Strong identifiability and parameter learning

in regression with heterogeneous response

| Dat Do⋄ | Linh Do‡ | XuanLong Nguyen⋄ |

| University of Michigan, Ann Arbor⋄; Tulane University‡ |

Abstract

Mixtures of regression are useful for regression learning with respect to an uncertain and heterogeneous response variable of interest. In addition to being a rich predictive model for the response given some covariates, the model parameters provide meaningful information about the heterogeneity in the data population, which is represented by the conditional distributions for the response given the covariates associated with a number of distinct but latent subpopulations. In this paper, we investigate conditions of strong identifiability, MLE rates of convergence for the conditional density and model parameters, and the Bayesian posterior contraction behavior arising in finite mixture of regression models, under exact-fitted and over-fitted settings and when the number of components is unknown. This theory is applicable to common choices of link functions and families of conditional distributions employed by practitioners. We provide simulation studies and data illustrations, which shed some light on the parameter learning behavior found in several popular regression mixture models reported in the literature.

1 Introduction

Regression is often associated with the task of curve fitting — given data samples for pairs of random variables , find a function that captures the relationship between and as well as possible. As the underlying population for the pairs becomes increasingly complex, much effort has been devoted to learning more complex models for the regression function . In many data domains, however, due to the heterogeneity of the behavior of the response variable with respect to covariate , no single function can fit the data pairs well, no matter how complex is. Many authors noticed this challenge and adopted a mixture modeling framework into the regression problem, going back to [10, 32], and continuing with more recent applications, e.g., [1, 4, 26, 29, 28].

To capture the uncertain and highly heterogeneous behavior of response variable given covariate , one needs more than one single regression model. Suppose that there are different regression behaviors, one can represent the conditional distribution of given by a mixture of conditional density functions associated with underlying (latent) subpopulations. One can draw from modeling tools of conditional densities such as generalized linear models or more complex components to increase model fitness for the regression task [20, 14]. Making inferences in regression mixtures can be achieved in a frequentist framework (e.g., maximum conditional likelihood estimation (MLE) [3]), or a Bayesian framework [19]. In addition to enhanced predictability for the response variable given the covariate, a key benefit of regression mixture models is that the model parameters may be used to explicate the relationship between these variables more accurately and meaningfully.

Despite the aforementioned long history of applications, a satisfactory level of understanding of several key issues concerning model parameters’ identifiability and a large sample theory of regression mixture models remains far from being complete. This is perhaps due to the somewhat unusual position where regression mixture model based methods sit — like any regression problem one is interested in prediction performance, but unlike the traditional viewpoint of a single curve-fitting task one must come to terms with the multi-modality of the response variable due to the underlying data population’s latent heterogeneity. Thus, one must also be interested in the quality of parameter estimates representing such heterogeneity. There is a slowly growing theoretical literature, but most existing works are limited to the questions of consistency of estimation for the mixture of generalized linear models with some specific classes of conditional densities and link functions, or simulation-based methods [13, 22, 21, 37, 12, 36]. In particular, [13] investigates the identifiability of the mixture of Gaussian regression models with linear link functions. [22] generalizes the results for the exponential families. [37] further extends the identifiability results to more general link functions, but no analysis of parameter estimation. [36] shows the consistency for density learning of this model under the Bayesian setting. On parameter estimation behavior, more recently [23] proposed a penalized MLE method for model selection for the class of identifiable mixture of regression models with linear link functions and established rates of parameter estimation. [18] investigated the parameter estimation behavior for the Gaussian mixture of regression models.

In this paper, we study parameter identifiability, parameter estimation behavior, and prediction performance arising from the finite mixture of regression models. We work with general conditional density kernels and link functions, investigate both an MLE approach and a Bayesian approach for estimation. Consider a regression mixture model in the following form:

| (1) |

where is a vector including the explanatory variables, is the response variable. The conditional density function take the mixture form, where the discrete probability measure encapsulates all unknown parameters in the model, with being the mixing proportion, and and being parameters in a compact subspace of and of , respectively. We call the latent mixing measure associated with the regression mixture model. The link functions and are known, where are compact subsets of . The family of densities is given, where all of them are dominated by a common distribution on which can be either a counting or continuous measure. In many applications, the family is a dispersion exponential family distribution with parameter is modeled as the mean, and is modeled as the variance of so that the mixture of regression models can capture the average trends and dispersion of subpopulations in the data. We are interested assessing the quality of the conditional density estimates, as well as that of parameters , , and from i.i.d. samples , where distribution of given is given in the model (1) and follows some (unknown) marginal distribution on .

Our parameter estimation theory inherits from and generalizes several recent developments in the finite mixture models literature. [2] initiated the theoretical investigation of parameter estimation in a univariate finite mixture model by introducing a notion of strong identifiability. [27] developed a theory for both finite and infinite mixture models in a multivariate setting using optimal transport distances. [16] studied convergence rates in various families of vector-matrix distributions. A central concept in these papers is the notion of strong identifiability of (unconditional) mixtures of density functions. This is a condition on a parametrized family of density function of , as there is no covariate here. At a high level, it requires that the family of function , along with their partial derivatives with respect to the parameters up to a certain order, are linearly independent. Once this condition is satisfied, one can establish a lower bound on the distance between mixture distributions in terms of the optimal transport distances between the corresponding latent mixing parameters. Such a bound is called an inverse bound, which plays a crucial role in deriving the rates of parameter estimates.

With regression mixture modeling, we move from the unconditional mixtures described above to conditional mixture models. Thus, there are several fundamental distinctions. First, one works with the family of conditional density functions in the form , which involves both the conditional density kernel and the link function . A strong identifiability condition for conditional distributions that we develop will inevitably involve both variables and . The focus of inference is on the conditional distribution of given covariate , while the marginal distribution of is assumed unknown and of little interest. Accordingly, the identifiability condition must ideally require as little information from the marginal distribution of the covariate as possible. Moreover, given that the identifiability condition holds, the inverse bound that we establish will be a lower bound on the expected distance of the conditional densities, where the expectation is taken with respect to the marginal distribution of the covariate. This is also crucial because we will obtain rates of conditional density estimation in terms of the mentioned expected distance and use the inverse bound to derive the rates of convergence for the corresponding mixing parameters of interest.

Another interesting feature that distinguishes conditional mixtures from unconditional mixtures is that the former tends to satisfy strong identifiability conditions more easily than the latter. This is because of the role the covariate plays in providing more constraints that prevent the violation of the linear independence condition. For instance, it is trivial that an unconditional mixture of Bernoulli distributions is not identifiable, but it will be shown (not so easily) that the mixture of conditional distributions using the Bernoulli kernel is not only identifiable but also strongly identifiable. There are situations where there is a lack of strong identifiability, such as in the case of negative binomial regression mixtures, a model extensively employed in practice (e.g., see [29, 28]), but we shall show that such situations occur precisely only in a Lebesgue measure zero subset of the parameter space.

To summarize, there are several contributions made in this paper. First, we develop a rigorous notion of strong identifiability for general regression mixture models. We provide a characterization of such a notion in terms of simple conditions on the conditional density kernel and link function and show that they are satisfied by a broad range of density kernels and link functions often employed in practice. Second, we study several examples of regression mixtures when strong identifiability is violated and investigate the consequences. Third, we establish learning rates for regression mixtures given strong identifiability, under both Bayesian estimation and MLE frameworks. We consider three different learning scenarios: when the number of mixture components is known (i.e., exact-fitted setting), when only an upper bound is known (i.e., overfitted setting), and when even such an upper bound is unknown. Finally, we conduct a series of simulation studies to support the theory and discuss the connections with empirical findings in the regression mixture literature [21, 29, 31].

The rest of this paper is organized as follows. Section 2 provides preliminaries on the mixture of regression models. In Section 3, we present notions of strong identifiability and associated characterization for regression mixtures, followed by a set of inverse bounds. Building upon this strong identifiability theory, in Section 4, we establish the rates of conditional density estimation and parameter estimation. In Section 5, we carry out simulation studies and data illustrations to support our theory and discuss the empirical findings in the literature. Finally, Section 6 discusses future directions. All proofs are deferred to the Supplementary material.

Notation

Given a mixing measure , the mixture of regression model with respect to is denoted by . The joint distribution of is , where is an unknown distribution of covariate . denotes the expectation w.r.t. . We write for short, for , if there is no confusion. Denote , . Let be the space of mixing measures with exactly atoms in , and the space of mixing measures with no more than atoms in . If there is no confusion, we write and as and for short. For two sequence and , we write if there is a constant such that for all . We also write if , and if we have both and . The multiplicative constants in those inequalities will be specified in the main results for clarity. We use , and for the Hellinger distance, total variation distance, and Kullback-Leibler (KL) divergence between densities, respectively.

2 Preliminaries

Regression mixture models

A mixture of regression model may be applied with many different family distributions and link functions to fit a large range of data distributions. For example, when the response variable is continuous, we can choose the family of (conditional) density to be normal , and parametrize and via two link functions , for . These functions can be represented by polynomials or trigonometric polynomials with variable and coefficients . Alternatively, when is a counting variable, one can use the Binomial distribution if is bounded and the Poisson distribution otherwise. If one wishes to take into account the dispersion of , Negative Binomial distribution , where may be used. If the values of or need to be non-negative or belong to a compact set, one may apply functions such as exponential functions or the sigmoid (inverse logit) function compositing with a polynomial or trigonometric polynomial parametrized by . The general theory to be presented will be applicable to all these models, and others.

Wasserstein distances

As discussed in the Introduction, all parameters in the mixture model for the conditional distribution of the response given covariate are encapsulated by the latent mixing measure . In order to characterize identifiability and learning rates of parameter learning, one needs a suitable metric for the mixing measure . Wasserstein distances have become a useful tool to quantify the convergence of latent mixing measures in mixture models [27]. Given two discrete measures and on a normed space endowed with a norm , the Wasserstein metric, in which , is defined as:

where the infimum is taken over all joint distribution on such that . Note that for , if varies on such that and is compact, then

| (2) |

where is the Voronoi cell of in (see, e.g., [17]). Hence, for every atom of , there is a subset of atoms of converging to it at the same rate as . Therefore, the convergence in a Wasserstein metric implies the convergence of parameters in mixture models. In this paper, unless noted otherwise the space is chosen to be a compact subset of and is the usual distance.

Mixtures of conditional densities.

In a regression mixture model, a focus of inference will be on the conditional density , while there will be as little assumption as possible on the marginal distribution of covariate . It is clear from the representation of that the identifiability and parameter learning behavior of the regression problem will repose upon suitable conditions specified by , and the unknown parameter . The analysis of conditional density estimation requires us to control how large the conditional density family is. This can be accomplished by assuming Lipschitz conditions on , and . In particular, we say that is uniformly Lipschitz if there exists such that for all :

| (3) |

The link functions and are called uniformly Lipschitz if there are such that for all :

| (4) |

In a regression problem, one is interested in prediction error guarantee in addition to assessing the quality of parameter estimates. For a standard (single component) regression model, we often model , where is the mean parameter, i.e., . After estimating from the data, the prediction error is customarily taken to be the mean square error , where is the true parameter. For a regression mixture, let the true latent mixing measure be for which an estimate is denoted by . In this setting, due to the heterogeneous nature of the response, the predicted value for at any may be taken by the quantity , or its mean . As a result, the prediction error for the mean estimate can be written as . If one is interested in describing the prediction error in terms of both the mean trend and dispersion, one can use

Key inequalities

The following basic inequality controls the expected total variation distance between conditional densities by a Wasserstein distance between the corresponding parameters:

Lemma 2.1.

