2023

[1]\fnmCongying \surHan

[1]\orgdiv\orgnameUniversity of Chinese Academy of Sciences, \orgaddress\cityBeijing, \countryChina

2]\orgnameInstitute of Electrical Engineering, \orgaddress \cityBeijing, \countryChina

Applying Opponent Modeling for Automatic bidding in Online Repeated Auctions

Abstract

Online auction scenarios, such as bidding searches on advertising platforms, often require bidders to participate repeatedly in auctions for the same or similar items. We design an algorithm for adaptive automatic bidding in repeated auctions in which the seller and other bidders also update their strategies. We apply and improve the opponent modeling algorithm to allow bidders to learn optimal bidding strategies in this multiagent reinforcement learning environment. The algorithm uses almost no private information about the opponent or restrictions on the strategy space, so it can be extended to multiple scenarios. Our algorithm improves the utility compared to both static bidding strategies and dynamic learning strategies. We hope the application of opponent modeling in auctions will promote the research of automatic bidding strategies in online auctions and the design of non-incentive compatible auction mechanisms.

keywords:

Auction Theory, Multiagent Reinforcement Learning, Opponent Modeling, Strategic bidder1 Introduction

Online auctions are widely used in the distribution of advertising on electronic platforms. Using the appropriate mechanism to sell items, such as advertisements, can effectively increase revenue no1 ; no2 ; no27 ; no28 . The most widely used mechanisms in online auctions are the GSP (generalized second price) auction no1 ; no3 , and the VCG (Vickrey-Clarke-Groves) auction no4 ; no5 . Both are applications of the second-price auction mechanism, which can be run efficiently but is not revenue maximizing.

The well-known revenue maximizing mechanism is the Myerson auction no7 , which obtains the optimal mechanism that satisfies the IC (incentive compatibility) constraint under the assumption that the value of bidders is public information. Due to the difficulty in solving the optimal mechanism when the value function of bidders is complex or when there are multiple items, deep neural network methods (RegretNet no8 , ALGNet no9 , MenuNet no34 , Deep GSP no36 ) are applied to solve the optimal mechanism. The algorithms are implemented by repeatedly sampling the value function and solving an optimization problem with IC constraints, which makes training results close to the real optimal mechanism.

Similarly to classical auction theory, most of the research on online auctions has been considered from the perspective of mechanism design for sellers no35 . This is based on the assumption that the value distribution of bidders is public information. The seller can restrict bidders to only truthful bidding strategies by designing mechanisms that satisfy incentive compatibility. However, the value function of bidders in online auctions may be private information that can only be estimated using samples no30 ; no29 ; no31 . The distribution reporting model no10 states that when the bidder’s value function is private information, it can increase its utility by bidding according to some fake distribution. Adversarial learning maximizes the utility of strategic bidders when other bidders in the system use truthful bidding strategies no11 ; no12 .

We aim to design an algorithm for bidders to learn strategies and bid automatically. Our environment setting is diffirent from previous researches such as ZIP (zero intelligence plus) no39 ; no40 , which studied strategy learning for bidders through repeated competition under static mechanisms. We model the repeated auction environment as a multiagent reinforcement learning system, where the seller and each bidder are treated as independent agents and use algorithms (possibly different) to learn strategies. Bidders will repeat the auction for the same item, but the value and strategy may change over time. The difficulty for the automatic bidding of bidders is that it may face different mechanisms and opponent strategies at different moments.

The opponent modeling researches provide support for strategy training of agents in the above system. LOLA no18 is the first algorithm to achieve cooperation in the Prisoner’s Dilemma game by performing the opponent modeling process on each agent independently. The subsequent work COLA no20 states that the system will converge to the target equilibrium when the predictions of all agents for changes in the opponent strategy (lookahead rate) satisfy consistency.

In repeated auctions bidders will improve their utility when they bid specifically according to the private value. This requires bidders to learn to bid in response to a non-static mechanism and to predict the changes in the mechanism induced by the bidding strategy. We consider the gradient between the bidding strategy and the mechanism, and design an algorithm based on PG (pseudo-gradient). Our algorithm PG is able to learn more adaptive bidding strategies by predicting the impact of strategy changes on other agents. PG effectively improves the utility of bidders under the condition that the environment is partially observed and has a strong generalization capability.

Our contributions are as follows. We model the behavior of seller and bidders in repeated auctions as a multiagent learning system, and focus on the convergence results when all agents update their strategies simultaneously. We design an algorithm that allows bidders to learn automatic bidding strategies with higher utility using only partial observations. And we prove that the strategy corresponds to the equilibrium of the auction induced game. The PG algorithm achieves higher utility when other bidders use either a static or dynamic strategy, and can be applied to arbitrary environmental parameter settings. We propose Bid Net to represent the strategies learned by the bidders and provide a network structure suitable for gradient propagation. We apply the opponent shaping method to train the network and design an approximation algorithm based on PG algorithm. This is the first application of multiagent reinforcement learning with opponent modeling in auctions and we believe it will inspire the design of automatic bidding strategies.

To compare the effectiveness of different opponent modeling algorithms in repeated auctions, we tested the convergence results of the algorithms with the linear shading strategy family. The results show that only the PG algorithm can stably learn the target equilibrium strategy and maximize the average utility of the bidders. We also illustrate that Bid Net trained with the PG algorithm is an efficient improvement of the simple linear strategy through experiment. To illustrate the generalizability of our algorithm, we performed experiments on a series of different repeated auction systems. The results show that PG is effective in improving the utility of bidders in different environments.

The remainder of this article is organized as follows. Section 2 introduces related work. Section 3 describes the MARL (multiagent reinforcement learning) system corresponding to repeated auctions and how agents evaluate and learn bidding strategies. In Section 4, we introduce the Myerson mechanism with its corresponding neural network (Myerson Net). Then we propose Bid Net to represent bidding strategies and illustrate its effectiveness as a strategy approximation. In Section 5, we propose complete automatic bidding strategies, including a method for bidders to predict changes in other agents’ strategies and the PG strategy learning method. The experimental evaluation and results are discussed in Section 6. Finally, Section 7 concludes this work.

2 Related Work

2.1 Traditional auction theory

The main results of traditional auction theory are summarized in no37 and no38 discussed the representing and reasoning about auctions. For examples such as first-price auctions, second-price auctions, and their equivalent forms, a common assumption in research is that bidders will respond optimally to the current mechanism and the seller will evaluate the revenue of the mechanism in that equilibrium. This has inspired research on IC (incentive-compatible) auctions where the bidders’ truthful bidding strategy is the dominant strategy and will bid according to value.

The famous Myerson mechanism no7 achieves maximum revenue under IC constraints, but running the mechanism requires the seller to know in detail the value distribution function of each bidder. Recent studies have discussed the case where the seller run the Myerson mechanism with no access to information about the value distribution no8 . This can be interpreted as bidders repeatedly bidding on the same or similar items, and the seller adjust the mechanism until optimal by using the bid information as a value distribution. The conclusion is that in this environment bidders can maximize utility by bidding according to a particular virtual distribution no10 . This provides support for the design of an algorithm for bidders to learn bidding strategies based on private information.

2.2 Application of reinforcement learning in online auction

The rapid development of electronic business has provided a large demand for online auctions no41 . Unlike traditional auctions, online auctions often process large amounts of data in a short period of time and therefore require a high level of automation. Applications of reinforcement learning in automatic control and strategy learning have made progress in online auctions. The main results of reinforcement learning focus on automatic mechanism design, including learning optimal mechanisms no8 ; no9 , optimal reserve price setting no6 ; no27 , and balancing revenue and social welfare no32 ; no33 .

Several studies have modeled strategic bidders from the perspective of the Stackelberg game no11 ; no43 . However, studies rarely consider the scenario in which the seller and bidders interact in an auction as a multiagent game. The difficulty in applying MARL algorithms to auctions is the lack of theory about competition or general forms of games. Since the environment is non-cooperative and non-Markovian, most MARL algorithms, such as the decomposition of the value function no14 ; no44 and communication no15 ; no45 will not be applicable no17 . It is necessary to design different algorithm learning strategies for each bidder and the seller while ensuring system convergence.

2.3 Multiagent reinforcement learning with opponent modeling

For multiagent learning strategies in competition forms of games, the objective is usually to learn optimal responses or Nash equilibrium. Approaches include CO (consensus optimization) no23 , LSS (local symplectic surgery) no25 , etc. In recent studies PSRO (policy space responding oracle) no46 and its related algorithms no48 ; no47 have made progress. By creating a policy pool for each agent and continuously expanding it, PSRO has a good guarantee of convergence.

Unlike algorithms that aim at Nash equilibrium, opponent modeling focuses on shaping the strategy of opponent and obtaining higher utility in multiagent games. Taking the classical prisoner’s dilemma as an example, most algorithms are trained to result in an inefficient Nash equilibrium strategy (both agents choose to betray). The LOLA (learning with opponent learning awareness) no18 algorithm based on opponent modeling first achieves the equilibrium in which agents learn to cooperate. The SOS (stable opponent shaping) no19 algorithm combines LOLA with LookAhead no26 to ensure that the algorithm converges in the general game environments. CGD (competitive gradient descent) no24 improves the stability of the algorithm in competitive two-player games by avoiding the oscillatory behavior during gradient descent.

