Finding the Right Curve:

Optimal Design of Constant Function Market Makers

Abstract.

Constant Function Market Makers (CFMMs) are a tool for creating exchange markets, have been deployed effectively in prediction markets, and are now especially prominent in the Decentralized Finance ecosystem. We show that for any set of beliefs about future asset prices, an optimal CFMM trading function exists that maximizes the fraction of trades that a CFMM can settle. We formulate a convex program to compute this optimal trading function. This program, therefore, gives a tractable framework for market-makers to compile their belief function on the future prices of the underlying assets into the trading function of a maximally capital-efficient CFMM.

Our convex optimization framework further extends to capture the tradeoffs between fee revenue, arbitrage loss, and opportunity costs of liquidity providers. Analyzing the program shows how the consideration of profit and loss leads to a qualitatively different optimal trading function. Our model additionally explains the diversity of CFMM designs that appear in practice. We show that careful analysis of our convex program enables inference of a market-maker’s beliefs about future asset prices, and show that these beliefs mirror the folklore intuition for several widely used CFMMs. Developing the program requires a new notion of the liquidity of a CFMM, and the core technical challenge is in the analysis of the KKT conditions of an optimization over an infinite-dimensional Banach space.

1. Introduction

Agents in any economic system need to be able to exchange one asset for another efficiently. Some assets are frequently traded by many market participants, and for these assets, a seller offering a reasonable price can likely find a buyer quickly and vice versa. However, not every pair of assets is traded frequently, and sellers in these markets might have to wait a long time to find a buyer or accept a highly unfavourable price. The role of a market-maker is to fill this gap — to facilitate easy and rapid trading between pairs of assets for which otherwise there is very little trading activity. Market-makers trade in both directions on the market, buying and selling assets when traders arrive at the market (amihud1980dealership, ). In this sense, market-makers facilitate asynchronous trading between buyers and sellers, thereby increasing the market liquidity between two assets.

Our topic of study is a subclass of automated market-making strategies known as Constant Function Market Makers (CFMMs). A CFMM maintains reserves of two assets and provided by a so-called liquidity provider (LP), and makes trades according to a predefined trading function of its asset reserves (the eponymous "constant function"); specifically, a CFMM accepts a trade from reserves to if and only if . CFMMs earn revenue by charging a small commission on each trade (i.e. creating a bid-ask spread) but are subject to several associated expenses (amihud1986asset, ), such as the costs of maintaining the asset inventory and adverse selection by arbitrageurs (i.e., stale quote sniping). The loss of the LP relative to the counterfactual strategy of “buy-and-hold” is referred to as the “divergence loss” (milionis2022automated, ).

Automated market-making has long been an important topic of study (aoyagi2020liquidity, ; gerig2010automated, ; othman2013practical, ), but CFMMs have recently become some of the most widely used exchanges (uniswapv2, ; uniswapv3, ; balancer, ; egorov2019stableswap, ) within the modern Decentralized Finance (DeFi) ecosystem (werner2021sok, ). The success of CFMMs in DeFi is primarily due to their ability to run via smart contracts (mohanta2018overview, ) with a fairly low computation requirement on blockchains. CFMMs also reduce the barrier to entering the liquidity provision business or “market-making” (ammdemocratize, ). CFMMs have also been widely deployed in prediction markets as a method for aggregating opinions (hanson2007logarithmic, ; chen2010new, ). For completeness, we describe the precise translation from market scoring rules studied in the prediction markets literature to CFMMs in Appendix §A.

Example 1.1 (Real-world CFMMs).

-

(1)

The decentralized exchange Uniswap (uniswapv2, ) uses the product function .

-

(2)

The Logarithmic Market Scoring Rule (LMSR) (hanson2007logarithmic, ), used extensively to design prediction markets, corresponds to a CFMM with trading function (univ3paradigm, ).

-

(3)

The trading function has powered automated storefronts in online games (hyperconomy, ).

Despite facilitating billions of US dollars worth of trade volume per day, a complete formal understanding of CFMM design trade-offs is missing in the literature. Our goal, therefore, is to explain what guides a CFMM designer to choose one trading function over another. We provide an optimization framework which compiles a market-maker’s beliefs on future prices into an optimal CFMM trading function, making substantial progress towards an important open problem (timtweet, ).

1.1. Our Contributions

We develop a convex optimization framework that translates an LP’s beliefs about future asset valuations into an optimal choice of CFMM trading function. We show that a unique trading function always maximizes an LP’s expectation of the fraction of trades that a CFMM can settle (§3.2). Furthermore, our framework is versatile such that it can model a wide variety of real-world concerns, including fee revenue (§6), divergence loss (§6.2.1), so-called “Loss-Versus-Rebalancing” (milionis2022automated, ) (§6.2.2), and models of price dynamics (§3.4). To the best of our knowledge, this is the first unified framework for analysing and optimizing CFMMs for various objectives for a given belief function and therefore provides a guide to prospective LPs interested in using a CFMM.

We model an LP’s beliefs as a joint distribution on the future prices of the two assets with regard to a numeraire (§5). This belief could, for example, be generated from a price dynamics model. As one might expect, the optimization problem concerned only with maximizing the fraction of trades settled depends only on the distribution of the ratio of prices. However, expressing beliefs on future prices as a joint distribution enables optimizing for profit and loss through the same framework.

We measure the liquidity of the CFMM trading function as the amount of capital implicitly allocated for market-making at a given spot exchange rate. Specifically, the liquidity of a CFMM is the ratio between the size of a trade and the percentage change in the spot exchange rate (§3.1).

We analyze the steady-state dynamics of trade requests on a CFMM and arrive at a notion of “CFMM inefficiency” that approximates the probability that a CFMM cannot satisfy a trade request. CFMM inefficiency is a function of the inverse of the CFMM’s liquidity. Ultimately, we find that more complex objective functions considering an LP’s profit and loss become linear combinations of CFMM liquidity and CFMM inefficiency.

Careful analysis of the KKT conditions of our convex program allows us to invert the problem; given an arbitrary CFMM trading function, we can construct an explicit equivalence class of beliefs for which the given function is optimal. The main technique involves analysis of the KKT conditions of an optimization problem over an infinite-dimensional Banach space. We obtain closed-form solutions to the optimal CFMM designs for several important belief functions and objective functions. When not closed-form, the solution is still computationally tractable.

Our framework helps explain the choice of CFMM trading functions deployed in practice. In many cases, the optimal CFMM revealed by our framework matches the informal intuitions of practitioners. For example, the Uniswap V2 (uniswapv2, ) protocol in DeFi was designed using the constant product CFMM with the motivation that the available liquidity must be spread evenly across all exchange rates. In our framework, is the optimal CFMM trading function for the uniform belief function with the objective of minimising the expected CFMM inefficiency.

