Robust asymptotic insurance-finance arbitrage

Abstract.

In most cases, insurance contracts are linked to the financial markets, such as through interest rates or equity-linked insurance products. To motivate an evaluation rule in these hybrid markets, Artzner et al. (2022) introduced the notion of insurance-finance arbitrage. In this paper we extend their setting by incorporating model uncertainty. To this end, we allow statistical uncertainty in the underlying dynamics to be represented by a set of priors . Within this framework we introduce the notion of robust asymptotic insurance-finance arbitrage and characterize the absence of such strategies in terms of the concept of -evaluations. This is a nonlinear two-step evaluation which guarantees no robust asymptotic insurance-finance arbitrage. Moreover, the -evaluation dominates all two-step evaluations as long as we agree on the set of priors which shows that those two-step evaluations do not allow for robust asymptotic insurance-finance arbitrages.

Furthermore, we introduce a doubly stochastic model under uncertainty for surrender and survival. In this setting, we describe conditional dependence by means of copulas and illustrate how the -evaluation can be used for the pricing of hybrid insurance products.

Keywords: insurance-finance arbitrage under uncertainty, robust -rule, enlargement of filtration, absence of robust insurance-finance arbitrage.

1. Introduction

This paper develops and characterizes the absence of insurance-finance arbitrage under model uncertainty. Our starting point is the observation that most insurance contracts are strongly linked to financial markets, such as through interest rates or via direct links of the contractual benefits to stocks or indices.

However, due to the varied characteristics of insurance contracts – which are static, personalized products – and financial markets – where products are standardized and traded frequently – the approaches to model these markets and the corresponding valuation techniques are fundamentally distinct. In the literature, several different approaches have been proposed how to deal with both insurance and financial markets in a consistent manner (see e.g., Dhaene et al. (2017), Dhaene et al. (2013), Pelsser and Stadje (2014) and Semyon et al. (2008) and references therein).

The notion of insurance-finance arbitrage (IFA) was introduced by Artzner et al. (2022) with the aim of identifying a suitable notion of arbitrage in these markets. Characteristic of such markets is that, on the one hand, the insurance company may issue contracts to a large number of clients, yet, on the other hand, it is able to simultaneously hedge its positions by trading on the financial market. In order to model the two information flows that the insurance company has access to, we work with two filtrations. The smaller filtration represents the publicly available information on the financial market, denoted by , while the larger filtration additionally contains the insurer’s information. Given a pricing measure on the financial market and a statistical measure on a characterization of the absence of IFA in terms of the -rule is derived in Artzner et al. (2022).

Even if a large set of homogeneous data is available, statistical uncertainties in predicting the future evolution of insurance losses in the considered portfolio remain a problem that needs to be addressed. Hence, in this work we aim to take this uncertainty into account.

To do so, we fix the nullsets on the financial market which determines the set of equivalent martingale measures . Second, we consider a class of probabilistic models on with the -nullsets and study the associated -rule. Most notably, this framework allows us to model uncertainty on the insurance market under the assumption that we do not face any model risk on the financial market. Working with a class of potential models is in line with the growing literature on model risk and uncertainty (see e.g., Denis and Martini (2006), Peng (2019), Denis et al. (2010), Biagini et al. (2017), Soner et al. (2011) and Bouchard and Nutz (2005)).

To the best of our knowledge, this is the first study of insurance-finance arbitrage under model uncertainty. More specifically, we prove a characterization of robust insurance-finance arbitrage (RIFA) by using the -evaluation in Theorem 2.11.

Furthermore, we show that this result provides a theoretical foundation for a class of two-step evaluations introduced in Pelsser and Stadje (2014), which is applied for the pricing of hybrid products depending on the financial market, as well as on other random sources, e.g., insurance products. In particular, we prove that every two-step evaluation, which is the combination of a risk-free measure and a coherent -conditional risk measure, which is continuous from below, equals a -evaluation for a suitable subset on Thus, every two-step evaluation of this kind leads to a robust arbitrage-free price in the asymptotic insurance-finance setting.

We conclude the paper by suggesting possible applications in Section 4. First, we consider the case of two conditional independent random times such that the conditional distribution functions face a certain degree of uncertainty. Here, the random times represent the surrender time and the time of death of an insurance seeker. In this setting, we introduce a financial market via a Cox-Ross-Rubinstein model and consider finance-linked insurance benefits with surrender options. We also numerically provide the robust arbitrage-free price of these products. Most notably, we find that the uncertainty justifies the robust arbitrage-free price being higher than the supremum of all arbitrage-free prices under each possible model. We then generalize the framework by allowing some dependence structure between the random times described by a copula. By doing this, we show that the well-known Cox model under uncertainty is contained in the outlined setting.

The paper is structured as follows. In Section 2 we introduce the definition of a robust insurance-finance arbitrage and provide a characterization in our main result. After that, Section 3 studies the relation of the -rule to two-step evaluations. Then, in Section 4 we study an insurance-finance market with two conditionally independent random times and numerically provide the robust arbitrage-free prices for certain hybrid products. In addition, we consider a copula framework for the two random times under uncertainty.

2. Robust asymptotic insurance-finance arbitrage

Let be a measurable space and denote by the set of all probability measures on this space. We consider a discrete time model with times and introduce two different kinds of information flows described by the filtrations and on . The filtration represents publicly available information and contains all information available on the financial market. The filtration contains additional private information of the considered insurance company, which includes, for example, several datasets on its clients. In particular, we assume . Moreover, let and be a -field such that .

