[figure]capposition=top \newclipboardoutput-draft

Logs with zeros? Some problems and solutions††thanks: An earlier draft of this paper was titled “Log-like? Identified ATEs defined with zero-valued outcomes are (arbitrarily) scale-dependent.” We thank Isaiah Andrews, Kirill Borusyak, Jonathan Cohn, Amy Finkelstein, Edward Glaeser, Nick Hagerty, Peter Hull, Jetson Leder-Luis, Erzo Luttmer, Giovanni Mellace, John Mullahy, Edward Norton, David Ritzwoller, Brad Ross, Pedro Sant’Anna, Jesse Shapiro, Neil Thakral, Casey Wichman, and seminar participants at BU, Georgetown, Harvard/MIT, Southern Denmark University, Vanderbilt, Stanford, UC-Irvine, UCLA, UCSD, and the SEA annual conference for helpful comments and suggestions. Bruno Lagomarsino provided superb research assistance.

Abstract

\CopyabstractWhen studying an outcome that is weakly-positive but can equal zero (e.g. earnings), researchers frequently estimate an average treatment effect (ATE) for a “log-like” transformation that behaves like for large but is defined at zero (e.g. , ). We argue that ATEs for log-like transformations should not be interpreted as approximating percentage effects, since unlike a percentage, they depend on the units of the outcome. In fact, we show that if the treatment affects the extensive margin, one can obtain a treatment effect of any magnitude simply by re-scaling the units of before taking the log-like transformation. This arbitrary unit-dependence arises because an individual-level percentage effect is not well-defined for individuals whose outcome changes from zero to non-zero when receiving treatment, and the units of the outcome implicitly determine how much weight the ATE for a log-like transformation places on the extensive margin. We further establish a trilemma: when the outcome can equal zero, there is no treatment effect parameter that is an average of individual-level treatment effects, unit-invariant, and point-identified. We discuss several alternative approaches that may be sensible in settings with an intensive and extensive margin, including (i) expressing the ATE in levels as a percentage (e.g. using Poisson regression), (ii) explicitly calibrating the value placed on the intensive and extensive margins, and (iii) estimating separate effects for the two margins (e.g. using Lee bounds). We illustrate these approaches in three empirical applications.

1 Introduction

firstp When the outcome of interest is strictly positive, researchers often estimate an average treatment effect (ATE) in logs of the form , which has the appealing feature that its units approximate percentage changes in the outcome.111That is, when . A practical challenge in many economic settings, however, is that the outcome may sometimes equal zero, and thus the ATE in logs is not well-defined. When this is the case, it is common for researchers to estimate ATEs for alternative transformations of the outcome such as or , which behave similarly to for large values of but are well-defined at zero. The treatment effects for these alternative transformations are typically interpreted like the ATE in logs, i.e. as (approximate) average percentage effects. For example, among the 11 papers published in the American Economic Review since 2018 that interpret a treatment effect for , all but one interpret the result as a percentage effect or elasticity.222We found 17 papers overall using as an outcome variable, of which 11 interpret the units; see LABEL:tbl:selected-quotes-aer.

The main point of this paper is that identified ATEs that are well-defined with zero-valued outcomes should not be interpreted as percentage effects, at least if one imposes the logical requirement that a percentage effect does not depend on the baseline units in which the outcome is measured (e.g. dollars, cents, or yuan).

Our first main result shows that if is a function that behaves like for large values of but is defined at zero, then the ATE for will be arbitrarily sensitive to the units of . Specifically, we consider continuous, increasing functions that approximate for large values of in the sense that as . The common and transformations satisfy this property. We show that if the treatment affects the extensive margin (i.e. ), then one can obtain any magnitude for the ATE for by rescaling the outcome by some positive factor . It is therefore inappropriate to interpret the ATE for as a percentage effect, since a percentage is inherently a unit-invariant quantity, while the ATE for depends arbitrarily on the units of .

The intuition for this result is that a “percentage” treatment effect is not well-defined for an individual for whom treatment increases their outcome from zero to a positive value. For example, in our application to Carranza et al. (2022) in LABEL:sec:empirical, the treatment induces more people to have positive hours worked. The percentage change in hours is then not well-defined for individuals who would work positive hours under the treatment condition but zero hours under the control condition. Any average treatment effect that is well-defined with zero-valued outcomes must therefore implicitly assign a value for a change along the extensive margin. For logarithm-like transformations , the importance of the extensive margin is determined implicitly by the units of . To see why this is the case, consider an individual who works positive hours only if they are treated, so that and . Their treatment effect for the transformed outcome is , which becomes larger if the units of are re-scaled by some , e.g. if we convert from weekly hours worked to yearly hours worked. When the treatment has an extensive margin effect, the ATE for can thus be made large in magnitude by re-scaling by a large factor . By contrast, if we re-scale by a small factor , such that the resulting outcomes are close to zero, then , and so the ATE for will be small. By varying the units of the outcome, we can thus obtain any magnitude for the ATE for .

Our theoretical results also imply that if we re-scale the units of the outcome by a finite factor , the ATE for a log-like transformation will change by approximately times the effect of the treatment on the extensive margin. This result implies that sensitivity analyses that explore how the estimated ATE for changes with finite changes in the units of —or equivalently, how the ATE for changes with the constant —are essentially indirectly measuring the size of the treatment effect on the extensive margin.

We illustrate the practical importance of these results by systematically replicating recent papers published in the American Economic Review that estimate treatment effects for -transformed outcomes. In line with our theoretical results, we find that treatment effect estimates using are sensitive to changes in the units of the outcome, particularly when the extensive margin effect is large. In half of the papers that we replicated, multiplying the original outcome by a factor of 100 (e.g. converting from dollars to cents) changes the estimated treatment effect by more than 100% of the original estimate. We obtain similar results using instead of .

What, then, are alternative options in settings with zero-valued outcomes? Our second main result delineates the possibilities. We show that when there are zero-valued outcomes, there is no treatment effect parameter that satisfies all three of the following properties:

-

(a)

The parameter is an average of individual-level treatment effects, i.e. takes the form , where is increasing in .

-

(b)

The parameter is invariant to re-scaling of the units of the outcome (i.e. ).

-

(c)

The parameter is point-identified from the marginal distributions of the potential outcomes.

This “trilemma” implies that any target parameter that is well-defined with zero-valued outcomes must necessarily jettison at least one of the three properties above. \CopytargetparamintroOf course, the choice of target parameter should depend on the economic question of interest. Which of the three properties the researcher prefers to forgo will thus generally depend on their context-specific motivation for using a log-like transformation in the first place.

To that end, Section 4 highlights a menu of parameters that may be attractive depending on the researcher’s core motivation. We first consider the case where the researcher is interested in obtaining a causal parameter with an intuitive “percentage” interpretation. In this case, it may be natural to consider a parameter outside of the class of individual-level averages of the form . One prominent option is the ATE in levels as a percentage of the baseline mean, which in many cases can be estimated via Poisson regression (Santos Silva and Tenreyro, 2006; Wooldridge, 2010). The researcher might also consider alternative normalizations of the outcome that lead to intuitive units, e.g. expressing the outcome in per-capita units or converting it to a rank with respect to some reference distribution. Next, we suppose the researcher would like to capture concave preferences over the outcome; for example, the researcher might consider income gains to be more meaningful for individuals who are initially poor. In this case, it is natural to directly specify how much the researcher values a change along the extensive margin relative to the intensive margin—e.g., that a change from 0 to 1 is worth an percent change along the intensive margin. Finally, suppose the researcher is interested in separately understanding the effects of the treatment along both the intensive and extensive margins. In this case, the researcher may target separate parameters for the two margins—e.g., , the average effect in logs for individuals with positive outcomes under both treatments, captures the intensive margin. Separate effects for the two margins are not generally point-identified, but can be can be bounded using the method in Lee (2009) or point-identified with additional assumptions (Zhang et al., 2008, 2009).