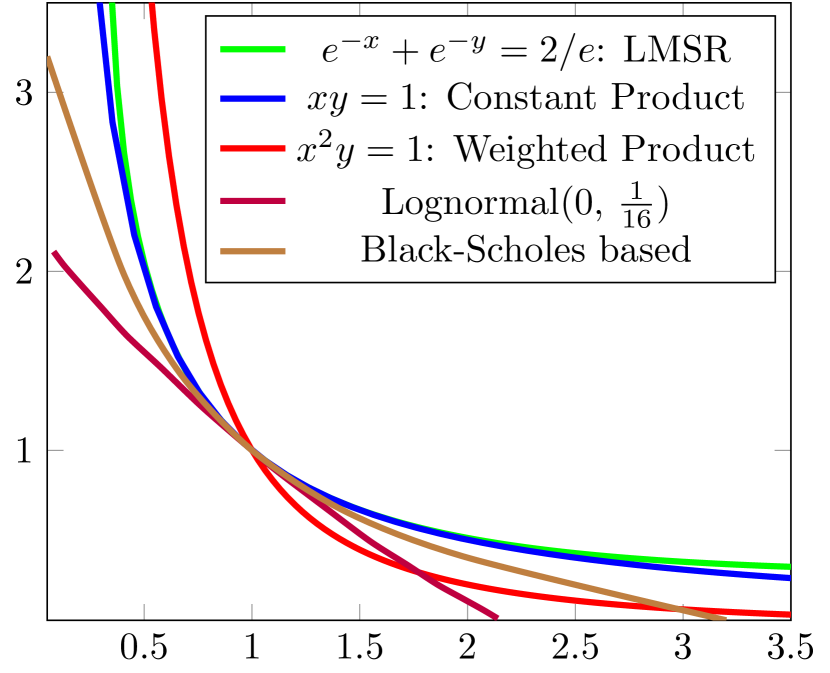

| CFMM | Trading Function | Liquidity | Belief |

| Constant product | 1 | ||

| Constant weighted product | |||

| LMSR based | |||

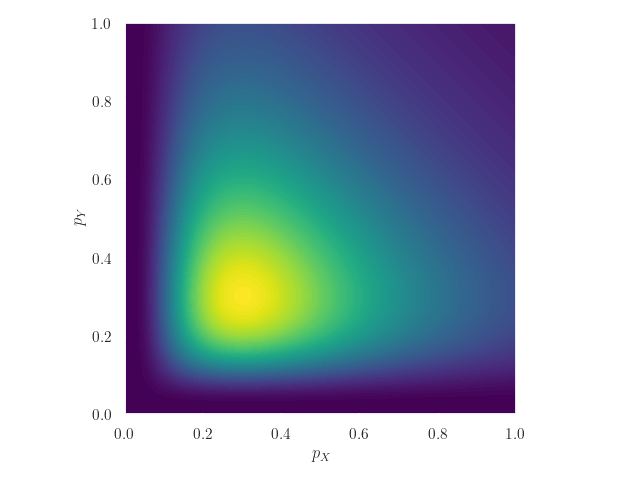

| Lognormal prior based | As in Figure 6 | ||

| Black-Scholes based | As in Figure 6 | Not closed form | As in equation 3.4. |

|

|

|

|

Figure 6 shows the trading functions and Figures 6 represent the belief functions for which the constant product, LMSR, constant weighted-product, and Black-Scholes-based CFMMs, respectively, are optimal for minimizing the CFMM inefficiency.111We provide, at the GitHub repositiry https://github.com/gramseyer/cfmm-liquidity-optimization, a Python script to generate the optimal CFMM trading functions for any user-defined belief function.

§2 formally defines a CFMM and gives some basic properties. §3 studies the steady-state dynamics of a CFMM and defines CFMM liquidity and inefficiency. §4 gives our convex optimization framework and analyzes its KKT conditions. §5 studies the beliefs implicit behind real-world CFMM deployments. Finally, §6 shows how to add consideration for profit and loss to our framework, and qualitatively studies how these considerations change the optimal trading function.

1.2. Related Work

The closest line of work (fan2022differential, ; neuder2021strategic, ; cartea2022decentralised, ; heimbach2022risks, ; bar2023uniswap, ) to our paper is the one which considers profit-maximizing market-making strategies which can be implemented via the Uniswap v3 (uniswapv3, ) protocol. Additionally, (neuder2021strategic, ; cartea2022decentralised, ; bar2023uniswap, ) design “rebalancing” strategies for the LPs, wherein they effectively modify the CFMM trading function periodically. In contrast, we consider designing CFMM trading functions from the first principles and do not use the Uniswap v3 framework. We also do not consider rebalancing the CFMM trading function in this work. A non-exhaustive list of papers in this line is:

-

•

Fan et al. (fan2022differential, ), study the question of maximizing risk-adjusted profit for LPs while accounting for the gas fee for traders. Their model assumes that all trading on a CFMM occurs only in response to price movements on an external market (i.e. arbitrageurs realigning the CFMM spot price to the external market). Their model suggests that risk-neutral LPs must allocate all of their capital at a single price point (§4.2, (fan2022differential, )), while ours better explains the choices of practitioners.

-

•

Neuder et al. (neuder2021strategic, ) study dynamic liquidity allocation strategies for risk-adjusted fee revenue maximization, but do not consider the “divergence loss” incurred in the process.

-

•

Cartea et al. (cartea2022decentralised, ) decompose the CFMM divergence loss into two components – the convexity cost (loss due to arbitrage) and the opportunity cost (the cost of locking up capital). They give a stochastic optimal control-based closed-form strategy for a profit-maximizing LP.

-

•

Heimbach et al. (heimbach2022risks, ) model liquidity positions on Uniswap V3 and perform a data-based analysis of the risks and returns of LPs as a function of the volatility of the underlying assets.

Similar to (cartea2022decentralised, ), Milionis et al. (milionis2022automated, ) show that a part of the divergence loss corresponds to the market risk and can be hedged by a rebalancing strategy; the remainder of the divergence loss corresponds to the profit made by arbitragers trading against the CFMM – they call this loss the LVR (loss-vs-rebalancing). When the variance of the price of relative to is they show that the rate of accrual of LVR (what they call the instantaneous-LVR) is where denotes the rate of change of in the CFMM with respect to the price under perfect arbitrage. Since the LVR is a linear function of our notion of liquidity, our convex optimization framework can accommodate the LVR as a cost for the LP in the objective function.

Automated market-making has also been studied extensively in the context of prediction markets (hanson2007logarithmic, ; chen2010new, ; chen2012utility, ). The theory of CFMMs and the dynamics around trading with CFMMs have been studied in DeFi (angeris2020improved, ; angeris2019analysis, ; angeris2021replicating, ; capponi2021adoption, ; bartoletti2021theory, ; bergault2022automated, ), and many different DeFi applications have been deployed or proposed using different CFMM trading functions (uniswapv2, ; uniswapv3, ; balancer, ; angeris2021replicatingwithoutoracles, ).

2. Preliminaries

Definition 2.1 (CFMM).

A CFMM trades between two assets and , and has a set of asset reserves — units of and units of . Its trading rule is defined by its trading function such that it accepts a trade of units of in exchange for units of if and only if .

All of the CFMM trading functions discussed in this work have the following properties.

Assumption 1.

A trading function is continuous, non-negative, increasing in both coordinates, and strictly quasi-concave. Further, it is defined only on the non-negative orthant.

The assumption that is increasing, quasi-concave, and never holds a short position in any asset (and is therefore only defined on the non-negative orthant) is standard in the literature (e.g. (angeris2020improved, )). We assume strict quasi-concavity for clarity of exposition. The CFMM’s trading function implicitly defines a marginal exchange rate (the “spot exchange rate”) for a trade of infinitesimal size.

Definition 2.2 (Spot Exchange Rate).

At asset reserves the spot exchange rate of a CFMM with trading function is at .

When is not differentiable, the spot exchange rate is any subgradient of . When , the spot exchange rate is , and when , the spot exchange rate is .

These definitions directly lead to some useful observations. We give the proofs in Appendix C.1.

Observation 1.

If is strictly quasi-concave, then for any constant and spot exchange rate , there is a unique point where and is a spot exchange rate at .

Observation 2.

Under Assumption 1, for a given constant function value , the amount of in the CFMM reserves uniquely specifies the amount of in the reserves, and vice versa.

Observations 1 and 2 imply that the amounts of and in the CFMM reserves can be written as functions and of its spot exchange rate for the trading function equals constant

In the rest of the discussion, we describe CFMM reserve states by the amount of in the reserves.

Observation 3.

is monotone nondecreasing.

3. Model

As used in Definition 2.2, we adopt the notation wherein exchange rates are given as the rate of a unit of in terms of (i.e., a trade of units of X for units of implies an exchange rate of ). Unless specified otherwise, refers to the CFMM spot exchange rate, denotes the exchange rate in an external market, and denotes the exchange rate of a particular trade.

We now turn to our trading model and our formulation of market liquidity.

Definition 3.1 (System Model).

-

(1)

There are two assets and , and a relatively liquid “primary” external market that provides a (public) reference exchange rate between and .

-

(2)

An LP creates a CFMM that trades between and by providing an initial set of reserves and choosing a CFMM trading function.

-

(3)

Whenever the reference exchange rate on the external market changes, arbitrageurs immediately realign the CFMM’s spot exchange rate with the reference exchange rate. 222 There is always a strictly profitable arbitrage trade to be made when the CFMM’s spot exchange rate differs from the reference exchange rate (angeris2021optimal, ); this phenomena is akin to “stale quote sniping” in traditional exchanges (baldauf2020high, ).

- (4)

We assume, however, that for small fluctuations in the CFMM spot exchange rate resulting from small trades, arbitrageurs do not realign the CFMM spot exchange rate. This assumption is reasonable since the trading fee and other associated costs (e.g., gas fee in DeFi) make such an action unprofitable.

Since the reference exchange rate is public knowledge, traders using the CFMM can compare the exchange rate that a CFMM offers with the reference rate. This difference is the slippage of a trade.

Definition 3.2 (Slippage).

The exchange rate of a trade of units of for units of is . Relative to a reference exchange rate of units of per , the slippage of this trade is

Traders in our model are willing to tolerate a fixed amount of maximum slippage .

Definition 3.3 (Trade Request).

A Trade Request with a CFMM is a request to SELL or BUY units of or , on the condition that the slippage of the trade is at most relative to the reference exchange rate — in other words, a trade request is a tuple (SELL or BUY, X or Y, k, , ).

Definition 3.4 (Trade Success).

