mathx”17

Correlation matrix of equi-correlated normal population: fluctuation of the largest eigenvalue, scaling of the bulk eigenvalues, and stock market

Abstract

Given an -dimensional sample of size and form a sample correlation matrix . Suppose that and tend to infinity with converging to a fixed finite constant . If the population is a factor model, then the eigenvalue distribution of almost surely converges weakly to Marčenko-Pastur distribution such that the index is and the scale parameter is the limiting ratio of the specific variance to the -th variable . For an -dimensional normal population with equi-correlation coefficient , which is a one-factor model, for the largest eigenvalue of , we prove that converges to the equi-correlation coefficient almost surely. These results suggest an important role of an equi-correlated normal population and a factor model in (Laloux et al. Random matrix theory and financial correlations, Int. J. Theor. Appl. Finance, 2000): the histogram of the eigenvalue of sample correlation matrix of the returns of stock prices fits the density of Marčenko-Pastur distribution of index and scale parameter . Moreover, we provide the limiting distribution of the largest eigenvalue of a sample covariance matrix of an equi-correlated normal population. We discuss the phase transition as to the decay rate of the equi-correlation coefficient in .

keywords:

Portfolio, Marčenko-Pastur distribution, financial correlations, factor model1 Introduction

For risk management and asset allocation, a sample correlation matrix is essential. One of the pillars of Markowitz portfolio theory (Markowitz, 1959; Elton et al., 2014) is the study of correlation (or covariance) matrices, e.g., the optimal weight of each financial asset, given a set of assets with average returns and risks, so that the overall portfolio offers the best return for a fixed level of risk or, alternatively, the smallest risk for a given overall return. For these optimizations, the eigenvalues of covariance/correlating matrices are important. However, the eigenvalues of a sample covariance matrix/correlation matrix in finance are dispersed with noise, so various ways to eliminate noisy eigenvalues from them are studied by Laloux et al. (2000), El Karoui (2008), Ledoit & Wolf (2004, 2012), Ledoit & Péché (2011), Donoho et al. (2018), to cite a few. For this purpose, Laloux et al. (2000) proposed to approximate heuristically the distribution of noisy eigenvalues of a sample covariance/correlation matrix, with Marčenko-Pastur distribution (Marčenko & Pastur, 1967) of random matrix theory. Their idea influenced on the statistical methods on vaccine design (Quadeer et al., 2018). We will discuss the heuristic of Laloux et al. (2000) mathematically, with an equi-correlated normal population, which plays an important role in various risk models such as dynamic equicorrelation (Engle & Kelly, 2012) and constant correlation model (Elton et al., 2014).

First of all, we fix the notation. Let be a random sample. By the data matrix, we mean . Let and . The -entry of is denoted by , and the -th row by . For the sample average of , write . Let and . The sample correlation matrix is, by definition,

Here, the notation is the Euclidean norm. The sample covariance matrix is denoted by . By a distribution function, we mean a nondecreasing, right-continuous function such that and .

We review the results on eigenvalue distributions from random matrix theory. The empirical spectral distribution of a symmetric matrix is, by definition,

where are the eigenvalues of , indexed in nonincreasing order. According to (Yao et al., 2015; Bai & Silverstein, 2010, p. 10), Marčenko-Pastur distribution with the sample size to dimension ratio index and scale parameter has a density

| (1) |

and has a point mass of value at the origin if . Here, ,

and denotes the indicator function. Marčenko-Pastur distribution has expectation . The distribution function of Marčenko-Pastur distribution of the sample to dimension ratio index and scale parameter is denoted by . We write for . Clearly, for all . We say a sequence of distribution functions converges weakly to a function , if for every where is continuous.

Proposition 1.1.

However, the eigenvalues of financial correlation matrices distribute similarly as the random matrix theory suggests, but somehow differently. Laloux et al. (2000) considered a sample correlation matrix “associated to the time series of the different stocks of the S&P500 (or other major markets)” where is the number of assets and is the number of observations. Laloux et al. (2000) found that the histogram of the eigenvalues of the financial, sample correlation matrix fits not the density of , but a scaled density, specifically, the density of

| (2) |

In addition to the fitting result, for the first eigenvalue of , Laloux et al. remarked the following:

The corresponding eigenvector is, as expected, the “market” itself, i.e., it has roughly equal components on all the stocks.

Laloux et al. (2000) interpreted the support of the density function of the fitting Marčenko-Pastur distribution, as the interval of noisy eigenvalues of the sample correlation matrix . Based on the findings of Laloux et al. (2000), in order to improve risk management, Bun et al. (2017) proposed “eigenvalue clipping: all eigenvalues in bulk of the fitting Marčenko-Pastur spectrum are deemed as noise and thus replaced by a constant value whereas the principal components outside of the bulk (the spikes) are left unaltered.” As portfolios of hundreds or thousands of assets becomes the target of research, many approaches have been proposed to deal with the problem of dimensionality. By the limiting regime of Proposition 1.1, we would like to understand mathematically why the heuristic of Laloux et al. (2000) is meaningful.

Let us hypothesize about the population of the stock prices Laloux et al. considered, from their remark on the eigenvector that “has roughly equal components on all the stocks.” It is comparable to an eigenvector corresponding to the largest eigenvalue of an equi-correlation matrix

where

| (3) |

SenGupta (1988) studied hypothesis tests on vs. . Ishii et al. (2021) developed nonparametric tests of the high-dimensional covariance structures such as a scaled identity matrix, a diagonal matrix and for cases.

In particular, when , is unbounded with respect to , and thus there is a ‘spectral gap’ between and . We presume that the population is a normal population with the population correlation matrix .

Then, for an equi-correlated normal population, we established the following scaling theorem for the limiting distribution of the bulk eigenvalues of the sample correlation matrix :

Proposition 1.2 (Akama & Husnaqilati (2022)).

Let be a sample correlation matrix formed from an -dimensional normal population such that the population correlation matrix is with deterministic . Suppose . Then, almost surely, the empirical spectral distribution converges weakly to

It is worth noting that the limiting spectral distribution (LSD) is similar to Marčenko-Pastur distribution (2) where the histogram of the eigenvalues of a financial correlation matrix fits to the density of (2). The index and the scale parameter correspond to and , respectively.

By comparing (2) to Proposition 1.2, we will show that the largest eigenvalue of the sample correlation matrix divided by the order of converges almost surely to the equi-correlation coefficient , as follows. Hereafter, and mean the almost sure convergence and the convergence in distribution respectively. Unless otherwise stated, the limiting regime is .

Theorem 1.3.

Suppose the assumptions of Proposition 1.2. Then,

-

1.

.

-

2.