Opponent modeling algorithms are usually able to exploit specific opponents to improve rewards and converge to equilibrium when all agents use the same algorithm. The article of COLA (consistent learning with opponent learning awareness) no20 analyzes the conditions for convergence of these algorithms. Since the value of bidders in online auctions is private information and different agents will be trained independently, it is reasonable to use opponent modeling to maximize utility.

3 Repeated Auctions and Opponent Modeling

In this section, we introduce the multiagent repeated auction environment. Bidders and the seller will play the auction game for the same item repeatedly and update their strategies independently at the end of each round. The objective of each player is to maximize its own reward. We also present the application of opponent modeling based strategy update approach in this environment.

3.1 Single-item auction with strategic bidders

First, we provide a definition of single-item auction with strategic bidders. We assume that the value of the bidders is derived from a fixed distribution . is the joint distribution. We denote the bidding strategy of the bidder by , where the bid is . And is the strategy parameter for the bidder . The linear shading strategy is an example of a bidding strategy.

We use to represent the seller’s mechanism, which consists of the allocation rule and the payment rule . The seller receives joint bids and exports allocation and payment according to its mechanism . And is the strategy parameter for the seller. The traditional first-price auction allocates item to the bidder with the highest bid and the payment is bid .

Assuming that the joint value distribution and bidding strategies of the other bidders are and , the utility of the strategic bidder will be:

| (1) |

where and . In single-item auctions, we require the allocation to be 0 or 1. Therefore the equation above can be written as:

| (2) |

where is the indicator function and . And the revenue of the seller is:

| (3) |

When the mechanism is fixed and the value function of the bidders is private information, induces a game in which the bidders bid according to some fixed ”fake distribution” and the seller considers the bids to be real distributions no10 . We explain the game induced by the mechanism through the definition and the equilibrium example.

Definition 1 (Induced game of mechanism ).

The induced game is a normal-form game , where is the set of bidders, is the set of actions for bidders and is the utility function. Given the joint action , the utility is derived by applying the mechanism with the assumption .

Theorem 1 (Equilibrium of Myerson auction induced game).

Assume that there are two bidders and their value distribution is (standard setting). If they adopt linear shading strategies , then the Nash equilibrium of the induced game of Myerson auction is ; if they adopt arbitrary increasing strategies ( is increasing with respect to ), then there is a Nash equilibrium .

Proof: First, we prove that in the standard setting, if the two bidders adopt linear shading strategies, then the Nash equilibrium of the induced game of Myerson auction is .

Considering that and , then the virtual value function of the Myerson auction is:

| (4) |

where is the density function of the value distribution , and is the distribution function.

Then we have:

| (5) | ||||

Similarly we have:

| (6) |

The strategies of both agents in the Nash equilibrium are best responses to each other, which indicates that their policy gradient is .

| (7) | ||||

So there exists an equilibrium which satisfies that

| (8) |

This indicates that the equilibrium of the induced game of Myerson auction is .

For an arbitrary increasing bidding distribution of bidders under standard setting, The proof of Nash equilibrium is given in no10 . Here we give a proof under simplified conditions when the bidding distribution is uniform under the composite of virtual value function:

| (9) |

This requires bidders to follow the bidding strategy:

| (10) |

We can obtain the utility function of bidder 1:

| (11) | ||||

Then we have:

| (12) |

We can see that satisfies . Similarly, we have satisfies , which indicates that it is a Nash equilibrium. The corresponding bidding strategy is .

The induced game is determined by the seller’s strategy parameter . Therefore the stationary state requires that is fixed and the strategies of bidders reach the equilibrium of the induced game. We introduce how agents learn this equilibrium in the next section.

3.2 Repeated auction and the MARL system

We consider the seller and strategic bidders to train the above strategy parameters in repeated auction environment for maximum reward. Since auctions for the same items will be repeated multiple times in similar applications such as bidding search and advertising placement, we can assume that the above single-item auction is repeated until the strategies of all agents converge.

At the moment , the strategy of bidders and the seller determines the utility and revenue of this auction round. For strategic bidders and the seller, the observations they receive are the joint bidding , mechanism parameter and their own rewards ( or ). When the value distribution is constant, we assume that using joint bidding we can obtain the joint strategy .

Based on the observations received and the objectives, agents will decide how to choose their strategy for the next round of auction. For the strategic bidder , we usually assume that it adjusts the previous strategy based on observation:

| (13) |

When the bidder is a naive learner no18 , it will maximize its utility assuming that the other agent strategies remain unchanged:

| (14) |

Or we can design gradient-based update methods with learning rate :

| (15) |

The opponent modeling approach is able to improve the reward of agents in strategy learning process. After predicting the change in the opponent’s strategy, the agent selects the corresponding best response:

| (16) |

A simple assumption is that the other agents are naive learners, which means that:

| (17) |

The different prediction of the strategy change of other agents is the main difference in the opponent modeling algorithm. In the following sections, we will specifically discuss the design of the opponent modeling algorithm applicable to repeated auctions.

This forms an MARL system when both the seller and bidders update their strategies through learning. We can see that the convergence result of the strategy in repeated auctions is consistent with the equilibrium of the induced game, where the bidding strategy and mechanism reach a stable point. Our goal is to provide a learning algorithm for bidders that maximizes their utility as the system converges.

4 The Strategies of the Seller and Bidders

In this section, we give the method to represent the strategies of the seller and bidders with neural networks to simplify the strategy space while ensuring reasonableness.

4.1 Myerson Mechanism and Myerson Net

The Myerson mechanism has been proven to be the optimal incentive compatible mechanism for single item auctions. It converts each bidder’s value into a virtual value by and applies a second price auction with reserve 0 to . The virtual value function is determined by the distribution of value and the density function for .

| (18) |

Since the mechanism is incentive compatible, bidders will bid truthfully and maximize the seller’s revenue no7 . We can see that the virtual value function determines both the allocation and payment of the mechanism.

Myerson Net no8 uses a parameterized network to learn virtual value functions and obtains optimal auction mechanisms by solving optimization problems. Since the portion of the second price auction allows the network to satisfy the IC constraint, we only need to use the bidding sample to learn the function assuming that . We give the definition of Myerson Net and explain rationality by its properties and experimental results.

Definition 2 (Myerson Net).

For joint bids from bidders , the seller first transforms each bid into a virtual value ( is the network parameter). The item is then allocated to the bidder with the highest positive virtual value. Payment is the minimum bid required for the winner to win:

| (19) |

From the definition we can directly obtain the following property.

Theorem 2.

For a Myerson Net , we add a strictly increasing function to each virtual value function that satisfies to obtain another mechanism . Then is equivalent to .

Proof: The two mechanisms are equivalent when they have the same allocation rule and payment rule. Given the joint bid , we assume that the allocation and payment of the bidder in the mechanism are and . From the definition, we can see that the allocation is only related to the sorting of the absolute value . , so the allocation rule is the same. If we assume that , then and . . Therefore, is equivalent to .

This property indicates that when the bidders’ strategies are fixed, the network parameters corresponding to the seller’s optimal mechanism are not unique but uniformly distributed. This provides support for the rapid convergence of the network to one optimal mechanism. We define the set of optimal mechanisms corresponding to a particular value distribution and the bidding strategy as the family of optimal mechanisms .

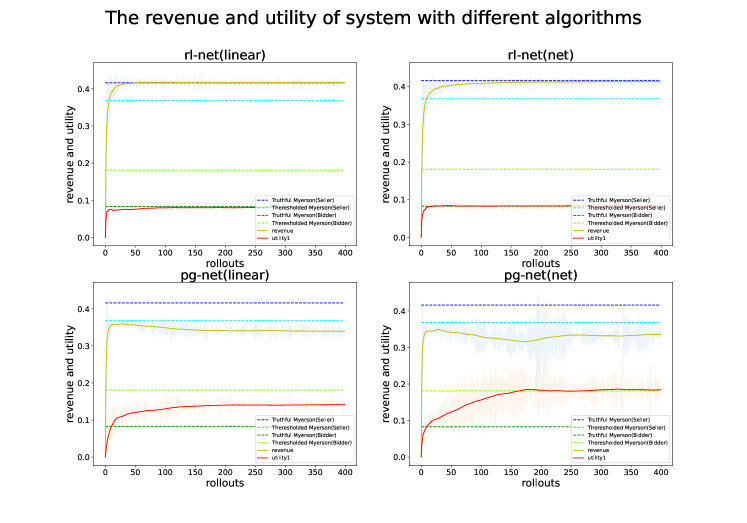

We selected several specific value distribution functions with bidding strategies and compared the virtual value functions output by Myerson Net after training with the optimal (obtained from Myerson Mechanism). The result is shown in Figure 1. From the figure we can see that compared to the real Myerson mechanism, the network output mechanism satisfies the property of Theorem 2. The Myerson Net converges to the family of optimal mechanisms and maximizes the seller’s revenue. Therefore, it is reasonable to use Myerson Net to represent the seller’s mechanism.