Section 5 provides a blueprint for estimating these alternative parameters in practice by applying our recommended approaches to three recent empirical applications, including a randomized controlled trial (RCT) (Carranza et al., 2022), a difference-in-differences (DiD) setting (Sequeira, 2016), and an instrumental variables (IV) setting (Berkouwer and Dean, 2022).

Related work.

The use of log-like transformations for dealing with zero-valued outcomes has a long history. The use of the transformation dates to at least Williams (1937), while Bartlett (1947) considers both the and inverse hyperbolic sine transformations.333Bartlett (1947) proposes using . \CopybwMore recent papers by Burbidge et al. (1988) and Bellemare and Wichman (2020), among others, provide results for that are frequently cited in economics papers using this transformation.444MacKinnon and Magee (1990) propose transformations of the form , where is estimated by assuming is normally distributed conditional on covariates.

Previous work has illustrated in simulations or selected empirical applications that results for particular transformations such as or may be sensitive to the units of the outcome (Aihounton and Henningsen, 2021; de Brauw and Herskowitz, 2021). In concurrent work, Mullahy and Norton (2023) show theoretically that the marginal effects from linear regressions using or are sensitive to the scaling of the outcome, with the the limits of the marginal effects approaching those of either a levels regression or a (normalized) linear probability model, depending on whether the units are made small or large. We complement this work by proving that scale-dependence is a necessary feature of any identified ATE that is well-defined with zero-valued outcomes, and that the dependence on units is arbitrarily bad for transformations that approximate for large values of . Thus, it is not possible to fix the issues with or by choosing a “better” transformation or using a different estimator. We also complement previous empirical examples by providing a systematic analysis of the sensitivity to scaling for papers in the American Economic Review using .

Other work has considered the interpretation of regressions using or from the perspective of structural equations models, as opposed to the potential outcomes model considered here. This literature has reached diverging conclusions: For example, Bellemare and Wichman (2020) conclude that coefficients from regressions have an interpretation as a semi-elasticity, while Cohn et al. (2022) conclude that these estimators are inconsistent and advocate for Poisson regression instead. Thakral and Tô (2023) show that the semi-elasticities implied by OLS regressions using or are sensitive to scale; they recommend instead the use of power functions , which they show are the only transformations (besides ) for which the implied semi-elasticities for OLS regressions are scale-invariant. In Appendix C, we show that these diverging conclusions stem from the fact that the structural equations considered in these papers implicitly impose different restrictions on the potential outcomes—some of which are incompatible with zero-valued outcomes—and consider different target causal parameters. This highlights the value of a potential outcomes framework such as ours, which makes transparent what causal parameters are identifiable and what properties they can have.

Finally, there is a long history in econometrics of explicitly modeling the intensive and extensive margins in settings with zero-valued outcomes, such as Tobin (1958) and Heckman (1979). Broadly speaking, these methods impose parametric structure on the joint distribution of the potential outcomes, which allows one to separate out the intensive and extensive margin effects of a treatment (see Appendix C for technical details). Of course, the parametric restrictions underlying these approaches may often be difficult to justify in practice, which perhaps has contributed to the growth in the use of log-like transformations in place of approaches that explicitly model the extensive margin. Our paper shows that the presence of an extensive margin should not simply be ignored by taking a log-like transformation. It also clarifies what parameters can be learned in such cases without imposing restrictions on the joint distribution of the potential outcomes.

1.1 Setup and notation

Let be a binary treatment and let be a weakly positively-valued outcome.555The transformation is sometimes used in settings where can be negative. We impose that , and thus do not consider this case. See Section B.2 for extensions of our results to settings with continuous treatments. We assume that , where and are respectively the potential outcomes under treatment and control. We suppose that in some (sub-)population of interest, for some (unknown) joint distribution . We denote the marginal distribution of under by for . We assume that neither nor is a degenerate distribution at zero.

2 Sensitivity to scaling for transformations that behave like

We first consider average treatment effects of the form for an increasing function . We note that corresponds to the ATE among the (sub-)population indexed by ; if refers to the sub-population of compliers for an instrument, for instance, then is the local average treatment effect (LATE), rather than the ATE in the full population. We are interested in how changes if we change the units of by a factor of . That is, how does

depend on ? Setting , for example, might correspond with a change in units between dollars and cents. Of course, if is strictly positive and , then is the ATE in logs and does not depend on the value of .

We consider “log-like” functions that are well-defined at zero but behave like for large values of , in the sense that as . This property is satisfied by and , for example. Our first main result shows that if the treatment affects the extensive margin, then can be made to take any desired value through the appropriate choice of .

Proposition 1.

Suppose that:

-

1.

(The function is continuous and increasing) is a continuous, weakly increasing function.

-

2.

(The function behaves like for large values) as .

-

3.

(Treatment affects the extensive margin) .

-

4.

(Finite expectations) for .666This assumption simply ensures that exists for all values of .

Then, for every , there exists an such that . In particular, is continuous with as and as .

1 casts serious doubt on the interpretation of ATEs for functions like or as (approximate) average percentage effects. While a percent (or log point) is entirely invariant to the units of the outcome, LABEL:prop:_can_get_any_valuefor_ATE shows that, in sharp contrast, the ATEs for these transformations are arbitrarily dependent on units.

2.1 Intuition for 1

Loosely speaking, the result in 1 follows from the fact that a “percentage” treatment effect is not well-defined for individuals who have but .777See Delius and Sterck (2020) for an intuitive discussion of this difficulty in the context of the transformation. They write, “the concept of elasticity itself does not make sense with zeros” (p. 21). Any ATE that is well-defined with zero-valued outcomes must implicitly determine how much weight to place on changes along the extensive margin relative to proportional changes along the intensive margin.

When behaves like for large values of , the importance of the extensive margin is implicitly determined by the units of . For intuition, suppose that we re-scale the outcomes so that the non-zero values of are very large. Then for an individual for whom treatment changes the outcome from zero to non-zero, the treatment effect will be very large, since . Extensive margin treatment effects thus have a large impact on the ATE when the values of are made large. By contrast, changing the units of does not change the importance of treatment effects along the intensive margin by much, since for and , we have that , which does not depend on the units of the outcome.

To see the roles of the extensive and intensive margins more formally, for simplicity consider the case where , so that, for example, everyone who has positive income without receiving a training also has positive income when receiving the training.888A similar argument goes through without this restriction, but then there are two extensive margins, one for individuals with , and the other for those with . Then, by the law of iterated expectations, we can write

When is large, for non-zero values of , and thus the intensive margin effect in the previous display is approximately equal to , the treatment effect in logs for individuals with positive outcomes under both treatment and control. This, of course, does not depend on the scaling of the outcome. However, the extensive margin effect grows with , since is increasing in while does not depend on . Thus, as grows large, the ATE for places more and more weight on the extensive margin effect of the treatment relative to the intensive margin. We can therefore make arbitrarily large by sending . By contrast, if , then with very high probability, and thus the ATE for is approximately equal to 0.

nuisancezeros1It is worth emphasizing that the arbitrary scale-dependence described in 1 exists whenever the treatment affects the probability that the outcome is zero, regardless of whether the extensive margin is of direct economic interest or not.999Without an extensive margin, ATEs for transformations defined at zero still exhibit scale-dependence, though perhaps not arbitrarily so. See Section 3.1 below for further discussion. In some settings, the presence of zeros may correspond to a discrete economic choice (e.g. not participating in the labor market), and thus may be of direct interest. In other settings—for example, if the outcome is a yearly count of publications which is sometimes zero for idiosyncratic reasons—the extensive margin may be a “nuisance” rather than a direct economic object of interest.101010One setting where nuisance zeros may arise is when the observed outcome is actually a mis-measured version of the true economic object of interest. For example, publications may be a noisy measure of true researcher productivity . One possible remedy in this setting is to model the measurement error to recover the treatment effect on rather than on . In a similar vein, Gandhi et al. (2023) models the measurement error in product shares in demand estimation, which are sometimes zero in finite samples. The result in 1 highlights that regardless of the source of the zeros, an ATE for a log-like transformation is not interpretable as a percentage, since the presence of the extensive margin effect makes it arbitrarily dependent on the units. Indeed, a percentage effect is not a well-defined for individuals moving from zero to non-zero outcomes. Whether the zeros correspond to a discrete economic choice or not will be relevant, however, when considering the choice of alternative target parameter, a topic we return to in Section 4 below.