If, moreover, the population is and , then

where

From the first assertion, i.e., the consistency of , of Theorem 1.3, Proposition 1.2 suggests that an equi-correlated normal population plays a role in Laloux et al.’s fitting result to the density of (2):

Corollary 1.4.

Assume the assumptions of Proposition 1.2. Then,

Once the largest eigenvalue of is found, Corollary 1.4 can suggest the support of the density of the fitting Marčenko-Pastur distribution to clean up (“eigenvalue clipping”), and then we can eliminate the eigenvalues in the support to let a small, but important eigenvalue (e.g., Markowitz solution) show up. Moreover, has been concerned by Friedman & Weisberg (1981).

The rest of the paper is organized as follows. In the next section, to generalize Proposition 1.2, we consider suitable factor models. Then, we establish the limiting spectral distribution of the sample correlation matrix generated from such a factor model. In Section 3, for returns of S&P stock prices (2012-1-4/2021-12-31), we compute the largest eigenvalues of financial correlation matrices divided by the order, and estimate the time average of equi-correlation coefficient by GJR GARCH (Glosten et al., 1993) with the correlation structure being ‘equicorrelation’ (Engle & Kelly, 2012). We show that predicts very well . In Section 4, for a nonnormal population with equicorrelation coefficient decaying in , we review the consistency and the asymptotic normality of , by citing Yata & Aoshima (2009). Then, for the limiting distribution of an appropriate scaling of a translation of of equi-correlated normal population, we discuss the phase transition from the normal population to Tracy-Widom distribution (Baik et al., 2005), as to the decay rate of . The proofs of Theorem 1.3, Corollary 1.4, and Theorem 2.3 are postponed in Section 5, Section 6, and Section 7, respectively, for the sake of the presentation.

2 From equi-correlated normal population to factor models in limit

Proposition 1.2 was proved by the following well-known fact (Fan & Jiang, 2019, (3.21)): Assume that , , and . Then, there are independent standard normal random variables , such that

| (4) |

Actually, an equi-correlated normal population is a factor model (Bai, 2003; Mulaik, 2009) consisting of 1 factor. See Example 2.2. Beside this 1-factor model, a 3-factor model and a 5-factor model are employed by Fama & French (1993, 2015) to describe stock returns in asset pricing and portfolio management.

Bai (2003) studied an inferential theory for a general factor model of large dimensions to which classical factor analysis does not apply, by using limiting regime . He derived the limiting distributions of the estimated factors and estimated factor loadings, the asymptotic normality of estimated common components, and their convergence rates. The convergence rate of the estimated factors and factor loadings can be faster than that of the estimated common components. These achievements are obtained under liberal conditions that allow for correlations and heteroskedasticities. Stronger results are obtained when the idiosyncratic errors are serially uncorrelated and homoskedastic. A necessary and sufficient condition for consistency of the estimated factors is derived for large but fixed .

We will study a factor model in the limiting regime . First, we recall a factor model (Bai, 2003; Mulaik, 2009):

Definition 2.1.

For a nonnegative integer , by a -factor model, we mean a data matrix

such that

’s are called idiosyncratic components. is the number of factors.

Example 2.2.

The decomposition (4) is a factor model such that , , , , and both of and are independent and normal.

are i.i.d., and for some -dimensional row vector . In this case, define

Then, is the portion of the specific variance to the limiting total variance of a variable .

The following generalizes Proposition 1.2. The LSD of a sample correlation matrix generated from a factor model is as follows:

Theorem 2.3.

Given a factor model. Suppose and Assumption 2. Then, almost surely, converges weakly to .

3 The largest eigenvalue of financial correlation matrix

For a dataset of returns of S&P500 stocks (or other major markets) for trading days, Laloux et al. (2000) fitted the histogram of the eigenvalues of the correlation matrix , to the density function of a scaled Marčenko-Pastur distribution.