Given , a set is called -polar if for some satisfies for all . Moreover, a property holds -quasi surely (-q.s.) if it holds outside a -polar set.

For a fixed -ideal of -nullsets , i.e., there exists a measure on such that are the nullsets of , we define the following sets of priors

| (2.1) |

and

| (2.2) |

Hereafter, we fix a probability measure , which determines the nullset on , and a subset of priors , which specifies the uncertainty about the model.

In the following, we introduce the concept of insurance-finance arbitrage. For simplicity, we consider only a single insurer. We also assume that the insurer is able to contract with an arbitrarily high number of clients so as to reduce its risks. To establish this, we consider a finite number of insurance seekers and treat the limits of portfolio allocations - a technique inspired by large financial markets (e.g., Klein (2000), Kabanov and Kramkov (1995), Klein et al. (2016)). Such strategies may lead to insurance arbitrages and it is partly our aim to characterize when and how such arbitrages can be achieved and under which conditions they can be avoided.

At the same time, the insurance company also trades on the financial market, potentially leading to a financial arbitrage. Thus, the combination of these concepts results in an insurance-finance arbitrage.

2.1. The insurance contracts

Insurance contracts offer a variety of benefits at future times in exchange for a single premium or a premium stream. We work with discounted quantities and, without loss of generality, we consider a single premium paid at time 0 and an aggregated benefit received at future time . More precisely, we denote by the premium to be paid at time and a -measurable benefit to be received by the th client at time . This allows to cover a wide range of contracts, particularly contracts depending on financial markets, such as variable annuities.

We assume that all insurance seekers under consideration can be treated as homogeneous (under each model ) and each insurance seeker pays the same premium in order to receive his or her personal benefit . This idea is formalized in the following assumption, which is a generalization of the framework of actuarial mathematics to stochastic assets, as discussed in Artzner et al. (2022).

Assumption 2.1.

For all , the following holds:

-

(i)

are -conditionally independent.

-

(ii)

for all .

-

(iii)

for all .

The insurance portfolio is obtained as a limit of allocations of contracts with a finite number of clients. An allocation at time , is -valued, deterministic and non-negative, where denotes the space of sequences with a finite number of non-zero elements. For , denotes the size of the contract with the th insurance client. The accumulated benefits and premiums associated with the allocation are given by and , while the associated profits and losses are denoted by

An insurance portfolio strategy is modeled as a sequence of allocations . Moreover, the profit and loss of an insurance portfolio strategy is given (if it exists) by

We introduce the following admissibility conditions for an insurance portfolio strategy .

Assumption 2.2.

-

(i)

Uniform boundedness: There exists such that

-

(ii)

Convergence of the total mass: There exists such that

-

(iii)

Convergence of the total wealth: There exists a -valued random variable such that

An insurance portfolio strategy which satisfies Assumption 2.2 is called -admissible.

2.2. The financial market

We introduce a financial market model in discrete time consisting of assets on For the discounted price of the th asset at time is given by the -measurable random variable and the bank account is given by We assume that the insurance company trades with -trading strategies on the financial market, where a -trading strategy is a -dimensional -predictable process with Note that each strategy can be extended by to a self-financing trading strategy , cf. (Föllmer and Schied, 2016, Remark 5.8). The associated gain process at time is then given by the discrete stochastic integral

As is typical, the absence of arbitrage in this market with respect to any restricted measure for can be characterized by the existence of an equivalent martingale measure, cf. (Föllmer and Schied, 2016, Theorem 5.16). The set of all equivalent martingale measures is denoted by and defined by

| (2.3) |

Remark 2.3.

Note that we consider uncertainty in a narrow sense on the financial market by taking into account a set of priors . More specifically, according to the definition of in (2.2), all nullsets on are already determined by The uncertainty of our model refers only to the additional insurance part defined on .

2.3. Robust insurance-finance arbitrage

Finally, we introduce the insurance-finance market on consisting of the benefits , the premium , and the discounted prices of the assets

In order to define a robust arbitrage in our setting, we use the concept of a robust arbitrage strategy introduced in Bouchard and Nutz (2005). Note, however, that we do not need to require convexity of .

Definition 2.4.

A -robust asymptotic insurance-finance arbitrage on the insurance-finance market is a pair consisting of an -predictable trading strategy and a -admissible insurance portfolio strategy such that

| (2.4) |

If there exists no such pair satisfying (2.4), then there is no -robust asymptotic insurance-finance arbitrage, which we denote by

Remark 2.5.

If for all it holds then is also satisfied. However, the converse statement is incorrect.

In the case of no model uncertainty, i.e., for a measure , it is shown in Corollary 5.2 in Artzner et al. (2022) that the following relation to the -rule holds. If there exists such that

| (2.5) |

then there exists no asymptotic insurance-finance arbitrage. Thus, according to Remark 2.5, an insurance-finance market fulfills if (2.5) holds for each . However, it should be noted that these conditions are not strictly necessary as we will demonstrate in the following.

2.4. Uniform essential supremum

In order to characterize the absence of a -robust asymptotic insurance-finance arbitrage, we aim to identify assumptions that allow us to take into account a robust version of the conditional expectations for in (2.5). Given a set of priors , it is in general not possible to consider “”, as the conditional expectation is only defined -a.s. and the priors in may have different nullsets. Furthermore, the supremum no longer needs to be measurable.