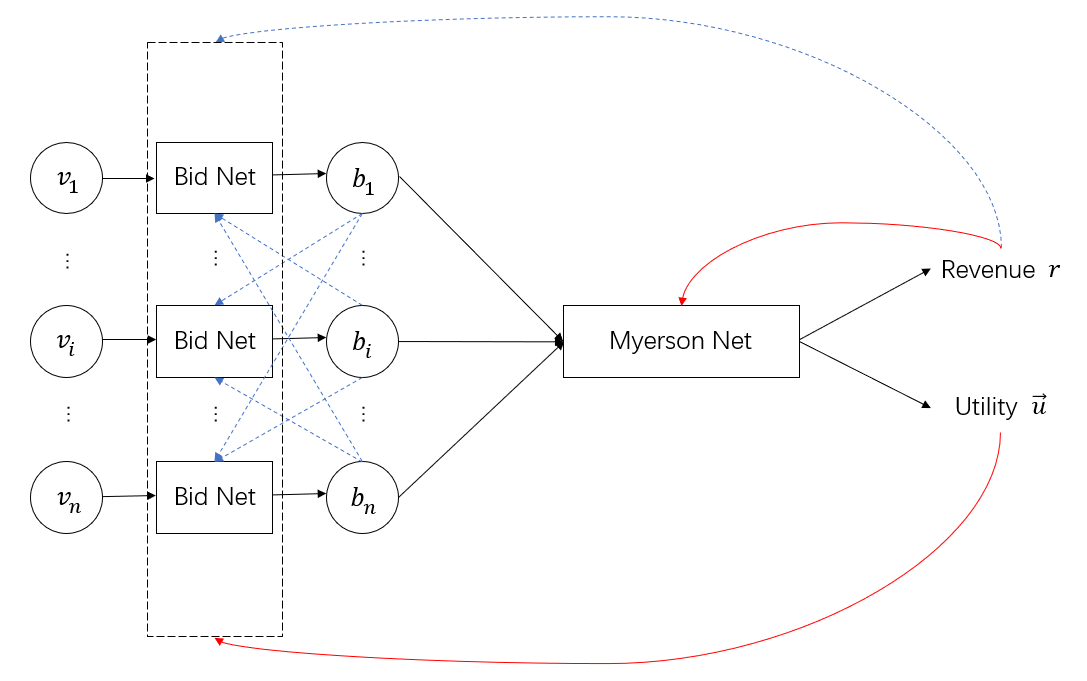

4.2 Bid Net

Since an optimal mechanism can be learned through strategy networks, we consider setting up a similar structure for the strategy learning of bidders. Constraints on the network structure should be chosen appropriately. Generalized families of strategies can hinder learning convergence, while simple approximations (such as linear shading ) may reduce the utility of bidders.

If we consider static strategies, then for the game induced by the Myerson auction, the Nash equilibrium in the standard setting is given in no10 :

However, its drawback is that does not always hold. This equilibrium strategy may lead to negative utilities for bidders with . When bidders do not have access to the dynamic mechanism update method, adopting a bidding strategy that does not satisfy IR (individual rationality) may reduce the bidders’ expected utility. Therefore, we require that the bidding strategy obtained by the network satisfies the following requirements:

-

1)

is increasing function about ,

-

2)

.

We can see that the family of linear shading functions also satisfies the requirements when .

We propose a parametric network (Bid Net) to represent the bidder’s strategy. The network first inputs the received values from the distribution into a multilayer perceptron. Monotonic outputs are combined with regularization constraints . This ensures that the output of the network meets both of these requirements. Since Bid Net training requires the use of gradient propagation algorithm and the operators associated with sorting cannot propagate the gradient, we use NeuralSort no21 ; no22 as an approximation. This allows Bid Net to automate training by back-propagating gradients. The structure of the Bid Net is shown in Figure 2.

To evaluate whether the strategy exported by Bid Net is a valid approximation to the bidder’s strategy, we test the utility of the different bidding strategies with Myerson Net in standard setting. The results are given in Figure 3. We can see that faced with different opponent strategies, the possible export strategy of Bid Net has improved utility compared to linear shading and approximates the equilibrium strategy. Therefore, it can be used for the training of the bidder strategy.

5 Opponent Modeling based Automatic Bidding Method

In this section, we will discuss the method of bidders to automatic bidding in repeated auctions. We assume that bidders and the seller interact in an infinitely repeated auction environment and update their strategies after each auction round. Bidders must adaptively adjust their strategies according to observations at the end of each auction to receive higher utility.

Since the seller and other bidders also update their strategies, agents need to consider both the current utility and the impact on subsequent states when evaluating strategy . We adopt representation similar to reinforcement learning and use to denote the utility expectation of the strategy for the bidder , then we have the following:

| (20) |

where is the discount factor.

For the agent who needs to choose a strategy at moment , the information available is partial observations before moment . Therefore, it is difficult to obtain unbiased estimates of . A direct approximation is , which means that the bidder assumes that the subsequent strategy of other agents () is not relevant to its strategy . Then its choice of action at the next moment will be based on the prediction of the opponent’s action:

| (21) | ||||

For the naive learner, it will assume that the strategies of other agents remain unchanged:

| (22) |

Then its gradient update direction for the strategy will be:

| (23) |

More accurate estimations for usually require first-order approximations:

| (24) | ||||

Assuming the update method of the opponent strategy, we can obtain different predictions for . The LOLA algorithm assumes that the opponent is a naive learner, which means . Assuming that the opponent is a LOLA learner leads to high-order LOLA (HOLA). Similar opponent modeling algorithms include SOS, COLA and others, which effectively learn Nash equilibrium or stable points with higher rewards in different game environments.

The article of COLA no20 points out that the effectiveness of the above opponent modeling algorithms depends on the consistency of the LookAhead rate of all agents. This means that agents in this environment need to choose strategies with consistency to ensure the convergence of the system. However, we have discussed earlier the asymmetry of the repeated auction environment: bidders have private information (value function) that allows them to adopt specific strategies to improve utility. Training strategies directly using opponent modeling algorithms does not maximize the utility of bidders.

Figure 4 illustrates the direction of propagation of the network parameter gradient for bidders and the seller in the MARL environment of repeated auctions. The blue curve in the figure indicates the effect of the change in the strategy parameters of bidder on the other agents in the system, which cannot be estimated by the opponent modeling approach above. We will show that it is necessary to take into account in automatic bidding.

Theorem 3.

If all bidders use only the first-order gradient to update strategy under the Myerson Net of the seller, their strategy gradient direction will lead to the truthful bidding strategy . The fixed point of the system is all bidders bidding truthfully.

Proof: Since the linear shading function family is included in the function family of Bid Net, we take a set of linear shading functions as an example. We assume that

| (25) |

and .

The bidder considers only the first-order gradient equivalent to it assumes that the mechanism is fixed . According to the above bidding strategy, we can obtain the virtual value function corresponding to the Myerson mechanism:

| (26) |

And we assume that . Then we have

| (27) | ||||

The last equation holds because

| (28) |

Then we have

| (29) |

This shows that the gradient always cause to increase when . Then we have

| (30) |

When and , we can assume that and . Since , we have through (30). This shows that has a lower bound . This indicates that the strategy parameter will converge to .

When we assume the mechanism is fixed, bidders updating the strategy using the first-order gradient direction always make increase and converge to 1 (truthful bidding strategy). This indicates that the bidder network must be trained with the high-order gradient, which requires predicting the impact of bidding strategies on mechanism changes. In order to obtain a more accurate prediction of the function for bidders, we will estimate by modeling as functions of :

| (31) |

Then we have:

| (32) | ||||

The convergence of the system in the repeated auction is equivalent to the convergence of the strategies of each agent. We can simplify the above equation by assuming that and then it will become:

| (33) |

where means the prediction of based on after updates.

We use to represent the strategy of other agents when the system converges, which means that:

| (34) |

We can always require that the system converge in finite time by reducing the step size of strategy updating. Assuming that the system converges after updates, we have:

| (35) |

When , the second item will be sufficiently larger than the first. Then we have:

| (36) |

Thus, the strategy selection function of the agent is as follows:

| (37) |

In fact, when a single bidder’s strategy is fixed in a repeated auction, the strategy updates of other bidders and the seller are synchronized and will affect each other. The convergence result is determined by the algorithm used by these agents. To avoid discussing the possibility of different stable points of the system, we assume that the strategy updates of other agents are independent and the bidders’ strategies change slowly . We found this assumption to be valid in our experiments for predicting the strategies of other agents under the condition that their private information is unknown leads to a large bias.