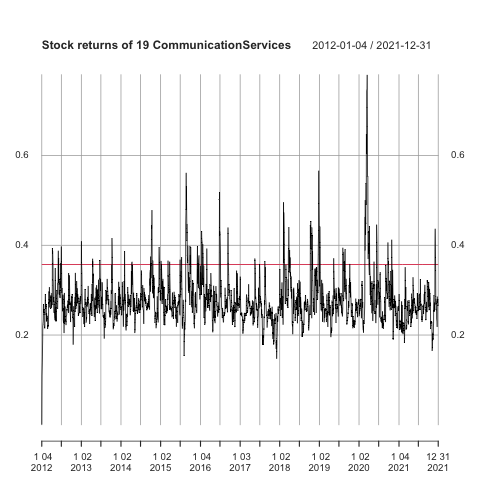

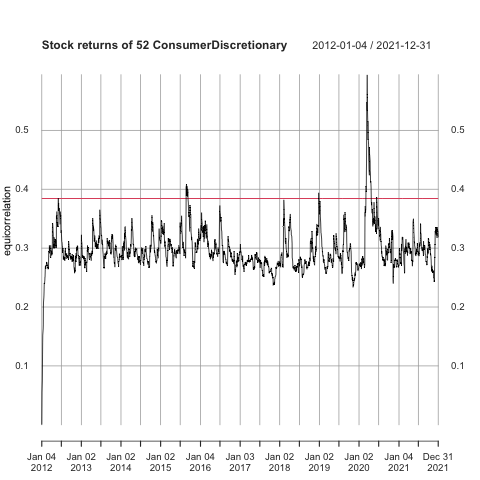

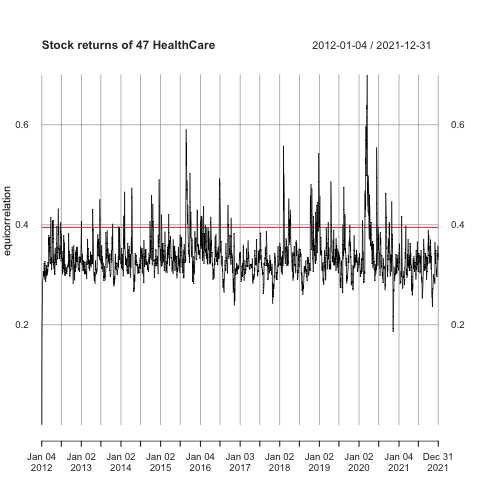

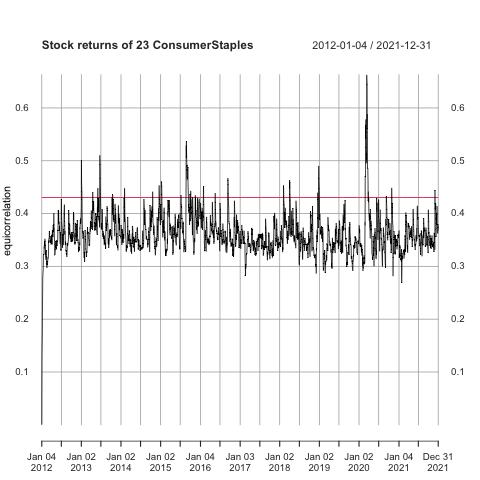

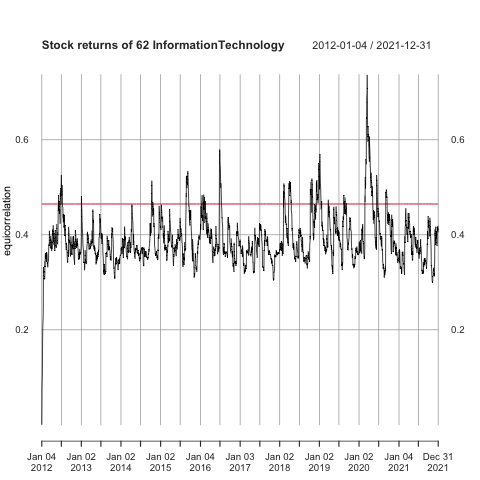

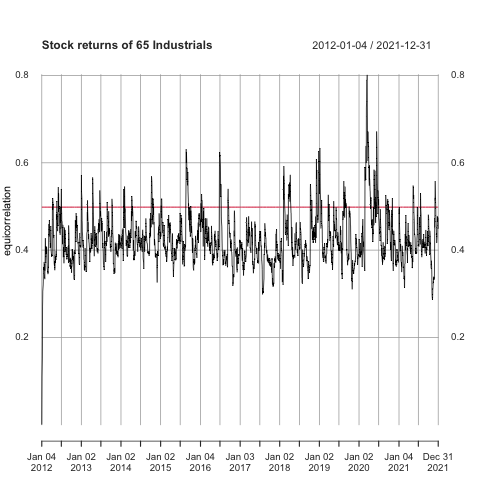

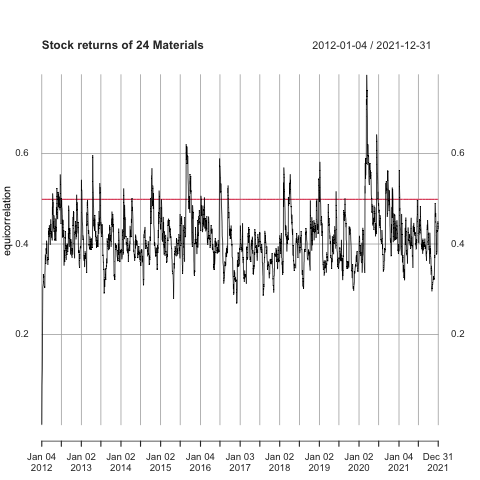

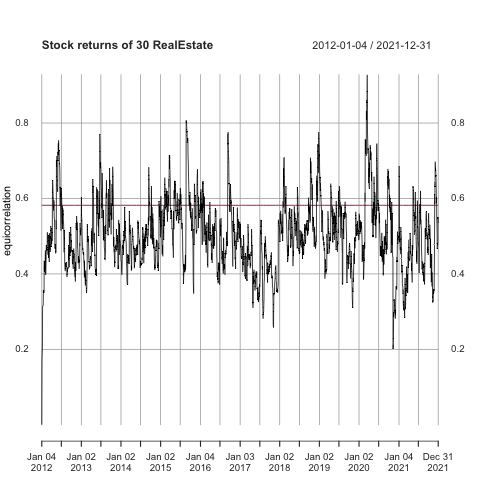

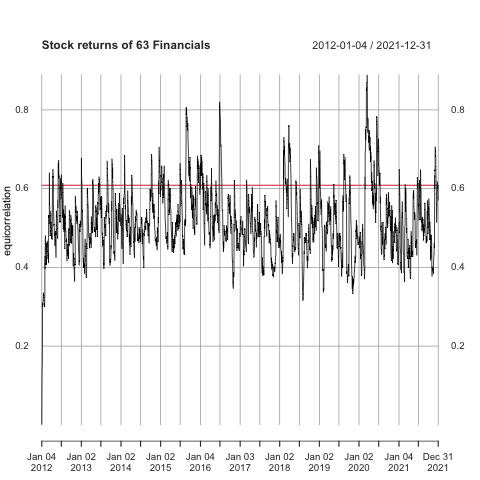

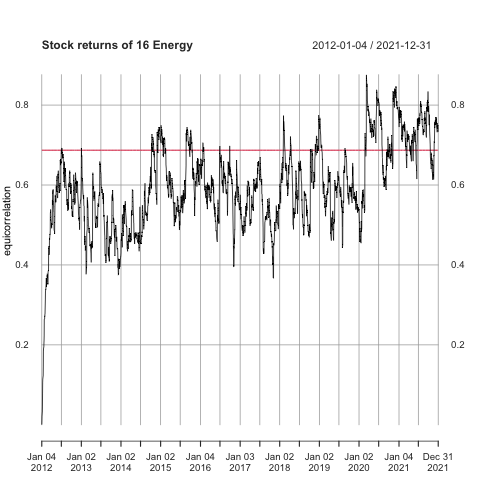

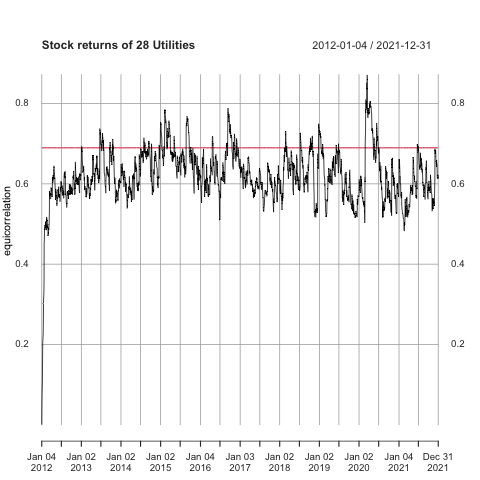

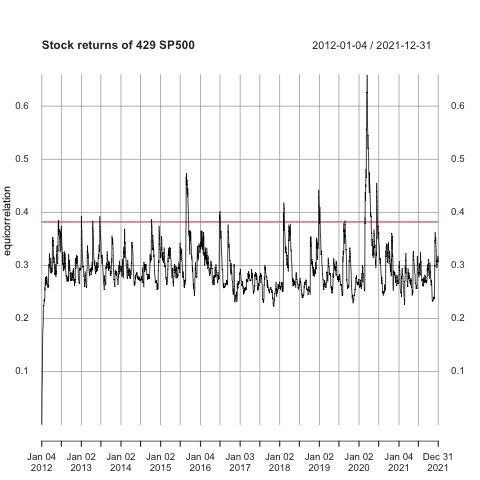

Naturally, the return of a stock is more correlated with the return of a stock of the same industry classification sector, than with the return of a stock of a different industry classification sector. We consider the 11 global industry classification standard (GICS) sectors of S&P500 stocks. For each GICS, for the dataset of the stock returns for the period 2012-01-04/2021-12-31, the time series of the equi-correlation coefficient is computed by GJR GARCH (Glosten et al., 1993) with the correlation structure being dynamic equicorrelation (Engle & Kelly, 2012) (We abbreviate this model to ‘GJR GARCH-DECO’). The program is due to Candila (2021).