The natural approach to solving this measurability issue is to work with the essential supremum instead of the supremum. However, for a general set of priors and a set of random variables on there may be no uniform essential supremum, i.e., a random variable such that

| (2.6) |

We refer to Föllmer and Schied (2016) for a precise definition of the essential supremum and to Bartl (2020), in whose work a general construction of such a nonlinear conditional expectation is studied.

The definition of the set in (2.2) allows us to consider for the set of random variables such that

| (2.7) |

Indeed, we observe that by -measurability together with the fact that for all the conditional expectation is not only -a.s. uniquely determined but also -a.s. for all . Then, there exists a uniform essential supremum which fulfills (2.6), as the following result demonstrates.

Lemma 2.6.

Let be the nullsets generated by the probability measure , and a set of -measurable random variables. Then

| (2.8) |

Proof.

We show that fulfills condition and in (Föllmer and Schied, 2016, Theorem A.37) on for all . Using the definition of , we geht the following:

| (2.9) |

Since is -measurable and for all , (2.9) also holds -a.s. for any . Relying on the construction of the essential supremum, see, for example (Föllmer and Schied, 2016, Theorem A.37), there exists a countable subset such that

Fix any , then for each random variable on such that

we get -a.s. ∎

In the following, for the fixed measure , which generates the -nullsets , we use the notation

2.5. Characterization of robust insurance-finance arbitrage

In the next result we use the essential supremum defined in Section 2.4 to characterize Furthermore, to prove this theorem, we use a measure extension which was studied for the first time in Plachky and Rüschendorf (1984) (see also Proposition 4.1 in Artzner et al. (2022)). For the reader’s convenience we state the existence result for such a measure.

Proposition 2.7.

Let be a probability space, a sub--algebra, and a probability measure on . Then, there exists a unique probability measure, denoted by on such that on and conditioned on .

Remark 2.8.

The measure on from Proposition 2.7 can also be characterized by each of the following more explicit expressions:

-

(i)

For all we have .

-

(ii)

The density of with respect to is given by .

This also shows that the measures and are equivalent.

As is well-known, the arbitrage-free prices of a -measurable claim in the financial market can be described by the set of expectations under all such that , cf. (Föllmer and Schied, 2016, Theorem 5.29). The following Lemma shows that if we fix we could even only use the measures such that and such that has bounded density with respect to to determine the set of arbitrage-free prices for .

Lemma 2.9.

Let be a discounted -measurable claim such that for some and let . Then, there exists such that and

Proof.

We define the process by . Then is a martingale measure for the extended market . According to (Föllmer and Schied, 2016, Theorem 5.16), it follows that this extended market is free of arbitrage and that there is an equivalent measure such that is a -martingale and The martingale property for implies and for it implies and . ∎

Lemma 2.10.

Let be a partition of and . Then the measure on defined by

| (2.10) |

for is well-defined, a probability measure and .

Proof.

We must show that . For the sake of contradiction we assume that for all . By the equivalence and , it follows that for all and thus . This is a contradiction and we obtain . Thus, is well-defined and a probability measure on . In order to prove we show that for all it holds that if and only if . First, we assume that . Then, once more using the equivalence we obtain for all and it follows that . On the other hand, if , then it follows that and thus . ∎

Next, we state the main result of this paper.

Theorem 2.11.

There is no -robust asymptotic insurance-finance arbitrage on if and only if one of the following statements is fulfilled.

-

(i)

For all there is a measure such that

-

(ii)

There is a measure such that

Proof.

We start with the only if direction and prove this using contraposition. Assume that neither nor are fulfilled, i.e.,

-

There is such that for all it holds that

and

-

For all we have

We have to show that there is a -robust asymptotic insurance-finance arbitrage on . Fix some which satisfies and define the set by

First, we consider the case . Note that can be interpreted as a contingent claim on . By we know that This means is greater or equal than every arbitrage-free price for . Thus, as shown by (Föllmer and Schied, 2016, Theorem 5.29, Corollary 7.9), there exists a -predictable (super-hedging) strategy such that

| (2.11) |

As both sides in (2.11) are -measurable and by the definition of Equation (2.11) holds -a.s. for all . We define the admissible strategy by

| (2.12) |

According to Assumption 2.1 and (Majerek et al., 2005, Theorem 3.5), we have

The strategy is a robust asymptotic insurance-finance arbitrage since by (2.11) and the argumentation below it holds for all that

Moreover, since , we have

| (2.13) |

Second, we consider . As for all and , it also holds and consequently . Then yields that for all

| (2.14) |

In this case is strictly greater than any arbitrage-free price for and thus also by (Föllmer and Schied, 2016, Theorem 5.29, Corollary 7.9) we can find a -predictable strategy such that

| (2.15) |

By once again choosing the insurance strategy given in (2.12), the pair is a -robust asymptotic insurance-finance arbitrage as it holds for all that

This concludes the proof of the only if direction and we proceed with the if direction. If holds, then for any we could assume that the martingale measure has bounded density with respect to , cf. Lemma 2.9. According to Corollary 5.2 in Artzner et al. (2022), there exists no -robust asymptotic insurance-finance arbitrage for each fixed measure and thus holds. For the reader’s convenience we provide a detailed proof of this statement. Fix . For the sake of contradiction assume that there is an admissible strategy such that

We define the process by

| (2.16) |

Using (Artzner et al., 2022, Proposition B.1) and assumption we obtain the following:

This shows that is a local -supermartingale. By (Föllmer and Schied, 2016, Remark 9.5) the value process is a local -martingale and thus is a local -supermartingale and fulfills

By (Föllmer and Schied, 2016, Proposition 9.6) the process is a -supermartingale and thus

According to Remark 2.8 it holds and we find a contradiction. This shows that implies .