The inequality established in the above lemma quantifies the impact of parameter estimation on the quality of conditional density estimation: if is well estimated, then so is the conditional distribution represented by the conditional densities . In order to quantify the identifiability and convergence of the unknown parameter , we will need to establish inequalities of the following type:

| (6) |

for all in some space of latent mixing measures, and depends on that space. Following [27, 38, 5], we refer to this as inverse bounds, because in our setting, they allow us to lower bound the distance between conditional probability models ( and ) by the distance between the parameters of inferential interest ( and ). Unlike prior works, our inverse bounds control the expected total variational distance under the marginal distribution of the covariate . A simple observation is that these inverse bounds are quantitative versions of the classical identifiability condition [34] for the regression problem, because if for a.e. , then the bound (6) entails that . Moreover, the inverse bounds play an important role in establishing the convergence rate for parameter estimation. They allow us to translate convergence rates for density estimation (left-hand side of Eq. (6)) into that of parameter estimation (right-hand side of Eq. (6)). The technique to prove inverse bounds is to rely on a notion of strong identifiability to be developed for regression mixture models in the following section.

3 Strong identifiability and inverse bounds

3.1 Conditions of strong identifiability

Identifiability and strong identifiability conditions play important roles in the theoretical analysis of mixture models [34, 2, 16]. They provide a finer characterization of the non-singularity of the Fisher information for mixtures of distributions [17]. In plain words, these conditions require that the kernel density function of interest and its derivatives up to a certain order with respect to all relevant parameters be linearly independent. For the mixture of regression model (1), the kernel density function is that of the conditional probability of variable given covariate . The following definition is our formulation of strong identifiability for the conditional density functions:

Definition 3.1.

The family of conditional densities (or in short, ) is identifiable in order , where (resp., ) with complexity level , if is differentiable up to order with respect to , and (A1.) (resp., (A2.)) holds.

-

(A1.)

(First order identifiable) For any given distinct elements , if there exist as such that for almost all (w.r.t. )

then for ;

-

(A2.)

(Second order identifiable) For any given distinct elements and , if there exist , and as such that for almost all (w.r.t. )

then for .

When we speak of strong identifiability without specifying the complexity level, it should be understood that the condition is satisfied for any complexity level . These strong identifiability conditions for conditional density functions are useful in deriving rates of convergence for the regression mixture model’s parameters even when the associated Fisher information matrices are singular, e.g., when the model has redundant parameters. Indeed, when showing the convergence rate of an estimator to the true mixing measure in the over-fitted setting, there might exist several redundant atoms of converge to a common atom of . The customary technique of applying the first-order Taylor expansion around may fail because the coefficients of these redundant components can be combined and canceled out. Instead, one needs to perform a Taylor expansion up to the second order around , necessitating the second-order identifiability condition developed here. It will be shown in the sequel that the strong identifiability conditions hold for most popular mixtures of regression models. There are notable exceptions which shall be discussed separately. For instance, a mixture of binomial regression models generally satisfies strong identifiability only up to a finite complexity level.

Since our model (1) is hierarchical with two levels of parameters:

| (7) |

it is difficult to directly verify conditions (A1.) and (A2.). We will show in the following that they can be deduced from the identifiability conditions of a family of (unconditional) distribution and family of functions . Recall from [16, 27]:

Definition 3.2.

The family of (unconditional) distributions (or in short, ) is identifiable in order with complexity level , for some , if is differentiable up to order in and the following holds:

-

(A3.)

For any given distinct elements , if for each pair of , where , we have such that

for almost all , then for all and pair .

Condition (A3.) for simply ensures that the mixture of distributions model uniquely identifies the mixture components. The strong identifiability conditions () are required to establish the convergence rates [2, 27]. In the model (1), there is a hierarchically higher level of parameters that we want to learn, and it connects to the observations through the link functions as . To ensure that and can be learned efficiently, we also need suitable conditions for and .

Definition 3.3.

The family of functions is called identifiable with complexity level respect to if the following conditions hold:

-

(A4.)

For every set of distinct elements , there exists a subset , such that

are distinct for every ; -

(A5.)

Moreover, if there are vector such that

where is a zero-measure set (i.e., ), then and .

Remark 3.1.

-

1.

Condition (A4.) is necessary for identifying regression mixture components. Indeed, for two distinct pairs and in , there may exists some point so that . If we only observe data at such , it is not possible to distinguish between and .

-

2.

In linear models, condition (A5.) reads that there is no multicollinearity: If we model , where ’s are pre-defined functions, then by substitute this into condition (A5.), we have must be linearly independent as functions of . Otherwise, the model is not identifiable with respect to parameters ’s.

- 3.

Hence, the two conditions in Definition 3.3 are necessary for learning parameters of the mixture of regression models. The following result shows that Definition 3.2 and Definition 3.3 give sufficient conditions to deduce the strong identifiability given by Definition 3.1, where the chain rule plays an essential role in its proof.

Theorem 3.1.

For any complexity level , if the family of distributions is strongly identifiable in order (via (A3.)) and the family of functions is identifiable (via (A4.) and (A5.)), then the family of conditional density is strongly identifiable in order , where .

3.2 Characterization of strong identifiability

Theorem 3.1 provides a simple recipe for establishing the strong identifiability of the conditional densities arising in regression mixture models (1) by checking the identifiability conditions of family and family . In the following, we provide specific examples.

Proposition 3.1.

(a) The family of location normal distribution with fixed variance is identifiable in the second order, for . The location-scale family is identifiable in the first order;

(b) The Poisson family is identifiable in the second order;

(c) The family of Binomial distributions with fixed number of trials is identifiable in the first order with complexity level if , and is identifiable in the second order with complexity level if ;

(d) The family of negative binomial distributions with fixed is identifiable in the second order.

The identifiability conditions (A4.) and (A5.) usually hold for parametric models, as we see below. We first define a general class of functions:

Definition 3.4.

We say a family of functions is completely identifiable if for any , we have almost surely in .

Proposition 3.2.

If and are both completely identifiable, then the family of functions satisfies condition (A4.).

Most functions used in parametric regression mixture models are completely identifiable.

Proposition 3.3.

Suppose that has a density with respect to Lebesgue measure on , then the following families of functions are completely identifiable and satisfy condition (A5.):

(a) Polynomial of finite dimensions

, where and ;

(b) Trigonometric polynomials in : , where ;

(c) Mixtures of polynomials and trigonometric polynomials as in (a) and (b): , where ;

(d) , where is a diffeomophism and is completely identifiable and satisfies condition (A5.).

Remark 3.2.

In a general linear model, or , where is the sigmoid (inverse logit) function. Both the exponential function and sigmoid function are one-to-one, and is a first-order polynomial, so the above results apply.

3.3 Inverse bounds for mixture of regression models

At the heart of our convergence theory for parameter learning in regression mixture models lies a set of inverse bounds, which are given as follows.

Theorem 3.2.

-

(a)

(Exact-fitted) Given for . Suppose that the family of conditional densities is identifiable in the first order, and the family of functions is identifiable (with the complexity level ). Then for all , there holds

(8) where the constant in this inequality depends only on , and (but not on ).

-

(b)

(Over-fitted) Given for and for some natural number . Suppose that the family of conditional densities is identifiable in the second order, and the family of functions is identifiable (with the complexity level ). Then for all , there holds

(9) where the constant in this inequality depends only on , and (but not on ).

If the true number of components is known, then Theorem 3.2 entails that the convergence rate for parameter estimations can be as fast as the convergence rate for conditional densities under the total variation distance. However, in practice, we may not know and fit the system by a large number . In this over-fitted regime, provided that the identifiability conditions for distribution and function are satisfied in the second order, the convergence rate for parameter estimation may be twice as slow as that of the conditional densities.

Based on the convergence behavior of the regression mixture model’s parameters, we can establish guarantees on the prediction error for the response variable. The following bounds will be useful for deducing the prediction error bounds from that of parameter estimates.

Proposition 3.4.

Suppose that the density and link functions are uniformly Lipschitz, then for all and , we have

and

where the constants in those inequalities only depend on Lipschitz constants of and .

3.4 Consequences of lack of strong identifiability

Strong identifiability notions characterize the favorable conditions under which efficient regression learning is possible in the mixture setting. Next, we turn our attention to the consequence of the lack of strong identifiability. Firstly, we note that the normal distributions satisfy the well-known heat equation: , so the mixture of normal regression model no longer satisfies the strong identifiability condition in the second order. This (Fisher information matrix’s) singularity structure is universal (i.e., holds for all ). Therefore, the inverse bounds presented in Theorem 3.2 may not hold and potentially lead to slow convergence rates for Gaussian mixtures (see also [18]).

Another interesting example arises in the negative binomial regression mixture models, which have been utilized in the traffic analysis of heterogeneous environments [29, 28]. These authors observed via many empirical experiments that the quality of parameter estimates and the prediction performance may be affected by the (overlapped) sample-mean values obtained from the data. However, there was a lack of precise theoretical understanding. Our theoretical framework can be applied to shed light on the behavior of this class of regression mixture model. It starts with the observation that the mixture of negative binomial distributions does not satisfy the first-order strongly identifiable condition. Moreover, we can identify precisely the instances where strong identifiability fails to hold and investigate the impact on the quality of parameter estimates and the prediction performance in such instances.

First, we note that the mean-dispersion negative binomial conditional density satisfies the following equation:

| (10) |

Thus, a 2-mixture of negative binomial distributions and such that

| (11) |

does not satisfy the strong identifiability condition in the first order, resulting in slow convergence for parameter estimation. It can be seen via the following minimax lower bound:

Theorem 3.3.

Consider a mixture of negative binomial regression model with link functions for and . Then for any measurable estimate of the mixing measure , the following holds for any :

| (12) |

Fortunately, not all are bad news for negative binomial regression mixtures. We will show that non-identifiability occurs only in a Lebesgue measure zero subset of the parameter space.

Proposition 3.5.

Given distinct pairs such that there does not exist two indices satisfying and , then the mixture of negative binomials is strongly identifiable in the first order. If we further assume that there does not exist two indices satisfying and , then the mixture of negative binomials is strongly identifiable in the second order.

Finally, we note that the theory established earlier (Theorem 3.1 and Theorem 3.2) represent sufficient conditions. There still may exist non-strongly identifiable families and that lead to strong identifiable . For example, the mixture of two Binomial distributions is not identifiable, because for instance, for and . However, the mixture of two logistic regression models is strongly identifiable (see Proposition B.1 in Appendix B) and enjoys the inverse bound as well as standard convergence rates. Unfortunately, such a result is difficult to generalize. This again highlights our general theory developed in this section, which is applicable to a vast range of kernels and link functions . The pathological phenomena described will be revisited in Section 5.

4 Statistical efficiency in learning regression mixtures

Building on the previous section, we are ready to present convergence rates of the maximum likelihood estimator, and a Bayesian posterior contraction theory for the quantities of interest.

4.1 Maximum (conditional) likelihood estimation

Given i.i.d. observations , where and , for . Denote the maximum likelihood estimate by

in the exact-fitted setting, and we change the in the above formula to , where in the over-fitted setting. It is implicitly assumed in this section that is measurable, otherwise a standard treatment using an outer measure of instead of can be invoked. To obtain the rate of convergence of to , we combine the inverse bounds above with the convergence of density estimates based on the standard theory of M-estimation for regression problems [35]. For conditional density estimation, the convergence behavior of to is evaluated in the sense of the expected Hellinger distance:

for all . To this end, recall several basic notions related to the entropy numbers of a class of functions. For any , set

and the Hellinger ball centered around :

The complexity (richness) of this set is characterized in the following entropy integral:

| (13) |

where is the bracketing entropy number. An useful tool for establishing the rate of convergence under expected conditional density estimation by the MLE is given by the following theorem, which is an adaptation of Theorem 7.4. in [35] or Theorem 7.2.1. in [9]).

Theorem 4.1.

Take in such a way that is a non-increasing function of . Then, for a universal constant and for

| (14) |

we have for all that .

Combining Theorem 4.1 with the inverse bounds established in Section 3, we readily arrive at the following concentration inequalities for the MLE’s parameter estimates based on the bracketing entropy numbers and its entropy integral given by Eq. (13).

Theorem 4.2.

-

(a)

(Exact-fitted) Suppose that is known, the entropy condition (14) holds, the family of conditional densities is identifiable in the first order, and is identifiable. Then, for any , there exist a constant depending on and universal constant such that

-

(b)

(Over-fitted) Suppose that is unknown but known, the entropy condition (14) holds, the family of conditional densities is identifiable in the second order, and is identifiable. Then, for any , there exist a constant depending on and and universal constant such that

For concrete rates of convergence, we need to estimate the entropy integral (13). For many parametric models, we will find that the convergence rate for the mixing measure is under for the exact-fitted setting and under for the over-fitted setting. In the following, we shall present a set of mild assumptions and show that under these assumptions, such parametric rates can be established.

-

(B1.)

(Assumptions on kernel densities) For the family of distribution , is uniformly bounded and uniformly light tail probability, i.e., there exist constant and constant such that for all or and .

- (B2.)

We note that:

Proposition 4.1.

The families of Normal, Poisson, Binomial, and negative binomial distribution satisfy condition (B1.).

The predictive performance of MLE for the regression mixture model is given as follows.

Theorem 4.3.

Given assumptions (B1.) and (B2.), and the dominating measure is Lebesgue over or counting measure on . Then, there exists a constant depending on , and a universal constant such that

Combining Theorem 3.2 and Theorem 4.3, we arrive at the convergence rates for the maximum (conditional) likelihood estimates for the model parameters:

Theorem 4.4.

-

(a)

(Exact-fitted) Suppose that is known, the family of conditional densities is identifiable in the first order, and the family of functions is identifiable. Furthermore, assume (B1.) and (B2.) hold, then for any , there exist constant depending on and a universal constant such that

-

(b)

(Over-fitted) Suppose that is unknown and is upper bounded by a known number , the family of conditional densities is identifiable in the second order, and the family of functions is identifiable. Furthermore, assume (B1.) and (B2.) hold, there exist constant depending on and a universal constant such that

4.2 Bayesian posterior contraction theorems for parameter inference

Given i.i.d. pairs such that for some true latent mixing measure , and . In the Bayesian regime, we model the data as where with being some prior distribution on the space mixing measures. Let denote the support of the prior on the mixing measure . The nature of the prior distribution depends on the several different settings that we will consider. In the exact-fitted setting, we assume is known, whereas the over-fitted setting means that the upper bound is given, but unknown. In both cases, so is in effect a prior distribution on . Later, we shall assume that neither nor an upper bound is given; instead, a random variable is used to represent the number of mixture components and endowed with a prior distribution.

By the Bayes’ rule, the posterior distribution of the parameter is given by

for any measurable set . Now, we want to study the posterior contraction rate of to the true latent mixing measure as . We proceed to describe several standard assumptions on the prior often employed in practice.

The case of known upper bound

-

(B3.)

(Prior assumption) Prior on space is induced by prior on , , where is a prior distribution of on , is a prior distribution of on , and is a prior distribution of on , independently for . We further assume that have a density with respect to Lebesgue measure on , respectively, which are bounded away from zero and infinity.

-

(B4.)

There exists such that for all satisfying , we have for only depends on .

The posterior contraction behavior for conditional densities is given as follows.

Theorem 4.5.

Assume that (B2.)-(B4.) hold. For any , there exists constant depending on such that as ,

| (15) |

Combining the above result with the inverse bounds developed in Section 3 leads to the contraction rates of the posterior distribution in the exact-fitted and over-fitted settings.

Theorem 4.6.

Suppose that assumptions (A1.)-(A3.) and (B2.)-(B4.) hold. Fix any .

-

(a)

(Exact-fitted) If , there exists some constant depending on such that

-

(b)

(Over-fitted) If , there exists some constant depending on such that

The case of unknown

Finally, when the number of components and its upper bound are unknown, there are various approaches for prior specification. Here, we adopt the widely utilized "mixture-of-finite-mixtures" prior [24]. In particular, the prior distribution on the space of mixing measures is induced by the following specification.

-

(B5.)

A prior distribution on with support in , i.e., for all .

-

(B6.)

For each , given the event , the conditional prior distribution of the mixing measure is induced by the following specification: on , , where is a prior distribution of on , is a prior distribution of on , and is a prior distribution of on , independently for . Assume that have a density with respect to Lebesgue measure on , respectively, which are bounded away from zero and infinity.

-

(B7.)

For each , there exists such that for all satisfying , we have for only depends on .

Theorem 4.7.

Assume that (A1.)-(A3.), (B2.), and (B5.)-(B7.) hold. There exists a subset , where such that for all and , there hold as

-

(a)

a.s. under ;

-

(b)

there is a constant depending on such that

5 Simulations and data illustrations

Regression mixtures vs unconditional mixtures

The characterization results (Theorem 3.1 and propositions in Section 3.2) provide easy-to-check sufficient conditions for strong identifiability (in the sense of Def. 3.1). Part of the sufficient conditions requires that the kernel density be strongly identifiable up to a certain order, a standard condition considered in the asymptotic theory for finite (and unconditional) mixture models [27, 15, 17]. It is noteworthy that the strong identifiability condition of a mixture of regression model given in Def. 3.1 is typically a weaker condition than that of a standard unconditional mixture model, because the presence of the covariate makes the conditional mixture model more constrained. Hence, it is possible that for an unconditional mixture of kernel densities strong identifiability and hence the inverse bound may not hold, but when is utilized in a regression mixture model instead, the strong identifiability and hence the inverse bound still holds.

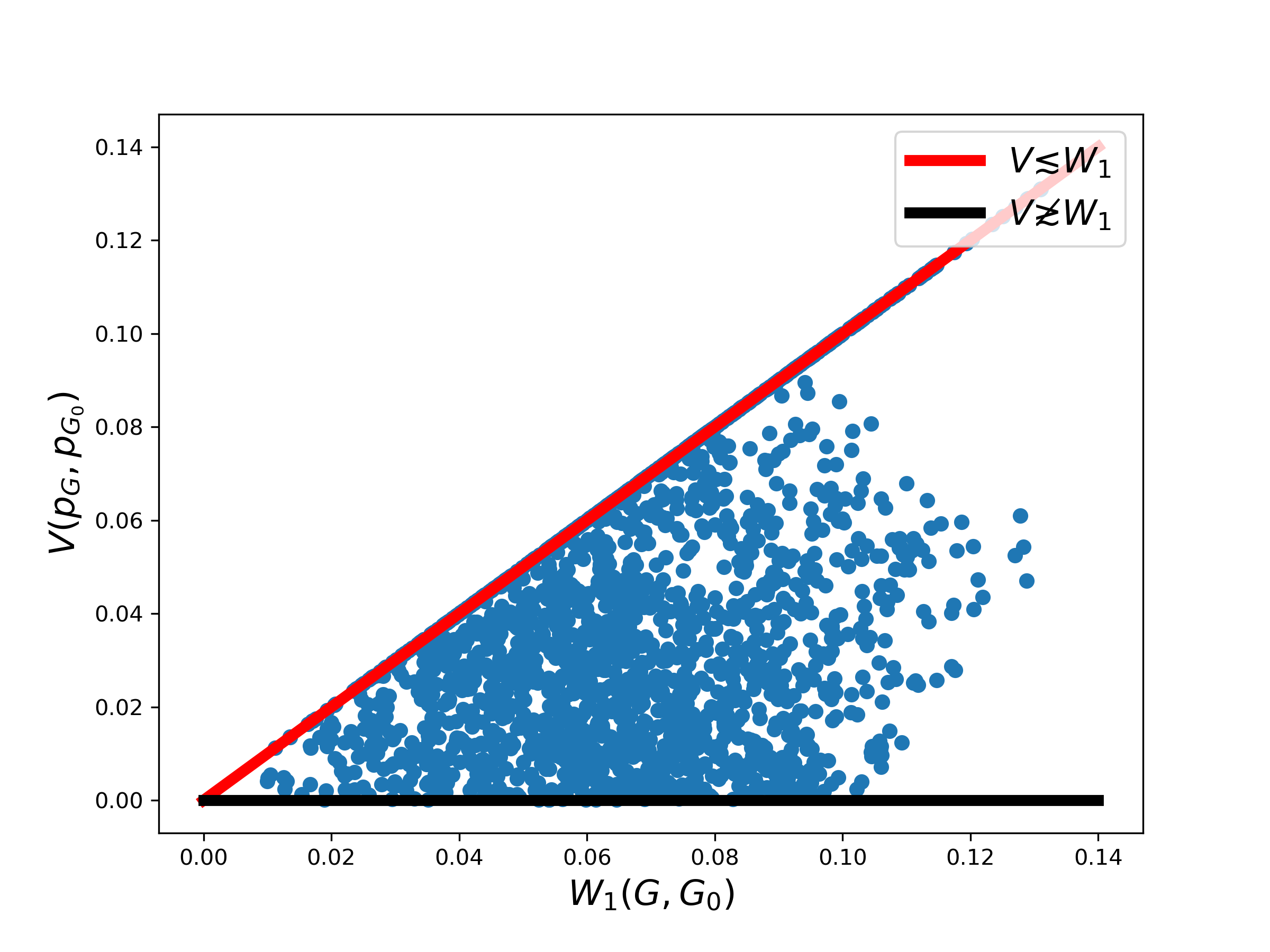

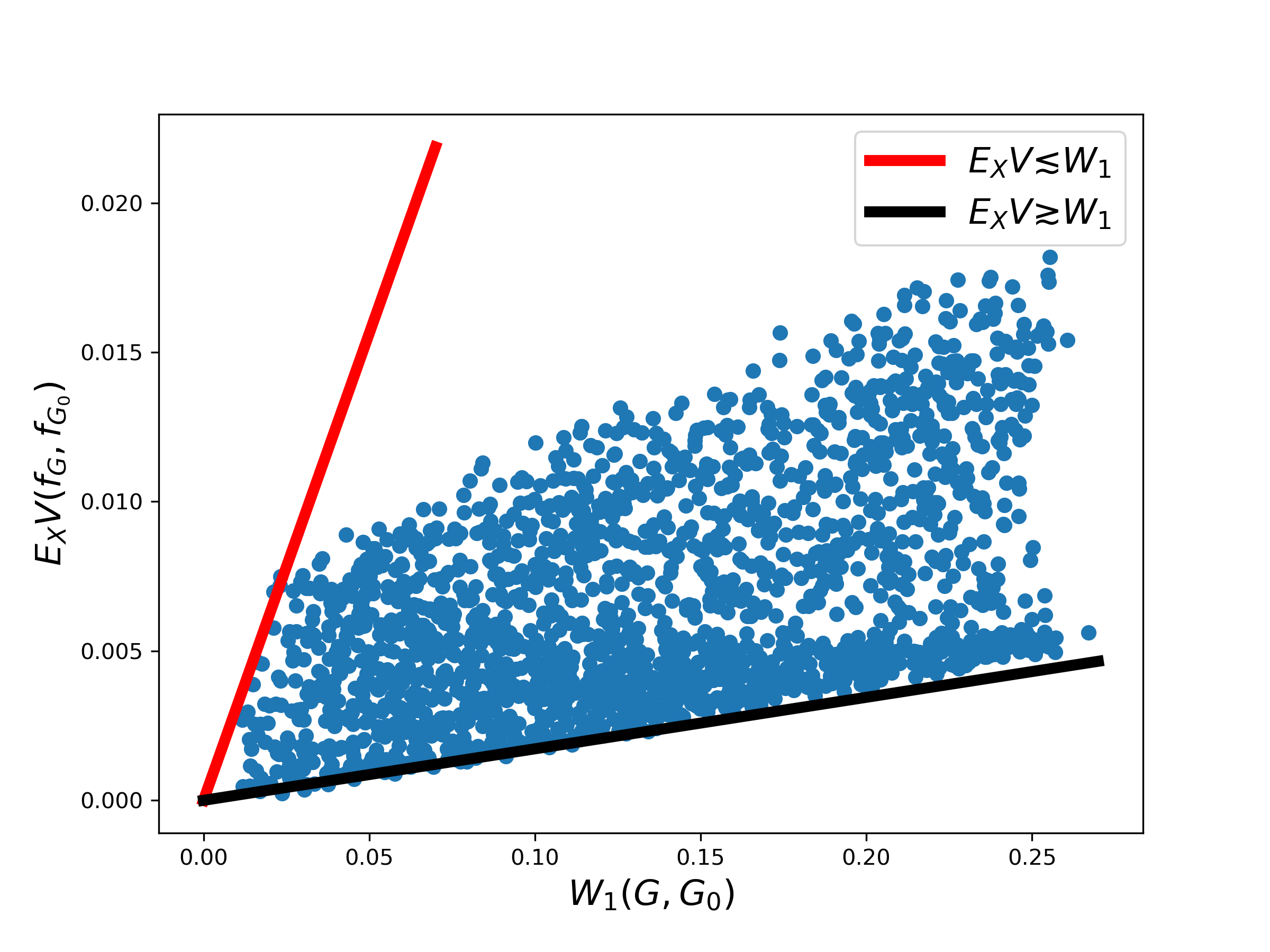

We demonstrate this observation by a theoretical result given in Proposition B.1 for the mixture of binomial regression models. To illustrate this result by a simulation study, let , for , where is a fixed natural number. From the discussion in Section 3, we know that this model is only strongly identifiable in the first order if . It means the inverse bound may not hold when . Let , so that , and , and then uniformly generate 2000 random samples of around . We compare against to see if the inverse bound holds or not. It can be seen in Fig. 5.1(a) that such an inverse bound does not hold. In contrast, for the mixture of binomial regression model under the same setting (a.k.a. mixture of two logistic regression): for and being the sigmoid function, the inverse bound as established by Theorem 3.2 still holds. We uniformly sample 2000 measure around and plot against , for . The relationship holds in this scenario (Fig. 5.1(b)). As a consequence, the mixture of logistic regression model still enjoys the convergence rate of for parameter estimation in the exact-fitted setting.

(a) Mixture of binomial distributions

(b) Mixture of binomial regression models

Simulation studies for exact-fitted and over-fitted settings

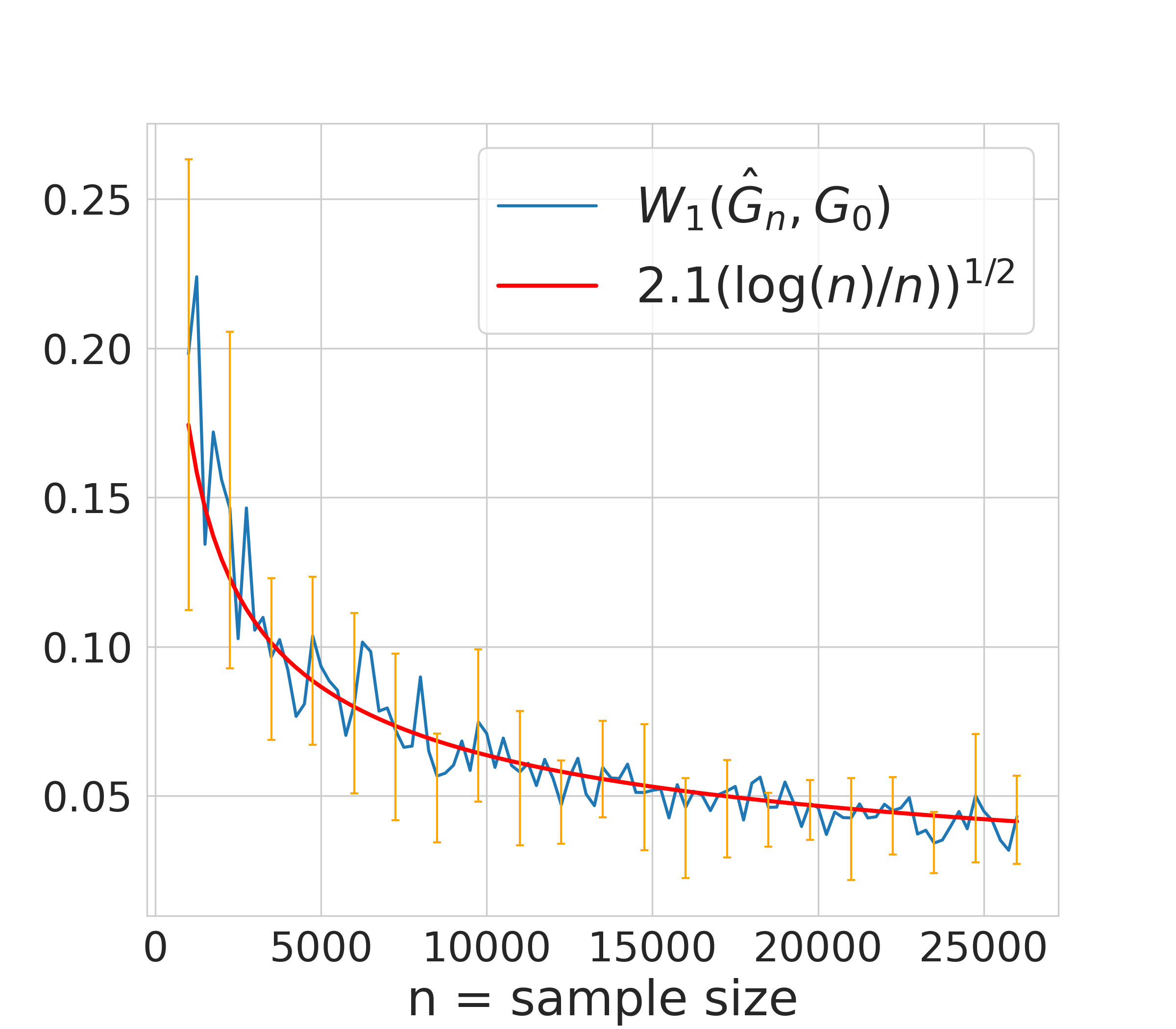

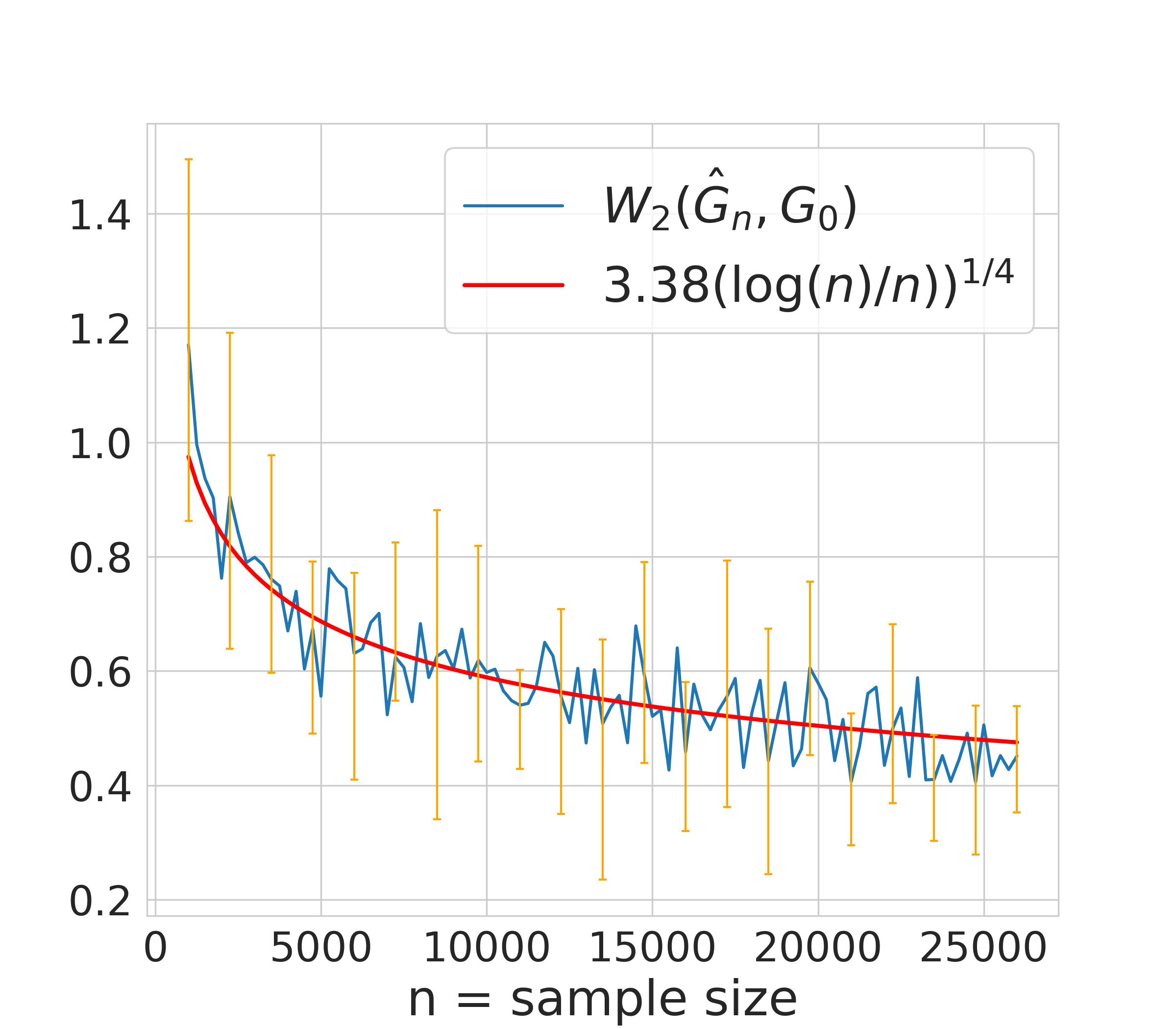

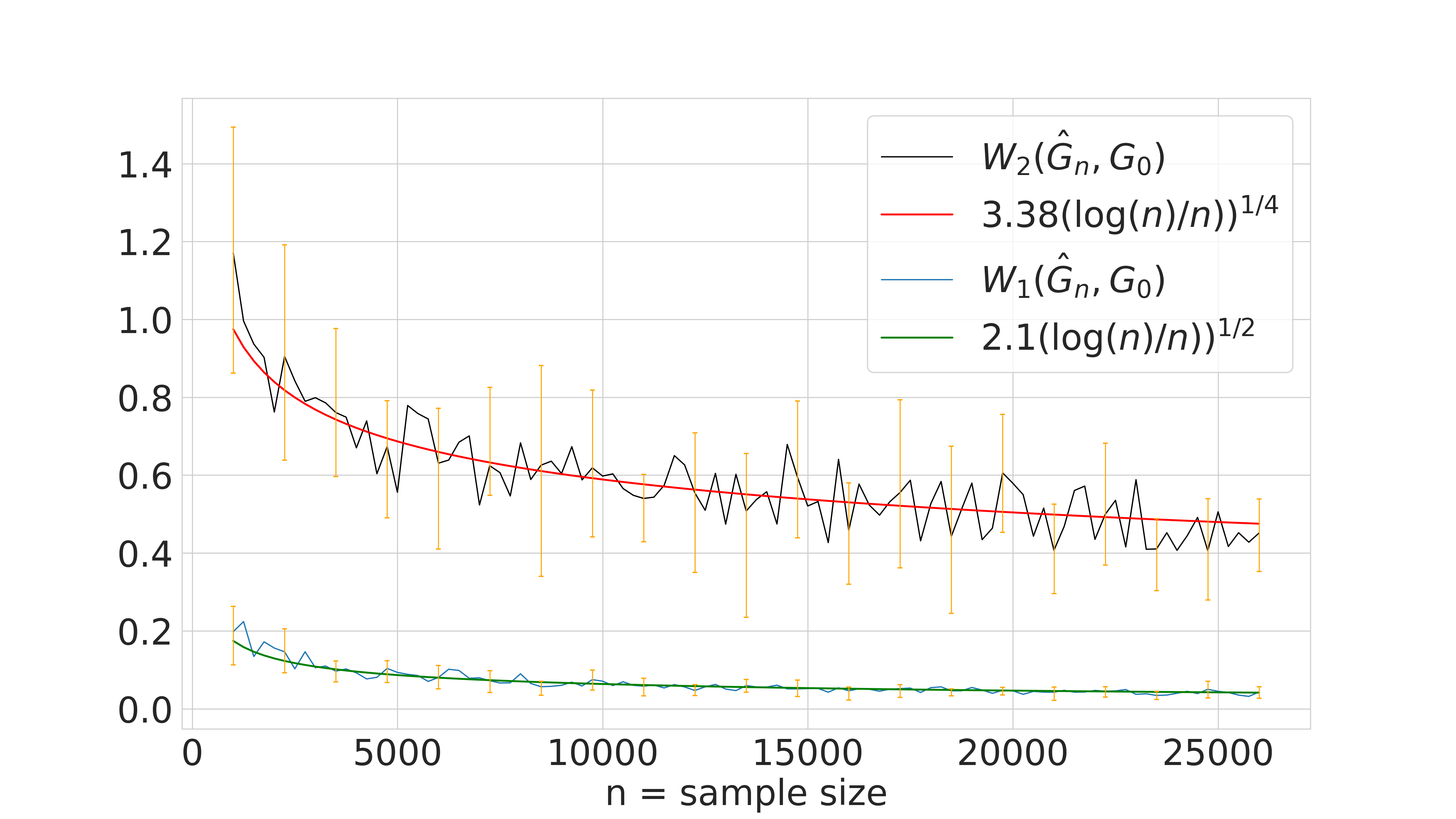

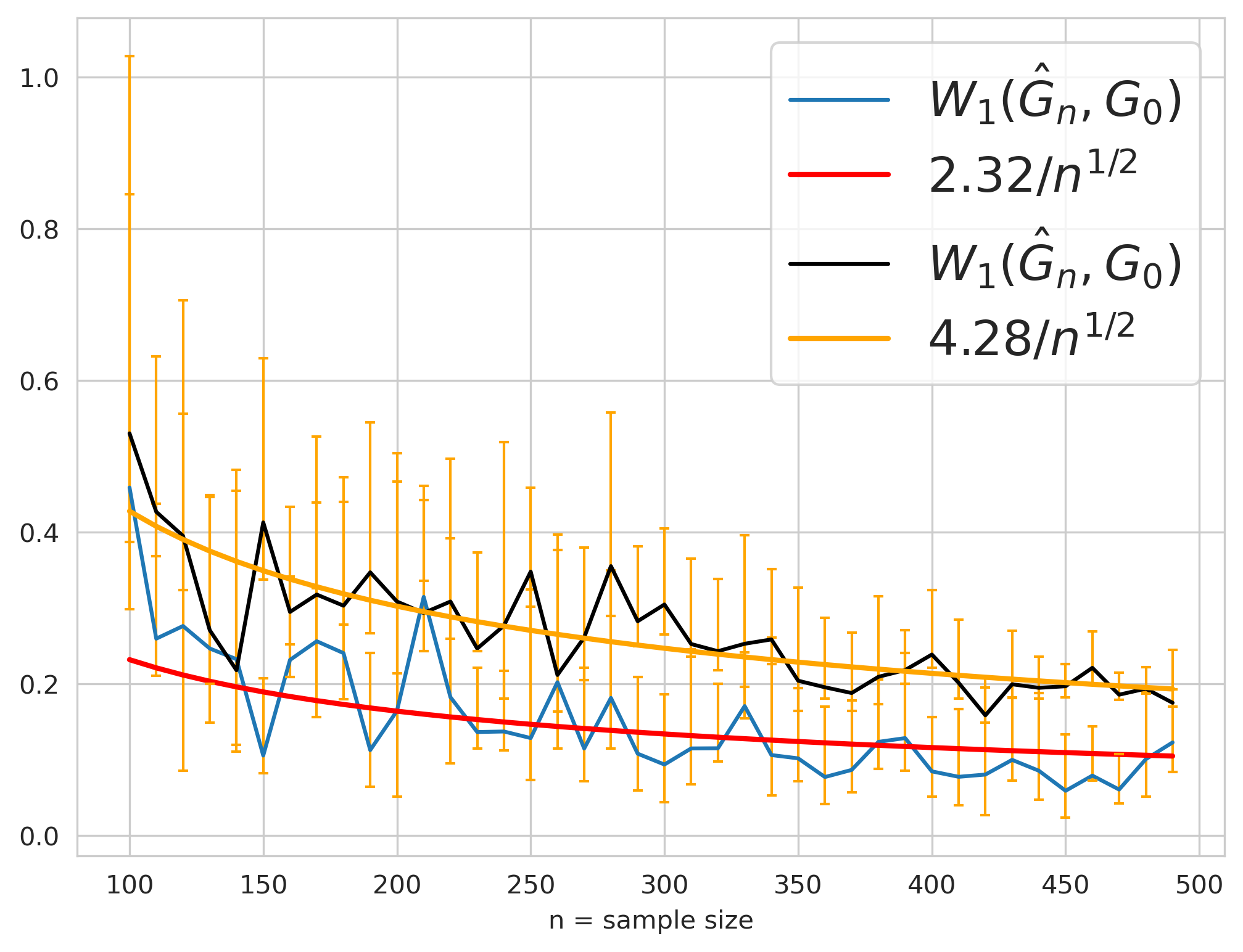

Next, we illustrate the parameter learning rates under both exact and over-fitted settings. Consider a mixture of normal regression model with a polynomial link function and fixed variance: , where . We simulate data from an uniform distribution on and then generated given from this model using , where . Because the variances of both components are known, and the link function is a polynomial, this model is strongly identifiable in the second order. The maximum (conditional) likelihood estimate of is obtained by the Expectation-Maximization (EM) algorithm . We considered two cases where the number of components of is known to be for the exact-fitted setting and set for the over-fitted setting. For each setting and each , we run the experiment times to obtain the estimation error as measured by the Wasserstein distances. In Fig. 5.2, the orange line presents the interquartile range of the 16 replicates obtained at each sample size . The error in the exact-fitted setting and the error in the over-fitted case are of order and , respectively. These results are compatible with the theoretical results established in Theorem 4.2.

(a) Convergence rate in exact-fitted case

(b) Convergence rate in over-fitted case

(c) Comparison of the two cases

Investigating the lack of strong identifiability

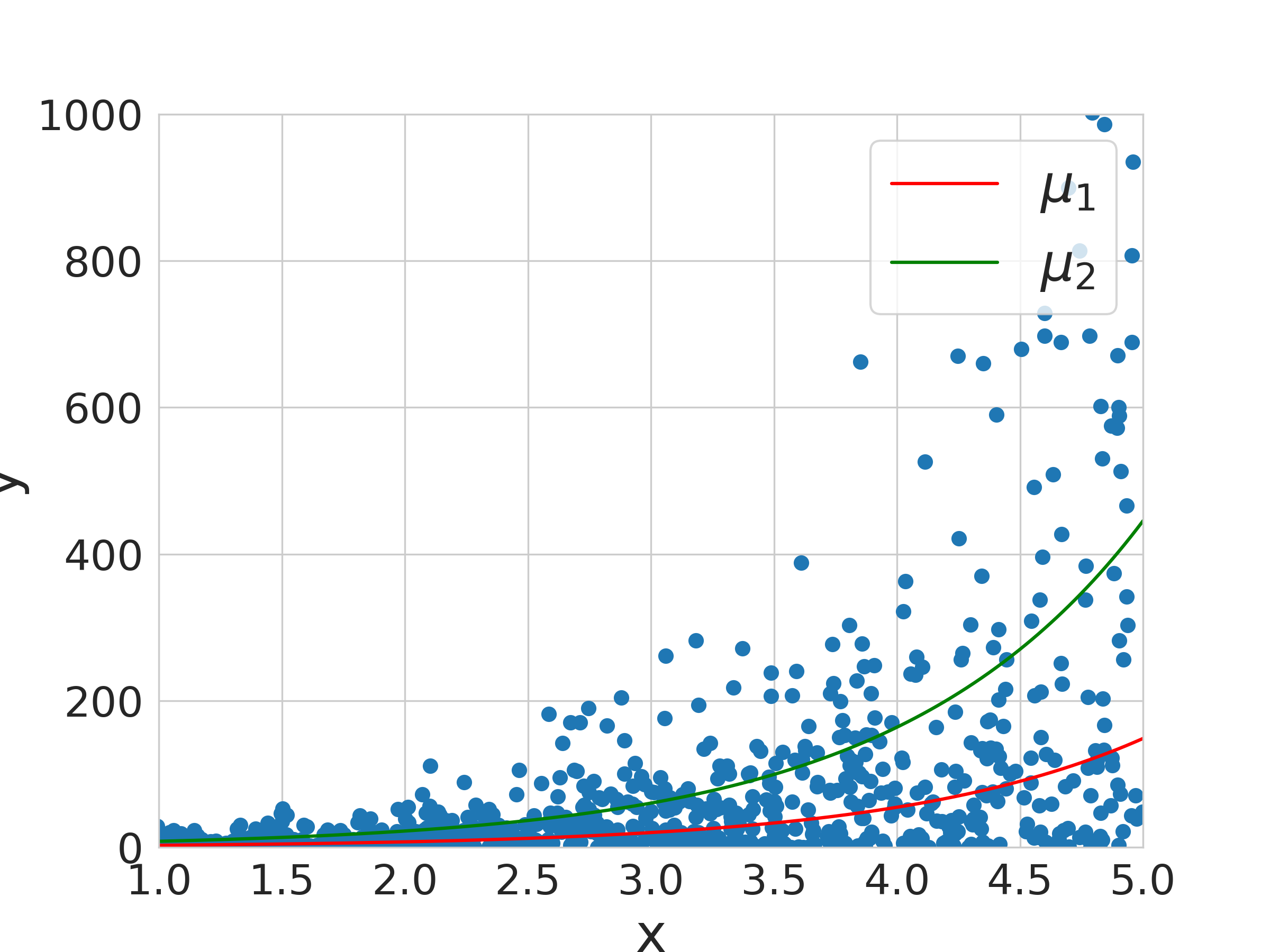

In Section 3.4, we discussed the lack of strong identifiability in the mixture of negative binomial regression models. Here, we conduct an experiment to show the posterior contraction rate of parameter estimation where the true model is not strongly identifiable (cf. Eq. (11) holds). A dataset is drawn from a negative binomial regression mixture model: , where the covariate, , is randomly generated from a uniform distribution over the interval ; the component means are , , where . The true latent mixing measure is , where the regression coefficients are , , the dispersion parameters are , and the mixing proportions are , . Under this simulation, Eq. (11) is satisfied. The simulated dataset is illustrated in Figure 5.3(a). This model is not strongly identifiable.

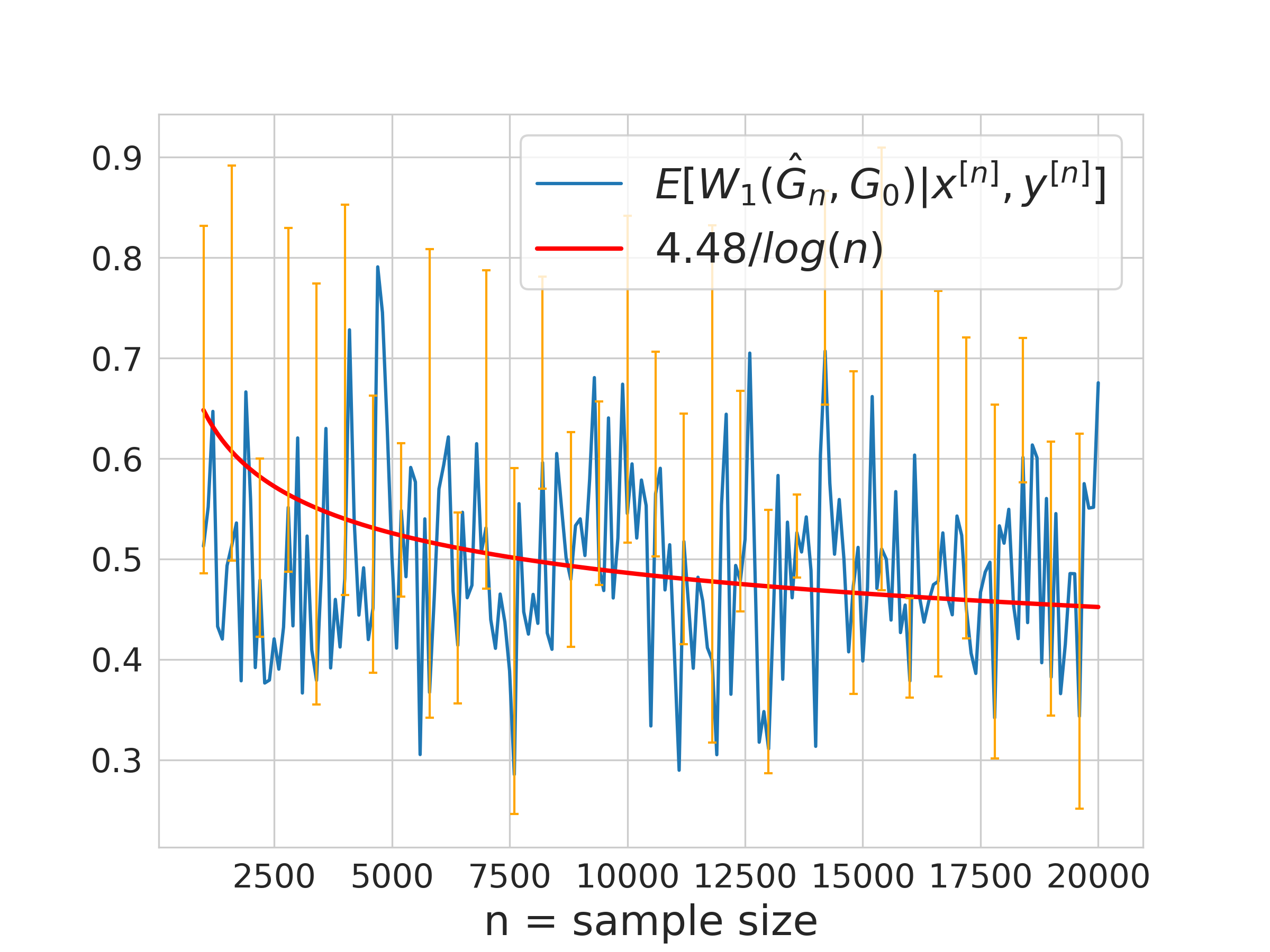

For model fitting, we adopt the Bayesian approach and consider the exact-fitted case. Let be the indicator variables such that , and . Then, we have , for and . To proceed with estimating the parameter set given the simulated data, , we investigate the posterior distributions of , and (for . Similar to [28], we choose the prior to be , (normal distribution with identity covariance matrix), and (a non-informative gamma distribution) for . The full posterior distribution is approximated using an MCMC algorithm with details given in Appendix F. For each different sample size , we run the experiment 8 times. For each time running, we produce 2500 MCMC samples, discard the first 500, and use the remaining samples to estimate the expected Wasserstein distances to . The estimation error averaged over the 8 runs is reported in Fig 5.3(b). The orange line presents an interquartile range of 8 results at each considered sample size. The error is plotted against the order . It can be seen that the error tends to reduce at an extremely slow speed, as validated by the slow minimax bound.

(a) Simulated data from a NB mixture

(b) Posterior contraction rate

Analysis of crash data

To validate the applicability of the proposed theoretical result in Section 3.2 illustrated via the simulation study above, we use the dataset collected in 1995 at urban 4-legged signalized intersections in Toronto, Canada. The same data has been explored and fitted by a mixture of negative binomial regression models by [28], where they showed the good quality of the dataset as well as the best-fitted model for it. This crash data set contains intersections, which have a total of reported crashes. In their paper, the authors explicated the heterogeneity in the dataset which came from the existence of several different sub-populations (i.e., the data collected from the different business environments, contains a mix of fixed and actuated traffic signals, and so on). Accordingly, the mean functional form has been used for each component as below:

| (16) |

where is the th component’s estimated number of crashes for intersection ; counts the entering flows in vehicles/day from the major approaches at intersection ; the entering flows in vehicles/day from the minor approaches at intersection ; and the estimated regression for component . According to [28], the best model for describing the dataset is a two-mixture of negative binomial regression where , , , .

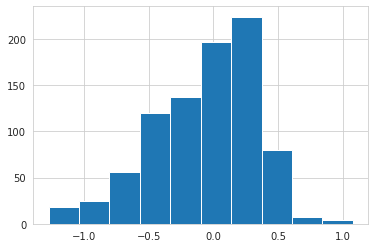

It can be seen that the two values of and nearly satisfy the second condition of the pathological case mentioned in Section 3.2 (i.e., ). If the first condition holds (i.e., ), then we would be in a singular situation. To verify this, we calculate for all samples . The histogram of this difference can be seen in Fig. 5.4(a). By the Anderson-Darling test, we see that this distribution is significantly different from the degenerate distribution at , with the calculated p-value for this test being . Hence, we are quite far from the pathological situations of non-strong identifiability. In theory, the method should still enjoy the convergence rate if the model is well-specified and exact-fitted. We further subsample this data and calculate the error of the estimator from the subsampled dataset to that of the whole dataset. For each sample size, we replicate the experiment 8 times and report the average error (in blue) and the interquartile error bar (in orange) in Fig. 5.4(b). We can see that the error is approximate of the order .

Finally, we conduct another subsampling experiment to focus on the data corresponding to . This data subset (with sample size ) represents a data population that is closer to the pathological cases of non-strong identifiability than that of the previous experiment. Note that the difference from the degenerate distribution at is still significant, so the convergence rate is still achieved in theory. In particular, the black line in Fig. 5.4(b) represents the average errors in this case after an 8-time running of the experiment. A noteworthy observation is that the closer the data population is to a pathological situation, the slower the actual convergence to the true parameters will be. This result provides an interesting demonstration of the population theory given in the previous section.

(a) Histogram of difference

(b) The blue line corresponds to the original data while the black line to subsamples chosen near a pathological situation.

6 Conclusion

We developed a strong identifiability theory for general finite mixture of regression models and derived rates of convergence for density estimation and parameter estimation in both Bayesian and MLE frameworks. This theory was shown to be applicable to a wide range of models employed in practice. It also invites interesting new questions. First, in our models mixture weights ’s do not vary with covarate . It would be interesting to extend the theory to the situation of co-varying weights. Second, while our theory is applicable to the case of unknown but finite number of mixture components, it remains challenging to extend such a theory for infinite conditional mixtures motivated from Bayesian nonparametrics [27, 14]. Finally, as demonstrated with the negative binomial mixtures, although the singularity situation (i.e., strong identifiability is violated) is rare, being in the vicinity of a singular model can be a far more common scenario. We would like to investigate more precisely the impact on parameter estimates when the true model is in the vicinity of a singular model, and to provide suitable statistical methods to overcome the inefficiency of inference in such situations.

Acknowledgments

This work is supported in part by the NSF Grant DMS-2015361 and a research gift from Wells Fargo.

References

- [1] Lluís Bermúdez, Dimitris Karlis, and Isabel Morillo. Modelling unobserved heterogeneity in claim counts using finite mixture models. Risks, 8(1):10, 2020.

- [2] Jiahua Chen. Optimal rate of convergence for finite mixture models. The Annals of Statistics, pages 221–233, 1995.

- [3] Wayne S DeSarbo and William L Cron. A maximum likelihood methodology for clusterwise linear regression. Journal of classification, 5(2):249–282, 1988.

- [4] Cody S Ding. Using regression mixture analysis in educational research. Practical Assessment, Research, and Evaluation, 11(1):11, 2006.

- [5] Dat Do, Nhat Ho, and XuanLong Nguyen. Beyond black box densities: Parameter learning for the deviated components. arXiv preprint arXiv:2202.02651, 2022.

- [6] Joseph L Doob. Application of the theory of martingales. Le calcul des probabilites et ses applications, pages 23–27, 1949.

- [7] Subhashis Ghosal and Aad Van der Vaart. Fundamentals of nonparametric Bayesian inference, volume 44. Cambridge University Press, 2017.

- [8] Subhashis Ghosal and Aad W Van Der Vaart. Entropies and rates of convergence for maximum likelihood and bayes estimation for mixtures of normal densities. The Annals of Statistics, 29(5):1233–1263, 2001.

- [9] Evarist Giné and Richard Nickl. Mathematical foundations of infinite-dimensional statistical models. Cambridge university press, 2021.

- [10] Stephen M. Goldfeld and Richard E. Quandt. A markov model for switching regressions. Journal of Econometrics, 1(1):3–15, 1973.

- [11] Bettina Grün and Friedrich Leisch. Finite mixtures of generalized linear regression models. In Recent advances in linear models and related areas, pages 205–230. Springer, 2008.

- [12] Bettina Grün and Friedrich Leisch. Identifiability of finite mixtures of multinomial logit models with varying and fixed effects. Journal of classification, 25(2):225–247, 2008.

- [13] Hennig and Christian. Identifiablity of models for clusterwise linear regression. Journal of classification, 17(2), 2000.

- [14] N. Hjort, C. Holmes, P. Mueller, and S. Walker. Bayesian Nonparametrics: Principles and Practice. Cambridge University Press, 2010.

- [15] N. Ho and X. Nguyen. Convergence rates of parameter estimation for some weakly identifiable finite mixtures. Annals of Statistics, 44:2726–2755, 2016.

- [16] N. Ho and X. Nguyen. On strong identifiability and convergence rates of parameter estimation in finite mixtures. Electronic Journal of Statistics, 10:271–307, 2016.

- [17] Nhat Ho and XuanLong Nguyen. Singularity structures and impacts on parameter estimation in finite mixtures of distributions. SIAM Journal on Mathematics of Data Science, 1(4):730–758, 2019.

- [18] Nhat Ho, Chiao-Yu Yang, and Michael I Jordan. Convergence rates for gaussian mixtures of experts. arXiv preprint arXiv:1907.04377, 2019.

- [19] Merrilee Hurn, Ana Justel, and Christian P Robert. Estimating mixtures of regressions. Journal of computational and graphical statistics, 12(1):55–79, 2003.

- [20] Robert A Jacobs, Michael I Jordan, Steven J Nowlan, and Geoffrey E Hinton. Adaptive mixtures of local experts. Neural computation, 3(1):79–87, 1991.

- [21] Thomas Jaki, Minjung Kim, Andrea Lamont, Melissa George, Chi Chang, Daniel Feaster, and M Lee Van Horn. The effects of sample size on the estimation of regression mixture models. Educational and Psychological Measurement, 79(2):358–384, 2019.

- [22] Wenxin Jiang and Martin A Tanner. On the identifiability of mixtures-of-experts. Neural Networks, 12(9):1253–1258, 1999.

- [23] Abbas Khalili and Jiahua Chen. Variable selection in finite mixture of regression models. Journal of the american Statistical association, 102(479):1025–1038, 2007.

- [24] J. W. Miller and M. T. Harrison. Mixture models with a prior on the number of components. Journal of the American Statistical Association, 113, 2018.

- [25] Jeffrey W Miller. A detailed treatment of doob’s theorem. arXiv preprint arXiv:1801.03122, 2018.

- [26] Chipo Mufudza and Hamza Erol. Poisson mixture regression models for heart disease prediction. Computational and Mathematical Methods in Medicine, 2016, 2016.

- [27] XuanLong Nguyen. Convergence of latent mixing measures in finite and infinite mixture models. The Annals of Statistics, 41(1):370–400, 2013.

- [28] Byung-Jung Park and Dominique Lord. Application of finite mixture models for vehicle crash data analysis. Accident Analysis and Prevention, 41(4):683–691, 2009.

- [29] Byung-Jung Park, Dominique Lord, and Jeffrey D Hart. Bias properties of bayesian statistics in finite mixture of negative binomial regression models in crash data analysis. Accident Analysis and Prevention, 42(2):741–749, 2010.

- [30] S. N. Rai and D. E. Matthews. Improving the em algorithm. Biometrics, 49(2):587–591, 1993.

- [31] Marko Sarstedt and Manfred Schwaiger. Model selection in mixture regression analysis–a monte carlo simulation study. In Data analysis, machine learning and applications, pages 61–68. Springer, 2008.

- [32] Helmuth Späth. Algorithm 39 clusterwise linear regression. Computing, 22(4):367–373, 1979.

- [33] Elias M Stein and Rami Shakarchi. Complex analysis, volume 2. Princeton University Press, 2010.

- [34] Henry Teicher. Identifiability of finite mixtures. The annals of Mathematical statistics, pages 1265–1269, 1963.

- [35] S. van de Geer. Empirical Processes in M-estimation. Cambridge University Press, 2000.

- [36] Kert Viele and Barbara Tong. Modeling with mixtures of linear regressions. Statistics and Computing, 12(4):315–330, 2002.

- [37] Shaoli Wang, Weixin Yao, and Mian Huang. A note on the identifiability of nonparametric and semiparametric mixtures of glms. Statistics and Probability Letters, 93:41–45, 2014.

- [38] Yun Wei and XuanLong Nguyen. Convergence of de finetti’s mixing measure in latent structure models for observed exchangeable sequences. arXiv preprint arXiv:2004.05542, 2020.

- [39] Wing Hung Wong and Xiaotong Shen. Probability inequalities for likelihood ratios and convergence rates of sieve mles. The Annals of Statistics, pages 339–362, 1995.

- [40] Bin Yu. Assouad, fano, and le cam. In Festschrift for Lucien Le Cam, pages 423–435. Springer, 1997.

Supplement to "Strong identifiability and parameter learning in regression with heterogeneous response"

In the supplementary material, we collect the proofs and additional information deferred from the main text. Section A includes the proofs for all main theoretical results. Section B includes the proofs for all remaining theoretical results. Section C and Section D provide a general theory of M-estimators convergence rates and posterior contraction rates in the regression setting, respectively. The EM algorithms for mixtures of regression are described in Section E.

Appendix A Proofs of main results

A.1 Identifiablity conditions and inverse bounds

Proof of Theorem 3.1.

We will divide the proof into first order and second order identifiability cases.

The case :

For some , suppose that there exist distinct elements , and as such that for almost all (w.r.t. )

then we want to show that for . Indeed, by the chain rule, the left-hand side of the above expression is equal to

Because of the identifiability of (condition (A4.)), there exists a set with such that are distinct. Therefore, by the first order identifiability of , we have

for all (possibly except a zero-measure set). Hence, by condition (A5.), we have for all . This concludes the first-order identifiability of the family of conditional densities .

The case :

For any , given distinct elements , , if there exist , and as and such that for almost all (w.r.t. )

then we want to show that for . Indeed, again, by the chain rule, the expression above is equivalent to

| (17) |

Because of the identifiability of (condition (A4.)), there exists a set with such that are distinct. By the second-order identifiability of , then we have

for all , possibly except a zero-measure set. Hence, by condition (A5.), from the third and fifth equation above, we have for all . These together with the second and fourth equation further imply that for all . We arrive at the second-order identifiability of family of conditional densities as desired. ∎

Proof of Theorem 3.2.

In order to prove part (a) of the theorem, we divide it into two regimes, local and global, and establish two following claims: for any ,

| (18) |

| (19) |

Proof of claim (18):

Suppose that this is not true, that is, there exists a sequence such that for all and as ,

This implies . Since , and are compact, there exists a subsequence of (which is assumed to be itself without loss of generality) that converges weakly to some , where are distinct. Hence, , and . Because for all , this implies

which means

By the zero-order identifiability of , we conclude that

| (20) |

If family is identifiable, then we argue that the set must equal . Otherwise, we can assume (without loss of generality) that , which means there exists a set with such that is distinct from any pair among for all . But this contradicts (20), because the left-hand side put a positive weight to the atom , which the right-hand side does not have. Hence, we have the set equals . Now, without loss of generality, we can assign . Because are distinct, there exists such that

are distinct, which together with Eq. (20) entail that for all . Thus, , while , a contradiction. Hence, claim (18) is proved.

Proof of claim (19):

Suppose this does not hold. Then there exists a sequence such that

| (21) |

We can relabel the atoms and weights of such that it admits the following form:

| (22) |

where , and for all . To ease the ensuing presentation, we denote , and for . Then, using the coupling between and such that it put mass on , we can verify that

| (23) |

The remainder of the proof is composed of three steps.

Step 1

(Taylor expansion) To ease the notation, we write for short

and

for all . Because is differentiable with respect to for all , by applying Taylor expansion up to the first order and the chain rule, we find that for all ,

where is Taylor remainder such that for . Combine the above expression for , we have

| (24) |

where . From Eq. (23), we have as for all .

Step 2

(Extracting non-vanishing coefficients) From Eq. (21) and (23), we have that

| (25) |

We can write

| (26) |

where , and . From the definition of , we have

therefore is in , is in and is in , by compactness of those sets, there exist subsequences of , and (without loss of generality, we assume it is the whole sequence itself) such that as for all . As , at least one of them is not zero.

Step 3

(Deriving contradiction via Fatou’s lemma) By Fatou’s lemma, we have

Since , we have

| (27) |

where at least one of are not 0. But by the identifiability of family of conditional densities (condition (A1.)), we have , and . Hence, we arrive at a contradiction and conclude claim (19).

For part (b) of the theorem, in a similar spirit we can achieve the conclusion by proving the following claims:

| (28) |

for any , and

| (29) |

The proof of claim (28) is similar to that of claim (18) and is omitted. Now we proceed to prove claim (29). Suppose this does not hold. So there exists a sequence such that

| (30) |

We can assume that all have the same number of atoms (by extracting a subsequence if needed) and relabel the atoms and weights of such that it admits the following form:

| (31) |

where , and for all , for all , and are distinct. For all , we denote , , and . We have

| (32) |

As in part (a) the remainder of the proof is divided into three steps.

Step 1

(Taylor expansion) To ease the notation, we write for short

for all . Because is differentiable up to the second order with respect to for all , by applying Taylor expansion up to the second order and the chain rule, we find that

where is Taylor remainder such that for . Therefore,

| (33) |

where . From the expression in Eq. (32), we have as for all .

Step 2

(Extracting non-vanishing coefficients) From Eq. (30) and (32), we have that

| (34) |

We can write

| (35) |

where

and

for all . From the definition of , we have

so that is always bounded below by for all , and does not converge to 0. Denote

for all . By compactness and subsequence argument, we can have that and , and as for all , and at least one of those limits is not zero.

Step 3

(Deriving contradiction via Fatou’s lemma) By Fatou’s lemma, we have

Since , the integrand in the right hand side of the above display is 0 for almost all . By the second order identifiability of , all the coefficients are 0, which contradicts with the fact derived in the end of Step 2. We arrive at the conclusion of claim (29).

∎

Proof of Proposition 3.2.

We want to prove that for and being completely identifiable, then for any and distinct pairs we have

are distinct almost surely. For any , because , we have either or . By the complete identifiability of and , we have either

or

Hence,

Now consider the set

we have

Therefore, are distinct on , where . ∎

Proof of Proposition 3.4.

(a) This comes directly from the fact that if and are Lipschitz. For any , we have

and

for any and all , where and are constants which only depend on and . Hence, for any coupling of and , we have

for and for all . Taking infimum with respect to the LHS, we have

Taking the expectation with respect to we obtain

(b) For any coupling of and we have

Taking infimum of all feasible , this implies

Doing similarly for , we have the conclusion. ∎

A.2 Convergence rates for conditional density estimation and parameter estimation

Firstly, we combine the inverse bounds (Theorem 3.2) with the convergence theory for density estimation to derive convergence rates for parameter estimation that arise in regression mixture models as presented in Theorem 4.2.

Proof of Theorem 4.2.

Recall that with the assumptions in this theorem, we have

and for any ,

for only depend on , and . Besides,

Combining these inequalities with the concentration inequality given in Theorem 4.1 to have

for the exact-fitted setting, since . In the over-fitted setting, a similar argument yields

∎

Next, we proceed to prove Theorem 4.3 which is concerned with the convergence rates of conditional density estimation.

Proof of Theorem 4.3.

The proof is a generalization of proof of Theorem 3.1 in [8]. First we prove that if for any fixed and for all , these claims hold

| (36) | ||||

| (37) |

then by applying Theorem 4.1, we can arrive at our conclusion. Indeed, since

for all densities , we have

for all . Thus, we can bound the bracketing entropy integral as follows

Hence, if we choose , then , is a non-increasing function, and for , we have

Therefore, the result of Theorem 4.1 says that there exist constant and such that

which is the conclusion. It remains to verify (36) and (37).