However, the computation time of the time series of the equi-correlation coefficient by GJR GARCH-DECO is large, although we can quickly compute the estimator of the equi-correlation coefficient by a power method. For each dataset, we compare the time series to of the correlation matrix .

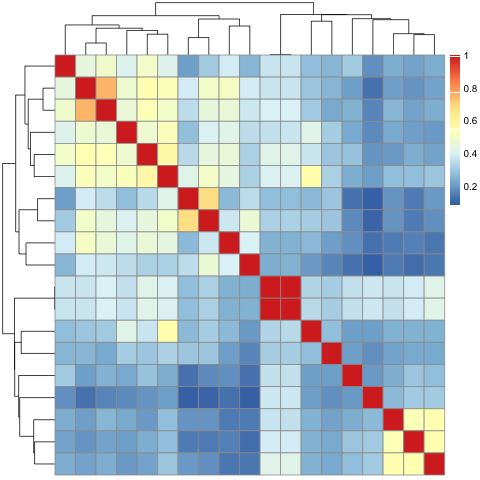

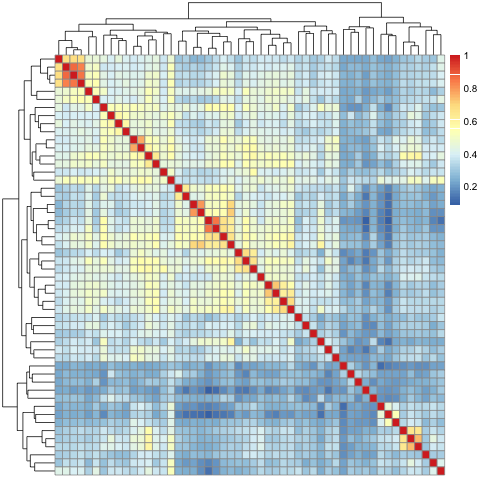

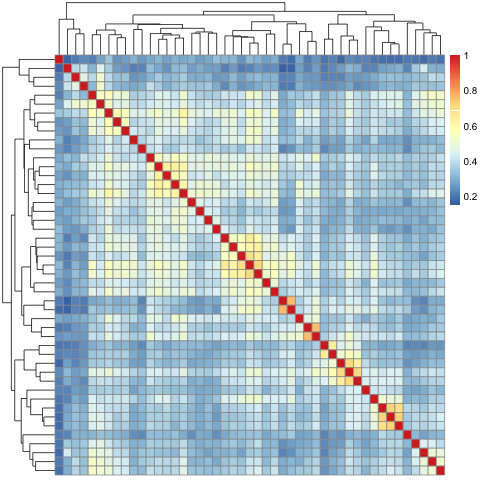

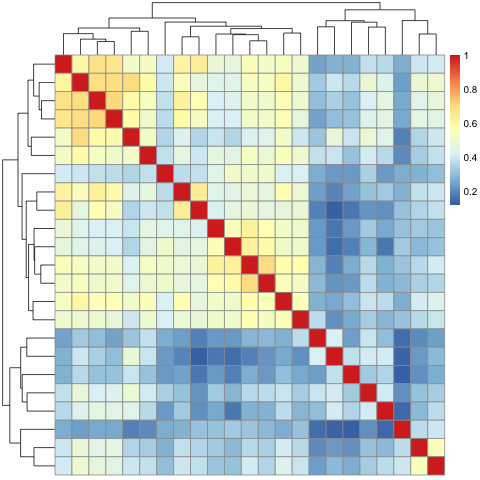

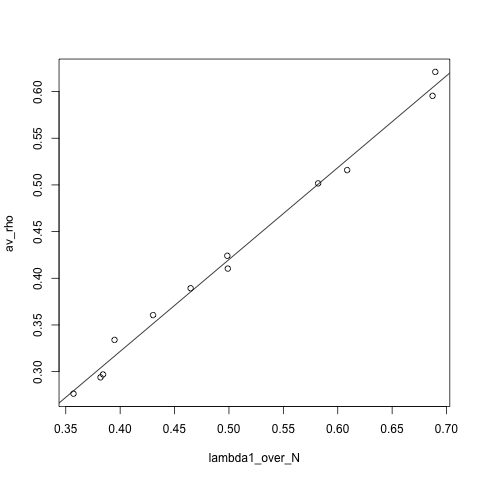

Figure 1 is the time series of equi-correlations for the 12 datasets. All the time series rise around March 2020, by the world-wide sudden crash after growing uncertainty due to the COVID-19 (Coronavirus disease 2019) pandemic. The time series of the equi-correlation coefficient of Energy sector kept high, even after the time series of the equi-correlation of the other 10 sectors of GICS as well as the total decrease. According to Figure 1, for each dataset, the time series is mostly smaller than . Let us consider the time average of equi-correlation coefficients estimated by GJR GARCH-DECO. Table 1 is the list of GICS, , , , and , for the period 2012-01-04/2021-12-31 (=trading days ). The rows of Table 1 are ordered in the increasing order of .