Let us now assume that holds. In a first step, we show that there exists a finite partition of given by and measures with such that

Based on the definition of the essential supremum, cf. (Föllmer and Schied, 2016, Theorem A.37), there exists a countable subset such that

| (2.17) |

Moreover, as the essential supremum is -measurable, (2.17) also holds -q.s. and -a.s. for all Thus, using and monotone convergence, we get the following:

Thus, there exists such that

For every we define the set as

and and for . Then are disjoint and build a partition of because for each there is such that

and thus we obtain

Moreover, we have

| (2.18) |

We define the measure using Equation (2.10). Moreover, let be an equivalent martingale measure such that

| (2.19) |

and such that the density of with respect to is bounded, cf. Lemma 2.9. Finally, we define the measure on as

Given that , cf. Remark 2.8, the measure is a probability measure on and satisfies . We find that is also a -martingale. Moreover, we obtain for all admissible insurance strategies with positive total mass that

| (2.20) |

where we use (2.18) and (Artzner et al., 2022, Proposition B.1). We now define the process as in (2.16). Using (2.20) it follows that is a -martingale with . Let be some -predictable strategy. Then, as in (Föllmer and Schied, 2016, Remark 9.5) the value process is a local -martingale and thus is a local -supermartingale. For the sake of contradiction we assume that is a -robust asymptotic insurance-finance arbitrage such that has positive total mass. Thus, it holds that

| (2.21) |

Given that , equation (2.21) is also true -a.s. Thus, according to (Föllmer and Schied, 2016, Proposition 9.6) the process is a -supermartingale and we obtain

This contradicts (2.21) because there cannot exist an admissible insurance strategy with positive total mass which fulfills (2.21). However, given that the pure financial market is arbitrage-free with respect to -predictable trading strategies , there could also not be an arbitrage such that has total mass . Overall, this leads to a contradiction and thus the result is proven. ∎

Remark 2.12.

Let us compare Theorem 2.11 in the case of with Theorem 1 in Rásonyi (2003). According to Assumptions 2.1 and 2.2, each condition and in Theorem 2.11 implies the absence of arbitrage in the sense of Definition 2.4 and there is no need for an additional boundedness assumption on the density of the corresponding martingale measures. By contrast, in Rásonyi (2003) the boundedness assumption on the density of the equivalent martingale measure is essential and cannot be substituted by means of Lemma 2.9, cf. Example 2 in Rásonyi (2003).

Motivated by Theorem 2.11 and the previous discussion (see e.g., Equation (2.5)), we define the following robust version of the -rule.

Definition 2.13.

Let and . Then, for -q.s., we define the -evaluation of by

| (2.22) |

Note that does not define a probability measure as it is the case for .

Remark 2.14.

If the set is directed upward, i.e., for all there exists such that

| (2.23) |

then, as demonstrated by (Föllmer and Schied, 2016, Theorem A.37), there exists a sequence such that

Using monotone convergence we find that

and that

Consequently, for a set of priors that is directed upwards in the sense of Equation (2.23), there is no -robust asymptotic insurance-finance arbitrage if and only if there is no asymptotic insurance-finance arbitrage with respect to for all .

Remark 2.15.

We now briefly consider the case of -trading strategies on the financial market introduced in Section 2.2, i.e., is a -dimensional -predictable process. This reflects the fact that the insurer has access to information on the financial market as well as on the insurance market. In order to define a no-arbitrage condition for the financial market, we introduce some more notation. Let We say that a measure is dominated by if there exists such that , and in this case we write . Next, we define the set

| (2.24) |

In this case we assume that for all there exists such that . Then, according to (Bouchard and Nutz, 2005, Theorem 4.5), there is no -robust arbitrage, denoted by , on the financial market, which means that for all -trading strategies

| (2.25) |

Given that every -trading strategy is also a -trading strategy, it is clear that implies , where and refers here to the -trading strategies and -trading strategies, respectively. It thus follows that implies and thus (i) or (ii) in Theorem 2.11 is satisfied. Here, is defined as in Definition 2.4, but with a -trading strategy . However, the corresponding if direction of Theorem 2.11 is more delicate and could therefore serve as a topic for future research.

3. Robust two-step evaluation

In this section we show that Theorem 2.11 provides a theoretical foundation for the so-called two-step evaluation, cf. Pelsser and Stadje (2014), Dhaene et al. (2017). This kind of evaluationis used for the pricing of hybrid products depending on the financial market, as well as on other random sources, e.g., individual risks depending on the policy holder of an insurance contract. The idea of a two-step evaluation is to combine actuarial techniques with concepts from financial mathematics. In the following, we recap the idea and the concept. However, note that in contrast to the existing literature we do not fix any probability measure on but only a prior on the measurable space .