We refer to this process (calculating using ) as the inner loop part of the algorithm. Considering that the seller does not have private information and can learn the strategy only by historical bids, it is reasonable to estimate that the seller is a naive learner. We can simulate this process through the Myerson Net by constraining the bidders’ strategies to . The complete procedure for the inner loop is given in Algorithm 1.

On the basis of the strategy predictions of the other agents obtained from the inner loop, we can derive the bidding strategy that maximizes the expected utility. To avoid instability caused by rapid strategy changes, we restrict the step size by . Then our goal is to solve the constrained optimization problem:

| (38) | ||||

Since the parameters in the optimization objective contain the output of the inner loop, it is difficult to calculate the policy gradient directly. We give the approximate calculation based on pseudo-gradient by defining the pseudo-gradient obtained from as:

| (39) | ||||

From the definition we can see that given the strategy update , we can calculate the pseudo-gradients with the inner loop. In order for the algorithm to choose an update step that is close to the direction of the true gradient, we generate a set of different directions of and select the positive gradient with the largest absolute value from all pseudo-gradients as the update direction of the Bid Net. The complete procedure for the PG algorithm is given in Algorithm 2.

We want the algorithm to converge to the equilibrium of the repeated auction induced game. For a single-item two-bidder auction, which induces a game containing two players, we give an intuitive proof of the convergence of the algorithm. Due to the lack of theory related to the equilibrium convergence of multiplayer games, we only illustrate experimentally the effectiveness of the algorithm in scenarios containing more than three bidders.

Theorem 4.

Assume that both bidders use the PG algorithm and the obtained from the inner loop belongs to the family of optimal mechanisms. When in algorithm 2, the system will converge to the equilibrium of the Myerson auction induced game.

Proof: First, we discuss the case where is constant. If converges as , the seller’s mechanism will also converge to the optimal mechanism family according to Theorem 2:

| (40) |

We consider the pseudo-gradient generation process:

| (41) |

Based on the assumption that belongs to the family of optimal mechanisms, even if , we will have:

| (42) |

Bidders will get the same utility in an equivalent mechanism, which means that:

| (43) |

From the continuity of and the network structrue of Bid Net we find that is continuous and bounded with respect to , where . As an example, in standard setting if and are one-dimensional linear multipliers, we have

| (44) | ||||

Similarly, when the bidding strategy that satisfies is a continuous bounded function with higher dimensions, we can also obtain the same conclusion. Then if the upper bound of the value domain of is strictly positive:

| (45) |

There must exist and , which satisfies that

| (46) |

As , there exists that satisfies this

| (47) |

This shows that the direction chosen when the algorithm does not converge is always the direction of rising utility. Considering that is bounded for , we prove that the algorithm converges when is constant.

Then we want to prove that if is a Nash equilibrium of the induced game, then it is also a stable point of the algorithm.

Since in equilibrium can be represented by , we can consider only bidders as players in the induced game. We assume that is a Nash equilibrium of the induced game; then for we have:

| (48) |

where

| (49) |

This shows that ,

| (50) | ||||

This shows that is also a stable point of the algorithm. It is obvious that when the joint strategy is not a Nash equilibrium, there is always an agent with . Therefore, the system always converges to the induced equilibrium of the repeated game.

In our experiments we find that the algorithm works even if the inner loop does not converge and is finite. From this theorem we can see that when a bidder uses the PG algorithm, it can learn the best response of a static opponent. When all bidders adopt the PG algorithm, the system will converge to the equilibrium of the game induced by the auction. The generalizability of the algorithm lies in the fact that almost no private information about the opponent is required. When the value distribution of other bidders is unknown, the algorithm can take the observed bids as the value distribution and assume the truthful bidding strategy. We will test the effectiveness of the algorithm according to experiments in the next section.

6 Experiments and discussion

6.1 Experiment in automatic bidding environment

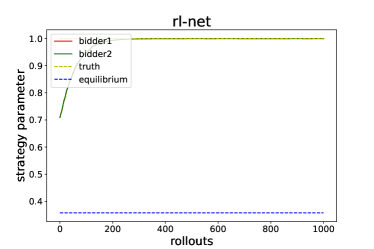

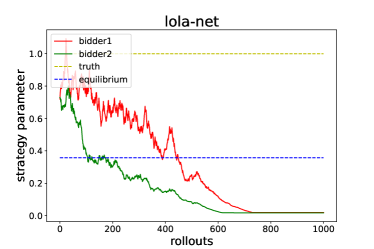

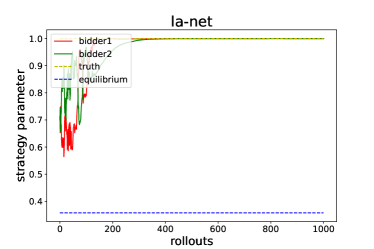

We first compare the utility of agents with different opponent modeling algorithms in the same automatic bidding environment. We choose the standard setting and require all bidders to use the linear shading strategy . In this environment both bidders will use the same algorithm to train strategy. At the end of each auction batch, bidders and the seller will observe the strategies (reflected as bids and mechanism) in that batch and the respective rewards . Then the seller will update the mechanism according to the Myerson Net and the bidders will update strategy based on their algorithm. Due to the linear shading strategy, an equilibrium of the above system is .