| No | GICS | ||||

|---|---|---|---|---|---|

| 1 | Communication Services | .0076 | .3571 | 19 | .2764 |

| 2 | Consumer Discretionary | .0207 | .3843 | 52 | .2967 |

| 3 | Health Care | .0187 | .3948 | 47 | .334 |

| 4 | Consumer Staples | .0091 | .4302 | 23 | .3606 |

| 5 | Information Technology | .0246 | .4648 | 62 | .3894 |

| 6 | Industrials | .0258 | .4985 | 65 | .4241 |

| 7 | Materials | .0095 | .499 | 24 | .4104 |

| 8 | Real estate | .0119 | .5819 | 30 | .5016 |

| 9 | Financials | .025 | .6086 | 63 | .5159 |

| 10 | Energy | .0064 | .6872 | 16 | .5954 |

| 11 | Utilities | .0111 | .6897 | 28 | .621 |

| 12 | The total | .1705 | .3819 | 429 | .2939 |

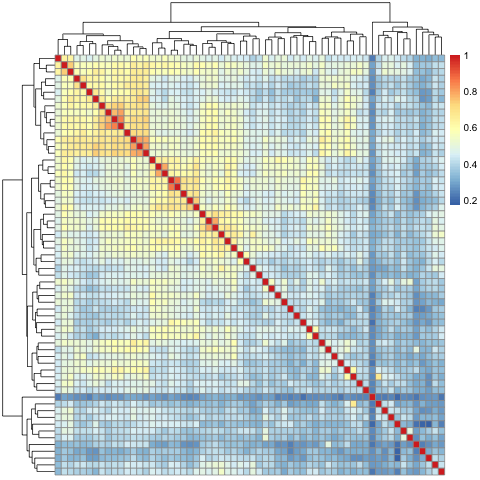

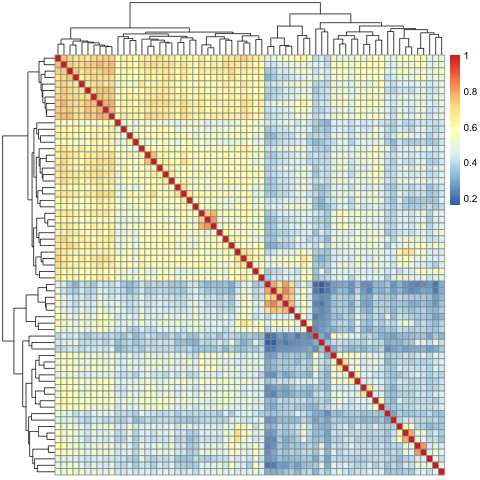

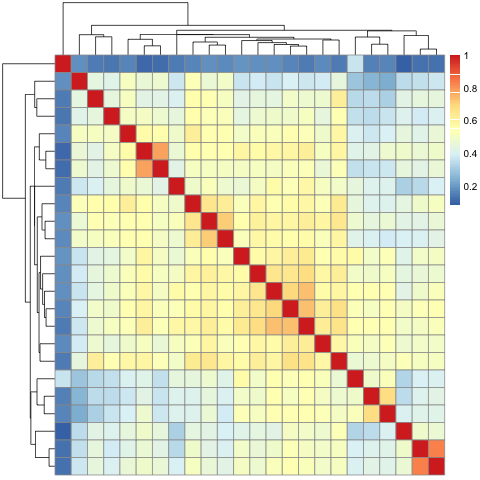

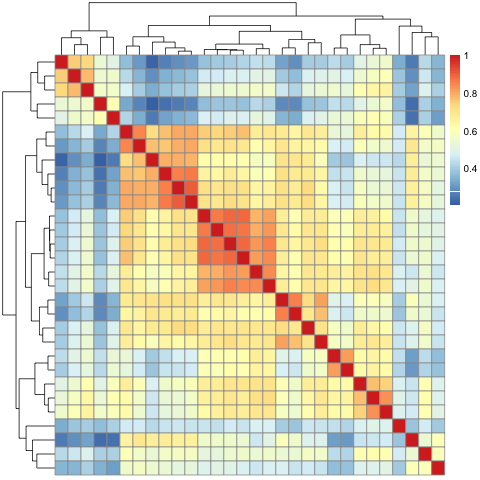

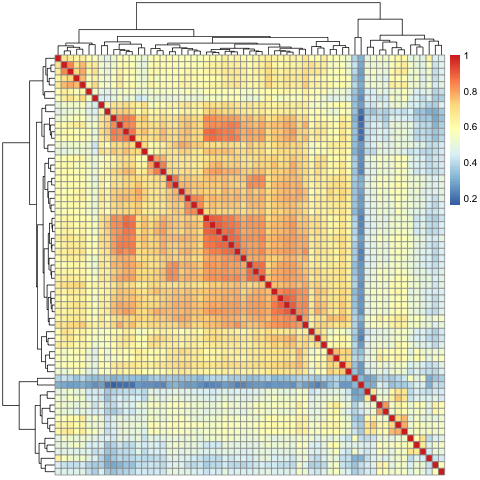

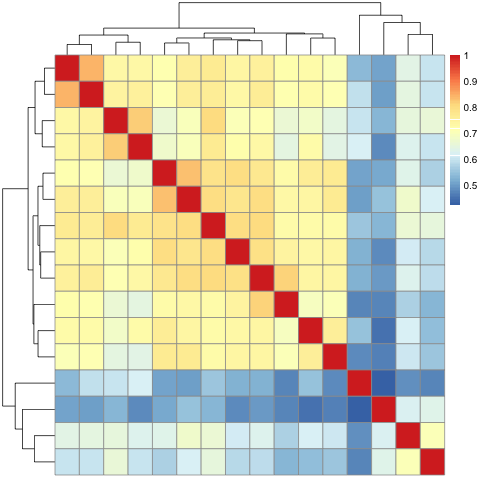

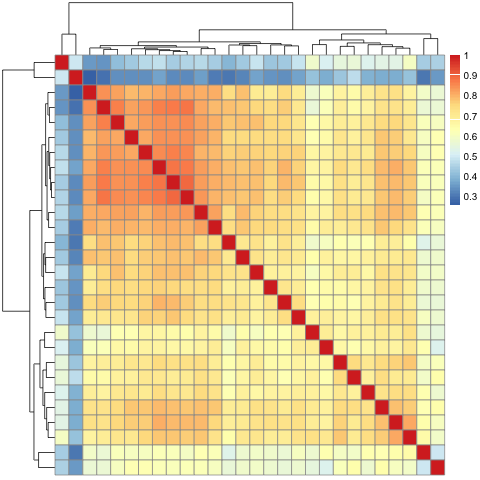

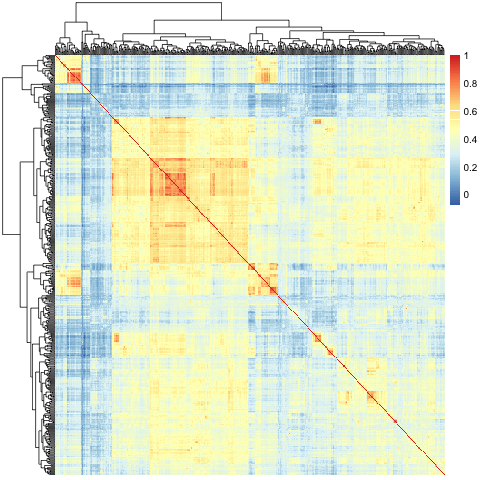

The last row of Table 1 is for the union dataset of the 11 GICS datasets. The union dataset is more ‘heterogeneous’ than the 11 GICS datasets. It has and smaller than the corresponding and for most of GICS. It means that correlations coefficients between different GICS’s are very small. Figure 2 are the heat maps with hierarchical clustering algorithms for the correlation matrices of the 12 datasets. According to the last heat map of Figure 2, the correlation matrix of the returns of S&P500 stocks has diagonal block structures as well as an almost dominant background.