Let be a -measurable random variable, representing the discounted payoff of an insurance product. In a first step we consider the -conditional risk of , i.e. , where is a suitable -conditional risk measure defined on the space of bounded random variables on , which is denoted by . This corresponds to an actuarial evaluation resulting in a -measurable random variable defined on the financial market In the second step we price on the financial market under an equivalent risk-neutral measure . Combining these, we arrive at the following two-step evaluation:

| (3.1) |

As already mentioned in Artzner et al. (2022), the -evaluation in (2.5) is a two-step evaluation with the -conditional risk measure as well as the new concept of the robust -evaluation from Definition 2.13. In the following we recap some well-known facts for conditional risk measures in order to highlight that for specific coherent -conditional risk measures the two-step evaluation in (3.1) can be rewritten by a -evaluation for a suitable choice of .

3.1. Robust representation of conditional risk measures

For the reader’s convenience we recall the definition of conditional risk measures (see e.g., Föllmer and Schied (2016)).

Definition 3.1.

A map is called a convex -conditional risk measure, if for all the following holds -a.s.:

-

(i)

Conditional cash invariance: for any .

-

(ii)

Monotonicity: implies .

-

(iii)

Normalization: .

-

(iv)

Conditional convexity: for with .

A convex -conditional risk measure is called coherent if it also satisfies the following condition:

-

(v)

Conditional positive homogeneity: for with

We say that is continuous from below if

-

(vi)

Continuity from below: pointwise on implies .

Moreover, we say that is a (coherent) convex risk measure if .

Definition 3.2.

Let be a financial market on and denote by the set of all martingale measures which are equivalent to . A map is called two-step evaluation if there is a -conditional risk measure and an equivalent martingale measure such that for all

We now show that Theorem 2.11 provides an economic foundation for the pricing of finance-linked insurance products via two-step evaluations. Indeed, by using results from Föllmer and Schied (2016), we formulate sufficient condition for a conditional risk measure in a two-step evaluation such that is -evaluation. In this way, the two-step evaluation characterizes the -robust asymptotic insurance-finance arbitrage-free price as characterized in Theorem 2.11.

Lemma 3.3.

Let be a convex -conditional risk measure which is continuous from below. Then is represented by

| (3.2) |

where the acceptance set , the penalty function and the set of priors are defined by

and

| (3.3) |

If, in addition, is a coherent -conditional risk measure, then there is a subset such that

| (3.4) |

Proof.

In the unconditional case the first statement follows from Theorem 4.16 and Theorem 4.22 as laid out by Föllmer and Schied (2016). Using the same idea as in the proof of Theorem 11.2 in Föllmer and Schied (2016) yields the conditional statement. For the second statement we refer to Corollary 4.19 for the unconditional case. Using similar arguments to those put forth in Corollary 11.6 in Föllmer and Schied (2016), the conditional statement follows. ∎

Thus, Lemma 3.3 shows that every two-step evaluation given by an equivalent martingale measure and a coherent -conditional risk measure which is continuous from below can be written as -evaluation for a suitable subset .

Remark 3.4.

If we a priori fix the nullsets on by a probability measure on such that , then we can define the conditional risk measure on , instead of working with In this case only needs to be continuous from above, as opposed to satisfying the stronger assumption of continuity from below, in order to have a representation as in Lemma 3.3, cf. Theorem 4.33 and Theorem 11.2 in Föllmer and Schied (2016). The drawback of this approach is that we consider uncertainty in a narrow sense because we fix all relevant nullsets on using a single probability measure . Nevertheless, this also leads to a robust pricing problem in the spirit of Section 2, which will be discussed in more detail in Remark 3.8.

Next, we provide some examples for the set in Lemma 3.3 and the associated -conditional risk measure in Equation (3.4).

Example 3.5.

Let be a probability measure on such that . We consider the set of priors given by

| (3.5) |

In this case, the associated risk measure is the conditional Average value at risk, denoted by , see also Definition 11.8 in Föllmer and Schied (2016). Note that in this case the set is dominated by the probability measure .

Example 3.6.

Let be a probability measure on such that . We consider the set of priors for given by

| (3.6) |

where denotes the relative entropy of with respect to and is defined by

Here, the associated risk measure is the coherent entropic risk measure, introduced in Föllmer and Knispel (2011). As in Example 3.5, the set is dominated by the probability measure .

In the following Proposition we show that pricing with two-step evaluations leads to arbitrage-free premiums in the sense of Section 2. This remarkable result is a consequence of Lemma 3.3 and Theorem 2.11.

Proposition 3.7.

Proof.

The result is a direct consequence of Theorem 2.11, since the -evaluation is an upper bound for the two-step evaluation and the chosen premium is even smaller by assumption. ∎

3.2. Construction of conditional iid copies

Our next goal is to apply Theorem 2.11 in the context of a robust two-step evaluation. More specifically, given a random variable describing an insurance benefit, we determine a robust arbitrage-free premium for by using Theorem 2.11 and by taking into account some actuarial constraints, which are reflected by the set of priors (see e.g., the sets and in Example 3.5 and 3.6, respectively).

To do so, two factors must to be considered. First, the assumptions of Theorem 2.11 must be satisfied. To this end, we construct a sequence of benefits which are copies of and which satisfy Assumption 2.1. Second, the set of priors must be shifted to the product space where we model the benefits . We observe that these steps contain some subtleties which we discuss in more detail in Remark 3.8 after formally introducing the setting.