A trade request buying for with maximum slippage succeeds if and only if the CFMM can satisfy the entire trade with an exchange rate and, for the reference exchange rate , . Similarly, a trade request selling for succeeds if and only if the CFMM can satisfy the entire trade with an exchange rate such that .

Trade requests are not partially fulfilled. Failed requests are not retried and are deleted. If a request succeeds, the CFMM transfers assets accordingly. Otherwise, the CFMM’s reserves are unchanged. This notion of trade success mirrors the operation of CFMMs in practice; users supply a trade size, exchange rate, and slippage parameter when submitting a trade request (e.g. (uniswapinterface, ; balancerinterface, )).

Putting these definitions together gives the trading model of our study.

Definition 3.5 (Trade Model).

There exists a static (in the short term) reference exchange rate . The size of the trade request is drawn from distribution . The choice of X or Y is arbitrary, but the trade is for BUY or SELL with equal probability. Each request has the same maximum slippage .

Every successful trade changes the reserves of the CFMM – this model induces a Markov chain on the state of the CFMM’s reserves. We assume that the Markov chain, at a given reference exchange rate, has sufficient time to mix before the reference exchange rate changes. Natural restrictions on the distribution of the trades (made explicit below) make this Markov chain ergodic. We study, therefore, the expected fraction of trade requests that a CFMM can satisfy when its state is drawn from the stationary distribution of this Markov chain (we formalize this notion in Definition 3.13).

3.1. Liquidity

Informally, a CFMM with high liquidity at a given exchange rate can sell many units of before its spot exchange rate changes substantially. Definition 3.6 captures precisely the set of asset reserve states of a CFMM in which the CFMM’s spot exchange rate is at most a factor away from the reference exchange rate . Recall from Observation 1 that the amount of asset in a CFMM’s reserves can be expressed as a function of the CFMM spot exchange rate .

Definition 3.6 ().

is the interval .

By Observation 3, , so is always well-defined.

Recall that is the exchange rate of a unit of in terms of . As motivation for the choice of this definition, consider the case where is a volatile asset and is the base numeraire currency. Here, Definition 3.6 precisely captures the amount of capital allocated to market-making in a range where the spot exchange rate of the volatile asset is within a factor of its reference exchange rate. In the general case where neither nor is the base numeraire currency, the actual amount of capital (in terms of base numeraire) allocated to market-making at a certain price point depends on the exchange rates of both and in the base numeraire. However, a similar intuition holds.

Since is expected to be small in practice, and to facilitate easier analysis in the rest of the paper, it is useful to extend Definition 3.6 to study the liquidity at a single exchange rate.

Definition 3.7 (Liquidity).

The liquidity at an exchange rate , , is .

Observe that naturally captures an allocation of capital to market-making on the full range of exchange rates. Recall from the System Model 3.1 (point 2) that the arbitrageurs always realign the CFMM’s spot exchange rate to the reference exchange rate. Therefore, here on, we denote the liquidity of a CFMM as a function of its spot exchange rate. Lemma 3.8 enables a natural restatement of in terms of in Lemma 3.9. We include the proof of Lemma 3.8 in Appendix §C.1. Lemma 3.9 follows from Definitions 3.6 and 3.7.

Lemma 3.8.

The function is differentiable when the trading function is twice-differentiable on the nonnegative orthant, is when or , and Assumption 1 holds.

Lemma 3.9.

If the function is differentiable, then .

The definition of liquidity implied by Lemma 3.9 is closely related to other definitions of liquidity in the literature. The Uniswap V3 whitepaper (uniswapv3, ) uses , which is equivalent to . Papers that build strategies for LPs on the Uniswap V3 protocol also adopt the same definition of liquidity (neuder2021strategic, ; heimbach2022risks, ; fan2022differential, ) as (uniswapv3, ). Milionis et al. (milionis2022automated, ) use for liquidity which is equivalent to ; they also introduce a notion of “instantaneous Loss-Versus-Rebalancing” for the CFMM expected cost of operation. This quantity is proportional to (Theorem 1, (milionis2022automated, )), which is equivalent to up to constant multipliers. We conclude this subsection with some convenient facts about .

Observation 4.

-

(1)

(when is differentiable).

-

(2)

-

(3)

The amount of that enters the CFMM’s reserves as the spot exchange rate moves from to (for ) is

-

(4)

The amount of in a CFMM’s reserves, with current spot exchange rate , is .

-

(5)

The amount of in a CFMM’s reserves, with current spot exchange rate , is .

Point 1 follows from the fact that and points 2-5 follow from Lemma 3.9.

3.2. CFMM Inefficiency

We need an expression approximating the fraction of trade requests a CFMM fails to satisfy. As discussed above, the trading model given in Definition 3.5 induces a Markov chain on the state of a CFMM’s reserves. We wish to quantify the expected fraction of trades that fail during the evolution of this chain. We assume that the reference exchange rate changes relatively infrequently (so that this Markov chain has time to mix) and study the chain’s stationary distribution.

The precise details of the induced Markov chain (we give an example below and another in Appendix §B) depends on the trade size distribution (and instantiation-specific assumptions). However, common to many natural distributions is the phenomenon that (when the reference exchange rate is ) the chance that a trade request of size units of fails is approximately . This approximation is closest when the sizes of the trades are much smaller than .

3.2.1. Example: Constant Trade Sizes

Definition 3.10 (Size-k Trade Distribution).

At each time step, a trade request arrives with probability and buys or sells units of , where buying or selling is chosen with equal probability (and each request tolerates a constant slippage ).

For the rest of this section, assume that the reference exchange rate is some unchanging . The requirement that ensures that the Markov chain is ergodic.

Lemma 3.11.

When trades are drawn from the size-k trade distribution (Definition 3.10), if the CFMM starts with units of , then the stationary distribution of the induced Markov chain is uniform over the points for some integers .

Furthermore, , where is the reference exchange rate.

Proof.

The only states reachable from under the size-k trade distribution are a subset of the points . A trade of size and maximum slippage fails if the spot exchange rate of the CFMM is already above . Thus, there must be some such that upper bounds the reachable state space. A similar argument shows that must exist. Note that and always exist, even when (in which case ).

By the quasi-concavity of the CFMM trading function, the overall exchange rate of a trade must be between the spot exchange rates before and after the trade. Therefore, for any , a trade to sell units of must succeed if . Thus, must be such that and . A similar argument holds for .

In other words, the set of reachable states is a sequence of discrete points, all but the endpoints of which must be in . Thus, , and .

The Markov chain, therefore, is a random walk on a finite sequence of points with an equal probability of moving in either direction (remaining in place at the endpoints instead of walking beyond the end). Standard results on Markov chains (e.g. Example 1.12, (levin2017markov, )) show that the Markov chain is ergodic and the stationary distribution is uniform over these points. ∎

Once this Markov chain mixes, therefore, the chance at any timestep that a trade fails is the chance that the trade fails if the CFMM is in a randomly sampled state on this Markov chain.

Lemma 3.12.

When trades are drawn from the discrete distribution of size (Definition 3.10), the probability that a trade fails is between and .

Proof.

Let , as defined in Lemma 3.11. The trade request failure chance is because trade requests only fail at the endpoints of the sequence of reachable states. At sell requests fail and at buy requests fail.

Since and (from Lemma 3.11), we have that . The clipping to is required for the probability in the case where ∎

When the trade failure probability is closely approximated by where the approximation error is The rest of this work makes the following assumption.

Assumption 2 (Small Trade Size).

Trade sizes are upper bounded by a constant.

Assumption 2 is not required to study the model in general – traders can submit trades of size comparable to units of , and it will be successful with non-zero probability. However, the assumption enables us to approximate the trade failure probability, which is required to compile it into a metric for the CFMM designers. See also that (Observation 4). If is relatively constant in a neighbourhood of exchange rate , then , and so, under Assumption 2, for any the chance that a trade fails is proportional to .

With this in mind, we define the following “CFMM inefficiency” metric.

Definition 3.13 (CFMM Inefficiency).

The CFMM’s inefficiency at an exchange rate , with regard to a trade of size units of , is . The inefficiency of a trade denominated in is equivalent to the inefficiency of a trade of size units of .

This metric has important implications for the performance of a CFMM. Consider, for example, a trader submitting a trade request of size units of repeatedly until it succeeds. The expected number of times they have to submit the trade is Apart from being an important metric in itself, the CFMM inefficiency is also a crucial factor when considering the LP’s profits, as we will see in §6. Since the CFMM inefficiency is a convex function of each it can directly be incorporated in the objective function of our optimization framework in §4.

3.3. A Liquidity Provider’s Beliefs

We represent an LP’s beliefs on future asset prices as a function of a base “numeraire” currency (such as USD), instead of one of or . This is because traders and LPs usually denominate their profits, losses, and trade amounts in their native currency. Note, however, that this does not restrict one from studying the case where one of and is the numeraire itself.