Although Figure 2 shows the various structures of for the 12 datasets, predicts well the time average of the time series of equi-correlation coefficients computed by GJR GARCH-DECO with much time. A regression analysis (Figure 3) for Table 1 shows:

4 Phase transition of limiting distribution of largest eigenvalue

In our setting, all the correlation coefficients among variables being the positive constant . It is, however, somehow unnatural in the limit We assume that

and the equi-correlation coefficient converges to 0 from above as .

For this setting with , the consistency of the largest eigenvalue and the asymptotic normality of for a nonnormal population follows from Yata & Aoshima (2009). Moreover, the limiting distribution of for an equi-correlated normal population seems to have a phase transition depending on the equi-correlation coefficient , as the limiting distribution of the largest eigenvalue of formed by a spiked population model does so with respect to the largest eigenvalue of the population covariance matrix (Baik et al., 2005).

4.1 Consistency and asymptotic normality of of nonnormal population

In (Yata & Aoshima, 2009), the consistency and the asymptotic normality of are proved without assuming the normality of the population.

Proposition 4.1.

Let a data matrix be where are centered, i.i.d. and . Suppose that the population covariance matrix is for some orthogonal matrix ,

| (5) | |||

Here , and are constants.

Let . Assume that are independent, the fourth moments of the entries of are uniformly bounded, and no is . Moreover suppose

-

(i)

for such that ; and

-

(ii)

and for such that .

Then, we have

The condition (ii) is relieved for (Yata & Aoshima, 2009, Theorem 2) if an independence condition is further assumed.

Proposition 4.2 ((Yata & Aoshima, 2009, Corollary 1)).

4.2 Phase transition of limiting distribution of for normal population as to decay rate of equi-correlation coefficient

The limiting distribution of an appropriate scaling of a translation of the largest eigenvalue of a sample covariance matrix is Tracy-Widom distribution if the equi-correlation coefficient is 0, by (Johnstone, 2001; Soshnikov, 2002), and a normal distribution if is a positive constant by Theorem 5.2. In view of Theorem 4.3 (2), we turn our attention to the case .

First, we recall (Baik et al., 2005, Theorem 1.1 and Corollary 1.1).

Proposition 4.4.

Assume and the population is , and be the eigenvalues of .

-

(a)

Suppose , , and . Then,

(6) where is the distribution function of a generalization of the Tracy-Widom distribution (Baik et al., 2005, Definition 1.1).

-

(b)

Suppose , , and . Then,

(7) where is the distribution function of a generalization of the Gaussian distribution (Baik et al., 2005, Definition 1.2).

This proposition suggests the following phase transition: For a normal population, if , then the largest eigenvalue satisfies the asymptotic normality in a sense of (6), and if , then an appropriate scaling of a translation of converges to the Tracy-Widom distribution in a sense of (7). This holds for by Theorem 4.3.

The detail of this phase transition will be studied elsewhere.

5 Proof of Theorem 1.3

We also consider centered (noncentered, resp.) variant of the sample covariance matrix (the sample correlation matrix , resp.):

Definition 5.1.

Let be . Define the following three matrices:

Theorem 5.2.

Assume that , is deterministic, is deterministic, nonsingular diagonal, and is deterministic. Suppose , , , , , , , or . Then, .

Proof 5.3.

First consider the case where , , and . Suppose . Then, all the entries of are standard normal, so they are independent and . Thus,

by (Bai & Yin, 1993, Theorem 2). Hence, Theorem 5.2 (1) holds for this case when .

Then, we prove for . For this, we recall (Merlevède et al., 2019, Proposition 2.1), which is due to (Ledoit & Wolf, 2018, Proposition 7.3) and (Cai et al., 2017, Theorem 2.1) according to Merlevède et al. (2019). Following (Van der Vaart, 2000, p. 8), we say a sequence of distribution functions is tight on , if for every , there is a constant such that

Proposition 5.4 (Merlevède et al. (2019, Proposition 2.1)).

Assume

-

1.

, the entries of are independent, standard normal, and is positive definite, symmetric, and deterministic.

-

2.

A sequence of empirical spectral distributions is tight on , and .

-

3.

.

Then,

The sequence of the empirical spectral distribution function of is a tight sequence on . To see it, consider and . For every integer , , so . Hence, . Therefore, we have the tightness of the sequence.

Then, by Proposition 5.4 with , Thus, we have established for every .

Now, we consider the case where and . We will derive for every , by using the following:

Proposition 5.5 (Bai & Yin (1993, Lemma 2)).

Let be a double array of i.i.d. random variables and let , and be constants. Then,

The centered sample covariance matrix is invariant with respect to the shifting of variables. By this invariance, we can assume It suffices to assure

By the triangle inequality for the spectral norm,

| (8) |

The last term is (a.s.). To see it, note that the -entry of is . Therefore, is an eigenvector of , corresponding to an eigenvalue . Clearly, and almost surely . Thus, it is also the case for . Considering the eigenvalue of is positive almost surely, the other eigenvalues are 0 almost surely.

By dividing (8) with , it holds almost surely that

| (9) |

By and , are standard normal random variables equi-correlated with . By decomposition (4), there are independent standard normal random variables such that . By the triangle inequality,

The first term of the right side tends to 0 in almost surely, by the law of large numbers. The second term of the right side tends to 0 in almost surely, by Proposition 5.5 with and . Thus,

| (10) |

Hence, . Since we have already established for every , we then derived for every .

We consider the case and . Because the noncentered sample correlation matrix is invariant under the scaling, we can assume

From of Theorem 5.2, we will guarantee

| (11) |

For a diagonal matrix

we have .

Recall that the spectral norm of a matrix is

Note . By the triangle inequality of the spectral norm and that for every and ,

| (12) | |||

| (13) |

Since we established from and , it suffices to verify

| (14) |

By decomposition (4), there are independent standard normal random variables such that . Hence,

Then

The right side converges almost surely to 0 by Proposition 5.5, because are i.i.d. of unit mean, are centered i.i.d., and are i.i.d. of unit mean. Hence,

| (15) |

from which implies

| (16) |

Suppose for sufficiently small . Then, for all , , which implies . Hence, for all , , because . Thus, . Therefore, from (16), (14) follows.

Thus, (11) is guaranteed. Therefore, follows because the assumption implies .