Let and be two measurable spaces on which we model purely financial and purely insurance events, respectively. On the product space we introduce the stochastic process and the random variable describing the financial market and a single insurance benefit, respectively. Moreover, let be a measure on which determines the nullsets in and be a set of probability measures on such that

We now shift to a set of priors on . Furthermore, on this space we copy the financial market to and construct insurance benefits which are iid conditionally on such that the law of for under every coincides with the law of under .

Remark 3.8.

We also emphasize that if the set is dominated by a measure , as is the case in Example 3.5 and 3.6, this will no longer hold for the shifted set . The reason for this is that absolute continuity of measures is not stable under countable products. Therefore, the seemingly not robust problem in the dominated case on is indeed a robust pricing problem on .

To be precise, we define

We denote by an element in and by an element in . Furthermore, we introduce the following projections on :

as well as the following the projections on :

Given a measure on , the aim is to define a probability measure on which fulfills the following properties:

| (3.7) |

and

| (3.8) |

If is a product measure given by for measures on and on , then the measure can be defined by . Otherwise, we construct via disintegration as follows. For some measure on the measure is defined as

| (3.9) |

where denotes the regular version of the conditional probability of given (see e.g., (Kallenberg and Kallenberg, 1997, Chapter 8)). Note that we implicitly assume its existence. This is no restriction, however, because , representing a financial market with assets and time steps, can always be assumed to have the form and, thus, is a Borel space. Moreover, using a monotone class argument, it follows that

is a probability kernel from to and, thus, the measure is well defined. If is a measure on , then (3.9) defines a measure on . In this case we have . Note that by using (3.9) we get the following:

and thus implies for all .

Let with , be a filtration on . Hereafter, we assume that is a -adapted stochastic process on describing the prices in a financial market. Moreover, let be the set of all martingale measures on which are equivalent some fixed measure on . The insurance and financial filtration on is denoted by and the insurance benefit, a random variable on , is denoted by . In order to shift all quantities to we define

and

Note that is assumed to be measurable with respect to and, thus, it does not depend on the second coordinate

We show that the measure defined in (3.9) satisfies the desired properties in (3.7) and (3.8) and is the unique measure with this property. For the reader’s convenience we provide the proofs of these results in detail in the Appendix.

Proposition 3.9.

Next, we characterize the set of all equivalent martingales measures on

Proposition 3.10.

The set of all measures on such that is a -martingale and which are equivalent to is given by

Proposition 3.11.

For any and we have the following:

We emphasize that Theorem 2.11 and Proposition 3.11 build a foundation of two-step evaluations from a new perspective. We shift the insurance benefit to an insurance-finance market such that the assumptions for Theorem 2.11 are fulfilled and characterize the robust insurance-finance arbitrage-free prices therein. Then, Proposition 3.11 shows that the prices in the shifted insurance-finance market coincide with the two-step evaluation of the initial benefit.

4. Modeling of insurance-finance markets

In this section we provide a model for an insurance-finance market and calculate the robust insurance-finance arbitrage-free premium by means of the -evaluation, cf. Theorem 2.11 and Definition 2.13.

As in Section 2.2, let be the bank account and denote by the discounted price process of a risky asset on We fix the -nullsets generated by a probability measure . We assume that the filtration is generated by . Next, we introduce the -valued random variables and representing the time of death and the time of surrender of a policy holder, respectively. Let the -algebra be given by and the filtration given by , where is the filtration generated by the processes and . Note that and are -stopping times but, in general, they are not -stopping times.

Given a parameter set , we introduce the law of the stopping times under the set of priors . In particular, we assume that for each the conditional laws of and are given by

| (4.1) |

where we assume that for fixed the mappings and are -conditional distribution functions.

4.1. Modeling under conditional independence

We assume that under every the random variables and are -conditionally independent, i.e.,

| (4.2) |

In order to determine the law of under it is now sufficient to fix a model for the restricted measures and use disintegration. Here, we could assume that for all because the -evaluation is invariant under the specific choice of the measures as the set of equivalent martingale measures only depends on the nullsets generated by .

We introduce the discounted survival benefit and the discounted surrender benefit using

| (4.3) | ||||

| (4.4) |

where is a -measurable random variable and is a -adapted process. The insurance benefit is then given by

| (4.5) |

An insurance seeker with such a policy receives the payment at the maturity if he survives until and does not surrender before time . If he surrenders at time he receives the payment .

Example 4.1.

We define the process by

| (4.6) |

for and . Here, denotes the interest rate associated with a guarantee . Furthermore, we assume that in case a policy holder surrenders the contract at time , he will receive the payment for , where denotes the penalty in form of a proportional deduction of the actual value. Thus, we set and for .

Example 4.2.

We consider the parameter set and assume that for every the conditional distribution function of the time of death in (4.1) is given by the well-known Gompertz model, i.e.,

| (4.7) |

In this example we assume that a policy holder is not allowed to surrender, which can be realized by setting .