Definition 3.14 (LP’s Belief).

The belief of an LP is a function such that it believes that at a future time, asset will have price (relative to the numeraire) and will have price with probability proportional to .

A belief function has the following properties:

-

(1)

is integrable on any set of the form for .

-

(2)

There exists so that the integral of on the set is nonzero.

-

(3)

The set is open, and is continuously differentiable on this set.

-

(4)

The integral of over its entire domain, is a finite positive value.

We do not normalize the belief function to integrate to 1 for ease of analysis later in the paper. This definition is strictly more flexible than a one-dimensional notion of a belief (i.e. a belief on the exchange rate between and ). A one-dimensional belief could be defined, for example, as nonzero only on the horizontal line where (with an appropriate adjustment to the notion of integrating over the belief). This flexibility will be important when we turn to the incentives of profit-seeking LPs (§6.2).

3.4. Belief Functions From Price Dynamics

An LP might not have just a belief about the distribution of future asset prices, but also some belief about how an asset’s price will evolve over time. Applying time-discounting to beliefs about dynamics results in a belief distribution as in Definition 3.14.

Let be any continuous, integrable function of asset prices, and and be stochastic processes that are believed to represent future asset price dynamics. Let be the joint probability density function at time of and induced by the stochastic processes. Denote the value of at time by The expected value of is

Denote the time-discounted value of at the initial time, with discounting parameter by . By linearity of expectation, the expected value of is

Observe that , where the expectation is over the price dynamics, is therefore equivalent to the expected value of with respect to the static belief function .

This holds for any integrable function , which includes CFMM inefficiency (as in Proposition 4.1) but also expected profit and loss (as in §6).

This framework captures the geometric Brownian motion (uhlenbeck1930theory, ) model of price dynamics via:

Here, and are the initial exchange rates of and relative to the numeraire. and are the drift parameters in the underlying Brownian motion of the log of and and are the corresponding variances. With time discounting, this induces the following belief function.

4. Optimizing for Liquidity Provision

How should LPs allocate capital to market-making at different exchange rates? This question is the core topic of our work. At any point in time, only the capital deployed near the reference exchange rate is useable for market-making. Thus, the “optimal” CFMM design necessarily depends on an LP’s belief on the distribution of future exchange rates.

We show here that an LP’s beliefs on future asset valuations can be compiled into an optimal CFMM design, which is the solution to a convex optimization problem (Theorem 4.4). Specifically, the optimization framework outputs a capital allocation (as in Definition 3.7) that minimizes the expected CFMM inefficiency (Proposition 4.1). Ultimately, we show that this relationship goes both ways; a liquidity allocation uniquely specifies an equivalence class of beliefs (Corollary 4.15). Per Observation 4, a liquidity allocation fully specifies a CFMM trading function.

This section discusses “optimality” from a viewpoint of minimizing CFMM inefficiency; however, we show in §6.1 that this optimization framework, with a different objective function, computes a CFMM that maximizes expected CFMM fee revenue. Furthermore, we show in §6.2 how to modify the objective of this program to account for losses incurred during CFMM operation.

4.1. A Convex Program for Optimal Liquidity Allocation

4.1.1. Objective: Minimize Expected CFMM Inefficiency

Proposition 4.1.

Suppose every trade order on a CFMM is for one unit numeraire’s worth of either or , and buys or sells the asset in question with equal probability. The expected CFMM inefficiency is . We define the integral only where . Further, we define to be when . is as in Definition 3.14.

Proof.

Suppose that a trader order is for unit of numeraire’s worth of with probability , and for unit of numeraire’s worth of with probability . The size of a trade denominated in is therefore , and the size of a trade denominated in is .

Recall from Definition 3.13 that at a given set of reference prices , the CFMM inefficiency for a trade buying or selling numeraire’s worth of is . Similarly, also from Definition 3.13, the CFMM inefficiency corresponding to a trade of numeraire’s worth of is . Hence, the overall expected CFMM inefficiency is

| (2) |

For clarity of exposition, we focus on the scenario where each order trades unit of the numeraire’s worth of value. Our model can study, however, scenarios where for general trade sizes and also when the trade size is a function of and . The CFMM inefficiency is a linear function of trade size. A distribution of trade sizes can be multiplied with the belief function.

Proposition 4.1 also implies that the trade failure chance is the same for a trader buying or . The in the denominator of the integrand in equation (2) appears because the liquidity is defined with respect to the reserves of asset Y, i.e., (recall Lemma 3.9). Overall, there is no distinction between and for the purpose of the CFMM inefficiency.

4.1.2. Constraints: A Finite Budget for Market-Making

The asset reserves of a CFMM are finite. Clearly, the best CFMM to minimize expected inefficiency has liquidity at every exchange rate , but this would require an infinite amount of each asset (Observation 4). We model an LP with a fixed budget who creates a CFMM when the reference exchange rates of and in the numeraire are and , respectively. With this budget, the LP can purchase (or borrow) any amount of and , say, and , subject to the constraint that . With this intuition, we have the following technical lemmas:

Lemma 4.2.

Given a purchasing choice of and , the LP can choose and set the initial spot exchange rate of the CFMM to be , subject to the following asset conservation constraints.

-

(1)

-

(2)

Proof.

Follows from Observation 4. ∎

Lemma 4.3.

Proof.

Duplicate and allocate the capital to any with to build . ∎

A rational LP sets the initial spot exchange rate of the CFMM to be equal to the current reference exchange rate (i.e. ). If not, a trader could arbitrage the CFMM against an external market. The arbitrage profit of this trader is the LP’s loss, which effectively reduces the LP’s initial budget.

Our convex program combines the above objective and constraints to compute an optimal liquidity allocation . The core of the rest of this work is in using this program to understand the relationship between LP beliefs and optimal liquidity allocations.

Theorem 4.4.

Suppose that the initial reference prices of assets and are and , and that an LP has initial budget and belief function .

The optimal liquidity provision strategy, , is the solution to the following convex optimization problem (COP). The decision variables are , and for each exchange rate 333 The optimization is over a Banach space with one dimension for each ; we elide this technicality when possible for clarity of exposition.

| (COP) | |||||

| (COP) | |||||

| (COP) | |||||

| (COP) | |||||

| (COP) | |||||

Proof.

The that solves COP minimizes the expected transaction failure chance (the expression in Proposition 4.1),444The normalization term in the denominator is dropped for clarity since it doesn’t change the solution of the problem. while satisfying the LP’s budget constraint. The objective and the constraints are integrals of convex functions and thus are convex.

This optimization problem is over a Banach space (there are uncountably many ). Well-established results from the theory of optimization over Banach spaces show that optimal solutions exist (Theorem 47.C, (zeidler1985, )) and the KKT conditions are well defined (§4.14, Proposition 1, (zeidler1995, )). ∎

A CFMM offers only a spot exchange rate ( relative to ), not a spot valuation for each asset (relative to the numeraire). In this light, we find that the objective function of COP can be rearranged to one that depends only on ratios of valuations.

Lemma 4.5.

Define to be the standard polar coordinates, with and .

Proof.

Follows by standard algebraic manipulations (). ∎

This rearrangement reveals a useful equivalence class among LP beliefs.

Corollary 4.6.

Any two beliefs give the same optimal liquidity allocations if there exists a constant such that for every ,

This corollary has important implications for the closed-form results we obtain in §5 for commonly deployed CFMMs. The analysis of a belief defined on the square gives the results for all beliefs defined analogously on for any

Corollary 4.7.

Define . Then

Lemma 4.8.

COP always has a solution with finite objective value.

Corollary 4.9.

On any set of nonzero measure, we cannot have and

4.2. Optimality Conditions

We first give some lemmas about the structure of optimal solutions to COP.

Lemma 4.10.

The following hold at any optimal solution.

-

(1)

-

(2)

-

(3)

Lemma 4.10 says that at optimum, the constraints of COP are tight. A full proof is in Appendix C.5. Using the result of Lemma 4.10, the KKT conditions (§5.5.3, (boyd2004convex, )) of COP are the following:

Lemma 4.11 (KKT Conditions).

Let , and be the Lagrange multipliers for COP, COP, and COP respectively. Let be the Lagrange multipliers for each constraint.

When

-

(1)

For all with , .

-

(2)

For all with , .

-

(3)

and .

When

-

(1)

For all with , .

-

(2)

For all with , .

-

(3)

and .

Proof.