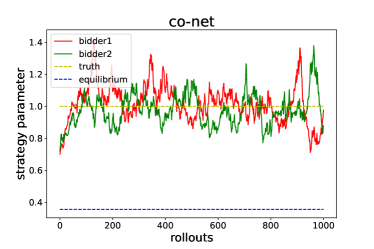

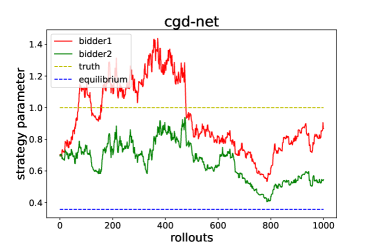

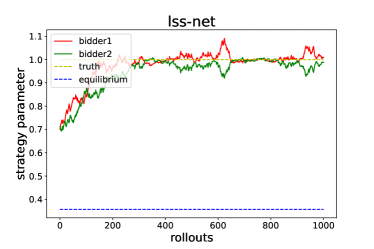

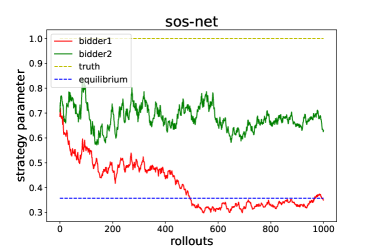

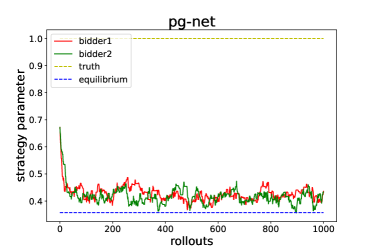

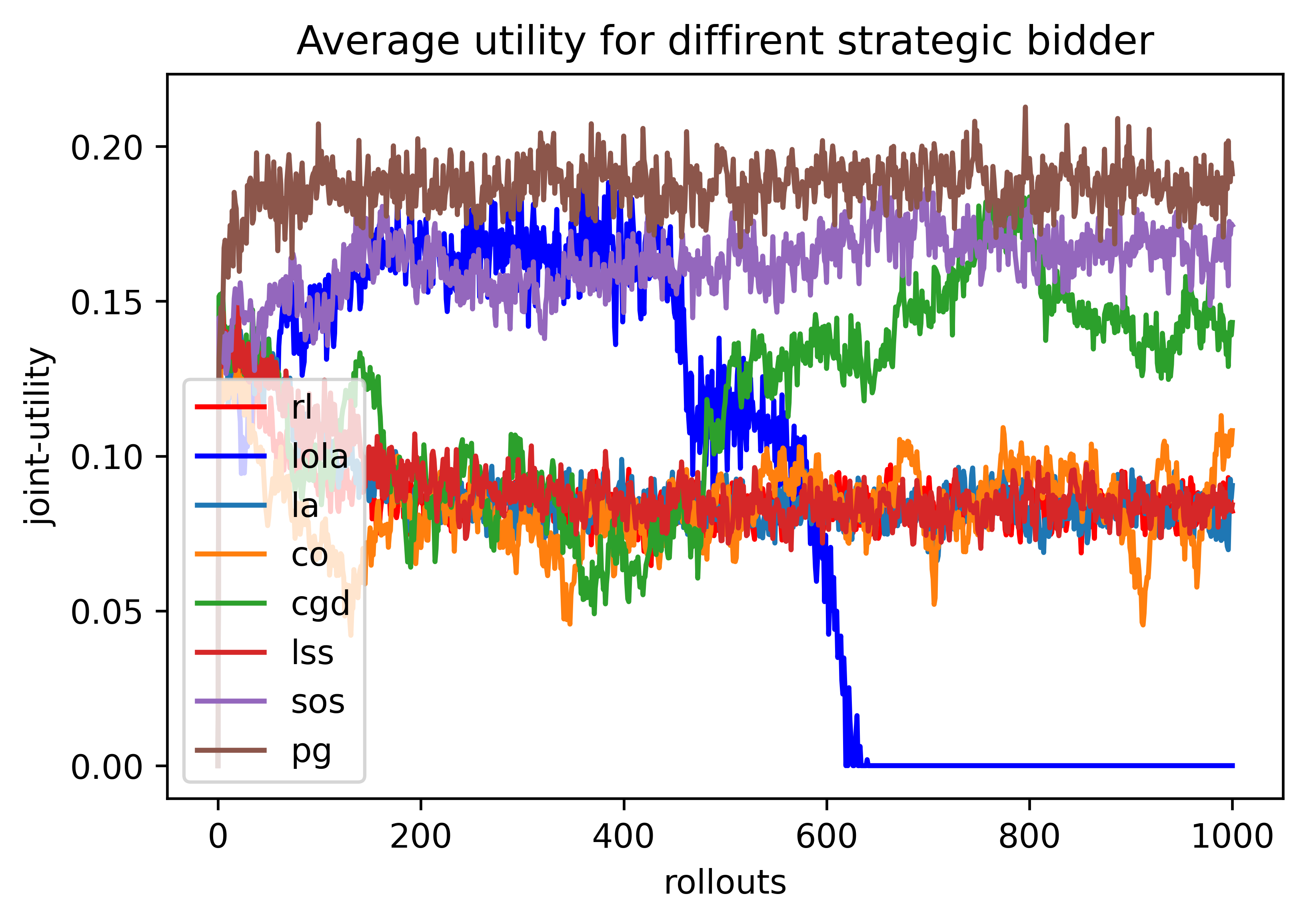

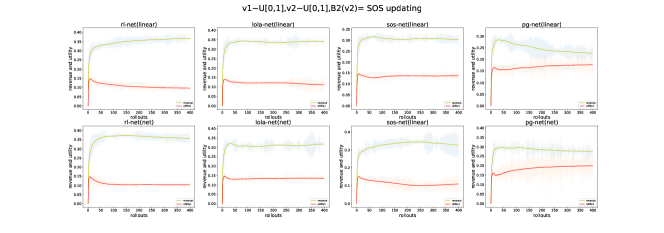

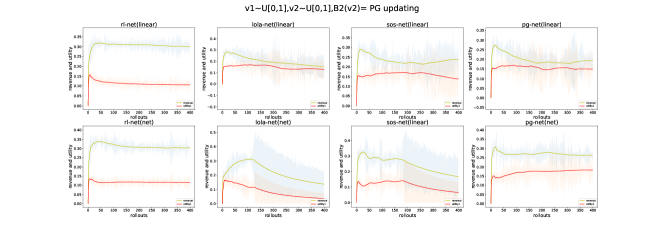

We compare the PG algorithm with some classical opponent modeling algorithms (RL, LOLA no18 , LA no26 , CO no23 , CGD no24 , LSS no25 , SOS no19 ) in the above environment (COLA no20 is not included due to its high computational complexity). The evolution of the agent’s strategy parameters during training is shown in Figure 5. From the figure we can see that most of the algorithms converge to the truthful bidding strategy, which is consistent with the conclusion in Section Five. Algorithms that include high order opponent predictions improve the utility of the bidders but lack stability. The PG training results are closest to the Nash equilibrium strategy. The possible reason for the gap between the result and the equilibrium is that we set a sufficiently small reserve price to prevent bidders from underbidding. The average utility of different agent system is shown in Figure 6. We can see that the PG algorithm obtains the maximum average utility in the automatic bidding task. The experimental results verify the conclusion we made in Theorem 4.

This experiment illustrates the feasibility of using the PG algorithm for automatic bidding. The convergence results of the system are stable and efficient when all bidders use the PG algorithm. We give the results in subsuquent experiments when the bidder use the PG algorithm and the opponents use other algorithms.

6.2 Experiment for Bid Net

We also test the effectiveness of Bid Net by comparing it with linear shading functions and optimal strategies. To visualize the performance of Bid Net, we use the standard setting and assume that the other bidder is fixed at the truthful bidding strategy. We compare the linear shading strategies and Bid Net that is trained by PG and RL respectively, and the results are given in Figure 7.

From the figure, we can see that the network trained with RL always converges to the truthful bidding strategy. The linear shading strategy trained by PG improves the utility of the strategic bidder, but not the optimal strategy. The strategy exported by Bid Net trained by PG algorithm is closest to the optimal strategy. This indicates that Bid Net can be used to represent the bidder strategy and the application of the PG algorithm allows Bid Net to be trained effectively.

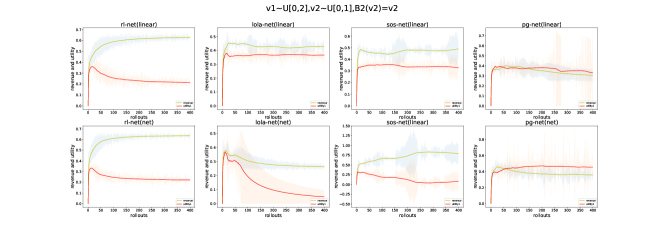

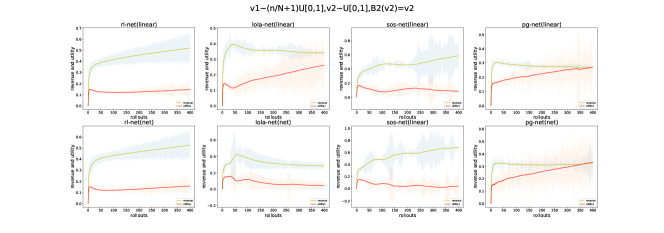

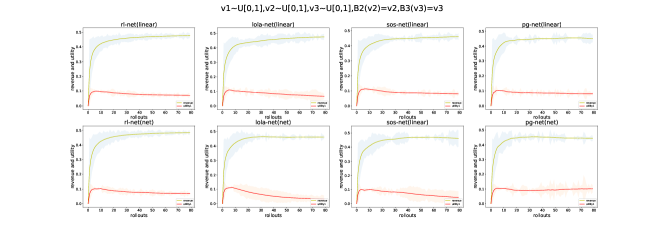

6.3 Experiment for different opponent and environment setting

We want to show that the PG algorithm can be effective against different environments and opponents. As an automatically bidding agent, it may face opponents with different and unknown algorithms, and its own value distribution may change over time. We conduct more experiments under these different conditions.

Experiments in which other bidders use static strategies include: ① Standard setting and another bidder uses the truthful bidding strategy. ② Standard setting and another bidder uses the Nash equilibrium bidding strategy. ③ The value distribution function of the bidders is asymmetric, which means that the private value distribution of bidders is different. ④ The value distribution function of the strategic bidder increases over time. This experiment is designed to show that the algorithm can be applied to dynamic environments such as changes in the value distribution due to changes in items. ⑤ Single-item three-bidders auction and the other bidders use the truthful bidding strategy. This experiment is designed to show that the algorithm is still valid in an environment with more than three bidders.

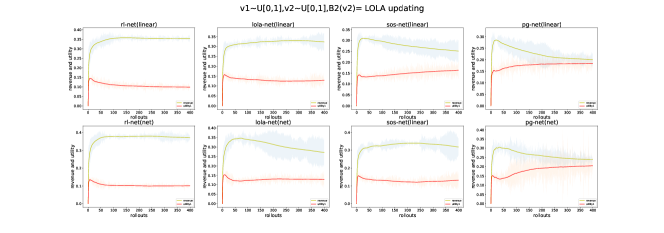

Experiments in which other bidders use dynamic strategies include: ⑥ Another bidder uses the LOLA algorithm to update the strategy. ⑦ Another bidder uses the SOS algorithm to update the strategy. In the above environment each bidder learns the strategy independently and has no access to the private information of other bidders.