We set for some risk-free rate and assume that follows a Cox-Ross-Rubinstein model (CRR model) (see Section 5.5 in Föllmer and Schied (2016)). This means that the stock price at time is given by the higher value for with probability and by the lower value for with probability , such that and . Furthermore, we denote by the filtration on given by for . Let for . The unique equivalent martingale measure can be characterized by the measure on such that are independent and

| (4.8) |

We apply the -evaluation on given by and Example 4.1 and get

where the arbitrage-free price for is given by

In this example the map is strictly decreasing in and . Thus, based on Remark 2.14, it holds that

| (4.9) |

In other words, the -robust price equals the worst-case price of all possible models.

Example 4.3.

We extend Example 4.2 and consider an insurance benefit which includes a surrender option. The parameter set is now given by and for every the conditional distribution functions of and in (4.1) are given by (4.7) and

| (4.10) |

The conditional probability to surrender before or at time in (4.10) tends to one if increases. The intuition behind this, which is related to the definition of the insurance benefit in (4.6), is as follows: if the value of the asset decreases, the value of the benefit will also decline. Therefore, the insurance seeker faces the risk of ending up with and thus the probability of needing to surrender increases. Conversely, if the value of the asset increases, the value of increases as well, giving the insurance seeker an incentive to surrender. Obviously, in both cases these considerations further depend on the penalty parameter . In summary, it is more likely that the insurance seeker surrenders in case the value of the asset deviates too much from the level .

In applications, we can choose, for example, the parameter set as the confidence intervals around the empirically observed values of The -evaluation of the benefit given by (4.5) and Example 4.1 is then given by

| (4.11) |

For fixed the function is decreasing in and and thus (4.11) falls to

| (4.12) |

Moreover, we want to compare the robust price in (4.12) with the supremum over all classical -evaluations for , which is given by

| (4.13) |

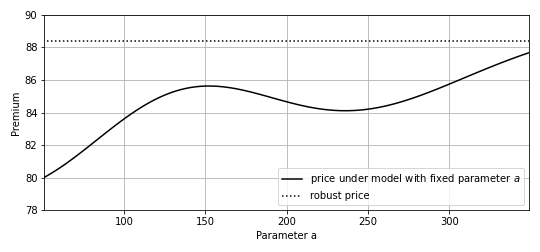

For the numerical evaluation we consider the time horizon and use the following parameters. In the CRR model we set , , and . Furthermore, we fix the strike , the penalty parameter , and the guaranteed interest rate . The parameter set is given by To calculate the value of the robust -evaluation in (4.12), we maximize for each path the function over by using the Nelder-Mead method. As already noted above, due to the monotonicity properties of with respect to and , we only optimize over While the maximum of for the parameter is numerically always attained at the upper boundary of , the optimal value for varies. In particular, we get the following numerical results for and :

| (4.14) |

with the difference given by These results indicate that the robust price, which reflects the model risk and which guarantees that the finance-insurance market is arbitrage-free, is strictly greater than the worst case price of all possible models. This is illustrated in Figure 1.

4.2. Modelling conditional dependence with copulas

In Section 4.1 we assumed that the random times and are -conditionally independent, see Equation (4.2). We now drop this assumption and allow some dependence between and which is modelled by a family of copulas . We assume that under each the law of is described by its marginal distribution functions and and the copula such that

| (4.15) |

We introduce the following notation for the marginal conditional survival probabilities:

The conditional survival function of is then given by

| (4.16) |

which can be described by defined by

such that (4.16) can be rewritten in

Note that is also a copula, cf. (Nelsen, 2007, Section 2.6).

Example 4.4.

A suitable class of copulas that depends on only one parameter is the class of Archimedean copulas (see (Nelsen, 2007, Section 4.2) or Schmidt (2007) for further details and related literature). Most of these copulas can be represented by an explicit formula, which leads to a high tractability for applications. The copula reflects the setting of Section 4.1, cf. Equation (4.2).

Let us consider the insurance benefit given in (4.5) and evaluate this benefit with the -rule. For we get

| (4.17) |

where we use in (4.17) that

Example 4.5.

We briefly show that the Cox model fits in the framework introduced above. To do this, let with for be two increasing processes on and and two random variables on For the parameter set

we choose such that for any with it holds that

Moreover, and are assumed to be conditionally independent of under each . We define the default times and using

where we use the convention In this case and are given by

Conclusion

In this paper we introduce a definition of robust asymptotic insurance-finance arbitrage and characterize the absence of arbitrage. Our main theorem provides an economic foundation for the pricing of finance-linked insurance products via -evaluations. Moreover, we show that valuation principles from a specific class of two-step evaluations can be written as -evaluation. We also apply our results in such a way as to model an insurance-finance market, before concluding with some numerical observations.

Appendix A Proofs of Section 3

Proposition A.1.

The law of under equals for all . Moreover, given any , the law of under equals the law of under .

Proof.

Let and . Then it holds that

where we use the definition of the conditional probability and the tower property in the third equality. The second statement then follows by

Proposition A.2.

Proof.

Proposition A.3.

The projections are -conditionally iid under and consequently also the insurance benefits are -conditionally iid under .

Proof.

Proposition A.4.

Proof.

Using Proposition A.1 and Proposition A.3 the measure fulfills (3.7) and (3.8). Moreover, let be a measure on which also satisfies (3.7) and (3.8) (where is replaced by ). Let be a finite subset and and for all . Then for given by

| (A.2) |

we get the following:

where we use (3.8) in the third equality and Proposition A.2 in the fourth equality. The same calculations can be done for . The sets in (A.2) form a -stable generator of and thus we obtain . This demonstrates the uniqueness. ∎

Proposition A.5.