These are the KKT conditions of COP. is a functional over a Banach space. This functional exists for every optimal solution by Proposition 1 of §4.14 of (zeidler1995, ). Note that that proposition requires the objective to be continuously differentiable in a neighbourhood of the optimal solution; this does not hold when the optimization problem is as written and there is some so that goes continuously to at (but is nonzero near ). In this case, one could replace by in the denominator of the objective, for some arbitrarily small . This would cause a small distortion in . We elide this technicality for clarity of exposition. Continuous differentiability of the objective on a neighbourhood where for all with follows from the assumption that is continuously differentiable on the set where , and that this set is open (in Definition 3.14). ∎

Corollary 4.12.

The integral is well defined for every and is monotone nondecreasing and continuous.

A proof is given in Appendix C.6. Lemma 4.11 and Corollary 4.12 together

imply that the behaviour of a CFMM that results from an optimal solution of COP is well-defined.

4.2.1. Consequences of KKT Conditions

The KKT conditions immediately imply the following facts about any optimal solution of COP.

Lemma 4.13.

-

(1)

and .

-

(2)

implies . Similarly, implies .

-

(3)

if and only if (unless, for , or for , ).

-

(4)

The objective value is .

-

(5)

.

Proof.

-

(1)

Multiply each side of the first KKT condition in Lemma 4.11 by (for with nonzero to get , integrate from to , and apply the second item of Lemma 4.10.

A similar argument (integrating from to ) gives the expression on .

-

(2)

If , then the right side of the equation in the previous part is nonzero, so must be nonzero. The case of is identical.

-

(3)

Follows from points 1 and 2 of Lemma 4.11.

-

(4)

The right sides of the equations in the first statement add up to the objective.

-

(5)

Follows from point 3 of Lemma 4.11 ∎

Lemma 4.13 shows that the fraction of liquidity allocated to an exchange rate is a function only of the LP’s (relative) belief that the future exchange rate will be . Specifically, except through an overall scalar, there is no interaction between the values of at different relative exchange rates.

Proposition 4.14.

At an optimum, is a function of , and .

Proof.

Follows from Lemma 4.11. ∎

Proposition 4.14 gives several important consequences. First, it shows that an optimal liquidity allocation can be inverted to give a set of belief functions that lead to that liquidity allocation.

Corollary 4.15.

A liquidity allocation and an initial spot exchange rate are sufficient to uniquely specify an equivalence class of beliefs (as defined in Corollary 4.6) for which is optimal.

Second, Proposition 4.14 actually enables an explicit construction of a belief that leads to .

Corollary 4.16.

Let and be initial reference valuations, and let denote a liquidity allocation. Define the belief to be when and , and to be otherwise. Then is the optimal allocation for .

Finally, the KKT conditions (Lemma 4.11) imply that linear combinations of beliefs result in predictable combinations of liquidity allocations. Towards this, we have the following result, which will also be useful in further proofs. Proofs of Corollaries 4.15, 4.16, and 4.17 are in Appendix §C.7.

Corollary 4.17.

Let be any two belief functions (that give and ) with optimal allocations and , and let be the optimal allocation for . Then is a linear combination of and .

Further, when and have disjoint support, is a linear combination of and .

5. Common CFMMs and Beliefs

We turn now to the CFMMs deployed in practice. What do the choices of trading functions in large CFMMs reveal about practitioners’ beliefs about future asset prices? In fact, the optimal beliefs for several widely-used trading functions closely match the widespread but informal intuition about these systems. Recall that and are the initial reference exchange rates. Also, recall the assumption that all trades are for the worth of 1 unit of the base numeraire currency (Proposition 4.1).

5.1. The Uniform, Independent Belief: Constant Product Market Makers

Proposition 5.1.

Let on and otherwise. The liquidity allocation that minimizes the CFMM inefficiency is the allocation implied by the trading function .

Of course, by Corollary 4.6, the belief that gives the constant product market maker is not unique. Importantly, rescaling the belief to one defined analogously on the rectangle for any constant does not change the optimal liquidity allocation. This invariance of the optimal liquidity allocation to such transformations of the belief applies to all results in this section.

Proof.

For the CFMM we have and . This implies and . Recall that This gives .

Proposition 5.1 captures the folklore intuition within Decentralized Finance regarding the circumstances in which constant product market makers are optimal. If an LP has no information regarding correlations in the reference valuations of assets (in terms of the numeraire), then the LP should choose one of these CFMMs because it allocates liquidity evenly across the entire range of exchange rates. To be specific, the liquidity available at a given exchange rate for purchasing from the CFMM is always proportional to the amount of in the reserves at that exchange rate.

5.2. Uniform Beliefs on Exchange Rate Ranges: Concentrated Liquidity Positions

Some CFMMs (e.g. (uniswapv3, )) allow LPs to create piecewise-defined trading strategies, often called “concentrated liquidity CFMMs.”

Definition 5.2 (Concentrated Liquidity CFMM).

A trading function for some constants , has nonzero liquidity on a smaller range of exchange rates than .

While a “concentrated liquidity CFMM” can be designed with any we focus on those which use since these have been widely adopted in practice after being introduced by (uniswapv3, ).

Observe that this trading function differs from the constant product trading rule when or reaches . There exists a range of exchange rates on which this CFMM makes the same trades as one based on the constant product rule. Outside of this range, the CFMM makes no trades. There is a direct mapping from to we omit it here for clarity of exposition.

This trading function corresponds to a belief pattern that is restricted in a similar way; on the specified range of exchange rates, the belief is the same as that of Proposition 5.1, and otherwise.

Proposition 5.3.

Let be two arbitrary exchange rates, and let if and only if , , and , and otherwise. The allocation that maximizes the fraction of successful trades is the allocation implied by a concentrated liquidity position with price range defined by and .

A proof is given in Appendix §C.8. LPs who make markets using concentrated liquidity CFMMs implicitly expect that while the valuations of the two assets may move up and down, their movements are correlated; that is, the exchange rate always stays within some range. This belief exactly matches that intuition.

Corollary 5.4.

The belief corresponding to multiple concentrated liquidity positions, which are defined on disjoint ranges of exchange rates, is a linear combination of the beliefs that correspond to the individual concentrated liquidity positions (as specified in Proposition 5.3).

Proof.

Application of Corollary 4.17. ∎

5.3. Skew in Belief Function: Weighted Product Market Makers

Weighted Constant Product Market Makers add weights to a constant product curve to get trading functions of the form , for some constant .

Proposition 5.5.

The belief function when and otherwise corresponds to the weighted product market maker .

A proof is given in Appendix C.11. This proposition shows that LPs who use weighted product market makers expect that the value of one asset will typically be much higher than that of the other. Informally, more liquidity is allocated towards the higher ranges of exchange rates than the lower ranges when (and vice versa for ). This CFMM, therefore, can satisfy a higher fraction of trades when the exchange rate is high (resp. low). On the other hand, a skewed allocation means that some price ranges suffer from much higher slippage for a fixed-size trade. This intuition mirrors the description of how LPs should choose the weight (balancerintuition, ) in a public deployment (balancer, ) of weighted product market makers. This theorem reduces to Proposition 5.1 when .

5.4. Logarithmic Market Scoring Rule

The logarithmic market scoring rule (LMSR) (hanson2007logarithmic, ), which has been used extensively in the context of prediction markets, corresponds to a CFMM with trading function (univ3paradigm, ).

Proposition 5.6.

The optimal trading function to minimize the expected CFMM inefficiency for the belief when and otherwise, is .

A proof is given in Appendix C.10. Observe that is symmetric about the line — that is to say, . We analyse this belief function in polar coordinates to get a better intuition. Note the term , which is maximized at . For initial exchange rates with , the LMSR expects the relative exchange rate to concentrate about . At extreme exchange rates ( or ), the belief goes to . The LMSR-based CFMM correspondingly allocates very little liquidity at extreme exchange rates.

6. Market-Maker Profit and Loss

Deploying assets within a CFMM has a cost, and LPs naturally want to understand the financial tradeoffs involved (instead of just minimising CFMM inefficiency). Specifically, LPs in CFMMs trade off revenue from transaction fees against losses due to adverse selection.

6.1. Fee Revenue

Many CFMM deployments charge a fixed-rate fee on every transaction. While some early instantiations automatically reinvested fee revenue within the CFMM reserves (uniswapv2, ), more recent deployments choose not to (uniswapv3, ). We consider the case where fees are not automatically reinvested and, for simplicity, the case where fees are immediately converted into the numeraire currency.

Observe that a percentage-based fee on a trade is, from the trader’s point of view, equivalent to a multiplicative factor in the exchange rate. Slippage also measures the deviation of a trader’s received exchange rate from the reference exchange rate. A transaction fee, therefore, has the same effect in our model on a CFMM’s ability to settle trades as a reduction in a user’s tolerated slippage.

The fee revenue depends on the rate of trade requests and the fraction of trades the CFMM can settle. Recall the probability of a trade request arriving at a time step from the system model in Definition 3.1 and the trade size distribution from the trade model in Definition 3.5. These can be compiled into a belief on the “rate” of trade requests that the LP expects the CFMM will see.