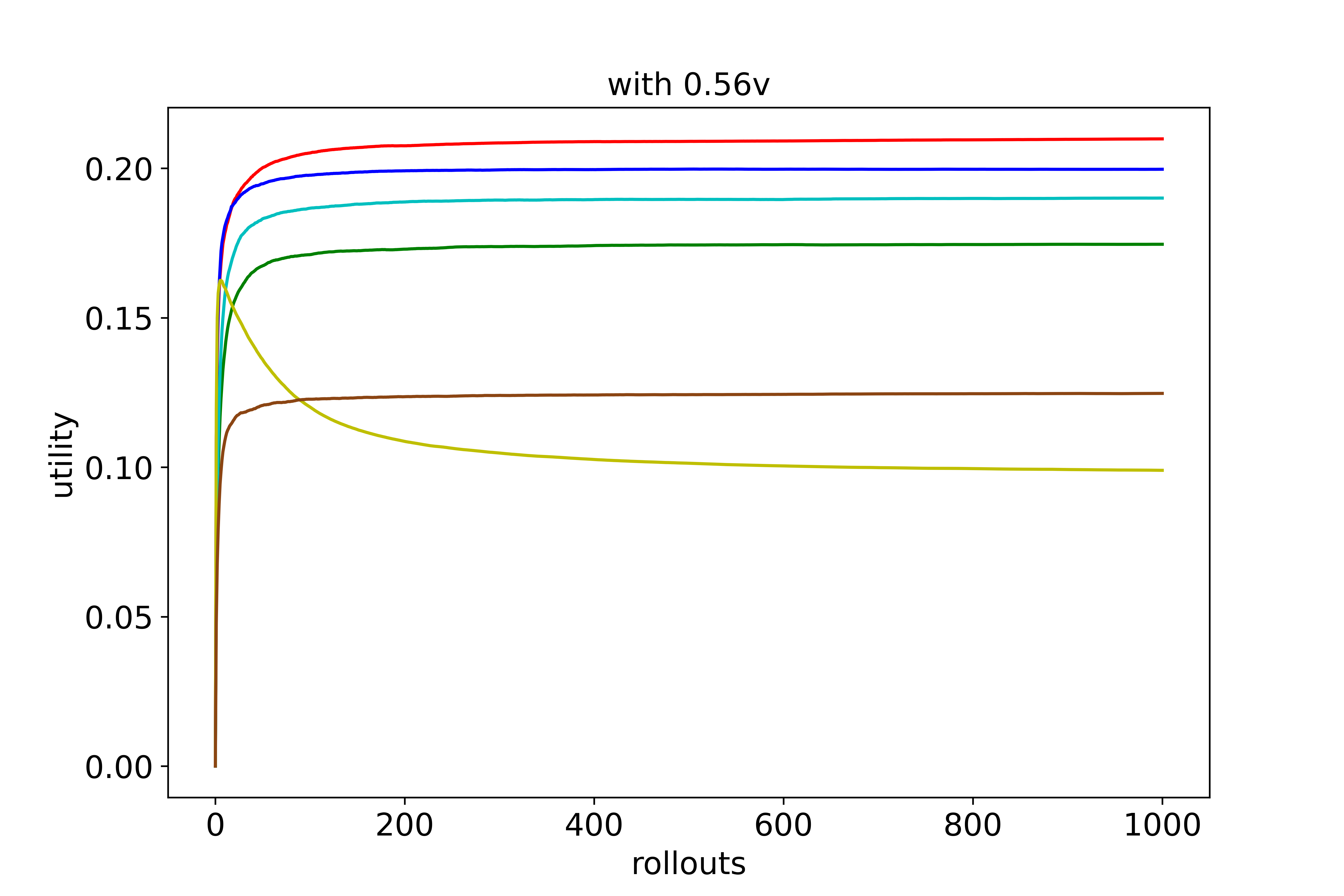

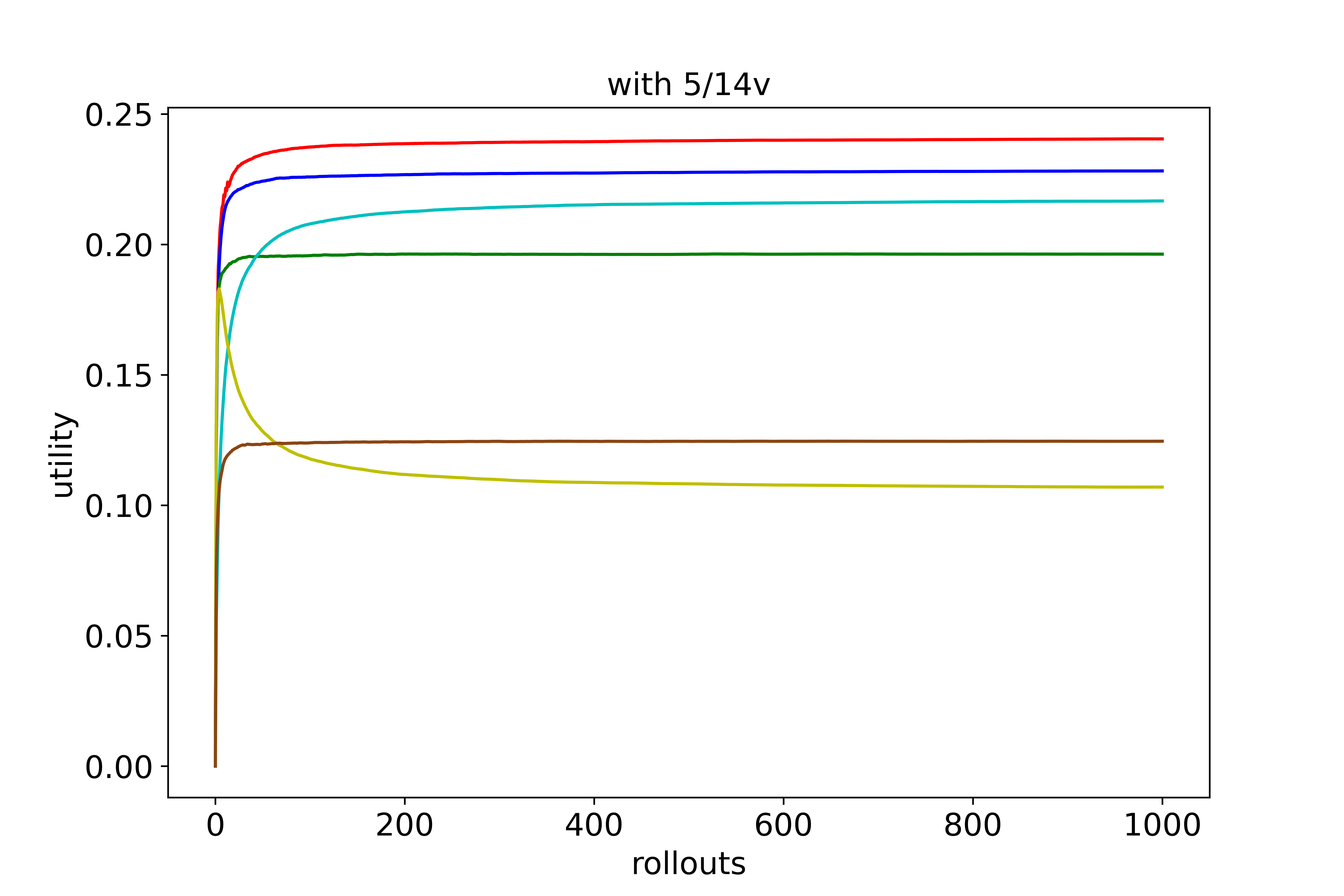

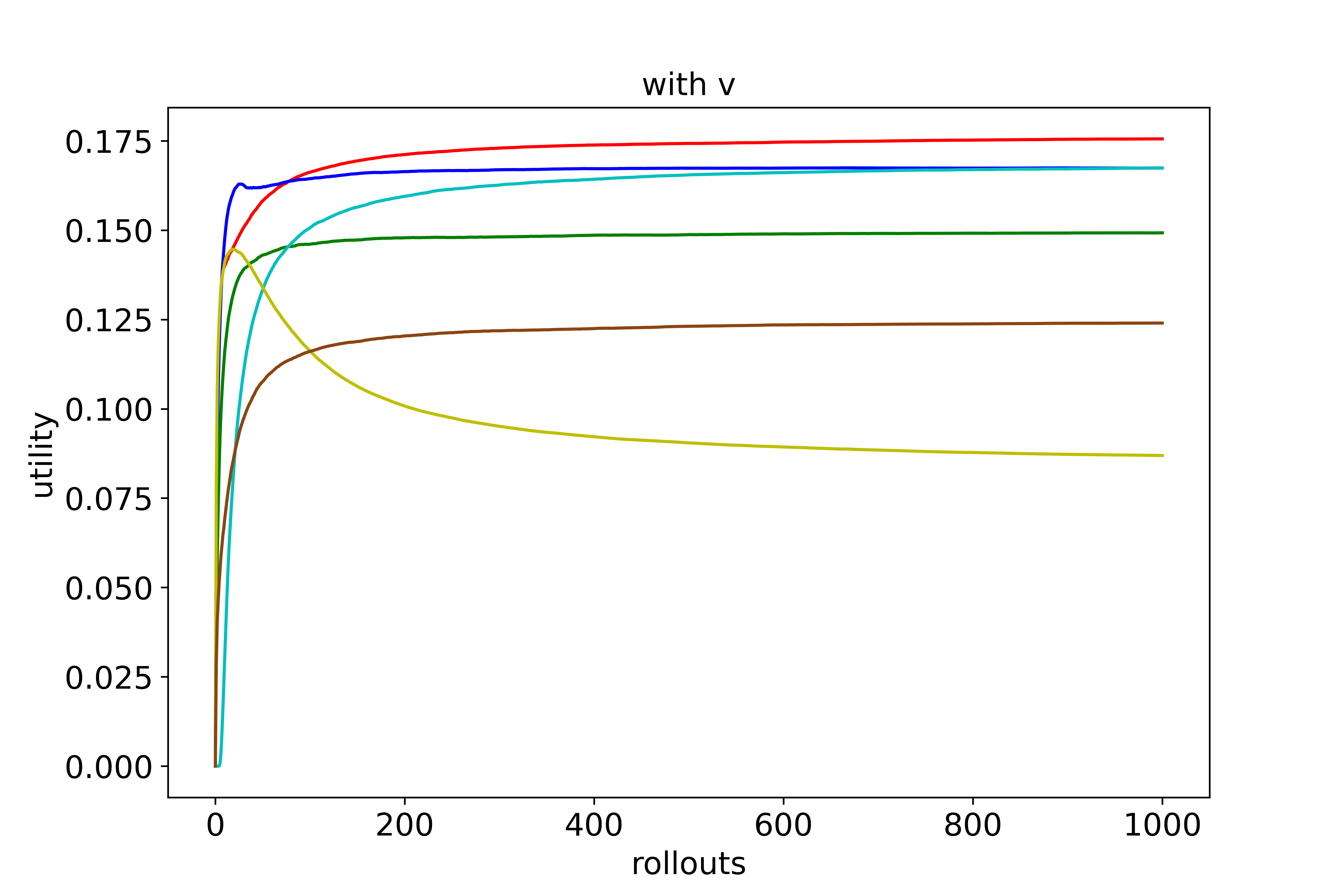

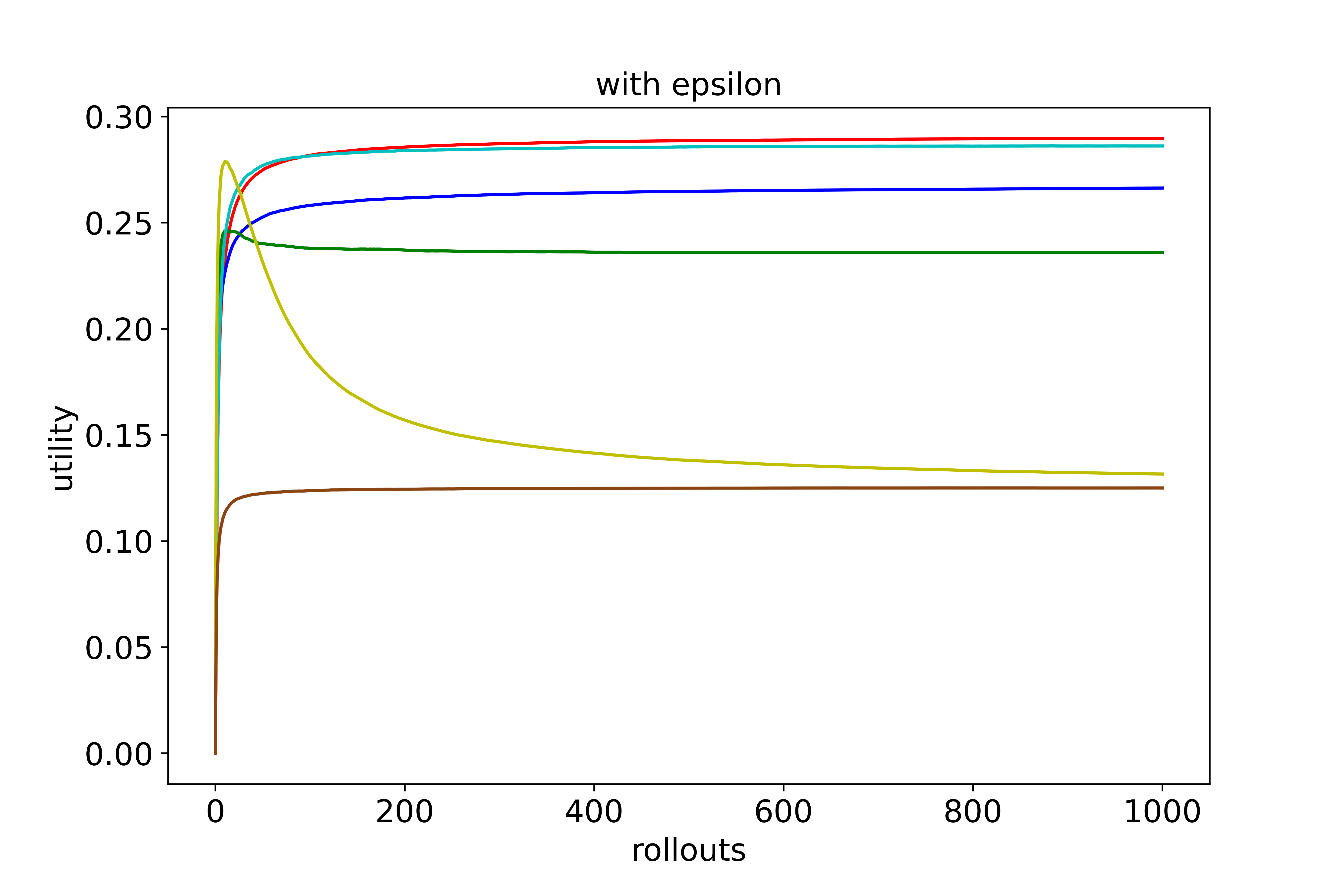

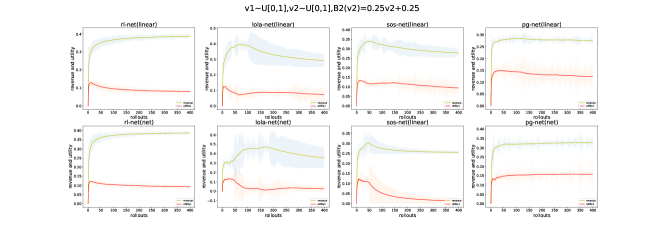

We evaluate the effectiveness of the algorithms in improving utility and social welfare by the utility of the strategic bidder and the seller’s revenue after 400 iterations. The results are presented in Table 1. Details of the experiments are given in Figures 8 to 14. From the table we see that the Bid Net trained with PG always maximizes the utility of the strategic bidder. Due to the more complex and parameterized network structure of Bid Net, the instability of direct applying opponent modeling algorithms can significantly reduce the utility. However, the PG algorithm is not affected by changes in the environment or opponent strategies, which shows its strong generalization ability. The parameters in the experiment of Algorithm 1 and Algorithm 2 were chosen as: .

| utility | RL | LOLA | SOS | PG | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| linear shading | Bid Net | linear shading | Bid Net | linear shading | Bid Net | linear shading | Bid Net | |||

|

0.09 | 0.09 | 0.15 | 0.01 | 0.12 | 0.04 | 0.18 | 0.20 | ||

|

0.08 | 0.09 | 0.07 | 0.03 | 0.10 | 0.02 | 0.12 | 0.16 | ||

|

0.21 | 0.22 | 0.37 | 0.05 | 0.33 | 0.08 | 0.33 | 0.46 | ||

|