2.1.1 Intuition for the special case of

We can also develop some intuition for 1 by considering the special case where . In that case, we have that

| (1) |

Note that

We thus see that the term inside the expectation in (1) diverges to for individuals with , and likewise diverges to when . If on average the extensive margin effect is positive, then there are more individuals for whom the limit is rather than , and thus (under appropriate regularity conditions) the ATE diverges to . Analogously, if the extensive margin effect is negative, then the ATE diverges to . Hence, we see that the magnitude of the ATE for diverges as when the average effect on the extensive margin is non-zero. By contrast, as , for both and , and thus the treatment effect converges to 0. 1 shows that this dependence on units occurs for any log-like transformation, not just , and thus this issue cannot be fixed by choosing a different log-like transformation (, , , etc.)

2.2 Additional remarks and extensions

Remark 1 (ATEs for ).

In some settings, researchers consider the ATE for and investigate sensitivity to the parameter . Observe that , and thus the ATE for is equal to the ATE for . Hence, varying the constant term for is equivalent to varying the scaling of the outcome when using . 1 thus implies that if treatment affects the extensive margin, one can obtain any desired magnitude for the ATE for via the choice of . In particular, the ATE for grows large in magnitude as , and small as .

Remark 2 (Finite changes in scaling).

1 shows that any magnitude of can be achieved via the appropriate choice of . How much does change for finite changes in the scaling ? 4 in the appendix shows that the change in the ATE from multiplying the outcome by a large factor is approximately times the treatment effect on the extensive margin,111111We say if . That is, as , grows strictly slower than .

| (2) |

Thus, the ATE for will tend to be more sensitive to finite changes in scale the larger is the extensive margin treatment effect. This implies that sensitivity analyses that assess how treatment effect estimates for change under finite changes in the units of —or equivalently, under finite changes of in —are roughly equivalent to measuring the size of the extensive margin.

Remark 3 (Extension to continuous treatments).

We focus on ATEs for binary treatments for expositional simplicity, although similar results apply with continuous treatments. In Section B.2, we show that when is a continuous treatment, any treatment effect contrast that averages across possible values of (i.e. a parameter of the form ) is arbitrarily sensitive to scaling when there is an extensive margin effect.

Remark 4 (Extension to OLS estimands).

It is worth noting that the results in this section show that population ATEs for are sensitive to the units of . These results are about estimands, and thus any consistent estimator of the ATE for will be sensitive to scaling (at least asymptotically). Thus, our results apply to ordinary least squares (OLS) estimators when they have a causal interpretation, but also to non-linear estimators such as inverse-probability weighting or doubly-robust methods. Nevertheless, given the prominence of OLS in applied work, and the fact that OLS is sometimes used for non-causal estimands, in Section B.3 we provide a result specifically on the scale-sensitivity of the population regression coefficient for a random variable of the form on an arbitrary random variable . Our result shows that the coefficients on will be arbitrarily sensitive to the scaling of when the coefficients of a regression of on are non-zero. Thus, the OLS estimand using a logarithm-like function on the left-hand side will be sensitive to scaling even when it does not have a causal interpretation.

Remark 5 (Statistical significance).

Equation (2) shows that is the dominant term in for large , which suggests that the -statistic for an estimator of will generally converge to that for the analogous estimator of the extensive margin effect, . 7 in the appendix formalizes this intuition when the treatment effects are estimated via OLS: As is made large, the -statistic for converges to that for the extensive margin estimate. In our empirical analysis of papers in the American Economic Review below, we find that indeed the -statistics for estimates of the ATE using are typically close to those for the extensive margin effect.

Remark 6 (When most values are large).

Researchers often have the intuition that if most of the values of the outcome are large, then ATEs for transformations like or will approximate elasticities, since for most values of . Indeed, in an influential paper, Bellemare and Wichman (2020) recommend that researchers using the transformation should transform the units of their outcome so that most of the non-zero values of are large. The results in this section suggest—perhaps somewhat counterintuitively—that if one rescales the outcome such that the non-zero values are all large, the behavior of the ATE will be driven nearly entirely by the effect of the treatment on the extensive margin and not by the distribution of the potential outcomes conditional on being positive. Moreover, the rescaling can be chosen to generate any magnitude for the ATE if the treatment affects the extensive margin.

Remark 7 (Zero extensive margin).

1 applies to settings where treatment has a non-zero effect on average on the extensive margin. This raises the question of whether the use of log-like transformations is justified in the absence of an extensive margin treatment effect. Our 3 below implies that the ATE for any log-like transformation will be sensitive to the units of the outcome for at least some distribution with strictly positive outcomes, but perhaps not arbitrarily so in the sense of 1 (see Section 3.1 for further discussion). Moreover, if one were confident that the extensive margin effect were exactly zero for all individuals, one could recover the ATE in logs for individuals with positive outcomes by simply dropping individuals with . The use of log-like transformations is thus somewhat difficult to justify even in settings without an extensive margin.

2.3 Empirical illustrations from the American Economic Review

We illustrate the results in this section by evaluating the sensitivity to scaling of estimates using the transformation in recent papers in the American Economic Review (AER). In November 2022, we used Google Scholar to search for “inverse hyperbolic sine” among papers published in the AER since 2018. We searched for papers using rather than since the former are easier to find with a simple keyword search. Our search returned 17 papers that estimate treatment effects for an -transformed outcome.121212We consider papers with both binary and non-binary treatments, as our theoretical results extend easily to non-binary treatments; see 3. Seven of the 10 papers we replicated used a binary treatment. Of these, 10 explicitly interpret the results as percentage changes or elasticities, and 6 of the remaining 7 do not directly interpret the units. See LABEL:tbl:selected-quotes-aer for a list of the papers and relevant quotes. Of the 17 total papers using , 10 had publicly available replication data that allowed us to replicate the original estimates and assess their sensitivity to scaling.131313We include one paper where there was a slight discrepancy between our replication of the original result and the result reported in the paper that only affected the third decimal place. For our replications, we focus on the first specification using presented in a table in the paper, which we view as a reasonable proxy for the paper’s main specification using .141414We use the first coefficient presented in a figure for one paper without any tables in the main text using . If the first specification is a validation check (e.g. a pre-trends test), we use the first specification of causal interest.

We assess the sensitivity of these results by re-running exactly the same procedure as in the original paper, except replacing with . Thus, for example, if the original paper estimated a treatment effect for the of an outcome measured in dollars, we use the same procedure to re-estimate the treatment effect for the of the outcome measured in cents. Since (2) shows that the sensitivity to scaling depends on the size of the extensive margin effect, we also estimate the extensive margin effect by using the same procedure as in the original paper but with the outcome .

| Treatment Effect Using: | Change from rescaling units: | ||||

| Paper | Ext. Margin | Raw | % | ||

| Azoulay et al (2019) | 0.003 | 0.017 | 0.003 | 0.014 | 464 |

| Fetzer et al (2021) | -0.177 | -0.451 | -0.059 | -0.273 | 154 |

| Johnson (2020) | -0.179 | -0.448 | -0.057 | -0.269 | 150 |

| Carranza et al (2022) | 0.201 | 0.453 | 0.055 | 0.252 | 125 |

| Cao and Chen (2022) | 0.038 | 0.082 | 0.010 | 0.044 | 117 |

| Rogall (2021) | 1.248 | 2.150 | 0.195 | 0.902 | 72 |

| Moretti (2021) | 0.054 | 0.068 | 0.000 | 0.013 | 24 |

| Berkouwer and Dean (2022) | -0.498 | -0.478 | 0.010 | 0.020 | -4 |

| Arora et al (2021) | 0.113 | 0.110 | -0.001 | -0.003 | -3 |

| Hjort and Poulsen (2019) | 0.354 | 0.354 | 0.000 | 0.000 | 0 |

Note: This table replicates treatment effect estimates using as the outcome in recent papers published in the AER, and explores their sensitivity to the units of . The first column shows the author(s) and date of the paper. The second column shows the treatment effect on using the units originally reported in the paper. The third column shows a treatment effect estimate constructed identically to the estimate in column 2 except using as the outcome instead of , e.g. converting from dollars to cents before taking the transformation. The fourth column shows an estimate of the size of the extensive margin, obtained using as the outcome. The final two columns show the raw difference and percentage difference between the second and third columns. The table is sorted on the magnitude of the percentage difference.

