 3.1] Suppose that for each firm , the function is twice differentiable, and there exist strictly increasing functions such that for all , . Then there exists a unique stable point.

Proof 7.35

Proof of Theorem 3.1. Note that the Hessian of is a positive diagonal matrix due to the conditions on . So, any stationary point is a local maximum. Hence, it suffices to show the existence of a unique stationary point.

Let be an matrix whose entry . If a stable point exists, it must satisfy , , and

| (9) |

following the same steps as the proof for Corollary 7.8. Adding this equation to its transpose, the stable point must satisfy

For a stable point, , using . Define to be an matrix with . Hence, the stable point must satisfy

| (10) | ||||