The set of all measures on such that is a -martingale and which are equivalent to is given by

Proof.

We show that for all it holds that

| (A.3) |

Let then we have

| (A.4) | ||||

Thus, it follows (A.3) and so we can conclude that implies The equivalence of and follows from the equivalence of and . For the other inclusion, let . We must now show that there exists such that . Define by

Then, by changing the roles of and the result follows using (A.4). ∎

Proposition A.6.

For any and we have the following:

Proof.

By using the same arguments as in the proof of Proposition 3.10, we find that

This implies that

The second statement follows analogously. ∎

References

- (1)

- Artzner et al. (2022) Artzner, P., Eisele, K.-T. and Schmidt, T. (2022), ‘Insurance-finance arbitrage’, arXiv preprint arXiv:2005.11022v4 .

- Bartl (2020) Bartl, D. (2020), ‘Conditional nonlinear expectations’, Stochastic Processes and their Applications 130(2), 785–805.

- Biagini and Zhang (2019) Biagini, F. and Zhang, Y. (2019), ‘Reduced-form framework under model uncertainty’, The Annals of Applied Probability 29(4), 2481–2522.

- Biagini et al. (2017) Biagini, S., Bouchard, B., Kardaras, C. and Nutz, M. (2017), ‘Robust fundamental theorem for continuous processes’, Stochastic Processes and their Applications 27(4), 963–987.

- Bouchard and Nutz (2005) Bouchard, B. and Nutz, M. (2005), ‘Arbitrage and duality in nondominated discrete-time models’, The Annals of Applied Probability 25(2), 823–859.

- Denis et al. (2010) Denis, L., Hu, M. and Peng, S. (2010), ‘Function spaces and capacity related to a sublinear expectation: Application to G-Brownian motion paths’, Potential Analysis 34(2), 139–161.

- Denis and Martini (2006) Denis, L. and Martini, C. (2006), ‘A theoretical framework for the pricing of contingent claims in the presence of model uncertainty’, The Annals of Applied Probability 16(2), 827–852.

- Dhaene et al. (2013) Dhaene, J., Kukush, A., Luciano, E., Schoutens, W. and Stassen, B. (2013), ‘Stassen, B.: A note on the (in-)dependence between financial and actuarial risks’, Insurance: Mathematics and Economics 52, 522–531.

- Dhaene et al. (2017) Dhaene, J., Stassen, B., Barigou, K., Linders, D. and Chen, Z. (2017), ‘Fair valuation of insurance liabilities: Merging actuarial judgement and market-consistency’, Insurance: Mathematics and Economics 76, 14–27.

- Föllmer and Knispel (2011) Föllmer, H. and Knispel, T. (2011), ‘Entropic risk measures: Coherence vs. convexity, model ambiguity and robust large deviations’, Stochastics and Dynamics 11(02n03), 333–351.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016), Stochastic finance, de Gruyter.

- Kabanov and Kramkov (1995) Kabanov, Y. M. and Kramkov, D. O. (1995), ‘Large financial markets: asymptotic arbitrage and contiguity’, Theory of Probability & Its Applications 39(1), 182–187.

- Kallenberg and Kallenberg (1997) Kallenberg, O. and Kallenberg, O. (1997), Foundations of modern probability, Vol. 2, Springer.

- Klein (2000) Klein, I. (2000), ‘A fundamental theorem of asset pricing for large financial markets’, Math. Finance 10(4), 443–458.

- Klein et al. (2016) Klein, I., Schmidt, T. and Teichmann, J. (2016), ‘No arbitrage theory for bond markets’, Advanced Methods in Mathematical Finance .

- Majerek et al. (2005) Majerek, D., Nowak, W. and Zieba, W. (2005), ‘Conditional strong law of large number’, International Journal of Pure and Applied Mathematics 20(2), 143 – 156.

- Nelsen (2007) Nelsen, R. B. (2007), An introduction to copulas, Springer Science & Business Media.

- Pelsser and Stadje (2014) Pelsser, A. and Stadje, M. (2014), ‘Time-consistent and market-consistent evaluations’, Mathematical Finance 24(1), 25–65.

- Peng (2019) Peng, S. (2019), Nonlinear expectations and stochastic calculus under uncertainty: with robust CLT and G-Brownian motion, Vol. 95, Springer Nature.

- Plachky and Rüschendorf (1984) Plachky, D. and Rüschendorf, L. (1984), ‘Conversation of the ump-resp. maxmin-property of statistical tests under extensions of probability measures’, Colloquium on Godness of Fit pp. 439–457.

- Rásonyi (2003) Rásonyi, M. (2003), ‘Equivalent martingale measures for large financial markets in discrete time’, Mathematical Methods of Operations Research 58(3), 401–415.

- Schmidt (2007) Schmidt, T. (2007), ‘Coping with copulas’, Copulas-From theory to application in finance 3, 34.

- Semyon et al. (2008) Semyon, M., Eugene, T. and Wüthrich, M. V. (2008), ‘Market consistent pricing of insurance products’, ASTIN Bulletin 38(2), 483–526.

- Soner et al. (2011) Soner, H. M., Touzi, N. and Jianfeng, Z. (2011), ‘Martingale representation theorem for the G-expectation’, Stochastic Processes and their Applications 121(2), 265–287.