0.15 | 0.16 | 0.26 | 0.04 | 0.09 | 0.04 | 0.27 | 0.33 | ||

|

0.06 | 0.06 | 0.09 | 0.01 | 0.08 | 0.01 | 0.04 | 0.11 | ||

|

0.11 | 0.12 | 0.16 | 0.14 | 0.12 | 0.16 | 0.20 | 0.31 | ||

|

0.12 | 0.11 | 0.13 | 0.10 | 0.14 | 0.15 | 0.18 | 0.32 | ||

7 Conclusion

We designed an automatic bidding strategy for bidders in repeat auctions. Using opponent modeling algorithms, bidders can learn bidding strategy to maximize their utility. We design Bid Net to represent bidding strategies and propose PG algorithm for training the network in repeated auctions. PG is able to learn the best responses in the face of static opponents and converges to the induced equilibrium when all agents adopt PG simultaneously. According to our experiments, we illustrate Bid Net as an improvement to the linear shading function and the effectiveness of PG algorithms by comparing it with other opponent modeling algorithms. PG significantly improves the utility of strategic bidders when both environmental parameters and other agents’ methods of updating their strategies are changed. We hope that this work will contribute to more research on bidder strategies in auctions and automatic bidding.

Acknowledgements

This paper is supported by National Key R&D Program of China (2021YFA1000403) and National Natural Science Foundation of China (No.11991022), and the Strategic Priority Research Program of Chinese Academy of Sciences, Grant No.XDA27000000.