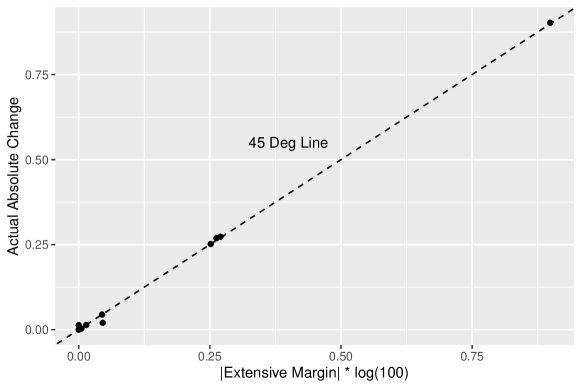

Note: This figure shows the relationship between the sensitivity of treatment effects using to re-scaling the units of and and the size of the extensive margin. For each replicated paper, this figure plots the absolute value of the change in the estimated treatment effect from multiplying the outcome by 100 (i.e. the absolute value of the Raw Change column in Table 1) on the -axis against times the absolute value of the extensive margin effect on the -axis. If the approximation in (2) were exact, all points would lie on the 45 degree line.

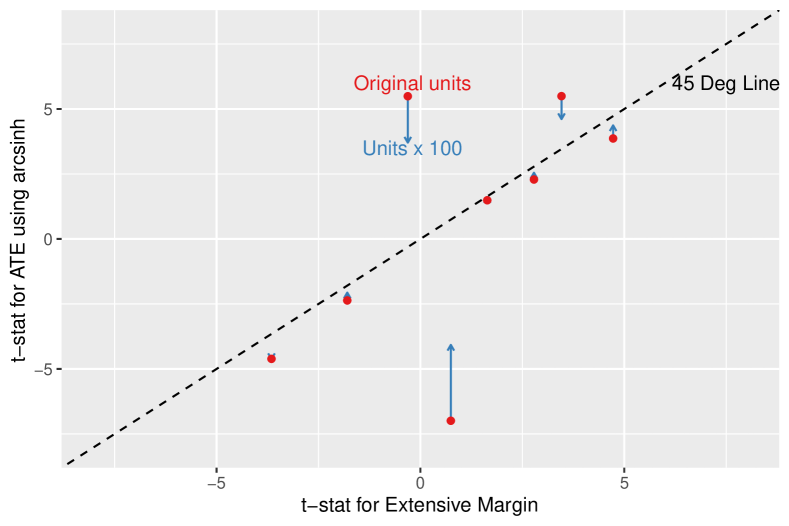

The results of this exercise, shown in Table 1, illustrate that treatment effect estimates can be quite sensitive to the scaling of the outcome when the extensive margin is not approximately zero. Indeed, in 5 of the 10 replicable papers, multiplying the outcome by a factor of 100 changes the estimated treatment effect by more than 100% of the original estimate. The change in the estimated treatment effect is less than 10% only in three papers, all of which have either zero or near-zero (1 p.p.) effects on the extensive margin. Figure 1 shows that the (absolute) change in the estimated treatment effect is larger when the extensive margin effect is larger, with the change lining up very closely with the approximation given in (2).151515In LABEL:fig:tstats, we plot the -statistics for the treatment effects estimates as well as those for the extensive margin effect. In line with the discussion in 5, we find that the -statistics for the treatment effect using tend to be similar to those for the extensive margin, except when the extensive margin is very small, and become even closer when multiplying the units by 100.

Using the same 10 papers, we also estimate treatment effects using as the outcome, and analogously explore how the results change when we multiply the units of by 100. (Four of the 10 papers that we replicate report an alternative specification using in the paper.) The results, shown in LABEL:tbl:recale-by-100-aer-log1p, are qualitatively quite similar those in Table 1, with five of the 10 treatment effect estimates again changing by more than 100%. These results underscore the fact that LABEL:prop:_can_getany_value_for_ATE applies to all log-like transformations, including both and for any constant .

3 Sensitivity to scaling for other ATEs

Our results so far show that ATEs for transformations that are defined at zero and approximate are arbitrarily sensitive to scaling. What other options are available when there are zero-valued outcomes? To help delineate alternative options, in this section we provide a result showing what properties a parameter defined with zero-valued outcomes can have. Specifically, we establish a “trilemma”: When there are zero-valued outcomes, there is no parameter that is (a) an average of individual-level treatment effects of the form , (b) scale-invariant, and (c) point-identified.161616Of course, not all parameters of the form can be interpreted as an average of individual treatment effects. For example is the fraction of individuals whose outcomes is positive under both treatments, rather than a treatment effect. Our results apply to all parameters of this form, regardless of whether they are average treatment effects per se. Any approach for settings with zero-valued outcomes must therefore abandon one of the properties (a)–(c); in Section 4 below we discuss several approaches that relax one (or more) of these requirements.

Before stating our formal result, we must make precise what we mean by scale-invariance and point-identification. We say that is scale-invariant if its value is the same under any re-scaling of the units of by a positive constant .

Definition 1.

We say that the function is scale-invariant if it is homogeneous of degree zero, i.e. for all .

jointdistWe next describe point-identification. We consider parameters that are identified without placing restrictions on treatment effect heterogeneity. As in Fan et al. (2017), this is formalized by considering parameters that can be learned if we know the marginal distributions of and , but not the full joint distribution of .

To connect treatment effect heterogeneity to the joint distribution of potential outcomes, consider the simple case of a randomized experiment. By examining the outcome distribution for the treated group, we can learn the marginal distribution of . Likewise, by examining the outcome distribution for the control group, we can learn the marginal distribution of . If treatment effects were assumed to be constant, then for each observed treated unit with outcome , we could infer their untreated outcome as , where is the average treatment effect. Hence, the joint distribution of would be identified. However, if we allow for treatment effect heterogeneity, then for an observed treated unit with outcome , we do not know what their value of would be, and thus we do not know the joint distribution of . This winds up being especially important in settings with an extensive margin, since when we observe the distribution of outcomes for treated units, it means that we do not know which of the treated units would have had a zero outcome under the control condition, and thus it is difficult to disentangle the intensive and extensive margins.171717In Appendix C, we discuss a variety of structural approaches that impose assumptions restricting the joint distribution, thus allowing us to separately point-identify the effects for the two margins.

With that intuition in mind, we now give a formal definition. Recall that denotes the joint distribution of , while denotes the marginal distribution of . We then say is point-identified if it depends on only through the marginals .

Definition 2 (Identification).

We say that is point-identified from the marginals at if for every joint distribution with the same marginals as (i.e. such that for ), . For a class of distributions , we say that is point-identified over if for every is point-identified from the marginals at .

We will denote by the set of distributions on . Thus, is point-identified over if it is always identified when takes on zero or weakly positive values. Our next result formalizes that it is not possible to have a parameter of the form that is both scale-invariant and point-identified over .

Proposition 2 (A trilemma).

The following three properties cannot hold simultaneously:

-

(a)

for a non-constant function that is weakly increasing in its first argument.

-

(b)

The function is scale-invariant.

-

(c)

is point-identified over .181818A minor technical complication arises from the fact that could be infinite for some . For the purposes of our result, it suffices to trivially define to be identified in this case. Alternatively, the same result holds if part (c) is modified to impose only that is point-identified over all distributions in with finite support, thus avoiding issues related to undefined expectations.

Any parameter defined with zero-valued outcomes must therefore abandon one of properties (a)–(c).