At last, we will demonstrate of Theorem 5.2. Because the sample correlation matrix is invariant under the shifting and scaling, we can assume and . For , we have where

Recall . By the same arguments as in (13),

Because follows from we assumed, it suffices to show

| (17) |

By ,

The first (second, resp.) term of the right side converges almost surely to 0, by (15) ((10), resp.). In a similar way as above, (17) is shown. Therefore, for every . This completes the proof of Theorem 5.2.

6 Proof of Corollary 1.4

From Proposition 1.2, converges to almost surely for every . It suffices to prove that converges almost surely to for any . By Theorem 1.3, , so . The distribution function of a Marčenko-Pastur distribution is continuous with respect to . Thus,

| (19) |

On the other hand, is continuous with respect to for each , in view of the density function (1). Therefore,

By this, (19), and the triangle inequality,

7 Proof of Theorem 2.3

7.1 LSD of sample covariance matrix generated from factor model

In this subsection, we provide the LSD of the sample covariance matrix generated from a factor model (Definition 2.1) in with Assumption 2. Let and be distribution functions. The Lévy distance between and is denoted by . For the definition, see (Huber & Ronchetti, 2009, Definition 2.7). By (Huber & Ronchetti, 2009, Theorem 2.9),

Proposition 7.1.

For every sequence of distribution functions, and every distribution function , converges weakly to if and only if .

By Huber & Ronchetti (2009, p. 36), the Kolmogorov distance between two and is defined as , and satisfies

| (20) |

Proposition 7.2 (Bai (1999, Lemma 2.6, the rank inequality)).

Theorem 7.3 (Scaling).

Given a factor model. Suppose and Assumption 2. Then, the following two hold almost surely:

-

1.

converges weakly almost surely to , if .

-

2.

converges weakly almost surely to .

Proof 7.4.

By Definition 2.1, the data matrix is written as

| (21) |

By Assumption 2 and Proposition 1.1 (1), the ESD of converges weakly to almost surely. Then, Proposition 7.1 implies

| (22) |

where by Assumption 2. Recall . Thus, by (20), Proposition 7.2, (21), and , it holds almost surely that

By this, (22), and the triangle inequality,

| (23) |

which implies the first assertion of this theorem through Proposition 7.1. By the same proposition, the second assertion of this theorem follows by the triangle inequality from (23) and

The last is because by (20), Proposition 7.2, and , it holds almost surely that

This completes the proof of Theorem 7.3.

7.2 LSD of sample correlation matrix generated from factor model

In this subsection, we provide the LSD of generated from a factor model (Definition 2.1) in with Assumption 2. By Assumption 2,

| (24) |

For ,

| (25) |

because

Lemma 7.5.

For a factor model with , if Assumption 2, then

Proof 7.6.

By (25), is equal to

| (26) |

We will compute the almost sure limits of the three terms of (26), in .

By the continuous mapping theorem (Van der Vaart, 2000, Theorem 2.3) applied to the continuous function , the limit of the first term of (26) is

| (27) |

By Assumption 2, , so the Cesàro sum (Abbott, 2015) satisfies On other hand, by Definition 2.1, are centered i.i.d. Thus, are i.i.d., for each . Since , the strong law of large numbers implies that

| (28) |

By this, the limit of the first term of (26) is:

| (29) |

Next, we consider the second term of (26). We will verify:

| (30) |

Let be an enumeration of . Because and are independent and centered, so are and . Then, . Because the entries of are independent random variables with unit variance for each , (24) implies . Moreover, . Hence, (30) follows from:

Proposition 7.7 (Kolmogorov sufficient condition (Gut, 2013, Theorem 6.5.4)).

Let be centered, independent random variables with finite variance. Then implies (a.s.).

Now, we prove Theorem 2.3.

Proof 7.8.

The sample correlation matrix and the noncentered sample correlation matrix (Definition 5.1) are invariant under scaling of variables. To the factor model, we can assume

| (31) |

without loss of generality. Moreover, we can safely assume that to prove that converges weakly to almost surely, because is invariant under shifting. It suffices to show that (a.s.), because Theorem 7.3 (2) implies (a.s.). By , (Bai, 1999, Lemma 2.7) gives an upper bound on the fourth power of the Lévy distance

| (32) |

On the right side of (32), , and

| (33) |

Since the rightmost term of (33) converges almost surely to a finite deterministic value by Lemma 7.5, (a.s.). Therefore, for the right side of (32), we have only to assure the following:

| (34) |

On the other hand, by and (Bai, 1999, Lemma 2.7), is at most the product of and . Here, and (a.s.) by Lemma 7.5. Hence, to prove that converges weakly to almost surely, it suffices to guarantee

| (35) |

(a) The proof of (35). The left side of (35) is where

| (36) |

because by the definition of and because Since Lemma 7.5 implies

| (37) |

our goal (35) follows from (a.s.). Because of this, we will verify

| (38) |

By (25), is

| (39) |

The first term of (39) tends almost surely to in , by (28) and the continuous mapping theorem for the continuous function .

Next, we will verify that the second term of (39) converges almost surely to , similarly as (30). Because and are independent and centered, so are and . By , we then have by (24). Moreover, are centered independent. Hence, by Proposition 7.7, the second term of (39) converges almost surely to 0:

For the third term of (39), we will verify

| (40) |

Because we suppose , there exists such that for all ,

| (41) |

Since are i.i.d. and , Proposition 5.5 implies: for every constant , almost surely, there exists such that for all we have . Hence, by (41), for all , it holds

Consequently, (40) has verified.

(b) The proof of (34). First, the left side of (34) is where

| (43) |

It is proved in a similar way for (a) as follows: By the definition, . By Definition 5.1, the -th column of is , so that of is . Thus,

Secondly, we will show and . From (36) and (43), it follows immediately

| (44) |

Thus,

| (45) |

As for the first term inside the right side,

By (24),

| (46) |

by the strong law of large numbers, because for each , are centered i.i.d.

Acknowledgments

References

- Abbott (2015) S. Abbott (2015) Understanding Analysis, 2nd edition. New York, NY: Springer.

- Akama & Husnaqilati (2022) Y. Akama & A. Husnaqilati (2022) A dichotomous behavior of Guttman-Kaiser criterion from equi-correlated normal population, J. Indones. Math. Soc. 28 (3), 272–303. See also arXiv:2210.12580.

- Bai (2003) J. Bai (2003) Inferential theory for factor models of large dimensions, Econometrica 71 (1), 135–171.

- Bai (1999) Z. D. Bai (1999) Methodologies in spectral analysis of large dimensional random matrices, a review, Stat. Sin. 9 (3), 611–662.

- Bai & Silverstein (2010) Z. D. Bai & J. W. Silverstein (2010) Spectral analysis of large dimensional random matrices, 2nd edition. New York, NY: Springer.