Definition 6.1 (Transaction Rate Model).

Denote as denote an LP’s prediction on the expected volume of trades (in terms of the numeraire) attempted on the CFMM when the reference prices are and and the trading fee is set to .

Proposition 6.2.

The expected revenue of a CFMM in one unit of time, using transaction fee , when the mean trade-size is worth units of the numeraire, is

Proof.

The expected revenue of the CFMM is exactly the transaction fee times the volume of trading that goes through the CFMM, which is equal to the predicted input trade volume, less the number of trades that the CFMM cannot settle. ∎

In any real-world setting, the fee influences the predilection of traders to use the CFMM. However, the transaction fee is a predetermined constant in many of the most widely used CFMM deployments. Uniswap V2, for example, sets a fixed fee (uniswapv2, ), and Uniswap V3 lets LPs choose between three choices of fee rates (uniswapv3, ). In this model, LPs would consider each fee rate they are allowed to set (or perform a grid search over many fee schedules), and then predict (through some external knowledge, outside the scope of this work) the transaction rate at that fee schedule.

Corollary 6.3.

The allocation that maximizes fee revenue is same as the that minimizes

which is in turn equal to the liquidity allocation which is optimal for an LP with belief and is concerned only with minimizing CFMM inefficiency.

In simpler terms, an expected distribution on future transaction rates is equivalent, in the eyes of the optimization framework, to a belief on future prices. A revenue-maximizing LP can therefore use the same optimization problem (with an adjusted input) as in Theorem 4.4.

Definition 6.1 assumes traders are attempting trades for exogenous reasons. However, in the real world, trade volume might depend on how effectively a market-maker provides liquidity. Note that when the trade input rate is independent of and then the objective of minimizing CFMM inefficiency produces the same liquidity allocation as an objective of maximizing the fee collected.

6.2. Liquidity Provider Loss

LPs may also suffer losses when asset prices change. As discussed in Milionis et al. (milionis2022automated, ) and Cartea (cartea2022decentralised, ), these losses come from two sources: first, from the asset price movements directly (exposure to market-risk), and second, from shifts in the relative exchange rate between the assets. As the relative exchange rate on the external market shifts, arbitrageurs can trade with the CFMM to realign the CFMM’s spot exchange rate with the external market’s exchange rate, making a profit in the process at the CFMM’s expense. Milionis et al. (milionis2022automated, ) show that the expected lose due to arbitrage is higher for CFMMs trading more volatile assets.

The CFMM’s loss can only be defined relative to a counterfactual choice; instead of engaging in market-making, an LP could deploy their capital in some other manner. For example, a simple counterfactual would be to hold a fixed amount of the numeraire or a fixed quantity of each asset and, at a future time, compare the value of this strategy with the value of the CFMM’s asset reserves.

Proposition 6.4.

The expected future value of the CFMM’s reserves, as per belief , is

where and denote the amounts of and held in the reserves at spot exchange rate , and is the characteristic function of the event .

This expression for is a linear function of each .

Proposition 6.4 follows from representing and in terms of integration of per Observation 4 and then changing the order of integration. A full proof is in Appendix C.11.

6.2.1. Divergence Loss

Observe that the expected value of a “buy-and-hold" counterfactual strategy does not depend on a chosen allocation . In this case, the expected loss of the market maker (relative to a counterfactual strategy with expected payoff ) is and is linear in each . This measurement of loss is typically called “divergence loss”.

6.2.2. Loss-Vs-Rebalancing

Alternatively, Milionis et al. (milionis2022automated, ) propose the “LVR” metric that compares a CFMM’s performance against that of a counterfactual strategy that makes the same trades in asset as a CFMM but at the reference exchange rate, not at the CFMM’s spot rate. This LVR is an expectation over a model of price dynamics but depends only on that model and the so-called “instantaneous LVR”, which is proportional to (Theorem 1 and Lemma 1, (milionis2022automated, )). Milionis et al. (milionis2022automated, ) show that the “instantaneous LVR” is equivalent to the loss to the CFMM due to arbitrage.

The overall LVR can be given by integrating the “instantaneous LVR” over the time period for which the LP operates the CFMM. Since the overall LVR is, therefore, a linear function of , it can be incorporated directly into our optimization framework.

6.3. Net Profit

Adding capital to a CFMM is profitable in expectation if and only if the expected fee revenue outweighs the expected loss. In the following, we analyze the net expected profit of an LP.

Lemma 6.5.

Let be as defined in Proposition 6.2 and be loss function which is linear in for each . An LP’s net expected profit, , is a concave function in for each .

Proof.

is clearly concave, and for any loss function which is linear in each variable , the whole function is concave in each . ∎

Crucially, Lemma 6.5 is applicable to both the divergence loss and the Loss-vs-Rebalancing.

Observation 5.

A profit-maximizing liquidity allocation by maximizing , and is computable via a convex optimization problem.

Not only, therefore, does our optimization framework allow an LP to design a CFMM that maximizes successful trading activity, but it can also guide a profit-maximizing LP to a profit-maximizing CFMM. Observe that the objective value of this convex program is positive precisely when the CFMM generates a profit.

6.4. Divergence Loss Shifts Liquidity Away From the Current Exchange Rate

The threat of divergence loss is in inherent tension with the potential of a CFMM to earn fee revenue by settling trades. A CFMM can, of course, vacuously eliminate divergence loss by refusing to make any trades (by allocating no liquidity to any price), and in general, higher liquidity at a given range of exchange rates leads to better CFMM performance at that range and higher divergence loss if the reference exchange rate moves away from that range.

When divergence loss is accounted for in the objective, our optimization framework computes a liquidity allocation that trades off fee revenue with divergence loss by shifting liquidity away from the current exchange rate i.e., towards more extreme exchange rates (closer to and ).

This qualitative behaviour is, however, not true of every possible loss function that an LP might add to the objective. Each function will have its own effect; nevertheless, the optimization problem can always be solved to compute an optimal allocation.

Theorem 6.6.

Let be the optimal liquidity allocation that maximizes fee revenue — the solution to the optimization problem for the objective of minimizing the following:

Let be the optimal liquidity allocation that maximizes fee revenue while accounting for divergence loss — the solution to the optimization problem for the objective of minimizing the following:

Let and be the optimal initial quantities of for the above two problems respectively.

Then there exists some such that for , and for , . An analogous statement holds for the allocations of .

The proof is technical and is given in Appendix C.11. In simple terms, the divergence loss might change the optimal initial choice of reserves, but given that choice, divergence loss causes liquidity to shift away from the current exchange rate. Qualitatively, the higher the magnitude of the expected divergence loss relative to the expected fee revenue, the larger the magnitude of this effect. This reflects the well-known intuition that when the reference exchange rate changes substantially, highly concentrated liquidity positions (like in §5.2) suffer higher losses than more evenly distributed liquidity allocations (like those of §5.1).

7. Conclusion

We develop in this work a convex program that, for any set of beliefs about future asset valuations, outputs a trading function that maximizes the expected fraction of trade requests the CFMM can settle. Careful analysis of this program allows for study of the inverse relationship as well; for any trading function, our program can construct a class of beliefs for which the trading function is optimal. Constructing this program requires a new notion of the liquidity of a CFMM, and the core technical challenge involves careful analysis of the KKT conditions of this program.

Unlike prior work, this program is able to explain the diversity of CFMM trading curves observed in practice. We analyze several CFMMs that are widely deployed in the modern DeFi ecosystem, and show that the beliefs revealed by our model match the informal intuition of practitioners.

Furthermore, our program is versatile enough to cover the case of a profit-seeking LP that must trade off expected revenue from trading fees against loss due to arbitrage. This program therefore can serve as a guide for practitioners when choosing a liquidity allocation in a real-world CFMM.