As a special case, 2 implies that the ATE for any increasing function defined at zero cannot be scale-invariant. This is because the ATE for takes the form in (a) with , and is also point-identified (part (c)). It follows that property (b) must be violated, i.e. there is some such that . 2 thus formalizes the sense in which it is not possible to “fix” the issues with ATEs for log-like transformations described above by taking alternative transformations of the outcome (e.g. ).

3.1 Implications for settings without an extensive margin

The trilemma in 2 applies for transformations of the outcome defined at zero. To prove 2, however, we establish an even stronger result: the only parameter satisfying properties (a) and (b) that is point-identified over distributions for which is strictly positively-valued is the ATE in logs.191919More precisely, the only such treatment effect is the ATE in logs or an affine tranformations thereof. This result, which is formalized in 3 in the Appendix, has some useful implications for settings in which the outcome is strictly positive.

First, it implies that the ATE for any transformation of the outcome other than will depend on the units of the outcome for at least some DGP where the outcome is strictly positive. The scale-dependence of log-like transformations such as or is thus not entirely limited to settings with an extensive margin.202020There is thus no conflict between our results and those in Thakral and Tô (2023), who note that semi-elasticities for OLS regressions using log-like transformations may depend on the units of the outcome even when is strictly positively-valued. We note, however, that while the ATE for such transformations may depend on the units of the outcome even without zero-valued outcomes, the dependence need not be arbitrarily bad in the sense of 1. Indeed, (2) shows that if there is no extensive margin, the ATE for a log-like transformation will be approximately insensitive to scaling once the values of are made large. This is intuitive, since if is strictly positively-valued, the ATE for a log-like transformation will be approximately equal to the ATE in logs when the values of are made large.

Second, 3 implies that even when and are strictly-positively valued, the average proportional effect is not point-identified. This parameter is empirically relevant: For instance, Andrews and Miller (2013) show that in the Baily (1978)–Chetty (2006) model with heterogeneous consumption responses to unemployment, the optimal level of unemployment insurance depends on a parameter of the form , where is consumption and is unemployment. Although the ATE in logs may approximate when the proportional effect of the treatment is approximately constant, our results imply that it is not possible to point-identify when allowing for arbitrarily heterogeneous proportional effects.

4 Empirical approaches with zero-valued outcomes

Our theoretical results above imply that when there are zero-valued outcomes, the researcher should not take a log-like transformation of the outcome and interpret the resulting ATE as an average percentage effect: Unlike a percentage, such an ATE depends on the units of the outcome. In this section, we highlight some other parameters that are well-defined and easily interpreted when there are zero-valued outcomes; in Section 5 below, we show how these parameters can be estimated in three empirical applications. Of course, any alternative parameter must necessarily drop one of the requirements in the trilemma in LABEL:prop:trilemma, but the choice of which to drop may depend on the researcher’s motivation.

To inform our discussion of alternative parameters, it is therefore useful to first enumerate several reasons why empirical researchers may target treatment effects for a log-transformed outcome rather than the ATE in levels:

-

(i)

The researcher is interested in reporting a treatment effect parameter with easily-interpretable units, such as “percentage changes.”

-

(ii)

The researcher believes that there are decreasing returns to the outcome, and thus wants to place more weight on treatment effects for individuals with low initial outcomes. For instance, the researcher may perceive it to be more meaningful to raise income from to than from to , yet both of these treatment effects contribute equally to the ATE in levels.

-

(iii)

The researcher is interested in both the intensive and extensive margin effects of the treatment, and is using the ATE for a log-like transformation as an approximation to the proportional effect along the intensive margin.

These three motivations suggest different ways of breaking out of the trilemma in 2. If the goal is to achieve a percentage interpretation, then one can consider scale-invariant parameters outside of the class . For instance, researchers can consider the ATE in levels expressed as a percentage of the control mean, or the ATE for a normalized parameter that already has a percentage interpretation. Alternatively, if the goal is to capture concave social preferences over the outcome, then it is natural to specify how much we value the intensive margin relative to the extensive margin—thus abandoning scale-invariance. Finally, if the goal is to separately understand the intensive margin effect, the researcher can abandon point-identification (from the marginal distributions) and directly target the partially identified parameter , the effect in logs for individuals with positive outcomes under both treatments. We address each of these cases in turn below, with a summary of some possible parameters in Table 2.

| Description | Parameter | Main property sacrificed? | Pros/Cons |

|---|---|---|---|

| Normalized ATE | Pro: Percent interpretation Con: Does not capture decreasing returns | ||

| Normalized outcome | Pro: Per-unit- interpretation Con: Need to find sensible | ||

| Explicit tradeoff of intensive/extensive margins | ATE for | Scale-invariance | Pro: Explicit tradeoff of two margins Con: Need to choose ; Monotone only if support excludes |

| Intensive margin effect | Point-identification | Pro: ATE in logs for the intensive margin Con: Partial identification |

Remark 8 (Statistical reasons for transforming the outcome).

We focus on settings where the researcher is interested in a parameter other than the ATE in levels. \CopyestimatedifficultIn some settings, the researcher may be interested in the ATE in levels, but simple regression estimators may be noisy owing to a long right-tail of the outcome (Athey et al., 2021). The researcher might then try to estimate the ATE in levels by first estimating the ATE for a log-like transformation, and then multiplying by the baseline mean. However, since the ATE for a log-like transformation depends on the units of the outcome—and is thus not a true “percentage” effect—the validity of this approach for recovering the ATE in levels will depend on the initial units of .212121Even in the case where is strictly positive and one first estimates the ATE in logs, this approach will only recover the ATE in levels under certain homogeneity assumptions, e.g. constant proportional effects. See Wooldridge (1992) for related discussion. We refer the reader to Athey et al. (2021) and Müller (2023) for alternative approaches to estimation and inference targeted to settings where the ATE in levels is of interest but the outcome has heavy tails.

identificationdid

Remark 9 (Transformation-specific identification).

Another reason that researchers may consider taking a transformation of the outcome is that a parametric assumption used for identification may be more plausible for some functional forms than others. For example, when the outcome is strictly positive, parallel trends in logs may be more plausible than parallel trends in levels if time-varying factors are thought to have a multiplicative impact on the outcome. We note that justifying parallel trends for a log-like transformation is especially tricky, however, since if parallel trends holds for the of an outcome measured in dollars, say, it will not generally hold for the of the outcome measured in cents (Roth and Sant’Anna, 2023). Thus, the parallel trends assumption is specific to both the transformation and the units of the outcome. Moreover, even if the researcher is confident in parallel trends for a particular log-like transformation and unit of the outcome, our results imply that they should not interpret the resulting ATT as an average percentage effect, since that ATT is dependent on the units in which the outcome is measured (1).

In what follows, we consider alternative parameters that may be of interest when the marginal distributions of the potential outcomes are identified for some population of interest. Such identification is obtained in RCTs or under conditional unconfoundedness (for the full population), as well in instrumental variables settings (for the population of compliers), as these designs do not rely on functional form assumptions for identification. If the original identification strategy relies on a functional form assumption (e.g. parallel trends), then obtaining identification of the alternative parameters discussed below may require different identifying assumptions. We discuss these issues in detail in Section 5.2, where we revisit the difference-in-differences application in Sequeira (2016).

4.1 When the goal is interpretable units

We first consider the case where the researcher’s primary goal is to obtain a treatment effect parameter with easily interpretable units, such as percentages.

Normalizing the ATE in levels.

One possibility is to target the parameter

which is the ATE in levels expressed as a percentage of the control mean. For example, if a researcher is studying a program meant to reduce healthcare spending , then is the percentage reduction in costs from implementing the program. This parameter is point-identified and scale-invariant, and thus has an intuitive percentage interpretation. Importantly, however, is the percentage change in the average outcome between treatment and control, but is not an average of individual-level percentage changes.222222This is roughly analogous to how quantile treatment effects show changes in the quantiles of the potential outcomes distributions, but not the quantiles of the treatment effects (without further assumptions). That is, does not take the form , thus avoiding the trilemma in 2.

We note that is consistently estimable by Poisson regression (see Gourieroux et al. (1984); Santos Silva and Tenreyro (2006); Wooldridge (2010, Chapter 18.2)) under an appropriate identifying assumption. With a randomly assigned , for example, estimation of by Poisson quasi-maximum likelihood (QMLE) consistently estimates the population coefficient , which satisfies . In Section 5 below, we illustrate how can be estimated by Poisson regression in practice in several empirical examples, including both an RCT and DiD setting.

nuisancezerosWe also emphasize that is influenced by treatment effects along both the intensive and extensive margins. In particular, the numerator of is the ATE in levels. Thus, if an individual has a treatment effect of say 1, that contributes the same to regardless of whether their outcome changes from 0 to 1 (an extensive margin change) or 1 to 2 (an intensive margin change). The parameter may therefore be attractive in settings where the researcher does not want to distinguish between the intensive and extensive margins. For example, if is a count of publications by a researcher in a particular year, and publications are sometimes zero owing to the idiosyncracies of the publication process, then it may be reasonable to view a change between 0 and 1 as similar to a change between 1 and 2. On the other hand, in settings where a zero corresponds to a distinct economic choice, such as not participating in the labor market, then it may be of interest to separate the effects along the intensive and extensive margin, as we discuss in more detail in LABEL:subsec:two_margins below.

elonmuskIt is also worth noting that if the researcher has determined that the ATE in levels is not of economic interest, then similar issues will likely arise for , since is just a re-scaling of the ATE in levels. For one, the ATE in levels (and hence ) imposes no diminishing returns, and thus might be dominated by individuals in the tail of the outcome distribution, particularly when the outcome is skewed. Whether this is warranted will depend on the economic question: if the policy-maker’s goal is to reduce healthcare spending, it may not matter whether the savings are produced mainly by reducing spending for a small fraction of individuals with catastrophic medical spending. On the other hand, a policy that increases every American’s income by $100 and one that increases Elon Musk’s income by $35 billion and has no effect on anyone else would have approximately the same value of , yet the former may be vastly preferred by an inequality-minded policy-maker. We therefore next turn to alternative approaches that place less weight on the tails of the outcome distribution.

Normalizing other functionals.

While normalizes the ATE by the control mean, one can obtain scale-invariance by normalizing other functionals of the potential outcomes distributions.232323Indeed, any functional is homogeneous of degree zero if and only if it can be written as the ratio of two homogeneous of degree one functionals. For example,

is the quantile treatment effect at the median normalized by the median of .242424Note that is well-defined only if . Put otherwise, it captures the percentage change in the median between the treated and control distributions. ( thus may be particularly relevant for politicians interested in maximizing the happiness of the median voter!) As is typically the case with quantile treatment effects, however, the numerator of need not correspond to the median of individual-level treatment effects. Moreover, in many settings, decision-makers may care about treatment effects throughout the distribution, not just at the median, in which case may not be the most economically-relevant parameter.

Normalizing the outcome.

A related approach to obtaining a treatment effect with more intuitive units is to estimate the ATE for a transformed outcome that has a percentage interpretation. One example is to consider an outcome of the form , where is the original outcome and is some pre-determined characteristic. For example, suppose is employment in a particular area. The treatment effect in levels for may be difficult to interpret, since a change in employment of 1,000 means something very different in New York City versus a small rural town. However, if is the area’s population, then is the employment-to-population ratio, which may be more comparable across places, and is already in percentage (i.e. per capita) units. We note that the ATE for is a scale-invariant, point-identified parameter of the form , and thus escapes the trilemma in LABEL:prop:trilemma by avoiding property (a).252525It is scale-invariant in the sense that . The viability of this approach, of course, depends on having a variable such that the normalized outcome is of economic interest. We suspect that in many contexts, reasonable options will be available, including pre-treatment observations of the outcome (assuming these are positive), or the predicted control outcome given some observable characteristics (i.e., , for observable characteristics ).

A second example is to use , where is the cumulative distribution function (CDF) of some reference random variable , as suggested in Delius and Sterck (2020). The transformed outcome then corresponds to the rank (i.e. percentile) of an individual in the reference distribution, and the ATE for can be interpreted as the average change in rank caused by the treatment. The ATE for is unit-invariant so long as and and measured in the same units. Outcomes of this form have become increasingly popular in the literature on intergenerational mobility, where corresponds to a child’s rank in the national income distribution. This approach has been found to yield more stable estimates than approaches using , which Chetty et al. (2014) show are sensitive to the choice of .262626Similar to the discussion in Footnote 21, the treatment effect in ranks cannot be converted back to obtain the ATE in levels without additional assumptions.

Finally, the researcher might report treatment effects on transformed outcomes of the form for different values of . For example, the researcher might report the impact of the treatment on the probability that an individual earns at least $50,000, $60,000, etc., and interpret it as the treatment effect on the probability of obtaining a “well-paying job.”272727The researcher could also report the implied CDF of and , from which one can infer the treatment effect on outcomes of this form for all . Such treatment effects have interpretable units as percentage points (i.e. changes in probabilities). We note that treatment effects for outcomes of this form combine the effect of the treatment along the intensive and extensive margin, since for example, a worker who has could either not work under control () or work under control but have earnings below $50,000.

4.2 When the goal is to capture decreasing returns

We next consider the case where the researcher wants to capture some form of decreasing marginal utility over the outcome. For example, when is strictly positively valued, the ATE in logs corresponds to the change in utility from implementing the treatment for a utilitarian social planner with log utility over the outcome, . Intuitively, this social welfare function captures the fact that the planner values a percentage point of change in the outcome equally for all individuals, regardless of their initial level of the outcome.

Of course, log utility is not well-defined when there is an extensive margin: A coherent utility function defined with zero-valued outcomes must take a stand on the relative importance of the intensive versus extensive margins. Recall from Section 2.1 that when using transformations like or , the scaling of the outcome implicitly determines the weights placed on these margins.

Instead of implicitly weighting the margins via the scaling of , a more transparent approach is to explicitly take a stand on how much one values the two margins of treatment. Of course, if one knows that their utility is captured by (for a particular unit of , say earnings in dollars), then the ATE for is appropriate. If one is unsure exactly of their utility function, then a rough calibration is to specify how much one values a change in earnings from 0 to 1 relative to a percentage change in earnings for those with non-zero earnings. If, for example, one values the extensive margin effect of moving from 0 to 1 the same as a percent increase in earnings, then one might consider setting for and . The ATE for this transformation can be interpreted as an approximate percentage (log point) effect, where an increase from 0 to 1 is valued at log points.282828Note that this transformation will generally only be sensible if the support of excludes , since otherwise the function is not monotone in over the support of . It is common, however, to have a lower-bound on non-zero values of the outcome; e.g., a firm cannot have between 0 and 1 employees. In our application to Sequeira (2016) below, we normalize the minimum non-zero value of to 1 when applying this approach.

We emphasize that for a fixed value of , this approach necessarily depends on the scaling of the outcome (thus avoiding the trilemma in 2). However, this may not be so concerning since the appropriate choice of also depends on the units of the outcome—e.g., saying a change from 0 to 1 is worth percent means something very different if 1 corresponds with one dollar versus a million dollars. In other words, ATEs for transformations such as may be difficult to interpret because the scaling of the outcome implicitly determines the relative importance of the intensive and extensive margins; this approach avoids that difficulty by explicitly taking a stand on the tradeoff between these two margins. Nevertheless, a challenge with this approach is that researchers may have differing opinions over the appropriate choice of (or more generally, over the appropriate utility function).

4.3 When the goal is to understand intensive and extensive margins

Finally, we consider the case where the researcher is interested in understanding the intensive and extensive margin effects separately. A common question in the literature on job training programs (Card et al., 2010), for instance, is whether a program raises participants’ earnings by helping them find a job—which would be expected only to have an extensive-margin effect—or by increasing human capital, which would be expected to also affect the intensive margin. In such settings, it is natural to target separate parameters for the intensive and extensive margins.

For example, the parameter

captures the ATE in logs for those who would have a positive outcome regardless of their treatment status. The parameter is scale-invariant but is not point-identified from the marginal distributions of the potential outcomes (thus avoiding the trilemma in LABEL:prop:trilemma), and therefore cannot be consistently estimated without further assumptions.292929 also does not take the form , although it can be written as where both the numerator and denominator take this form. However, Lee (2009) popularized a method for obtaining bounds on under the monotonicity assumption that, for example, everyone with positive earnings without receiving a training would also have positive earnings when receiving the training.303030See, also, Zhang and Rubin (2003) for related results, including bounds without the monotonicity assumption. Bounds on can be reported alongside measures of the extensive margin effect, such as the change in the probability of having a non-zero outcome, . One can also potentially tighten the bounds (or restore point-identification) by imposing additional assumptions on the joint distribution of the potential outcomes—we provide an example of this in our application to Carranza et al. (2022) below; see Zhang et al. (2008, 2009) for related approaches.313131We note that the Lee (2009) bounds will tend to be tight when the extensive margin effect is close to zero. As noted in LABEL:rmk:finite_changes_in_scale, this is precisely the setting where ATEs for log-like transformations are relatively insensitive to finite changes in scale.

We note that the parameter is generally distinct from the “intensive margin” marginal effects implied by two-part models (2PMs), which were recommended for scenarios with zero-valued outcomes by Mullahy and Norton (2023), among others. In Appendix D, we consider the causal interpretation of the marginal effects of 2PMs, building on the discussion in Angrist (2001). Our decomposition shows that the marginal effects from 2PMs yield the sum of a causal parameter similar to as well as a “selection term” comparing potential outcomes for individuals for whom treatment only has an intensive margin effect to those with an extensive margin effect. It thus will generally be difficult to ascribe a causal interpretation to the marginal effects of 2PMs without assumptions about this selection.

5 Empirical applications

In this section, we focus on three concrete empirical applications to illustrate how the alternative parameters described in Section 4 can be estimated in practice. To illustrate a range of possible applications, we consider a randomized controlled trial, a difference-in-differences design, and an instrumental variables design.

5.1 An RCT setting: Carranza et al. (2022)

Carranza et al. (2022) conduct a randomized controlled trial (RCT) in South Africa. Individuals randomized to the treatment group are provided with certified test results that they can show to prospective employers to vouch for their skills. Individuals in the control group do not receive test results.323232Some individuals are also assigned to a “placebo” arm in which they are provided the test results but the form does not include the individual’s name, and thus cannot credibly be shared with employers. We focus on the effect of the main treatment relative to the pure control group. They then investigate how this treatment impacts labor market outcomes such as employment, hours worked, and earnings. We focus here on the effects on hours worked.

Original specification and sensitivity to units.

Carranza et al. (2022) estimate the effect of their randomized treatment on the inverse hyperbolic sine of weekly hours worked. Formally, they estimate the OLS regression specification

| (3) |

where is average weekly hours worked for unit , is an indicator for whether unit was in the treatment group, and is a vector of controls.333333Carranza et al. (2022) include individuals receiving the “placebo” treatment in the sample and add an indicator for receiving the placebo treatment in . We follow the same practice, although the results are similar if units receiving the placebo treatment are dropped. Their estimate of the ATE () is 0.201 (see column (1) in Table 3). They interpret this as a 20% change in hours: “Certification increases average weekly hours worked, coded as zero for nonemployed candidates, by 20 percent” (p. 3560).

| arcsinh(weekly hrs) | arcsinh(yearly hrs) | arcsinh(FTEs) | |

| Treatment | 0.201 | 0.417 | 0.031 |

| (0.052) | (0.096) | (0.012) | |

| Units of outcome: | Weekly Hrs | Yearly Hrs | FTEs |

Note: This table shows estimates of the average treatment effect in Carranza et al. (2022) on the inverse hyperbolic sine of hours worked, estimated using (3). In the first column, the outcome is the inverse hyperbolic sine of weekly hours, as in the original paper. The remaining columns use the inverse hyperbolic sine of annualized hours (weekly hours times 52) or the inverse hyperbolic sine of the number of full-time equivalents worked (weekly hours divided by 40). Standard errors are clustered at the assessment date (the unit of treatment assignment) as in the original paper.

However, the results in Section 2 suggest that the estimate of should not be interpreted as a percentage effect, since it depends on the units of the outcome. To illustrate this, in columns (2) and (3) we re-estimate specification (3) with redefined to be (a) yearly hours worked, i.e. weekly hours times 52, or (b) the number of full-time equivalents (FTE) worked, i.e. weekly hours divided by 40. The results change quite substantially depending on the units used, with an estimate of 0.417 using yearly hours and 0.031 using FTEs. We therefore turn next to alternative approaches with a percentage interpretation in this setting.

Percentage changes in the average.

The average number of (weekly) hours worked was 9.84 in the treated group and 8.85 in the control group. A simple summary of the treatment effect is thus that average hours worked were 11% higher in the treated group (). This is an estimate of the parameter discussed in Section 4.1 above. A numerically equivalent way to obtain this estimate of 11% is to use Poisson quasi-maximum likelihood estimation (Poisson QMLE) to estimate

| (4) |

and then calculate (see column (1) in LABEL:tbl:_poissoncarranza).343434This estimation is done in the sample of treated units and control units, discarding the placebo group. One could equivalently retain the units in the placebo group and add an indicator for the placebo group to (4). This formulation in terms of Poisson QMLE is useful since it allows us to include covariates to potentially increase precision. Column (2) of Table 4 shows the estimate of from estimating

| (5) |

by Poisson QMLE, with smaller standard errors than in column (1) (0.069 vs. 0.081).

| (1) | (2) | |

| 2.180 | 0.150 | |

| (0.058) | (0.311) | |

| 0.106 | 0.150 | |

| (0.072) | (0.060) | |

| Implied Prop. Effect | 0.112 | 0.150 |

| (0.081) | (0.069) | |

| Covariates | N | Y |

Note: the first two rows of column (1) show the estimates of the coefficients and in (4), estimated using Poisson QMLE. The third row shows the implied estimate of the proportional effect, , calculated as . The second column shows analogous estimates using (5), which adds controls for pre-treatment covariates (we do not show the coefficients on the controls in the interest of brevity). Standard errors are clustered at the assessment date (the unit of treatment assignment) as in the original paper.

Separate estimates for the extensive/intensive margins.

As shown in Table 1, the treatment in Carranza et al. (2022) has an estimated extensive margin treatment effect of 0.055, meaning that it increases the fraction of people with positive hours worked by 5.5 percentage points. We may be interested in whether the overall 11% increase in hours worked is driven entirely by the extensive margin, or whether there is an intensive margin effect. That is, does the treatment increase hours only by bringing people into the labor force, or does it also allow people who would have worked anyway to find jobs with more hours (e.g. full-time instead of part-time)? To this end, we can use the method of Lee (2009) to compute bounds for the effect of the treatment for “always-takers” who would have positive hours worked regardless of treatment ().353535We again exclude units receiving the “placebo treatment.” The Lee bounds approach requires the monotonicity assumption that anyone who would work positive hours without the treatment would also work positive hours when treated (i.e., ). This seems reasonable if workers only share the information provided by the treatment when it helps their job prospects. It could be violated, however, if workers mistakenly share their test score results when in fact employers view them negatively.

Column 1 of Table 5 reports bounds of for the effect of the treatment on log hours worked by the always-takers, while Column 2 shows bounds of for weekly hours (in levels). Unfortunately, in this setting the Lee bounds are fairly wide, including both a zero intensive-margin effect as well as fairly large intensive-margin effects (up to 28 log points). Thus, without further assumptions, the data is not particularly informative about the size of the intensive margin.

We can, however, say more if we are willing to impose some assumptions about how the always-takers, who would work regardless of treatment status (), compare to the compliers (), who only work positive hours when receiving the treatment. We might reasonably expect that the compliers are negatively selected relative to the always-takers and thus would work fewer hours when receiving treatment. We can formalize this by imposing that , i.e. that average hours worked for compliers under treatment is % lower than for always takers. Columns 3 through 5 of Table 5 report estimates of the average effect on the always-takers, assuming , and , respectively.363636Under the assumptions in Lee (2009), , where . Plugging in , it follows that . Further, . Our estimation plugs in sample analogs to these expressions to estimate . If we assume that always-takers and compliers work an equal number of hours under treatment (), then our point estimates suggest that there is actually a negative intensive-margin effect for the always-takers ( weekly hours). Under the assumption that compliers work 25% fewer hours (), the estimated effect for always-takers is near zero ( weekly hours), consistent with no important intensive margin. Finally, if we assume compliers work half as many hours as the always-takers (), then our estimates suggest a positive intensive margin effect ( weekly hours). Our assessment of the importance of the intensive margin thus depends on how negatively-selected we think compliers are relative to always-takers.

| (1) | (2) | (3) | (4) | (5) | |

| Lower bound | |||||

| Upper bound | |||||

| Point estimate | |||||

| units | Log(Hours) | Hours | Hours | Hours | Hours |

Note: This table shows bounds and point estimates of the intensive margin treatment effect in Carranza et al. (2022), i.e. the treatment effect on hours worked for “always-takers” who would work positive hours regardless of treatment status. The first first two columns of the table show Lee (2009) bounds for the effect of treatment on the always-takers when the outcome is and weekly hours, respectively. Columns 3 through 5 show point estimates for the effect on weekly hours worked for always-takers under the assumption that average hours worked by “compliers” (who work only when treated) are lower than for the always-takers. Standard errors are calculated via a non-parametric bootstrap using 1,000 draws, clustered at the assessment date level.

5.2 A DiD setting: Sequeira (2016)

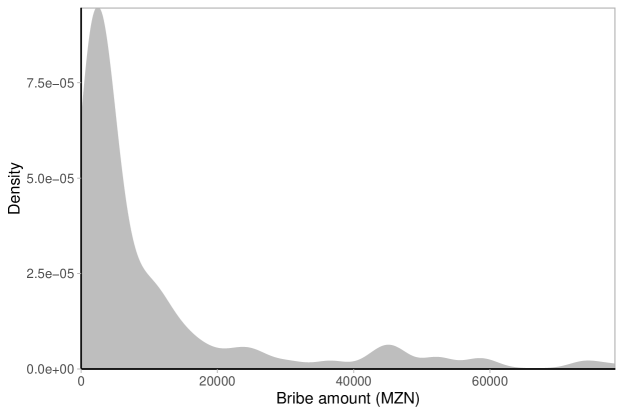

Sequeira (2016) studies a decrease in tariffs on trade between Mozambique and South Africa which occurred in 2008. She is interested in whether the reduction in tariffs reduced bribes paid to customs officers (among other outcomes). To study this question, she utilizes a difference-in-differences design comparing the change in bribes paid for products that were affected by the tariff change to that for a comparison group of products that did not experience a change in tariffs.

Original specification and sensitivity to units.

Sequeira (2016) has repeated cross-sectional data with information on the bribe amount paid on shipment in year . She estimates the regression specification

| (6) |

where is an indicator for whether shipment is for a product type affected by the tariff change in 2008, is an indicator for whether year is after the tariff change, and is a vector of covariates related to shipment in period . Sequeira (2016) estimates (6) with measured in 2007 Mozambican Metical (MZN) and obtains (SE ). However, estimating the same specification with measured in thousands of U.S. dollars instead yields an estimate of (SE ).373737We use the conversion rate of as of January 1, 2007, as provided by fxtop.com. These results reinforce the conclusion from LABEL:sec:_loglikeresults that treatment effects for should not be interpreted as approximating a percentage effect.

In what follows, we discuss a variety of alternative approaches that may be reasonable in this context. We note that in a non-experimental setting like this, different approaches may rely on different identifying assumptions. We therefore explicitly discuss the identifying assumptions needed by each of the methods we discuss.

Proportional treatment effects.

One natural approach here is to target the average proportional treatment effect on the treated,

This is the percentage change in the average outcome for the treated group in the post-treatment period.

Identification of requires us to infer the counterfactual post-treatment mean outcome for the treated group, . Of course, one approach to obtain such identification would be to assume parallel trends in levels. However, given that the treated and control groups have different pre-treatment means (see the bottom panel of Table 6), it may be unreasonable to expect that time-varying factors (e.g. the macroeconomy) have equal level effects on the outcome. An alternative identifying assumption is to impose that, in the absence of treatment, the percentage changes in the mean would have been the same for the treated and control group. As in Wooldridge (2023), this can be formalized using a “ratio” version of the parallel trends assumption,

| (7) |

Intuitively, (7) states that if the treatment had not occurred, the average percentage change in the mean outcome for the treated group would have been the same as the average percentage change in the mean outcome for the control group. Under (7), we can thus estimate the counterfactual percentage change in the mean outcome for the treated group using the observed percentage change for the control group.

Table 6 shows that the sample mean of the outcome for the treated group decreased by 75% between the pre-treatment and post-treatment periods (from 4,742 to 1,172 (MZN)). Under the ratio parallel trends assumption (7), this suggests that the mean outcome for the treated group would also have decreased by 75% in the absence of treatment, thus implying an estimate of for the counterfactual mean outcome for the treated group. The actual post-treatment mean for the treated group is 465, which is 82% below this implied counterfactual. This implies that the tariff reduction reduced the average bribe in the post-treatment period by 82%, i.e. . Conveniently, this estimate can also be obtained using Poisson QMLE to estimate

| (8) |

and then computing , as shown in column (1) of Table 6.

| (1) | (2) | |

| Post Treatment | ||

| Prop. Effect | ||

| Covariates | N | Y |

| Treated Group Means (Pre, Post): | 10527 | 465 |

| Treated Group Means (Pre, Post): | 4742 | 1172 |

Note: this table shows Poisson regression estimates of (8) and (9) in columns (1) and (2), respectively. The first row of the table shows the estimate . The second row shows , which is the implied estimate of the proportional treatment effect . The coefficients on control variables are omitted for brevity. Standard errors are clustered at the four-digit product code as in the original paper. The mean bribe amounts (in MZN) by treatment group and time period are displayed in the bottom panel. The pre-period refers to the year 2007, whereas the post-treatment period is an average over the years 2008, 2011, and 2012 (the three post-treatment years for which data is available).

We can also re-incorporate the covariates by estimating

| (9) |

which yields an estimate of of , as shown in the second column of Table 6. As formalized in Wooldridge (2023), this estimate will be a consistent estimate of if (7) holds conditional on , and the conditional expectation of takes the functional form implied by (9) (assuming has mean 1 conditional on the covariates). The approach with covariates thus suggests that the tariff change reduced the average bribe for treated products by 72% in the post-treatment period.

Sequeira (2016)’s data only contains information on one year prior to treatment (2007), and so in this context it is not possible to evaluate the plausibility of (7) using periods prior to the policy change of interest. If multiple pre-treatment periods were available, however, one could estimate a Poisson QMLE event-study of the form

| (10) |

where is the time relative to the treatment date. The event-study coefficients for are analogous to “pre-trends” coefficients in typical difference-in-differences event-studies, and are informative about whether the pre-treatment analogue to (7) holds.383838More precisely, the exponentiated coefficients correspond to the implied “placebo” proportional treatment effects for periods before treatment. We recommend plotting the exponentiated coefficients in event-studies, although we note that for . As with typical tests for pre-trends, one should be cautious that a failure to reject the null that the pre-treatment coefficients equal zero does not necessarily imply that the identifying assumption is satisfied (Kahn-Lang and Lang, 2020; Roth, 2022). One can (partially) address these issues by applying sensitivity analysis tools for event-studies (e.g. Rambachan and Roth, 2023) to estimates of (10) to further gauge the robustness of the findings to violations of the identifying assumptions. We also refer the reader to Wooldridge (2023) for extensions of the Poisson regression approach to settings with staggered treatment timing.

Log effects with calibrated extensive margin value.