- Bai & Yin (1993) Z. D. Bai & Y. Q. Yin (1993) Limit of the smallest eigenvalue of a large dimensional sample covariance matrix, Ann Probab 21 (3), 1275–1294.

- Baik et al. (2005) J. Baik, G. Ben Arous & S. Péché (2005) Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices, Ann Probab 33 (5), 1643–1697.

- Bun et al. (2017) J. Bun, J.-P. Bouchaud & M. Potters (2017) Cleaning large correlation matrices: Tools from random matrix theory, Phys. Rep. 666, 1–109.

- Cai et al. (2017) T. Cai, X. Han & G. Pan (2017) Limiting laws for divergent spiked eigenvalues and largest non-spiked eigenvalue of sample covariance matrices, arXiv:1711.00217.

- Candila (2021) V. Candila (2021) dccmidas: A package for estimating DCC-based models in R, R package version 0.1.0.

- Donoho et al. (2018) D. Donoho, M. Gavish & I. Johnstone (2018) Optimal shrinkage of eigenvalues in the spiked covariance model, Ann Stat 46 (4), 1742–1778.

- El Karoui (2008) N. El Karoui (2008) Operator norm consistent estimation of large-dimensional sparse covariance matrices, Ann Stat 36 (6), 2717–2756.

- Elton et al. (2014) E. J. Elton, M. J. Gruber, S. J. Brown & W. N. Goetzmann (2014) Modern portfolio theory and investment analysis, 9th edition. New York, NY: John Wiley & Sons.

- Engle & Kelly (2012) R. Engle & B. Kelly (2012) Dynamic equicorrelation, J Bus Econ Stat 30 (2), 212–228.

- Fama & French (1993) E. F. Fama & K. R. French (1993) Common risk factors in the returns on stocks and bonds, J. Financ. Econ. 33 (1), 3–56.

- Fama & French (2015) E. F. Fama & K. R. French (2015) A five-factor asset pricing model, J. Financ. Econ. 116 (1), 1–22.

- Fan & Jiang (2019) J. Fan & T. Jiang (2019) Largest entries of sample correlation matrices from equi-correlated normal populations, Ann Probab 47 (5), 3321–3374.

- Friedman & Weisberg (1981) S. Friedman & H. F. Weisberg (1981) Interpreting the first eigenvalue of a correlation matrix, Educ. Psychol. Meas. 41 (1), 11–21.

- Glosten et al. (1993) L. R. Glosten, R. Jagannathan & D. E. Runkle (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks, J Finance 48 (5), 1779–1801.

- Gut (2013) A. Gut (2013) Probability: A Graduate Course. New York, NY: Springer.

- Huber & Ronchetti (2009) P. J. Huber & E. Ronchetti (2009) Robust statistics, 2nd edition. Hoboken, NJ: John Wiley & Sons.

- Ishii et al. (2021) A. Ishii, K. Yata & M. Aoshima (2021) Hypothesis tests for high-dimensional covariance structures, Annals of the Institute of Statistical Mathematics 73 (3), 599–622.

- Jiang (2004) T. Jiang (2004) The limiting distributions of eigenvalues of sample correlation matrices, Sankhyā: The Indian Journal of Statistics (2003–2007) 66 (1), 35–48.

- Johnstone (2001) I. M. Johnstone (2001) On the distribution of the largest eigenvalue in principal components analysis, Ann Stat 29 (2), 295–327.

- Laloux et al. (2000) L. Laloux, P. Cizeau, M. Potters & J.-P. Bouchaud (2000) Random matrix theory and financial correlations, Int. J. Theor. Appl. Finance 3 (3), 391–397.

- Ledoit & Péché (2011) O. Ledoit & S. Péché (2011) Eigenvectors of some large sample covariance matrix ensembles, Probab. Theory Relat. Fields 151 (1), 233–264.

- Ledoit & Wolf (2004) O. Ledoit & M. Wolf (2004) Honey, I shrunk the sample covariance matrix, J. Portf. Manag. 30 (4), 110–119.

- Ledoit & Wolf (2012) O. Ledoit & M. Wolf (2012) Nonlinear shrinkage estimation of large-dimensional covariance matrices, Ann Stat 40 (2), 1024–1060.

- Ledoit & Wolf (2018) O. Ledoit & M. Wolf (2018) Optimal estimation of a large-dimensional covariance matrix under Stein’s loss, Bernoulli 24 (4B), 3791–3832.

- Markowitz (1959) H. M. Markowitz (1959) Portfolio selection: efficient diversification of investments. New York, NY: John Wiley & Sons.

- Marčenko & Pastur (1967) V. A. Marčenko & L. A. Pastur (1967) Distribution of eigenvalues in certain sets of random matrices, Mat. Sb. 72, 507–536.

- Merlevède et al. (2019) F. Merlevède, J. Najim & P. Tian (2019) Unbounded largest eigenvalue of large sample covariance matrices: Asymptotics, fluctuations and applications, Linear Algebra Appl 577, 317–359.

- Mulaik (2009) S. A. Mulaik (2009) Foundations of factor analysis, 2nd edition. Boca Raton, FL: CRC press.

- Quadeer et al. (2018) A. A. Quadeer, D. Morales-Jimenez & M. R. McKay (2018) Co-evolution networks of HIV/HCV are modular with direct association to structure and function, PLoS Comput. Biol. 14 (9), 1–29.

- SenGupta (1988) A. SenGupta (1988) On loss of power under additional information: An example, Scand. J. Stat. 15 (1), 25–31.

- Soshnikov (2002) A. Soshnikov (2002) A note on universality of the distribution of the largest eigenvalues in certain sample covariance matrices, J. Stat. Phys. 108 (5), 1033–1056.

- Van der Vaart (2000) A. W. Van der Vaart (2000) Asymptotic statistics. Cambridge: Cambridge University Press.

- Yao et al. (2015) J. Yao, S. Zheng & Z. Bai (2015) Large sample covariance matrices and high-dimensional data analysis. New York, NY: Cambridge University Press.

- Yata & Aoshima (2009) K. Yata & M. Aoshima (2009) PCA consistency for non-gaussian data in high dimension, low sample size context, Commun. Stat. Theory Methods 38 (16).

- Yata & Aoshima (2010) K. Yata & M. Aoshima (2010) Effective PCA for high-dimension, low-sample-size data with singular value decomposition of cross data matrix, J. Multivar. Anal. 101 (9), 2060–2077.

- Yata & Aoshima (2012) K. Yata & M. Aoshima (2012) Effective PCA for high-dimension, low-sample-size data with noise reduction via geometric representations, J. Multivar. Anal. 105 (1), 193–215.