References

- (1) Balancer swap interface. https://app.balancer.fi/#/trade, accessed 07/04/2022

- (2) Uniswap swap interface. https://app.uniswap.org/#/swap?chain=mainnet, accessed 07/04/2022

- (3) Hyperconomy. https://github.com/patrick-layden/HyperConomy and https://dev.bukkit.org/projects/hyperconomy (2012), accessed 2/4/2022

- (4) Adams, H., Zinsmeister, N., Robinson, D.: Uniswap v2 core (2020)

- (5) Adams, H., Zinsmeister, N., Salem, M., Keefer, R., Robinson, D.: Uniswap v3 core. Tech. rep., Tech. rep., Uniswap (2021)

- (6) Amihud, Y., Mendelson, H.: Dealership market: Market-making with inventory. Journal of financial economics 8(1), 31–53 (1980)

- (7) Amihud, Y., Mendelson, H.: Asset pricing and the bid-ask spread. Journal of financial Economics 17(2), 223–249 (1986)

- (8) Angeris, G., Chitra, T.: Improved price oracles: Constant function market makers. In: Proceedings of the 2nd ACM Conference on Advances in Financial Technologies. pp. 80–91 (2020)

- (9) Angeris, G., Chitra, T., Evans, A., Boyd, S.: Optimal routing for constant function market makers (2021)

- (10) Angeris, G., Evans, A., Chitra, T.: Replicating market makers. arXiv preprint arXiv:2103.14769 (2021)

- (11) Angeris, G., Evans, A., Chitra, T.: Replicating monotonic payoffs without oracles. arXiv preprint arXiv:2111.13740 (2021)

- (12) Angeris, G., Kao, H.T., Chiang, R., Noyes, C., Chitra, T.: An analysis of uniswap markets. arXiv preprint arXiv:1911.03380 (2019)

- (13) Aoyagi, J.: Liquidity provision by automated market makers. Available at SSRN 3674178 (2020)

- (14) Balancer Labs: Balancer v2 documentation: Weighted pools. https://web.archive.org/web/20220625080037/https://docs.balancer.fi/products/balancer-pools/weighted-pools (2021)

- (15) Baldauf, M., Mollner, J.: High-frequency trading and market performance. The Journal of Finance 75(3), 1495–1526 (2020)

- (16) Bar-On, Y., Mansour, Y.: Uniswap liquidity provision: An online learning approach. arXiv preprint arXiv:2302.00610 (2023)

- (17) Bartoletti, M., Chiang, J.H.y., Lluch-Lafuente, A.: A theory of automated market makers in defi. In: International Conference on Coordination Languages and Models. pp. 168–187. Springer (2021)

- (18) Bergault, P., Bertucci, L., Bouba, D., Guéant, O.: Automated market makers: Mean-variance analysis of lps payoffs and design of pricing functions. arXiv preprint arXiv:2212.00336 (2022)

- (19) Boyd, S., Vandenberghe, L.: Convex optimization. Cambridge university press (2004)

- (20) Capponi, A., Jia, R.: The adoption of blockchain-based decentralized exchanges. arXiv preprint arXiv:2103.08842 (2021)

- (21) Cartea, Á., Drissi, F., Monga, M.: Decentralised finance and automated market making: Predictable loss and optimal liquidity provision. Available at SSRN 4273989 (2022)

- (22) Chen, Y., Pennock, D.M.: A utility framework for bounded-loss market makers. arXiv preprint arXiv:1206.5252 (2012)

- (23) Chen, Y., Vaughan, J.W.: A new understanding of prediction markets via no-regret learning. In: Proceedings of the 11th ACM conference on Electronic commerce. pp. 189–198 (2010)

- (24) Egorov, M.: Stableswap-efficient mechanism for stablecoin liquidity. Retrieved Feb 24, 2021 (2019)

- (25) Fan, Z., Marmolejo-Cossío, F., Altschuler, B., Sun, H., Wang, X., Parkes, D.C.: Differential liquidity provision in uniswap v3 and implications for contract design. arXiv preprint arXiv:2204.00464 (2022)

- (26) Gerig, A., Michayluk, D.: Automated liquidity provision and the demise of traditional market making. arXiv preprint arXiv:1007.2352 (2010)

- (27) Hanson, R.: Combinatorial information market design. Information Systems Frontiers 5(1), 107–119 (2003)

- (28) Hanson, R.: Logarithmic markets scoring rules for modular combinatorial information aggregation. The Journal of Prediction Markets 1(1), 3–15 (2007)

- (29) Heimbach, L., Schertenleib, E., Wattenhofer, R.: Risks and returns of uniswap v3 liquidity providers. arXiv preprint arXiv:2205.08904 (2022)

- (30) Levin, D.A., Peres, Y.: Markov Chains and Mixing Times, vol. 107. American Mathematical Soc. (2017)

- (31) Martinelli, F., Mushegian, N.: Balancer whitepaper. Tech. rep. (9 2019), accessed 2/4/2022

- (32) Milionis, J., Moallemi, C.C., Roughgarden, T., Zhang, A.L.: Automated market making and loss-versus-rebalancing. arXiv preprint arXiv:2208.06046 (2022)

- (33) Mohanta, B.K., Panda, S.S., Jena, D.: An overview of smart contract and use cases in blockchain technology. In: 2018 9th international conference on computing, communication and networking technologies (ICCCNT). pp. 1–4. IEEE (2018)

- (34) Neuder, M., Rao, R., Moroz, D.J., Parkes, D.C.: Strategic liquidity provision in uniswap v3. arXiv preprint arXiv:2106.12033 (2021)

- (35) Othman, A., Pennock, D.M., Reeves, D.M., Sandholm, T.: A practical liquidity-sensitive automated market maker. ACM Transactions on Economics and Computation (TEAC) 1(3), 1–25 (2013)

- (36) Peaster, W.: Amms: a milestone in the history of derivatives markets (Feb 2022), https://www.defipulse.com/blog/amms-derivatives-markets-history, accessed 12/12/2022

- (37) Robinson, D.: Uniswap v3: The universal amm. https://web.archive.org/web/20210622195731/https://www.paradigm.xyz/2021/06/uniswap-v3-the-universal-amm/ (Jun 2021)

- (38) Roughgarden, T.: Tweet thread on cfmm research directions (Nov 2021), https://twitter.com/Tim_Roughgarden/status/1465095782533582858, accessed 11/07/2022

- (39) Uhlenbeck, G.E., Ornstein, L.S.: On the theory of the brownian motion. Physical review 36(5), 823 (1930)

- (40) Werner, S.M., Perez, D., Gudgeon, L., Klages-Mundt, A., Harz, D., Knottenbelt, W.J.: Sok: Decentralized finance (defi). arXiv preprint arXiv:2101.08778 (2021)

- (41) Zeidler, E.: Nonlinear Functional Analysis and its Applications III: Variational Methods and Optimization. Springer Science & Business Media (1985)

- (42) Zeidler, E.: Applied Functional Analysis: Main Principles and their Applications, vol. 109. Springer Science & Business Media (1995)

Appendix A CFMMs and Market Scoring Rules

We highlight here for completeness the equivalence between market scoring rules (hanson2003combinatorial, ) and CFMMs. Chen and Pennock (chen2012utility, ) show that every prediction market, based on a market scoring rule, can be represented using some “cost function.”

A prediction market trades types of shares, each of which pays out 1 unit of a numeraire if a particular future event occurs. The cost function of (chen2012utility, ) is a map from the total number of issued shares of each event, , to some number of units of the numeraire. To make a trade with the prediction market (i.e. to change the total number of issued shares to ), a user pays units of the numeraire to the market.

One discrepancy is that traditional formulations of prediction markets (e.g. (chen2012utility, ; hanson2007logarithmic, )) allow an arbitrary number of shares to be issued by the market maker, but the CFMMs described in this work trade in assets with finite supplies. Suppose for the moment, however, that a CFMM could possess a negative quantity of shares (with the trading function defined on the entirety of , instead of just the positive orthant). This formulation of a prediction market directly gives a CFMM that trades the shares and the numeraire, with trading function for the number of shares owned by the CFMM, and the number of units of the numeraire owned by the CFMM. Observe that for any trade and , . This establishes the correspondence between prediction markets and CFMMs.

In our examples with the LMSR, we consider a CFMM for which (i.e., it doesn’t exchange shares for dollars, but only shares of one future event for shares of another future event). The cost function for the LMSR is The CFMM representation with this cost function follows by setting it to a constant.

Appendix B Continuous trade size distribution

Definition B.1.

Let be some distribution on with support in a neighborhood of .

A trader appears at every timestep. The trade has size units of , where is drawn from . A trade buys or sells from the CFMM with equal probability.

This definition implicitly encodes an assumption that the amount of trading from to is balanced in expectation against the amount of trading from to .

An additional assumption makes this setting analytically tractable.

Assumption 3 (Strict Slippage).

Trade requests measure slippage relative to the post-trade spot exchange rate of the CFMM, not the overall exchange rate of the trade.

In other words, a trade request succeeds if and only if it would move the CFMM’s reserves to some state within . Assumption 3 implies a pessimistic view of the trade failure probability. However, the following result signifies that Assumption 3 is reasonable.

Lemma B.2.

Proof.

See that the strict-quasi concavity of the trading function implies a “convex-pricing” of any asset. For any buy trade, the marginal exchange rate received is non-decreasing in the size of the trade. Therefore the slippage of a buy trade of units is at least as much as the strict slippage of a buy trade of units. A similar argument follows for sell trades. ∎

We now analyze the Markov chain over the CFMM’s state, the stationary distribution of which gives us the trade failure probability under Assumption 3.