References

- \bibcommenthead

- (1) Edelman, B., Ostrovsky, M., Schwarz, M.: Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords. American Economic Review 97(1), 242–259 (2007)

- (2) Shen, W., Peng, B., Liu, H., Zhang, M., Qian, R., Hong, Y., Guo, Z., Ding, Z., Lu, P., Tang, P.: Reinforcement mechanism design: With applications to dynamic pricing in sponsored search auctions, vol. 34, pp. 2236–2243 (2020)

- (3) Afshar, R.R., Rhuggenaath, J., Zhang, Y., Kaymak, U.: A reward shaping approach for reserve price optimization using deep reinforcement learning. In: 2021 International Joint Conference on Neural Networks, pp. 1–8 (2021)

- (4) Cai, Q., Filos-Ratsikas, A., Tang, P., Zhang, Y.: Reinforcement mechanism design for e-commerce. In: Proceedings of the 2018 World Wide Web Conference, pp. 1339–1348 (2018)

- (5) Gomes, R.D., Sweeney, K.S.: Bayes-nash equilibria of the generalized second price auction. In: Proceedings of the 10th ACM Conference on Electronic Commerce, pp. 107–108 (2009)

- (6) Varian, H.R., Harris, C.: The vcg auction in theory and practice. American Economic Review 104(5), 442–45 (2014)

- (7) Varian, H.R.: Online ad auctions. American Economic Review 99(2), 430–34 (2009)

- (8) Myerson, R.B.: Optimal auction design. Mathematics of Operations Research 6(1), 58–73 (1981)

- (9) Duetting, P., Feng, Z., Narasimhan, H., Parkes, D., Ravindranath, S.S.: Optimal auctions through deep learning. In: Proceedings of the 36th International Conference on Machine Learning, vol. 97, pp. 1706–1715 (2019)

- (10) Rahme, J., Jelassi, S., Weinberg, S.M.: Auction learning as a two-player game. In: International Conference on Learning Representations, pp. 1–16 (2021)

- (11) Shen, W., Tang, P., Zuo, S.: Automated mechanism design via neural networks. In: Proceedings of the 18th International Conference on Autonomous Agents and MultiAgent Systems, pp. 215–223 (2019)

- (12) Zhang, Z., Liu, X., Zheng, Z., Zhang, C., Xu, M., Pan, J., Yu, C., Wu, F., Xu, J., Gai, K.: Optimizing multiple performance metrics with deep gsp auctions for e-commerce advertising. In: Proceedings of the 14th ACM International Conference on Web Search and Data Mining, pp. 993–1001 (2021)

- (13) Kanoria, Y., Nazerzadeh, H.: Dynamic reserve prices for repeated auctions: Learning from bids. In: Web and Internet Economics, pp. 232–232 (2014)

- (14) Balcan, M.-F.F., Sandholm, T., Vitercik, E.: Sample complexity of automated mechanism design. In: Advances in Neural Information Processing Systems, vol. 29 (2016)

- (15) Balcan, M.-F., Sandholm, T., Vitercik, E.: A general theory of sample complexity for multi-item profit maximization. In: Proceedings of the 2018 ACM Conference on Economics and Computation, pp. 173–174 (2018)

- (16) Cole, R., Roughgarden, T.: The sample complexity of revenue maximization. In: Proceedings of the Forty-Sixth Annual ACM Symposium on Theory of Computing, pp. 243–252 (2014)

- (17) Tang, P., Zeng, Y.: The price of prior dependence in auctions. In: Proceedings of the 2018 ACM Conference on Economics and Computation, pp. 485–502 (2018)

- (18) Nedelec, T., Baudet, J., Perchet, V., El Karoui, N.: Adversarial learning in revenue-maximizing auctions. In: Proceedings of the 20th International Conference on Autonomous Agents and MultiAgent Systems, pp. 955–963 (2021)

- (19) Nedelec, T., Karoui, N.E., Perchet, V.: Learning to bid in revenue-maximizing auctions. In: Proceedings of the 36th International Conference on Machine Learning, vol. 97, pp. 4781–4789 (2019)

- (20) Bagnall, A., Toft, I.: Autonomous adaptive agents for single seller sealed bid auctions. Autonomous Agents and Multi-Agent Systems 12, 259–292 (2006)

- (21) Cli, D.: Minimal-intelligence agents for bargaining behaviors in market-based environments. Hewlett-Packard Labs Technical Reports (1997)

- (22) Foerster, J., Chen, R.Y., Al-Shedivat, M., Whiteson, S., Abbeel, P., Mordatch, I.: Learning with opponent-learning awareness. In: Proceedings of the 17th International Conference on Autonomous Agents and MultiAgent Systems, pp. 122–130 (2018)

- (23) Willi, T., Letcher, A.H., Treutlein, J., Foerster, J.: COLA: Consistent learning with opponent-learning awareness. In: Proceedings of the 39th International Conference on Machine Learning, vol. 162, pp. 23804–23831 (2022)

- (24) McAfee, R.P., McMillan, J.: Auctions and bidding. Journal of economic literature 25(2), 699–738 (1987)

- (25) Mittelmann, M., Bouveret, S., Perrussel, L.: Representing and reasoning about auctions. Autonomous Agents and Multi-Agent Systems 36(1), 20 (2022)

- (26) Yao, S., Mela, C.F.: Online auction demand. Marketing Science 27(5), 861–885 (2008)

- (27) Ostrovsky, M., Schwarz, M.: Reserve prices in internet advertising auctions: A field experiment. In: Proceedings of the 12th ACM Conference on Electronic Commerce, pp. 59–60 (2011)

- (28) Cesa-Bianchi, N., Gentile, C., Mansour, Y.: Regret minimization for reserve prices in second-price auctions. IEEE Transactions on Information Theory 61(1), 549–564 (2015)

- (29) Mohri, M., Medina, A.M.: Learning theory and algorithms for revenue optimization in second price auctions with reserve. In: Proceedings of the 31st International Conference on Machine Learning, vol. 32, pp. 262–270 (2014)

- (30) Nedelec, T., Calauzenes, C., Perchet, V., El Karoui, N.: Robust stackelberg buyers in repeated auctions. In: International Conference on Artificial Intelligence and Statistics, pp. 1342–1351 (2020)

- (31) Rashid, T., Samvelyan, M., Schroeder, C., Farquhar, G., Foerster, J., Whiteson, S.: QMIX: Monotonic value function factorisation for deep multi-agent reinforcement learning. In: Proceedings of the 35th International Conference on Machine Learning, vol. 80, pp. 4295–4304 (2018)

- (32) Qiu, W., Wang, X., Yu, R., Wang, R., He, X., An, B., Obraztsova, S., Rabinovich, Z.: Rmix: Learning risk-sensitive policies for cooperative reinforcement learning agents. In: Advances in Neural Information Processing Systems, vol. 34, pp. 23049–23062 (2021)

- (33) Jiang, J., Lu, Z.: Learning attentional communication for multi-agent cooperation. In: Advances in Neural Information Processing Systems, vol. 31, pp. 1–11 (2018)

- (34) Hu, S., Xie, C., Liang, X., Chang, X.: Policy diagnosis via measuring role diversity in cooperative multi-agent RL. In: Proceedings of the 39th International Conference on Machine Learning, vol. 162, pp. 9041–9071 (2022)

- (35) Hernandez-Leal, P., Kaisers, M., Baarslag, T., de Cote, E.M.: A Survey of Learning in Multiagent Environments: Dealing with Non-Stationarity (2017). http://arxiv.org/abs/1707.09183

- (36) Mescheder, L., Nowozin, S., Geiger, A.: The numerics of gans. In: Advances in Neural Information Processing Systems, vol. 30, pp. 1–11 (2017)

- (37) Mazumdar, E., Jordan, M.I., Sastry, S.S.: On Finding Local Nash Equilibria (and Only Local Nash Equilibria) in Zero-Sum Games (2019). https://arxiv.org/abs/1901.00838

- (38) Lanctot, M., Zambaldi, V., Gruslys, A., Lazaridou, A., Tuyls, K., Pérolat, J., Silver, D., Graepel, T.: A unified game-theoretic approach to multiagent reinforcement learning, vol. 30, pp. 1–11 (2017)

- (39) Liu, X., Jia, H., Wen, Y., Hu, Y., Chen, Y., Fan, C., Hu, Z., Yang, Y.: Towards unifying behavioral and response diversity for open-ended learning in zero-sum games, vol. 34, pp. 941–952 (2021)

- (40) Zhou, Z., Fu, W., Zhang, B., Wu, Y.: Continuously discovering novel strategies via reward-switching policy optimization. In: International Conference on Learning Representations, pp. 1–30 (2022)

- (41) Letcher, A., Foerster, J., Balduzzi, D., Rocktäschel, T., Whiteson, S.: Stable opponent shaping in differentiable games. In: International Conference on Learning Representations, pp. 1–20 (2019)

- (42) Zhang, C., Lesser, V.: Multi-agent learning with policy prediction. In: Proceedings of the Twenty-Fourth AAAI Conference on Artificial Intelligence, pp. 927–934 (2010)

- (43) Schaefer, F., Anandkumar, A.: Competitive gradient descent. In: Advances in Neural Information Processing Systems, vol. 32, pp. 1–11 (2019)

- (44) Grover, A., Wang, E., Zweig, A., Ermon, S.: Stochastic optimization of sorting networks via continuous relaxations. In: International Conference on Learning Representations, pp. 1–23 (2019)

- (45) Liu, X., Yu, C., Zhang, Z., Zheng, Z., Rong, Y., Lv, H., Huo, D., Wang, Y., Chen, D., Xu, J., Wu, F., Chen, G., Zhu, X.: Neural auction: End-to-end learning of auction mechanisms for e-commerce advertising. In: Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery and Amp; Data Mining, pp. 3354–3364 (2021)