Proof of claim (36)

Since and are compact, for all , there exists a -net of and of with the cardinality and . We also know that there exists a -net for such that ([8]). We consider the following subset of

We can see that

For any , there exist and such that and for all . Let and , by triangle inequality, we have

where we apply the assumptions that is bounded uniformly in , and the uniform Lipschitz of and . Hence forms a -net of . This implies that

Taking the logarithm of both sides, we arrive at the conclusion of claim (36).

Proof of claim (37)

We first construct an -bracketing for under norm. Let be a small number that we can choose later, and is a -net for under , for . Denote by an upper bound for for all . From our assumptions, we can construct an envelope for as follows

where we can assume that and . Then, we can create the brackets by

Because for all , we have a such that , it can be seen that for all . Therefore, . Besides, for any and , we have

| (38) |

where we use the change of variable formula , and the fact that when is the Lebesgue measure:

for all . Notice that if is a probability mass function (i.e., is discrete), we can change the integral to sum, and the result still holds because

Now, let , we have

where . Hence, there exists a positive constant which does not depend on such that

Let , we have . Combining with inequality yields

Thus, we have proved claim (37). ∎

Finally, we obtain upper bounds on the tail probability for some popular family of distributions in order to verify that they satisfy all conditions of Theorem 4.1.

Proof of Proposition 4.1.

Since the parameter space is compact, we can assume it is a subset of some , where and . If the family of distribution is discrete, then obviously its probability mass function is bounded uniformly by 1.

(a) For the family of normal distribution , we have that

| (39) |

for all or .

(b) For the family of Binomial distribution , we can see that it is discrete and domain of is bounded. Therefore the conclusion is immediate.

(c) For the family of Poisson distribution , we have that and

for all due to the inequality .

(d) For the family of negative binomial distribution , we also have , and

for all large enough compared to and . ∎

A.3 Posterior contraction theorems

Proof of Theorem 4.5.

Checking condition (i):

We need to show that the prior distribution puts enough mass around the true (conditional) density function , i.e., to obtain a lower bound for . First, consider the ball for a constant to be chosen later. By Lemma 2.1, we have , where depends on . Because for all sufficiently large , we have . By Theorem 5 in [39], we have

Hence, for , we have

However, for all such that , we have

Due to assumption (B1.), the prior measure of this set is asymptotically greater than Hence

as .

Checking condition (ii):

We need to provide an upper bound for the entropy number . By Lemma 2.1,

We use the same strategy as in the proof of Theorem 4.3. Since and are compact, for all , there exists an -net of and of with the cardinality and . Moreover, there exists an -net for such that . We consider the following subset of

Note that

For any , there exist and such that and , for all . Let and , by the triangle inequality, we have

This implies that the covering number

Taking logarithm of both sides, we obtain . Now, we are ready to apply Theorem D.1 to conclude the proof. ∎

Proof of Theorem 4.6.

Now we are to establish the consistency of the number of parameters and the posterior contraction rate of the latent mixing measure in a Bayesian estimation setting, where the regression mixture model is endowed with a "mixture of finite mixture" prior. The proof makes a crucial usage of Doob’s consistency theorem ([7] Theorem 6.9, or [25] Theorem 2.2).

Proof of Theorem 4.7.

For each latent mixing measure , we write as its number of (distinct) support points. Recall that we have a prior on , which is a subset of the complete and separable Wasserstein space endowed with metric . By assumption, (and hence ) is identifiable. By Doob’s consistency theorem [6] (or [7] Theorem 6.9), there exists such that and for any , i.e. those that that have supporting atoms, we have

almost surely in . For the mixture of finite mixtures prior, represents the (random) number of components. Moreover, by assumption, given , the prior distributions on and are absolutely continuous, and set . Thus, under the induced prior on the mixing measure, we have for -almost all . This entails that there exists such that and for any we have

Now, for any , by the calculus of probabilities

Thus, , provided that . Then, with , we can bound:

The first term goes to 0 -almost surely, thanks to the argument above. For the second term, we apply the first part of Theorem 4.6 to conclude that it tends to 0 in -probability.

∎

Appendix B Proofs of remaining main results

B.1 Basic inequalities

Proof of Lemma 2.1.

Let and recall that . To ease the presentation, denote and for . We have

for any coupling of and . But because of the uniform Lipschitz assumption of and , we have

and then

Therefore,

for all . Taking infimum of all feasible to obtain

∎

Remark B.1.

By inspecting the proof above, we see that the results still hold if we change the uniform Lipschitz condition of and to the integrability of the Lipschitz constants, i.e. there exist for all such that

for all , and . This condition is weaker than the uniformly Lipschitz condition in .

B.2 Identifiability results

Proof of Proposition 3.1.

(c) First, we will establish the first order identifiability condition when . Suppose that are distinct and there exist , such that

| (40) |

for all . Direct calculation gives

| (41) |

Because this is a system of linear equations of , it suffices to show that the following matrix has independent columns

Multiplying this matrix with the following upper triangular matrix

we only need to prove the following matrix

has independent columns. Because , it suffices to prove that , for

| (42) |

In the following, we will prove that , so that it is different from 0 if are distinct as in our assumption. We borrow an idea in calculating the determinant of the Vandermonde matrix. Note that is a polynomial of , with the degree of each no more than . Let us treat as a variable, while as constants, and prove that

is a polynomial having degree of and can be factorized as . It suffices for us to show all attains as solutions, and similar for other ’s. It can be seen that is a determinant of a matrix with identical first two columns, therefore . For the derivative of , we use the derivative rule for product to have that equals

As the first matrix has identical first and -th columns, its determinant equals 0. Hence, equals

Now consider . It is the determinant of a matrix that has identical first two columns, so . Continuing to apply the derivative rule for products of functions, we have that equals

Substitute in the formula above, the first matrix has identical first and -th column, and the second matrix has identical first two columns. Hence, . Continue applying derivative one more time, we have equals

The first matrix has two identical columns, so its determinant is 0. Meanwhile, when we substitute into the other three matrices, each also has identical columns. Hence, . We obtain that . By treating as variables respectively and applying the same argument, we have

whenever are distinct.

The proof for establishing the second order identifiability when is similar, where the determinant of the derived matrix is .

(d) For the family of negative binomial distributions, the density is given as

Suppose that are distinct, and there exist such that for every

| (43) |

We will show that . Indeed, Eq. (43) is simplified as below

| (44) |

for all . Without loss of generality, assume is the largest value in the set of . This implies that is also the largest value in the set of . Dividing both sides of Eq. (B.2) by , we obtain

| (45) |

Let in (B.2), we get . After dropping in (B.2), the remaining terms of the equation is divided by , we have

| (46) |

Taking the limit both sides of Eq. (B.2), we get . Continuing this procedure, we set and in Eq. (43), then divide on both sides of the remaining equation. The final result leads to the following:

| (47) |

It is clear to see that when approaches in Eq. (B.2). We have shown that . Inductively, we obtain that for . ∎

Proof of Proposition 3.3.

Since is absolutely continuous with respect to the Lebesgue measure on , it is sufficient to prove the result in this proposition with respect to the Lebesgue measure.

(a) We will prove this part by applying an inductive argument with respect to (dimension of covariate ). Suppose . For , the equation is a non-trivial polynomial equation, it only has a finite number of solutions. Thus the set of solution has Lebesgue measure zero, so we have a.s.

Assume now that the proposition is valid up to the parameter space dimension . Now we prove that it is correct for . Using a similar argument as above, it suffices to show that the set of solutions for any non-trivial polynomial has zero measure. Indeed, consider any such polynomial of degree of variable , we can write , where and . The polynomial then can be written as :

| (48) |

where are polynomial of , at least one of which is non-trivial.

Now, partition the set of the solutions for this polynomial into two measurable sets , where

The Lebesgue measure of set is using the induction hypothesis. While for any in set , for each such , there exist only a finite number of to satisfy (48), which has zero Lebesgue measure in . Therefore, we can use Fubini’s theorem to deduce that the measure of is also zero. Thus, has measure zero. We have established that is completely identifiable for any polynomial .

Turning to the verification of Assumption (A5.), since is again a non-trivial polynomial of , (A5.) is also satisfied using the same argument above.

(b) Similar to part (a), we only need to prove that a non-trivial (not all coefficients are 0) trigonometric polynomial of :

| (49) |

has a countable number of solutions. Write , where is the imaginary unit, we can rewrite a non-trivial trigonometric polynomial above as

| (50) |

where and are computed from , and the tuple is non-trivial. Set , this becomes a polynomial in , which has a finite number of solutions, by the fundamental theorem of algebra. Combining this with the fact that only has a countable solution in , we arrive at the conclusion. The condition spelled out in Assumption (A5.) also holds because the derivative of a trigonometric polynomial is still of the same form.

(c) Similar to above, we express a non-trivial mixture of polynomials and trigonometric polynomials in the form:

| (51) |

which is a holomorphic function in . This function is known to have an isolated set of solutions, which has zero measure [33]. Thus, these functions are completely identifiable. Conditions in Assumption (A5.) also follow because the derivative of a function of this type is still of the same form.

(d) Given , where is diffeomorphic.

To verify the complete identifiability condition, it can be seen that for : , so that the complete identifiability of can be deduced from what of .

To verify Assumption (A5.), note that . Since (as is a diffeomorphism), the two equations below are equivalent.

Hence, satisfies assumption (A5.) if does.

∎

The following result illustrates the discussion in Section 5 by showing that a mixture of binomial regression model may be strongly identifiable even though the (unconditional) mixture of binomial distributions is not identifiable in even in the classical sense.

Proposition B.1.

Suppose that the link function for , and the density kernel , where . Moreover, the support of contains an open set in . Then, the mixture of two binomial regression components associated with the mixing measure , where , is strongly identifiable in the first order.

Proof.

Consider . Suppose that for some we have

for all . Then we will show that . Denote , we have . Besides, , so that

| (52) |

and

| (53) |

Because Eq. (53) satisfies for all in an open set, and it is an analytic function of , it satisfies for all (identity theorem) [33]. Without the loss of generality, we assume . If , then by dividing both sides of Eq. (53) by , one obtains

Let , we have or (depending on whether or ) and all other terms go to 0. Hence . Next, dividing both sides of Eq. (53) by , one obtains

Let , we have . Therefore,

which implies . In the other case where , we let in Eq. (53) and notice that then . Similarly let , we have . Then Eq. (53) becomes

But notice that , so by letting , we are back to the case . Similar to the case , we can transform to go back to the first case (because Eq. (53) satisfies for all ). Hence, in all cases we have . Hence, strong identifiability in the first order is established. ∎

Remark B.2.

-

1.

The fact that mixture of Binomial distributions is not identifiable in general can be seen from a simple example: for all valid . That is also the reason why one cannot include the intercept parameter in the definition of in the proposition above.

-

2.

The proof technique of this proposition is to perform analytic continuation so that the identifiability equation satisfies for all then we can examine the limits . Extending this proof technique mixture of more components (more than 2) is generally more challenging because several components can have the same limit as . We once more highlight the usefulness of Theorem 3.1 and Theorem 3.2 for providing the guarantee for a large class of identifiable mixture densities.

B.3 Minimax bound for mean-dispersion negative binomial regression mixtures

Proof of Theorem 3.3.

Step 1. We will prove that for any there exist and a sequence such that:

| (54) |

Intuitively, we want to choose to be in the pathological case described in equation (10). In particular, choose where such that for all . Let , we have . A combination of chain rule with equation (10) yields:

| (55) | ||||

for all . Now, choose a sequence such that for all ; , for all ; and for all . It can be checked that

Meanwhile, using Taylor’s expansion up to second order with integral remainder, we have