Lemma B.3.

Proof.

It is sufficient to show that for any measurable set , , where is a uniform measure on and is a state transition kernel induced by the trade distribution. Denote a trade by wherein implies that the trader sells (and the CFMM buys) units of Y and implies that the trader buys (and the CFMM sells) units of Y.

After a trade starting from point the Markov chain M lands in if either (that is, the trade succeeds) or if and (that is, the trade fails and the initial state was in ). These events are mutually exclusive for any fixed trade since it can only either succeed or fail.

Let be the probability of trade per the distribution in Definition B.1. We have the following.

The second term of the above expression is the probability that the Markov chain M ends up in a state in set due to a successful trade. Since the distribution of trades is symmetric about per Definition B.1, the second term of the above expression is equal to the probability that the Markov chain M in a state in set ends up in after a successful trade. Therefore:

Proposition B.4.

The probability that a trade of size units of fails is approximately , where the approximation error is up to Assumption 3.

Proof.

The probability that a (without loss of generality) sell of size units of fails is equal to the probability that a state , drawn uniformly from the range , lies in the range . Lemma B.3 shows this probability is . ∎

Appendix C Omitted Proofs

C.1. Omitted Proofs of §2 and §3

Restatement 0 (Observation 1).

If is strictly quasi-concave and differentiable, then for any constant and spot exchange rate , the point where and is a spot exchange rate at is unique.

Proof.

A constant defines a set . Because is strictly quasi-concave, this set is strictly convex. Trades against the CFMM (starting from initial reserves ) move along the boundaries of this set. Because this set is strictly convex, no two points on the boundary can share a gradient (or subgradient). ∎

Restatement 0 (Observation 2).

If is strictly increasing in both and at every point on the positive orthant, then for a given constant function value , the amount of in the CFMM reserves uniquely specifies the amount of in the reserves, and vice versa.

Proof.

If not, then would be constant on some line with either or constant. ∎

Restatement 0 (Observation 3).

is monotone nondecreasing.

Proof.

If is decreasing, the level set of , i.e., cannot be convex. ∎

Restatement 0 (Lemma 3.8).

The function is differentiable when the trading function is twice-differentiable on the nonnegative orthant, is when or , and Assumption 1 holds.

Proof.

Observation 2 implies that the amount of in the reserves can be represented as a function of the amount of in the reserves. By assumption, the level sets of (other than for ) cannot touch the boundary of the nonnegative orthant.

Because is differentiable and increasing at every point in the positive orthant, the map from reserves to spot exchange rates at must be a bijection from to . Because is twice-differentiable, must be differentiable, and so the map must also be differentiable. The map from spot exchange rates to reserves is equal to , and so is differentiable because is differentiable and is differentiable. ∎

Restatement 0 (Lemma 3.9).

If the function is differentiable, then .

C.2. Omitted Proof of Corollary 4.6

Restatement 0 (Corollary 4.6).

Any two beliefs give the same optimal liquidity allocations if there exists a constant such that for every ,

Proof.

Follows by substitution. rescales the derivative of the objective with respect to every variable by the same constant and thus does not affect whether an allocation is optimal. ∎

C.3. Omitted Proof of Corollary 4.7

Restatement 0 (Corollary 4.7).

Define . Then

Proof.

The first line follows by Lemma 4.5 (recall that ), the second by substitution of and (and changing the direction of integration — recall when ), and the third by substitution. ∎

C.4. Omitted Proof of Lemma 4.8

Restatement 0 (Lemma 4.8).

The optimization problem of Theorem 4.4 always has a solution with finite objective value.

Proof.

Set for and otherwise. Then

The first term of the last line is finite, as per our assumption on trader beliefs.

Set and . Clearly both and are finite. Finally, rescale each , , and by a factor of to get a new allocation , , and satisfing the constraints and that still gives a finite objective value. ∎

C.5. Omitted Proof of Lemma 4.10

Restatement 0.

The following hold at any optimal solution.

-

(1)

-

(2)

-

(3)

Proof.

The third equation holds since the objective function is strictly decreasing in at least one (where the belief puts a nonzero probability on the exchange rate ), so any unallocated capital could be allocated to increase this on a neighbourhood of and reduce the objective.

The first equation holds because any unallocated units of could be allocated to for a set of in some neighbourhood of some and thereby reduce the objective. If there is no where the belief puts a nonzero probability, then all of the capital allocated by the third constraint to could be reallocated into increasing and thereby decreasing the objective.

The second equation follows by symmetry with the argument for the first. ∎

C.6. Omitted Proof of Corollary 4.12

Restatement 0 (Corollary 4.12).

The integral is well defined for every and is monotone nondecreasing and continuous.

Proof.

The last item of Lemma 4.10 shows that if and only if . When is nonzero, it is either or (depending on the value of ).

By our assumption on trader beliefs, is a well-defined function of and is integrable. Thus, both and are integrable. Monotonicity follows from and continuity from basic facts about integrals. ∎

C.7. Omitted Proof of Corollaries 4.15, 4.16, and 4.17

Restatement 0 (Corollary 4.15).

A liquidity allocation and an initial spot exchange rate are sufficient to uniquely specify an equivalence class of beliefs (as defined in Corollary 4.6) for which is optimal.

Proof.

It suffices to uniquely identify for each , up to some scalar. Lemma 4.13 shows that is a function of an optimal and Lagrange multipliers or , and because , we must have that is specified by and up to some scalar . ∎

Restatement 0 (Corollary 4.16).

Let and be initial reference valuations, and let denote a liquidity allocation. Define the belief to be when and , and to be otherwise. Then is the optimal allocation for .

Proof.

Recall the definition of in 4.7. For the given belief function standard trigonometric arguments show that when , we have and that when , we have .

Let be the allocation that results from solving the optimization problem for minimising the expected CFMM inefficiency for belief . Lemma 4.13 part 3, gives the complementary slackness condition of and its corresponding Lagrange multiplier. With this, Lemma 4.11 gives the following: when , , and when , .

In other words, for all , , so and differ by at most a constant multiplicative factor. But both allocations use the same budget, so it must be that and . ∎

Restatement 0 (Corollary 4.17).

Let be any two belief functions (that give and ) with optimal allocations and , and let be the optimal allocation for . Then is a linear combination of and .

Further, when and have disjoint support, is a linear combination of and .

Proof.

Note that is a linear function of each , and thus For any with and nonzero , .

Similarly, for nonzero , .

If either or is nonzero at , then

Therefore,

An analogous argument holds for .

The second statement follows from the fact that that when only one of or is nonzero, we must have that either or . ∎

C.8. Omitted Proof of Proposition 5.3

Restatement 0 (Proposition 5.3).

Let be two arbitrary exchange rates, and let if and only if , , and , and otherwise. The allocation that maximizes the fraction of successful trades is the allocation implied by a concentrated liquidity position with price range defined by and .

Proof.

A concentrated liquidity position trades exactly as a constant product market maker within its price bounds and , and makes no trades outside of that range.

By Lemma 4.10, the optimal is for outside of the range . Inside that range, by Proposition 4.14, differs from the optimal liquidity allocation for the constant product market maker by a constant, multiplicative factor (the same factor for every ). Thus, the resulting liquidity allocation has the same behavior as a concentrated liquidity position. ∎

C.9. Omitted Proof of Proposition 5.5

Restatement 0 (Proposition 5.5).

The belief function when and otherwise corresponds to the weighted product market maker .

Proof.

This trading function gives the relation and thus , for and is some initial state of the CFMM reserves.

Thus, as defined by the trading function, .

Corollary 4.16 shows that a belief that leads to this liquidity allocation is

on the rectangle and elsewhere, for some constant . The result follows by rescaling the belief function (Corollary 4.6). ∎

C.10. Omitted Proof of Proposition 5.6

Restatement 0 (Proposition 5.6).

The optimal trading function to minimize the expected CFMM inefficiency for the belief when and otherwise, is .

Proof.

This trading function implies the relationship

Combining this with the equation (for some constant ) gives and thus . From the definition of liquidity, we obtain .

C.11. Omitted Proof of Proposition 6.4

Restatement 0 (Proposition 6.4).

The expected future value of the CFMM’s reserves, as per belief , is

where and denote the amounts of and held in the reserves at spot exchange rate , and is the characteristic function of the event .

This expression for is a linear function of each .

Proof.

The first equation follows by substitution of the equations in Observation 4.

Note that for any , the term for any appears in the integral if and only if . The result follows from rearranging the integral to group terms by . ∎

C.12. Omitted Proof of Theorem 6.6

Restatement 0 (Theorem 6.6).

Let be the optimal liquidity allocation that maximizes fee revenue — the solution to the optimization problem for the objective of minimizing the following: